Abstract

Blockchain and cryptocurrencies are transformative fintech breakthroughs that infiltrate the financial sector; however, they have many drawbacks and limits. Consumers have shown an insufficient level of acceptance of these innovations. This paper elucidates the main reasons for the effective growth of a cryptocurrency from user behavior. The objective is to determine what factors influence consumers’ intentions to engage in blockchain-based cryptocurrency dealings. Considering the complexity of emerging technologies, this paper applied an integration model which assumes various external elements such as financial literacy, performance expectancy, facilitating conditions, effort expectancy, awareness, trust, design, and social influence. Smart PLS3 has been used. The most critical determinant of a cryptocurrency’s growth is “design.” On the other hand, “design” affects effort expectancy positively, and social influence affects trust. Awareness, performance expectancy, financial literacy, and effort expectancy significantly affect intentions to use cryptocurrency. It’s worth mentioning that it is the first research to examine Pakistani customers’ perceptions of Bitcoin and their ability to partake. As a result, it is intended to serve as a base for potential research in this area.

Introduction

New financial innovations are introduced every day, but most fail to thrive. Blockchain has been a part of the global economy for more than 10 years. It has significantly impacted the financial industry, posing a direct hazard to established companies’ future. Some scholars have regarded it as a reliable technology (Miakotko, 2017), though blockchain and cryptocurrencies are unpredictable systems, making potential use in the financial system challenging to forecast (F. Shahzad et al., 2018). Blockchain technology is well-known for providing a stable forum for crypto transactions. Other innovations built into the blockchain mechanism include disruption ledgers and smart contracts, merging into various blockchain networks and implementations, such as Ethereum, and IBM Hyper ledger in multiple other technologies (Houben & Snyers, 2018). Nakamoto (2008) outlined a groundbreaking technology for creating a truly distributed P2P financial framework, claiming that “a truly peer-to-peer version of electronic cash will enable online transfers to be transferred directly from one party to another without passing through a financial institution.”

Blockchain is “a digitalized, distributed transactional ledger, having similar replicas stored on various database servers operated by different entities” (Schatsky & Muraskin, 2015). While there is a probable risky association with blockchain, it is essential to mention that crypto is only among the many possibilities presented by blockchain science (Carson et al., 2018). According to one report by WEF, Blockchain will store 10% of GDP by 2027, with an estimated yearly growth rate of 62.1% before 2025 (Business Wire, 2017).

While blockchain is supposed to significantly affect and implement various monetary industries and services, cryptocurrencies remain the most relevant. As per World Bank, non-fiat/quasi-electronic money is not secured by any underlying securities, has no tangible worth and economic value, and is not a responsibility of any organization (Natarajan et al., 2017). Cryptocurrencies are electronic tokens focused on blockchain technologies and employing cryptographic techniques and methods. According to the Federal Reserve of the United States, the existing payment mechanism is slow, unreliable, ineffective, non-collaborative, and not fully globalized (No, 2017). Crypto was a possible solution to many of these issues (Deloitte, 2015).

Today, every company may utilize blockchain technology to generate cryptocurrency and evaluate its suitability for use in an ICO (initial coin offering). The current cryptocurrency may be employed as an inside business environment payment mechanism to give entry to the ecosystem’s goods or services, a claim to an asset or liability, or a speculation cryptocurrency whose valuation focuses on consumer perceptions. The scope is extensive, and it will continue to expand shortly. Consequently, the question is raised: what are the primary elements that can lead clients and traders to accept a cryptocurrency?

This “cryptocurrency chaos” presents numerous possibilities as well as numerous challenges. Illegal operations involving cryptocurrencies are a reality, particularly for Bitcoin, the first and the most widely utilized cryptocurrency (Turner & Irwin, 2018). Bitcoin has been studied as a blockchain. Cryptocurrency has been used in illegal activities such as tax avoidance, money smuggling, and illicit transfers (Bloomberg, 2017). Another disadvantage is that Bitcoin is a complicated technology to master; for sure consumers, using Bitcoins is a big obstacle (Krombholz et al., 2016). Non-users of Bitcoins feel unable to utilize it, according to a qualitative survey by Gao et al. (2016), showing a barrier to the general adoption of cryptocurrencies. In addition to a lack of technical knowledge, financial literacy will stifle the growth of cryptocurrencies.

In brief, cryptocurrencies have several benefits, such as swift, reliable, accessible, and secured transactions. Still, they also have drawbacks, including risk, technical and economic difficulties in utilizing them, and a hazy societal concept of cryptocurrency ownership. The complexity and implications of the blockchain and cryptocurrency revolution necessitate an interdisciplinary analysis of its impacts and impediments. Although considerable studies have been conducted on BTC, the leading commonly used and significant cryptocurrency nowadays (Holub & Johnson, 2018), crypto still lacks literature, generally owing to its rarity and novelty.

This research has made a unique contribution to this area. In particular, many prospective investors and people are still confused about blockchain technology and cryptocurrencies, particularly Bitcoin, and their functions, which may have hampered the widespread use and funding of blockchain-based cryptocurrencies in different settings. The unique suggested model may be considered a new addition to the prior studies. It brings a fresh viewpoint to predicting consumer behavior and assisting future technological adoption.

First, this article reflects on the crucial considerations that every cryptocurrency must recognize to compete in the volatile cryptocurrency sector. Then, it analyzes the impact of facilitating conditions (FC), perceived risk (PR), effort expectancy (EE), social influence (SI), performance expectancy (PE), awareness (A), financial literacy (FL), trust (T), and design (D) on intents to utilize cryptocurrencies using technology acceptance models. Determining a cryptocurrency’s most meaningful attributes will enable current and potential market participants to concentrate on crypto’s most essential features. The survey-based research was executed in Pakistan with university-literate youngsters with a rudimentary understanding of the internet.

Second, the study could provide professionals with a better knowledge of consumers’ perception of cryptocurrency, which can then be utilized to develop risk-reduction methods and trust-building processes to improve and promote users’ online trade adoption, particularly in the growing field of cryptocurrency.

Third, regulating the associated factors broadens the study area of economic repercussions based on crypto use. In short, a study from this viewpoint may help us better grasp the critical effect of relevant variables on the adoption of fintech-related technology cryptocurrency in Pakistan.

The following are the objectives of this research:

To see whether associated elements (Figure 1) affect consumers’ intentions to utilize cryptocurrency like Bitcoin.

