Abstract

Climate change is bringing unpredictable risks to human beings. Green finance will strongly promote economic transformation. Drawing on a 2006 to 2021 provincial panel and guided by a multi-channel theoretical framework, this study econometrically evaluates how green finance affects regional carbon abatement. The results show that green finance significantly promotes the total amount of carbon emissions abatement by playing the functions of resource allocation and risk management, and this conclusion passes the robustness test. The mediating effect between them mainly includes energy structure adjustment, industrial structure optimization, and technological innovation. The interaction test reveals that green finance interacts with (i) energy-structure adjustment, (ii) industrial-structure optimization, and (iii) technological innovation; these three pairwise interactions are mutually reinforcing and, through their coordinated development, jointly curbing carbon emissions. Furthermore, there is regional heterogeneity in this kind of influence. Due to the large space of industrial low-carbon transformation, this effect is more pronounced in the central and western regions. Further tests show that green finance can simultaneously reduce carbon emissions and control air pollutants, which means the significant “from pollution to carbon” synergistic effect of green finance. This study provides valuable insights into how China can promote its dual carbon goals through green financial tools from the perspective of regional heterogeneity.

Keywords

Introduction

Climate change is triggering global environmental risks, prompting worldwide consensus on the imperative of a low-carbon transition. Against this backdrop, China’s “2030 Carbon Peak, 2060 Carbon Neutrality” target is not only a practical commitment to the Paris Agreement but also a core strategy to drive the economic growth model from resource dependency to innovation-driven transformation.

Green finance is pivotal for low-carbon development (Ji & Zhang, 2019; Soundarrajan & Vivek, 2016). Lee (2020) emphasizes that green finance requires collaboration between the government and the market. Governments must establish policy frameworks, such as green bond standards and information disclosure mechanisms, to enhance market transparency, while the private sector should channel capital toward green initiatives through banking systems, bond markets, and institutional investors. Green finance, as a broad term, encompasses capital flows into sustainable projects, eco-friendly products, and policies that foster a sustainable economy. Goshu and Tadesse (2022) clarifies that green bonds specifically fund projects with significant environmental benefits, green credit supports eco-friendly projects via mortgage and industrial loans, and green funds provide long-term financing for environmentally conscious enterprises. In China, green finance refers to financial services provided for green industries, energy, transportation, construction, etc. In order to promote green finance development, China began to implement the construction of Green Finance Reform and Innovation Pilot Zones (GFRIPZ) in 2017. The effectiveness of this policy in facilitating the transition to low carbon and green investment has been confirmed by recent studies (Chen et al., 2025; Cui et al., 2024). As a result, China’s green finance has witnessed a sharp increase. The outstanding scale of green bonds surpassed 1.2 trillion yuan, securing the second position worldwide. Green finance plays a catalytic and supportive role in achieving low carbon development.

Although existing researches have preliminarily confirmed that green finance is conducive to promoting environmental improvement, three significant limitations remain. First, the research perspective focuses on how green finance affects environmental pollution (e.g., SO2, PM2.5) or carbon emission intensity. This indicates that these studies have overlooked the direct regulatory role in the total carbon emissions. However, the decline in carbon emission intensity may be accompanied by an increase in total emissions due to economic expansion, which does not truly reflect the effectiveness of emission reduction. This focus on intensity or productivity is common in recent literature (J. Li et al., 2024; W. Liu & Zhu, 2024). Second, the mechanism of action, particularly the interplay between different channels, remains unclear. Although theoretical deductions have been made on how green finance mitigates carbon emissions by catalyzing shifts in the energy mix, industrial upgrading, or technological innovation (H. Li et al., 2025; Ran & Zhang, 2023), there is a lack of empirical support based on provincial panel data for mediating effects, and the interactive synergy among energy structure, industry, and technology has not been revealed. Third, there are methodological flaws. Extant quantitative analyses predominantly depend on a single indicator—commonly the share of green credit—and have not yet developed an integrated index that simultaneously incorporates green credit, bonds, and insurance (Q. Li et al., 2025; Ran & Zhang, 2023). In addition, these studies often overlook regional heterogeneity and spatial spillover effects (notably the stronger capacity for industrial restructuring and emission abatement in central and western China), which recent research has shown to be significant (Chen et al., 2025; X. Yang et al., 2024), thereby yielding potentially biased evaluations of policy efficacy. These limitations collectively form a composite gap of “absence of a total perspective—unverified mechanisms—methodological one-sidedness,” which hinders a systematic understanding of how green finance can promote carbon abatement.

The potential contributions of this research are mainly reflected in two aspects. At the theoretical level, this study is the first to integrate a three-tier transmission path of “resource allocation—structural optimization—technological iteration” and introduces the “pollution-to-carbon” co-reduction hypothesis, revealing the co-reduction mechanism through which green finance indirectly constrains carbon emissions by reducing atmospheric pollutants, and a synergistic effect also noted by Fan et al. (2024) at the firm level. This method breaks through the limitations of traditional carbon emission intensity indicators and conducts research from three dimensions: total quantity control, regional differences, and coordinated emission reduction. At the methodological level, this study constructs a provincial green finance composite index (covering dimensions such as credit, bonds, and investment), and based on the STIRPAT model, quantitative analysis was conducted from three aspects: panel fixed effect, mediating effect, and interaction effect. For the first time, this study unifies the analysis of total carbon emissions and the green finance index, and quantifies the mediating contribution rates and interactive synergistic effects of energy structure (the proportion of clean energy), industrial structure (the proportion of the tertiary sector), and technological innovation (the amount of green patents). Empirical research has found that the inhibitory effect of green finance on carbon emissions in the central and western regions is more obvious than that in the eastern regions. It reveals the positive synergy effect between the contribution of technological innovation and the interaction term between energy structure and industrial upgrading, providing precise evidence for the path of regional differentiated policies and the “dual carbon” goals.

The structure of the paper is as follows: Section “Literature Review” is the literature review. Section “Theoretical Analysis and Hypothesis” expounds the theoretical framework and, based on this, proposes the research hypotheses. Section “Research Design” introduces the construction and measurement strategies of the composite index. Section “Empirical Results” presents the results. Section “Discussion” is the discussion of the results. Section “Research Limitations and Prospects” presents the research limitations of this article and the prospects for subsequent studies. In section “Conclusion,” there is a summary of the entire study.

