Abstract

This paper first theoretically analyzes the impact mechanism of digital finance on industrial structure upgrading, and then empirically analyzes the relationship between digital finance and industrial structure upgrading. The results show that the development of digital finance can promote the upgrading of industrial structure. Further analysis shows that the proper allocation of government attention is also key to achieving digital finance development and industrial structure upgrading. The above conclusions provide policy implications between the development of digital finance and the upgrading of industrial structure in China.

Introduction

China’s economy has shifted from rapid development to a high-quality development stage. Since the past industrial development pattern no longer suitable for the current economic development demands, it is urgent to transform and upgrade China’s industrial structure to adapt to the new development situation. There is no doubt that finance is the blood of the real economy and provides an important guarantee to promote the high-quality development of the real economy. However, in the process of development, traditional finance is usually hindered by “financing difficulties, financing expensive” (Mohamed, 2020), “financial supply and demand channels are not smooth” (X. Jiang et al., 2021), “information asymmetry” (G. Xu, 2018) and other issues, resulting in the traditional financial system being unable to meet the financing needs of the real economy, which has become a major obstacle to the quality of financial services. Moreover, after the outbreak of the “new coronavirus” epidemic, the production and operation have been seriously affected, and the development of traditional financial offline outlets has also been seriously restricted. How to find the new dynamic energy of financial services for the real economy has become more urgent, which has become an important problem to promote the upgrading of China’s industrial structure.

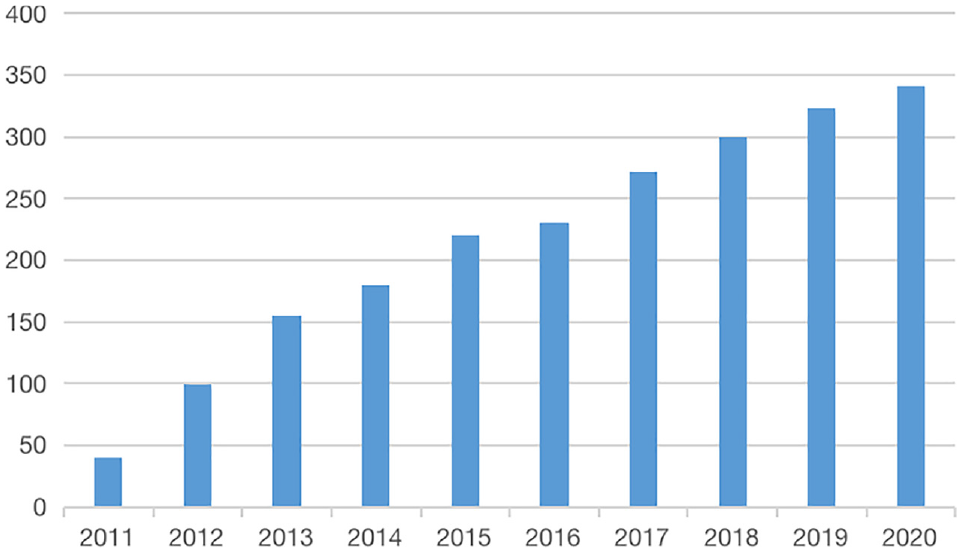

Innovation is the key driving force for development, and technological progress is one of the decisive factors to ensure sustained economic growth (Ozili, 2018). With the rapid development of block-chain, cloud computing, and big data, making digital technology in the financial field has given rise to new digital finance industry. Using the advantages of digital finance can improve the convenience of digital payment, break through the limitation of time and space, reduce the uncertainty risks, and achieve structural change and efficiency improvements in finance (Arif et al., 2020). As shown in Figure 1, China’s digital finance business has grown by leaps and bounds from 2011 to 2022, with the average value of the Digital Finance Index for each province being 40 in 2011 and growing to 341 by 2020, thus showing that the value of digital finance has been greatly exploited.

Mean Distribution of Digital Finance Index 2011 to 2020 (Provincial Data).

In recent years, China’s economy is turning to high-quality development, with more emphasis on industrial restructuring and optimization. Under the guidance of China’s development strategy, the government has been actively leading and promoting local industrial restructuring and transformation and upgrading. Figure 2 shows the contribution rate of different industries to GDP from 2012 to 2021, among which, the contribution rate of primary industry is steadily increasing, while the contribution rate of secondary industry shows a trend of first decreasing and then increasing, and the tertiary industry has become the industry that absorbs the most employment and has a key driving role in China’s economic growth.

Contribution of the development of each industry to GDP (2012–2021).

The complex, non-linear interactions and synergistic development among the subjects within an industry constitute the internal evolution of the industrial structure (Y. Liu et al., 2021), and the transformation of manufacturing into advanced manufacturing and the transition of services into productive services is an important symptom of the internal evolution of the industrial structure. At the same time, the optimization of industrial structure is often closely related to the factor endowment of a country. Most studies have found that digital finance, supported by emerging science and technology, has subtly promoted the optimization and upgrading of China’s industrial structure in terms of income growth, capital accumulation, consumption demand and technological innovation.

However, the existing literature finds that there are also some research gaps in the process of economic growth and industrial structure optimization and upgrading in China: on the one hand, the research on digital finance is still in its initial stage, and the concept definition, statistical classification, measurement and comprehensive evaluation index system related to it are not mature enough, thus leading to relatively weak theoretical research and mechanism testing of digital finance development and industrial structure upgrading; On the other hand, how can digital finance give full play to its advantages to promote the upgrading of industrial structure? What impact does it have on industrial structure upgrading under different government attention? These questions still have not been reasonably explained and need to be further explored.

Therefore, exploring the regional heterogeneity characteristics, mechanism and practical utility of “digital finance—industrial structure upgrading” has theoretical significance and practical value for improving the development of digital finance in China and improving the quality and efficiency of digital financial services in the real economy. In view of this,this paper analyzes the impact of digital finance on industrial structure and explores the transmission mechanism. On this basis, this paper discusses the heterogeneity of digital finance on industrial structure upgrading under different regional characteristics, further analysis of its impact in the context of government financial supervision.

The possible academic contributions and innovations of this study are as follows. First, compared with the previous literature studying digital finance and industrial structure, on the one hand, to test whether digital finance can promote the upgrading of industrial structure while exploring how digital finance can promote the upgrading of industrial structure based on regional characteristics; On the other hand, this study discusses the transmission mechanism of “digital finance—industrial structural upgrading,” which enriches relevant literature; Besides that, this study examines the impact of digital finance on industrial structure upgrading in the context of different governmental attention. The above makes the results of this paper more reliable and also enriches the theoretical basis of digital finance and industrial structure.

Second, the existing studies on digital finance and industrial structure mainly focus on the exploration of causality (Liu et al., 2021), and there are few articles involving mechanism exploration. In addition, compared with previous studies, adding the threshold effect of government attention has more research value, mainly in the following two aspects: first, some studies discuss the impact on digital finance in the context of government financial regulation, but do not categorize its regulatory results, and cannot deeply analyze the effect of government activities on digital finance; second, compared with OLS and FE regressions, using the threshold effect model is more conducive to analyzing the effect of digital finance on industrial structure under different government attention.

Third, the related research on industrial structure is mainly based on the relationship with the quality of economic development. Compared with the existing literature, this paper combines the development strategy of digital economy, takes digital finance and industrial structure as the main variables, takes into account the development characteristics of different regions, and explores the different impacts on the upgrading of industrial structure, thus providing a feasible path for the upgrading of industrial structure and high-quality economic development, and enriching the research on the impact of digital finance on industrial structure.

