Abstract

This paper presents a systematic review of literature on the implementation of artificial intelligence (AI) in accounting and auditing. Drawing on peer-reviewed articles and scholarly papers, it maps the current landscape of AI integration, highlighting applications, benefits, and challenges. The review also explores ethical, organizational, and regulatory factors shaping adoption, emphasizing research gaps, and guiding future practice. Findings indicate that AI enhances operational efficiency, improves financial reporting credibility, automates routine tasks, and strengthens fraud detection through tools such as machine learning and predictive analytics. AI is also shifting auditors’ roles from retrospective inspections to real-time monitoring and decision-making. However, adoption faces challenges, including high costs, ethical concerns such as job displacement and data privacy, unequal readiness across regions, and limited empirical studies on AI in accounting and auditing. The review underscores the need for updated regulatory guidelines, inter-disciplinary collaboration, and reforms in accounting education to equip professionals for AI-driven environments. It also stresses the importance of psychological and organizational determinants, such as perceived usefulness, ease of use, and trust in shaping adoption. Overall, the paper concludes that while AI holds significant potential to transform accounting and auditing, effective adoption requires addressing structural, ethical, and educational challenges. These insights offer valuable guidance for practitioners, academics, and policymakers to better harness AI in the financial sector.

Plain Language Summary

Artificial intelligence (AI) is changing the way accountants and auditors work. Instead of only doing routine tasks, professionals can now rely on AI to process large amounts of data, detect unusual patterns, and improve the accuracy of financial reports. This review looked at recent research on how AI is being used in accounting and auditing, and what challenges still exist. We found that AI can save time, reduce errors, and make fraud detection faster and more reliable. At the same time, there are concerns about privacy, job security, and the costs of adopting new systems. For businesses, regulators, and universities, the message is clear: AI offers big opportunities, but it also requires new skills, ethical safeguards, and updated rules. Our study provides a roadmap to help professionals and policymakers prepare for a future where AI is a key part of financial decision-making.

Introduction

Artificial Intelligence (AI) is reshaping the landscape of accounting and auditing. This study investigates the integration of AI technologies within accounting and audit functions, highlighting its impact on operational efficiency, fraud detection, compliance, and professional competencies. Despite increasing discourse around digital transformation, there is limited consensus on how AI is being adopted, the challenges faced, and its implications for accounting information systems (AIS). Our objective is to bridge this gap by conducting a structured analysis of the literature and identifying emerging themes, challenges, and opportunities.

The literature discussed here is reflective of a multi-dimensional shift in the discipline. For instance, extensive reviews have established that AI enhances the effectiveness of traditional accounting procedures and increases the accuracy of financial reporting by automating complex processes. In parallel, studies focusing on fraud prevention reveal that AI’s capabilities in anomaly detection and real-time monitoring are pivotal in mitigating risks. However, these innovations must be synchronized with internal controls and human oversight to be truly effective. Additionally, empirical surveys have shed light on the readiness and perceptions of auditors, highlighting both the social and technical challenges that accompany the integration of advanced technologies into established audit practices.

This article integrates the evidence from a broad array of research contributions. Multiple studies, including systematic literature reviews and meta-analyses, have emphasized the two-sided character of the impact of AI: on the one side, there is irrefutable potential for increased productivity, real-time analysis of data, and improved decision-making; on the other side, challenges such as high implementation costs, ethics issues, job displacement, and technology training needs persist. Further, the international perspective provided by studies conducted in many economic and cultural settings highlights that while all have universally recognized benefits of AI, strategic investment and tailored regulatory frameworks are required to maximize its advantages.

AI in accounting and auditing is defined as the application of computational systems capable of performing tasks that typically require human intelligence. Specifically, this includes:

Machine Learning (ML): Algorithms that learn from historical financial data to detect anomalies, forecast trends, and classify transactions.

Natural Language Processing (NLP): Tools that interpret and generate human language for tasks such as reading contracts, extracting insights from financial disclosures, and automating audit documentation.

Robotic Process Automation (RPA): Software bots that execute rule-based tasks such as invoice processing, reconciliation, and report generation.

These technologies are integrated into accounting information systems to enhance audit quality, reduce manual workload, and improve decision-making accuracy. The review focuses on their empirical applications, adoption challenges, and implications for professional practice.

Beyond defining these technologies, it is crucial to ask why a systematic literature review (SLR) at this juncture is warranted and what it can contribute to both theory and practice. Conducting a systematic literature review on AI in accounting and auditing is particularly important at this stage of technological transformation. While numerous studies examine discrete applications of AI, the evidence remains fragmented across disciplines, regions, and methodological approaches. An SLR enables a transparent and replicable synthesis of the literature, consolidating scattered insights into a coherent body of knowledge. By systematically mapping adoption drivers, barriers, and outcomes, this review contributes not only to academic scholarship but also to practice and policy by clarifying where consensus exists and where gaps remain.

