Abstract

The impact of environmental regulation (ER) on corporate sustainability has been widely studied, but few studies have comparatively analyzed this process from the dual perspectives of formal and informal environmental regulation (FER&IER). The impacts of top-down FER and bottom-up IER on firms remain an area that warrants further investigation. This study uses data from Chinese A-share listed companies between 2011 and 2023 to compare and analyze the impact of FER and IER on corporate sustainability. The results reveal that: (a) Both FER and IER enhance corporate sustainability, with the effect being more pronounced among state-owned enterprises, non-heavily polluting firms, and in the central and eastern regions. (b) Financing constraints, free cash flow, labor input, and R&D investment play differentiated roles under varying environmental regulatory contexts, and these channels collectively shape corporate sustainability. (c) FER and IER complement each other, promoting different sustainability dimensions. This research provides novel insights into the theoretical and empirical link between environmental regulation and long-term corporate development.

Keywords

Introduction

Against the backdrop of increasingly extreme climate change, the role of environmental regulation (ER) has become more prominent (Liao & Xiao, 2025). This has prompted governments worldwide to actively implement sound regulatory policies to achieve environmental protection goals. Over the past two decades, China’s climate policy uncertainty (CCPU) has increased year by year (See Figure 1), accompanied by a growing emphasis by authorities on ER (Ma et al., 2023). As the world’s second-largest economy, China has significantly strengthened ER through various measures, thereby improving environmental quality and advancing the green economy (Gao et al., 2025). Specifically, China not only enacted the most stringent Environmental Protection Law in its history but also introduced the Code of Conduct for Citizens’ Ecological and Environmental Behavior in 2022 to promote low-carbon lifestyles. In addition, China’s environmental non-governmental organizations, such as Friends of Nature, have developed considerable influence and continue to play an active role in environmental supervision. However, the pressure to prioritize environmental protection over economic growth for the sake of environmental protection presents numerous practical challenges. Therefore, approaches to balancing sustainable economic growth with environmental protection have gradually become a key issue that is closely monitored and thoroughly explored in academic research (Gao & Wang, 2023; Y. Wang et al., 2020).

Trend of the annual CCPU index.

Although ER plays a critical role in reconciling economic growth with environmental protection, its precise definition remains contested in the academic literature. Formal environmental regulation (FER) refers to coercive measures imposed by governments through laws, policies, and other binding instruments to regulate the environmental behavior of firms and individuals. In contrast, informal environmental regulation (IER) denotes environmental pressures exerted by social actors such as the public, including media supervision and consumer choices. Given the broad scope of ER, its potential impacts extend across a wide range of economic and social domains. At the macro level, these factors include: urban green innovation efficiency (H. Peng et al., 2021), green economy and renewable energy growth (Zhao et al., 2022), and green productivity in industrial sectors (Qiu et al., 2021), among others. For example, Zou and Wang (2024) utilized an extensive array of data on China’s ER policies and energy transition measures, employing statistical analysis techniques to probe the pivotal role of ER in advancing energy transition. At the micro level, the factors affected include: corporate innovation (Jaffe & Palmer, 1997), corporate debt costs (X. Ni et al., 2022), and corporate capacity utilization rates (Li & Du, 2022), among others. Moreover, Farooq et al. (2024) mentioned that while ER has a significant suppressive influence on investment decisions, it simultaneously promotes corporate green innovation.

Among the various micro-level factors influenced by ER, corporate sustainability has garnered significant attention. Sustainable development is the development that satisfies present demands without compromising future generations’ ability to fulfil their own needs (Brundtland & Mansour, 2010). In existing literature, corporate sustainability is typically explained from three perspectives: environmental, economic, and social (Shahzad et al., 2020). These three core elements are referred to as the “Triple Bottom Line,” which has the potential to impact both present and future generations (Elkington, 1997). Since corporate ESG performance inherently carries economic significance, corporate sustainability based on the “Triple Bottom Line” is fundamentally aligned with ESG principles. Furthermore, as extreme climate events become more frequent alongside the ongoing process of economic globalization, an increasing number of companies are using enterprises’ ESG as a criterion for their sustainability. The influence of ER on firms’ sustainability can be examined through its multi-dimensional effect on ESG performance.

ER can indirectly influence corporate sustainability through various levels, particularly through the interaction mechanisms across the environmental, social, and corporate governance dimensions. At the environmental level, ER can effectively improve corporate environmental performance (W. Zhang, Luo, et al., 2022). Specifically, urban environmental legislation and environmental orientation can enhance corporate environmental performance (B. Zhang et al., 2023). ER also influences corporate green innovation and green investment (D. Peng & Kong, 2024). At the social level, ER can affect TFP and green economic growth (Y. Liu et al., 2022). Meanwhile, the high-quality development of Chinese society is closely linked to ER (J. Wang & Zhang, 2022). At the corporate governance level, ER can control corporate behavior and impact corporate green investment (Q. Zhong et al., 2022). One study suggests that environmental law can influence corporate governance (Ong, 2001). This research also recommends legally encouraging companies to improve their management culture to explicitly incorporate environmental concerns into decision-making processes. In conclusion, ER, through the interaction of the E, S, and G dimensions, constructs a bridge that influences firms’ sustainability.

Despite the growing literature on ER and corporate sustainability, several gaps remain. It is still unclear whether both FER and IER exert significant positive effects on corporate sustainability, and their underlying mechanisms and heterogeneity have not been systematically examined. While a few studies have touched upon these issues, comparative research on FER and IER remains scarce and is often constrained by inconsistent definitions, limited scope, and methodological subjectivity. Addressing these gaps provides the second motivation of this study. To this end, we employ a panel dataset of Chinese A-share listed firms from 2011 to 2023 and adopt a fixed-effects model to investigate the impacts of ER from both formal and informal perspectives. First, we verify the effects of ER on corporate sustainability from a dual-dimensional lens and conduct a series of robustness checks to ensure the reliability of the findings. Second, we explore the heterogeneous effects of FER and IER across regions, ownership structures, and industries, while unveiling the mechanisms of financing constraints and free cash flow through mediation models, and further testing the moderating roles of labor input and R&D investment. Finally, we examine how FER and IER differentially influence firms’ performance across the three ESG pillars.

The marginal contributions of this study are reflected in several key aspects. First, this study offers a comparative analysis of how FER and IER influence corporate sustainability. By unpacking their underlying mechanisms, it provides theoretical explanations for their distinct mediation channels and moderating directions. Unlike prior work that assumes uniform mechanisms, this paper contrasts the mediating roles of financing constraints and free cash flow, as well as the moderating effects of labor and R&D investment, thereby uncovering the differentiated pathways through which FER and IER operate. Second, it further examines the heterogeneous effects of FER and IER on corporate sustainability. The comparative results demonstrate that both types of regulation significantly enhance sustainable development among firms located in central and eastern regions, state-owned enterprises, and non–heavily polluting industries, providing tailored insights for different types of firms. Third, this study advances beyond the conventional reliance on aggregate ESG indicators by revealing the distinct driving effects of FER and IER across the three ESG pillars, offering strategic guidance for firms in responding to differentiated regulatory regimes.

