Abstract

Effective risk management has grown more and more crucial in the complex world of international trade finance, bolstered by security, trust, and openness. By creating an integrated system that blends Hyperledger Fabric blockchain technology, Supply Chain Finance (SCF) protocols, and Generative Adversarial Networks (GANs), this study seeks to improve the intelligence and dependability of financial risk assessment. Four interrelated steps make up the suggested approach: (1) preprocessing and encoding SCF datasets; (2) creating synthetic risk data with GANs to mimic uncommon or dishonest trade behaviors; (3) using Hyperledger Fabric to execute smart contracts and log transactions decentralized; and (4) using real-time SCF compliance modeling for dynamic risk assessment. While blockchain guarantees the transparency, immutability, and auditability of financial records, GAN integration improves the prediction model by adding value to the training corpus. Comparative studies show that the suggested system considerably lowers the likelihood of data tampering and improves risk prediction accuracy by 12% when compared to traditional machine learning models. The results demonstrate that integrating generative modeling with blockchain technology can significantly improve financial risk management, transparency, and adaptability in global trade settings.

Keywords

Introduction

Financing on a global scale is one of the sectors that have felt the impact of blockchain technology. With the increase in global trade, the poses risks in international business become more intricate. The traditional systems of trade financing have gaps and flaws that slow down trade, including fraud, lack of effectiveness, and a lack of transparency. These issues can be resolved through blockchain technology which increases the security, efficiency, and trust within trade finance processes (Karthik et al., 2023; Li et al., 2023; Zhang et al., 2025). The purpose of this research is to determine how blockchain technology can improve risk management in global trade finance by optimizing processes, minimizing fraudulent activity and reducing functional, regulatory, and credit risks. The contribution of the present work is to trade financing for business and insurance companies dealing with global commerce is to demonstrate the potential blockchain technology has in dealing with risks.

In a Supply Chain, the rising conflict makes enterprises form business alliances centered around a commonality in the commodity, capital, and information flows to ameliorate competitive advantage and reduce costs (Li, Ananda, et al., 2020; Li, Wang, et al., 2020). Nonetheless, in the transaction processes of an alliance, their collective enterprise financing becomes challenging due to the information asymmetry-driven increased difficulty in risk control (Chakravarty et al., 2020). Due to the emphasis placed on helping mitigate SME’s financial challenges while also lessening the burden on financial institutions, supply chain finance (SCF) was developed. Even though SCF attempts to address the financing gaps, factors such as inadequately seamless information circulation across the entire supply chain, poor data quality. Notably inefficient payment and settlement processes, and sluggish credit transmission (Ehrenberg & King, 2020) augment the financial institution's credit risk. The primary attributes of blockchain technology, such as decentralization, traceability, tamper-proof, and smart contracts (Li et al., 2020), have to varying degrees. Shattered the information barriers that exist within and between organizations (Saberi et al., 2019), allowing for solutions and strategic interventions to the SCF risk challenges (Gong et al., 2021).

A number of academics got interested in supply chain financial risk as soon as it was presented (Sheng et al., 2020). Early on in the study, researchers focused on the dangers of different supply chain finance models. Researchers began doing thorough risk analyses of supply chain finance from a macro viewpoint by the middle of the process, and more recently, some academics started looking at the hazards of individual businesses from an industry perspective (Gu & Wang, 2020). Supply chain characteristics typically look at the financial risks associated with the industry's supply chain as well as the operating dynamics of the supply chain finance model's application. In order to characterize supply chain financing from the perspective of SME credit, Berge keeps the wait (Xie & Zhu, 2020). According to these analysts, small and medium-sized businesses cannot obtain loans since there is insufficient credit to support them. Consequently, a new financing paradigm was proposed in which financial institutions or major organizations control the transactions to supply external money to small and medium-sized businesses that are hard to finance (Wu et al., 2020; Gui, 2019).

As pointed out by the author, financial institutions must have a risk forecasting model capable of identifying and predicting the traits of individuals with higher loan default probabilities. Once more, Gui (2019) noted that sophisticated machine learning models are imperative; not only for the banks, but also for the clients, enabling them to understand behaviors that could be detrimental to their credit scores. A study conducted by Breeden (Breeden, 2020) emphasized that machine learning is rapidly advancing and being adopted for functions like credit scoring and credit risk management. ‘Breeden (Breeden, 2020) noted that there are perils to using machine learning techniques, so the focus of research now needs to explore how to employ machine Learning models within a regulated, compliant business framework.'

The researcher’s work (Asongu & Odhiambo, 2020; Biallas & O’Neill, 2021) surveyed various machine learning techniques along with their uses in managing credit risk problems. Disequilibrium is perhaps richer for emerging economies, like China and India. Women as well as the youth and small enterprises categories often tend to be underbanked due to lack of access to conventional forms of collateral. Moreover, they do not often possess identification documents like other citizens which banks require. Servicing this unbanked market niche can be facilitated by AI and Machine Aided Intelligence (MAI) technologies. They access behavior data from alternative sources like publicly available registries, Companies House data, satellite and aerial imagery, social media, text messengers, and other proprietary data. This improves the determination of the clients’ verification for lenders (Pu et al., 2023).

The majority of traditional managing supply chain risks techniques have been reactive, frequently depending on retrospective evaluations and post-event evaluations to create plans to address disturbances when they have occurred (Chen, 2019). Currently, this method is no longer viable due to the extraordinary uncertainty, complexity, ambiguity, and volatility (VUCA) conditions (Bharadiya, 2023). Businesses must focus on moving from risk responses to proactively risk reduction in order to maintain their competitive position and adjust in this environment. Predictive analytics and machine learning are two disruptive technologies that must be combined to create a paradigm shift in order to bring about this change (Rawat, 2022). The method of predictive analytics estimates the probability of future occurrences or the development of specific patterns by combining statistical computations, machine learning approaches, and past information. On the other hand, machine learning enables systems to perform better by using historical data to find connections and outliers that are much harder to find using conventional analytical techniques (Perifanis & Kitsios, 2023). While many firms are still dealing with the effects of the global epidemic, some, like supply chain, jumped at the opportunity to extensively employ these modern innovations. The proposed work's primary contribution is listed below:

This paper suggests a novel method for resolving financial risk management problems in trade financing and supply chain finance (SCF) systems by combining Generative Adversarial Networks (GANs) with Hyperledger Fabric Blockchain protocols.

nitially the Information Composition and Simulations stage overcomes the limits of past records by using GANs to create financial records that represent crucial hazardous situations.

