Abstract

This study examines the determinants of Foreign Direct Investment (FDI) inflows into 24 economies in the Middle East and North Africa (MENA) region from 1980 to 2023. Utilizing Dunning’s Eclectic Paradigm (OLI framework), institutional theory, and transaction cost economics, this research investigates how ownership, location, and internalization advantages influence FDI decisions in a region characterized by significant resource dependence and institutional heterogeneity. To ensure the robustness of our findings, we employ second-generation panel data techniques, including Fully Modified Ordinary Least Squares (FMOLS), Dynamic Ordinary Least Squares (DOLS), Common Correlated Effects Mean Group (CCEMG) and Augmented Mean Group (AMG). These methodologies effectively address issues such as Cross-Sectional Dependence (CSD) and Slope Heterogeneity (SH). Our results indicate that institutional quality, particularly in relation to control of corruption and government effectiveness, exerts a strong positive impact on FDI inflows. Conversely, natural resource abundance demonstrates a negative relationship with overall FDI, thus corroborating the “resource curse” hypothesis within the MENA context. Market size significantly positively influences FDI attraction. Notably indicators of political stability and regulatory quality do not consistently show statistical significance across the model, implying that broader stability metrics may inadequately capture investor sentiment. In contrast, control of corruption and government effectiveness emerge as more salient institutional mediators of FDI decisions. These findings contribute to the existing literature by providing a context-specific analysis of FDI dynamics in the MENA region, employing advanced econometric estimators that have been underutilized in prior studies, and enhancing methodological transparency through the construction of composite variables. The results furnish actionable insights for policymakers seeking to attract sustainable foreign investment through institutional reform and macroeconomic stabilization.

Plain Language Summary

Foreign direct investment happens when companies from one country invest in businesses or operations in another country. FDI can bring many benefits, such as jobs, new technology, and economic growth. In this study, we looked at what makes countries in the Middle East and North Africa more or less attractive to foreign investors. We examined data from 24 MENA countries over more than 40 years (1980–2023). We focused on several key factors: how strong and stable the economy is, how well the government functions, whether corruption is low, how rich the country is in natural resources like oil, and how politically stable it is. Our findings show that foreign investors care a lot about good governance. Countries with less corruption, better government services, and stronger legal systems attract more FDI. Economic stability also matters when inflation is low and interest rates are predictable, foreign investors feel more confident. Surprisingly, having lots of natural resources like oil does not always help attract FDI. In fact, countries that rely too much on these resources often see fewer investments, possibly because they may neglect other important sectors like manufacturing or technology. Market size meaning how big the economy and population are plays a major role. Larger markets tend to draw more foreign firms looking to grow their business. Interestingly, political stability by itself didn’t seem to strongly affect investment decisions. Instead, investors appear to focus more on actual government performance and policies. These results give us a clearer idea of what governments in the MENA region can do to attract more foreign investment. Improving governance, keeping the economy stable, and reducing reliance on natural resources could make a big difference. This study helps both researchers and decision-makers understand how to create better conditions for foreign investment, which can lead to stronger economies and better opportunities.

Keywords

Introduction

Foreign direct investment (FDI) is defined as capital movements (inflows and outflows) resulting from the activities of multinational corporations (MNCs) in international markets (Agiomirgianakis et al., 2004). Over the past four decades, FDI has emerged as a significant and preferred instrument for international finance and capital generation, consistently fostering economic development, and facilitating internationalization, even amidst global challenges (Janicki & Wunnava, 2004; Susic et al., 2017).

Empirical evidence indicates that FDI positively influences the host economy's income levels, productivity enhancement, and overall economic growth (Sokang, 2018), while simultaneously contributing to the reduction of income inequality and improved social well-being among individuals (Moudatsou, 2003; Ravinthirakumaran & Ravinthirakumaran, 2018). Consequently, FDI inflows also facilitate the transfer of intangible assets, including managerial skills and advanced technologies (Gupta & Singh, 2016; Jadhav, 2012).

Numerous countries in North Africa and the Middle East (MENA) are actively seeking to increase FDI inflows into their economies by implementing new policies and refining existing frameworks (Abdelkarim et al., 2012).

The MENA region is characterized by substantial resource wealth, accounting for approximately 60% of the world’s oil reserves and 45% of global natural gas reserves, thereby indicating its significant and dynamic role in the global economy (Emara et al., 2019). Statistics reveal that MENA economies represent 10% of the world's population, 4.30% of the global labor force, and 29.55% of the world’s natural resource rents (WDR, 2019). Furthermore, MENA economies engage in trade valued at $1.295 trillion, representing 2.66% of global trade, with exports and imports totaling $566 billion and $729 billion, respectively, compared to $800 billion in 2005 (WDR, 2005). Notably, data indicate that FDI inflows into MENA peaked at $96,210,683,505, primarily due to Saudi Arabia’s successful efforts in attracting FDI through improvements and reforms in policies governing real estate, petrochemicals, refining, construction, and trade (WIR, 2010).

Despite these initiatives, the MENA region continues to experience comparatively low levels of FDI flows relative to other global regions. In 2020, net FDI inflows into MENA constituted just 3.63% of global FDI net inflows, in stark contrast to the 28.93% represented by the BRICS (Brazil, Russia, India, China, and South Africa), 5.32% of MINT inflows (Mexico, Indonesia, Nigeria, and Turkey), and 24.05% of those flowing into the European Union (EU) (Giroud & Ivarsson, 2020). Various factors contribute to this shortfall, including levels of regional integration and reform (Makdisi et al., 2006), the presence of poorly structured and low-quality institutions that deter capital flows (Jabri & Brahim, 2015), and issues related to transparency and corruption levels (Hassan, 2017).

Numerous studies have analyzed the impact of specific factors, including bureaucracy, corruption, employment protection, and legal institutions on FDI flows (Bénassy-Quéré et al., 2007) and measured the relationship between macroeconomic instability and FDI inflows (Chan & Gemayel, 2004). Additionally, other determinants of FDI that have garnered scholarly attention encompass market openness, infrastructure, rates of return on investment, inflation, economic growth, political stability, human capital indices and the availability of natural resources (Globerman & Shapiro, 2002; Mosallamy & Abbas, 2016). Furthermore, some research endeavors have sought to develop and construct dynamic models of the determinants of FDI flows (Abonazel & Shalaby, 2020; Rogmans & Ebbers, 2013).

There is no consensus regarding a universally accepted set of factors that can be characterized as the primary determinants influencing FDI inflows into specific regions or economies. Nevertheless, the aforementioned studies illustrate varying sets of regressors utilized by each research endeavor, revealing a lack of agreement on the perspectives, methodologies, sample selection, and analytical tools pertaining to the potential determinants of FDI (Chakrabarti, 2001).

This study addresses notable research gaps by systematically identifying and quantifying the effects of key determinants influencing FDI inflows across 24 MENA economies from 1980 to 2023. These economies include Afghanistan, Algeria, Bahrain, Djibouti, Egypt, Iran, Iraq, Jordan, Kuwait, Lebanon, Libya, Mauritania, Morocco, Oman, Pakistan, Qatar, Saudi Arabia, Somalia, Sudan, Syria, Tunisia, the United Arab Emirates, the State of Palestine and Yemen (Abed & Davoodi, 2003). Building upon Dunning’s Eclectic Paradigm (OLI framework), this research integrates insights from institutional theory and transaction cost economics to examine how ownership, location and internalization advantages shape FDI decisions within this often volatile and institutionally diverse context. Our analysis incorporates an extensive array of variables reflecting not only resource-seeking and market-seeking motives but also the significant influences of institutional quality, macroeconomic policies, and political risk. Drawing on recent empirical findings (e.g., Bhujabal et al., 2024; Mim & Saïdane, 2023; Triki et al. 2022), this research provides updated and context-specific insights into how governance structures, regulatory quality, and macroeconomic stability collectively affect FDI attractiveness in the MENA region.