AI has the potential to significantly enhance both accounting practice and audit quality. For example, global audit firms are already employing AI-driven anomaly detection systems that identify unusual journal entries with far greater accuracy than traditional sampling methods. Financial institutions deploy NLP tools to analyze loan contracts and compliance reports, reducing the time spent on document review from days to minutes. Similarly, corporations use RPA to automate repetitive processes such as invoice reconciliation, which in some cases has reduced costs by up to 70%. These examples demonstrate that AI is not an abstract concept but a concrete tool already transforming efficiency, reliability, and fraud prevention in real-world practice. Leading audit firms are already embedding AI technologies into practice in tangible ways. For instance, PwC’s Next Generation Audit employs AI agents to automate anomaly detection and documentation drafting under human oversight, improving both efficiency and integrity in financial reporting. Similarly, NLP-driven tools such as PwC’s AI-assisted disclosure checking and search capabilities enable auditors to review financial statements and documentation more quickly and accurately, enhancing audit quality. In parallel, Robotic Process Automation (RPA) is being deployed in internal audit functions to handle repetitive tasks like reconciliations, thereby boosting productivity, expanding risk coverage, and strengthening compliance. Collectively, these applications demonstrate that AI in accounting and auditing is no longer theoretical but is actively reshaping professional practice (Byrne, 2025).

At the same time, critical challenges highlight the urgency of scholarly synthesis. Ethical concerns surrounding algorithmic bias, opacity, and auditor accountability remain unresolved. Workforce adaptation introduces pressing concerns around new skill requirements, potential job displacement, and shifts in professional identity. Furthermore, regional disparities persist: while developed economies emphasize regulatory alignment and governance, developing economies struggle with infrastructural limitations and high implementation costs. These issues demonstrate that the benefits of AI adoption are not uniform, making it imperative to examine adoption patterns across contexts. By situating this review within these debates, the study underscores its relevance and provides a timely roadmap for future research, practice, and policy.

The Integration of AI in Accounting and Auditing

The pervasive influence of AI has transformed both audit and accounting practices. Jejeniwa et al. (2024) provided an extensive review showing that AI optimizes efficiency and precision in financial reporting, which implies that automation is redefining conventional financial processes. Similarly, Santra (2024) emphasized that AI is not only a technological development but also an agent of radical transformation in the underlying structures of accounting and auditing practices. Abbas (2025) further elaborated on these findings by presenting digitalization in management accounting, where although automation of mundane tasks can maximize efficiency, but data privacy and ethical concerns still need to be resolved. Together, these studies emphasize that the AI revolution is not one-dimensional. It brings greater productivity while requiring adjustments in skills and organizational design.

AI as a Tool for Fraud Detection

One dominant theme in the literature is how AI can be used to advance fraud detection. Mallesha and Hymavathi (2024) discussed the ability of AI to mitigate risks via sophisticated anomaly detection, pattern analysis, and real-time monitoring. Hernandez Aros et al. (2024) supported this by showing how the application of machine learning for fraud detection, particularly in credit card fraud applications, has reported encouraging accuracy rates. Similarly, Odufisan et al. (2025) dealt with the Nigerian context, where AI and machine learning technologies were used to reinforce fraud prevention facilities across sectors. The studies conclude that, although regional differences appear in execution, AI tools play a major role in coping with and countering the rise of financial fraud sophistication.

AI in Auditing Practices and Auditor Readiness

Several studies have examined the shift in auditing practices with the effect of AI. Al-Mawalia et al. (2025) noted that social influence, hedonic motivation, and auditors’ technology readiness significantly affect the use of AI in auditing environments. At the same time, research by Karmańska (2022) and Leocádio et al. (2024) shows that the integration of AI increases not only audit effectiveness and communication with clients but also causes a redefinition of auditors’ roles, from reactive assessors to proactive overseers. Kokina et al. (2025) followed up on this debate by focusing on empirical opportunities and challenges in large public accounting firms, therefore provides evidence that while AI has real-world benefits, successful implementation is still contingent upon cultural and technical readiness.

