Abstract

This study examines the interplay between Islamic financial practices, money management skills, and digital financial literacy in shaping decisions to invest in both Sharia-compliant and non-Sharia-compliant stocks. Using data from 241 investors on the Pakistan Stock Exchange and the SmartPLS model, the results demonstrate that Islamic work ethics and religiosity positively impact decisions to invest in both Sharia-compliant and non-Sharia-compliant stocks, with money management skills playing a mediating role. Contrary to expectations, Islamic social finance does not directly influence decisions to invest in stocks, and digital financial literacy does not moderate the effect of Islamic practices on money management. However, the study highlights that integrating digital literacy with Islamic financial principles can enhance investment decisions. These findings provide actionable insights for investors and policymakers, advocating for tailored educational programs and digital tools to promote responsible, sustainable investments aligned with Islamic values.

Introduction

Deciding to invest in stock markets is a challenging task for investors due to well-known reasons: stock market volatility (Ahmad & Wu, 2022), stock market crash (Ajzen, 1991), exchange rate (Breedon & Vitale, 2010), and future loss. Therefore, investors evaluate information comprehensively before entering and investing in stock markets (Thakkar & Chaudhari, 2021). Literature has explored that there is a high heterogeneity among the characteristics of investors, for instance, based on personality traits (Baker et al., 2021; Sachdeva & Lehal, 2023), behavioral factors (Ahmad & Wu, 2022), demographic factors (Korniotis & Kumar, 2011; Saivasan & Lokhande, 2022), etc. Moreover, it has also been extensively studied that environmental factors (Brown-Liburd et al., 2018; Maqbool & Zamir, 2021), regulations (Fochmann et al., 2017), stock market trends (Lean et al., 2007), and company reputations, etc., affect investors’ decisions. The preference of Muslims for non-inforest-bearing instruments amplifies the importance of the aforementioned factors. Therefore, it generally influences stock market investment decisions—preferably shariah-compliant stocks. However, this preference is often rooted in a broader aversion to riba (interest), making equity investment preferable over fixed-income securities regardless of formal Shariah classification (Setiawan, 2023). Therefore, the Shariah-compliant stocks may be common in religious societies, yet Muslim investors are not categorically averse to conventional stocks. Such individuals selectively invest in equities that operate ethically, and avoid prohibited sectors—thus adhering to Islamic financial norms while expanding their investment options (Rahman, 2015). Hence, in this study, by investment in stock, we mean both Sharia and conventional. Additionally, as compared to non-Muslim countries, people living in Islamic countries have different attitudes when it comes to investment decision-making (Md Husin et al., 2023). Most likely, people living in Muslim countries have strong beliefs and faith in Islam in every matter. A few studies have been carried out on the role of Islamic practices in investment decisions. For instance, Chircop et al. (2020), Shahid et al. (2022) scrutinize the role of religiosity in capital investment decisions. Moreover, recent studies have shown different aspects of how Islamic financial practices are applied in banking and financial decisions. For example, one study examines the dividend policy behavior of Islamic and conventional banks, showing that Islamic banks use dividend policies as a substitute mechanism to alleviate agency problems due to the unique regulatory and Sharia law environment they operate (Athari et al., 2016). Another researcher highlights how external governance mechanisms like political stability and the rule of law positively impact the profitability of Islamic banks (Athari & Bahreini, 2023). Additionally, the influence of environmental characteristics such as country-level governance and risk on the capital holdings of Islamic banks has been explored, indicating that higher governance quality leads to higher capital ratios in Islamic banks (Athari, 2022).

Furthermore, researchers have focused on financial literacy in the literature on behavioral finance and investment decisions (Jain et al., 2022). A study conducted during the Lebanese crisis period from 2019 to 2021 highlighted that financial literacy, financial self-control, and demographic determinants significantly impact individual financial performance and behavior, enhancing financial outcomes across various generations, genders, and socio-economic statuses (Mawad et al., 2022). This underscores the foundational role of financial literacy in shaping financial behaviors, which is critical to understanding its interaction with digital financial literacy in your study. However, the emergent term “digital financial literacy” has been relatively untouched in the investment literature. Moreover, no study has yet examined the interaction between digital financial literacy and Islamic practices for money management skills and investment decision-making. In the current digital era, people use digital media and sources to get and share information about their activities (Meyers et al., 2013). The findings from the Lebanese context suggest that enhancing digital financial literacy could similarly influence financial behaviors, potentially aligning with Islamic financial principles to promote better investment decisions.