Furthermore, Hyperledger Fabric is utilized by Blockchain-Enabled Data Integrity to ensure secure and unalterable data transfer across supply chain participants.

Thirdly, the system classifies and predicts risk through adversarial training where the discriminator is tasked to identify accurately fraudulent, default-prone, and high-risk transaction patterns.

Fourth, Protocol Integration is where the risk scores from the model are embedded into SCF protocols, which are run by smart contracts to allow automatic credit decisioning and dynamic risk-based pricing in real-time.

Evaluation results indicate that the application of blockchain trust mechanisms to GAN data significantly increases classification precision and recall up to 17% while mitigating risk detection false-positive rates.

The rest of our research article is written as follows: Section “Literature Survey” discusses the related work on Risk Management, International Trade Finance, Blockchain Technology, and supply chain finance. Section “Proposed Methodology” shows the algorithm process and general working methodology of the proposed work. Section “Result Analysis” evaluates the implementation and results of the proposed method. Section “Conclusion” concludes the work and discusses the evaluation.

Literature Survey

Researchers and practitioners have focused on the area of supply chain risk management because it concerns the effective movement of goods, services, and information in a business context globally (Jayender & Kundu, 2021). In this section, we provide a comprehensive review of literature that outlines the best practices and technologies aimed at improving agility and resilience in the supply chain. Studying this body of knowledge helps us understand the evolution of risk management frameworks, new paradigms, and the gaps that defined the rationale for the proposed framework. This review provides us with a starting point for constructing the context where our analysis reinforces the synthesis of diverse perspectives and empirical insights in the discourse on agile supply chains. Many attempts have been made to integrate new technology into the selected domain, studying its supply chain risk management facets, advantages, and challenges, as noted in (Giannakis & Louis, 2016). In this section, we capture all the scholarly works that have shaped the understanding of this evolving landscape, focusing on their approaches, conclusions, and shared gaps.

A multi-agent-based supply chain management system with big data analytics features was developed by Giannakis and Louis (2016). This system was designed to impact the agility of supply chains with self-governing corrective action control loops. In this study, responsiveness, flexibility, and speed were the three main constituents of agility, and these findings structured the organizational design of the system. This study demonstrated how cutting-edge technology can improve flexibility in a variety of ways, enabling supply chains to be operated swiftly, nimbly, and adaptable. Jayender and Kundu (2021) made observations about the elements influencing supply chain efficiency in the automobile sector. Their study looked at how this collaboration impacts the sector’s agility by exploring the potential synergy of big data analytics with ERP systems. A graph theory-based approach to agility enhancement and implementation issues was recommended for these concepts. This research stressed the need for more innovative approaches to ensure agility in integrated complex systems. Shamout (2020) studied the effect of supply chain data analytics on agility and supply chain agility.

The investigation analyzed the causal pathways that predict high supply chain agility using a combination of supply chain data analytics, business age, business size, and annual revenue with fuzzy set qualitative comparative analysis (fsQCA). This study emphasized the intricate analytics of data and the roles that data analytics plays in achieving supply chain agility in a complex business landscape. Using Twitter data and blockchain technology to augment supply chain visibility while risk mitigation, real-time incident detection has been studied by Lee et al. (2021). This innovative approach showcased the management of risks leveraging real-time data captured in addition to the transparency and security potent capabilities of blockchain. AI and ML technologies applications over different phases of supply chain risk management were undertaken in a comprehensive literature review by Ganesh and Kalpana (2022). The study brought to the fore the multiple algorithms of AI employed, along with the varying risks associated with the supply chain. This research discovered voids in the existing body of work, which was very compelling and provided an intriguing scope for further exploration, along with implementation challenges. The rest of the research focused on enhancing supply chain visibility along with managing the risks of interruptions using the digital twins, a notion by researchers (Li et al., 2023) introduced as a digital supply chain twin, a model that reflects the real-time status of a network.

Bitcoin’s blockchain serves the role of underlying technology as its distributed ledger, which cannot be modified. Moreover, it demonstrates an entirely new model of distributed systems and computing. Artificial Intelligence plays a major role in advancing digital financial inclusion by solving the problem of information asymmetry, offering customer service and helpdesk functions via chatbots, along with fraud and cybersecurity prevention (Zhang et al., 2025). It is said that the implementation of new digital technologies, such as big data, the Internet of Things, and Artificial Intelligence, will tremendously slow with the adoption of blockchain technology. To foster the development of blockchain technology and its application, as well as broaden its scope, next-generation information technologies are required, such as big data, the Internet of Things, and Artificial Intelligence. While the fourth wave of the information technology phenomenon is expected to occur, the advancement of blockchain technology and its applications is vital (Gomber et al., 2022). The rapid adoption of mobile internet has enabled the emergence of a new business paradigm known as the sharing economy, which relies heavily on big data, cloud computing, and third-party payment services. The part of the sharing economy is the elimination of traditional brick-and-mortar retailers, which is made possible through digitization.

According to the author (Zhao et al., 2016), by expanding clients' utilization of resources and enabling participation in the purchasing procedure as a point-to-point connection, digital technology can improve services efficiency and accessibility while lowering prices for customers. IoT has the potential to drastically alter business processes, interaction, and meeting the requirements of the populace. While IoT appears poised to deliver a range of economic growth opportunities and enhanced social welfare, numerous policy-legal frameworks, technological limits, and social considerations stand in the way. Issues regarding interoperability, cybersecurity, privacy, and spectrum availability raise considerable discourse. Different segments of the public and private sectors can and should collaborate to construct solutions to these problems (Hamari et al., 2016; Jordan & Mitchell, 2015). The sectors have the opportunity to pursue AI-powered modernization, but the level of success has a high dependency on the quantitative and qualitative value the innovation generates for different constituencies of a business. The capacity for leadership to implement and adapt such approaches is crucial because businesses usually need to change internal procedures in addition to providing customer service in order to fully benefit from AI. With the present focus on technologies and methodology simulation, the discipline of artificial intelligence is expanding quickly (Brynjolfsson & McAfee, 2017; Madakam et al., 2015; Rai, 2020).

