Abstract

This study explores the impact of supply chain finance on industrial efficiency and the internal mechanism. The super-efficiency model and quantitative analysis method were used based on the time series data of the ICT industry in Shenzhen from 2005 to 2020. In order to better investigate the impact of supply chain finance on industrial efficiency, this study categorized industrial efficiency into operational efficiency and innovation efficiency to reflect the durability and virtuousness of the industry development. Results indicate that supply chain finance has an inverted U-shaped nonlinear effect on industrial efficiency. Even though the long-term effect on operational efficiency is positive, the effect on innovation efficiency reveals an inverted U-shape, mainly due to the mediating effect of industrial concentration. Theoretically, this study sheds light on the intricate effects of supply chain finance at the industrial level, and also provides valuable insights into the potential inhibition mechanism, which enriches and deepens the related research on the supply chain finance from the nonlinear perspective, make the research findings more consistent with the fact of industrial development and avoid the linear stereotypes of the existing theory consensus. Practically, it is conductive to an objective understanding for managers and policymakers, so that supply chain finance can facilitate both operational and innovation efficiencies and realize the effective integration of supply chain finance and industrial development.

Plain Language Summary

The purpose of this study aimed to explore the impact of supply chain finance on industrial efficiency. Authors conducted quantitative analysis based on the time series data of the ICT industry in Shenzhen from 2005 to 2020. In order to better investigate the impact of supply chain finance on industrial efficiency, this study categorized industrial efficiency into operational efficiency and innovation efficiency to reflect the durability and virtuousness of the industry development. Results indicate that supply chain finance can indeed greatly improve industrial efficiency. However, this improvement is more from the perspective of operational efficiency at the industrial operation level. In the long run, excessively developed supply chain finance will lead to excessive concentration on the supply side, and excessively powerful supply chain finance enterprises will also squeeze the survival space of small and medium-sized enterprises in the serviced industry, ultimately causing the entire industry to lose its innovative vitality due to the increased industrial concentration. Theoretically, this study sheds light on the intricate effects of supply chain finance at the industrial level, and also provides valuable insights into the potential inhibition mechanism, avoid the linear stereotypes of the existing theory consensus. Practically, it is conductive to an objective understanding for managers and policymakers to realize the effective integration of supply chain finance and industrial development. This study also encountered limitations from sample range and particularity, which make it faced the challenge of theoretical robustness when extending to traditional industries.

Keywords

Introduction

In recent years, supply chain finance has emerged rapidly as a new business model. It has penetrated ICT, the nonferrous metals industry, steel, food, chemical products, and many other fields, forming a full swing of development in the high-tech and traditional industries (Abbasi et al., 2018). According to the existing literature, supply chain management enterprises can effectively manage the capital, logistics, and information flow between the upstream and the downstream enterprises of the industry they serve using supply chain finance (Guo et al., 2022) and significantly improve industrial efficiency. It is a consensus that supply chain finance is conducive to improving industrial efficiency (Lam et al., 2019; S. Li & Chen, 2019). However, there is a debate between this stereotyped consensus and the observed reality of the ICT industry in Shenzhen, which is the most innovative city in China. The birth of supply chain finance in Shenzhen is almost synchronized with the development of the ICT industry, which has a long-term cooperative relationship and gradually developed into a world-class industrial cluster. However, contrary to the cluster and rapid development of supply chain finance, Shenzhen’s ICT industry’s development has gradually slowed down. Some small and medium-sized ICT firms have closed down and moved out, and the pace of innovation in the industry has slowed. This phenomenon attracts attention from both theoretical and practical perspectives which indicate it needs to objectively understand the function of supply chain finance in the industry level. Therefore, we further refine the realistic question to a theoretical question of “what’s the effect of supply chain finance on industry efficiency?”

Different from previous studies which focused on the effects of industrial structure (Ivanov et al., 2022), industrial concentration(Abdel-Basset et al., 2020), economies of scale (Chen et al., 2022), and environmental governance (L. Zhang et al., 2021), scholars have paid more attention to the impact of supply chain finance on industrial efficiency in recent years (Vu et al., 2022). Literature shows that supply chain finance, as a business model innovation (He & Tang, 2012), has dramatically changed the transaction structure and value mode of the industrial chain (Danese & Romano, 2011) through the integration and collaboration of capital flow, logistics, information flow and business flow between the upstream and downstream firms. Business model innovation at the individual level of supply chain firms has significantly influenced the service industry (Frank et al., 2019), thus improving industrial efficiency (Ali et al., 2018). However, industrial efficiency includes operational efficiency and innovation efficiency (H. Zhang et al., 2019), reflecting the durability and virtuousness of the industry development. Most existing studies take operational efficiency to represent industrial efficiency without considering innovation efficiency, thus leading to linear research findings that supply chain finance is beneficial to improving industrial efficiency.

In order to reveal the complex impact of supply chain finance on industrial efficiency and the internal mechanism, this study intends to adopt the time series data and employ transaction cost theory as well as network theory to address the question of “What is the relation between supply chain finance and efficiency in high-tech industry.” Research findings will theoretically contribute to the supply chain finance field and help us examine the emerging business model of supply chain finance more objectively and rationally in practice to promote the efficient integration of supply chain finance and industrial innovation.

The subsequent sections of this paper are structured as follows. Section 2 provides a comprehensive literature review on the subject of supply chain finance and its relationship with industrial efficiency. Based on the findings from the literature, hypotheses are formulated to guide the empirical analysis. Sections 3 and 4 outline the methodology employed for the empirical analysis and present the corresponding results. In Section 5, the findings are discussed in detail, highlighting the implications and significance of the results. The study concludes in this section, summarizing the limitations encountered during the research process and suggesting future research.

Theoretical Background and Hypotheses

Supply Chain Finance and Industrial Efficiency

The influence of supply chain finance on industrial efficiency mainly comes from “financial governance” and “supply chain management.” This study will examine the relationship between supply chain finance and industrial efficiency from these two aspects.

