Abstract

Green transformation leadership motivates employees to participate in the development of green products and processes, enabling the company to launch green products or services. Upper echelon theory suggests a link between leadership style, strategic decisions, and control systems that enhances overall performance. This study examines the impact of top managers’ green transformational leadership style on the selection of green production strategies, the implementation of environmental management accounting, and environmental performance, also considering the role of perceived environmental uncertainty as a moderator variable in the research model. A survey of 198 CEOs from Vietnamese manufacturing firms showed that all hypotheses were statistically significant. Findings suggest that CEOs with green transformational leadership play a vital role in improving environmental performance. Furthermore, aligning green transformation leadership style, green production strategies, and environmental management accounting enhances the environmental performance of Vietnamese manufacturers, which is crucial for maintaining long-term competitive advantage.

Plain Language Summary

This study is based on a survey of 198 CEOs of medium- and large-sized manufacturing enterprises in Vietnam. The results have shown the existence of relationships between the CEO’s green transformational leadership—green production strategy—environmental management accounting—and environmental performance. The appropriate application of this relationship enhances the environmental performance of the business. In particular, under the moderator impact of perceived environmental uncertainty, the behavior of choosing a green production strategy and using information from environmental management accounting are significantly affected. Furthermore, this study’s research model incorporates the upper echelons theory, a concept that has not received much attention in the accounting field thus far.

Keywords

Introduction

Leadership is vital for managing the environmental aspects of organizations (S. Zhou et al., 2018). Transformational leadership style encourages creativity and inspires colleagues, also to share the leader’s vision, enhancing the organization’s creativity and performance (Kaur et al., 2020). Past studies recommend that companies adopt top managers with green transformational leadership to inspire and encourage employees to exhibit environmentally friendly work behaviors, to achieve sustainable performance (Chen & Chang, 2013; Lathabhavan & Kaur, 2023). The green transformational leadership (GTL) promotes employees’ enthusiasm for environmental sustainability, fosters innovative green practices, and enhances the performance of eco-friendly businesses. Prior research indicates that green transformation leadership is significant and beneficial for company performance (Ng, 2017).

An eco-conscious firm often relies on green transformational leadership of top executives, leading to enhanced competitive advantage, as shown by Yang Spencer et al. (2013) and Özgül and Zehir (2023). Achieving environmental performance involves utilizing firm resources such as the CEO’s green transformation leadership, a planning process that integrates corporate strategy with ecological concerns, and the implementation of environmental management accounting. Environmental management accounting is gaining popularity as firms strive for sustainability (Ali et al., 2023; Appannan et al., 2023). Stakeholders have impacted the prioritization of environmental concerns and the evaluation of environmental performance by top managers (Rodrigue et al., 2013). Implementing environmental strategies and utilizing environmental management accounting are considered crucial competitive advantages for organizations seeking to enhance their corporate environmental management (Gunarathne et al., 2021; Liem & Hien, 2024a; Lisi, 2015).

Earlier research on the connection between accounting and sustainability has primarily focused on the disclosure of corporate social responsibility and how eco-efficiency influences company performance (Awaysheh et al., 2020; Hou, 2019; Hussain et al., 2018). Several critical review studies have identified persistent gaps in the literature that have not been explored, particularly regarding the impact of combined company resources like green transformation leadership, environmental strategy, and environmental management accounting on enhancing corporate sustainability efforts (Hanif et al., 2023; Hart & Dowell, 2011; Yang & Zhang, 2023). Furthermore, there has been limited empirical examination of these links to this day, especially without considering the context of emerging economies like Vietnam. Although green transformational leadership (GTL), green production strategy (GPS), and environmental management accounting (EMA) greatly influence environmental performance (EP), limited research exists on how these factors enhance EP within the manufacturing industry (Hanif et al., 2023; Liem & Hien, 2024b). Furthermore, little attention is given to the combination of EMA as a powerful support system in the process of implementing environmental strategies and achieving EP. Upper echelons theory (UET) provides a link between top managers’ GTL style, GPS, control system (EMA), and environmental performance of the organization (Hambrick & Mason, 1984). However, the application of UET to study these relationships is often overlooked, especially in the field of management accounting (Liem & Hien, 2024b). To enhance the organization’s eco-friendly reputation and gain a sustainable edge over competitors, businesses must minimize their negative environmental impact, adopt sustainable practices, develop and execute strategies that reduce waste, promote a healthy environment, conserve energy, and improve overall environmental performance (Hanif et al., 2023). Thus, this research aims to fill this void and enrich the current body of knowledge.

The Upper Echelons Theory was originally proposed by Hambrick and Mason (1984), and this theory has been used in this research to set up a model to consider how CEO’s GTL assists manufacturing companies in implementing GPS and EMA to improve EP. The context of Vietnam was chosen for this study for several reasons. In Vietnam, the implementation of ISO 14001 certification and corporate social disclosure remains voluntary, and warrants more comprehension (Filippini & Srinivasan, 2022; Q. A. Nguyen & Hens, 2015). In addition, Vietnam is facing the challenge of maintaining a balance between promoting economic development while still preserving the natural environment (X. P. Nguyen et al., 2021; Vo et al., 2023).

This research is expected to provide multiple contributions. Initially, it is the inaugural study that integrates the influences of GTL, GPS, EMA, and the moderating factor of PEU on the EP of firms. We propose that top management in manufacturing firms should adopt GTL, GPS, and EMA practices to develop and sustain the internal capabilities required to enhance green performance and achieve environmental performance (Hanif et al., 2023). Second, the findings of this study contribute to the growing body of empirical research exploring how leadership style, environmental strategy, and environmental accounting factors affect environmental performance, thereby responding to the call from numerous scholars for further investigation into this area (Hanif et al., 2023). The research model proposed in this study is more thorough than the ones examined by Hanif et al. (2023) and Yang and Zhang (2023). Additionally, the study considers the CEOs’ perceived environmental uncertainty (PEU) factor as a moderating variable in certain relationships. Thirdly, based on UET, this study provides a general guide for CEOs to understand, predict, control strategy, and design a control system within the organization. Currently, the UET is still rarely used in the field of management accounting. Fourthly, this research helps manufacturing enterprises properly coordinate resources to achieve optimal EP and a competitive advantage. Finally, this result can serve as a reference for top decision-makers in organizations to continuously improve EP.

