Abstract

Green innovation plays a crucial role in fostering economic growth alongside environmental preservation. This study investigates the relationship between the issuance of green bonds and green innovation among peer companies, utilizing green patent data. The findings reveal that the issuance of green bonds significantly bolsters the level of green innovation among peer companies. Strategic innovation appears to be more pronounced than substantive innovation. The mechanism analysis indicates that the issuance of green bonds influences peer companies to engage in green innovation activities by alleviating their financing constraints and increasing their level of R&D investment. The heterogeneity analysis reveals that the impact of green bond issuance on green innovation among peer companies is particularly pronounced in capital-intensive companies and industries with high concentration. This study not only contributes evidence to the theory of “peer learning” but also provides a theoretical basis for expanding the economic benefits associated with green finance.

Introduction

To achieve the “double carbon” goals—carbon peaking and carbon neutrality—the Chinese government has recently emphasized the need to establish a market-oriented green financial system. This initiative aims to promote green finance and facilitate the healthy growth of industries focused on energy conservation and environmental protection. Within the green financial framework, these policies encapsulate dual roles in financial resource allocation and environmental regulation. These policies serve as a complementary approach to traditional environmental regulation and enable the government to use market mechanisms, such as financial regulation, in the field of environmental governance. Among various green financing policies, green bonds have emerged as a promising option that is encouraged by the government and embraced by enterprises. As a significant instrument of green finance, green bonds essentially combine environmental protection objectives with financial mechanisms. They aim to encourage companies to issue green bonds, thereby directing their focus towards green investment and research and development, as well as enhancing their environmental performance.

To promote the growth of the green bond market, the National Development and Reform Commission issued the “Guidelines for Green Bond Issuance” on December 31, 2015. Additionally, they released the “Catalog of Projects Supported by Green Bonds” to guide the issuance of green bonds. As a result, the green bond market in China has flourished. Subsequently, in March 2017, the China Securities Regulatory Commission issued the “Guiding Opinions on Supporting the Development of Green Bonds,” and the National Association of Financial Market Institutional Investors issued the “Guidelines for the Business of Green Debt Financing Instruments for Non-Financial Enterprises,” both of which were based on the “Guidelines for the Issuance of Green Bonds” as a reference document. These policy documents offer guidance and institutional support for China’s green bond market, fostering its rapid and diversified development. In 2020, the People’s Bank of China, the National Development and Reform Commission, and the China Securities Regulatory Commission jointly issued the “Notice on Printing and Distributing the Catalog of Green Bond Supported Projects (2020 Edition),” to realize the “dual carbon” goal. This initiative took into account the old version of green bond standards and timely aligned them with international standards.

In response to the increasingly severe global climate change issue, China, as a responsible major country, has introduced Chinese wisdom and solutions. In 2022, the Green Bond Standards Committee released the “China Green Bond Principles,” establishing a domestically unified and internationally aligned green bond standard, enhancing the purity and recognition of green bonds. To standardize, diversify, activate, and open the green bond market, the People’s Bank of China implemented five measures in 2023, including enhancing the quality and transparency of green bonds, supporting various industries in achieving low-carbon transformation and expanding the types and maturities of green bonds to stimulate investment and financing demand and supply. Furthermore, efforts were made to strengthen international cooperation and exchanges related to green bonds. According to the “China Sustainable Bond Market Report 2022,” by the end of 2022, the cumulative value of green bonds issued in China reached US286.9 billion, ranking behind the United States with 380 billion. While issuance volumes elsewhere have declined, China’s green bond issuance increased by US$15.1 billion in 2022 an increase of 22% compared to the previous year. This growth reflects China’s determination to achieve its “double carbon” goal and has continued to receive a positive response from the market.

Green technology innovation, as a technological activity aimed at promoting green technology development and improving the ecological environment, is considered a crucial factor in coordinating economic growth and environmental protection in the pursuit of the “double carbon” goal. Theoretical research and policy formulation related to stimulating corporate green innovation has presented two distinct perspectives: “Resource Compensation” and the “Porter Hypothesis.” The former suggests promoting corporate green technology innovation through government subsidies. While moderate government subsidies are beneficial for corporate innovation, the current excessive resource compensation through environmental subsidies, coupled with insufficient supervision, hinders green technology innovation. The latter perspective emphasizes incenting green technology innovation through more stringent environmental regulations. However, scholars have demonstrated that strong environmental regulation, such as supervision costs, sewage charges, and environmental protection taxes, hurt green technology innovation. As crucial actors in green development, enterprises actively practice green development in their production and operational activities, a role that significantly contributes to sustainable economic development. However, green technology innovation is characterized by externalities, substantial investment, and high risks. Profit-maximizing enterprises are often reluctant to invest in green technology innovation without adequate motivation. In light of China’s financial market which is an important part of the world’s emerging markets, this study aims to explore whether green bonds encourage peer companies to engage in green innovation activities based on the peer learning effect.