Fourth, some emerging and developing countries simply define digital finance as ease of access, without lowering the threshold of financial costs for the target demand group. This means that providing digital finance to the poor and low-income people does not mean that they have better access to digital financial services. Moreover, even if digital financial products and services are guaranteed to be available to all, digital finance will only be accepted by all if it is cheaper to access them than to walk into a banking hall. However, as China is putting more emphasis on the development of the digital economy, more comprehensive digital financial services have also emerged, and is using digital technology step by step to make up for the deficiencies in the development of digital finance in other emerging and developing countries. Therefore, this paper fills this research gap and discusses the relationship between digital finance and industrial structure upgrading in the Chinese context.

To test the impact of digital finance on industrial structure upgrading, the rest of this paper is listed as follows: The second part is a literature review and research hypotheses; The third part explains the research design of this paper, indicating data sources, estimation models, and variable explanations; The fourth part presents our benchmark regression results, endogenous and robustness checks, heterogeneity analysis, and transmission mechanism; The fifth part is to analyze the impact of digital finance on industrial structure upgrading under the perspective of government regulation; In the sixth part, we put forward corresponding policy suggestions according to the conclusions.

Literature Review and Hypothesis

Digital Finance and Industrial Structure

Relevant Studies on Digital Finance

With the advent of the digital economy, digital finance, which combines digital technology and traditional finance, has become the focus of academic circles. As digital technologies such as big data, blockchain and artificial intelligence have widely penetrated into the financial sector, they have greatly changed the traditional financial organizational structure and business form, giving rise to higher quality financial services and financial products, and promoting financial efficiency improvement and rational allocation of resources (Cai & Harrison, 2021). It has caused significant changes in traditional finance and gradually spread to other economic fields, promoting the high-quality development of China’s economy. Specifically, it has shown in the following aspects.

At the level of enterprise development, digital finance reduces the information asymmetry between the financial sector and financing subjects, effectively avoids the problems of adverse selection and moral hazard in the traditional financial market, and breaks the traditional financial boundary constraint, providing convenient resources for enterprise development by accelerating the speed of capital flow. The continuous proliferation and extensive penetration of digital finance in various business fields has broken the time and space constraints of capital transactions, accelerated the flow of funds throughout society, and increased the financing channels and financing methods for innovative subjects. Digital finance can also promote the transformation of traditional financial institutions, strengthen risk management capabilities, and enhance the efficiency of the traditional financial system led by banks. digital finance will also reduce the biased credit decisions and rent-seeking space in the credit approval process, alleviate enterprise budget constraints, and improve the efficiency of financial resource allocation, thus effectively promoting enterprise development.

At the level of residents’ lives, digital finance has enriched the service functions and access channels of traditional finance, and can promote financial services to be more grounded, inclusive and extended with the help of diversified digital technologies, so as to solve the problems of difficult and expensive financing for socially disadvantaged groups more effectively.

Numerous studies have found that digital finance not only expands the channels of financial service supply, but also helps to increase residents’ income and improve the current situation of income imbalance between urban and rural residents (Carter, 1997). Therefore, digital finance plays a role that cannot be ignored in promoting urban-rural development and narrowing the urban-rural income gap. Regarding the impact of digital finance on the income of urban and rural residents, some studies have found that digital finance can improve the financial accessibility of the poor. B. J. Chen and Lin (2014) conducted a study based on micro data from the China Household Survey and further found that the poverty reduction effect of digital finance was significantly and positively related to the poverty level. Baiquni and Ishak (2019) found that the coupling effect between digital finance development and rural revitalization index is continuously increasing, which is conducive to promoting rural revitalization and contributing to the reduction of urban-rural income gap.

At the level of green development, digital finance, as a kind of resource-saving innovative service, has strong green attributes, which can reduce pollution through online services, realize the decarbonization of financial services, and help promote green and low-carbon development (Chekima et al., 2016). On the one hand, digital finance achieves decarbonization. Digital finance uses Internet finance, network banking and other business models to realize contactless transactions through online virtual platforms, breaking through the limitations of traditional finance caused by the number of outlets and high labor costs, as well as reducing energy consumption of cash, paper and car rides, reducing carbon emissions in the transaction process and realizing the decarbonization of financial services (Goh & Balaji, 2016). On the other hand, digital finance promotes the greening of consumption. Digital finance uses mobile payment functions and other trading platforms to open up new channels for recycling, reduce resource waste and increase residents’ participation in environmental protection, thus promoting green consumption (X. Chen, 2007).

Relevant Studies on Industrial Structure

The upgrading of industrial structure is the intrinsic driving force of high-quality development of our economy. In the historical process of industrial structure development, the optimization of industrial structure, mainly characterized by sequential transfer of industries, structural upgrading of industrial sectors and industries, and internal evolution of industries, is the source of high-quality economic development (Manente & Zanette, 2010). The steam and electricity revolutions have promoted the evolution of industrial structure from agriculture-led to industry-led. In recent years, the digital industry has developed at a high speed and become an important driving force of China’s economic development, driving the continuous innovation of business models and the acceleration of a new round of industrial revolution. China’s traditional industries are struggling to survive, while the digital industry is showing explosive growth, forcing the digital transformation of traditional industries. In the context of the current deep adjustment of the world economic landscape and increasingly fierce industrial competition, China is in a critical period of economic structural transformation and upgrading. The study of the key elements that promote industrial structure upgrading can explain the new problems that arise in the development of China’s industrial structure, and can also further explore new directions and paths for industrial structure upgrading, helping China’s economy achieve higher quality development.

In the existing studies, many scholars have conducted a lot of research on the impact of industrial structure upgrading on economic growth. As a key variable of modern economic growth, the level of industrial structure development reflects the quality of economic development (Shi et al., 2020). Using Chinese provincial panel data, Qian Chunhui et al. (C. Sun et al., 2020) divided the industrial structure change into industrial structure rationalization and industrial structure advanced, and found that the impact of both industrial structure rationalization and industrial structure advanced on economic growth has obvious stage characteristics, and the positive effect of industrial structure rationalization on economic growth is stronger than that of industrial structure advanced in the long run. Zhang (2008) found that industrial restructuring is beneficial to the high-quality development of China’s economy, and there is a structural dividend of industrial structure upgrading on China’s economic growth, which is conducive to the improvement of China’s green total factor productivity. Based on neoclassical theory, Abdelkafi et al. (2013) selected the share of clean energy industry and labor productivity as proxy variables for industrial structure upgrading and economic high-quality development, respectively, and found that there is a nonlinear relationship between the impact of industrial structure upgrading on economic high-quality development in the context of environmental regulation policies that first inhibits and then promotes.

Some other scholars have studied technological innovation and industrial structure upgrading in the same framework. Baden-Fuller and Haefliger (2013) argues that capital-biased technological progress can promote economic growth rate and industrial structure upgrading, thus promoting high-quality economic development. Howell (2016) analyzed Chinese provincial panel data using SDR model, SER model, SAR model, and panel threshold model and found that the joint effect of science and technology innovation and industrial structure upgrading can promote economic growth.

The Relationship Between Digital Finance and Industrial Structure

Financial service is the booster of effective resource allocation and industrial structure upgrading, and the expansion of financial service scale will narrow the gap between regions and promote industrial structure transformation. Digital finance has the advantages of low service threshold and low cost, and as the digitalization of financial services continues to upgrade, it will bring about significant improvements in credit resource allocation efficiency and industrial financing, which will have a more far-reaching impact in the process of industrial structure upgrading (Mina & Imai, 2017).