The following sections of the paper are organized as follows: Section 2 depicts the literature review; Section 3 describes the theoretical analysis and research hypothesis; Section 4 depicts an explanation of the data and research methodology; Section 5 reports the empirical results and discussion; Section 6 contains the further analysis; and Section 7 summarizes the conclusion and policy recommendations.

Literature Review

We begin by discussing the classification of ER, the proxy indicators of corporate sustainability, and the potential ways in which FER and IER may influence the process of corporate sustainability. Existing literature categorizes ER into three classifications: command-and-control regulation, market-based incentives, and public participation (Ren et al., 2018; Y. Sun & Zhou, 2024). Command-and-control regulation is mandatory and typically achieves environmental protection goals through government enforcement of relevant policies. During the early stages of China’s ER design, command-and-control regulation played a dominant role (Long & Zhang, 2012). However, overly stringent ER may stifle the initiative of economic entities, whereas market-based incentives can help mitigate this issue. Market-based ER utilizes economic instruments to alter the costs and profits associated with pollution, allowing firms to navigate between financial and environmental protection (Qin et al., 2024). However, rational companies tend to prioritize their interests when responding to market-based ERs, often reducing expenses to ease the financial load imposed by environmental pollution (Fabra & Reguant, 2014). Additionally, polluters are not only constrained by government organizations and their policies but also by public oversight, which is an element of public involvement in ER. The public can report various non-environmentally friendly behaviors to the relevant authorities through different channels, exercising the right to supervise. Gu et al. (2021) indicate that public environmental concerns do not place the economic responsibility for pollution operations directly on companies. Instead, compliance with ERs can enhance a company’s reputation.

Another explanation categorizes ER into formal and informal categories (Lee et al., 2022). An examination of the existing literature shows that some researchers use regulatory indicators associated with government organizations to proxy for FER. These include investments in industrial pollution control in corporate ratings of government environmental pressure (Wu et al., 2022) and the level of treatment of certain pollutants (Levinson, 1996). S. Zhong et al. (2021) measure the intensity of FER using the number of environmental recommendations passed by local governments. Besides, IER is typically viewed as an effective supplement to formal government-imposed regulation, mainly encompassing environmental information disclosure, public environmental advocacy, Baidu search indices, and various composite measures (Tan et al., 2024). For example, J. Wang (2025) selected a series of indicators from the company’s location to comprehensively gauge the IER’s strength, similar to the approach of Pargal and Wheeler (1996).

Although existing literature offers varied explanations of ER, analyzing it from formal and informal perspectives seems to provide a relatively comprehensive explanation. As discussed above, there is an overlap between the command, market, and public categories of ER and the categories of formal and informal regulation. According to H. Zhang, Xu, et al. (2022), FER can encompass command-and-control and market-based ER, while informal regulation also includes various forms of public environmental concern. Some scholars have measured ER from other perspectives, such as industry and region, but these do not extend beyond the aforementioned regulatory categories (Jiang et al., 2021). Therefore, after researching the definition and measurement of ER, this paper explores whether ER, from both formal and informal perspectives, can influence corporate sustainability.

Corporate sustainability has become an increasingly important goal for managers across various industries (Meuer et al., 2020). Current literature provides several interpretations of corporate sustainability. First, some studies explain corporate sustainability through the three factors of environmental, social, and economic dimensions (Machado et al., 2021; Tjahjadi et al., 2021). These three factors are generally called the “Triple Bottom Line.” A specific interpretation is that a company is sustainable when it achieves prosperity in the economic, environmental, and social justice dimensions (Jeurissen, 2000). Several internationally recognized indices also use this approach for comprehensive measurement, such as the DJSI, FTSE KLD 400 Social Index, and STOXX Europe Index. Additionally, Shahzad et al. (2020) developed sustainability metrics for the environmental, economic, and social aspects, exploring the positive effects of green innovation on corporate sustainability from these three perspectives. Second, some studies use corporate ESG as a stand-in for corporate sustainability. Specifically, the performance in ESG metrics reflects a company’s commitment to sustainability, balancing short-term profits with long-term social growth and ecological protection (Du et al., 2024). With the growing international recognition of corporate ESG performance, more and more studies have used ESG to explain corporate sustainability (Velte, 2023). Especially in emerging markets in developing countries, many companies seek good ESG performance to align with sustainable development concepts. Therefore, ESG performance is closely related to corporate sustainability, and this paper also uses ESG performance as a proxy for corporate sustainability.

This study, grounded in Porter’s hypothesis and stakeholder theory, compares and analyzes the impact processes of FER and IER on corporate sustainability. Porter’s hypothesis emphasizes the innovation driven by top-down FER, which may further promote corporate sustainability. For instance, Chinese retail firms can enhance digital empowerment to meet FER requirements, thus driving green and low-carbon collaborative development and improving sustainability (T. Sun et al., 2024). Stakeholder theory posits that firms must consider public interests, represented by consumers. In response to bottom-up IER, Chinese firms can improve the level of digital green public services and environmental information disclosure to promote sustainable development (T. Sun, Di, Cai, & Du, 2025; T. Sun, Di, Hu, et al., 2025). Moreover, the relationship between environmental regulation and sustainable development has been extensively examined in the context of low-carbon transformation, particularly from the perspectives of policy effectiveness, regional differences, and firm behavior (Di, Chen, Shi, Cai, & Liu, 2024; Di, Chen, Shi, Cai, & Zhang, 2024; Di et al., 2023).These studies provide important theoretical insights into green consumption, carbon emission reduction, and industrial development, laying the foundation for firms seeking sustainable development.

Nevertheless, there are limited studies that directly explored the influence of ER on corporate sustainability from formal and informal perspectives. Previous research often separates ER from corporate sustainability, with few studies directly investigating the influence of ER on sustainability. Additionally, while there are a few research papers examining the influence of ER on corporate sustainability, these studies still have space for enhancement regarding the proxy and measurement of ER. For example, Lu and Cheng (2023) used the “Environmental Protection Law” as an exogenous shock event and employed the DID methodology to determine the influence of ER on firms’ ESG. This approach, which uses a specific legal shock as a proxy for regulation, is a narrow and specific form of ER, and other environmental constraints could also influence corporate ESG. Therefore, to fill the gap in current research, this work further explores the correlation between ER and corporate sustainability from the perspectives of FER and IER.

Theoretical Analysis and Research Hypothesis

The research hypothesis framework of this paper is illustrated in Figure 2.

The research hypothesis framework.

Porter’s hypothesis suggests that moderately stringent ERs can stimulate firms to innovate, thereby enhancing their long-term competitiveness. Consistent with this logic, FER raises compliance costs as a coercive regulatory pressure. While this initially reduces productivity (Porter & van der Linde, 1995), the “strong version” of Porter’s hypothesis argues that firms will actively seek innovation-driven solutions to offset rising costs (Yan et al., 2024). Such innovation, including process optimization and technological upgrading, not only mitigates cost burdens but also strengthens firms’ resource endowments, ultimately improving their long-term competitiveness and sustainability. In contrast, IER operates through pressures imposed by stakeholders such as the public, media, and consumers. Social scrutiny and media exposure heighten firms’ reputational risks and reshape consumer preferences, compelling firms to voluntarily adopt greener production modes to safeguard legitimacy. This bottom-up pressure motivates firms to reconfigure their strategies and product portfolios, thereby facilitating proactive sustainability transitions.