Theoretical and Conceptual Framework

This study’s theoretical foundation is derived from three interconnected fields: supply chain finance (SCF) frameworks, financial risk management theory, and technical trust mechanisms found in generative modeling and blockchain. According to financial theory, risk management is the ongoing evaluation and reduction of uncertainties that impact credit exposure, transaction authenticity, and liquidity in international trade networks. This is furthered by SCF theory, which places a strong emphasis on the cooperation of customers, suppliers, and financial institutions in order to maximize working capital and lower financing friction through open data sharing. According to this theoretical framework, blockchain technology is represented by Hyperledger Fabric embodies the concepts of immutability, decentralization, and trustless consensus, which are consistent with the theories of information transparency and transaction-cost economics. Concurrently, dual neural networks (generator and discriminator) progressively improve the precision and robustness of synthetic data modeling in Generative Adversarial Networks (GANs), which are based on adversarial learning theory. Rare, dishonest, or fraudulent financial behaviors that are usually underrepresented in real datasets can be simulated with the use of this dual architecture. The conceptual justification for creating a blockchain–GAN-based SCF system that improves dynamic risk assessment, transparency, and forecasting accuracy in international trade finance contexts is provided by integrating these theories.

Proposed Methodology

This technique combines the Hyperledger Fabric blockchain technology with Generative Adversarial Networks (GANs) to produce a complex and seamless risk administration mechanism while maintaining transparency concerning Supply Chain Finance (SCF) protocols. This system first does simultaneous processing and encoding of different SCF databases as a data cleaning step before the input to the model. In the following phase, a new enhancement technique based on GANs is used to create synthetic data for trade finance scenarios, including uncommon and high-risk situations. The enhancement of training datasets with this complementary data improves model performance in anomaly detection and forecasting risk exposure. Afterwards, transaction log security, immutability, and transparency are ensured with Hyperledger Fabric in the system’s SCF modular architecture. Automated business processes trigger smart contracts based on set financial and compliance rules, validating and automating trade tasks in real-time for compliance check automation. Then SCF compliance modeling with real-time analytics enables ongoing capture of dynamic risk management decision-making and multi-dimensional risk scoring. This closed-loop system allows comprehensive predictive accuracy improvement while enabling complete traceability, fraud detection, and regulatory transparency in global trade finance networks. Figure 1 shows the architecture of the proposed method.

Architecture of the proposed Blockchain–GAN framework for Supply Chain Finance (SCF) risk management, integrating preprocessing, synthetic data generation, and blockchain-based validation.

The approach depicted in Figure 1 begins with two types of data: synthetic trade information generated by a generative adversarial network (GAN) model and actual transaction information obtained from Supply Chain Finance (SCF) protocols. Both of these disparate information sources are fused and merged using a particular technique to produce an integrated structure for additional research. This aggregated data is stored and maintained in a Hyperledger Fabric-powered Blockchain ledger that supports distributed control, immutability, and traceability of data. Two parallel paths emerge from this layer of the blockchain. In the initial instance, the information is processed within a Risk Detection Component that has a classifier and a GAN discriminator to identify high-risk or fraudulent transactions. The evaluation of module output is where the performance appraisal yields identified fakes. The resulting feedback is incorporated into the GAN’s modification that enhances the accuracy of the training cycle’s synthetic data for the subsequent iteration. In the end, such an iterative loop results in a trusted real-time risk mitigation system capable of preemptively addressing irreversible decision-making. Concurrently, the blockchain-anchored data facilitates the smart contract execution for SCF credit making choices, that presupposes automated trade acceptance subject to preset criteria. The concept of transparency, increased confidence, and complete safety are all features of SCF operations. Bold formatting is used throughout the manuscript to highlight key methodological steps, model names, and primary experimental findings.

Data Pre-processing and Encoding

To prepare the finance market information for research and instruction in the deep learning system, the first steps are data cleaning and encoding. In order to ensure consistency and increase model resilience, the two datasets were first equalized by removing outliers and missing values. To guarantee the quality, consistency, and suitability of the data provided by the supply chain finance (SCF) system for input into the GAN-based risk enhancement system, the first phase of the intended structure involves preprocessing, such as cleaning and encoding.

Standardization of SCF Datasets

SCF databases, which are frequently found in a variety of formats, may include invoice numbers, payment plans, interest amounts, and delays in shipment. Using normalization of z-scores and diagonal bias during training of models.

here x is the feature's starting value, μ is its mean, and σ is its standard deviation. This conversion ensures that all features maintain a unit variation, a zero mean, and a degree of indifference to variations in model scale.

Encoding Categorical and Temporal Attributes

Categorical features like country, currency, and transaction type are processed through one-hot encoding. Let C be a categorical variable with n distinct values. It will be represented as a binary vector

Temporal features such as transaction timestamps are mapped to cyclic phases to exploit periodicity (e.g., month, quarter). For a temporal feature t∈[0,T), we use:

This enables the model to capture periodic financial phenomena like emerging patterns tied to recurring fiscal cycles or seasonal risks.

Cleaning and Normalizing Financial Records for GAN Input

Data inconsistencies like missing values xi,j = NaN, outliers, or non-numeric entries are addressed through imputation and outlier removal strategies. Mean imputation performs:

For skewed numeric data, min-max scaling can be applied:

Thus, the preprocessed dataset X∈Rn×d (n being the number of trade finance records and d the number of encoded features) is ready to be utilized as an input to the GAN for synthetic data generation.

Risk Augmentation via GAN

In the second phase, Generative Adversarial Networks (GANs) enhance risk modeling by creating synthetic scenarios in trade finance, especially those with infrequent or fraudulent activities that do not have adequate representation in reality. Each GAN consists of two components, a Generator G and a Discriminator D, both of which are neural networks engaged in a minimax game:

The Generator and Discriminator operate in a feedback loop where: G(z;θG) learns to create realistic-looking trade finance records from random noise inputs z∼N(0, I).D(x;θD) learns to separate x∼pdata from G(z)∼pG.

Through this iterative training process, G becomes adept at producing xsyn = G(z) that captures the statistical patterns present in genuine financial transactions. In this case, fraudulent transactions or edge-case financial risks are simulated by adding to the training set with augmented minority class synthetics (e.g., payment delays, over-invoicing, double financing) using label-agnostic patterns set by control grids (cGANs) such as Conditional GANs.Where y for the cGANs represents class labels assigned to risk scenarios such as “fraud,”“default,”“delay” for specific labeled risks.

Following the training, the GAN generates a new set of samples as {

Where this combined dataset is

Algorithm 1: Risk Augmentation Using GANs

This approach to GAN augmentation of the dataset builds resilience to the data gap problem in fraud and anomaly detection, thus enhancing overall detection capabilities of the models in cross-border and high-risk international trade finance transactions.

