Abstract

As an important fiscal policy of local governments, local government borrowing has an increasingly prominent impact on micro-enterprises. However, there is still a lack of effective verification on whether local government debt (LGD) will affect the Environmental, Social, and Corporate Governance (ESG) performance of enterprises. This paper uses micro data of Chinese listed companies from 2011 to 2020 and LGD data at the prefecture-level city layer to test the impact and mechanism of the expansion of LGD on corporate ESG performance by establishing panel regression models and mediating effect models. The results show that the expansion of LGD significantly reduces the ESG performance of local enterprises and presents a long-term inhibitory effect. The mechanism analysis indicates that the expansion of LGD suppresses corporate ESG performance by crowding out corporate credit resources, reducing government fiscal subsidies to enterprises, thereby worsening corporate cash flow. Furthermore, the negative impact of LGD expansion on corporate ESG performance is more pronounced in non-state-owned enterprises, those with high leverage, high industry competition, high technological intensity, low marketization, and low financial development levels. Furthermore, the expansion of LGD mainly reduces corporate social and environmental responsibility but has no significant impact on internal governance. The inhibitory effect of LGD on ESG is not caused by publicly issued urban investment bonds but stems from non-publicly issued debts. This paper extends the research on the microeconomic consequences of LGD to the field of corporate ESG, providing insights for comprehensively assessing the risks of LGD and promoting the construction of corporate ESG.

Introduction

Since the outbreak of the global financial crisis in 2008, under the influence of national macroeconomic policies, Chinese local governments have rapidly expanded local government debt (LGD) through the establishment of financing platforms, gradually highlighting the risks associated with LGD (J. Zhu et al., 2022). In recent years, affected by the COVID-19 pandemic and changes in the international and domestic environment, the growth rate of the real economy has continuously slowed down, and the rigid expenditures of local governments have continued to increase. With the promotion of proactive fiscal policies by the state, the scale of LGD has reached a new high. According to data from the Ministry of Finance, by the end of December 2022, the balance of China’s LGD amounted to 35.06 trillion yuan, a 4.29-fold increase from 2008. LGD, as an important fiscal policy for mobilizing social funds and covering fiscal deficits, plays a significant role in promoting infrastructure construction and economic growth (DeLong et al., 2012; Panizza & Presbitero, 2014). However, it is worth noting that a large body of global research indicates that the expansion of LGD squeezes fiscal resources, thereby affecting the investment and financing activities of enterprises (Croce et al., 2019; Demirci et al., 2019; Y. Huang et al., 2020).

With the setting of “dual carbon” goals and the proposal of the new development concepts of “innovation, coordination, green, openness, and sharing,” China has placed great emphasis on the construction of ecological civilization, and the concept of green and sustainable development has been deeply rooted in people’s hearts (W. Chen et al., 2022; Mao & Failler, 2022). Enterprises are the basic units of economic and social development transformation and the backbone of sustainable development. To measure the sustainable development capability of enterprises, the performance of enterprises in environment, social, and governance (ESG) has attracted widespread attention (F. He, Ding, et al., 2023; Umar et al., 2020). The concept of ESG, originating from ethical investment and responsible investment (Michelson et al., 2004), refers to the performance of enterprises in ESG aspects and has become one of the important indicators for evaluating the sustainable development of enterprises (C. Cai et al., 2023; Chang et al., 2023; Ren et al., 2023). In practice, capital is a key element for enterprises to undertake ESG construction, and activities such as environmental investment require substantial capital input (Porter & Linde, 1995). The expansion of government debt and the resulting squeeze on corporate funds may have a significant impact on corporate ESG activities.

Currently, few studies have explored the impact of local governments behavior on corporate ESG from the perspective of local governments, with more research focusing on the role of LGD in enterprise development and innovation, and there is no consensus in the literature. On one hand, some scholars have pointed out that the formation process of LGD mainly relies on the financial system, and the high correlation between finance and fiscal policy reduces the accessibility of corporate sector to funds from the financial sector, squeezes out corporate R&D investment, and the expansion of LGD also increases corporate financing costs, negatively affecting the overall development of enterprises (Fan et al., 2022; Y. Huang et al., 2020; Y. Liang et al., 2017). On the other hand, some scholars have noted that LGD directed toward infrastructure construction such as transportation promotes urban economic development and the flow of human and material capital resources between regions (Siddiqui & Malik, 2001), enhancing the spillover effect of knowledge between regions. Enterprises benefit from the spillover effect, saving R&D time and costs, increasing innovation investment, and improving their total factor productivity, thus gaining a more advantageous position in market competition (Gilbert et al., 2008). Given the divergent views in existing research, this paper seeks to explore whether the expansion of LGD affects corporate ESG, what the impact is, and what the mechanism of action is. Further, which specific ESG indicators are most affected by changes in LGD? Are there specific debt factors that have a greater impact on ESG aspects? Does the expansion of LGD have a differentiated impact on the ESG of different enterprises, industries, and regions? Answering these questions not only helps to expand research in the fields of LGD and ESG but also provides theoretical support and practical guidance for listed companies to further improve their ESG systems and practice ESG concepts to promote high-quality enterprise development.

To answer these questions, this paper selects data from Chinese A-share listed companies from 2011 to 2020 as research samples, first examining the impact of LGD on corporate ESG performance and its mechanisms. The results show that the expansion of LGD, by crowding out corporate credit resources and reducing government financial subsidies to enterprises, deteriorates the cash flow of enterprises, ultimately suppressing corporate ESG performance. Moreover, based on differences at the enterprise level, industry level, and regional level, the paper conducts a heterogeneity analysis, finding that the impact of LGD on ESG is more pronounced in non-state-owned, high-leverage, high-competition, high-technology-intensive enterprises, and in regions with low marketization and low financial development levels. Finally, the paper analyzes the impact of LGD on the three sub-indicators of ESG and the impact of different types of debt on corporate ESG, finding that LGD mainly reduces corporate responsibility for social and environmental issues, but its impact on internal governance is not significant. Meanwhile, compared to publicly issued debt, privately issued debt has a greater impact on ESG.

The potential marginal contributions of this paper are as follows: First, this study enriches ESG-related research from a macro-level perspective. Existing literature mainly examines the impact of internal financial characteristics, management characteristics, and external economic development, financial development, etc., on corporate ESG (Aabo & Giorici, 2022; Y. Cai et al., 2016; H. Liang & Renneboog, 2017; Post et al., 2011; Ren et al., 2023), while this paper, from the perspective of local fiscal conditions, explores the impact of local government financing behavior on corporate ESG and its transmission pathways, providing a new literature supplement to the factors affecting corporate ESG.

Second, this study extends the breadth of research on the impact of LGD on micro-enterprises. Since the outbreak of the international financial crisis in 2008, under the promotion of proactive fiscal policies, the scale of LGD has rapidly climbed, and the economic consequences of high government debt, especially LGD, have attracted widespread attention from scholars. Current literature on the impact of LGD on enterprises mostly focuses on the role of LGD on corporate investment, financing, innovation, and other financial indicators (Fan et al., 2022; Gao et al., 2021; S. Li & Qi, 2023; Y. Liang et al., 2017; J. Wang et al., 2020), with few studies paying attention to the impact of LGD on corporate social and environmental responsibility. This paper explores the impact of LGD on corporate ESG, filling this research gap and enriching the literature on the impact of LGD on enterprises.

