Abstract

This study is the first to examine how limit-to-arbitrage factors impact the distress risk puzzle in Vietnam before and after implementing bankruptcy regulations. Our research utilizes asset pricing models, portfolio sorting methodologies, and the Fama and French four-factor model to analyze an unbalanced panel with 35,255 firm-month observations from non-financial firms in the Vietnam stock market from 2008 to 2021. We find a persistent negative correlation between distress risk and corporate profitability, even after accounting for limit-to-arbitrage factors. Notably, this trend is more pronounced among larger firms. Intriguingly, the distress risk puzzle disappears after the introduction of bankruptcy regulations. Additionally, we observe that limit-to-arbitrage factors suppress stock returns due to mispricing issues, supporting liquidity risk theory. Our study provides valuable insights into the distress risk puzzle, especially in emerging markets.

Introduction

Financial distress happens when an organization or individual cannot fulfill repayment obligations due to high fixed expenses, a considerable portion of illiquid resources, or income vulnerability to financial slumps. The relationship between distress risk and stock returns is significant for investors because its direct relation to investors requires a premium for bearing this type of risk, such as holding financially distressed firms in their portfolios (Andreou et al., 2021). Understanding bankruptcy risk helps portfolio managers consider and allocate assets rationally. By investing in different industries and economic regions, they can enhance portfolio diversification to minimize the impact of bankruptcy risk on overall returns. By diversifying their portfolios, they can spread the risk across different sectors and reduce the potential negative impact of bankruptcy on overall profitability.

Limit to arbitrage factors also influence stock returns. The popular proxies of limit to arbitrage factors are idiosyncratic volatility, illiquidity, and turnover ratio. Gu et al. (2018) indicate that the higher the limit to arbitrage, the lower the IVOL premium. Limits to arbitrage can harm investors because they make the stock market inefficient. However, Hung and Yang (2018) report that the negative IVOL puzzle emerges only in stocks with higher modified MAX relative to the prior month. Furthermore, during the raging COVID-19 epidemic, turnover is the sole limit to the arbitrage factor that generates profits for investors (Duong et al., 2021).

Chiaramonte et al. (2015) report that the Z-score model performed well as CAMELS variables, demonstrating an excellent predictive ability of distress risk, especially during the financial crisis. However, the Z-score has the advantage of requiring fewer accounting data. He also found that Altman’s Z-score model retains its predictive ability even when employing different calculating methods. Altman et al. (2017) showed that the Z-score model works well in international markets. Therefore, we follow Altman (1968) and Duong et al. (2022) to compute the Z-score as the primary proxy of the distress risk.

This study was conducted in Vietnam for several significant reasons. Vietnam’s business environment has experienced notable fluctuations, exemplified by data from the Vietnam Business Registration Administration. Despite a modest decrease in newly established enterprises in 2020 compared to the previous year, there was a striking surge in business exits, particularly evident with over 35,000 enterprises leaving the market in the first quarter alone. Descriptive statistics from our sample underscored a worrisome average Z-score value of 1.13 for listed firms in Vietnam, signaling severe default risk.

The relationship between limits-to-arbitrage and their influence on stock returns has attracted considerable scholarly attention. Sha et al. (2023) uncovered a noteworthy finding, indicating that the negative correlation between distress risk and returns is notably accentuated in stocks subject to stricter limits-to-arbitrage. This phenomenon stems from the constrained ability of investors to short sell overpriced stocks with heightened distress risk, driven by the limited availability of lendable shares and associated high arbitrage costs. However, a research gap exists concerning how limit-to-arbitrage factors intersect with distress risk anomalies in Vietnam’s market, characterized by stringent regulatory constraints. Notably, Vietnam enforces caps on daily share sales, with limits set at 7% on the Ho Chi Minh Stock Exchange (HOSE) and 15% on the Hanoi Stock Exchange (HNX). Additionally, Vietnam’s robust development of small and medium enterprises (SMEs), limited access to formal financing, and greater legal challenges compared to larger companies highlight the prevalence of financial constraints among smaller businesses (Bui et al., 2021). Therefore, investigating how limits to arbitrage affects financial distress risk puzzle in Vietnam is worth investigating.

