Abstract

This study offers a behavioral explanation for peer influence on dividend payments in China. It specifically shows how investors’ reliance on reference points leads them to value the dividends of a focal firm more highly when these dividends align with those of peer firms. Managers cater to these investor preferences to capitalize on short-term mispricing, as suggested by the catering theory. Using data from A-share non-financial listed companies on the Shanghai and Shenzhen stock exchanges from 1995 to 2023, this study examines the peer influences of both cash and stock dividends separately using the instrumental variable method, confirming the presence of both effects. Detailed analyses demonstrate that the catering theory is more strongly associated with the influence of cash dividends than with that of stock dividends. The influence of cash dividends is especially pronounced under conditions of high arbitrage restrictions, short managerial horizons, or low catering costs, which supports the catering explanation. This study not only complements existing theoretical explanations for peer influences on dividends but also enriches the catering theory proposed by Baker and Wurgler, providing empirical evidence of dividend peer influences in emerging capital markets.

Introduction

Traditional financial theory asserts that a firm’s financial decisions are primarily determined by its own characteristics and operate independently of the decisions made by other firms. However, recent studies challenge this notion, revealing that the financial choices of a firm are considerably influenced by the actions of its peer firms within the same reference group. This peer influence plays a pivotal role in shaping major financial decisions, such as corporate capital structure (Leary & Roberts, 2014), stock splits (Kaustia & Rantala, 2015), IPOs (Aghamolla & Thakor, 2021), and investment strategies (Bustamante & Frésard, 2021).

Dividend distribution is recognized as a critical financial decision. Traditional dividend theories, such as those proposed by Miller and Modigliani (1961) and Bhattacharya (1979), fail to fully explain the observed similarities or convergence in dividend policies among firms. Expanding the scope of research to include industry-wide analyses, Grennan (2019) and Adhikari and Agrawal (2018) found that a firm’s cash dividend decisions are significantly influenced by the dividend policies of peer firms within the same industry. They propose two main theoretical frameworks: the first centers on industrial competition, suggesting that firms closely monitor and respond to the dividend decisions of their peers to maintain competitive parity. The second framework emphasizes information acquisition, proposing that managers glean insights by observing the behavior and characteristics of other comparable firms, using this knowledge to inform their decision-making processes. These theories underscore the impact of peer behaviors and information on a firm’s actions, yet often neglect the crucial role of investors.

Investor needs should be a primary consideration when a company devises its dividend policy. Furthermore, classical dividend theories already integrate investor behaviors and characteristics into their models (Baker & Wurgler, 2004a; Bhattacharya, 1979; Elton & Gruber, 1970; Farrar & Selwyn, 1967; Rozeff, 1982). By incorporating the influence of investors into our understanding of dividend peer effects, we can achieve a more comprehensive perspective on corporate behavior.

This study proposes that managers adopt the dividend decisions of their peers to cater to the psychological reference points of investors, a phenomenon termed managerial catering, consistent with catering theory (Baker & Wurgler, 2004a). This leads to peer influences on dividend distribution. Recognizing the distinct purposes of cash and stock dividends, the study separately investigates peer influences on these two types of dividends, referred to as cash-cash and stock-stock influences. The existence of these peer influences is confirmed, and their robustness is supported by three additional tests. To further understand the role of managerial catering in these peer influences, the study examines the impact of arbitrage restrictions, managerial horizons, and catering costs on dividend peer influence. The findings suggest that catering theory is related to the influence of cash dividend peers and, specifically during periods of high stock dividends, to the influence of stock dividend peers.

The research contributes to the field in several ways. Firstly, it both theoretically analyzes and empirically examines the peer influences on stock dividend payments. Prior studies, such as those by Adhikari and Agrawal (2018) and Grennan (2019), which focus on data from publicly listed firms in the United States, primarily address the peer influences of cash dividends and share repurchases. In contrast, stock dividends are a significant form of dividend payment for publicly listed companies in China and are highly valued by investors. Thus, the Chinese capital market offers a unique context for studying stock dividend distributions. While Yan and Zhu (2020) also explore the peer influences of dividend payments among Chinese listed companies, they aggregate cash dividends, stock dividends, and reserve transfers, which complicates the separate analysis of cash and stock dividends’ peer influences. This research, therefore, provides a more detailed analysis of stock dividend peer influences within the Chinese capital market context.

Second, this study broadens the exploration into the mechanisms underlying cash dividend peer influences. Prior research, utilizing samples from publicly listed companies across various countries, has established the significance of these influences (Adhikari & Agrawal, 2018; Grennan, 2019; Lee & Seo, 2023; Yan & Zhu, 2020). However, the mechanisms driving this phenomenon are not well-understood. Lieberman and Asaba (2006) proposed competition and information acquisition as potential explanations, but these fail to consider the significant role of investors. Consequently, this study builds on the framework that managers address the demands of irrational investors by catering to their dependency on peer reference points, aiming to boost short-term stock prices. Moreover, it investigates how arbitrage constraints, managerial horizons, and catering costs influence cash dividend peer influences, drawing on dividend catering theory by Baker and Wurgler (2004a).

Third, this study contributes new empirical evidence to the field of behavioral finance. Traditional financial theory posits that capital markets are perfect and that both managers and investors act rationally to maximize benefits. In contrast, behavioral finance recognizes that rationality is limited for both parties. This discrepancy has led to the development of three theoretical frameworks: irrational investors with rational managers, irrational managers with rational investors, and both parties being irrational. In this context, investors are irrational, showing dependency on peers’ dividend reference points. Under stringent arbitrage constraints, with more myopic managers and minimal catering costs, managers are more likely to cater to investors, thereby intensifying the impact of dividend peer influences.

The remainder of this study is organized as follows: Section 2 presents the literature review and hypothesis development. Section 3 describes the data and methodology. Section 4 provides the results of summary statistics, peer effect tests, robustness checks, catering mechanism tests, and further analysis. Section 5 offers the conclusions of this study.

Literature Review and Hypothesis Development

Peer influence suggests that individual behavior within a reference group is dictated by the average actions of others in the group, a phenomenon known as endogenous social interaction (Manski, 1993). Research across education and sociology demonstrates substantial peer impact on both academic performance and social behavior (Burke & Sass, 2013; Asirvatham et al., 2014; Choi et al., 2018; Griebeler, 2019). Similarly, corporate finance studies have revealed parallel patterns of peer influence in corporate behaviors and decision-making, including corporate social responsibility (Cao et al., 2019), capital structure (Leary & Roberts, 2014), cash holdings (Chen et al., 2019), stock splits (Kaustia & Rantala, 2015), and IPO decisions (Aghamolla & Thakor, 2021).

Researchers such as Adhikari and Agrawal (2018) and Grennan (2019) note significant peer impact on the dividend policies of companies listed in the U.S. within their respective industries. This influence is primarily analyzed through competition theory and information acquisition theory, which provide insights into the forces driving peer effects in dividend strategies. However, these theories fall short in addressing the role of investors directly.

The theoretical frameworks related to the decisions of investors and managers are grouped into four categories: rational managers with rational investors, irrational investors with rational managers, irrational managers with rational investors, and both irrational managers and investors. In an ideal capital market, where both managers and investors are rational, the market price of a firm would accurately reflect its intrinsic value. However, when faced with irrational investors, managers often adapt their strategies to cater to these investors’ preferences, particularly to correct short-term price misalignments. Baker and Wurgler (2004a) introduced the catering theory, which highlights how managers adjust to investor characteristics and preferences. Given the relative immaturity of the Chinese capital market, characterized by a high volume of individual investors and their speculative tendencies, the catering theory is especially pertinent in explaining the interactions between managers and irrational investors.

