Abstract

Corporate sustainability development has emerged as a significant concern globally. However, there is an inherent conflict between the corporate’s goals of maximization of profit and achievement of sustainable development. The increasing environmental responsibility offers a solution to reconcile this contradiction. Therefore, this paper aims to empirically investigate the influence of corporate environmental responsibility on corporate sustainable development and the mediator effect of corporate environmental strategy based on the nature of strategy that it can transform temporary and one-sided-focused activities into chronical and holistic actions. The study conducted two stages of data collection, gathering a total of 324 data sets from China in 2022, which were subsequently analyzed. The findings demonstrate that corporate environmental responsibility has a significant positive impact on corporate sustainable development, with corporate environmental strategy playing a crucial intermediary role. And this research offers theoretical contribution by extending literature on sustainable development and provides significant managerial implications.

Introduction

As external stakeholders, including consumers, communities, and governments, become more engaged in business operations, companies are increasingly focusing on benefits beyond mere economic gains (Battilana et al., 2022). Therefore, achieving sustainable development, which emphasizes the integration of long-term economic prosperity, social equity, and environmental circularity and friendliness into corporate practices and management (Bansal & Roth, 2000), has emerged as a significant concern for the corporates (Smith et al., 2022). However, plenty of research indicates that while many managers have recognized the importance of sustainable development over the past two decades, they often perceive it as a trade-off between economic revenue and other interests (Lashitew, 2021). As a result, both practitioners and academics seek approaches that can effectively promote sustainable development (Christ & Burritt, 2019; Mansell et al., 2020).

Corporate environmental responsibility which is inspired by the widely-accepted environmental awareness has the potential to serve as a breakthrough point for enhancing corporate sustainable development (Sharma & Henriques, 2005; Young & Tilley, 2006). Numerous scholars have suggested that corporate environmental responsibility can strengthen corporate focus on environmental protection and promote green innovation (Kraus et al., 2020; Yang & Gao, 2023). However, by retrieving the related literature, we find that there are chasms between corporate environmental responsibility and sustainable development as follows:

First, corporate environmental responsibility in more focus on improving the operations to decrease negative influence on environment (Tan & Zhu, 2022), just like the point proposed by Porter and van der Linde (1995) that most environmental issues stem from low production efficiency and the ineffective use of environmental resources. Therefore, they suggested that companies can enhance production efficiency through effective environmental management and strategic investments in cleaner production which can help the companies to achieve sustainable business success (Kramer & Porter, 2006). Actually, corporate sustainable development is a whole concept which integrates and balances the three dimensions of society, environment, and economy (Fischer et al., 2020), in this sense, it is not proper to directly link corporate social responsibility and sustainable development just like we believe in it intuitively.

Second, corporate environmental responsibility often emphasizes short-term benefits which entails the corporate can’t hold the responsibility chronically (Bansal & DesJardine, 2014). For example, some scholars argue that the investment on environment protection can lead to increased costs, reduced efficiency, and potentially negative economic performance (Ambec & Lanoie, 2008), meanwhile capital markets, especially immature ones in developing countries, pay more attention to short-term profits than long-term profits of enterprises, which leads to the reluctance of enterprises to make environmental investment (Sindhi & Kumar, 2012), therefore, environmental responsibility can’t be a permanent activities in corporate.

Third, most extant studies on the impacts of corporate environmental responsibility focus on its direct effects, which induce that there is a lack of research on the specific impact of corporate social responsibility on sustainable development (Madaleno et al., 2022), because it has been widely acknowledged the relationship between corporate environmental responsibility and its sustainable development requires the implementation of various action paths to improve corporate sustainability through corporate environmental responsibility instead of a direct influence (Aggarwal, 2013; Li; Cao et al., 2017).

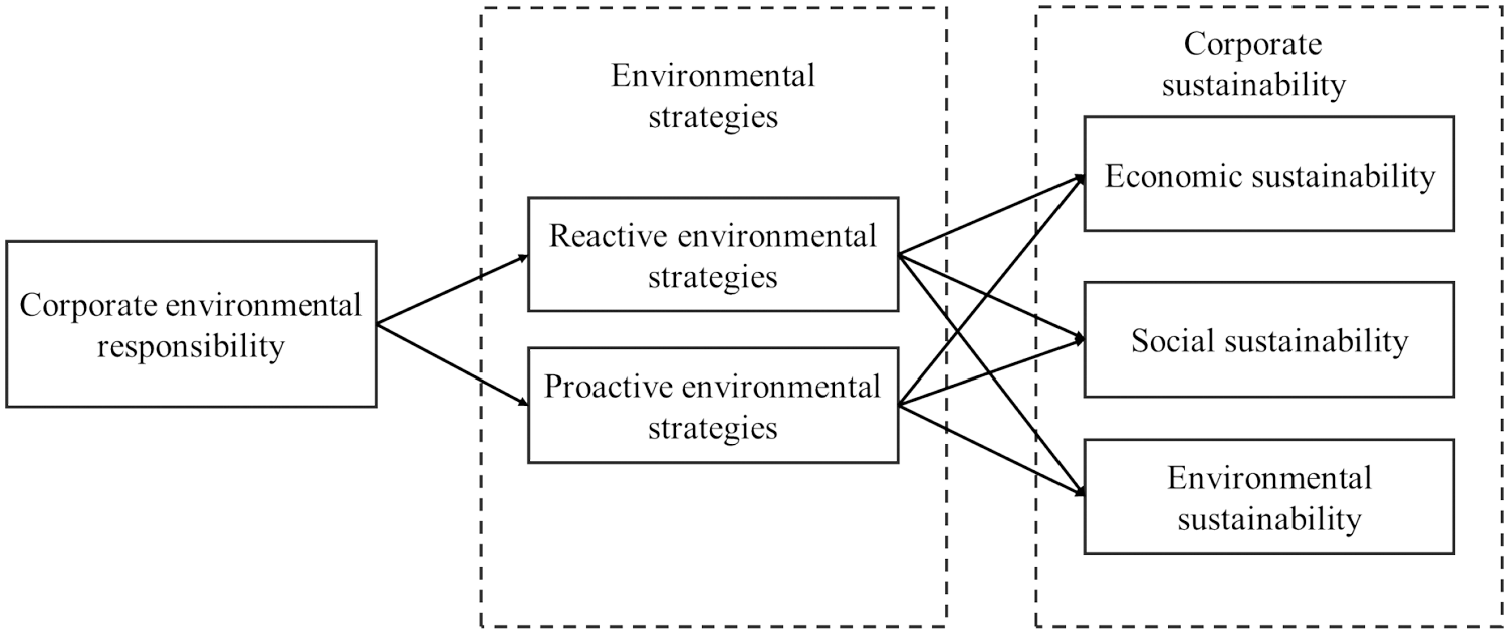

Therefore, there are great chams between corporate environmental responsibility sustainable development and whether the corporate environmental responsibility can boost its sustainable development is still up in the air, thus, we propound our research questions: Dose the corporate environmental responsibility boosts its sustainable development, and if so, how it works? Since strategy possesses with the essence of both comprehensiveness and long-term orientation (Lumpkin & Brigham, 2011),which has the feasibility to transform the partial and short-term corporate environmental responsibility into the comprehensive and long-term sustainable development (Zhou et al., 2024), thus our study considers the crucial role of corporate environmental strategy in achieving sustainable development. We construct a theoretical model of “corporate environmental responsibility-corporate environmental strategy-corporate sustainability” and test it empirically.