Furthermore, a notable observation is that the enactment of corporate bankruptcy laws in Vietnam significantly reduced the bankruptcy rate from 5.6% to 2.8%. Hence, it is imperative to delve into the relationship between bankruptcy risk and the country’s bankruptcy laws, exploring the legislation’s profound impact on Vietnam’s bankruptcy landscape.

We collected data from listed firms in Vietnam from 2008 to 2021 to close the literature gap. We employ the Fama and French three-factor model, the Carhart four-factor model, portfolio sorting methods, and two-step Fama and MacBeth (1973) regressions to analyze an unbalanced sample of 35,255 firm-month observations. Our findings indicate a persistent distress risk anomaly, implying that firms with higher distress risk generate lower returns and vice versa. This phenomenon is a puzzle because the traditional risk and returns relationship implies that firms with higher risks should generate extra returns to compensate for bearing higher risks. Investors prefer firms with higher growth than distressed ones, so they are reluctant to invest in these firms. Thus, there is an inverse relationship between distress risk and stock returns in Vietnam.

Secondly, the distress risk anomaly persists after controlling the limit to arbitrage factors. These findings align with Duong et al. (2022), Chava and Purnanandam (2010), and Liu et al. (2019). We also observed that the distress risk puzzle is even more pronounced in large corporations than in small and medium-sized businesses. Our finding aligns with the “too big to fall” Hypothesis, suggesting that larger firms have better risk management expertise than small and medium-sized companies. Distress risk in more prominent firms is less significant than in smaller firms. Our findings are robust after employing alternative estimation methods such as portfolio sorting and two-step Fama and MacBeth (1973) regressions.

Finally, our findings indicate that the limits of arbitrage factors reduce cross-sectional stock returns. These findings align with Hung and Yang (2018), Gu et al. (2018), and Duong et al. (2021). Gu et al. (2018) explain that investors tend to take advantage of the mispricing of stocks to earn additional profits. Therefore, arbitrage constraints can hinder investors from capturing profitable trading opportunities. Hung and Yang (2018) indicate that the higher limit to arbitrage causes stocks to become mispriced, reducing stock returns. Finally, our findings indicate that the distress risk puzzle disappears after enacting the corporate bankruptcy regulation in Vietnam.

Our study extends the growing literature on the distress risk puzzle in the following ways. Firstly, Asis et al. (2021) employ the logit model to estimate the determinant of distress risk. However, the logit model is suitable for low-frequency data, which could better fit studies with high-frequency data. Because low-frequency data from financial statements are published quarterly, clarifying the variation of monthly stock returns could be more efficient. Therefore, this study is more suitable for the three- and four-factor models, the two-step estimations of Fama and MacBeth (1973), and portfolio sorting approaches. Finally, our research enriches the literature by examining how regulatory factors and limit-to-arbitrage affect the distress risk anomaly.

In addition, our study also complements Liu et al. (2019) and Duong et al. (2022) because they examine the relationship between default risk and subsequent stock returns. Liu et al. (2019) also report that state ownership strongly affects the predictability of the distress risk puzzle in China. However, Liu et al. (2019) implement Merton’s structural model to measure default risk. Our study follows Duong et al. (2022) in employing accounting-based models. We consolidate data from the stock market and financial statements to mitigate the data limitations in Vietnam, so the accounting-based method is more suitable for conducting this study in Vietnam.

The paper structure is as follows: The Literature review is in Section 2. Section 3 presents Data and Methodology. The results and discussions are in Section 4. Section 5 is the conclusion and implications.

Literature Reviews

Distress Risk and Stock Returns

Altman (1968) proposed the Z-score as the first bankruptcy indicator because it could accurately forecast the likelihood of a company’s insolvency. Altman et al. (2017) evaluated the bankruptcy prediction power of the Z-score model using an extensive global set of data. The results are consistent in China, Europe, Colombia, and the USA. The Z-score model works exceptionally well with a prediction accuracy of about 0.75 and a classification accuracy above 0.90, which can improve further. Ohlson (1980) proposed using the probability of bankruptcy (O-score) to calculate the distress risk. However, the results could be more satisfactory because the prediction rate of this model is much lower than that of the Z-score approach. As a result, we conclude that Altman’s Z-score is suitable for anticipating bankruptcy.

