Abstract

The rise of crowdfunding has transformed the funding landscape for startups, offering an alternative to conventional financing avenues. This study focuses on equity crowdfunding and investigates the dynamics of herding behavior among investors and its influence on campaign success. We analyze 680 equity crowdfunding campaigns from Wadiz, the largest platform in South Korea (2016–2021). In contrast to traditional funding, equity crowdfunding creates a two-sided market through its platform-based service, fostering interactions between entrepreneurs seeking funds and investors seeking opportunities. The time-limited nature of campaigns further encourages sequential decision-making and potential herding behavior. Unlike prior studies that have predominantly emphasized entrepreneurial and campaign-related factors, this study highlights the pivotal role of investor behavior, recognizing fellow investors as valuable signaling entities within the platform. Using OLS regression, logistic regression, interaction analysis, and Propensity Score Matching (PSM), we find that early participation by professional investors increases the odds of campaign success by approximately 14%. Furthermore, the effect is more pronounced in the IT industry, where information asymmetry is especially severe. Our findings demonstrate the signaling role of professional investors in mitigating information asymmetry and improving campaign outcomes, providing actionable insights for entrepreneurs, investors, and platforms in the evolving landscape of equity crowdfunding.

Plain Language Summary

Crowdfunding allows many small investors to fund new business ideas online. However, ordinary investors often face difficulties in judging whether a project is trustworthy because they have less information than professional investors. This study examines how early participation by professional investors influences the success of equity crowdfunding campaigns in South Korea. We collected data on 680 campaigns from Wadiz, the largest crowdfunding platform in South Korea, between 2016 and 2021. We compared campaigns that received early funding from professional investors with those that did not. Our analysis shows that professional investors play an important signaling role. When they invest early, other investors are more likely to follow, which increases the chance that a campaign reaches its funding goal. This pattern is especially strong in the information technology (IT) sector, where information gaps between entrepreneurs and investors are large. The findings suggest that professional investors can reduce information uncertainty for ordinary investors, helping them make decisions with more confidence. For entrepreneurs, attracting professional investors at an early stage can improve the chances of success. For policymakers and platform operators, highlighting professional investor involvement may encourage broader participation and strengthen the crowdfunding market.

Introduction

Information and communication technology has facilitated the breakdown of physical boundaries and led to a diversification of fundraising options for startups. Crowdfunding emerged as an alternative source of funding when traditional financing options such as bank loans or venture capital were unavailable (Agrawal et al., 2015; Samoilenko et al., 2021). It has grown increasingly popular among entrepreneurs seeking to raise capital independently, helping them maintain autonomy over their businesses (Uzialko, 2024). According to the Global Alternative Finance Market Benchmarking Report (Ziegler et al., 2020), the global crowdfunding market has expanded steadily, and the OECD (2023) highlights its growing role in supporting small- and medium-sized enterprises. These trends underscore the increasing importance and resilience of crowdfunding as a dynamic fundraising avenue.

Despite this growth, uncertainty remains regarding the most effective strategy for ensuring project success. Given that crowdfunding typically targets a large online audience, the funding performance or success rate of a campaign is a crucial factor (Khavul, 2010). Scholars have explored various determinants of crowdfunding success, particularly in the context of equity-based crowdfunding, where investors receive monetary rewards such as stocks and bonds (Y. Chen et al., 2020; Duan, 2024). Information asymmetry poses a key challenge, similar to conventional companies, prompting research into mitigating mechanisms. Prior studies highlight financial characteristics (Nitani et al., 2019), ownership structure (Cosma et al., 2019; Nitani et al., 2019), founder characteristics (Ahlers et al., 2015; Piva & Rossi-Lamastra, 2018; N. Wang et al., 2021), and third-party authentication (Kleinert & Volkmann, 2016; Ralcheva & Roosenboom, 2020) as important factors. However, few studies have distinguished between professional and amateur investor herding, leaving a notable research gap.

This study examines the distinctive characteristics of equity crowdfunding, focusing on potential network effects and herding behavior among investors. The platform-based and time-limited nature of equity crowdfunding creates a two-sided market wherein entrepreneurs seek funds and investors seek opportunities, facilitating interactions that may trigger herding behavior. Existing literature has predominantly emphasized firm- and campaign-level factors (Ahlers et al., 2015; Cosma et al., 2019; Lukkarinen et al., 2016; Vismara, 2016, 2018), while investor-centered dynamics remain understudied. Within these platforms, investor behavior provides valuable signals due to transparent disclosure of funding progress. Accordingly, this study investigates whether early participation by professional investors triggers herding behavior among other investors, and whether this effect varies depending on the degree of information asymmetry. By considering the signaling role of professional investors and comparing effects across industries, this research offers insights that may inform more effective equity crowdfunding strategies for entrepreneurs.