Literature Review

Recent literature has rapidly advanced our understanding of the relationship between green finance and carbon abatement, shifting from broad correlations to detailed, mechanism-based empirical analyses. This review synthesizes the latest findings into four key streams:

Firstly, the direct impact of green finance on carbon emissions. A growing body of evidence confirms that green finance policies and instruments directly contribute to carbon reduction in China (W. Liu & Zhu, 2024). At the city level, studies utilizing quasi-natural experiments around China’s GFRIPZ find that the policy significantly accelerates low-carbon transition (Chen et al., 2025). Similarly, research on Chinese prefecture-level cities shows that green finance not only significantly reduces carbon emission intensity but also enhances carbon emission efficiency (W. Liu & Zhu, 2024). This effect extends to the micro-level. A study of Chinese industrial firms from 2008 to 2015 finds that green finance markedly reduces both CO2 and atmospheric pollutants, achieving a synergistic reduction effect for SO2 and CO2 emissions, primarily by enhancing the energy efficiency of corporate (Fan et al., 2024). Methodologically, the field has evolved from using single indicators like green credit to constructing multi-dimensional composite indices. For instance, the index developed by Ran and Zhang (2023) covers seven sub-systems, including green credit, investment, insurance, bonds, and fiscal support, to more comprehensively measure regional green finance development. Q. Li et al. (2025) have also adopted a similar multi-dimensional approach. Quantitative analyses reveal that expanding green credit significantly curbs carbon emissions, particularly in secondary industries, by incentivizing industrial upgrades (Cao et al., 2023). Green venture capital (VC) demonstrates notable carbon reduction impacts in Asia, Africa, and Latin America, though its efficacy varies with regional economic development and policy environments (B. Yang et al., 2021). Green VC also channels social capital into eco-friendly sectors, spurring corporate technological innovation (Guo et al., 2024). Z. Li et al. (2024) finds that China’s green finance reforms significantly lower industrial energy consumption and enhances carbon efficiency through financial and technological innovation. However, Zhang et al. (2019) notes that despite growing recognition, green finance remains underrepresented in mainstream economics and finance journals, signaling vast research potential.

Secondly, core transmission mechanisms. The literature has converged on two primary channels through which green finance influences carbon emissions: optimizing the industrial structure and fostering green technological innovation. Green finance steers funds away from highly polluting, energy-intensive industries and toward cleaner, high-value-added sectors, thereby promoting industrial structure optimization (Olaf, 2005), with industrial upgrading and technological innovation serving as core pathways through which green finance drives sustainable development (Y. Wang et al., 2021). Moreover, the regulatory role of environmental regulations further amplifies this intermediary mechanism (Sheng & Du, 2023). The study by Cui et al. (2024) finds that the GFRIPZ policy forces heavily polluting enterprises to make green investments by tightening financing constraints on them. This process directly drives a broader low-carbon transition (Chen et al., 2025). Amin et al. (2025) also confirms that renewable energy and green growth contribute to curbing carbon emissions. Green finance provides essential funding for the R&D and adoption of low-carbon technologies. Numerous studies confirm that green innovation also plays a mediating role (H. Li et al., 2025; J. Li et al., 2024; W. Liu & Zhu, 2024; Ran & Zhang, 2023). X. Yang et al. (2024) also note that incorporating technological advancement into the analytical framework more clearly reveals the intrinsic logic of green credit’s emission reduction effects. It indirectly reduces carbon emissions by alleviating financing constraints and fostering green technological innovation, with notable spatial spillover effects. H. K. Liu and He (2021) further demonstrates that green finance simultaneously balances the nonlinear regulatory effects of environmental policies between innovation compensation and cost burden.

Thirdly, heterogeneity and spatial spillover effects. The impact of green finance is not uniform across regions or firm types. Fan et al. (2024) finds that the role of green finance in promoting carbon abatement is more obvious in non-state-owned enterprises. At the city-level, J. Li et al. (2024) point out that the impact of green finance on carbon productivity is more significant in non-resource-based cities, owing to their more diversified industrial structures and stronger innovation capacities. Furthermore, recent studies increasingly employ spatial econometric models to capture inter-regional dynamics. Q. Li et al. (2025) hold that green finance will also spill over to surrounding regions through technological diffusion and policy coordination. Chen et al. (2025) find that the GFRIPZ policy not only accelerates the local low-carbon energy transition but also generates significant cross-regional spatial radiation effects. However, in a cautionary finding, Lu et al. (2025), using remote sensing data, show that green finance may induce a green relocation effect, revealing the existence of an intra-city carbon transfer effect.

In summary, while recent empirical studies have firmly established that green finance in China promotes carbon abatement through industrial structure optimization and green innovation, significant gaps remain to address. Firstly, much research focuses on carbon emission intensity or efficiency, offering only indirect insights into the control of total emissions, which is critical for achieving absolute climate targets. Secondly, although individual mediating pathways are well-documented, their interactive synergies—such as how technological innovation moderates the effect of financial policies—are still insufficiently explored and represent a key research frontier. Finally, while spatial spillovers are acknowledged, the underlying mechanisms (e.g., financial diffusion vs. technology diffusion) and their potential to create unintended consequences like carbon displacement are not yet well understood. These gaps—concerning the focus on total emissions, the lack of interactive mechanism analysis, and the need for a more comprehensive spatial framework—may influence the implementation effect of green finance in promoting carbon reduction.

In response to these limitations, this paper constructs a multi-dimensional green finance index and uses provincial panel data from 2006 to 2021 to examine the causal relationship between these two factors. Specifically, we construct STIRPAT-based panel models, mediation effect models, and interaction effect models to analyze both direct and indirect pathways, providing a holistic assessment of how green finance can more effectively promote carbon abatement.

Theoretical Analysis and Hypothesis

Theoretical Analysis of Green Finance’s Impact on Carbon Emissions

Recently, the deepening intersection of climate and financial crises have heightened interest in identifying pathways to address both challenges synergistically (van Veelen, 2021). Their relationship has become increasingly complex and multi-faceted (Bridge et al., 2020; Christophers, 2016), with short-term solutions remaining elusive (Ouma et al., 2018). From an economic perspective, green finance impacts carbon emissions through two primary mechanisms. First, it alleviates financing constraints for green and low-carbon enterprises by streamlining loan procedures, reducing financing costs, and enhancing returns for green projects. Simultaneously, it imposes stricter financing limitations on high-pollution and high-energy-consuming industries (“dual-high” industries hereafter), and increases loan approval requirements, raises costs, and diminishes returns for dual-high projects, thereby fostering the growth of green industries and reducing total carbon emissions. For instance, the Chinese government explicitly prioritizes lending support and preferential interest rates for corporations in green and low carbon economy. Conversely, loan volumes for heavily polluting firms have declined significantly, with interest rates potentially adjusted upward due to environmental risk assessments (Zhen, 2023). Second, green finance incentivizes corporations to integrate social responsibility into their objectives while strengthening consumer awareness of environmental protection. This alignment encourages firms to invest in low-carbon technologies, and develop competitive green products.

