Abstract

The impact of fintech on the performance of traditional banking remains contentious, with its underlying economic mechanisms still an urgent research priority. Utilizing panel data from 2010 to 2022, this study investigates the dynamic relationship between fintech development and traditional banking performance. The results demonstrate that emerging digital financial sectors, as early adopters of fintech, generate positive externalities on traditional banking performance through business model innovation. Conversely, traditional banks’ internal fintech adoption exhibits a U-shaped relationship with their performance. These findings comprehensively reveal the dynamic interplay between fintech and commercial banking evolution, offering critical insights for informing development strategies for digital finance.

Plain Language Summary

“How FinTech is Changing Traditional Banks: A Surprising Story” We know that technology like mobile payments and online lending (FinTech) is changing banking, but is this good or bad for traditional banks? This question is hotly debated, and we need clearer answers. Our study looked at real data from 2010–2022 to see how FinTech affects banks. Here’s what we found: New FinTech players HELP banks: Surprisingly, when digital finance companies (like online lenders or payment apps) grow, they actually boost traditional banks’ performance. How? By forcing banks to innovate and try new business ideas. Banks’ own tech journey is a ROLLER COASTER: When banks invest in FinTech themselves, it’s not smooth sailing. At first, their performance often dips. But if they stick with it, things eventually turn around and improve significantly. (Think: “short-term pain, long-term gain”). Why this matters: This research shows the complex dance between new tech and old banks. It helps banks, startups, and regulators make smarter decisions about the future of finance in the digital age.

Introduction

The banking sector serves as the cornerstone of China’s financial industry, a vital component of the national economic lifeline and a key pillar for building a financially robust nation. Under the new economic normal, the industry has shed its halo of high growth, wide interest spreads, and substantial profits, gradually entering a new era of transformational development. Such transformation requires the propulsion of New Quality Productive Forces, meaning a new form of productivity that breaks away from traditional economic growth models, with the digital industry constituting its primary characteristic and core element (M. Zhou et al., 2024). FinTech (as defined by Huang and Huang in 2018, with terms such as digital finance, internet finance, tech finance, and financial technology being essentially synonymous; this paper does not distinguish between these terms) emerges as the most dynamic and disruptive force driving banking transformation.

It has fundamentally altered—even upended—traditional banking models and developmental paradigms, reshaping the entire financial ecosystem. Taking Ant Group as an example, its rapid business expansion is evidenced by its 2023 Sustainability Report, which reveals that it provided inclusive financial services to 87 million micro and small enterprises in 2023. The Peking University Digital Inclusive Finance Index, calculated based on its operational data, surged from a provincial average composite score of 40.00 in 2011 to 379.44 in 2022, marking a nearly tenfold increase. Fintech equips traditional banks with potent tools for upgrading and transformation. By seizing this opportunity to integrate neo-factor productivity, the banking sector can achieve new leaps in operational efficiency and cost reduction (You et al., 2023).

However, the impact or even disruption caused by FinTech does not guarantee a smooth transformation for traditional banking. Technological innovation does not always unleash the driving force of new quality productive forces (Jiang, 2024), as it relies on “creative transformation” to achieve an “orderly retreat” (Fang & Yang, 2024). FinTech was first adopted by emerging digital financial sectors entities such as Ant Financial, which directly competed with traditional banks.

In the payment sector, third-party platforms like Alipay and WeChat Pay rapidly captured significant market share with their convenient payment experiences and massive user bases. This was followed by intense competition in liability-side businesses, where FinTech companies launched products such as Yu’e Bao and Lingqiantong, attracting users with high liquidity and relatively higher returns, leading to the erosion of traditional banks’ deposits and wealth management products. On the asset side, emerging digital financial sectors players leveraged big data to reduce information asymmetry, enabling precise and rapid credit assessments and expanding the boundaries of credit services.

The comprehensive competition has directly contributed to the narrowing of net interest margins for traditional banks, compressing profit margins and posing significant challenges to their sustainability. Nevertheless, traditional commercial banks are also active adopters of new quality productive forces. The digital transformation of traditional banks requires substantial investment. According to the 2024 China FinTech Innovation Development Insight Report by Analysys Qianfan, financial institutions’ technology investment grew from RMB 173 billion in 2019 to RMB 275.8 billion in 2023. On the other hand, FinTech also presents new opportunities. Most commercial banks, with their state-owned enterprise backgrounds, face relatively few barriers in communicating with public sectors. By leveraging FinTech, they have facilitated information exchange and sharing with various departments (e.g., tax bureaus, industry and commerce bureaus, social security bureaus, and customs), breaking down data silos and fragmented information systems, enabling more precise customer marketing, business expansion, and performance growth.

Academic conclusions on the impact of FinTech on traditional banking performance are not uniform. Some scholars argue that FinTech directly competes with traditional banks, creating a crowding-out effect or negative impact (P. Guo & Shen, 2019; Saklain, 2024; J. Wang, 2015; You et al., 2023). Others believe FinTech has a positive effect on traditional banks’ performance (L. H. Guo & Zhu, 2021; J. J. Li & Jiang, 2021; M. F. Liu & Jiang, 2020; X. H. Wang & Zhao, 2023; X. L. Xie & Wang, 2022). The key reason for this disagreement lies in data limitations: (a) short research time spans, as the initial year of digital transformation for commercial banks was 2015 (J. J. Li & Jiang, 2021), and existing studies often end in 2016 or 2018, while the effects of technological application may be lagged; (b) no consensus on how to measure FinTech levels, such as whether to use the Peking University Digital Financial Inclusion Index, commercial banks’ business data, or investment data; (c) inconsistent research objects, as existing studies are limited to national branches of a single commercial bank, short-term tax survey data, or listed banks, with regional data for all banks nationwide being challenging to obtain; and (d) the relationship between FinTech and traditional banking performance may not be linear.

Performance is crucial for the sustainable development of traditional banking. Given practical observations and academic debates, it is necessary to focus on banking performance to explore the relationship between FinTech, as a new quality productive force, and traditional banking, and to analyze whether the development of new quality productive forces and traditional banking aligns with the principle of “before disruption” and the characteristic of “seeking progress while maintaining stability.”

This paper examines the relationship between FinTech, as a new quality productive force, and the performance development of traditional commercial banks from the perspective of new quality productive forces, and clarifies the “construction-disruption” relationship between new quality productive forces and traditional commercial banks. Essentially, FinTech is an optional tool, while banks are rational profit-maximizing entities in the financial market. By analyzing the economic mechanisms behind FinTech and the performance development of traditional banking, this paper addresses two questions: (a) What effects does FinTech, as an external technological force, have on the performance of traditional banking? (b) How does the digital transformation process of traditional commercial banks impact their development? The aim is to provide references for policy-making to achieve “creative transformation” and integrate new quality productive forces in traditional banking.

