Abstract

Countries in Sub-Saharan Africa (SSA) continue to seek pathways that can accelerate industrial growth. Among the various drivers, foreign direct investment (FDI) has emerged as a key determinant of industrialization in the region. However, previous studies on the FDI–industrialization nexus have largely overlooked the moderating role of trade openness. This study therefore examines the impact of FDI on industrialization in SSA, with particular attention to the role of trade openness. Using panel data from 30 SSA countries covering the period 2000 to 2022, the analysis employs both Fixed Effects and Random Effects estimators. The results indicate that FDI inflows significantly and positively influence industrialization, whereas FDI outflows exert a negative effect. Moreover, trade openness moderates this relationship by strengthening the positive effect of FDI inflows and intensifying the negative effect of FDI outflows on industrialization. These findings highlight the importance for SSA governments to design and reinforce policies that encourage FDI inflows and expand trade openness in order to foster industrial development. In addition, the results underscore the need for policies that support local industries, thereby enhancing their competitiveness and capacity to attract foreign investors.

Introduction

In recent years, foreign direct investment (FDI) has been widely recognized as a catalyst for industrialization (Jie & Shamshedin, 2019; Mühlen & Escobar, 2020). FDI plays a crucial role in enabling economies to industrialize by facilitating the transfer of technology, capital, and managerial expertise from advanced to emerging nations. Industrialization, in turn, has become an indispensable driver of social progress and modernization, particularly as the global economy enters a new phase characterized by large-scale industrial expansion. For every country, industrialization offers significant benefits, including economic transformation, job creation, and improved living standards.

For developing economies, especially those in Sub-Saharan Africa (SSA), industrialization is a key pillar of sustainable development, aligning with the Sustainable Development Goals (SDGs) through its economic, social, and ecological dimensions (Ayamba et al., 2020). Scholars have also argued that trade liberalization can accelerate both industrialization and economic growth (Majumder & Rahman, 2020; Miah & Majumder, 2020). Consequently, SSA countries have engaged in a range of trade agreements to regulate cross-border flows of goods and services (Katircioglu et al., 2023). This process has significantly expanded trade openness across the region, thereby boosting industrial activity and contributing to broader economic development.

Trade openness, in particular, is viewed as a policy strategy that facilitates access to advanced and cost-effective technology, high-quality inputs, and managerial know-how (Majumder & Rahman, 2020; Miah & Majumder, 2020). These elements enhance local production capacity, attract FDI, and stimulate industrialization. Free trade also benefits consumers by improving efficiency and lowering prices. As Adofu and Okwanya (2017) note, domestic exporters in open economies can exploit economies of scale by accessing larger markets. For SSA, the expansion of industrial sectors is critical to addressing persistent challenges such as unemployment, poverty, and low living standards. Over the past two decades, the region has therefore liberalized trade further to encourage imports, expand exports, and integrate into the global economy.

Despite growing interest in this subject, prior research on the effects of FDI on industrialization has produced mixed results, often due to differences in methodology and sample size (Ayamba et al., 2020; Ngouhouo & Ewane, 2020; Voumik & Ridwan, 2023). More importantly, most studies have examined only the direct effect of FDI on industrialization, neglecting the potential moderating role of trade openness. Similarly, earlier studies typically considered FDI inflows but overlooked FDI outflows, which may also have significant implications for developing economies (Jie & Shamshedin, 2019; Mühlen & Escobar, 2020). These limitations highlight the need for new research that incorporates both inflows and outflows of FDI, while also testing for the influence of trade openness using robust econometric approaches and larger samples.

Accordingly, this study seeks to address four objectives: (a) to examine the impact of FDI inflows on industrialization in SSA; (b) to assess the effect of FDI outflows on industrialization; (c) to investigate the moderating role of trade openness in the relationship between FDI inflows and industrialization; and (d) to analyze how trade openness moderates the relationship between FDI outflows and industrialization.

In terms of innovation and motivation, this study differs from earlier research and provides new insights into the relationship between FDI and industrialization. Unlike previous studies that focused primarily on the direct effect of FDI on industrialization, the present research offers novel empirical evidence on the moderating role of trade openness in this relationship. From a methodological standpoint, earlier studies often relied solely on industry as the measure of industrialization, which proved to be restrictive. Using industry as the only proxy limits the applicability of empirical results in the current era of industrial and urban development. To address this limitation, the present study incorporates urbanization as an additional variable to capture broader dimensions of industrialization.

Another contribution lies in the application of extensive reliability and robustness tests to ensure the validity of the findings and their usefulness for policy. While many earlier studies overlooked important diagnostic checks such as stationarity and cross-sectional dependence, this study explicitly incorporates them. These tests are crucial for guiding the choice of appropriate estimation strategies and for producing results that policymakers can trust. Furthermore, this research uses a relatively large dataset, covering 30 SSA countries over a 22-year period, and introduces a carefully selected control variable to strengthen the analysis. This represents a significant improvement over earlier studies with smaller samples and fewer controls.

SSA was selected as the focus of this study because several countries in the region have recently experienced notable advances in both FDI and industrialization. To achieve the study’s aims, secondary data were obtained from the World Development Indicators (WDI) database for the years 2000 to 2022. Due to data availability, 30 out of the 46 SSA countries were included in the sample. The analysis employed the Fixed Effects (FE) estimator as the primary method, with the Random Effects (RE) estimator used for robustness checks. The results confirm that trade openness significantly moderates the relationship between FDI and industrialization in SSA. These findings suggest that policies on FDI, industrialization, and trade openness must be strengthened, restructured, and effectively enforced to maximize the region’s industrial growth.

The remainder of the paper is structured as follows: Section “

Literature Review

FDI in Sub Saharan Africa

FDI has increased significantly in Africa due to the favorable business environment than other prospective countries (Marandu et al., 2019). Investor confidence has increased due to several African countries’ improving political stability and governance. A big draw for foreign investment has been Africa’s burgeoning middle class, expanding consumer market, and new resources (Edziah et al., 2022). Historically, FDI has gone chiefly to Africa’s extractive and natural resource sectors. Significant investments have been made in the oil and gas industry in South Africa, Nigeria, and Angola. Diversification has, however, become more apparent, with investments increasingly concentrating on value addition and downstream sectors like petrochemicals and refining (Abdul-Mumuni et al., 2023).

Along with the extractive industries, industrial and infrastructure growth have drawn significant attention as essential investment areas in Africa. In industries including textiles, apparel, automotive, and electronics, countries like Ethiopia, Kenya, and Rwanda have become prominent investment destinations (Zhou et al., 2022). In addition, funding for infrastructure projects in housing, telecommunications, energy, and transportation is increasing, supporting the continent’s development goal.

Sub-Saharan African countries have changed their stances on regulations regarding foreign investment over the last two decades, providing attractive incentive plans that draw foreign investors in response to World Bank demands and some industrialized nations on emerging economies to open up their capital accounts. In recent times, FDI has surpassed all other forms of foreign aid as the primary source of financing for many nations in the developing world, especially countries in SSA (Appiah et al., 2023). Many Sub-Saharan African governments have adopted foreign direct investment-friendly policies trying to entice foreign investors, demonstrating their significance on the supply of international finance (Osei, 2024). Foreign direct investment flows steadily grew from $1.69 billion in 1990 to $31.595 billion in 2018. With a stock of $474 billion in 2013, FDI into SSA has expanded by about six times since 2000 (Osei et al., 2023). Contrasted with other parts of the globe, Sub-Saharan Africa is second only to Asia regarding its share of the growth of FDI inflows throughout the chosen timescale (Ostic et al., 2022).

