Abstract

This study investigates the impact of relational engagement and institutional frameworks on the financing performance of infrastructure projects in Indonesia, with a particular focus on the mediating role of innovative financing mechanisms. Data were collected via a survey of 100 key stakeholders in the infrastructure sector and analyzed using Partial Least Squares Structural Equation Modeling (PLS-SEM). The findings indicate that innovative financing significantly enhances financing performance, while robust institutional frameworks positively influence both the adoption of innovative financing and overall financing outcomes. Relational engagement emerges as a crucial factor, directly improving institutional conditions, fostering innovative financing strategies, and ultimately boosting financing performance. The study also uncovers several indirect effects: for example, institutional factors improve financing performance through their positive impact on innovative financing, and relational engagement indirectly enhances financing performance by strengthening institutional frameworks that support innovative financing mechanisms. These results underscore the dynamic interplay among stakeholder relationships, formal institutional structures, and financing innovations. The research provides practical recommendations for policymakers and infrastructure developers – notably, to strengthen stakeholder collaboration and develop effective institutional environments – in order to optimize infrastructure financing strategies and project outcomes.

Plain Language Summary

This study explores how collaboration, institutional structures, and innovative financing influence the financial success of infrastructure projects in Indonesia. Using survey data from 100 stakeholders in the sector, the research shows that innovative financing plays a key role in improving financial outcomes. Strong institutional frameworks also support innovative financing and better financial results. Among all factors, collaboration between stakeholders (relational engagement) has the greatest impact, as it positively influences institutional structures, financing strategies, and overall project success. The study highlights that institutional frameworks and innovative financing work together to improve financial performance. Collaboration among stakeholders indirectly boosts financial outcomes by strengthening institutions and enabling innovative financing solutions. These findings underline the importance of building strong partnerships and effective institutional support to ensure the financial sustainability of infrastructure projects. This research offers practical guidance for policymakers and project developers on creating successful financing strategies through collaboration and robust institutional setups.

Keywords

Introduction

Infrastructure development in Indonesia faces challenges of growing demand and sustainable financing. Conventional mechanisms, such as public budget allocations and bank loans, remain insufficient. Consequently, the government increasingly employs Public–Private Partnerships (PPPs) and innovative instruments – blended finance, green bonds, and impact investing – to mobilize private capital and distribute risk. Regulatory reforms have strengthened transparency and governance. Nonetheless, project success depends on more than capital alone. The quality of stakeholder relationships and institutional frameworks is critical. Grounded in stakeholder theory (Freeman, 1984, 2023), effective stakeholder engagement – characterized by trust and collaboration – is essential for achieving favorable outcomes in PPP infrastructure projects. At the same time, we draw on institutional theory and governance theory to complement the stakeholder perspective. Institutional theory suggests that robust formal institutions (clear regulations, effective governance structures, and supportive norms) create an enabling environment for complex collaborations like PPPs (DiMaggio & Powell, 1983; North, 1990). Governance theory, especially as applied to public–private collaborations, highlights that well-designed governance mechanisms (e.g., fair risk-sharing arrangements, accountability systems, and incentive structures) help align stakeholder behaviors with project goals (Klijn & Teisman, 2005). These theoretical lenses create a comprehensive foundation where stakeholder relationships function in an institutional context and governance mechanisms guide them to influence project financing outcomes.

Despite increasing recognition of these factors, there remains a research gap in understanding how relational engagement and institutional setup work together to influence financing performance, and specifically the role of innovative financing in this nexus. Prior studies have often examined financial innovation in infrastructure in isolation (Arezki et al., 2017; Mostafavi et al., 2014) or focused on stakeholder management qualitatively. Our study aims to provide empirical evidence on the interconnections among these dimensions. Through a survey of key stakeholders in Indonesia’s infrastructure sector, we capture their views on relationships, institutional quality, innovative financing, and project financing outcomes. Indonesia presents an insightful case, as it has pursued aggressive infrastructure development via PPPs in recent years, making it an ideal setting to explore these dynamics.

We propose that: (a) relational engagement among stakeholders and institutional frameworks are both critical determinants of infrastructure financing performance; (b) innovative financing mechanisms (IF) serve as a mediating bridge that can amplify the effects of those determinants – for instance, strong relationships and institutions may facilitate the adoption of innovative financing, which in turn improves performance; and (c) understanding these relationships can yield practical strategies for policymakers.

Hypothesis Development

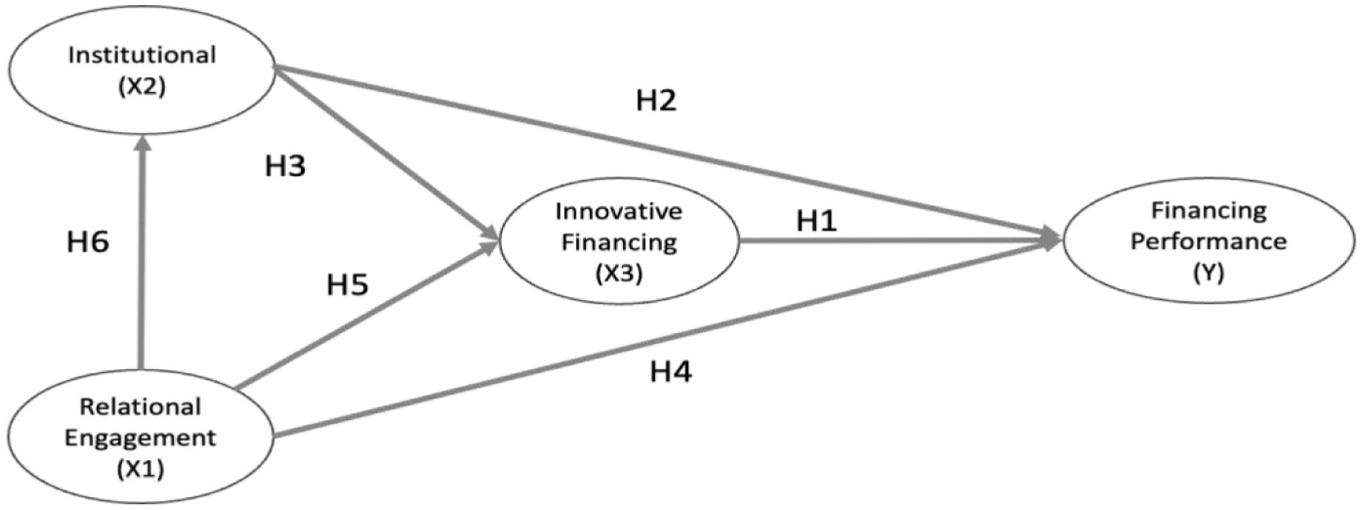

The conceptual model for this study is depicted in Figure 1 (Hypothesized Research Model). In this model, Relational Engagement and Institutional Setup (factors) are positioned as independent variables, Innovative Financing acts as a mediating variable, and Financing Performance is the dependent outcome. The directional arrows illustrate the hypothesized relationships, including direct effects and mediated pathways. Using stakeholder theory and building on institutional and governance perspectives, we develop 11 hypotheses that test direct and indirect relationships.

Hypothesized research model.

Direct effects: how each of the main factors (relational engagement, institutional factors, innovative financing) influences financing performance, and how relational engagement influences institutional factors and innovative financing, and how institutional factors influence innovative financing.