The mechanisms of various green financial instruments further elucidate their impact. Green investment banks and funds mitigate risks and costs through scale and specialization, improving investment efficiency and returns to attract capital to low-carbon sectors. Fiscal-subsidized green loans and bonds lower financing costs for green projects, mobilizing market funds for climate-friendly initiatives. Green IPO channels and stock indices enhance financing accessibility for green firms, directing capital into sustainable industries and indirectly reducing investment costs. Green insurance internalizes environmental risks through premiums, increasing financing costs for dual-high projects and deterring polluting investments. Green credit guarantees, supported by tax rebates from renewable energy spillover effects, reduce financial risks and boost returns for green projects (Taghizadeh-Hesary & Yoshino, 2019). Additionally, market-based mechanisms enable pricing of emissions, leveraging price signals, term transformation, and risk management to curb corporate emissions and incentivize low-carbon innovation.

The interaction between these two factors is closely tied to the synergy between pollution reduction and decarbonization. For example, reducing coal consumption concurrently decreases air pollutants, while automotive emission controls accelerate the growth of new energy vehicles, lowering carbon emissions. Qiang et al. (2023) highlights that integrated measures reduce extreme weather events, pollutant emissions, and control costs while optimizing economic structures. Thus, green finance indirectly reduces carbon emissions by these synergistic effects.

Based on this, this study proposes hypothesis 1: Green finance promotes carbon emission reduction.

Analysis of the Mechanism of Green Finance and Energy Structure Adjustment Affecting Carbon Emission

Energy structure adjustment serves as a critical pathway for promoting carbon abatement and advancing carbon peaking. Without appropriate restructuring of the energy mix, efforts to combat climate change cannot be fully resolved (Chevallier et al., 2021). Since the 1970s, coal consumption in LMICs has been a primary driver of rising carbon emission intensity, and coal production reduction is recognized as a key measure to decarbonize energy systems (Watts et al., 2018). Europe has leveraged green finance instruments to support energy efficiency industries, with the EU allocating €200 billion of its stimulus plan primarily to climate action and energy efficiency (Mert, 2023). In China, green finance facilitates energy structure optimization through capital allocation, aiming to control coal consumption, promote cleaner fossil energy utilization, and accelerate non-fossil energy development.

For one thing, green finance has effectively supported coal clean utilization, natural gas substitution in key sectors, excess capacity phase-outs, and scattered coal management. The proportion of coal in primary energy consumption has decreased by 15 percentage points in the past decade.

For another, guided by national policies and capital investments, green finance has channeled funds via green credit, green bonds, and venture capital to bolster non-fossil energy investments, driving the development of hydropower and nuclear and so on. Consequently, the share of new energy sources such as hydropower has increased from 7.5% in 2007 to 15.7% in 2019.

Energy structure adjustment also fosters green finance development. Building a low carbon, clean, and secure energy system is essential to achieving carbon peaking and neutrality targets. Estimates by Tsinghua University researchers indicate that under the 2°C target, China’s energy system requires approximately ¥100 trillion in new investments from 2020 to 2030. Under a 1.5°C target, this figure rises to ¥138 trillion. Energy restructuring presents vast growth opportunities for green finance, enabling economies of scale while helping the financial sector mitigate climate risks and enhance capital returns. Beyond their individual growth trajectories, energy restructuring and green finance exhibit synergistic interactions, jointly advancing carbon reduction.

Therefore, this study proposes Hypothesis 2: Green finance promotes carbon reduction by adjusting the energy structure, and there is an interaction effect between the two to jointly promote carbon reduction (Hypothesis 2a).

Mechanism Analysis of Green Finance and Industrial Structure Optimization Affecting Carbon Emission

Existing studies demonstrate that green finance and its policies can curb investments in “dual-high” industries (Da et al., 2022; F. Wang et al., 2024; Xiu et al., 2015) while stimulating investment growth in green industries (Weimin et al., 2023; Xiaodong et al., 2021; Xingshuai et al., 2022; Yue et al., 2022). Regarding the inhibitory effects on “dual-high” enterprises, green credit policies restrict credit availability to polluting sectors, compelling firms to transition to low-energy and low-emission industries, thereby accelerating industrial restructuring (Da et al., 2022). Xiu et al. (2015) demonstrate that green credit effectively constrains the expansion of dual-high industries to reduce energy conservation. Green funds limit financing channels from polluting firms, alleviate funding constraints for green projects, and significantly raise long-term financing costs for polluters (F. Wang et al., 2024). From the perspective of green enterprise investment growth, green finance policies lower financing costs for eco-friendly firms, impose financing penalties on polluters, and incentivize green innovation and environmental performance improvements (Xingshuai et al., 2022). Green credit policies should align with clean energy objectives by enhancing financial support for renewable sectors, optimizing energy composition, restricting capital flows to polluting enterprises, and advancing the green economic transition (Xiaodong et al., 2021). Green finance raises financing barriers for energy-intensive enterprises, compelling them to adopt green production and innovation, while directing financial resources toward low-pollution sectors through policy incentives (Weimin et al., 2023). Yue et al.’s (2022) comprehensive review synthesizes green finance’s impact on heavy-polluting firms, highlighting that green credit policies suppress their investments through dual mechanisms of financing constraints and industrial upgrading, while fostering clean technology R&D.

Industrial structure optimization also drives green finance development. First, low-carbon industrial transitions generate demand for green finance, including financing needs for energy efficiency upgrades in traditional dual-high industries and investments in clean energy, new energy vehicles, and big data sectors. Second, it fosters innovation and refinement of green financial systems. Green financial innovations—such as green securities and new market development—are closely linked to sustainable development, indicating the role of product and service innovation in greening infrastructure systems (Juan et al., 2018). By advancing green finance, the financial sector mitigates its environmental risks and enhances its social responsibility profile. Thus, green finance promotes industrial structure optimization, which in turn reinforces green finance development. The two exhibit synergistic interactions, jointly contributing to carbon reduction.

Therefore, this study proposes Hypothesis 3: Green finance promotes carbon reduction by optimizing the industrial structure, and there is an interaction effect between the two to jointly promote carbon reduction (Hypothesis 3a).