Emerging Trends and Areas for Future Research

Different systematic literature reviews and meta-analyses have synthesized existing studies to offer the way forward for future research. For instance, Ayad and El Mezouari (2024) in their systematic review established opportunities alongside risks of AI uptake in accounting and agree with calls for additional research into ethical impacts, human-augmented with AI, and calibration of technology to an organization’s needs. In addition, Tandiono (2023), Nwosu et al. (2022), and (Abdo-Salloum & Al-Mousawi, 2025) indicate that the changing climate of accounting education and business process digitalization call for the existing curricula to be reformed to instill skills necessary in an AI-driven world. Finally, studies focused on individual contexts such as those by Patel et al. (2023) and Tritama et al. (2025), highlight that while the twin impact of AI (making things more efficient but also creating challenges such as high costs of implementation) is universal, the future will be shaped by strategic investment and the creation of robust regulatory systems.

Theoretical Framework

To synthesize findings on AI adoption in accounting and auditing, this review draws on established theories of technology adoption and innovation. Three perspectives are particularly relevant: the Technology Acceptance Model (TAM), the Technology–Organization–Environment (TOE) framework, and Institutional Theory.

The Technology Acceptance Model (TAM; Davis, 1989) highlights the importance of perceived usefulness and perceived ease of use in shaping individual adoption of new technologies. This model has been widely applied in accounting and auditing contexts (Al-Mawalia et al., 2025), where it explains how auditors’ and accountants’ perceptions influence their willingness to integrate AI into professional practice.

The TOE framework (Tornatzky & Fleischer, 1990) extends the analysis by considering organizational and environmental factors. Technological readiness, organizational culture, and external pressures such as regulation and market competition all play critical roles in adoption. This framework is particularly useful in understanding how firms differ in their ability to invest in and deploy AI systems.

Finally, Institutional Theory (Scott, 2008) explains why adoption patterns vary across regions and professional settings. Coercive pressures (e.g., regulation), normative pressures (e.g., professional ethics), and cultural-cognitive logics shape how organizations legitimize and implement AI (Carpenter & Feroz, 2001). This perspective is essential for interpreting the contrasting evidence between developed economies, where regulatory and ethical considerations dominate, and developing economies, where infrastructural and resource challenges are more prominent.

Together, TAM, TOE, and Institutional Theory provide a multi-level theoretical foundation for this review. These frameworks align with the conceptual model developed in this study, which organizes adoption into drivers, moderating factors, and outcomes, while accounting for feedback loops and institutional context.

Methodology

This study adopts a systematic review methodology, guided by the PRISMA (Preferred Reporting Items for Systematic Reviews and Meta-Analyses) framework to ensure transparency, rigor, and replicability. The review process involved four key stages: identification, screening, eligibility, and inclusion.

Search Strategy

A comprehensive literature search was conducted across multiple academic databases including Google Scholar, Scopus, Web of Science, and ScienceDirect. The search covered publications from January 2021 to May 2025. Keywords used included combinations of:

“Artificial Intelligence” AND “Accounting”

“AI in Auditing”

“Fraud Detection” AND “Machine Learning”

“AI Adoption” AND “Accounting Information Systems”

“Systematic Review” AND “Auditing”

Boolean operators and truncation were applied to refine the search. The initial search yielded 41 articles.

Inclusion and Exclusion Criteria

To ensure relevance and quality, the following criteria were applied:

Peer-reviewed journal articles, conference papers, and working papers.

Studies published between 2021 and 2025.

Articles focusing on AI applications in accounting and/or auditing.

Empirical, theoretical, or review-based studies with clear methodology.

Non-English publications.

Studies not directly related to accounting or auditing.

Articles lacking methodological transparency or empirical grounding.

Duplicate records and inaccessible full texts.

Screening and Selection Process

The initial search yielded 41 records. After removing five duplicates, 36 titles and abstracts were screened. At this stage, five studies were excluded for not meeting the scope of AI in accounting or auditing. The full text of 31 articles was then assessed against the inclusion and exclusion criteria, resulting in a final set of 31 studies included in this review. The study selection process is illustrated in

PRISMA flow diagram.