Finally, the contribution of this paper also lies in enriching the research on macro-microeconomic cross-disciplinary topics. In emerging and transition economies, the degree of government intervention in the macroeconomy and micro-enterprises is high, making the relationship between macroeconomic policy and micro-enterprise behavior an important topic of interest for scholars. Using Chinese listed companies as a sample, this paper builds a “macro policy-micro enterprise behavior” analysis framework from a macro-micro integrated perspective, expanding the research on macro-micro integrated economic propositions. Moreover, the research of this paper also provides certain references for other emerging and transition economies with a high degree of government intervention.

Literature Review and Theoretical Hypothesis

Literature Review

Research on Local Government Debt

Local government debt, a component of overall government debt, is the financial obligation undertaken by local governments to achieve government objectives, requiring local fiscal funds for debt repayment (J. Zhu et al., 2022). In recent years, the rapid expansion of LGD has drawn widespread attention from scholars. Literature related to LGD mainly focuses on the causes of its expansion and the consequences thereof. Regarding the causes of LGD expansion, studies have approached it from several angles: Firstly, from the perspective of promoting economic development, existing research suggests that various institutional arrangements aimed at recovering and promoting economic development have led to the rapid growth of LGD (Y. Liang et al., 2017). Secondly, from the perspective of fiscal systems, some studies have identified the devolution of fiscal rights as a key factor contributing to debt accumulation (Alesina & Passalacqua, 2016; S. Guo et al., 2022; Neyapti, 2010). Thirdly, from the perspective of intergenerational equity, it has been argued that government financing through bond issuance can spread investment costs across generations, thereby lightening the burden on the current population and contributing to intergenerational equity (Alesina & Tabellini, 1990). Besides these factors, soft budget constraints (Catrina, 2012; Krol, 1996; Qian & Roland, 1998) and political promotion incentives (G. Guo, 2009) are also cited as causes for the expansion of debt.

The fundamental purpose of local government borrowing is to develop the local economy and promote economic growth. Hence, there has been extensive and rich discussion among scholars about the impact of LGD on economic growth, but no consensus has been reached. Some scholars believe that local governments, by incurring debt, can invest in public service areas that private capital is reluctant to enter, improve public infrastructure, and ultimately stimulate economic growth (Kaas, 2016). Other scholars argue that, in the long term, the accumulation of LGD crowds out private investment, ultimately suppressing economic growth (Mitze & Matz, 2015; Teles & Mussolini, 2014). Yet others suggest that the impact of LGD on economic growth is nonlinear (Law et al., 2021). Additionally, some studies have explored the impact of LGD on financial risk (W. J. Zhao & Zhang, 2021; Y. Zhao et al., 2022), urbanization (S. Li & Cao, 2020).

Regarding the impact of LGD on micro-enterprises, most research has focused on financial indicators such as corporate innovation (Fan et al., 2022; S. Li & Qi, 2023), corporate leverage (Y. Liang et al., 2017; J. Wang et al., 2020), corporate investment (Y. Huang et al., 2020), corporate tax burden (Tang et al., 2023; Peng & Lin, 2024), and corporate productivity (J. Zhu et al., 2022). Currently, only a few scholars have explored the impact of LGD on non-financial indicators such as corporate environmental protection, green innovation, and social responsibility fulfillment. For example, W. Chen et al. (2022) indicated that the expansion of LGD negatively affects corporate green innovation. Wan et al. (2024), using Chinese listed companies as a sample, found that LGD is negatively correlated with local corporate social responsibility performance, indicating that government debt financing behavior suppresses corporate social responsibility participation. W. Tang et al. (2022) also suggested that the expansion of LGD scale reduces the willingness and performance of companies in fulfilling social responsibilities. Zhou et al. (2023) explored the relationship between LGD and corporate pollution emissions, observing that an increase in LGD heightened the intensity of pollutant emissions.

There are three main ways to measure local government debt. The first is to adopt the cash balance equation of investment amount (W. Chen et al., 2022). This method adopts the method of estimation, based on the basic principle of equality of input and expenditure, and believes that the total investment in fixed assets should be equal to the sum of various sources of funds, and derives the amount of local government debt according to this principle. This method is easy to understand and calculate, but the disadvantage is that it is not accurate. The second is to use urban investment bonds as a proxy variable for local government debt (Peng & Lin, 2024, Zhou et al., 2023). The main reason for adopting this method is that among the various types of debts borrowed by financing platform companies, compared with non-standardized financing methods such as bank loans, trust financing, and financial leasing, the data of bonds issued by financing platforms (i.e., urban investment bonds) are relatively transparent and easy to obtain. However, since urban investment bonds only account for a portion of the financing platform’s debt, adopting this approach would underestimate the size of the debt. Third, the interest-bearing debt of financing platforms is used as a measure of local government debt (Fan et al., 2022; Y. He, Ma, et al., 2023; Liu et al., 2023; Xu et al., 2021). At present, this method is recognized and used by more and more scholars, and has gradually become the mainstream method of measuring local government debt.

Corporate ESG Research

ESG, which integrates socio-economic development, environmental protection, corporate governance, and social responsibility, aligns closely with the construction of ecological civilization and the concept of sustainable development, holding significant theoretical value and practical significance for achieving sustainable development in society and the economy (Z. Li et al., 2022). ESG performance is widely recognized as important non-financial information, serving as a key indicator for measuring sustainable development of enterprises on the international stage (Burke, 2022; K. Wang et al., 2023). Specifically, “E” represents the responsibility of enterprises in environmental protection, including reducing pollution and innovating green products. “S” represents the active assumption of social responsibility by enterprises, maintaining good relationships with stakeholders, including labor standards, product liability. “G” represents corporate governance, including governance mechanisms and behaviors (Michaud & Magaram, 2006).

Currently, scholars have conducted rich research on corporate ESG, focusing mainly on exploring its economic consequences. For instance, good corporate ESG performance can reduce financing costs (Chang et al., 2023), promote innovation (Dong et al., 2022), alleviate financial risks (Broadstock et al., 2021; Sassen et al., 2016), reduce the risk of stock price crashes (Murata & Hamori, 2021), and enhance corporate value (Chelawat & Trivedi, 2016; Duque-Grisales & Aguilera-Caracuel, 2021). It is clear that the ESG concept not only represents corporate social responsibility but also embodies value creation for enterprises, showcasing the positive externalities of enterprises as market entities. Good ESG performance by enterprises not only promotes sustainable development in society and the environment but also drives internal growth, enhances brand effect and resilience against risks, and strengthens investor confidence. Therefore, identifying factors that affect corporate ESG construction and ratings is particularly important. Furthermore, only a few studies have examined the drivers of corporate ESG performance from macro or micro perspectives. From a micro perspective, scholars have explored the impact of corporate size (Drempetic et al., 2020), management characteristics (Aabo & Giorici, 2022; McCarthy et al., 2017; Post et al, 2011), and equity features (Dyck et al., 2019; Z. Li et al., 2021) on corporate ESG. From a macro perspective, studies by Cai et al. (2016), Liang and Renneboog (2017), Ren et al. (2023) have examined the effects of economic development, legal systems, digital finance, and other factors on corporate ESG.