Theoretical Background and Hypothesis Development

Upper Echelon Theory (UET)

Upper echelon theory was first published in 1984 by two authors, Hambrick and Mason. Over time, this theory has been supplemented by Hambrick et al. (2005). UET has demonstrated that the characteristics of upper managers, including demographic characteristics, psychology, and leadership style, have an impact on strategic choice behavior as well as the control system and overall organization performance. Based on UET, we determined that the top manager’s green transformation leadership characteristic would be an antecedent factor affecting the selection of GPS and EMA implementation, and the dependent variable would be EP.

The model chooses the managerial discretion factor as the moderator variable (Hambrick & Mason, 1984). Managerial discretion consists of three groups of factors: (a) environmental factors; (b) organizational factors; and (c) characteristics of the upper manager. Environmental uncertainty poses a significant challenge for top managers and plays a fundamental role in their decision-making (Townsend et al., 2018). Perceived environmental uncertainty reflects top managers’ perception of the environment and is a characteristic that highlights the difference in perception of different managers toward the environment. While top managers perceive high levels of uncertainty, their behavior changes dynamically in response to environmental factors (Schmitt et al., 2018). The research model selects perceived environmental uncertainty (PEU) as the moderator variable (see Figure 1).

Conceptual model of UET.

Green Transformational Leadership (GTL)

GTL is a leadership style characterized by leaders who recognize a need for change and effectively inspire and encourage individuals to pursue a shared goal actively (Avolio et al., 1999). All members of the organization raise awareness toward the sustainable development of the organization, as well as their personal responsibility to society (Begum et al., 2022). The cultivation of employees’ creativity relies on the presence of distinct attributes, which can be classified into four different dimensions: inspiring motivation, intellectual stimulation, charisma, and customized concern. Leaders employ inspirational motivation as a means to inspire and stimulate their followers, enhancing their enthusiasm for innovative thinking. Cognitive stimulation enables employees to gain diverse viewpoints, obtain knowledge, and resolve problems.

Green transformational leadership is demonstrated through managers motivating employees to achieve environmental goals or inspiring employees across the organization to achieve EP (Chen & Chang, 2013). This leadership style encourages people to prioritize organizational goals over personal ambitions, provides guidance and assistance in many situations, and fosters passion among employees to create innovative ideas for the organization (F. H. Awan et al., 2023). According to Chen and Chang (2013), employees tend to exhibit greater creativity and innovation when supervisors encourage and support novel ideas, present constructive challenges, and share a forward-thinking vision. Top managers with GTL style will play an important role in motivating and guiding their subordinates to actively participate in environmentally friendly activities and initiatives (S. Zhou et al., 2018).

Green Production Strategy (GPS)

The extent to which environmentally friendly business operations and processes are integrated into a company’s strategy is known as the company’s environmental strategy (Banerjee et al., 2003). Environmental tactics are often driven by laws or competition rather than the company’s fundamental beliefs (Paulraj, 2009). A green production plan in modern manufacturing is a manifestation of the sustainable development strategy (Zameer et al., 2020). The term “green” is frequently replaced with “sustainable,” referring to items made from environmentally friendly resources, produced using eco-friendly methods, resulting in environmentally friendly results, and being environmentally friendly when disposed of (Zhang et al., 2022). These are common attributes associated with green manufacturing (D’Angelo et al., 2023). Junior et al. (2018) and Baah et al. (2021) argue that the GPS of corporate is aimed at minimizing negative environmental impacts from production activities rather than eliminating these negative impacts.

Environmental Management Accounting (EMA)

Daft and Weick (1984) argued that EMA is a management tool that provides financial and non-financial information to help management optimize economic performance and minimize negative environmental impacts. The EMA system provides necessary information for CEOs to help reduce their company’s environmental impacts and improve decision-making under external pressures (Daddi et al., 2016; Swalih et al., 2024). EMA collects, analyzes, and reports physical information (on energy use, raw materials, waste) and monetary information (on costs, profits, savings) related to the environment. Thereby, helping to increase economic efficiency and promote sustainable business development. EMA involves combining environmental and economic accounting information to show how they are interconnected and impact corporate performance due to managers’ decisions (Gerged et al., 2024). Organizations can gather, compile, and evaluate environmental data using a system such as EMA (Schaltegger & Burritt, 2017). The EMA can provide top management with pertinent information on pollution reduction, aiding in decision-making and performance management (Qian et al., 2011).

Environmental Performance (EP)

Environmental performance refers to the ability to reduce the level of environmental impact, minimize environmental damage caused by an organization’s activities, demonstrate the organization’s responsibility toward the environment, or achieve results in organizational governance that minimize environmental impact (Aftab et al., 2023). ISO 14031 defines EP as the outcome of an organization in handling its environmental factors. Various definitions of EP exist, but they typically emphasize the results of management actions related to the environment and the activities themselves. This aligns with the definition of environmental performance as outlined by ISO 14031. We contend that the ISO 14031 definition is comprehensive and concise, meeting the criteria for a good definition as outlined by Suddaby (2010) and Mansour et al. (2021). It can be viewed as a widely accepted definition that incorporates the key features of previous academic definitions. ISO 14031 helps organizations measure, evaluate, and improve their environmental impacts by setting indicators, targets, and considering the relationship between operations and the environment (Wagner, 2020).