With the continuous improvement of the financial system, financial services can effectively alleviate the information asymmetry problem, which in turn stimulates capital accumulation and technological innovation, and promotes industrial structure optimization and economic development (Shen et al., 2021). There is a long-term equilibrium relationship between the efficiency of financial services and the upgrading of industrial structure, and by lowering the threshold of access to financial services and promoting the free development of capital market, it can effectively promote the transformation of industrial structure and improve the efficiency of economic operation (Akbar et al., 2017). The innovation of the financial system represented by digital finance has alleviated the information asymmetry within and across industries, reduced the financing cost of enterprises, and influenced industrial development and technological innovation from the “horizontal effect” and “structural effect” (X. Wang & He, 2020). The comprehensive application of digital technology has greatly reduced the cost of digital financial services (Yi & Zhou, 2018), and thanks to the rapid upgrading of algorithms and computer technology, digital finance can quickly and accurately match the demand side of the industrial chain, providing timely and effective financial and service support for industrial structural upgrading (Bali Swain & Floro, 2014), and further promoting the rational allocation of financial resources to promote industrial upgrading.

Some studies suggest that digital finance can promote industrial structure upgrading by reducing the income gap between urban and rural areas. Digital finance can provide diversified and professional wealth services for customers, complement the supply deficit of the traditional financial sector, enhance the reasonable level of asset structure allocation on a large scale, promote income growth from the perspective of wealth value, and also improve the income gap situation (Huang & Chang, 2014), drive industrial human resources and sustainable industrial optimization.

It has also been argued that digital finance can promote industrial structural upgrading by realizing the capital accumulation effect. The main contribution to China’s industrial upgrading path is still the input of capital factors (Ahsan & Haque, 2017), and capital accumulation is a strong foundation to support industrial development. Diversified financial development largely promotes the effective transformation of capital accumulation into investment and supports the optimization and upgrading of economic structure through the resource allocation of finance (Zhao et al., 2018). The new financial service model represented by digital finance is further enhancing the capital accumulation of our financial system, while also alleviating the capital constraints of enterprises (X. Liu et al., 2021). By taking advantage of data acquisition, assessment processing and matching, digital finance has efficiently realized the accurate matching of capital and investment and financing, and delivered continuous financial support for the optimization and upgrading of industrial structure. Accordingly, we propose Hypothesis 1.

The Mechanism of Digital Finance Influencing Industrial Structure Upgrading

Technology Innovation Mechanism

At present, how China’s digital finance promotes the upgrading of industrial structure and improves the quality and efficiency of financial services to the real economy, has become one of the key issues to achieve high-quality economic development in China.

Technological innovation is an important bridge between the development of digital finance and the upgrading of industrial structure, as well as an effective supply of the financial market to the development of the real economy. A large number of studies have shown that digital finance can facilitate technological innovation (Keliuotytė-Staniulėnienė & Kukarėnaitė, 2020): The first one is taken from a micro perspective through the alleviation of financing constraints and financial costs as a logical mechanism. Then, to optimize corporate financial behavior, reduce financial leverage and moral hazard mechanism (Rana et al., 2019). Digital finance can also systematically evaluate innovative subjects in an all-round way, screen out innovative projects with potential, and guide capital to flow into more efficient projects. In addition, digital finance can enhance the innovation efficiency of economic agents through real-time tracking of the progress of innovative projects and refined risk pricing. Finally, from a macro perspective, the level of marketization is used as mechanism to promote enterprise technological innovation. Digital finance takes advantage of information such as cloud computing and big data to reduce the problem of information asymmetry between the financial sector and market players, to a certain extent, it can improve the transparency of information between “supply-side” and “demand-side,” improve the efficiency of financial allocation and risk management capability of enterprises.

On this basis, the ability to quickly promote corporate financing and maximize the utility of the resources obtained in the innovation process can drive corporate technological innovation. Some studies even divided enterprise technological innovation into core innovation and ordinary innovation for comparison, and finally found that digital finance promotes core innovation and inhibits ordinary innovation, indicating that digital finance would guide enterprises to carry out high-efficiency core innovation and avoid wasting innovation resources (Gu et al., 2018); some studies also considered enterprise technological innovation as a dynamic process, so they divided enterprise technological innovation into three stages (the stage of technological research and development, the stage of privatization, and the stage of industrialization) for research to further explore the different impacts of digital finance on enterprise innovation (Liu et al., 2021).

Enterprises are important subjects of economic activities, and they are also the representative subjects of high-quality economic development at the micro-level, while enterprise innovation to promote industrial structure upgrading is an effective path to achieve high-quality economic development. The theory of endogenous growth studies that “endogenous technological progress is the key factor to ensure sustained economic growth.” And has been expanded by some studies since then, which also confirms that technological innovation can drive industrial upgrading (Quan et al., 2020), and also confirms the relationship between complementarity and dependence. Yi et al. noted that the “structural effect” and “horizontal effect” in technological innovation can enhance industrial structural transformation and promote economic development (Lin & Yan, 2015). Kong et al. found that strategic emerging industries can effectively enhance the innovation capacity and willingness of enterprises (Kong et al., 2015). Through the above literature review, we found that enterprise technology innovation is the fundamental mechanism in the path of “digital finance-industrial structure upgrading,” that is, digital finance promotes industrial structure upgrading through improving enterprise technology innovation. Accordingly, we propose Hypothesis 2.

Mechanism of Resident Consumption

China is accelerating the establishment and improvement of a long-term mechanism to promote consumption, give full play to the basic role of consumption in expanding domestic demand, promote the expansion and quality of consumption, and enhance the role of consumption in promoting the development of the real economy. According to the classical consumption theory, the consumption level of residents ultimately depends on consumption willingness and ability, social system environment, market supply capacity. With the rapid development of digital finance in China, financial products have gradually become rich and diversified, and gradually meet and stimulate consumer demand, which makes many scholars gradually focus on digital finance and consumer research (Kapoor, 2014).

On the one hand, it is the influence of digital finance on the consumption level. A study analyzed the impact of digital finance on consumption level based on a spatial econometric model, and found that digital finance can effectively promote consumption level through intermediary mechanisms such as income, mobile payment, consumer credit and insurance (Herrenbrueck, 2019). Some studies have also found that digital inclusive finance can improve the consumption level and optimize the consumption structure through two mechanisms: narrowing the urban-rural income gap and optimizing the industrial structure, providing a realistic basis for expanding domestic demand and economic transformation and upgrading in China (H. Jiang & Jiang, 2020). Fu et al. studied the heterogeneous impact of digital finance on different categories of rural formal financial demand and found that digital finance had an impact on traditional banking financial services, but at the same time improved the informal financial needs of rural residents and promoted the consumption level (Fu & Huang, 2018). Based on an empirical analysis of objective data, He et al. explored the relationship between digital finance and residential consumption from a micro perspective. They believed that the inherent third-party payment technology of digital finance enhanced the convenience of payment, accelerated consumption decision-making and promoted the growth of consumption (He & Song, 2020).

On the other hand, it is the impact of digital finance on consumption upgrading. Some studies have found that the credit function of digital finance helps to reduce the liquidity constraints of residents and also alleviate the problem of cross-temporal allocation of funds, thus increasing consumer willingness and stimulating consumption upgrading (Fu & Huang, 2018). At the same time, digital finance simplifies the “psychological account” effect of consumers in the payment process (H. Sun & Hu, 2013) and promotes consumption upgrading.

Among the troika of economic development, consumption should play a fundamental role in China ’ s industrial development. Using the theory of “demand creation,” Sun et al. found that consumer demand will lead to changes in the proportion of consumer spending, which will naturally lead to innovation and progress of enterprises, coordinated economic development, industrial structure upgrading, green ecological balance, and the happiness of residents (Pablo-Martí & Arauzo-Carod, 2020). Many authors have considered that various structural policy instruments can stimulate consumption upgrading, thereby promoting industrial structure optimization and upgrading (N. Wang, 2014). Wang also analyzed from the perspective of consumer sociology, and found that with the expansion of consumption units, the consumption level of consumers has gradually increased (Qiu et al., 2018). Under the free movement of labor, local consumption upgrading can further promote the optimization and upgrading of urban industrial structures. Nowadays, China’s digital finance continues to raise the level of consumption and stimulate consumption upgrade, which has gradually forced the transformation and upgrading of industrial structure. Accordingly, we propose Hypothesis 3. The conceptual framework is shown in Figure 3.