Africa’s production value-added, export figures, and industrial percentage of GDP have not been inspiring (Signé, 2018). The level of industrialization cannot be inferred from the fact that foreign direct investment inflows of SSA have outperformed those in all other areas except Asia between 1990 and 2018. However, manufacturing’s share of the GDP has been falling, and its value-added has not kept pace (Opoku & Yan, 2019).

On average, foreign investment into the Southern African region has entered South Africa’s market. United Nations Conference on Trade and Development (2018) reports a reversal in FDI to South Africa in 2017 to $2.0 billion. According to the study, foreign direct investment into the southern area rose by 13% in 2018 to $32 billion, with South Africa receiving the most significant share of this total at over $5.3 billion, a significant rise from the previous year. According to Bank (2019), FDI accounted for around 1.6% of West African Economic and Monetary Union (WAEMU) member states’ GDP from 1980 to 2017. Estimates put the total FDI received by WAEMU members at $561 million in 1980 and $3 billion in 2017. Cote d’Ivoire got the largest FDI of any WAEMU member over the same period. Cote d’Ivoire recorded an average FDI of $2.86 billion US dollars, whereas Senegal averaged $2.10 billion US dollars. Togo’s average yearly FDI of around 386 million US dollars is among the least in the WAEMU area. These numbers highlight the role of FDI in the financial revitalization of WAEMU’s industrial sector. Since 2007, FDI projects in East Africa have risen at a compound annual growth rate of 19.9%, the highest in Africa (Opoku & Boachie, 2020). Scale and technical issues stem from the large influx of FDIs into the region. FDIs were expected to amount to 7.2% of Africa’s GDP by 2020. FDI boosts domestic rivalry and expenditure on technology, improving industrialization (Agudze & Ibhagui, 2021).

Exports have traditionally been considered a driver of economic growth, making it crucial to empirically evaluate the effects of FDI on the export earnings of a host country. In general, it is accepted that FDI boosts exports for the country receiving it by increasing the country’s capital for exports, assisting in transferring of technology and new goods for exports, a pathway into diverse and broad foreign markets, and developing and enhancing the specialized and managerial skills of the inhabitants of the country. FDI may also reduce or replace local investment and savings, move technologies that are low-level or not appropriate for the host country’s variables proportions, focus on the host country’s local market rather than expanding exports, stifle the growth of indigenous firms that could day become exporters, and fail to aid in the development of the host country’s flexible competitive advantages.

When it comes to luring FDI to Africa, Ethiopia has emerged as a rising star. Significant investments have been made in manufacturing, agriculture, and renewable energy due to the country’s stable political climate, inexpensive workforce, and welcoming investment laws (Ostic et al., 2022). Ethiopia’s strategic position as a hub for East Africa and its sizable domestic market add to the country’s allure as a place for investments. Also, Nigeria has seen a boom in FDI inflows in recent years as Africa’s biggest economy. Oil and gas, manufacturing, telecommunications, and financial services are just a few industries that have seen investments because of the nation’s vast oil reserves, growing consumer market, and continuous economic reforms (Asamoah et al., 2019). However, obstacles to continued FDI expansion in the nation still exist, including corruption, security worries, and poor infrastructure (F. O. Agyeman et al., 2022).

Institutional Theory

According to the institutional theory, the institutional environment has a significant influence on how multinational corporations that engage in FDI interrelate (Yiadom et al., 2022). This environment consists of both formal structures and such as laws, policies protecting property rights, and procedures for enforcing contracts, as well as informal institutions (social customs and cultural norms; Opoku & Boachie, 2020). Thus, the institutional framework of a country or region determines the inflow and outflows of investment to impact industrialization. The theory further suggests that countries with strong legal system and open regulations environments often draw in more foreign direct investment which increases industrialization (Shijian & Agyemang, 2022). This justifies that the increase in fixed capital formulation in SSA region is due to the open environmental, societal norms and value which has increased industrialization recently. This increased investment catalyzes the development of new businesses and supports the growth of existing ones, thereby advancing industrialization (Katircioglu et al., 2023; Yiadom et al., 2022). This is because when countries develop due to FDI, there is a commensurate rise in production and industrial activity, which often depends on industrialization processes. In light of this, the industry may rise due to the rising demand for FDI in most countries in SSA. The theory incorporates essential concepts, including market dynamics, capital accumulation, technology transfer, comparative advantage, trade openness, and spillover effects (Osei et al., 2023). Thus, the institutional mechanism may impact these factors affecting foreign direct investment and industrialization.

Moreover, the theory argues that trade openness promotes FDI by providing corporations access to broader markets, facilitating economies of scale, and fostering competitiveness and efficiency thereby promoting industrialization. Furthermore, when businesses collaborate and interact across borders, trade openness promotes technological and information transfer thereby enhancing investment patterns (Opoku & Boachie, 2020). In addition, the extent to trade openness will impact FDI and industrialization will be determined by the institutional norms, values, and beliefs, market regulations, intellectual property right and government regulations.

Economic Integration Theory

Anis et al. (2022) outline that economic integration theory looks at the basis and impacts of regional or global economic integration. Specifically, the theory examines the underlying drivers for integration, the mechanisms involved in the integration process, and the effects that arose for the involved countries (A. O. Agyemang et al., 2025b). The theory explores the benefits, such as enhanced market penetration, economies of scale, and industrialization, along with the challenges, such as costs incurred during the transition stages. This theory focuses on the advantages of regional economic integration in enabling FDI flows and fostering industrial growth, such as constructing shared markets, free trade regions, and customs unions (Shijian & Agyemang, 2022).

The economic integration theory further highlights the importance of market access in luring FDI. Nations may increase their market size by lowering trade barriers and fostering more favorable business conditions through regional economic integration projects (Wang et al., 2025). A greater amount of FDI that can assist industrialization will come into the area as a result of the enhanced market access, according to Zhang et al. (2021). Furthermore, economic integration encourages the link between intra-regional commerce and makes it easier to build regional value chains. By participating in regional integration accords, nations may gain from increasing trade and investment within the area. Through this integration, local industries may have the chance to join global production networks, draw FDI for manufacturing with an eye toward exports, and advance industrialization (Appiah et al., 2022; Katircioglu et al., 2018).

Empirical Review and Hypothesis Development

The link between FDI and industrialization in SSA may be better understood through economic integration theory. Economic integration may attract FDI inflows by expanding markets and lowering investor transaction costs. Regional cooperation and minimal trade and investment barriers define economic integration. Through the creation of an inviting investment climate and investment facilitation, the integration of sub-Saharan African countries into regional economic communities like the East African Community or the Economic Community of West African States plays a crucial role in attracting FDI and promoting industrial development (Shijian & Agyemang, 2022).

According to Wako (2021), the contribution of neoclassical economics to understanding the effects of FDI on industrialization in SSA is that by bringing in money, technology, managerial expertise, and access to global markets, FDI may considerably aid the process of industrial growth. Increased foreign direct investment may help Sub-Saharan nations, which often suffer capital and cal restrictions, since it promotes economic development, provides employment, and boosts overall productivity.