Using data from the China Financial Yearbook (2010–2022), commercial banks’ annual reports, the Peking University Digital Financial Inclusion Index, and the Peking University China Commercial Bank Digital Transformation Index, this paper constructs an analytical framework based on the rise of FinTech as a new quality productive force, its technological spillover effects, and the integration efforts of traditional commercial banks. It investigates the dynamic impact of new quality productive forces on the performance of traditional banking.

The innovations of this study are reflected in the following three aspects: (a) Theoretical Perspective Innovation: This research is the first to systematically reveal the interaction dynamics between FinTech development in emerging financial sectors and the digital transformation of traditional banking, grounded in the technology diffusion theory. (b) Data Methodology Innovation: We employ authoritative province-level banking statistics for empirical analysis. Unlike prior literature that predominantly used banks’ headquarters locations as proxies for their operational provinces (geographic misidentification), our data construction better aligns with the reality of nationwide bank operations, significantly mitigating spatial measurement bias. (c) Conclusion Innovation: Our empirical findings resolve the longstanding debate in existing literature regarding FinTech’s positive/negative impact on traditional banking performance. We are the first to identify a nonlinear U-shaped relationship between them, providing new empirical evidence to reconcile theoretical ambiguities.

Literature Review

Fintech is an emerging tool in the financial field. The development of internet finance in China has not been smooth. For example, in 2018, several well-known P2P platforms successively collapsed, triggering hesitation and cautious observation among scholars and traditional commercial banks regarding the application of fintech. Currently, there is no consensus in academia on the relationship between fintech and the performance of traditional banking. The key related issues mainly include the measurement of fintech, the positive and negative impacts of fintech on the performance of traditional banking, and the underlying mechanisms.

Measuring the Development Level of FinTech

In the Chinese context, there are two main approaches to measuring “FinTech”: the first is the Peking University Digital Financial Inclusion Index, and the second involves constructing indicator systems based on banks’ FinTech business activities or technology investment data. The Peking University Digital Financial Inclusion Index, developed by F. Guo & Wang (2020), is a comprehensive index based on Ant Group’s original business data, used to measure regional FinTech levels. As a pioneer and the largest FinTech company in China, Ant Group’s FinTech level is representative. Many scholars have applied this index to FinTech-related research (Q. Z. Fu & Huang, 2018; G. Wang & Chen, 2022; X. L. Xie et al., 2018; Yi & Zhou, 2018; You et al., 2023; X. Zhang et al., 2019). Alternatively, some scholars use banks’ FinTech business activities or investment data to construct indicator systems for measuring development levels (L. H. Guo & Zhu, 2021; J. J. Li & Jiang, 2021; M. F. Liu & Jiang, 2020; X. L. Xie & Wang, 2022).

FinTech Adoption, Innovation Diffusion, and Bank Digital Transformation

The adoption of FinTech, the diffusion of technological innovation in the banking industry, and changes in bank performance are closely interrelated. Existing research indicates that the primary motivations for banks to adopt FinTech are to enhance operational efficiency, expand customer service channels, and respond to competition from emerging FinTech firms (Allen et al., 2023). Technical implementation models include embedding into ecosystems through open APIs, deploying AI-driven intelligent assistants to improve customer trust and retention, and leveraging cloud computing to build agile core systems (Cheng & Qu, 2020). Practical cases in Chinese banking include Guizhou Bank’s use of large-model technology to develop an intelligent customer service system, significantly improving the efficiency of internal data queries and business processing, and Chongqing Bank’s digital transformation system, which greatly reduced the approval cycle for inclusive loans (Safiullah & Paramati, 2024). The Diffusion of Innovations theory (Rogers, 2003) provides a framework for understanding the technology adoption process, and its S-curve pattern is notably evident in the banking sector. The diffusion pathway in China’s banking industry shows a trend of spreading from large banks to small and medium-sized banks, and from retail banking to corporate banking, with the effects of diffusion moderated by factors such as bank size, type, and corporate governance levels (Li, 2025). Furthermore, studies emphasize that FinTech and traditional banks do not have a simple substitution relationship but rather exhibit significant complementarity (Adbi & Natarajan, 2023), particularly in the field of inclusive finance, where the presence of bank accounts can substantially enhance the positive impact of FinTech tools on the savings behavior of disadvantaged groups. Ultimately, the essence of banks’ digital transformation is a systematic change encompassing strategy, organization, technology, and operations (Christensen, 1997), and this transformation typically requires integrated efforts in top-level design, organizational agility, data ecosystem construction, and risk management system upgrades (Goel & Kashiramka, 2025).

Research on the Impact of FinTech on Traditional Banking Performance

The financial industry operates in a relatively homogeneous manner. As an emerging digital financial sectors, FinTech inherently competes with and “crowds out” traditional banking businesses. Scholars such as J. Wang (2015), Man (2016), J. Chen and Wang (2016), and P. Guo and Shen (2019) argue that FinTech diverts deposits and wealth management sources, significantly impacting banks’ liability-side businesses. Lu Xiaoming (2014) points out that online lending platforms, with their low interest rates, low thresholds, and fast processing, are more attractive to borrowers, thereby constraining banks’ loan businesses. These constraints directly affect banking performance. You et al. (2023), using county-level tax data from 2011 to 2016, found that FinTech increases banks’ operating costs and management expenses, leading to declining performance and stalled development. X. L. Xie and Wang (2022), based on data from 2011 to 2018, empirically demonstrated that the development of emerging digital financial sectorsnegatively impacts banking performance, and banks’ own digital transformation does not directly enhance performance. Saklain (2024) found that although FinTech in Australia does not weaken banks’ market power, it significantly increases their sensitivity to systemic risk.

However, some scholars have reached opposite conclusions. Z. L. Liu (2016) and X. H. Wang and Zhao (2023) believe that FinTech encourages traditional banks to actively transform, creating a positive “catfish effect” that promotes performance growth. Cappa et al. (2021) and Liang et al. (2022) noted that the application of FinTech enhances banks’ competitiveness. J. J. Li and Jiang, (2021) and L. H. Guo and Zhu (2021), using four years of data from a single national bank, concluded that FinTech overcomes physical branch limitations, reduces information asymmetry, expands potential customer bases, and benefits performance growth. M. F. Liu and Jiang (2020), analyzing data from 2008 to 2017, found that while FinTech hinders cost efficiency, it significantly improves banks’ profitability. Focusing on the banking sectors in Europe and the United States, Bian et al. (2023) demonstrated that FinTech adoption significantly enhanced the operational efficiency and market value of European banks. Meanwhile, regarding the United States, Karim and Lucey (2024) point out that a complex ecosystem integrating tech giants, FinTech firms, and traditional banks is evolving there.

