Abstract

This review study examines the existing literature on internal audit (IA) in the United States to identify how internal audit functions (IAFs) have evolved in response to global shifts in business practices. Despite growing attention to IA, the literature remains fragmented, limiting a comprehensive understanding of how IA has evolved in response to business practices. Through a systematic review, this study analyzes 171 studies published between 1984 and 2023 retrieved from the Scopus database. This study investigates the characteristics of the literature and topics discussed, focusing on six key aspects: the practice of IA, the role of IA, the quality of IA, information technology (IT) auditing, risk management, and the relationship between IA and other parties. The results reveal a paradigm shift in the activities undertaken by internal auditors and a significant transition in the literature from discussing traditional topics to new topics related to environmental changes, the climate crisis, geopolitical challenges, and technological developments. The results also emphasize the need for more theory-based, empirical, and comparative studies on IA in different contexts and sectors. This paper identifies substantial gaps in IA literature and proposes directions for future research agendas, particularly concerning the influence of politics, culture, and the effects of COVID-19 on IA practices. These insights provide valuable guidance for IA practitioners, researchers, standard setters, and the Institute of Internal Auditors (IIA) in refining frameworks and understanding global IA trends.

Keywords

Introduction

Background

Internal auditing (IA) is an independent, objective activity that provides consulting and assurance services designed to add value and enhance an organization’s performance (Abdelrahim & Al-Malkawi, 2024). By employing a structured, systematic, and disciplined approach, IA supports organizations in achieving their goals by assessing the efficiency of risk management processes and strengthening governance practices (IIA, 2024). However, the IA profession currently faces significant challenges, both at the micro level within organizations and at the macro level due to stakeholders’ perceptions of its inadequate contributions. This perception has threatened the importance and legitimacy of IA as a profession (Lenz & Jeppesen, 2022), and has undermined its highly valued professional status in society, which provides unique value (Ayaya & Pretorius, 2021). The World Economic Forum (2020) indicates a decline in demand for the audit profession. The report’s findings also reveal that auditing and accounting are ranked fourth in the order of required jobs. Therefore, there have been increasing calls to present a roadmap for understanding the mechanism for developing IA from various fields. For example, Lenz and Jeppesen (2022) emphasize the need for more research focused on linking professional and academic aspects, given that the IA profession has not fully progressed to achieve the desired goals in the previous period. On the other hand, Hazaea, Zhu, Khatib, and Elamer (2022) highlighted a lack of knowledge regarding the factors that influence and a comprehensive understanding of the functions and profession of IA, which has affected its implementation and practice. This would require documentation of IA practices (tools of trade, services, clients) to build a unique value offering.

Problem Statement

Despite the significance of IA to organizations and societies, many studies have confirmed that IA is a black box that has yet to be fully understood (Abdullah et al., 2018; Lenz et al., 2018; Prasad et al., 2021). To make IA more comprehensible, further research is essential in order to build foundational knowledge and demystify its complexities and practices. In this context, and in light of the growing calls for more analyses, there is a pressing need for a systematic literature review (SLR) to investigate the reality and practice of IA based on previous literature assess the current state of the field and outline a roadmap for future research to address the gaps. While other forms of literature review, such as traditional narrative reviews and scoping reviews, offer valuable insights, an SLR is particularly well-suited for this study as it provides a rigorous, transparent, and replicable methodology that systematically identifies, evaluates, and synthesizes relevant studies (Aghileh et al., 2024). According to Kraus et al. (2022, 2021) conducting an SLR mainly aids in identifying research gaps, which guide future studies to address them through relevant empirical and conceptual studies.

In the United States, the regulatory requirements for IA are undergoing significant changes, contributing to the activation of internal audit functions (IAFs) and the strengthening of controls related to financial reporting (Hass et al., 2006). In addition, the regulatory environment for IA in the United States is such that a larger portion of resources allocated for implementing IAFs is directed toward ensuring compliance with the Sarbanes-Oxley Act (SOX), a legislative mandate and regulatory framework that supports the practices of corporate governance (PwC, 2006). Moreover, the rise in the application of IAFs has been associated with several factors, including global competition, high stakeholder expectations, and increased communication (Burnaby & Hass, 2011). However, the scope of IA in the United States has significantly broadened from traditional functions to governance, compliance, and risk assessment as various governance bodies, such as the American Committee for Sponsoring Organizations, determine the basic conditions for expansion and work to provide various guidelines for its implementation (Jung & Cho, 2022).

While other review studies in recent years have focused on discussing the IA literature in different countries, such as China (Hazaea et al., 2021), the Middle East and North Africa (Al-Akra et al., 2016), Europe (Hazaea, Zhu, Khatib, & Elamer, 2022), and the Arab World (Hazaea et al., 2023), in light of these expansions and measures in the United States, there is a pressing need to specifically examine the direction of research. In this context, the literature indicates limited efforts to study and evaluate the IA literature in the United States through the presence of Hass et al. (2006) which focused mainly on discussing some limited literature to investigate the development in the practice of IAFs. On the other hand, unlike Kotb et al. (2020) and Roussy and Perron (2018), which relied on specific periods from 2005 to 2017 and 2018, the geographical scope was not confined to the United States but encompassed entire countries, and research papers were taken from ABCD and ABS classifications. Our study addresses these gaps by ensuring that this paper (i) discusses IA literature that uses a sample or discusses the practice of IA in the United States market only; (ii) uses Scopus, the largest and most comprehensive database for literature (Nerantzidis et al., 2022); (iii) imposes no restrictions on a specific timeframe, so this study covers all literature from 1984 to 2023. By not imposing any restrictions on the time frame of publication of the literature, the evolution of IA, including regulatory changes, underlying theories, and publication trends, can be captured over time, ensuring a comprehensive understanding of IA practices and highlighting their progress in the United States market; (iv) considers all facets of studies that discuss IA.