To ensure the robustness and reliability of our findings, we employ advanced second-generation panel data estimation techniques, specifically the Common Correlated Effects Mean Group (CCEMG) and Augmented Mean Group (AMG) estimators, which are well suited to address challenges posed by cross-sectional dependence, and slope heterogeneity inherent in regional panels. Methodological transparency is further enhanced through the application of Principal Component Analysis (PCA) for constructing composite indicators for market size and availability of natural resources.

Through these rigorous approaches, this paper makes three significant contributions to the field of international business and development economics. First, it provides a novel, context-specific analysis of FDI dynamics in the MENA region, distinguishing this study from broader global or single-country analysis. Second, it significantly enhances methodological rigor through advanced econometric techniques and PCA, yielding more reliable insights into the complex determinants of FDI. Third, the study not only re-evaluates traditional drivers but also elucidates the underexplored mediating role of institutional quality (e.g., Voice and Accountability, Rule of Law, Regulatory Quality, government effectiveness, rule of law and political stability) and the precise impact of natural resource abundance, including the potential “resource curse” phenomenon, in attracting sustainable FDI to the MENA region.

The remainder of this paper is organized as follows: a Literature Review and Theoretical Framework section, which examines the theoretical foundations and existing empirical literature on FDI determinants and identifies the research gap; a Methodology section that delineates the data and methodological approach, including model development; a Results section that presents and discusses the empirical findings; a Discussion section that contextualizes these findings in relation to previous studies; and, finally, a Conclusion section that summarizes the key findings, policy implications, limitations, and recommendations for future research.

Literature Review and Theoretical Framework

This section provides a thorough examination of the theoretical foundations and empirical evidence pertaining to the determinants of FDI inflows, with a specific focus on factors pertinent to the distinct context of the MENA region. It elucidates how established theoretical constructs inform our comprehension of FDI behavior and how these concepts guide our empirical analysis.

Theoretical Foundations of FDI

FDI plays a critical role in global economic integration and development. Its determinants are widely studied in international business literature, with several theoretical frameworks providing insights into how MNCs evaluate host economy for investment opportunities.

Dunning’s Eclectic Paradigm (OLI framework)

The most influential theoretical framework in this context is Dunning’s Eclectic Paradigm, also known as the OLI framework. This paradigm asserts that firms are more likely to engage in FDI when they possess ownership advantages, operate in locations that provide competitive advantages, and can internalize these benefits more effectively than through market transactions (Dunning, 1980, 1988a, 1988b).

Ownership Advantages (O): refers to firm-specific assets such as brand equity, proprietary technology, managerial expertise, and economies of scale, which enable MNC’s to surpass local competitors.

Location Advantages (L): Encompass host country characteristics like natural resource availability, market size, labor costs, infrastructure, and crucially, institutional quality.

Internalization Advantages (I): Emerge when firms opt to conduct operations internally rather than through arms-length contracts. This preference is often motivated by high transaction costs or inadequate legal enforcement (Williamson, 1979, 1986), which ensures control over proprietary assets and mitigates the risks associated with external market transactions.

This study builds upon the OLI framework to systematically analyze how FDI inflows into the diverse MENA region are influenced by a combination of macroeconomic, institutional, political, market size and Availability of natural resources factors, thereby enhancing our understanding of the determinants of FDI in complex emerging markets.

Institutional Theory and Transaction Cost Economics (TCE)

Recent advancements in institutional theory underscore that FDI decisions are significantly contingent upon the quality of a host country’s institutions, encompassing essential elements such as the control of corruption, the rule of law, and regulatory effectiveness (Mim & Saïdane, 2023; Tun et al., 2012). Robust institutions play a critical role in mitigating uncertainty and reducing transaction costs for foreign investors, thereby augmenting a country's appeal as an investment destination (Bénassy-Quéré et al., 2007; Ölmez et al., 2024; Sabir et al., 2019).

Transaction Cost Economics (TCE), initially introduced by Coase (1937) and subsequently refined by Williamson (1986) and North (1990), complements this perspective. TCE examines how institutional inefficiencies elevate transaction costs such as those arising from inadequate contract enforcement, bureaucratic delays, or policy unpredictability. These escalated costs, if not counterbalanced by other locational advantages, can considerably deter inward FDI by diminishing the profitability and security of investments. Consequently, we hypothesize that indicators of institutional quality, including control of corruption (CC), government effectiveness (GE) and regulatory quality (RQ), will exhibit positive and significant correlations with FDI inflows (Sabir et al., 2019).

Political Risk Theory

Political risk is defined as the probability that political events such as abrupt regime changes, civil unrest, expropriation, or sudden policy shifts will have detrimental effects on business operations and FDI (Asiedu, 2006; Yılmaz, 2024). This concept is a crucial factor for MNCs when determining optimal capital allocation strategies (Gonzalez-Bravo, 2020).

The relationship between political stability and FDI is complex and varies according to the nature of investment and the specific industry in question. For instance, resource-based FDI may exhibit a higher tolerance for political risk due to the long-term potential for resource extraction, whereas investments in the service or manufacturing sectors are likely to avoid unstable environments (Brada et al., 2006; Burger et al., 2016). in light of recent geopolitical developments and ongoing regional challenges in the MENA region, it is anticipated that political risk will generally exert a negative impact on FDI inflows, particularly for long-term investments that necessitate significant sunk costs and a high degree of confidence in policy continuity (Triki et al., 2022).

Determinants of FDI Inflows

This subsection examines the primary categories of determinants of FDI, establishing a direct connection to the theoretical foundations previously articulated and delineating our hypotheses regarding their influence on FDI inflows within the MENA region.

Market Size and Economic Openness

Market size serves as an indicator of the demand-side potential within a host economy and constitutes a well-established locational advantage within OLI paradigm. Larger markets provide MNCs with enhanced sales volumes, economies of scale in both production and distribution (Eckert et al., 2022), as well as diminished entry risks attributable to heightened consumer demand.

Empirical research consistently demonstrates a positive correlation between market size often presented by GDP per capita or total GDP and FDI inflows (Asongu et al., 2018; Cieślik & Hamza, 2022; Lautiera & Moreau, 2012). Economies characterized by larger populations and expanding middle classes, such as Egypt, Iran, and Morocco, have emerged as particularly appealing to foreign investors seeking extensive market access and regional supply chain opportunities.

In support of our hypothesis H5, we poised that market size exerts a positive and significant influence on FDI inflows within the MENA region, aligning with market-seeking motivations in multinational investment decisions.

Natural Resources and the “Resource Curse” Hypothesis

Natural resources represent a significant location advantage that traditionally attracts resource-seeking FDI, within extractive industries. However, empirical evidence consistently highlights a dual nature of resource abundance, while it may incentivize sector-specific FDI, it can also result in adverse spillover effects such as Dutch disease, rent-seeking behavior, and weakened institutional frameworks collectively termed the “resource curse” (Chiyaba & Singleton, 2024; Garg et al., 2025; Lu et al., 2020).

In the MENA region, oil and gas rents constitute a substantial portion of national income. Nevertheless, numerous countries within this region experience limited economic diversification and inadequate institutional development, which can detract from the sustainability of the long term investments (Mina, 2007; Rogmans & Ebbers, 2013).

Consequently, we hypothesize that the availability of natural resources operationalized through Principal Component Analysis (PCA) to ensure robust measurement will exhibit a negative correlation with overall FDI inflows, thereby supporting the Resource Curse hypothesis (H2).

Institutional Quality

Strong institutions defined by characteristics such as transparency, accountability, effective regulation, and minimal corruption are essential for mitigating investor uncertainty and transaction costs. This enhancement significantly increases the attractiveness of a host country for FDI (Bénassy-Quéré et al., 2007; Saha et al., 2022; Tabash et al., 2024).