Indirect (mediated) effects: how relational engagement and institutional factors may indirectly affect financing performance through innovative financing or through each other.

Below, we articulate each hypothesis with theoretical rationale and references to existing studies.

Rationale: Innovative financing mechanisms (such as blended finance, green bonds, or impact investing) are designed to mobilize capital from diverse sources and tailor financial structures to project needs. Prior research indicates that projects employing innovative financing often achieve higher success rates and more efficient resource allocation (Mostafavi et al., 2014; Yoshino et al., 2019). They attract a broader pool of investors and can reduce the cost of capital by distributing risk more optimally (Gouldson et al., 2015; Ottinger & Bowie, 2015). For example, a green bond issuance might tap into climate-focused investors at competitive rates, or a blended finance structure might leverage public funds to de-risk private investments, thereby improving overall project viability. From a stakeholder perspective, innovative financing can align the interests of different parties by structuring incentives (e.g., providing guarantees or shared returns) to ensure commitment to project success.

However, it is also important to consider a critical viewpoint: the need for innovative financing could signal constraints in raising conventional funding. Diversifying financial sources might indicate that traditional sources (like bank loans or government budget) were insufficient, which can be a symptom of underlying risk or credit concerns. Moreover, certain innovative instruments come with trade-offs – for instance, green bonds can entail additional reporting requirements and potentially higher transaction costs, and they may not always yield lower interest rates than regular bonds (fixedincome.com, 2024). These nuances suggest that while innovative financing is generally expected to improve performance by injecting capital and reducing costs, its net benefit must be weighed against any extra complexity or signals of risk it carries. On balance, drawing from both practical evidence and stakeholder theory (which highlights collaborative financial problem-solving), we hypothesize a positive effect: if a project employs innovative financing approaches, it will likely achieve better financing performance (e.g., lower effective costs, more timely financial closure, and greater financial sustainability).

Rationale: Institutional factors refer to the strength and quality of the formal frameworks governing infrastructure projects – including regulatory systems, governance structures, legal norms, and the capacity of institutions to enforce rules. Strong institutions reduce uncertainty for investors, enhance confidence, and provide clear guidelines for project implementation. In PPP projects, for instance, well-defined regulations and a competent PPP unit can streamline approvals and reduce uncertainty. Studies show that effective governance (e.g., anti-corruption measures, rule of law) and regulatory support correlate with improved infrastructure financing outcomes by creating a stable investment environment. For example, Wibowo and Alfen (2015) found that in countries with strong PPP regulations, projects had lower cost overruns and faster financial closure. Institutional theory suggests that when the “rules of the game” are clear and fair, stakeholders are more willing to commit resources, which improves project performance. In Indonesia’s case, initiatives like the establishment of the Indonesia Infrastructure Guarantee Fund and specialized PPP units signal an institutional commitment that can attract investors by reducing political and contractual risks. Therefore, we expect that strong institutional factors (effective governance, clear policies, capable agencies) will directly lead to better financing performance – manifesting in outcomes such as reduced financing costs, timely project completion within budget, or successful mobilization of funds. This hypothesis aligns with governance theory: projects embedded in sound institutional environments tend to have more favorable financial results.

Rationale: We posit that a supportive institutional framework is a key enabler for innovative financing solutions. Strong institutions (rules and regulations) create the conditions for financial innovation by providing legitimacy and reducing risks associated with new financing instruments. For instance, when regulations allow for and encourage instruments like municipal bonds or public asset recycling, innovative financing can flourish. Conversely, bureaucratic hurdles or unclear laws can stifle financial innovation. Prior evidence suggests that countries or sectors with well-established PPP laws and financial regulations see more frequent use of novel financing mechanisms (Dappe et al., 2022; Prayuda et al., 2023). Supportive regulations and specialized government agencies (e.g., a PPP commission or infrastructure fund) can streamline processes, reduce transaction costs, and foster public–private collaboration in financing. Institutional theory also implies that organizations (or projects) will adopt innovative practices when the institutional environment supports them (Scott, 2014). In our context, this means effective institutional factors – such as clear guidelines for blended finance, government incentives for issuing project bonds, or availability of guarantees – will positively influence the adoption and successful implementation of innovative financing in projects. We expect a direct positive relationship: better institutions lead to more innovative financing usage.

Rationale: Relational engagement captures the degree of trust, collaboration, and effective communication among project stakeholders (public agencies, private investors, lenders, etc.). According to stakeholder theory, when stakeholders are actively engaged and maintain good relationships, projects benefit from smoother coordination, knowledge sharing, and conflict resolution (Clarkson, 1995; Freeman, 1984). Empirical studies corroborate that strong stakeholder relationships contribute to better project execution and outcomes (Jayasuriya et al., 2024; Tian et al., 2023; Warsen, 2023). In PPP infrastructure projects, relational engagement might involve regular multi-party meetings, transparent information exchange, and mechanisms for joint decision-making. These practices ensure that all parties have a shared understanding of project goals and can address issues proactively, thereby avoiding costly delays or disputes. For instance, if the public and private partners trust each other, they are more likely to resolve unforeseen issues (like minor cost overruns or design changes) amicably rather than resorting to legal action, saving time and money. Additionally, relational engagement can garner public support (through community outreach and involvement), which can be crucial for preventing project stoppages due to social opposition. Thus, we hypothesize that higher relational engagement leads to improved financing performance. “Improved performance” here can mean projects stay closer to budget, secure necessary funding more easily, and achieve financial close faster – all as a result of cohesive stakeholder alignment. This hypothesis essentially reflects the idea that relationships matter financially: projects with collaborative partners will likely incur fewer financing risks and extra costs, directly benefiting the bottom line.

Rationale: We expect that strong stakeholder relationships will promote the use of innovative financing mechanisms. Prior research indicates that relational engagement can foster creativity and flexibility in problem-solving (Aben et al., 2021), which extends to financial solutions. For example, a government agency that has a good working relationship with investors might be more open to structuring a blended finance deal or issuing a revenue bond, as there is mutual confidence in each party’s commitments. Trustful relationships also make negotiations of complex financial terms smoother – stakeholders are more likely to agree on innovative contract terms (like performance-based payments or guarantees) if a strong rapport exists (Nederhand & Klijn, 2019). In essence, relational engagement creates an environment conducive to financial innovation: stakeholders share information about new financing opportunities, align their interests (perhaps through memoranda of understanding or informal agreements), and exhibit flexibility to try unorthodox approaches to funding. Hence, we hypothesize a direct positive link: if stakeholders are highly engaged and collaborative, a project is more likely to implement innovative financing strategies (as opposed to defaulting to purely traditional finance).

Rationale: This hypothesis considers that stakeholder relationships can also shape and strengthen the institutional frameworks governing a project. In PPPs, effective relational engagement might translate into stakeholders collectively advocating for or developing better institutional arrangements. Prior studies suggest that strong collaboration among stakeholders can lead to improved governance practices and more responsive institutions (Liu et al., 2023; Nederhand & Klijn, 2019; Trebilcock & Rosenstock, 2015). Here, we align with governance theory: relational engagement can be seen as a form of relational governance that complements formal contracts. Trust and communication enable stakeholders to fill gaps in formal institutional structures by creating informal norms and joint solutions. Over time, these can solidify into institutional improvements. Additionally, a united front of stakeholders (e.g., private investors and government bodies together) can have greater influence in pushing for institutional support, such as regulatory adjustments or dedicated resources for the project. Therefore, we hypothesize that relational engagement positively influences the quality/effectiveness of institutional factors. In practical terms, a project with strong stakeholder engagement might experience more effective institutional support – for example, a more coordinated inter-agency effort, streamlined permitting processes, or improved oversight – compared to a project where stakeholders are siloed or in conflict.