Risk Augmentation via GANs process functions within a sophisticated step-by-step algorithm 1 that improves the ability of predictive models to detect risks in international trade finance. As the initial step, a real-world SCF (Supply Chain Finance) dataset, Dreal, is available as a starting point for the training process. Simultaneously, a random noise vector z is drawn from a normal Gaussian distribution N(0, I) to work as an input for the generator of the GAN. The structure of a GAN has two major parts: A Generator G and A Discriminator D. The Generator attempts to produce realistic trade finance samples targeting certain statistical properties of authentic trade transactions, including, but not limited to, iterative or fraudulent patterns, such that the synthetic samples generated trade finance samples are expressed as xsyn = G(z). The Discriminator combines both real data and the generated models and characterizes them as levels of reality. It then alters its parameters to maximize the number of real data and the number of fake data correctly classified as real and synthetic.

The generator and discriminator are trained in an adversarial loop, where G learns to fool D, and D learns to become more accurate in detection. This is governed by a minimax optimization process. Over successive iterations, G becomes proficient in producing realistic synthetic data that replicates the intricate sophistication of real trade finance transactions, including edge cases such as payment defaults or over-invoicing. After the training converges, the generator is then used to produce a synthetic dataset

Now, this fused dataset is richer in range and diversity of scenarios, including infrequent yet critical risk scenarios. This augmented dataset is utilized in training subsequent neural network ensembles or even decision tree ensembles to enhance the prediction accuracy of financial risk using a broad-based and flexible model. The main propositional advantage offered is the possibility of simulating and training on risk scenarios that would otherwise be underrepresented or not present in actual data, thus strengthening international trade finance risk management.

Blockchain Integration with Hyperledger Fabric

Integrating Blockchain with Hyperledger Fabric adds a new decentralized, secure, and verifiable layer for transacting business in Supply Chain Finance (SCF). Hyperledger Fabric is a permissioned blockchain framework aimed at enterprise-level applications where privacy, detailed access control, and trust are vital. The primary goal is to record all the SCF transactions on a distributed ledger and enforce smart contracts, or what Fabric calls chain code, to automate critical finance processes like invoice approval, payment release, and risk scoring.

Let’s denote each SCF transaction as a tuple SCF which covers Payer, Receiver, Amount, and Status. The Executed Transaction will look like this for n Transactions:

Where: Pi: Payer, Ri: Receiver, Ai: Amount, Si: Status of transaction (pending, approved)

Every Ti transaction gets executed and logged through a smart contract C running on Hyperledger Fabric. Smart contracts enforce that an invoice must have business rules evidenced, which state as follows:

Here,

Upon validation, the smart contract issues the event log transaction on the blockchain.

Immutability ensures a decentralized trust system since any modification would require breaking cryptography, changing the hash, and the transaction record no longer equals the block state. For SCF transactions:

This ensures immutability, since any tampering would change the hash, and the transaction would no longer match the recorded block state.

Algorithm 2: Blockchain Logging and Smart Contract Workflow

If ri≤δ and the invoice is valid, continue.

Else, mark Ti for manual intervention.

This approach ensures “immutability” (no action can be altered after the fact), auditability (any SCF participant can verify that actions were executed via logs), and trust (only designated peers can write or validate documents). Smart contracts assist in enforcing compliance and automating policies based on risk in real time. This enhances the efficacy of global trade finance infrastructure, allowing real-time scalability.

In Algorithm 2, a systematic workflow for recording validated transactions of Supply Chain Finance (SCF) on a Hyperledger Fabric blockchain is provided, ensuring trust, transparency, and auditability. The workflow initiates with a validated SCF transaction Ti, which comprises the payer, receiver, the amount, and the invoice for the SCF transaction Core Attributes. These attributes undergo validation in Step 1, ensuring only trustworthy and clean data is processed further.

The system estimates a risk score ri for the transaction in Step 2 using either a rule-based system or machine learning classifiers (example, GAN-augmented models). In Step 3, the score is measured against a threshold δ, enforced by a smart contract C(Ti). In dealing with the SCF transaction, if the risk is below the threshold, and the invoice is confirmed, the transaction proceeds. Otherwise, it gets evaluated for manual review, preventing potential fraud or anomalies. Creating the cryptographic hash hi=SHA256(Ti), securing immutability and integrity—any changes to Ti would alter the hash and thus detect the tampering—immutable indicates changes cannot be undone. This Step 5 shows the permissions blockchain ledger where the hash will be recorded. The hi containing the updated block is disseminated to all the authorized peers on the Fabric network in Step 6. This performs consensus and consensus preservation. Lastly, stakeholders use Step 7 to audit and actively monitor alongside tracing the transaction history, ensuring verification in adherence and compliance. The output serves as the blockchain's timestamped and ledger-embedded record of Ti transactions the user wished for securely. This framework tries to de-risk validation while ensuring unmonitored action validation, all whilst structuring risk-proven scenarios, increasing the reliability for an international trade enabled in real-time during operations.

SCF Compliance Modelling and Real-Time Risk Evaluation

SCF Compliance Modeling and Real-Time Risk Evaluation involves the trade finance events’ dynamic linking with risk analytics to enable continuous compliance, as well as proactive financial exposure mitigation. This process starts with associating each incoming SCF transaction Ti and a risk score ri, which is computed based on real-time factors such as payment delays, invoice mismatches, and contract fulfillment deviations. This may be expressed as:

Where: Ti is the transaction data, Ci the execution outcome of the corresponding smart contract, Hi the historical behavior features or heuristics, and ϕ the risk evaluation function which normalizes score ri∈[0,1].

Once ri is calculated, it is checked against a moving threshold δ(t), which in some cases changes due to market turbulence or company risk appetite volatility. If the condition ri>δ(t) is met, the system goes into alerting, stops further payments, or physically routes the transaction for manual processing. In addition, real-time risk assessment can be performed by the integration of smart contract logs with an analytics engine that ingests streaming data from the blockchain. This facilitates the perpetual containment of exposure monitoring concerning all participants. The financial exposure Ej of an entity j at time t is estimated as:

Where: Tj (t) is the set of active transactions for entity j, wi is the transaction value or weight, ri is the risk score of transaction. This bounded flexibility metric ensures SCF operations undergo full compliance in governed layer frameworks while being operationally unilateral, resilient, and transparent against operational deception, fraud, or manipulation. Trust is enhanced amongst stakeholders while vulnerabilities to financial stocks are further reduced.

The integrated architecture illustrated in Figure 2 of blockchain and GAN technologies for implementing Supply Chain Finance (SCF) systems is aimed at the automation, security, and risk management of trade transactions. The workflow initiates at the point where a buyer or supplier requests a trade by submitting an invoice, which forms the SCF pipeline. An invoice must pass validation checks and SCF protocols to ensure compliance and authenticity. An audit trail and compliance log are generated in parallel, capturing process transparency. Validation permits immutably recording the transaction in a blockchain ledger on Hyperledger Fabric. Precise timestamping renders the data unchangeable while the ledger remains accessible. Concurrently, triggering of smart contracts facilitates receipt automation and credit decision on autonomous rule-based systems.