Related Literature and Hypotheses

Equity Crowdfunding

Equity crowdfunding has a significant impact on early-stage venture funding (Vulkan et al., 2016). For entrepreneurs seeking to secure financing, it is imperative to identify the factors that determine campaign success. One of the most important challenges is reducing information asymmetry and signaling quality and credibility to potential investors (Vismara, 2018). As shown in Table 1, previous research has largely examined determinants of success from the entrepreneur’s perspective. These studies have focused on how company and founder characteristics—such as firm age, number of shareholders and directors, presence of business angels, industrial shareholders, and professional skills—serve as signals to investors, drawing on criteria traditionally used by venture capitalists and angel investors (Courtney et al., 2017; Lukkarinen et al., 2016; Vismara, 2016).

Prior Research on Equity Crowdfunding.

On the other hand, some studies have investigated crowdfunding from the investor’s perspective. In uncertain markets like crowdfunding, investors may mimic the behavior of others, a phenomenon known as herding behavior, which has been widely analyzed in financial markets (J. Du, 2023). In crowdfunding, herding is particularly relevant because funding occurs sequentially and all investment activity is transparently disclosed to potential backers. While early crowdfunding research predominantly addressed reward-based models, in which backers receive non-monetary benefits (e.g., products or experiences), equity-based crowdfunding involves financial returns through shares or hybrid securities. This distinction is critical because equity crowdfunding more closely resembles traditional financial markets and magnifies concerns about information asymmetry. Accordingly, this study focuses on equity-based crowdfunding, while briefly acknowledging insights from reward-based research.

Although a few studies have examined herding effects in equity crowdfunding from the investor perspective, most have been limited to demonstrating the existence of herding behavior on platforms (Crosetto & Regner, 2018; Petit & Wirtz, 2022). Only a handful have analyzed its implications for campaign success (Hornuf & Neuenkirch, 2017; Vismara, 2018), leaving this as a critical gap that our study addresses.

Signal Theory: Herding Effect

Formal economic models assumed perfect information in decision-making processes, often overlooking information asymmetries (Stiglitz, 2002). This assumption suggested that marketplaces with information asymmetries would function similarly to those with perfect information (Lu & Li, 2023). However, research on financial decision-making reveals that, particularly in unstable markets, investors exhibit reduced confidence and are more susceptible to the influence of others’ decisions (Herzenstein et al., 2011; Hilton, 2001; Li et al., 2025). This phenomenon is termed the herding effect, defined as the tendency of investors to imitate or cluster when trading securities (Herzenstein et al., 2011). Investors essentially replicate the investment decisions of their peers and mimic their behavior, especially in situations with low credibility (Wohlgemuth et al., 2016).

According to signal theory, the value of a signal may vary depending on the investor’s type. In equity-based crowdfunding, which resembles traditional funding channels by offering stocks or bonds as rewards, investments from seasoned experts with substantial experience and expertise may serve as reliable signals to other investors. Despite the significance of professional investors, existing studies on equity crowdfunding lack empirical research on their influence (Hornuf & Neuenkirch, 2017; Vismara, 2018). Hence, this study aims to concurrently explore the herding effect and the impact of professional investors as determinants of campaign success. It contributes to existing research by empirically examining whether the herding effect influences crowdfunding success and whether this influence is more pronounced in sectors characterized by relatively high information asymmetry, such as the IT industry, compared to other industries (Jeon et al., 2024).

Recent studies highlight that the herding effect in crowdfunding may be moderated by campaign- and investor-level characteristics. For example, campaign duration and investor diversity can influence the extent to which early participation signals are amplified in subsequent investment decisions (Chen et al., 2024; Dao et al., 2024). Although our dataset does not allow us to empirically test these moderators, acknowledging their potential impact enriches the theoretical foundation of our hypotheses and underscores the complexity of herding dynamics in equity crowdfunding. Furthermore, the IT industry provides a particularly suitable context for this study because it is characterized by substantial information asymmetry due to technological complexity and rapid innovation. This makes professional investors’ early participation especially salient as a credible signal.