Baker and Wurgler (2004a) initially proposed the catering theory of dividends. They asserted that “the decision to pay dividends is driven by prevailing investor demand for dividend payers. Managers cater to investors by paying dividends when investors put a stock price premium on payers and by not paying when investors prefer non-payers.”Baker and Wurgler (2004b) further provided empirical evidence that the propensity to pay dividends increases when a proxy for the stock market dividend premium is positive and decreases when it is negative. Additionally, Baker et al. (2009) suggested that when investors assign higher valuations to low-priced firms, managers respond by issuing shares at lower price levels, and vice versa. In summary, managers in markets with limited arbitrage cater to the preferences and characteristics of investors to boost the short-term stock price.

Building on the catering theory, the reason managers mimic the dividend decisions of their peers is to align with the psychological reference points of investors, thereby aiming to enhance the stock price of their own firm. Managers understand that investors use the dividend payouts of their peers as benchmarks; consequently, they align their dividend decisions with those of their peers to cater to investor expectations.

Specifically, investors often demonstrate reference point dependence, a behavioral bias common in individual decision-making (Bleichrodt, 2007). Decision-makers focus more on changes in economic conditions relative to a reference point than on the absolute outcomes. Generally, investors have used historical or recent benchmarks (Arkes et al., 2008), expectations, and comparisons with others (C. H. Lin et al., 2006) as reference points for their stock investment decisions. Regarding dividend distribution, investors exhibit a psychological dependence on a firm’s historical dividends as a reference point. Baker et al. (2016) proposed the behavioral dividend signaling model, suggesting that investors use the dividend amount from the previous period as a psychological reference point for the current period’s dividends. This study indicates that the dividend decisions of peer firms can also serve as crucial psychological reference points for investors when assessing the attractiveness of a firm’s dividend decisions. In this context, investors show greater demand and preference for firms whose dividends are close to or exceed those of their peers and show aversion to firms whose dividends are significantly lower than those of their peers. By anchoring their dividend payments to those of peer firms and distributing dividends similar to their peers, firms cater to the psychological reference points of investors, making them more likely to be favored by investors.

Catering to investors’ psychological reference points may lead to an increase in the current share prices of businesses within markets characterized by limited arbitrage capital. Consequently, managers are likely to cater to these reference points and capitalize on recent increases in stock prices, thereby contributing to the phenomenon of dividend peer influence. Based on the preceding analyses, the following hypothesis is proposed:

The theoretical model for catering developed by Baker and Wurgler (2004a) identifies three critical factors that influence catering behavior: arbitrage restrictions, the managerial horizon, and the costs associated with catering. This study conducts a detailed analysis of the impact of these three factors on the peer influence of dividend decisions.

Arbitrage restriction is identified as the primary factor influencing stock prices. Baker and Wurgler (2004a) observed that limitations on arbitrage significantly allow investor demands to influence a firm’s current stock price. Although arbitrageurs typically help correct prices to reflect fundamental values, they face numerous challenges in typical capital markets. For instance, short-term arbitrageurs experience “noise trader risk” (Shleifer, 2000), a risk arising when prices deviate from their fundamental values due to noise traders’ actions and may be further manipulated. This scenario can force short-term arbitrageurs to exit their positions prematurely, often at a loss. Like ordinary investors, arbitrageurs are risk-averse. Research has shown that factors such as high informational uncertainty, low shareholder sophistication, and significant potential transaction costs (Ali et al., 2003; Lam & Wei, 2011; Y. E. Lin et al., 2020) can heighten arbitrageurs’ perceived risks and reduce their risk tolerance, thus restraining arbitrage activities. These limitations may allow an inflated stock price to persist, benefiting the catering firm through a short-term stock premium. Therefore, greater arbitrage restrictions not only enhance the incentive to cater but also amplify the peer influence on dividend decisions. This leads to the formulation of hypothesis 2.

The second factor involves the managerial horizon. Managers assess the benefits of catering to current mispricing against the associated costs before deciding whether to imitate their peers. This managerial trade-off is influenced by the managerial horizon, which determines how much emphasis is placed on the current stock price versus the long-term value of the company. The longer the managerial horizon, the greater the emphasis on the firm’s long-term value. Managers often pursue private benefits from rising stock prices, such as enhancing the value of CEO stock options (Aboody & Kasznik, 2000; Yermack, 1997), facilitating insider sales (Lou, 2014), and warding off hostile takeovers. Due to these incentives, they frequently display short-sighted and self-interested behavior (Haynes et al., 2015). Their tenure is finite, leading them to prioritize the firm’s value only within their term of office. They focus primarily on their performance and the benefits accruing during their tenure. However, mechanisms such as stock options (Bergstresser & Philippon, 2006; Stein, 1989) and compensation plans (Garel, 2017) are designed to mitigate managerial myopia, introducing variability in managers’ horizons across different companies. Additionally, the length of a manager’s remaining tenure can influence their horizon—a new manager with a long tenure ahead tends to have a longer horizon, whereas one nearing departure may become more self-interested and short-sighted. In summary, the shorter the managerial horizon, the greater the emphasis on short-term stock premiums and the stronger the influence of peer dividends. This leads to the formulation of hypothesis 3:

The third factor pertains to the costs of catering, which also affect managerial trade-offs. Catering to investor demands and imitating peer firms’ dividend payments can incur additional costs. According to the perfect market hypothesis, the cost of paying dividends is negligible, and dividend decisions do not impact the firm’s long-term value, which depends on the cash flows generated by investment projects (Miller & Modigliani, 1961). However, in an imperfect market, imitation behavior may involve costs due to the trade-off between dividend decisions and investment decisions. For firms with substantial internal profits and cash flows, the cost of imitating other companies in paying dividends is relatively low. Conversely, for firms with limited internal profits and cash flows, an increase in dividend payments may diminish the funds available for investment projects. These firms might resort to external financing to support both dividends and investment projects, leading to high imitation costs. Based on this discussion, hypothesis 4 is proposed:

Data and Methodology

Data Description

The financial and stock trading data utilized in this study are derived from the China Stock Market & Accounting Research (CSMAR) Database. This research encompasses data from all A-share listed companies on the Shanghai and Shenzhen stock exchanges from 1995 to 2023. After excluding financial firms and those designated as under special treatment (ST and PT) and removing instances with missing values, the dataset includes 37,833 firm-year observations across 3,301 firms. Continuous variables have been winsorized at the 1st and 99th percentiles to mitigate the influence of outliers. Additionally, these variables have been standardized—adjusted to have a mean of zero and a standard deviation of one across the sample—to simplify the interpretation of the coefficients, as discussed in prior studies (Feld & Zölitz, 2017; Grennan, 2019; Leary & Roberts, 2014).

Selecting an appropriate reference group is crucial, as it supports the analysis of dividend peer influence, which examines the interactions of dividend payments among firms within the same group. The Shenyin Wanguo tertiary industry classification standard is utilized to define the reference group owing to its enhanced accuracy in identifying peer firms within specific industry divisions (Zhang et al., 2022). This method is consistent with the methodologies outlined by Leary and Roberts (2014). As a result, the dataset encompasses 158 industries and 3,196 year-industry observations, averaging 12 firms per industry.

