Abstract

The Insurance industry participates in various processes that are characterized by data exchange, which is modified or updated by many parties. Hence, the insurance industry can benefit from the adoption of blockchain technology. However, there is a lack of understanding of the technology, the legal implications and the issues in implementing the technology. This paper aims at finding potential opportunities for the insurance sector on the implementation of blockchain technology. It also discusses issues and concerns for insurance companies wanting to adopt block chain technologies. A search was carried out for relevant electronic bibliographic databases (searched by means of keywords), articles published in scientific journals, websites of consultancy firms and blockchain developers, and reference lists of relevant review articles. Articles were screened and eligibility was based on participants, procedures, interventions comparisons, outcomes (PICO) model and criteria for PRISMA (Preferred Reporting Items for Systematic Reviews). A total of 23 papers were finalized after scrutiny for this study whereby the results disclose that blockchain, as a single source of reality, has the potential to improve productivity and mitigate the complexity of the insurance processes. Examples of real-world applications and insurance use cases are presented to demonstrate the strengths & capabilities of the technology. This study also considers the present-day issues, risks and concerns in the implementation of the blockchain technology. Finally, the challenges and obstacles in the application of Blockchain technology in the Insurance Sector is highlighted and presented.

Keywords

Introduction

The world is gradually switching to digitization where many businesses have recently begun researching blockchain technology for adoption in their business processes. In the recent years, scores of industries are spending time and money on learning about the viability of blockchain and the effect of its adaptability in the organization (Kantur & Bamuleseyo, 2018; Nizamuddin & Abugabah, 2021). Whilst many have anticipated innovations namely big data, social media, cloud computing, and artificial intelligence to shape and influence the next decade of business, Blockchain is the most disruptive of all in the numerous industries of the world economy like finance and banking, health care, manufacturing, e-commerce, and food sectors. Skepticism was also expressed concerning blockchain’s real potential (Akande, 2018). Industries like healthcare, pharmaceutical, banking and finance, e-commerce, etcetera, have adopted blockchain to a greater extent which has proved to be a huge success. One particular industry that has not picked up pace in adopting new technologies as compared to other industries, is the Insurance industry (Yu & Yen, 2018). The primary reasons for this could be career advancement within the management and the internal struggles over resources (Knights & Murray, 1992). However, that is about to change. The Block chain Insurance Industry Initiative (B3i) was founded in 2016 as a partnership between insurers and reinsurers to find out how all the different stakeholders in the value chain (B3i, 2017) could benefit from Distributed Ledger Technology (DLT) (Kantur & Bamuleseyo, 2018). Blockchain technology, for instance, can provide more than just a means of generating digital currencies. Blockchain processes can potentially eliminate all third parties, such as banks and governments, who provide the trust in the transactions (Alcazar, 2017).

Blockchain and Smart Contracts are both new phenomenons in the global market as there is limited information on either of the two. As the name entails, a “blockchain” is, in its simplest terms, a “chain” of previously validated transaction “blocks” that constitutes an immutable digital ledger and a distributed, resilient basis for value transfers (Eling et al., 2021). Nevertheless, the pioneering recognition to blockchain has come with an uptick in the attendant speculation. Blockchain technology is threatening to become the “next big thing” and all kinds of blockchain-based projects are being proposed (Kar & Navin, 2021). The idea of smart contracts was introduced by the cryptographer Nick Szabo in 1997, which, in short, enables a user to invoke the terms of a digital contract through an user interface (Szabo, 1997). Smart contracts are fragments of code that are self-executing and stored in the blockchain. The code may, for example, contain certificates, personal data, licenses, or wills. Such smart contracts can be used in all sectors, but those most likely to be disrupted in the next decade are the banking and insurance sectors. It is easy to access it, because the blockchain is public, decentralized, and distributed, and at the same time provides a safe and secure way of storing information (Cuccuru, 2017).

Morabito (2017) argues that falsified claims, labor-intensive processes, fragmented data sources, and legacy underwriting approaches, are the major challenges faced by insurance today. These contribute to low customer satisfaction. Creating policies on the blockchain, such as smart contracts would provide power, consistency and traceability for each claim and may result in automatic payouts.

Every industry needs to keep up with the markets’ dynamic nature in terms of trends and technology in order to survive (Ankitha & Basri, 2019; Grima et al., 2020). Similarly, insurance companies must adapt to modern technologies like AI and blockchain to avoid facing disruption in the market. Blockchain is a new and emerging technology where information is stored on a shared database known as blocks which carries features that makes the stored data “transparent,” “traceable,” “unforgeable,” and “collective maintenance” (Zhao, 2020). Furthermore, blockchain will offer companies new and better types of insurances (health, travel, life, property and casualty, reinsurance or otherwise), fraud detection and risk prevention through smart contracts. Also, minimal labor intensive processes, fragmented data sources, legacy underwriting models, and clearer information on third-party software to name a few (Morabito, 2017). From a customer’s perspective, the handling of insurance claim will be more automated and faster (Nath, 2016).

Although technology has permanently transformed entire industries over the past decade, in many respects the multi-trillion dollar global insurance industry has remained trapped in the past with little customer service advancement or innovation. Many customers still contact insurance brokers by phone to buy new plans, amid the emergence of online brokers. Policies are frequently processed on paper contracts, making claims and payments that are prone to error and often requiring human intervention and oversight. Compounding this is the inherent uncertainty of insurance, including the risk—the key product of insurance, consumers, brokers, insurers and reinsurers. Each phase in this collaborative process is a possible failure point in the overall system, where data can be lost, policies misinterpreted, and settlement times lengthened.

Enter blockchain technology—a form of decentralized record-keeping that is cryptographically secure. Insurance is one of the basic services offered to reduce costs and assist individuals during an emergent situation. Challenges related to liability and authenticity of documents takes a long time to overcome through conventional methods (Shetty & Basri, 2018). Blockchain in this case serves as a simpler yet sophisticated way to reduce various risks involved in an insurance company (Sharifinejad et al., 2020). Moreover, its core element of redundancy, immutable storage, and encryption makes sure that records stored are secure and accurate (Akande, 2018).