Supply Chain Finance, Financial Governance, and Industrial Efficiency

Industry development needs sufficient financial capital, while supply chain finance focuses on the comprehensive management of capital flow in the supply chain (Moretto & Caniato, 2021; Wuttke et al., 2013). By providing advanced capital and settlement services to the supply and demand sides, supply chain finance optimizes the capital flow in the industrial chain (Pérez-Elizundia et al., 2021), reduces the traditional loan application and mortgage costs, provides new financing avenues, and reduces the financial cost of enterprises (Zhou et al., 2020). Finally, supply chain finance completes the financial governance by integrating financial and industrial capital (Lam et al., 2019). This integration improves the efficiency and reliability of capital flow within the supply chain, leading to enhanced industrial efficiency. By facilitating the smooth and effective movement of capital, supply chain finance helps reduce financial constraints, enhances liquidity, and promotes financial stability in the industrial sector. This, in turn, allows businesses to allocate resources more efficiently, optimize production processes, and improve overall operational performance.

In summary, the link between supply chain finance, financial governance, and industrial efficiency is established through the optimization of capital flow within the supply chain. Supply chain finance improves the efficiency and reliability of capital flow by providing advanced capital and settlement services, reducing financial costs for enterprises, and integrating financial and industrial capital. This contributes to enhanced industrial efficiency by facilitating resource allocation, optimizing production processes, and improving overall operational performance.

Supply Chain Finance, Supply Chain Management, and Industrial Efficiency

Supply chain management is the premise and cornerstone of supply chain finance. Supply chain management can integrate information flow, capital flow, business flow, and logistics in the industry to form a development trend, dramatically changing the supply chain’s transaction structure and value mode (Barykin et al., 2021). Based on supply chain management activities, supply chain finance focuses on the coordination and integration of financial resources and helps to integrate industrial development and financial innovation deeply. Through integrating supply chains, relevant industries can be upgraded and reformed, SMEs can raise funds, and core enterprises can be transformed. Enterprises at each node of the industrial chain can be encouraged to strengthen cooperation. Thus, a closer industrial network and information governance community can realize a virtuous cycle for the whole industry.

Literature shows that supply chain finance promotes industrial efficiency. The influencing mechanism is as follows: through financial governance and supply chain management, supply chain finance improves the efficiency and reliability of capital flow, builds an information governance community, and reduces transaction costs, thus promoting efficiency. Therefore, we predict that:

H1: Supply chain finance is positively related to industrial efficiency.

Supply Chain Finance and Operational Efficiency

According to the transaction cost theory, the existence of the transaction cost is mainly due to the characteristics of the transaction, such as the specificity of the assets, the uncertainty and the frequency of the transaction. In the network based on supply chain finance, SMEs have established a long-term cooperation relationship with the core enterprises, which ensures the specificity of assets, increases the frequency of transactions, activate the scale effect, and thus makes the overall transaction cost relatively low. At the same time, the frequent transactions of enterprises in the supply chain enhance the liquidity of information and reduce the asymmetry. Therefore, the impact of supply chain finance on industrial operational efficiency is mainly generated from two aspects: “scale effect” in the production field and “transaction cost” in the circulation field.

Supply Chain Finance, Scale Effect, and Operational Efficiency

One of the key ways to advance industrial technology and boost labor productivity is to expand the market (Nielsen, 2018). Scale effect has a direct and far-reaching influence on industrial operation and development (Santiago-Ramos & Feria-Toribio, 2021). By linking the supply chain with the industrial environment, supply chain finance boosts the formation and development of the industrial base, enables the industry to form a scale effect in a specific region, which improves the density of industrial economic activities, forming a positive impact on the operational efficiency of the industry.

Supply Chain Finance, Transaction Costs, and Operational Efficiency

Many industries have high transaction costs, resulting in blocked commodity circulation and low operational efficiency. According to a scholar (Yu et al., 2019), supply chain finance uses the macro-industrial chain logic to improve communication and cooperation among supply chain partners and encourage benefit sharing and cooperative business growth among enterprises in each node. By providing multi-mode, reliable, and professional financing services to the core enterprises (Tessmann & Elbert, 2022) and customers of the industrial chain (Lu et al., 2022), supply chain finance can reduce commodity risks, price fluctuations, and transaction costs (Pellegrino et al., 2019), significantly improve the efficiency between enterprises, thus enhance the operational efficiency (Bag et al., 2020).

According to the existing literature, supply chain finance has improved operational efficiency. The influencing mechanism is as follows: supply chain finance improves the industrial cluster in the production field and forms a scale effect. At the same time, supply chain finance reduces the transaction cost in the circulation field and ultimately promotes operational efficiency. Therefore, we predict that:

H2: Supply chain finance is positively related to operational efficiency.

Supply Chain Finance and Innovation Efficiency

Based on network theory, the structure of supply chain, with network characteristics, forms a relationship collection with core enterprises as the focus. Firms need a stable supply chain relationship when carrying out innovative activities. As a new financial tool, supply chain financial service can not only solve the problem of capital shortage, but also rebuild a closer supply chain relationship network system. The development of supply chain finance is a process of relying on the credit guarantee of core enterprises and providing loans by financial institutions to the supply chain members, which can promote the closer cooperation among the members of the supply chain network and enhance the overall competitiveness and innovation ability of the whole industry. Therefore, the impact of supply chain finance on innovation efficiency is mainly generated from two aspects: the “business linkage” of the industrial chain and the “credit empowerment” of SMEs.

Supply Chain Finance, Business Linkage, and Innovation Efficiency

Suppliers and customers are essential carriers of industrial and technological innovation and requirement information, carrying the accumulation of innovative knowledge and technology (Peters, 2022). Supply chain finance focuses on suppliers, customers, and core enterprises in the industrial chain to rationally allocate and integrate internal capital, facilities, information, and other production factors (Dekkers et al., 2020), especially for knowledge, technology, talent, and aspects of “business linkage” (Kaewnaknaew et al., 2022). Supply chain finance enables the free flow of innovation elements and drives the spillover of technology and knowledge (Moon, 2022), as well as strengthens enterprises in each node of the industrial chain, thus effectively promoting the collaborative innovation of the industry.