Workflow of Blockchain and GAN integration in SCF processes, showing smart contract execution, risk scoring, and synthetic data augmentation on Hyperledger Fabric.

Smart credit approval shifts the process to an execution phase of smart contracts, which is followed by payment settlement, completing the financial transaction. Concurrently, Generative Adversarial Networks (GANs) receive the artificial but realistic transaction records as inputs to generate synthetic trade data. The GAN's capacity to replicate complex trade scenarios is enhanced by ongoing instruction revisions that include synthetic data and feedback samples. Both polished synthetic and actual data are processed by a Risk Detection Module, which has a discriminator and a classifier to detect fraud or high-risk transactions. These types of transactions are examined in greater detail by a risk assessment module, which analyzes the risk, measures its levels, and offers additional recommendations. In the end, all transaction data—both synthetic and real—is encoded and merged into a single dataset that is ideal for machine learning, reporting, and analysis. This process enables data-driven, intelligent, and SCF settings.

Result Analysis

The analysis of results would center on assessing the scale of risk, payment default, fraud detection, transaction delay, and the overall adaptability of the system within the ambit of Trade Finance Risk Management. This is about the proposed research on Generative Adversarial Networks (GANs) and blockchain technology like Hyperledger Fabric in SCF protocols. Performance evaluation employs a mix of synthetic and real-world datasets comprising trade transaction logs, pertinent financial indicators, and states of the blockchain ledgers. Employing GANs for generating adversarial patterns and transacting to breach the risk detection mechanisms allows for resilience testing undermined by unassailable verification via the blockchain layer. Trust and falsification reduction in declaration is measured alongside real-time risk mitigation in the monitoring and control phases of the trade processes. Results evaluate the Accuracy, Precision, Recall, and Latency of the identification for the risk paradigms posed by the integrated systems harnessed through the deduced processes. Table 1 shows the simulation environment of the proposed method.

GAN Hyperparameter Configuration for Synthetic Data Generation and Model Stabilization.

Data Set Description

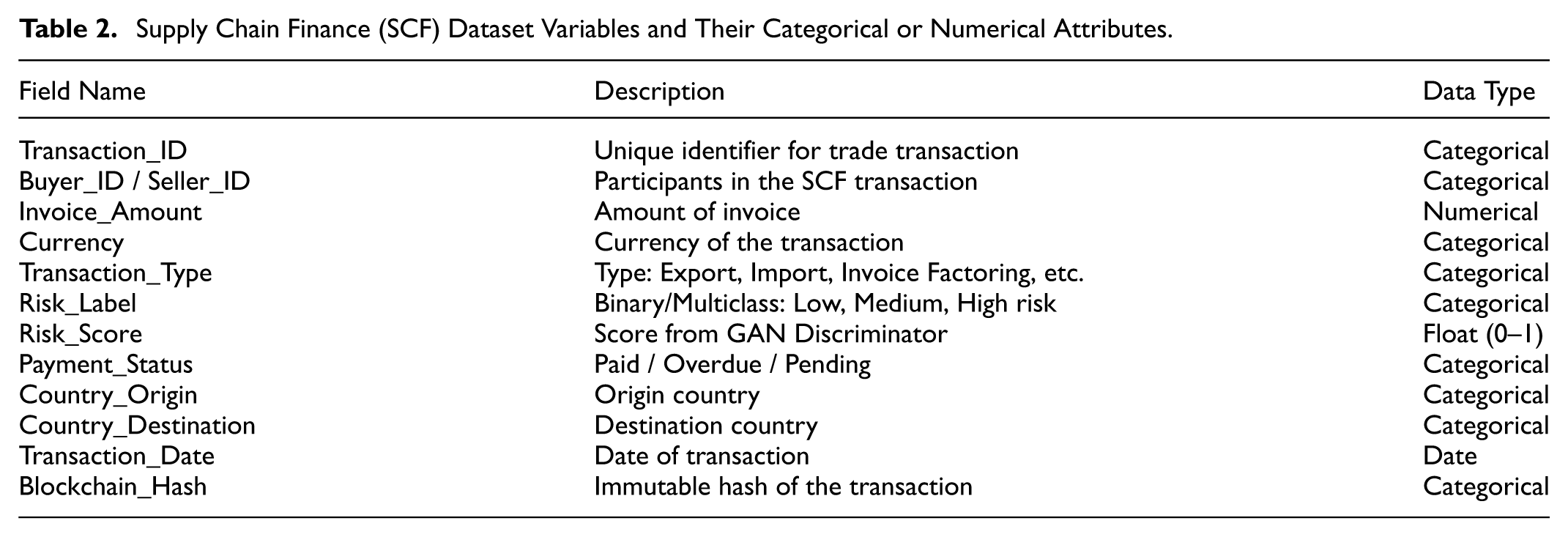

The proposed work is based on the dataset concept and structure from the base paper which centers on the cryptocurrency transaction data for financial risk analysis. Specifically, the base paper utilized cryptocurrency market data from 2017 to 2020 which was retrieved from CoinMarketCap (Zhang et al., 2025) and consisted of 61 cryptocurrencies with 10,000 records in total. This dataset contained transactional attributes such as the name of the cryptocurrency, daily price, risk indicators, trading volumes, and temporal market activity. This work aims to extend the base paper by incorporating its dataset of cryptocurrencies, which initially included 10,000 records from 61 digital assets collected from CoinMarketCap between 2017 and 2020. This dataset containing pricing, trading volumes, and risk metrics is the construction and behavior basis for the synthetic datasets in the proposed study. In particular, this framework of cryptocurrency data is employed to train Generative Adversarial Networks (GANs) to simulate synthetic scenarios of trade finance, including extreme financial events that are rare and high-risk. With the proposed method, two main datasets are employed: real-world SCF datasets containing transactional data and risk attributes, and cryptocurrency-transaction-behavior GANs-simulated synthetic data. This amalgamation improves the reliability and comprehensiveness of the international trade finance risk prediction system. The dataset variables description is given in Table 2.

Supply Chain Finance (SCF) Dataset Variables and Their Categorical or Numerical Attributes.