Having stated the direct relationships (H1–H6), we also propose a series of mediated relationships where Innovative Financing (IF) acts as a mediator. These hypotheses examine whether relational engagement or institutional factors can improve financing performance indirectly by enabling innovative financing.

Rationale: This hypothesis posits an indirect pathway: strong institutional factors → greater adoption of innovative financing → improved financing performance. Even if institutional factors (like policies) have some direct effect on performance (as per H2), their impact could be amplified via innovative financing. Strong institutions may facilitate innovative financial arrangements (as argued in H3); once these arrangements are in place, they can lead to better performance outcomes (H1). Thus, innovative financing acts as a channel through which institutions exert influence on final outcomes. Previous studies support this mediated view – for example, Arezki et al. (2017) and Wang et al. (2018) indicate that countries with supportive institutions only realized improved infrastructure performance when they also implemented novel financing schemes to leverage those institutions. We expect that in our model, the data will show that the effect of institutional setup on financing success is partly (or fully) carried by innovative financing mechanisms. In other words, good institutions help projects adopt innovative financing, which in turn drives high performance. Formally, Institutional Factors → Innovative Financing → Financing Performance is the mediating sequence to be tested.

Rationale: This hypothesis examines whether institutional factors mediate the effect of relational engagement on performance. Relational engagement might lead to better financing results because it first improves the institutional context of the project. As per H6, engaged stakeholders can strengthen institutional arrangements. Improved institutional frameworks (clearer rules, better governance) would then lead to better financing performance (H2). Thus, relational engagement could indirectly boost performance by way of creating a more enabling institutional environment. Wibowo and Alfen (2015) provide evidence that PPP projects with strong public-private relationships also benefited from adaptive institutional arrangements, which ultimately contributed to project success. Trebilcock and Rosenstock (2015) similarly argue that collaborative stakeholder relationships can drive reforms or arrangements that improve project governance. Therefore, we hypothesize an indirect effect: Relational Engagement → Institutional Factors → Financing Performance. If supported, this would suggest that one reason projects with high stakeholder engagement perform well is that those stakeholders help establish better institutional conditions (like improved oversight or aligned regulations), which in turn yield superior financing outcomes.

Rationale: This is a dual-mediation hypothesis where relational engagement’s effect on performance runs through both institutional factors and innovative financing in sequence. Under this scenario, we propose: engaged stakeholders improve institutional factors (as per H6); strong institutional factors facilitate innovative financing (H3); and innovative financing enhances performance (H1). This chain would mean relational engagement indirectly leads to better performance by first influencing institutions and then enabling financial innovation. Such a complex pathway recognizes that transformational improvements in outcomes might require both improved governance and novel funding approaches. Some scholars have hinted at this synergy: Myagkova et al. (2022) and Solheim-Kile et al. (2019) note that collaborative stakeholder environments paired with supportive institutions are conducive to implementing new financing solutions, which together yield sustainable project benefits. We thus hypothesize Relational Engagement → Institutional Factors → Innovative Financing → Financing Performance as a significant mediated pathway. Supporting this would highlight the interconnected nature of all four constructs, showing that relational and institutional improvements together set the stage for leveraging innovative finance to achieve high performance.

Rationale: This hypothesis considers innovative financing as a mediator between relational engagement and performance. Even if relational engagement has a direct benefit (H4), part of its effect may occur because engaged stakeholders are more likely to adopt innovative financing (H5), which then results in better performance (H1). For example, when stakeholders trust each other, they might collectively decide to use a creative financing approach (like an infrastructure investment trust or a public bond issuance) that they would not attempt in a low-trust scenario. Once implemented, that financing method improves project funding and outcomes. This mediating idea finds support in practical observations: Delphine et al. (2019) and Erkul et al. (2020) observed that stakeholder engagement mechanisms – such as public forums and joint committees – often lead to identification of innovative funding opportunities which then enhance project delivery. Additionally, stakeholder engagement can help overcome hurdles in executing new financing (e.g., by rallying political support or community buy-in for a bond measure). Hence, we hypothesize Relational Engagement → Innovative Financing → Financing Performance as a significant indirect effect. If confirmed, it would imply that a key reason stakeholder engagement boosts performance is that it unlocks the use of better financing techniques.

Rationale: Finally, we hypothesize that relational engagement might indirectly affect the adoption of innovative financing via institutional factors. In other words, Relational Engagement → Institutional Factors → Innovative Financing. This acknowledges that while H5 posits a direct effect of relationships on financing innovation, there could also be an indirect route: engaged stakeholders first work to improve or navigate the institutional setting (H6), and a strengthened institutional framework then directly supports innovative financing (H3). For instance, in a project with high stakeholder engagement, stakeholders might collectively push for a special regulatory approval or an institutional arrangement (like a government guarantee or the creation of a project finance vehicle) that then makes an innovative financing possible. Badu et al. (2013) and Gazley (2013) provide evidence that collaborative stakeholder actions can lead to changes in institutional or policy support which, in turn, enable new forms of financing or partnership structures. Thus, we include H11 to test this subtler mediation: that relational engagement could facilitate innovative financing primarily by shaping institutional conditions in its favor.

Methodology

Questionnaire Design and Distribution

To empirically examine the hypotheses, we conducted a structured survey targeting professionals involved in Indonesian PPP infrastructure projects. All survey constructs were drawn from previously validated instruments in prior studies and adapted to the Indonesian PPP context. Adaptation involved minor rephrasing of items to align with local terminology and project conditions. For example, to measure Relational Engagement (REG), we included items reflecting trust and communication, such as “There is a high level of trust among the public and private stakeholders involved in the project” and “Stakeholders openly share information and support each other’s goals.” These items were informed by sources like Amadi et al. (2018) and Edquist (2001), with wording adjusted to explicitly refer to PPP project stakeholders in Indonesia. For Institutional Factors (IST), we adapted items capturing governance effectiveness and transparency (e.g., “The regulatory framework for this project is clear and effective,”“Decision-making processes are transparent and free of undue bureaucracy”), drawing on Wibowo and Alfen (2015) and Suhadi (2018). Innovative Financing (IFG) was measured with items based on definitions of financial innovation in infrastructure (Mostafavi et al., 2014; Tufano, 2003) – for instance, “The project utilizes an innovative financing mechanism (such as blended finance, special bonds, etc.) as a major source of funding” and “The financing approach for this project is more innovative than those traditionally used in similar projects.” Financing Performance (FPE) was assessed using perception-based indicators covering three dimensions referenced by Mostafavi et al. (2014) and Mostafavi and Abraham (2010): (a) process efficiency, (b) cost effectiveness, and (c) development outcomes. Example FPE items included “The financing arrangement has minimized the project’s financing costs compared to conventional methods” and “The project’s financing is contributing positively to broader economic outcomes (e.g., growth, productivity).” These items were rated by respondents based on their agreement on a 1–5 Likert scale (1 = Strongly Disagree, 5 = Strongly Agree).