Existing research exhibits significant divergences regarding the impact of FinTech on the performance of traditional banking, which can be systematically attributed to the following four reasons: First, there is a lack of uniformity in the measurement standards for FinTech development levels, particularly regarding a clear definition of the conceptual distinctions and applicable scopes between the two mainstream indicators—the Peking University Digital Financial Inclusion Index and the internal FinTech indicator system within the banking sector. Second, the research time coverage is limited, with most studies ending in 2016 or 2018, failing to adequately capture the lagged effects brought about by bank digital transformation (which began in 2015). Third, the selection of research subjects varies significantly due to data availability constraints; existing literature often relies on nationwide branches of a single bank, short-term tax survey data, or listed bank samples, lacking more representative industry-wide regional-level evidence. Fourth, most existing studies implicitly assume a linear relationship and have not examined the potential non-linear relationship between FinTech and banking performance.

In response to the gaps and inconsistencies in the existing literature, this study, building on prior theoretical foundations, explicitly proposes to regard FinTech as an New Quality Productive Forces driving the overall transformation of the financial industry and aims to achieve close integration between the literature review and subsequent theoretical hypotheses. This paper constructs a logically progressive research framework along three dimensions: first, analyzing the direct impact of FinTech application by emerging digital financial sectors entities on the performance of traditional banks; next, examining the interaction and spillover mechanisms of technology application between emerging digital financial sectors and traditional banking; and finally, exploring the internal pathways through which traditional banks’ own application of FinTech affects their operational performance.

Theoretical Analysis and Hypotheses

The Impact of Emerging Digital Financial Sectors on Traditional Banking

Fintech, as a disruptive innovation (Christensen, 1997), was initially driven and popularized by emerging digital financial sectors. In the market structure, traditional banks and these emerging entities play the roles of “incumbents” and “entrants,” respectively. According to the theory of disruptive innovation, incumbents tend to focus on sustaining innovations, relying on existing resources and current customer demands for gradual optimization, while entrants often leverage breakthrough technologies or business models to enter from low-end or niche markets, gradually reshaping the industry landscape (X. Xu et al., 2023). In China, the rise of digital finance can be traced back to the establishment of Alipay’s account system in 2004 (Huang & Huang, 2018). Key drivers such as Ant Group and Tencent Financial Technology did not originate from within the traditional banking system but entered the market as external forces (You et al., 2023). It is worth noting that the impact of fintech on the banking industry is not merely a substitution of services but also a structural and ecological symbiosis (Karim & Lucey, 2024).

Specifically, this impact is first reflected in the payment and deposit business sectors. Emerging payment institutions, with their efficient, convenient, and small-value high-frequency service features, quickly gained an advantage in the long-tail market, significantly accelerating financial disintermediation. According to data released by the People’s Bank of China in the second quarter of 2024, non-bank payment institutions processed 343.5 billion online payment transactions, 4.56 times the number of electronic payment transactions processed by banks, indicating a significant substitution effect in small-value retail payment scenarios. The shift in payment channels further led to structural changes in the form of funds: digital payments significantly reduced the demand for cash, with the ratio of M0 to M2 decreasing from 6.15% in 2010 to 3.60% in 2023. Although most non-bank payment funds still return to the banking system in the form of deposits (e.g., through reserve accounts and money market funds), their cost structure has undergone significant changes. Money market fund products, represented by Yu’e Bao, have transformed traditional demand deposits into liability sources requiring higher returns, forcing commercial banks to launch similar high-cost wealth management products to maintain competitiveness, thereby systematically raising the overall liability costs of the banking industry.

From the perspective of lending business, fintech did not directly enter the mainstream core credit market of traditional banks but first served financially disadvantaged groups (e.g., small and micro enterprises, unsecured borrowers), therebycreating new market spaces. These characteristics are also consistent with the theory of disruptive innovation. Ant Group’s early credit services primarily targeted merchants on the Taobao platform—customers who were excluded from mainstream services by traditional banks due to their small size, high risk, and lack of collateral. Therefore, in terms of lending customer base, fintech and traditional banks exhibit a complementary rather than purely competitive relationship. More importantly, lending businesses in emerging sectors often adopt a joint loan model in collaboration with traditional financial institutions. According to data disclosed by the China Banking and Insurance Regulatory Commission, over 90% of the funds for such businesses come from the banking industry. This indicates that fintech has, to some extent, expanded the asset scale of the banking industry, particularly enhancing the capacity for inclusive financial services (Huang & Huang, 2018).

In summary, the rise of emerging digital finance sectors has promoted the growth of deposit and loan business scales in the traditional banking industry. Moreover, the impact and changes brought by emerging digital finance sectors to deposits and loans are actively chosen by banks rather than passively accepted. Each profit-maximizing enterprise opts to expand businesses that align with its profit objectives. Therefore, as traditional banks choose to increase their deposit and loan businesses, their operating profits should also rise. Based on this, this paper concludes that the influence of emerging digital finance sectors on the performance of traditional banking is positive, promoting its development. The following hypothesis is proposed:

Technological Spillover From Emerging Digital Financial Sectors to Traditional Commercial Banks

The banking industry exhibits a high degree of homogeneity in terms of products and services. For consumers, the core businesses of various banks—such as deposits, loans, wealth management, payment settlement, and foreign exchange services—show minimal differences in functionality and features. This makes it difficult for consumers to develop strong brand preferences, leading to significantly higher price elasticity of demand. According to Romer’s (1990) endogenous growth theory on knowledge externalities, when consumers exhibit high price elasticity (i.e., high substitutability) toward a knowledge-based product, that knowledge tends to possess strong positive externalities. Since the financial products offered by the banking industry (including both traditional banks and emerging digital financial sectors) are inherently highly substitutable, the underlying knowledge and technologies also demonstrate significant externality characteristics. Therefore, when the application of fintech in emerging digital financial sectors generates positive demonstration effects, the resulting technological spillover effects are likely to be particularly pronounced (Jaffe, 1986).

As a new technological paradigm, fintech was initially promoted and popularized by emerging digital financial sectors. The origin of digital finance in China can be traced back to the introduction of Alipay’s account system in 2004 (Huang & Huang, 2018). Subsequently, by 2005, internet-based financial models such as peer-to-peer (P2P) lending rapidly emerged and experienced explosive growth until 2018, when industry risks became apparent, leading to the exit of a large number of platforms (He, 2020). In recent years, fintech supported by integrated technologies such as big data, cloud computing, blockchain, and the Internet of Things has entered a phase of stable development. Traditional banks’ attitudes toward fintech have evolved from initial hesitation and resistance to cautious observation, and finally to active embrace and adoption (You, 2023). This shift is closely related to the demonstration effect of financial technology applications on performance.

Based on Jaffe’s (1986) knowledge spillover model, the high homogeneity and knowledge mobility in financial services enable the experience and technologies accumulated by emerging digital financial sectors in fintech applications to significantly enhance traditional banks’ awareness and willingness to adopt related technologies through demonstration effects, talent mobility, and competitive imitation. After observing the positive performance of emerging entrants, traditional banks quickly engage in technological learning and integration, thereby improving their own fintech capabilities. Accordingly, the following hypothesis is proposed:

Digital Transformation and Development of Traditional Commercial Banks

In the process of advancing digital transformation, traditional commercial banks need to invest substantial human resources, hardware equipment, and information technology systems to reorganize and upgrade existing factors of production. In the initial stages of adopting digital technologies, particularly in internet-related areas, they often face high upfront fixed costs. These costs include system design, model development and training, promotion, and multiple rounds of debugging (P. Xie, 2015). At the same time, during the early phase of transformation, the contribution of new quality productivity to bank performance is not yet evident, and the digital user base is still under development. As a result, it is difficult to achieve significant commercial value or revenue growth at this stage. The combination of delayed returns and high costs means that the integration of fintech may have a certain negative impact on bank performance in the short term.