Hypotheses

Funding decisions in crowdfunding platforms are exposed to the influence of herding due to the sequential nature of funding dynamics (Agrawal et al., 2014). The existing literature on crowdfunding shows that previous capital raising has a positive effect on subsequent funding (Hornuf & Neuenkirch, 2017; Vismara, 2018). The accumulated capital from prior contributions positively affects late contributions (Burtch et al., 2016). These results indicate that investment by others becomes a signal for campaign success to investors in crowdfunding. According to the signaling theory literature, signals’ credibility and trustworthiness depend on their source (Gomulya & Mishina, 2017; Mavlanova et al., 2012). The credibility of signals by investors also depends on their expertise or type. In particular, the effectiveness of signals sent by the crowds and the experts is very different. Existing venture literature reveals that observable endorsements from experts are a valuable signal that effectively indicates venture quality (Courtney et al., 2017; Kim & Viswanathan, 2018). For instance, ventures that received angel investments had higher survival and growth rates and were more likely to attract Venture Capitalists (VCs) and other institutional investors. Given the distinction in expertise, experience, and wealth between general (crowd) investors and professional investors such as VCs, Angel investors, the professional investor’s signal can be expected to have higher reliability. Several empirical studies report that funding from investors with expertise and experience increases subsequent investment, leading to equity crowdfunding success. Therefore, the investment of professional investors in the campaign’s early stages will be a credible signal.

In the two-sided structure of equity crowdfunding platforms, signals function across multiple actors. Professional investors provide cues not only to crowd investors, who rely on these signals to reduce information asymmetry, but also to entrepreneurs and platform operators. Entrepreneurs benefit from validation when professionals participate, while platforms leverage such signals to increase campaign visibility. This multi-directional signaling process highlights the relevance of signal theory in explaining how professional investors shape outcomes in equity crowdfunding.

The IT sector, often associated with deep-tech innovations, is characterized by rapid technological change and high uncertainty, which exacerbate information asymmetry between entrepreneurs and ordinary investors (Ji et al., 2020; Liu et al., 2017; Molhova, 2014; Xiao et al., 1998). Thus, despite improved data availability on crowdfunding platforms, significant gaps remain, making professional investors’ signals particularly critical in IT campaigns (P. Du et al., 2020; Escobari & Serrano, 2016). In such an environment, signals from professional investors become especially salient as they validate project quality and reduce uncertainty for general investors. Therefore, the herding effect triggered by professional investors is expected to be more pronounced in IT campaigns than in other industries.

In summary, this study posits two hypotheses:

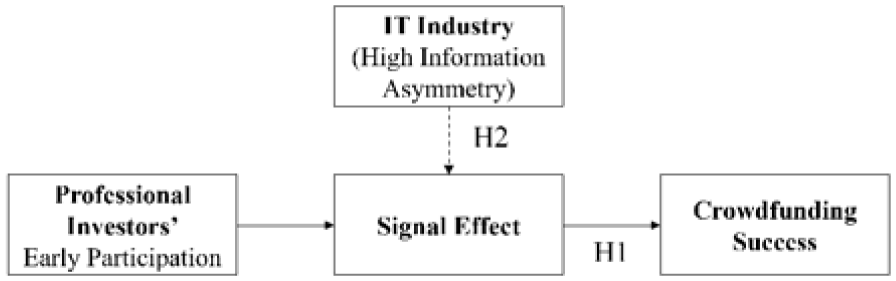

The conceptual framework of this study is summarized in Figure 1. As shown, early participation by professional investors is hypothesized to positively influence crowdfunding success (H1). Furthermore, the IT industry is expected to strengthen this effect, given its higher level of information asymmetry (H2).

Conceptual model: Effects of professional investors’ early participation on crowdfunding success, with IT industry as a moderator.

Data and Method

Data Collection

This study relies on data gathered from Wadiz (wadiz.kr), the largest and most representative equity crowdfunding platform in South Korea, which accounts for the majority of campaigns during the study period. Equity crowdfunding was officially introduced in South Korea following the revision of the Capital Market Act on January 25, 2016. Our dataset spans approximately 5 years, covering campaigns launched between January 25, 2016, and January 22, 2021. Under this Act, individual investors are restricted to a maximum of  5 million (approximately $4,000) per campaign. Investments above this threshold are classified as professional or institutional, and we adopt this legal standard to identify professional investors. Campaign information was collected through web scraping of the platform and manually validated to ensure accuracy. Of the 710 equity crowdfunding campaigns launched during this period, 30 campaigns with incomplete data were excluded, resulting in a final sample of 680 campaigns. For each project, we compiled information on campaign characteristics (e.g., fundraising goals, project duration, final pledges, and categories) and company-related data (e.g., ownership and governance structures, corporate capital and age, prior funding experience, and third-party certification). The final sample of 680 campaigns includes 487 stock-type and 193 hybrid-type campaigns. In terms of industry distribution, 252(37.1%) campaigns belong to the IT sector, 143(21.0%) to manufacturing, 79(11.6%) to retail, and the remaining 206(30.3%) are spread across education, finance and other sectors.