Analysis of the Mechanism of Green Finance and Technological Innovation Affecting Carbon Emission

Financial development facilitates the dissemination and application of knowledge and technologies, accelerating the diffusion of low-carbon innovations (Ping et al., 2022). Green finance policies exhibit a pronounced signaling effect. Preferential funding for low-energy and low-emission (“dual-low”) enterprises reduces their R&D financing costs, thereby accelerating technological innovation and amplifying the Porter effect of green finance. While these policies increase financing difficulties for dual-low firms, they also incentivize their green transition. A critical determinant of polluting firms’ reform lies in the proportion of capital controlled by green investors: if a firm’s capital costs exceed the expenses of reforming its polluting activities, it faces pressure from exclusive ethical investments to assume social responsibility (Heinkel et al., 2001). From a financing constraint perspective, green finance strengthens incentives for green production by alleviating funding barriers for dual-low enterprises through mechanisms such as matching funds and so on. This fosters advancements in green innovation technologies, reduces energy consumption, and lowers carbon emissions (Yu et al., 2021). Practically, green finance directly invests in green technologies—such as clean energy and battery technologies—whose maturation and industrialization cut emissions. Additionally, green finance shifts regional economies from investment-driven to innovation-driven models, enhancing total factor productivity and further reducing carbon emissions.

The maturation of low-carbon technological innovation also benefits green finance. While such innovations inherently carry high risks and returns, their growing maturity lowers technical risks, supported by policy-backed risk-sharing mechanisms and clearer high-return prospects, enabling rapid capital appreciation for green finance. For instance, under stringent environmental regulations, low-carbon innovations enhance the competitiveness of traditional industries, reducing risks for green finance. The development of clean energy technology has given green venture capital excess returns, and created substantial demand for green financial products. Thus, technological innovation and green finance likely exhibit synergistic interactions, jointly advancing carbon reduction.

Therefore, this study proposes Hypothesis 4: Green finance promotes carbon reduction through technological innovation, and there is an interaction effect between the two to jointly promote carbon reduction (Hypothesis 4a).

Research Design

Research Model

Basic Model

York et al. (2003) revised and extended the IPAT model, proposed by Ehrlich and Commoner in the 1970s to establish the STIRPAT model. Both models are widely applied in studies on carbon emission drivers. The standard IPAT model is expressed as:

By taking logarithms and converting it into a panel regression model, Equation 2 is derived:

Replacing I with carbon emissions (CO2) and incorporating control variables X′, the STIRPAT model is formulated as Equation 3:

Here, the dependent variable lnco2 is the logarithm of carbon emissions.

Mediation Effect Model

To examine the mediation effect, the following mediation effect models are constructed based on Equation 4:

Equations 5 to 7, combined with Equation 4, form the mediation effect models. A mediation effect exists if the regression results of Equation 4 show that coefficient β3 is negative, β4 is positive, and β6 is negative—all statistically significant—while γ1 is positive, δ1 is negative, and ρ1 is positive. This indicates that green finance facilitates energy structure diversification, reduces the proportion of the secondary industry, and enhances technological innovation, thereby confirming the mediation effects in promoting carbon emission reduction.

Interaction Effect Model

To analyze the interaction effects between green finance and the above three variables that are not mutually independent and exhibit bidirectional influences—the following interaction effect models are constructed:

Here,

Variable Descriptions and Data Explanation

Variable Description and Data Sources

The study sample interval and object of this paper are among 30 provinces and regions in China from 2006 to 2021. The variables involved and the data sources are described as follows:

Dependent variables. The logarithm of carbon emissions (

The explanatory variable is the Green Finance (GF). GF represents four dimensions: green credit, green investment, green insurance, and government support. Based on standardized processing, these indicators are comprehensively calculated using the entropy method. Specifically, the proportion of interest expenses in the six major energy-intensive industries out of total industrial interest expenses is calculated based on industry interest data. The data for environmental pollution control investment comes from the China Environmental Yearbook, the depth of agricultural insurance is sourced from the China Insurance Yearbook, and the original data for fiscal environmental protection expenditure as a percentage of general budget expenditure is obtained from the National Bureau of Statistics website.

Control variables are divided into two categories: one is mechanism-related, and the other is ordinary. Mechanism-related control variables include: Technological innovation capability (RDG), represented by the ratio of fiscal science and technology expenditure to GDP. Industrial structure, indicated by the proportion of the secondary industry (SEC). Energy structure adjustment, represented by the energy consumption diversification index (EH), calculated using the Hefliner-Hirschman Index based on the consumption of 20 different types of energy, including raw coal, gasoline, and so on. Ordinary control variables include: Logarithm of the resident population (

Descriptive Statistics and Empirical Considerations

The research period spans 2006 to 2021.As can be seen from Table 1, the logarithm of total carbon emissions (

Descriptive Statistics of the Variables.

Both the amount of carbon emissions and the GF have displayed upward trends since 2006. Without controlling for variables such as population, wealth, and technological innovation, a positive correlation between the two would inevitably emerge. Therefore, empirical regressions must incorporate these controls and account for time effects. Only by isolating the influence of major factors can the true impact of these two factors be disentangled, ensuring robust empirical results.