The literature above provides a solid foundation for this study, but the following issues remain: (1) In the field of LGD research, while the drivers of LGD and its macroeconomic effects have been extensively explored, the ecological and environmental impacts have not received sufficient attention, particularly whether LGD financing leads to changes in corporate ESG behavior, which warrants further investigation. (2) In the field of corporate ESG research, few scholars have examined LGD as a driving factor for corporate ESG performance from a governmental perspective, especially in terms of its internal mechanisms affecting corporate ESG performance. This study posits that enterprises, as the micro-bearers of regional development, play a decisive role in positively responding to regional policies and promoting green governance through their strategic deployment and investment philosophies. Therefore, clarifying the transmission channels through which LGD expansion affects corporate ESG, and revealing the mechanisms by which LGD influences corporate strategic development, are significant.

Theoretical Hypothesis

Local Government Debt and Corporate ESG Performance

Corporate ESG evaluates enterprises’ performance in environmental, social, and corporate governance aspects, requiring businesses to take responsibility and act in environmental protection, social responsibility, and corporate governance (F. He et al., 2022; Mu et al., 2023; W. Zhu et al., 2024). The expansion of LGD affects corporate ESG from the perspectives of debt sources, debt allocation, and debt repayment.

From the perspective of debt sources, local government borrowing impacts the allocation of credit resources, reducing the availability of external financing for enterprises through price and capital competition mechanisms, thereby increasing corporate financing costs and leading to more severe financing constraints (Croce et al., 2019; Demirci et al., 2019; Y. Liang et al., 2017). Since ESG construction requires financial support, insufficient cash flow can suppress enterprises’ willingness to improve the environment, undertake social responsibilities, and conduct corporate governance (Lys et al., 2015; Wan et al., 2024; Zhou et al., 2023).

From the perspective of debt allocation, LGD is mainly used for public investments such as infrastructure construction (S. Li & Cao, 2020). Improved infrastructure helps businesses reduce transportation costs, expand product market size, and enhance scale economies. However, infrastructure investment can lead to higher financial market interest rates (Cavallo & Daude, 2011), increasing financing costs and making enterprises more inclined to choose short-term projects over sustainable ESG projects. At the same time, excessive investment and redundant construction not only result in severe resource waste but also cause significant economic fluctuations, worsening the external economic environment (Woo & Kumar, 2015). Enterprises in unstable, high-risk economic environments may adopt more opportunistic behaviors, lowering their ESG performance (Rhee et al., 2021; Shrestha & Naysary, 2023).

From the perspective of debt repayment, local government borrowing strengthens reliance on land finance, and the resulting rise in housing prices leads to more credit resources flowing to the real estate sector (Han & Kung, 2015), distorting corporate investment structures and reducing investment in ESG. Based on the above, this paper proposes the following hypothesis:

Hypothesis 1: The expansion of LGD scale suppresses corporate ESG performance.

Mechanism of LGD Affecting ESG Performance

Given China’s underdeveloped financial system, bank loans remain the primary source of funding for corporate investment activities (Allen et al., 2017; Wan et al., 2024). For government departments, the funding source for LGD also primarily comes from bank credit (Y. Huang et al., 2020; M. Y. S. Zhang & Barnett, 2014). Thus, in a specific region, due to the fixed total amount of credit resources, there is a competitive effect between credit resources available to government departments and those available to the corporate sector (Wan et al., 2024). When government debt increases, to ensure timely debt repayment, government departments can negotiate with local financial institutions to obtain credit resources preferentially, thereby reducing the credit funds available to enterprises (Y. Guo et al., 2016; Lugo & Piccillo, 2019; Su et al., 2015). Also, local government borrowing mainly targets long construction cycles and large capital demands in urban infrastructure and transportation (Gao et al., 2021; Tao, 2015), leading to a long-term occupation of bank credit funds, further exacerbating corporate financing constraints and lowering the level of corporate ESG investment. Accordingly, this paper proposes the following hypothesis:

Hypothesis 2: The expansion of LGD reduces corporate ESG by decreasing the scale of corporate credit.

From the theory of economic externalities, the ecological environment is a public good with unclear property rights. If a company undertakes ESG construction and improves environmental performance, other companies or residents can enjoy the benefits brought by the environmental improvement without compensation, where the private marginal cost often exceeds the social marginal cost. Therefore, from the perspective of rational agents, there is insufficient motivation for companies to engage in ESG, and appropriate government intervention must be taken to exert a facilitating effect (Ge et al., 2022). Government subsidies, as the “visible hand” of the government department to compensate for market failures and guide resource allocation, can intervene in the market, directly increase corporate cash flow, provide financial support for ESG construction, and motivate companies to engage in ESG construction (Yu et al., 2023). However, when the scale of LGD expands, with unchanged fiscal revenue, local governments may choose to reduce fiscal expenditures to repay debt on time (Acharya et al., 2012; Xu et al., 2021). As fiscal subsidies decrease, on one hand, it directly reduces the cash flow available for ESG construction, leading to a lower level of corporate ESG. On the other hand, it sends a negative signal to the market, limiting corporate financing channels (J. Chen et al., 2018), leading to insufficient funds for ESG construction, and ultimately suppressing corporate ESG performance. Accordingly, the following hypothesis is proposed:

Hypothesis 3: The expansion of LGD will lower corporate ESG by reducing corporate fiscal subsidies.

As the scale of LGD expands, the fiscal pressure on local governments increases (S. Li et al., 2018), and to increase fiscal revenue to alleviate the fiscal burden, government departments may increase the tax collection intensity on companies, raising fiscal revenue through increased tax income (W. Chen et al., 2022; G. He et al., 2020). Moreover, as local government’s debt repayment pressure rises, companies will not only be subject to higher taxes and fees but also face stricter tax regulation by tax authorities, restricting corporate tax planning activities. Facing a heavier tax burden, companies will prioritize their day-to-day production and operation activities, seeking financial performance optimization through investment in profitable projects, with insufficient investment motivation for environmental protection, social responsibility fulfillment, etc. (Zhou et al., 2023), ultimately leading to a decline in the ESG level. Based on this, the following hypothesis is proposed:

Hypothesis 4: The expansion of LGD will lower corporate ESG by increasing the corporate tax burden.

Data and Empirical Design

Data Source and Sample Selection

This paper uses data from Chinese A-share listed companies from 2011 to 2020, matched with prefecture-level LGD data as the research sample. Corporate-level data are sourced from the China Stock Market & Accounting Research Database (CSMAR), regional-level data from the National Bureau of Statistics, and LGD data from the WIND database. In processing the data, this paper follows the practices of existing literature, excluding financial and ST (Special Treatment) companies and samples with missing data during the sample period.

Empirical Design

To investigate the impact of LGD on corporate ESG, we construct a fixed-effects model that includes a series of variables at both the corporate and regional levels (Hong et al., 2023; Hsu et al., 2014; Zhou et al., 2023). The model is set up as follows:

where, ESGit is the dependent variable, representing the ESG of company i in year t. Debtmt is the explanatory variable, indicating the scale of government debt in the city m where company i is in year t. Controls are other control variables. δi represents individual fixed effects, φt represents time fixed effects, and εit is the random error term. If the hypothesis is valid, the regression coefficient β < 0 and significant, suggesting that the larger the scale of LGD in a company’s location, the lower the company’s ESG performance.