5 million (approximately $4,000) per campaign. Investments above this threshold are classified as professional or institutional, and we adopt this legal standard to identify professional investors. Campaign information was collected through web scraping of the platform and manually validated to ensure accuracy. Of the 710 equity crowdfunding campaigns launched during this period, 30 campaigns with incomplete data were excluded, resulting in a final sample of 680 campaigns. For each project, we compiled information on campaign characteristics (e.g., fundraising goals, project duration, final pledges, and categories) and company-related data (e.g., ownership and governance structures, corporate capital and age, prior funding experience, and third-party certification). The final sample of 680 campaigns includes 487 stock-type and 193 hybrid-type campaigns. In terms of industry distribution, 252(37.1%) campaigns belong to the IT sector, 143(21.0%) to manufacturing, 79(11.6%) to retail, and the remaining 206(30.3%) are spread across education, finance and other sectors.

Terminology and Scope

To ensure terminological clarity, we distinguish between two types of securities observed in Wadiz investment campaigns: Equity-based crowdfunding refers to campaigns in which firms issue common or preferred shares, thereby distributing ownership to investors. Investors become shareholders and may earn returns through dividends or capital gains. Hybrid crowdfunding refers to campaigns in which firms issue hybrid securities—such as convertible bonds (CB) and bonds with warrants (BW)—that combine features of both debt and equity. These are essentially debt contracts but include rights to convert into equity under certain conditions.

Importantly, plain corporate bonds without equity-conversion features are not available on Wadiz, because equity-based crowdfunding under the Capital Market Act restricts their issuance. This study primarily focuses on equity-based crowdfunding campaigns. The dataset consists of 487 stock-type campaigns and 193 hybrid-type campaigns. Hybrid campaigns are incorporated as a control variable in the empirical analysis to ensure analytical rigor, while the main analysis centers on stock-type crowdfunding campaigns.

Variables and Research Models

Dependent Variables

The dependent variable in this study was campaign success, measured in two ways. First, equity crowdfunding success is defined as a binary outcome: a value of one indicates that the campaign achieved at least 80% of its target (values above 100% are possible in cases of overfunding), and zero otherwise. According to the Financial Investment Services and Capital Markets Act of Korea, campaigns reaching 80% or more of their goal were considered successful. Second, we use the percentage of the target capital raised during the campaign. To address skewness in this variable, we applied the natural logarithm before performing statistical analyses.

Independent Variables

In South Korea, individual investors are restricted to investing up to 5 million. Thus, an investor surpassing this amount was classified as a professional investor in this study. Herding behavior denotes investors’ tendency to replicate others’ actions. Previous research has measured the herding effect based on the initial number of investors or the funding amount after the campaign commences, considering it a crowdfunding campaign success factor. In this study, the herding effect was defined as the investment made by professional investors during the first week after the campaign’s launch.

Controls

This study included Share_L, a variable representing the proportion of shares held by the largest shareholder and related parties. It was calculated based on the ownership information disclosed in the investment prospectus of each campaign. Funding experience was represented as a dummy variable, coded as 1 if the entrepreneur has a history of successful funding and 0 otherwise. The crowdfunding platform furnished information regarding whether the company has received six certifications, with this variable calculated by summing the number of certifications each company has acquired. Consistent with prior research on the determinants of success in equity crowdfunding (Ahlers et al., 2015; Vismara, 2016), this study includes control variables for the target capital of the entrepreneur’s campaign, serving as an indicator of project size (Ahlers et al., 2015). Recognizing that successful pitches can conclude before the campaign period ends, and the platform can extend campaign duration at its discretion when the target amount is not achieved, the analysis accounts for these ex-post changes in campaign duration by introducing a control variable (Duration) in regression analyses (Vismara, 2016). Campaign duration was quantified as the number of days between the first and last day of a campaign.

Additionally, this study includes corporate capital and age as company characteristics. Firstly, capital was utilized as a proxy to gauge the company’s size, acquired through investment planning. The company’s age was calculated as the difference between the year of the campaign and the year of the company’s foundation, serving as an indicator of entrepreneurial skill in business development. Consistent with prior studies, this study controls for the number of concurrently running competitive campaigns. This variable is measured based on the overlap in start and end dates of other campaigns, following prior literature to capture potential competition during the campaign period. Lastly, the category dummy variable was integrated, controlling for IT, retail, and manufacturing categories, which constitute the predominant portion of the sample in this study.