As traditional commercial banks gradually deepen their application of fintech and surpass a critical threshold, the diminishing marginal costs of digital factors and the increasing returns to scale begin to take effect (Rogers, 2003). Fintech not only enhances banks’ information processing and operational efficiency, effectively reducing unit operating costs, but also strengthens profitability and market competitiveness by expanding into new business areas such as inclusive finance (P. Guo & Shen, 2015). Based on the S-curve theory of technology adoption, the impact of technological performance often exhibits nonlinear evolution—transitioning from an initial investment phase to a mature returns phase, with a critical inflection point in between. In summary, the following hypothesis is proposed:

Research Design

Data Sources

FinTech Level of Emerging Digital Financial Sectors

The Peking University Digital Financial Inclusion Index (F. Guo & Wang, 2020) is adopted as a measure. This index is selected as a proxy for the FinTech level of emerging digital financial sectors based on the following two reasons:

On the one hand, the index was jointly compiled by the Peking University Digital Finance Research Center and Ant Group, constructed based on actual transaction data from various FinTech businesses of Ant Group across China. As the most representative emerging digital financial sectors enterprise in China, Ant Group operates in multiple areas such as payments, credit, and wealth management, extensively applying cutting-edge technologies like big data, artificial intelligence, and cloud computing in real business scenarios. Therefore, the index, built on real business data from this enterprise, effectively reflects the depth and breadth of practical applications of digital financial technologies. It objectively captures the entire process of translating FinTech concepts into productive forces, demonstrating strong timeliness, representativeness, and measurement validity. This study utilizes provincial-level data of this index from 2011 to 2022, facilitating the capture of the dynamic evolution of digital financial technology at a macro-regional level.

On the other hand, due to concerns such as business confidentiality and data accessibility, operational data from other emerging FinTech enterprises are generally not publicly available, and systematic, continuous, and comparable panel data at the regional level are particularly scarce. Among existing publicly available indicators, the Peking University Digital Financial Inclusion Index is one of the very few high-quality data sources that comprehensively and objectively reflect the development level of digital financial technology in China. As such, it has become a widely adopted authoritative indicator in academic research.

Regional Banking Data

Provincial-level banking economic data are manually compiled from the China Financial Statistical Yearbook. Missing values are supplemented by querying the official website of the National Financial Regulatory Administration, and a few remaining missing values are filled using interpolation. This data is derived from official statistics of local People’s Bank of China branches. It should be noted that internet finance products such as Ant Group’s “Ant Credit Pay,” Tencent’s “Weilidai,” and JD.com’s “Jintiao” are not included in the People’s Bank of China’s statistics (Z. Xu, 2018). The yearbook data is considered a reliable source for measuring the performance of traditional banks.

The data processing procedure is as follows: First, we located the textual sections on “Financial Industry Development” for each provincial-level region, from which we extracted data such as total banking assets, total liabilities, and net profit. These data were then organized into panel data by region and year. Taking the 2020 yearbook (already uploaded as an attachment) as an example, relevant indicator descriptions are provided on page 102. Based on these, the required data were extracted and compiled year-by-year and region-by-region to form the dataset used in this study.

Digital Transformation of Commercial Banks

The China Commercial Bank Digital Transformation Index, compiled by Peking University (X. L. Xie & Wang, 2022), is used. This index is calculated based on data from 246 commercial banks that have publicly available annual reports for at least three years between 2010 and 2021, combined with external data such as patent information. It evaluates three dimensions: strategic digitalization, business digitalization, and management digitalization. The sample covers large state-owned commercial banks, joint-stock commercial banks, city commercial banks, rural commercial banks, foreign banks, and private banks, accounting for over 96% of the total assets of China’s commercial banks. The sample is highly representative and comprehensive.

Other Data

Additional data are sourced from individual commercial banks’ publicly available annual reports, the Wind database, and provincial Statistical Yearbooks. The marketization index is calculated using the method proposed by Fan et al. (2003).

Methodology and Variable Selection

Impact of Emerging Digital Financial Sectors on Traditional Banking Performance

This paper constructs a panel regression model to examine the impact of emerging digital financial sectors on the performance of traditional banking. The model is as follows:

In the model, the subscript i represents the region, and t represents the time period. The dependent variable

Technology Spillovers From the Use of Fintech in the Emerging Digital Financial Sectors Industry to the Traditional Banking Sector

The FinTech level of emerging digital financial sectorsand the degree of digital transformation in traditional banking are not directly causally related. Traditional commercial banks do not immediately “take action” in response to the improvement in FinTech levels of emerging digital financial sectors. For example, during the phases following the launch of Alipay in 2004 and the rise of internet finance in 2005, traditional commercial banks remained in a state of “hesitation and observation.” It is only after emerging digital financial sectorsdemonstrate the positive effects of integrating FinTech as a new quality productive force, aligning with the “construction before disruption” characteristic, that significant technological spillover occurs. Therefore, this paper argues that the positive impact of FinTech on banking performance is a causal relationship, while the technological spillover from the development of FinTech in emerging digital financial sectorsto traditional banking is a correlational relationship. This paper uses correlation coefficients to analyze the trend between the two.

Consistent with the above, the digital transformation of traditional commercial banks is measured using the annual data of the Peking University China Commercial Bank Digital Transformation Index. The FinTech level of emerging digital financial sectorsis proxied by the Peking University Digital Financial Inclusion Index. Since the Peking University Digital Financial Inclusion Index does not provide annual data, this paper aggregates the provincial-level indices to calculate a national index. Given that the index is based on per capita actual business transactions in each region, aggregating provincial data to form a national index is both reasonable and reliable.

Digital Transformation and Development of Traditional Banking

Based on theoretical analysis, the impact of digital transformation on the performance of traditional commercial banks follows a “U-shaped” relationship, initially decreasing and then increasing. The following model is constructed to examine the impact of digital transformation on bank performance:

Where, the subscript j represents the individual commercial bank, and t represents the year. The dependent variable

Descriptive Statistical Analysis of Variables

Variables Related to the Impact of Emerging Digital Financial Sectors on Traditional Banking Performance

Descriptive statistics for the variables related to the impact of emerging digital financial sectors on traditional banking performance are presented in Table 1. The core indicator of profitability is the return on assets (ROA), and the core explanatory variable is the Peking University Digital Financial Inclusion Index.

Descriptive Statistical Analysis of Variables Related to the Impact of Emerging Digital Financial Sectors.