Key institutional indicators used in this study include:

Control of Corruption (CC)

Rule of Law (RL)

Voice and Accountability (VA)

Empirical evidence consistently indicates that the quality of institutions exerts a profound influence on FDI decisions. robust institutions bolster investor confidence, diminish risk perception, and facilitate sustainable capital inflows (Awdeh & Jomaa, 2024; Cieślik & Hamza, 2022; Sabir et al., 2019).

Consequently, we hypothesize that institutional quality exerts a positive and significant effect on FDI inflows (H1).

Macroeconomic Policy Variables

Macroeconomic stability is a critical determinant in the attraction of FDI. Key Indicators including inflation, interest rates and exchange rate volatility, significantly influence the investment environment and affect the decision-making processes of multinational corporations.

High inflation diminishes real returns on investment and introduces considerable uncertainty regarding future economic conditions, rendering host economies less appealing to foreign investors (Aziz & Mishra, 2016; Esen et al., 2025; Khatabi et al., 2020). In similar vein, elevated real interest rates escalate the cost of capital, potentially deterring investment unless counterbalanced by exceptionally high expected returns (Al-Shakrchy et al., 2023; Esen et al., 2025; Marial, 2009; Omankhanlen, 2011). Al-Shakrchy et al. (2023) demonstrate that macroeconomic instability during global shocks has a pronounced impact on FDI inflows in the MENA region, while Kamal et al. (2023) highlight that the consistency of monetary policy is vital for sustaining investor confidence.

Consequently, we hypothesize that inflation (INF) and real interest rates (RIR) negatively influence FDI inflows (H4). Although excessive exchange rate volatility increases risk and discourages long-term investments, moderate exchange rate depreciation (EXR) may enhance export competitiveness and improve profitability for foreign investors engaged in tradable goods sectors (Ayele, 2022; Chikwira & Jahed, 2024; Jabri et al., 2013). Therefore, moderate fluctuations in exchange rates may present a degree of attractiveness for export-oriented investments.

Political Risk and Stability

While the broader political stability (PS) does not consistently exhibit statistical significance in our findings, indicators such as control of corruption and government effectiveness demonstrate stronger correlation with FDI inflows.

This suggests that investors may exhibit heightened sensitivity to predictable regulatory frameworks and effective governance rather than to the overarching type of political regime (Brada et al., 2006; Gani & Al-Abri, 2013). This observation further supports our hypothesis H3, which posits that political instability will exert a detrimental effect on FDI, particularly in fragile and conflict-affected economies.

Indicators related to political risk used in our study include:

Political Stability and Absence of Violence/Terrorism (PS)

Government Effectiveness (GE)

Regulatory Quality (RQ)

Each hypothesis is grounded in theoretical frameworks and supported by prior empirical evidence, thereby ensuring robust conceptual underpinnings and alignment with ongoing academic discourse.

Methodology

This study employs a rigorous methodological framework rooted in contemporary panel data econometrics to examine the determinants of FDI inflows into 24 countries in the MENA region from 1980 to 2023. The methodology adheres to a systematic approach encompassing variable construction, data selection, model specification and the implementation of advanced estimation techniques designed aimed at addressing significant econometric challenges including cross-sectional dependence (CSD), slope heterogeneity (SH), and endogeneity.

Variable Construction and Empirical Measurement

To ensure robust measurement and mitigate issues related to multicollinearity among raw indicators, two key explanatory variables market size (MS) and availability of natural resources (ANR) were constructed using Principal Component Analysis (PCA), a widely accepted multivariate technique in panel data analysis dimensionality reduction (Asongu et al., 2018; Bhujabal et al., 2024; Nxumalo & Makoni, 2021). The PCA method is conducted by estimating the eigenvalues of the correlation matrix derived from the original variable dataset. Typically, the initial principal components associated with the highest eigenvalues are recognized as accounting for the majority of the variance among the dataset and its variables. Consequently, these components are regarded as encapsulating the most pertinent information regarding the original dataset (Kurul, 2017).

Market Size (MS)

Constructed using:

GDP per capita (constant 2010 USD)

Population growth rate (% annual)

Trade openness (exports + imports / GDP)

These indicators were standardized and subjected to PCA to extract the first principal component, which captures the dominant pattern of variation across the three sub-indicators. The resulting composite index reflects the overall market potential of each country in attracting foreign investors through demand pull and scale economies.

Availability of Natural Resources (ANR)

Constructed using:

Ore and metal exports (% of merchandise exports)

Oil and natural gas rents (% of GDP)

Fuel exports (% of merchandise exports)

Renewable energy consumption (% of total final energy use)

Each indicator was normalized and subjected to PCA analysis to derive a singular composite index that encapsulates the overall availability of natural resources. This methodology enhances measurement accuracy and ensures replicability relative to prior studies that utilize isolated proxies or arbitrary aggregation methods.

The construction of these variables have been incorporated into the methodology section to guarantee transparency and reproducibility.

Variables and Data Collection

The variables utilized in this study have been meticulously chosen based on both established theoretical frameworks and substantial empirical evidence derived prior research on FDI.

The dependent variable in this analysis is FDI inflows, operationalized as net inflows (Balance of Payments, current US dollars).

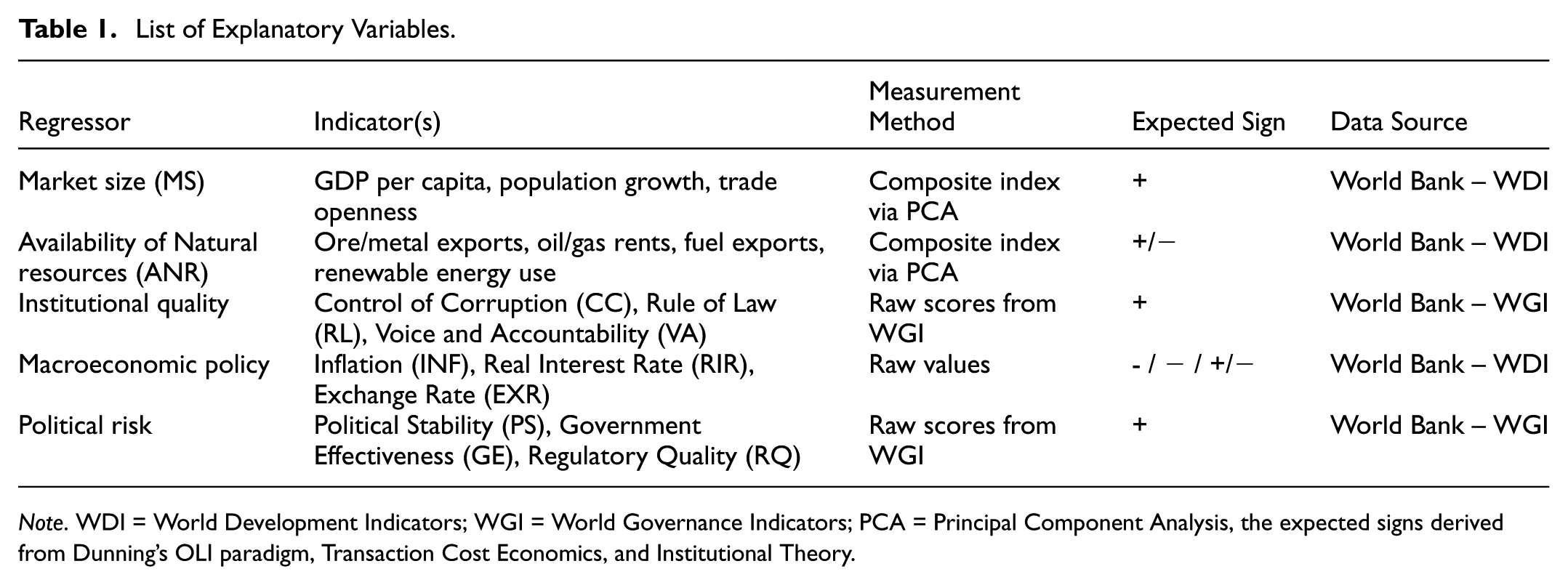

The independent variables are categorized to encompass the diverse determinants of FDI in the MENA region, including market characteristics, natural resource endowments, institutional quality, political risk, and macroeconomic conditions. The specific variables along with their measurements, expected signs and data sources, are delineated in Table 1.