Research Models

Given that the dependent variables in Equations 1 are dummy variables, this study employs logistic regression and probit analysis, and ordinary least squares regression analysis for Equation 2. The description of variables is outlined in Table 2, and the two equations, Equation 1 (DV=Success) and Equation 2 (DV=lnPercent pledged), are presented below.

Descriptions of Variables.

Results

Empirical Results for H1

Prior to hypothesis testing, diagnostic checks were performed for multicollinearity and normality. We conducted a VIF test and as all values were below 2, confirming multicollinearity is not a concern. Regarding normality, deviations were mainly attributable to tail asymmetry; however, given the sufficiently large sample size (n = 680) and the asymptotic properties of maximum likelihood estimation, such departures are unlikely to affect the validity of the results.

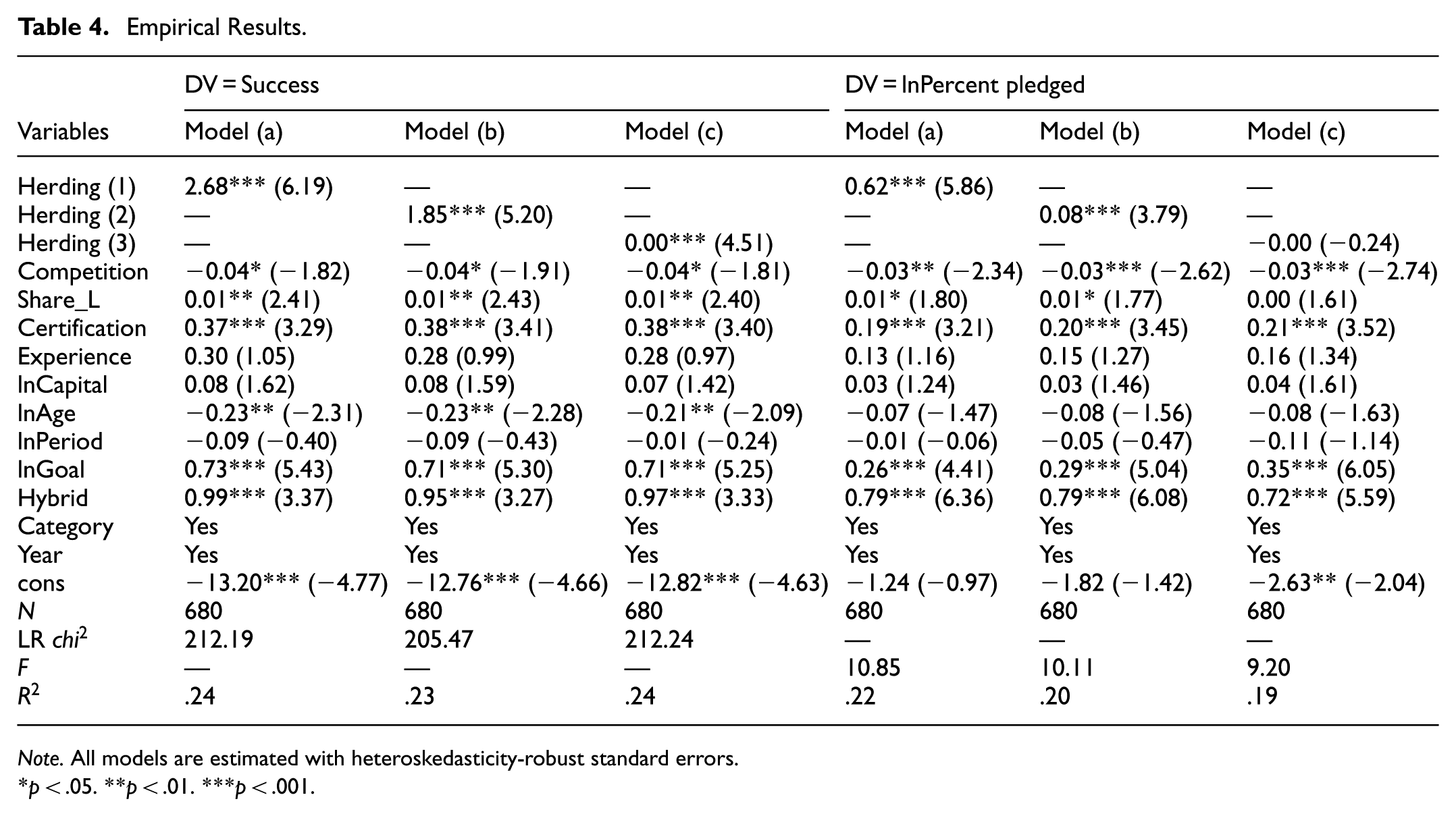

This study identified a significant influence of the herding effect on campaign success across all models, indicating that campaigns receiving early funding from professional investors were more likely to attain their target funds. This finding substantiates the hypothesis and aligns with prior research, underscoring that the involvement of investors with expertise and experience in the initial phase of a campaign imparts reliable and valuable signals to other investors, consequently enhancing the probability of campaign success. A one-unit increase in Herding(1) raises the odds of campaign success by approximately 14 times (or about 1,362%). For Herding(2), the effect corresponds to about 6.37 times (or roughly 537%) higher odds of success. In contrast, Herding(3) shows no meaningful effect, as its odds ratio is approximately 1. Descriptive statistics for the variables employed in this study are presented in Table 3, while Table 4 outlines the analysis results.