Model and Variables for Dividend Peer Influence

The empirical investigation of peer influence on corporate dividend payments is conducted using model (1). Hypothesis 1 is tested by assessing whether the dividend payments of peer firms significantly and positively influence the dividend payments of the focal firm. The following are the details of the model and variables:

Probit and Tobit models are utilized, depending on the nature of the dependent variables. The variable Dividt denotes either the cash or stock dividend of firm i in industry d during period t. In China, cash and stock dividends represent two distinct yet essential forms of dividend distribution. These forms are analyzed in two aspects: the propensity to pay dividends and the dividend level. The propensity to pay dividends is measured using a binary variable that equals 1 if a firm pays dividends and 0 otherwise. The dividend level is assessed using the dividend per share (DPS).

The independent variable, PeerDiv-idt, calculates the average cash or stock dividend of other firms within the same industry as firm i (excluding firm i itself) over period t. This variable represents the dividend payments of peer firms. Similarly to the focal firm’s dividends, peer firms’ dividends are analyzed in terms of their propensity to pay dividends and their dividend levels. The propensity to pay dividends among peer firms is evaluated by the proportion of these firms that pay dividends. The average DPS among these firms is used to assess the level of dividends.

In alignment with Hypothesis 1, model (1) anticipates that β significantly exceeds zero, indicating that the dividends of peer enterprises positively influence the dividends of the focal firm.

In the analysis of control variables, the need for refinancing (RFN) is utilized to address the impacts of China’s dividend regulation policy. RFN is defined as the inclination of publicly listed companies to issue additional shares and convertible bonds in the capital market. According to the regulation policy, companies with refinancing needs must ensure that their dividend distributions over the past 3 years comply with the policy stipulations. If a company plans to refinance within the next 3 years, it must adjust its current year’s dividend distribution to meet these policy requirements. RFN is assigned a value of 1 if a firm announces a refinancing plan for the current year, the following year, or the year after next; otherwise, it is assigned a value of 0.

Additionally, the model incorporates other variables that influence dividend distribution, as identified in prior research (Brav et al., 2005; Fama & French, 2002; Harris & Raviv, 1991; Myers, 1984; Nguyen & Wang, 2013). These variables include asset tangibility (Tang), book leverage (Debtr), profitability (Profit), growth (SGR), cash flow risk (CFR), firm size (Size), maturity (Age), market assets to book ratio (MABA), stock price (Price), and life cycle (RETE). The definitions of these variables are provided in Table 1. In model (1), Controlsidt represents the control variables for the focal firm i in industry d in year t. PeerControls-idt denotes the control variables for peer firms, defined as the average of the corresponding variables across all peer firms. The model also includes controls for industry fixed effects (Id) and year fixed effects (Tt).

Variable Descriptions.

Construction of Instrument Variables

Manski (1993) suggested that a reflection problem arises when model (1) is used to estimate peer influence. Specifically, it is difficult to determine whether group behavior influences individual behavior or merely reflects it. To address this endogeneity, the instrumental variable method is employed to examine peer influence.

In the existing research (Adhikari & Agrawal, 2018; Grennan, 2019), peers’ idiosyncratic returns and idiosyncratic risks serve as two instrumental variables for the endogenous variable of peers’ dividend payments. Idiosyncratic returns (IdioRet) are defined as the change in stock price attributable to firm-specific factors, i.e., the difference between the actual stock return of the firm and the expected stock return based on systematic factors. Idiosyncratic risk (IdioRisk) refers to the volatility of idiosyncratic returns, measured by the standard deviation of monthly idiosyncratic returns.

The extended Fama-French three-factor model (Fama & French, 1993) is initially used to calculate expected stock returns

In model (2),

In model (3),

Instrumental variables must satisfy the relevance and exclusion restriction criteria to be considered valid. Detailed analyses have been conducted, demonstrating that the mentioned instruments meet these criteria. Due to word limits, the validity of the instruments is discussed in Supplemental Materials.

Model and Variables for Catering Mechanism

Model (4) is adopted to examine hypotheses 2–4, whether arbitrage restrictions, the managerial horizon, and the cost of catering have the expected effects on cash and stock dividend peer influence, respectively.

Model (4) conforms to model (1) by introducing the interaction term between peer firms’ dividend payments (PeerDiv-idt) and the factors (Factoridt). Factoridt represents the measurement variables of arbitrage restrictions, the managerial horizon, as well as the catering cost. In accordance with Leary and Roberts (2014), peer firms’ dividends are interacted with indicator variables identifying the respective factor’s lower and upper thirds. Accordingly, the corresponding interactions between idiosyncratic return and indicator variables serve as instruments for previous interaction terms.

Following Ali et al. (2003) and Lam and Wei (2011), the trading volume (Volume) and the number of institutional shareholders (Inst#) are employed to measure arbitrage restrictions. The lower trading volume up-regulates the transaction costs, such that a greater limit is imposed on arbitrage. The number of institutional shareholders measures investor sophistication, thus reducing arbitrage risk and further decreasing the arbitrage restrictions.

The horizon of the manager is examined using option incentives (Option) (Bergstresser & Philippon, 2006) and the remaining term of office (RemainTerm) (Kabir et al., 2018). Contracts (e.g., stock option) are developed to counter the myopia of managers (Bergstresser & Philippon, 2006; Stein, 1989). A manager with option incentives places a greater focus on the long-term value of the firm. Moreover, the managers’ remaining tenure is capable of altering their horizons. A manager who is new to the position and has a lengthy remaining term tends to have a longer horizon. When approaching the time of departure, self-interest and short-sightedness may be increased.

The catering costs are examined using the degree of financing constraints and equity costs. A firm’s financing constraint is examined based on the KZ index, obtained from the CSMAR Database, and determined in accordance with the idea of Kaplan and Zingales (1997). Firms with high financing constraints are subjected to higher external financing costs, such that they are more reluctant to imitate peers. The equity costs (EquityCost) are estimated using the Capital Asset Pricing Model (CAPM). Table 1 lists the details on the variables.

Results

Summary Statistics

Table 2 displays the summary statistics for the variables used to analyze the influence of dividend peers. The left column details the mean, median, and standard deviation of these variables for focal firms, while the right column provides the same statistics for peer firms.

Summary Statistics.

Note. The table presents summary statistics of the variables used in our main analyses. Firm specific characteristics denote variables corresponding to firm i’s value in year t. Peer firm averages are constructed as the average of all firms within an industry-year combination, excluding the ith observation.

The table includes data on dependent, independent, instrumental, and control variables used in the empirical analyses. The dataset encompasses 37,833 firm-year observations utilized in the regressions. Notably, 62.6% of these observations are from firms that issue cash dividends, and 10% distribute stock dividends. The average percentage of peer firms paying cash dividends is 63.2%, and for stock dividends, it is 11.1%, closely aligning with the figures for the focal firms. The mean cash dividends per share are 0.104 for focal firms and 0.110 for peer firms. For stock dividends, the average DPS are 0.052 for focal firms and 0.061 for peer firms. The instruments—idiosyncratic returns and risks of peer firms—show mean values of −0.020 and 0.098, respectively. The average values of the control variables are similar between the focal and peer firms.

Peer Influence on Cash and Stock Dividend Payment

This section discusses the regression results concerning the peer influence on cash and stock dividends from two perspectives: the propensity to pay dividends and the level of dividends paid.