Supply Chain Finance, Credit Empowerment, and Innovation Efficiency

Technological innovation requires continuous financial support (Abid et al., 2022). Due to the constraints financing, recent financial difficulty and expensive financing create many challenges for SMEs with innovative thinking and excellent development potential. By providing multi-mode financing services, supply chain finance strengthens credit management, improves the credit system of the industrial chain, and realizes credit empowerment. Supply chain finance can improve the relative credit of firms, reduce financing costs (Pérez-Elizundia et al., 2020), and make more funds invested in innovation activities. Meanwhile, supply chain finance breaks the trust barrier. It reduces credit risk for SMEs, which makes them play their creative or technical advantages after obtaining financing, bringing innovation and vitality to industrial development.

The present study suggested that supply chain finance promotes the innovation efficiency of the industry (Roshchyk et al., 2022). The influencing mechanism is as follows: supply chain finance promotes the “business connection” of production and innovation elements among enterprises and provides financial support for innovation activities through credit empowerment, thus promoting innovation efficiency. Therefore, we predict that:

H3: Supply chain finance is positively related to innovation efficiency.

Empirical Analysis

Modeling Framework

This paper employs the expanded Douglas production function and constructs the following model to test the above hypotheses and conduct an empirical analysis at two levels: ① Assess the overall effect of supply chain finance on industrial efficiency. ② Examine the sub-effects of supply chain finance on operational efficiency and innovation efficiency.

The reason for choosing the extended Douglas production function is its ability to capture the relationship between inputs (supply chain finance) and output (operational efficiency and innovation efficiency). This model can comprehensively analyze the impact of supply chain finance on industrial efficiency, as well as the effects on operational efficiency and innovation efficiency separately. On the basis of expanded Douglas production function, the following model is constructed:

(1) The overall effect test model of supply chain finance on industrial efficiency

(2) The sub-effect test model of supply chain finance on operational efficiency

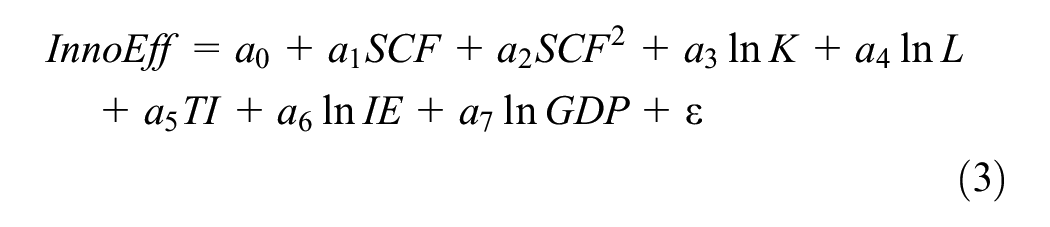

(3) The sub-effect test model of supply chain finance on innovation efficiency

To better present the modeling process, the diagram lays out as Figure 1.

Diagram of research method.

Variable Definition

Dependent Variable

Industrial efficiency (InEff), Operational efficiency (OperEff), and Innovation efficiency (InnoEff) are dependent variables in this study. When the existing literature calculates efficiency, it usually uses DEA (data envelopment analysis), which has less restriction on the selection of indicators, to determine the efficiency of different DMUs (Decision Making Units) by using cross-sectional data and the input-output of relevant variables (Z. Li et al., 2017). According to the characteristics of the time series data, to compare and rank multiple units, this paper uses the super efficiency DEA model (SE-DEA) (Huang et al., 2021) to measure industrial efficiency, operational efficiency, and innovation efficiency. The SE-DEA model enables a comprehensive evaluation of efficiency by considering both technical and allocative efficiency. By employing time series data from the ICT industry in Shenzhen spanning from 2005 to 2020, this study captures the dynamic nature of industrial efficiency and facilitates the identification of long-term trends and patterns. This methodological approach ensures the robustness and reliability of the research findings, thereby enhancing the credibility and validity of the outcomes.

Selecting appropriate input-output indicators is the crucial step to measuring the value of efficiency accurately. Based on the indicators system developed by scholars (Cai et al., 2019) in studying industrial efficiency (Goyal et al., 2018), this paper takes the indicators of employees, fixed assets, and operating income as the leading input-output indicators. As the primary data and essential factor of the industrial environment, the number of enterprises (Zheng & Hu, 2006) is used as the input indicator of industrial efficiency. The primary business income of an industry is a vital symbol to measure the development of industrial operations (Khlystova et al., 2022), which also serves as the output indicator of operational efficiency. At the same time, innovation efficiency is closely related to the innovation and R&D activities in the entire industry (Bican & Brem, 2020), so its input-output is measured by the corresponding indicators of the main body (Liu et al., 2020). In addition, considering the uniqueness of the sample, this paper combines the industrial environment with the unique embodiment of the internal operation and innovation activities of the industry and incorporates the subjective evaluation score into the indicator system (Xu et al., 2022), thus constructs the following efficiency measurement indicators (see Table 1).

Classification and Description of Each Efficiency Measure Index.

Independent Variables

Supply chain finance is the core independent variable in this study. Supply chain finance is a financing method different from traditional bank financing. It provides comprehensive financial products and services to the upstream and the downstream enterprises of the supply chain by relying on core customers and natural trade backgrounds, using the method of self-compensating trade financing to close the capital flow or control the fundamental right through professional means such as accounts receivable pledge registration and third-party supervision (Lu et al., 2020). From the specific collateral, accounts receivable financing, inventory financing, advance payment financing, and order credit financing are the typical modes of supply chain finance (H. Zhang et al., 2019). Following the provisions of the Notice on Adjusting the Statistical Caliber of Deposits and Loans of Financial Institutions issued by the People’s Bank of China and scholars, preliminary research on the measurement of supply chain finance (H. Zhang et al., 2019), “short-term loan,”“financial leasing” and “bill financing” are used as the measurement indicators of supply chain finance (Weibin & Ke, 2012), which is the core independent variable in this paper. We summarize the above three data types to measure supply chain finance in the overall industry (SCF). To investigate the long-term impact of supply chain finance on industrial efficiency and make the test more realistic, this study adds the quadratic term SCF2 of the core independent variable to the model (1). Thus the final results are obtained by logarithmic processing.