Perceived Environmental Uncertainty (PEU)

Environmental uncertainty refers to an unpredictable situation, such as climate change or natural disasters, as well as the uncertainty of market dynamics, including consumer needs, competitive challenges, and technological advancements (Darvishmotevali et al., 2024). These factors prompt companies to take action, either presently or in the future (Pondeville et al., 2013). According to Lewis and Harvey (2001), this alteration resulted in the emergence of novel uncertainties about the natural environment, sometimes referred to as ecological environmental uncertainty. Several studies have provided evidence that environmental uncertainty within the natural environment has the potential to significantly impact an organization’s environmental strategy and accounting practices (Latan et al., 2018; Lewis & Harvey, 2001). According to López-Gamero et al. (2011), managers may experience a sense of uncertainty regarding the trajectory of forthcoming technology, legal frameworks, evolving consumer preferences, and social norms, as well as the operational consequences arising from regulatory changes. The presence of unpredictability can serve as a catalyst for a corporation to engage in investment activities, implement significant changes, and undertake substantial commitments. The corporation undertakes these actions to identify competitive opportunities and facilitate experimentation with new strategies.

Hypothesis Development

Green Transformational Leadership and Green Production Strategy

The leadership style approach of top executives within organizations is vital for the selection and execution of strategies (Hambrick & Mason, 1984). According to Çop et al. (2021), GTL plays an essential role in promoting environmental sustainability initiatives, as noted by Li et al. (2020). This leadership style fosters green innovation by leveraging current market insights and trends, acquiring financial resources, adopting cutting-edge green technologies, and training employees to support innovative processes (Xie et al., 2019). These leaders shape their team members’ perceptions, attitudes, thoughts, and understanding of environmental issues, while also motivating them to share their views on sustainable manufacturing practices (Chen & Chang, 2013). GTL increases the likelihood of achieving green innovation (U. Awan et al., 2021). According to S. Zhou et al. (2018), CEOs who adopt a green transformational leadership (GTL) style play a crucial role in shaping environmentally friendly production strategies. The strategic resources linked to GTL serve as essential assets that enable firms to acquire new knowledge and promote the development of green products and processes in the marketplace (Begum et al., 2022).

Green Transformational Leadership and Environmental Performance

Transformational leaders positively impact organizational performance through their behavior and attitude, as well as employee engagement, economic health, green performance, and psychological performance (Barling et al., 2009). How employees perceive the environmental performance of their organization is strongly influenced by the green transformational leadership style of top management (Zhu et al., 2005). Multiple studies have demonstrated a strong connection between transformative leadership and positive organizational results (Chang et al., 2014). Green transformational leaders who approach problems with innovative perspectives by inspiring effectively and fostering collaboration among team members can enhance perception, learning, integration, and coordination (Overstreet et al., 2013). GTL positively impacts EP by promoting green work engagement within its organization (Çop et al., 2021).

Green Transformational Leadership and Environmental Management Accounting Implementation

Control systems are selected, implemented, designed, and used by top management (Hambrick & Mason, 1984). A leadership style will have a major impact on the way a manager uses accounting information (Naranjo-Gil et al., 2006; Liem & Hien, 2024b). The leadership style of a manager impacts the utilization of accounting information for decision-making (Avolio, 2010). GTL entails leaders inspiring and motivating their followers to go beyond expected environmental performance levels and to actively pursue the achievement of environmental objectives (Chen & Chang, 2013, p. 109). Traditional accounting standards will not provide the necessary and complete information for managers to assess and monitor the impact of their organization’s production and business activities on the environment (Novovic Buric et al., 2022). EMA is a part of business management accounting that helps improve business performance in both financial and environmental aspects (Burritt et al., 2002). EMA is associated with the information needs of environmental management in organizations, assisting managers in the decision-making process (Sánchez-Medina et al., 2014).

Green Production Strategy and Environmental Performance

The effectiveness of a strategy significantly influences the overall performance of an organization (Hambrick & Mason, 1984). Kraus et al. (2020) found that having an environmental strategy leads to notable improvements in environmental performance. Environmental strategies consist of various actions aimed at reducing the adverse impacts of business operations on the environment (Liu et al., 2005). Such actions include using sustainable resources, conserving energy, minimizing waste, and establishing environmental management systems (Zhang et al., 2022). When top management prioritizes environmental concerns, it allows the organization to create a guiding framework (Hart & Dowell, 2011). Manufacturing firms that implement proactive strategies tend to achieve higher levels of environmental performance (Rodrigue et al., 2013).

Green Production Strategy and Environmental Management Accounting Implementation

For environmental initiatives to be successfully implemented, they must be gradually incorporated into all aspects of the organization’s control system (Jonsson, 2000). A high fit between organizational structure and governance systems will greatly promote the successful implementation of strategy (Gerdin & Greve, 2004). EMA supports managers in making long-term strategic decisions, such as production optimization, technology investment, and product development, which benefit both the economic and the environment (Le et al., 2019). EMA collects, analyzes, and reports physical and monetary information (on costs, profits, savings) related to the environment (Latan et al., 2018). EMA information facilitates efficient decision-making and enhances environmental performance by managing environmental costs and leveraging available benefits (Le et al., 2019).

Environmental Management Accounting Implementation and Environmental Performance

Ferreira et al. (2010) state that EMA helps organizations fulfill environmental duties and discover financial gains from enhanced ecological and economic efficiency. Z. Zhou et al. (2017) indicated that this method reveals information that companies can use to achieve better environmental and financial results. EMA implementation allowed managers to maximize resource use and enhance EP (Pondeville et al., 2013). EMA can improve an organization’s EP by providing information and insights into its management systems related to environmental issues, leading to better decision-making (Chaudhry et al., 2020). Systems aim to achieve corporate goals and sustainable environmental results (Guenther et al., 2016). Previous studies show that implementing EMA can boost a firm’s EP (Asiaei et al., 2022).