This article presents three main contributions. Firstly, it adds to the research on the economic benefits of green bonds. While previous studies mainly focused on themselves’ issues such as maturity mismatch (Pang et al., 2022) and green premiums (R. Zhang et al., 2021), this article explores the impact of green bond issuance on peer companies. The study shows that issuing green bonds not only benefits the issuing company, but also encourages peer companies to engage in green innovation activities, providing evidence for the peer effect theory.

Secondly, it broadens the scope of research on corporate green transformation from the perspective of proactive change. While previous research mainly focused on green credit policies to assess corporate green innovation (Tan et al., 2022), this article emphasizes the significance of green bonds as a part of the green financial system. The study confirms that issuing green bonds by focal companies plays a role in transmitting “green signals” to the same industry and clarifies the internal mechanism of green bond issuance in stimulating green innovation of peer companies from the perspectives of financing constraints and R&D investment.

Thirdly, the study distinguishes between substantive innovation and strategic innovation (Liu et al., 2022; Tan et al., 2022), which is crucial for achieving “double carbon” goals. Previous research mainly concentrated on the total amount of green innovation. The findings of this study provide essential policy implications for improving the construction of the green financial system and directing financial resources to fully empower enterprises in their green transformation.

Literature Review

Research on green bonds primarily focuses on three key areas. First, the motivation behind issuing green bonds is often attributed to the so-called “green premium.” According to R. Zhang et al. (2021), green bonds offer lower financing costs compared to other bond types, and the average spread of green bond issuance is approximately 25 basis points lower. Second, regarding issuance pricing, Fatica et al. (2021) examined the yield term structures of green bonds and traditional bonds in the U.S. municipal bond market. They found that market investors expect a yield on green bonds that is higher than ordinary bonds, which leads to relatively lower issuance pricing for green bonds. Finally, regarding the economic impact, academic circles primarily examine the micro-effects of green bond issuance. For instance, Tang and Zhang (2020) found that stock prices positively responded to green bond issuance and further explored potential channels such as green attributes, institutional ownership, and stock liquidity through which green bonds affect stock valuation.

A second area of literature examines the factors influencing green technology innovation. Existing research primarily examines the impact of policy guidance, corporate financial status, and manager characteristics on green innovation. In terms of policy guidance, Liu et al. (2022) emphasized the significant improvement in the level of green innovation among heavily polluting enterprises in pilot areas due to the emissions trading pilot policy (ETS). Similarly, Tan et al. (2022) discovered that the implementation of the “Green Credit Guidelines” led to a substantial increase in overall green innovation in some restricted industries. In terms of corporate financial status, D. Li et al. (2018) underscored the tendency for companies that prioritize cost-effectiveness constraints and quality management to emphasize formalization and standardization concepts, which may inhibit corporate green innovation. In terms of manager characteristics, Quan et al. (2023) highlighted the positive influence of a CEO’s foreign experience on corporate green innovation. This effect is particularly pronounced in non-state-owned enterprises, non-heavy polluting enterprises, and companies operating in areas with lower degrees of marketization.

A third strand of literature examines the interplay between green bond issuance and green technology innovation, pertinent to this study’s focus. Previous studies have examined the impact of green bond issuance on green innovation, focusing on how it helps alleviate financing constraints (Glavas, 2023), attract investor attention (Pham and Luu Duc Huynh, 2020), and adjust investment strategies. Tolliver et al. (2021) conducted natural experiments with green bond issuance and confirmed that green bonds consistently foster corporate green innovation, particularly in non-heavy polluting industries, where the effect is more pronounced.