Control Variables

According to the existing literature, the control variables in the model include capital input (K), labor input (L), technology level (TI), information environment (IE), and regional gross product (GDP).

At the industry level, industrial development depends on two key factors, capital input and labor input. This study uses the annual investment in fixed assets and the number of employees in the ICT industry. The technological development level is an essential measure of industrial innovation, which is measured as the ratio of R&D investment of the ICT industry to the operating income (Zhao et al., 2021) in this study.

At the regional level, information transmission is an environmental factor for the production and development of the ICT industry, expressed by the sum of the number of fixed telephones, mobile telephones, and Internet usage in Shenzhen (T. Li et al., 2023) in this study. The economic development of an industry is closely related to the external economic development of the region, so this study uses GDP as an indicator to measure the economic development level of Shenzhen. All the control variables are obtained by logarithmic processing. In addition, ε denotes the random error term.

Selection of Samples and Data Sources

Considering the history of supply chain finance in China, the characteristics of industrial distribution, the compatibility with the research topic and the data availability, we select the ICT industry in Shenzhen as the research objects. ICT industry refers to the Information and Communication Technology industry, which is a typical high-tech industry. Unlike the emergence of supply chain finance in other industries, the development of the ICT industry and supply chain finance has more than 10-year history in Shenzhen, which provides ideal time series data. In this study, the relevant data from 2005 to 2020 were selected from the Statistical Yearbook of China, Statistical Yearbook of Shenzhen, and Shenzhen Association of Logistics and Supply Chain Management. The missing data were supplemented by interpolation method. The subjective scores of some dependent variables were conducted by expert opinion, following the convenient principal (Meng et al., 2023). The respondents include experts and scholars from universities and academic institutions of supply chain finance and industrial economy as well as top managers engaged in supply chain finance and ICT related business, such as Renmin University of China, Dalian University of Technology, Dongbei University of Finance and Economics, Shenzhen Yuehai Supply Chain Corporate, Grace Asia Supply Chain Company, SJet Supply Chain, and other supply chain enterprises. Before the final questionnaires were sent to the experts, a pretest was conducted to ensure the subjective indicators are an effective supplement to the objective indicators. Five scholars from Liaoning University and five managers from supply chain finance firms evaluated the subjective indicators to confirm they are appropriate and can be evaluated based on their expertise and working experience. Finally, a total 80 questionnaires were distributed to the experts, and 80 valid questionnaires were collected, the mean value of the expert ratings was used as the year data of the corresponding indicators.

Descriptive Statistics

Table 2 provides descriptive statistics of relevant variables, with the statistical interval from 2005 to 2020. It can be seen from the data that the mean value of industrial efficiency is 1.043, the minimum value is 0.738, and the maximum value is 1.290. The mean operational and innovation efficiency values are 1.038 and 0.930, respectively. Supply chain finance has significantly increased in 16 years, and the capital input, labor input, technology level, information environment, and Shenzhen’s GDP changed considerably.

Basic Data Characteristics of Each Variable.

Results

Supply Chain Finance and Industrial Efficiency

Time series data analysis is a crucial part of econometric research. Since most time series are non-stationary, it often leads to “spurious regression” (Ghouse et al., 2021). This method is to adjust non-stationary sequences to stationary sequences by difference. Suppose the linear combination of series after difference is stationary. In that case, we considered the time series of the combination to have a cointegration relationship, and there is a long-term equilibrium relationship between different variables. Therefore, based on the time series data, this paper uses Unit root analysis, EG cointegration test, VECM model, and Granger causality test to explore the impact of supply chain finance on industrial efficiency and investigate whether there is and what kind of relationship exists among variables. The stability of the long-term equilibrium relationship between the two is tested.