Abbas and Ali (2022) and Ozili (2019) stated that there is an inverse relationship between bank profitability and bank risk. He suggests that risky activities lead to higher provision of losses, eroding profitability. P. Gao et al. (2018) report a negative relationship between financial distress and stock returns. P. Gao et al. (2018) argue that mispricing is the most reasonable cause because investors have irrational expectations for distressed companies. In contrast, the risk-adjusted returns of these companies are relatively low. Andreou et al. (2021) also suggest that investors overvalue the stocks of financial distress firms. They also show that corporate earnings management practices partly influence mispricing.

Conversely, Chava and Purnanandam (2010) report a positive correlation between financial distress and stock returns. This observation stems from investors demanding higher returns for stocks with higher risk. Furthermore, Liu et al. (2019) provide empirical evidence of a positive link between distress risk and stock market returns in the context of China. It is noteworthy, however, that this outcome applies mainly to non-state-owned enterprises and smaller firms. The rationale is that non-state-owned corporations do not typically offer higher returns as compensation to investors when the business faces distress risk. Imran Hunjra et al. (2020) underscore the principle that when constructing a portfolio to achieve elevated returns, it must be willing to embrace a commensurate level of risk. Andreou (2015) also shows that short-term changes of distress risk, are associated with the higher option implied moments of future stock returns. The risk-return trade-off theory emphasizes that investors must be willing to embrace more significant levels of risk in pursuit of higher profits. Imran Hunjra et al. (2020) demonstrated that, through a momentum strategy, investors can achieve remarkable returns from stocks characterized by elevated risk levels. Avramov and Zhou (2010) also uncovered that stocks with high levels of credit risk often outperform their counterparts in exploring the relationship between financial distress, patterns in cross-sectional average stock returns, and momentum profits. This study suggests that the higher the risk, the greater the rate of return.

As prior studies mixed impacts of distress risk and stock returns and as follow the trade-off and the liquidity risk theory, we propose the following Hypothesis:

H1: Distress risk negatively affects stock returns.

Limits to Arbitrage and Stock Returns

Hung and Yang (2018), alongside Gu et al. (2018), propose three arbitrage limit proxies, including illiquidity (ILLIQ), idiosyncratic volatility (IVOL), and turnover ratio (TURN). Lei et al. (2013) unearthed an inverse association between illiquidity and stock returns in China. Illiquid stocks exhibit heightened susceptibility to trading activity, precipitating selling pressure on these stocks. Consequently, a negative correlation between capital gains, illiquidity, and stock returns ensues. Conversely, Chiang and Zheng (2015) ascertain a positive correlation between market illiquidity risk and stock returns across global markets. Moreover, they discern that illiquidity manifests varying effects on different stock categories. The trade-off theory posits an inverse correlation between distress risk and returns, recognizing an optimal capital structure for a firm maximizing overall value. Within this structure, a delicate balance is achieved, weighing the benefits of leveraging through debt (e.g., tax advantages and reduced cost of capital) against its drawbacks (e.g., distress risk). Phan et al. (2022) argues that when a business faces distress risk, it must address this financial challenge by enhancing liquidity, restructuring debt, or adjusting financial strategies. However, these remedial actions often incur >costs, such as elevated interest payments or the need for corrective measures, potentially diminishing profits. The liquidity risk theory also suggests that investors anticipate higher stock returns, termed a liquidity risk premium, to compensate for the increased risk associated with holding fewer liquid stocks. Stocks of severely distressed firms tend to be illiquid, resulting in reduced profitability (Isayas, 2021).

Ang et al. (2006), Zhong (2018), and Duong et al. (2021) observed that stocks with greater IVOL have lower returns and vice versa. On the other hand, Bali et al. (2011) report a positive relationship between IVOL and stock returns. It is because Bali et al. (2011) estimate IVOL from the CAPM model, while Ang et al. (2006), Zhong (2018), and Duong et al. (2021) estimate IVOL from Fama and French’s three factors model.

Hung and Yang (2018) discovered that turnover adversely affects stock returns in Taiwan. Zhang et al. (2021) found that equities with lower turnover have higher returns in China. Turnover strongly correlates with retail investors seeking speculations and irrational pursuits (Zhang et al., 2021).