Guiding Review Questions

This study aims to expand knowledge and address gaps in previous reviews by focusing on five key questions:

Nature and Boundaries of IA

Wibowo et al. (2021) observe that the roles of IA defined by the IIA (1999) have extended from being providers of advisory services on internal controls to providers of assurance services. The guideline issued by the IIA (2017) has further expanded the IA roles to include managing risks and enhancing governance. In short, Abdelrahim and Al-Malkawi (2024) sum up that IAs are expected to be independent and objective agents that provide consulting and assurance services designed to add value and enhance organizational performance. Literature has revealed that the major role of IA has changed from evaluating and reviewing controls and monitoring the preparation of reports and regulatory risks (Carcello et al., 2005) to becoming an internal watchdog on systems of internal control as well as an assessor of firms’ governance structures, mitigating risk, promoting growth, and identifying areas of wastage and inefficiency as well as areas needing improvement to increase returns. IAs are expected to move beyond Gacoń (2013) who reports that the level of professionalism in discharging their tasks and in ensuring that financial statements adhere to auditing and accounting principles and regulations, as well as possessing relevant academic qualifications and professional certificates, and attending continuous professional training and education, to caring for their clients and society. IAs are expected to be ethical and professional in discharging their duties, protecting the rights of all stakeholders and maintaining the integrity of the profession (Abbott et al., 2022; Alzeban & Gwilliam, 2014; Martin et al., 2014).

Important and Objectives of the Study

To our knowledge, no study has conducted a SLR on impact assessment IA in the United States, except for Hass et al. (2006), which analyzed literature up to 2006. This paper contributes to the development of literary and intellectual knowledge about IA through: (i) this wide-ranging extensive analysis provides an in depth understanding of how IA has evolved in the United States market, particularly in response to the major financial crises and the COVID-19 pandemic. Focusing on the United States market, which has distinct regulatory requirements such as compliance with SOX, this study makes a unique contribution by guiding future empirical and conceptual research, that would provide essential guidelines for professionals and academics in a way that contributes to the development and strengthening of the IA profession; (ii) providing a detailed investigation of the topics covered in the literature and identifying gaps for future studies to address, thereby enhancing the understanding of all aspects related to IA; (iii) examining the topics and approaches used in defining how the IAFs developed over time and the factors that contributed to that; and (iv) integrating the results of this study with those from other studies on IA in other countries, such as China (Hazaea et al., 2021), Europe (Hazaea, Zhu, Khatib, & Elamer, 2022), and the Middle East (Al-Akra et al., 2016), to help organizations like the Institute of Internal Auditing (IIA) develop new frameworks, identify strengths, enhance key themes, and address weaknesses, thereby establishing a proper IA practice mechanism that effectively achieves organizational objectives. Finally, this study will provide practical insights that can assist practitioners in enhancing IAFs while significantly contributing to academic discourse by addressing identified research gaps.

The rest of this paper is structured as follows: Section 2 outlines the methodology of the study. Section 3 details the results of the SLR. Section 4 discusses the findings and proposes a future research agenda, followed by a conclusion; limitations are addressed in Section 5.

Methodology

SLR Design

The SLR method is the most common, applied, and reliable method for collecting literature that discusses a specific topic (Booth et al., 2020). Several recent studies have advocated systematic approaches to analyzing the literature (Hazaea, Zhu, Khatib, & Elamer, 2022; Wut et al., 2022). SLR can enhance the literature investigation process and reduce bias (Massaro et al., 2016). This review follows a rigorous method and a specific, clear methodology with defined steps for identifying, collecting, and examining the literature on IA in the United States. This contributes to an overview of IA practices and provides suggestions for future research. This review contributes to an overview of IA practices and offers suggestions for future research. We adopted methods used in previous studies, such as those by Hazaea et al. (2021), Hazaea, Zhu, Khatib, Bazhair, and Elamer (2022), Nerantzidis et al. (2022), and Singh et al. (2022) to minimize biases in compiling and discussing the literature. The methodology for obtaining the literature for analysis included several steps as follows:

Study Population and Data Sources

We use the SLR approach to ensure all the papers published from 1984 to 2023 were included in this study. A search was conducted in the Scopus database for literature that includes the following keywords in the main title of the manuscript, the abstract and the keywords of the literature: “internal audit - auditing”

Sampling Procedure

This study discusses the literature that has been published regarding IA in the United States in light of two crises that had a major role in changing the objectives of IA, namely:

The financial crisis of 2008 to 2009.

The COVID-19 crisis (2019).

It highlights the increasing pressures companies face in managing and enhancing their reputation regarding environmental, social, and governance (ESG) issues. Thus, IA is recognized as a crucial factor in enhancing risk management and ensuring compliance with ESG initiatives.

We use the following steps to obtain the samples:

Data Analysis

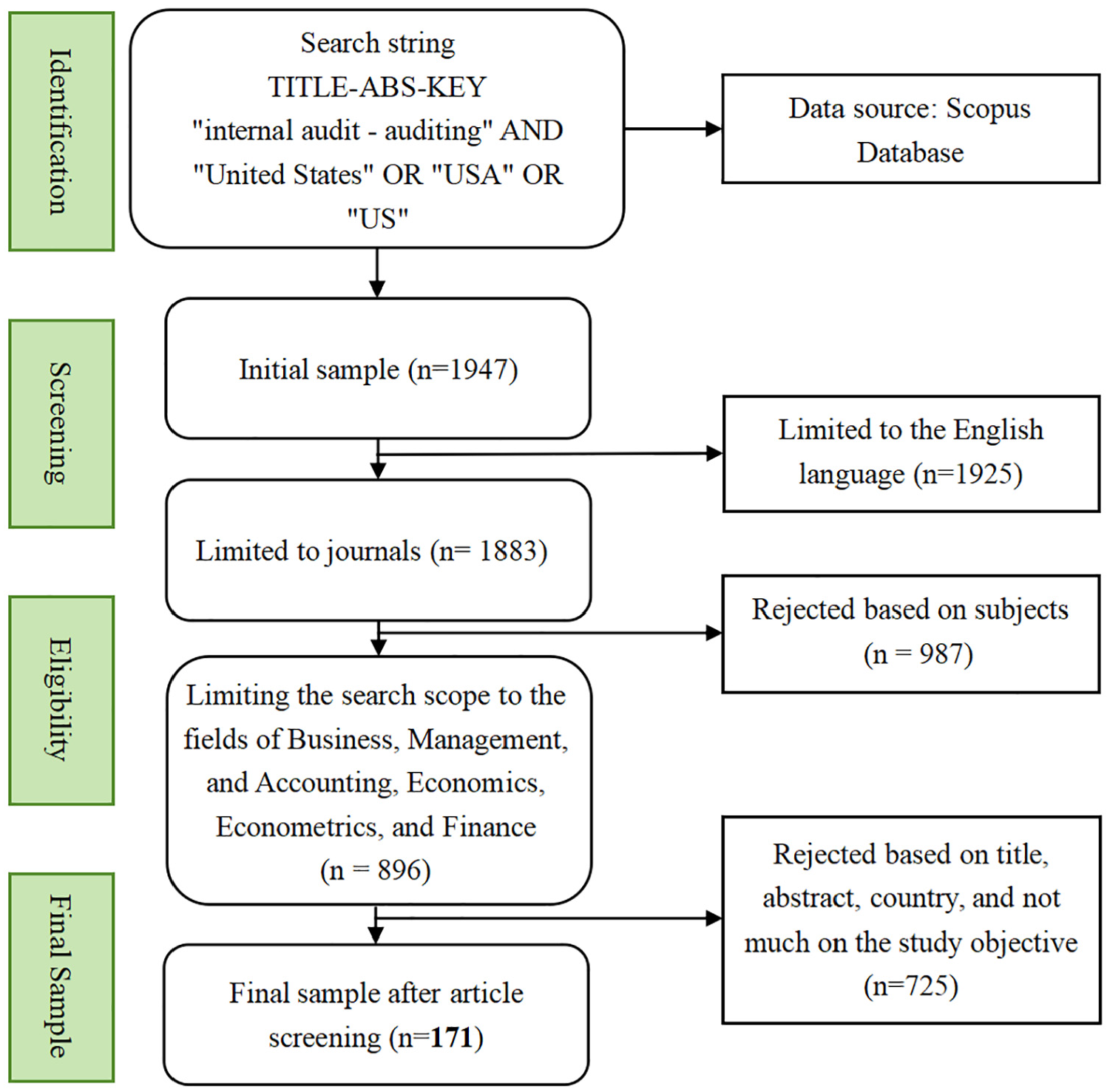

We downloaded all remaining literature (171 studies) and examined the annual trends, theoretical backgrounds, journal names where the studies were published, and the topics the literature focused on. We also extracted directions for future studies to address current gaps. Figure 1 illustrates the protocol for obtaining the literature sample.

Research protocol.

Results of SLR

Publication Trends

Figure 2 illustrates the distribution of the literature used in this study based on publication year. It shows that the literature on IA in the United States saw a significant rise after 2009. The increase in IA literature can be linked to the financial crisis that transpired during 2007 to 2008, regulatory requirements, the increase in globalization and the expansion of trade in various countries. In addition to the failure of some companies such as Enron and World Com, this prompted research into the significance and implementation of IA (Burnaby & Hass, 2011; Hazaea, Zhu, Khatib, & Elamer, 2022). Additionally, the requirements of Section 404 of the SOX in the United States, created a demand for research on the implementation of IA regulations (Grabmann & Hofer, 2014; Parker & Johnson, 2017). Therefore, these changes led to the need to search for a mechanism through which IA can be implemented and the issuance of special laws and instructions. Conversely, the stakeholders interest in robust regulations and procedures to enhance IA effectiveness motivated academics to research this field, increasing IA-related publications (Fraser et al., 2020).

Publications trends by year.

In recent years, companies have engaged in sustainability activities, and researchers have explored the activation and practice of IAFs using various methods, such as Artificial Intelligence (AI), to identify mechanisms that achieve stakeholder objectives. According to the study by Hazaea, Zhu, Khatib, and Elamer (2022) the importance of the practice and functions of IA in preserving institutions and companies while promoting sustainability by academics and others has formed a large and broad trend in the recent period, allowing for the identification of the correct mechanisms that can be followed to achieve the objectives of stakeholders. Christ et al. (2021) confirm that several emerging topics related to IA remain underexplored, prompting researchers to investigate these areas further. These topics include innovations in IT, auditing, and rapid auditing. Therefore, it can be said that stakeholders have a strong interest in understanding the correct practice of IA and its implementation to enhance sustainability. IA is seen as an important factor in strengthening governance and contributes significantly to control and risk management within companies. IA research has evolved significantly over time, reflecting positively on the changes and needs of institutions and regulatory environments in this regard. By dividing the sample under investigation into three stages, the first stage includes the literature before 2001, the second stage includes the literature between 2001 and 2019, and the third stage includes the literature after 2019. We categorized each study based on the topic it covered and discovered that the first phase concentrated on the customary responsibilities of IAFs, including compliance, regulatory control improvement, and fraud detection. Furthermore, a dearth of research has been done on the interaction between IA and audit committees, governance, and external audit. The second phase of IA research covered a wider range of topics, including the effects of laws like the SOX law, the application of standards to ensure risk mitigation, and the role of information technology (IT) in enhancing IA effectiveness. It also included a discussion of how IA supports governance, fraud prevention, and earnings management. In the third stage, the literature explores the role of IA in enhancing decision-making and investment strategies. In addition, the literature has expanded the discussion of the role of IA in enhancing governance and its impact on audit committees.