Variables Related to Technological Spillover From the Integration of FinTech in Emerging Digital Financial Sectors to Traditional Banking

When analyzing the technology spillover effects of fintech adoption by emerging digital financial sectors on traditional banking, this study employs the Peking University Digital Inclusive Finance Index (National Aggregate) and the China Commercial Bank Digital Transformation Index (National Aggregate, lagged by one period) as proxy variables. The Peking University Digital Inclusive Finance Index (2011–2022) is aggregated from provincial-level data, while the China Commercial Bank Digital Transformation Index (lagged by one period) spans 2011 to 2022. Descriptive statistics are presented in Table 2.

Descriptive Statistical Analysis of Variables Related to Technological Spillover From Emerging Digital Financial Sectors to Traditional Banking.

Variables Related to Digital Transformation and Performance Development of Traditional Banking

The descriptive statistics for the variables used to examine the impact of digital transformation on the performance development of traditional banking are presented in Table 3.

Descriptive Statistical Analysis of Variables Related to Digital Transformation of Traditional Commercial Banks.

Empirical Results and Analysis

FinTech Impact on Commercial Banking

Using a dual fixed-effects model, Table 4 demonstrates emerging digital financial sectors (reflecting new quality productivity) significantly increased ROA (β = .0119*** without controls). Coefficients remain significant at 1% with controls (β = .0119***), demonstrating robustness. This confirms the construction effect where digital finance enhances traditional banks’ profitability.

Baseline Regression Results of the Impact of Emerging Digital Financial Sectors on Traditional Banking Performance.

Note. Standard errors are reported in parentheses. Standard errors are clustered at the provincial level.

, * denote significance at 1%, 10% levels.

FinTech Spillovers and Bank Digital Transformation

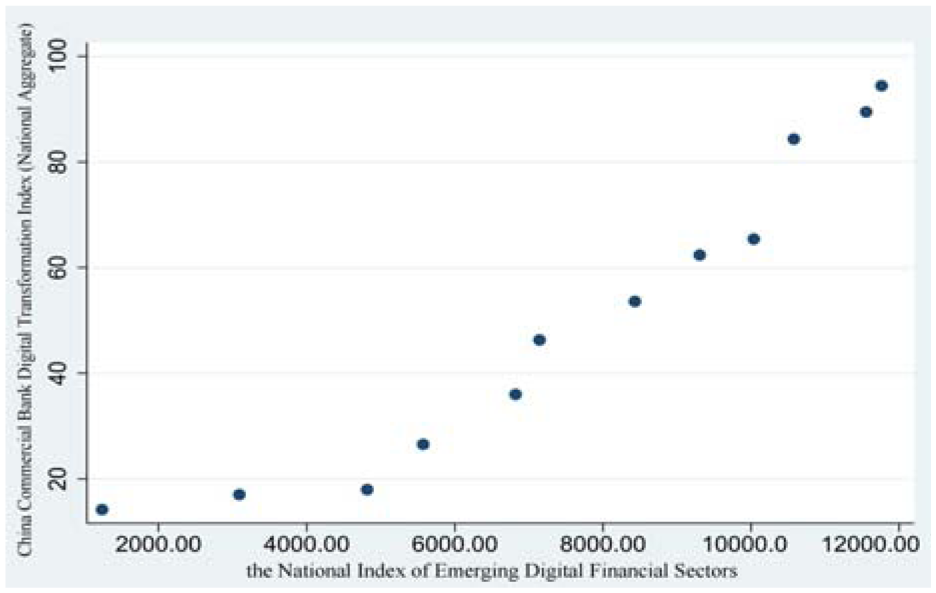

Using a one-period lag of the China Commercial Bank Digital Transformation Index to account for learning effects and delayed impacts, analysis of 2011 to 2022 data reveals a strong correlation (r = .9591) with emerging digital financial sectors indices. Despite data limitations, the high correlation persists.

Figure 1’s scatter plot visually confirms this relationship between emerging digital financial sectors indices and lagged bank transformation indices.

Correlation analysis between the National Index of emerging digital financial sectors and the Lagged National Index of China’s Commercial Banks (Lagged by one period).

Digital Transformation and Performance in Traditional Commercial Banking

Consistent with Hypothesis 3, the integration of new quality productivity in traditional commercial banks exhibits a U-shaped relationship with performance. Empirical results confirm negative first-order and positive quadratic coefficients for the core explanatory variable. Data were winsorized at the 1% level to address outliers. As shown in Table 5, Columns (1) to (2) present ROA results without/with controls, both demonstrating statistically significant U-shaped patterns. Similar patterns hold for ROE analyses.

Benchmark Regression Results of Digital Transformation and Performance in Traditional Commercial Banks.

Note. Standard errors in parentheses. Standard errors are clustered at the commercial bank level.

, **, and * denote significance at 1%, 5%, and 10% levels.

U-test results reject the null hypothesis (p < .01), confirming significant U-shaped relationships. Inflection points occur at digitalization indices 65 (ROA) and 78 (ROE), with ROE’s later turnaround attributable to debt-driven profit mechanisms in commercial banking.

Empirical alignment: The 2018 national digitalization index (65) coincides with ROA’s inflection point, marking the profitability transition threshold.

We added a figure (Figure 2), which plots the fitted curves between bank ROA/ROE and the Digital Financial Development Index, respectively, with the inflection points clearly marked (Digital Financial Index = 65 for ROA; Digital Financial Index = 78 for ROE). The figure clearly demonstrates that before the inflection point, the impact of digital financial development on bank profitability is negative, while beyond this threshold, it shows a significant positive relationship, strongly supporting the existence of a U-shaped relationship. As shown in Figure 2:

Relationship between ROA/ROE and digital.

In the early stages of digital transformation, banks face high fixed costs and substantial investments in digital initiatives. Before reaching a certain threshold, banks must make significant investments in digital infrastructure construction (such as cloud computing platforms, AI-powered risk management systems, and data middleware), acquisition of technical talent, and business process reengineering. These costs are incurred intensively in the short term, while corresponding returns have not yet materialized, leading to a negative return on digital investment and exerting downward pressure on ROA. Only after digital finance operations reach a certain scale (e.g., in terms of user base, transaction volume, and data accumulation) does the unit operating cost decline due to economies of scale, allowing the upfront fixed costs to be amortized. Meanwhile, organizational learning curves begin to take effect, improving the efficiency of technology application, enhancing the accuracy of risk control, and increasing cross-selling opportunities, thereby driving significant improvements in profitability. This inflection point essentially marks the transition of a bank’s digital transformation from the “investment phase” to the “return phase,” validating the critical mass characteristic of returns on digital technology investments.

This study further applied the nonparametric LOWESS method with a bandwidth of 0.8 to reestimate the turning points. After removing all control variables as well as individual and year fixed effects, digital transformation (digital) shows a clear “trough”-shaped turning point at a digitalization index value of 60 in its relationship with bank profitability (ROA). Similarly, for return on equity (ROE), a distinct trough is observed at a digitalization index of 70.8. These findings are largely consistent with those obtained using the U-test method, further corroborating our earlier conclusions.