Unit Root Analysis

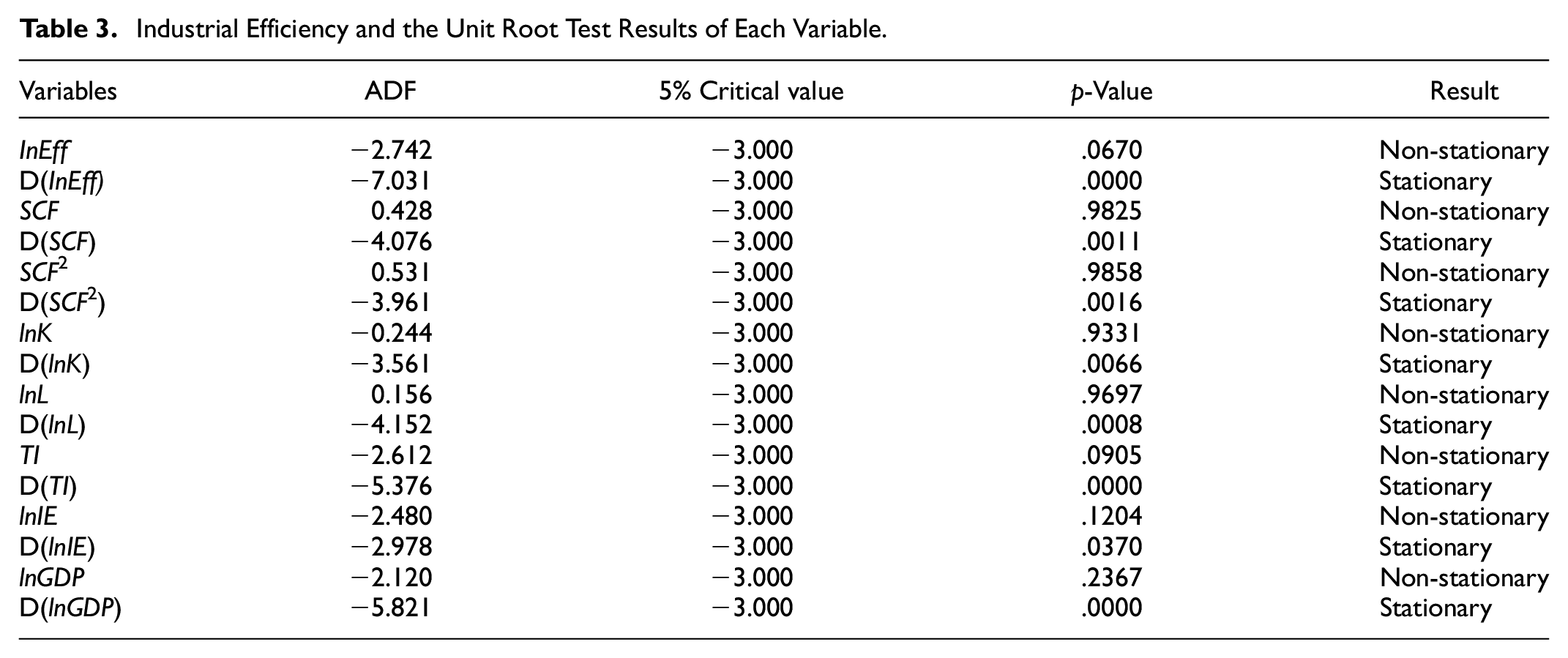

For model (1), it is necessary to conduct a unit root test for each variable before the analysis. This paper adopts the Augmented Dickey-Fuller (ADF) test, which is more commonly used in empirical analysis, and the test results are shown in Table 3.

Industrial Efficiency and the Unit Root Test Results of Each Variable.

Cointegration Test

After the different first-order series of each variable is stationary, it is necessary to conduct a cointegration test to establish a cointegration relationship. Johansen test and EG test (Engle-Granger two-step cointegration test) are the main methods for testing the cointegration of time series data. To determine the cointegration of time series variables, this paper uses the EG test, which is suitable for the small sample size of data and the low degree of freedom restriction.

① The test of a single equation. This is the first step of the EG test, which separately considers the impact of the independent variable on the dependent variable, applying the OLS regression method to estimate the regression model as follows:

The ADF test is conducted on the residual series formed by the residual set of each of the regression models, and the results are shown in Table 4.

The Cointegration Relationship Between Industrial Efficiency and Variables.

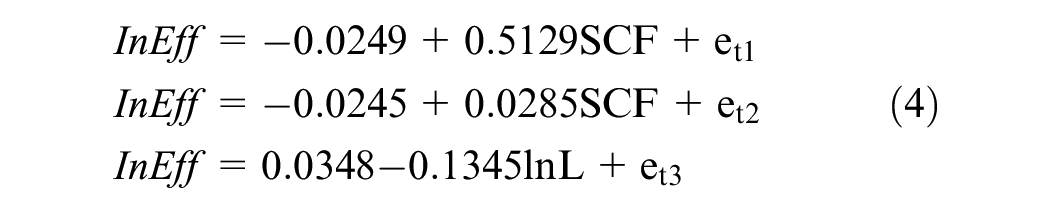

The results show that industrial efficiency InEff cointegrates with supply chain finance SCF and its quadratic term SCF2, capital input lnK, labor input lnL, and regional gross product lnGDP. There is a cointegration relationship between them at the .05 significance level. Therefore, the long-run equilibrium equation of industrial efficiency and other independent variables can be obtained:

② The cointegration tests of the population equations. When the overall residual test is conducted on Equation 5, the ADF value is −2.472, which was greater than the critical value of .05 significance levels. Therefore, the null hypothesis that there is a cointegration test should be rejected. When the variables lnK and lnIE are excluded, the ADF value is −3.37, and the residual series is stable at the .05 significance level. Thus, these two variables should be excluded, and there is a long-term equilibrium relationship between industrial efficiency and supply chain finance. Therefore, Equation 6 is transformed into:

Stability Test

This paper uses the VECM model (Vector Error Correction Model) to test the stability of time series data, as most economic variables have long-term equilibrium relationships and are affected by short-term fluctuations (Jian et al., 2019). Therefore, the VECM vector error correction model is used to analyze the stability of the cointegration relationship among variables. The VECM model allows for short-run fluctuations among the variables while restricting the long-run behavior of the endogenous variables to converge to their cointegration relationship (Yussuf, 2022). The specific model equation is as follows:

Pt is n first-order difference stationary sequence vectors, M is the lag order of the VECM model, ecmt-1 is the correction error term reflecting the long-term equilibrium relationship between variables, and

The primary term and quadratic term of industrial efficiency and supply chain finance are substituted into the above model for analysis, and the stability test (Amemiya, 1985) of VECM model estimation is carried out by using the characteristic root of the coefficient matrix. The results are shown in Figure 2:

VECM stability diagram of industrial efficiency.

The results show that except for the unit root assumed by the VECM model itself, all eigenvalues of the adjoint matrix fall within the unit circle, so the long-term equilibrium relationship between the primary and quadratic terms of industrial efficiency and supply chain finance is stable and effective.

Causality Analysis

This paper uses the Granger test to investigate the causality of time series data. In the case of time series, the causal relationship between two variables, X and Y, is defined as follows: if variable X causes the change of variable Y, the change of X should occur before the change of Y, which means the variable X helps to explain the future changes of the variable Y, and the variable X is the cause of the variable Y (Feige & Pearce, 1979). Since the variables of industrial efficiency and supply chain finance after a first difference are cointegrated, the results of the Granger causality test are shown in Table 5.

Granger-Causality Tests Between Supply Chain Finance and Industrial Efficiency.

Results in Table 5 show that when the lag periods are 2 to 4 periods, there is a unidirectional Granger causality running from supply chain finance to industrial efficiency, indicating that the change in supply chain finance directly affects the improvement of industrial efficiency but not vice versa. The causal relationship between the two has a 2 and 4 period lag.

Based on the above empirical tests, when the correlation between supply chain finance and industrial efficiency is discussed in a single equation, the regression coefficient value of .5129 is significantly positive, indicating that without considering other factors, the improvement of supply chain finance will improve industrial efficiency. In the overall equation, there is a long-term equilibrium relationship between industrial efficiency and each variable after the unit root test and cointegration test. Among them, the regression coefficient of the primary term of supply chain finance is 18.811, while the regression coefficient of the quadratic term is −1.054, indicating that supply chain finance has an evident inverted U-shaped nonlinear impact on industrial efficiency, which denies the null hypothesis that supply chain finance has a significant positive impact on industrial efficiency, so H1 is rejected.