Prior studies report that limits to arbitrage decrease the efficiency of the market. According to the information asymmetry Hypothesis, it is difficult to grasp and effectively estimate the worth of assets when information is fair and consistent. Arbitrageurs are less ready to take hazardous bets when there is much information ambiguity. Because of these constraints, market mispricing might persist, and market efficiency will take time to reach (Gu et al., 2018).

We propose the following Hypothesis as prior studies mixed impacts of limit-to-arbitrage factors and stock returns.

H2: Limit to arbitrage factors reduce cross-sectional stock returns.

Data and Methodology

Data

We compile data from financial statements and Vietstock.com of non-financial firms on the HOSE and HNX between January 2008 and March 2021. We incorporate the book-to-market ratio (BM) and size (LnSize) from Fama and French (1992, 1993) into each model. Following Hung and Yang (2018), we remove enterprises with less than 10 trading days to exclude firms with trading restrictions within that month. Furthermore, we mitigate the look-ahead bias by following Fama and French (1992) to match accounting data from fiscal year t-1 to earnings from fiscal year t − 1 through returns from July of year t to June of year t + 1 to confirm that all financial ratios are available. Following Duong et al. (2021), we winsorize variables at 5% and 95% percentile to prevent the outlier issue. We follow Duong et al. (2022) to exclude observations that do not have adequate information to estimate the required variables. Finally, our sample has 35,255 firm-month observations from January 2008 until March 2021.

Research Methodology

Following Altman (1968), we estimate the Z-score as a proxy for the distress risk. The higher Z-score value implies lower distress risk and vice versa. The Z-score function is as follows:

Where:

X1: Working capital/Total assets.

X2: Retained Earnings/Total assets.

X3: Earnings before interest and taxes/total assets.

X4: Market value equity/Book value of total debt.

X5: Sales/Total assets.

We follow Duong et al. (2022) to construct Model 1, which examines the influence of financial distress on cross-sectional stock return. In model 2, we also add the BM and SIZE to evaluate the impact of distress risk after controlling for them:

Following Gu et al. (2018), Hung and Yang (2018), and Duong et al. (2021), we employ three proxies of limits to arbitrage: illiquidity (ILLIQ), idiosyncratic volatility (IVOL), and turnover ratio (TURN). We follow Amihud (2002) to divide the stock returns by monthly trading volume to calculate illiquidity (ILLIQ) for every stock in month t. We follow Ang et al. (2006) and Duong et al. (2021) to measure IVOL for an individual stock.

Furthermore, we follow L. Gao et al. (2019) to add a momentum factor to the model. Finally, we follow Coad et al. (2018) to add firm age (AGE) as the number of years stock has been listed on the stock market at the end of the previous fiscal year. All the variable definitions are explicitly described in Appendix A.

Results

Descriptive Statistics

Table 1 demonstrates the amounts of observations (N), the average value of the stocks across the months (Mean), standard deviations (Std Dev), and the 90th and 10th percentiles for each factor. This table includes a summary of the Vietnamese stock market. The Z-score of Vietnamese manufacturing enterprises is 1.15 on average, which implies that Vietnamese companies have an extremely high level of bankruptcy risk (Duong et al., 2023). The average IVOL value is roughly 9.58%, the 90th percentile is 3.45%, and the 10th percentile is 5.37%, higher than in Taiwan (Duong et al., 2021). Furthermore, the average value of SIZE, BM, stock return (Ret), company age (AGE), illiquidity (ILLIQ), turnover ratio (TURN), and momentum (MOM) are 26.08, 1.67, 1.31, 5.93, 0.32, 7.00, and 10.57, respectively.

Descriptive Statistics Among Firm Characteristics.

Note. Table 1 shows sample descriptive statistics. All variable definitions are described in Appendix A. The sample contains 35,255 firm-month observations from January 2008 to March 2021.