To determine which elements have the most impact on the Intention to utilize cryptocurrency.

Proposed model.

The remainder of the paper is organized as follows: Section 2 covers related research in the conceptual framework and presents the hypothesis; Section 3 explains the methodology; section 4 results; Section 5 contains the discussion of the results, recommendations for implication, limitations, and future studies; and Section 6 contains the conclusion.

Conceptual Framework

Investment behavior has been extensively researched in various fields, concentrating on multiple investment assets and using diverse adoption models. For example, Ali (2011) studied the investing behavior of individual Australian investors. Furthermore, Pascual-Ezama et al. (2014) investigated investor behavior in the Spanish stock market using the TPB (theory of planned behavior). TPB was also used by Sudarsono (2015) to investigate the behavioral intentions of Indonesian investors. Cucinelli et al. (2016) used TPB to analyze the financial behavior of Italian clients and advisers. It was discovered that attitude, SN, and perceived behavioral control substantially impacted financial behavior, although previous investment and financial knowledge had little effect. Trang and Tho (2017) also looked at the impact of perceived risk and investment performance on investment behavior in Vietnam’s developing market.

However, relatively few researches have been undertaken in blockchain technology, notably Bitcoin, to analyze investor behavior toward these asset classes. In this respect, Jonker (2018) performed one of the most recent research, which looked at the users’ intention and actual use of Bitcoin in the Netherlands. The survey discovered that shops’ use of Bitcoin is still limited. However, most respondents expressed an interest in adopting cryptocurrency payments soon. In previous research, it is found that blockchain has been found advantageous in Islamic finance. Chong (2021) delivered a thoughtful discussion on the many blockchain applications in Islamic finance that may be used to foster accountability and transparency amongst parties engaged in providing Shariah-compliant services and products.

According to Fosso Wamba et al. (2020), Bitcoin, blockchain, and fintech technologies are expanding, and enterprises are adopting them for competitive advantage. Henry et al. (2018) investigated bitcoin knowledge and used it in Canada in similar research. Trimborn et al. (2020) did another research that looked at the relative liquidity of bitcoin against conventional assets. Alaeddin and Altounjy (2018) investigated the attitudes and intentions of Malaysia’s generation “Z” to adopt cryptocurrencies and other blockchain-based tools in their financial decision-making. According to Fosso Wamba et al. (2020), the greatest practical bitcoin issues are user awareness and comprehension; in other words, it is difficult to comprehend how the system and its infrastructure work and then accept to embrace it.

To summarize, past research on blockchain-based cryptocurrencies suggests they are feasible investments that may help increase returns while reducing overall risk via suitable diversification tactics. Furthermore, cryptocurrencies still have limited acceptance, and Bitcoin knowledge is often linked to lower educational levels and younger generations. Few empirical studies look at Muslims’ intentions to adopt new financial technologies like blockchain-based cryptocurrencies (Ayedh et al., 2021; Elasrag, 2019; Rabbani et al., 2020).

As a result, this study aimed to see whether an explanatory model of the desire to utilize new financial technology, such as blockchain-based cryptocurrencies, could be tested. Several researchers (Lallmahomed et al., 2017; Sultana et al., 2016) employed different models or combinations of models to assess the adoption rate of new technology depending on the scenario. Davis (1989) was the first to investigate an individual’s attitude toward adopting modern technologies. To evaluate the acceptance of Bitcoin as a method of exchange in Pakistan, we employ UTAUT as a core research model, including several essential elements of adoption: perceived risk (perception risk theory), awareness, design, trust, and financial literacy. Performance expectation, effort expectancy, social influence, and favorable environments all have a direct and positive impact on the inclination to utilize technology, according to UTAUT models.

The UTAUT (Unified Theory of Acceptance and Use of Technology) and its expansion UTAUT2 are frameworks that describe how people and organizations embrace new technology (Venkatesh et al., 2003, 2012). Both are focused on Technology Acceptance Models (TAM and TAM2), which are in turn rooted in TRA (theory of reasoned action) and TPB (theory of perceived behavior) (Ajzen, 1991; Davis, 1989; Hill et al., 1977; Venkatesh & Davis, 2000). Performance expectancy (PE), social norms (SI), and facilitating conditions (FC) all have a clear and constructive impact on the decision to use technology, according to UTAUT models. Performance expectancy (PE) is described as one’s idea or view that utilizing a particular technology to improve one’s performance will be beneficial. The ease of using a specific technology is defined as effort expectancy (EE). Social influence (SI) is how individuals consider others to believe they can utilize a particular technology. The extent to which consumers feel they have the indispensable technical and organizational foundation to use a given high tech is recognized as facilitating conditions (F.C.) (Venkatesh et al., 2003). According to scholars, facilitating conditions of fintech play a vital role in financial services (Popova, 2021).

Hypothesis Development

Performance Expectancy and Effort Expectancy

Several reports have analyzed the impact of such factors on financial technology adoption. Still, there is no unanimity on their effect on the intent for using these. Conversely, considerable differences were found depending on the technology employed and the intended audience. For example, Moon and Hwang (2018) found that SI and EE positively affect the Intention of crowdfunding, but FC and PE do not. On the other hand, Kim et al. (2018) found that SI, EE, and PE positively influenced the decision to utilize a fingerprint payment system. Makanyeza and Mutambayashata (2018) acknowledged that while PE and EE had a beneficial influence on plastic capital, SI and FC had no more significant effect. PE and EE positively affect the usage of related monetary sites in the US state of Colombia (Sánchez-Torres et al., 2018). Khan et al. (2017) reported that Behavioral Intention’s vital determinants are PE and FC to use internet banking; however, there is no support that EE or SI plays a role.

Several reports have examined mobile banking adoption. For example, Farah et al. (2018) observed that SI, EE, and PE are determinants of the intent to utilize mobile banking-related services or products in Pakistan but that FC has no impact on adoption. EE and PE significantly affect the plan to use mobile microcredit/finance services for specific customer sections (depending on age, gender, and religion) but not for others (Warsame & Ireri, 2018). Furthermore, these authors show that SI influences the decision to utilize mobile microcredit services in all categories.

In research on payment acceptance made through mobile, Hussain et al. (2019) discovered that SI, PE, FC, and EE had a considerable impact on behavioral intent, particularly among the individuals in the base-of-the-pyramid (BoP) group, that is, those having a short paid volume. Mahfuz et al. (2016) researched m-banking in Bangladesh and found that SI and EE are the most crucial behavioral purpose antecedents. Furthermore, they discover that FC and PE do not significantly affect the intent to use technology.