Robustness Checks

Endogeneity Tests

To address endogeneity concerns arising from omitted variables and sample self-selection, this study employs three distinct instrumental variables (IVs) to test for model endogeneity: (a) The one-period lagged Peking University Digital Financial Inclusion Index is a widely adopted instrumental variable in existing literature (Y. D. Li et al., 2020; D. Y. Liu & Huang, 2023). It exhibits strong correlation with the current Digital Financial Inclusion Index while remaining unaffected by the contemporary performance of traditional banking sectors. (b) Mobile telephone exchange capacity serves as crucial infrastructure for the development of FinTech, yet it is not directly related to the performance of traditional banking sectors examined in this study. (c) Following the approach of Yin et al. (2021) and Yu et al. (2022), we adopt an interaction term between the spherical distance from each provincial capital to Hangzhou and the one-period lagged Peking University Digital Financial Inclusion Index. Hangzhou, where Ant Group is headquartered, represents a key technological hub for the development and diffusion of FinTech. The spherical distance from each provincial capital to Hangzhou serves as a proxy for regional FinTech development. To mitigate potential collinearity between geographical distance and year-fixed effects, this distance is interacted with the lagged Digital Financial Inclusion Index. Both components of this interaction term are exogenous to the contemporary performance of traditional banking sectors. All three instrumental variables satisfy the conditions of relevance and exogeneity.

Table 6 presents the two-stage least squares (2SLS) regression results. Columns (1), (3), and (5) demonstrate the relevance between the instrumental variables and the original explanatory variables, all of which are statistically significant. Columns (2), (4), and (6) report the F-values of the three instrumental variables as 655.512, 12.991, and 44.66, respectively—all significantly greater than 10, allowing us to reject the weak instrument hypothesis. The Hansen J statistic from the Sargan–Hansen over identification test is 0 in all cases, indicating no over identification issue. The 2SLS regression results are significantly positive and consistent with the hypothesis 1 and hypothesis 3, confirming the robustness of our findings.

Impact of Emerging Digital Financial Sectors on Traditional Banking Performance: Instrumental Variable Approach.

Note. Cluster-robust standard errors in parentheses (provincial level).

denote significance at 1% levels.

Digital Transformation and Performance in Traditional Commercial Banks

The regression model examining the relationship between the digital transformation of traditional commercial banks and their performance may suffer from endogeneity issues due to omitted variables and sample self-selection. In particular, there may be a bidirectional causal relationship between the performance of traditional commercial banks and their digital transformation. Therefore, a robustness discussion is essential. This paper employs an instrumental variable (IV) approach to test the robustness of the baseline regression results.

Two instrumental variables are selected: (a) The first instrumental variable is the one-period lagged value of the digital transformation index of Chinese commercial banks (Z. Wang & Lyu, 2023). This variable is constructed based on the original digital transformation index and exhibits strong relevance. At the same time, it has no direct impact on the performance of traditional commercial banks, thereby satisfying the conditions for a valid instrumental variable. (b) The second instrumental variable is constructed using the Bartik method (Y. Zhou & Miao, 2023; G. Wang & Chen, 2022). The construction procedure is as follows: First, compute the first-difference of the digital transformation index (denoted as digital). This is obtained by subtracting the previous period’s value from the current period’s value. Then, interact the one-period lagged value of digital with its first-difference. The resulting interaction term serves as the Bartik instrument. This variable is also derived from the digital transformation index of Chinese commercial banks, which ensures strong relevance. Meanwhile, it is not directly linked to the performance of traditional commercial banks, thus meeting the criteria for a valid instrumental variable.

The results of the two-stage regression are presented in Table 7. The F-statistics for the two instrumental variables are 111.453 and 44.390, respectively, both significantly greater than 10, indicating that the selected instruments are not weak. The Hansen-J statistic is 0 in both cases, confirming that there is no over-identification problem. Columns (3) and (6) report the results of the two-stage least squares (2SLS) regression using the instrumental variables, which are consistent with the main hypothesis tests, demonstrating the robustness of our findings. Additionally, a U-test was conducted on the two-stage regression model to verify the U-shaped relationship, and the results confirm that the U-shaped relationship is statistically significant.

Digital Transformation and Performance in Traditional Commercial Banks: Instrumental Variable Approach.

Note. Cluster-robust standard errors in parentheses (bank-level clustering). “—” indicates excluded variables in the corresponding stage.

denote significance at 1% levels.

Mechanism Analysis

FinTech Impact and Traditional Banking Performance

To investigate the underlying channels of new quality productivity’s “construction effect”, we examine deposit/loan dynamics and asset quality. This study employs deposits, loans, and non-performing loan (NPL) ratios as proxy measures for productivity expansion, maintaining control variables consistent with baseline specifications (Tables 8 and 9).

Impact of Emerging Digital Financial Sectors on Traditional Banking Performance: Mechanism Analysis.

Note. Cluster-robust standard errors in parentheses (provincial-level clustering).

, ** denote significance at 1%, 5% levels.

Impact of Emerging Digital Financial Sectors on Traditional Banking Performance: Mechanism Analysis.

Note. Cluster-robust standard errors in parentheses (provincial-level clustering).

denote significance at 1% levels.

As shown in Table 8 Columns 1to 2, emerging digital financial sectors significantly increase deposits (coefficients: 1,989** and 2,011**). While platforms like Ant Group initially compete for deposits, digital payment innovations ultimately channel funds into bank accounts by reducing cash usage. Collaborative lending mechanisms drive loan growth (Columns 3–4: 790.6*** and 766.0**), as FinTech firms rely on traditional banks for credit expansion. Despite a negative coefficient, digital finance shows no significant impact on non-performing loan ratios (Columns 5–6: −0.00358 and −0.0141), indicating stable credit quality. Controls and fixed effects remain consistent with baseline models.

Table 9 demonstrates that emerging digital financial sectors significantly enhances traditional banking profitability. Columns 1to 2 show a robust positive impact on net profit (16.96*** with controls), while Columns 3 to 4 reveal substantial asset expansion (1,298*** with controls). The composite ROA improvement of 1.31% (versus a mean ROA of 1.00) indicates that profit growth outpaces asset expansion, driving overall profitability.

