Abstract

Urbanisation is a global issue, and remittances are also a key financial channel contributing to economic development in countries. However, the relationship between remittances and urbanisation is quite faint in current academic literature. This paper aims to provide new findings to fill this theoretical gap. Unlike previous research, this study may be the first to use a large international sample of 96 countries from 1990 to 2020 to investigate the impact of remittances on urbanisation. In addition, the results are diverse when the database is estimated at various sizes, including a full sample and subsamples by region and income level. The regression results unveil that remittances have a positive effect on urbanisation if the estimation uses the full sample. However, when examining subsamples by region, the results show that remittances only support urbanisation in less developed regions. Moreover, the findings from the regression indicate that remittances can reduce urbanisation in high-income countries. Migration, private investment and government spending have robustly positive effects on urbanisation in most samples. Additionally, foreign direct investment has a positive effect on the development of urbanisation in subsamples. However, the estimated results confirm that household expenditures can harm urbanisation. Finally, some implications are included for increasing the future efficiency of the policy-making process.

Introduction

Global urbanisation has occurred rapidly in recent decades (Henderson & Turner, 2020). Moreover, urbanisation is an inevitable social phenomenon in countries’ development processes (Arboleda, 2015; Goodfellow, 2017; Kuddus et al., 2020). Developed countries are witnessing a slower trend in the speed of urbanisation, however, while the rate of urbanisation is increasing rapidly in developing countries (Collier, 2017; Gu, 2019). The relationship between urbanisation and socioeconomic issues has been studied in recent times and it is still receiving much interest from both academics and policymakers (Streule et al., 2020). For example, urbanisation has been shown to spark economic growth (Pradhan et al., 2021), enhance per capita income (Arouri et al., 2014) and improve households’ standard of living (Henderson & Turner, 2020).

Urbanisation offers benefits through the financial system or investment in redevelopment projects or housing financialisation (Baliga & Weinstein, 2022). In the globalisation era, remittances have been one of the key monetary and financial flows worldwide. In recent decades, international finance, such as remittances, is an element that might be closely related to the real estate market and urbanisation in recipient countries (Ahmed et al., 2021; Hamouri, 2020; Klaufus, 2010). Nevertheless, the connection between remittances and urbanisation remains largely unexplored, both theoretically and empirically. Remittances have been increasing and growing year by year, particularly in developing countries (Chowdhury, 2016). Additionally, remittances have become the second-largest source of external finance in developing countries after foreign direct investment (FDI) (Aggarwal et al., 2011; Giuliano & Ruiz-Arranz, 2009; Glytsos, 2002). In particular, remittances have been stable and tended to increase despite the global socioeconomic crises in recent decades (Kenneth, 2019).

While remittances are widely acknowledged as vital for economic growth (Bucevska & Naumoski, 2023; Islam, 2021), their influence on urbanisation remains underexplored, both in terms of theoretical perspectives and empirical research. There is little empirical evidence to clarify the impact of remittances on urbanisation, creating a research gap for this academic topic. This study seeks to examine the effects of remittances on urbanisation in order to address the existing gap in the current literature. In addition, the empirical results help in identifying policy implications to solve the problem of creating measures to optimise remittance flows toward urbanisation.

In general, this study provides three main contributions to the current literature. First, remittances are used as a factor affecting urbanisation in a global sample of countries; therefore, the results show new findings regarding urbanisation issues. This study may be the first to focus on the relationship between remittances and urbanisation with a massive sample of countries. Second, by dividing the research into subsamples, the study has critical policy implications for policymakers in various regions at different income levels. Third, this paper delivers the most up-date perspective regarding the remittances–urbanisation nexus and helps expand the current theoretical framework, which is currently quite thin.

This paper is structured into five sections. The Literature Review provides the theoretical framework and a brief overview of previous empirical studies. The Methodology section presents the econometric model and describes the data. The Results and Discussion section includes correlation analysis, estimated results for the full sample, for subsamples by region, for the subsamples by income level and discuss. Finally, the Conclusion and Policy Implications section summarizes the findings and offers suggestions for policymakers.

Literature Review

Theoretical Framework

Urbanisation has been recognised as a global issue in this century (OECD, 2012). An increased urbanisation level can lead to an increase in economic growth (Brunt & García-Peñalosa, 2021; Pradhan et al., 2021). Consequently, economic growth leads to increased investment in education, health and infrastructure and shifts the economy to productive sectors and higher income (Arouri et al., 2014; Mishra et al., 2009; Rosenthal & William, 2004). In addition to influencing economic growth and investment trends (Nguyen & Nguyen, 2018), urbanisation significantly contributes to changing economic structures and altering population dynamics. Urbanisation causes the economic structure to gradually shift from agriculture to industry, manufacturing and services (Jones, 1991). At the same time, urbanisation helps increase labour productivity and incomes through specialisation and division of labour (Aziz et al., 2012; Moomaw & Shatter, 1996). Moreover, urbanisation leads to the development of better health facilities and transport infrastructure (Arouri et al., 2014; Mishra et al., 2009; Rosenthal & William, 2004). These investments usually first occur in urban areas and large cities (Elliott et al., 1996). Therefore, urbanisation has the effect of causing people to migrate from rural areas to big cities (Elliott et al., 1996; Poumanyvong & Kaneko, 2010).