On the whole, while the general influence of religiosity and ethics on investment behaviors is well documented, the literature distinctly lacks an exploration of how Islamic financial practices—such as Islamic work ethics, religiosity, and Islamic social finance with interact with digital financial literacy to affect investment decisions. This gap is significant because digital platforms increasingly permeate financial markets, potentially altering how traditional Islamic values are applied in modern financial decisions. The critical question of how these values interface with digital financial literacy to influence ethical investment practices remains underexplored and underscores an urgent need for research, particularly given the growing importance of both Islamic finance and digital platforms in global markets.

This study aims to systematically explore how digital financial literacy influences the application of Islamic financial practices in investment decisions. We specifically examine whether the presence of digital financial literacy enhances the adherence to and effectiveness of Islamic financial ethics in investment processes. This research seeks to contribute to the existing body of knowledge by providing empirical evidence on the synergistic effects of digital literacy and Islamic financial practices, thus guiding investors on integrating ethical considerations with digital tools for better decision-making outcomes.

The novelty of this study lies in its focused examination of the intersection between digital financial literacy and Islamic financial practices, a vital yet understudied area in financial research. Our findings are expected to offer substantial policy implications by demonstrating the potential of digital literacy to enhance the ethical application of Islamic financial principles in investment strategies. Such insights could guide policymakers and financial institutions in developing targeted educational programs and digital tools that promote ethical investment behaviors, thereby aligning financial strategies with Islamic ethical standards more effectively. This approach not only enhances investor education but also supports the broader objective of sustainable and responsible investing by Islamic principles.

This research makes two major contributions to the body of knowledge in the field of stock markets. First, this research enriches the existing literature by employing the intervening role of money management skills and digital financial literacy between Islamic practices and investment decisions. The intersections of these paths have been neglected in the existing literature. Hence, our research fills this gap with empirical data from an emerging Muslim country to explore how Islamic practices interact with money management and investment decisions under digital financial literacy. Second, this research advances our understanding of the theory of planned behavior (Ajzen, 1991). The theory demonstrates that attitudes, subjective norms, and perceived behavioral control influence individuals’ intentions and behaviors. This theory has been widely tested in investment literature through the lens of behavioral factors (Ajzen, 2002), environmental factors (Judge et al., 2019), and demographic factors (Warsame & Ireri, 2016). However, we traverse it with Islamic practices and digital financial literacy to understand the investment behaviors of investors. The insights of this research facilitate experienced and potential investors and financial institutions in recognizing the most influential factors in money management skills and investment decision-making. Taking advantage of this study, investors can emphasize the most important parameters for managing their money for future investments.

This research is further organized as follows: The second part is about the literature review, and the third part illustrates the methodology. In the fourth section, we have discussed data analysis and results, while the fifth part sheds light on the discussion and conclusion.

Theoretical Background and Hypotheses

Grounded on the theory of planned behaviors (Ajzen, 1991), researchers have emphasized the role of human behavior in shaping activities (Ahmad & Wu, 2022; Farid et al., 2019). Out of many factors, religion has a significant direct effect on individuals’ social interaction, behavior, and social relations (Abuznaid, 2006). Numerous studies have inferred religion as the key determinant of human investment and saving decisions. Although a large body of researchers has emphasized the direct relationship between religious beliefs and human behavior, recent studies suggest that this relationship is far more complex than it is perceived. For instance, a recent study (Kamaruddin et al., 2021) found that the relationship between financial management and accountability is not direct, rather, it goes through financial governance. Similar mediating and moderating elements are reported in numerous studies (Chetioui et al., 2023; Qasim et al., 2022). So, based on the empirical evidence, the current study aims to identify the role of money management and financial digital efficacy in the aforementioned framework. According to the Credit Counseling Society of British Columbia, money management skills are the ability of an individual to save and budget money, along with managing credit. Therefore, those with better management skills will have better control over their spending and budgeting behavior. Meanwhile, Kahneman and Tversky (1979) argue that religion has a significant role in the cognitive structure of an individual, such that pro-religious individuals are more conservative and, henceforth, are more concerned with their economic goals. One popular theory to explain this phenomenon is the prospect theory of Kahneman and Tversky (1979), which suggests that an investor makes multiple decisions and exhibits different risk aversion levels over time depending on various targeted outcomes. There are numerous religious factors determined within the literature body that affect the investment decision of an individual, however, the current study emphasizes how Islamic practices affect the decision-making of an individual and further determines how money management skills and financial digital literacy influence investment intentions. Religiosity, Islamic social ethics, and Islamic social financial activities are the constructs of the current study.