The Propensity to Pay Dividends

Table 3 explores whether a firm’s decision to pay dividends is influenced by the dividend policies of its industry peers. The analysis in columns (1) to (6) utilizes Probit models with instrumental variables (IV-Probit), appropriate for binary dependent variables, as seen in these columns. The method of estimation is conditional maximum likelihood. Following the approach of Adhikari and Agrawal (2018), both instrumental variables are lagged by 1 year. Columns (1) to (3) focus on the impact of cash dividend decisions among peers. Specifically, column (1) shows the first-stage results concerning the influence of peers on the decision to pay dividends, where the dependent variable is the fraction of peers that pay cash dividends (PeerPayCash), and the instruments include peers’ idiosyncratic returns and risks. Column (2) presents the second-stage results, which regress the focal firm’s likelihood of paying dividends on the proportion of its industry peers that pay dividends. Dividend payments tend to be sticky, indicating that a firm’s continued dividend payments may reflect this stickiness rather than peer influence. To further investigate this, column (3) examines the impact on dividend initiation, detailing second-stage results for firms that did not pay cash dividends in the preceding year.

Peer Effect on the Propensity to Pay Dividend.

Note. The table presents the results of whether a firm’s decision to pay dividend is affected by the corresponding decisions of its industry peers. Column (1) lists the first stage results of the peer effect for the decision to pay cash dividends. Column (2) lists the second-stage results, which is the regression of the focal firm’s propensity to pay cash dividends on the proportion of cash dividend-paying firms among its industry peers. Column (3) lists the results of the peer effect for cash dividend initiation. Likewise, columns (4) and (5) list the results of the first-stage and second-stage regressions of the peer effect for the decision to pay stock dividends. Column (6) lists the second-stage results of the peer effect for stock dividend initiation. The t-statistics robust to heteroskedasticity is presented in parentheses. All columns control for the industry and year fixed effects. The Cragg-Donald Wald F statistic for weak instrumental variable test, the Sargan p-value for the overidentification test, and the number of observations are reported at the bottom of the table.

, **, and * indicate statistical significance at the 1%, 5%, and 10%, respectively.

for Cragg-Donald Wald F statistic indicates the F-value exceeds the critical value at 15% (11.59).

Similarly, the influence of peers regarding stock dividends is analyzed in columns (4) to (6). Columns (4) and (5) detail first-stage and second-stage results, respectively, related to the decision to pay stock dividends. Column (6) provides the second-stage analysis of the influence on decisions to initiate stock dividends.

At the bottom of Table 3, the Cragg-Donald Wald F statistic and the Sargan p-value are reported. The F-values in all columns exceed the 15% critical threshold, indicating no issues with weak instrumental variables. Additionally, the p-values for the over-identification tests are all above 10%, suggesting that the instrumental variables do not suffer from over-identification issues.

As demonstrated by the results in column (1), the two instruments effectively predict the propensity of peer firms to pay cash dividends, with all instrument coefficients achieving significance at the 1% level. Similarly, the results in column (2) show that the fitted value of PeerPayCash from the first stage significantly and positively influences a focal firm’s decision to pay cash dividends. The marginal effect at the sample mean in column (2) is 0.281, indicating that an increase of one standard deviation in the fraction of firms paying cash dividends raises the propensity of the focal firm to pay cash dividends by 28.1%. Adhikari and Agrawal (2018), utilizing data from U.S. publicly traded companies, found a comparable marginal effect of 26%, slightly lower than that observed in China. In column (3), the coefficient is significantly positive at the 5% level, suggesting that an increased propensity among peer firms to pay dividends can motivate the focal firm to initiate dividend payments.

In column (4), the two instrumental variables robustly predict the propensity of peer firms to pay stock dividends, with coefficients significant at the 1% level. In column (5), the fitted value of PeerPayStock from the first stage significantly and positively affects the focal firm’s decision corresponding to that variable. In column (6), the coefficient remains significantly positive at the 1% level, indicating that the decision to initiate stock dividends is influenced by the propensity of peer firms to pay stock dividends.

Overall, the decisions of peer firms to pay cash dividends significantly and positively influence the focal firm’s decisions to pay and initiate cash dividends. A similar conclusion applies to stock dividends. The peer influence on stock dividends is both numerically and statistically more significant than that on cash dividends. The findings presented in Table 3 suggest that the higher the proportion of peer firms paying cash dividends, the more likely the focal firm is to pay cash dividends. This assertion holds true for stock dividends as well. The positive peer influences support Hypothesis 1 and provide a foundation for subsequent tests of the catering theory.

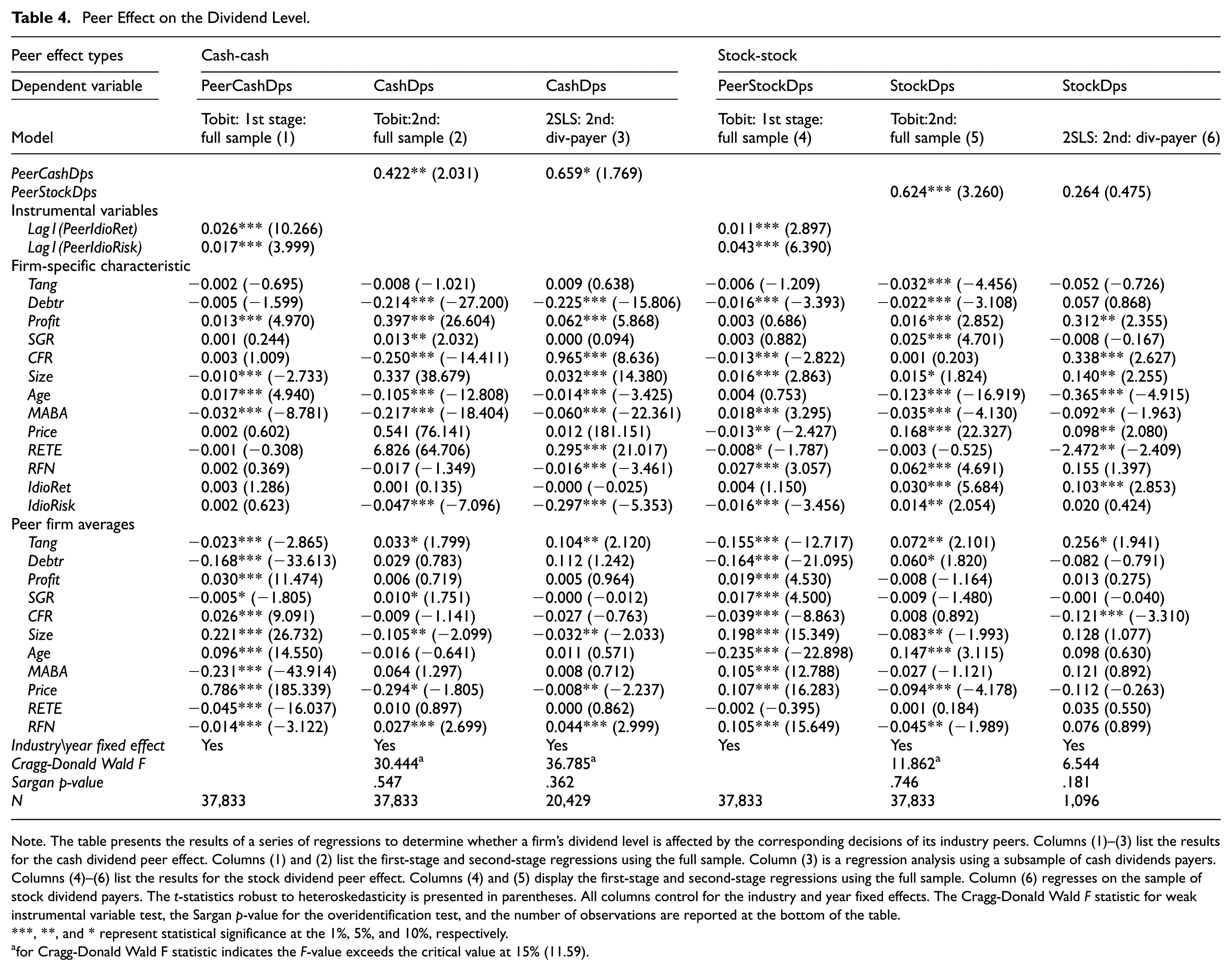

The Dividend Level

Table 4 presents the findings of several regressions aimed at evaluating the influence of industry peers’ dividend levels on a firm’s dividend policy. The first three columns illustrate the impact of cash dividends from peer companies, while columns (4) to (6) explore the effects of stock dividends. The Cragg-Donald Wald F statistics demonstrate strong correlations between the instrumental variables and the endogenous explanatory variables in the cash dividend analyses. However, for the stock dividend analyses, the instruments only meet the criteria for the weak instrumental variable test in the regression using the full sample. The instrument cited in column (6) may be subject to issues related to weak instrumental variables. The analysis primarily focuses on results that adequately pass the weak instrument test. The p-values for the over-identification tests exceed 10% across all columns, suggesting that the two instruments do not exhibit over-identification issues.