H1: Performance expectancy (PE) affects the intent positively to use cryptocurrency.

H2: Effort expectancy (EE) affects the intent positively to use cryptocurrency.

Social Influence

Since social norms represent the trust level in technology and its impact, social influence is a particular construct (Chaouali et al., 2016). Many research and methods suggest that social influence is essential in describing consumer behavioral intent (Chaouali et al., 2016; Hsu & Lu, 2004; Malhotra & Galletta, 1999). Social factors have aided teamwork, resulting in a trusting belief (Alenazy et al., 2019). According to the TRA model, subjective standards and attitudes affect consumer behavior (Davis, 1989). Social forces are perceived when people engage with each other, share knowledge, and connect through the IT mechanism (Hsu & Lu, 2004). This kind of human contact gives rise to a group (Hsu & Lu, 2004). The level of trust arises from families or associates who approve of how innovative goods or services are used, enhancing Trust and use (Chaouali et al., 2016). Social influence affects users of blockchain technologies and the corresponding implementations.

H3: Social influence (SI) positively affects the intent to use cryptocurrency.

H4: Social influence (SI) affects the trust of blockchain-based cryptocurrency transactions significantly and positively.

Facilitating Conditions

Mendoza-Tello et al. (2018) depicted that perceived usefulness is essential in deciding whether or not to utilize cryptocurrencies for online transactions. Still, they find little evidence that SI regulates decisions. Schaupp and Festa (2018) researched cryptocurrency adoption, concentrating on the TPB, SI, and perceived behavioral control (how simple or hard it is to utilize cryptocurrencies) considerably: people who seem to imagine cryptocurrencies as smooth and uncomplicated to use and who get favorable social feedback on them are more inclined to utilize them. In a Chinese acceptability study, F. Shahzad et al. (2018) noticed that perceived ease of use and perceived usefulness influenced the decision to adopt Bitcoin significantly. The following hypothesis is suggested based on these results about fintech acceptance:

H5: Facilitating conditions (FC) affect intents positively to use cryptocurrency.

Perceived Risk

In behavioral science, perceived risk (PR) is characterized as a shopper’s assessment of ambiguity and possible negative consequences of utilizing or acquiring a commodity or service (Faqih, 2016). Several recent studies have studied perceived risk’s influence on the willingness to use financial technology, with different outcomes. In their research on the choice to use e-banking, Khan et al. (2017) found that perceived security is a significant predictor of behavioral intentions. Although PR has a minor effect on the intent to utilize e-banking, Shaikh et al. (2021) consider it critical in the pre-adoption phase, impacting other factors that directly affect the intention to utilize it.

As per Farah et al. (2018), in Pakistan, PR is not a determining element in using e-banking. Because of increased risk, markets can quickly lose customers (Dvorský et al., 2018; Oláh et al., 2017). Moon and Hwang (2018) also proved that there is no proof that PR affects the intent to use crowdfunding. In the cryptocurrency literature, Mendoza-Tello et al. (2018) showed that possible danger is not crucial in addressing the intention to use cryptocurrencies for electronic payments. The following theory suggests cryptocurrency as an evolving fintech with potential risk.

H6: The perceived risk affects intents adversely to use cryptocurrency.

Financial Literacy

According to Stolper and Walter (2017), financial literacy (FL) is a person’s understanding of main financial principles and ability to employ them in business decisions. FL has been shown in some experiments to be a predictor of financial behavior. Stolper and Walter (2017) said that a high degree of economic understanding is linked to more saving behavior, saving planning, stock exchange interaction, and better financial product selection; a lower or limited degree of financial knowledge, contrastingly, is linked to worse business decisions, more pricey loans, and expensive credit card privileges.

Individuals having greater financial literacy levels are more prone to conservative financial choices. Hastings et al. (2013) found that financial knowledge affects decisions on credit cards, equities, house loans, and pension savings accounts. Furthermore, Lam and Lam (2017) illustrated how financial understanding has a major impact on difficulties related to online shopping, such as addiction and impulsive spending. Based on the fact that cryptocurrency is a fintech commodity, and in light of the results above about the impact of FL on financial product use, we proposed the following hypothesis:

H7: Financial literacy affects the desire positively to adopt cryptocurrency.

Trust

Trust relates to customers’ ease and protection while utilizing technology (McCloskey, 2006). Social types of relationships can be treated by a trustworthy system that responds to unavoidable trust variability (Fortino et al., 2019b). Keen stated that a client’s trust has a direct and positive impact on e-buying and actions toward electronic activity and that mainly occurred for novel operations or structures right through the phase of development and expansion (Keen, 1997). Maintaining effective and viable communication and sustaining trust in trades and business relations is vital. It is a characteristic of trustworthy interactions that can minimize the danger of risk factors.

Those with reasonable opinions and attitudes about a specific technology will be more open to trusting it and affirming its protection than those with pessimistic attitudes. This indicates the good partial association between risk and acceptability when Trust is considered (Eiser et al., 2002). Trust has a strong positive impact on the ease of use when the client has enough faith in an online store to contemplate revealing their personal and financial details, representing an elevated level of confidence in the convenience of buying online (McCloskey, 2006).

In the blockchain, the risk likelihood for consumers should be minimal, and the level of trust should be strong. Trust significantly impacts both attitude and the PEoU of accessible technologies. Until now, the scientific and financial markets did not have enough trust in Blockchain technology. Therefore, the risks outweigh the advantages (Wunsche, 2016). Furthermore, various individuals agree that blockchain is challenging to use and manage technology. However, trust can be more robust if confidence is established by a blockchain-based consensus mechanism such as proof of stake (PoS) (Fortino et al., 2019a). In addition, IBM Hyperledger is a blockchain grid with a collective management framework that ensures user data security and trust (Demirkan et al., 2020). Thereby, it is proposed that:

H8: Trust positively and significantly affects intent to use cryptocurrency.

H9: Trust positively and significantly affects effort expectancy toward intent to use cryptocurrency.