Journal Distributions

In this section, we review the distribution of the literature samples used in this study based on the scope of the journals in which they were published. Table 1, section 1, shows that 158 studies were published in accounting journals. Of these, 67 (39.18%) appeared in influential auditing journals: “Auditing: A Journal of Practice & Theory” (12 studies), Managerial Auditing Journal (43 studies), Current Issues in Auditing (5 studies), International Journal of Auditing (4 studies), “Journal of Accounting, Auditing & Finance” (1 study), and “International Journal of Accounting, Auditing and Performance Evaluation” (1 study). The remaining 91 studies (53.22%) were in highly influential specialized accounting journals, with Accounting Horizons having the most )14 studies (. Examining the nature of the journals, we see that the high number of studies in Managerial Auditing Journal and Auditing: A Journal of Practice & Theory confirms their key role in auditing research. Publication in top auditing and accounting journals highlights the importance of this research for advancing IA and indicating rigorous IA research valued for improving practice and sustainability. The results suggest the literature’s value in defining IA role in adding organizational value and maintaining corporate sustainability. Finally, the analysis reveals that 13 studies (7.60%) were published in management journals, addressing IA issues related to IT and systems, such as: Kim et al. (2009), Li et al. (2018), Steinbart et al. (2013), and Vasarhelyi et al. (2012). Thus, a smaller portion of articles is in management journals related to IA’s interaction with IT and systems. Figure 3 illustrate the distribution of the literature by journals.

Results of the SLR.

Source. Hazaea et al. (2021) and Hristov et al. (2021).

Note. Other theories *1/ includes/ Contingency theory(3), motivation theory (3), source credibility theory (2), psychology theory (2), theory of planned behavior (1),diffusion of innovation theory (1), structuration theory (1), microeconomic theory(1), cultural relativism theory (1), Brunson’s theory of organizational (1), belief function theory (1), responsibility theory (1), the theory of cultural (1), accountability theory (1), grounded theory (1), theory of technological dominance (1), vocational theory (1), social cognitive theory (1),feature-based theory of sensemaking triggers (1), spillover theory (1) organization behavior theory (1), Hogarth’s theory (1),the underlying theory (1), economic incentive theory (1),financial incentive theory (1), corporate finance theory (1), rationality cognition theory (1), behavioral decision theory (1), Dempster-Shafer theory (1), self-categorization theory(1), social theory(1), game theory (1), signaling theory (1), assurance theory (1), availability theory (1), TQM theory(1), economic theory (1), leadership theory (1 )and impression management theory (1). Others*2// includes/MANOVA, Sensitivity analysis, Logistic regression, Pearson pairwise correlations, Robustness/Loan analyses. Others*3/ includes /implication of IA, behavioral aspects, criti- cal thinking, developing of IA, decision-making, internal auditors and job stress, reliance on IA, internal auditor communications, determinants and consequences, data analytics, outsourcing of IA activities, IA style, regulation related to IA, IA fees.

Publications by journals.

Theories Underpinning

We extracted the theories utilized in the IA literature in the United States, adhering to the methodology of prior studies, such as (Hazaea, Zhu, Khatib, Bazhair, & Elamer, 2022; Schmidt & Günther, 2016). Table 1 indicates that only 69 studies were grounded in theories, explaining IA development and practice in the United States context. Nerantzidis et al. (2022) reported that not grounding IA literature in theory makes the results harder to understand. Beck and Stolterman (2016) demonstrated that descriptive literature without theoretical grounding contributes minimally to the development of new theories or provides deep explanations. The results reveal that agency theory was used in 12 studies, affirming its widespread use in IA research. According to Adams (1994) and Hazaea, Zhu, Khatib, and Elamer (2022) agency theory can provide insights into implementing and applying IA, clarify the significance of IAF, delineate the roles of internal auditors, and investigate IA nature. Therefore, theories have been applied in IA literature as a tool to explain IA implementation mechanisms, add knowledge, investigate IA roles, and extract new information to advance IAFs (Abdolmohammadi, 2012; Aikins, 2013; Islam & Stafford, 2022; Li et al., 2018; Wallace & Kreutzfeldt, 1991).

Therefore, only a fraction of United States IA literature employs theories as an explanatory basis. Agency theory is the most common. Using theories broader application would enhance understanding of IA within the United States context by providing conceptual grounding to explain development, implementation, roles, and inform advancements. Future studies could explicitly use practice theory to promote a deeper understanding of IA and its practice as an important theory in the social sciences. It is worth noting that the change in the direction of using theories has developed significantly, as the literature prior to 2001 primarily focused on limited studies on the use of agency theory and its view of organizational behavior, decision behavior theory, and basic economic theories. However, in the post-2001 stage, the use of theories has expanded to encompass behavioral decision-making theories, technology theories, and theories of social and cultural behavior and their effects on the practice of IA. In the last stage, the use of theories has further evolved to include those related to achieving sustainability, such as social theory and social identity theory, in addition to leadership theory.

Organization Focus

We followed previous literature that discussed IA in geographic areas other than the United States (Hazaea et al., 2021; Hazaea, Zhu, Khatib, & Elamer, 2022). Consequently, we explored the type of organization from which the data were obtained. The results show that the research pertaining to the public sector ranked highest, with 44 studies (25.73%). This may be attributed to government encouragement for researchers when faced with a problem that must be solved or because the public sector is more exposed to risks than other sectors (Hazaea et al., 2021). Second, there were 24 studies (14.03%) applied to stock exchanges, likely due to the relative ease of accessing company reports compared to the data of private companies, on which a limited number of studies were applied (Hazaea, Zhu, Khatib, & Elamer, 2022). Finally, the investigation reveals that 83 studies (50.57%) didn’t specify the data source, whereas the studies are case studies or were conducted theoretically/reviews and did not determine the data source. It should be noted that some researchers face difficulty smoothly obtaining company data, in addition to auditors’ inability to provide any data without higher management approval (Hazaea, Zhu, Khatib, Bazhair, & Elamer, 2022; Nerantzidis et al., 2022). Based on the findings, the focus should shift toward conducting studies utilizing private sector data, either through reports or by using primary data collection tools such as questionnaires and interviews. In addition, future studies should broaden empirical research across all sectors based on data analysis and reports. This will enhance the effectiveness of the literature findings and improve IA practices.