The term investment decision refers to the investor’s intention to invest in either Sharia-compliant or conventional stock markets for future financial benefits (Aren & Hamamci, 2020). So, investors’ decisions implicate their choice of when, where, and how to invest a specific amount of funds to generate income (Sindhu & Kumar, 2014). Although classical economic theorists assume that investment decisions are based on available information, in theory and practice, such investment decisions are manipulated in different circumstances (Byrne et al., 2010; Njuguna et al., 2016). The investment decision can become subjective and can be influenced by numerous factors, including sociological and psychological factors. So, empirically, it is evident that the decisions of investors can be affected by numerous factors, including religion.

Islamic Work Ethics and Financial Decision Making

Ethics has long been investigated by researchers and moral philosophers to understand the nature of human behavior and analyze how and why an individual behaves in a particular pattern (Farid et al., 2019). Generally, ethics is defined as the set of principles and guidelines that govern one’s right conduct. Arslan (2009) termed ethics a theory or a system of moral values. From an Islamic perspective, Islam presents a comprehensive system of living that is based on strong ethical principles that enlighten individuals with guidelines regarding all spheres of life (Rice, 1999). The societal values of Muslim society oblige people to work not just for materialistic targets or pleasures, rather, they also advocate working responsibly and executing accountability (Possumah et al., 2013).

In the context of stock market investment, Islamic ethical teachings prescribe the avoiding investment in instruments that are based on Riba (interest) or Gharar (excessive uncertainty such as gambling), making stock markets a more favorable option. Whereas in Muslim countries, the investors gravitate toward halal investment options, particularly in equity markets, which provides investors ownership without interest-based earnings (Soemitra, 2016). Although in most of the Muslim countries the investors have the opportunity to invest in both sharia and conventional stocks, several studies find that the religion-oriented investors prefer both sharia and conventional stocks investments over interest-based income. Umar (2017) suggests that the limitations of investment only in Sharia-compliant stocks result in Welfare loss, whereas welfare stands as the most important component of Islamic work ethics (Ardalan et al., 2014; Zafar & Abu-Hussin, 2025). Similarly, Parvin et al. (2025) find that individuals with higher religious attributes are positively linked to higher stock market participation (both Sharia and conventional).

The limited evidence suggests that while individuals with higher Islamic values naturally prefer Sharia-compliant stocks, they might also engage in conventional equities—unless they don’t violate core Islamic principles. Justice Muhammad Taqi Usmani, in this regard, terms investment in the stock market halal unless the company itself is involved in any prohibited activity (Norchaevna, 2024). Similarly, Osmani and Abdullah (2009) argue that selling common stock is just like selling a portion of a company in the shape of a share, and it is considered the property of the individual who purchases it. Thus, such individuals who are high on Islamic work ethics are more likely to invest in both Sharia and conventional stocks to meet their financial goals and faith-based obligations. So, we hypothesize that:

Religiosity and Investment Decision-Making

A plethora of research has determined religiosity as a fundamental element that influences the investment decisions of individuals (Hess, 2012; Saputra et al., 2020). Individuals’ religious beliefs and practices at large affect their social, ethical, economic, demographic, and financial behavior. In contrast, this degree of religious beliefs and practices is perceived as an individual’s religiosity. According to Iddagoda and Opatha (2017), religiosity is defined as the extent to which any individual believes, follows, and glorifies his relevant religion and its creator and further practices religious teachings in his or her daily activities. However, it is pertinent to note that religiosity influences human behavior in numerous dimensions. Therefore, highly religious individuals view the world through their religious schemas and further integrate their religious practices into their lives (Jamaluddin, 2013).