Design

The influence of technical features such as visual appeal, navigation, and architecture on users’ inclination to use the device is called design (Zhou et al., 2009). DeLone and McLean (1992) suggested that efficiency metrics, which substantially impact IT execution and design quality standards, may affect the framework and knowledge quality. Despite the widespread internet usage, there are still several explanations why citizens cannot adopt new technology, such as the speed of hardware and software through time and poor reaction. In addition, complicated website architecture will result in high traffic and a lack of framework usability (DeLone & McLean, 1992). Additionally, website architecture can be a top priority for entrepreneurs. It should provide a user-friendly design to improve device adoption and ease of use through positive perceptions and experience (Hsu & Lu, 2004). Furthermore, robust architecture, user-friendly platforms, rapid communications, and response time influence PEoU’s attitude concerning the blockchain industry and technology. A user-friendly layout and a well-designed program/application positively and considerably affect the effort expectancy of Bitcoin proceedings or transactions sustained by blockchain technology. As a result, we propose that:

H10: Design positively affects the effort expectancy to use cryptocurrency.

Awareness

The public’s awareness and understanding of Bitcoin and its operation and management strategies are projected to impact investment activity substantially (Henry et al., 2018). It’s worth noting that increased understanding minimizes the level of uncertainty related to Bitcoin investing. Henry et al. (2018) researched Bitcoin usage and its comprehension in Canada and found that 64% of Dominion of Canadians are aware of Bitcoin; nonetheless, just 2.9% utilize it. Additionally, males and those with a university or college degree were more likely to be aware of Bitcoin; however, unemployed people were more likely to be aware of Bitcoin. On the other side, Bitcoin possession was linked to younger people and a high school diploma. Finally, the findings revealed that Bitcoin acceptance is positively associated with knowledge. Alaeddin and Altounjy (2018) depicted that the level of knowledge and confidence influences generation “Z”’s Intention to use cryptocurrencies and related technologies. According to Fosso Wamba et al. (2020), the most real Bitcoin obstacles are consumer knowledge and comprehension; in other terms, it is difficult to understand how the program and its infrastructure work and then accept to implement it.

Since cryptocurrencies are still relatively young, and there is a perception that there is a lack of understanding and information on how they operate, prospective investors will typically seek guidance and feedback from their social networks about whether or not to invest in them. This is especially important since conventional financial advisors/brokers will not necessarily consider investing in Bitcoin compared to other financial assets. This complies with Henry et al. (2018), who observed that Bitcoin knowledge and awareness have a massive impact on its usage. Interestingly, respondents’ ability to get broad and ordinary details or insights about Bitcoin, including its advantages and potential hazards, and the strategies often utilized to manage a Bitcoin investment, is assessed.

H11: Awareness substantially affects the consumers’ intentions to use cryptocurrency.

Methodology

We sampled responders over the age group of 20 of 222 people in Pakistan who have university-level degrees using a structured and self-adjoint virtual survey. The study was restricted to people who clearly understand the internet due to the survey’s online nature. In addition, since cryptocurrencies were built on blockchain technology, as mentioned in the introduction, a basic understanding of technical and financial expertise was needed to work with them. As a result, we concentrated on college-educated individuals to interview people expected to have a good knowledge of these developments. As a result, we guaranteed that the respondents had the bare minimum of expertise. Other reports support using a highly qualified target audience to ensure that responders have an executive level of FL to guarantee that the data gathered suits the study objective (Stolper & Walter, 2017).

Sampling and Data Collection

The questionnaire was sent to 500 people, out of which 300 responded. We took 222 responses from various backgrounds over 1 month using an online survey from 15th April 2022 to 15th May 2022 using convenience sampling. The demographic details for the respondents are shown in Table 1.

Responders’ Demographic Profile.

Table 1 shows that males accounted for 73% of the collected data, while 27% were females. The majority of the responders, 63.96%, were between 20 and 30 years old. Regarding the respondents’ education, 45.05% were in the Ph.D. category occupying the most positions in the survey. Furthermore, concerning respondents’ occupations, 51.80% were students, the highest percentage. 45.05% had a higher income level than PKRs 50,000. As shown, salary levels were extreme, which is understandable considering that the study comprised people with a college education who were more prone to higher incomes. We found that 62% of respondents had fintech experience.