The Moderator Role of Perceived Environmental Uncertainty

PEU is a cognitive trait of top managers, and this trait is a factor of managerial discretion; therefore, top managers’ traits play a moderating role in UET (Hambrick & Mason, 1984). PEU is predicted to moderate the relationships between: (a) top managers’ leadership style and organizational strategy, and (b) top managers’ leadership style and organizational control systems (such as EMA).

The environmental strategy can be influenced by the unpredictable character of the environment (Lewis & Harvey, 2001). Certain scholars in the field of strategy suggest a clear correlation between the perception of environmental uncertainty and the implementation of proactive strategies (Miles et al., 1978). GTL style is particularly suitable in a company with less stable situations (Bass, 1990). In light of the uncertain circumstances, managers are likely to exhibit heightened levels of assertiveness, engage in greater risk-taking, and employ more innovative strategies to adapt to an increasingly volatile corporate landscape, as evidenced by the research conducted by Miles et al. (1978). Companies must take initiative in adopting innovative strategies to effectively handle the interaction between their operations and their environmental surroundings (Shrivastava & Hart, 1995). According to Asiaei et al. (2022), when organizations perceive the business environment as characterized by uncertainty, they tend to allocate resources toward enhancing organizational capabilities and adopting a green production strategy.

The unpredictability of the environment can markedly influence an organization’s accounting functions. Today’s companies face challenges due to environmental uncertainty, which stems from a lack of understanding in management accounting and the swift accessibility of environmental information (Latan et al., 2018). In the face of considerable uncertainty, leveraging intelligent information can enhance managerial decision-making and lessen environmental impacts by offering various alternatives and solutions. Research by Chang and Deegan (2010) indicates that environmental uncertainty drives the adoption of EMA. EMA information is used to monitor and assess EP by developing and implementing suitable environmental accounting practices (Phan et al., 2017). In an organization, EMA plays a vital role in environmental conservation (Asiaei et al., 2022).

Figure 2 presents the research model built by the authors.

Proposed research model.

Methodology

Variables Measurement

This study inherits the measurement scales constructed and used in previous studies. The GTL scale is derived from Singh et al. (2020)‘s study and comprises four items. The GPS scale includes four items, inherited from the research of Zameer et al. (2020). The EMA implementation scale includes six items and is based on the research of Chaudhry et al. (2020). The EP scale is based on the research of Lisi (2015) and Yang Spencer et al. (2013). The scales of the PEU variable are inherited from the study of Latan et al. (2018).

The survey questionnaire used in this study consisted of two distinct components. In the initial phase, we gathered demographic information on the participants, as well as additional details such as tenure and age. The second part of the study included questions on GTL, GPS and EMA implementation, firms’ EP and CEOs’ PEU. In the second part of the questionnaire. We employed a 5-point Likert scale ranging from 1 (strongly disagree) to 5 (strongly agree). The contents of the scales are presented in Table 1.

Variables Measurement.

Sample and Data Collection

Manufacturing firms are the primary focus of EMA research due to their high resource consumption and environmentally hazardous practices (Latan et al., 2018). Therefore, it is worthwhile and intriguing to research how the EMA is used in this field, since it may have implications for the Vietnamese governments and companies. An important component of strategic planning is the practice of using accounting information to make decisions by executives. The strategic decisions are significantly influenced by the CEOs of manufacturing businesses. Therefore, the respondents to the survey were chief executive officers of the organization. According to the Ministry of Planning and Investment (2020), the majority of manufacturing enterprises in Vietnam are located in the southern region. This is due to the favorable economic and topographic conditions found in the southern region of Vietnam. The CEOs will receive the questionnaire and a cover letter. We distributed the survey instrument using a web-based approach since it enables faster and more affordable data collection from a large, geographically dispersed sample (Couper, 2008; Dillman et al., 2014). We adhere to web and mobile survey criteria published by Dillman et al. (2014) when creating and executing the survey. We conducted pretesting in accordance with Mokhtar et al.’s (2016) method before distributing the official questionnaire.

Consequently, the questionnaire underwent a pretesting phase, including three CEOs who possess expertise in the relevant domain. To incorporate the feedback, we made adjustments to the questionnaire, such as changing the order of questions in the questionnaire and changing the wording to increase the clarity and comprehensibility of the questionnaire. In addition, we conducted pilot interviews with five experienced CEOs on the web version, and then continued to make some minor adjustments to the questionnaire based on the suggestions of these CEOs.

This study was conducted in accordance with ethical principles and established research codes of conduct. Participants were business executives (CEOs) over 18 years old, surveyed both online (via Google Forms) and in person. For the online survey, written informed consent was obtained electronically, as respondents could proceed only after ticking a box confirming that they had read the study information and agreed to participate. For the in-person survey, informed consent was obtained verbally after the same information had been provided. In all cases, participation was voluntary, anonymity was maintained, and no sensitive personal information was collected.

The survey questionnaire targets over 3,276 CEOs of manufacturing enterprises in Vietnam who have personal email addresses (collected through the companies’ websites, business clubs, and business associations, etc.). The convenience sampling method was chosen to conduct sampling for this study because there was relative homogeneity in the population (Malhotra et al., 2007). The survey will be conducted through two methods: (a) a Google Form survey, where, upon receiving an email invitation to participate, the CEOs will click on the link attached in the email and complete the designed questionnaire. We sent an email inviting participants to participate in the survey, and then we continued to send three more emails to individuals who did not respond. In addition, we directly called individuals who accepted to participate in the survey but did not return the questionnaire (Latan et al., 2018). And (b) a direct survey through the authors’ connections, where the questionnaire is sent directly to the CEOs. Small businesses are excluded from the official study sample because, with this type of business, they often lack the resources to design a control system (like EMA) within their organizations (T. T. Nguyen, 2014). The PLS-SEM analysis addresses the drawback of small sample sizes in research by stringent criteria, and the study employs bootstrapping when testing hypotheses (Liem & Hien, 2020a). Therefore, the results still ensure reliability, accuracy, and can be representative of the population.