We conducted a two-stage survey to collect 324 questionnaires of representative samples and empirically test the hypothesis based on these datasets. The data analysis results show that corporate environmental responsibility can enhance corporate sustainability, and corporate environmental strategies plays the role of mediating variables between them. However, when analyzing the impact of corporate environmental responsibility on the dimensions of corporate sustainability, we discover that the impact of corporate environmental responsibility on social sustainability is not significant, while there is a significant positive impact on economic and environmental sustainability.

Our research provides a comprehensive analysis of the role of corporate environmental strategy in the relationship between corporate environmental responsibility and corporate sustainability. It demonstrates that companies, after taking on environmental responsibilities, can guide functional departments to engage in green innovation behaviors by making corporate environmental strategic decisions. These decisions ultimately lead to better sustainability outcomes. The article also examines the intermediary effects of the two dimensions of corporate environmental strategy separately and analyzes the feasibility of different implementation paths. This analysis offers companies new insights and ideas for achieving sustainable development.

The remaining parts of this article are organized as follows. Firstly, literature review is conducted to explore the concepts of corporate social responsibility, corporate sustainable development, and corporate environmental strategy. This helps identify the research gaps addressed in this article. Meanwhile, the hypotheses are developed. Then methodology is described. The data is then analyzed to empirically test the hypotheses. Finally, the study concludes by deliberating the theoretical contributions and practical implications.

Literature Review

Corporate Environmental Responsibility and Corporate Sustainability

Literature Review on Corporate Environmental Responsibility and Corporate Sustainability

Corporate environmental responsibility refers to a set of measures implemented by companies to minimize the harm they cause to the natural environment (Holtbrügge & Dögl, 2012). These measures focus on the company’s ecological activities aimed at preventing or mitigating negative environmental impacts (Shrivastava, 1995). Specifically, they include market mechanisms such as carbon emissions trading, market information disclosure, inventories of toxic substance emissions, and independent formulation of green energy-saving plans by companies (Chen et al., 2018). Early scholars primarily examined corporate environmental responsibility from the perspective of public goods and argued that it complements, rather than replaces, government interventions in environmental protection (Reinhardt & Stavins, 2010). However, Porter and van der Linde (1995) proposed that most environmental issues stem from low production efficiency and the ineffective use of environmental resources. They emphasized the important role of businesses in environmental governance and suggested that companies can enhance production efficiency through effective environmental management and strategic investments in cleaner production.

Corporate sustainability originating from the point that Bansal (2005) introduced the concept of sustainability into corporate research is defined as a three-dimensional framework that encompasses economic prosperity achieved through value creation, social equity achieved through corporate social responsibility, and environmental integrity through corporate environmental management. Therefore, integrating and balancing these three dimensions of social, environmental, and economic factors, while prioritizing long-term aspects of business activities, are fundamental aspects of sustainable development (Fischer et al., 2020). And recent studies on corporate sustainability have once again highlighted the significance of these three-dimensional characteristics (Hahn et al., 2014; Singh et al., 2022).

In detail, economic sustainability refers to the responsibility of enterprises to actively engage in managing competitive markets and positively influence their stakeholders at national and global levels (Chow & Chen, 2012). It is crucial for a business to achieve economic sustainability in order to ensure its survival (Hristov et al., 2019). Social sustainability refers to managing companies in a way that reduces social inequalities, improves quality of life, and strengthens relationships with various stakeholders (Chow & Chen, 2012). The aim of social sustainability is to positively influence all current and future relationships with stakeholders, ensuring their loyalty to the business (Le, 2023). Environmental sustainability refers to the efforts made by companies to manage their operations in a way that minimizes harm to the environment, including land, air, water, and more (Gupta, 1995). The key for enterprises to enhance environmental sustainability lies in conducting production and operational activities within the carrying capacity of the ecosystem (Qu et al., 2022). This involves reducing environmental pollution to the greatest extent possible, minimizing resource consumption, and minimizing the ecological footprint of the enterprise (Chow & Chen, 2012).

The literature review on these two concepts confirms the differences between them which is involved in introduction. Corporate environmental responsibility primarily focuses on the operational level, which encompasses the routine activities of a company. These operations typically exhibit two key characteristics: short-term and unilateral. The short-term nature implies that the company’s activities are continuously influenced by both internal and external factors. On the other hand, the unilateral aspect suggests that operations often prioritize cost reduction and efficiency enhancement, leading to a focus on minimizing environmental impact through cost-effective means. In contrast, sustainable development is characterized by a long-term and holistic approach. Consequently, there exist distinctions between these two concepts, with limited research exploring their direct interplay and lacking empirical evidence, which serves as research gap for our study.

Hypotheses Between Corporate Environmental Responsibility and Corporate Sustainability

In this part, we initially assume the relationship between corporate environmental responsibility and economic sustainability as follows: first, corporate environmental responsibility can enhance their reputations and competitive advantages, helping them achieve long-term economic returns and economic sustainability. Environmental responsibility can boost corporate reputation by appealing to consumers, enhancing legitimacy, and influencing environmental regulations (Walker et al., 2014). Additionally, it can drive environmental innovation within companies, leading to competitive advantages through various strategies such as product differentiation, pollution control, and technology advancements. These advantages can create entry barriers, open up new market opportunities, and improve overall market positioning (Guo et al., 2018). Research indicates that a positive market reputation and competitive edge can translate into sustained economic benefits, ensuring economic sustainability in the long run. And this finding is supported by research by Song et al. (2017) which suggests that while a company’s environmental management may not have an immediate effect on current performance, it can significantly enhance economic performance in the subsequent period. Clarkson et al. (2013) also argue that environmental information disclosure can boost corporate value. Building upon this, M.-C. Wang (2016) expands on these findings and proposes that both mandatory and voluntary environmental information disclosure can bring economic benefits to enterprises.

Second, corporate environmental responsibility drives companies to engage in green product innovation which includes various environmentally-friendly product development practices such as energy conservation, pollution prevention, by-product recycling, and non-toxic design. Green product innovation can enhance product durability and recyclability, minimizing raw material usage, and eliminating harmful substances (Kivimaa & Kautto, 2010), which are critical element for sustained performance growth (Y. Z. Wang & Ahmad, 2024). By focusing on green product innovation, companies can create high-quality, eco-friendly products that set them apart from competitors, allowing them to command premium prices and ultimately boost profitability (F. Zhang & Zhu, 2018). This approach involves redesigning products using non-toxic or biodegradable materials to reduce environmental impact and enhance energy efficiency (Lin et al., 2013). Investing in green product innovation helps companies open up new market opportunities and facilitates success with eco-friendly products. Thus, research suggests that green product innovation plays a pivotal role in fostering green competitiveness, enhancing corporate environmental image, and improving financial performance (Dangelico & Pujari, 2010). Based on the above analysis, this study proposes the following hypothesis:

H1a: Corporate environmental responsibility enhances corporate economic sustainability.