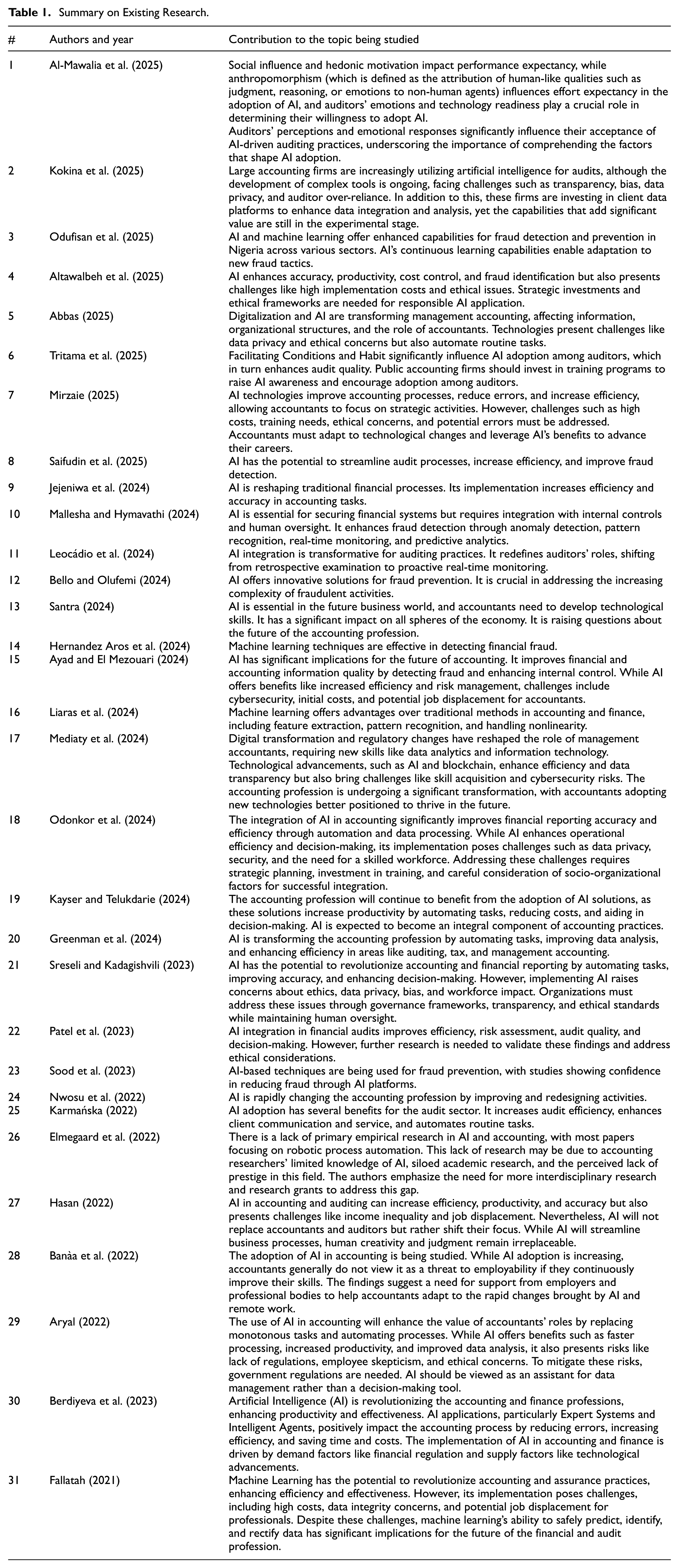

Data Extraction and Quality Assessment

Data extraction was conducted systematically by recording key study characteristics from each selected paper. These characteristics included the authors and publication year as well as their key contribution to topic. This structured extraction enabled the aggregation of comparable data across studies, as illustrated in Table 1.

Summary on Existing Research.

Quality assessment was performed with pre-specified criteria for systematic reviews. All studies were evaluated based on their research design, clarity of methodology, quality of data analysis, and clarity of findings and conclusions. The evaluation ensured that synthesis would be done from high-quality evidence to allow for sound conclusions regarding the impact of AI on accounting and auditing practices.

This study contributes to AIS literature by offering a structured analysis of AI’s role in accounting and auditing. It identifies key adoption trends, gaps in research, and practical implications for educators and practitioners. Future research should explore longitudinal impacts, regulatory developments, and education strategies for AI in accounting.

The extracted data were synthesized using a narrative approach, identifying common themes and divergences across the literature. Key themes included:

The synthesis process involved cross-referencing findings from the dataset with recent articles identified via Google Scholar, thereby ensuring that both established and emerging insights were captured comprehensively.

Results

The systematic review of the literature reveals a multifaceted transformation in accounting and auditing practices driven by the integration of AI. Table 1 presents the key contributions of research conducted since 2021 on the integration of artificial intelligence in accounting and auditing.

The following sections synthesize the key findings and provide an in-depth analysis of recurring themes, regional insights, and methodological variations.

AI Integration and Operational Efficiency

Across the dataset, different studies imply the fact that AI contributes significantly to operational efficiency and accuracy in accounting and auditing procedures. Jejeniwa et al. (2024) and Santra (2024) report that the use of AI technologies such as automation and high-level data analytics has resulted in cost-effective financial reporting and less human effort. Abbas (2025) also emphasizes that digitalization in management accounting comes with the promise of automating manual processes, thereby improving accuracy while challenging traditional roles. In this context, AI has been a double-edged sword, maximizing performance while demanding a shift in professionals’ capabilities and organizational practices.