List of Explanatory Variables.

Note. WDI = World Development Indicators; WGI = World Governance Indicators; PCA = Principal Component Analysis, the expected signs derived from Dunning’s OLI paradigm, Transaction Cost Economics, and Institutional Theory.

The data utilized in this study were primarily obtained from publicly accessible and reputable international databases. Specifically, we referred to the World Bank’s World Development Indicators (WDI) for macroeconomic and market size variables, as well as the World Governance Indicators (WGI) for proxies related to institutional quality and political risk. The final dataset consists of a balanced panel of 24 MENA economies observed annually over the period from 1980 to 2023. This extensive temporal and cross-sectional coverage provides sufficient statistical power to identify long-term trends, dynamic relationships, and structural changes in FDI behavior across the region.

Model Specification

Building upon the theoretical foundations and empirical findings presented in preceding sections, and in accordance with the methodologies proposed by Azam and Haseeb (2021) and Khan et al. (2020), we delineate the following dynamic panel data model to estimate the long-run relationship between FDI inflows and their key determinants in the MENA region:

The econometric form of Equation 1 can be expressed as follows:

Where:

- FDIit : FDI inflows for country i at time t.

- Xkit Denotes a vector of an explanatory variables, including market size (MS), availability of natural resources (ANR), institutions (CC, RL, VA), political risk (PS, GE, RQ), and macroeconomic policy variables (INF, EXR, RIR).

- αi: Represents the country-specific interception, capturing unobserved time-invariant heterogeneity across countries.

- εit: the error term that captures unobserved heterogeneity and random disturbances.

The subscript i denotes the cross-sectional units (countries), while t refers to the temporal dimension (years). importantly, the coefficients βki are explicitly permitted to vary across countries, thereby accommodating potential slope heterogeneity, which is a critical econometric feature that will be formally tested and addressed in our subsequent empirical analysis.

This functional form is grounded in Dunning (1980, 1988a, 1988b) OLI framework. By incorporating variables that reflect ownership, location, and internalization advantages, our model offers a robust empirical framework suitable for rigorous panel data analysis within the context of FDI.

Estimation Techniques

To ensure robust and reliable estimation results, this study employs a series of advanced econometric techniques that are suitable for heterogeneous panels exhibiting CSD, which frequently observed in regional analyses including those related to MENA region. Adhering to a rigorous methodological approach in accordance with the works of Ahmed et al. (2021) and Azam and Haseeb (2021), we advance through the following steps:

- Cross-Sectional Dependence (CSD) test: This preliminary test evaluates the extent to which common global shocks or unobserved factors influence all units (countries) simultaneously, thereby indicating the presence of CSD.

- Slope Homogeneity (SH) test: Subsequently, we assess whether the relationships between FDI and its determinants are consistent across all countries or exhibit significant variations, thereby testing slope homogeneity.

- Unit Root test: To ascertain the order of integration of the variables and mitigate the risk of spurious regression results, we conduct appropriate unit root tests specifically designed for panel data.

- Alternative heterogeneous estimators: to conduct a comprehensive comparative analysis and address heterogeneity, we initially utilize Fully Modified Ordinary Least Squares (FMOLS) and Dynamic Ordinary Least Squares (DOLS), recognizing their widespread application in panel data research.

- Primary and robust heterogeneous estimators: To achieve the most consistent and reliable estimates for our panel data, which exhibits both CSD and SH, we utilize Common Correlated Effects Mean Group (CCEMG) and Augmented Mean Group (AMG) estimators. These methodologies also function as critical robustness checks for our primary findings.

These following subsections details these procedures.

Cross-sectional Dependence (CSD), Slope Homogeneity (SH), and Unit Root Analyses

Given the increasing economic interdependence among MENA countries and the potential for common global shocks to simultaneously impact these nations (Khalid & Shafiullah, 2021), it is imperative to test for CSD prior to conducting further analysis. Neglecting to account for CSD may result in biased standard errors, inconsistent estimates, and inferences (Chudik & Pesaran, 2015; Li et al., 2021).

To detect CSD, we utilize the CS-test developed by Pesaran (2015), which can be articulated in the following equation:

Where: N: denotes the number of cross-sectional units (e.g., countries, firms), T: represents the number of time periods and

In the event that significant CSD is identified, traditional unit root tests may become invalid due to their underlying assumption of independence across cross-sections. Consequently, we employ the cross-sectionally augmented IPS (CIPS) unit root test introduced by Pesaran (2007) to evaluate the stationarity properties of the series. This second-generation test accommodates cross-sectional dependence and yields more accurate results relative to conventional Augmented Dicky-Filler (ADF) or Philips-Perron (PP) tests (Shariff & Hamzah, 2015).

The CIPS statistics can be articulated as follows:

where

Additionally, we conduct the SH test proposed by Pesaran and Yamagata (2008) to assess whether the relationships between FDI and its determinants are uniform across countries. Rejection of the null hypothesis of slope homogeneity suggests that a mean group estimator is more suitable than a pooled estimator (Su et al., 2021). The SH test can be expressed in the following equations:

where

Alternative Heterogeneous Panel Estimators

To estimate the long-run elasticities of FDI with respect to each determinant, we employ two widely recognized heterogeneous panel estimators:

- Fully Modified Ordinary Least Squares (FMOLS): Developed by Phillips and Hansen (1990), this method addresses issues of serial correlation and endogeneity in the regressors, yielding asymptotically unbiased and efficient estimates.

The general cointerating regression for panel data is given by the following equation:

Where: i = 1,…,N denotes the cross-sectional units, t = 1,…,T denotes the time periods, Yit is the dependent variable for unit i at time t, xit is a (K × 1) vector of regressors for unit i at time t, βi′ is the (K × 1) vector of cointegrating coefficients that are allowed to be heterogeneous across units and αit is the error term, which is assumed to be stationary for a cointegrating relationship

- Dynamic Ordinary Least Squares (DOLS): Introduced by Saikkonen (1992) and Stock and Watson (1993), this approach incorporates leads and lags of first-differenced regressors to enhance efficiency and mitigate bias in cointegrated panels.

The general cointerating regression for panel data is given by the following equation:

Where: yit is the dependent variable for individual i at time t, xit is a vector of M regressors for individual i at time t, αi represents the individual-specific intercepts (fixed effects), which capture unobserved heterogeneity across units, βi is the M × 1 vector of long-run cointegrating coefficients for individual i, Δxit−k represents the first differences of the regressors xit at lead and lag orders k, k ranges from −Ki (leads) to Ki (lags), where Ki is the optimal number of leads and lags, which can also be unit-specific, δ ik is the coefficient vector for the k-th lead/lag of the differenced regressors and eit is the idiosyncratic error term, which is assumed to be stationary for each i.

Although FMOLS and DOLS methodologies are widely employed, their primary theoretical framework is desinged for estimating long run cointegration among I(1) non stationary variables (Phillips & Hansen, 1990; Stock & Watson, 1993). These methodologies address endogeneity and seral correlation within such cointegrating regressions, their effectiveness in addressing CSD and SH directly on I(0) stationarity data is limited (Apergis et al., 2007; Khan et al., 2020), and may yeild inconsistent estimates (Chudik & Pesaran, 2015) in the presence of endogeneity arising from unobserved common factors(Gengenbach et al., 2006). Consequently, we implement more robust and theoretically appropriate estimators as outlined below. The FMOLS and DOLS results will thus serve as valuable benchmarks for comparison, illustrating how findings may differ under alternative modeling assumptions prevalent in the broader literature.