Table 1 summarizes the constructs along with example measurement items used in the questionnaire. Each survey item was rated on a five-point Likert scale, where 1 = “Strongly Disagree” and 5 = “Strongly Agree.”

Constructs and Example Measurement Items.

Note. All items were rated on a 1–5 Likert scale: 1 = strongly disagree, 5 = strongly agree. Table presents a subset of items for illustration.

Before the main survey, we conducted a pilot test with five infrastructure finance and academic experts at the Indonesia Infrastructure Guarantee Fund (IIGF). Their feedback improved item clarity and cultural relevance, confirming face validity for the Indonesian PPP context. The survey began with an informed consent statement explaining the study’s purpose, assuring anonymity, and confirming voluntary participation; consent was indicated by proceeding. Ethics approval was obtained from the Ethical Committee on Social Studies and Humanities at the National Research and Innovation Agency of the Republic of Indonesia (Ethical Clearance No. 062/KE.01/SK/02/2025). The questionnaire was distributed via email and a secure online platform using purposive sampling (see Section Respondent Profiles and Sampling). Data collection spanned 6 weeks with follow-up reminders. Responses were completed individually and recorded securely. To reduce common method bias, we mixed the order of questions from different constructs and assured respondents that there were no right or wrong answers. Post-hoc statistical checks (Section Measurement Model Results) confirmed that single-source data did not unduly inflate correlations. Nonetheless, reliance on self-reported perceptual measures introduces a risk of response bias (e.g., social desirability). We sought to mitigate this through the anonymous survey design and statistical controls; a Harman’s single-factor test indicated no dominant factor (largest explained variance ∼34% < 50% threshold; Podsakoff et al., 2003), suggesting common method bias is not a serious concern.

Respondent Profiles and Sampling

The study targeted Indonesian PPP infrastructure stakeholders, including government officials, private investors, financial institution professionals, academics, and consultants with over 5 years’ experience and involvement in major PPP projects. Using purposive sampling, we selected participants based on their expertise and decision-making roles across planning, financing, and implementation stages, ensuring respondents were highly relevant to the research objectives and reflective of the sector’s specialized nature.

A total of 100 respondents completed the survey. This sample size was determined both by the available pool of experts and methodological considerations. The population of qualified PPP stakeholders in Indonesia is relatively limited – while the exact population is not formally defined, it likely numbers only a few 100 individuals at most (given PPP projects are a niche area). Therefore, 100 respondents represent a considerable portion of this expert community. In terms of PLS-SEM requirements, a sample of 100 is adequate; it exceeds the common “10-times rule” (which in our model would suggest a minimum of ∼50, based on the largest number of indicators in a construct) and benefits from the fact that PLS-SEM can handle small-to-medium samples efficiently (Hair et al., 2022).

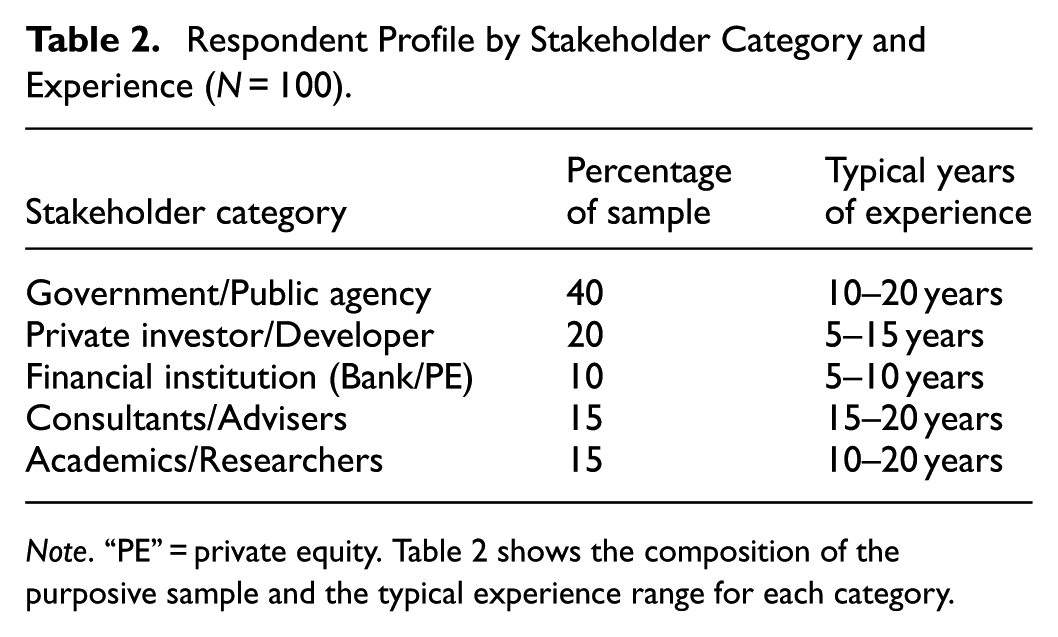

The demographic profile of respondents is summarized in Table 2. The average experience of respondents in the infrastructure sector was notably high: government officials typically had 10 to 20 years, financial industry professionals 5 to 10 years, and academics/consultants around 15 to 20 years. This indicates that respondents were seasoned professionals, lending credibility to their survey responses and insights. Most respondents (around 60%) had been involved in more than three PPP projects, suggesting familiarity with a variety of project experiences. Approximately 40% were from public sector agencies, 30% from private investors or financial institutions, and the remainder from consultants and academia, which provided a balanced perspective across stakeholder groups.

Respondent Profile by Stakeholder Category and Experience (N = 100).

Note. “PE” = private equity. Table 2 shows the composition of the purposive sample and the typical experience range for each category.

This purposive expert sampling approach ensured that respondents could provide informed evaluations of PPP financing dynamics. However, it carries implications for generalizability (as discussed later in Limitations). Within Indonesia’s PPP context, the sample is deemed highly relevant and reasonably comprehensive in covering the main actors of interest.

Data Analysis Procedures

We used Partial Least Squares Structural Equation Modeling (PLS-SEM) with SmartPLS 4 software to analyze the data. PLS-SEM was chosen due to its suitability for predictive models and smaller samples, as well as its ability to handle complex models with both direct and indirect relationships. The analysis proceeded in two stages: (a) assessment of the measurement model and (b) assessment of the structural model (hypothesis testing).

Measurement model evaluation involved checking indicator loadings, internal consistency (Cronbach’s alpha and composite reliability), convergent validity (average variance extracted, AVE), and discriminant validity (Fornell–Larcker criterion and cross-loadings). All constructs were modeled as reflective latent variables. Where necessary, we dropped survey items with low loadings (below 0.6) to improve construct reliability, although in this study most items exceeded the threshold. Cronbach’s alpha and composite reliability values above .7 for each construct indicated satisfactory internal consistency. AVE values were above 0.50, supporting convergent validity. Discriminant validity was confirmed as each construct’s square-root of AVE was greater than its correlations with other constructs, and no cross-loading exceeded the intended item’s loading. We also assessed common method bias using a full collinearity approach (Kock, 2015) – all variance inflation factors (VIFs) were below 3.3, further suggesting that common method variance was not a critical issue in our data (this complements the earlier Harman test result).