Fraud Detection Capabilities

One of the dominant themes in the literature review is the increased proficiency of AI in the detection and prevention of financial fraud. Mallesha and Hymavathi (2024) note that the pattern recognition, anomaly detection, and real-time monitoring capacity of AI has tremendously alleviated the threat of fraud. To supplement these findings, Hernandez Aros et al. (2024) and Odufisan et al. (2025) report evidence that machine learning algorithms applied to real-world datasets have improved the detection of fraudulent activity, particularly in credit card transactions and other high-risk domains. This evidence base suggests that, as a fraud prevention device, AI is extremely effective but depends on being integrated with traditional internal controls and continuous human surveillance to assist in mitigating ethical and operational challenges.

Auditor Readiness and Adoption of AI

Several pieces of work scrutinize the complexities of auditor readiness to implement AI tools. Al-Mawalia et al. (2025) report that attitudes toward technology by auditors (under the influence of social influence, hedonic motivation, and readiness) are the ultimate determinants of AI adoption in auditing practice. This argument is corroborated by findings of Kayser and Telukdarie (2024), who employed the Technology Acceptance Model (TAM) theoretical foundation to investigate influencers of AI adoption by auditors. In addition, Karmańska’s (2022) questionnaires and Leocádio et al.’s (2024) conceptual frameworks indicate that while AI enhances audit quality and client communication, it also necessitates a radical shift in auditors' roles from traditional past-oriented examiners to future-oriented, real-time monitors.

Regional Perspectives and Methodological Insights

The information provides blended regional trends in the uptake of AI adoption. For example, research conducted in Nigeria, South Africa, and other developing economies (Jejeniwa et al., 2024; Nwosu et al., 2022; Odufisan et al., 2025) generally suggests concerns of expensive implementation costs and lack of appropriate infrastructural abilities, yet simultaneously indicates significant efficiencies gains and even a potential leapfrogging benefit in leveraging recent technology. On the other hand, European scholarship (Karmańska, 2022; Leocádio et al., 2024) tends to focus on how AI enhances auditing processes in strict regulatory frameworks with emphasis on striking a balance between innovation and adherence to well-established ethical standards.

Moreover, the methodological diversity across the literature from systematic reviews and meta-analyses (Ayad & El Mezouari, 2024; Tandiono, 2023) to surveys and qualitative interviews (Al-Mawalia et al., 2025; Kokina et al., 2025), further enriches the understanding of AI’s implications in accounting and auditing. This plurality of approaches not only lends robustness to the overall findings but also highlights the dynamic interplay between technology adoption and organizational change.

Synthesis of Key Challenges and Opportunities

As great as is the potential for accounting and auditing transformation via AI, so too are the inherent challenges that the research reveals. At the top of these are ethical issues regarding data privacy, job displacement, and strong testing of algorithmic choices. Ethical issues are emphasized in various papers (e.g., Abbas, 2025; Santra, 2024), with an appeal for regulatory systems that facilitate technical advancement with strong mechanisms of governance. In addition, the significant expense of deployment and the high technology factor in applying AI in developing markets are warning signs against the scalability of AI solutions across different economic conditions.

On the other hand, the study also points out enormous opportunities. The potential of AI to revolutionize conventional accounting functions, improve fraud detection, and offer real-time financial analysis is an opportunity to create more nimble and robust financial systems. Future studies are invited to bridge the gaps identified by concentrating on region-specific issues, streamlining ethical frameworks, and investing in training programs that develop the required technological skills among accounting professionals.

In summary, the systematic review of the literature reveals that while AI integration in accounting and auditing significantly enhances efficiency and fraud detection capabilities, it also raises substantial challenges regarding auditor readiness, ethical considerations, and infrastructural disparities. The integration of diverse methodologies and the regional perspectives captured in the dataset underscore the need for ongoing research and tailored implementation strategies to fully harness AI’s transformative potential.

Discussion

Findings indicate a growing but uneven integration of AI in accounting and auditing. While automation and data analytics are well explored, areas such as ethical implications, trust in AI, and audit assurance remain underdeveloped. Practitioners are challenged by data quality, talent shortages, and regulatory ambiguity. Our synthesis reveals a need for interdisciplinary research and adaptive frameworks that incorporate AI governance and training. The synthesis of the literature reveals a dynamic interplay between innovation and challenge in the application of artificial intelligence (AI) within accounting and auditing.