Measurement Development

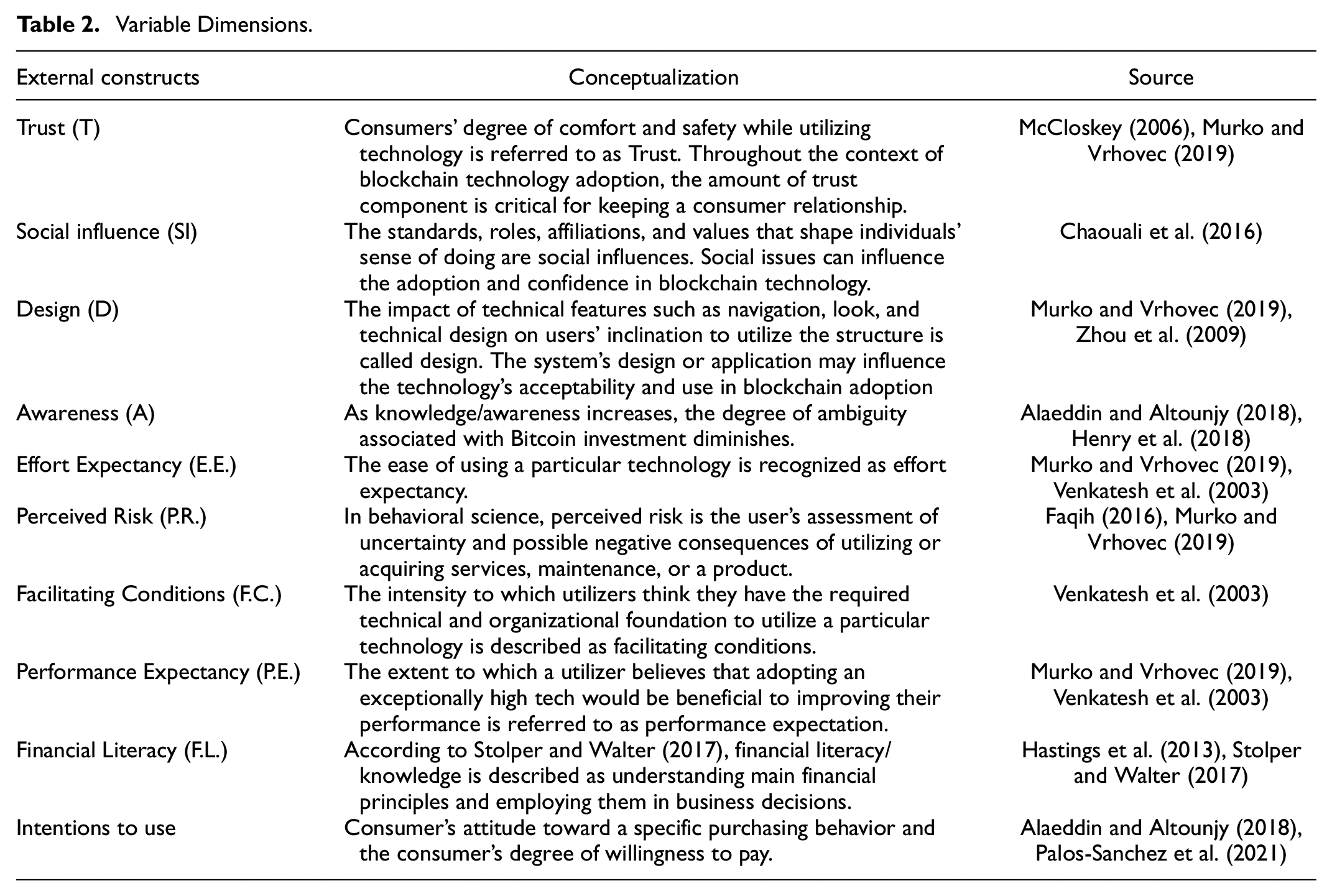

Our measuring scales are built on scales that are generally acknowledged and utilized in the technology adoption literature. The constructs, products, and fundamental concepts of each one are listed in Table 2. According to Stolper and Walter (2017), there are two fundamental methods to determine FL: (i) by utilizing a survey to check individuals’ financial understanding and (ii) by using self-assessments. We used a self-assessment method, considering that people make choices dependent on their view of facts rather than reality. From the standpoint of customer behavior, this suggests that consumers would respond based on the expectations of their financial expertise rather than their real knowledge related to finance. As a result, the self-perception of financial literacy will be crucial in determining whether or not to use cryptocurrencies. The Source of all the items has been mentioned in Table 2. Items are mentioned in the Appendix A. Variables are noted in Figure 1.

Variable Dimensions.

Results

Smart PLS version 3 has been used to evaluate the surveyed data by Partial Least Squares-Structural Equation Modeling (PLS-SEM) technique (Al-Maroof & Al-Emran, 2018). Because this is an exploratory study, PLS-SEM is the ideal method for obtaining the best findings (Hair et al., 2016; Henseler et al., 2015). Hair et al. (2016) suggested that researchers examine all items’ outer loadings and the average variance extracted (AVE) to determine convergent validity in the reflective measurement approach. The path coefficients of determination were assessed in terms of the structural model (Hair et al., 2016; Henseler et al., 2015; Selya et al., 2012). As a result, all of the above criteria were put forth to justify this experiment’s measurement and structural model.

Measurement Model Assessment

Hair et al. (2016) stated that each item’s reliability and validity should be assessed along with the factor loading. A measure’s consistency is referred to as reliability. To be regarded as reliable, a measure should provide consistent results under consistent circumstances, and the value for each item’s loading must be equal to or higher than (0.6).

Cronbach’s Alpha values should also be equivalent to or higher than (.7). Furthermore, the grand mean value of the squared loadings of the items linked to the construct. The AVE is the standard measure for determining convergent validity. That’s the amount of variation explained by a latent construct’s indicators.

The construct articulates more than 50% of the variance of its items if its AVE value is (0.5) or above (Hair et al., 2016). Composite reliability values and Cronbach’s Alpha exceed (.7), and AVE values are more than (0.5), as indicated in Table 3. As a result, the convergent validity of constructs is established. This research should look at the HTMT and Fornell-Larcker criteria to determine discriminant validity. AVE value’s square root is compared to latent variable correlations using the Fornell-Larcker criteria, which are explained in Table 3.

Internal Consistency Reliability and Convergent Validity.

Internal Consistency Reliability and Convergent Validity

Results demonstrate that all constructs and indicators correspond to the reflective measurement requirements, that is, all indicators have loadings greater than 0.6 (Figure 2). The AVE is more than 0.5. Cronbach’s alpha and composite reliability values exceeded .70 (Table 3). Finally, the outcomes depicted that all indicators are appropriate, convergence validity is confirmed, and data internal consistency is achieved.

Loadings.

Discriminant Validity

Fornell and Larcker (1981) suggested that the square root of the average variance extracted by a construct must be greater than the correlation between the construct and any other construct in the model to attain discriminant validity. All constructs in Table 4 meet this criterion.

Fornell-Larcker Criterion.

The Heterotrait-Monotrait (HTMT) correlation criteria evaluate the discriminant validity findings, as shown in Table 5. The results satisfy the HTMT criteria with values below the threshold of 0.90, implying that discriminant validity has been established (Henseler et al., 2015).

Heterotrait-Monotrait (HTMT).