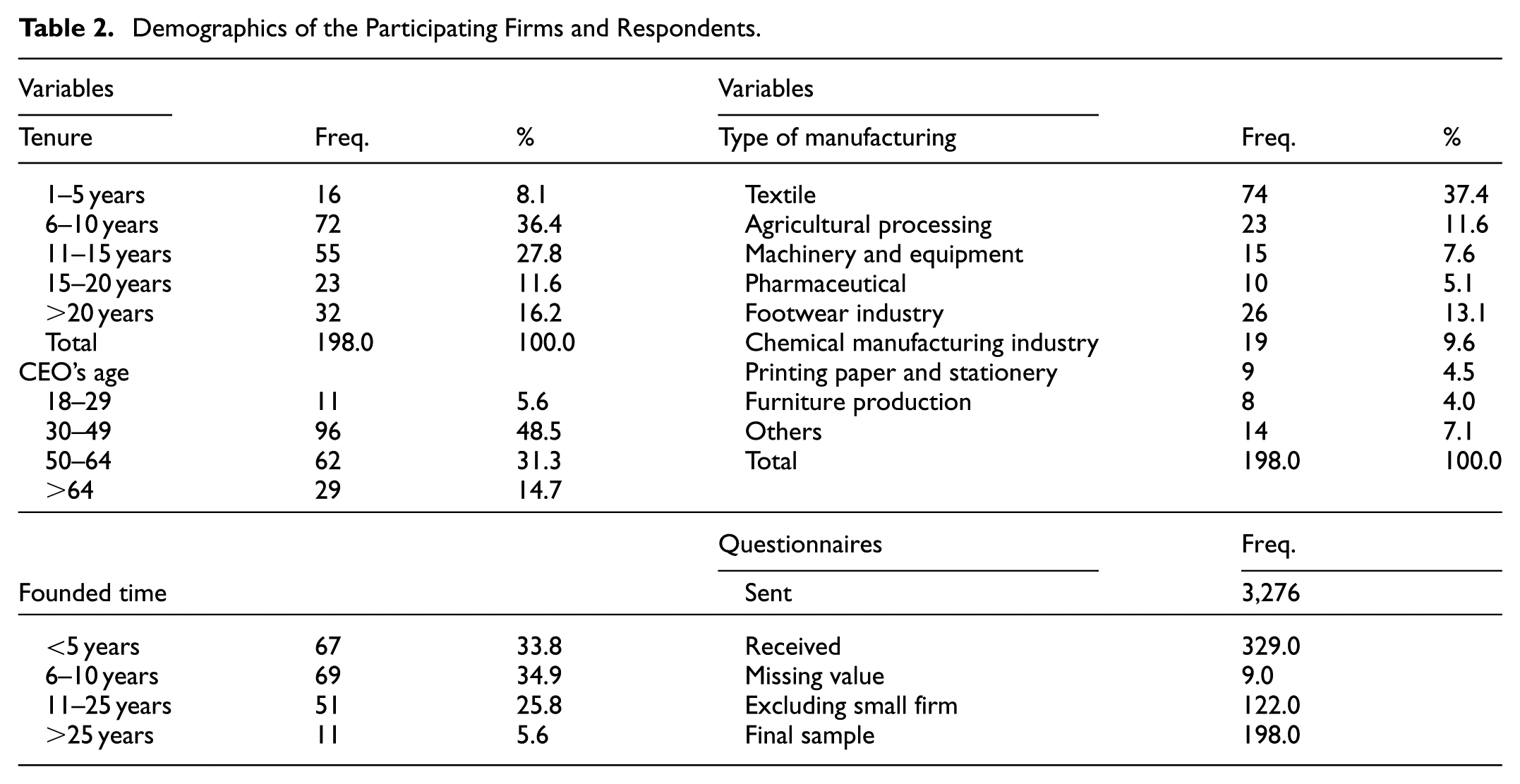

Following the 4-month survey administration period in 2023, a total of 329 responses were received. However, 9 responses were incomplete, and 122 responses from small-scale firms were excluded from the analysis, leaving 198 legitimate responses (6.04% usable response rate). Previous studies on the development of EMA implementation in industrialized nations found a similar low response rate (Christ & Burritt, 2013; Mokhtar et al., 2016). Table 2 shows the profiles of the respondents’ firms.

Demographics of the Participating Firms and Respondents.

Results

This study employs PLS-SEM, Version 3 of SmartPLS (Ringle et al., 2015), for data analysis. The field of management accounting and control literature widely uses Version 3 (Heinicke & Guenther, 2020). The use of the Partial Least Squares (PLS) is justified by its suitability for conducting causal-predictive analysis on complex models (Chin & Newsted, 1999). Moreover, the use of a small sample size has always been a problem considered by many researchers; however, this problem has been overcome when using the PLS method (Chin, 1998).

Measurement Model

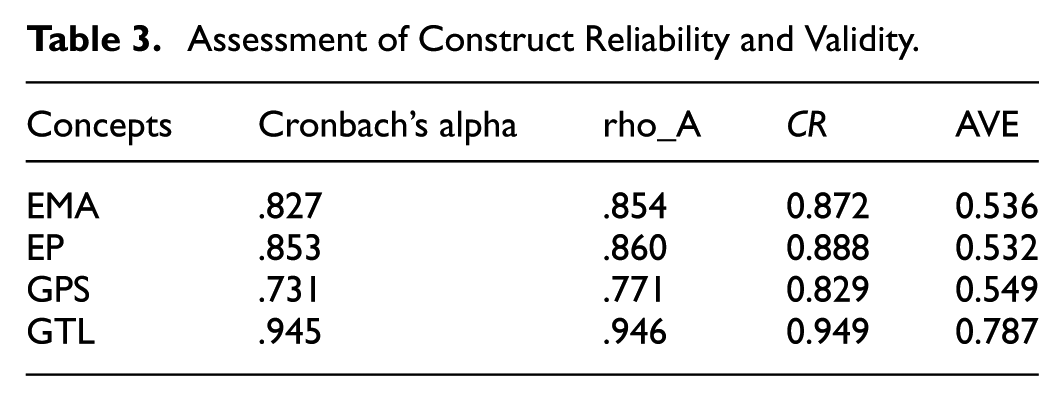

All the values in Table 3 support the convergent validity because they exceed the predetermined threshold values (Fornell & Larcker, 1981). This measure reflects the reliability of the items associated with each construct, and all factor loadings exceeded the recommended threshold of 0.7, except for the two lowest factor loadings, which were 0.649 and 0.599 (Figure 3). The reliability of the items is further reinforced by rho_A (Dijkstra & Henseler, 2015). The structural model’s output was deemed satisfactory.