Review of Literature

Blockchain refers to the continuous chain of blocks that contain information built according to requirements by adhering to strict governing rules. A blockchain can be comprehended as a ledger or a chronological database of one or many transactions wherein those transactions are stored in blocks (Peters & Panayi, 2016). This trust is built without any influence of a central authority (Benton & Radziwill, 2017), the blocks are written on the chain after consensus among members of the network. The very essence of blockchain is that it is encrypted to be immutable, once the block is written, it cannot be modified or tampered with. More often, multiple copies of block chains are stored on many different computer systems in the form of distributed ledgers, that are independent of each other (Kim & Laskowski, 2018). Several industries in the global market have taken a technologically advanced step by adopting and implementing blockchain for the purpose of transparency and traceability. Blockchain technology provides a decentralized and open platform that allows the creation of a transparent, secure, and robust database (Lipsey et al., 2005); and it’s called a blockchain because it can be interpreted as a chain of blocks interlinked with mathematically determined data using complex algorithms, also known as cryptography. It is an electronic ledger that can be private or public in nature that uses a global peer-to-peer network to offer an open platform in which transactions are recorded chronologically. It allows a distributed transaction which further creates a chain of transactions where all parties involved, trust the system (Bordekar et al., 2019).

The application of information technology to insurance industry has been profoundly debated and discussed. Technologies like Big Data, Blockchain, Smart Contract, etc. are prophesied to dramatically change the functioning of insurance sector and make lives of all parties involved, hassle free (Yu & Yen, 2018). Insurance being one of the fundamental services offered to the citizen of the world, it makes an individual’s life easier. It helps the insured during a situation of emergency and reduces costs. Forging of documents for financial gain, theft of insured property, challenging scenario of proving liability are a few of the challenges faced by an insurance company. Conventional methods of addressing these challenges take a significant amount of time, money, and labor. Compared to other global industries in the market, the insurance industry has been considerably slow to adopt new technologies (Gatteschi, 2018).

Although internet protocols facilitate the exchange of information, blockchain protocols define the online exchange of value. The first group of blockchain technology is blockchain 1.0, a three-layer technology stack consisting of: a decentralized database or ledger that has a history of transactions, a protocol performing financial transactions and a digital currency (cryptocurrency).

Blockchain technology first appeared in a white paper written by a group or person under the fictitious name Satoshi Nakamoto. Blockchain is the underlying infrastructure of the Bitcoin cryptocurrency, a peer-to-peer electronic cash type. Bitcoins can be sent directly from one party to another without the need for a trusted third party like a bank to avoid double spending.

In addition, Blockchain 2.0 consists of contracts, economic, market and financial applications which, beyond cash transactions, use blockchain. Smart contracts, intelligent property, inventories, shares, loans, mortgages, land, and property titles are examples.

Blockchain 3.0 is made up of numerous applications that do not include cash, money, financial markets, trade, or other economic activities. Health, science, digital identity, government, education and different facets of culture are examples of such applications.

Smart Contracts

Smart contracts are a part of blockchain technology that streamlines several processes, which at a given period of time are running across different systems and databases. They are implemented on top of blockchain technology as a platform to make authentication and similar tasks automatic, which can, in case of manual authentication, exhibit a high risk of error or abuse (Deloitte, 2016b). Implementation of such a technology can bring about a drastic change in the insurance industry as offers and policies can be translated to computer codes at will. Cryptographic algorithms and similar sophisticated digital processes are used to protect information like participant identity and personal details, secure transactions and confirm the authenticity of transactions.

Murphy and Cooper (2016) have indicated four main characteristics of a smart contract. These contain the following:

Digital Form—it is about code, data, and program running

Embedded—contractual clauses or functional results are embedded in the software as a computer code

Technologically Controlled Performance—payment release and other acts are allowed by the technology.

When initiated, the effects with which a smart contract is encoded to execute, cannot be stopped unless an outcome depends on an unmet condition.

Therefore, a blockchain based smart contract is a contract between two or more parties that is securely stored and executed digitally using a secure code (Christopher, 2016). Without the intervention of middlemen, smart contracts allow blockchain users to transfer something of value, transparently. Smart contracts stipulate the rules between two parties, as do physical contracts. Smart contracts can also however, unlike physical contracts, track insurance payments or claims and hold both the parties accountable. Insurance policies may be written as coded, decentralized smart contracts in which the company commits to help cover the potential future medical expenses toward the individual who agrees to pay money to the insurance provider in exchange. Blockchain smart contracts can produce immutable data based on the records of an insurance policy owner who may approve or deny any insurance claims submitted to the company. These smart contracts make the entire process automated and the contracts to be self-executing in nature. Thus, for a policyholder and the insurance company, it becomes easier and vital to use it (Nam, 2018).

Bibliometric Analysis

Though VOS- viewer has an extravagant visualization and is capable of loading and exporting data from various sources, Biblioshiny contains a more extensive set of techniques which is suitable for practitioners for better loading and exporting of data in a robust way. (Moral-Muñoz et al., 2020) In the current study a bibliometric analysis was conducted in the graphic add-on “biblioshiny” for the package “bibliometrix” in R. Studio. This package is well suited for science mapping with respect to segmentation in the body of knowledge (Burda et al., 2020). Italian scholar Massimo Aria developed the “Biblioshiny “tool in the R language environment. Bibliometrix and Biblioshiny packages are free and open source. Biblioshiny being more flexible is able to fulfill the whole literature analysis and data flow process which ultimately prevent researchers from involving into tedious multi-step operations (Xie et al., 2020). This improves work efficiency and reduces the probability and intensity of errors. Biblioshiny is suitable for processing multi-step computing tasks where researchers can rewrite the relevant R language program code accordingly depending upon their own requirements. (Taqi et al., 2021). It utilizes the shiny package for encapsulating the core code of Bibliometric and creates a web-based online data analysis framework for a synthesized study in an efficacious and constructive manner in comparison to VOS- viewer.