Empirical Results

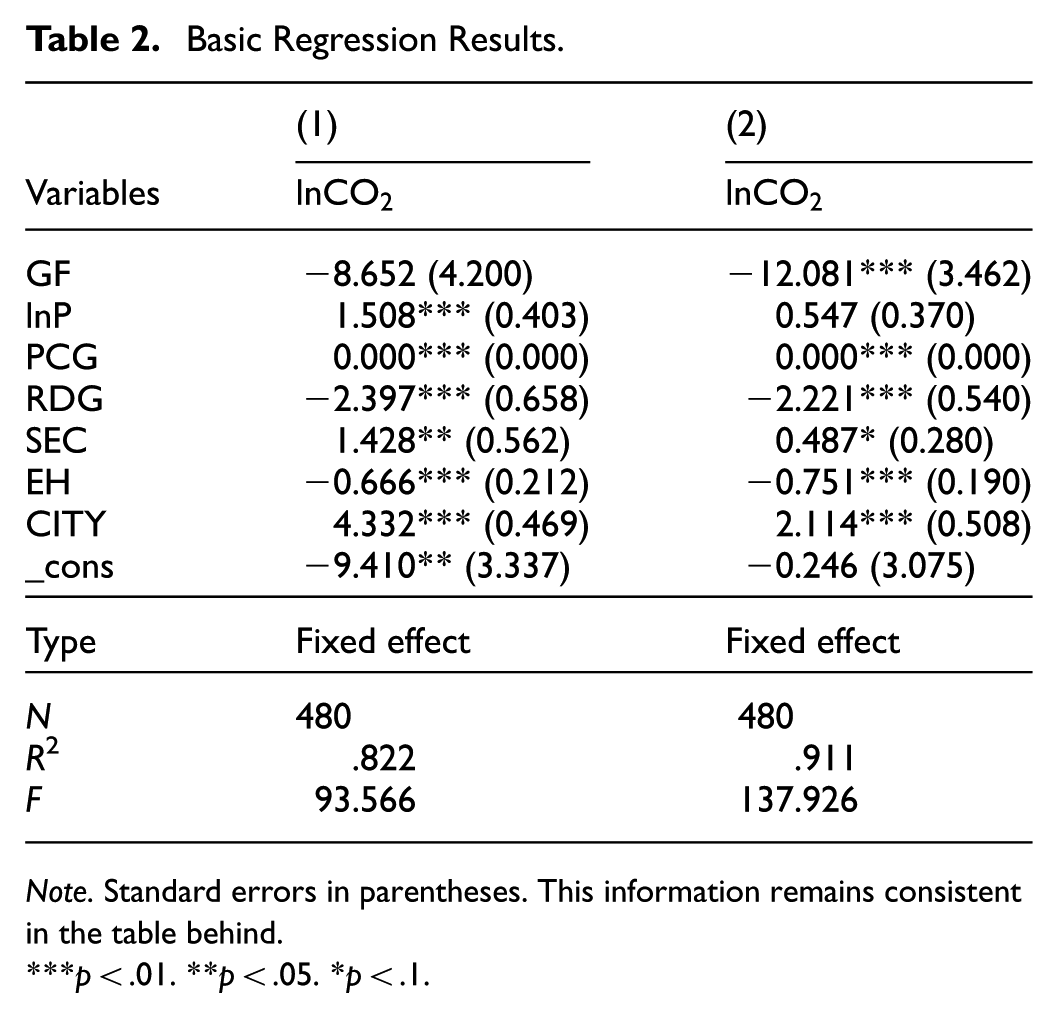

Basic Regression Results

The statistical software used in this study is STATA 15. A fixed-effects panel model is ultimately selected for regression. Table 2 reports the STIRPAT-based regression estimates results. Column (1) reports results without time effects controlled, while Column (2) includes time effects. Key findings are as follows:

Basic Regression Results.

Note. Standard errors in parentheses. This information remains consistent in the table behind.

p < .01. **p < .05. *p < .1.

In Column (1), the negative coefficient of GF indicates that green finance contributes to carbon reduction. After controlling for time effects in Column (2), the coefficient of GF becomes significant, suggesting that time trends significantly promote the carbon reduction effect of green finance. Theoretically, green finance reduces carbon emissions through mechanisms such as financing constraints, cost effects, and return rate effects. It promotes pollution and carbon reduction synergistically by providing comprehensive green financial services, restricting “dual-high” industries, by which validating Hypothesis 1.

The negative coefficient of RDG shows that technological innovation can effectively reduce pollutions. Among these, “dual-high” enterprises can promote carbon abatement in traditional industries through technological upgrades, renovations, and the introduction of energy-saving equipment. Innovations in clean energy, new energy vehicle technology, and power grid technology directly boost the carbon abatement, which aligns with expectations. However, as industrial structure optimization occurs, the significance of the secondary sector’s impact on carbon emissions decreases, generally consistent with expectations. The negative coefficient of EH indicates that controlling coal consumption, promoting the clean use of fossil fuels, and advancing non-fossil energy development have significantly reduced total carbon emissions through energy structure adjustment and diversification, which matches reality.

Population size is significantly positively correlated with energy consumption, which aligns with reality. As per capita wealth and living standards improve, and consumer demand increases, thereby promoting carbon emissions, which aligns with reality. The coefficient of CITY is positive, indicating that urbanization drives changes in lifestyle, including buildings, transportation, and consumption, significantly increasing the total carbon emissions, which aligns with reality.

Most variables align with theoretical expectations or empirical reality. The high R2 values (.8–.9) confirm robust model specification and reliable results.