The conceptual framework.

Methodology

Model Setup

This study is designed to investigate the impact of digital finance on the upgrading of industrial structure in China. The paper firstly builds the following formula to test the direct transmission mechanism:

where "

Because the first-order lag term of the explained variable is used as the explanatory variable in the model, it can cause endogenous problems by correlating the independent variable with the random disturbance term. Continuing to process static panel data such as OLS and GLS will result in biased and non-consistent estimators. Therefore, this paper uses a two-step system GMM to estimate the model, if the p-value of AR (1) is less than .05 and the p-value of AR (2) is greater than .05, It shows that the residual term of the differential equation does not exist a sequence correlation, that is, the estimation results are valid.

Measurement of Variables

Dependent Variable

The explained variable in this paper is the upgrading of the industrial structure. The Entropy-Weight method is used to calculate the comprehensive index of industrial structure upgrading, industrial structure rationalization and industrial upgrading rate to measure industrial structure upgrading. The advanced industrial structure is measured by the proportion of the tertiary industry in the secondary industry (Liu et al., 2021), rationalization of industrial structure expressed by Theil Index (Chen et al., 2021), the industrial upgrading rate is calculated as follows: Primary industry/GDP+(Secondary industry/GDP) *2+ (Tertiary industry/GDP) *3.

Independent Variable

The explanatory variable in this paper is the development of digital inclusive finance. The digital finance index used in this paper was created by Peking University to reflect the development of digital inclusive finance. The index reflects the degree of development and equilibrium of digital inclusive finance in China, and it covers three dimensions of digital financial services: coverage breadth, usage depth, and digitization level. Coverage breadth reflects the account coverage, usage depth reflects the real effect of the development of digital finance, and the digitization level is the embodiment of Internet technology.

Control Variables

According to the current situation of China’s development, economic growth rate, government intervention, employment rate, price stability, road facility construction and urbanization level are selected as control variables. The specific contents are as follows:

First, the economic growth rate. This control variable is a dynamic indicator reflecting the degree of change in the level of economic development, and it is also a basic indicator reflecting whether the regional economy has internal vitality. This paper uses the regional GDP growth rate to measure it.

Second, government intervention. Fiscal policy is one of the two major instruments of macroeconomic regulation (the other major instrument, monetary policy, is reflected by traditional financial indicators), Fiscal expenditure and tax policy can adjust the total market demand and thus affect the economic development of the region. This paper measures the government intervention by the proportion of fiscal expenditure in GDP.

Third, the employment rate. The employment rate is associated with regional productive activities, which will bring about population concentration in a certain period and further affect industrial development. Therefore, this paper uses the ratio of urban unit employment to regional total population to measure the employment rate.

Fourth, price stability. The more stable the residential price index is, the more people’s consumption habits and consumption patterns can fully adapt to the development of the current macroeconomic environment. In this paper, we choose the consumer price index (CPI) and take logarithmic processing.

Fifth, the construction of road facilities. Transportation is an important support to promote social progress, guide the layout of productive forces, and shape the new pattern of regional development, while the construction of road facilities provides a reliable guarantee for transportation, which will directly improve the efficiency of regional economic operation and the upgrading of industrial structure. In this paper, Road facility construction = ( railway mileage + highway mileage ) / provincial area.

Sixth, the level of urbanization. The level of urbanization is the pronoun of country development, and it is also an important standard to measure urban development. In this paper, the measurement of urbanization level is the proportion of regional population and area, and then processed by taking the logarithm. The specific indicators are shown in Table 1.

Variables and Data Sources.

Data Source

Considering the availability of data, this paper used the panel data from 31 provinces of China during 2011 to 2020 for the empirical analysis. The data were mainly derived from the China Statistical Yearbook, China Science and Technology Statistical Yearbook, and the Wind database. To reduce the effect of heteroskedasticity on the results, all non-ratio and non-standardized variables are logarithmically processed. The descriptive statistics of each data are shown in Table 2. Digital finance and enterprise technology innovation shows the characteristics of “large mean and small standard deviation”. From the perspective of control variables, different provinces also have significant differences in economic growth rate, government intervention, employment rate, price stability, road facility construction, and urbanization level.

Descriptive Statistical Results of Main Variables.

By classifying the descriptive statistical analysis into regions, it can be found that each variable shows different characteristics in the central, eastern and western. From the perspective of industrial structure upgrading, the mean value of the western region is the largest and the mean value of the eastern region is the smallest, which shows that the industrial development in the western region has been strongly supported and shows good results. From the perspective of the overall development level of digital finance, the mean values of the eastern, central and western regions are all stable around 5, which shows that digital finance is developing steadily. Descriptive Statistical Results of Main Variables as shown in Table 3.

Descriptive Statistical Results of Main Variables.

Main Variable Test

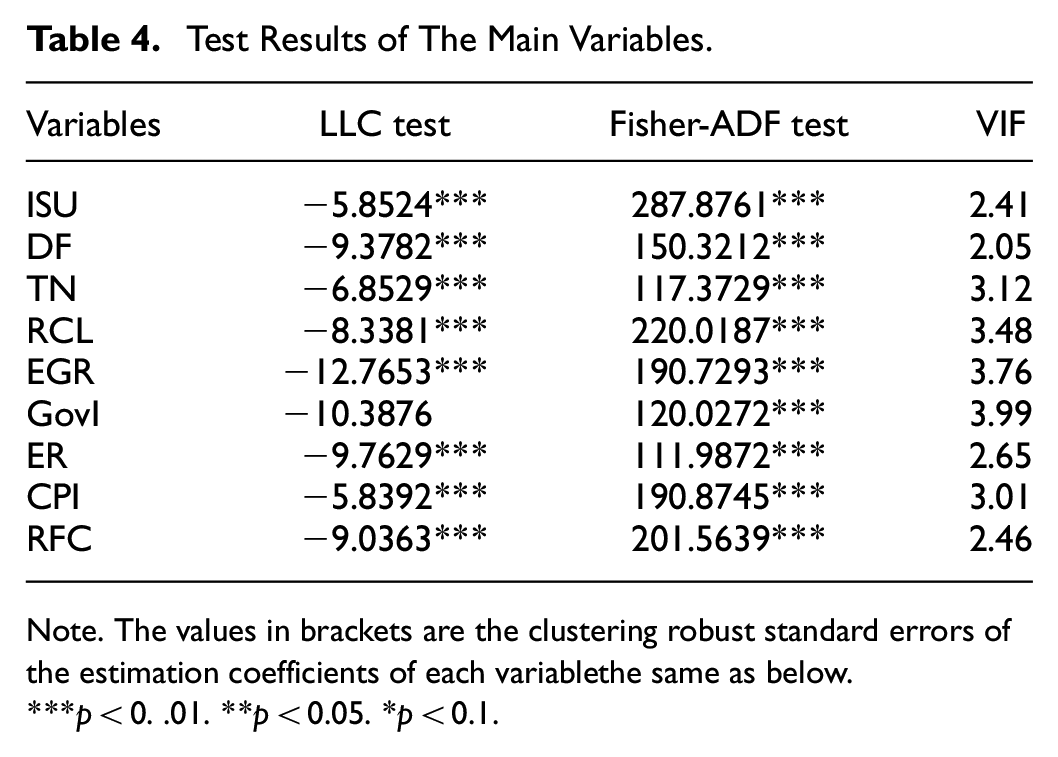

Table 4 reports the results of unit root tests for the LLC and Fisher-ADF methods. Since this study analyzes 10-year time effects with a large time span, unit root tests are required as a way to prevent problems such as pseudo-regression and t-test failure for unbalanced panel data, thus ensuring the stability of the data analysis. The data in this paper belong to the strongly balanced panel data, and when the LLC test is used to test the data, when P is less than .05, it means that the data are stable. The table shows that the LLC and Fisher-ADF test results of all variables are significant, which means that the data have passed the stability test. In addition, this paper also conducted the variance inflation factor (VIF) test, and the data showed that the VIF values of all variables were less than 5, and the average VIF value was 2.99, indicating that the data did not have the problem of multicollinearity. In addition, this paper also tested the normal distribution of the main variables through the Jarqua-Bera method, in which the p-value of industrial structure was .6523 (p > .05), which could not reject the original hypothesis, that is, the data of this variable conformed to the normal distribution characteristics, and the p-value of digital finance was .5986, which also conformed to the normal distribution characteristics.