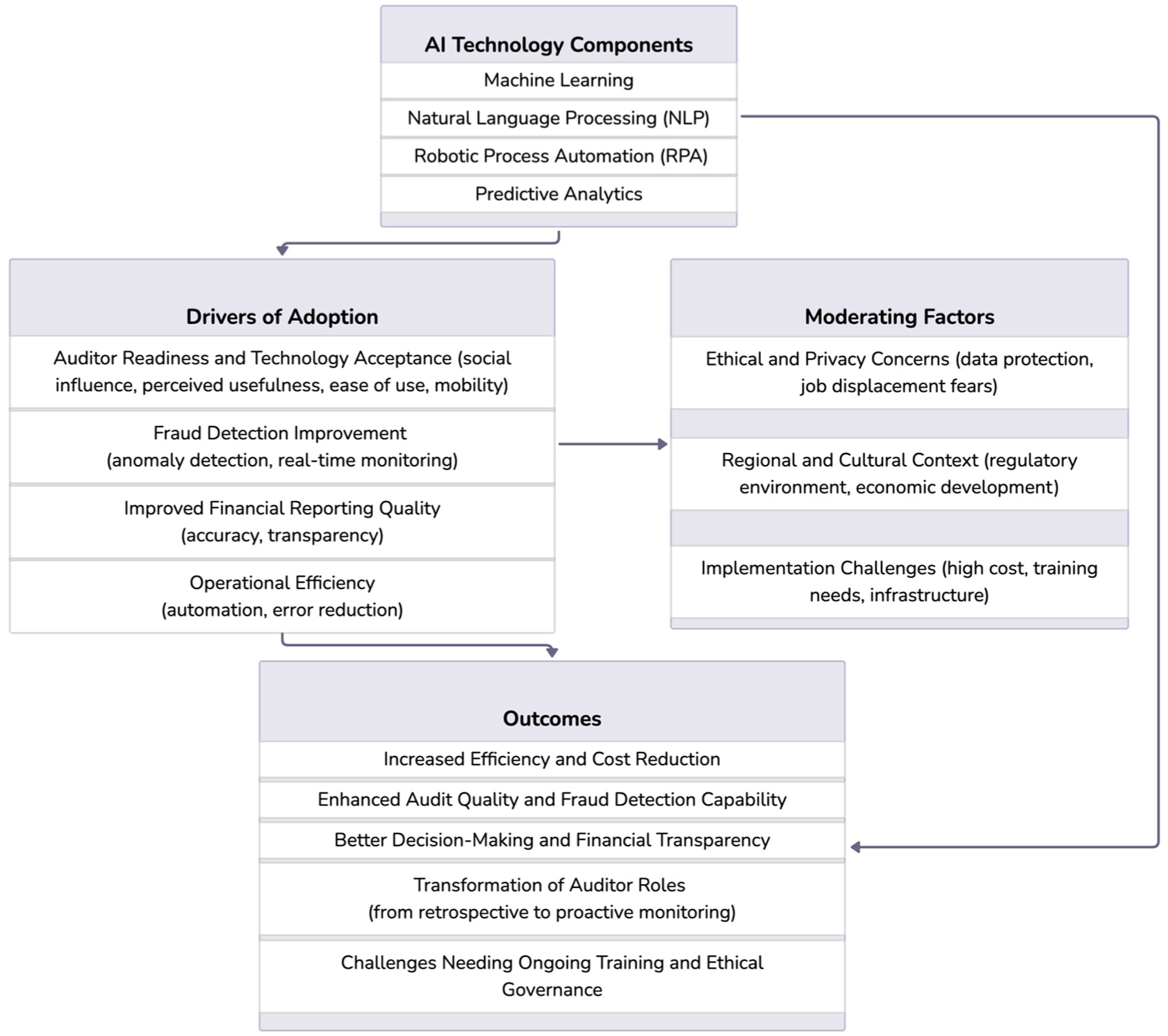

Figure 2 presents a conceptual framework synthesizing the findings of this review, illustrating how AI technologies interact with adoption drivers, moderating factors, and outcomes in accounting and auditing contexts.

Conceptual framework for AI adoption.

Th ius review reveals a dynamic and multi-layered transformation in accounting and auditing practices driven by artificial intelligence. To synthesize these insights, a conceptual framework was developed that organizes the literature into four interrelated layers: AI technology components, drivers of adoption, moderating factors, and outcomes.

At the foundation, AI technologies such as machine learning, natural language processing, robotic process automation, and predictive analytics serve as the core tools reshaping financial processes. These technologies are not merely technical upgrades; they represent a shift in how data is processed, interpreted, and acted upon in accounting environments.