Structural model evaluation focused on path coefficients (β estimates) and their significance via bootstrapping (5,000 resamples), R2 values for endogenous constructs, effect sizes (f2), and model fit indices. We report one-tailed p-values for hypothesized directional relationships. The significance level was set at 0.05 (with p < .001, p < .01, and p < .05 noted where applicable). We also computed indirect effects for mediation hypotheses and used variance accounted for (VAF) to gauge the proportion of total effect mediated. Additionally, we examined predictive relevance (Q2) using the blindfolding procedure, and found Q2 > 0 for key constructs, indicating the model has acceptable predictive relevance for the sample. Goodness-of-fit measures such as SRMR (standardized root mean residual) were considered, with our final model’s SRMR around 0.07, below the suggested cutoff of 0.08 for PLS-SEM, implying a good model fit (Hair et al., 2022).

Results

Measurement Model Results

All constructs in the model demonstrated adequate reliability and validity. Composite reliability scores ranged from 0.84 to 0.92 for the four latent variables, exceeding the 0.70 threshold. Cronbach’s alpha values were similarly high (all > .80), indicating strong internal consistency. The AVE for each construct was above 0.60 (REG = 0.64, IST = 0.58, IFG = 0.69, FPE = 0.63), meeting the convergent validity criterion (AVE > 0.50). Although the AVE for Institutional Factors was 0.58, slightly below 0.60, it is still above the minimum threshold and considered acceptable given strong composite reliability.

Discriminant validity was confirmed via the Fornell–Larcker criterion: each construct’s AVE square root was greater than its correlations with other constructs. For example, the correlation between Relational Engagement (REG) and Institutional Factors (IST) was high (r ≈ .68) but still lower than the square roots of AVE for REG (0.80) and IST (0.76). No inter-construct correlation exceeded 0.80, further alleviating multicollinearity concerns. Additionally, cross-loading checks showed that each survey item loaded highest on its intended construct relative to others. These results suggest that the measurement model is sound, providing a solid foundation for examining the structural relationships.

Descriptive statistics indicated generally positive perceptions: the mean scores for REG, IST, and FPE were around 4.0 on the five-point scale, suggesting that on average, stakeholders felt their projects had good relationships and strong institutional support, and they perceived financing performance to be above moderate levels. The mean for IFG (3.45) indicates a moderate presence of innovative finance mechanisms across projects – not universally high, which is expected as some projects still rely on traditional financing approaches.

The correlation matrix (all bivariate correlations significant at p < .01) provided initial insight into relationships: REG–IST (r = .682), REG–IFG (0.725), REG–FPE (0.639); IST–IFG (0.611), IST–FPE (0.556); IFG–FPE (0.784). These strong associations – particularly between innovative financing and performance, and between relational engagement and the other factors – hint at the potential for significant direct and mediated effects. However, correlation alone does not establish causality or the presence of mediation, so we proceed to the structural model for hypothesis testing.

Structural Model Results (Direct Effects)

The hypothesis tests for direct effects (H1–H6) are summarized in Table 3. All direct paths were positive and significant. We highlight key findings below:

Hypothesis Testing Results – Direct Effects (H1–H6).

Note. All hypotheses H1–H6 are supported at p < .05 or better. Coefficients are standardized; t-values and p-values derived from 5,000-sample bootstrapping.

Innovative Financing → Financing Performance (H1): Path coefficient β = .449, t = 5.87, p < .001. This confirms that greater use of innovative financing is associated with significantly better financing performance. In practical terms, projects that integrated mechanisms like blended finance, special bonds, or other non-traditional funding reported higher satisfaction with financing outcomes (e.g., cost savings, sufficient funding) compared to those relying purely on conventional finance. This strong effect (an almost “large” effect size by Cohen’s f2 standards) underscores the value of financial innovation: it appears to translate into real performance gains in our sample of PPP projects.

Institutional Factors → Financing Performance (H2): β = .210, t = 2.05, p = .041. There is a positive direct influence of institutional quality on performance, albeit smaller in magnitude. This suggests that, even when controlling for other factors, a well-functioning institutional environment (clear regulations, effective governance, competent agencies) can directly contribute to better project financial outcomes. While this effect is weaker than that of innovative financing, it is still important – implying that efforts to strengthen institutions (e.g., policy reforms, improving inter-agency coordination) will pay off in terms of project performance.

Institutional Factors → Innovative Financing (H3): β = .392, t = 4.52, p < .001. Strong institutional frameworks significantly encourage the adoption of innovative financing. This aligns with our theory that clear policies, support mechanisms, and stable governance give stakeholders the confidence and ability to utilize novel financing instruments. For example, respondents in contexts with well-defined PPP regulations and reliable government support were more likely to report using innovative funding structures. This relationship highlights that improving institutional quality can have the added benefit of enabling more creative financial solutions.

Relational Engagement → Financing Performance (H4): β = .327, t = 3.98, p < .001. Greater stakeholder engagement (trust, collaboration) is directly associated with better financing performance. Projects where stakeholders work well together tend to have more favorable financing outcomes – likely due to more efficient implementation and joint problem-solving that reduce delays and unexpected costs. This finding resonates with stakeholder theory arguments and prior studies emphasizing the tangible benefits of good relationships (e.g., fewer disputes or renegotiations that could financially strain a project).

Relational Engagement → Innovative Financing (H5): β = .581, t = 6.71, p < .001. This is one of the strongest paths in the model. It shows that high relational engagement substantially increases the likelihood and extent of using innovative financing. Stakeholders who communicate frequently and trust each other evidently can coordinate on implementing creative financial solutions more effectively. The path coefficient of ∼.58 suggests that improving relational engagement by one standard deviation (roughly moving from “agree” to “strongly agree” on trust/communication items) corresponds to about a 0.58 standard deviation increase in the project’s use of innovative financing – a sizable jump, indicating a very practical impact of stakeholder dynamics on financing strategy.

Relational Engagement → Institutional Factors (H6): β = .682, t = 8.33, p < .001. This is the largest direct effect observed, underscoring that stakeholder engagement is a powerful predictor of the perceived strength/effectiveness of institutional support in a project. In contexts where stakeholders are highly engaged, respondents also rated the institutional environment as much more supportive. This could reflect that engaged stakeholders proactively work with or within institutions to make them function better for the project. It might also reflect some perceptual bias (i.e., good relationships coloring perceptions of institutions positively), but given the robust result and consistency with qualitative evidence, it likely represents real improvements in institutional coordination fostered by relational dynamics.

To sum up the direct effects: all the hypothesized pairwise relationships in our model do exist and are positive. The results give us confidence in stating that innovative financing, institutional quality, and stakeholder engagement each contribute to better financing performance, with innovative financing and stakeholder engagement showing particularly strong impacts. Additionally, stakeholder engagement strongly enhances institutional frameworks and the use of innovative financing, and good institutions also facilitate innovative finance adoption.