The association between FDI inflows and industrialization in West African nations was found to be positive and substantial by Hakim (2020), suggesting that FDI inflows encourage the expansion and development of the industrial sector. Similarly, Voumik and Ridwan (2023) provided evidence that FDI inflows had a favorable influence on industrialization in West African nations, resulting in more jobs, knowledge transfer, and increased industrial sector productivity. This was consistent with Sun et al. (2020) findings, which indicate that FDI inflows positively contribute to industrialization by promoting capital creation, stimulating technical developments, and raising the industrial sector’s competitiveness. Shijian and Agyemang (2022) discovered, contrarily, that FDI inflows in several African countries have resulted in de-industrialization since resource-seeking investments predominate, and manufacturing sectors are neglected. This was consistent with the results of Liu et al. (2023), who noted that FDI inflows into Sub-Saharan Africa had been centered on extractive industries, resulting in minimal diversification and underdeveloped manufacturing sectors, impeding industrialization. Zhou et al. (2022) observed that higher levels of FDI inflows were related to increased industrialization, which is in contrast to the earlier negative results, demonstrating that FDI performs a vital role in the industrial growth of SSA countries. This was supported by Opoku and Boachie (2020), who identify a positive link between FDI inflows and industrialization, hypothesizing that FDI inflows encourage technical advancement, the construction of human capital, and the development of infrastructure, all of which contribute to industrial expansion. The results of Oduola et al. (2022), who discovered that FDI inflows favorably affect industrialization by encouraging exports, developing backward and forward links, and increasing productivity in the industrial sector, provided more evidence.

According to a study by Odugbesan et al. (2022), access to resources and markets rather than encouraging industrialization were the critical motivations for FDI outflows from SSA. Similarly, Nyeadi and Adjasi (2020) study found that FDI outflows from SSA were mostly intended for profit repatriation and tax avoidance rather than industrial sector investment. This was consistent with the study by Munir and Ameer (2020), who found that FDI outflows from SSA were often focused on safer and more developed markets rather than industrial sector investments. Similar findings were made by Osei (2024), who discovered that FDI outflows from West African countries tended to concentrate on low-value-added activities like trade rather than investing in the industrial sector.

In contrast to the negative findings, a study by Megbowon et al. (2019) found that FDI outflows from SSA had a favorable influence on knowledge spillovers and technology transfer, which helped to drive industrialization. This was similar to the findings of Mamba et al. (2020), who found that FDI outflows from SSA favorably affected local businesses’ expansion and development, which helped promote industrialization. Similar findings were made by Lin and Agyeman (2021), who discovered that foreign direct investment outflows favorably impacted the economic growth and modernization of regional supply networks, which aided industrialization. The results of Lin and Agyeman (2021), who discovered that FDI outflows from SSA had a beneficial influence on export competitiveness and led to industrialization, provided more evidence. Similar findings were made in a study by Megbowon et al. (2019), who discovered that foreign direct investment outflows from SSA favorably affect regional integration and commerce, which helped promote industrialization.

A study by Karim et al. (2022) revealed that FDI outflows from North Africa favorably influenced technology absorption and innovation, contributed to industrialization, and provided more support. In contrast, a study by Kongkuah et al. (2021) found that FDI outflows from SSA were constrained by elements including poor capital markets and inadequate technical capacity, which reduced their influence on industrialization. Similarly, Osei (2024) showed that rather than being motivated to industrialize further, FDI outflows from SSA were mainly driven by strategic asset-seeking objectives.

Trade openness moderates FDI inflows and industrialization by allowing access to more significant markets, chances for specialization, and technology transfer. Moreover, whereas trade obstacles may impede both FDI inflows and industrialization, a good trade environment strengthens the benefits of FDI on industrialization (Bulus & Koc, 2021; Katircioglu et al., 2021). As a result, the degree of trade openness significantly affects how foreign direct investment inflows and industrialization.

Trade openness significantly moderates the association between FDI outflows and industrialization. It contends that when local businesses develop abroad and take advantage of possibilities for international commerce, a greater degree of trade openness promotes an increase in FDI outflows. Additionally, trade openness promotes the expansion of local businesses and economic diversity, which supports industrialization by controlling information and technology transfer. The moderating effect of trade openness highlights how FDI outflows, global commerce, and industrial growth are intertwined and any possible synergies and gains that may result from these interactions. Based on the literature reviewed, the following hypotheses are proposed.

Methods

Research Design

The author employs secondary data extracted from WDI from 2000 to 2021. Due to the unavailability of data in some of the research variables respective to some countries in SSA, only 30 of the 46 SSA nations were chosen for the study. Data for the study was obtained from the Word Development Indicator (WDI) database (2023). This database provides data for the variables annually. Table 1 shows the population and sample statistics for the study’s included and excluded nations. Stata version 17 was employed for the empirical studies.

Population and Sampling.

Variables Description

Table 2 shows the summary of study variables.

Summary of Study Variables.

Model Construction

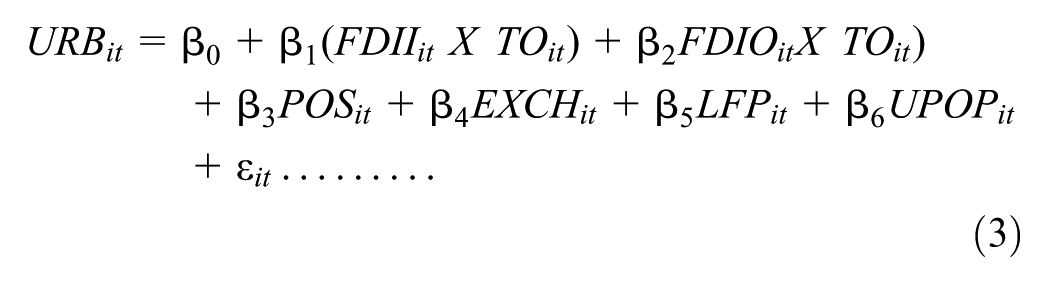

To analyze the effect of FDI on industrialization in SSA, the study adapted a model by Edziah et al. (2022) which is express in the following multiple linear regression model:

Where IND represents industry (including construction, value-added; % GDP), URB represents urbanization (% of urban growth population), FDII represents Foreign Direct Investment Inflow, FDIO represents Foreign Direct Investment Outflow, TOP represents Trade openness, POS represents Political stability, EXCH represents Exchange rate, LFP represents Labor force participation, UPOP represents Urban population growth, ε represents Error term, t represents the year, I represent the country.

Estimation Strategy

This study employs a panel data regression framework to analyze the effects of foreign direct investment (FDI) and trade openness on industrialization in Sub-Saharan Africa (SSA). The dataset combines cross-sectional observations from 30 SSA countries with time-series data covering the period 2000 to 2022, making panel regression the most appropriate technique. Compared with purely cross-sectional or time-series models, panel data methods allow for the control of unobserved heterogeneity, capture both temporal and country-specific dynamics, increase the degrees of freedom, and reduce multicollinearity. These advantages improve both the efficiency and the reliability of the estimates.