Co-occurrence network

On the basis of the keyword data, co-occurrence features of various keywords related to “Blockchain” and “Insurance” are considered which aims to depict the significant trends of keyword co-occurrence. Taking into consideration the existing pluralism of denotations regarding the essence of the study on Blockchain and Insurance, we first outlined the existing connections to the well-established knowledge categories. The Keywords co-occurrence network is determined based on the number of occurrences, association, and co-occurrence of each keyword in published documents on Blockchain and Insurance. The title words co-occurrence network analysis, association, and node of 50 most frequently used words in published documents on Block chain studies are featured in the above Figure 1.

Co-occurrence network analysis.

Each node signifies the keywords while the lines denote the co-occurrence network or times each title word appear with other title words in published documents on Blockchain and Insurance. Each node’s size or diameter signifies the strength of occurrence of each Keyword in the published document on Blockchain and Insurance where the Louvain clustering algorithm with a repulsion force of 0.1 is being utilized

The construction of a co-occurrence network permits us to scout and explore the conceptual structure of the scrutinized research domain. The observation from Figure 1 posits that the research domain was subdivided into three main clusters the ones highlighted in red were devoted to a highly generalized notion of Blockchain predominantly connected to Insurance industry, smart contracts, Ethereum, internet of things, cryptocurrency, bitcoins, consensus, blockchain security while the other highlighted in blue was particularly in the domain of Health insurance or healthcare, blockchains, data sharing, decentralizations, and IOT. Also, the cluster in green indicated the proximity to the keyword in connection to insure tech, technology. risk, fintech banking related to finance. For the sound purpose of innovative research, the Blockchain cluster is evidenced to be of particular interest and great significance. The prominent fact that is noticed is that notions of Blockchain, Insurance, Cryptography, Electronic currency (bitcoins) are situated very close to one and other that contributes to their semantic similarity and proximity. Hence cluster 1 indicated in red offers the ground for a precursory description of the fundamental logic of blockchain Insurance construct. The collective usage of the keyword gives us a strong foundation and a robust background for administering an in-depth analysis of the studies through this stream of research. However, it is not advisable to solely rely on these results, but a mechanistic process of investigation alongside would have high yielding outcome benefits. Therefore, the above-mentioned findings and results are for preliminary consideration that are to be developed further by righteousness and rectitude of an in-depth investigation of the research papers from the dataset. In this network a lot of concepts and co-occurrence are tied to accentuate the betweenness and closeness of interconnections amidst the concepts which are shown in the Table 1.

Co-word Network Analysis (Keywords).

Conceptual Structure Map

This study also illustrates the conceptual structure map of each word that continuously appears in research papers on the theme of Blockchain Insurance refer Figure 2. By fragmenting it based on mapping the relationship between one word and another through area mapping we can see that each word is placed according to the values of Dim 1 which is 74.06% and Dim 2 which is 10.61% to produce a mapping between words whose values do not differ much. In this data, there are two parts of the area that are divided, namely the red and blue areas, each area contains words that are related to each other. Based on the picture above, the red area shows more, and various words included in it closely connected with “blockchain,” “insurance,” “smart contracts,” “risk assessment,” “cryptography,” “emerging technology,” “bitcoins” suggests that many research papers link between the words listed in this area. The blue area shows the connectivity with health insurance as a separate domain connected to “medical records” and “electronic health records.” The closeness and the nearness of the words reflects the mapping and the relation toward each other frequently used by the researchers in their study.

Search strategy.

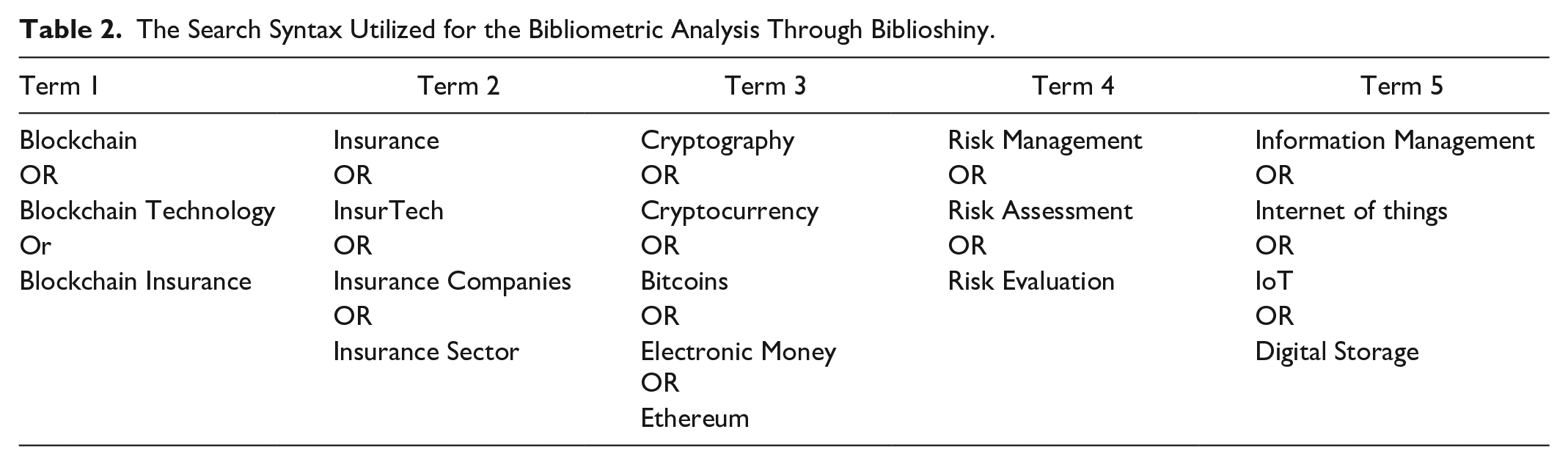

“Blockchain” AND “Insurance” AND “Cryptography” AND Risk Management” AND “Information Management” were the search operators in our present study and each term also depicted the following keywords in the search syntax.