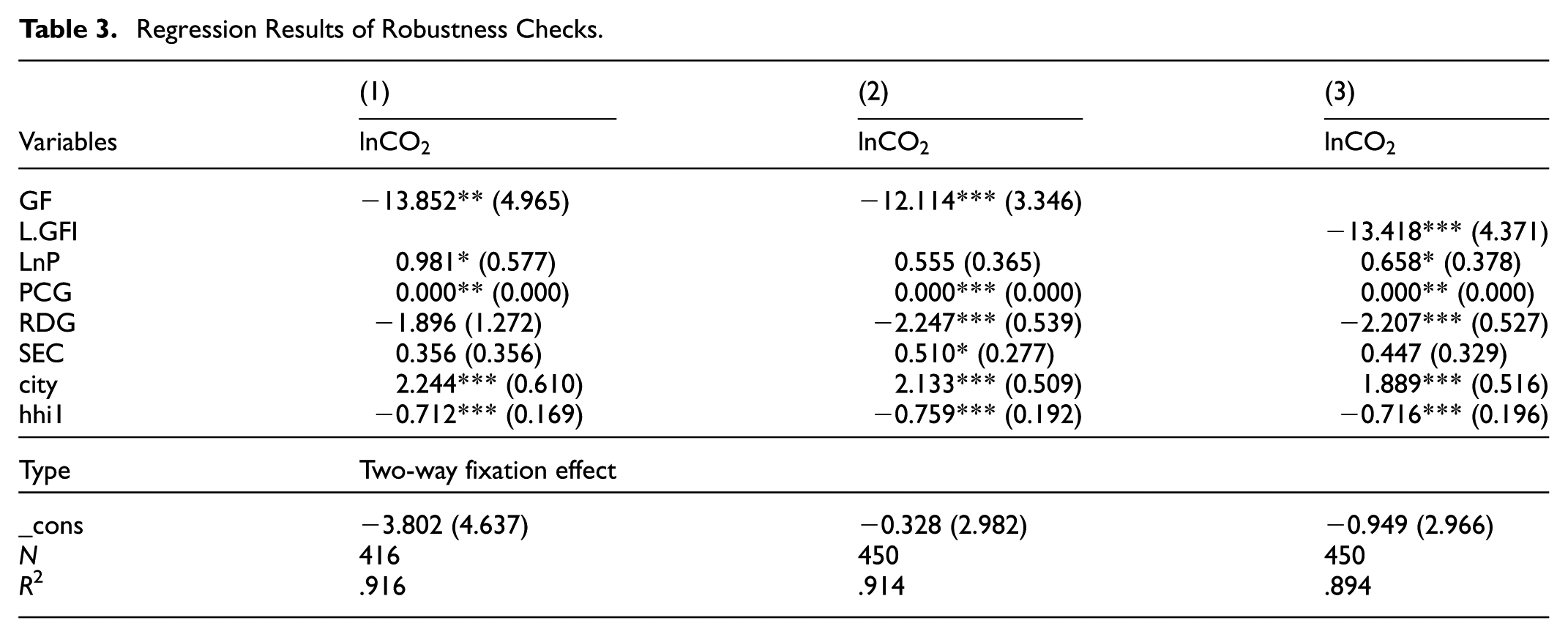

Robustness Tests

This paper conducts three types of robustness checks:

First, we re-estimate the model after excluding the four centrally administered municipalities—Beijing, Tianjin, Chongqing, and Shanghai. The results, reported in Column (1), show that the GF coefficient retains a negative and statistically significant coefficient, confirming that the baseline findings are not driven by these cities. After accounting for population, affluence, and technological factors, green finance continues to exert a significant downward pressure on aggregate CO2 emissions, thereby facilitating the attainment of economy-wide emission-control targets.

Second, we exclude the impact of the 2008 financial crisis by removing observations from that year. Column (2) shows that the GF coefficient remains negative, confirming that the core findings are robust even after eliminating abnormal economic fluctuations.

Third, to capture potential delayed effects, we re-estimate the model using the 1-year lagged value of GF. It can be seen from Column (3) that the lagged coefficient remains negative and significant, which also verifies the robustness of the initial results (Table 3).

Regression Results of Robustness Checks.

Mechanism Analysis

Mechanistic Analysis Based on Mediation Effects

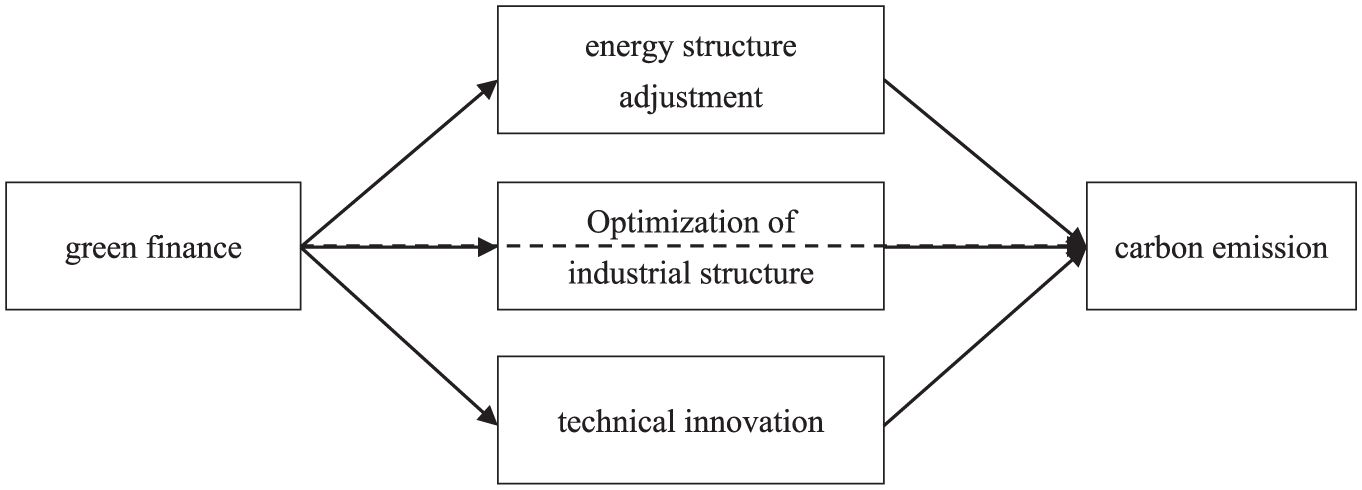

Table 2, based on the STIRPAT model regression results, reveals that energy restructuring, industrial optimization, and technological innovation significantly reduce total carbon emissions. To further verify whether green finance lowers carbon emissions through mediating mechanisms involving these pathways (as illustrated in Figure 1), we conduct additional regressions using the energy consumption diversification index (eh), secondary industry share (sec), and technological innovation level (rdg) as dependent variables, with gf as the explanatory variable.

The intermediary effect mechanism.

In the regression result (3) in Table 4, the positive coefficient of GF means green finance promotes energy diversification and structural adjustment. Green finance restricts financing in the coal industry, promotes the clean utilization of fossil fuels, and simultaneously facilitates the utilization of clean energy sources such as hydropower, wind power, solar power, and so on. It also optimizes the energy use structure through electrification. In the regression result (4), the coefficient of GF is negative. The “targeted financing constraints” and cost adjustments of green finance help reduce production capacity in “dual-high” industries, thereby lowering pollution emissions; support from green finance helps expand and accelerate the development of “dual-low” industries, promoting progress in low-carbon green technologies. The green finance system can alleviate an “overweight” industrial structure and encourage companies to make proactive adjustments by changing the financing costs and availability for different types of industries, ultimately achieving industrial structure optimization. In the regression result (5), the GF coefficient is positive, indicating that green finance enhances technological innovation levels. Green finance promotes low-cost access to R&D funds for enterprises, accelerating technological innovation; it also encourages enterprises in “dual-high” industries to develop clean projects, applying energy-saving technologies and equipment through technological transformation, upgrades, and introductions; direct investment in green innovation technologies accelerates the maturity and industrialization of green technologies.

Regression Results of the Mediation Effects.

Combining the results from Tables 4 and 2, we conclude three mediating mechanisms: energy restructuring, industrial optimization, and technological innovation. These findings validate Hypotheses 2, 3, and 4.

Mechanistic Analysis Based on Interaction Effects

This paper continues to discuss the influence of the interaction effect (Figure 2). To test these interactions, we first conducted panel Granger causality tests and subsequently incorporated pairwise interaction terms into a two-way fixed-effects regression model.

The interactive effect mechanism.