Structural Model Assessment

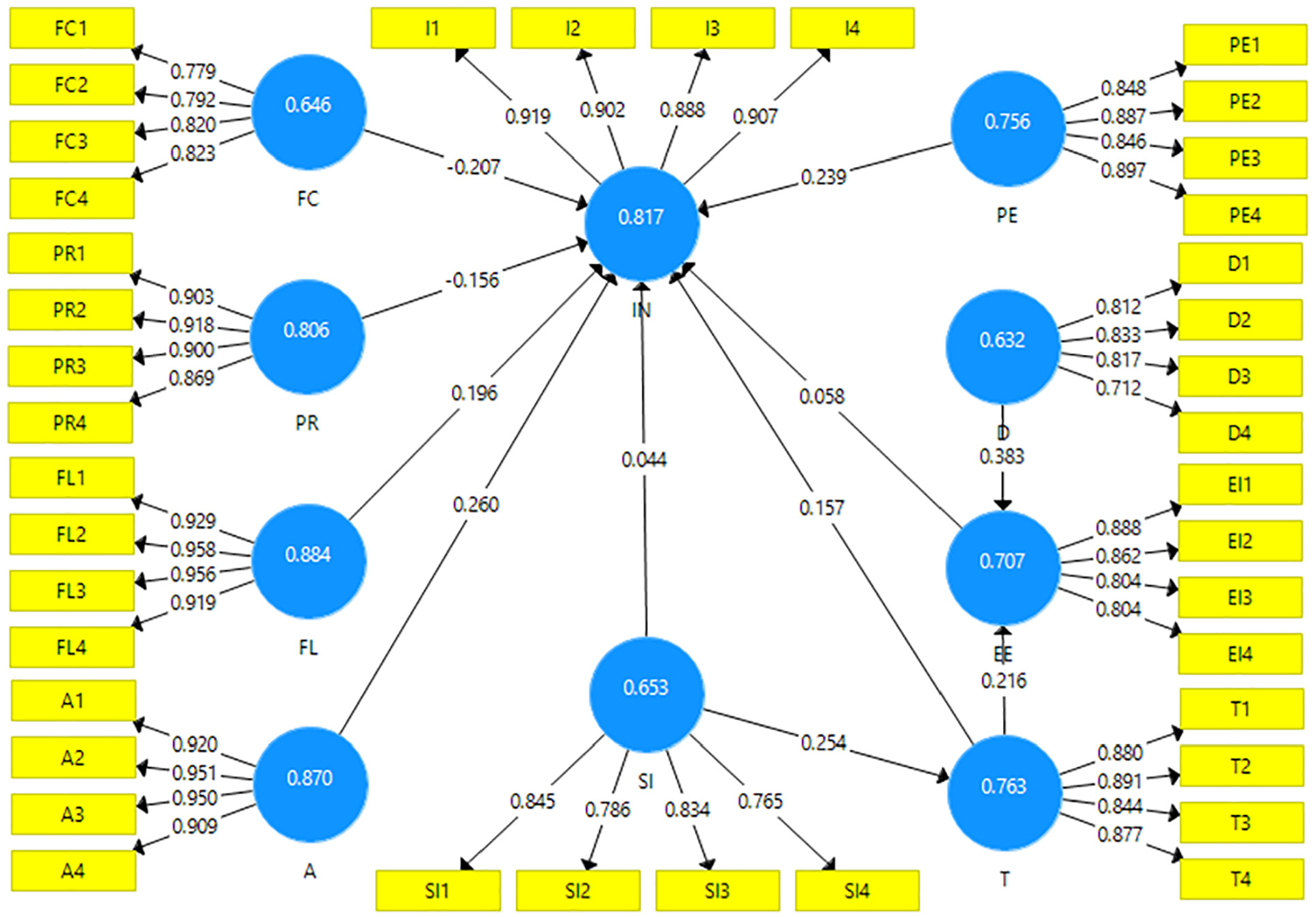

A bootstrapping method with 5,000 sub-samples was performed to evaluate the structural model and verify the assumptions. The structural model is assessed concerning the estimates and hypothesis tests regarding the causal relations among variables specified in the path diagram (Figure 3).

Structural equation model.

Collinearity

Table 4 indicates that construct correlations are robust, ranging from .795 to .940. The possibility of multicollinearity could be explicitly investigated using regression analysis. In regression analysis, the variance inflation factor (VIF), which quantifies the extent to which other predictor variables characterize a predictor variable, is a typical metric of collinearity (Hair et al., 1998). A threshold VIF of less than or equivalent to 10 (i.e., tolerance >0.1) is often recommended (Hair et al., 1998). In our research, we utilized Smart PLS 3, and the AVE values were lesser than 10. Table 6 shows the VIF values for all of the model’s constructs. The VIF of all constructs is less than 3, except FC, which is less than 5, still indicating that the structural model has no collinearity problems.

Inner V.I.F. Values.

Hypothesis Testing

The path coefficient was examined using a bootstrapping procedure with 5,000 subsamples. Table 7 summarizes the testing results of the hypothesis, indicating that H1, H4, H7, H6, H7, H8, H9, H10, and H11 are supported, whereas H2, H3, and H5 are not supported statistically.

Hypothesis Testing.

An Explanatory Model of the Intention to Use Cryptocurrency

As presented in Table 8, the model’s goodness of fit is good. The explanatory factors explain 0.262 in the intent for using cryptocurrencies; thus, R2 indicates that the model’s explanatory power is good.

R2.

Impact of Associated Factors

According to the findings, design has the highest explanatory power for an individual investor’s intention to use cryptocurrency. Social influence affects trust, trust impacts intention to use, and design impacts effort expectancy.

The first result is that the variable “design” (D -> EE) has a strong explanatory power that a path coefficient is 0.383, the second one is awareness (A -> IN) with a path coefficient of 0.260, and the third one is social influence (SI -> T) having path coefficient 0.254.

H1 (PE -> IN, B = 0.238, p = .000) defines the path between performance expectancy and intentions to use cryptocurrency. Our study is in line with those of others who discovered this factor to be a determining factor in the intent to utilize a particular fintech, such as service of biometric payment (Kim et al., 2018), plastic money (Makanyeza & Mutambayashata, 2018), e-payments via cryptocurrencies (Mendoza-Tello et al., 2018), and acceptance of Bitcoin in China (F. Shahzad et al., 2018).

H2 (EE -> IN, B = −0.058, p values = .480) defines the path between effort expectancy and intentions. Regarding Bitcoin fintech, EE has positively impacted cryptocurrency adoption and acceptance in China (Schaupp & Festa, 2018; F. Shahzad et al., 2018). However, in this study, our findings do not support the impact of effort expectations on crypto adoption. H3 (SI -> IN, B = 0.045, p = .549) explains the path between social influence and intentions. Our study shows that social influence has a non-significant effect in determining the intent to utilize cryptocurrencies. While one research showed the effect of a social norm on acceptance to be non-significant, other studies, Schaupp and Festa (2018) found it significant. However, H4 (SI -> T, B = 0.254, p = .000) explains the path between social influence and Trust has a significant effect.

H5 (FC -> IN, B = −0.208, p = .37) describes the path between facilitating conditions and intentions. There seems to be no agreement on the positive impact of FC on adopting financial technology concerning utilizing cryptocurrency. Although it is significant, somehow, it has a negative impact. Several researchers have verified its impacts, including Hussain et al. (2019) and Khan et al. (2017). In contrast, others didn’t prove that it affects fintech acceptability (Farah et al., 2018; Makanyeza & Mutambayashata, 2018; Moon & Hwang, 2018). Likewise, our findings did not support the hypothesis.