Upon reviewing the existing literature, it is evident that current research on the economic benefits of green bond issuance largely concentrates on issues such as shareholder wealth and corporate financing constraints. There is a dearth of studies focused on whether these economic benefits can catalyze corporate green innovation activities. While some studies have conducted relevant policy tests around the 2012 “Green Credit Guidelines,” the impact of various types of green financing methods, such as green credit, green bonds, green development funds, green insurance, and carbon finance, on corporate green innovation behaviors and mechanisms of action may vary. With China’s green bond market still in a developmental stage, uncertainty persists regarding whether the signals sent by green bond issuance will be replicated by other companies in the same industry, leading to an “innovation spillover” effect. The existing literature does not address this question. Additionally, although the financing cost of green bonds may appear to be solely linked to the issuer’s economic interests, it inherently influences the implementation of green projects across the industry and future investment directions, ultimately impacting the long-term green transformation of the national economy and the achievement of the “double carbon” goal. Therefore, our study is conducive to an in-depth exploration of the causal relationship between corporate green bond issuance and green innovation activities.

Theoretical Analysis and Research Hypotheses

This study begins by providing definitions for several key terms before delving into the mechanism of action. Firstly, the core issue addressed in this study is the green innovation spillover effect resulting from the issuance of green bonds. This effect refers to the motivation it creates for companies in the same industry to actively engage in green technology innovation. Secondly, the “focal company” is defined as the entity generating this effect, whereas “peer companies” denote other companies in the same industry, excluding the focal company (Yuan et al., 2022).

The peer learning effect among enterprises describes a scenario where decision-makers emulate or draw insights from the actions of their industry counterparts (Xiong et al., 2016). This behavior is influenced by two main factors: the uncertainty of the environment and the limited rationality of decision-makers. In an uncertain environment, decision-makers may lack the necessary causal information to accurately predict the outcomes of their actions or plans. In response to this uncertainty, companies often turn to imitating or learning from their peers as a natural strategy. By observing and learning from the actions of other companies, they can gain valuable information to better cope with the external uncertainties they face (Lieberman & Asaba, 2006). Formal and informal channels play a key role in facilitating the exchange of information among peer companies. For example, Leary and Roberts (2014) noted that stock prices of peer companies can provide insights into future growth opportunities and other relevant information. Additionally, companies also adjust their investment decisions based on signals received from their peers. Leary and Roberts (2014) discovered that corporate decisions are not only influenced by competitive strategies, but also by the learning of specific characteristics of competitor companies. This suggests that companies adjust their decisions based on what they learn from their peers, ultimately impacting their own investment choices.

Since 2016, China’s green bond market has experienced rapid development. However, many small and medium-sized companies may be unable to benefit from green bond issuance if they do not meet the specific criteria. This increases the uncertainty of their external environment. Therefore, peer companies find imitating or learning from the focal companies to be a viable and effective strategy for dealing with incomplete information and uncertainty when making investment decisions. On one hand, when the focal companies issue green bonds, they send a signal to the market about their commitment to environmental responsibility. At the same time, peer companies could compensate for the regret of not being able to issue green bonds by making strategic decisions beneficial to environmental protection. For instance, reducing pollutant emissions, developing a circular economy, and saving energy. Additionally, peer information attracts quality investors, reduces reputational risks, lowers financing costs, and encourages investment in green technology research and development. Existing studies have found a positive impact of green bond issuance on other companies in the same industry (Flammer, 2021; Tang & Zhang, 2020). On the other hand, if a company issues green bonds solely for “greenwashing,” it risks losing social trust and incurring higher financing costs. On the contrary, if green bond issuance guarantees that funds are allocated to green projects, it would lead to greater attention to the industry by society as a whole (Nygaard & Silkoset, 2023). This, in turn, can improve the efficiency of corporate investment and financing, and elevate the level of corporate green innovation. Based on the above analysis, this study hypothesizes the following:

H1: The issuance of green bonds improves green innovation among peer companies.

Compared to general innovation, green technology innovation entails a lengthy profit cycle and a high-risk coefficient (W. Zhang et al., 2022). Consequently, easing financing constraints plays a critical role in corporate green technology innovation (Hao et al., 2023; Zheng et al., 2022). It is noteworthy that the debt repayment period of green bond financing aligns well with the long cycle of green technology innovation activities (Maria Herrera & Minetti, 2007; Pang et al., 2022). Moreover, when companies issue green bonds, it generates a “signal” that spreads within the industry, broadening financing channels not only for the focal companies but also for peer companies (Yi et al., 2022; Zhao et al., 2023). This, in turn, raises substantial funds for green technology innovation. If issuing green bonds can alleviate the financial challenges of the focal company and channel capital toward environmental protection industries and organizations, it can generate green spillover effects and positively impact the focal company’s green technology innovation. From an investor’s perspective, proactive disclosure of non-financial information, such as environmental and social responsibility, by companies issuing green bonds can enhance the company’s ethical and socially conscious image. This proactive disclosure also serves to establish the company’s credibility and mitigate investors’ doubts stemming from information asymmetry (Z. Li et al., 2020; R. Zhang et al., 2021). Additionally, the high degree of homogeneity among peer companies provides an objective and realistic basis for the dissemination of green bond signals within the industry. As a result, investors infer that companies not issuing green bonds also exhibit environmental responsibility tendencies and possess green development potential. This reduces credit risk expectations for peer companies and facilitates their access to more capital for green innovation activities. Based on the analysis above, this study proposes the hypothesis:

H2: The issuance of green bonds reduces the financing constraints within industries, thereby improving green innovation among peer companies.

The enhancement of enterprises’ level of independent innovation relies on the support of R&D investment (Irfan et al., 2022; Xu et al., 2020). Before the issuance of green bonds, insufficient resources flowed into green technology innovation due to higher R&D costs and lower environmental governance pressure. In cases where companies can meet environmental governance standards through direct investment in environmental protection, they may opt to forego more challenging green innovation activities (Liu et al., 2022; Lv et al., 2021). However, the issuance of green bonds can promote R&D investment through financing cost channels and social supervision channels. Firstly, the “green” premium attached to green bonds can reduce whole industries’ R&D costs, thereby increasing their willingness to allocate funds to R&D. Secondly, the more stringent environmental information disclosure system associated with green bonds enables investors to make more accurate valuation decisions based on a company’s environmental performance (El Ghoul et al., 2018). Consequently, with the entire industry receiving high attention, peer companies have incentives to increase their investment in R&D and enhance their environmental competitiveness. While R&D investment does not necessarily have a direct proportional relationship with output outcomes, higher R&D investment leads to a greater accumulation of human capital and technical knowledge, thus providing support for innovation output (Peng et al., 2020). Therefore, the issuance of green bonds contributes to a “resource effect” on corporate green innovation by incentivizing peer companies’ R&D investment. Based on the analysis above, this study proposes the hypothesis:

H3: The issuance of green bonds prompts R&D investment within industries, thereby improving green innovation among peer companies.

Research Design

Sample Selection and Data Sources

Data from Chinese A-share listed companies spanning from 2010 to 2020 were collected for this study. Financial data were obtained from the Wind database and data on green patents were obtained through comprehensive screening and sorting of patents from the State Intellectual Property Office, based on the green patent classification standard published by the World Intellectual Property Organization. ST, *ST, PT, and financial firms were excluded. All continuous variables were winsorized at the 1% and 99% thresholds to mitigate extreme values.

To ensure the continuity of corporate annual data, this article retains companies with a listed company age of more than 10 years during the data cleaning process. After cleaning, a total of 11,336 observations were obtained, including 288 observations for green bonds and 11,048 observations for ordinary bonds. To study the peer issues, we removed green bonds issued by the focal companies and then eliminated 1,173 missing values, resulting in 9,875 observations. This study provides the number of green bonds issued by each industry in the sample since 2016 in Appendix 1.

Empirical Models and Variable Specification

Baseline Model

To begin with, this study estimates the following specification:

Where i denotes the companies, t denotes the year, and ε denotes the random disturbance term. Gp is the dependent variable, indicating the level of green technology innovation of peer companies; Green is the core independent variable, indicating the dummy variable affected by the focal companies; Controls denotes a series of control variables. This study uses the lag as one of the control variables to alleviate possible endogeneity in the regression model. We control the firm fixed effect

Variable Definition and Description

Independent Variable

Gp represents the green innovation level of peer companies, which is measured by the number of green patents they have acquired. Green patents are commonly employed as the level of green innovation (Barros, 2021; Yao et al., 2020). Additionally, drawing on W. Zhang et al. (2022), this study further categorizes green technology innovation into strategic innovation (Gup) and substantive innovation (Gip).

Green invention patents possess higher technical content and present a greater level of difficulty, making them high-level technological innovation projects. Conversely, green utility patents exhibit lower technical levels and are relatively less challenging, often utilized to cater to government policies. Consequently, this study categorizes corporate green technology innovation into two dimensions: substantive green innovation and strategic green innovation. Specifically, the quantity of granted green invention patent authorizations serves as a measure of substantive green innovation, while the quantity of granted green utility patent authorizations serves as a measure of strategic green innovation. Finally, during the estimation process, these three green patent authorizations are respectively increased by 1 and then logarithmically transformed.