Taken together, both FER and IER are key drivers of corporate sustainability. Existing studies also confirm that both types of regulation positively contribute to environmental performance, social responsibility, and long-term growth (Cao et al., 2021; Chiou et al., 2011; D. Zhang, 2021). Given this, the paper’s first hypothesis is as follows:

ER not only affects corporate production but also signals to the capital markets, thereby deteriorating the financing environment for firms (Geng et al., 2021). This is consistent with signaling theory, which suggests that firms convey signals to external stakeholders (e.g., investors) through their actions and disclosures. Moreover, ER has a notable negative influence on both short-term and long-term external financing for firms, with a more pronounced effect on short-term financing (Xu et al., 2022). Although both FER and IER affect firms’ financing, their mechanisms differ. FER intensifies government constraints on external financing, whereas IER effectively restrains firms’ internal financing behavior (X. Liu et al., 2018). Moreover, financial constraint theory posits that firms’ financing decisions are largely contingent upon their financial condition. The tightening of financing constraints (FC) induced by FER exacerbates financing difficulties, which may hinder corporate sustainability. This occurs because intensified financing constraints often reduce firm performance and thereby weaken profitability (D. Zhang & Lucey, 2022). A decline in profitability diminishes production incentives, significantly undermining sustainability.

Similarly, under public scrutiny, firms tend to experience heightened financing constraints. Heightened IER may reinforce such constraints and reduce firms’ free cash flow (FCF) (Y. Sun, Zhu, et al., 2025). IER, manifested through public attention, may play a monitoring role over FCF, thereby suppressing it. Since FCF is positively associated with corporate sustainability (Chams et al., 2021), IER could impede sustainability by diminishing FCF. However, compulsory FER does not lend itself to a straightforward linkage with FCF. Drawing on rent-seeking theory, overly stringent government regulation may induce firms to engage in behaviors such as bribery of supervisory agencies in order to circumvent regulatory pressure. Such practices complicate the relationship between FER and FCF and weaken the mediating role that FCF would otherwise play. Building on this, the next set of hypotheses is formulated as follows:

During corporate sustainability development, the labor force and R&D investment serve as moderators in firms’ adaptation to external ERs. On the FER side, it inevitably influences corporate production processes, resulting in alterations to labor demand. Strict ER reduces the demand for labor (M. Liu et al., 2017), and companies generally react to regulatory pressure by eliminating jobs rather than slowing down their hiring rates (Walker, 2011). According to economies of scale theory, a firm’s labor demand is directly tied to its production scale, which in turn affects corporate sustainability. Moreover, stringent FER can raise compliance costs and strain resources, prompting firms to cut sustainability-related investments. These financial pressures may reduce R&D spending, hinder green innovation, and weaken sustainability performance.

In contrast, IER is primarily driven by non-coercive factors, which render it more adaptive and flexible. Stakeholder theory asserts that firms need to account for the expectations of various stakeholders, including workers and investors (Freeman, 1984). At the same time, modern corporate theory suggests that firms seek support from various social stakeholders to gain more benefits. Accordingly, firms are more inclined to heed the concerns of workers and investors, particularly those related to environmental issues, thereby sustaining adequate labor and R&D investment. Additionally, laborers themselves can exercise public oversight, and a greater workforce might be more beneficial for the implementation of IER, thus promoting corporate sustainability. According to the theory of innovation, corporate R&D activities are the engine of economic growth, and R&D investment is considered a core driver of innovation and sustainability (Z. Zhang, Zhu, et al., 2022). IER expects firms to increase their R&D investment, thereby promoting corporate sustainability. Drawing from this, the third set of hypotheses is proposed as follows:

Data and Research Methodology

Baseline Model

This research constructs the following baseline model to investigate the influence of ER on corporate sustainability:

Where subscripts i and t symbolize firms and years, respectively; CSit denotes corporate sustainability, measured by ESG scores; ERit represents two types of ER, namely FER and IER; Controlsit includes a set of control variables. Additionally, firm, year, industry, and city fixed effects are incorporated, denoted as λFirm, ηYear, κInd, and μCity, respectively. εit is the random error term. All estimates employ firm-level clustered robust standard errors.

Sample and Data

The study uses Chinese A-share listed firms during the 2011 to 2023 period as the study sample. Firm-level data are obtained from the CNRDS platform and the CSMAR database. ER’s data are drawn from the Baidu Search Index and the National Bureau of Statistics of China. Corporate sustainability is measured using the comprehensive ESG score published by the Huazheng ESG rating system. The data undergoes the following processing steps: (a) Financial organizations are eliminated from the data; (b) Firms categorized as S.T. and *S.T. are excluded; (c) Data points with incomplete financial variables are removed. To mitigate estimation bias attributable to extreme values, each continuous variable is winsorized at the 1% threshold on both ends. A total of 4,159 A-share listed firms and 31,443 firm-year observations are included in the final sample.

Variable Definitions

Corporate Sustainability

Following P. Chen (2023), this research adopts the ESG composite score to assess corporate sustainability. The Huazheng ESG framework consists of three pillars, 16 themes, and 44 key indicators, covering a broad spectrum of aspects ranging from climate change to business ethics. As an evaluation metric from environmental, social, and governance dimensions, the ESG score effectively reflects corporate quality and long-term sustainability.

Environmental Regulation (ER)

This study constructs ER indicators from both formal and informal perspectives. Building on existing research, FER refers to environmental governance measures implemented by formal entities, such as government agencies or relevant organizations, and is typically characterized by its enforceability. In contrast, IER is driven by public attention and oversight of environmental issues, which can exert pressure on companies, but lacks legal enforceability.

Following Song et al. (2021), FER intensity is proxied by the ratio of industrial pollution control investment to the value-added of the secondary industry. Pollution control investment is closely linked to FER, as mandatory regulations increase local environmental costs, thereby reflecting the stringency of regional ERs. A higher ratio indicates stricter FER. Referring to Fan et al. (2024), this study measures IER intensity using the Baidu Search Index for the term “environmental pollution.” As Baidu is a leading Chinese search engine, its search index reflects public attention to environmental issues. The search index includes data from both mobile and PC platforms, and this study aggregates both sources and scales them by dividing by 100. A higher search index indicates a stronger IER.