Type of Test/Methods

The results of the investigation revealed that multiple regression, ANOVA, and t-tests were used significantly compared to the rest of the tests. The ANOVA test was applied in studies examining the role of internal auditors in detecting fraud Carpenter et al. (2011) and assessing the performance of internal auditors by company CEOs based on cultural group and professional level Abdolmohammadi (2012), and IA evaluation by external auditors (R. Desai et al., 2017). Descriptive statistics, path coefficients, and ANCOVA results were employed in three studies to explore management perceptions of IAFs Farkas et al. (2019), the impact of practicing IAFs on stakeholder and investor perceptions of the credibility of financial reporting disclosure Holt (2012), and the relationship between IA and external audits (Brody et al., 1998). Investigations reveal that certain tests are commonly used, especially in the IA literature, owing to their reliance on primary data, which remains limited in application, such as the Structural Equation Modeling (SEM) model. Future studies must address this issue.

Research Instruments

Additional analysis revealed that the literature heavily depended on primary data collected via questionnaires. Specifically, 52 studies (30.41%) employed this method to collect data and explore the topics and methods of IA (Glover et al., 2008; Kotb et al., 2014; Li et al., 2018; McCartney et al., 2002; Raghunandan et al., 2001). Questionnaires are among the most crucial means of obtaining real and reliable data, especially for accounting majors (Roopa & Rani, 2012). Interviews were used in only nine studies (5.26%), such as (Christ et al., 2015). The findings also indicate that company reports were referenced in 39 studies (22.80%), while 48 studies (28.07%) were theoretical/review-based. Case studies and content analysis were used in 23 studies (13.45%). The investigation highlights the necessity for more studies employing interviews as one of the most important tools for collecting data on IA, through which auditors’ perceptions, experiences, and opinions about how IA is practiced can be discerned. Finally, future studies should place greater emphasis on reports to compare and evaluate the performance of IA before and after the COVID-19 crisis.

Thematic Analysis

This section reviews the thematic distribution of the literature under investigation. We followed Hazaea, Zhu, Khatib, and Elamer (2022) and Nerantzidis et al. (2022) to organize this classification enabling us to determine the subject of each study after summarizing the goals, trends, and results of each study individually. This classification can contribute to identifying the gaps that can be addressed in future research. It should be noted that there is literature discussing different topics, which has been classified under “Others” to avoid bias. It is evident from Table 1 that several topics have attracted researchers, such as cooperation between internal auditors and other parties like audit committees and external auditors (25 studies, 14.62%), practicing IA (24 studies, 14.03%), the use of technology in IA, and the discussion of the procedures followed in IA and standards (18 studies, 10.54%). The role of IA was discussed in the largest number of studies, reaching (35 studies, 20.47%). In addition, education and IA were addressed in only 4 studies, including one by Calvin and Holt (2023), which aimed to investigate the role that IA education plays in enhancing the efficiency of external auditing and improving the quality of financial reporting. The results showed that companies located near centers for IA education gain many benefits, the most significant of which are reducing audit delays, paying lower audit fees, improving weaknesses in control processes, and reducing financial statement errors.

Finally, it should be emphasized that despite the extensive research on United States organizations, some topics have only been addressed in a few literatures. These topics include the challenges IA may face in a democratic market, the reasons behind IA’s failure in specific organizations, the impact of community culture on IA practices, and how IA responds to environmental changes such as the financial crisis and the COVID-19 pandemic. The findings also highlight a scarcity of literature on contemporary IA-related subjects, such as IT audit, AI, and sustainability. Furthermore, no research has been conducted to address the potential solutions or strategies that could enhance IA’s effectiveness in the face of these challenges. This gap emphasizes the need for future studies to explore these critical areas and provide insights into how IA can adapt and thrive in rapidly changing environments. Future studies could discuss how IA can be developed in light of COVID-19 and the importance of legislation and standards that regulate work amid unexpected crises.

IT Auditing

Academics and practitioners have emphasized the significance of utilizing technology and analytics in the IA (Cao et al., 2015). IT can establish and activate an effective IA system, which aids in safeguarding institutions’ funds (Li et al., 2018). The literature explores the evolution of IT auditing in the United States, its role in strengthening control, and the development of standards that regulate it (Yang & Guan, 2004). IA factors are relevant to IT audits (Abdolmohammadi & Boss, 2010). The impact of technological advancements on the practice of IAFs (Kotb et al., 2014). The results show that IT auditing contributes to IA (Kotb et al., 2014). Four factors related to IT audits in IAFs have been identified: the age of IAFs, training, the number of organizational employees, and the Certified Information Systems Auditor (CISA) system auditor certification. At the same time, Certified Public Accountant (CPA), Certified Internal Auditor (CIA), and Certified Management Accountant (CMA) do not show a positive correlation with the application of IT auditing. Kim et al. (2009) reported a positive impact on the acceptance of IT related to organizational factors, contributing to the anticipated ease of use and perceived benefits of utilizing IT. On the other hand, social factors, such as internalization and image, do not encourage internal auditors to embrace IT. Finally, individual factors reflected in output quality, job relevance, and result demonstration encourage internal auditors to accept IT due to its benefits in ease of use and safety. This literature provides extensive knowledge on the importance of IT auditing and its role in enhancing and improving IAFs. However, it did not adequately address the type of IT to use or specify the skills internal auditors need. Future studies should address this. Table 2, shows the methodology and results of some of the literature that discussed IT and IA.