Supply Chain Finance and Industrial Operational Efficiency

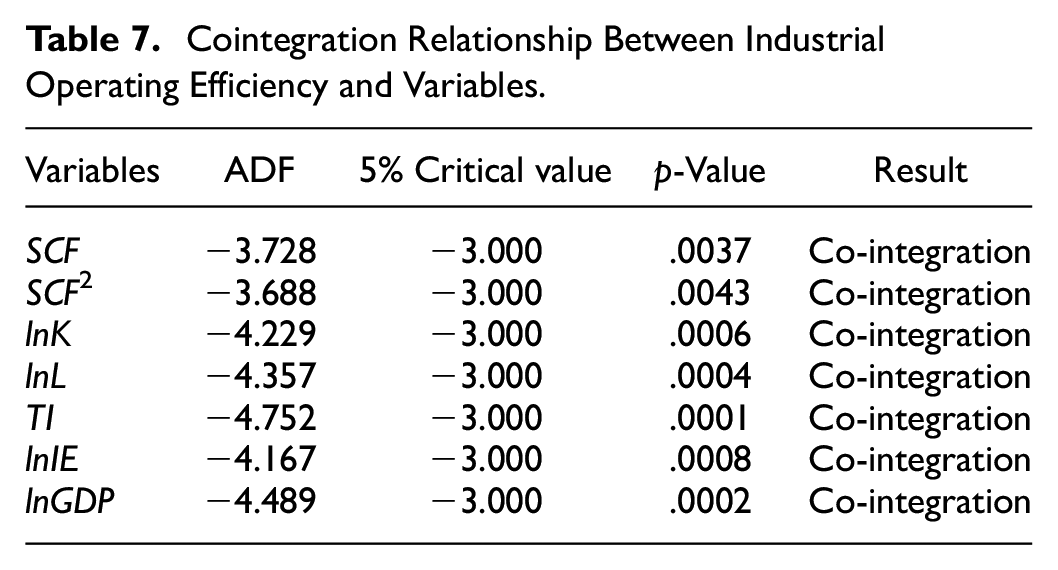

For Model (2), the industrial operation efficiency is taken as the dependent variable, and the unit root test and cointegration test are conducted successively. The test results are shown in Tables 6 and 7.

ADF Test Results of Operational Efficiency and Variables.

Cointegration Relationship Between Industrial Operating Efficiency and Variables.

From the results in Table 6, it can be seen that in the single-equation regression, the operation efficiency (OperEff) has a cointegration relationship with all variables at the .05 significance level. According to Table 7, the residual series of the single equation between the operation efficiency and each variable is stable, and the long-term equilibrium equation of the industrial operation efficiency can be obtained:

It should be noted that when the overall residual test is conducted on Equation 7, the ADF value is −2.564, which is greater than the critical value at the .05 significance level. Therefore, the null hypothesis should be rejected. When the quadratic variable SCF2 and economic development level lnGDP are excluded, the ADF value is −2.884, and the residual series is stable at the .05 significance level. Therefore, there is a long-term equilibrium relationship between operational efficiency and supply chain finance with the exclusion of these two variables. Thus, Equation 7 is transformed into:

The VECM stability test of Equation 8 shows that the long-term equilibrium relationship between the primary term of operation efficiency and supply chain finance is stable (see Figure 3). Further Granger causality test shows that supply chain finance is the reason that affects the change in operational efficiency. Supply chain finance can promote operation efficiency but not vice versa (see Table 8).

VECM stability diagram of operational efficiency.

Granger-Causality Test Between Supply Chain Finance and Industrial Operation Efficiency.

The former coefficient of SCF is positive. Supply chain finance positively influences operational efficiency in the long run. The increasing maturity of supply chain finance and product systems positively impacts operational efficiency. This conclusion verifies H2.

Supply Chain Finance and Innovation Efficiency

For Model (3), the innovation efficiency is taken as the dependent variable, while the unit root test and cointegration test are conducted in turn. The test results are shown in Tables 9 and 10.

ADF Test Results of Innovation Efficiency and Variables.

Cointegration Relationship Between Innovation Efficiency and Variables.

It can be seen from the table that the innovation efficiency (InnoEff) has a cointegration relationship with all variables at the .05 significance level, that is, there is a significant long-term equilibrium relationship between the innovation efficiency and them, so the overall equilibrium equation is obtained:

After the ADF and EG cointegration tests, the above equilibrium equation proves a long-term equilibrium relationship between supply chain finance and innovation efficiency. The VECM stability test further verifies that the long-term equilibrium relationship between innovation efficiency and supply chain finance development is stable (see Figure 4). Further Granger causality test shows that supply chain finance is the reason for the change in innovation efficiency, but not vice versa (see Table 11).

VECM stability diagram of innovation efficiency.

Granger-Causality Tests Between Supply Chain Finance and Innovation Efficiency.

In the single equation test, the linear regression coefficient of supply chain finance is significantly negative, indicating that an increase in supply chain finance will decrease innovation efficiency. However, when the quadratic term of the core independent variable is added to the regression equation, regression Equation 9 shows that the regression coefficient of the core independent variable is 1.885. The regression coefficient of the quadratic term is −0.092, indicating that supply chain finance has an inverted U-shaped nonlinear effect on innovation efficiency that first promotes and then inhibits. It is denied that supply chain finance has a significant positive impact on innovation efficiency in the hypothesis. Therefore, H3 is rejected.

The Mechanism of Supply Chain Finance on Industrial Efficiency

The above research shows a nonlinear relationship between supply chain finance and industrial, operation, and innovation efficiency. Supply chain finance has an inverted U-shaped nonlinear effect on industrial and innovation efficiency, while it positively affects operational efficiency. Therefore, this study needs further analysis to reveal the internal mechanism of supply chain finance on industrial efficiency. In contrast, industrial concentration as a related variable of supply chain finance has entered our attention. In Shenzhen, the development of the supply chain finance and ICT industry is accompanied by the formation of industrial concentration. The integrated development of the supply chain finance and ICT industry have formed a strong “centripetal force,” which promotes industrial concentration.