Control Variables

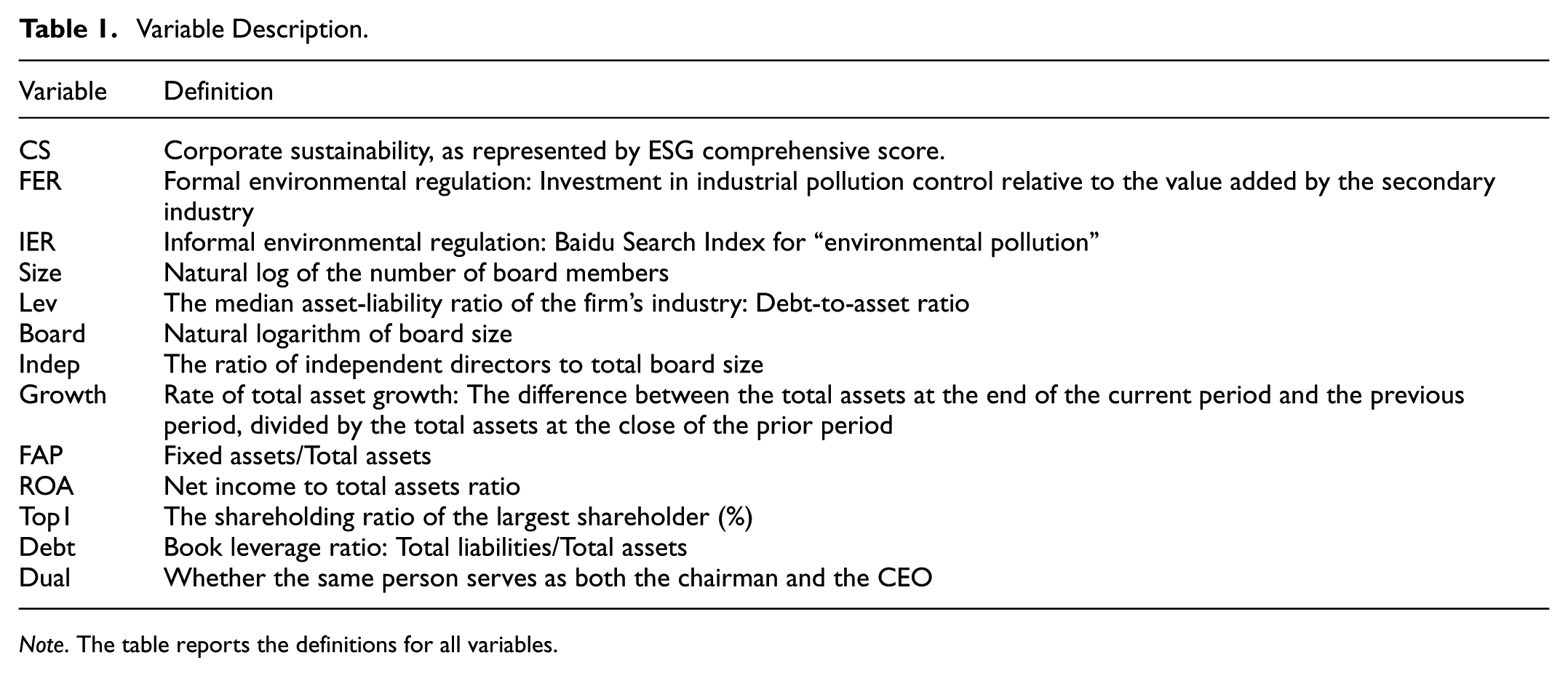

Following Gao, Tan, and Duan (2024), the variables are controlled for in this study: firm size (Size), median industry leverage ratio (Lev), board size (Board), Percentage of independent directors (Indep), rate of revenue growth (Growth), fixed asset proportion (FAP), return on assets (ROA), the ownership proportion of the biggest shareholder (TOP1), debt ratio (Debt) and CEO duality (Dual). The data are sourced from the CSMAR database, with a detailed summary provided in Table 1.

Variable Description.

Note. The table reports the definitions for all variables.

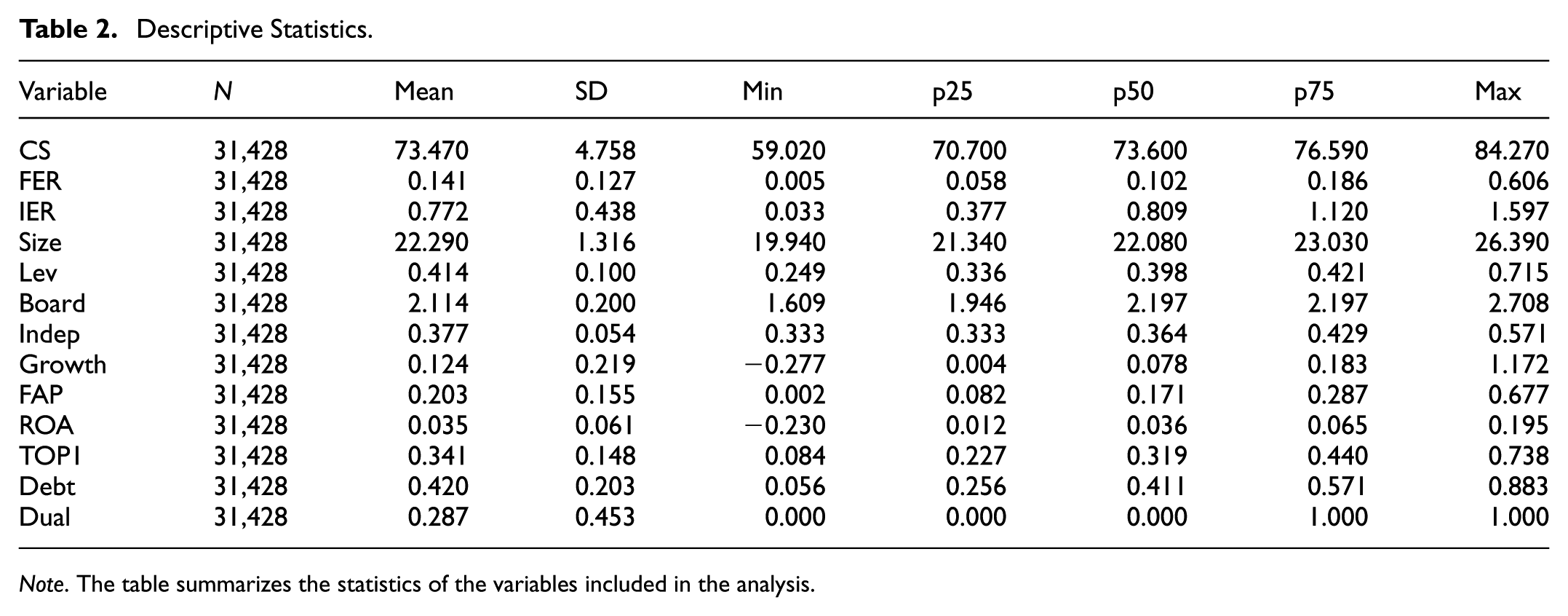

Descriptive Statistics

The descriptive statistics of the principal variables are shown in Table 2. Specifically, the CS score has an average value of 73.470, accompanied by a standard deviation of 4.758. More than 75% of firms have a CS score above 70, with most clustering between 70 and 80. This indicates relatively minor variations in corporate sustainability among A-share listed firms in China. The mean FER is 0.141, spanning from 0.005 to 0.606, accompanied by a standard deviation of 0.127, suggesting significant disparities in FER across provinces. The mean IER is 0.772, with a minimum of 0.033, a maximum of 1.597, and a standard deviation of 0.438, highlighting considerable variation in IER across firms. Furthermore, Table 2 presents the quartiles for the primary variables, providing a comprehensive view of their distributional characteristics.

Descriptive Statistics.

Note. The table summarizes the statistics of the variables included in the analysis.