Sample of Studies on IT Auditing/IA Technology.

Source. Authors’ own work.

Note. ML = multivariate regression; SEM = structural equation modeling; PLS = partial least squares; CAEs = chief audit executives.

IA and Other Parties

The benefits of practicing the IA profession can be effectively realized if there is a constructive and robust relationship between IA and the organization’s management in accordance with regulations, laws and standards (Magdas & Raita, 2022). This section reviews the literature discussing the relationship between IA and other parties, such as external auditing and the audit committee. The literature examines the relationship between IA and the audit committee (Jung & Cho, 2022; Montondon, 1995; Raghunandan et al., 2001; Rezaee & Lander, 1993; Schneider, 2009), as well as between IA and external auditors (Brody et al., 1998; V. Desai et al., 2010; R. Desai et al., 2017; Malaescu & Sutton, 2015; Reinstein et al., 1994). Oversight by audit committees has been found to enhance IA efficiency and effectiveness (Montondon, 1995). In this regard, Magdas (2022) reported that regular dialog between the firm’s audit committee and internal auditors is essential for improving internal communication. The results also indicate that the external auditor’s evaluation of IA is based on several factors, most importantly the efficiency of internal auditors and their objectivity (Messier & Schneider, 1988).

This literature can provide a systematic and specific mechanism to establish robust foundations regulating the relationship between the internal auditors, the external auditors, and the audit committees’ members. It’s important to note that the role of IA differs from that of external audits and audit committees. In their study, Al-Twaijry et al. (2004) indicated that IA differs fundamentally from external auditing, since it evaluates all internal operations and controls in the institution. As opposed to IA, external auditing provides an opinion on the integrity and compliance of financial statements. Specifically, the audit committees are responsible for supervising the internal and external auditing of their tasks in a way that ensures independence and objectivity (Sarens & De Beelde, 2006).

Future studies could examine effects that may cause any of the three parties to indulge in their work. Additionally, future studies could explore the relationship between audit committees and external auditing. Table 3 illustrates some of the literature methods, and results related to this topic.

Sample of Studies on the Relationship Between IA and Other Parties.

Source. Authors’ own work.

Note. OLS = ordinary least square.