Much of the capital flowing into countries-often in the form of international aid and remittances – has been concentrated on urban land and real estate (Abbas et al., 2023; Kagochi & Kiambigi, 2012; Obi et al., 2020). When remittances are sent to recipient countries, they serve as an immediate financial resource for households, often used to improve living conditions, particularly in repairing or expanding existing homes (Obeng-Odoom, 2010). Remittances are not tied to debt repayment obligations like bank credit, therefore, they can be used for long-term targets of households. The households may also construct new, larger residences or acquire additional agricultural land for housing development (Kagochi & Kiambigi, 2012). These practices contribute to the process of urbanisation. As the number of private homes grows alongside rising urbanisation, governments are prompted to plan and develop urban infrastructure systems to accommodate this expansion. Remittances can also serve as financial resources in the form of informal credit (Ambrosius & Cuecuecha, 2016), enabling households to expand their property ownership in the real estate market. In regions where remittance inflows are substantial, the real estate market tends to grow due to increased demand from recipient households (Khan et al., 2022; Kulikauskas, 2016).

Previous Empirical Studies

Several studies have reported the relationship between remittances and urbanisation. For example, in an empirical study, Buckley and Mathema (2007) reported that remittances created more family housing and could help provide new jobs. At the same time, however, remittances were also significantly driving up housing prices. Therefore, remittances could contribute to slower rural-to-city migration. Nonetheless, this empirical study did not explain the link between remittances and urbanisation. Obeng-Odoom (2010) concluded that rapid population growth and low incomes led to housing shortages in Ghana. Migration to rich countries was a solution for some Ghanaians to solve this problem when they sent back their salaries to build houses in their homelands. The study’s results show that remittances enhanced urbanisation in Ghana. The results did not include other international financial variables in their analysis. Meanwhile, Klaufus (2010) investigated the expanding process of urbanisation in intermediate cities in Central America. The study described the construction boom of high class real estate regions for the middle class. However, many people in this income group could access migrant remittances, and the study results suggested that sustainable urbanisation was challenged by the privatisation of urban planning. But the connection between urbanisation and international finance was not discussed or analysed in this study.

In recent decades, the Bangladesh economy received record levels of remittance income. Mottaleb et al. (2016) explored variables related to housing prices in Bangladesh with particular attention to the role of remittance income. The results showed that remittances contributed to raising housing prices in Bangladesh. Therefore, the link between remittances and urbanisation was unveiled for Bangladesh (Mottaleb et al., 2016). In a study on real estate and urbanisation in African cities, Goodfellow (2017) argued that today real estate must be both a driving force and a symbol of urban development. However, the incentives to invest in urban land and real estate that were shaping urban transition in some of the world’s least urbanised countries have received little attention. In general, in developing countries, the real estate market and housing products are places for investment from financial flows such as remittances.

Recently, Cismaş et al. (2020) reported on the one hand that remittances were a financial source for living expenses in low-income countries. On the other hand, remittances were part of a diversified financial portfolio and could stimulate the financial sector in middle-income countries. Therefore, remittances did not influence the real estate market or urbanisation. This finding from a high-income country in Eastern Europe does not appear to be a common phenomenon when examined across a multi-country sample. Hamouri (2020) explored the potential effect of remittances on the real estate market in Jordan. The results confirmed that remittances had a positive impact on the real estate market through investment, construction and the expansion of development in large areas. Moreover, the results demonstrated that the ratio of population and per capita income had positive impacts on investment in the real estate market in Jordan. The number of remittances sent from abroad to Jordan increased, which led to an increase in investment in the real estate market and urbanisation. The findings unveil to a relationship between remittances and urbanisation that requires further clarification in cross-national samples.

Wijburg et al. (2020) analysed transnational real estate networks that affected trading activities in the Cuban housing market. The study’s results indicated links between the legalisation of housing prices set between Cuban migrants and a few foreign investors in cooperation with Cubans residing in Cuba. These activities could provide benefits for urbanisation when investors use money from abroad for buying properties in Cuba’s cities, towns and beach resorts. In another study, Ahmed et al. (2021) investigated the link between foreign capital inflows and the housing market in Pakistan. The study revealed that housing prices in Pakistan have significantly increased year by year. The prices of houses were pushed by foreign financial sources such as remittances and FDI as well as domestic elements including population, urbanisation and migration (Ahmed et al., 2021). The results implied that the remittances had a considerable contribution to urbanisation by increasing the income level of households.

In sum, previous results regarding the link between remittances and urbanisation are quite complex and unclear. Furthermore, most studies use old databases, which can lead to mistakes in the current policy-making process. There is high demand for a study focusing on the effect of remittances and urbanisation using an updated international database. To the best of our knowledge, there is no research focused only on the link between remittances and urbanisation. Therefore, this study contributes by filling the empirical research gap in the current literature.