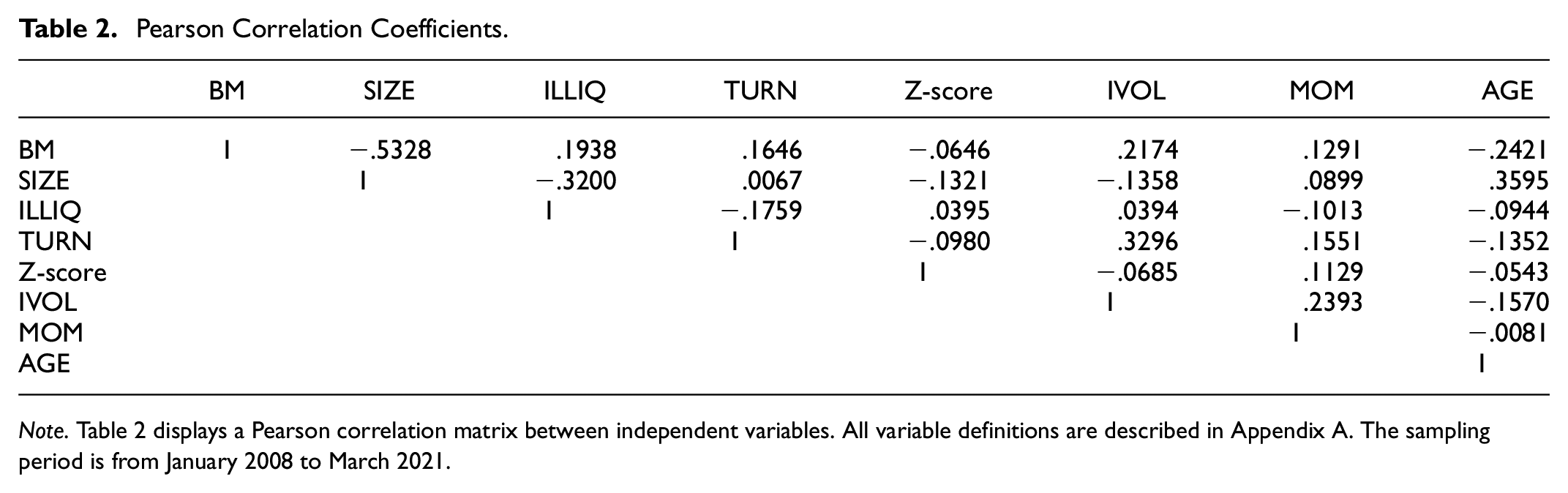

Pearson Correlation Matrix

Table 2 reports the Pearson correlation analysis for independent variables. The table reveals that the book-to-market ratio negatively correlates with SIZE, Z-Score, and AGE, whereas the other five factors positively correlate. The correlation coefficient between SIZE and BM is roughly −.5328, indicating a moderate correlation. In short, all correlation coefficients are less than 0.6, so our sample does not have multicollinearity issue.

Pearson Correlation Coefficients.

Note. Table 2 displays a Pearson correlation matrix between independent variables. All variable definitions are described in Appendix A. The sampling period is from January 2008 to March 2021.

Empirical Results From the Asset Pricing Models

Table 3 analyzes the company’s analytics from largest to smallest by BM and Size to generate SMB and HML factors. We follow Duong et al. (2022) to construct the Z-score Factor (WML_Z). UMD is a factor-mimicking portfolio for momentum in the Carhart four-factor model.

The Fama and French Four-factor Model Augmented With Distress Risk Across Five Distress Risk Quintiles.

Note. Table 3 shows the returns on portfolios sorted by distress risk. RMRF is the excess return. SMB and HML are Fama and French’s factor-mimicking portfolios for size and book-to-market equity. UMD is a factor-mimicking portfolio for momentum. WML is the highest Z-score minus the lowest Z-score. Columns (1) to (5) report the monthly equal-weighted excess returns of the Z-score factor in different portfolios by Z-score.

, **, and * indicate three statistical significance levels. T-statistics are in parentheses.

Table 3 reports indicate the distress risk anomaly because a higher Z-score positively impacts stock returns cross-sectionally. In other words, stocks with less financial distress risk generate higher returns. This result aligns with Duong et al. (2022), P. Gao et al. (2018), and Andreou et al. (2021). However, our findings are inconsistent with Chava and Purnanandam (2010) and Liu et al. (2019) because they report that higher distress risks empower stock returns, aligning with the risk and return Hypothesis.

The estimation results from The Fama and French three-factor model augmented with Z-score and the Carhart four-factor model augmented with Z-score suggest that the HML_Z factors are positive and increase gradually across Z-score subsamples. Our findings imply an inverse relationship between distress risk and stock returns.