Test Results of The Main Variables.

Note. The values in brackets are the clustering robust standard errors of the estimation coefficients of each variable the same as below.

p < 0. .01. **p < 0.05. *p < 0.1.

Correlation Coefficients

Table 5 reports the correlations of the main variables. The correlation between digital finance and industrial structure upgrading is significantly positive. Among the control variables, the correlations between government intervention, employment rate, road facility construction, and urbanization level and industrial structure are significantly positive. These results provide preliminary support for our hypothesis that digital finance is positively correlated with industrial structure upgrading.

Correlation Coefficients.

The Empirical Results

Baseline Results

The model is estimated based on a two-step system GMM to study whether digital finance can promote industrial structure upgrading. Table 5 displays the benchmark regression results. In model 1, digital finance had a positive driving effect on industrial structure upgrading at the level of 1%. This finding indicates that the development of digital finance in China can promote the upgrading of industrial structure and accelerate the level of industrial structure optimization. This is consistent with the findings of Song et al. (2021a). Therefore, Hypothesis 1 is true.

Digital finance has different effects on the industrial structure of different regions, and there are obvious heterogeneous characteristics of regional distribution in China. The empirical results are shown in Table 6. Model 3 shows that the development of digital finance in the eastern part of China is positive but not significant. It shows that the eastern region has given priority to economic development, and traditional finance has gradually met the needs of regional industrial development in the early stage. The new products and services provided by digital finance are only an appropriate complement to traditional finance, resulting in the impact of digital finance on the “empowerment” of the industrial structure of the eastern region is not obvious. Model 2 shows that the role of digital finance in promoting industrial structure upgrading in the central region is significantly positive at the level of 1%. It shows that the central region of China has a strong late-development advantage, which can effectively reduce market information asymmetry and resource allocation distortion while promoting the development of digital finance, it can also fully release economic vitality to promote industrial structure upgrading under the new development paradigm of China. Model 4 shows that digital finance can also promote the upgrading of industrial structure in western China. For the western region, due to the relatively poor geographical position, the level of economic development is relatively slow. As a new driving force for financial development, digital finance can narrow the “digital divide” and release certain economic dividends, creating a “catfish effect” in the region and promoting the upgrading of the industrial structure in the western region.

Baseline Regression Results.

Note. The values in brackets are the clustering robust standard errors of the estimation coefficients of each variable—the same as below.

p < 0.01. **p < 0.05. *p < 0.1.

The estimation results of control variables show that the coefficient of the employment rate is significantly positive in Models 2 to 4, indicating that the employment rate can accelerate the upgrading of industrial structure. It may be that the expansion of the employment rate increases the production capacity of enterprises, and the productivity of enterprises further stimulates the transformation and upgrading of industrial structure. The effect of government intervention on industrial structure upgrading is positively but not significantly, this may indicate that the government, as the “visible hand” in the process of social progress, still needs to gradually improve its policies and systems to adapt to social needs. The results of AR (1) and AR (2) based on the Arellano-Bond test, there is a first-order autoregressive and no second-order autoregressive. Moreover, the Sargan test results indicate that the selected instrumental variables in this paper are robust and effective, and there is no over-identification problem.

Robustness Test

Endogenous Treatment

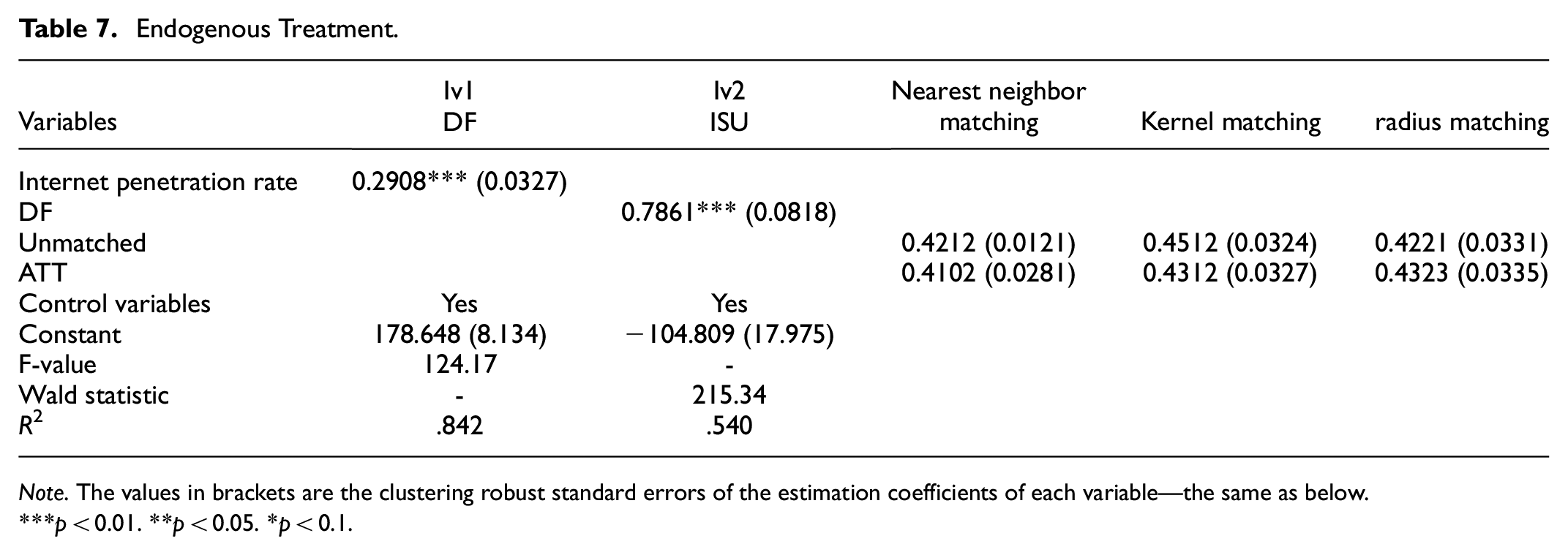

The two-step system GMM method is used to deal with the lag of the dependent variable. Eliminate the endogenous problems caused by the reverse causality of “the faster the industrial structure is upgraded, the better the development of digital financial”. Based on this, this paper takes the research of Qiu et al. and uses the Internet penetration rate of each province as an instrumental variable for the two-stage least squares regression (2SLS) (M. Song et al., 2021). Both the first stage F-value and the second stage Wald statistic in Table 7 passed the test, indicating that there is no weak instrumental variable and over-identification problem in the instrumental variable test.

Endogenous Treatment.

Note. The values in brackets are the clustering robust standard errors of the estimation coefficients of each variable—the same as below.

p < 0.01. **p < 0.05. *p < 0.1.