Methodology

Econometric Model

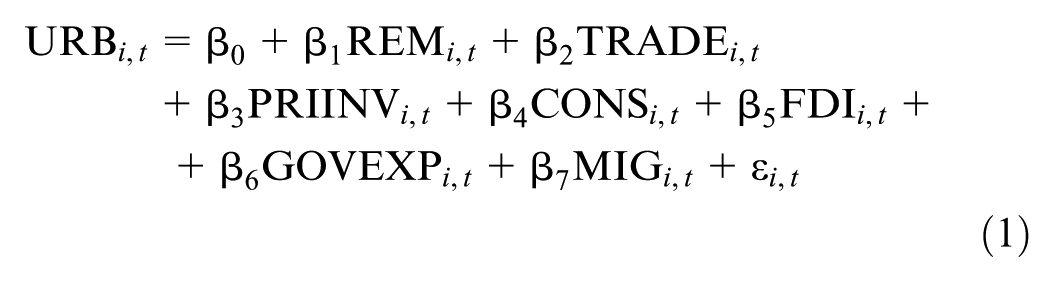

Based on previous studies (Buckley & Mathema, 2007; Hamouri, 2020), in the econometric model, the dependent variable is urbanisation and remittances is the independent variable. Several other factors that can affect urbanisation are included as control variables, such as trade openness (Hofmann & Wan, 2013; Hussain & Imitiyaz, 2018; Shahbaz et al., 2015), private investment (Charney, 2001; Liu et al., 2018), household spending (Arouri et al., 2014; Haryanto et al., 2021), FDI (Dash et al., 2020; Shen & Lin, 2017), government spending (Davis & Henderson, 2003; Fox, 2012; Yang et al., 2019) and migration (Chen et al., 2011). Therefore, the econometric model is established as per the following equation:

Where, URB denotes urbanisation; REM represents remittances, TRADE is trade openness, PRIINV denotes private investment, CONS is household spending, FDI is foreign direct investment, GOVEXP represents government expenditures and MIG is migration. In addition, i is the cross-sectional unit with iϵ [1, N] and t denotes periods.

For the quantitative procedure, the regression of equation (1) applied three techniques including the Ordinary least squares (OLS), the General least squares (GLS), the 2-Stage Least Squares (2-SLS) and Generalised Method of Moments (GMM). First, a panel OLS estimation is employed with both a fixed effects model (FEM) and a random effects model (REM). In detail, FEM estimation is useful when the omitted variables are correlated with explanatory variables, as it helps eliminate omitted variable bias arising from unobserved characteristics (Wooldridge, 2010). Besides, REM estimation utilises both within and between variations, potentially yielding more precise estimates under appropriate conditions (Greene, 2018). For selecting the better model between FEM and REM, this study employed the Hausman test (Hausman, 1978). The Hausman test helps check the null hypothesis that the unobservable individual-specific random errors are uncorrelated. If the p-value is lower than .05, the null hypothesis will be rejected. REM is biased, and an FEM result is better. However, panel OLS regression has received some concerns as it may produce biased and inconsistent coefficients due to some issues with econometric models such as heteroskedasticity and autocorrelation.

Therefore, in the second step, the GLS method is employed in the regression process (Wooldridge, 2010). This method can eliminate heteroskedasticity and autocorrelation problems in the estimated equation.

In third step, the 2-SLS estimation is employed for dealing-with the endogeneity problem in the econometric model (Wooldridge, 2010). The Durbin–Wu–Hausman test is used to check for this diagnotic issue by using the ‘estat endog’ command in Stata. Finally, the GMM method is used to estimate the econometric model (Arellano & Bond, 1991), using the ‘xtabond2’ in Stata. It is widely recognised as one of the most powerful approaches for addressing endogeneity and other econometric issues (Ullah et al., 2018). Some tests, including the Arellano-Bond and Sargan tests, will be employed to examine the presence of endogeneity in the estimated results. Based on recommendations from previous studies (Bellemare et al., 2017; Reed, 2015), endogenous variables can be substituted with their lagged values.

Data Description

This paper uses a database directly downloaded and calculated from the World Development Indicators (World Bank, 2025). In detail, remittances, trade openness, private investment, household spending, FDI, government expenditures and migration are obtained from the World Bank. Based on previous studies, the remittance variable is measured as the percentage of personal remittances received relative to GDP (Giuliano & Ruiz-Arranz, 2009; Sobiech, 2019), while the urbanisation variable is represented by the proportion of the urban population in the total population (Abbas et al., 2023; Pradhan et al., 2021). A brief description of the definitions and measurements of the variables is provided in Table 1.

Definitions and Measurements of the Variables.

Source. Authors’ own calculations.

This study obtains an unbalanced panel dataset of 96 countries for the period 1990 to 2020. We tried our best to collect the largest international sample but some countries were excluded because they did not have enough data for the variables. In addition to the full sample, several sub-samples have been created based on region and income level. The subdivision of these sub-samples is based on data from the World Development Indicators (World Bank, 2025).