Empirical Results and Discussion

Baseline Regression

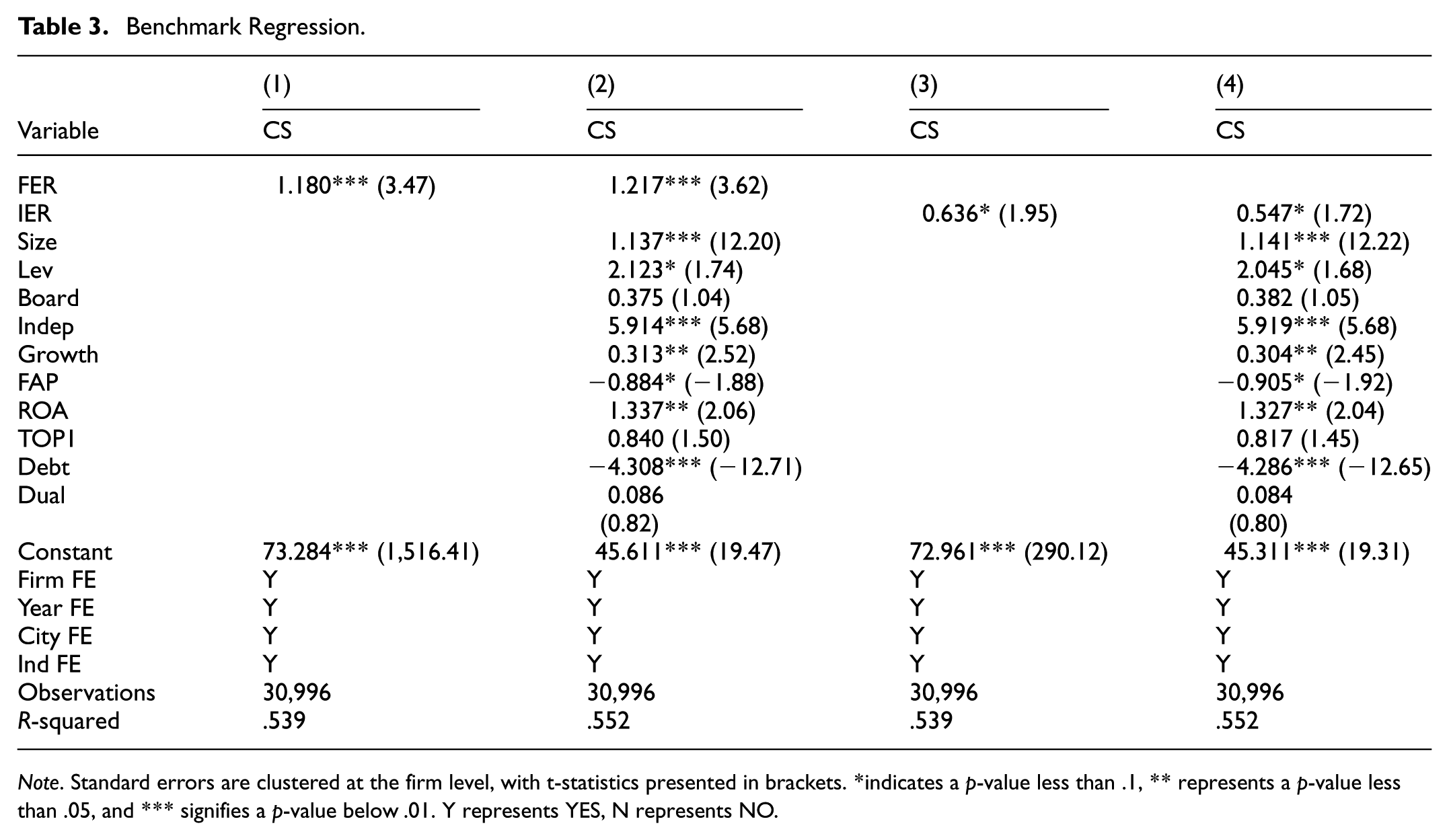

Table 3 reports the fundamental regression results on the association between ER and corporate sustainability. Using ESG scores as the proxy for corporate sustainability, this research examines the influence of both FER and IER. In Table 3, the first and third columns include only fixed effects. The second and fourth columns further incorporate control variables. These findings indicate that both FER and IER significantly promote corporate sustainability, underscoring the broadly positive effect of ER. However, firms failing to adapt to FER and IER may face increased social risks, reduced investments, and potential administrative penalties for continuing inefficient production. Conversely, compliance with ERs can help firms avoid these constraints, fostering green innovation and sustainable development (L. Ni et al., 2023). Thus, firms tend to make rational choices regarding the opportunity costs associated with ER, adapting to FER and IER to enhance their sustainability. These results provide empirical support for Hypothesis H1.

Benchmark Regression.

Note. Standard errors are clustered at the firm level, with t-statistics presented in brackets. *indicates a p-value less than .1, ** represents a p-value less than .05, and *** signifies a p-value below .01. Y represents YES, N represents NO.

One possible explanation is that firms’ compliance with ERs can reduce their long-term constraints and enhance their capacity for sustained development. As a top-down, legally enforceable regulation, FER may compel firms to engage in green innovation and adopt more sustainable development paths to avoid government penalties (Farooq et al., 2024). Meanwhile, IER, which encompasses pressures from social actors such as consumers and media, may encourage firms to adopt green practices to enhance their public image and respond to consumer demand for more environmentally responsible products (Fan et al., 2024). At the same time, IER, driven by public opinion pressure, may motivate firms to adopt green production practices to enhance their public image and respond to consumer demand for environmentally friendly products.

Furthermore, results from columns (2) and (4) reveal that firm size, industry median leverage, the proportion of independent directors, total asset growth, and return on assets positively influence corporate sustainability (Y. Chen et al., 2024). This suggests that firms with larger asset bases and higher independent director ratios tend to exhibit stronger sustainability performance (Cucari et al., 2018). However, fixed asset ratios and leverage negatively impact corporate sustainability, implying that firms with higher fixed assets and leverage face greater sustainability challenges. Therefore, to improve sustainable performance, firms should maintain lower fixed asset and leverage levels.

Robustness Checks

To verify the robustness of the baseline model, we conduct a series of robustness checks at this stage. First, we replace the sample data of FER and IER to test their generalizability. Second, we exclude firms with less than 5 years of data due to excessive missing values, which diminishes their reference value. Third, we have incorporated new control variables into the fundamental regression to mitigate the problem of missing variable bias. Furthermore, we replace or add joint fixed effects to control for additional unobserved variables. Finally, we employ the instrumental variables method to address the endogeneity issue in the original model. Overall, the outcomes of these robustness checks are consistent with the fundamental regression. The specific details can be found in Appendix A.

Mechanism Analysis

Mediating Effect

To determine the role of FC and FCF in the correlation between ER and corporate sustainability, we built a mediation effect model as follows:

Where Mit represents the corresponding mediating variable, CSit denotes corporate sustainability, measured by the ESG score; ERit represents the two types of ER; the subscripts i and t refer to the firm and the year, respectively, while other variables, including fixed effects and the fundamental regression model, remain the same.