To further explore the mechanisms through which LGD affects corporate ESG, we use the methodology described by Hsu et al. (2014), Gomber et al. (2018), and Cao et al. (2021) to construct models: First, regressing LGD on ESG as shown in Model (1); second, regressing LGD on mediating variables as shown in Model (2); third, incorporating the mediating variables into Model (1) and regressing both LGD and the mediating variables on ESG as shown in Model (3).

The mediating variables Mit are credit scale, government subsidies, and corporate tax burden. The steps to test for mediating effects are as follows: If β significant in Model (1), proceed with regressions for Models (2) and (3). If both coefficients for the mediating variables β1, ω are significant, a mediating effect exists. If β1, ω at least one of the coefficients is not significant, further testing using the Sobel test is required.

Variable

Explained Variables

Corporate ESG performance. Referring to the research of W. Li and Pang (2023), Ren et al. (2023), Q. Huang et al. (2022), and W. Chen et al. (2022), this paper obtains corporate ESG rating data from Bloomberg. Bloomberg began monitoring and assessing global companies’ ESG issues relatively early. It conducts ESG ratings through collecting data from multiple sources, including annual reports, sustainability reports, and corporate websites. The rating system uses both quantitative and qualitative methods to rate ESG situations, with scores ranging from 0 to 100. Higher scores indicate better quality of ESG-related information of the listed companies. The rating system assigns equal weight to the three primary indicators: environmental, social, and governance, each constituting one-third of the score. The environmental category includes seven secondary indicators such as energy, air quality, and waste management; the social category includes six, such as community and customer, health and safety, and supply chain; and governance includes eight, such as diversity, board composition, and compensation clauses. The Bloomberg database ultimately provides a comprehensive ESG rating score and scores for the environmental, social, and governance dimensions, covering over 100 countries and regions and approximately 13,000 companies, which represents 88% of the global market value. Moreover, this paper also considers using the Huazheng ESG rating for robustness checks, which has also been widely applied (Chang et al., 2023; Mu et al., 2023; X. Zhang et al., 2023).

Explanatory Variables

Local government debt. Currently, China’s LGD is mainly divided into two parts: one part consists of bonds issued by provincial governments with clear budget constraints, known as “within-system” local government bonds, after the implementation of the new Budget Law and issued by the Ministry of Finance. The other part consists of interest-bearing debts of financing platforms primarily based on local investment and financing platforms, including non-standardized debts raised through bank loans, PPP, trusts, and financial leasing, and standardized debts mainly in the form of urban investment bonds (Zhou et al., 2023).

Referencing Y. Huang et al. (2020) and Liu et al. (2023), this paper selects the interest-bearing debt of local financing platforms as the proxy variable for local government debt. The reasons are twofold: firstly, local government bonds undergo strict government approval at issuance, are subject to strict budget constraints, and are guaranteed by government fund income and tax revenue, while the interest-bearing debts of local financing platforms have lower transparency and lack stable funding sources. Therefore, compared to government bonds, the hidden debt risks of local financing platforms, which lack supervision and have higher repayment risks, have a greater impact on the real economy. Secondly, local government bonds are issued by provincial governments, while debts of local financing platforms can be independently raised and issued by prefecture-level cities. Therefore, using the interest-bearing debt of local financing platforms can more accurately reflect the essence and differences of LGD between prefecture-level cities.

The specific measurement of the LGD variable first involves retrieving the list of city financing platforms from the Wind database. Then, the interest-bearing debt data of the financing platforms are summed up to their respective cities, thus obtaining the scale of LGD at the prefecture-level city. Finally, the logarithm of the debt scale is taken as the proxy variable for local government debt, represented by Debt.

Mediating Variables

The mediating variables selected in this paper include corporate credit size, government subsidies, and corporate tax burden. Corporate credit size is measured by the ratio of interest-bearing debt to total debt. Government subsidies refer to the government grants noted in the financial statement footnotes under profit and loss items, summing up the government subsidies received by each sample company in the year. To eliminate the scale effect, the government subsidies are logarithmically transformed. Corporate tax burden is the sum of value-added tax, business tax and surcharges, and income tax, which is also logarithmically transformed.

Control Variables

Following the practices in existing literature (F. He, Ding, et al., 2023; Mu et al., 2023; Wan et al., 2024; Yang et al., 2023), this paper selects a series of variables at the enterprise and city levels as control variables, including enterprise size (Size), measured by the natural logarithm of total assets at the end of the period; leverage ratio (Lev), measured by the ratio of total liabilities to total assets at the end of the period; fixed asset investment (Fix), measured by the ratio of net fixed assets to total assets; the shareholding ratio of the largest shareholder (First), measured by the ratio of the number of shares held by the largest shareholder to the total number of shares; return on assets (Roa), measured by the ratio of net profit to total assets at the end of the period; property rights (Owner), assigned 1 if a state-owned enterprise, otherwise 0; book-to-market ratio (MB), measured by the ratio of total assets to market value; operating cash flow (Cashflow), measured by the ratio of net cash flow from operating activities to total assets; economic condition of the enterprise’s city (GDP), measured by the GDP of the region where the enterprise is located; foreign direct investment (Fdi), measured by the ratio of foreign direct investment to GDP in the region where the enterprise is located; population size (Pop), taking the natural logarithm of the total population at the end of the year in the region where the enterprise is located. Additionally, time fixed effects and firm fixed effects are controlled.

The specific meanings and measurements of each variable are presented in Table 1.

Variable Definitions.

Summary Statistics

Table 2 reports the statistical characteristics of the main variables. From the table, the mean value of corporate ESG is 20.803, with a minimum value of 1.239 and a maximum value of 60.743, indicating a significant variation in ESG among the sampled firms. The mean value of LGD (Debt) is 0.3011, with a minimum value of 0 and a maximum value of 4.563, and a standard deviation of 1.299, showing large fluctuations and indicating substantial differences in government debt levels across regions.

Summary Satistics.

Empirical Analysis

Baseline Results

Table 3 presents the regression results of the baseline model. Column (1) considers only the univariate effect of LGD on corporate ESG, controlling solely for time fixed effects. Columns (2) to (4) show the regression analysis results after progressively including individual fixed effects, firm-level, and city-level control variables. It is evident across all regression outcomes that the coefficient of the core explanatory variable, LGD (Debt), is significantly negative at least at the 5% level, suggesting that, overall, the expansion of LGD suppresses corporate ESG, thereby confirming Hypothesis 1. From an economic standpoint, taking column (4) as an example, the coefficient for LGD is −1.062, indicating that a 1% increase in LGD reduces corporate ESG by 1.062%. The enlargement of LGD may constrain corporate ESG by consuming regional credit resources and exacerbating firms’ financing constraints, thereby worsening firms’ cash flows. Our study results align with previous findings that government revenue and debt are significant factors revealing the ecological footprint (Ramzan et al., 2023). Zhou et al. (2023) explored the relationship between LGD and corporate pollution emissions, observing that an increase in LGD heightened the intensity of corporate pollutant emissions. Wan et al. (2024) discussed the impact of LGD on local corporate social responsibility, finding a negative correlation between LGD and local corporate social responsibility performance, indicating that government debt financing behavior suppresses corporate participation in corporate social responsibility. Since both environmental and social responsibilities are crucial components of ESG, it follows that the increase in LGD adversely affects corporate ESG performance.