Considering the regional differences in economic development, the full sample was divided into six subsamples including Latin America and the Caribbean (18 countries: Argentina, Bolivia, Brazil, Barbados, Colombia, Costa Rica, Dominican Republic, Ecuador, Guatemala, Guyana, Honduras, Jamaica, Mexico, Nicaragua, Peru, Paraguay, El Salvador, Venezuela), Europe and Central Asia (31 countries: Albania, Austria, Belgium, Bulgaria, Switzerland, Cyprus, Germany, Denmark, Spain, Estonia, Finland, France, United Kingdom, Greece, Croatia, Hungary, Ireland, Iceland, Italy, Kyrgyz Republic, Luxembourg, Netherlands, Norway, Poland, Portugal, Romania, Russian Federation, Slovak Republic, Slovenia, Sweden, Turkey), the East Asia and the Pacific (10 countries: Australia, China, Fiji, Japan, Cambodia, Korea Rep, Malaysia, Philippines, Thailand, Vanuatu), Middle East and North Africa (6 countries: Algeria, Egypt Arab Rep, Israel, Jordan, Malta, Tunisia), Sub-Saharan Africa (26 countries: Benin, Burkina Faso, Botswana, Cote d’Ivoire, Cameroon, Congo Rep, Gabon, Ghana, Guinea, Guinea-Bissau, Kenya, Madagascar, Mali, Mozambique, Mauritius, Niger, Nigeria, Rwanda, Sudan, Senegal, Sierra Leone, Eswatini, Seychelles, Togo, Tanzania, South Africa) and South Asia (5 countries: Bangladesh, India, Sri Lanka, Nepal, Pakistan).

In addition, the full sample was also separated into three groups based on per capita income at low, medium and high levels. The first group is low-income countries including 11 countries (Burkina Faso, Congo Rep, Guinea-Bissau, Madagascar, Mali, Mozambique, Niger, Rwanda, Sierra Leone, Sudan, Togo), the second group is middle-income countries including 52 countries (Albania, Algeria, Argentina, Bangladesh, Benin, Bolivia, Botswana, Brazil, Cambodia, Cameroon, China, Colombia, Costa Rica, Cote d’Ivoire, Dominican Republic, Ecuador, Egypt Arab Rep, El Salvador, Eswatini, Fiji, Gabon, Ghana, Guatemala, Guinea, Guyana, Honduras, India, Jamaica, Jordan, Kenya, Kyrgyz Republic, Malaysia, Mauritius, Mexico, Nepal, Nicaragua, Nigeria, Pakistan, Paraguay, Peru, Philippines, Russian Federation, Senegal, Seychelles, South Africa, Sri Lanka, Tanzania, Thailand, Tunisia, Turkey, Vanuatu, Venezuela) and the third group is high-income countries including 33 countries (Australia, Austria, Barbados, Belgium, Bulgaria, Croatia, Cyprus, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Israel, Italy, Japan, Korea Rep, Luxembourg, Malta, Netherlands, Norway, Poland, Portugal, Romania, Slovak Republic, Slovenia, Spain, Sweden, Switzerland, United Kingdom). The study sample may be the largest and the first one used in research on this topic. Table 2 presents a statistical summary of the study data.

Descriptive Statistics of the Variables.

Source. Authors’ own calculations.

The descriptive statistical analysis shows that the average urbanisation rate is 56.32% ranging from 5.41% (the minimum level) to 98.07% (the maximum level). Besides, the average remittance volume is 3.02% of GDP, ranging from the lowest of 0.002% to the highest of 32.5% of GDP in the receiving countries.

Results and Discussions

Correlation Analysis

Table 3 presents the correlation matrix analysis of the relationship between urbanisation and the independent variables. Based on the calculated results, first, all correlation coefficients are significant at the 5% level. Second, except for the household final consumption expenditure variable, the relationships between the other independent variables and urbanisation are positive. These correlation analysis results help to predict a positive effect of remittances on urbanisation in this study.

Correlation Analysis Result.

Source. Authors’ own calculations.

Represents the statistical significance level of 5%.

Subsequently, the Variance Inflation Factor (VIF) is used to assess multicollinearity among the independent variables. In Table 3, all VIF values are relatively small, ranging from 1.24 (the minimum) to 1.73 (the maximum). Because all VIFs are well below 10, Equation (1) does not suffer from multicollinearity.

Estimated Results for the Full Sample

In the first step, a panel OLS technique was used to include the estimation of equation (1) with both FEM and REM. From the results obtained (Table 4), a Hausman test helped to select the better model. The testing result shows that Prob > χ2 = .000 (<.05), so the FEM is accepted. In addition, a modified Wald test and Wooldridge test also confirmed that the FEM result faced heteroskedasticity and autocorrelation problems. Therefore, the GLS method was applied in the quantitative analysis process. The 2-SLS and GMM estimation methods are employed to address the endogeneity problem in the model. The Durbin–Wu–Hausman test indicates that endogeneity is not present at the 5% significance level (for 2-SLS), while the Arellano–Bond and Sargan tests also confirm the validity of the GMM estimation at the 1% level.

Regression Model Results.

Source. Authors own work.

Note. p-Value is in ( ).

Represent statistical significance levels of 1%, 5% and 10%, respectively.