Flow Chart

Scopus identified N = 362 documents related to “Blockchain” AND “Insurance” AND “Cryptography” AND Risk Management” AND “Information Management” whereby after applying the document type, editorials, notes, and short surveys were excluded which were five in number, further, were limited to language English, where seven articles were in other languages were excluded and the retrieved strategy reached N = 339 of which 327 documents were removed after title and abstract screening refer Table 2. N = 23 articles were eligible and considered to be highly relevant where the Biblioshiny tool was utilized for the analysis refer Figure 3.

The Search Syntax Utilized for the Bibliometric Analysis Through Biblioshiny.

Flow chart.

PICO (Population, Interventions, Comparisons, Outcomes)

The current systematic literature review adopts the PICO guidelines encompassing Population as Insurance Adopters in Block Chain, Interventions which include the opportunities and challenges of implementing blockchain, comparators are not applicable in the present context and the outcome refers to decentralization of processes, elimination of third parties for trust, transparency in transactions and availability of distributed ledgers, simplification of documentation, contracts etc., using smart contracts, with sufficient security and privacy protection.

Method

The review follows the guiding principles prescribed by Tranfield et al. (2003) for systematic review in management and business research. Eligibility and screening evaluation observed participants, interventions, comparisons, outcomes (PICO), and the suggestions of PRISMA (Preferred Reporting Items for Systematic reviews). PRISMA guidelines include a 27-object specification and a four-phase flow diagram that suggests items most crucial for the transparent reporting of a review. By aiding researchers to document a deductive roadmap in their systematic evaluation, it offers the checklist referring to the rationale, objectives, protocol and registration, eligibility standards, source of information, search, and selection of the study, data collection technique, data objects, the risk of bias in individual research, précis measures, synthesis of outcomes, and the threat of bias throughout the research studies. It additionally provides an explicit declaration eliciting information on the PICO model.

We have in particular, concentrated on analytical questions and a specific research approach for this review. The research query is defined and elaborated in the first segment, while search strategy encompassing inclusion criterion, identification of the database and search phrases are given as follows: Inclusion criteria: Intervention—object of the study: Blockchain Technology in the Insurance Industry; outcome: promising implementation methods of blockchain technology in the insurance industry; nature of the study: longitudinal/cross-sectional study; publication: academic journals; population: Insurance sector looking to explore Blockchain Technology and the benefits of implementing blockchain, smart contracts, distributed accounting and asymmetric encryption; Period: 2008 to present; Language: English. Search approach: We have used a few search techniques to look up research articles, searches in several digital databases on the internet and iterative references of articles retrieved, and hand searches. The database consists of Emerald Insight, Springer LINK, JSTOR, Sage, ScienceDirect (Elsevier), SSRN and EBSCO. These databases are specially considered as well-established databases with utmost coverage of highly ranked peer-reviewed journals in the research topic considered.

The search strategy involved a preliminary search with the use of phrases, namely: Distributed Ledger Technology, Blockchain, Insurance, Risk Management, ERM Framework, InsurTech, Technology Impact, Cryptography, Cryptocurrency, Bitcoin, Insurance Blockchain uses AND cases, Blockchain AND Insurance, Distributed Ledger AND Insurance, Smart Contracts, Cybersecurity, Ethereum. A total of 23 research papers met the inclusion standards of the studies.

Results

Blockchain technology makes it possible for insurance companies to make processes easy, anonymous, invariable, and securely transparent as it serves as a decentralized system of data storage (Sharifinejad et al., 2020). There are scores of avenues for the insurance sector to reinvent itself to become more effective in its work process. The potential of Blockchain to establish trust in a trustless environment by using shared ledgers and fortified cybersecurity protocols has positive implications for the future growth of the insurance industry. Blockchain is poised, along with artificial intelligence and big data, to make headway in InsurTech through three basic features in particular.

Fraudulent activities from customers poses major concern for the company as it costs the insurance sector huge amounts of money in settling claims due to loopholes, deliberate overseeing and frauds. With the implementation of blockchain technology, the entire insurance industry can work together to safeguard itself from fraud. If the policy owner makes any false or fraudulent statements (or if the insurance provider denies to cover a previously negotiated condition), the smart contract will automatically dissolve and the premium/s paid will be transferred back to the individual. The mechanism provides a sense of reciprocal confidence between the two parties for two reasons: all data is displayed in a transparent manner, and the slightest contractual deviation results in reimbursement to the concerned damaged party (Daley, 2020).

According to an earlier report by Kim and Kang (2017), it is argued that in terms of products and services, blockchain would bring immense market opportunities to the insurance sector (Kantur & Bamuleseyo, 2018). According to this report, some of the possible use cases for blockchain technology include:

Travel and life insurance—providers will create a “pay-as-you-go” insurance model that will offer immediate payouts if delays or cancelations occur.

Management of claims—businesses can automate coverage verification and streamline claim resolution, improving operating performance and reducing costs.

Personal accident insurance—providers will create a crystal clear and all-in-one claims path that will maximize the satisfaction of costumers.

Record keeping—businesses can establish, organize and preserve records in a single, accurate and usable database.

Reinsurance claims—businesses will be able to automate simple claims through smart contracts and models of reinsurance.

Digital identity—to digitalize and verify customer records, businesses can use blockchain data and digital ledgers; thus, enhancing compliance.