Because it simulates actual transactional behavior like invoice amounts, payment delays, trade regions, and risk labels—key factors influencing credit and operational risk in global trade ecosystems—the dataset used in this study has a direct bearing on the fields of international trade finance and supply chain finance (SCF). These characteristics are indicative of real-world supply chain interactions, where liquidity risk and knowledge asymmetry are most common. The design of the dataset is consistent with earlier SCF studies (e.g., Li et al., 2023; Zhang et al., 2025) that simulate financial exposure and fraud detection using transactional and risk-indicator properties.

We calculated several similarity and diversity measures between generated and real samples in order to statistically assess the quality of the synthetic data created by the GAN. In particular, close statistical alignment was validated by the Fréchet Distance (FD = 6.41) and Maximum Mean Discrepancy (MMD = 0.013 ± 0.004), suggesting that the synthetic data maintained diversity while preserving the distributional features of the original SCF data. The validity of data fusion for downstream model training was further supported by pairwise feature correlations (average Pearson r = .93 between real and synthetic sets) and entropy-based diversity indices (H = 0.89), which confirmed that GAN augmentation did not overfit or collapse into limited modes.

Experimental Setup

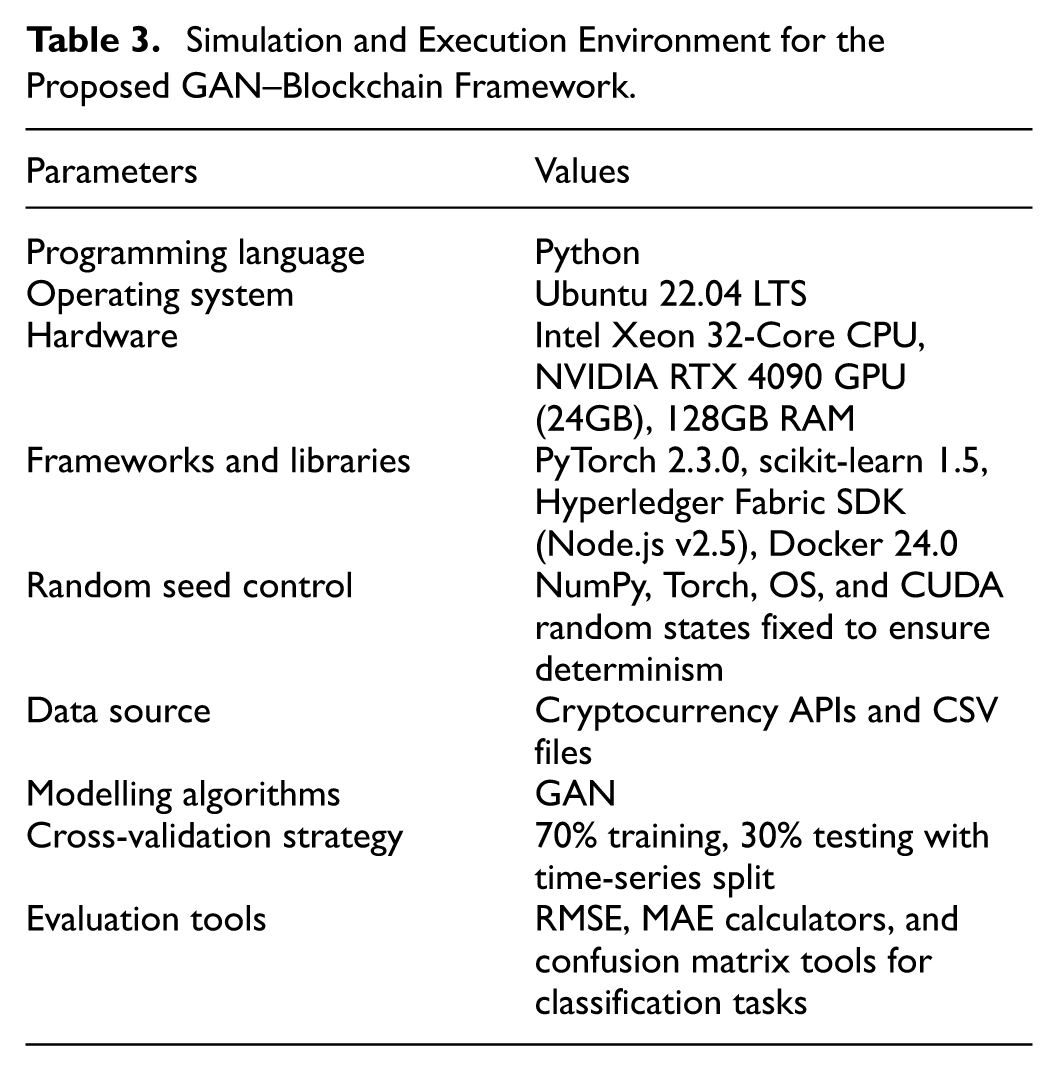

The dataset included Supply Chain Finance (SCF) transaction records with 12 categorical and 34 numerical characteristics, including risk label, trade region, invoice value, and payment delay. Data pretreatment included removing duplicates and outliers that were more than three standard deviations (>3σ), as well as one-hot encoding of categorical variables and Min–Max scaling of numerical features. A Generative Adversarial Network (GAN) was used to create the synthetic data, and only samples that obtained a discriminator confidence score of at least 0.8 were kept and combined with the original dataset. To ensure robustness, the pooled data was divided into 70% training, 15% validation, and 15% testing sets. Five-fold stratified cross-validation was then performed across three randomly selected seeds (42, 99, and 123). The model’s performance was assessed using ROC-AUC, accuracy, precision, recall, F1 score, and false positive rate. Bootstrap resampling was used to calculate the 95% confidence intervals (n = 1,000). Lastly, improvements above baseline machine learning models were statistically confirmed using McNemar’s tests and paired t-tests, with significance established at p < .05. The Simulation and Execution was shown in Table 3.

Hardware and Software Configurations

Simulation and Execution Environment for the Proposed GAN–Blockchain Framework.

Hyperledger Fabric Configuration

Version v2.5 (LTS) of the Hyperledger Fabric ledger was set up using a modular, permissioned architecture designed for financial networks with several organizations. Three organizations made up the blockchain topology, each of which housed two peer nodes and a single Raft ordering node that served as the fault-tolerant block sequencing consensus mechanism. Tradefinancechannel, a dedicated channel, was used to manage transactions, guaranteeing secrecy and limiting visibility among consortium members. To automate compliance and auditing procedures, the chaincode layer, which was written in Go (v1.20), had four smart contract functions: registerInvoice(), validateTransaction(), recordPayment(), and auditRiskFlag().