On the one hand, industrial concentration accelerates the expansion of production scale, which has an “incentive” effect on regional economic growth by guiding industrial restructuring (Chai et al., 2021). On the other hand, with the improvement of supply chain finance, the relative scarcity of resource factors and the excessive density of capital factors caused by industrial concentration has become increasingly prominent (Bai & Bian, 2016). At this time, supply chain finance has a reverse crowding-out effect on industrial efficiency, inhibiting its improvement. Overall, this paper introduces industrial concentration as the model’s mediating effect and explicitly analyzes the mechanism of supply chain finance and industrial efficiency.

Supply Chain Finance, Industrial Concentration, and Industrial Operational Efficiency

According to the financing mode provided by supply chain finance, relevant industries can expand their scale, and extend the fields involved in the industrial chain, thus gradually forming a scale effect so that the professional and technical personnel in the industry can match the positions in the labor market, and improve the labor productivity and resource utilization rate of the whole industry (Wang et al., 2022). By promoting the exchanges, cooperation, and coordinated development of enterprises, supply chain finance will reduce the transaction costs between enterprises, significantly improve the response speed of upstream and downstream enterprises in the industrial chain, then make the logistics, distribution, as well as other production and operation activities of the industrial chain more flexible and efficient. Therefore, supply chain finance mainly plays an “incentive” effect on operation efficiency through industrial concentration.

Supply Chain Finance, Industrial Concentration, and Innovation Efficiency

In the early stage of development, supply chain finance can effectively promote industrial innovation through industrial concentration, integrating internal resources of the industry, promoting the connection of upstream and downstream enterprises of the industrial chain, improving the allocation rate of innovation factors such as talents and technology (Fan et al., 2020), and effectively promoting industrial collaborative innovation. However, with the expansion of supply chain finance, the influence of industrial concentration continues to strengthen, which brings a “crowding out” effect on the financing and transaction of small and medium-sized enterprises that lack capital and credit conditions in the industry. Although small and medium-sized enterprises have strong innovation ability and growth vitality, due to the “risk avoidance” of supply chain finance enterprises and the “indirect crowding out” (Graafland & de Bakker, 2021) of large enterprises eager for their development, some small and medium-sized enterprises are forced to face the crisis of financing difficulties and business decline, which suffocates the “innovation vitality factor” existing in the industry and hinders the progress of industrial innovation. Therefore, supply chain finance has an inverted U-shaped impact on innovation efficiency through industrial concentration, which is first “encouraging” and then “crowding out.”

Therefore, considering operation and innovation efficiency dimensions, the long-term relationship between supply chain finance and industrial efficiency could be better. However, there are two opposite effects of “incentive” and “crowding-out,” These effects may fluctuate in different stages of supply chain finance development. In short, under the influence of supply chain finance, industrial efficiency shows a trend of first increasing, then stable development, or even declining.

To verify the above mechanism, this paper examines the mediating effect of industrial concentration based on model (1), that is, supply chain finance affects industrial concentration and then affects industrial efficiency. Based on data availability, this paper uses the location quotient (LQ) to measure the industrial concentration effect. The proportion of ICT industry employment in Shenzhen in the total urban employment divided by the national proportion in the same period was selected for measurement. The specific model used is as follows:

The procedures are as follows: ① Test the impact of supply chain finance and its quadratic term on industrial concentration, focusing on the regression coefficients a1 and a2 in the Model (1). ② Test the regression coefficients β1 and β2 in Model (9) and γ3 in Model (10). The above empirical results have verified that the primary term a1 of supply chain finance in ① has a long-term positive equilibrium relationship with industrial efficiency. In contrast, the second term a2 has a long-term negative equilibrium relationship with industrial efficiency. Therefore, this part focuses on the data of β1, β2, and γ3. According to the test, β1, β2, and γ3 pass the ADF and EG cointegration tests. A long-term equilibrium relationship with dependent variables indicates that the industrial concentration with location entropy has a mediating effect.

The test results of Model (9) and Model (10) are shown in Table 12. Among them, column 1 reports the ADF test of location quotient (LQ). The results show that the series is stationary after the first difference and can be tested for cointegration. Columns 2 to 4 indicate that the mediating variables pass the EG cointegration test. This shows a long-term equilibrium relationship between industrial concentration, supply chain finance, and industrial efficiency. That is, industrial concentration, as an intermediary variable of supply chain finance, affects industrial efficiency in long-term equilibrium.

Mechanism Test Between Supply Chain Finance and Industrial Efficiency.

It should be noted that in the single equation test, the location quotient (LQ) and the gross regional development (GDP) reject the cointegration test at the .05 significance level, so Models (9) and (10) do not include the variable lnGDP in the overall test. In addition, the coefficient β1 before SCF in Model (9) is 58.854, and the coefficient before SCF2 is −3.433, indicating that supply chain finance has an inverted U-shaped nonlinear impact on industrial concentration. At the same time, in the test result of Model (10), γ3 is 0.012, which is significantly positive, indicating that industrial concentration positively promotes industrial efficiency. The above results verify the theoretical mechanism that supply chain finance acts on industrial efficiency by influencing industrial concentration.

General Discussion

Conclusions and Discussions

In order to empirically test the impact of supply chain finance on industrial efficiency, this study used the time series data of the ICT industry in Shenzhen from 2005 to 2020. Results indicate that supply chain finance has an inverted U-shaped nonlinear effect on industrial efficiency. Even though the long-term effect on operational efficiency is positive, the effect on innovation efficiency reveals an inverted U-shape, mainly due to the mediating effect of industrial concentration.

The results can be regarded as an extension to the research of Ali et al. (2018, 2019), which investigate the impact of supply chain finance at the firm level, while we extended the existing knowledge to the industry level, which enriches and deepens the research of the supply chain finance. To some extent, it is also consistent with the claims of Weibin and Ke (2012) and Pfohl and Gomm (2009) which raised positive role of supply chain finance, which can help to reduce the financing constraints and optimize the financial flows. On this basis, we further explored from the nonlinear perspective, and provided valuable insights into the potential inhibition mechanism, make the research findings more consistent with the fact of industrial development and avoid the linear stereotypes of the existing theory consensus.