Within this framework, two estimators were applied: the Fixed Effects (FE) model and the Random Effects (RE) model. The FE model was selected as the primary estimator because it controls for unobserved country-specific characteristics that remain constant over time, such as geography, historical factors, or institutional structures, which could bias the relationship between FDI, trade openness, and industrialization. The RE model assumes that these unobserved effects are uncorrelated with the regressors and therefore produces more efficient estimates when this assumption holds. To guide the choice between the two, a Hausman specification test was conducted, and the results confirmed the suitability of the FE model. The RE model was nevertheless estimated as a robustness check to verify the consistency of the results.

To further ensure robustness, a series of diagnostic tests were conducted. These included tests for stationarity to avoid spurious regressions, cross-sectional dependence to capture potential spillover effects across countries, and serial correlation to account for persistence in the panel data. By combining the FE estimator as the main model, the RE estimator as a robustness check, and rigorous diagnostic testing, this study ensures that the empirical results are both statistically sound and relevant for policy.

Data Processing

The authors first conducted a cross-sectional dependence test to ascertain if CD was present in the study variables. The stationarity test was then conducted to determine if the dataset was stationary at the level or first difference. Also, the authors conducted a cointegration test to examine the long-term connection among the study variables. According to the findings from the preliminary tests, the authors selected FE and RE estimators for the multiple regression analysis. Moreover, to confirm the accurate estimator for the study we performed the Hausman test. Finally, we conducted the heterogeneity test to confirm our empirical analysis.

Results and Interpretation

Descriptive Statistics

In their most basic form, descriptive statistics are specialized methods that assist in correctly analyzing, characterizing, and summarizing data from gathered study result in a significant, valuable, and effective approach (Jijian et al., 2021). The mean, mode and median are the basic tendencies in descriptive statistics. Table 3 displays descriptive data.

Descriptive Statistics.

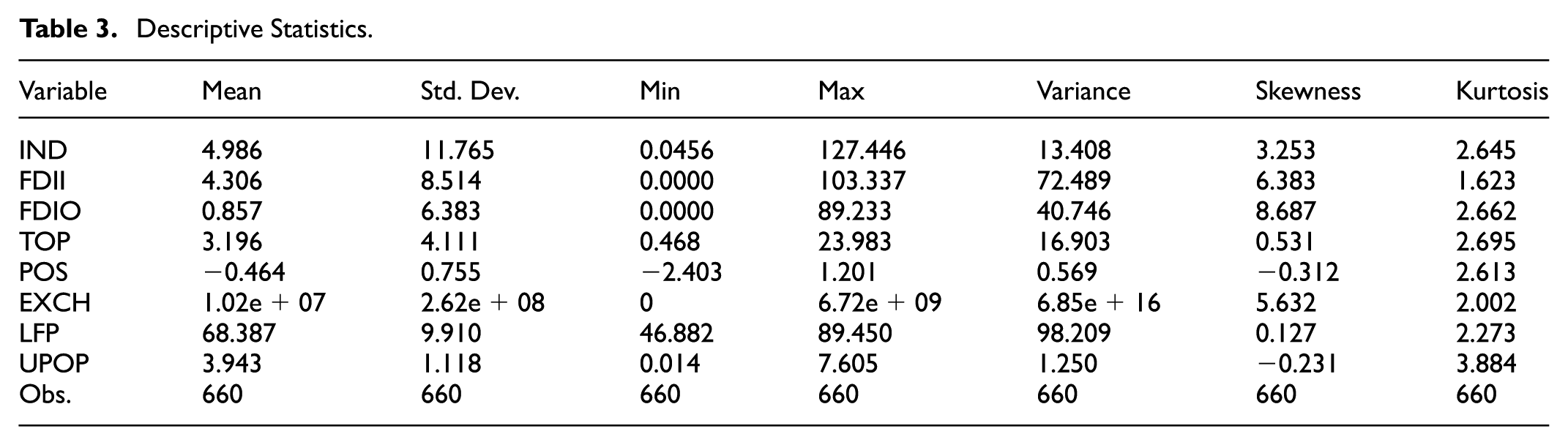

Table 3 presents the descriptive statistics of the study variables. Industrialization (IND), measured as the share of GDP devoted to industry (including construction and value-added manufacturing), ranged from 0.0456% to 127.446%, with a mean of 4.986%. This wide variation highlights the significant differences in industrial development across SSA countries. The standard deviation of 11.765 confirms this dispersion, reflecting the presence of both relatively industrialized economies and those with very limited industrial output. Importantly, earlier negative values reported for IND were the result of coding errors during data processing; these have now been corrected using the original World Development Indicators (WDI) dataset, which confirms that industrial shares of GDP are, by definition, non-negative.

With respect to foreign direct investment, inflows (FDII) as a percentage of GDP ranged between 0% and 103.337%, with a mean of 4.306%. This indicates that while many SSA countries receive modest FDI relative to GDP, a few have attracted exceptionally high inflows, producing large variation in the sample. Similarly, foreign direct investment outflows (FDIO) had a mean of 0.857%, ranging from 0% to 89.233%. This demonstrates that outward investment from SSA remains relatively low overall but is significant for a small number of countries. The earlier negative values reported for FDII and FDIO were also due to erroneous entries during data cleaning, which have now been corrected to ensure accuracy.

Trade openness (TOP), measured as the ratio of exports and imports to GDP, ranged from 0.468% to 23.983%, with an average of 3.196%. This variation highlights the heterogeneity of global trade integration across SSA economies. While some countries remain only marginally connected to international markets, others demonstrate relatively high levels of openness, reflecting differences in trade policy frameworks, infrastructure development, and economic diversification. The dispersion in TOP suggests that trade openness plays an uneven role in shaping industrialization outcomes across the region.

Regarding the control variables, political stability (POS) averaged −0.464, underscoring the persistence of governance and security challenges in many SSA countries. Such instability can undermine investor confidence and slow industrial growth. Exchange rates (EXCH) exhibited wide variation, ranging from relative stability in some economies to significant volatility in others, reflecting disparities in monetary management and macroeconomic fundamentals. Labor force participation (LFP) ranged from 46.882% to 89.450%, with an average of 68.387%, indicating considerable diversity in labor market engagement across SSA. Finally, urban population growth (UPOP) averaged 3.943% annually, with values between 0.014% and 7.605%, reflecting the rapid demographic transitions that continue to shape industrial and economic development in the region.

Cross-Sectional Dependency (CD) Analysis

Indeed, several parameters, including the strength of the linkage between cross-sections and the kind of cross-sectional dependency, influence the effect of cross-sectional dependence in the estimate (Ostic et al., 2022). The degree and kind of cross-sectional correlations are two of the numerous variables that affect how much a cross-sectional dependence (CD) has on an assumption (Cobbinah et al., 2025). A significant loss in approximating efficiency will arise from disregarding cross-sectional dependency (Osei et al., 2023). In this study, the Frees Test Cross-Sectional Dependence is applied. Table 4 shows the findings of the CD results.

Cross-Sectional Dependency Test—Frees.

As indicated in Table 4, Frees’ test results reject the null hypothesis of cross-sectional dependence. Frees’ test recorded the critical values for = .10, = .05, and = .01 based on the Q distribution when T ≤ 30. The Frees’ statistic falls below the significance level at = 0.01. Therefore, it follows that CD is not present in the observables. This indicates that a shock in one of the countries is unlikely to affect the other.

Stationary Analysis

To reduce the spurious regression issue, it is essential to look into the normality of panel data and the order of integration (Twum et al., 2022; Zhu, Osei, et al., 2024). The test was used to determine if our data set is static at a level. Table 5 reports the outcomes of these examinations.