Primary and Robust Heterogeneous Estimators

To achieve the most consistent and reliable estimates that explicitly account for unobserved common factors, CSD and SH within our I(0) panel we employ two advanced estimation techniques:

- Common Correlated Effects Mean Group (CCEMG) estimator: as proposed by Pesaran (2006), this estimator mitigates the impact of unobserved common factors by augmenting the regression model with cross-sectional averages of both dependent and independent variables. This modification yields consistent estimates, even in the presence of pronounced CSD.

CCEMG can be expressed by the following equation:

Where: yit is the dependent variable for unit i at time t, xit is a K × 1 vector of observed regressors for unit i at time t, α i is the individual-specific intercept (fixed effect), βi is a K × 1 vector of heterogeneous slope coefficients for unit i. This is the primary parameter of interest, and its heterogeneity is crucial, ft is an M×1 vector of unobserved common factors that affect all units at time t, γi is an M × 1 vector of factor loadings, which are heterogeneous across units. and eit is the idiosyncratic error term, assumed to be i.i.d. across units and time, and generally uncorrelated with ft and xit.

- Augmented Mean Group (AMG) estimator: Developed by Eberhardt and Teal (2010), this estimator builds upon the CCEMG framework by permitting a dynamic specification and testing for the existence of a common dynamic process across countries. AMG entails a two-step procedure that effectively accounts for unobserved common factors and yields a pooled coefficient for the long-run relationship.

AMG can be expressed by the following equation:

Where: yit the dependent variable for unit i at time t, αi the individual-specific intercept, βi′ heterogeneous slope coefficients for unit i, xit the vector of observed regressors for unit i at time t, δi is a heterogeneous coefficient on this common dynamic process, allowing each unit to respond differently to the common factor, ct are the coefficients on the time dummies and vit is the purged error term.

Both estimators demonstrates superior performance in panel data characterized by CSD and heterogeneity rendering them particularly appropriate for the MENA context. Notably, The AMG estimator introduces a dynamic common correlated effects approach, accommodating time-invariant coefficients and country-specific dynamics (Azam & Haseeb, 2021; Su et al., 2021).

These advanced estimation techniques are well sutited for our panel data, ensuring that our results are consistent and reliable in the presence of endogeneity, serial correlation, and heterogeneous slopes, while robustly accounting for CSD. They constituate the foundation of our primary findings and serve as critical robustness checkes for one another, thereby enhancing the validity and generalizability of our inferences.

Results

This section presents the empirical findings obtained from our econometric analysis, which investigates the determinants of FDI inflows in the MENA region over the period from 1980 to 2023. Our analysis adheres to a systematic methodological framework, initiating with diagnostic tests for cross-sectional dependence (CSD), slope homogeneity (SH) and unit root characteristics. The concluding phase involves the application of various robust estimation techniques, including FMOLS, DOLS, CCEMG, and AMG.

CSD, Unit Root and SH Tests

To ensure methodological rigor and the appropriateness of our subsequent empirical analysis, we first conducted a series of diagnostic tests to ascertain the key characteristics of our panel data. These diagnostics are essential for selecting suitable estimation techniques that yield consistent and efficient results.

We commenced our analysis by evaluating CSD among MENA economies utilizing Pesaran (2004) CD test. The null hypothesis of this test posits the absence of cross-sectional dependence. As presented in Table 2, the test yielded statistically significant values across all variables except for VA, leading us to robustly reject the null hypothesis of no cross-sectional dependence at the 1% significance level. This strong evidence of CSD suggests that common unobserved factors or global/ regional shocks significantly influence FDI dynamics across the MENA countries within our sample. Neglecting such interdependencies would result in biased and inconsistent estimates from traditional panel models.

Results of the CSD and CIPS Unit Root Tests.

, **, and * indicate statistical significance at the 1%, 5%, and 10% levels, respectively, CIPS critical values are −2.78, −2.65, and −2.58 at 1%, 5%, and 10% level of significance.

Given the confirmed CSD, we proceeded with second-generation unit root tests that specifically address such dependencies. We applied the Cross-sectionally Augmented IPS (CIPS) test, developed by Pesaran (2007), the null hypothesis of the CIPS posits that all series contain a unit root, indication non stationarity. The results from the CIPS test presented in Table 2 reveal that all variables are stationary at their levels, leading us to reject the null hypothesis for each series. This finding indicates an order of integration of I(0) for all variables. this is a significant since all series are stationary at their levels, there is no need to conduct cointegration tests (such as Westerlund or Pedroni tests), as cointegration is property of non stationary (I(1)). Our analysis can directly proceed to the application of certain panel cointegration techniques or robust estimators to investigate long-run relationships among the variables without necessitating differencing.

Furthermore, we conducted the SH test as proposed by Pesaran and Yamagata (2008). The null hypothesis for this test posits that the slope coefficients are homogeneous across the panel units. As illustrated in Table 3, the test strongly rejected the null hypothesis of homogeneous slopes across countries, evidenced by highly significant Delta and Delta adjusted statistics. This significant finding underscores the inherent heterogeneity in the responsiveness of FDI to its various determinants across the diverse sample of MENA countries. Such heterogeneity robustly justifies the application of heterogeneous mean group estimators such as FMOLS and DOLS rather than traditional pooled models such as Fixed Effects (FE) and Random Effects (RE), as the latter would impose restrictive and inaccurate assumptions of homogeneity (Francois et al., 2022; Maeso-Fernandez et al., 2006). These diagnostic steps collectively ensure that our subsequent estimation techniques are appropriate for the data structure, adequately account for the observed characteristics and capable of yielding consistent and reliable results.

Hashem Pesaran and Yamagata (2008) Test for slope heterogeneity.

, **, and * indicate statistical significance at the 1%, 5%, and 10% levels, respectively.

Results from Alternative Heterogeneous Estimators (FMOLS and DOLS)

Table 4 presents the long-run estimates derived from two prevalent heterogeneous panel estimators FMOLS and DOLS. These results provide initial insights into the direction and magnitude of each determinant’s impact on FDI inflows.

Long-run Panel Results Through FMOLS and DOLS Estimators.

, **, and * indicate statistical significance at the 1%, 5%, and 10% levels, respectively.

Our key findings are as follows:

Availability of Natural Resources (ANR): This variable exhibits a negative and statistically significant at the 5% level in both FMOLS and DOLS regressions. Specifically, a 1% increase in natural resource availability is associated with an approximate 3.35% decrease in FDI inflows under FMOLS, and a 2.30% decline under DOLS. These findings provides strong support for the “resource curse” hypothesis (H2). This indicates that within the MENA context, an increased availability of natural resources may paradoxically inhibit foreign direct investment (FDI). This phenomenon may be attributed to factors such as the Dutch disease, rent-seeking behaviors, or the prevalence of less diversified economies.

Market Size (MS): the results reveal a positive and significant relationship across both models. A 1% increase in market size is linked to a notable 4.31% rise in FDI inflows under FMOLS and a 5.07% increase under DOLS. This supports hypothesis H5, reinforcing the significance of market-seeking motives in foreign investment decisions (larger economies offer more opportunities to foreign firms, hence substantial pull-on foreign capital).

Exchange Rate (EXR): This variable exhibits a positive and statistically significant (at the 1% level in FMOLS and 10% significant in DOLS). This suggests that currency depreciation may enhance export competitiveness and attract foreign investors in tradable good sectors. However, the lower significance in DOLS indicates potential volatility influenced by broader macroeconomic conditions.

Inflation (INF): This variable demonstrates a negative and highly significant correlation. A 1% increase in inflation is associated with a 7.89% decline in FDI under FMOLS and a 13.31% decrease under DOLS. These results support Hypothesis H4, High inflation erodes purchasing power, escalates operational costs, and creates an environment of uncertainty, all of which serve to deter FDI.