In Table 4, all methods including FEM, GLS, 2-SLS, GMM indicate that remittances have positive and significant effects on countries’ urbanisation processes. The highter the percentage of remittances in the GDP of recipient countries, the higher the urbanisation level. Specifically, a 1% increase in remittances would lead to a 0.213% increase in the urbanisation level according to the FEM estimation, a 0.306% rise according to the GLS estimation, a 0.444% rise according to the 2-SLS estimation and a 0.028% increase based on the GMM method. This evidence is a critical finding when, for the first time, a large international sample of countries was used for estimation. Our result expands the current literature by identifying a positive effect of remittances on urbanisation in a global sample including 96 countries. Our finding is also supported by discussions in previous studies by Buckley and Mathema (2007) and Hamouri (2020). Remittances boost household income, giving recipient families more financial means to renovate and enlarge their homes. They also enable these households to buy additional farmland and construct bigger houses. Moreover, the increased spending power raises local demand for goods, leading to the expansion of existing factories or the establishment of new ones to boost production capacity. Consequently, remittances play a role in driving urbanisation

The impact of trade openness on urbanisation is negatively significant for the GLS, 2-SLS, GMM estimations, where a 1% increase in trade openness would stimulate urbanisation to decrease by 0.074%, 0.965% and 0.018%, respectively. The situation is the same for remittances, where private investment also positively affects urbanisation in both estimated models. In detail, a 1% increase in private investment would lead to a 0.03% increase in urbanisation level for the FEM estimation, a 0.112% in the GLS model, a 0.121% for the 2-SLS estimation and a 0.011% for the GMM. This result identifies a positive effect of private investment on urbanisation in a global sample including 96 countries. Increased private investment leads to the expansion of production and triggers the conversion of agricultural land into industrial zones and the construction of new factories. This phenomenon explains the impact of private investment on urbanisation. Our result is in also line with previous studies such as Charney (2001) and Liu et al. (2018). The FDI variable has a positive effect on urbanisation, with coefficients that are significant at the 5% level in the 2SLS method and at the 1% level in the GMM method. Therefore, the findings suggest that FDI promotes urbanisation in recipient countries. Our results extend previous findings such as those by Wu and Chen (2016) in China or Udemba and Philip (2022) in Indonesia or Grekou and Owoundi (2020) in some African countries, by using a larger global sample.

In the GLS and 2-SLS estimation, the household expenditure variable is found to harm urbanisation. This finding means that an increase in household expenditures can reduce urbanisation. Specifically, a 1% increase in household expenditures would lead to a 0.635% decrease in the urbanisation level for the GLS model, a 0.725% with the 2-SLS, and a 0.009% with the GMM at a 1% significance level. This result is also consistent with previous works of Arouri et al. (2014) and Haryanto et al. (2021). The effect of government spending is positive on urbanisation, which is unveiled by the GLS and 2-SLS model. A 1% increase in government spending would stimulate a 0.432% increase in the urbanisation level according to the GLS, a 0.296% with the 2-SLS method and a 0.002% with the GMM. This finding means that government spending has an important role in countries’ urbanisation process. This finding is supported by previous studies (Davis & Henderson, 2003; Fox, 2012; Yang et al., 2019).

Due to missing values in the international migrant stock data (MIG variable), the GMM method could not be applied, and this variable was excluded from the model in the GMM estimation. Migration can have a positive effect on urbanisation. This result is robust when confirmed by FEM, GLS, 2-SLS estimation. A higher number of people joining the migration flow can lead to an increase in urbanisation status in countries. This evidence highlights the findings in previous studies (e.g. Chen et al., 2011). However, unlike previous studies, the current results expand the existing literature by using a larger international sample.

Estimated Result for the Subsamples by Region

In this section, the full sample is divided into six subsamples by region, namely Latin America and the Caribbean, Europe and Central Asia, East Asia and the Pacific, the Middle East and North Africa, Sub-Saharan Africa and South Asia. By estimation with subsamples, the results show more detail on the effect of remittances on urbanisation in various regions. Because of variances in socioeconomic characteristics between regions, the results provide further evidence for discussion regarding the relationship between remittances and urbanisation.

First, in Table 5, the FEM estimation shows that there results among the regions differ. In particular, remittances have a significantly positive impact on urbanisation only in Sub-Saharan Africa. This result is consistent with previous studies by Buckley and Mathema (2007). In detail, a 1% increase in remittances can increase the urbanisation rate by 0.570% in Sub-Saharan Africa at the 1% significance level. Positive effects from remittances on urbanisation were also found in Europe and Central Asia, East Asia and the Pacific and South Asia, but the coefficients are not statistically significant.

Regression Results by Region, FEM Estimation.

Source. Authors own work.

Note. p-Value is in ( ).

Represent statistical significance levels of 1%, 5%, respectively.

The impact of trade opening on urbanisation is positive and significant only in Europe and Central Asia – all the coefficients are insignificant in other regions. The finding of international trade helping increase urbanisation is consistent with previous studies such as Hamouri (2020). Private investment also has a significantly positive effect on urbanisation in two regions: Latin America and the Caribbean and Sub-Saharan Africa. This evidence demonstrates a positive effect of private investment on urbanisation (Charney, 2001; Liu et al., 2018).