Then we postulate the relationship between corporate environmental responsibility and social sustainability as follows: the impact of corporate environmental responsibility on social sustainability can be understood through the lens of stakeholders. Enterprises are inherently influenced by the demands of diverse stakeholders who grant a “social license” for a business to function, playing a crucial role in shaping a company’s decisions regarding different practices (Parsons et al., 2014), thus the corporates should address these needs through their operations. Freeman and Reed highlighted the significant pressure companies face from various stakeholders to prioritize their interests, potentially driving companies to develop specific capabilities to effectively manage and enhance their competitive position across economic, social, and environmental dimensions (Freeman & Reed, 1983; Zhao et al., 2023). As a result, companies should strive to comprehend their stakeholders, engage with them, and align the company’s actions with stakeholder interests (Salem et al., 2016).

In our research context, social sustainability is achieved when an enterprise evaluates various stakeholders, including employees, local communities, and shareholders, in the areas of environment, society, and governance. These stakeholders are becoming increasingly concerned about social issues related to products, manufacturing processes, packaging, and distribution. This necessitates companies to prioritize environmental and social considerations as crucial aspects of their management practices (Anser et al., 2020). Corporate environmental responsibility will be influenced by stakeholders’ demands to reduce waste and emissions, enhance resource efficiency and productivity, and minimize the environmental impact of operations, products, and facilities (Nejati et al., 2014). Practices that harm natural resources will be discouraged. Furthermore, stakeholders will expect integrity, respect, standards, transparency, and accountability in corporate social responsibility, particularly in corporate environmental responsibility (Pucheta-Martínez & Gallego-álvarez, 2019). Due to pressure from various stakeholder groups, organizations will place greater emphasis on accountability and transparency regarding a wide range of corporate behavior issues (Kolk, 2008). Based on the above analysis, this study proposes the following hypothesis:

H1b: Corporate environmental responsibility enhances corporate social sustainability.

We finally speculate the relationship between corporate environmental responsibility and environmental sustainability as follows: first, participation in activities related to corporate environmental responsibility is considered as a necessary obligation in the current ecological environment and is often seen as a key motivator for managers to promote environmental protection (Jiang et al., 2018). The level of a company’s commitment to environmental responsibility directly influences its involvement in community environmental well-being and its impact on the natural environment (Ahmed et al., 2020). Therefore, managers are increasingly prioritizing their responsibilities toward the environment issues, and handle these issues serve as the main drivers for enhance the quality of the environment (Hart & Ahuja, 1996). Specifically, environmentally responsible behaviors by enterprises involve reducing pollution and waste, which contribute to improving community well-being and play a crucial role in enhancing and safeguarding the natural environment (Khan et al., 2021). The extent of participation in activities related to corporate environmental responsibility directly correlates with the social sustainability of the company.

Second, similar to economic sustainability, green product innovation can also contribute to enhancing environmental sustainability. Green process innovation involves making changes to production processes to focus on energy conservation, pollution prevention, waste recycling, and the use of non-toxic processes. This innovative approach helps companies reduce the negative impact of their production activities on the environment (F. Zhang & Zhu, 2018). The primary objective of green process innovation is to decrease energy consumption during production or repurpose waste into valuable products (Y. Z. Wang & Ahmad, 2024). Implementing green process innovation entails modifying manufacturing processes and systems, such as reducing harmful emissions and waste, recycling and reusing materials, cutting down water and energy usage, improving resource efficiency, and transitioning from fossil fuels to bioenergy (Kivimaa & Kautto, 2010). Through environmental management practices driven by green innovation, companies can make significant strides in improving the environment (Wagner, 2010), ultimately leading to sustainable environmental development. Based on the above analysis, this study proposes the following hypothesis:

H1c: Corporate environmental responsibility enhances corporate environmental sustainability.

Overall, Kramer and Porter (2006) and Mansell et al. (2020) highlighted the need for enterprises to connect with society and create economic value by addressing societal needs and challenges in order to achieve sustainable business success. Therefore, as the government, community, and public demand for various responsibilities of enterprises continues to increase, enterprises need to disclose various information to the public. according to the research by Rahman and Post (2012), companies that undertake corporate environmental responsibility will disclose information on governance mechanisms, environmental protection, social responsibility, and other aspects to the outside world. In order to ensure that this information meets the requirements of stakeholders, it is necessary to enhance the sustainability of the enterprise in all aspects. In detail, from an individual standpoint, the information disclosure should include environmental information on waste disposal, as well as valuable data on wastewater and emissions (Kasych et al., 2020). From a product perspective, corporate environmental responsibility involves the development of green products and the reduction of environmental impact caused by existing products. From a business policy viewpoint, companies need to establish new shared values, incorporate the “triple bottom line” (people, planet, and profit) into their corporate strategies, and emphasize their significance for corporate development (Naidoo & Gasparatos, 2018). In terms of corporate performance, corporate environmental responsibility demonstrates a company’s commitment to integrating environmental awareness into its operations, thereby enabling it to minimize its environmental footprint and achieve sustainable development (Govindan et al., 2020). Based on the above analysis, this study proposes the following hypothesis:

H1: Corporate environmental responsibility enhances corporate sustainability.

Mediator Effect of Corporate Environmental Strategy

Corporate Environmental Strategy

Generally speaking, strategy is the comprehensive plans of a company for a long period of time in the future (Cummings & Daellenbach, 2009), and it has the functions that transform short-term behaviors into the blueprints that enterprises adhere to in the long term (Reeves & Haanaes, 2015). As we pointed out earlier, environmental responsibility is short-term, one-sided, while sustainable development is long-term and holistic. In our research context, corporate environmental strategy transforms short-term and one-sided environmental responsibility into sustainable development in the growth period, Therefore, it is reasonable for us to use corporate environmental strategy as an intermediary between these two variables.

In detail, environmental strategy, the selection of environmentally friendly practices and activities (Holt & Ghobadian, 2009; Neumann, 2017), be seen as the company’s choices and commitments or decisions (Mazzolini, 1981), which are influenced by managers’ perceptions of environmental risks and opportunities, organizational capabilities, and availability of slack resources (Barney et al., 2010). In the context of environmental management, companies need to consider various decision-making areas such as products, processes, organizations and systems, supply chains and recycling, as well as external relationships (Menguc et al., 2010). A company’s environmental strategy is influenced by the specific environmental management fields it operates in and the resources invested in these fields. These choices result in different types of environmental strategies (Bobby Banerjee, 2001).