To ensure the reliability of the research results, this paper continues to use Propensity Score Matching (PSM) method for endogeneity. First, the probability of industrial structure upgrading in the sample regions is estimated by Logit to obtain the propensity score of industrial structure upgrading in each region. Then, nearest neighbor matching, kernel matching, and radius matching were used to match the propensity scores estimated from the sample, while each covariate passed the balance test to eliminate the sample differences, and the causal effect of digital finance development on industrial structure upgrading was obtained after matching. the estimation results of the PSM method are shown in Table 7, and the estimated coefficients of the matched average treatment effects (ATT) were all positive and significant at 1%. The results are also more similar to the estimated results of the unmatched main regression model, and this finding further verifies the reliability of this study.

Robustness Test

In this paper, we manually collated the Baidu search indices of keywords related to financial technology (Fintech) in each province from 2011 to 2020 to replace the digital finance index, the main reasons are as follows: First, the search index of keywords related to Fintech can reflect the development of digital finance to a certain extent Ripberger (2011), Jagtiani and Lemieux (2017) pointed out that the data people search on the Internet are demand-based data, which can be used for status quo tracking and trend prediction; Internet search behavior is more representative information in network big data, which can help to make macroeconomic prediction. Second, the Baidu search index of keywords can be counted at the province and year levels, thus meeting the requirements of provincial panel data in this study.

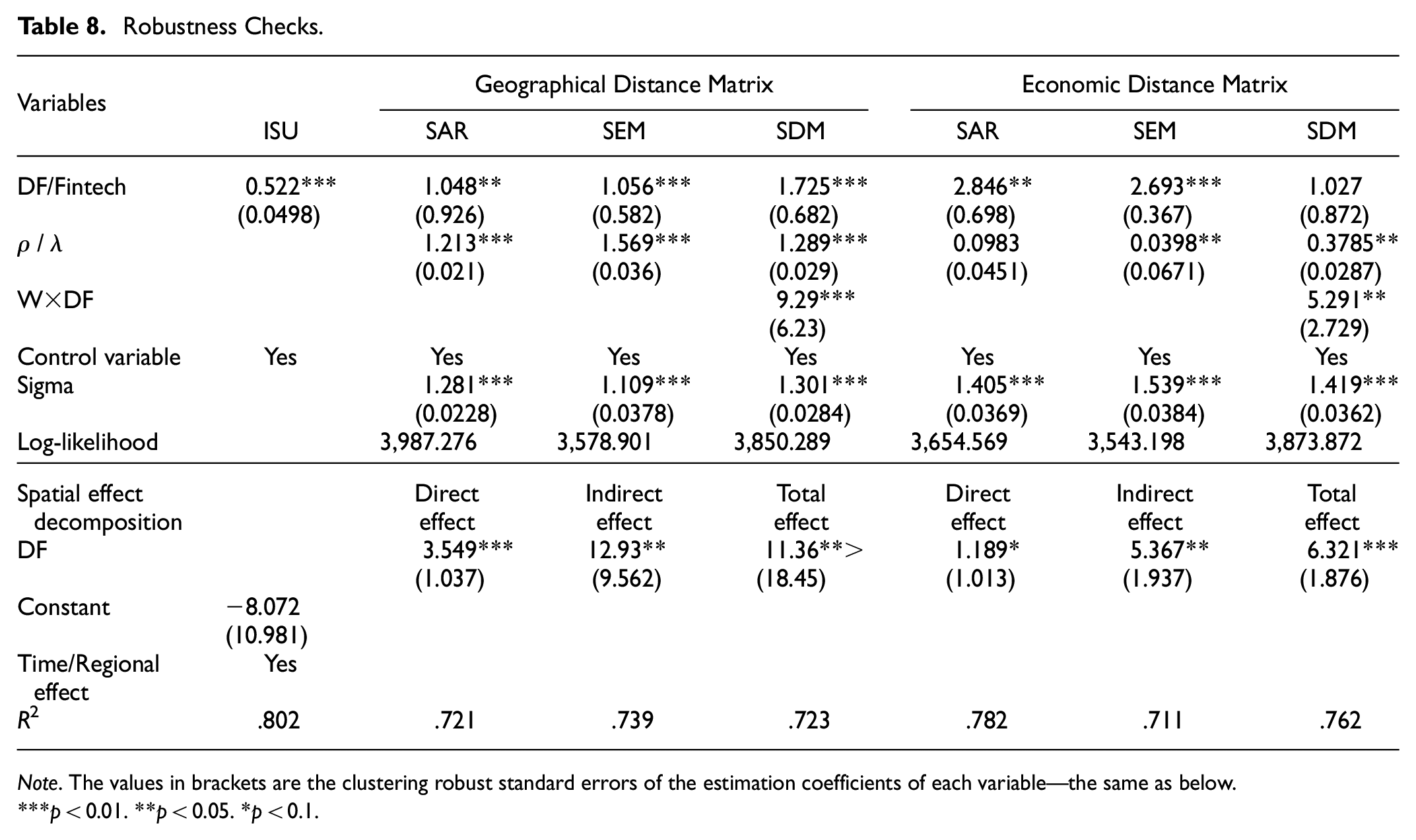

The steps are as follows: refer to the research results of some scholars (S. Chen & Zhang, 2021), and combine with Baidu search index to determine the keywords related to financial technology. The basic technology perspective includes “big data, cloud computing, blockchain”; the capital payment perspective includes “online payment, mobile payment, third-party payment”; the financial service perspective includes “network financing, network loan, electronic banking.” The perspective of financial technology includes “Internet finance, financial technology.” Finally, all the Baidu search indices of the above keywords were collected, and then the indexes synthesized by the entropy method were divided by the number of resident population in each province to measure the development level of digital finance in each province. The results, as shown in column 1 of Table 8, show that the results of digital finance and industrial structure upgrading are still significantly positively correlated at the 1% level. Therefore, hypothesis 1 is verified.

Robustness Checks.

Note. The values in brackets are the clustering robust standard errors of the estimation coefficients of each variable—the same as below.

p < 0.01. **p < 0.05. *p < 0.1.

This paper further conducts robustness tests and uses the spatial regression partial differencing method to decompose the spatial spillover effects of digital finance on industrial structure, and the results are shown in Table 8 for the direct effects, indirect benefits and total effects. It can be seen that digital finance and industrial structure have positive indirect effects in both the geographic distance matrix and the economic distance matrix, and all of them are significant at the 5% confidence level, indicating that the development of digital finance in neighboring cities will also promote the industrial structure in the region, which is consistent with the above findings. In the direct effect results, the effects of digital finance on industrial structure upgrading were found to be positive and passed the significance test of 1% in the geographic distance matrix, indicating that the development of digital finance in the region can also promote the development of local industrial structure. The significance in the economic distance matrix is 10%, which may be due to the fact that the regional economy is successfully transforming but the financial system has not yet been completely transformed, thus weakening the role of digital finance in promoting the industrial structure. However, from the total effect results, the impact of digital finance on industrial structure is significantly positive, which means that in general, digital finance in neighboring regions will promote the development of industrial structure. This result again verifies hypothesis 1.

Heterogeneity Results

The previous section examined the role of digital finance in promoting industrial structure upgrading, and this section continues to explore the question of how digital finance can promote industrial structure upgrading based on regional characteristics. Digital finance makes up for the deficiency of traditional finance in underdeveloped areas, and reduces operating costs through digital technology, but also solves the problem of financial exclusion, which both mitigates the financial risks caused by information asymmetry and enhances the sustainability of financial services supply. Its financial services “inclusiveness” and digital technology “technology” are new dynamic energy to promote the development of the real economy. So, is the relationship between digital finance and industrial structure upgrading related to regional development characteristics? What is the performance in different regions? This section will explore such questions.