Real Interest Rate (RIR): Exhibits a negative relationship with FDI inflows. A 1% rise in RIR is estimated to reduce FDI by about 12.83% (FMOLS) and 15.81% (DOLS), aligns with expectations that higher borrowing costs deter investment. This reinforces H4, which highlights macroeconomic policy variables as essential determinants of investor confidence.

Control of Corruption (CC): Strongly positive and significant relationship is evident. This provides robust empirical support for H1, demonstrating that better governance and reduced corruption significantly enhance investor confidence and mitigate risk perception, thereby attracting more FDI

Government Effectiveness (GE): This variable is positively significant in both models. A 1% improvement in government effectiveness is associated with a 1.54% increase in FDI under FMOLS and a 2.91% increase under DOLS. These findings support Hypothesis H1, underscoring the critical role of Effective governments providing stable policy environments, efficient public services, and reliable regulatory frameworks, all of which are attractive to foreign investors.

Rule of Law (RL): The effects are mixed, with marginal significance in FMOLS (p = .0577) and moderate significance in DOLS (p = .028). The positive coefficient suggests that legal frameworks may still influence investor confidence, although their impact appears limited without strong enforcement mechanisms.

Voice and Accountability (VA): This variable is statistically significant and positively related to FDI in both models. A 1% increase in VA corresponds to a 1.46% increase in FDI under FMOLS and a 2.79% increase under DOLS. This finding supports the notion that democratic participation can enhance investor confidence when complemented by effective institutions. This suggests that a more open and accountable political system can be seen as a positive signal by investors.

Political Stability (PS): Interestingly, this variable is significant in FMOLS and not statistically significant in DOLS. This suggests that in the MENA region, perhaps more granular, institutional factors may better capture investor concerns regarding political risk than a broad measure of stability.

Regulatory Quality (RQ): The results indicate that RQ is insignificant in FMOLS and negatively significant in DOLS, reflecting inconsistent impacts depending on model specification. This highlights the nuanced influence of regulatory environments on FDI location decisions.

Results from Primary and Robust Heterogeneous Estimators (CCEMG and AMG)

To enhance the reliability of our findings and comprehensively address concerns related to CSD, SH and unobserved common factors, we employed CCEMG and AMG estimators. The long run results derived from advanced estimators are presented in Table 5.

CCEMG and AMG Estimators Long-term Results.

, **, *, level of significance at 1%, 5%, and 10%, respectively.

Both the CCEMG and AMG estimators corroborated with the robustness of our previous findings models. The signs of the estimated coefficients exhibited remarkable consistency with those obtained from our initial analysis, however, minor variations in magnitude and significance levels were observed, reflecting adjustments made for unobserved common factors and country-specific dynamics.

Notably, under these robust checks:

The negative and statistically significant effect of natural resources on FDI remained robust across both estimators, further solidifying the “resource curse” hypothesis (H2) within the context of MENA. The magnitudes of the negative impact varied, but the deterrent effect is evident.

The positive and highly significant effect of market size on FDI inflows remained robust under both methods, consistently supporting the significance of market-seeking motives for foreign investment.

Exchange Rate (EXR): The exchange rate continued to demonstrate a positive and significant relationship with FDI, suggesting that currency depreciation is a consistent attractor for foreign capital.

Inflation (INF) and Real Interest Rate (RIR): Both inflation and real interest rates maintained their robust negative and highly significant impacts on FDI inflows, strongly reinforcing the critical importance of macroeconomic stability for attracting foreign capital (H4).

Government Effectiveness (GE): Government effectiveness consistently exhibited a strong positive and highly significant relationship with FDI, providing robust evidence for the critical role of sound governance structures in enhancing investor confidence (H1).

Control of Corruption (CC) Control of corruption continued to exhibit a positive and significant relationship under both estimators, powerfully reinforcing the importance of robust governance reforms for attracting FDI in the MENA region, thus strengthening support for (H1).

Political Stability (PS) and Regulatory Quality (RQ): Both political stability and regulatory quality continued to show no statistically significant relationship with FDI, highlighting their nuanced or non-primary role as individual drivers in this context.

Rule of Law (RL): The rule of law consistently demonstrated a positive and significant relationship with FDI, indicating that strong legal frameworks remain important for investor confidence.

Voice and Accountability (VA): Voice and accountability also exhibited a consistent positive and significant relationship with FDI, suggesting that democratic participation can indeed enhance investor confidence when complemented by effective institutions.

These consistent results across multiple advanced estimation techniques including those specifically designed to handle complex panel data issues further validate the conclusions drawn from our traditional models and strongly support the methodological approach of this study. They underscore the necessity of adopting sophisticated panel econometric techniques when analyzing heterogeneous regions such as MENA, where simpler fixed-effects or random-effects models are likely to produce biased estimates.

Discussion

The empirical findings of this study provide valuable and detailed insights into the multifaceted determinants of FDI inflows throughout the diverse MENA region. These results are rigorously analyzed in relation to the theoretical frameworks previously established, particularly OLI framework, institutional theory, and transaction cost economics. Furthermore, they are carefully contextualized within the distinct socio-political and economic landscape of the MENA region.

The Role of Institutional Quality

One of the most significant and consistent findings of this study is the strong positive relationship between institutional quality and FDI inflows. Specific indicators, such as control of corruption (CC) and government effectiveness (GE), rule of law (RL) and voice and accountability (VA) exhibit statistically significant and positive coefficients across all estimators employed, including FMOLS, DOLS, CCEMG, and AMG. These findings provide robust empirical support for the predictions of both institutional theory and transaction cost economics, which posit that strong, transparent institutions mitigate uncertainty and reduce transaction costs for foreign investors, thereby significantly enhancing a country's attractiveness as an investment destination (Globerman & Shapiro, 2002; Sabir et al., 2019). In environments where property rights are protected, contracts are reliably enforced, and corruption is minimized, multinational corporations (MNCs) encounter fewer operational risks and experience greater predictability, fostering confidence in long-term commitments.

Within the unique context of the MENA region, these findings corroborate recent scholarly work, including that of (Awdeh & Jomaa, 2024; Azzaki et al., 2023; Bhujabal et al., 2024; Cieślik & Hamza, 2022; Mim & Saïdane, 2023). These studies collectively emphasize the pivotal role of ongoing institutional reforms in attracting and sustaining FDI, particularly within post-conflict or transitioning economies. Our results strongly suggest that policymakers aiming to bolster FDI should prioritize comprehensive governance reforms that enhance transparency, accountability, and regulatory effectiveness.

Natural Resources and the Enduring Resource Curse Hypothesis

The consistently negative and statistically significant coefficient of the availability of natural resources (ANR) variable provides robust empirical support for the “resource curse” hypothesis within the MENA region. Specifically, our findings indicate that higher natural resource rents are associated with diminished total FDI inflows. This suggests that, rather than uniformly attracting investment, resource wealth may deter diverse, long-term FDI due to associated phenomena such as rent-seeking behavior, neglect of broader institutional development, and an overreliance on volatile extractive industries. This conclusion aligns closely with the assertions made by (Chiyaba & Singleton, 2024; Elheddad, 2018; Lu et al., 2020), all of whom document a crowding-out effect of resource availability on non-extractive FDI. It distinctly underscores the imperative of implementing economic diversification initiatives and extensive governance reforms in resource-rich nations within the MENA region to attract investment beyond the primary sector. (Bhujabal et al., 2024) bolster this perspective by positing that institutional quality is pivotal in mediating the relationship between natural resource rents and FDI. This suggests that resource endowment can effectively translate into sustained and diverse sectoral investment only within contexts characterized by robust and transparent governance frameworks. Our findings align with the conclusions of (Mina, 2007; Rogmans & Ebbers, 2013), who identified that dependence on natural resources often hampers broader economic development by eroding institutional integrity and stifling innovation in alternative sectors. This stands in contrast to earlier studies that highlighted the allure of resource-based FDI while neglecting critical institutional dynamics.