We also calculated total effects (the sum of direct and indirect effects) for a broader perspective. For example, the total effect of Relational Engagement on Financing Performance was approximately 0.327 (direct) + (various indirect components summing to ∼0.555) ≈ 0.882. This exceptionally high total effect means that improving relational engagement has a profound overall impact on performance, channeled through multiple routes (some direct, much of it indirect via institutions and financing). Similarly, Institutional Factors’ total effect on Performance is the direct 0.210 + indirect via IFG (∼0.196) ≈ 0.406. Innovative Financing’s total effect on Performance is essentially its direct 0.449 (since its indirect effect on itself in mediated chains is not applicable beyond the direct path). These totals reinforce that Relational Engagement is arguably the most influential single factor when considering how it cascades through the system, followed by Innovative Financing, then Institutional Factors.

Structural Model Results (Indirect Effects and Mediation)

As shown in Table 4, all hypothesized mediation pathways (H7–H11) were statistically significant. We interpret each mediated effect below:

Hypothesis Testing Results – Indirect Effects (H7–H11).

Note. Indirect effect significance determined via bootstrapping. “InnovFin” = Innovative Financing. All mediated hypotheses H7–H11 are supported. Mediation is considered partial if a direct effect also exists alongside the indirect path.

H7 (IST → IFG → FPE): Indirect effect β ≈ .196 (product of IST → IFG and IFG → FPE paths), p < .001, supporting the mediation hypothesis that innovative financing transmits the effect of institutional factors onto performance. This partial mediation implies that part of the reason institutions improve performance is because they enable innovative financing. In practical terms, if Indonesia strengthens its institutions (e.g., streamlining regulations, improving governance), one benefit is that more innovative financing deals can occur, which then lead to better project outcomes. We still observed a direct IST → FPE effect (H2), so the mediation is partial (institutions have some direct influence too, perhaps through things like reducing perceived risk or improving credibility). We computed the variance accounted for (VAF) by this mediation: (indirect 0.196)/(total ∼0.406) ≈ 48%. Thus, nearly half of the influence of institutional factors on performance runs through innovative financing – a noteworthy proportion highlighting IFG’s role as a conduit for institutional impact.

H8 (REG → IST → FPE): Indirect effect β ≈ .132, p < .01. This confirms that Institutional Factors mediate part of the effect of Relational Engagement on Performance. In other words, engaged stakeholders improve financing outcomes in part because they first improve the institutional environment, which then boosts performance. The mediation here is partial, as Relational Engagement also had a direct effect on performance (H4). Nonetheless, this pathway underscores that one mechanism by which stakeholder engagement translates to better outcomes is through shaping stronger institutions or governance during project implementation.

H9 (REG → IST → IFG → FPE): Dual indirect effect β ≈ .155 (estimate derived from REG → IST, IST → IFG, and IFG → FPE product), p < .01. This supports the complex dual-mediation chain: Relational Engagement influences Institutional Factors, which enables Innovative Financing, which in turn enhances Performance. While this particular mediated effect size may appear modest, it is important theoretically – it demonstrates that all three factors in tandem can create a compounded pathway to success. Practically, this implies that high stakeholder engagement can set in motion improvements in institutional support and financial innovation that together yield better performance, highlighting a synergy in which the presence of both strong institutions and innovation is needed to fully capitalize on strong stakeholder relations.

H10 (REG → IFG → FPE): Indirect effect β ≈ .261, p < .001. This indicates that innovative financing mediates a significant portion of the effect of Relational Engagement on Performance. Even though stakeholder engagement alone helps performance (direct H4), a substantial part of its benefit comes from the fact that engaged stakeholders are more likely to implement innovative financing, which then drives improved outcomes. The magnitude of this indirect effect (0.261) is notable – it suggests that if stakeholders work well together, a good share of the performance gains occur because those relationships enable the adoption of better financing methods (e.g., new funding sources, risk-sharing financial structures) that directly impact the project’s financial success.

H11 (REG → IST → IFG): Indirect effect β ≈ .267, p < .001. This confirms that relational engagement also strongly influences the uptake of innovative financing through the institutional channel. In simpler terms, stakeholders who are highly engaged tend to improve the institutional conditions (policies, support mechanisms) of a project, which then makes innovative financing possible or easier to implement. This was a “mediation of a mediation” scenario complementing the direct REG → IFG path (H5). The significance of H11 suggests that some of the relationship between stakeholder engagement and financial innovation is indirect, operating by first reforming or leveraging institutions. It highlights the layered nature of how people and processes interact: good relationships can shape better rules and support, which then enable new financial solutions.

Overall, the structural model results paint a consistent picture: relational engagement and institutional setup work together, largely through innovative financing, to drive superior financing performance. In the next section, we discuss these findings in light of the theoretical frameworks and practical context, and reflect on their implications and limitations.

Discussion

This study examines the interplay among relational engagement, institutional factors, innovative financing, and financing performance in Indonesian infrastructure PPPs. Drawing on stakeholder theory, institutional theory, and governance perspectives, we argue that strong stakeholder relationships and robust institutions enhance financing outcomes via innovative mechanisms. The empirical results (Section 4) support this integrated framework. Below, we discuss the findings in detail, relate them to existing theory, and consider broader implications. We also note the contextual particularities of Indonesia’s PPP landscape and how they might influence the generalizability of our insights.

The Pivotal Role of Innovative Financing

One of the clearest outcomes of our analysis is that innovative financing (IFG) significantly enhances financing performance. The path coefficient of .449 (p < .001) for IFG → FPE (H1) underscores that projects employing innovative financing approaches tend to achieve better financial outcomes. This aligns with prior assertions in the literature that innovative financing can “attract a wider pool of investors and increase overall capital availability,” thus improving the likelihood of meeting funding needs on favorable terms. Innovative financing strategies – such as blended finance arrangements, the issuance of infrastructure bonds, or public guarantee schemes – often reduce the cost of capital or fill financing gaps that traditional sources leave open. Our findings provide empirical backing to those arguments, with stakeholders reporting tangible performance benefits when such mechanisms were in use.

However, our study also adds nuance to the narrative around innovative financing. We acknowledge that diversification of financial sources through innovation can signal underlying challenges. For instance, if a project resorts to multiple unconventional funding streams, it might indicate that standard funding (like bank loans) was not readily obtainable – possibly due to perceived risks. Mobilizing various capital sources may reflect difficulty in raising sufficient capital through conventional means, a cautionary perspective seldom highlighted in enthusiastic discussions of financial innovation. Moreover, we noted that green bonds, while innovative and beneficial for sustainability goals, have potential disadvantages such as higher issuance costs and rigorous reporting requirements (fixedincome.com, 2024). These drawbacks can make green bonds less financially attractive than plain-vanilla bonds in certain cases (e.g., if the “greenium” or interest rate advantage is small). Incorporating these points allows our study to move beyond the simplistic view that “innovation is always beneficial.” We argue that innovative financing is powerful but must be applied with careful attention to context and trade-offs.

For instance, if an innovative instrument like a revenue bond is used because commercial banks found the project too risky, stakeholders should acknowledge that underlying risk and perhaps seek additional risk mitigation (such as guarantees or credit enhancements) to truly realize performance gains. Our finding that IFG is strongly beneficial likely reflects cases where innovative financing was indeed used appropriately, complementing strong stakeholder and institutional support. In less favorable scenarios (e.g., if financial innovation is attempted in a vacuum without stakeholder buy-in or institutional backing), the performance impact might be neutral or even negative – an area future research could explore in more depth.