Stationarity Test.

A CIPS Unit Root Test, as shown in Table 5, shows that neither the constant nor the constant with trends for FDIO and POS was integrated at level, with values reported falling short of the actual thresholds of 2.07 and −2.58, respectively. The remaining variables were included in both the constant and constant with trend conditions. Since not all of the parameters were level-integrated, the stationarity test was conducted using the first difference instead. After initial categorization, we integrated all of the study variables concurrently, taking trends into account. The initial point of difference between the variables is hence the location of integration.

Cointegration Analysis

Cointegration testing determines the extent to which two variables are intertwined throughout time (Osei et al., 2025). Multiple regression analyses are not warranted because there is no protracted link among the study variables, as shown by the lack of a cointegration test (Twum et al., 2022). To examine the protracted correlation among the variables and their respective trends, the Pedroni Trend Cointegration test was used. Table 6 presents the Pedroni Trend cointegration test.

Pedroni Trend.

Numerous trend tests have probabilities below .01, demonstrating a 1% significant level, as shown in Table 6. Therefore, while cointegration is not rejected outright, it is not accepted as the null hypothesis either. This suggests a lasting connection among the factors analyzed in the integrated analysis.

Estimation Techniques

The study primarily employed the Fixed Effects (FE) estimator in the R1 regression analysis, with the Random Effects (RE) estimator used in R2 as a robustness check to ensure the reliability of the results. Fixed effects control for time-invariant factors like firm culture or location, focusing on within-entity variation to ensure that changes over time within the same entity explain the dependent variable (Osei et al., 2023). This makes fixed effects ideal for capturing dynamic changes and providing stronger causal insights. On the hand, random effects utilize both within- and between-entity variation, allowing for more efficient estimation when certain assumptions hold (Zhu, Wiredu, et al., 2024). Employing these estimators show the robustness of our findings. To determine which estimator is more appropriate between the Fixed Effects and Random Effects, we performed a Hausman test, as presented in Table 9.

The study is grouped into 12 Models. Models 1 to 6 focus on the impact of FDI on industrialization. Specifically, Model 1 examines the effect of FDII (FDI inflows) on industrialization in SSA, while Model 2 analyzes the influence of FDIO (FDI outflows). Model 3 evaluates the combined effects of FDII and FDIO on industrialization. In Model 4, the moderating role of trade openness (TOP) on the relationship between FDII and industrialization is assessed, and Model 5 extends this analysis to FDIO. Model 6 explores the moderating role of TOP on both FDII and FDIO in relation to industrialization.

Models 7 to 12 shift the focus to urbanization, replacing industrialization as the dependent variable to test the robustness of the results in SSA. Model 7 evaluates the impact of FDII on urbanization, while Model 8 assesses the influence of FDIO on urbanization. Model 9 investigates the combined effects of FDII and FDIO on urbanization. Model 10 examines the moderating role of TOP on FDII and urbanization, and Model 11 analyzes the same moderating effect on FDIO and urbanization. Finally, Model 12 evaluates the moderating role of TOP on both FDII and FDIO in their impact on urbanization.

The results of the estimation analysis are presented in Table 7, while Table 8 highlights the findings on the moderating role of trade openness in the relationship between FDI and industrialization.

Multiple Regression Analysis.

= 1%, ** = 5%, * = 10%.

Moderating Role Findings.

= 1%, ** = 5%, * = 10%.

Hausman Test.

Table 7 shows the results of the estimation techniques for Models 1 to 6. Wald chi2 values of 254.47, 320.14, 410.60, 667.84, 767.19, and 185.81, respectively, for each Model R2. The result indicates that the approach is statistically applicable to the study. In addition, the estimation techniques in Table 7 for Models 7 to 12 displays Wald chi2 values for Model R2. The R2 values are 311.35, 424.42, 524.66, 605.50, 711.79, and 1913.15 for each model accordingly. The findings indicate that, statistically, the approach is essential for the empirical study.

By using FE as the primary estimator, Model 1 (R1) findings posit a positive and statistically significant link between foreign direct investments inflow (FDII) and Industrialization (IND). This indicates that FDI inflow stimulated industrialization in SSA. The favorable link means that a change upsurge of FDII of sampled countries in SSA will increase industrialization by 0.1754. The favorable link is statistical significance at a level of 1% since the p-value is less than 1%. Therefore, the first hypothesis is rejected according to the estimation analysis results.

The results from R1 in Model 2 show that the effect of FDIO and industrialization (IND) is positive but statistically insignificant. The positive slope relationship implies that a unit increase in FDIO will not increase SSA industrialization. The results also revealed that if the sample countries transfer their investments to foreign economies by a unit point, SSA will not improve industrialization. The results show that FDIO did not induce industrialization in SSA. Hence, hypothesis two is approved, and as a result, it follows the assumptions.

Furthermore, when the two independent variables were summed up, Model 3 (R1) displays that FDII is statistically significant at a 1% level and positively impacts industrialization. At the same time, FDIO is positive but statistically insignificant and does not impact industrialization in SSA. The result displayed the same relationship when a single independent parameter was used in Models 1 and 2. This result agrees that an upsurge in FDII by 0.1672 will increase industrialization, whereas an increase in FDIO will not increase industrialization by 0.0273 in sampled countries in the SSA region.

In addition, when trade openness was introduced as moderating variable, Model 4 (R1) showed a positive relationship between FDII and industrialization which is statistical significance at a 1% significance level. The result displays an increase in the foreign direct investment inflow coefficient when the moderating variable, trade openness, was added. Also, results reveal that if the sample countries liberate their trade by a unit, it will increase foreign direct investment inflow and industrialization by 50.99%. Therefore, we accept the hypothesis.

Similarly, introducing the moderating variable, trade openness, Model 5 (R1) shows a positive relationship between FDIO and industrialization but is statistically insignificant at all levels. In addition, the foreign direct investment outflow coefficient rises when trade openness is added. The results reveal that if trade openness increases by a unit, foreign direct investment outflow will increase by 64.56%, which will not increase industrialization.

Furthermore, when trade openness was added to foreign direct investment inflow and outflow variables, Model 6 (R1) showed a positive and significant association between FDII and industrialization. The favorable link is statistical significance at a 1% significance level. This means if the sample countries in SSA open their trade by a unit, it will increase foreign direct investment inflow and industrialization by 0.6158. However, Model 6 (R1) findings posit that FDIO has a negative and insignificant relationship with industrialization. It implies that SSA countries increasing their trade openness will increase foreign direct investment outflow, decreasing industrialization by 0.7495. Finally, the coefficient of both foreign direct investment inflow and outflow increase in Model 6 (R1), indicating that trade openness plays a role in foreign direct investment flows.

Concerning the findings of the robustness test of the Random Effect (RE) estimator in various models, Model 1 (R2) shows a positive and statistically significant linkage between FDII and Industrialization at a 1% significance level. The result reveals that an upsurge in SSA’s foreign direct investment inflow will increase industrialization by 0.1755. This result of the Fixed Effect estimator for the primary estimation agrees with the Random Effect estimator results.