The Influence of Macroeconomic Policy Variables

The results consistently indicate that inflation (INF) and the real interest rate (RIR) exert a significant negative influence on FDI inflows. An increase in either of these factors signals macroeconomic instability, elevates the cost of capital for potential investors, and subsequently diminishes overall investor confidence. This is particularly pronounced among firms evaluating stable environments for long-term projects that entail substantial sunk costs. These findings align closely with those presented by Al-Shakrchy et al. (2023); Kamal et al. (2023) and Khatabi et al. (2020), all of whom emphasize the importance of sound and predictable monetary policies in sustaining robust investment flows. High inflation, particularly, diminishes the actual returns on investment and generates considerable uncertainty regarding future economic conditions, thereby rendering host nations less attractive to foreign investors. Our findings further corroborate prior research conducted by Aziz and Mishra (2016) and Jabri et al. (2013), which underscore the susceptibility of FDI to macroeconomic stability. Additionally, we provide a nuanced contrast to several studies, such as Habash (2006) and Tan et al. (2021), which concluded that exchange rate fluctuations had no significant impact on the short run, potentially due to discrepancies in data coverage or estimation methodologies.

The exchange rate (EXR) variable demonstrates a positive and significant relationship with FDI. This indicates that currency depreciation may enhance export competitiveness and profitability for foreign investors primarily engaged in the tradable goods sector. However, the marginal significance observed suggests potential volatility in this relationship, which may be affected by broader macroeconomic conditions and industry-specific factors. . Our findings further corroborate prior research conducted by Al-Shakrchy et al. (2023); Aziz and Mishra (2016) and Burger et al. (2016).

Political Risk and Stability

While the majority of institutional quality indicators namely control of corruption, government effectiveness, rule of law, and voice and accountability demonstrate a clear positive and statistically significant impact on FDI inflows, the empirical results indicate that Political Stability (PS) and Regulatory Quality (RQ) are statistically insignificant across all estimators employed (FMOLS, DOLS, CCEMG, and AMG). This persistent lack of statistical significance suggests that, within the context of the MENA region and the specified time period, these broader indices of the political environment and regulatory frameworks may not exert a statistically significant influence on FDI inflows. Instead, it appears that international investors prioritize the fundamental characteristics of the domestic business environment and the principles of good governance over the degree of democratic participation or the mere existence of regulatory frameworks.

This finding implies that investors' perceptions of political risk are more accuratly captured by more specific institutional factors, such as the effectiveness of government, the control of corruption, and the predictability of the legal system, rather than by a generalized stability index. It is plausible that absence of overt corruption, coupled with efficient administration and robust legal frameworks, mitigates perceptions of political instability more than any singular broad indicator. Likewise, the apparent insignificance of regulatory quality suggests that the quality of enforcement and the predictability of regulations often anticipated within or rule of law are of greater importanace to investors than the mere existence of laws in isolation. These findings align with prior research on the MENA region, including studies by Gani and Al-Abri (2013); Kobeissi (2005) and Rogmans and Ebbers (2013), all of which contend that investor confidence is predicated on on tangible advancements in governance and economic freedom rather than on broader, occasionally superficial, political or regulatory frameworks.

Consequently, our results emphasize that strategic enhancements in bureaucratic efficiency, robust legal frameworks and policy coherence can serve as significant levers for augmenting FDI, even in politically complex environments.

Market Size and Economic Openness

Our findings consistently indicate that market size (MS) exerts a substantial and statistically significant positive effect on FDI inflows across all estimators employed (FMOLS, DOLS, CCEMG and AMG). The observed elasticities, which range from approximately 0.16% under the AMG estimator to over 4% under FMOLS and CCEMG, underscore the fundamental importance of market-seeking incentives in multinational investment decisions.

This outcome is congruent with the research conducted by Abonazel and Shalaby (2020) as well as Bassem (2025); El Fakiri and Cherkaoui (2024) and Khatabi et al. (2020), who demonstrate that larger domestic markets facilitate critical scale economies and attract investments through demand-side stimuli. Additionally, this finding strongly supports the Ownership-Location-Internalization OLI paradigm, wherein locational advantages such as population size, purchasing power, and overall economic activity significantly influence FDI location choices.

However, our results also present an intriguing point of comparison, particularly given the markedly reduced elasticity observed with the AMG estimator. This aligns with research conducted by Saad Alshehry (2020), which identified comparatively smaller impacts of market size in specific Gulf Cooperation Council (GCC) countries. This suggests that, while market size remains an essential indicator, its influence may be moderated by additional variables such as regional integration levels, infrastructure development, and the maturity of certain markets within the MENA region. Importantly, this implies that market size alone is frequently insufficient to attract diverse FDI unless it is effectively complemented by robust institutional and policy reforms, a significance that is consistently highlighted by other findings within this study.

Comparison With Prior Studies and Policy Implications

Discussion of Key Findings and Contributions

Our thorough analysis of determinants of FDI inflows in the MENA economies presents several findings that align with existing literature, while also providing unique contributions to the fiel of International Business as follows:

Consistency With Prior Reach

The study in hand, robustly confirms that market size remains a critial determinant for FDI inflows, which aligins with market seeking motives. Additionally, the analysis reveal consistent evidence that macroeconomic stability which characterized by lower interest rates and inflation levels are essintial for gaining foreign investors confindence and facilitating more captial inflows to the region. Furthermore, the results strongly supports the Dutch disease or resource curse hypothesis for MENA economies, which indicates that natural resource abundance may negatively affect FDI inflows by displacing these inflow in non extractive sectors.

Distinct Contribution of This Research

Our study distinguishes itself from previous studies in several significant ways, offering novel insights into FDI determinants in the MENA context:

I. Methodological rigor: Unlike previous panel studies that often failed to sufficiently account for CSD, SH and unobserved common facotrs, this novel applications of advanced estimators such as CCEM and AMG produces considerably more reliable and unbiased estimates. This methodological robustness underscores the consistency of our primary findings across various econometric specifications.

II. In depth institutional insights: The study in hand, extends the contributions of scholars such as Hassan (2017) and Jabri and Brahim (2015) by by systematically identifying the specific dimensions of institutional quality that exert the most significant influence on FDI inflows. The empirical findings consistently reveal a robust positive correlation between FDI inflows and control of corruption, rule of law, voice and accountability and government ecffectiveness. This comprehensive analysis underscores the multifaceted nature of governance reforms necessary to enhance the investment climate within the complex regional context of MENA economies.

III. Complex political risk assessment: This research interrogates the conventional, often reductionist perspective that positions aggregate political stability as a singularly significant determinant of FDI. Our findings consistently indicate that PS is statistically insignificant, implying that investors in the MENA region may prioritize more tangible aspects of the economic environment. This observation suggests that concerns regarding political risk are more accurately represented by the performance of institutions such as effective governance, reliable legal frameworks, and the absence of corruption rather than by broad indicators of political tranquility. This conclusion aligns with the work of Gani and Al-Abri (2013); Handoyo (2024); Kobeissi (2005) and Rogmans and Ebbers (2013), all of whom emphasize the intricate relationship between political factors and FDI in the region. Furthermore, the persistent insignificance of regulatory quality highlights that the effective enforcement and predictability of regulations not merely their existence are critical for fostering investor confidence.

Policy Implications and Managerial Insights

Our comprehensive findings significantly contribute to the expanding body of literature that emphasizes the necessity of profound institutional reform, coupled with consistent and predictable policy frameworks, as essential determinants for attracting and sustaining diversified FDI in emerging and often fragile economies, particularly within the MENA region. From a policy perspective, the findings elucidate several actionable insights for governments in the MENA region:

- Centrality of institutional reforms: Enhancing core governance indicators, such as control of corruption, government effectiveness, rule of law, and voice and accountability, is crucial for significantly improving the investment climate. These reforms directly alleviate investor uncertainty and diminish transaction costs.