Baseline Results.

Note. Figures in parentheses are the robust standard errors.

, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

The results demonstrate that the expansion of LGD suppresses corporate ESG performance. Therefore, it is crucial for policymakers to consider whether the suppressive effect of LGD on corporate ESG is merely short-term or if it will pose a long-term obstacle to corporate ESG performance. To examine the dynamic impact of the expansion of LGD on corporate ESG, this paper processes LGD with lags (lags 1–4), with the results as shown in Table 4. It can be observed that the estimated coefficients of the core explanatory variable (Debt) pass the significance tests across lags 1 to 4. This indicates that, despite the unavoidable diminishing marginal effects over the long term (the absolute value of the LGD coefficient decreases, indicating a diminishing suppressive effect on corporate ESG: |−0.651| > |−0.476| > |−0.396| > |−0.153|), the suppressive effect of LGD on corporate ESG remains robust over the long term. This further validates the reliability and robustness of the conclusion that LGD suppresses corporate ESG.

Dynamic Impact of LGD on Corporate ESG.

Note. Figures in parentheses are the robust standard errors.

, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Endogeneity Tests

This paper employs the following methods to mitigate potential endogeneity issues.

(1) Use of the instrumental variable (IV) method. Following Demirci et al. (2019), this paper selects healthcare expenditure from public fiscal spending as an instrumental variable for LGD and uses the two-stage least squares (2SLS) method for the instrumental variable regression, with results shown in Table 5 columns (1) and (2). Column (1) shows the results of the first stage regression, where the regression coefficient of the instrumental variable (IV) is significantly positive at the 1% level. This indicates that an increase in healthcare spending in a region leads to an expansion of LGD in that area, confirming the relevance assumption of the instrumental variable. Column (2) shows the results of the second stage regression, where the coefficient of LGD (Debt) is significantly negative at the 10% level. This suggests that after addressing potential endogeneity issues using an instrumental variable, the conclusion still holds, namely, that the expansion of LGD significantly reduces corporate ESG.

(2) Use of the system GMM model. The system GMM method eliminate the endogeneity bias that may arise in static panel data models to some extent and has been widely applied in empirical analysis (Law et al., 2018; Sun & Chen, 2022; J. Zhu et al., 2022). The regression results shown in Table 5 column (3) indicate that the p-values for the AR (1) autocorrelation test are 0, the p-values for the AR (2) are greater than .1, and the p-values for the Hansen test are greater than .1, suggesting that the system GMM model constructed in this paper is appropriate. Observing the coefficient of LGD (Debt), it is significantly negative, indicating that using the system GMM model, the core conclusion still valid, that is, the expansion of LGD suppresses corporate ESG.

Endogeneity Tests.

Note. Figures in parentheses are the robust standard errors.

, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Robustness Test

To further validate the effectiveness of the research results, this paper conducts robustness tests using the following methods:

(1) Changing the measurement method of the explanatory variable. By using the ratio of LGD size to GDP as a proxy variable for local government debt, the model (1) is re-regressed, and the results are shown in Table 6 column (1). It is observed that after changing the measurement method of the explanatory variable, the relationship between LGD and ESG remains significantly negative.

(2) Changing the measurement method of the dependent variable. The robustness test is conducted using the Huazheng ESG rating data instead of the measurement indicators used in the main regression. The regression results shown in Table 6 column (2) indicate that the impact coefficient estimate of LGD on corporate ESG performance remains significantly negative.

(3) Excluding samples from municipalities directly under the central government. Given that the behavioral patterns of municipal governments may differ from those of ordinary prefecture-level cities, to eliminate this impact, all samples from cities that are municipalities directly under the central government were excluded. The regression results after excluding specific samples, as shown in Table 6 column (3), still show that the coefficient of LGD (Debt) remains significantly negative at the 1% level. In summary, the conclusions of this paper are valid.

Robustness Tests.

Note. Figures in parentheses are the robust standard errors.

, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Mechanism Analysis

The test results previously discussed show that the expansion of LGD significantly suppresses corporate ESG. To further verify the mechanism through which LGD affects corporate ESG, the following section will explore the mechanisms identified in the theoretical analysis from three aspects: credit scale, government subsidies, and corporate tax burden.

Credit Scale

Columns (1) and (2) of Table 7 report the test results using credit scale as a mediating variable. The results in column (1) show that the coefficient of LGD (Debt) is significantly negative, indicating that LGD significantly reduces the credit scale available to businesses. Column (2) incorporates credit scale into the baseline regression model, where the coefficient for LGD (Debt) remains significantly negative and the credit scale (Credit) is significantly positive. This passes the mediation effect test, suggesting that credit scale is one of the mechanisms through which LGD affects corporate ESG, confirming Hypothesis 2. This is mainly because the expansion of LGD crowds out the credit resources available to enterprises, exacerbating their financing constraints, forcing companies to reduce their ESG in a limited funding situation. This result supports the viewpoint of Peng and Lin (2024), who argue that financing constraints on enterprises will intensify as the financing needs of local governments increase, forming a “crowding out effect.”Liu et al. (2023) also believe that LGD has a strong credit resource crowding out effect on local enterprises, manifested in reduced financing for businesses and increased financing costs.

Mechanism Tests.

Note. Figures in parentheses are the robust standard errors.

, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Government Subsidies

Columns (3) and (4) of Table 7 present the regression results with government subsidies as a mediating variable. From column (3), it is evident that the coefficient of LGD is significantly negative, indicating that the expansion of LGD significantly reduces the financial subsidies to enterprises. Column (4) adds government subsidies, and the results show that the coefficient for government subsidies is significantly positive, while the coefficient for LGD remains significantly negative. This suggests that government subsidies play a partial mediating role in how LGD affects corporate ESG performance, verifying Hypothesis 3. The main reason is that the fiscal pressure brought about by the expansion of government debt size leads governments to cut financial subsidies to enterprises, reducing the funds available for ESG, thereby suppressing corporate ESG performance. This result is consistent with Xu et al. (2021), which discusses the relationship between LGD and corporate innovation. They found that as LGD increases, local governments, to avoid debt default, consume limited fiscal resources of the region and reduce financial subsidies to enterprises, thereby “crowding out” corporate innovation.

Corporate Tax Burden

Columns (5) and (6) of Table 7 show the regression results with corporate taxation as a mediating variable. The results in column (5) indicate that the coefficient of LGD is significantly positive at the 10% level. Incorporating corporate taxes into the baseline model, the coefficient for LGD passes the significance test, but the coefficient for corporate taxes is not significant. Further application of the Sobel test shows that it does not pass the 10% significance level, hence, the empirical test results do not support the hypothesis that corporate taxes have a mediating effect. One possible explanation for this outcome is that with the continuous expansion of local government debt, on one hand, the rising debt repayment pressure on local governments may prompt government departments to increase the intensity of tax collection from enterprises, increasing tax revenue to improve fiscal income (G. He et al., 2020). On the other hand, the significant “crowding out effect” of LGD on corporate financing exacerbates financing constraints, which may increase companies’ efforts to avoid taxes (Peng & Lin, 2024). Under the combined effect of these two factors, the impact of corporate tax burden on ESG performance is minimized.