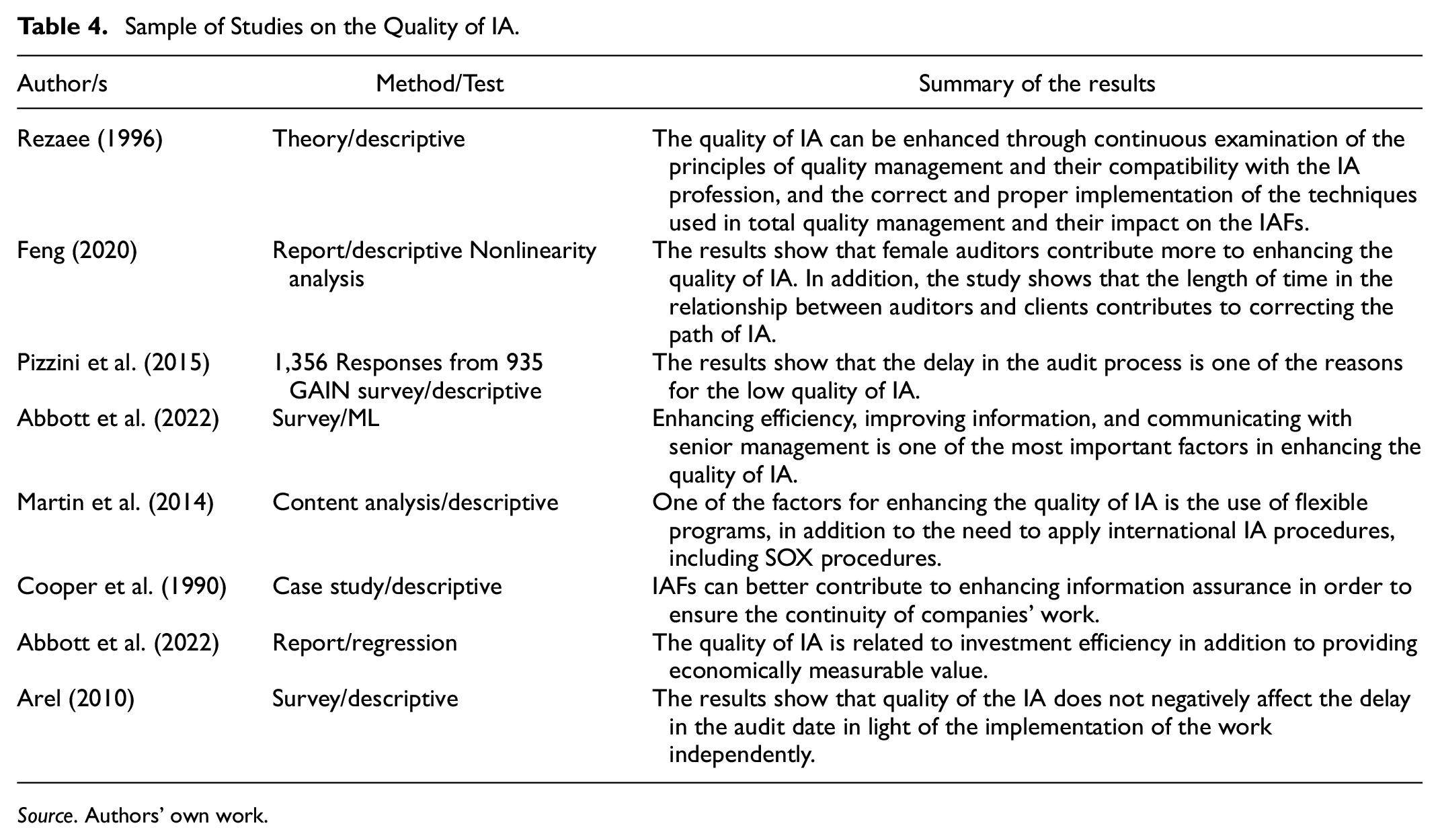

IA Quality

Reforming the mechanisms and practices of auditing is an important issue to enhance the confidence of investors and companies in the auditing profession. Previous studies discussed how to enhance the effectiveness and quality of IA (George-Silviu & Melinda-Timea, 2015). The quality of IA can be improved through a continuous assessment of quality management principles and their alignment with the IA profession is essential (Rezaee, 1996). Compliance with internal corporate controls is important (Lamoreaux, 2016). Customer cooperation, an appropriate budget for IA practices, and consulting auditors for clients are also critical (Aikins, 2013). The independence of the internal auditor is vital (Abbott et al., 2015). Senior management support is necessary (Kaplan & Schultz, 2007). Additionally, a risk management system and ongoing training for auditors are critical (D’Onza et al., 2020). On the other hand, some studies indicate that the quality of IA is influenced by several factors, most importantly, customer pressure and audit fees (Elshafie, 2016). Although this topic has been extensively discussed, several factors have not been examined, such as the impact of politics on IA quality and its effects on the national economy, the significance of implementing AI programs, and their role in improving the quality of IA and risk management. Future studies can address these research gaps. Finally, some studies that have examined the quality of IA are summarized in Table 4.

Sample of Studies on the Quality of IA.

Source. Authors’ own work.

Risk Management and Fraud Detection

Risk management and fraud control are among the most important topics related to IA. The literature explores the connection between IA and risk management, showing that the risks associated with participation do not influence external auditors’ dependence on IAFs (Petherbridge & Messier, 2016). According to Zainal Abidin (2017), IA quality can significantly enhance risk control and establish a more robust and organized system. Conversely, identifying operational and strategic risks is the responsibility of internal auditors, who must adapt IA mechanisms and strategies to effectively mitigate risks (Hazaea, Zhu, Khatib, Bazhair, & Elamer, 2022). This topic has been inadequately addressed. Future studies may address this gap. Additionally, future studies could examine the role of IA in risk management, especially unexpected risks like COVID-19, and outline the appropriate mechanisms IA can implement in accordance with IIA policies and regulations. Table 5 presents the findings of several studies discussing this topic.

Sample of Studies on Risk Management and Fraud Detection.

Source. Authors’ own work.

Future Research Directions

The interest of the community and stakeholders in the IAFs has significantly increased in understanding the correct mechanisms for practising IAFs for several reasons, most importantly the failure of some companies like Enron and the financial crisis that occurred in 2008, in addition to rapid environmental changes such as COVID-19. In light of these variables, interest in conducting research that could contribute to a correct understanding of IAFs has increased. The investigation results indicated an increase in the number of studies discussing IA since 2009, likely due to the 2008 global financial crisis prompting academics and research centers to seek a comprehensive, clear definition that enables IA practice as required. The findings also revealed that the term IA is rapidly developing based on the environmental developments that have taken place, which contributed to changing the IA concept from a means to combat fraud to a method of adding value to companies. Regarding the literature’s theoretical foundation, the results show a significant number of studies are not grounded in specific theories, with only a few studies grounded in traditional theories like agency theory and institutional theory. This represents a major gap in the IA literature, given the importance of theories in clarifying results. In this context, future studies could explore IA through traditional and modern theories, such as stakeholder theory and risk management theory, to provide deeper insights into the role of IA in governance and compliance and expand knowledge and better explain results. Future studies should build on theories contributing to the application of various social, behavioral, philosophical, and economic theories, which may enhance the understanding of IA mechanism practice and explain the various factors that will enhance or influence this profession.

The results indicate that the literature has been published in auditing and accounting specialty journals, indicating its quality and the importance of the results. The results also show that the literature has addressed various IA-related topics, expanding on AI, IT, audit analytics, and sustainability. In addition, Carcello et al. (2005) addressed the factors that motivate American companies to invest in IAFs. The results showed that the total IA budget is influenced by several factors related to the company’s risks, audit characteristics, and the company’s ability to pay for monitoring operations. Conversely, factors related to increasing the IA budget include the company’s size, financial industries, financial leverage, and the relative amount of inventory, services, and facilities.

Future studies could also broaden the data to include regions like China, Europe, or Middle Eastern countries, comparing it to United States data. This would enhance knowledge and understanding differences based on culture, politics, society, and stakeholders’ knowledge of the importance of professions. Based on the results of this review, there is a gap in the literature related to AI, big data analytics, and blockchain technologies used in IA. Therefore, future literature can explore how these technologies can be integrated into IA practice to enhance the accuracy and efficiency of IA operations. Previous literature’s progress and limitations can be identified through the points presented in Tables 6 and 7.

Progress of the Literature.

Source. Authors’ own work.

Limitations and Future Research Directions.

Source. Authors’ own work.

Conclusion

This study aimed to provide a thorough review of IA literature discussed in the United States, with the objective of providing a clear vision of how IA research has developed. It also critiqued the published literature to date while providing a roadmap for future research to help develop and strengthen IAFs. Using SLR to analyze the literature, this study aims to answer five questions.

Regarding Q1, the investigation shows that the increase in IA literature can be linked to the financial crisis that transpired during 2007 to 2008, regulatory requirements, the increase in globalization, and the expansion of trade in various countries, in addition to the failure of some companies such as Enron and WorldCom. Additionally, the requirements of Section 404 of the SOX in the United States created a demand for research on the implementation of IA regulations. Furthermore, stakeholders’ interest in robust regulations and procedures to enhance IA effectiveness motivated academics to research this field. In recent years, companies have engaged in sustainability activities.