Descriptive Statistics.

Empirical Results.

Note. All models are estimated with heteroskedasticity-robust standard errors.

p < .05. **p < .01. ***p < .001.

Furthermore, this study investigated the impact of control variables on campaign success. The percentage of the largest shareholder exhibited a significant positive effect on campaign success, consistent with previous research highlighting that heightened shareholder commitment serves as a positive signal for investors. Additionally, third-party certification positively influenced campaign success, signaling investors about the campaign’s quality. The target amount of the campaign showed a positive effect on success, while the funding period had a negative effect, aligning with findings from previous studies. Lastly, this study revealed that bonds exerted a statistically significant positive effect on campaign success, attracting more attention and boasting a high likelihood of success, particularly in project-like campaigns such as those in the art and film domains.

To address potential endogeneity concerns, we conducted a comprehensive analysis employing the Propensity Score Matching method. In accordance with Geva et al. (2019), our investigation focused on matching samples based on campaign and company characteristics, with the results outlined in Table 5. Notably, the analysis underscored a consistently significant positive effect of the herding effect on the success of equity crowdfunding, even after accounting for endogeneity. These findings were consistently reiterated in analyses featuring the number of professional investors and the investment amount by professional investors as independent variables. The overall inference drawn from the analyses is that, irrespective of the variables considered, the greater the participation of professional investors in the initial stages of an equity crowdfunding campaign, the higher the likelihood of achieving success.

Empirical Results of Propensity Score Matched Sample.

Note. All models are estimated with heteroskedasticity-robust standard errors.

p < .01. ***p < .001.

Empirical Results for H2

Examining potential variations in the impact of early professional investor herding effects on equity crowdfunding success concerning the degree of information asymmetry, an additional analysis was conducted to explore the interaction effect between the IT industry and herding (

Interaction Effect Between Herding Effect and IT Category.

Note. All models are estimated with heteroskedasticity-robust standard errors.

p < .05. **p < .01. ***p < .001.