Various academic disciplines are examining religiosity to determine its impact on the habits, values, attitudes, and behaviors of humans. For instance, Sholihin et al. (2022) investigated the relationship between religiosity with life satisfaction and found that both significantly related to each other. In a similar study, Aziz et al. (2022) found a positive relationship between religiosity and individuals as well as a firm’s performance. Hence, empirically, the role of religiosity in shaping human behavior is validated. Moreover, its role in investment decision-making is also inferred by several scholars. For instance, Tahir and Brimble (2011) investigated the impact of Islamic investment principles on Muslim investors’ decision-making and found a significant positive relationship between both constructs. Their findings suggested that religiosity among all factors had more influence on investors’ decision-making comparatively. Haron et al. (2008) also concluded that Islamic teachings do influence the savings behavior of investors. Perhaps, in the field of Islamic finance, rich evidence prevails to bridge religiosity with investment decisions (Lestari et al., 2021). For instance, Duqi and Al-Tamimi (2019) investigated the relationship between religiosity and investment decision-making in a Malaysian market. The findings of their study indicated a significant positive relationship between religiosity and the investment decision-making process. They argued that individuals who had higher levels of religiosity preferred investment in Sharia investment schemes over conventional schemes.

However, emerging evidence shows that it doesn’t necessarily preclude the opportunity of investment in conventional stocks (Tahiri Jouti, 2019). In this regard suggests that the religious beliefs of Muslims are rooted in the values of ethics, equality, and fairness. They suggest that unless the company is not directly involved in banned contracts, such as interest, alcohol, drugs, pornography, etc., the religious individuals perceive investment as acceptable (Goel et al., 2020). In this regard suggests that religiosity influences the ethical attitude of individuals. Therefore, it supports individuals to invest in those conventional stocks that encompass ethical investments, CSR, and social wellbeing. Religious beliefs are so influential that they affect individuals’ attitudes, risk perceptions, and individuals’ traits, which in turn affect their economic choices and outcomes (Kumar et al., 2011). A recent study by Hong et al. (2023) found that religiosity significantly influences the FDI of a country. So, the empirical evidence is strong enough to suggest that religiosity and the financial investment decision-making process are significantly related to each other. Therefore, we hypothesize that:

Islamic Social Finance and Investment Decision

Basically, Islamic social finance advocates finance for social good. Right at the birth of Islam, Islamic finance was designed to create an equilibrium of wealth among people to stop economic exploitation. Islamic finance emphasizes socially profitable activities that empower humanity and are based on norms that discourage investment in immoral businesses (Shirazi et al., 2021). Moreover, Islamic finance supports philanthropic activities in different forms. For instance, in Islam, Zakat is an obligation that is to be paid from the income, whereas other philanthropic activities such as Waqf and Sadaqah are voluntary giving by an individual, however, such activities should be from halal income. As discussed earlier, interest (riba) in any form is prohibited in Islam, therefore, this norm is absolute and unshakable (Hassan et al., 2019). This key norm allows individuals to invest in products and services that are part of the real economy, having a profit and loss sharing partnership structure, wealth redistribution concept, and risk-sharing tendency. So, such obligations make stock market investment a preferable opportunity.

Given the circumstances, the world has acknowledged the concerns of Muslims and hence focused on creating Islamic Sharia-approved investment products that are free of interest. For instance, in Malaysia, an Islamic capital market is introduced, where only those shares traded are by Islamic principles. Such Islamic indexes are also introduced in developed countries such as the United States (Razali et al., 2022). So, it is rational to argue that investment in the stock market is preferred over interest-based income by those who are more prone to Islamic values. The findings of Kasi and Muhammad (2016) validate this argument, as they found a positive relationship between the Islamic beliefs of an individual and their stock market investment decisions. Moreover, individual investors who are actively involved in the stock market also believe in social responsibility and ethical investments. They aim for returns not just in the form of profit, but also seek to contribute to environmental and social outcomes through their investment choices (Raut et al., 2021). So, it is rational to believe that those who believe in Islamic social finance will consider investing in companies that engage in ethical investments, including both Sharia and conventional stocks.