The result in Model 2 (R2) posits that the effect of FDIO on industrialization is positive but not statistically significant. The positive slope relationship implies that a unit increase in FDIO will not encourage industrialization by 0.1171. It means that FDIO failed to boost industrialization in SSA. The result is similar to the Fixed Effect estimator findings in Model 2 (R1).

In addition, Model 3 (R2) results reveal the same positive and statistical relationship between FDII and industrialization at a 1% significance level. It affirms that an increase in FDII by 0.1665 will increase industrialization. However, the connection between foreign direct investment outflow and industrialization is positive but insignificant. It means an increase in foreign direct investment outflow will not boost the industrialization of sampled countries in the SSA region. The results corroborate with the result of the FE estimator in Model 3 (R1).

With the introduction of trade openness, Model 4 (R2) shows a positive and significant link between FDII and industrialization at a 1% significance level. If the SSA countries balance their trade openness by a unit, it will increase FDII and industrialization by 0.4101 coefficient value of FDII when TOP was added.

Furthermore, Model 5 (R2) reveals that a positive link between foreign direct investments and industrialization is positive and not statistically significant at all levels after introducing trade openness. If trade openness among countries SSA increases by a unit, foreign direct investment outflow by 0.4506, will affect industrialization. Foreign direct investment outflow coefficient value upsurges when trade openness is added to the model. This agrees with the Fixed Effect estimator results in Model 5 (R1).

Regarding the link between FDII and outflow and industrialization after introducing trade openness, Model 6 (R2) results display a positive and statistically significant association between FDII and industrialization. The result indicates that if the sample countries in SSA increase their trade openness by a unit, it will increase foreign direct investment inflow and industrialization by 0.5156. However, Model 6 (R2) results revealed a negative and insignificant association between FDIO and industrialization. This means that FDIO failed to improve industrialization by a unit of trade openness in sample countries by 0.6454.

Using FE as the primary estimator, Model 7 (R1) results display a positive link between FDII and urbanization (URB). The findings also revealed a favorable and statistically significant link between FDII and URB at a 5% significance level. The positive slope relationship implies that a unit upsurge in FDII will increase the urbanization of SSA-sampled countries by 0.0979. Hence, hypothesis two is supported since the result follows the assumptions.

Model 8 (R1) results revealed a positive relationship between foreign direct investments outflow (FDIO) and urbanization but insignificant. The positive link means that a unit upsurge in FDIO of sampled countries in SSA will not increase urbanization. Therefore, the corresponding hypothesis of the study is rejected.

Moreover, the two independent variables (FDII and FDIOO) were included in Model 9; R1 displays a positive link between FDII and the urbanization of the sampled SSA countries. The positive link is statistical significance at a level of 5% for FDII. The findings agree that an increase in FDII of 0.0272 will increase urbanization in SSA countries. However, the result reveals that the impact of FDIO on urbanization is positive but insignificant. An increase in foreign direct investment outflow will not increase the urbanization of sampled countries in SSA. The result displayed the same relationship as when one independent variable was used in Models 7 and 8.

The Hausman test results show that the FE estimator is suitable for the estimation analysis considering the Chi2 value of 17.46 which is statistically significant at 1%. This indicates the rejection of the null hypothesis of RE estimator and accept the alternative hypothesis of FE estimator. For the purposes of the estimating methodologies, the FE estimator is chosen as the primary estimator and the RE estimator is chosen as the robustness estimator.

Discussion for the Moderating Role of Trade Openness

Furthermore, in Table 8 when TOP was introduced as moderating variable, Model 10 (R1) showed a negative slope relationship between FDIO and urbanization which is statistical significance at a 5% significance level. The result reveals that if the sample countries increase their trade openness by a unit, it will decrease foreign direct investment inflow and urbanization by 0.5098. Also, the coefficient of FDII when TOP was added increased. Therefore, we accept the hypothesis.

However, when trade openness was included, Model 11 (R1) revealed a positive link between FDIO and urbanization. This result is not statistically significant. The findings affirm that if countries in SSA liberate their trade, foreign direct investment outflow will not increase urbanization. In addition, the foreign direct investment outflow coefficient upsurges when trade openness is added to the model.

In addition, when trade openness was added to Model 12, which involved foreign direct investment inflow and outflow variables, the results displayed a positive and significant link between FDII and urbanization. The positive relationship is statistical significance at a 5% significance level. This means if the sample countries in SSA increase their trade openness by a unit, it will increase foreign direct investment inflow and boost urbanization by 0.6233. However, Model 12 (R1) results revealed a negative relationship between FDIO and urbanization. The result also shows the relationship is statistical significance at a 5% significance level. On the other hand, increasing trade openness in the SSA region will increase foreign direct investment outflow, decreasing urbanization by 0.7046. Finally, the coefficient of both foreign direct investment inflow and outflow increase in Model 12 (R1), indicating that trade openness plays a role in foreign direct investment flows.

Regarding the Random Effect (RE) estimator results of the robustness test in various models 7 to 12, Model 7 (R2) shows a favorable and statistically significant relationship between FDII and industry urbanization at a 5% significance level. The result reveals that an upsurge in SSA’s foreign direct investment inflow will increase urbanization by 0.1076. This result of the Fixed Effect estimator for the primary estimation agrees with the Random Effect estimator results.

The result in Model 8 (R2) posits a positive link between FDIO and urbanization but is insignificant at all levels. The positive slope relationship implies that a unit increase in FDIO will decrease urbanization by 0.2537. The findings follow the Fixed Effect estimator results in Model 8 (R1).

In addition, Model 9 (R2) results reveal a positive and statistical relationship between FDII and outflow on urbanization at a 5% significance level, respectively. It implies that an increase in FDII will increase urbanization by 0.0400, whereas an increase in FDIO will decrease urbanization by 0.2329 in sampled SSA countries. The results corroborate with the result of the FE estimator in Model 9 (R1).

With the introduction of trade openness in Model 10 (R2), the results show a negative and significant relationship between FDII and urbanization at a 5% significance level. If the SSA countries open their trade by a unit, it will decrease foreign direct investment inflow and urbanization by 0.41014060. The coefficient value of foreign direct investment inflow rises up after adding trade openness to the model.

Moreover, after introducing trade openness in Model 11, R2 reveals a positive relationship between FDIO and urbanization, which is statistically significant at a 5% significance level. If trade openness among SSA countries increases by a unit, foreign direct investment outflow will reduce urbanization by 0.4847. Foreign direct investment outflow coefficient value upsurges when trade openness is added to the model. This agrees with the Fixed Effect estimator results in Model 11 (R1).

The model introduced trade openness regarding the link between FDII and outflow and industrialization; the results in Model 12 (R2) display an adverse and statistically significant association between FDII and urbanization at a 5% significance level. The result indicates that if the sample countries in SSA increase their trade openness by a unit, it will decrease foreign direct investment inflow and industrialization by 0.5181. However, Model 12 (R2) results revealed a negative and significant relationship between FDIO and urbanization at a 5% significance level. It affirms that increased trade openness in sample countries will lead to an upsurge in FDIO and a decrease in urbanization.