Fama and MacBeth Cross-Sectional Regressions

Table 4 also reports that the Z-score positively correlated to stock returns. Specifically, when the Z-score increases by one score, the cross-sectional stock returns increase by about 20%. Therefore, our findings show an inverse relationship between distress risk and stock returns. While our results align with those of Duong et al. (2022), they are inconsistent with those of Liu et al. (2019). Our findings support Hypothesis 1. Our findings align with the liquidity risk theory but do not support the trade-off theory. Specifically, we observe a negative correlation between the likelihood of bankruptcy and profitability. This relationship can be attributed to the increased costs associated with capital acquisition for firms facing heightened distress risk. Recognizing the elevated risk of default or financial distress, lenders and investors may demand higher interest rates or returns. Consequently, the company’s cost of capital rises, posing obstacles to generating favorable returns for its shareholders.

Fama and MacBeth (1973) Regression Results.

Note. Table 4 reports the Fama & MacBeth regression results. All variable definitions are reported in Appendix A. The study period is from January 2008 to March 2021.

, **, and * indicate three statistical significance levels. T-statistics are in parentheses.

We further test whether the Z-score anomaly persists across size subsamples by dividing stock into quintiles. The first quintile includes the smallest stocks, while the fifth quintile has the most extensive stocks. Our findings indicate that the distress risk anomaly appears even more substantial in large firms, implying that one additional score leads to around 28% higher stock returns. However, the coefficients of the Z-score are insignificant in small and micro firms. This result is consistent with de Groot and Huij (2018), who did not find distress risk results in small firms. Small businesses frequently have a moderate scale and flexible operations, so they can swiftly alter their company strategy in challenging circumstances. The modest size also aids in mitigating the impact of unanticipated occurrences and lowering the chance of insolvency.

Table 4 reports that the limit-to-arbitrage factors such as ILLIQ, IVOL, and TURN negatively affect stock returns in all models. The higher limit-to-arbitrage discourages investors from generating arbitrary trading profits, seriously causing stocks to become mispriced. Therefore, mispriced stocks generate lower returns. Our findings align with Lei et al. (2013), Ang et al. (2006), Zhong (2018), Hung and Yang (2018), and Zhang et al. (2021). However, our findings suggest a significant relationship between limit to arbitrage and stock returns persists in small firms only. Our findings support Hypothesis 2, indicating an inverse relationship between limit-to-arbitrage factors and stock returns. In micro firms, the limit to arbitrage is insignificant. Smaller companies frequently have fewer assets and are less likely to attract external financings. As a result, limits-to-arbitrage factors usually have little impact on the shares of tiny enterprises. Table 4 reports that after controlling limits arbitrage factors, the coefficients of Z-reduce from 0.2656 to 0.2015. Limit to arbitrage factors make stocks of distressed companies more challenging to sell because they are illiquid. Limit to arbitrage factors amplify mispricing, so investors may only partially earn returns from investing in less distressed stocks.

Finally, Table 4 reports that corporate bankruptcy regulation significantly affects distress risk in Vietnam. The Z-score puzzle disappeared after the bankruptcy regulation in Vietnam was enacted. Sautner and Vladimirov (2018) explain that tighter controls on bankruptcy have helped troubled companies reduce indirect distress costs, thereby reducing the risk of bankruptcy of a business. Bankruptcy Law 2014 has made the legal procedure of resolving bankruptcy cases more transparent, fairer, and more professional. This regulation has aided in increasing stakeholder confidence and facilitating company reorganization and resumption.

Robustness Test by Univariate Portfolio-Level Analysis

This section tests whether our findings are robust using a univariate portfolio sorting methodology. We follow Duong et al. (2022) to sort stocks into terciles by Z-score. We also estimate the return difference between the highest and lowest Z-score stocks. Table 5 reports a positive returns gap between the lowest and highest Z-score subsamples. Our findings indicate that the lower the distress risk, the higher the stock return. The return difference between the low and high Z-score portfolios is 0.69% per month in value-weighted portfolios. The return difference in equal-weighted portfolios is 0.52% per month. Our findings are consistent with Duong et al. (2022). Finally, Table 5 reports that the distress risk puzzle disappears in the micro and small stocks. The distress risk puzzle also disappeared after the bankruptcy regulation was implemented.

Average Returns on Portfolios of Stocks Sorted by Z-score.