Peer Effect on the Dividend Level.

Note. The table presents the results of a series of regressions to determine whether a firm’s dividend level is affected by the corresponding decisions of its industry peers. Columns (1)–(3) list the results for the cash dividend peer effect. Columns (1) and (2) list the first-stage and second-stage regressions using the full sample. Column (3) is a regression analysis using a subsample of cash dividends payers. Columns (4)–(6) list the results for the stock dividend peer effect. Columns (4) and (5) display the first-stage and second-stage regressions using the full sample. Column (6) regresses on the sample of stock dividend payers. The t-statistics robust to heteroskedasticity is presented in parentheses. All columns control for the industry and year fixed effects. The Cragg-Donald Wald F statistic for weak instrumental variable test, the Sargan p-value for the overidentification test, and the number of observations are reported at the bottom of the table.

, **, and * represent statistical significance at the 1%, 5%, and 10%, respectively.

for Cragg-Donald Wald F statistic indicates the F-value exceeds the critical value at 15% (11.59).

First, we examine the impact of peer influence on the cash dividend level as presented in the findings. Column (1) details the first-stage regression using the full sample, where the average cash dividends per share of peer firms (PeerCashDps) are regressed against the idiosyncratic returns and risks of these peer firms. The two instrumental variables effectively predict the dividend levels of peer firms, with coefficients significant at the 1% level. Column (2) showcases the second-stage results, again utilizing the full sample. In this stage, the regression analyses the cash dividends per share of a focal firm based on the fitted value of PeerCashDps from the first stage. An IV-Tobit model is employed here, considering the dependent variable is predominantly continuous but includes significant instances of zero values. The results confirm that the fitted value of peer firms’ dividends per share significantly and positively affects the dividend per share of the focal firm. The marginal effect at the sample mean in column (2) is 0.142, indicating that an increase of one standard deviation in the average cash dividend per share of peer firms leads to a 0.142 standard deviation increase in the cash dividend per share of the focal firm. Column (3) presents a regression using a subsample of firms that pay cash dividends. The dependent variable here is continuous; hence, a two-stage least squares (2SLS) approach is applied to assess the impact of peer firms’ dividend levels on the dividend decisions of the focal firm. The coefficient is 0.659, significant at the 10% level, suggesting that for every standard deviation increase in the average cash dividends per share of peer firms, the dividend per share of the focal firm increases by 0.659 standard deviations. Yan and Zhu (2020) employed a similar IV approach to investigate the peer influences on dividend payouts among Chinese listed companies, yielding a significant coefficient of 1.279. However, their findings are not directly comparable to those of this study because they measure dividends as the aggregate of cash dividends, stock dividends, and reserve transfers. This research offers an advantage by providing separate coefficients for the peer influences on cash and stock dividends.

Columns (4) to (6) present the results for stock dividends. Both instrumental variables effectively predict the average stock dividend per share of peer firms, with coefficients statistically significant at the 1% level, as shown in column (4). The second-stage results of the IV-Tobit model, using the entire sample, are displayed in column (5), where the average dividend per share of peer firms significantly and positively affects the dividend per share of the focal firm. Column (6) employs 2SLS on a sample of firms that pay stock dividends, but here, the coefficient of PeerStockDps is not significant.

Overall, Table 4 suggests that the cash dividend level is significantly and positively influenced by the dividend decisions of peer firms, both in the full sample and the subsample. The influence of stock dividends is also significant and positive when using the full sample; however, it becomes insignificant in the subsample of stock dividend payers. Additionally, the influences of stock dividends are both numerically and statistically more significant than those of cash dividends. The results indicate that the higher the average cash dividends paid by peer firms, the more inclined the focal firm is to increase its own cash dividends. This pattern is also evident with stock dividends. The positive peer influences on dividend levels support Hypothesis 1, setting the stage for further tests of the catering mechanism.

Robustness Checks

Peer Influence with Lagged Peer Influence

The contemporary measure of peers’ dividend payments is adopted in the primary regression, rather than a lagged one. Adhikari and Agrawal (2018) suggested that peer influences are likely to be identified more precisely if there is little time lag for other variables to take effect. Moreover, contemporary indicators are selected for the peer characteristics since dividend announcements are generally declared around March and April of the following year, and there is a time lag between dividend distribution and other financial indicators.

Nonetheless, for robustness purposes, the explanatory and control variables are lagged by one year, and the regressions are repeated to examine whether a 1-year lag in the peer firms’ dividend decisions will affect the focal firm. The results are listed in Table 5.

Peer Effect with Lagged Peer Influence.

Note. The table presents the regressions of whether a one-year lag of the peer firms’ dividend decisions would have an effect on the corresponding decisions of the focal firm. Columns (1) and (2) display the outcomes of the peer effect for the propensity to pay cash dividends and dividend level. Columns (3) and (4) show the findings of the peer effect for the propensity to pay stock dividends and dividend level. The t-statistics robust to heteroskedasticity is presented in parentheses.

and * indicate statistical significance at the 1% and 10% levels, respectively.

for Cragg-Donald Wald F statistic indicates the F-value is greater than the critical value at the 15% level (11.59).

In Table 5, columns (1) and (2) list the outcomes of the peer influence for the propensity to pay cash dividends and dividend level, respectively. Both coefficients are statistically positive at 1%. The two instrumental variables display significant correlations with the dividend decisions of peer firms, as presented in the first stage results, and both pass the weak instrumental variable and over-identification tests, thus verifying the validity of the instrumental variables.

Columns (3) and (4) list the findings of the peer influence of the propensity to pay stock dividends and dividend level. The lagged proportion of stock dividend payers among peer firms has a significantly favorable influence on the tendency of the focal firm to pay stock dividends. However, the coefficient of lagged PeerStockDps in column (4) is not significant at the 10% level. In general, the results in Table 5 support research hypothesis 1, except that the peer influence of stock dividend level becomes insignificant.