Heterogeneous Tests

The previous discussion focused on the impact of LGD on corporate ESG across the whole sample. However, in reality, the influence of LGD on ESG is not isolated, it is also affected by factors at the firm, industry, and regional levels. Therefore, this section seeks to explore the heterogeneous impact of LGD on ESG under different corporate, industry, and regional characteristics.

Firm-level Heterogeneity

This part examines the moderating role of firm-level factors, specifically the nature of ownership and leverage ratio. Specifically, the whole sample is divided into state-owned enterprises (SOEs), non-state-owned enterprises (non-SOEs), high-leverage, and low-leverage groups based on the nature of ownership and leverage ratio levels, respectively. The subsample regression results are shown in Table 8. It is observed that in the samples of SOEs and non-SOEs, the coefficient of LGD is significant only in the non-SOEs group and not significant in the SOEs group, indicating that the expansion of LGD only suppresses the ESG of non-SOEs. The main reasons are, on one hand, within the context of China, the implicit government guarantee provides SOEs with better external financing conditions and channels than non-SOEs, allowing them to occupy most of the credit resources over the long term, objectively leading to less financing constraints for SOEs (Liu et al., 2023; Tang et al., 2023; Zhong et al., 2019). In contrast, non-SOEs, especially private enterprises lacking credit endorsement, generally face financing constraints due to severe information asymmetry with financial institutions (Shen et al., 2020). The expansion of LGD further exacerbates the financial difficulties of non-SOEs, making it difficult for them to have sufficient funds for ESG investments. On the other hand, SOEs play an important role in China’s economic development, carrying significant responsibilities in supporting national sustainable development goals, and have a leading and exemplary role at different levels such as environment, social, and corporate governance. Therefore, SOEs have external motivations to further enhance their ESG performance to meet the requirements of ESG-related policies issued by the government and regulatory agencies, thus being able to overcome the negative impacts brought about by the expansion of local government debt. Considering these factors together, the impact of LGD expansion on the ESG of non-SOEs is more significant.

Firm-level Heterogeneity Analysis.

Note. Figures in parentheses are the robust standard errors.

, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Furthermore, we find that in both high-leverage and low-leverage groups, the coefficient of LGD is significantly negative, but in the high-leverage group, the absolute value of the Debt coefficient is larger, indicating a stronger suppressive effect on corporate ESG. The likely reason is that China’s financial system is still dominated by indirect financing, with corporate debt funds mainly sourced from bank loans. The higher the leverage ratio, the more reliant a company is on bank loans. The expansion of LGD significantly crowds out the credit resources of regional commercial banks, and for companies with a higher leverage ratio, this “crowding-out effect” on credit share is greater. Companies facing financing difficulties lack the motivation to build ESG, leading to a more significant negative relationship between LGD and corporate ESG in high-leverage companies.