Environmental strategies can be categorized as either reactive or proactive, depending on the main drivers of corporate actions and environmental behavior in competitive situations (Bresciani & Oliveira, 2007). Reactive environmental strategy involves incorporating environmental issues into the strategic system to mitigate negative impacts (Piwowar-Sulej, 2022). Companies adopting this strategy aim to maintain a neutral stance toward environmental changes while responding to environmental regulations, stakeholder pressures, and market demands (Dzhengiz & Niesten, 2020; Papagiannakis et al., 2014). On the other hand, proactive environmental strategies view environmental management practices as opportunities for positive development and aim to gain a competitive advantage by integrating them into the overall business strategy (Abbas & Sağsan, 2019; Lucas, 2010). Firms following a proactive approach strive to anticipate market and environmental trends, introduce new products, and adopt innovative production technologies (Sharma, 2000). These two types of environmental strategies have different focuses, so we will also examine the mediating role of these two types of environmental strategies separately.

Hypotheses of Mediator Effect of Corporate Environmental Strategy

Corporate environmental strategy can be considered as a favorable approach to manage and control external environmental risks (Anderson, 2002). It emphasizes the importance of improving corporate environmental legitimacy, providing expertise and advice, formulating relevant secondary strategies, facilitating resource acquisition, and establishing strong external relationships with various stakeholders (Helfaya & Moussa, 2017). Hart (1995) argues that an enterprise’s internal resources and capabilities are rare, valuable, unique, and irreplaceable. These resources and capabilities can lead to a sustainable competitive advantage for the enterprise. Hart also emphasizes the importance of corporate environmental strategy in improving sustainability. He categorizes corporate environmental strategies into three functions: pollution prevention, product management, and sustainable development. Pollution prevention aims to prevent waste emissions during the production process rather than cleaning up after pollution is generated. This function is associated with lower product and service costs (Yu & Chen, 2014). Product management extends pollution prevention strategies throughout the product life cycle, considering the needs of all business stakeholders (Sangle, 2005).

Additionally, preventing the negative impacts of environmental issues can enhance corporate sustainability. Sustainable development, focusing on maintaining an environmentally friendly production process in the uncertain future, is the most crucial component of corporate environmental strategy. This approach considers the impact of corporate environmental strategic decisions on economic, social, and environmental sustainability (Wijethilake, 2017). Therefore, corporate environmental strategy can help companies gain a solid competitive position in the long term and improve overall sustainability. Based on the above analysis, this study proposes the following hypothesis:

H2: Corporate environmental strategy plays a mediating role between corporate environmental responsibility and corporate sustainability.

A reactive environmental strategy primarily focuses on complying with environmental regulations and implementing end-of-pipe remediation. Firms that adopt this strategy often resort to defensive lobbying as a response to changes in environmental regulations and stakeholder pressure (Aragón-Correa & Sharma, 2003). Companies employing reactive environmental strategies tend to have limited environmental responsiveness in decision-making areas and primarily prioritize pollution control and regulatory compliance (Banerjee, 2001). Companies with higher pollution levels typically concentrate their efforts on specific decision-making areas and allocate significant resources to improve their environmental strategies in those areas (Orazalin, 2020).

Some companies, under the pressure of environmental risks and the needs of stakeholders, may adopt a passive approach and view their environmental behavior solely as a response to environmental regulations (Murillo-Luna et al., 2008). However, the needs of stakeholders are becoming increasingly diverse and the requirements for environmental and social aspects are also becoming stricter (Reed, 2008). For example, the government has formulated stricter carbon emission policies, and companies must comply with relevant carbon emission indicators before they can produce (Y.-J. Zhang et al., 2015). Various laws and regulations prohibiting employment discrimination have also been formulated, and companies must consider relevant regulations when recruiting (Rosales et al., 2023). In such cases, enterprises only passively respond to stakeholder needs, integrating these needs into environmental strategies can achieve sustainable development of the environment and society (Vo et al., 2023). In other words, instead of taking proactive measures to prevent pollution, these firms prefer to invest in pollution control technologies that do not require major changes to their production processes or cause significant disruptions (Pinkse et al., 2023). It is important to note that implementing a reactive environmental strategy does not imply neglecting environmental responsibilities or taking no action to address environmental issues. Rather, it signifies that companies choose a relatively low-risk and manageable approach to environmental protection (Amores-Salvadó et al., 2021). A reactive environmental strategy is one of the ways in which corporate environmental responsibility is practiced within a company to meet the needs on the sustainability of external stakeholders (Sharma & Vredenburg, 1998). It also contributes to the three dimensions of corporate sustainability: economic sustainability, social sustainability, and environmental sustainability, by serving as a mediator between them.

Based on the above analysis, this study proposes the following hypotheses:

H2a1: Reactive environmental strategies play a mediating role between corporate environmental responsibility and economic sustainability.

H2a2: Reactive environmental strategies play a mediating role between corporate environmental responsibility and social sustainability.

H2a3: Reactive environmental strategies play a mediating role between corporate environmental responsibility and environmental sustainability.

The core of a proactive environmental strategy involves redesigning and changing products and processes to proactively prevent negative impacts on the environment. The purpose of this strategy is to take all necessary actions to avoid potential pollution of the ecological environment (Aragón-Correa & Sharma, 2003). Sharma (2000) defines a proactive environmental strategy as a unique business model where a company autonomously takes actions to reduce environmental impact during production and operations, going beyond mere compliance with regulations or standard practices. Companies implementing proactive environmental strategies must invest in and adopt new technologies and develop new organizational capabilities to effectively implement the strategy and ultimately gain a competitive advantage (Sharma & Vredenburg, 1998).

By reducing waste and cost, improving product and process quality, and leveraging unique capabilities, companies implementing proactive environmental strategies are more likely to gain advantages in sustainability (Sharma & Vredenburg, 1998). Such strategies enable enterprises to reduce their ecological footprint and prevent damage to the surrounding environment’s land, air, and water resources (Bansal, 2005). A proactive environmental strategy involves a proactive approach in innovating environmental technology, producing cleaner products, using clean energy, and minimizing negative environmental impact, leading to improved sustainability performance (Steurer et al., 2005). Moreover, this strategic model not only contributes to economic sustainability by creating and distributing goods and services but also enhances social sustainability by ensuring equal resources and opportunities, improving the social value of enterprises, and establishing a green image or good reputation.

Based on the above analysis, this study proposes the following hypotheses:

H2b1: Proactive environmental strategies play a mediating role between corporate environmental responsibility and economic sustainability.

H2b2: Proactive environmental strategies play a mediating role between corporate environmental responsibility and social sustainability.

H2b3: Proactive environmental strategies play a mediating role between corporate environmental responsibility and environmental sustainability.

According to analysis above, we build our research model and present it in Figure 1.

The research model.

Methodology

We utilized a questionnaire survey to collect data. To ensure the survey method’s credibility, all scales employed in the study were derived from established literature, and the scale items were tested considering the Chinese organizational situation and context. Necessary adjustments were made, and the reliability and validity tests confirmed that the modified questionnaire adhered to statistical standards. The study measured all scales on a 7-point Likert scale, where “1” represented “completely disagree” and “7” represented “completely agree.”