Note. Table 5 reports the VW and EW return gaps and the Fama-French Three-Factor alpha differences between high and low Z-score portfolios. Table 5 reports the average raw and risk-adjusted returns across Z-score terciles. The study period is from January 2008 to March 2021.

, **, and * indicate three statistical significance levels. T-statistics are in parentheses.

Robustness Tests by Bivariate Portfolio-Level Analysis

This section tests whether our findings are robust using a dependent portfolio sorting methodology. First, we sort stocks into terciles based on the Z-score. Then, within each Z-score portfolio, we sort stocks into terciles based on their BM, SIZE, MOM, ILLIQ, TURN, IVOL, and AGE. The value-weighted returns gap between high and low Z-score portfolios after controlling for BM, SIZE, momentum (MOM), illiquidity (ILLIQ), turnover (TURN), idiosyncratic volatility (IVOL), and AGE is reported in Table 6.

Returns on VW Portfolio Sorted by Z-score and Other Variables.

Note. Table 6 reports the VW return gap and the Fama-French Three-Factor alpha difference between high and low Z-score portfolios after controlling for firm characteristics. Table 6 also reports the average raw and risk-adjusted returns across Z-score terciles. The study period is from January 2008 to March 2021.

, **, and * indicate three statistical significance levels. T-statistics are in parentheses.

Panel A report The VW average return gap between the high and low Z-score portfolios for the whole sample. Positive and significant return gaps exist between the Z-score and other control variables. Three-factor Fama French alpha differences are also statistically significant. Our findings confirm the persistence of the Z-score anomaly, even after controlling for firm characteristics.

Panel B and C report that the VW average return gap between the high and low Z-score portfolios in micro and small firms is statistically insignificant. However, the return gap between the high and low Z-score stocks is positive and significant in large stocks. Therefore, the Z-score anomaly is more robust in large firms than in smaller ones. The prominence of large corporations in the market spotlight amplifies the impact of any signs of distress or instability. Given the heightened attention from investors, even minor indicators of trouble within these firms can prompt widespread concern and investor panic. Consequently, such occurrences can significantly undermine the business profits of big companies.

We test the relationship between stock returns and Z-scores in panels E and F after the Vietnamese government enacted the corporate bankruptcy law in 2015. In panel E, the VW average monthly returns difference between High Z-score and Low Z-score portfolios after controlling for SIZE, ILLIQ, and TURN are 0.68%, 0.71%, and 0.81% per month, respectively. However, after the Vietnamese government enacted the bankruptcy law in 2015, there were statistically insignificant return differences between the Z-score and other control variables, except BM, IVOL, and AGE. Our research indicates that the Z-score anomaly diminishes following the implementation of bankruptcy law in Vietnam. The enactment of such legislation establishes a comprehensive legal framework for addressing distressed companies. This clarity diminishes uncertainty among investors, creditors, and companies themselves, as they now possess well-defined procedures and rights in the event of financial distress. With clearer guidelines and processes, stakeholders will likely feel more assured in their interactions with distressed firms, reducing the risk of financial distress escalating into insolvency.

Table 7 also reports the EW average return differences between the high and low Z-score portfolios. This result is similar to Table 6, implying that the Z-score puzzle persists after controlling for limit-to-arbitrage factors. In addition, the Z-score puzzle is even more pronounced in larger firms than before the enactment of Vietnam’s bankruptcy law.

Returns on Equal Weighted Portfolios Portfolio Sorted by Z-score and Other Variable.

Note. We dependently sort stocks into terciles by Z-score and other variables. Table 7 reports the EW return gap and the Fama-French Three-Factor alpha difference between high and low Z-score portfolios. Table 7 also reports the average raw and risk-adjusted returns across Z-score terciles. The study period is from January 2008 to March 2021.

, **, and * indicate three statistical significance levels. T-statistics are in parentheses.

Conclusion

This study is a pioneering attempt to examine how limit-to-arbitrage factors impact the distress risk puzzle before and after the enactment of bankruptcy regulations. We utilize asset pricing models, portfolio sorting techniques, and the Fama and French four-factor model to analyze an unbalanced panel with 35,255 firm-month observations from non-financial companies listed on the Vietnam stock market between 2008 and 2021.