Digital Transformation and Performance in Traditional Commercial Banks

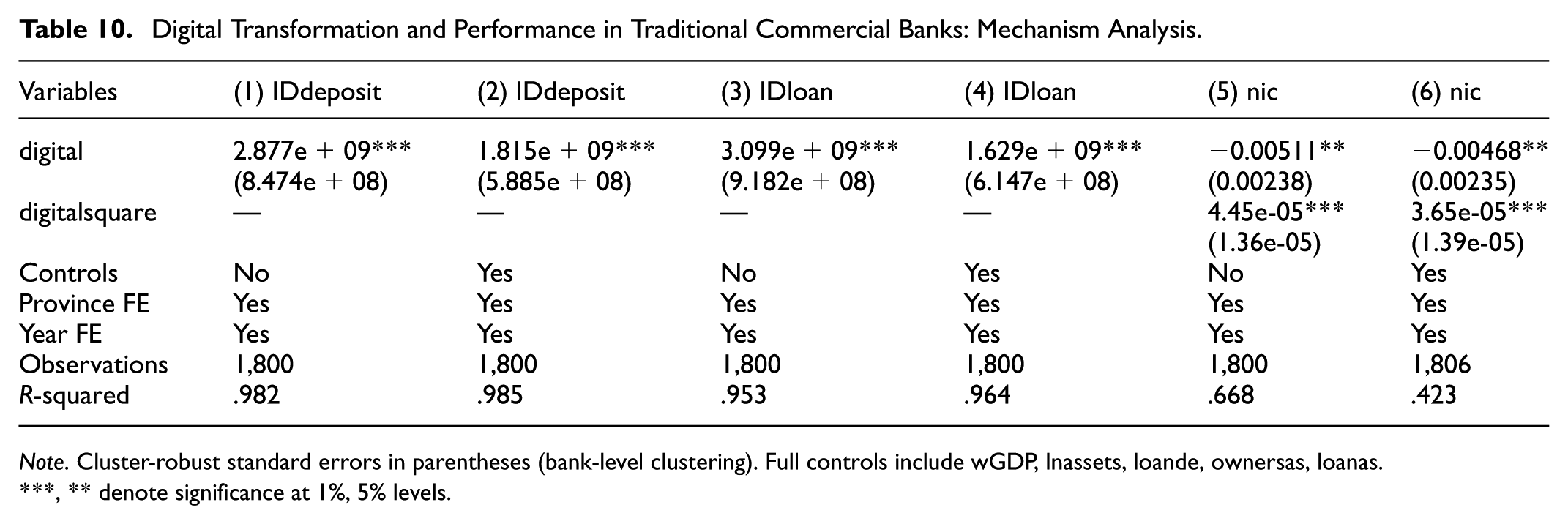

This study examines how digital transformation enhances traditional banks’ performance through productivity expansion and cost efficiency. Table 10 reveals that digital transformation significantly boosts deposits (Columns 1–2: 2.877e+09*** and 1.815e+09***) and loans (Columns 3–4: 3.099e+09*** and 1.629e+09***), while reducing net interest margins (Columns 5–6: −0.00511** and −0.00468**). This dual effect—scale expansion with margin compression—creates a win-win scenario for banks and social welfare. Further cost-efficiency analysis is warranted to fully explain performance dynamics.

Digital Transformation and Performance in Traditional Commercial Banks: Mechanism Analysis.

Note. Cluster-robust standard errors in parentheses (bank-level clustering). Full controls include wGDP, lnassets, loande, ownersas, loanas.

, ** denote significance at 1%, 5% levels.

Table 11 reveals an inverted U-shaped relationship between digital transformation and cost ratios. Initial digital adoption increases cost-to-income ratios (0.0639*** with controls) and overhead costs (9,982*), reflecting upfront investments in technology and talent. As digital systems mature, economies of scale emerge, reducing marginal costs (−0.000571*** for cost-income ratio). This nonlinear pattern aligns with digital economies’ increasing returns to scale.

Digital Transformation and Performance in Traditional Commercial Banks: Cost Efficiency Analysis

Note. Cluster-robust standard errors in parentheses (bank-level clustering). Full controls include wGDP, lnassets, loande, ownersas, loanas.

, * denote significance at 1%, 10% levels.

Based on the baseline regression results (Table 5) and the cost efficiency analysis (Table 11), the impact of digital transformation on the performance of traditional commercial banks exhibits a significant U-shaped pattern, while its effect on cost efficiency follows an inverted U-shaped trajectory. These two patterns are intrinsically linked through a clear transmission mechanism.

As shown in Column (2) of Table 11, the linear term of digital transformation (“variable digital”) has a significantly positive coefficient (0.0639*) on the cost-to-income ratio (“variable costincome”), while the quadratic term is significantly negative (−0.000571*). This indicates that digital transformation initially increases operational costs substantially, consistent with an inverted U-shaped trajectory—first rising and then declining. The rising costs primarily stem from high fixed investments in technology, large-scale system development and debugging expenses, and early-stage learning curve effects (P. Xie, 2015). The cost inflection point can be derived from the first-order condition at approximately digital = 56, calculated as:

Meanwhile, Column (2) of Table 5 shows that the linear term of digital intensity (“variable digital”) has a negative coefficient (−0.00427*) on ROA (“IDROA”), and the quadratic term is positive (3.31e-05*), indicating that bank performance initially decreases and then increases with the progression of digital transformation, forming a U-shaped curve. The profit inflection point is located at digital = 64.5, calculated as:

A comparison of the two inflection points reveals that the profit inflection lags behind the cost inflection by approximately 8.54 digital units. Economically, this gap can be interpreted as the “initial surge in costs delaying the profit inflection point by about nine digital units.”

As can be seen from the above calculation results, during the process of banks adopting fintech (i.e., digital transformation), the “inflection point” of the cost-to-income ratio occurs earlier than that of ROA. This gap further validates Hypothesis 3 of this paper. In the early stages of digital transformation in the banking industry, significant costs such as model training and data collection are required, while returns have not yet materialized. After a period of accumulation, returns begin to accumulate, the cost-to-income ratio starts to decline, and the “inflection point” of the cost-to-income ratio appears. However, the profits have not yet driven the overall ROA to reach its “inflection point.” After a further period of sustained effort, the profits brought by fintech continue to rise, and ROA also approaches an impending “inflection point” signaling an upward trend.

Heterogeneity Analysis

The 2016 watershed—marked by MyBank’s digital lending innovations and accelerated FinTech adoption—reveals divergent impacts. Table 12 demonstrates a significant U-shaped digital transformation-performance relationship post-2016 (Column 1: digital = −0.00420**, digitalsquare = 2.58e-05***; U-test p = .0105), contrasting with insignificant pre-2016 effects (Column 2). This aligns with China’s formal FinTech institutionalization phase starting 2016 (J. J. Li & Jiang, 2021; X. L. Xie & Wang, 2022), explaining prior studies’ negative findings using pre-2016 data that missed productivity integration dynamics.

Heterogeneous Effects of Digital Transformation on Performance

Note. Cluster-robust standard errors (bank-level) in parentheses.

, ** denote significance at 1%, 5% levels.

The U-test confirms a significant U-shaped relationship post-2016 (p = .0105), rejecting the null hypothesis of linearity. Earlier studies using pre-2016 data reported negative FinTech impacts on profitability, likely due to omitting post-2016 productivity integration effects when banks institutionalized digital technologies.

Further, we applied the Bai-Perron test for multiple structural breaks to verify the threshold year of 2016, using a bandwidth of 0.8. The test yields an F-statistic of 16.40 (p-value = .00), which strongly rejects the null hypothesis of no break, thus confirming the existence of a threshold effect.