Using the method proposed by Dumitrescu and Hurlin (2012), we examined the Granger causal relationships among green finance (GF), energy structure (EH), industrial structure (SEC), and technological innovation (RDG). Results in Table 5 indicate bidirectional Granger causality between GF and EH, GF and SEC, and GF and RDG at a two-period lag, confirming statistical causality. These results support the existence of potential interactions.

Granger Causality Test Results.

Regression results with interaction terms are presented in Table 6.

Regression Results of the Interaction Effect Between Green Finance and Related Variables.

As shown in Column 6, both GF and EH coefficients are negative, while the GF × EH coefficient is negative. This indicates that green finance, energy structure adjustment, and their interaction jointly promote carbon reduction. The interaction effect between GF and energy structure adjustment is manifested as follows: Green finance can control coal consumption, promote the clean utilization of fossil fuels, and optimize the energy structure by advancing non-fossil energy development. Energy structure adjustment can achieve the scale effect of green finance, and enhance financial capital appreciation. This verifies Hypothesis 2a proposed in this paper. In Column (7), the positive or negative nature of the coefficient of GF, SEC, and GF × (1/SEC) suggests that green finance is beneficial for carbon reduction, whereas an overly heavy industrial structure is detrimental to carbon reduction. There is an interactive effect between GF and SEC, which is reflected in how green finance, through cost-benefit analysis, hinders the development of “dual-high” industries and thereby optimizes the industrial structure. Therefore, it is necessary to create demand for green finance in the context of low-carbon transition and promote innovation and improvement in the green finance system. This verifies Hypothesis 3a proposed in this paper. In Column (8), both the GF coefficient, the RDG coefficient, and the GF × RDG coefficient are negatives.

This indicates that the interaction effect between green finance and technological innovation exists and is beneficial for carbon reduction. Moreover, the interaction effect between the two is specifically manifested as follows: green finance promotes the research and application while technological innovation helps green finance control environmental risks and achieve rapid value appreciation. This verifies Hypothesis 4a proposed in this paper.

These results confirm the hypothesized interactive effects of green finance in driving carbon reduction through energy restructuring, industrial optimization, and technological innovation.

Regional Heterogeneity Analysis

In order to further analyze the regional differences in green finance development and carbon emission levels across eastern and central-western China, this study divides 30 provincial regions into two subsamples (eastern vs. central-western) for regression analysis. The regression results are presented in Table 7.

Results of Regional Heterogeneity Analysis.

The regression results after classification have undergone significant changes. The coefficient of GF indicates that green finance has no significant impact in the eastern region. Due to the more developed economy in the east, which started early in energy conservation and greenhouse gas control, many provinces and cities have entered or are approaching a plateau in total carbon emissions, thus potentially limiting the carbon reduction effect of green finance. In the regression result (10), the GF coefficient is negative, suggesting that for the central and western regions, insufficient early-stage carbon emission control has left ample room for green finance to promote industrial transformation, thereby significantly enhancing carbon reduction. Additionally, there are noticeable differences in the impacts of population, wealth levels, technological innovation, and energy diversification on the eastern and central-western regions. These two regions face issues such as insufficient green and low-carbon technology and over-reliance on heavy industries, making it less effective to optimize industrial structures and promote technological innovation in controlling carbon emissions. These findings collectively indicate that these two regions are the primary areas where green finance can significantly promote carbon reduction. Green finance holds great potential in improving low carbon technology levels, optimizing energy structures, and promoting industrial green transformation in these regions. In contrast, the eastern region needs to strengthen low carbon technological innovation to control carbon emissions.

By the “Pollution and Carbon” Effect Test

Pollution reduction and carbon mitigation exhibit synergies. For instance, reducing coal consumption to curb carbon emissions simultaneously lowers air pollutants such as SO2, CO2, and NO2. Beevers and Carslaw (2005) finds that London’s congestion charge policy reduced air pollution while cutting CO2 emissions by 19.5% through reduced private vehicle use. Qiang et al. (2023) further confirms synergies between climate action and pollution governance. Considering the shared synchronized dynamics of air pollution and carbon emissions, green finance may achieve a “pollution-to-carbon” synergistic effect—reducing carbon emissions by controlling air pollution. To test this hypothesis, we construct the following mediation models:

Step 1: Model for Green Finance’s Impact on Air Pollution

Here, the dependent variable is air pollution (

Step 2: Model for Green Finance, Air Pollution, and Carbon Emissions

This model incorporates

According to Column (11) of Table 8, the negative coefficient of GF indicates that green finance significantly reduces air pollution levels through various direct and indirect effects such as investments in air pollution control. Compared with the results in Column (12), the significance of the coefficient of GF is notably higher, suggesting a closer relationship. The positive coefficient of pm2.5 indicates a significant positive correlation between air pollution and carbon emissions. The more severe the air pollution is, the higher the carbon emission levels, which also suggests that while reducing pollution, it can effectively control carbon emissions. Based on the principle of mediation effect, combining the results in Column (11) and (12), it is demonstrated a significant “pollution-to-carbon” effect.

Regression results of the “pollution and carbon” effect.

Discussion

Discussion of Key Findings

The empirical results of this study provide multi-dimensional evidence. We not only confirm its significant overall effect but also uncover its complex transmission pathways and heterogeneous characteristics.

First, the core finding of this study is that green finance development significantly curbs total carbon emissions. This conclusion serves as a crucial complement to numerous studies that have focused on carbon emission intensity or efficiency (e.g., J. Li et al., 2024; W. Liu & Zhu, 2024). While reducing carbon intensity is a vital step in the low-carbon transition, aggregate economic expansion can still lead to an increase in total emissions. Therefore, by directly focusing on “total emissions control” as the ultimate goal, this study provides more direct evidence for assessing the actual contribution of green finance to China’s “dual carbon” targets.

Second, this study identifies and validates that energy structure adjustment, industrial structure optimization, and technological innovation are the three core transmission channels through which green finance impacts carbon emissions, and it further reveals a significant interactive synergistic effect among them. Although previous studies have explored these mediating pathways individually (e.g., H. Li et al., 2025; Ran & Zhang, 2023), few have empirically tested their interactions. Our research demonstrates that green finance does not operate on these channels in isolation; rather, it amplifies its abatement effect through a mutually reinforcing positive feedback system. For example, technological innovation supported by green finance reduces the cost of clean energy, thereby accelerating energy structure adjustment. This systemic perspective deepens our understanding of the mechanisms of green finance.