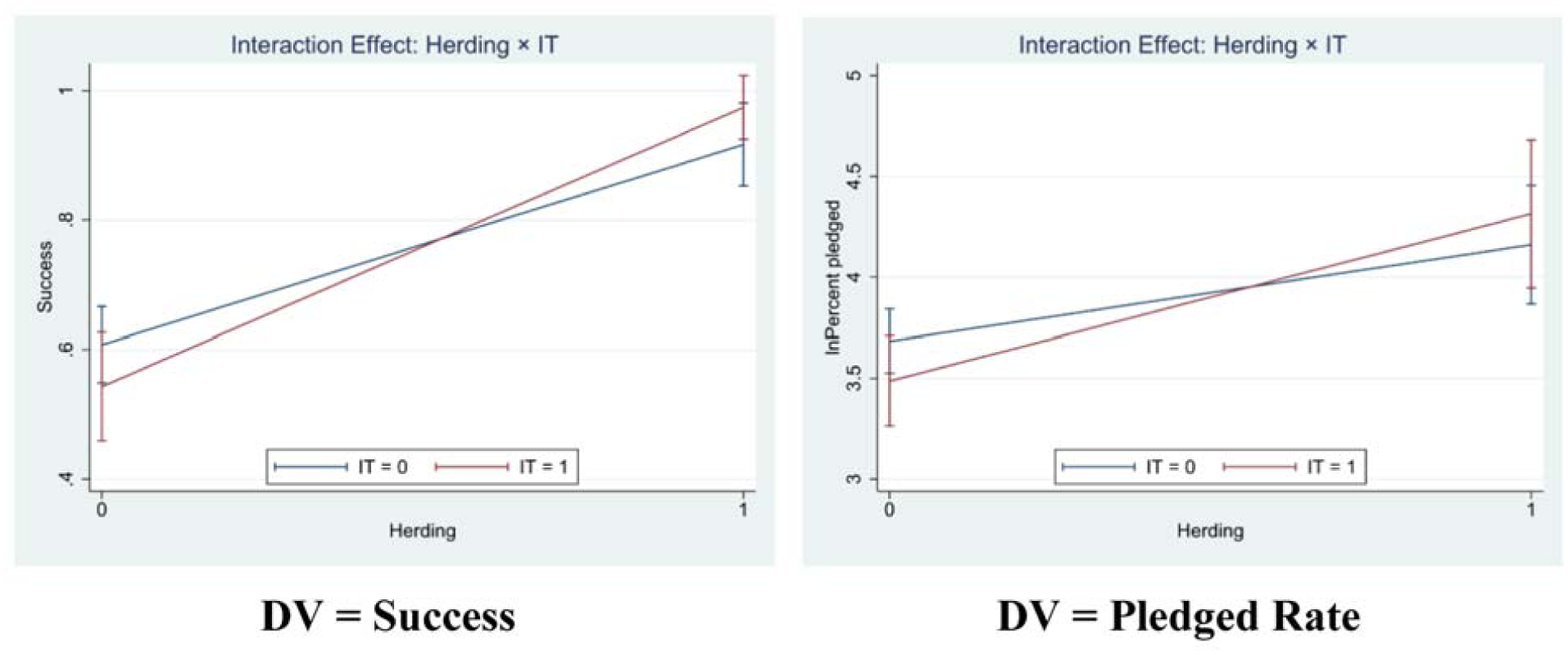

To illustrate the interaction effect between IT category and herding behavior, we provide interaction plots based on the results of Model (a). In Figure 2, the x-axis indicates the presence of herding behavior (0 = No, 1 = Yes), while the y-axis represents either the success rate or the pledge rate of the campaign.

Interaction effect of Herding and IT.

The plots show that when herding is absent (Herding = 0), IT-related campaigns tend to exhibit lower success probabilities than non-IT campaigns. This implies that IT campaigns lacking early participation from professional investors are less likely to succeed. In contrast, when herding behavior is present (Herding = 1), the success rate increases for both IT and non-IT campaigns. However, the improvement is particularly notable in IT-related campaigns, suggesting that early participation by professional investors has a stronger positive influence in the IT sector.

This interaction pattern is consistently observed across both dependent variables—success rate and pledge rate—indicating a statistically significant moderating effect of industry type on the relationship between herding behavior and crowdfunding outcomes.

Discussion and Implications

Discussion of Findings

The findings of this study confirm that early participation by professional investors significantly increases the likelihood of crowdfunding success. This effect is consistent with signaling theory, in which signals are valued according to the credibility of their source. Our results extend this literature by showing that the signaling role of professional investors is not only statistically significant but also strategically important in the uncertain and transparent environment of crowdfunding.

More importantly, the analysis highlights how industry context shapes the strength of these signals. In the IT sector, where technological complexity and uncertainty exacerbate information asymmetry, professional investors’ actions function as particularly salient cues for other investors. This finding suggests that industry-specific conditions can amplify the signaling role of professionals, pointing to an important boundary condition of herding effects in equity crowdfunding.

These results move beyond prior studies that focused primarily on the existence of herding behavior. Instead, they clarify under what conditions professional investors’ signals matter most, thereby enriching the theoretical understanding of investor behavior in two-sided crowdfunding platforms.

Implications for Research

This study contributes significantly by investigating the dynamic aspects inherent to the platform. The research implications derived from this study are outlined below. First, this study advances existing literature by specifically considering the herding effect of professional investors, recognized as highly reliable signal actors. Unlike traditional funding channels, crowdfunding operates on a platform-based model with a transparent funding process, introducing campaign-based dynamics. However, prior studies predominantly focused on static information and signals related to companies or entrepreneurs, overlooking the unique dynamics intrinsic to crowdfunding platforms (Cosma et al., 2019; Nitani et al., 2019; N. Wang et al., 2021). Additionally, crowdfunding’s distinctiveness lies in the transparent disclosure of each campaign’s funding process through the platform, elevating the significance of initial funding for each campaign. Nevertheless, existing studies either failed to demonstrate herding behavior or did not distinguish between investor types (Hornuf & Neuenkirch, 2017; Vismara, 2018). The results of this study filled the research gap of the existing study in that they confirmed that there was a herding behavior and that there was an influence of professional investors.

Secondly, the herding effect, confirmed in previous studies, has been empirically verified in this research. Prior studies on equity crowdfunding primarily centered on demonstrating the existence of herding behavior among investors, rather than delving into its influence on campaign success (Estrin et al., 2022; Walther & Bade, 2020; W. Wang et al., 2019). This study is significant in that it not only reaffirms the existence of the herding effect in the equity crowdfunding market, as claimed in previous studies, but also empirically analyzes it based on actual data and presents the results.