Dependent Variable

Green is a dummy variable, that represents an explanatory variable in the Staggered DID model (i.e.,

Control Variables

Controls represents control variables. We control for the following variables: enterprise size (Size), debt level (Lev), profitability (Pot), enterprise age (Age), cash flow (Oct), proportion of independent directors (Indratio), and ownership concentration (Top), and nature of property rights (SOE) as control variables. All variables are defined explicitly in Table 1.

Variable Definitions.

Descriptive Statistics

Table 2 presents the result of descriptive statistics. As shown in Table 2, it can be seen that companies affected by the issuance of green bonds by the focal companies account for approximately 42% of the total sample. The average number of green patents is 0.2, and the maximum value is 6.27; the average number of green invention patents is 0.09, and the maximum value is 5.14; the average number of green utility patent authorizations is 0.14, and the maximum value is 6.22. This result shows that the level of green technology innovation is still low. The remaining control variables are consistent with the existing literature.

Variable Descriptive Statistics.

Empirical Analysis

Benchmark Regression Analysis

Table 3 presents the relationship between the issuance of green bonds and green innovation, as determined by the Staggered DID model. In Column (1), the relationship between the focal companies’ issuance of green bonds and peer companies’ green technology innovation is examined. The coefficient of Green is 0.045 and significant at the 1% level. Columns (2) and (3) explore the relationship between the focal companies’ issuance of green bond issuance and substantive innovation and strategic innovation of peer companies, respectively. The results indicate positive coefficients for Green in both cases, with significance levels of at least 10%. Particularly noteworthy, the coefficient for strategic innovation is significantly larger than that for substantive innovation.

Benchmark Regression Results.

Note:***, ** and * represent significance at 1%, 5% and 10% levels, respectively.

Respectively, columns (4), (5), and (6) introduce a series of control variables. The coefficients of Green regression results are still positive and statistically significant at least at the 5% level, demonstrating a certain degree of robustness, that is the focal companies’ issuance of green bonds has significantly fostered green technology innovation among peer companies, resulting in an apparent “innovation spillover” effect. Moreover, it is noteworthy that, when the focal companies issue green bonds to stimulate peer companies’ green innovation, strategic innovation is about twice as high as substantive innovation.

Several factors may underpin this outcome. Firstly, companies driven by the goal of maximizing profits may focus on increasing the quantity of green innovations in the short term, without delving into more intricate green innovations to secure green bond financing. Additionally, when firms within the same industry witness that the issuance of green bonds by prominent companies can mitigate financial restrictions, they too may seek to obtain additional financing through similar means, potentially resorting to strategic green innovation as a form of greenwashing. Overall, this result supports the hypothesis H1.

Robustness Tests

To further verify the reliability of the conclusions of this study, we conducted the following robustness tests.

According to Tan et al. (2022), certain scholars have suggested that China’s green credit policy has had a notable impact on promoting green technology innovation among companies within the same industry. Coincidentally, the time frame of this policy aligns with the period covered in this study’s sample. To ensure the conclusions are not confounded by the influence of this policy, this article will exclude the sample group of enterprises affected by the green credit policy and conduct a revised regression test.

Based on the research conducted by Tan et al. (2022), this study classifies listed companies operating in the “high pollution, high energy intensity, and over-capacity (THOS) industries” as green credit-restricted industries. These industries include nuclear power generation, hydropower generation, water conservancy and inland port engineering and construction, coal mining and washing, oil and natural gas mining, ferrous metal mining and dressing, non-ferrous metal mining and dressing, non-metal mineral mining and dressing, and other mining industries. If a listed company falls into any of these nine industries after 2013, it is considered to be affected by the green credit policy and is consequently excluded from the sample data. The model is then re-estimated, and the results are presented in columns (1), (2), and (3) of Table 4.

Robustness Tests.

Note:***, ** and * represent significance at 1%, 5% and 10% levels, respectively.

Secondly, as there may be a time delay in green innovation, this paper incorporates the average value of green patents from the preceding 3 years as an alternative variable for re-testing in Model (1). The obtained regression results are displayed in Columns (4), (5), and (6) of Table 4.

After a series of robustness tests such as excluding policy interference and adding fixed effects, this study found that the coefficient of Green is still positive and is significant at least at the 5% level, indicating that the conclusion of this article is reliable, that is, the issuance of green bonds by the focal companies has an obvious “innovation spillover” effect.