Data Collection

The investigation topic of this study focuses on examining the impact of corporate environmental responsibility on corporate sustainability. The theoretical framework encompasses variables including corporate environmental responsibility, corporate environmental strategy, and corporate sustainability. These variables are considered at the corporate macro-decision-making level. To obtain in-depth and accurate information within a company, it is necessary to involve more middle and senior managers in the survey. Unlike ordinary employees, these managers possess a better understanding of the company’s environmental decisions, encountered challenges, and future development directions. They also possess deeper insights into corporate environmental governance at the macro level. Therefore, this study has chosen middle and senior managers of enterprises, as well as ESG professionals within the enterprise, as the research subjects.

This study collected data from an association of consulting firms in an eastern province of China. Although the association is based in a single province, the consulting firms have clients nationwide, making the data representative and random. To ensure data quality, a two-stage data collection method was employed. The first wave of data collection took place in June 2021, focusing on gathering the data of corporate environmental responsibility. The second wave of data collection occurred in May 2022, specifically targeting corporate environmental strategies and corporate sustainability. In the first wave, 1,147 questionnaires were sent out, and 887 valid questionnaires were received. For the second wave, a total of 324 valid questionnaires were recovered, which will be used for subsequent data analysis and hypothesis testing. The implementation of a two-stage data collection approach helps mitigate the potential impact of common method bias.

Measurement

Corporate Environmental Responsibility

Based upon previous research conducted by He and Chen (2009), Chuang and Huang (2018), and Chen et al. (2018), this study utilizes 12 measurement items to conduct a survey on corporate environmental responsibility.

Corporate Environmental Strategy

In this study, the selection of measurement items for corporate environmental strategy is primarily based on the research conducted by Aragón-Correa and Sharma (2003), Sharma and Vredenburg (1998), Buysse and Verbeke (2003), and Garcés-Ayerbe et al. (2016).

Corporate Sustainability

This study synthesized the scale items from Chow and Chen (2012) and Antolín-López et al. (2016), considering the unique circumstances of Chinese organizations. The researchers also consulted with experts and scholars in the field of corporate social responsibility and sustainable development to develop a measurement scale for corporate sustainability. The final scale consisted of 18 items.

Control Variables

To analyze the impact of corporate environmental responsibility on corporate sustainability, it is important to consider various corporate characteristics that can influence corporate environmental behavior. These characteristics include corporate location, industry, type, and scale (Chen et al., 2018; Chow & Chen, 2012; Chuang & Huang, 2018). In our study, we selected industrial types, enterprise ownership, enterprise size, and enterprise establishment time (age) as control variables. We categorized enterprise types into state-owned enterprises, foreign-funded enterprises, joint ventures, and private enterprises. Additionally, we measured enterprise size based on the number of persons in the enterprise. And the industrial types can be seen in our descriptive analysis in Table 1.

Descriptive Analysis of Sample.

All the items of the variables can be seen in Table 2.

Results of Reliability Analysis.

Descriptive Analysis of Sample

Table 1 presents the distribution of sample companies based on ownership, company size (measured by the number of employees), years of establishment, and industry types. Descriptive statistical analysis reveals that the characteristics of the sample enterprises generally follow a normal distribution, suggesting a certain level of representativeness. This study evaluates nonresponse bias by comparing mean differences on key variables between data from the first and second halves of the recall. The results of the independent sample T-test indicate that there are significant differences in corporate environmental responsibility (p = .691), proactive corporate environmental strategy (p = .778), reactive corporate environmental strategy (p = .567), and economic sustainability (p = .199). However, there are no significant differences in social sustainability (p = .756) and environmental sustainability (p = .761), indicating that non-response bias is not a serious concern.

Data Analysis

Reliability and Validity Analysis

This study utilizes Cronbach’s α and the CITC (Corrected Item-Total Correlation) of each measurement item as indicators to assess the reliability of the scale. The Cronbach’s α of the total questionnaire is .878, while the Cronbach’s α of corporate environmental responsibility, corporate environmental strategy, and corporate sustainability are .963, .951, and .957, respectively, all surpassing .8. These values are presented in Table 2. The table reveals that the Cronbach’s α coefficient of each variable exceeds .8, and the CITC value of each item for every variable is above 0.5. Additionally, removing any item does not improve the value of Cronbach’s α. Consequently, it can be inferred that the final scale employed in this study exhibits good internal consistency and reliability, demonstrating high reliability and suitability for further research.

In order to ensure the validity of the data, this study examines four aspects: content validity, construct validity, convergent validity, and discriminant validity. The scales used in this study are mature scales quoted from foreign literature. These scales were double-blindly translated and collated with domestic experts, scholars in related fields, and several doctoral students. The scale items were discussed and revised by the team based on the conclusions of the discussion. To ensure the suitability of the scale in the Chinese context, scales that did not fit the Chinese organizational context were screened, and only items suitable for the Chinese context were retained. Therefore, the scale used in this study can be considered to have good content validity.

This study assessed the structural validity of the scale using four indicators: KMO (Kaiser-Meyer-Olkin), Bartlett’s test of sphericity, approximate chi-square, minimum factor loading, and cumulative variance contribution rate. The measurement results are presented in Table 3. The KMO values for all variables exceed 0.700, surpassing the standard threshold. The Sig. values are all .000, indicating high significance. Additionally, the smallest factor loading after extracting the common factors is 0.781, which is greater than 0.700. The lowest cumulative variance contribution rate is 65.33%. Based on these findings, it can be concluded that the scale demonstrates good structural validity.

Results of Structural Validity.

In addition, this study also utilized confirmatory factor analysis to assess the structural validity of the scale. The fitting indicators χ2, df, RMSEA, NFI, IFI, TLI, and CFI were employed to evaluate the model’s fitting effect. The results indicated that the three-factor model exhibited optimal goodness of fit, with a χ2/df ratio of 2.677, RMSEA of 0.082, CFI of 0.941, TLI of 0.869, IFI of 0.913, and NFI of 0.901.