- Economy diversification beyond natural resource dependence: Policymakers should implement structural reforms that promote economic diversification and mitigate the adverse effects associated with the resource curse. This necessitates the encouragement of non-extractive sectors and the establishment of a more balanced investment landscape.

- Maintenance of macroeconomic stability: Sustaining low inflation and appropriately managing real interest rates are vital for fostering investor confidence and promoting stable capital inflows.

- Leveraging market potential: Although often inherent, capitalizing on market size necessitates complementary reforms to maximize its attractiveness FDI.

For MNCs, the results suggests that investment decisions in the MENA region should extend beyond conventional indicators such as general political stability, aggregate market size, and resource availability. Instead, investors ought to prioritize comprehensive assessments of specific institutional and governance metrics as well as the tangible effectiveness of the domestic business environment.

Conclusion

This paper investigates the determinants of FDI inflows into the MENA region from 1980 to 2023. Employing advanced panel econometric methodologies, including FMOLS, DOLS, CCEMG and AMG estimators, this study reveals several significant insights regarding the impact of institutional quality, macroeconomic stability, political risk, and natural resource availability on FDI decision-making within this diverse and institutionally heterogeneous region.

Summary of Key Findings

Our key findings identifies consistently several critical factors influencing FDI in MENA. First, institutional quality, particularly in terms of control of corruption and government effectiveness, plays a pivotal determinant that significantly enhances the attractiveness of FDI, by reducing transaction costs and investor uncertainty. Second, macroeconomic stability, characterized by low inflation and sound real interest rates, is essential for sustaining investor confidence. Third, the availability of natural resources consistently exhibits a negative relationship with FDI inflows, providing a strong support for the "resource curse" hypothesis. Fourth, market size exerts a robust positive influence on FDI inflows, confirming the significance of market-seeking motives. Finally, exchange rate depreciation appears to facilitate FDI, whereas political stability and regulatory quality did not consistently demonstrate statistical significance, indicating that investors prioritize tangible governance rather than political narratives or mere presence of regulations. These findings are in alignment with recent empirical studies in the region such as Cieślik and Hamza (2022); Mim and Saïdane (2023) and Triki et al. (2022), thereby reinforcing the importance of robust governance and sound macroeconomic fundamentals in shaping FDI inflows within volatile and institutionally fragile settings like MENA.

Contribution and Policy Implications

This study contributes significantly to both academic literature and policy discourse. Methodologically, it rigorously addresses critical panel data challenges including CSD, SH, endogeneity and unobserved common factors through the innovative application of advanced estimators, thereby affirming the robustness of its core findings. Empirically it provides a complex, context-specific analysis of FDI determinants in MENA economies, systematically identifying key institutional dimensions beyond aggregate measures most influential in attracting FDI. The findings of this research reinforce the relevance of institutional theory in explaining FDI behavior in emerging economies while offering a priced perspective on political risk.

From a policy perspective, our results yield actionable insights for governments in the MENA region:

- Prioritize comprehensive institutional reforms: Enhancing transparency, reducing corruption, strengthening regulatory frameworks and maintaining sound accountability is vital for improving the business environment and boosting investor confidence, even in politically challenging settings.

- Promote economic diversification: Implementing structural reforms to mitigate the resource curse fostering non-extractive sectors is critical.

- Maintain macroeconomic stability: Sustaining sound monetary and fiscal policies which controls inflation, and interest rates, are paramount and vital for improving investment climate and significantly reduces operational risks for multinational enterprises, thereby increasing investor confidence.

- Improve regulatory quality: Even in the absence of large-scale political change, strengthening bureaucratic efficiency, legal enforcement, and contract reliability can serve as powerful strategic levers for boosting FDI. Investors often value predictable and efficient regulatory environments over broad political narratives.

- Encourage regional cooperation and trade liberalization: Reducing trade barriers and enhancing regional economic integration can create larger, more predictable markets for foreign firms, which is particularly beneficial for smaller or conflict-affected economies within the region.

- Leverage market potential strategically: Market size advantages should be complemented with supportive policies and infrastructure.

Limitations and Directions for Future Research

This study significantly contributes to the understanding of the determinants of foreign direct investment (FDI) in the Middle East and North Africa (MENA) region. However, several limitations must be acknowledged, as they delineate the boundaries of our findings and suggest promising avenues for future inquiry.

First, the temporal scope of our analysis (1980–2023) does not encompass post-2023 global developments that are reshaping FDI dynamics, including shifts in global supply chains, the acceleration of green and digital investments and recent geopolitical disruptions in the region. Future research should extend the time frame to incorporate these contemporary shocks, including the lingering effects of the pandemic, energy crises and evolving regional conflicts, to assess their impact on FDI inflows into MENA economies.

Second, data constraints have restricted the granularity of our analysis. The unavailability of consistent subnational governance indicators, firm-level FDI data and sector-disaggregated investment flows across the full sample precludes a more nuanced examination of industry-specific determinants. Furthermore, aggregating FDI across all sectors may obscure critical differences among extractive industries, manufacturing, services and emerging green investments. Future studies should adopt a sectoral approach to elucidate how variables such as digital infrastructure, innovation capacity, environmental regulations and sustainability indicators influence location decisions. Additionally, incorporating more refined measures such as infrastructure reliability, total factor productivity (TFP) and capital openness would significantly enhance empirical models of FDI determinants.

Third, while we employed advanced second-generation panel estimators to address cross-sectional dependence and heterogeneity, certain unobserved country-specific effects may still influence our results. Future research could leverage alternative methodologies, such as the cross-sectionally augmented autoregressive distributed lag (CS-ARDL) model or dynamic common correlated effects (DCCE) estimators with panel-corrected standard errors (PCSE), to more effectively address endogeneity, non-stationarity and mixed-order integration. Such approaches would yield more robust estimates of both short- and long-run relationships.

Finally, our analysis primarily focused on conventional institutional and macroeconomic factors, which may underrepresent the significance of complex socio-political dynamics. Future work should expand the set of explanatory variables to include measures such as corruption distance (between home and host countries), conflict intensity (differentiating between types of violence and their differential impacts on investor behavior) and religious or sectarian tensions. Moreover, the influence of political Islam on government effectiveness and foreign investment policy formulation in MENA countries remains underexplored and warrants dedicated investigation. Beyond variable expansion, theoretical innovation is also necessary; alternative frameworks such as transaction cost theory (TCT), the Uppsala model, network theory, the market imperfections approach and the resource-based view (RBV) should be empirically tested and adapted to the unique institutional and geopolitical context of the MENA region.

By addressing these limitations through more granular data, advanced methodologies, and broader theoretical and contextual lenses, future research can enhance our understanding of FDI determinants and support more effective, evidence-based policy design in the MENA region.

Footnotes

Acknowledgements

The authors are very grateful to the editor and anonymous referees for their insightful and valuable suggestions that have led to an improved version of this paper.

Ethical Considerations

This study is based on publicly available secondary data and does not involve human or animal participants. Therefore, formal ethical approval was not required.

Consent to Participate

No informed consent was required, as this research uses anonymized, aggregated data from public international databases and does not involve interaction with human subjects.

Author Contributions

All authors contributed to the study conception and design. Material preparation, data collection and analysis were performed by correspondent Author. The first draft of the manuscript was written by correspondent Author. Second and third authors (respectively) commented on previous versions of the manuscript. All authors read and approved the final manuscript.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability

The data used in this study are publicly available from the World Bank’s World Development Indicators (WDI) and the Worldwide Governance Indicators (WGI) databases. No proprietary or confidential data were used.