To be better understand our research findings, discussion is provided as follows:

Firstly, supply chain finance has an inverted U-shaped non-linear effect on industrial efficiency, which means supply chain finance will promote industrial efficiency. However, when supply chain finance reaches a threshold level, it will inhibit further improvement of industrial efficiency. This finding breaks the stereotype that supply chain finance positively affects industrial efficiency. As a business model innovation at the operational level, supply chain finance can indeed greatly improve industrial efficiency. Nevertheless, the improvement of industrial efficiency by supply chain finance is not always positive, as industrial efficiency includes both operational efficiency and innovative efficiency. Supply chain finance greatly optimizes the connection and flow of information, capital, and logistics between upstream and downstream industries, making the capital flow, logistics warehousing, and trade information of the entire industry chain more smoothly, thereby greatly enhancing industrial efficiency. Whereas, this improvement is more from the perspective of operational efficiency at the industrial operation level. In the long run, excessively developed supply chain finance will lead to excessive concentration on the supply side, and excessively powerful supply chain finance enterprises will also squeeze the survival space of small and medium-sized enterprises in the serviced industry, ultimately causing the entire industry to lose its innovative vitality due to the disappearance of a large number of SMEs.

Secondly, different from operational efficiency, supply chain finance has an inverted U-shaped influence on innovation efficiency. When supply chain finance reaches a critical level, it will increase innovation efficiency in the short term while preventing further advancement. The finding sheds light on the profound impact of supply chain finance on industrial innovation efficiency. By effectively addressing the funding bottleneck that SMEs face in the innovation process, supply chain finance provides funding channels, logistics support, and information empowerment to a large number of SMEs that possess orders, technology, and aspirations, but lack assets, brands, and funding. This greatly facilitates SMEs in the emerging stage of the industry to innovate and start businesses, thereby enhancing industrial efficiency. However, in the long run, excessively developed supply chain finance could lead to an excessive concentration on the supply side, and excessively powerful supply chain finance enterprises could also squeeze the survival space of SMEs in the serviced industry. As supply chain finance enterprises develop and grow, they may also selectively choose customers and support high-quality clients to become larger and stronger, ultimately causing the entire industry to lose its innovative vitality due to the disappearance of a large number of SMEs.

Thirdly, the further test illustrates that supply chain finance mainly influences the efficiency of ICT industries by affecting industrial concentration. It verifies the internal mechanism by enhancing financing strategies, bolstering resource integration, and fostering industrial linkage, thus influencing industrial efficiency. Industrial concentration is the intermediary mechanism through which supply chain finance affects industrial efficiency. In the early stages of supply chain finance development, supply chain finance enterprises and the SMEs serve develop together. However, as both parties grow, supply chain finance will accelerate the rapid increase of industrial concentration in the service industry, leading the industry to evolve rapidly into an oligopoly state. The increase in industrial concentration means that a large number of SMEs with high innovation vitality disappear, ultimately resulting in a reversal of the curve of industrial efficiency, especially industrial innovative efficiency.

Theoretical Contribution and Practical Implication

The theoretical contribution of this study is mainly reflected in three aspects. First, compared with the existing research based on the financing effect of supply chain finance to explain its driving role of firm level, this study conduct a more broader view of industry. It is helpful to enrich the discussion of the economic effect of supply chain finance and deepen the theoretical explanation of supply chain finance driven industrial operation and innovation. Second, this study enriches and deepens the related research from the nonlinear perspective, make the research findings more consistent with the fact of industrial development and avoid the linear stereotypes of the existing theory consensus. Third, compared with the existing research focuses on the direct effect of supply chain finance on efficiency, this study explores and verifies the mediating role of industrial concentration, which facilitate to build the theoretical logic of reverse crowding out effect of supply chain finance on industrial innovation efficiency, helps to reveal the internal promotion and potential inhibition mechanisms of supply chain finance and innovation efficiency.

This study offers managers or policy makers valuable insights into the significance of supply chain finance. By leveraging this knowledge, managers or policy makers can make well-informed choices and formulate policies that facilitate the seamless amalgamation of supply chain finance and industrial growth. Through a comprehensive understanding of the potential limitations of supply chain finance on innovation efficiency, managers or policy makers can strive to mitigate these drawbacks and optimize the favorable influence of supply chain finance on industrial efficiency.

Research Limitations and Prospects

We analyzed the effect of supply chain finance on industrial efficiency and came to a tentative conclusion using the time series data of the ICT industry as a sample. Due to the impact of data availability, project funding, and other reasons, this study has the following limitations: First, the limitation of sample range. This study used only the time series data of a single region and industry for analysis rather than cross-region and cross-industry panel data. Therefore, the research conclusion of this study is confronted with the challenge of theoretical universality. We suggest using cross-region and cross-industry panel data for analysis in the future to verify the universality of the theory. Second, the particularity of sample selection. Since technology advances quickly and there is intense internal competition within the ICT sector, a change in innovation efficiency is evident. However, in non-ferrous metals, steel, grain, and other industries with a slower pace of technological change, the industry may need more sensitivity in terms of innovation. Therefore, the conclusion of this study may only apply to high-tech industries, and it faces the challenge of theoretical robustness when extending to traditional industries. In future studies, we will verify the impact of supply chain finance on traditional industries.

Footnotes

Acknowledgements

We acknowledge the detailed guidance and comments offered to us by the SAGE Open editors and reviewers to improve the manuscript.

Author Contributions

JM, XW, and JY contributed to conception and design of the study, analyzed the data, and wrote the initial draft of the manuscript and putting forward the main propositions. XW and JY collected the data. JM was responsible for reviewing and editing the manuscript. All authors contributed to manuscript revision, and read and approved the submitted version.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Ethics Statement

Ethical review and approval was not required for the study on human participants in accordance with the local legislation and institutional requirements.

Data Availability Statement

The data analyzed in this study is subject to the following restrictions: The data was private and not available to the public. Requests to access these datasets should be directed to