According to the mediation framework of Wen and Ye (2014), the product α1γ2 represents the indirect effect, while γ1 denotes the direct effect. When the indirect and direct effects share the same sign, the result is a mediation effect; when they differ in sign, it constitutes a suppressor effect. A suppressor effect is a strict subset of mediation effects. In addition, α1γ2/β1 reflects the proportion of the total effect explained by the mediation pathway, and |α1γ2/γ1| captures the ratio of indirect to direct effects (See Figure 3). We also refer to these two measures, following Wen and Ye (2014), as the mediation ratio and suppression ratio, respectively. In our analysis, financing constraints act as a suppressor in the mechanism through which FER and IER enhance corporate sustainability, with suppression ratios of 0.011 and 0.037, respectively. Free cash flow suppresses only the positive effect of IER on corporate sustainability, with a suppression ratio of 0.016.

Mediation model diagram.

This research first examines how FC affects the role of ER in enhancing corporate sustainability. The study finds that both FER and IER exacerbate FC, thereby weakening their positive impact on corporate sustainability. However, under the heightened financing constraints induced by FER and IER, firms that comply with regulatory requirements can benefit from improved reputational standing and greater market acceptance, which in turn enhances their sustainability performance. Such firms may also receive policy support in the form of subsidies, tax incentives, or preferential access to government procurement. These advantages collectively contribute to better sustainability outcomes. Therefore, the suppressing effect of FC does not alter the direction of the total effect. FER and IER still contribute positively to corporate sustainability.

Additionally, this study investigates the mediating mechanism of FCF. We find that there is no direct relationship between FER and FCF, but FCF directly promotes corporate sustainability. During the process of FER promoting corporate sustainability, FCF does not serve as a mediating factor. One possible explanation is that, under stringent FER, firms may divert part of their FCF to rent-seeking activities, leading regulatory authorities to relax environmental assessment standards (Tang et al., 2024). In other words, firms may bypass a comprehensive green transformation of their production systems by expending only a small amount of capital. Such selective rent-seeking behavior complicates the process through which FER constrains FCF. However, IER is negatively correlated with FCF, which can also directly foster corporate sustainability. Thus, FCF has a mediating effect, meaning that IER inhibits the positive impact of FCF on corporate sustainability. These findings validate Hypotheses H2a and H2b. The detailed results are presented in Tables 4 and 5.

Channel Analysis (1).

Note. Standard errors are clustered at the firm level, with t-statistics presented in brackets. * indicates a p-value less than .1 and *** signifies a p-value below .01. Y represents YES, N represents NO.

Channel Analysis (2).

Note. Standard errors are clustered at the firm level, with t-statistics presented in brackets. *indicates a p-value less than .1 and *** signifies a p-value below .01. Y represents YES, N represents NO.

Moderating Effect

The mechanism through which ER impacts corporate sustainability may not be limited to a mediating effect. To further explore the underlying mechanisms, this study creates a moderating effect model as follows:

Where Channelit represents the moderating variable, CSit denotes corporate sustainability measured by ESG scores; ERit signifies the two types of ER, and ERit×Channelit is the interaction term between ER and the moderating variable. Subscript i denotes the firm, while subscript t indicates the year, and other variables and fixed effects match the benchmark regression model. If the coefficient φ3 of ERit×Channelit is statistically marked, it implies the existence of a moderating effect. A significantly positive φ3 demonstrates that the moderating variable increases the favorable effect of ER on corporate sustainability, whereas a significantly negative φ3 implies that the moderating variable weakens this effect. The detailed results are presented in Table 6.

Channel Analysis (3).

Notes. Standard errors are clustered at the firm level, with t-statistics presented in brackets. * indicates a p-value less than .1, ** represents a p-value less than .05, and *** signifies a p-value below .01. Y represents YES, N represents NO.

This study first identifies labor as the mechanism linking ER and corporate sustainability. The results indicate that excessive labor weakens the positive impact of FER on sustainability, as it leads to increased management complexity, which in turn escalates the risk of non-compliance. This happens because excessive labor increases management complexity, which leads to a higher risk of non-compliance with formal regulatory standards. The more complex the management, the more difficult to achieve sustainability. However, an increase in labor can lead to greater public oversight, thereby enhancing the role of IER in promoting corporate sustainability. A larger workforce may facilitate better public oversight, such as through civil society groups, media, or public pressure, thereby strengthening the informal regulations’ impact on promoting sustainability.

Additionally, this paper analyses the role of R&D in fostering corporate sustainability under ER. We find that R&D investment weakens the positive impact of FER on corporate sustainability. A possible explanation is that R&D expenditure diverts resources that could be used to address FER requirements. Moreover, the green innovations driven by R&D are lagging in nature, which temporarily hampers corporate sustainability in the short term. However, it is also since R&D can drive green innovation, improve corporate reputation and competitive advantage, thereby strengthening the positive effects of IER (Bataineh et al., 2024). And the public is generally supportive of firms increasing R&D, which aligns with the values promoted by IER, driven by public oversight. This positive sentiment, in turn, positively moderates corporate sustainability. These findings validate Hypotheses H3a and H3b.

A Firm-Level Case

We next introduce a representative Chinese enterprise case, BYD, to illustrate how different types of ER specifically impact corporate sustainability (see Figure 4). On the one hand, FER, through strict emission standards and new energy vehicle subsidies, forces companies to bear higher compliance costs. At the same time, BYD, under the constraints of the dual-credit policy, increased R&D investment to upgrade key technologies such as batteries and motors. While this process exacerbated financing constraints in the short term, BYD gradually mitigated these pressures and accumulated long-term competitive advantages with government subsidies and capital market financing. On the other hand, IER, through public and media attention to the safety and environmental performance of BYD, prompted BYD to proactively conduct public testing of its Blade Battery during its rollout, enhancing its reputation. Furthermore, public attention has led to greater transparency in free cash flow management, avoiding overinvestment and waste of resources. Furthermore, BYD has achieved an overall improvement in its ESG performance by optimizing its workforce and continuously increasing R&D investment. Not only has it significantly reduced emissions in the environmental dimension, but it has also demonstrated outstanding performance in social and governance dimensions, thereby solidifying its leading position in China’s new energy vehicle industry.

A representative case from BYD.

Heterogeneity Analysis

Considering that both ER and corporate sustainability have broad definitions, and their relationship is complex, empirical results may exhibit heterogeneity. Thus, this section investigates the varying effects of ER on corporate sustainability from several perspectives.

Geographical Location of Enterprises

First, this research segments the sample enterprises into two categories according to their location: western China and central-eastern China, following the approach of C. Wang et al. (2024). The results are presented in Table 7. In the western region, neither type of ER shows a significant relationship with corporate sustainability. However, in the central and eastern regions, both FER and IER are found to promote corporate sustainability. This difference may be attributed to factors such as the sparse population, underdeveloped infrastructure, and weaker environmental awareness in the western district, which affects the execution of ER. The western region of China, heavily reliant on industries with lower environmental friendliness, such as mining and agriculture, often faces difficulties in balancing economic development with environmental protection. The sparse population and lack of infrastructure may prevent Western enterprises from cultivating environmental consciousness. Moreover, insufficient environmental awareness may cause these companies to focus on short-term profits at the expense of long-term sustainability. As a result, in enterprises in the western district, the positive effects of ER on sustainability are less significant, whereas the situation is the opposite in other regions. In contrast, the central and eastern regions typically implement policies more effectively, with both the government and civil society playing a more active role in urging firms to fulfill their environmental responsibilities.