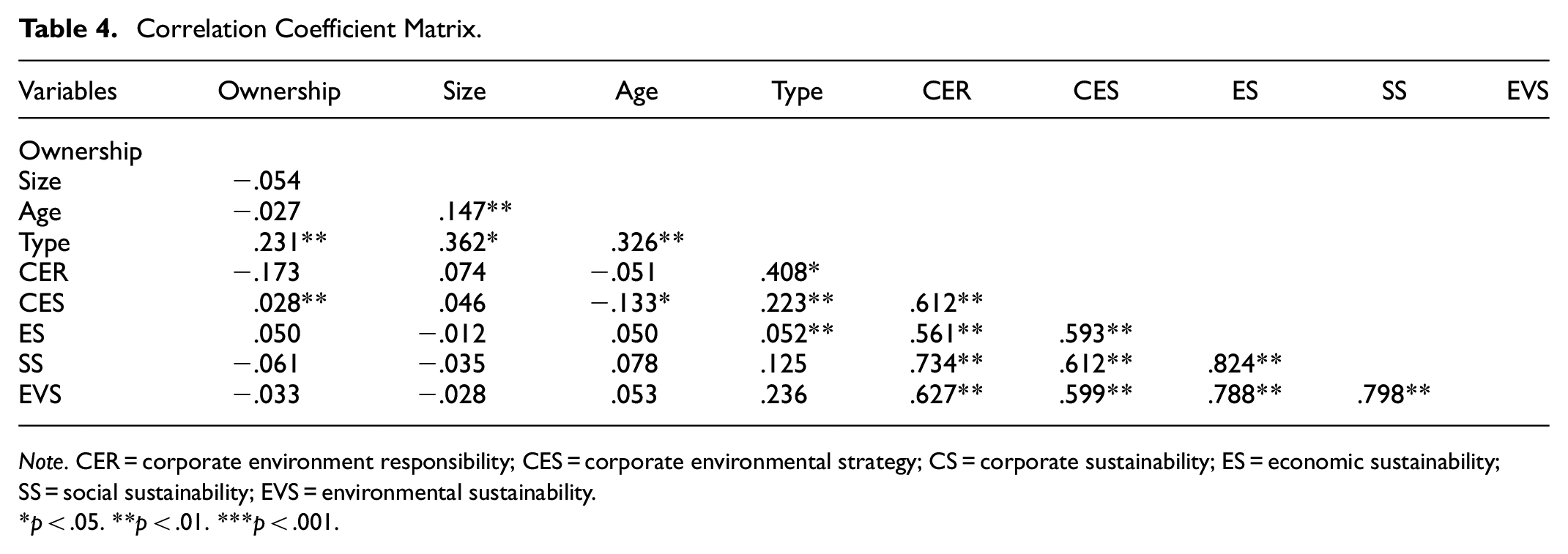

This study analyzed the correlation coefficient between variables and measured the correlation between any two variables and their dimensions. The results are presented in Table 4. The table reveals that, with the exception of the correlations between the control variables and between each variable and the control variables (which are mostly insignificant), the correlations between other variables are significant. This suggests that further hypothesis testing can be conducted.

Correlation Coefficient Matrix.

Note. CER = corporate environment responsibility; CES = corporate environmental strategy; CS = corporate sustainability; ES = economic sustainability; SS = social sustainability; EVS = environmental sustainability.

p < .05. **p < .01. ***p < .001.

To minimize the common method bias problem caused by respondents’ self-evaluation, this study employed Harman’s single factor test. The results of the test indicated that the first common factor, without rotation, accounted for only 26.4% of the variance explanation, which is below the threshold of 30%. Therefore, it can be concluded that there is no significant common method bias present. Furthermore, during the confirmatory factor analysis, the goodness of fit for the single-factor model was found to be significantly worse compared to the five-factor model. This suggests that the data used in this study does not exhibit any noticeable common method deviation.

Hypothesis Test

Main Effect Test

This study utilizes a linear regression model with SPSS 29.0 to investigate the influence of corporate environment and responsibility on corporate sustainability. The results of the main effect test are presented in Table 5. According to the findings in the table, corporate environmental responsibility has a significant positive impact on corporate sustainability (β = .141, p < .01), confirming the research hypothesis H1. Moreover, corporate environmental responsibility also has a positive impact on economic sustainability (β = .122, p < .01), supporting the research hypothesis H1a. However, there is no significant impact of corporate environmental responsibility on social sustainability (β = .136, p > .05), failing to verify the research hypothesis H1b. On the other hand, corporate environmental responsibility has a significant impact on environmental sustainability (β = .171, p < .001), confirming the research hypothesis H1c.

Results of Main Effect Test.

p < .05. **p < .01. ***p < .001.

According to Table 5, the impact of corporate environmental responsibility on social sustainability is not significant. And we speculate that the possible reasons are as follows: (1) Corporate environmental responsibility primarily addresses environmental issues, while social sustainability focuses on fairness and justice, which causes a significant distinction between the two. Therefore, it might be hardly to achieve social sustainability through taking environmental responsibility. (2) Within the organizational landscape of China, many companies and managers may not view economic, social, and environmental sustainability as interconnected dimensions. Instead, they perceive these aspects as distinct systems with minimal overlap. Consequently, when companies prioritize environmental governance, the impact is predominantly seen at the economic and environmental levels, rather than the social level. As a result, Chinese manufacturing companies are likely to enhance social sustainability through avenues like social donations and welfare programs, without integrating social responsibility attributes with environmental concerns or the core business model.

Mediator Effect Test

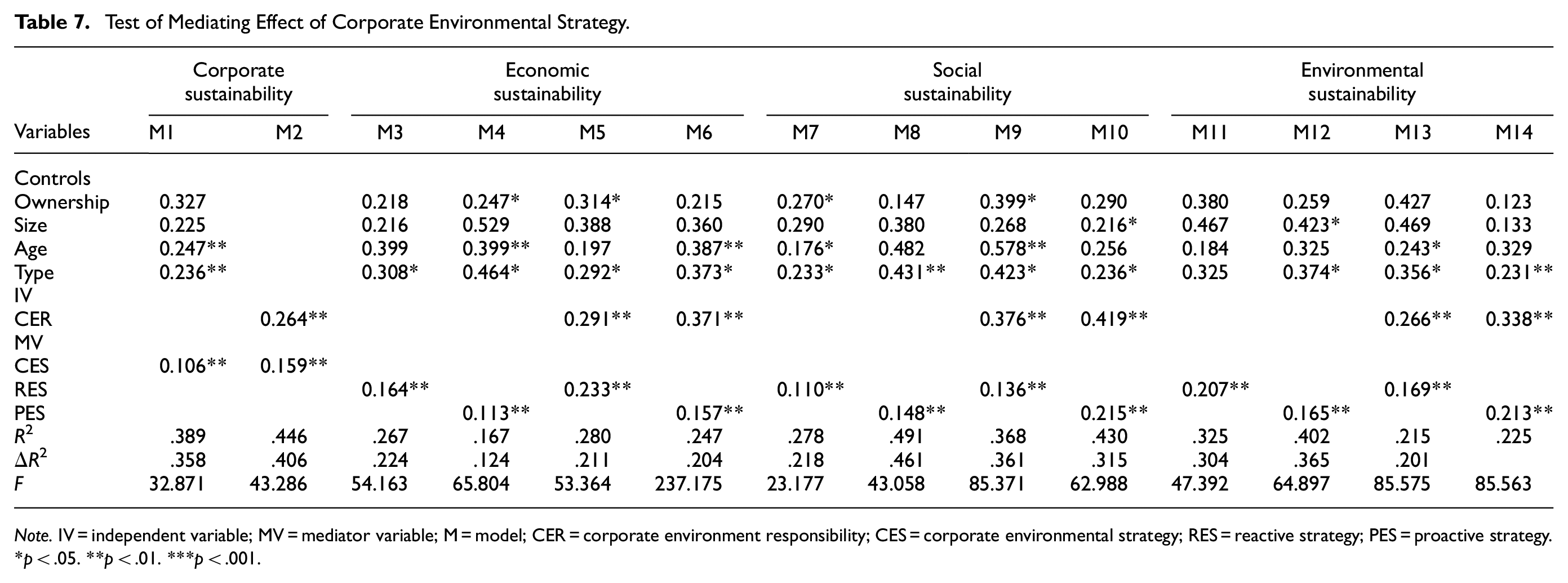

We utilized SPSS 29.0 to conduct stepwise regression analysis to examine the mediating effects of corporate environmental strategy between corporate environmental responsibility and corporate sustainability, and the statistical findings are presented in Table 6. In the stepwise regression approach, the criteria for assessing the presence of a mediating effect include significant impacts of the independent variables on the dependent variable, the independent variable on the mediating variable, and the mediating variable on the dependent variable. If all three criteria are met, the mediating effect is considered to exist (Taylor, 1997).