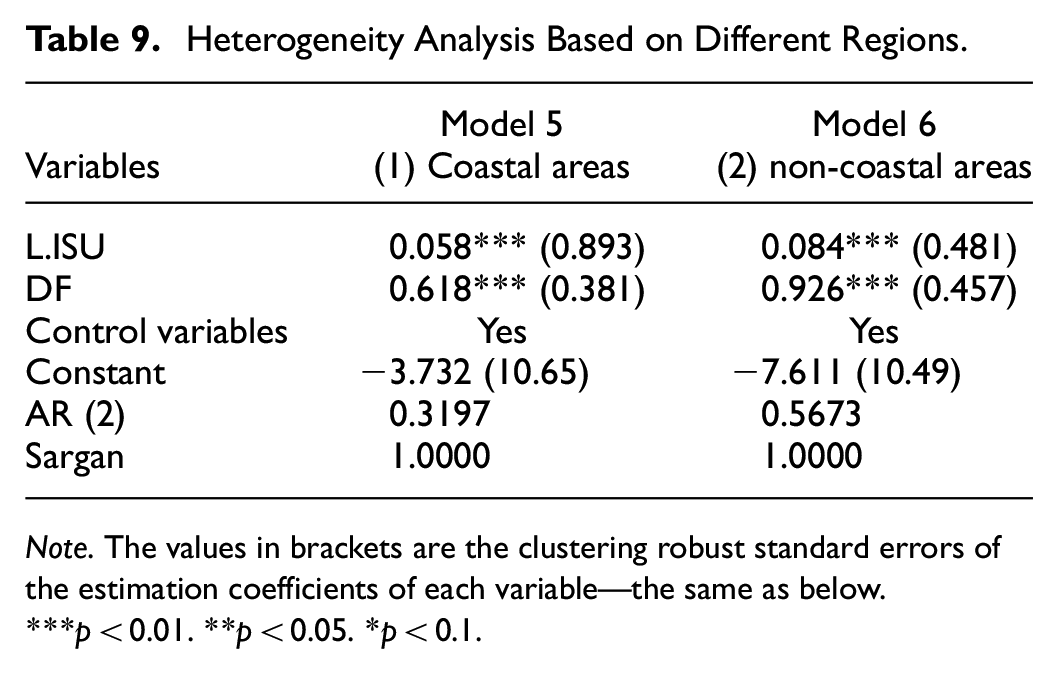

Heterogeneity Analysis Based on Different Regions

The results in Table 9 show that the effect of digital finance on industrial structure upgrading is better in non-coastal regions. The possible explanations are twofold: first, the development of non-coastal regions would be limited by economy and technology in the past, while digital finance carries technological advantages that can enhance the rapid development of digital industry in non-coastal areas, thus promoting economic development. Second, digital finance can increase financing opportunities for enterprises through a more convenient way, thus optimizing digital capacity and promoting industrial structure upgrading.

Heterogeneity Analysis Based on Different Regions.

Note. The values in brackets are the clustering robust standard errors of the estimation coefficients of each variable—the same as below.

p < 0.01. **p < 0.05. *p < 0.1.

Heterogeneity Analysis Based on Digital Finance Sub-Dimensions

From the regression results in Table 10, the coefficients of digital financial breadth, depth, and digitization are all significantly positive at the 1% level, which means that the breadth of coverage, depth of use, and digitization can significantly contribute to the upgrading of industrial structure. The coverage breadth expanded the enterprise financing platform, reduces financing costs and information asymmetry, and helps upgrade and adjust the industrial structure. And the digitization level saves time costs through big data, block-chain, cloud computing and other technologies, provides a guarantee for the optimization and upgrading of industrial structure. In terms of depth of use, it is found that the usage depth can also promote the upgrading of industrial structures. On this basis, it is also found that the usage depth has an “inverted U-shaped” relationship with the upgrading of industrial structures. It shows that there is an optimal state of industrial structure upgrading for the usage depth. Before reaching the optimal state of industrial structure, the greater the depth of digital finance use, the more it can promote the industrial structure upgrade. However, beyond the optimal state, it may be constrained by other factors.

Heterogeneity Analysis Based on Digital Finance Sub-Dimensions.

Note. The values in brackets are the clustering robust standard errors of the estimation coefficients of each variable—the same as below.

p < 0.01. **p < 0.05. *p < 0.1.

Transmission Mechanism

On the one hand, digital finance gives full play to the connotation of “technology is the means, finance is the essence,” solve the problem of “difficult and expensive financing” for enterprises, and provide the guarantee for their technological innovation. The upgrading of industrial structure is also inseparable from scientific and technological progress and innovation-driven enterprises, which should take technological innovation as the main supply side of China’s current development, increase technological factor investment and realize the adaptability of the supply system to domestic demand. On the other hand, digital finance can use its advantages to promote the development of new models, enhance social consumption capacity, realize consumption expansion and quality improvement, and provide powerful support for the smooth operation of the main domestic circulation mechanism.

The benchmark regression shows that digital financial development can promote industrial structure upgrading, but it fails to explain the “ black box ” mechanism. Based on this, this section continues to analyze the transmission mechanism between “digital finance—industrial structure upgrading.”

Among them, mediating variables are enterprise innovation (Innovative), household consumption level (con), other variables are defined and measured in the same way as before.

If the coefficient of the interaction term is significantly positive, it implies that the development of digital finance accelerates the expansion of intermediary mechanisms, which in turn promotes the upgrading of industrial structure. If the coefficient of the interaction term is significantly negative, it indicates that the selected mediating variable is not a key mechanism for digital finance to promote industrial structure upgrading.

Table 11 shows the test results of the mediation mechanism. Model (1) shows that digital finance is positively related to industrial structure upgrading. Model (2) shows that digital finance promotes enterprise technology innovation, and the coefficient of interaction term shows that digital finance can promote industrial structure upgrading by improving enterprise technology innovation. In other words, part of the impact of digital finance on industrial structure upgrading is realized through enterprise technology innovation. Therefore, enterprise technology innovation is an inherent mechanism for digital finance to promote industrial structure upgrading, and this empirical result supports Hypothesis 2.

Transmission Mechanism.

Note. The values in brackets are the clustering robust standard errors of the estimation coefficients of each variable—the same as below.

p < 0.01. **p < 0.05. *p < 0.1.

Model 3 analyzes the transmission mechanism by consumption level. The results show that digital finance can increase the consumption level, which passes the significance test at the 1% level and the regression coefficient is positively correlated. The interaction term shows that digital finance can stimulate the upgrading of industrial structure by increasing the level of resident consumption. That is, resident consumption is one of the intermediate mechanisms between digital finance and industrial structure, and this result verifies hypothesis 3.

Further Analysis: A Threshold Effect Analysis Based on Government Attention

This paper previously explored the impact of digital finance on industrial structure upgrading, but did not examine the relationship between digital finance and industrial structure upgrading under different government attention. Since government performance depends on the allocation of its attention, how to play the role of government attention has become a topic of research significance. This section will explore the impact of digital finance on industrial structure upgrading from the perspective of government financial regulation and environmental regulation. In choosing indicators, the government’s financial regulatory expenditure is used to represent financial regulatory attention, and the number of environmental administrative penalties proposed by the government represents environmental regulatory attention. The threshold effect test is conducted through financial regulation and environmental regulation to analyze the effect of digital finance on industrial structure upgrading under different governmental attention. Based on this, this paper constructs a threshold regression model with financial regulatory attention and environmental regulatory attention as threshold variables (Thresh) in turn, as follows.

where

The rapid rise of the Internet has promoted the development of big data, and traditional financial services have gradually extended toward digitalization and convenience. It is in this context that digital finance has emerged, not only to reduce the “digital divide,” but also to bring convenience and lower transaction costs to its users. However, digital finance also has technical defects. Based on this, the Chinese government began to gradually allocate its attention to financial regulation and environmental regulation.