Peer-to-peer insurance—providers can create a peer-to-peer network without the need for an intermediary to create and set up smart contracts.

Surety insurance—firms will create an asset source of surety bonds information that is accessible to all members in real-time.

The insurance sector can benefit from the adoption of blockchain technology where the operations span across multiple countries and has many actors including the end user. The insurance sector is subject to a multitude of different trade, legal, and regulatory regimes. Block chain technologies can help businesses record all their transactions in encrypted blocks which are immutable. The insurance industry can be connected via a de-centralized network wherein the transactions are recorded across distributed ledgers. The trust for transactions can be provided by the blockchain members through consensus, thereby eliminating the need for third parties. Contracts and Insurance policies can be recorded electronically as smart contracts with a set of rules for the terms, conditions, duration of the policy etc.

Blockchain Use Cases in the Insurance Business

The introduction of block chain is led by some of these organizations. The insurance companies which adopted technology are mentioned below (Daley, 2020).

Etherisc

Place: Munich, Germany

What they do: Etherisc is a platform for open-source development that focuses on decentralized applications for insurance.

Application of Blockchain Insurance: For various sectors of the insurance industry, Etherisc develops decentralized, blockchain-centric applications. The organization is focused on reducing inefficiencies, namely high transaction fees and extensive claim-processing times, using ledger technology.

Real-life use case: Six separate decentralized insurance-related applications have already been developed by Etherisc. One of them is a crop insurance app for farmers to recognize their land and crops and any weather losses. Another app insures members of Etherisc against probable hacking of crypto wallets.

Guardtime

Place: Irvine, California

What they do: Guardtime builds blockchain solutions in cyber security, public policy, banking and finance, defense, and logistics.

Application of Blockchain Insurance: Guardtime recently partnered with the logistics giant Maersk to develop a maritime insurance network based on blockchain, in order to manage risk, use smart contracts and set up an immutable shipping chain to aid insurers to provide coverage.

Real-life use case: The Insurwave framework of the organization was able to handle the insurance processes for over 1,000 vessels in the first year. More than 500,000 ledger transactions dealing with relevant maritime insurance data are also planned on the site.

Fidentiax

Place: Singapore

What they do: FidentiaX is the world’s first tradeable insurance policy marketplace.

Application of Blockchain Insurance: With FidentiaX, users are able to purchase, sell or store their insurance policies on the blockchain of the company. The blockchain-powered marketplace uses tokenization to take current policies into account and put them in the encrypted database. Users are able to cash out on their respective policies in real-time, purchase policies from others or find all their insurance details in one place.

Real-life use case: ISLEY, a blockchain-powered digital ledger for insurance policies, was recently developed by FideniaX. ISLEY provides clients with a full summary of their insurance policies, sends notifications when their premiums are due, and shows the entire policy history with an immutable record.

B3I

Place: Zurich, Switzerland

What they do: The Blockchain Insurance Industry Initiative (B3i) is a consortium of insurers founded to investigate the utility of blockchain and Distributed Ledger Technology (DLT) to the insurance industry.

Application of Blockchain Insurance: Founded in late 2016, the company’s mission is to use blockchain to enhance the management of data and payments, minimize risk and make insurance more accessible. Many applications devoted to their mission are currently being worked upon by the company.

Real-life use case: A blockchain prototype for property reinsurance contracts is B3i’s first completed venture. The company was able to implement the entire reinsurance contract process on a safe and secure blockchain, with the involvement of 38 insurers and brokers.

Fizzy

Place: Paris, France

What they do: Fizzy, an insurance tool for flight delays, is a subsidiary of the multinational insurance giant AXA.

Application of Blockchain Insurance: Fizzy uses blockchain to guarantee instant coverage and compensation for members whose flights are delayed for more than 2 hours. The blockchain of the company supplements travel insurance that typically does not cover financial losses that incurred due to flight delays.

In order to lock in terms of payments and policy details, the tool uses smart contracts. Users just have to enter their flight details, configure their coverage and make a payment. Blockchain can then aid Fizzy to check flight delay data immutably and reimburse customers.

Real-life use case: Fizzy’s instant blockchain-based flight delay payments covered 80% of all worldwide flights by December 2018.

Lemonade

Location: New York City, NY

What they do: Lemonade incorporates AI and Distributed Ledger Technology to provide tenants and homeowners with insurance starting at $5 and $25 a month, respectively.

Application of Blockchain Insurance: Blockchain comes into play through smart contracts, at Lemonade. The business model of the firm takes a fixed charge from each monthly payment and allocates the balance to potential claims. If a claim is made, the smart contracts of the blockchain will automatically attempt to validate the loss so that a customer can get paid instantly.

Real-life use case: Lemonade’s AI and blockchain combination will pay its customers in 3 seconds on approval of a claim. (For customer satisfaction in renter’s insurance, Lemonade was voted number 1 of 270 companies).

Teambrella

Venue: Saint Petersburg, Russia

What they do: Teambrella is an insurance marketplace whereby the team co-insures claims, rather than being a centralized insurance provider.

For example, a member of Teambrella in the U.S. will inform the team that his or her dog needs emergency surgery. The rest of the team will vote on whether to pay for the operation of the pup and how much of the cost they can cover.

Application of Blockchain Insurance: To execute insurance payments, Teambrella uses blockchain and smart contracts. Members of one Teambrella group are locked in a smart contract and use these contracts to vote for each claim transparently and execute payment.

Real-life use case: The organization currently has four insurance pilot groups in Peru, The Netherlands, Argentina and Germany; concerned with bicycle damage and pets. They are in the process of growing their operations to include pet insurance in the U.S., and automobile insurance in Russia.

Present Application of Blockchain to the Insurance Sector

The blockchain implementations work on reducing inefficiencies, high transaction fees and extensive claim-processing time, using distributed ledger technology. The data and payments are recorded securely, thereby minimizing risk and making insurance more accessible. “Self-purchase insurance,” “automatic claim settlement,” “fraud detection,” and “fund flow record monitoring” are currently the main applications of blockchain in the insurance industry. More particulars are as follows (Zhao, 2020).