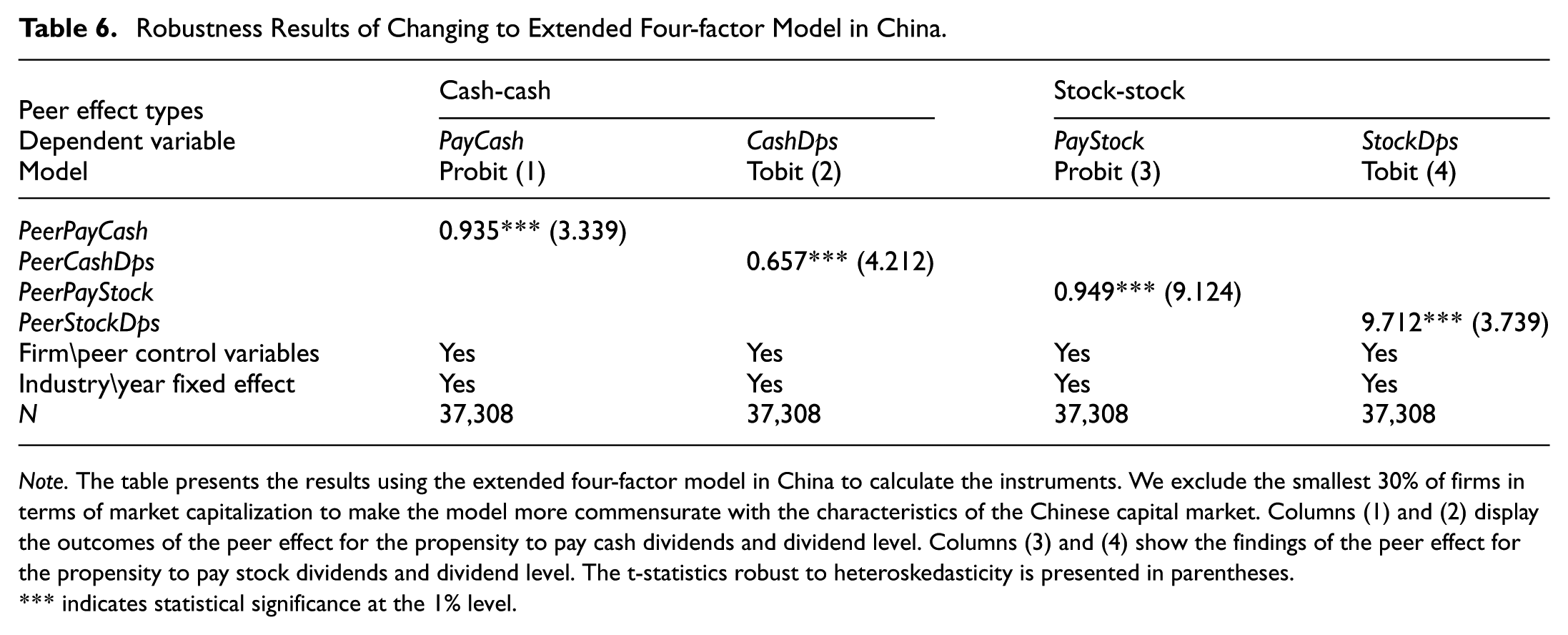

Changing the Model for Calculating Instrumental Variables

The reliability of instrumental variables is critically significant for empirical results. In the primary regression, we adopt the extended Fama-French three-factor model to calculate instrumental variables by removing the effects of industry, market, size, and value factors from stock prices. To further mitigate possible systematic risks, the extended four-factor model is employed in China. Additionally, following Liu et al. (2019), we exclude the smallest 30% of firms by market capitalization to better align the model with the characteristics of the Chinese capital market. Furthermore, we construct the market factor, size factor, value factor, and sentiment factor monthly.

The results, presented in Table 6, show that the peer influences on the decision to pay dividends and the dividend level are significantly positive for both cash and stock dividends, corroborating the findings of the main regression. This outcome indicates that the choice of model for calculating the instrumental variables does not influence the empirical findings.

Robustness Results of Changing to Extended Four-factor Model in China.

Note. The table presents the results using the extended four-factor model in China to calculate the instruments. We exclude the smallest 30% of firms in terms of market capitalization to make the model more commensurate with the characteristics of the Chinese capital market. Columns (1) and (2) display the outcomes of the peer effect for the propensity to pay cash dividends and dividend level. Columns (3) and (4) show the findings of the peer effect for the propensity to pay stock dividends and dividend level. The t-statistics robust to heteroskedasticity is presented in parentheses.

indicates statistical significance at the 1% level.

Other Robustness Tests

Several firms in the sample have paid dividends consistently for an extended period and have yet to continuously pay dividends for a number of years. Such firms exhibit paying and non-paying behavior that peer firms may not influence. Thus, during the test of the peer influence of cash dividends, the sample of firms that have been paying cash dividends for 15 consecutive years and more is removed, totaling 5279 samples. Firms that have never paid cash dividends for 15 straight years and more, totaling 1871 samples, are also removed. Likewise, in examining the peer influence of stock dividends, firms that have paid stock dividends for 15 or more consecutive years are eliminated, totaling 16 samples. Firms that have not paid stock dividends for at least 15 straight years are also eliminated, for a total of 8747 samples. The results are listed in Table 7.

Other Robustness Test Results.

Note. The table presents results of removing the firms that have paid or not paid dividends for a long period of time. Columns (1) and (2) display the outcomes of the peer effect for the propensity to pay cash dividends and dividend level. Columns (3) and (4) show the findings of the peer effect for the propensity to pay stock dividends and dividend level. The t-statistics robust to heteroskedasticity is presented in parentheses.

indicates statistical significance at the 1% level.

In Table 7, the results are still highly significant after the firms that have paid or not paid dividends for an extended period are removed. The above-mentioned firms do not affect the primary regression results.

Catering Mechanism Analysis

According to the catering theory, managerial behavior is primarily influenced by three factors: arbitrage restrictions, managerial horizons, and catering costs. This analysis examines the effects of these factors on peer influence to determine whether managerial decisions regarding cash and stock dividends are driven by catering incentives. The robustness of the instruments employed in this analysis is supported by the Cragg-Donald Wald F statistic, which is presented at the bottom of each panel in Table 8.

The Influence of Arbitrage Restrictions, the Manager’s Horizon and Catering Costs on Cash Dividend Peer Effect.

Note. The table presents the impact of arbitrage restrictions, the manager’s horizon and the catering costs on cash dividend peer effect. Panels A, B and C present the results for arbitrage restrictions, the manager’s horizon and the catering costs respectively. The t-statistics robust to heteroskedasticity is presented in parentheses.

, **, and * indicate statistical significance at the 1%, 5%, and 10% levels, respectively.

for Cragg-Donald Wald F statistic indicates the F-value is greater than the critical value at the 15% level (4.58).

Table 8 demonstrates the impact of arbitrage restrictions, managerial horizons, and catering costs on peer influence concerning cash dividend decisions.

Regarding arbitrage restrictions, Baker and Wurgler (2004a) suggest that limitations on arbitrage allow investor demands to affect the firm’s current stock price. Such restrictions help maintain a high stock price, enabling the firm to capitalize on short-term stock premiums. Consequently, as proposed in Hypothesis 2, increased arbitrage restrictions enhance the incentive to cater, thereby intensifying the peer influence on dividend decisions. In Panel A, trading volume, denoted as “Volume,” significantly and negatively influences the peer impact on both the propensity and level of cash dividends in columns (1) and (2), which meets our expectations. Lower trading volumes, indicative of higher transaction costs and stronger arbitrage constraints (Mashruwala et al., 2006), lead firms to more frequently imitate their peers to cater to investors. The number of institutional investors, represented as “Inst#,” significantly and negatively impacts the peer influence on the propensity for cash dividends, as shown in columns (3) and (4), but does not significantly affect the level of dividends. Firms with a larger base of institutional investors typically exhibit greater investor sophistication and maturity, which mitigates arbitrage risk and, consequently, reduces arbitrage constraints. Therefore, these firms are less inclined to mimic their peers. Overall, the results in Panel A strongly support Hypothesis 2.