The mediating layer captures the drivers of adoption, including operational efficiency, fraud detection capabilities, improved financial reporting quality, and auditor readiness. These drivers are influenced by both organizational investment and regulatory support, highlighting the importance of institutional alignment in successful AI integration.

Moderating factors such as ethical concerns, implementation challenges, regional context, and human-AI interaction add complexity to the adoption process. These elements do not operate in isolation but actively shape how AI technologies are received and utilized. For instance, trust in AI systems and auditors’ emotional responses can significantly influence the effectiveness of adoption, suggesting that human factors are as critical as technical ones.

The outcomes of AI adoption are multifaceted. Increased efficiency, enhanced audit quality, and improved fraud detection are frequently cited benefits. However, the transformation of auditor roles (from retrospective examiners to proactive monitors) signals a deeper professional shift. This evolution demands ongoing training, ethical governance, and adaptive learning environments to ensure that auditors remain equipped to navigate AI-enhanced workflows.

Importantly, the framework introduces a feedback loop from outcomes back to auditor readiness. This loop emphasizes that AI adoption is not a one-time event but a continuous process requiring iterative learning and organizational adaptation. As AI tools evolve, so too must the competencies and ethical standards of those who use them.

By integrating these layers, the framework offers a holistic view of AI adoption in accounting and auditing. It moves beyond descriptive summaries to provide a structured lens for understanding the interplay between technology, human behavior, institutional context, and professional transformation. This synthesis contributes to the literature by proposing a conceptual roadmap for future empirical research and policy development.

Collectively, these discussions articulate a vision of AI as a transformative tool for accounting and auditing. It has the potential to drive economic efficiency and innovation while contributing to broader objectives such as sustainable development and ethical governance.

While the reviewed studies consistently demonstrate AI’s potential to improve efficiency and fraud detection in accounting and auditing, the evidence reveals important contradictions and tensions. For example, Jejeniwa et al. (2024) and Abbas (2025) emphasize productivity gains from automation, whereas Kokina et al. (2025) underscores risks of auditor over-reliance and algorithmic opacity. Similarly, while Aryal (2022) argues AI complements human judgment, Hasan (2022) warns of potential job displacement and inequality.

These divergent findings can be better understood through the Technology Acceptance Model (TAM), which suggests that adoption hinges on perceived usefulness and ease of use. Indeed, Al-Mawalia et al. (2025) show that social influence and hedonic motivation strongly shape auditors’ willingness to adopt AI, highlighting that technical capability alone does not guarantee acceptance. From an Institutional Theory perspective, regional regulatory and cultural environments further explain variation: studies in Europe stress regulatory compliance and ethics (Karmańska, 2022; Leocádio et al., 2024), whereas research in developing economies highlights infrastructure and cost barriers (Odufisan et al., 2025).

This systematic review therefore reveals three critical research gaps:

Longitudinal adoption dynamics – Few studies track how attitudes toward AI evolve over time.

Ethical implications and trust – Despite frequent mentions of ethics, little empirical work examines how auditors and clients build trust in AI systems.

Quantitative synthesis – There is a need for meta-analytic studies comparing fraud detection accuracy across AI models and contexts, to move beyond anecdotal claims of “improvement.”

By mapping these convergences, contradictions, and gaps, our review contributes not just a descriptive summary but a conceptual synthesis that can guide future research and practice in accounting and auditing.

The reviewed studies reveal both convergence and divergence in the role of AI in accounting and auditing. A clear consensus exists that AI enhances efficiency and fraud detection (Jejeniwa et al., 2024; Mallesha & Hymavathi, 2024; Santra, 2024). However, important contradictions emerge. While Aryal (2022) and Banàa et al. (2022) suggest AI complements human judgment and does not endanger employment if continuous learning is pursued, Hasan (2022) and Abbas (2025) raise concerns about potential job displacement, inequality, and ethical risks. Similarly, while large-firm studies (Kokina et al., 2025) report strategic integration of AI, they also caution against over-reliance on opaque algorithms, highlighting limits in transparency and accountability.

The quality of evidence across studies also varies. Conceptual frameworks and reviews dominate (e.g., Ayad & El Mezouari, 2024; Santra, 2024), but empirical contributions remain limited, particularly large-sample studies or longitudinal analyses (Elmegaard et al., 2022). This imbalance underscores the need for more robust, data-driven research to validate widely claimed efficiency and fraud detection gains.