Heterogeneity Test

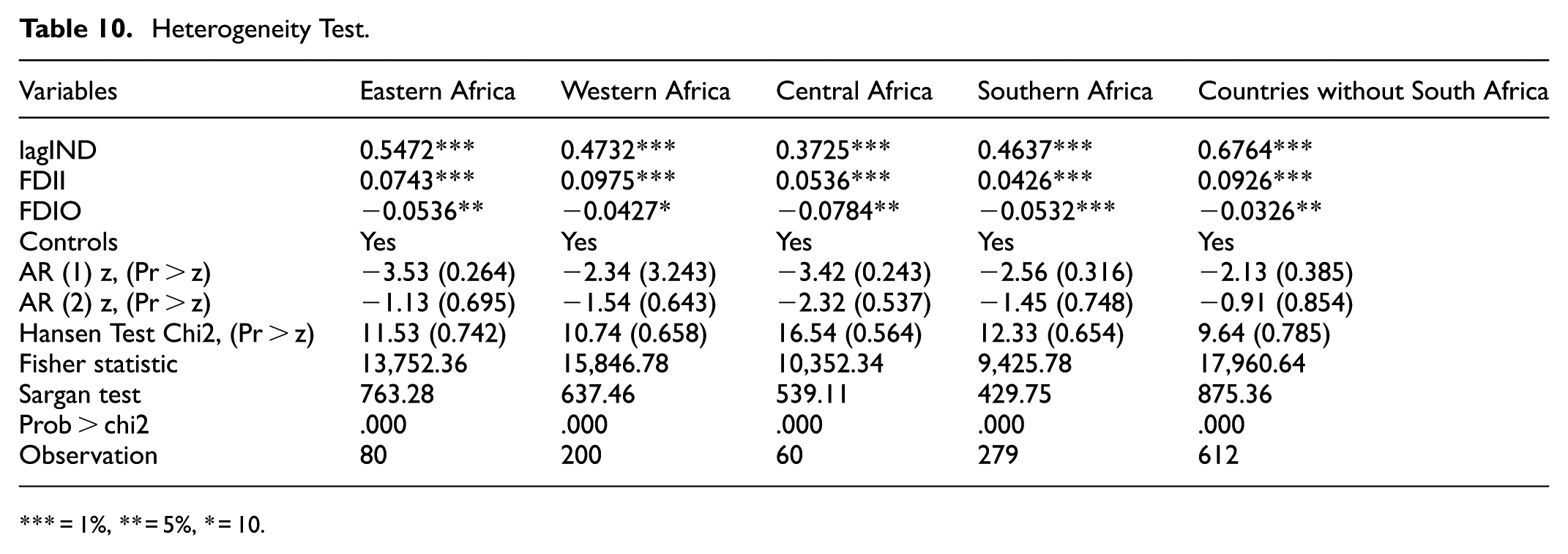

To perform heterogeneity for the analysis we divided the countries in SSA according to regions. Thus, the countries are grouped according to their regions in SSA, and we employed the dynamic system generalized method of moments (GMM) estimator to validate our findings. The GMM estimator eliminate possible endogeneity, autocorrelation and heteroskedasticity problems (A. O. Agyemang et al., 2025a). The findings show that FDI inflows positively impact industrialization while FDI outflows negatively impact industrialization in the various SSA regions. This provides further evidence of our primary findings. Moreover, we tested heterogeneity for the countries excluding South Africa since it has major contribution in the SSA nations. Thus, to confirm our findings we tested the countries without the major contributor of SSA, thus; South Africa to assess the main impact of FDI on industrialization in the region. The findings show that FDI inflows positively impact industrialization while outflows negatively impact industrialization. This shows that excluding South Africa, SSA FDI inflows contributes greatly to industrialization while FDI outflows decrease industrialization in the region which provides further evidence to the primary findings. Table 10 shows the heterogeneity test.

Heterogeneity Test.

= 1%, ** = 5%, * = 10.

Discussion of Results

Like many others, the Sub-Saharan Africa (SSA) area recognizes industrialization as critical to any successful economic growth plan. Foreign direct investment is one way global and local economies increasingly support emerging economies’ efforts to industrialize. Hence, it was postulated that there is a favorable and significant connection between FDI inflow and industrialization.

According to the regression findings, FDII has a highly substantial positive impact on industrialization in SSA nations. The finding held up over a battery of robustness tests, with any deviations staying within the margin of error. Foreign direct investment inflow was especially helpful to the manufacturing and industrial sectors. In line with Hauge (2019), FDI inflow enters into industry sectors, enhancing production output and exportation, which is a crucial reason why FDI inflow is positively impacting industrialization. Foreign direct investment inflow in industrialization has been shown to increase both output and exports and boost local business productivity by exposing them to innovative manufacturing, administration, and trade practices from around the world. Therefore, the first hypothesis of the study was accepted. The findings are similar to prior studies (Appiah et al., 2023). For example, if SSA nations were better able to soak up FDI inflows, their industrialization rates would rise significantly. It is also important to note that the SSA country’s ability to absorb foreign aid increased during the study’s time frame. The outcomes likewise contradict that of Müller (2021), who found that foreign direct investment inflow had an insignificant but beneficial effect on the industrialization of SSA countries. The explanation is that FDI inflow is resource-seeking, creating expatriate affiliate-dominated socioeconomic zones susceptible to deception. Müller (2021) continued that SSA could not create an atmosphere conducive to foreign direct investment because of this.

In addition, when examining how FDI outflow affects industrialization, the preliminary results and the robustness check results show that FDI outflow negatively impacts industrialization in SSA nations. The mechanism of the findings is due to the local resources that have been used to invest in other countries which has decreased industrialization in the SSA countries. Thus, investors in SSA prefer investing in foreign countries which has decreased industrialization in the countries. Moreover, the findings indicate that most of the natural resources used for industrial purposes have been invested in other countries, decreasing local firms purchasing power and therefore declining industrialization in the region. These findings reveal that FDI outflow did not promote industrialization and could indicate the dearth of the sector’s mutual dependency on the expansion mechanism. Regarding the above, the authors assumed a negative relationship between FDI outflow and industrialization. The results followed the hypothesis. Hence, the second hypothesis is accepted. It is possible that inadequate SSA government support and a lack of a conducive atmosphere to encourage domestic investment in the industry sector are to blame for the inability of FDI outflow to help industrialization. To begin, the role of government in industrialization was marginal at best. It is possible that the causative factors’ lack of variation led to this outcome.

Nevertheless, studies by authors like Joshua et al. (2022) and Agbloyor et al. (2016) suggests that some African countries have taken industrialization-unfriendly policies, including monopolistic constraints like exclusively exploring liberties, exclusively contracts with suppliers, and domestic market restrictions. In addition, the government’s inability to create an appropriate supportive atmosphere is hindering the growth of private industry, especially in the manufacturing industry. This is evidenced by the World Bank’s publication of commercial circumstances and oversight parameters for nations worldwide, which show that African nations perform poorly.

The combined results of the FE and RE estimations point to a positive and significant link between trade openness, FDII, and industrialization in SSA. Based on these findings, the hypothesized favorable relationship between FDI inflow and industrialization is moderated by trade openness. Therefore, hypothesis three was accepted. This conclusion aligns with past studies suggesting that trade liberalization as a proportion of GDP has significantly affected the industrialization of economies (Appiah et al., 2023). When trade opens up, industries with higher added value generate a more significant percentage of GDP. Therefore, compared to the initial industry argument, commerce helps modernize emerging economies. Initially, trade liberalization facilitates cross-border investments, thereby boosting the outflow of FDI and slowing the pace of industrialization in developing nations. Hence, we accept the null hypothesis that FDI and TOP are positively correlated. This finding is consistent with Adom & Amuakwa-Mensah (2016), who found the impact of TOP on FDI and industrialization.