Industry-level Heterogeneity

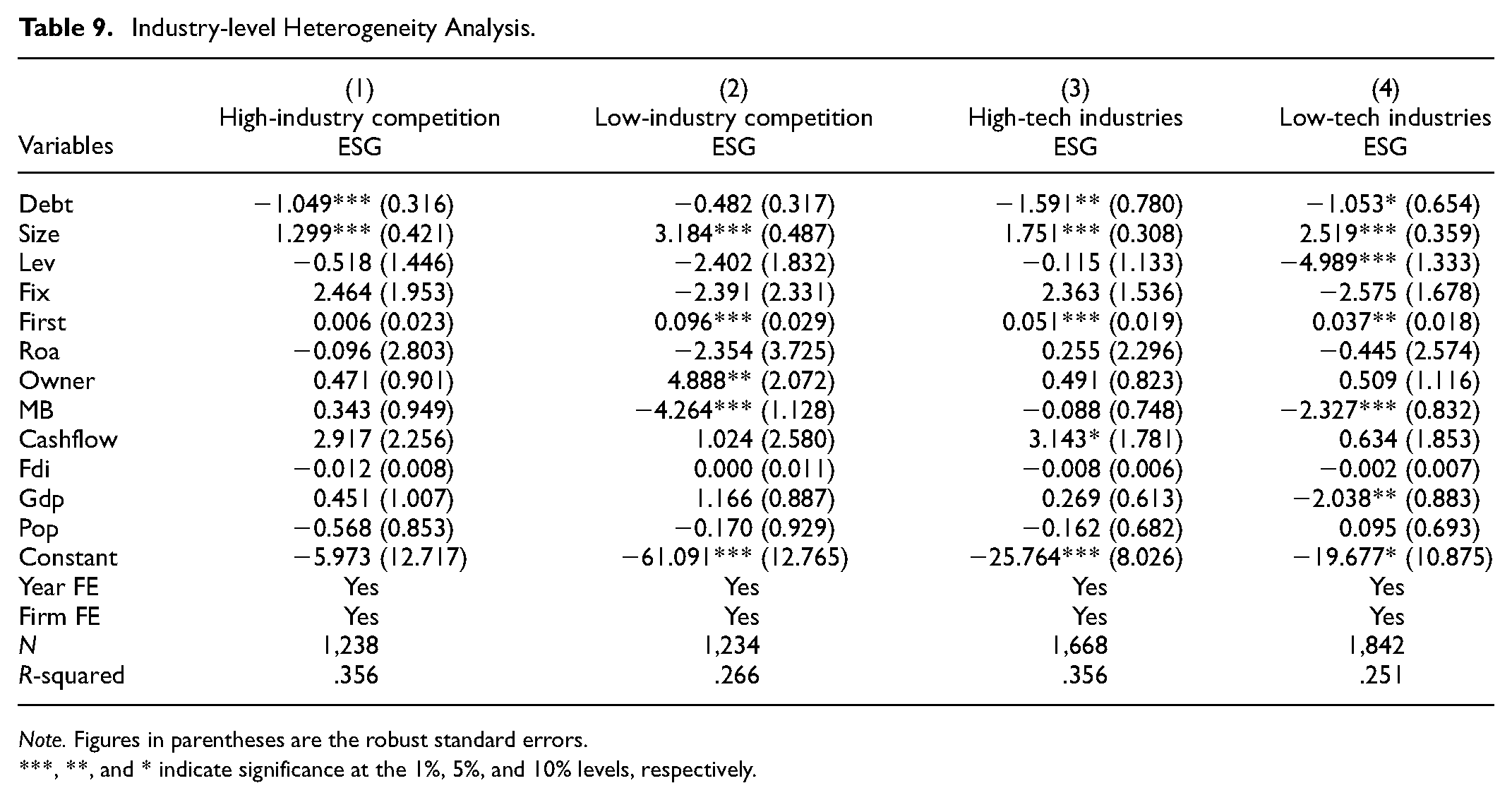

This section discusses the moderating role of industry-level factors from the perspectives of industry competition and industry technology intensity. Specifically: (1) This paper uses the proportion of the top four companies’ main business revenue to the total industry main business revenue as an approximate substitute for industry competition. The higher this ratio, the lower the industry competition. Based on the mean value of industry competition intensity, the sample is divided into high industry competition and low industry competition groups. (2) According to the classification method of high-tech industries by the Organization for Economic Cooperation and Development (OECD), the sample is divided into high technology-intensive and low technology-intensive industries. If a company belongs to a high technology-intensive industry, it is assigned a value of 1; otherwise, it is assigned a value of 0. The subsample regression results are shown in Table 9, where columns (1) and (2) indicate that the Debt coefficient is significantly negative only in the high industry competition group and not significant in the low industry competition group. This may be because, the more intense the industry competition, the greater the competitive pressure faced by enterprises. Under the premise of limited resources, enterprises can only focus all their efforts on daily production and operations, making it difficult to consider environmental protection and social responsibility. The expansion of LGD worsens the financing constraints for enterprises, reducing their financial flexibility, which makes it harder for enterprises in highly competitive industries to effectively improve their ESG. Columns (3) and (4) show that in both high technology-intensive and low technology-intensive industries, the coefficient of LGD is significantly negative, but in high technology-intensive industry groups, the absolute value of the Debt coefficient is larger, indicating a stronger suppressive effect of LGD expansion on corporate ESG. The possible reason is mainly that compared to low technology-intensive industries, high-tech industries often face higher technical and market risks, and are more dependent on the level of external financial services. Additionally, technology is an indispensable part of ESG construction for enterprises, especially in environmental management, waste management and governance, renewable resources and clean energy utilization, natural resource protection, etc., all of which rely on technological research and innovation. The expansion of local government debt, by increasing the cost of corporate financing and crowding out credit resources, reduces the efficiency and quality of financial services. The lack of funds significantly impacts corporate technological innovation, therefore, in high technology-intensive industries, the impact of LGD expansion on corporate ESG is more significant.

Industry-level Heterogeneity Analysis.

Note. Figures in parentheses are the robust standard errors.

, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Regional-level Heterogeneity

This part examines the moderating role of regional-level factors from the perspectives of financial development level and degree of marketization. Specifically, the sample is divided into the following categories based on the characteristics of the regions where the enterprises are located: (1) According to the level of regional financial development, the sample is divided into high financial development level groups and low financial development level groups, where the level of financial development is measured by the ratio of loans from financial institutions to deposits at financial institutions. (2) According to the degree of regional marketization, the sample is divided into high marketization and low marketization groups, where the marketization index is measured using the marketization index published by Fan Gang’s team. The subsample regression results are shown in Table 10. From the coefficient of Debt, in the low financial development level and low marketization level groups, the impact of LGD on corporate ESG is significantly negative, while in the high financial development level and high marketization groups, the impact of LGD on corporate ESG is not significant. The reason for these results may be that in regions with a high degree of marketization and developed financial industries, the channels for funding LGD financing and corporate financing are relatively diversified. Government and corporate sectors no longer rely solely on bank credit for financing, which can alleviate the financing constraints faced by enterprises and weaken the impact of LGD on corporate ESG. In regions with a low level of marketization and underdeveloped financial industries, where financing channels for enterprises are limited and local governments have a strong intervention capability in financial resources, the efficiency of credit fund allocation is low, potentially exacerbating the corporate funding shortages caused by rising local debt.

Regional-level Heterogeneity Analysis.

Note. Figures in parentheses are the robust standard errors.

, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Further Analysis

Analysis of ESG Structure

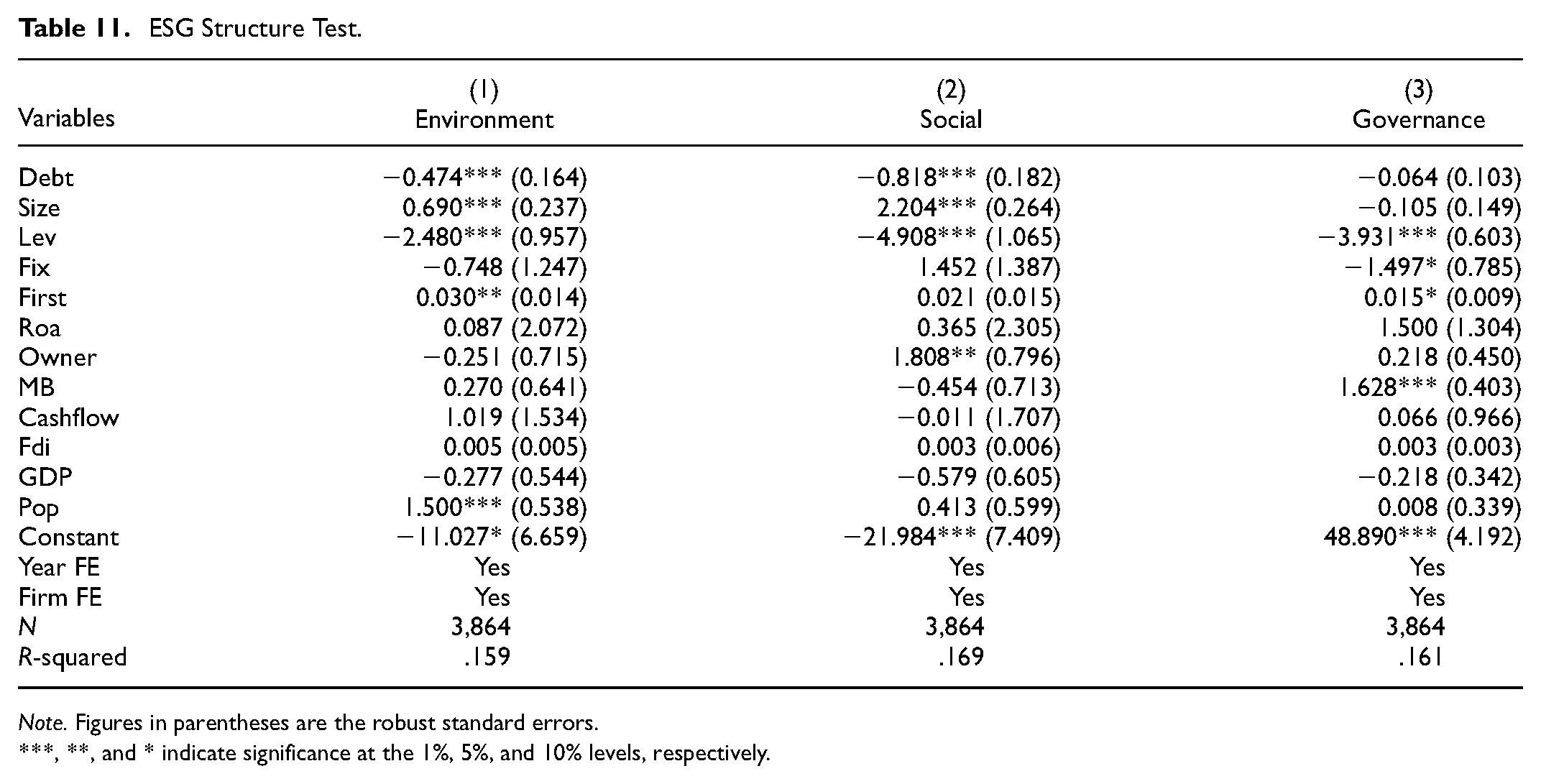

The previous research focused on the comprehensive impact of LGD expansion on overall ESG. Given that corporate ESG encompasses environmental, social, and corporate governance dimensions, does the expansion of LGD suppress these dimensions equally? To address this question, this paper further examines the impact of LGD on the three sub-indicators of corporate ESG. The regression results, as shown in Table 11, indicate that the expansion of LGD primarily reduces corporate social and environmental responsibilities, but its impact on internal governance is not significant. This might be because, compared to social and environmental responsibilities, internal governance has the greatest utility for a company. In scenarios where LGD continually expands and encroaches upon corporate resources, companies tend to allocate their limited resources to organizational structure governance and internal ethical risk management, reducing their responsibility toward external social and environmental duties.