H6 (PR -> IN, B = −0.156, p = .008) describes the path between perceived risk and intentions. Our results show that PR is a significant element concerning cryptocurrency use. Our results do not align with Walton and Johnston (2018). H7 (FL -> IN, B = −0.197, p = .002) elucidates the path between financial literacy and intentions. It is found significant concerning cryptocurrency use in Pakistan. We discovered that financial literacy has a predictive value for Bitcoin adoption. Other research on FL has shown that individuals with more FL are not prone to rash decisions (Lam & Lam, 2017). H8 (T -> IN, B = 0.157, p = .013) tells the path between Trust and intentions. It is found that Trust has a greater impact on the Intention to use crypto in Pakistan. Our findings align with Albayati et al. (2020). H9 (T -> EE, B = 0.215, p = .000) describes the path between trust and effort expectancy. Where p values are .000, thus it is found to be significant. Our research agrees with Albayati et al. (2020). H10 (D -> EE, B = 0.383, p = .000) explains the path between the design and effort expectancy. p values are accurate. The hypothesis is supported. Our findings are in line with Albayati et al. (2020). H11 (A -> IN, B = −0.260, p = .000) explains the path between awareness and intentions. Our hypothesis is supported here. Our findings are in line with Henry et al. (2018).

Discussion

This study aimed to see whether an explanatory model utilizing novel fintech, viz blockchain-based cryptocurrencies, could be tested. Variables from UTAUT technology acceptance models were used to create the suggested model. In addition, other factors from the model were also included as variables mainly utilized in the fintech acceptance study. Most research indicates that EE impacts fintech adoption (e.g., Farah et al., 2018). If a consumer thinks he will have to spend more time learning or dealing with transactions via a more complicated system requiring more effort, it will hinder their tendency to use that system, or vice versa. Our study found that consumers find these factors proposed in the model important to using cryptocurrency.

H1 defines the path between performance expectancy and intentions to use cryptocurrency. This hypothesis is accepted, showing that Pakistani users are satisfied with the cryptocurrency’s performance. It shows that the purpose of their using cryptocurrency is being fulfilled. Using cryptocurrencies will increase their chances of achieving essential objectives. Their standard of living by using cryptocurrencies is improving, or their experience with Bitcoin is far superior to their expectations. However, concerning H2 defines the path between effort expectancy and intentions, where EE has positively impacted cryptocurrency adoption and Bitcoin acceptance in China (Schaupp & Festa, 2018; F. Shahzad et al., 2018); it is not supported by our findings statistically. Consumers may face difficulty in learning how to use cryptocurrencies. They find it complicated and inapprehensible and feel like not being skillful at paying with Bitcoin. It shows that interacting with Bitcoin requires a lot of mental effort. Thus, cryptocurrency service providers should manage all these issues for better development in the blockchain industry. H3 explains the path between social influence and intentions. Our study showed that social influence has a non-significant effect in determining the intent to utilize cryptocurrencies.

Considering social influence with Trust like our hypothesis 4, we find that this route significantly benefits. SI is more influencing people’s lives and behaviors. When people engage with one another, there will be a considerable effect. Thousands of personal ideas and beliefs are shared on social media, influencing other people’s decisions to use or not utilize new technologies. Because Trust is essential in blockchain technology for consumers’ behavior to be supported, the social element is a big part.

When analyzing significant or insignificant factors statistically, many considerations should be considered, such as perceived risk in our hypothesis 6 is found significant. In some previous studies, for example, according to Shaikh et al. (2021), PR is not a decisive variable in utilizing m-banking technologies, even though it is a crucial pre-adoption phase. According to Farah et al. (2018) and Moon and Hwang (2018), PR does not predict the choice to adopt a new fintech aligned with our results. In research focused on cryptocurrencies, Mendoza-Tello et al. (2018) demonstrate that PR is not a substantial element in determining the intent to utilize cryptocurrencies for E-Payments. Similarly, Walton and Johnston (2018) indicate that the perceived security risk does not affect consumers, attitudes about bitcoin or their desire to use it. In contrast, our studies showed that it does affect.

Concerning H7, vast literature examines the issue of whether high levels of FL induce better financial decision-making (Stolper & Walter, 2017). The bulk of studies shows a positive connection between measures of FL and good financial conduct in different areas, as we shall examine shortly. According to our findings, more financial expertise does affect the adoption of cryptocurrencies. This is because FL enables individuals to make more informed financial choices. It may be better not to engage and invest in certain instances, while it may be advantageous to invest in others. Our findings contribute to prior results. More extraordinary financial expertise enables a client to assess an investment more correctly (e.g., whether or not to finance in Bitcoin vs. Ethereum based on the state of the money market at any particular moment), but not just the technologies that support it (cryptocurrency technologies in the current circumstances). As a result, FL may impact investment decisions; it significantly impacts technology decisions, which is the subject of this study. As a result, from the FL standpoint, the choice to adopt or not utilize a cryptocurrency may be determined by financial factors rather than technological acceptability criteria.

Trust positively influences customers’ intentions toward blockchain-based apps. These impacts have something to do with the user, Trust, and belief. A consumer with a high level of trust is more likely to utilize new technology, which may raise customer expectations and encourage them to use such new blockchain technology-based applications. Thus, our hypothesis 8 is significant.

Thought trust is critical in this research since it substantially impacts Intention. It is one of the most effective ways to inspire people to believe in new technology and to boost their Trust in how efficiently it can be utilized with less effort; here in this research, results of hypothesis 9 show because EE does not affect intents; thus, Trust does not affect EE in our study.

Application design impacts EE for the same technology; it improves consumers’ compatibility with various apps if they understand and engage favorably. Design affects people psychologically.

H11 is supported. The proportion of participants is familiar with cryptocurrency’s usage, advantages, and administration. Users are likely to utilize a product or service if they are fully informed.

Our findings align with Henry et al. (2018), who showed that Bitcoin awareness and knowledge substantially affected its use. It’s worth noting that respondents’ knowledge is measured by their ability to get basic details on Bitcoin, including its advantages and potential risks and the techniques frequently employed to manage a Bitcoin investment. Awareness, in this case, is when responders perceive that they have sufficient knowledge about the management and dealing of cryptocurrency; the same is found in our findings. It is discovered that respondents believe knowledge and awareness regarding blockchain technology and Cryptocurrency Bitcoin investment is essential, which may undoubtedly influence their attitudes toward cryptocurrencies and their decision to put money in or not in Bitcoin.