In contrast, household expenditures are found to harm urbanisation in the Middle East and North Africa region, where a 1% increase in household expenditures causes a decrease in urbanisation by 0.303% at a 1% significance level. This result is aligned with previous works of Arouri et al. (2014) and Haryanto et al. (2021). This evidence can be explained due to the trade-off between the necessary demands of households in poor countries, for example, they can use money for buying food instead building or buying a house.

The study also finds that FDI can enhance urbanisation in Sub-Saharan Africa because its coefficient is significantly positive, meaning that the more value of FDI received, the more urbanisation countries obtain. Some concerns regarding the impact of FDI on urbanisation in Sub-Saharan Africa include that the environment can be harmed (Lokonon & Mounirou, 2019). However, the estimated results cannot reveal the effect of government expenditure on urbanisation because all coefficients of this variable are not significant.

Based on the regression results, migration has both positive and negative effects on the urbanisation process. Migration has a positive impact on urbanisation in Europe and Central Asia and East Asia and the Pacific. In particular, a 1% increase in migration leads to a 0.206% and a 1.81% increase in urbanisation in Europe and Central Asia, and East Asia and the Pacific region, respectively. This evidence highlights findings in previous studies (Chen et al., 2011). The results also show that migration harms the urbanisation process in Latin America and the Caribbean, where a 1% increase in migration causes an urban decrease of 3.831%. For other regions, the coefficients are not significant.

Second, the GLS estimation is applied to investigate the study issues. In Table 6, because of the negative coefficients, the remittances have a reducing effect on urbanisation. Remittances can harm urbanisation in most regions, including Latin America and the Caribbean, Europe and Central Asia, East Asia and the Pacific, the Middle East and North Africa and South Asia. Specifically, a 1% increase in remittances would reduce urbanisation by 0.195% in Latin America and the Caribbean, 1.155% in Europe and Central Asia, 1.447% in East Asia and the Pacific, 1.078% in the Middle East and North Africa and 1.226% in South Asia.

Regression Results by Region, GLS Estimation.

Source. Authors own work.

Represent statistical significance levels of 1%, 5% and 10%, respectively.

Remittances, however, were found to have a positive impact on urbanisation in the Sub-Saharan Africa region. This result is in line with the FEM estimation. The positive effect of remittances on urbanisation can be explained by the financial flows being transferred to investment in recipient countries, thereby increasing urbanisation (Hamouri, 2020). In contrast, in some other regions, remittances harm urbanisation. This finding is also discussed in some related studies (e.g. Barajas et al., 2009; Catrinescu et al., 2009; Chami et al., 2005), where the negative impact of remittances on urbanisation is understood to be because remittances are mainly used for consumption. Therefore, remittances do not stimulate urbanisation.

Trade openness has a significantly positive effect on urbanisation in Europe and Central Asia, the Middle East and North Africa, Sub-Saharan Africa and South Asia. A 1% increase in trade openness stimulates urbanisation to increase by 0.044%, 0.079%, 0.188% and 0.083% in Europe and Central Asia, the Middle East and North Africa, Sub-Saharan Africa and South Asia, respectively. The results show that trade openness has a significant positive impact on urbanisation in most regions, which is consistent with previous studies (Henderson & Turner, 2020). However, trade openness is found to have harmful effects on urbanisation in Latin America and the Caribbean and East Asia and the Pacific, where a 1% increase in trade openness causes urbanisation to decrease by 0.261% and 0.028% in Latin America and the Caribbean and East Asia and the Pacific, respectively.

The estimated results confirm that private investment can enhance urbanisation because the coefficients of this variable are significantly positive in all regions. The coefficient is 0.069% in Latin America and the Caribbean, 0.061% in East Asia and the Pacific, 0.047% in the Middle East and North Africa, 0.268% in Sub-Saharan Africa, 0.13% in South Asia and 0.008% in Europe and Central Asia. This evidence is supported by previous empirical results, such as Charney (2001) and Liu et al. (2018).

The estimated results also highlight the negative effect of household spending on urbanisation. Household spending is found to have reduced the impact of urbanisation in most regions, excluding East Asia and the Pacific. The finding is aligned with previous studies, such as Arouri et al. (2014) and Haryanto et al. (2021).

The impact of FDI on urbanisation is positive in two regions: Latin America and the Caribbean and Sub-Saharan Africa, where an FDI increase of 1% stimulates urbanisation to increase by 1.271% and 0.293% in Latin America and the Caribbean and Sub-Saharan Africa, respectively. This result is in line with previous work conducted by Shen and Lin (2017) and Dash et al. (2020). On the other hand, FDI delivers a harmful effect on urbanisation in Europe and Central Asia, where a 1% increase in FDI leads to a 0.042% decrease in urbanisation. The results indicate that FDI has s significantly positive impact on urbanisation in less developed countries, but this variable is not a driving force affecting urbanisation in developed countries.