Historically, claims were primarily carried out through KYC (know your customer), while KYC was de-intermediated by automated claims. KYC is one of the key processes of identification frequently used by business entities around the world and has been in use by financial institutions since 2,000. When required, customers can give insurance companies access to their identity data. The customer can prevent duplicate authentication procedures once the KYC profile is checked and recover the checked identity data when other businesses need it. KYC based on blockchain technology has many benefits, such as disintermediation, transparent transactions and no centralized control.

Several organizations have used the features of blockchain de-mediation to change the way information is processed. For instance, Stratumn—an insurance company based in Paris, France; shares substantiated customer information through blockchain, which in turn saves cost and time for each demand side of information, to validate if the customer meets the insurance purchase requirements; therefore, consumers can buy insurance independently. Let’s take a further case. Ant Insurance launched the “blockchain + claim” project in December 2018, in which electronic notes could be used as claim notes (Kim and Kang 2017).

Detection of fraud primarily utilizes smart contract technology based on blockchain technology. Smart contracts are special protocols designed for the automated validation and compliance of contracts. In particular, smart contracts allow us, without the need for third parties, to perform traceable, permanent, and secure transactions. A smart contract includes all the transaction details and will execute the resulting procedure only if the specifications are fulfilled. The distinction between smart contracts and conventional paper contracts is that computers generate smart contracts. For instance, “Taikang Online” had an “Anti-Moth” project that used blockchain technology-based Insurance fraud detection. The company’s intelligent contracting system can deduce if the client is planning on insurance and satisfies the insurance criteria that not only preserves privacy but can simultaneously stop insurance fraud (Wang and Kogan, 2018).

3. The existence of distributed ledgers enables records of capital flows to be monitored over time. A distributed ledger is characterized as one that is managed in a decentralized form, across multiple locations and does not require a third party to maintain the validity of the data it holds (such as a bank or clearinghouse). A distributed ledger is a database consisting of several independent computers (nodes); it is the duty of the nodes to check, store and update information. The distributed ledger has the functionality of a distributed witness, making it incredibly difficult to target and attack the network. Only one entity owns a copy of the ledger in a centralized ledger. All nodes of the network however, have a copy of the same ledger in case of a distributed ledger. Without the consent of all participating nodes, no single entity can make changes to the ledger, as any new changes will be applied to all nodes within seconds. To store all of the data, it uses cryptography and can only be opened by using the key and encrypted signature. The distributed ledger will therefore not only explain the long-term monitoring of capital flow data, but also ensure the complete security of the stored information.

The “mutual insurance” project by Xinmei Life, is China’s first “blockchain + mutual insurance” project. Its account capital flow is transparent using blockchain technology. For audit monitoring, the data remains unchanged and permanent.

Furthermore, the streamlining of processes offers better user experience for clients to apply for claims (Nath, 2016). A blockchain, as a single source of truth has the potential to reduce complex procedures while also increasing efficiency in the system.

The primary advantages of using blockchain technologies are:

Advanced (Progressive) Automation Using Blockchain Technologies

Because millions of insurers, healthcare providers, patients, and consumers are involved in the insurance ecosystem (Shetty & Basri, 2017), it is easy for the industry to get hindered by money-and time-wasting inefficiencies resulting from billions of forms, human error and poor coordination between parties (Shetty & Basri, 2020).

Digital ledger systems such as blockchain can support to automate obsolete procedures, save billions of paperwork hours per year, and reduce human error because the chain safely records all forms and data. Blockchain technology helps to distribute power, the trust and integrity is networked into the system. Via distributed ledger technology, inclusion is achieved, the rights of all parties are preserved. Correspondence between significant parties in an insurance claim can also be enhanced. If stored on a blockchain, doctors and insurers can safely access the medical history of a patient to determine correct policies and procedures going forward.

Stronghold Cybersecurity

The potential of Blockchain to guard confidential information while preserving privacy is particularly appealing to an industry that relies heavily on data garnered from being at the intersection of health, work and personal life. Blockchain ledgers are decentralized, so no one authority can corrupt or manipulate them. Instead, to ensure a consistent recording of events, all data is chronologically time-stamped.

And although blockchain information is encrypted, participants (nodes) on a chain are often completely transparent, implying that all nodes may view the behavior and actions of an individual whose identity remains undisclosed. This helps blockchains to rule out suspicious activity easily and take care of issues before they become an utmost problem.

When a company adopts blockchain technology, it creates a visible change in how the claims are handled. It becomes more efficient and effectively streamlined in nature. This approach goes ahead to drastically reduce fraud as long as identities of participants in enforced to be stored and authenticated on blocks using codes. This would mean that participants would not be able to exploit the policy while potential criminals will not be able to tamper with another individual’s personal data.

Check list of Issues and Concerns

Technology Based Challenges in Implementation

Most organizations have currently implemented blockchain based solutions for particular use cases and not for their entire operations. Organizations will have to integrate the blockchain based solutions with their existing information systems and network. There is also the challenge of choosing the correct technology stack, getting the IT support for the application. Cryptographic methods to validate and write the block, the authentication methods, digital certificates and signatures need for transactions need to be identified. Blockchain based Apps for the different players in the network will have to be designed and developed. The cost of adoption of the new technology will have to be evaluated to see if it further reduces costs or mitigates risk.

The Challenges of the Legality and Non-repudiation of Smart Contracts

The legality of the smart contracts, distributed ledgers and the processes may differ in each country. The use of smart contracts poses different concerns from a legal perspective. Parties which are interested in smart contracts may be anonymous. One party may sign an agreement with a minor, for instance. This poses the possibility of the agreement being enforceable. Although procedures exist to determine age before the entry of a blockchain transaction, such a scenario may be difficult for the police to investigate. Whether such a contract is binding is a question.