Regional comparisons further highlight contextual differences. In developed economies such as Europe, AI adoption is often framed within strict regulatory and ethical constraints (Karmańska, 2022; Leocádio et al., 2024), with emphasis on maintaining trust and compliance. In contrast, developing contexts (e.g., Nigeria, South Africa) highlight challenges of infrastructure, costs, and uneven readiness (Jejeniwa et al., 2024; Odufisan et al., 2025), alongside opportunities to leapfrog legacy systems. These differences suggest that AI adoption is not uniform but contingent on institutional, economic, and cultural contexts.

Taken together, this review contributes a critical synthesis that highlights where the literature aligns (efficiency, fraud detection), where it diverges (employment impact, ethics, transparency), and where contextual differences matter (developed vs. developing economies). This comparative analysis reveals pressing gaps: the need for empirical validation, region-specific policy frameworks, and deeper examination of trust and ethical governance in AI-enabled accounting.

Theoretical Integration

The adoption of AI in accounting and auditing can be better understood when findings are situated within established adoption and innovation theories. Our review reveals that no single framework fully captures the complexity of adoption; rather, insights emerge from integrating multiple perspectives.

Technology Acceptance Model (TAM). TAM explains how perceptions shape individual adoption. Studies highlighting efficiency and productivity gains (Jejeniwa et al., 2024; Santra, 2024) align with perceived usefulness, while those noting skill barriers and resistance (Abbas, 2025; Hasan, 2022) reflect challenges to perceived ease of use and trust. This duality explains contradictory findings about whether AI complements or threatens professional roles.

Technology–Organization–Environment (TOE) framework. TOE extends the analysis to organizational and contextual factors. Evidence of successful adoption in large firms with strong infrastructure (Kokina et al., 2025) illustrates the role of technological and organizational readiness, whereas challenges in developing economies (Odufisan et al., 2025) highlight environmental constraints such as regulatory gaps and resource scarcity.

Institutional Theory. Regional variations are well captured by Institutional Theory. European studies (Karmańska, 2022; Leocádio et al., 2024) emphasize compliance and ethical norms, consistent with coercive and normative institutional pressures, while African studies stress cost and infrastructure challenges (Jejeniwa et al., 2024), reflecting differing institutional logics.

Together, these theories explain the uneven adoption patterns identified in the literature. By synthesizing TAM, TOE, and Institutional Theory, our framework clarifies that AI adoption in accounting is not determined solely by technical capacity but is shaped by an interplay of individual perceptions, organizational readiness, and institutional environments. This integrated lens advances theoretical understanding and offers a roadmap for future empirical research.

Conclusion

This systematic review demonstrates that AI is reshaping accounting and auditing through automation, data analytics, and decision-support capabilities. Building on prior findings, the paper contributes a theoretical synthesis integrating TAM, TOE, and Institutional Theory, illustrating that AI adoption depends not only on technological readiness but also on human, organizational, and regulatory contexts.

Beyond these theoretical insights, the review offers practical implications: auditors should pursue hybrid models that combine AI with professional judgment; regulators must establish adaptive guidelines for transparency and accountability; and educators should embed AI competencies within accounting curricula.

This study identifies clear avenues for future research, including longitudinal analyses of adoption trajectories, comparative evaluations of AI models’ fraud detection accuracy, and deeper investigations into ethical trust-building in AI-enabled environments. Collectively, these directions can support a more responsible and evidence-driven integration of AI in accounting and auditing.

Finally, this research has several limitations that should be considered when interpreting the findings. While it provides a comprehensive synthesis of research on artificial intelligence in accounting and auditing, several limitations should be acknowledged. First, the review is limited to studies published between 2021 and 2025 in English-language journals, which may exclude relevant insights from earlier or non-English research. Second, the review did not perform a quantitative meta-analysis due to the heterogeneity of research designs and measures used across studies. Third, publication bias may have influenced the findings, as studies reporting positive outcomes of AI adoption are more likely to be published than those with null or negative results. Finally, because the study focuses on published academic sources, the perspectives of practitioners and policymakers are underrepresented, limiting the practical dimension of the synthesis. Recognizing these limitations, future research should employ longitudinal and mixed-method designs, and include practitioner-based studies to provide deeper empirical and practical insights into artificial intelligence’s impact on accounting and auditing.

Footnotes

Consent to Participate

This article does not contain any studies with human participants or animals.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

All data analyzed in this study consist of previously published articles that are publicly available through academic databases. No new primary data were created or collected for this systematic review.

AI Declaration

During the preparation of this manuscript, the author used ChatGPT (OpenAI) to assist with language refinement and editing under the author’s direct supervision. The tool was used to improve clarity, grammar, and readability. The author reviewed and edited all content generated by the tool and takes full responsibility for the integrity and accuracy of the final manuscript.