In addition, the impact of government expenditure on urbanisation is positive in four regions, including Europe and Central Asia, East Asia and the Pacific, the Middle East and North Africa and South Africa. Specifically, a 1% increase in government spending stimulates urbanisation to increase by 1.117%, 2.456%, 1.136% and 1.604% in Europe and Central Asia, East Asia and the Pacific, the Middle East and North Africa and South Asia, respectively. The estimated results imply that the government expenditure variable has an enhancing effect on urbanisation in most countries when dividing the full sample into subsamples by region. The evidence is also supported by previous studies (Davis & Henderson, 2003; Fox, 2012; Yang et al., 2019). Government spending, however, may harm urbanisation in Sub-Saharan Africa because the coefficient of the variable is 0.738 at a 1% significance level. This result can be traced back to government spending that is not being used properly.

Finally, through the regression results, migration has an important role in supporting the urbanisation process. In detail, migration deliveries a positive effect on urbanisation in Latin America and the Caribbean, East Asia and the Pacific and the Middle East and North Africa where a 1% increase in migration leads to a 0.333%, 0.535% and 0.183% increase in urbanisation in Latin America and the Caribbean, East Asia and the Pacific and the Middle East and North Africa, respectively. This evidence highlights previous findings (Chen et al., 2011). The coefficients are not significant; thus, the real effect cannot be concluded in other regions.

Estimated Result for the Subsamples by Income Level

For assessing the impact of remittances on urbanisation based on income levels, the full sample is separated into three groups. The first group includes low-income countries (11 countries), the second has middle-income countries (52 countries) and the third group covers high-income countries (33 countries).

In the FEM estimation (Table 7), the empirical results indicate that there are differences among income groups. In detail, remittances have a significantly positive effect on urbanisation in low-income countries. A 1% increase in remittances could stimulate a 0.619% increase in urbanisation in low-income countries. High population growth rates create a high demand for new housing in low-income countries. Therefore, when receiving remittances, households in low-income countries tend to prioritise improving the quality of their housing, building new homes or even purchasing houses. Moreover, because agricultural land prices are typically low in low-income countries, remittances can enable households to purchase agricultural land and construct new homes. Although having positive signs, the coefficients are not statistically significant in middle- and high-income countries. In fact, remittances are often sent by migrant workers or temporary salaried workers living and working in developed countries to their families in their home countries (many of them come from low-income countries) (Chowdhury, 2016). These monetary flows are used to invest in housing and urban real estate, which would lead to increased urbanisation (Goodfellow, 2017; Hamouri, 2020). However, remittances have quite a small impact on urbanisation in middle- and high-income countries.

Regression Results for the Subsamples by Income, FEM Estimation.

Source. Authors own work.

Note. p-Value is in ( ).

Represent statistical significance levels of 1%, 5% and 10%, respectively.

The estimated results reveal that trade openness has a significantly positive effect on urbanisation in both low- and high-income countries, where a 1% increase in trade openness will lead to a 0.147% and 0.042% rise in urbanisation in low- and high-income countries, respectively. This evidence implies that international trade is good for the development of cities (Hamouri, 2020). Furthermore, private investment significantly affects only middle-income countries, and this effect is positive on urbanisation. In detail, a 1% increase in private investment leads to a 0.141% increase in urbanisation. This finding shows that the higher the number of domestic companies, the higher the level of urbanisation (Liu et al., 2018). Thus, through the obtained results, both trade openness and private investment have a positive impact on the urbanisation process.

Although household spending harms urbanisation, its coefficient significantly affects only middle-income countries. This evidence means that an increase in household spending could slow urbanisation. The situation represents a trade-off in the daily expenditures in households (Haryanto et al., 2021). In line with the evidence from previous studies regarding the role of FDI on urbanisation, the estimated results show that FDI has a positive effect on urbanisation but only significantly affects middle-income countries. This finding demonstrates that FDI plays a crucial role in the process of urbanisation (Dash et al., 2020; Shen & Lin, 2017).

Analysing subsamples by income level, the results confirm that government spending has a significantly positive effect on the process of urbanisation in the high-income group. Specifically, a 1% increase in government spending leads to a 0.205% increase in urbanisation. This finding suggests that public-sector expenditures play a critical role in the expansion of cities (Davis & Henderson, 2003; Fox, 2012; Yang et al., 2019).

The migration variable can support the development of urbanisation in middle-income countries. Specifically, a 1% increase in migration stimulates a 0.711% increase in urbanisation. A higher number of people entering the migration flows can lead to an increase in urbanisation in countries (Chen et al., 2011).

In the GLS estimation (see Table 8), the regression results confirm that remittances can harm urbanisation in high-income countries. A higher rate of remittances in GDP leads to a lower rate of urbanisation in high-income countries, where a 1% increase in remittances would result in a reduction in urbanisation by 3.070%. Although the coefficients of remittances are positive in low-income and middle-income groups, the results are not significant. Therefore, the effect of remittances on urbanisation in these groups cannot be clearly concluded. As urbanisation is quite slow in high-income countries, remittances are not the source of the development of cities. In high-income countries, population growth is very slow, so remittances do not significantly increase the new housing demand. Additionally, because the quality of housing is already high, the demand for housing expansion or repair is low. As a result, remittances are more likely to be used for consumption. When people in high-income countries receive financial flows from overseas, they may use them for savings, recreation or tourism and more. Thus, remittances do not have the effect of stimulating the housing market and may be reducing the urbanisation process (Barajas et al., 2009; Catrinescu et al., 2009; Chami et al., 2005).