Managing asset and financial transactions through a smart contract may pose a challenge, particularly if either party does not understand the programmable logic and code (representing the terms and conditions) in terms of how it behaves. Another problem is when parties’ exchange an external agreement containing all legal terms and conditions that will bind the parties and represent the actions of the smart contract. “As autonomous business agents advance through smart contract creation and compliance protocols, blockchain technology will minimize the risk and speed up the adoption of artificial intelligence-driven e-commerce if the external document represents how the code will behave. The problem in dispute is As autonomous business agents advance through smart contract formation and compliance protocols. The parties should mutually agree in the event of any errors in the code. The parties should pursue a court order demanding that the smart contract code representing their actual status, be amended.

The implementation of a smart contract does not fit into the conventional territorial jurisdiction, thereby making it difficult to decide which laws are to be enforced in order to deal with contractual issues relating to a particular smart contract. Moreover, there is a challenge to decide on which court has the prerogative to hear legal arguments that pertain to smart contracts being used. For example, if one of the parties’ challenges whether a smart contract is legally binding, it is difficult to settle and arbitrate conflicts resulting from smart contract performance. It is difficult to foresee with certainty how such a problem will be solved, considering that there is no central enforcement agency.

Challenges and obstacles in the application of Blockchain technology to the Insurance Sector

There are many governance, legal, data security, and technological challenges facing the application (Zhao, 2020), particularly in the following aspects:

There is still a long way to go in truly appreciating knowledge sharing. The insurance market is an asymmetric information market in which the customer and the insurer each have their own set of information that they do not want to share about each other. For example, insurance firms often try to gather sufficient information about the health of the insured when the insured buys life insurance, while the customer often wishes to mask those health conditions. Therefore, to achieve the full exchange of knowledge and information on medical insurance and other forms of insurance, a broad consensus on the creation of blockchain must be established by the entire society. Therefore, achieving total sharing of information through industry-wide adoption of blockchain is difficult.

Different insurance products have distinct business structures or models that function differently, such as life insurance and property insurance. The operating earnings of insurance institutions would be influenced by each of these variables, such as business networks, actuarial models, and consumer groups. Whether a particular insurance policy is acceptable for the implementation of blockchain technology needs to be independently demonstrated, but the insurance companies’ research on this aspect is just beginning. Therefore, it will take considerable time and orderly steps to facilitate the introduction and application of blockchain technology in the entire insurance industry. There is a general mistrust of insurance firms because of the regular incidence of consumer fraud and the company’s rejection in the insurance industry. It is a fact that there is often a lack of trust and confidence between policyholders, insurers and intermediaries in service. Although blockchain technology can simplify the process of purchasing insurance and making claims, it can intensify mistrust. As a result, insurance firms either need to do more to create trust with customers or to strengthen the insurance process in order to reduce the cost of credit. Many insurance companies have a limited understanding of blockchain and have not yet explained how blockchain will sustain their business growth strategically. They lack the aptitude to conduct pilot projects and advance their production practices. While blockchain can connect insurance companies with other relevant industries, however, we must stress that the insurance industry is linked to everything from health care to education, to even business operations. Therefore, it takes high connection costs and an immense amount of work to create a complete blockchain. The legal framework also presents obstacles to blockchain-based insurance. There is risk that such insurance may be effectively barred by the legal system and the likelihood that, even though blockchain-based insurance prevents enforcement regulation, the absence of a legal system could lead to inefficiencies, such as preventing the effective investment of premiums. Finally, if blockchain-based insurance prospers, this may offer economic effectiveness, but at the cost of other legal system priorities such as ensuring that insurance pricing does not take certain factors into account. While DLT can strengthen security of data, it is not “bullet-proof” and can typically give rise to three key types of possible risk of liability: risk of ledger transparency, cyber risk, and operational risk. The authors of the Working Paper of the European Banking Institute point out that, paradoxically, the increased degree of transparency by which every node operator has access to data stored on a distributed ledger, allows for the data stored on the distributed ledger to be re-personalized or facilitates nodes to make a conversant guess as to the identities entering those transactions. In turn, this leads to two key legal threats, privacy of data and insider trading and market manipulation. In most jurisdictions, data privacy or protection laws as well as prohibitions against insider trading and market abuse, bear essential civil and criminal penalties, ensuring that DLT programs have to pursue a careful course in the management of data security and transparency. To quote an instance, in June 2016, a “hack” of Decentralized Autonomous Organization (“DAO”), a decentralized investment fund created by a network of smart contracts that sought to build a virtual company on the distributed ledger Ethereum (a blockchain-based distributed computing platform and operating system that is open source, public, with smart contract features); illustrated cybersecurity problems and the operational risks involved. A consumer exploited a flaw in the original code or algorithm of the blockchain underlying the DAO platform to redirect 3.6 million of the USD 50 million worth of Ether (roughly one-third of the total value of the DAO), outside of the DAO network. The combination of errors in coding and the lack of a clear-cut governance solution, presented participants with major challenges. In turn, this involved backtracking to the block containing the “hacked” transaction and the development of a new block (to replace the previous block) to transfer the funds to an address where investors were only able to withdraw their investments in return for their DAO tokens (representing their DAO shares). This had the effect of almost all funds being restored, but by substituting the old block with the new and latest rules, that led to a “hard fork” in the Ethereum blockchain. This has been criticized as creating a dangerous precedent by weakening DLT’s immutability, which is seen as a crucial technological asset (Tarr, 2018).