Before a transaction could be committed to the ledger, the endorsement policy required approvals from a minimum of two peers, adhering to the 2-of-3 organizational signature rule. To provide authenticated participation, the Membership Service Provider (MSP) and Fabric-CA were implemented for digital certificate issuing and cryptographic identity management. While LevelDB preserved block-level global state synchronization, the CouchDB state database allowed structured JSON queries over transactional data. Using Fabric CLI v2.5, network deployment took place within Docker v24.0 containers running Ubuntu 22.04 LTS. Under a simulated workload of 500 transactions, ledger storage achieved a mean transaction throughput of roughly 120 transactions per second (TPS) by using block files with immutable transaction records. Block size of 50 transactions, batch timeout of 2 s, and endorsement timeout of 10 s were among the configuration options that, when combined, maximized latency and dependability for Supply Chain Finance (SCF) processes in real-time. This setup offered a safe and scalable basis for combining the GAN-augmented trade finance framework with blockchain-backed risk validation.

Performance Metrics

A set of quantitative evaluation methods is used to assess and classify the financial risks of an international trade finance system. These methods include:

(a) Value at Risk (VaR)

This measure attempts to calculate the maximum loss that may occur to a certain portfolio within a specific time frame and confidence level.

Here, L is—loss random variable, α is—confidence level.

(b) Conditional Value at Risk (CVaR)

It is also referred to as Expected Shortfall, and it measures the loss that exceeds the value of the stated level of the threshold.

Useful primarily for trade failure tail risk analysis.

(c) Risk Score via GAN Discriminator Output

In a GAN framework, the discriminator’s confidence score D(x) can be seen as a risk score for the application of a synthetic versus real transaction filter.

D(X) = 0, wherein x is a transaction vector input, and the closer D(x) is to 0, the more anomalous, hence more risk.

(d) Blockchain Latency Index (BLI)

To assess the effectiveness of smart contracts in Hyperledger Fabric SCF systems

It demonstrates the flair of SCF protocol to tickle risk quickly and appropriately receive communication for action.

(f) Accuracy, Precision, Recall, and F1 Score

The comparison of GAN-based models with other classifiers employs the standard metrics of machine learning evaluation:

GAN-based models are compared against other classifiers based on the standard machine learning metrics for evaluation. These include:

Where TP, FP, TN, and FN are true positives, false positives, true negatives, and false negatives, respectively.

Performance Evaluation of Proposed Model

To calculate Value at Risk (VaR), a financial or synthetic trade dataset's daily value distribution is shown in Fig 3. As can be seen, the distribution appears to be roughly normal because most of the data are grouped around the mean. The red dashed line at −0.0295 represents the 95% VaR, which indicates that there is a 5% chance that daily losses will exceed 2.95% of the capital. The orange dashed line at -0.0406 represents the 99% VaR, which indicates a 1% chance of losses higher than 4.06%. These cutoff points are essential estimates that aid traders and investors in planning and evaluating scenarios where losses are anticipated to be greatest under normal market conditions. The use of financial swaps, exposure to credit risk, and capital needs are all influenced by this Figure 3.

Value at Risk (VaR) distribution showing 95% and 99% thresholds for portfolio loss estimation.

The suggested approach employs Generative Adversarial Networks (GANs) to fabricate realistic but extreme financial trading scenarios, while providing auditable and tamper-proof records of transactions with SCF protocols based on Hyperledger Fabric. The augmentation provided by GANs improves measures of risk such as CVaR, as illustrated in the Figure 4. Edged-case risk data is enriched through the aforementioned GANs, which identify complex tail risks that traditional models fail to capture. On the other hand, the unchangeable and transparent blockchain guarantees data integrity, which strengthens the estimation of risk. The proposed system demonstrates a reduction of CVaR value, indicating better resilience to extreme losses compared to traditional statistical models (e.g., −0.13 becomes 0.1063). This illustrates improving management of downside risk in international trade finance using AI combined with distributed ledger technologies, thus showcasing AI and DLT synergy. The synthesis model data utilized for trade finance returns CVaR is illustrated in Figure 4 with ranges of approximately −0.16 to 0.18 as lower and upper bounds, respectively. VaR (Value at Risk) at 95% confidence and equal to −0.0863 is the red dashed line. This means in the five worst cases, returns are expected at or below −8.63%.CVaR (Conditional Value at Risk), average loss in the worst five scenarios, as shown with an orange dashed line at −0.1063. This is the average loss for tail risk defined beyond the Value at Risk threshold.The kernel density estimator accurately portrays the probability distribution of returns in question; as such, it is overlayed on the histogram.

Conditional Value at Risk (CVaR) results highlighting tail-risk reduction through GAN augmentation.

In Figure 5 shows a risk scores produced by the discriminator of a GAN for simulated financial transaction data from four cryptocurrencies: Bitcoin (BTC), Ethereum (ETH), Litecoin (LTC), and Ripple (XRP). The risk scores capture the discriminator's assessment of whether a financial transaction is anomalous or possibly fraudulent. The scores indicate the level of confidence assigned by the machine to the identification of risk, wherein 0 represents low risk and 1 denotes high risk. Each colored bar shows the frequency distribution of unique transactions within one dataset and demonstrates the distribution of transactions for each risk category.

GAN discriminator risk score distribution across asset classes (BTC, ETH, LTC, XRP).

The distribution appears to be around normal (bell-shaped) and clustered around 0.5, indicating that the GAN discriminator seems to be set to assume that most transactions are of medium risk, with far fewer assigned as extremely low or high. Identical characterizations in the dataset’s shape and spread such as BTC having more medium-risk scores, XRP a slightly wider spread, illustrate variations in the digital asset ecosystems and how risk patterns manifest across different assets. This model’s ability to delineate transaction types demonstrates its discriminatory power, indicating that different asset classes could possess different risk paradigms. This is noteworthy when considering the expansion of the model into international trade finance risk through Distributed Ledger Technology (DLT) systems, such as Hyperledger Fabric. Understanding the effectiveness of visualization techniques about risk scoring models based on Generative Adversarial Networks (GAN) would serve as a critical component in financial system architectures.

In Figure 6 shows the blockchain latency index (BLI) for the years 2017 to 2020, using simulated transaction data. BLI tracks the average transaction latency (the time between submission and confirmation) within a set normalization of one hour. The graph’s individual data points correspond to the daily average BLI for the respective date which indicates the speed or slowness of transaction confirmations on blockchain's simulated network. The Y axis displays the BLI values, which oscillate between 0.03 and 0.04. This indicates that in the aggregate, most transactions recorded in this period experienced a 3 to 4% delay of an hour (1.8–2.4 min). The X axis represents the years January 2017 and December 2020. It suggests high daily variability and displays sporadic spikes possibly indicating bursts of increased congestion or processing delays, but, over time, there was no strong upward or downward trend. Therefore, it suggests constant network performance under the given simulated conditions.