Regarding Q2, the results of the investigation showed a wide use of agency theory compared to other theories that were used in a few studies. However, the results showed the need to use theories related to the environment, decision-making, and social and economic theories (see Table 7 for more information on this). Results also indicate a need to support future literature with theories that would enhance results and clearly present problems and solutions.

Concerning Q3, the investigation revealed that interpretive interviews and analytical research are less common than questionnaire-based research. This investigation shows a scarcity of data-driven studies from private and non-profit institutions. Concerning Q4, the results indicated progress in exploring new IA-related topics such as IT, AI and sustainability and clarifying mechanisms for addressing the main risks. Despite this progress, the results showed a limited absence of research discussing other topics, such as AI use in IA and mechanisms of IAF practice during sudden crises like the COVID-19 pandemic. The literature also highlights the emergence of numerous opportunities and challenges for internal auditors from the complex and dynamic regulatory environment, business operation complexity, and significant IT development. The results indicate a need for further research on various topics, contributing to increasing knowledge and a deeper understanding and clearer description of the true meaning of IA, thereby enhancing its vital role in organizations as a key aspect of corporate governance.

However, the results demonstrated topic diversity, despite the absence or scarcity of some topics, such as the relationship between IA and AI, crisis effects on IAF application, and the mechanisms for applying international IA standards during financial crises and emergency environmental changes. Future research could help establish a specific IA practice based on actual implementation, contributing to flexible, emergency-accommodating IA implementation. To answer Q5 we have designed Table 7 specifically to address this question.

The originality and value of this review stem from its systematic and comprehensive approach to assessing the IA literature in the United States, spanning nearly 39 years. The findings not only provide a roadmap for future research but also provide critical insights for professionals aiming to strengthen IAFs in response to evolving environmental challenges such as financial crises, natural disasters like COVID-19, and ESG compliance. The application of SLR, combined with a focus on key regulatory transitions and crises, positions this study as an essential resource for both academic and professional audiences. Therefore, by addressing gaps in the literature, this study contributes to a more complete understanding of the role of IA in risk management, governance, compliance, and performance improvement, ultimately leading to the evolution of the IA profession.

Implications

In addition to what was discussed in the section on future research directions and in Table 7, we present in detail the theoretical, managerial, and practical contributions as follows:

Theoretical Implications

This study can shed light on the extent to which IA practice is affected by regulatory frameworks such as SOX, enhancing our understanding of institutional theory in how external pressures shape regulatory practices. In addition, the study highlights the significance of IA in enhancing governance and reducing agency costs, which supports agency theory and illustrates how IA works to enhance competitive advantage and risk management, thereby reinforcing risk management theories and their resource-based perspective. Thus, this study emphasizes the necessity of employing theories to deepen the understanding of IA research and to ensure the accurate interpretation of results. This study is important for researchers, especially doctoral students because it provides an in-depth, general, and comprehensive view of the current status of IA in one of the most organized and professionally applied countries, which contributes to opening new and rich horizons for future research.

Managerial Implications

This study offers several important managerial implications. It provides a roadmap for researchers and professional organizations that regulate the IA profession, such as IIA, both in the United States and globally. In order to enhance the performance of IAFs in their organizations, managers should focus on IT auditing, environmental and social compliance, governance, and fraud detection. The study highlights that effective IAFs contribute significantly to enhancing governance, compliance, and risk management, especially in the context of SOX. As a result, managers can benefit from this to ensure a greater level of organizational oversight and operational efficiency through enhancing the effectiveness of the IA system.

Practical Implications

This review highlights the role of advanced IA in improving the performance of institutions, as it plays an important role not only in implementing traditional functions but also in enhancing corporate governance and achieving sustainability. Further, this review’s findings suggest that IA practices need to be improved through the use of IT and AI technologies, as well as real-time monitoring of regulatory risks. Furthermore, this review calls for interested organizations, including the IIA, to create frameworks that clarify how these technologies can be applied to IA. This review demonstrates the importance of focusing on the effectiveness of IA and its organizational importance in order to ensure the confidence of stakeholders and enhance its effectiveness. Finally, this review can be utilized in teaching, either on the topic it addresses or in seminars and classes focused on preparing a literature review, serving as an example of how to conduct a SLR.

Limitations

In line with other studies, this review was limited to the literature in the Scopus database only, which limits the potential to utilize other databases such as WoS, ABS, and ABDC. Future research could also include studies from the IIA Research Foundation, which, while not always published in academic journals, has equally valuable information. Additionally, the interpretation of literature results may be subjective and influenced by the knowledge and investigation of the researcher in some instances. Therefore, future studies could broaden the analysis and discussion. This review has created a search string that incorporates strict terms for searching literature titles, keywords, and abstracts. However, these terms may not cover all relevant literature. Therefore, we encourage future research to enhance our search string to include additional pertinent literature. While our study employs the SLR approach based on a manual investigation without relying on any software programs, future studies may benefit from incorporating bibliometric tools such as SciMAT, which can strengthen the results, especially in the analysis of co-citation networks and thematic development.

Footnotes

Acknowledgements

All the authors are grateful to editor, and anonymous reviewers for their helpful comments and suggestions during the review process.

Author Contributions

Saddam A. Hazaea: methodology, visualization, data collection and processing, writing—original draft, writing—review and editing: Chun Cai: supervision, writing—review and editing. Ebrahim Mohammed Al-Matari: data collection and processing, visualization: Mohammed A. Al-Bukhrani: data collection and processing, visualization. H. Gin Chong: writing—review and editing. All authors read and approved the final manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

An Ethics Statements

Not applicable (This article does not contain any studies with human participants or animals performed by any of the authors).

Data Availability Statement

Most of the 171 studies are cited in this paper; the rest are available from the first author upon request.