Assessment of Construct Reliability and Validity.

Results from model analysis using PLS-SEM.

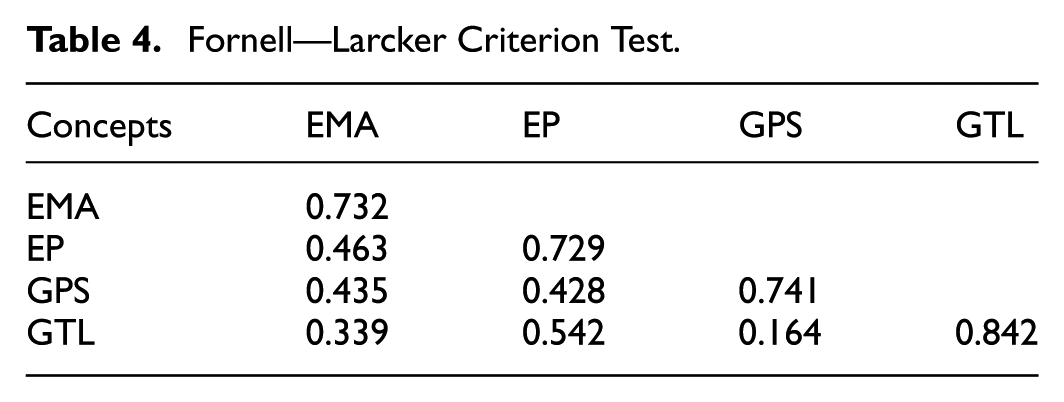

The results presented in Table 4 show that the AVE value has been reinforced and proves that the discriminant validity in the study is guaranteed.

Fornell—Larcker Criterion Test.

As demonstrated by Hair et al. (2017), Table 5 shows HTMT values that are below the predetermined cutoff of 0.90, demonstrating the existence of discriminant validity.

Heterotrait-Monotrait Ratio (HTMT).

Structural Model

Due to the absence of distributional predictor assumptions in PLS, the statistical significance of raising the route coefficient is assessed through the utilization of bootstrapping (Hair et al., 2017). Before evaluating structural correlations, collinearity should be tested to avoid bias in regression results. All VIF values in this study were less than 5 (Hair et al., 2017). R2 values of .75, .50, and .25 are categorized as strong, moderate, and weak, respectively, by Hair et al. (2017). The model’s EP, EMA implementation, and GPS have respective R2 values of .690, .542, and .485. To assess R2, the effect size (f2) is used. The f2 coefficient is used to assess the impact level of the independent variable on the dependent variable, and thresholds such as 0.02 show that the impact level is weak, threshold 0.15 shows that the average level, and above the threshold value 0.35 shows that the impact level is strong (Hair et al., 2017). According to the findings, GTL (f2 = 0.212) shows a substantial impact on EP, whereas EMA (f2 = 0.072) and GPS (f2 = 0.095) show small effects. Researchers also added the Q2 value as a criterion to enhance the predictive accuracy of the R2 value. This measurement serves as an indication of the model’s out-of-sample predictive power. Low, medium, and high predictability are indicated by Q2 values of 0.02, 0.15, and 0.35, respectively. For GPS, EMA, and environmental performance, the corresponding Q2 values are 0.204, 0.242, and 0.407. The SRMR value should be less than 0.08 or 0.10 when analyzed by PLS-SEM (Hu & Bentler, 1998); the current study reports a SRMR value of 0.06.

To examine the proposed hypotheses, the authors employed the PLS-SEM technique. The outcomes of this analysis are displayed in Figure 3 and Table 6. The obtained results showed that the green transformational leadership style of top managers has a positive impact on the choice of GPS, EMA implementation, and EP. All the hypotheses tested were statistically significant with a p-value < .05. Hence, sufficient evidence exists to support hypotheses from H1 to H6.

Hypothesis Testing.

One of the issues that needs to be clarified in this study is how PEU acts as a moderating variable. The analysis shows that PEU measurement concepts are reliable (with Cronbach’s alpha over .8, CR above 0.9, and AVE above 0.7).

The choice of method to analyze the impact of the moderator variable in the research model has been considered by the authors. In which the two-stage method has shown its superiority. According to Chin et al. (2003), the two-stage moderator analysis involves a causal approach where the first stage examines the relationship between independent and moderator variables, while the second stage assesses the link between moderator and dependent variables.

The relationship between GTL and GPS is influenced by CEOs’ PEU, as indicated by Table 7 and Figure 4 (β = .181; p < .05). Similarly, the connection between GTL and EMA implementation is also influenced by CEOs’ PEU (β = .214; p < .05), illustrated in Figure 5. Higher CEO’s PEU enhances the effect of GTL on GPS and EMA implementation. Thus, both hypotheses H7a and H7b are validated.

Testing Results for Moderator Effects.

PLS-SEM results for the moderating effect (GTL × PEU → GPS).

PLS-SEM results for the moderating effect (GTL × PEU → EMA).