Heterogeneity Test (1).

Notes. Standard errors are clustered at the firm level, with t-statistics presented in brackets. **represents a p-value less than .05, and ***signifies a p-value below .01. Y represents YES, N represents NO.

Ownership Type of Enterprises

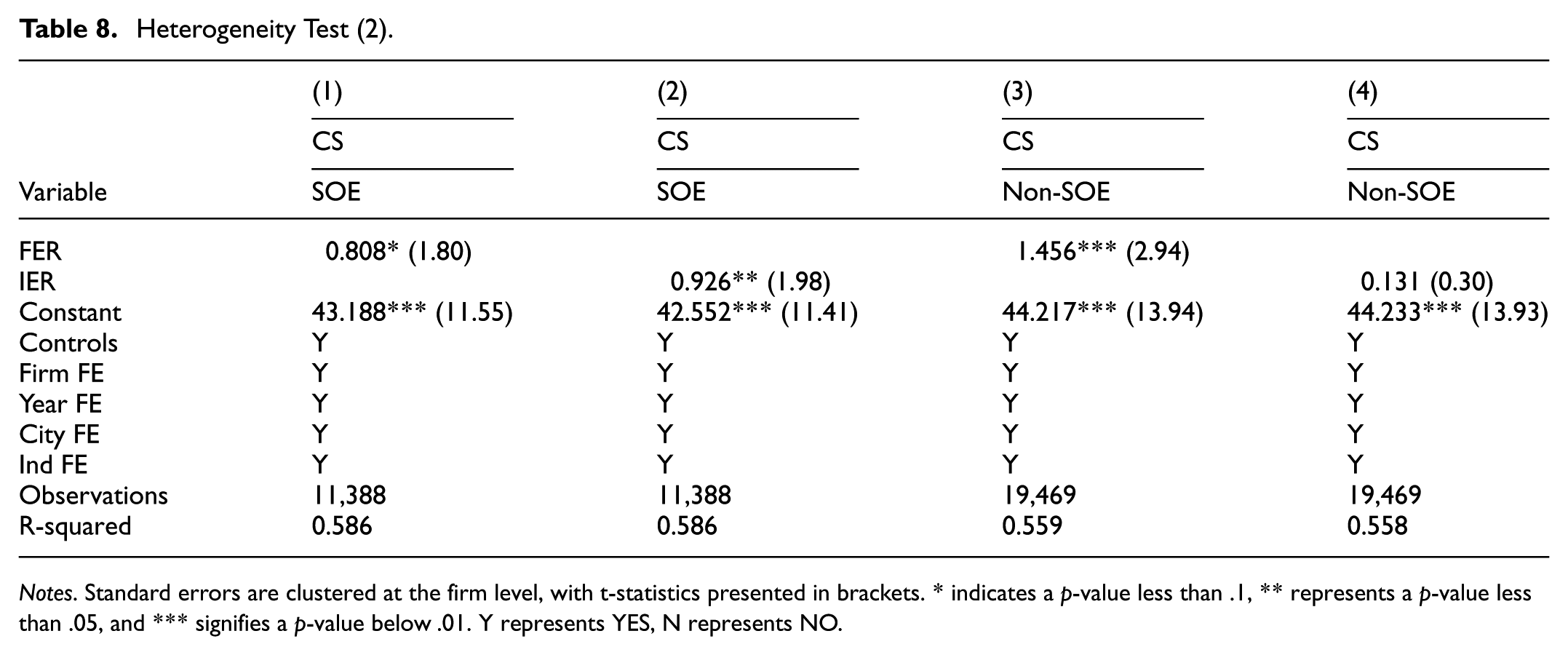

Next, the sample enterprises in this study are segmented into SOEs and N-SOEs. The results are presented in Table 8. In state-owned enterprises, both FER and IER significantly promote corporate sustainability. However, in N-SOEs, only FER is found to enhance corporate sustainability. One possible explanation is that IER, as public supervision, lacks enforceability, and N-SOEs often focus on profit maximization. Therefore, IER does not show a significant connection to corporate sustainability. In other words, compared to public supervision and non-compulsory social responsibility, such as environmental protection, N-SOEs are more likely to prioritize short-term profits (Boateng & Huang, 2017), and long-term sustainability is not their primary goal. However, N-SOEs tend to cooperate with mandatory FER. On the other hand, SOEs are often located in sectors such as energy and public utilities, where the government typically provides more support and conveniences, especially in terms of policy implementation and enforcement (Landoni, 2020). Therefore, both FER and IER have a favorable influence on corporate sustainability in SOEs.

Heterogeneity Test (2).

Notes. Standard errors are clustered at the firm level, with t-statistics presented in brackets. * indicates a p-value less than .1, ** represents a p-value less than .05, and *** signifies a p-value below .01. Y represents YES, N represents NO.

Industry Pollution Intensity

Additionally, this research adopts the methodology of Gao, Zhou, and Wan (2024) by segmenting the sample enterprises in high-pollution and low-pollution industries as per their industry pollution intensity. The detailed results are presented in Table 9. We find that, for firms in high-pollution industries, neither type of ER has a significant impact on corporate sustainability. However, for firms in low-pollution industries, both FER and IER significantly promote corporate sustainability. One possible explanation is that high-pollution enterprises are subject to stricter ER and greater social-environmental expectations (C. Wang et al., 2024), which may lead to mixed outcomes for these enterprises. In other words, some high-pollution enterprises might fail to fulfil the legal requirements or public expectations in time, resulting in poor ESG performance. Simultaneously, some high-pollution firms may resort to “greenwashing” or rent-seeking behaviors to evade regulation, thereby maintaining a positive corporate image. This leads to a distortion of ESG performance, making the impact of environmental regulations on corporate sustainability more complex. However, it is also possible that some high-pollution enterprises can meet social expectations, and like low-pollution enterprises, FER and IER positively strengthen their sustainability.

Heterogeneity Test (3).

Note. Standard errors are clustered at the firm level, with t-statistics presented in brackets. ** represents a p-value less than .05, and *** signifies a p-value below .01. Y represents YES, N represents NO.