Furthermore, industrialization in SSA is hampered by the fact that native companies are forced to invest in foreign economies due to trade openness. As a result of increased FDI outflow, investment capital may be redirected away from domestic economies and toward those of other countries (Nnadozie et al., 2021). This might lead to a de-industrialization spiral. The findings from the study disagree with the assumption that FDI outflow and industrialization have a favorable association moderated by trade openness. Hence, the fourth hypothesis has been rejected. Consistent with the results of Appiah et al. (2023), which demonstrate that trade has not promoted industrialization in SSA.

In addition, it is reasonable to infer from the results that FDI inflow is crucial for urbanization. Foreign direct investment inflow increases urbanization and productivity in an industry. Foreign direct investment inflow helps countries better organize the funds and expertise they need to progress industrialization. The evidence-based results (Adejumo & Asongu, 2020) on FDI inflow’s implications for urbanization and industrialization are congruent. However, according to the study’s findings, there was no discernible impact of FDI outflow on urbanization. The employment outlook in SSA’s industrial sectors remains unchanged due to investments in other international economies. No new jobs will be created in SSA sectors due to an increase in FDI outflow.

The findings show that the effect of FDI outflow on urbanization in SSA is significantly affected by trade openness, primarily by SSA. Trade liberalization negatively impacts urbanization due to FDI outflows, but FDI inflows positively impact industry urbanization when SSA economies attract investments abroad. The primary findings suggest that freer trade promotes FDI inflow, boosting industrialization and urbanization. This means that people are being encouraged to seek careers in manufacturing. Similarly, Mamba et al. (2020) reported the same result as the study’s multiple regression analysis reveals that employment significantly boosts output.

Conclusion and Policy Implications

Conclusion

Regardless of the benefit of FDI on industrialization in SSA countries, there needs to be more study to explore its importance in the national context with the moderating role of trade openness. Therefore, the study examines the effect of FDI on industrialization and the moderating role of trade openness in SSA countries. The empirical analysis employed secondary data that was taken from the Word Development Indicator database for the SSA nations. The study selected the years from 2000 to 2022 for the empirical investigation. The analysis in the paper also used stepwise regression with the FE as the primary estimator and RE robustness estimators. The findings demonstrate that FDI inflow revealed a favorable and significant relationship with industrialization. However, FDI outflows revealed a negative and insignificant association with the industrialization of the countries in SSA. Also, the moderating role of TOP revealed a positive and significant link between FDII and the industrialization of countries in SSA. Trade liberalization was found to have a significant bearing on FDI inflows and industrialization. Considering the viewpoint of SSA countries, trade liberation is particularly driven by the importation of technologies and inputs for production. Lastly, the impact of the moderating role of TOP on FDIO and industrialization is positive but insignificant.

SSA’s trading practice transfers assets and investments to foreign economies rather than fostering value addition, which is now a must for industrialization. Also, the SSA region’s dependence on exporting unprocessed materials such as gold and other minerals, coffee, and skins explains the inverse connection between trade openness and industrialization. However, SSA relies on importing consumer products such as flour, vegetable oil, and clothing, which have a more negligible impact on the country’s ability to expand its manufacturing sector. This is why increased trade openness hinders industrialization. Therefore, this study fills the gab in literature on the impact of FDI on industrialization the moderating role trade openness in the context of SSA countries.

The study employed secondary data for both the independent, independent, control and moderating variables from the World Development Indicators database which was used for the empirical analysis. The study then selected the years from 2000 to 2022 for the empirical analysis. The authors then employed Fixed Effect and Random Effect estimators which was used for the empirical investigation. The results reveal that FDII has a positive and statistically significant relationship with industrialization while FDIO has a negative and insignificant link with industrialization. Moreover, the moderating results reveals that with the inclusion of TOP, FDII and industrialization will increase positively in SSA countries while FDIO will decrease.

Based on the results it is recommended that to increase industrialization in SSA countries government all around SSA should implement and promotes policies to increase foreign direct investment in the respective countries. Moreover, it is suggested that trade restriction, embargo, and tariffs place on imported goods and service into Africa should decrease in order to increase invention and technology thereby increasing industrialization. Also, government in SSA countries should support and promote local industries in terms of capital accumulation and investment in order to attract more foreign investor to invest in local companies in Africa to increase industrialization. Lastly, the tax placed on investors should decrease in Africa in order to promote FDI and industrialization.

Policy Implications

Global development of FDI present a novel insight for countries to prioritize the need for industrialization to increase economic growth and development. The growth of an economy is basically based on factors like industrialization, FDI, and urbanization. Therefore, to effectively develop a country, there must be a study to propose measures and policies to guide the action of policy makers for the attainment of the country’s goal. In terms of FDI and industrialization moderating by trade openness our results depict the following policy implication in SSA.

Firstly, SSA government should restructure their policies and regulation on FDI to increase industrialization and boost economic growth. Policies on import and export should be strengthen and restructure to control inflows and outflows of goods and service and to promote industrialization. Also, strict measures should be imposed on foreign direct investment outflows in order to control gross domestic product and increase industrialization in SSA countries.

Since FDII reveals a positive impact on industrialization, government in SSA should imposed policies that will bind foreign companies entering Africa to incorporate or merge with local companies to increase the capacity of the local companies in terms of technology, capital, profit, expert, experience in produce so as to increase industrialization.

Furthermore, government in SSA should develop a policy to support infant industries to increase in local production and to promote industrialization. Tax on local industries should be reduce in order to encourage local industry production. Policy makers must institute measure and policies to reduce tax, reform local and corporate tax which will promote industrialization and urbanization.

Finally, policies on trade openness should be strengthen and reorganized to control the aspect of industrialization and FDI. Since most countries are prioritizing free trade, there must be effective measure to control open trade and increase industrialization.

Limitations and Future Research Directions

While the study provides novel insights into the relationship between FDI, trade openness, and industrialization in SSA, several limitations should be acknowledged. First, the reliance on secondary data from the WDI database may not fully capture all aspects of industrialization, such as informal economic activities or localized industrial practices. Additionally, some countries within SSA may have incomplete or inconsistent data, which could potentially introduce bias into the results. To address these data limitations, future studies could incorporate alternative sources, such as firm-level surveys or industry-specific reports, which would capture sector-specific variations and informal economies that are critical to understanding industrial growth in SSA. Furthermore, integrating qualitative indicators, such as governance quality, business climate assessments, and innovation indices, would enhance the comprehensiveness of future analyses and provide deeper insights into the dynamics of industrialization.

Another limitation is the temporal scope, which covers only the period from 2000 to 2022, potentially missing important long-term trends or shifts in industrialization patterns that may have occurred prior to 2000. Extending the study’s timeframe would provide a clearer picture of the long-term effects of FDI and trade openness on industrialization. Including earlier data would also allow researchers to capture historical shifts and better understand the factors that have shaped the industrial landscape in SSA. Additionally, future research could explore sector-specific impacts of FDI on industries such as manufacturing, technology, or agriculture, as FDI often influences different sectors in distinct ways. By focusing on sectoral dynamics, researchers could offer more targeted policy recommendations for industrial growth, tailored to the needs of specific industries within SSA.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.