Discussion

The findings indicate that hypotheses H1, H2, and H3 were confirmed. In advancing the organization’s green production strategy, green transformational leadership, which is an aspect of top managers’ sustainable development, cannot be overlooked (Begum et al., 2022; S. Zhou et al., 2018). Green transformational leadership contributes to the enhancement of the organization’s green production strategy by actively fostering a favorable green psychological climate and providing material and spiritual support to employees (Xie et al., 2019). The creation of a favorable green psychological climate by employees, who have received both material and spiritual support from top leaders, serves as a motivating factor for them to participate actively in their work, adopt environmentally friendly behaviors, and recognize their personal obligation to enhance the organization’s green product. Environmental performance was another factor that was investigated in this study. EP is substantially influenced by green transformational leadership, which is consistent with the findings of Çop et al. (2021) and Zhu et al. (2005). This may be because the green transformational leader inspires confidence and optimism in his/her followers, emphasizes values through symbolic actions, provides practical examples, and empowers them. The green transformational leader will inspire and boost the self-esteem of their followers as they collaborate to improve environmental performance. Furthermore, the findings provide evidence to support H3 in full. This research further corroborates the findings of Sánchez-Medina et al. (2014), when top managers possess green transformative leadership, they are more likely to embrace an information system, such as EMA, that enables them to gather environmental-related information. The EMA is regarded as a valuable resource that provides environmental-related information, supported by environmental performance indicators. The findings of Begum et al. (2022), Xie et al. (2019), and S. Zhou et al. (2018) are supported by this result.

Based on the results above, we found that hypotheses H4 and H5 were verified. Green production strategies have been shown to improve environmental performance. The results supported the findings of Kraus et al. (2020) and Quan et al. (2018), who discovered that environmental strategies considerably improve environmental performance. Green production is a significant resource for Vietnam’s industries as they strive for a more environmentally friendly and sustainable economy. The greening of production also creates new needs for businesses, aligning with the overall trend of development, while also strengthening their position and competitiveness in both home and foreign markets. The green production strategy has a good and significant impact on the implementation of the EMA. A well-implemented environmental management accounting system helps managers in the process of implementing and pursuing green production strategies to make important decisions, such as lowering production costs, increasing productivity, investing in machinery to produce better, greener, and higher-quality products, resulting in lower prices to meet customer demands. This finding is consistent and adds experimental support to studies by Gerdin and Greve (2004), Latan et al. (2018), and Le et al. (2019). Environmental management accounting provides information that evaluates a company’s profitability, revenue, and environmental costs, allowing top managers to make valuable decisions. If the EMA is applied appropriately, businesses can minimize input elements such as raw materials, energy, and labor used in pollution generation, boost resource efficiency, gain a competitive advantage, and improve their environmental performance. So the hypothesis H6 is accepted, and the results are consistent with the study of Asiaei et al. (2022).

Another goal is to determine whether perceived environmental uncertainty can act as a moderator in two relationships: (a) GTL and GPS, and (b) GTL and EMA implementation. This objective pertains to the testing of H7a and H7b, which was fully supported. Many scholars have found that environmental uncertainty is one of the factors that encourages the adoption of EMA, and perceived environmental uncertainty also has an impact on the choice of an innovative strategy (Aragón-Correa & Sharma, 2003; Bass, 1990; Lewis & Harvey, 2001). CEOs are facing both environmental and market uncertainty. Under the CEOs’ PEU, there is an increasing demand for green production strategies that satisfy market demand as well as for environmental information. The utilization of a GPS strategy by the CEOs and the implementation of EMA are perceived as practical measures that assist top managers in making informed decisions within uncertain environments. The implementation of GPS guarantees a sustainable production process for businesses. The results of this study are consistent with the findings of Lewis and Harvey (2001), who observed that environmental uncertainties have an impact on the accounting procedures of organizations. Furthermore, this experimental work adds to the evidence and reinforces the UET proposed by Hambrick and Mason (1984). In addition to confirming the moderating role of the external environment in the interaction between the top manager’s leadership style (GTL) and: (a) selecting an environmental strategy (GPS); and (b) the organization’s management system (EMA).