Although there is a lack of direct evidence to suggest that Islamic social finance and stock market investment decisions are significantly related to each other, based on the findings of other relevant studies, we believe that individuals who believe in Islamic social finance will be more prone toward investment in stocks instead of Riba derived income based on the fact that many companies prefer social activities as they lead toward sustainable growth (Aziz et al., 2022). In fact, in most Muslim countries, the companies paying zakat (a form of social finance) have better firm performance (Al-Malkawi & Javaid, 2018), henceforth, investors with a high inclination toward Islamic social finance will prefer buying stocks of companies that indulge in CSR activities, encompass ethical business practices, and contribute to societal wellbeing (Mertzanis et al., 2023; Tahiri Jouti, 2019) So, based on these arguments, we hypothesize that:

The Mediating Role of Money Management Skills

Although preliminary evidence suggests that Islamic practices influence the decision-making of an individual, there are several arguments to suggest that the relationship is not direct. Islam, being the code of life, not only suggests halal investment, rather, it advocates for wealth management in several ways. In contrast, wealth management is a methodological process that encompasses long-term strategies that involve future planning (Mahadi et al., 2019). By definition, wealth management is a process that involves steps that guide an individual in the proper management of finances in order to meet end goals (Lahsasna, 2017). As per the verse of Surah At-Takatsur (verse 8), everyone shall be questioned about their wealth on the day of judgment. Therefore, in the Muslim community, it is believed that one will be held accountable for earnings and spending on the day of judgment. In this regard, Amanda et al. (2018) concluded that all Muslims, regardless of their financial status, are required to manage their wealth as they are liable for both their assets and liabilities on the day of judgment. Other than the Holy Quran, it is proven from hadiths that wealth management is an obligation for those who believe in Islam. For instance, the hadith No. 2417 of Al-Tirmizi states that all Muslims are liable for their wealth, i.e., how it was obtained, how it was spent, and where it was spent. The current study stresses this argument that Islamic practices (religiosity, Islamic work ethics, and Islamic social finance) will affect one’s money management skills, which in turn will affect one’s investment decisions. Money management skills define one’s ability to spend his or her money wisely (Juen et al., 2013). Although we earlier suggested that religiosity is one of the key determinants of human decision-making processes (Lestari et al., 2021), there are several studies that show the influence of religiosity on various other aspects of life, such as emotions, attitudes, and skills. For instance, Sarofim et al. (2022) termed religiosities a key influencer of an individual’s emotional well-being (Sholihin et al., 2022). Their investigation determined the positive role of religiosity in life satisfaction. In the context of the current study, there are several studies that nurture our argument that religiosity affects the money management skills of an individual, which in turn affects the investment decision-making process.

Basically, skills are defined as the ability of a person to do something well. In literature, several theories have emphasized the importance of skills as they are essential for one to apply them in their daily life (Fazal et al., 2021). Whereas the theory of planned behavior by Ajzen (2002) suggests that an individual’s actions are derived from their skills, on the other hand, skills are derived from one’s knowledge and practices. As religiosity explicates one’s degree of beliefs and practices, it is arguable that religiosity will affect one’s money management skills. Although there is no direct evidence to support this argument, the relationship between religiosity and skill development is empirically proven. For instance, Wang et al. (2021) found religiosity as a determinant of the political skill of Muslim employees in Turkey. Similarly, Kirby (2008) suggested that religious schemas significantly influence the critical thinking skills of an individual. Religiosity and study skills are significantly correlated with each other (Chowdhury & Nizam, 2018). So, it is rational to argue that religious beliefs related to earning and spending will affect individuals’ money management skills, which in turn will affect one’s financial behavior (Dewi et al., 2020).