From a practical standpoint, this result encourages policymakers and project developers to embrace financial innovation, especially in infrastructure sectors that have historically relied on government funding. The Indonesian government’s push toward PPPs and instruments like viability gap funding and guarantee schemes is vindicated by our findings – these are forms of innovation that, when implemented in the right conditions, correlate with success. Our study thus supports ongoing global trends such as blended finance initiatives, infrastructure investment trusts, and project bond markets as effective means to improve infrastructure financing outcomes (OECD, 2014). However, we also caution practitioners to ensure these instruments are accompanied by transparency and capacity-building, to mitigate any potential downsides.

Institutional Frameworks: Foundation for Success

The results confirm that institutional factors (IST) positively affect both financing performance and the uptake of innovative financing (supporting H2 and H3). A robust institutional setup – encompassing clear regulations, effective governance, and competent agencies – directly improved performance (β ≈ .21) and had an even stronger effect on enabling innovative financing (β ≈ .39). This aligns with the literature finding that effective governance reduces uncertainty and transaction costs, thus fostering better project outcomes. For example, when procurement processes are transparent and legal enforcement is credible, investors will demand a lower risk premium, thereby lowering project financing costs (Yescombe & Farquharson, 2018). Likewise, supportive institutions (like a dedicated PPP unit or legal provisions for special financing vehicles) create avenues for innovation by making it easier to deploy new financing structures.

Our findings echo global observations: countries with mature PPP laws and institutions (such as the UK or Canada) have achieved more consistent PPP project performance (reflecting H2), and they more frequently employ innovative financing modalities (reflecting H3). In Indonesia, ongoing improvements – like the establishment of the Indonesia Infrastructure Guarantee Fund (IIGF) and revisions to PPP regulations – are reflected in our respondents’ positive assessments of institutional factors. The significant link from IST to IFG empirically validates policy efforts that focus on institutional readiness as a precursor to financial innovation. Essentially, good institutions are the “soil” in which innovative financing seeds can grow.

That said, our discussion of institutional effects must also recognize context. Indonesia’s institutional environment, while improving, still faces challenges such as bureaucratic red tape, decentralization issues, and policy uncertainties (Prayuda et al., 2023). The moderate effect size we found for IST → FPE (f2∼0.15) indicates that institutions matter, but by themselves may not guarantee success if other factors lag. For example, a project in Indonesia with an excellent regulatory framework but poor stakeholder engagement might still struggle. This underscores the importance of the interplay with relational factors, discussed next. It also suggests that our institutional findings are tied to the Indonesian context: in other environments, the baseline institutional quality might differ, and thus the relative impact could be larger or smaller. We caution that while strong institutions are universally beneficial, the path to improved performance often requires complementary ingredients (like stakeholder buy-in) especially in emerging economies.

Stakeholder Relational Engagement: The Human Element

Perhaps one of the most striking outcomes is the prominence of Relational Engagement (REG) in our model. REG had the largest direct effects on both institutional factors (β ≈ .68) and innovative financing (β ≈ .58), as well as a solid direct effect on performance (β ≈ .33). The total effects analysis revealed that relational engagement influences financing performance both directly and through multiple indirect paths, making it arguably the most influential single construct in the model. This underscores a key message: the way stakeholders interact can make or break an infrastructure project’s financing.

This finding is firmly in line with stakeholder theory, which argues that managing stakeholder relationships is critical to organizational success (Freeman, 1984). Our contribution is demonstrating this quantitatively in a PPP context. The result confirms qualitative observations in PPP literature that “PPP is as much about people as about finance”– trust between a government and a private partner can reduce risk contingencies; effective communication can resolve issues that might otherwise escalate into costly disputes; and a collaborative ethos can lead to joint problem-solving (Roehrich et al., 2014; Yescombe & Farquharson, 2018). For example, one survey respondent (via an open comment) noted that “regular coordination meetings between the ministry and the concessionaire helped us identify a funding shortfall early and arrange a top-up through a public guarantee”– a real-life illustration of how relational engagement facilitated an innovative financial solution.

Moreover, relational engagement’s strong link to institutional factors (H6) suggests that stakeholders collectively help shape the governance context of the project. In projects where trust and communication are high, stakeholders are more likely to collaborate in navigating bureaucratic hurdles or lobbying for supportive policies. This dynamic essentially means that human factors (relationships) can reinforce structural factors (institutions). Our data supports this: highly engaged stakeholder groups rated the institutional environment of their projects as more favorable, implying either an actual improvement or at least a shared perception of better institutional support in those cases. In practice, this might manifest as more effective inter-agency coordination or more flexible application of regulations in projects where the public-private team is working well together.

In sum, the “human element” captured by relational engagement proves to be a cornerstone of project financing success. For policymakers and project leaders, this underscores the importance of stakeholder management: investing in trust-building, transparent communication, and partnership culture is not just a soft, feel-good measure, but a hard factor that significantly shapes financial outcomes. Our findings give quantitative weight to that argument within the PPP infrastructure sphere.

Synthesis: An Integrated Stakeholder–Institution–Finance Framework

Bringing the pieces together, our supported hypotheses draw a holistic picture: relational engagement and institutional setup are interdependent factors that together facilitate innovative financing, and all three contribute to superior financing performance. This integrated understanding is one of the key contributions of our study. Prior research often siloed these aspects – some studies (often in engineering or policy domains) examined how institutions affect PPP outcomes, others focused on stakeholder management, and others on financing techniques. We demonstrate quantitatively that these elements cannot be fully understood in isolation:

A project might have access to cutting-edge financial instruments, but if stakeholder relationships are poor, implementing those instruments could falter (e.g., negotiation breakdowns or lack of consensus on risk allocation). Conversely, even high trust and good governance cannot overcome a fundamentally unsustainable financial structure.

Our results – especially the support for the dual mediation chain (REG → IST → IFG → FPE in H9) – suggest that the best outcomes arise when all elements align: strong relationships create strong institutions, which enable innovative financing solutions, leading to strong performance. It’s a virtuous cycle consistent with a systems perspective on project delivery.

One practical manifestation of this synergy is seen in Indonesia’s recent successful PPP projects. For instance, the Central Java Power Plant PPP eventually reached financial closure after significant stakeholder negotiation and government support. It combined political guarantees (institutional support) with a novel financing mix including export credit agency funds (innovative financing), which was only feasible after extensive stakeholder consensus-building following earlier setbacks. Our framework would interpret that success as the result of relational engagement (the government worked closely with the private consortium and local community after initial delays) and institutional backing (the government provided guarantees and regulatory clarity), which then allowed a complex financing package to come together. The outcome was a financially viable project where initially traditional financing alone had failed.

Given our integrated findings, policymakers should adopt a comprehensive approach to PPP project preparation. This means concurrently strengthening institutional frameworks (e.g., clear PPP regulations, strong PPP units), fostering stakeholder engagement (e.g., stakeholder mapping and formal engagement plans, transparent communication strategies, conflict resolution mechanisms), and exploring innovative financing options (e.g., viability gap funding, green bonds, Islamic finance instruments). The maximum benefit is achieved when these efforts are coordinated. For example, as Indonesia launches an infrastructure project, it could set up a multi-stakeholder steering committee (stakeholder engagement), ensure that any regulatory impediments are addressed or that special decrees are issued if needed (institutional support), and hire transaction advisers to design an optimal financing structure possibly including guarantees or blended finance (innovation). Our study provides evidence that investing in all these fronts in tandem is justified.