Discussion

This study systematically examines how fintech, as a New Quality Productive Forces, influences traditional banking performance through the dynamic processes of external competition, technological spillovers, and its own technology adoption. Our findings not only provide new evidence for understanding the relationship between fintech and banking but also offer a rational explanation for the controversies in the existing literature.

First, we confirm that the development of emerging digital financial sectors exerts a significant positive impact on traditional bank performance (Hypothesis 1). This conclusion diverges from the view proposed by You et al. (2023) and P. Guo & Shen (2019), who argue that fintech primarily generates a “crowding-out effect.” We believe this discrepancy stems from differing interpretations of the fundamental state of China’s financial markets. This study supports the view proposed by Huang and Huang (2018) that China’s financial markets exhibit significant “financial repression.” emerging digital financial sectors entities like Ant Group initially expanded the overall market size by tapping into the “long-tail” customer segments neglected by traditional banks. However, through mechanisms such as “joint lending” and banks’ extensive payment settlement systems, the majority of funds still flow back into the traditional banking system. Our empirical analysis confirms that the development of emerging digital financial sectors significantly promotes the expansion of bank deposit and loan scales while also positively impacting return on assets (ROA).

Second, we reveal that technology spillover effects serve as the critical bridge connecting external shocks to internal transformation (Hypothesis 2). We find a high correlation between the fintech level ofemerging digital financial sectors industries and the lagging digital transformation index of commercial banks (with a correlation coefficient of .959), empirically supporting the behavioral shift of traditional banks from initial “hesitation and observation” to “actively embracing” fintech. Successful practices in emerging sectors provide traditional banks with clear, replicable digital paradigms and positive demonstrations, significantly reducing uncertainty and trial-and-error costs during transformation. This suggests that competition from emerging sectors functions more like a “catfish effect” (Z. L. Liu, 2016; Wang & Lyu, 2023), compelling banks to enhance efficiency and explore new markets.

Third, the most policy-relevant finding is the discovery of a significant “U-shaped” relationship between traditional banks’ digital transformation and their performance (Hypothesis 3). This conclusion reconciles conflicting findings from prior research (e.g., the negative results by X. L. Xie & Wang (2022) versus the positive results by J. Li & Jiang (2021)). This study demonstrates that both conclusions may hold true, as they respectively reveal the effects at different stages of digital transformation: During the initial phase of traditional banks’ digital transformation, substantial costs are incurred before profitability materializes. As transformation progresses, the marginal cost of utilizing digital elements decreases while returns increase. Once digitalization crosses a critical threshold (identified in this study as corresponding to a digital transformation index of approximately 65), profitability emerges and ROA rebounds. Mechanism analysis confirms: As digital transformation advances, the cost-to-income ratio and management expense ratio exhibit a pronounced inverted U-shaped trajectory, while deposit and loan scales continue to expand. Despite narrowing net interest margins, scale expansion and cost optimization ultimately ensure enhanced profitability.

This study also has several limitations: First, despite employing methods such as instrumental variables and dual fixed effects to mitigate endogeneity issues, the relationship between fintech and bank performance may still suffer from endogeneity problems like omitted variables. Second, the empirical analysis uses provincial panel data, where provincial data aggregation masks urban-rural disparities. For example, rural FinTech development levels are relatively high in coastal provinces/cities, whereas urban-rural disparities are more pronounced in inland provinces. Third, the absence of systematic, continuous cost-benefit data in the China Financial Yearbook prevents a detailed cost-benefit decomposition when analyzing the impact mechanisms of emerging digital financial sectors on traditional commercial bank performance. Fourth, the use of Peking University’s Digital Finance Inclusion Index as a development metric for emerging digital financial sectors suffers from overreliance on Ant Group data. Future research could collect more comprehensive and micro-level banking survey data (e.g., at the city or county level) and incorporate data from other emerging financial sectors (such as Tencent Group). This would help address endogeneity concerns through improved methodologies, validate the findings of this study, and further uncover the “black box” mechanism through which digital transformation impacts performance.

Conclusions and Policy Implication

FinTech has emerged as a powerful driver for innovation and transformation in the banking sector, with its fundamental impetus being quality and efficiency improvement. This study examines the impact of FinTech on traditional banking performance through its application in emerging digital financial sectors and the digital transformation process of commercial banks. The main findings are: First, FinTech, initially adopted by digital finance sectors, positively influenced traditional banking performance. This positive effect persists despite intensified competition because China’s banking market remains financially constrained rather than saturated, creating non-zero-sum competition. Digital finance operations directly increased traditional banks’ deposit/loan volumes while indirectly transforming their business models, collectively improving ROA. Second, digital finance sectors demonstrated strong technology spillover effects, with their FinTech level showing significant lagged correlation with banks’ digital transformation index. Third, banks’ accelerated digital transformation exhibits a U-shaped performance relationship. Early-stage investments in specialists and infrastructure initially reduce profitability, but stabilized models/algorithms later decrease marginal costs and increase returns, creating an inverted U-shaped cost curve while expanding deposit/loan scales. Fourth, using 2016 as a threshold, post-2016 integration of new productive forces shows significant U-shaped performance impact (decline then rise), while pre-2016 results were insignificant, explaining previous findings of FinTech’s limited positive effects. Policy implications include: (a) Deepening FinTech-bank integration to optimize processes, efficiency and costs; (b) Monitoring dynamic FinTech-performance relationships across different stages, Particular attention should be paid to the critical threshold around a digital transformation index of 65 for traditional banks. Below this level, banks may experience declining profitability that hinders their ability to sustain digital transformation efforts and achieve long-term sustainability. To address this, policymakers could consider implementing targeted support measures, such as temporary subsidies or tax incentives, specifically designed for institutions whose digitalization levels have not yet reached this inflection point; (c) Addressing SME banks’ digitalization cost challenges, as their limited upfront investment capacity risks liquidity shortages before reaching the profitability inflection point in the U-shaped transformation trajectory.

Supplemental Material

sj-docx-1-sgo-10.1177_21582440251387934 – Supplemental material for FinTech and Traditional Banking Performance in China

Supplemental material, sj-docx-1-sgo-10.1177_21582440251387934 for FinTech and Traditional Banking Performance in China by Meijing Xie and Hengshan Deng in SAGE Open

Footnotes

Ethical Considerations

This study utilized publicly available data and did not involve human or animal subjects. As such, it was exempt from requiring ethics committee approval in accordance with journal guidelines.

Funding

This article is supported by the following funding projects: Guangdong Provincial Education Science Planning Project (Grant No. 2025GXJK0843); Key Project of Guangdong Finance & Trade Vocational College; Qingyuan Key Project of Philosophy and Social Sciences (Grant No. QYSK2025006); Special Project of Qingyuan Science and Technology Think Tank (Grant No. QYZKGJ-2025-30).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The datasets generated during and/or analyzed during the current study are available from the corresponding author on reasonable request.

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.