Results of the Impact of Corporate Environmental Responsibility on Corporate Environmental Strategy.

p < .05. **p < .01. ***p < .001.

Therefore, we first investigated the impacts of corporate environmental responsibility on the corporate environmental strategy and its two dimensions, namely reactive environmental strategy and proactive environmental strategy. The samples were divided into groups based on these standards: the top 50% of samples were classified as proactive environmental strategies, while the bottom 50% were classified as reactive environmental strategies. The last two columns of Table 6 present the test results that corporate environmental responsibility has a positive impact on reactive environmental strategy (β = .286, p < .01), and it also has a significant positive effect on proactive environmental strategy (β = .177, p < .01).

Subsequently, according to the criteria for testing of mediating effects, variables were gradually added to the regression equation and the results are presented in Table 7. The first column of Table 6 indicates that corporate environmental responsibility has a significant influence on corporate environmental strategy (regression coefficient of 0.123, significance level < .01). And M1 in Table 7 demonstrates that corporate environmental strategy significantly affects corporate sustainability (regression coefficient of 0.106, significance level < .01). In M2, corporate environmental responsibility and corporate environmental strategy are simultaneously included in the regression equation. While the regression coefficients between corporate environmental responsibility, corporate environmental strategies and corporate sustainability show slight changes, the significance level remains <.01. This aligns with the standard for the presence of mediating effects in stepwise regression. Thus, the corporate environmental strategy acts as an intermediary in the relationship between corporate social responsibility and corporate sustainable development, thus H2 is supported.

Test of Mediating Effect of Corporate Environmental Strategy.

Note. IV = independent variable; MV = mediator variable; M = model; CER = corporate environment responsibility; CES = corporate environmental strategy; RES = reactive strategy; PES = proactive strategy.

p < .05. **p < .01. ***p < .001.

Similarly, in Table 6 the second column indicates that the regression coefficient of corporate environmental responsibility on responsive environmental strategy is 0.286, with a significance level <.01. M3 in Table 7 reveals that the regression coefficient of reactive strategy on corporate economic sustainability is 0.164, with a significance level <.01. When corporate environmental responsibility and reactive environmental strategy are simultaneously included in the analysis (M5), the regression coefficient between the two and corporate sustainability experiences a slight change, but the significance level remains <.01, indicating that responsive environmental strategy plays a crucial role in corporate environmental responsibility and economic sustainability. Thus H2a1. According to the same standard, it can be seen that H2a2, H2a3, H2b1, H2b2, and H2b3 are all supported.

After conducting stepwise regression to examine the mediating role of corporate environmental strategy, this study utilized the Bootstrapping method with 5,000 samples to create a 95% confidence interval for further validation. The results, displayed in Table 8, reveal that the confidence intervals for the mediating effects of reactive and proactive environmental strategies between corporate environmental responsibility and economic sustainability, social sustainability, and environmental sustainability do not encompass 0, indicating a significant mediating effect. Moreover, even with the inclusion of mediating variables, the regression coefficients between the independent variable of corporate environmental responsibility and the three sustainability dimensions remain significant, suggesting that all mediating variables contribute to a partial mediating effect. Consequently, Hypotheses H2, H2a1, H2a2, H2a3, H2b1, H2b2, and H2b3 are reaffirmed.

Analysis of the Mediating Effect.

Note. CER = corporate environment responsibility; CES = corporate environmental strategy; RES = reactive strategy; PES = proactive strategy; CS = corporate sustainability; ES = Economic sustainability; SS = social sustainability; EVS = Environmental sustainability.

Furthermore, the mediator effects were compared between reactive strategies and proactive environmental strategies to assess their influence (Table 9). Results indicate that when the dependent variable is economic sustainability, the mediating effect of reactive environmental strategy surpasses that of proactive environmental strategy. Similarly, for social sustainability and environmental sustainability, the mediating effect of reactive environmental strategy is found to be stronger than that of proactive environmental strategy. This suggests that reactive environmental strategies are more effective in reducing costs and generating green income in the long term, thereby significantly improving economic performance of enterprises. On the other hand, proactive environmental strategies are crucial for the future development of enterprises in terms of social and environmental impact.

Divergence Test of the Mediator Effect of Corporate Environmental Strategy.

p < .05. **p < .01. ***p < .001.

Robustness Test

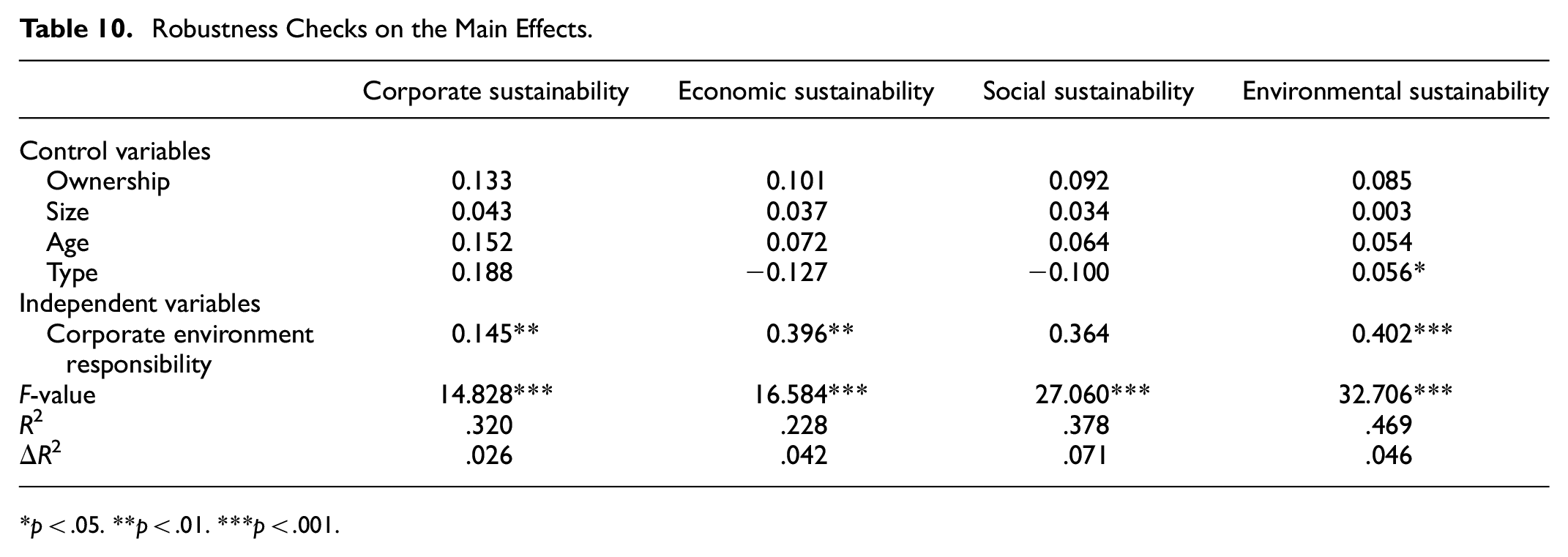

To ensure the generality of our research findings, we conducted a robustness test by replacing the samples. After the deadline for the second wave of data collection in May 2022, we received 129 samples. As not all 129 samples provided sufficient data for analysis, we randomly chose 100 questionnaires from the 324 samples collected before the deadline to create a new sample set comprising 229 samples. Regression analysis was then performed on this new sample set, revealing that while there were slight variations in coefficient values, the significance level of the independent variable’s impact on the dependent variable were unchanged, which means that the results are consistent in these two tests.