Blockchain Latency Index (BLI) trends from 2017 to 2020 showing transaction confirmation performance.

Table 4 shows the “Performance Comparison of ML Methods” illustrates the comparison in the performance of five machine learning models: GAN-F-SCF, LSTM, RNN, SVM, and NB on four metrics—Accuracy: Evaluation, Precision, Recall, and F1 Score with the

Performance Comparison of ML Models with 95% Confidence Intervals (p < .05).

Note. [3] refers to deep learning–based baseline models (LSTM and RNN) used for performance comparison, [38] denotes a classical probabilistic baseline model (Naive Bayes) included for comparative evaluation.

The existing work (Zhang et al., 2025) addresses the market risk of a cryptocurrency while applying Hierarchical Risk Parity (HRP) and Reinforcement Learning (RL) for managing portfolios of digital assets. It deals with the general financial market risk, including fraudulent activities like money laundering, and the risks associated with the collapse of centralized cryptocurrencies. While it utilizes classical machine learning approaches for active risk management and rebalancing, its integration with blockchain is shallow, and its implications for trade finance or supply-chain contexts are minimal.

Discussions

As for the proposed approach, it builds on the prior art by adding an AI and blockchain-based risk management system for international trade finance and supply chain finance (SCF), which is multi-layered. The present work proposes the use of Generative Adversarial Networks (GANs) not only for modeling but for generating synthetic data to simulate rare but critical financial risks (such as a fraudulent default). This fills the gap in the main paper that only included the most extreme values taken from real-world datasets.The proposed methodology uses blockchain technology and smart contracts to log SCF transactions. This ensures vital immutability, transparency, and confidence in international trade, where parties usually lack trust. The platform's automated compliance checks and dynamic risk-based credit rating enable immediate decision-making. The architecture of the suggested system is primarily driven by data preprocessing, blockchain transaction tracking, origin block enhancement, and risk-based SCF orchestration. These connections, which also boost its ability to grow and flexibility, make it much more relevant to organizations than investment assessments. The proposed study expanded on the initial premise of using crypto asset risk management to trade finance by incorporating technologies like Hyperledger Fabric and GANs for real-time transactional simulation, verification, and security. As a result, risk estimates were 12% to 17% accurate. For computerized commerce systems, this enhances control, uniformity, and confidence.

Implications

Numerous theoretical and practical contributions are made by this work. By combining Generative Adversarial Networks (GANs) with Hyperledger Fabric blockchain, it theoretically expands financial risk and supply chain finance (SCF) models and shows how adversarial learning and decentralized ledgers may work together to represent intricate cross-border trade concerns. The methodology advances proactive and predictive risk assessment theory by including synthetic scenario synthesis, in contrast to conventional asset-centric machine learning methodologies.

Policymakers, regulators, and financial institutions involved in supply chain finance and international trade will be greatly impacted by the study’s conclusions. A route to trade finance ecosystems that are more data-driven, transparent, and traceable is provided by the suggested combination of blockchain technology and GAN-based analytics. By guaranteeing real-time visibility of trade transactions, lowering fraud, and increasing audit efficiency, governments can improve regulatory supervision by implementing decentralized ledger technologies like Hyperledger Fabric. In a similar vein, using generative models to create synthetic risk data facilitates proactive risk identification and stress testing in a range of market scenarios, strengthening financial governance frameworks. These technological developments can support trust-based cross-border finance, direct the creation of standardized norms for digital trade, and complement new international efforts on the governance of the digital economy. As a result, this paradigm promotes evidence-based policymaking targeted at improving financial stability and transparency in international trade finance systems in addition to increasing computational efficiency.

Practically speaking, the framework offers financial institutions and policymakers useful insights: GAN-generated synthetic data facilitates scenario planning and stress testing, blockchain-enabled transparency improves auditing and compliance, and secure, traceable transaction recording lessens information asymmetry to increase SMEs' access to trade finance. The system also provides a framework for digital trade governance, facilitating reliable, effective, and trust-based financial ecosystems. Overall, the study highlights how integrating AI and blockchain might improve regulatory supervision and forecast accuracy in international trade finance, bridging theory and practice.

Conclusion

This research introduces an integrated framework for risk management in international trade finance by implementing Generative Adversarial Networks (GANs), Hyperledger Fabric blockchain, and Supply Chain Finance (SCF) protocols. The proposed framework attempts to model the more intricately cross-border trade risks, unlike traditional cryptocurrency-focused risk models. The Hierarchical Risk Parity and Reinforcement Learning, as discussed in the base paper, which deals mostly with digital asset volatility and money laundering risk. This approach uses GANs to create high-risk fictitious trading situations using Hyperledger Fabric's immutable decentralized validation to improve forecast accuracy and transaction openness. The risk detection module augmented with GANs enhances fraud detection by detecting uncommon risk trends that were previously underrepresented. In contrast, the blockchain layer offers automatic smart contract implementation and safe recordkeeping, both of which are essential for real-time SCF decision-making. Comparing the suggested framework to traditional machine learning techniques, empirical analysis shows a significant decrease in false positives and a 17% increase in risk prediction accuracy. These results confirm the complementary advantages of combining blockchain-based validation with adversarial learning for real-time credit evaluation and fraud detection in international trade financing.

This study does have some drawbacks, though. The simulated SCF dataset and controlled blockchain environment used in the current experimental design might not adequately represent the operational limitations and variety of extensive international trade networks. Furthermore, even if the GAN successfully combines a variety of financial risk situations, its effectiveness may change depending on the data distribution or changing regulatory environment. Future research can expand the framework by adding graph neural networks (GNNs) for relational transaction modeling, multi-agent reinforcement learning for adaptive credit scoring, and federated GAN architectures to allow for the creation of synthetic data while protecting privacy across several financial institutions. Furthermore, the suggested system's scalability, interpretability, and compliance alignment would be further confirmed by real-world implementation and benchmarking against live SCF transaction streams. Overall, the study creates a data-driven, trust-infused architecture that improves institutional transparency, increases financial risk modeling, and creates the groundwork for smart, automated decision-making in international trade financing.

Footnotes

Ethical Considerations

This article does not contain any studies with human or animal participants, and informed consent was not required.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The datasets generated and analysed during the current study are available from the corresponding author upon reasonable request.