The discussion on managerial horizons (Hypothesis 3) focuses on the trade-off between the emphasis managers place on current stock prices and long-term value. Short-sighted managers often prioritize immediate increases in stock prices, sacrificing the firm’s long-term value. As shown in Column (2) of Panel B, the influence of peer dividend levels is significantly weaker for firms that provide managerial option incentives compared to those that do not. These incentives encourage a focus on long-term considerations rather than merely short-term stock price gains, thus reducing the tendency to imitate peers. According to Column (3), managers with shorter remaining tenures are more likely to mimic the dividend decisions of their peers, focusing on short-term performance and personal interests to satisfy investors. Overall, the findings in Panel B support Hypothesis 3.

Regarding catering costs, Hypothesis 4 posits that the effort to meet investor expectations and mimic the dividend payments of peer firms can incur additional costs. Firms facing higher catering costs are less likely to imitate their peers. In Column (2) of Panel C, firms with greater financial constraints—indicative of higher external financing costs—are less inclined to align with their peers’ dividend decisions. These constraints lead to increased catering costs, prompting firms to adopt a non-catering strategy. Similarly, analysis in Column (4) shows that a higher cost of equity correlates with a weaker influence of peers on cash dividend levels. Thus, the findings in Panel C validate Hypothesis 4.

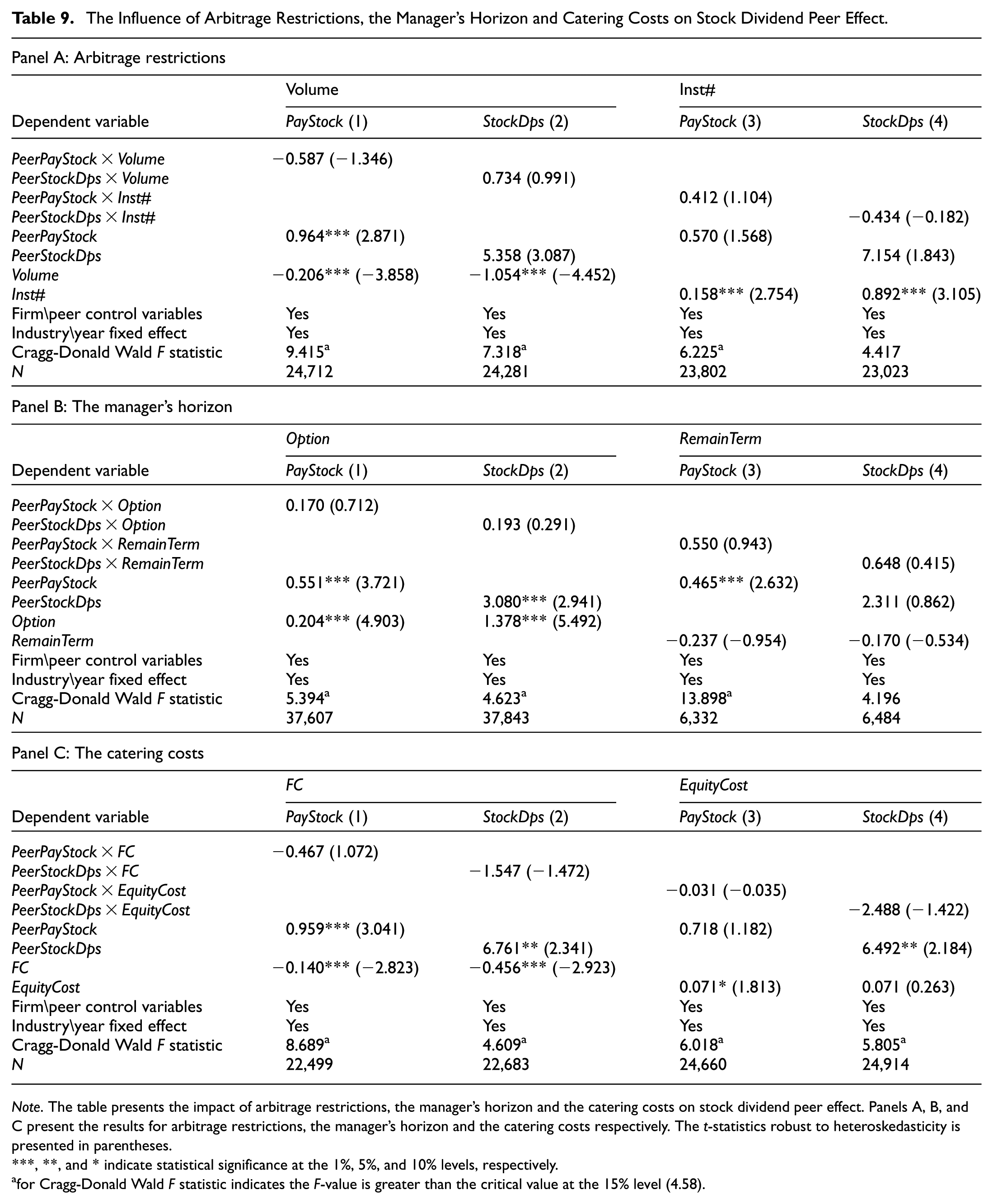

Contrary to cash dividends, the empirical data on the effects of arbitrage restrictions, managerial horizons, and catering costs on the peer influence of stock dividends (Table 9) show no alignment with the research hypotheses. The coefficients of the interaction terms for these factors are all insignificant, indicating that the results in Table 9 do not support Hypotheses 2, 3, and 4.

The Influence of Arbitrage Restrictions, the Manager’s Horizon and Catering Costs on Stock Dividend Peer Effect.

Note. The table presents the impact of arbitrage restrictions, the manager’s horizon and the catering costs on stock dividend peer effect. Panels A, B, and C present the results for arbitrage restrictions, the manager’s horizon and the catering costs respectively. The t-statistics robust to heteroskedasticity is presented in parentheses.

, **, and * indicate statistical significance at the 1%, 5%, and 10% levels, respectively.

for Cragg-Donald Wald F statistic indicates the F-value is greater than the critical value at the 15% level (4.58).

The phenomenon of peer influence on cash dividends is well explained by the catering theory, though its application to stock dividends has been less clear. Our further investigation into stock dividends reveals that during the high stock dividend period (2007–2015), the catering theory also accounts for the observed peer effects in stock dividend decisions. Figures 1 and 2 illustrate the trends in cash and stock dividends from 1995 to 2023. Figure 1 displays the average cash and stock dividend per share, while Figure 2 depicts the annual proportion of firms distributing cash and stock dividends. Both figures show a fluctuating yet upward trend in cash dividend payments and in the proportion of firms opting to pay cash dividends. This trend aligns with the catering theory, which suggests that firms adjust their cash dividend payments to meet investors’ psychological expectations, often mirroring the practices of their peers, thereby fostering a general increase in both the prevalence and size of cash dividends across the market.

Average cash dividend and stock dividend per share from 1995 to 2023.

Proportion of firms paying cash dividends and stock dividends from 1995 to 2023.

The dynamics of stock dividends, however, are more nuanced. Two distinct periods are evident: the high stock dividend period from 2007 to 2015, and the subsequent regulatory period from 2016 to the present. During the high stock dividend period, Figure 1 indicates that firms frequently issued large stock dividends, sometimes distributing as many as 5 shares for every 10 owned. Concurrently, Figure 2 shows a substantial proportion of firms paying stock dividends during this period. Investor reactions to these stock dividend announcements were significantly positive (Wang et al., 2021). Thus, it can be inferred that during this period, firms likely aligned their stock dividend distributions with those of their peers, in accordance with the catering theory’s premise of catering to investors’ psychological benchmarks.