Similarly, we conducted additional tests to re-examine the mediating effect of corporate environmental strategy. The statistical analysis revealed that while there were slight variations in the coefficient values, the direction of the coefficient, indicating how the independent variable influences the dependent variable, remained consistent across different significance levels and Table 10 and Table 11 detailed the results. The results show that H2, H2a1, H2a2, H2a3, H2b1, H2b2, and H2b3 are supported in the robustness test.

Robustness Checks on the Main Effects.

p < .05. **p < .01. ***p < .001.

Robustness Checks on the Mediating Effect.

Note. IV = independent variable; MV = mediator variable; M = model; CER = corporate environment responsibility; CES = corporate environmental strategy; RES = reactive strategy; PES = proactive strategy.

p < .05. **p < .01. ***p < .001.

Conclusion and Contribution

Conclusion

This study aims to investigate the relationship between corporate environmental responsibility and corporate sustainable development, exploring the potential mechanisms through which they are connected. Our findings suggest that corporate environmental responsibility can enhance corporate sustainability by establishing a link between environmental responsibility and sustainability strategies. This connection helps in transitioning short-term behaviors into long-term sustainable practices. Our theoretical framework proposes a sequence of “corporate environmental responsibility → corporate environmental strategy → corporate sustainability.” Empirical evidence supports the notion that corporate environmental responsibility positively impacts corporate sustainability, with the mediating effect of environmental strategies further reinforcing this relationship. Moreover, our study categorizes corporate sustainability into economic, social, and environmental dimensions. Results indicate that corporate environmental responsibility significantly contributes to economic and environmental sustainability, in addition to social sustainability. By classifying environmental strategies into reactive and aggressive categories based on companies’ responses to environmental challenges, we show that both types of strategies play a crucial role in mediating the effects of corporate environmental responsibility on economic and environmental sustainability.

Theoretical Contributions and Managerial Implications

This study establishes a comprehensive framework for understanding the relationship between corporate environmental responsibility, corporate environmental strategy, and corporate sustainability to make theoretical contributions.

First, our research contributes to the field of sustainable development by providing a theoretical framework that captures the entire process of how companies transition from environmental awareness to strategic decision-making and ultimately achieve corporate sustainability. We discovered a direct correlation between corporate environmental responsibility and corporate sustainability. Previous studies have shown that companies require additional investment to take on environmental responsibilities. As the impact on performance takes time to manifest, current research also emphasizes the importance of green innovation. This study reveals that corporate environmental responsibility has a direct influence on the sustainable development of enterprises and represents an extension of the impact of such responsibility.

Second, currently there are two inconsistent views on the impact of corporate environmental responsibility on corporate economic outcomes. While some studies suggest that corporate social responsibility can increase profits, a significant number of studies argue that corporate environmental responsibility may raise costs and reduce profitability, ultimately affecting corporate performance negatively. Excessive disclosure of environmental information can also result in increased scrutiny and controls on companies, potentially reducing profits. However, this study reveals that embracing environmental responsibilities can enhance economic sustainability in the long run. Despite potential short-term declines in economic returns, companies that prioritize environmental responsibilities may ultimately benefit from sustainable development, aligning social and economic responsibilities. And the results confirm the study of Song et al. (2017) that while a company’s environmental management may not have an immediate effect on current performance, it can significantly enhance economic performance in the subsequent period. These findings contribute to the understanding of the relationship between corporate environmental responsibility and economic sustainability.

Third, our research highlights the role of corporate environmental strategy as a mediator between corporate environmental responsibility and corporate sustainability. Additionally, the study examines the mediating effects of different dimensions of corporate environmental strategy on the relationship between corporate environmental responsibility and corporate sustainability. Therefore, the study discovers the internal mechanism by which corporate environmental responsibility affects sustainable development of enterprises.

And our study offers managerial implications as follows. First, enterprises should thoroughly consider their relationship with the natural environment and accurately comprehend their responsibilities in conserving resources and protecting the environment. No enterprise can thrive independently of the ecological environment. To achieve true sustainable development, it is imperative for enterprises to establish a positive connection with the surrounding ecological environment. Given that enterprises inevitably generate significant carbon emissions during production and operation, they are considered key players in environmental governance. On one hand, enterprises should strive to minimize carbon emissions by upgrading production methods and management models. On the other hand, when faced with necessary carbon emissions that cannot be reduced, enterprises should proactively assume environmental responsibilities and employ other methods to purify the natural environment, thereby minimizing damage to the ecological environment.

Second, managers should recognize that corporate environmental strategy is not a short-term solution employed by companies during crises, but rather should be integrated into the corporate strategic framework and be a crucial aspect of the company’s daily production and operations. Both reactive and proactive environmental strategies should be incorporated into the corporate strategic framework, rather than being mere responses to specific environmental pressures or sanctions. With the increasing societal focus on environmental issues, business managers should understand that addressing environmental concerns will always be intertwined with the functioning and performance of enterprises, gradually becoming one of several significant business objectives and a determining factor for achieving sustainable development. Environmental responsibility awareness is poised to become a future development trend, and corporate environmental strategy should receive the same level of attention as other core company strategies, becoming a long-term area of concern for the company.

Limitations

This study has several limitations. First, despite efforts to include various types of manufacturing enterprises and cities dominated by manufacturing enterprises in China, the questionnaire distribution was constrained by geographical, time, and human factors, preventing a truly comprehensive representation of data requirements of random. Second, the two-stage data collection approach employed in this study may not fully capture the long-term impact of corporate environmental responsibility on sustainable development. Collecting data over a longer period and analyzing it as panel data could yield more accurate results. In future studies, we aim to collect panel data to further test the research conclusions. Third, there may be other mechanisms besides corporate environmental strategy that influence corporate environmental responsibility and sustainability, but this study did not investigate them. Subsequent research will explore these alternative mechanisms. Forth, we have proposed two possible reasons for the insignificant impact of corporate environmental responsibility on social sustainability, but have not tested it. In future research, we will strengthen the theoretical basis for explanation and conduct empirical testing.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Ethics Statement

Not applicable.

Data Availability Statement

Data will be made available on request.