Furthermore, our research reveals significant regional heterogeneity, with the effects in the central and western regions being notably better than those in the eastern regions. This finding corresponds with the research of Chen et al. (2025) on the effectiveness of the GFRIPZ policy. Our study further uncovers the spatial distribution of this policy effectiveness: the marginal abatement benefits of green finance are the highest in the central and western regions, which have greater potential for low carbon transformation. This suggests that future green finance policy resources should be allocated differentially to maximize national capital abatement efficiency.

Finally, this study provides provincial evidence of the significant “from pollution to carbon” synergistic effect of green finance. Our research demonstrates that green finance investments aimed at controlling atmospheric pollutants (e.g., PM2.5), due to the common origins of pollution and carbon emissions, simultaneously yield significant carbon abatement co-benefits. This finding provides macro-level support for the synergistic reduction effect observed at the firm level by Fan et al. (2024) and offers strong empirical justification for building an integrated environmental-climate co-governance policy framework in China.

Implications of the Study

Overall, this study provides rich policy implications for China on how to more effectively utilize green finance to realize the “dual carbon” goals. Given the regional heterogeneity and the complexity of the transmission mechanism, more targeted, differentiated, and precise strategies must be adopted.

First, implement differentiated regional green finance strategies to optimize capital allocation efficiency.

(1) For the central and western regions: Our research reveals that green finance has immense emission reduction potential in these areas. Policy should, therefore, focus on utilizing green credit and green industrial funds to promote the green transformation and capacity phase-out of heavy industries. Stricter credit constraints should be imposed on dual-high industries, while providing low-cost financing for the regions’ abundant renewable energy projects.

(2) For the eastern region: The study indicates that the effect of green finance is limited in this area, where CO2 emissions are approaching a plateau. The policy focus here should pivot from the industrial side to the technological and consumption sides. It is imperative to vigorously develop green bonds, green venture capital (VC), and tech finance to support the R&D and commercialization of cutting-edge low carbon technologies (e.g., energy storage, carbon capture), fully leveraging the technological innovation channel.

Second, design precise green finance incentive tools to unblock key transmission pathways.

(1) Strengthen the linkage between financial instruments and industrial policy: To better leverage the “industrial structure optimization” pathway, regulatory authorities should refine the Green Credit Guidelines. Loan interest rates and credit lines should be directly linked to a firm’s specific energy efficiency and emission levels, applying punitive rates to “dual-high” enterprises and offering clear credit support for the service sector and strategic emerging industries to accelerate capital reallocation.

(2) Deepen the integration of green finance and tech finance: Given that “technological innovation” is a critical mediating channel, national or regional green technology innovation guidance funds should be established. These funds can adopt a “government + market” model to attract private capital into promising green start-ups. Green patent output could also be used as a key metric for enterprises to obtain preferential green credit, thereby incentivizing substantive green innovation.

(3) Leverage the unique advantages of different financial instruments: For large-scale renewable energy infrastructure projects (energy structure adjustment), the green bond market should be vigorously developed to provide stable, long-term capital. For high-risk, frontier innovation projects (technological innovation), greater reliance should be placed on green venture capital to share risks and unlock value.

Last but not the least, establish a “Pollution-to-carbon” Co-reduction financial policy framework to maximize synergy. This study empirically confirms a significant synergistic “from pollution to carbon” effect. Therefore, policymaking should not treat environmental governance and climate action as separate issues. We recommend that the evaluation criteria for green finance projects incorporate dual indicators for both pollutant reduction (e.g., PM2.5, SO2) and carbon abatement. Projects demonstrating significant co-reduction benefits should be granted higher financing priority and more favorable terms, thereby achieving dual environmental and climate goals at a lower societal cost.

This study systematically reveals the interactive rather than isolated mechanism by which green finance affects the total carbon abatement, enriching the relevant literature. It makes up for the shortcomings of previous studies, such as the lack of an overall perspective, unverified mechanisms, and the one-sidedness of research methods. Furthermore, regional heterogeneity and the “pollution-carbon” synergy effect do indeed provide an effective basis for different regions to make targeted use of green financial policies to achieve carbon control targets.

Research Limitations and Prospects

Although this study has taken into account the rigor of the research as comprehensively as possible, it must be said that the paper still has certain limitations, which are also issues that need to be paid attention to in subsequent research.

First, although we employed two-way fixed-effects models and lagged variables to mitigate endogeneity, we cannot entirely rule out potential biases arising from bidirectional causality or unobserved omitted variables. Future research could overcome this limitation by utilizing city-level or firm-level data to leverage quasi-natural experiments more effectively or by employing dynamic panel models such as the system GMM approach to further strengthen causal inferences.

Second, due to the availability of data, our quantitative analysis did not cover some factors that have an impact on policy effectiveness, such as institutional capacity, the strictness of regulatory enforcement, the participation of stakeholders, and the local social and cultural background. Subsequent research can adopt a hybrid approach, combining econometric analysis with qualitative comparative analysis (QCA), to more comprehensively assess the impact of various factors on the effectiveness of green finance.

Finally, this study was conducted using provincial data, which might have masked significant heterogeneity at a finer granularity level. The policy effects of green finance may vary significantly among different cities within the same province or among different types of companies. Future research using microdata at the city or company level will be extremely valuable for revealing these more subtle influences and providing more precise policy recommendations for specific urban areas or industries.

Conclusion

This paper systematically analyzes the impact, mechanism, and heterogeneous effects of China’s green finance policies on carbon emissions by using the comprehensive green finance index and provincial panel data from 2006 to 2021. Our research yields several key conclusions.

First, green finance development significantly curbs total carbon emissions, providing direct evidence of its critical role in achieving absolute climate targets. Second, this effect is transmitted through three core pathways—energy structure adjustment, industrial structure optimization, and technological innovation—which operate not in isolation but through a mutually reinforcing synergistic interaction. Third, the policy of green finance can be seen as a substantially stronger carbon abatement effects in the central and western areas, where the potential for industrial low-carbon transformation is the greatest. Finally, this study provides the first macro-level evidence of a significant “from pollution to carbon” synergistic effect, demonstrating that green finance achieves climate co-benefits by simultaneously reducing air pollution.

By focusing on total emissions, verifying interactive mechanisms, and uncovering regional and synergistic effects, this paper underscores that leveraging green finance is not merely a funding mechanism but a systemic tool that, if designed with regional and sectoral precision, can powerfully drive China’s transition to carbon-neutral economy.

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by Guangdong Basic and Applied Basic Research Foundation (grant number 2023A1515010619) and Guangdong Provincial Education Science Planning Project (Higher Education Special Project, grant number 2025GXJK0467).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The datasets used in this study are available from the corresponding author on reasonable request.