Further Analysis

E/S/G Regression

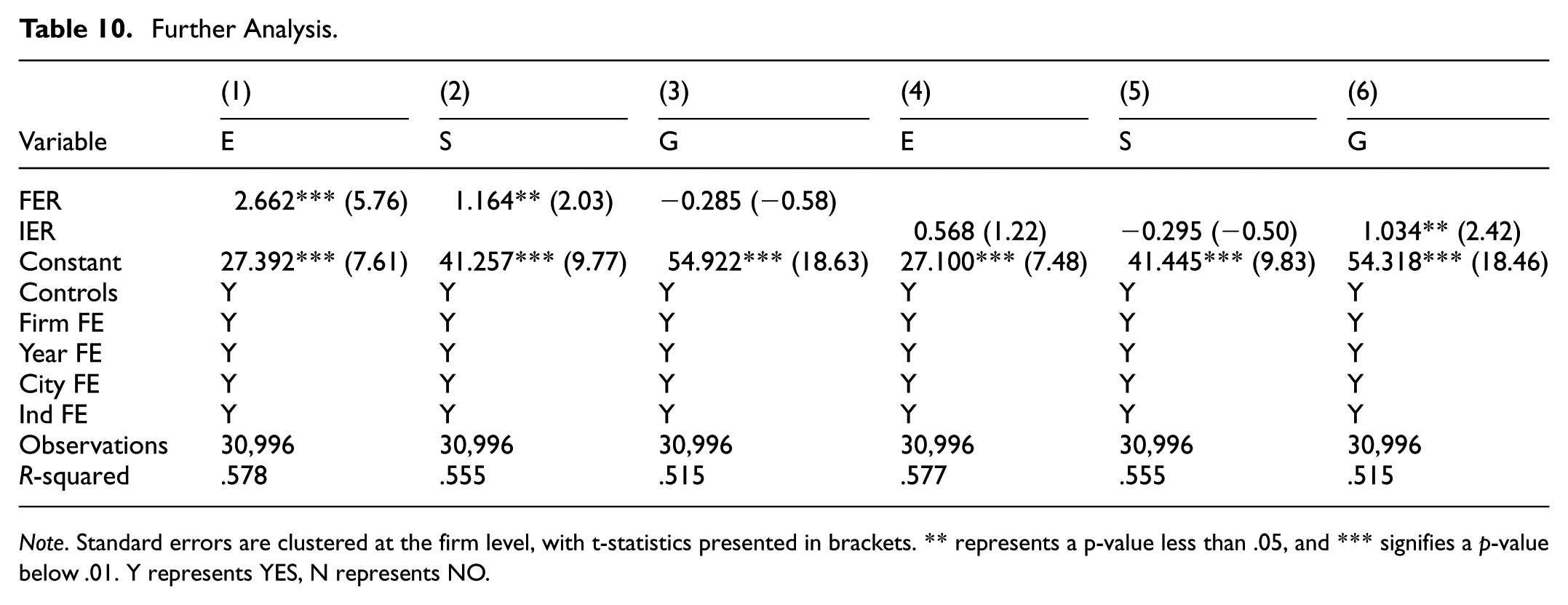

Existing corporate ESG performance typically includes three main pillars: environmental (E), social (S), and governance (G). Considering that the Huazheng Index not only measures the holistic ESG score but also provides detailed marks for E/S/G, the scores used in this study are derived from the Huazheng Index. Drawing on the practices of Han and Gao (2025), this section investigates the influence of ER on each of the ESG pillars from the perspectives of FER and IER, with the outcomes reported in Table 10. As illustrated in the first three columns of Table 10, FER has a positive influence on both E and S, but no significant relationship with G. These results suggest that FER encourages organizations to focus on environmental protection and social values, thus driving improvements in ESG performance and improving sustainable development. In contrast, the last three columns show that IER only has a positive impact on G, with no significant relationship to E and S. This suggests that IER is more focused on corporate governance processes and can effectively improve governance performance, thus promoting corporate sustainability.

Further Analysis.

Note. Standard errors are clustered at the firm level, with t-statistics presented in brackets. ** represents a p-value less than .05, and *** signifies a p-value below .01. Y represents YES, N represents NO.

The lack of a significant relationship between FER and the G pillar may stem from the limited effectiveness of top-down FER in regulating internal corporate management. In other words, FER primarily targets corporate production emissions and social responsibilities, with minimal intervention in internal management. Within the context of China’s high-quality social development, the government typically focuses more on corporate production quality, pollutant emissions, and societal impact, and formulates policies such as FER accordingly. As a result, internal corporate issues, such as managerial chaos, are not a key concern for the government or regulatory bodies when implementing FER. In contrast, bottom-up IER has a significant positive impact on corporate management performance. The rationale lies in the active involvement of the public in the corporate production process, where public interests are directly influenced by corporate executives. Consequently, public attention becomes an effective supervisory force on internal management. Therefore, IER, driven by public concern, significantly enhances corporate management performance. However, rational crowds usually prioritize their own interests, and the lack of enforceability in IER limits its impact on the E and S pillars of corporate sustainability.

Conclusion and Policy Recommendations

This research, as per data from Chinese A-share listed enterprises between 2011 and 2023, uses fixed-effects models to examine the influence of FER and IER on corporate sustainability. The findings demonstrate that both FER and IER significantly encourage corporate sustainability. This result is reliable, as it has been confirmed through a sequence of robustness verifications, ensuring the credibility of the positive impact of both types of ER on sustainability. Additionally, we find that FC masks the impact of both FER and IER, while FCF only masks the influence of IER. Corporate labor and R&D investment negatively moderate the influence of FER on sustainability but positively moderate the influence of IER. In the heterogeneity analysis, we discover that, in firms located in central and eastern regions, SOEs, and non-heavy-polluting industries, both FER and IER significantly promote sustainability. Further analysis reveals that FER enhances sustainability by improving environmental and social performance, while IER strengthens sustainability by improving governance performance.

Built on the study findings, this research offers several policy suggestions. First, the government should develop a differentiated ER to avoid a cookie-cutter solution, enhancing policy operability and local adaptability, while balancing environmental protection and economic growth. Specifically, in industrial regions such as Hebei, gradual policies combined with fiscal incentives can be implemented to encourage firms to meet regulatory standards. In contrast, more stringent regulations can be enforced in economically developed areas like Beijing and Shanghai. This differentiated approach to regulation helps strike a balance between environmental protection and economic growth.

Second, regional policy coordination and cooperation should be strengthened, with suitable environmental standards and increased support for areas with low compliance. Effective communication with businesses is essential to reduce excessive compliance costs. Firms in the western regions can obtain government subsidies for green projects, which help them gradually adapt to higher environmental standards, thereby improving overall compliance rates.

Third, companies should improve their social responsibility by integrating environmental protection strategies into their core competitiveness, actively complying with ERs, and establishing strong internal environmental management teams to enhance brand value and sustainability. Research shows that companies focusing on green innovation and workforce management not only enhance their brand value but also gain a competitive advantage in the market. For instance, companies like Huawei and Tesla have gained high levels of consumer trust by positioning sustainability as a core part of their brand. The government can incentivize firms that exceed environmental targets through policy rewards, thereby encouraging more companies to adopt environmental management systems.

Finally, environmental protection requires the participation of society. The government should strengthen public education to raise environmental awareness and encourage widespread involvement in climate governance. Companies can collaborate with environmental organizations to conduct regular training on ERs, improving employees’ environmental awareness and compliance capabilities. Specifically, public environmental awareness can be enhanced through school education, community activities, and corporate partnerships. At the same time, firms can collaborate with environmental organizations to provide regular environmental training for their employees, thereby improving their ability to comply with environmental regulations.

Footnotes

Appendix A

Acknowledgements

The authors confirm that there is no funding or external support to declare for this research.

Ethical Considerations

This article does not contain any studies with human or animal participants.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data are available from the corresponding author on request.*