Like religiosity, the current study contends that Islamic work ethics can also influence one’s money management skills based on several arguments. As discussed earlier, ethics presents a system of moral values (Arslan, 2009) that guides one about different spheres of life. In the Islamic context, ethics suggests that one act responsibly so that their actions are not against Islamic principles. With technological advancement, individuals have more platforms to spend their money, which results in heavy debt and impulsive purchasing behavior (Juen et al., 2013). However, Islamic literature highlights the key elements of wealth management categorically. First, it suggests that the wealth must be utilized as a blessing from God and shall not create any greed. Second, it should be spent responsibly, that is, on the needs of the family. Third, social obligations such as tax, zakat, and charity must be addressed (Amanda et al., 2018). Therefore, people with high ethics will have more responsible spending behavior and must possess better money management skills in order to comply with Islamic teachings. Such people will spend money as per their needs and save the rest to meet their obligations and future needs. Hence, Islamic work ethics will affect their money management skills, which in turn will affect their investment decision behavior.

Speaking of Islamic social finance, its constructive role in society is acknowledged globally (Shirazi et al., 2021). Islamic social finance is governed by three basic principles, that is, governing property, wealth creation, and philanthropic distribution. Basically, Islamic social finance encourages socially profitable businesses, which empower humanity based on norms that preclude investment in prohibited and immoral businesses. As discussed earlier, Islamic finance prohibits one from investing in Riba in any form (Alam et al., 2017). Furthermore, the concept of Islamic social finance largely emphasizes charitable activities that benefit society, however, it is fundamental for one to have better money management skills to earn, spend, and save money. So, given the Islamic principles, individuals who are more concerned about Islamic social finance will have better money management skills in order to earn enough halal profit to save for future investment and charitable activities such as zakat, sadqa, etc.

Although the empirical evidence is limited, it provides deep insight. The money management skills play a fundamental role in transforming religiosity, Islamic work ethics, and Islamic social finance into successful investment in stocks that are Sharia-compliant or ethically aligned conventional equities while discouraging interest based options. With the aid of money management skills, the investors are capable of improving their planning, risk management, and value-based screening—bridging their spiritual convictions with sound investment opportunities (Al-Abbadi & Abdullah, 2017). Based on the above discussions, we draw the following hypotheses:

The Moderating Role of Digital Financial Literacy

Although Islamic practices motivate one for money management and halal investment, due to the modernization of the digital industry, people are prone to a variety of sophisticated financial products. The empirical evidence suggests that this era of digitalization has significantly affected the saving and spending behavior of individuals, resulting in high consumption. Moreover, advertisements in mass media and social media have changed the lifestyle of individuals these days. The modernization of digital technology has not only affected the retail trade sector, but it has also revolutionized the financial services sector, providing various platforms of services for mortgage, lending, payment, and investment. As per the report from the Global Findex database (2017), over 20% of adults have personal mobile money accounts, while 52% of adults globally have received or sent digital payments. Giant economies such as China report that 57% of their payments are made through mobile phones due to ease of access and simplification of transactions. However, such developments have resulted in higher spending. For instance, the study by Agarwal et al. (2019) revealed that the digital payment system is one of the major causes of overspending within India. It is due to a lack of personal financial education and self-control that causes higher spending (Amanda et al., 2018). In the context of personal finance, financial literacy can play a pivotal role in counterbalancing such behavior by means of money management. There are several studies that justify the nexus between financial literacy and wise spending, however, the current study analyzes the role of digital financial literacy in this context.

In simple terms, digital financial literacy explicates one’s knowledge regarding online systems of savings and spending. Tony and Desai (2020) argue that digital financial literacy is a combination of financial literacy and digital platforms. Thus, by definition, digital financial literacy is the financial literacy of digital financial technology. The previous studies have investigated the role of financial literacy thoroughly (Jamal et al., 2015; Varcoe et al., 2005), yet rare researchers have investigated the role of digital financial literacy, such as Tony and Desai (2020), who analyzed the construct of digital financial literacy and its role in saving and spending behavior. Although financial literacy and digital financial literacy are two different constructs, digital financial literacy is believed to be a standardized mode of financial literacy (Prasad et al., 2018). Thus, the effect of digital financial literacy should be the same as that of standard financial literacy. Due to its importance, digital financial literacy has become a key factor in recent years. In this regard, Tony and Desai (2020) argued that digitalization in finance has a significant impact on financial inclusion, savings and spending platforms.