From 2016 to 2023, both the average stock dividend per share and the proportion of companies paying stock dividends have consistently declined. This trend is due to regulatory influences and shifts in investor preferences. Specifically, in February 2016, the Shenzhen Stock Exchange began tying stock dividend plans to company performance, with additional regulatory guidelines introduced subsequently. Following the adoption of the registration-based system in 2021, stringent disclosure requirements and regulations against non-standard practices led companies to curtail stock dividend distributions. Moreover, these regulatory changes significantly dampened the previously positive market reactions to stock dividend announcements (Wang et al., 2021). The link between stock dividends and firm performance reduced information asymmetry, while constraints on major shareholders’ sales heightened investor concerns about potential opportunistic behaviors. As a result, the declining investor interest in stock dividends prompted companies to adjust their distribution strategies to better align with shareholder preferences. Consequently, there was no incentive for companies to appeal to investors’ psychological benchmarks by paying stock dividends.

In summary, the period from 2007 to 2015, characterized by high stock dividend payouts, supports the catering theory predictions. However, the period from 2016 to 2023 does not. To verify this, we analyzed the effects of arbitrage restrictions, managerial horizon, and catering costs on the peer influences of stock dividends during both periods. The findings, detailed in Table 10, reveal that during the high dividend period, arbitrage restrictions had no significant impact on peer effects, whereas managerial horizon and catering costs significantly supported the catering theory, as hypothesized in Hypotheses 3 and 4. In contrast, during the regulatory period, arbitrage restrictions, managerial horizon, and catering costs showed no significant influence on the peer effects of stock dividends, underscoring the lack of corporate motivation to cater to investors’ psychological preferences during this phase.

Comparison of Catering Behavior: High Versus Regulated Stock Dividend Periods.

Note. The table reports the effects of arbitrage restrictions, managerial horizon, and catering costs on the stock dividend peer effect during the high stock dividend period (2007–2015) and the regulatory stock dividend period (2016–2023). Panels A, B, and C present results for arbitrage restrictions, managerial horizon, and catering costs, respectively. Arbitrage restrictions are proxied by trading volume (Volume), managerial horizon by option incentives (Option), and catering costs by the degree of financing constraints (FC). Robust t-statistics adjusted for heteroskedasticity are reported in parentheses.

, **, and * denote significance at the 1%, 5%, and 10% levels, respectively.

Further analysis

In the hypothesis proposed in this study, the motivation for listed companies to imitate the dividend decisions of their peer firms is that investors use the dividend decisions of their peer firms as a psychological reference point to determine the attractiveness of the dividend decisions of the focal firm. In accordance with this motivation, our test uses the following model (5).

The above-mentioned model examines whether a significant difference exists in investors’ market reaction to dividend announcement between focal firms whose dividend exceeds peer firms and those whose dividend is lower than peers. CARidt represents the cumulative abnormal return in the event window (−3, +3). The independent variable AbovePidt indicates whether the dividend per share of firm i over year t exceeds the average of all dividend-paying firms in industry d. If DPSidt is higher than or equal to the industry average, AbovePidt is considered 1; otherwise, it is considered 0. It is expected that the coefficient β1 of AbovePidt notably exceeds zero, i.e., investors take the dividend of peer firms as the psychological reference point to judge the focal firm’s dividend and have a significantly higher positive market response to the focal firm whose dividend exceeds its peer firms. The results are listed in Table 11.

Investors’ Reference Point Dependence on Peer Firms’ Dividends.

Note. The table presents results of whether there is a significant difference in investors’ market reaction between focal firms whose dividend is higher than peer firms and those whose dividend is lower than peers.

and * indicate statistical significance at the 1% and 10% levels, respectively.

As indicated by the results, the coefficients of AboveP for cash and stock dividends notably exceed zero at 1%. Companies with cash DPS (stock DPS) equal to or greater than the industry average have a CAR(−3,+3) of 0.073 (0.188) standard deviations higher than companies with cash DPS (stock DPS) below the industry average. The above-described finding supports the theoretical expectation that investors judge the dividend payout of the focal firm using their peer firms’ dividend payments as a psychological benchmark.

Conclusion

Existing research has applied theories of industrial competition and information acquisition to elucidate the influence of peers on cash dividends. However, the pivotal role of investors has often been neglected. This study incorporates investors into its analytical framework. It uses data from A-share non-financial listed companies on the Shanghai and Shenzhen stock exchanges spanning from 1995 to 2023 to demonstrate that peer influences on both cash and stock dividends are pronounced in China. The impact on cash dividends is especially strong among firms facing higher arbitrage restrictions, shorter managerial horizons, and lower catering costs, endorsing the managerial catering mechanism. Conversely, for stock dividends, the managerial catering mechanism primarily accounts for the peer effects observed during the high stock dividend period from 2007 to 2015.

The limitations of this research, along with potential avenues for future exploration, include: First, although significant peer influences are noted in stock dividend payments, the catering theory predominantly explains peer effects during the high stock dividend era (2007–2015). Future studies could probe the mechanisms underlying stock dividend peer effects in the regulatory environment post-2016, an area we are currently investigating.

Second, the analysis of investors’ market reactions to peer influences is not exhaustive. Further examination reveals that investors assign greater value to companies whose dividends surpass those of their peers, supporting the catering theory. However, this study does not distinguish between individual and institutional investors due to methodological constraints. Future research could examine how these investor groups respond differently to corporate dividend peer influences. Moreover, considering the significant impact of financial analysts on listed companies’ stock prices, exploring analysts’ views on dividend peer influences could yield deeper insights into managerial catering behaviors.

Third, this study focuses on A-share listed companies in the Chinese capital market, which exhibits several unique characteristics. Notably, China’s capital market is predominantly driven by retail investors and is relatively immature, with a tendency towards speculation. These attributes may exacerbate behavioral biases such as investor peer-reference dependence and managerial catering. Despite these specificities, the findings provide valuable insights for other emerging capital markets. Theoretically, catering behavior arises from investor reference dependence, limited arbitrage, and short-term managerial incentives—conditions prevalent not just in China. Therefore, the motivations for catering identified here may also emerge in other emerging markets with similar behavioral and structural dynamics, suggesting that the findings could be relevant to comparable economies globally.

This study presents several implications. For managers, it is essential to use the dividend policies of peer firms as a psychological benchmark to assess the appeal of their own firm’s dividend payments and to avoid excessively idiosyncratic dividends. Additionally, cash and stock dividends are influenced by different underlying mechanisms of peer influence. Managers should select the type of dividend that best suits their specific requirements. For investors, it is important to recognize that imitation among firms is common and often targets short-term gains, which could undermine long-term value. Value investors should maintain their focus on the unique characteristics and business conditions of the specific firm when making investment decisions.

Supplemental Material

sj-docx-1-sgo-10.1177_21582440251386673 – Supplemental material for Managerial Catering and Peer Influence on Dividend Payments

Supplemental material, sj-docx-1-sgo-10.1177_21582440251386673 for Managerial Catering and Peer Influence on Dividend Payments by Ying Li, Tianyu Zhang and Yu-En Lin in SAGE Open

Footnotes

Ethical Considerations

The research uses publicly available data and involves no direct interaction with human participants.

Consent to Participate

The research involves no human participants and consent requirements are not applicable.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is supported by the funds below.

Shenyang Institute of Science and Technology program under funding No.MS-2023-20. Macau University of Science and Technology Foundation under funding No.FRG-25-053-MSB.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.