ESG Structure Test.

Note. Figures in parentheses are the robust standard errors.

, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Debt Structure Analysis

Local government financing platform debt includes both publicly issued and non-publicly issued debt, with the former primarily being city investment bonds and the latter mainly bank loans (Peng & Lin, 2024). Compared to city investment bonds, non-publicly issued debt should have a greater impact on local enterprises for three reasons. First, city investment bonds constitute a small proportion of financing platform debt, with non-publicly issued debt being the real main body of local government debt. It has a larger scale and a stronger crowding-out effect on financial resources. Second, city investment bonds are issued in exchanges and the interbank market, allowing for national financial market financing, which has a smaller impact on the local capital market; non-publicly issued debt relies more on local commercial bank financing, having a greater impact on local enterprises. Third, city investment bonds are publicly issued, requiring stricter information disclosure and more regulated fund usage, possibly leading to relatively higher investment efficiency. Therefore, this paper hypothesizes that non-publicly issued debt from financing platforms will significantly crowd out local corporate ESG investments, whereas city investment bonds will not.

To test this hypothesis, this paper separately examines the impact of city investment bonds and non-publicly issued debt on corporate ESG investments. Here, the logarithm of the balance of city investment bonds issued in a company’s region is represented as Debt1, and the logarithm of the difference between interest-bearing debt of financing platforms and city investment bonds is represented as Debt2. The regression results are shown in Table 12. The estimation result in column (1) shows that the balance of city investment bonds does not have a significant impact on corporate ESG investment. The regression result in column (2) indicates that non-publicly issued debt crowds out local corporate ESG investments, with the estimate coefficient being significant at the 1% level.

LGD Structure Test.

Note. Figures in parentheses are the robust standard errors.

, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Conclusions, Policy Recommendations, and Future Research

Conclusions

This paper examines the impact of LGD on corporate ESG among A-share listed companies in China from 2011 to 2020, utilizing prefecture-level city LGD data. The empirical findings indicate that: (1) LGD expansion significantly suppresses corporate ESG, a conclusion that holds after addressing endogeneity concerns, replacing variables, and removing specific samples, with LGD having a long-term suppressive effect on corporate ESG. (2) The expansion of LGD both crowds out corporate credit resources and reduces government financial subsidies to corporations, leading to limited corporate funding and lower ESG levels. (3) The negative relationship between LGD expansion and corporate ESG is more pronounced in regions with low marketization, low financial development levels, and among non-state-owned, high leverage ratio, high industry competition, and high technology-intensive companies. (4) The expansion of LGD primarily reduces corporate social and environmental responsibilities, but its impact on internal governance is not significant. The suppressive effect of LGD on ESG is not driven by publicly issued city investment bonds but by non-publicly issued debt.

Policy Recommendations

Based on the findings, we recommend the following policies:

First, the results suggest that LGD severely squeezes corporate investment, reducing the level of corporate ESG and hindering the potential for long-term economic growth. The central government must limit excessive borrowing by local governments, control the size of their debt reasonably, and optimize the financing structure of local governments. Moreover, debt structure analysis indicates that non-publicly issued debt has a greater impact on ESG than publicly issued debt; thus, it is imperative to strictly limit local financing platforms from acquiring funds through non-public channels such as bank loans and trust funds. Furthermore, accelerating the reform of inter-governmental fiscal relations and advancing the income distribution between central and local governments can effectively alleviate medium- and long-term fiscal pressures on local governments. Providing local governments with more rights, expanding their tax base, and coordinating local government powers are also essential.

Second, the research findings suggest that the expansion of LGD primarily constrains corporate funds by crowding out corporate credit resources and reducing fiscal subsidies to enterprises, thereby leading to a decrease in corporate ESG levels. Based on this, it is recommended to vigorously promote regional financial development, encourage the continuous innovation and improvement of high-end core technologies such as artificial intelligence, big data, cloud computing, and promote the digital and informational transformation of the financial industry. Strengthening the deep integration of the digital economy industry and the financial industry will cultivate a diversified and multi-level financing environment, provide abundant and effective financial support for enterprises, and fully motivate enterprises to improve their own ESG performance. At the same time, it is necessary to reduce excessive intervention in the allocation of financial resources, actively advance the marketization process of the region, enhance the market mechanisms of financial institutions, especially city commercial banks, strengthen financial regulation, and improve the efficiency of credit resource allocation to provide a quality environment for the development of corporate ESG.

Third, concerning the heterogeneity test results, it is necessary to formulate supportive financing policies related to corporate ESG, especially for non-state-owned and high-tech intensive enterprises. Specific financing projects and channels should be introduced for environmental governance, social responsibility, and corporate governance, providing rapid and sufficient financial support for the construction of corporate ESG. This targeted assistance aims to bolster the ESG development of enterprises. At the same time, it is crucial to improve the tracking and supervision systems of related financing projects to prevent misallocation and misuse of funds.

Limitations and Future Research

This paper quantitatively discusses the relationship between LGD and corporate ESG in China, yet it is faced with the following limitations that necessitate further research.

First, there are limitations in measuring local government debt. Due to data availability, this paper adopts the practice of most scholars by using the list of local financing platforms in the Wind database as the basis for measuring the scale of local government debt. However, this approach has two main issues: firstly, the list inaccurately categorizes a small number of bonds issued by non-financing platform companies as urban investment bonds; secondly, there is a significant problem of omission. Since the China Securities Regulatory Commission (CSRC) implemented list-based management, local governments have established new financing platform companies, most of which have not been included in the list-based management. Given these issues, future research should endeavor to collect and organize a more accurate list of financing platforms to measure the scale of LGD more accurately and minimize data errors as much as possible.

Second, under the guidance of the CSRC on investors actively practicing the concept of ESG investing, most external investors consider ESG information a critical part of their communication with target companies and focus on the construction of the target company’s ESG system in their investment decisions. Therefore, the impact of LGD on corporate ESG performance and whether it leads to changes in investor behavior or market reactions is worth further study.

Additionally, aside from LGD policies, other policies implemented by local governments, such as environmental regulation policies and green bond policies, may also impact corporate ESG. Future research could explore how these policies interact with debt levels to influence corporate ESG.

Footnotes

Authors Contributions

Feifei Li: Software, Visualization, Writing-original draft, Conceptualization, Funding acquisition.

Ruile Xue: Writing-review and editing, Conceptualization.

Songying Wang: Conceptualization, Visualization, Data Management.

Mingyue Du: Conceptualization, Formal analysis, Writing-review and editing, Supervision.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/ or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was financially supported by the Business Administration Discipline construction project of Yuncheng University (GSGL2403) and Shanxi Philosophy and Social Science Project (2023YY289).

Ethical Approval

There are no ethical issues involved in this thesis and no harm will be caused to individual organisms. This entry does not apply to this thesis.

Consent to Participate

Not applicable

Consent to Publish

The authors have consented to publish the article.

Data Availability Statement

The data that support the findings of this study are available from the corresponding author upon reasonable request.