Limitations and Future Research

This study has several limitations that suggest avenues for future research. First, it focuses exclusively on Indonesian PPP infrastructure projects using a purposive sample of experts, limiting generalizability. While this approach ensures informed responses, it may introduce selection bias, as respondents might have stronger interests or opinions on PPPs and financial innovation than the broader population. Replicating the study in other emerging economies – such as India or Brazil – or conducting comparative cross-country analyses could reveal whether stakeholder and institutional effects differ across political, economic, and cultural contexts. Similarly, comparative studies across different infrastructure sectors or project types (e.g., energy vs. transportation, or transport vs. social infrastructure) would help determine if the observed relationships are sector-specific or hold broadly across PPP settings.

Second, the cross-sectional and perceptual nature of the data limits causal inference. Though theoretical reasoning supports the assumed causal directions (e.g., engagement preceding performance), reverse causality or omitted variables cannot be ruled out. Longitudinal research tracking projects over time could clarify these dynamics more definitively. Third, measurement of complex constructs like relational engagement and institutional quality relies on perception-based surveys, which are inherently subjective. While we adapted validated scales, some dimensions may remain uncaptured and responses can reflect personal or organizational biases. Combining subjective data with objective indicators – such as actual financial metrics or governance indices – would improve validity and reduce potential response bias (e.g., due to social desirability or common rater effects).

Fourth, the sample size of approximately 100 respondents, largely from financial institutions and government agencies, may not fully represent all stakeholder perspectives. Future research could employ larger, more diverse or random samples (where feasible) to enhance representativeness. Fifth, our model does not account for certain project-level or macroeconomic factors that might affect financing outcomes. Variables such as project sector, size, or risk profile could moderate the influence of stakeholder and institutional dynamics. Including these factors in an expanded model would refine the analysis and potentially reveal context-specific patterns (for example, perhaps relational engagement matters even more in higher-risk projects, or institutional quality is especially critical in certain sectors).

Additionally, this study focused on financing performance as the primary outcome. While central to our research question, other dimensions – such as service quality, environmental sustainability, or on-time delivery – also define PPP success. Expanding outcome measures in future studies would offer a more comprehensive understanding of how stakeholder, institutional, and financial factors contribute to overall project success.

Despite these limitations, the study makes a meaningful contribution by providing quantitative evidence of the mediating role of innovative financing between stakeholder engagement, institutional quality, and financing performance in an emerging economy context. It advances the conversation by empirically linking people, processes, and financial tools in infrastructure development.

Future research can build on this foundation through comparative, longitudinal, and sector-specific studies, integrating objective data and additional constructs such as risk allocation or political support. Such efforts would advance a richer, more nuanced theory of PPP success, one that is sensitive to institutional and stakeholder complexities across diverse settings.

Practical Implications and Recommendations

Based on our findings, we propose several practical recommendations for infrastructure finance stakeholders in emerging markets like Indonesia. First, prioritize stakeholder management as a core element of project planning by developing formal engagement strategies, establishing conflict resolution mechanisms, and forging partnerships early to facilitate smoother financing and execution. This might include stakeholder workshops, community outreach for public acceptance, and regular multi-party coordination meetings. Second, strengthen institutional frameworks by simplifying regulations, promoting transparency, and building capacity through specialized PPP training programs. International experience-sharing (e.g., learning from established PPP units in other countries) can further accelerate institutional development. Third, encourage financial innovation – for example, consider blended finance arrangements, local-currency infrastructure bonds, or green financing instruments – while ensuring rigorous due diligence to address the complexity and potential hidden costs of these tools. Fourth, adopt a holistic approach to project preparation that integrates technical, financial, stakeholder, institutional, and legal considerations. Development partners and government agencies should coordinate these aspects rather than working in silos, perhaps via interdisciplinary task forces for major projects. Finally, invest in capacity building for both public and private sector actors. Public officials would benefit from improved skills in communication and negotiation to enhance stakeholder engagement, while private financiers and developers should deepen their understanding of government processes and public accountability requirements. Sharing successful case studies (domestic or international) can inspire and guide replication of best practices in innovative financing and collaboration.

In making these recommendations, we keep in mind that our study indicates success stems from synergy. Thus, a project team or policy-maker should continually ask: Have we fostered trust among key players? Are the rules of the game clear and supportive? Can we finance this in a smarter, more creative way than usual? If the answer to all is yes, the project is likely poised for better outcomes.

Conclusion

This study advances the discourse on infrastructure finance by empirically showing how stakeholder relationships and institutional frameworks jointly shape project outcomes, with innovative financing as a key mediating mechanism. Evidence from Indonesia’s PPP sector reveals that relational engagement and institutional quality significantly enhance financing performance, reinforcing each other through innovative solutions. Our findings highlight that human and institutional “software” (trust, collaboration, good governance) is as vital as engineering and financial “hardware.” For Indonesia, ongoing reforms to strengthen PPP frameworks and stakeholder collaboration are well-founded and linked to improved outcomes. More broadly, this research offers quantitative support for viewing infrastructure finance as a multi-dimensional challenge – integrating stakeholder theory, institutional theory, and governance theory around the use of financial innovation. We encourage breaking disciplinary silos and fostering collaboration between practitioners of finance, policy, and stakeholder management. Ultimately, cultivating trust, partnership, and robust institutions is essential to unlocking the full potential of innovative financing and ensuring sustainable infrastructure development.

Footnotes

Acknowledgements

The authors wish to express their sincere gratitude to Universitas Padjadjaran (UNPAD) for their invaluable support. This publication charge is funded by UNPAD through the Indonesian Endowment Fund for Education (LPDP) on behalf of the Indonesian Ministry of Higher Education, Science and Technology and managed under the EQUITY Program (Contract No. 4303/B3/DT.03.08/2025 and 3927/UN6.RKT/HK.07.00/2025). Additionally, the authors wish to extend their sincere appreciation to the dedicated team at the Indonesia Infrastructure Guarantee Fund (IIGF) Institute and the experts at the IIGF Institute. Their significant input and support have been instrumental in shaping this research.

Author Contributions

Conceptualization: PI and YA; Methodology: PI and AW; Software: PI; Validation: PI, YA, AW, and KS; Formal analysis: PI, YA, AW, and KS; Investigation: PI and AAF; Resources: PI; Data curation: PI and AAF; Writing – original draft preparation: PI; Writing – review and editing: PI, KS and AAF; Visualization: PI and AAF; Supervision: YA; Funding acquisition: PI. All authors have reviewed and approved the final version of the manuscript for publication.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The publication of this work was supported by Padjadjaran University (UNPAD).

Declaration of Conflicting Interests

The authors declared the following potential conflicts of interest with respect to the research, authorship, and/or publication of this article: The authors hereby declare that there are no conflicts of interest related to this study. No financial, professional, or personal relationships have influenced the design, execution, analysis, or reporting of this research. The study was conducted independently, ensuring objectivity and integrity in all aspects of the research process.

Data Availability Statement

The data that supports the findings of this study are available from the corresponding author, Pratomo Ismujatmika, upon reasonable request.