Our research reveals a persistent distress risk anomaly, indicating that firms with higher distress risk tend to yield lower returns. Specifically, we find that a one-point increase in the Z-score corresponds to an approximately 20% increase in cross-sectional stock returns. These findings are consistent with the observations of Duong et al. (2022) but diverge from the conclusions of Liu et al. (2019). Our results support both the liquidity risk theory and the trade-off theory. Furthermore, our analysis highlights that larger firms’ distress risk anomaly is even more pronounced. A one-point increment in the Z-score is associated with approximately 28% higher stock returns in large enterprises. This result suggests that larger companies are more susceptible to the impact of distress risk. Their size makes investors react more sensitively to instances of distress risk, thereby negatively affecting profitability. In addition to this, our investigation reveals that limit-to-arbitrage factors exert a negative influence on stock returns across all our models. Notably, we also find that implementing the corporate bankruptcy regulations in Vietnam affects distress risk. The Z-score puzzle disappears following the enactment of these regulations, implying that well-defined legal frameworks enhance investor confidence in the recovery prospects of distressed businesses.

The findings of this research carry significant implications for investors and market participants, particularly those operating within the Vietnamese financial landscape. Our study reveals that stocks characterized by higher distress risk tend to yield diminished returns, which prompts strategic considerations for investors. Investors should carefully contemplate the prudent reallocation of their investment portfolios. Mitigating exposure to equities exhibiting elevated distress risk can be a strategic move. This suggestion involves a more discerning approach to asset allocation, favoring financially robust and stable stocks to counterbalance potential vulnerabilities.

Moreover, our empirical findings are relevant for large corporations and their managers. It highlights that bankruptcy risk and limits to arbitrage have a more pronounced impact on firms with substantial capital. Consequently, businesses should consider adjusting their debt ratios in their operational strategies. Implementing more robust debt enforcement measures within the bankruptcy framework, as suggested by Sautner and Vladimirov (2018), can help reduce indirect distress costs and create a conducive environment for effective restructuring before resorting to bankruptcy proceedings. Another crucial implication of our research is that companies must enhance their corporate governance practices in response to distress risk. With bankruptcy risk and limits to arbitrage exerting a more significant impact on firms with substantial capital, it becomes essential for large corporations and their managers to prioritize governance mechanisms that promote transparency, accountability, and risk oversight. By implementing robust corporate governance frameworks, companies can effectively identify and mitigate distress risk factors, safeguarding shareholder value and bolstering investor confidence. This recommendation includes establishing independent board oversight, enhancing disclosure practices, and fostering a culture of ethical conduct and compliance.

Furthermore, our research offers valuable insights for government policymakers aiming to alleviate financial distress through efficient corporate regulatory reforms. Policymakers should focus on refining and strengthening bankruptcy regulations and enforcement mechanisms. This study underscores the substantial influence of bankruptcy regulation in mitigating distress risk, which can, in turn, enhance investor confidence and provide a robust safety net for businesses facing financial challenges. In addition, initiatives to enhance financial literacy among entrepreneurs and business owners can play a pivotal role. When businesses possess a deeper understanding of financial management principles, they are better equipped to navigate financial turbulence, manage debt effectively, and make informed decisions that reduce distress risk. Government agencies can facilitate improved access to finance for businesses, significantly smaller enterprises that may encounter difficulties in obtaining credit. Ensuring a conducive environment for affordable loans and financing options can significantly reduce distress risk in the business landscape.

Although our study contributes to the growing literature on the distress risk puzzle in emerging markets, we have data limitations because it only focuses on listed firms in Vietnam. In other words, our findings may not be relevant to other emerging markets due to different market microstructures. Future studies may consider a broader context by performing a cross-country analysis to investigate the influence of distress risk and limit-to-arbitrage factors on stock returns.

Footnotes

Appendix A

Variable Definitions.

Acknowledgements

We thank anonymous reviewers for constructive feedback, which support us in developing the manuscript.

Author Contribution Statement

Khoa Dang Duong (

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study is supported by Ton Duc Thang University and Van Lang University.

Ethical Statement

This study does not involve human studies.

Informed Consent

This study does not involve human studies.

Data Availability Statement

The data that support the findings of this study are available from the corresponding author, [Dr. Hoa Thanh Phan Le], upon reasonable request.