Lastly, this study empirically analyzes and suggests that the impact of the herding effect on crowdfunding success is more pronounced in the IT industry, where information asymmetry is relatively high compared to other industries. Previous research on investor herding effects consistently showed a positive impact on funding success, irrespective of information asymmetry (Liu et al., 2017). This study enhances the existing literature by comparing the signal effects of investors across industries, considering information asymmetry.

Implications for Practice

This study unfolds several practical implications, offering insights for various stakeholders in the crowdfunding ecosystem. Primarily, the active involvement of professional investors during the initial phase of campaign funding emerges as a crucial signal that significantly influences other investors. Crowdfunding platforms, such as Wadiz, adopt a transparent approach by disclosing information such as the type and quantity of participating investors for each campaign. This transparency not only establishes trust but also proves to be an effective strategy in enhancing crowdfunding success rates. By recognizing the strategic importance of professional investor participation, crowdfunding campaigns can strategically position themselves to attract a broader investor base.

For platform operators, one implication is the potential value of emphasizing professional investor participation. Platforms could feature such participation more prominently on campaign pages or create badges for campaigns endorsed by professional investors. These design choices may amplify the signaling effect and reduce information asymmetry for general investors.

Moreover, entrepreneurs can draw valuable practical insights from this study, particularly in devising effective fundraising strategies in the early stages of a campaign. The findings underscore the imperative for entrepreneurs to actively seek the involvement of reputable and confidence-inspiring investors during the campaign’s initiation. This early collaboration with professional investors not only sets a positive tone for the campaign but also contributes significantly to its overall success. Entrepreneurs can leverage these insights to refine their fundraising strategies and enhance their likelihood of achieving target funds.

Lastly, this study unveils a practical implication related to industry-specific variations in information asymmetry. Recognizing that information asymmetry varies across industries, this study emphasizes the pivotal role of professional investors in sectors where the divide between professional and general investors is pronounced. In such information-intensive domains like the IT industry, the influence of professional investor signals becomes particularly significant, contributing to the success of crowdfunding campaigns. This insight is valuable for industry participants, highlighting the strategic importance of professional investor engagement in sectors characterized by heightened information asymmetry.

The practical implications can be categorized by stakeholder group. For entrepreneurs, securing professional investors at an early stage can substantially improve the chances of success by sending credible signals. For general investors, recognizing the participation of professionals offers a reliable heuristic for evaluating campaigns. For platforms, highlighting or certifying professional involvement can improve transparency and boost investor trust.

Limitations and Future Research Directions

This study examines how early professional investor signals in the early stages of crowdfunding influence subsequent investors and campaign success. While the findings provide important insights, several limitations remain.

First, our analysis primarily captures the initial involvement of professional investors but does not fully explain the trajectory of success throughout subsequent funding stages. Future research should adopt longitudinal designs to explore how reliable investor participation evolves across the entire campaign period. This study also relies on cross-sectional campaign-level data, which restricts our ability to trace sequential decision-making and dynamic herding patterns across time. Future research using longitudinal or transaction-level data would enable deeper insights into the temporal dynamics of herding behavior.

Second, the study does not incorporate a comparative analysis of different types of signals. Because crowdfunding platforms provide diverse forms of information to mitigate asymmetry, future research could compare the relative effects of signals from entrepreneurs, platforms, and investors, thereby offering strategic implications for campaign design. Relatedly, self-pledge funding by entrepreneurs or relatives represents an alternative form of expertise, but data limitations prevented its inclusion in our analysis.

Third, while our analysis centers on the IT industry, other high-information-asymmetry sectors such as biotechnology may provide valuable contexts to investigate the role of professional investors. Extending the study to multiple industries would allow researchers to test whether herding dynamics operate similarly across sectors, enhancing external validity.

Finally, the findings should be interpreted in light of South Korea’s regulatory and cultural environment. The Capital Market Act, which imposes a 5 million cap on individual investments, shapes the dynamics of equity crowdfunding and may amplify the signaling role of professional investors. In addition, Korea’s strong emphasis on IT entrepreneurship may have contributed to the pronounced herding effect observed. Future research should replicate this study in countries with different institutional frameworks and cultural settings to enable cross-national comparisons.

Footnotes

Ethical Considerations

This study does not involve human or animal subjects and therefore did not require ethical approval.

Author Contributions

Jeehyung Jo and Sodam Kim contributed equally to this work and share first authorship.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Innovation Team Project of the Department of Education of Guangdong Province [Grant number: 2022WCXTD022].

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data will be available upon reasonable request.