This research has made a unique contribution to this area. In particular, many prospective investors and people are still confused about blockchain technology and cryptocurrencies, particularly Bitcoin, and their functions, which may have hampered the widespread use and funding of blockchain-based cryptocurrencies in different settings.

Recommendations and Implications

Based on the obtained results, we suggest various ways to deal with the cryptocurrency and blockchain-related services sector with a higher chance of success.

The first suggestion is to consider the risk of operating in such areas. Customers and potential investors consider putting their investment in or dealing with these new technical assets very hazardous, given the current technological progress. Thus, the first crypto regarded as “risk-free” may gain a competitive edge over the current market.

Second, the ease of use, efficiency, and performance of a new cryptocurrency’s product and service design (or existing cryptocurrency innovation initiatives) should be prioritized. Significant marketing measures need to guarantee cryptocurrency as a high-value-added product for customers. The more weight a cryptocurrency provides, the further likely it is to be utilized. In the Bitcoin market, focusing on utility is a suggested approach.

The third suggestion is to create enabling circumstances/facilitating. Even though the intent to utilize an existing or future cryptocurrency is proportionally not strongly dependent on the circumstances under which prospective consumers can conduct business with them, variables like the science and technology-related knowledge required to operate well with a cryptocurrency, the suitability of a client’s technological advances with digital currency technical requisites, and the availability of generally recognized cryptocurrency exchanges are still important.

The fourth suggestion is related to the design/layout of the site or applications in terms of the client’s efforts to utilize a cryptocurrency. Even if the time and effort needed to understand and use a cryptocurrency are not among the essential criteria for adoption, it is crucial in our research. Any improvement in a cryptocurrency’s suitability, practicability, and versatility will positively impact the desire to utilize it. The user’s intent is influenced by the design of the apps. As a result, it is preferable to offer an application that is simple to use and free of complexities.

Limitations

Finally, there are several limitations to this study. First, we target a very narrow demographic: college-literate individuals with a solid understanding of the internet. Regardless of our debate and reasoning for this choice, subsequent research should concentrate on other segments to better understand Bitcoin adoption in society. One more latent limitation is that the current research was limited to Pakistan. Suppose the research study had a broader geographical range or was performed in different countries with different cultures. In that case, the results might have been different (e.g., the previously mentioned m-banking research results varied based on region, whereas the ING research by Exton and Doidge (2018) disclosed different views depending on the part of the world). As a result, further study should be carried out in other nations.

Another consideration for future research that can be considered is the long-term viability of cryptocurrency and blockchain computing/mining. The approach was intended to measure just the Intention of consumers, not their actual use rate. However, this points to a future study path in which we may use actual statistics to back up our results. As stated by Krause and Tolaymat (2018), the mining process for Bitcoin necessitates rigorous computing capacity and high power consumption; it is approximated that the energy required to mine one US dollar of Bitcoins was 17 megajoules between 2016 and 2018, compared to 5 megajoules needed to mine one US dollar of gold. Thus, according to this study, sustainability issues may impact the growth of cryptocurrencies.

Future Work

Cryptocurrency is a new technology that is constantly developing. This way, the outcomes of current research should be taken carefully. Furthermore, technologies will evolve in the coming years, as will people’s understanding of fintech. Thus, future studies should incorporate a longitudinal study/systematic review to monitor the development of cryptocurrency acceptance and adapt the model to current conditions.

Future scholars are asked to examine Bitcoin’s potential implications (e.g., investment purposes). Second, numerous international banking sector, exchanges, and investment firms have already marketed Bitcoin-linked securities, financing, and forthcoming pacts with Bitcoin (S. J. H. Shahzad et al., 2020); as a result, portfolio/risk administrators may be the focus of additional research on how they intend to use Bitcoin as a strategy and portfolio diversifier. Third, no centralized authority may be reachable to guarantee user security since Bitcoin decentralizes financial networks and is susceptible to hacker attacks. Furthermore, the operation cannot be undone once the transaction is finished. Future studies should examine issues like the difficulty of purchasing Bitcoin. Fourthly, it’s not as if all pertinent factors influencing a person’s decision to utilize cryptocurrencies are considered. According to Qiuyan, cultural, legal, social, and psychological factors influence purchasing choices (Zhong et al., 2019). This study investigated social influences and determinants, such as trust. However, it is advised that researchers do in-depth research using culture as a moderator; as a result, these factors may be included in future studies to facilitate greater understanding. Technophobia, regulations (regulatory support), perceived risks associated with Bitcoin, cost considerations, and the impact of well-known websites on trust, transparency, price value, traceability, and desire to utilize cryptocurrencies are other variables that may be explored. Fifth, the absence of rules governing Bitcoin may encourage the black market; as a result, it’s critical to investigate Bitcoin’s shadow economy since it may be used for tax evasion, money laundering, terrorist financing, and the acquisition of illegal items.

Conclusion

The current research uses the UTAUT2 and Perceived risk theory to examine Pakistani people’s intention to use cryptocurrency. According to the findings, the perceived risk factors are not significant. In contrast, the most critical determinant of a cryptocurrency’s growth is “design,” followed by awareness, performance expectancy, trust, financial literacy, and effort expectancy. There is evidence of a link between design and effort expectance. Furthermore, social influence was found to have an impact on trust. Social influence, perceived risk, and facilitating conditions are not linked with intentions to use cryptocurrency.

Interestingly, this is the first study investigating Pakistani consumers’ attitudes toward bitcoin and their capacity to use it. Consequently, it’s a starting point for future research in this field. The study will aid bitcoin authorities in offering extra incentives to digital currency users and formulating/updating laws by considering the purpose. The findings may assist government agencies in managing blockchain technology in corporate operations, and commercial banks improve and upgrade their blockchain products and services to increase profit margins. In this study, the regularization and clustering algorithm for cryptocurrencies and the use of blockchain technology are advocated. Last but not least, the literacy of the novice user is crucial.

Footnotes

Appendix A

Author Contributions

Chunling Li supervised and funded the research. Nosherwan Khaliq conceptualized and wrote the original draft. Leslie Chinove used software. Usama Khaliq participated in data collection, reviewing, and editing. József Popp and Judit Oláh did the formal analysis. All authors read and approved the final manuscript.

Availability of Data Materials

The datasets analyzed during the current study are available from the corresponding author upon reasonable request.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial supportor publication o/or publication of this article: Chunling Li managed the funding procedure.