This section presents the nonlinear effects of digital finance and industry structure. Table 12 shows a panel threshold existence test with 300 iterations of sampling by bootstrap. The results show that the financial regulation and environmental regulation thresholds pass the significance test for the single and double threshold estimates. In contrast, the triple threshold estimates do not pass the significance test.

Threshold Effect Test Results of Loan Size and Carbon Emissions.

Table 13 reports digital finance regression results and industrial structure upgrading under single and double thresholds, which also have different effects on industrial structure when the thresholds are in different intervals. In the financial regulation model, the single-threshold results show that when the financial regulation threshold is less than 3.633, the regression coefficient of digital finance on industrial structure upgrading is 3.429 and significant at the 1% confidence level. When the financial regulation threshold is greater than 3.633, the regression coefficient of digital finance on industrial structure upgrading becomes 3.467 and is also significant at the 1% confidence level. The regression results are more clearly reflected by the double threshold,when the financial regulation threshold is less than 3.633, the regression coefficient of digital finance and industrial structure is 3.296 and significant. When the numerical threshold is between 3.633 and 4.218, the regression coefficient of digital finance and industrial structure is 3.518 and significant, and when the numerical threshold is greater than 4.218, the regression coefficient of digital finance and industrial structure becomes 3.613 again, and also significant at 1% confidence level.

Threshold Estimation Results.

Note. *** indicate statistical significance at the 1% levels.

The results of the single-threshold and double-threshold regressions show that the impact of digital finance development on industrial structure varies with the change of threshold and has a marginal incremental effect, that is, the promotion effect of digital finance on industrial structure will gradually increase. In the environmental regulation threshold model, the regression results of single threshold and double threshold also show that digital finance can accelerate the upgrading of industrial structure, and it also shows the non-linear characteristic of marginal increment.

Therefore, government attention should be shifted to accelerate the establishment of a new type of digital government. On the one hand, information technology can be used to improve the efficiency of government financial regulation and environmental regulation. On the other hand, digital financial means can be used to provide more governance resources for the government, to play the regulating role of the government as the “visible hand” in the whole society, and promoting the combination of “promising government” and “efficient market” to promote the upgrading of industrial structure, to crack the main problem that hinders “financial services to the real economy.”

Conclusion

Conclusions

Based on the provincial panel data of China from 2011 to 2020, this paper empirically tests the impact, mechanism and regulatory issues of digital finance on industrial structure upgrading, and obtained the following conclusions: Firstly, digital finance can significantly promote the upgrading of industrial structure. Secondly, the heterogeneity analysis explores how digital finance relies on regional characteristics to promote industrial structure upgrading. Thirdly, the analysis of the mechanism finds that digital finance promotes industrial structure upgrading mainly through increasing corporate technological innovation and household consumption. Fourth, the rational allocation of government attention can play the significant role of government as a “visible hand” in the development of the whole society, while accelerating the combination of “promising government” and “efficient market” to promote the upgrading of industrial structure.

Policy Recommendations

This paper has the following important policy implications: First, it is recommended that financial institutions provide diversified digital financial services. Financial institutions can provide various types of financial services to consumer groups at different levels and take full advantage of digital technology to bring “digital dividends” to customers. On the one hand, for banking financial institutions, it is necessary to improve the digital financial service platform, update the application channels for credit business, digital payment and insurance, and formulate flexible and controllable loan terms and loan limits, so as to reduce financial risks and protect the rights and interests of users. On the other hand, for non-bank financial institutions, provide users with convenient online payment tools, especially through the use of open digital platforms such as WeChat to lower the threshold of consumption and encourage consumption, and jointly create a favorable environment for the development of digital finance. In addition, most financial institutions can provide customers with one-stop financial services such as account services, money funds, credit cards and other deposits, investments, remittances and loans through the innovative advantages of digital finance.

Secondly, to improve the problem of unbalanced regional development. Due to the special spatial agglomeration of China has produced a series of economic development imbalance problems (H. Song et al., 2021). To alleviate such problems, on the one hand, we can promote financial education, on the other hand, we can accelerate the infrastructure construction. In terms of financial education, financial knowledge can be disseminated in an easy-to-understand way, and financial education can also be popularized among rural residents and vulnerable groups in underdeveloped areas, reduce the urban-rural income gap and narrow the “digital divide.” In terms of infrastructure construction, as the development of digital finance relies on local hardware measures such as digital communication technology, China also needs to continue to establish a complete digital financial ecosystem, that is, to promote the development process of the “new infrastructure” to lay a solid foundation for the development of digital finance.

Third, improve the quality of digital financial services. On the “supply-side,” digital finance can reduce the cost of enterprise financing through artificial intelligence and patent inventions, alleviate the problem of “difficult financing and expensive financing,” and promote enterprise innovation and technological upgrading. On the “demand-side,” China is accelerating the establishment and improvement of long-term mechanisms to promote consumption, bring into full play the basic role of consumption in expanding domestic demand. On the one hand, digital finance can give full play to digitalization, convenience and other features, and continuously innovate the functions of digital payment, credit and transfer. On the other hand, we should improve the diversified and wide-covering service system, rapidly promote the potential of financial services to the real economy, and further realize the promotion effect of financial services on high-quality economic development.

Fourth, establish digital financial management and regulatory system. The government should establish a digital financial regulatory approach, promote the integration of “promising government” and “efficient market,” and improve the compliance regulation and risk control of financial innovation products. At the same time, it is necessary to further improve the consumption system, credit system, payment system, and other laws and regulations to protect the legitimate rights of digital financial consumers and data privacy, so as to make the development of digital finance in China have a direction and rules.

Strengths of This Paper and Future Perspectives

In the future, the application scope of digital finance can be gradually expanded, and its advantages can be continuously developed to more fields such as energy and agriculture, forming many digital scenarios and improving the efficiency of digital industry.

First of all, in the energy sector, we should deeply integrate technologies such as big data and blockchain with digital finance, carry out comprehensive applications, realize the integration of the two elements of “energy” and “finance,” and apply them to new energy trading, power trading, commerce and other fields to promote the marketization of energy trading. In addition, to accelerate the process of energy digitization, the improve the quality of digital financial services, encourage incentive policies for industrial innovation, and guide the development of energy toward energy-saving industries.

Second, in the field of agriculture, the scale effect of digital platforms should be gradually expanded and the development of agricultural finance should be steadily promoted. Guided by market demand, the guidance of industrial policies should be strengthened to promote the organic integration of digital finance and agriculture. The practical mode of integration of digital finance and agricultural economy can not only promote low-carbon industrial cooperation among regions and reduce the risks faced by agricultural development, but also enrich and improve the new agricultural industrial service system, so that regions can give full play to their comparative advantages through resource integration and promote the development of agricultural modernization.

There are still some shortcomings in this paper, and we hope the follow-up research can make up for them. On the one hand, whether there are other micro-mechanisms for digital finance to promote industrial structure upgrading remains to be explored. On the other hand, the construction system of industrial structure upgrading index can be further optimized. In short, under the unprecedented changes of the century, with the continuous development of China’s economic construction, highlighting the reliable advantages of high-quality economic development. At the same time, digital finance has also been integrated into our lives. It is necessary to continuously optimize the role of digital finance in promoting the real economy to further achieve the goal of high-quality economic development.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work is financially supported by the National Social Science Foundation of China (23CZZ039) and Research Initiation Program for Introducing Talents in Guizhou University of Finance and Economics (2023YJ20).

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.