Parallel Trend

To evaluate the treatment effects in each period, we estimate the model (2):

where,

Figure 1 shows the dynamic effects of innovation levels in corporate green technology. Specifically, Figure 1a depicts the temporal trend of the average level of green patents in the industry. The analysis of the figure demonstrates an upward trend in the total green patents, green invention patents, and green utility patents since 2016. Moreover, the upward trend is particularly pronounced for the total green patents and green utility patents. This dynamic trend aligns with the findings of the basic regression analysis. Figure 1b to d present the results of the parallel trend tests conducted on the total green patents, green invention patents, and green utility patents, respectively. The figure analysis reveals that before the influence of green bond issuance on green patents, there were no significant differences observed between the treatment group and the control group, signifying the comparability of the two groups. However, after the impact of green bond issuance in the same industry, there is a significantly positive difference between the treatment group and the control group, and this trend continues to rise. This result verifies that the conclusion of this study passes the parallel trend test.

Green innovation dynamic effect: (a) industry average level of green innovation by year, (b) green innovation dynamic effects, (c) green invention innovation dynamic effects, and (d) green utility innovation dynamic effects.

Placebo Test

This study applies a method of randomly selecting the time and issuing company for green bond issuance, thus constructing a counterfactual experiment resembling the sample to validate the causal relationship, which is referred to as a placebo test (W. Zhang et al., 2022). Since the “pseudo-Green” is generated randomly through the aforementioned process, it is predicted that the estimated coefficient of “pseudo-Green” tends to be close to zero. The model estimation was repeated 500 times using the same random process, and a kernel density map of the estimated coefficients was generated (Figure 2) for the placebo test. The results reveal that the mean values of the estimated coefficients generated through the random process are in proximity to zero. These findings provide reliable evidence supporting the conclusion that the issuance of green bonds by the focal companies has a “spillover effect” on the level of green innovation among peer companies.

Placebo test.

Mechanism Analysis

Drawing on the method of Di Giuli and Laux (2022), this study employs a two-stage test approach. First, in the first stage, estimate the impact of Green on the mechanism variable (M); in the second stage, use the fitting mechanism variable (

where, M is the mechanism variable,

Mechanism Analysis of Financing Constraints.

Note:***, ** and * represent significance at 1%, 5% and 10% levels, respectively.