Conclusions

Theoretical Implications

Our study makes multiple contributions to the existing body of literature. Firstly, the impact of integrated organizational resources, including intangible assets, on the continuous enhancement of EP was investigated in this study. We responded to the calls of Christ and Burritt (2013), Latan et al. (2018), and Hanif et al. (2023) to extend their testing, taking into account the consequences of implementing the EMA. Secondly, our research contributes to advancing the UET theory (Hambrick & Mason, 1984) by understanding and explaining the reasons behind the shift toward green innovation and the EP of enterprises. Furthermore, applying UET offers a theoretical basis for understanding how and why top executives foster green innovation and enhance environmental performance within their organizations. The integration of GTL, GPS, EMA, and EP in this research is a necessity, as suggested by Hiebl (2014) and Vo et al. (2023). A more comprehensive understanding of GTL’s effects on strategy, control systems, and EP is thereby facilitated, as suggested by Hambrick and Mason (1984). The dominant behavioral perspective in the existing literature regarding CEOs’ leadership in green transformation proves effective in improving employees’ skills, motivations, and prospects. However, it does not thoroughly explain the internal processes within a company striving to achieve its environmental performance objectives. The UET framework offers a different approach that seeks to explain the involvement of top management in linking various resources. The concept of UET, which recognizes the importance of EP on a company’s competitiveness, has been widely supported by scholars such as Marcus and Fremeth (2009). The findings of our study highlight the significance of GTL, GPS, and EMA implementation in facilitating the achievement of the company’s EP. Thirdly, this study adds to the current understanding of GTL style by investigating how top leaders participate in collecting data regarding the environment. Leaders, which seeks to influence people to achieve an organization’s strategic objectives, have historically evolved independently until recently. Our research reveals a form of leadership that can be derived from CEOs, which remains relatively underexplored. Scholars argue that the support of CEOs and other top executives is essential for realizing the benefits from GPS and EMA (Begum et al., 2022; Sánchez-Medina et al., 2014). This suggests that when the leadership style of top leaders, GPS, and EMA have the same underlying values, the effects are maximized (Hambrick & Mason, 1984; Liem, 2021; Liem & Hien, 2020a, 2020b; Vo et al., 2023). Further investigation in the field of leadership style has the potential to enhance our comprehension of green transformational leadership, GPS, and EMA, as suggested by Zhu et al. (2005). In addition, when using UET to demonstrate how GTL integrates with GPS and control systems like EMA, we believe that top leadership is a valuable resource that serves as a competitive advantage, one that other companies struggle to replicate (Begum et al., 2022). Therefore, based on the results of this study, we believe that CEOs with GTL characteristics are a strategic resource that companies should leverage to form and implement GPS as well as EMA, thereby influencing the process of green innovation and environmental performance. Fourthly, the UET model identifies managerial discretion as a moderator role. Numerous scholarly investigations have advocated for more exploration of moderator variables of UET (Hiebl, 2014; Pavlatos & Kostakis, 2018; Vo et al., 2023). The PEU is considered an external environmental component, and this study utilizes PEU scales to assess several environmental factors, including the environmental laws implemented by governments in the regions where firms operate, as well as the strategies taken by competitors in connection with the natural environment. Hence, the introduction of the PEU as a moderator variable is regarded as a noteworthy theoretical contribution to this research. The benefit of PEU helps top managers identify aspects of the organization’s business environment that CEOs perceive as highly volatile, allowing them to develop appropriate strategies and actions in response. The findings from this study indicate that the aspects above become more uncertain as societal interest increases. Especially when the influence of PEU on the process of implementing GPS and control systems, such as EMA, is significant. The CEOs with PEU will significantly impact their management behavior. The results of this study indicate that the perception of an unstable environment significantly affects the ability to implement GPS processes as well as the design and implementation of the organization’s green control systems. In this context, maintaining and improving the organization’s green competitive position will reflect the green governance capabilities of top managers in coping with the uncertainty they face. Finally, this study contributes to the call by Hiebl (2014) and Hambrick (2007) for further research to explore the moderating variables when using UET. Vietnamese enterprises should implement environmental accounting practices that yield sustainable advantages for both the community and the organization. In general, the results of our research enhance the current body of EMA literature in developing countries by offering additional insights from a transitional economy such as Vietnam, which has its distinct cultural, socioeconomic, and political features.

Managerial Implications

Our study makes a significant contribution to the practice in several ways. Our findings indicate that utilizing GPS and EMA to enhance EP can be highly beneficial when accompanied by a CEO with GTL. Additionally, based on the use of UET and the results of this study, we propose that the company should design and implement activities related to GPS and EMA to enhance green innovation and EP under the continuous supervision of CEOs with GTL characteristics. Likewise, it would be hasty to recommend actionable steps solely on the results of this one study. Nonetheless, a growing body of research suggests that a company’s EP is influenced by a mix of social settings, characteristics of the top leader, strategic choices, and an established formal control system, including an EMA system. Top leaders in Vietnamese manufacturing companies must strategically combine these resources to attain peak ecological effectiveness, thereby creating a sustainable competitive advantage for the organization. Additionally, reaching the highest levels of EP is a demanding endeavor and should be regarded as an opportunity for transformation and positive influence. The primary focus of this study pertains to the perception and behavior exhibited by chief executive officers (CEOs). Furthermore, the effective execution and distribution of this communication throughout the entire business are crucial. Upper-level executives must articulate the principles, skills, and advantages of transitioning into an environmentally friendly enterprise, as well as the reasons behind its necessity.

In recent years, the subject of environmental deterioration, as well as the growing phenomenon of climate change, has received substantial and increasing attention. As a result, there is an increasing desire for firms to take responsibility for resolving society’s growing concerns. Top leaders of Vietnamese manufacturing businesses cannot ignore the green transformation trend in a market that is increasingly demanding environmentally friendly products. Integrating green production strategies into the core of development strategies will be critical for firms seeking to increase their competitive edge, attract foreign investment, and transition to a green economy effectively and sustainably. According to the findings of this study, the successful adoption of a green production strategy must begin with top-level leadership understanding. The agreement and determination of top managers are critical to the effective implementation of a GPS or a green transition. Consider selecting a CEO who is concerned about environmental issues and can lead the entire organization in successfully implementing environmental performance, which should be viewed as a critical component of sustainability initiatives within Vietnamese businesses. Furthermore, to successfully implement a GPS, top managers should demonstrate GTL and a sustainable strategic orientation. They also need to embed environmental sustainability into operational processes and organizational culture, effectively manage organizational change, and establish mechanisms to measure, monitor, and analyze data. These mechanisms enable firms to assess how green production strategies affect business value across dimensions such as brand equity, market share, operating costs, and revenue.

Limitations and Future Research Directions

Future researchers can examine some limitations of this work. First, although this study solely focuses on GTL, top managers’ leadership styles can take many other forms. Thus, this feature has to be investigated further in future research. Second, because this study is cross-sectional, it requires an extended period of time to assess its EP before, during, and after GPS and EMA were implemented. Lastly, the implementation of the EMA and the financial performance of environmental measures must be measured in future studies.

Footnotes

Ethical Considerations

The authors declare that all research involving human participants was conducted in strict accordance with the Declaration of Helsinki or comparable ethical guidelines. Participants (CEOs) remained anonymous, participation was entirely voluntary, and no sensitive personal data were collected.

Consent to Participate

The survey was administered both online and in person. For the online survey, written informed consent was obtained electronically by requiring participants to tick a box confirming that they had read the study information and agreed to participate. For the in-person survey, informed consent was obtained verbally after the same information had been provided. In all cases, participants were informed of the study’s purpose and their right to withdraw at any time before submitting their responses.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study is funded by Van Hien University, Vietnam and Industrial University of Ho Chi Minh City, Vietnam.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data supporting this study’s findings are available from the corresponding author upon reasonable request.