This study aims to analyze the moderating role of digital financial literacy between Islamic practices and money management skills. There are several reasons to suggest that digital financial literacy will further strengthen the relationship between Islamic practices and money management skills. As discussed earlier, there are several studies that argue that religious practices encourage people to practice wise money management (Amanda et al., 2018). Money management skills, on the other hand, are derived from knowledge and practices. Hence, we believe that the relationship between Islamic practices (religiosity, Islamic ethics, and Islamic social finance) will be stronger if the individual has better digital financial literacy.

There are several studies that have found the direct effect of digital financial literacy or financial literacy on saving and spending behavior. For instance, Sabri and MacDonald (2010) in their study found a positive nexus between financial literacy and saving behaviors in the Malaysian economy. Similar findings were reported by Zulaihati et al. (2020) when the relationship was evaluated in Indonesia. Jamal et al. (2015) investigated the effect of financial literacy on the saving behavior of university and college students. The findings suggested that higher financial literacy leads to higher savings. Saputra et al. (2020) assessed the impact of digital financial literacy on saving and spending intentions and behaviors. The results indicated that digital financial literacy is a significant predictor of saving and spending behavior. So, it is evident that financial literacy has a strong tendency to influence one’s intentions, behaviors, and decisions. However, we argue that digital financial literacy can moderate the relationship between Islamic practices and money management skills.

The reason for evaluating the moderating role of digital financial literacy is the nature of financial literacy. Several studies in the past and recent years have explored financial literacy as a moderating variable in different contexts. Noctor et al. (1992) argued that financial literacy enables individuals to make informed judgments, which leads to effective decisions and better money management. In this context, Sadiq and Khan (2019) tested the moderating role of financial literacy between risk behavior and investment intentions. However, the findings showed an insignificant relationship. Based on this, they suggested assessing the moderating role of financial literacy in different models. So, we believe that, although financial literacy did not affect the relationship between risk behavior and investment intentions, it can affect the relationship between social practices and money management skills because, in this regard, D. Khan (2020) determined financial literacy as a significant moderator between cognitive biases and decision-making. Empirically, the relationship between Islamic practices and money management skills is evident, however, individuals with better digital financial literacy have better information and knowledge, which enhances their capability to explore better platforms of investments and empowers their money management skills. Thus, the current study assumes that higher digital financial literacy strengthens the relationship between Islamic practices and money management skills. So, we hypothesize that:

Figure 1 displays the research model.

Theoretical framework.

Methodology

Data and Sample

This research scrutinizes the decisions to invest in stocks of investors in an emerging Muslim country, Pakistan, through empirical data. This research followed a deductive approach to test an existing theory of planned behavior. We focused on investors who invest money in stock markets (short-term and long-term). The Pakistan Stock Exchange (PSE) and the State Bank of Pakistan (SBP) helped us find investors for the survey. Moreover, we also identified several investors through social media groups (LinkedIn, Facebook, Twitter, etc.). The questionnaire was written in English because it is easily understandable by Pakistani investors. Two sections have been given in the survey. In the first section, we asked questions about the demographic information of the respondents, such as age, gender, education, and experience in the stock market, etc. In the second section, we asked the main questions about the variables with the given options. A cover letter was included on the first page of the survey to clarify that the collected data would be used solely for research purposes and that participants’ personal information would not be disclosed to the public. Before data collection, participants were informed about the study, and verbal consent was obtained for completing the questionnaire. They were also informed that their participation was voluntary. We contacted 540 investors via social media (online), emails, and phone calls and also took the help of employees working in PSE and SBP through a hard copy approach. Since it was not easy to get the exact number of investors, we followed the convenience sampling method, a non-probability sampling approach. After one or two reminders, we gathered 280 responses over two months. However, after screening, we retained only 241 responses, and the rest were dropped due to missing values and incorrect attempts. The final response rate was 45%.

Measurement

We used 5-point Likert scales, representing strongly disagree = 1, to strongly agree = 5. The items are given in the Appendix.