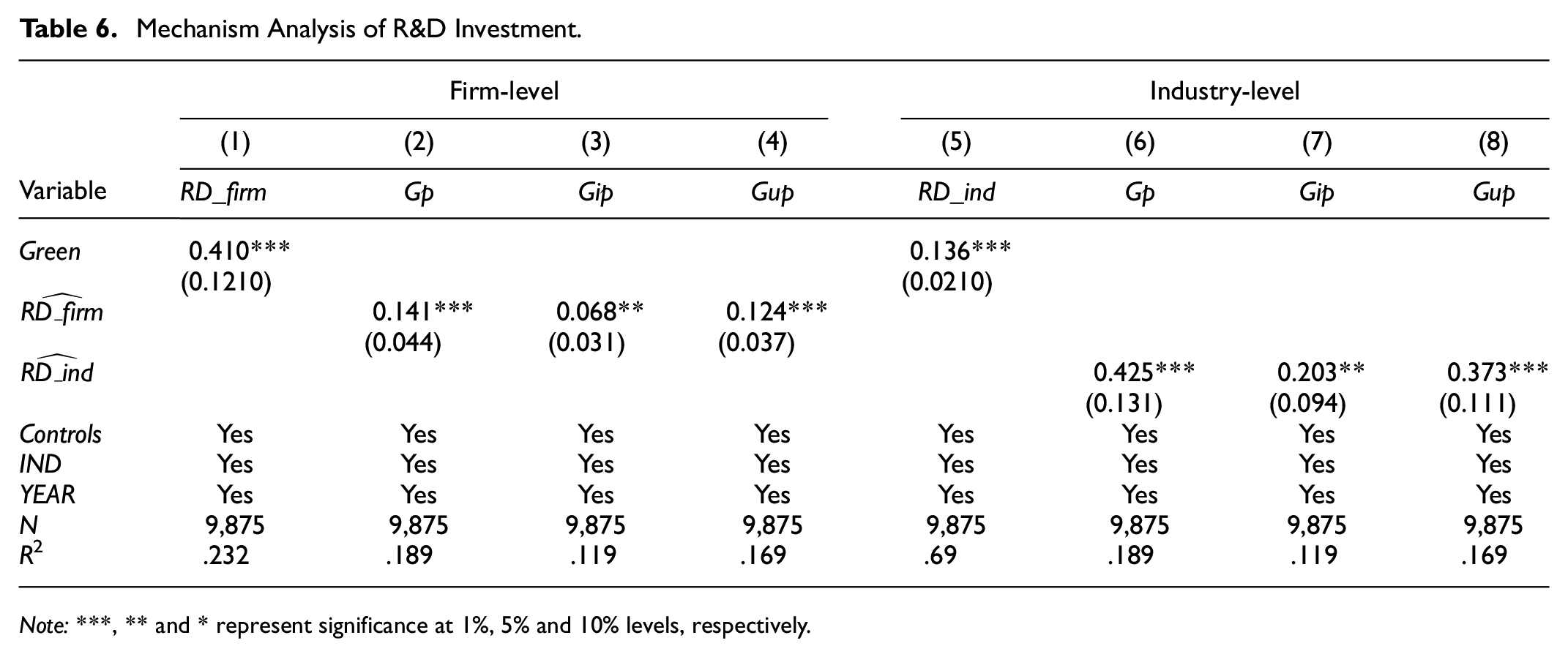

Mechanism Analysis of R&D Investment.

Note:***, ** and * represent significance at 1%, 5% and 10% levels, respectively.

Firstly, regarding the perspective of financing constraints. Drawing on Glavas (2023) this study used the SA index as a proxy variable to evaluate corporate financing constraints. This study calculated both firm-level (SA_firm) and industry-level (SA_ind) financing constraints, and the industry-level SA index is the median value of the industry SA index. The results are presented in Table 5. In column (1), the coefficient of Green is −0.254 and exhibits significance at the 1% level, indicating that the issuance of green bonds significantly mitigates the level of financing constraints among peer companies. The coefficient of

Furthermore, regarding the perspective of R&D investment. This study utilizes the natural logarithm of enterprise R&D expenditure as a proxy variable to assess R&D investment. This study calculated both firm-level (RD_firm) and industry-level (RD_ind) R&D investment, and the industry-level RD index is the median value of the industry RD index. The test results are presented in Table 6. In column (1), the coefficient of Green is 0.410 and exhibits significance at the 1% level, indicating that the issuance of green bonds has significantly increased the R&D investment levels of peer companies. The coefficient of

Heterogeneity Analysis

To explore the heterogeneous effects of the “innovation spillover” from green bond issuance, this study categorizes the sample into labor-intensive and capital-intensive enterprises, as well as industries with high and low concentration. Regression analysis is then conducted, and the corresponding results are presented in Tables 7 and 8.

Heterogeneity of Enterprise Nature.

Note:***, ** and * represent significance at 1%, 5% and 10% levels, respectively.

Heterogeneity of Industry Concentration.

Note:***, ** and * represent significance at 1%, 5% and 10% levels, respectively.

Firstly, drawing on Khedmati et al. (2020), this study classifies enterprises into two categories: labor-intensive enterprises (defined as those with per capita capital greater than the industry’s median per capita capital) and capital-intensive enterprises (defined as those with per capita capital less than the industry’s median per capita capital). The results are presented in Table 7. The coefficient of Green is positive and statistically significant at least at the 10% level for capital-intensive enterprises.

This result likely stems from the intrinsic characteristics of green technology innovation. Green technology innovation is characterized by long cycles and high risks, necessitating enterprises engaged in green innovation activities to possess ample financial resources as support. Labor-intensive enterprises primarily rely on labor input and the accumulation of labor experience in their production activities. Their product technology tends to have low added value, with competitive advantages primarily centered around cost and output rather than innovation activities (M. L. Wang, 2023). On the other hand, capital-intensive enterprises benefit from adequate capital reserves, enabling them to provide essential financial support for corporate innovation activities (Cai et al., 2020). Consequently, the influence of green bond issuance in stimulating green technology innovation activities among peer companies is particularly evident within capital-intensive firms.

Secondly, the Herfindahl–Hirschman Index (HHI) is employed to gauge the concentration level at the industry level. A higher index value indicates greater industry concentration, which corresponds to lower market competitiveness (Yannelis & Zhang, 2023). The results are displayed in Table 8. The analysis of the table reveals that the coefficient of Green is positive and statistically significant at least at the 10% level for high industry concentration (low market competitiveness).