Study Implications

Fraudulent activities are a constant occurrence in the insurance industry. Blockchain technology will help bring down the risk of fraud, through the creation of a global level tamper-proof ledger. This will further lower the risk of insured property as well. A digital ledger protects, and tracks insured articles throughout its life and also contains details such as its ownership, characteristics, nature, etc. This makes it possible to verify the authenticity of the item in question by various stakeholders in the supply chain. Such a digital ledger is also known as a “digital thumbprint.” Participants can transfer data without third party intervention, which results in keeping transactions shorter, faster and simpler as they are processed digitally and automatically rather than manually (Chekriy & Mukhin, 2018). Blockchain technology will pave the way for hassle free automation resulting in the elimination of human input in certain areas of operation. For instance, in case of catastrophe insurance, a system based on smart contracts can be put into motion to improve the process of claim management. When a particular event that meets the terms and conditions of the contract/policy occurs, the smart contract automatically executes payments to relevant parties that are part of the contract/policy. Improved efficiency and decreased cost of operation are two areas that companies strive for on a daily basis in order to maximize profits. Blockchain goes a long way in facilitating the same, as smart contracts eliminate challenges such as manual processing of data, human error and differences owing to timeliness of data. Persistent challenges like these are eliminated by means of verifying coverage information readily available in the blocks. Blockchain technology ensures a significant decrease in operating costs of insurance companies as it can achieve permanent audit tracking (Zhao, 2020). Blockchain technology facilitates smooth collaboration between banks and insurers through systems integration. Different systems are integrated into a single platform by using data stored in those systems. Platforms like Know Your Customer (KYC) aims at improving sharing of customer data between the insurance industry and banks so as to make sure there is transparency and avoid conflicts (Savitha et al., 2019). With the adaptation of blockchain technology, KYC related tasks may be reduced to zero, thus shortening the overall processing time and improving customer satisfaction. Smart contracts also streamline different processes by automating computational processes and authentication (Hans et al., 2017). This decreases the occurrence of “moral hazard” that has been tampering with the smooth functioning of insurance companies (Zhao, 2020). Providing the best insurance offer keeping the customer’s needs above all, goes a long way in satisfying customers and being ahead of competitors. Blockchain enables the development of new market horizons where insurers will be in a better state to develop customized services through insurance offers (Cohn et al., 2017). Customer engagement is vital for customer satisfaction, and blockchain technology improves engagement methods with customers, where the data is verified and digital in nature. Customers will not need to submit documents more than once. There is greater transparency in transactions that paves the way for better monitoring and detection of fraudulent activities. Insurers enjoy the liberty to automate the processing of insurance claims by integrating with third party vendors who take up the task of claiming for insurance through a consorted network of insurers. Apart from this, smart contracts will trigger payments only after certain conditions are validated (Deloitte, 2016a).

Conclusion

Blockchain technology along with distributed ledgers have been capturing massive attention by triggering multiple projects in insurance industries. The different application fields for blockchains in insurance believe to be manifold, establishing a good amount of trust. The interface that exists between the physical world and the digital realm may turn out to be the weak link that hinders the digital trust originated by a blockchain system in the insurance sector. The primary purpose of this study was to understand and acknowledge how the insurance sector may foster with a recognizable wave of change in terms of technological adaption, through the implementation of blockchain technology and smart contracts. Blockchain has given rise to a significant change in industries such as Food & Beverages and Pharmaceutical Supply Chain, as they are now open to scores of new opportunities. Blockchain is however praised to be a technological innovation that is allowing to revolutionize different society trades and interactions. This technology is at an infancy stage and has huge potential to extemporize, make it more efficient and effective, though it is already considered to be the safest platform to store and process data. This paper summarizes the current possible application of blockchain technology to the insurance industry in particular. The technology landscape is rapidly expanding where it is vital and challenging to develop a firm grasp of answering the question of what the core technologies have to offer in blockchain insurance, mainly highlighting to their data processing capabilities. In this paper, Blockchain insurance, distributed ledger, cryptography, and smart contract has been analyzed. Blockchain in has the potential to generate disruption in the insurance industry it incorporates in triggered smart contracts, envisages better pricing and risk assessment and increases the back-end efficiency. A bright focus on designing an efficient approach for the processing of insurance related transactions that is based on a blockchain-enabled platform is the need of the hour in the service industry. In order to realize the actual potential of blockchain, insurers should incorporate other technologies in tandem, that includes advanced analytics, internet of things and artificial intelligence. The use of blockchain and blockchain based smart contracts by the insurance industry can bring about more transparency that benefits a company through making it more trustworthy, since data entered in the blockchain cannot be tampered with. Companies have alluring opportunities to inculcate innovative skills and improve their performance with the implementation of smart contracts. For instance, better customer engagement, decreased time frame with reference to claims handling, elimination of report duplication, payment automation and avoidance of disputes may be experienced as a result of smart contracts. Blockchain technology attempts to promise in revolutionizing the insurance industry, with an umbrella of bold claims by facilitating and elevating the speed of claims settlements thus leading to improvement of fraud management. In this paper, we have synthesized and examined the factors that actually influence the extent of blockchain penetration and proliferation in the insurance industry. It is evident from this study that automation primarily leads to reduced human intervention which results in the processing of accurate data, error-free processes, and reduced cost. Built-in trust makes it possible to protect all parties involved, from fraudulent activities. No change comes without challenges and the same applies to insurance companies adapting to blockchain technology. Implementation of this technology will not be swift and can result in a complete overhaul as manual work will be automated which in turn can lead to reorganization of routines, processes and people. On the brighter side, adapting to newer and better technologies like blockchain and blockchain based smart contracts can help companies stay ahead in the market and avoid risk of disruption from competitors. The adoption of blockchain technology may also be slow owing to it being an overtly expensive venture for a company. Observing companies that have adapted to it, reaping benefits such as major cost cuts, improved operational efficiency, security and transparency, other companies are likely start implementing the same in order to keep pace with competition and enjoy the profits of the technology. The results predominantly emphasize the necessity for the industry to have a keen understanding of how blockchain can be executed across various insurance tasks for obtaining a tangible and better view of the remarkable benefits for its customers, staff and the management.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.