Regression Results for Subsamples by Income, GLS Estimation.

Source. Authors own work.

Represent statistical significance levels of 1%, 5%, respectively.

Trade openness stimulates urbanisation when its coefficient is significantly positive in the case of low-income countries, but the effect is the opposite in middle- and high-income countries. These results align with previous studies, such as Hamouri (2020). The difference in the estimated results can be explained due to the priority of households, which is related to international trade. The standard of houses in poor countries is improved with trade but the priority in other groups is for other demands for living. This observation proves that urbanisation is relatively slow in developed countries.

Private investment has a significant positive effect on the urbanisation of middle- and high-income countries. A 1% increase in private investment leads to a 0.064% and 0.052% increase in urbanisation in middle- and high-income countries, respectively. Private investment has always been shown to have a positive effect on urbanisation when analysing the full sample or subsample by region or subsample by income level. This demonstrates the positive impact of private investment on urbanisation and our findings confirm and expand the previous results in some previous studies, for example, Charney (2001) and Liu et al. (2018).

Household expenditures reduce urbanisation in middle- and high-income countries. Therefore, increased household spending could slow down the development of urbanisation. Moreover, FDI is found to have positive impacts on urbanisation but this effect is only seen in high-income countries. This evidence highlights the crucial role of FDI in socioeconomic issues in recipient countries, for example, in urbanisation where a 1% increase in FDI leads to a 0.097% increase in urbanisation.

However, the effect of government expenditures received both positive and negative signs for urbanisation. In low-income countries, this variable reduces urbanisation, and the opposite result is seen in high-income countries. This finding indicates that government spending plays a vital role in countries’ urbanisation. Moreover, this result is supported by previous studies (Yang et al., 2019). Migration enhances the development of urbanisation in middle- and high-income countries. The estimated result shows that a higher number of migrating people contributes to an increased rate of urbanisation in countries. In the low-income group, the migration variable harms urbanisation.

Conclusion and Policy Implications

Urbanisation is rapidly occurring across the globe. In this inevitable phenomenon, developed countries have a high urbanisation rate and developing countries have robust processes. This paper focuses on the effect of remittances on urbanisation. Unlike related studies, this paper may be the first to employ a large international sample including 96 countries. For deeper analysis and comparison, the database is divided into three categories: the full sample, subsamples by region and subsamples by income. The empirical result unveils that remittances enhance urbanisation in the full sample. When examining the subsamples by region, the results show that remittances only support urbanisation in poor countries. Furthermore, in the subsamples by income, the estimated evidence finds that remittances harm urbanisation in the case of high-income countries.

In the future, remittances will remain a vital resource for developing countries, and these financial flows will increase under fast globalisation. The link between remittances and urbanisation is a critical research issue in the global development process. Therefore, our findings help improve the efficiency of remittances in supporting forward sustainable pathways for urbanisation. From the empirical results, some implications are provided for policymakers. First, governments should manage remittance flows more effectively by directing financial flows to invest in urban areas with well-considered planning. Governments in low-income countries should implement housing programs for low-income households that include access to preferential loans. Since remittances are often received in instalments, households should be encouraged to purchase homes through instalment plans for convenience. Governments’ supportive financial policies such as offering loans with favourable interest rates, are essential to help households enhance their housing quality. Second, urban development plans and national urbanisation strategies must be implemented with careful consideration. The landscapes of cities should follow medium-term and long-term strategies to build new urban areas. If homeland countries have high-quality cities, migrating people can be enticed to send more remittances to their hometowns. Third, cities that are designed with green, clean and beautiful platforms stretching into many areas should help urbanisation follow sustainable development. Finally, the study results are useful for policymakers to manage remittance flows in the most effective way to improve people’s quality of life and sustainable development in the future. For example, public programs that support entrepreneurship should be encouraged to help remittance-receiving households launch their own business ventures. Then remittances plays a critical role in new employment creation and boosting productivity.

Limitations and Future Research Suggestions

Despite the contributions of this paper to the theoretical framework and empirical findings, it still has some limitations. First, the econometric model does not include interaction variables to clarify the indirect effects of remittances on urbanisation. Second, the study focuses only on the linear effects, without exploring potential nonlinear relationships between remittances and urbanisation. Third, the paper does not consider variables related to institutional quality or the business environment quality (such as the corruption isue) in relation to urbanisation. Finally, remittances are currently measured only as a percentage of GDP, however, they should be represented using a more diverse set of metrics.

Therefore, future studies should incorporate interaction variables into the econometric model to unveil the indirect effects of remittances on urbanisation. In addition, independent variables could be transformed into squared terms to analyse nonlinear impacts or to identify possible threshold points. Besides, remittances should be added to other measurements (e.g. growth rate) instead of percentage of GDP and the migration variable should have more observations. Finally, socio-economic characteristics in recipient countries, such as institutional quality or corruption indices, should also be considered to enrich the findings.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analysed during the current study.