Generally speaking, monopoly or oligopoly companies can leverage their strong market position and advantages to exert control over prices, leading to the acquisition of excessive profits in the market. In industries characterized by higher concentration (indicating lower market competitiveness), companies possess stronger monopoly advantages, allowing them to secure ample funds through enhanced bargaining power (Selwyn & Leyden, 2022; Z. Zhang et al., 2022). When faced with competitive pressure from peers who issue green bonds, companies can secure sufficient funds for implementing green innovation initiatives through their strong bargaining power. In such instances, as the concentration in the industry decreases (indicating higher market competitiveness), companies find themselves in a weaker position with diminished bargaining power. When confronted with competitive pressure arising from the issuance of green bonds by peers, companies may lean towards adopting more conservative measures for emission reduction, rather than engaging in green innovation activities.

Conclusion and Policy Suggestions

Green bonds play a vital role in China’s green financial system, serving as an important driver of green recovery and supply-side structural reform in the post-epidemic era. This paper utilizes green bonds as a case study and employs a staggered DID model to investigate the spillover effects of green bond issuance on the green technology innovation of peer companies. The findings affirm that the issuance of green bonds strongly facilitates the enhancement of peer companies’ green innovation levels, thus exhibiting a positive impact on both green invention patents and green utility patents. Moreover, these effects are sustainable over time. These results not only validate the effectiveness of peer learning within the bond market but also expand the economic benefits associated with green bonds. The Mechanism analysis demonstrates that the issuance of green bonds fosters green innovation by alleviating financing constraints and increasing investment in research and development (R&D). The findings aid management in ensuring the enterprise’s sustainable development by informing strategic decision-making. Additionally, through heterogeneity testing, it is discovered that the “innovation spillover” effect of green bond issuance is particularly significant in capital-intensive industries and those with high concentration.

This study contributes to the existing literature by examining the causal link between green bond issuance and corporate green innovation activities. However, there are still some limitations. Firstly, due to data accessibility issues, there is a need for further in-depth discussion on the subsequent economic impact of substantial green innovation and strategic innovation. For instance, empirical evidence is required to better understand the relationship between green innovation and greenwashing. Secondly, this study is grounded in the “peer learning” theory and tests the hypothesis that the issuance of green bonds by a company reduces the financing constraints of peer companies, increases their R&D investment and stimulates them to engage in green innovation. Nevertheless, it is important to acknowledge that there may be additional factors influencing companies’ decisions to pursue green innovation activities, which necessitates further exploration. For instance, government environmental regulations could serve as an external inducement for companies to engage in green innovation activities.

The findings of this research offer valuable insights for national policies on financial environmental protection and corporate strategies for environmental sustainability. Firstly, there is a need to continue promoting the growth of the green bond market and optimize the institutional arrangements surrounding green bonds, thus maximizing the role of green “signal” dissemination. Among the reasons why green bonds possess financing advantages, it is vital to acknowledge that it is not solely due to the promotion of relevant policies. More importantly, comprehensive and stringent information disclosure plays a pivotal role in reducing information asymmetry and enabling investors to make well-informed investment decisions. Therefore, it is imperative to strengthen the information disclosure system for green bonds, mandate regular disclosure of the latest progress of green projects and the environmental benefits achieved, and minimize information asymmetry.

Secondly, there is a need to enhance the promotion and awareness of green investment and responsible investment concepts, fostering a culture of green investment across all sectors. This can be accomplished by establishing diverse communication and learning platforms to enhance investors’ understanding of “green” concepts. Encouraging more investors to prioritize and invest in corporate green projects, guiding the general public to take note of corporate environmental information, and ensuring corporations fully comprehend the dual function of green finance as a tool will all help advance the “green and efficient” development of the capital market.

Thirdly, the real economy should be encouraged to invest in green industries utilizing market-oriented means to stimulate enthusiasm for corporate social responsibility and facilitate high-quality development in this sector. To this end, further improvements must be made to the green bond market system. Local governments should be incentivized to establish substantive preferential policies such as green bond discounts, cash rewards, tax exemptions, and policy guarantees. This will invigorate market participants’ enthusiasm for engagement in the green bond market and allow for the full realization of both the environmental effects and wealth effects of green bonds.

Footnotes

Acknowledgements

Thanks to the Humanities and Social Sciences Project of the Ministry of Education of China; and the National Social Science Foundation of China for funding.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Ministry of education of Humanities and Social Science project of China [grant numbers 21YJA790004]; and the National Social Science Fund of China [grant number 22BJL007].

Data Availability Statement

All relevant data are within the paper.