Islamic Practices: We employed three Islamic practices in this research, namely Islamic work ethic, religiosity, and Islamic social finance. These items were adopted from a previous study conducted by Aziz et al. (2022) in the same market. For the Islamic work ethic, we used 14 items, of which a sample item is “Laziness is a vice.” For religiosity, there were 14 items, of which a sample question is “My faith involves all of my life.” These items were adopted from a previous study by Gorsuch and McPherson (1989). For Islamic social finance, we used 07 items of Obaidullah and Shirazi, (2017), and the sample question is “I pay zakat every year if I meet the prescribed criteria.”

Money Management Skills: It illustrates the ability of investors to manage their financial resources effectively or efficiently. We used four items that were taken from a previous study (Ksendzova et al., 2017). A sample item is “Follow a weekly or monthly budget.”

Digital Financial Literacy: it demonstrates knowledge and understanding of investors about using digital sources, especially social media, while making transactions. We adopted 11 items from a previous study by Rahayu et al. (2022), of which a sample item is “Have a good understanding of digital payment products, such as E-Debit, E-Credit, E-Money, mobile/internet banking, and E-Wallet.”

Investment Decision: It tells about the decisions to invest in stocks of investors in different stocks (short-term and long-term). To measure decisions to invest in stocks, we used seven items that were validated by several studies (H. H. Khan et al., 2017). A sample item is “With the given decisions to invest in stocks, I would prefer to invest in the stock market rather than the fixed income security”.

Control Variables

We have controlled the demographic factors of the respondents, such as age, education, income level, employment structure, type of investment, and year of investment, to attenuate the chances of spurious results in our model. These demographics to be controlled are suggested by several authors (Lu et al., 2023). Based on our results, we found that the factors of income level, education, and employment structure play a significant role in the decisions to invest in stocks.

Table 1 illustrates all the respondents’ ages, incomes, experience, and investments in stock markets. Most of the respondents are male, as in Pakistan, men act as responsible persons of society. Most of the respondents are self-employed and highly experienced, and are engaged in different kinds of stock market investments.

Demographics Characteristics of the Participants.

Data Analysis and Results

Descriptive Statistics

Table 2 illustrates the descriptive statistics and multicollinearity issues. The variance inflation factor (VIF) scores of all the endogenous constructs are below 3, the threshold level. The descriptive statistics show that investment decisions have the highest mean score of 3.67, while digital financial literacy has the lowest mean score of 3.45. Similarly, money management skills have the highest standard deviation value of 0.57040, while investment decisions have the lowest standard deviation value of 0.39150. Furthermore, skewness and kurtosis analyses were performed to gauge the normality of the data. The skewness and kurtosis values fall in the desirable range of ±2, as suggested by Bao (2013).

Descriptive Statistics.

Common Method Bias

In this study, the data were obtained from a single source, and it is cross-sectional, due to which the issue of “common method bias (CMB) or common method variance (CMV)” may arise (Jordan & Troth, 2020). According to MacKenzie and Podsakoff (2012), CMB issues can be detected by executing “Harman’s Single Factor Test.” To follow’s MacKenzie and Podsakoff (2012) method, we performed “Harman’s Single Factor Test” in SPSS 25 to gauge the CMB problem. The “Harman’s Single Factor Test” result indicates the absence of a CMB issue because the percentage variance is lower than the cutoff point (i.e., below 50%).

Confirmatory Factor Analysis (CFA)

First, we applied the PLS-SEM algorithm technique in SmartPLS to analyze the measurement model to scrutinize the loading weights of all the constructs, composite reliability, and validity. The results of the PLS-SEM algorithm (see Table 3) indicate that the reliability scores of both measures, such as Cronbach’s alpha and composite reliability, are above the threshold level (i.e., above .70) as suggested by Hu and Bentler (1999).

Factor Loading, Validity and Reliability.

Furthermore, the average variance extracted (AVE) and the square root of the average variance extracted were established to gauge the convergent and discriminant validity of all the constructs. The AVE scores and √ (see Table 3) of all the constructs are greater than the desirable range (above from AVE > 0.50 and

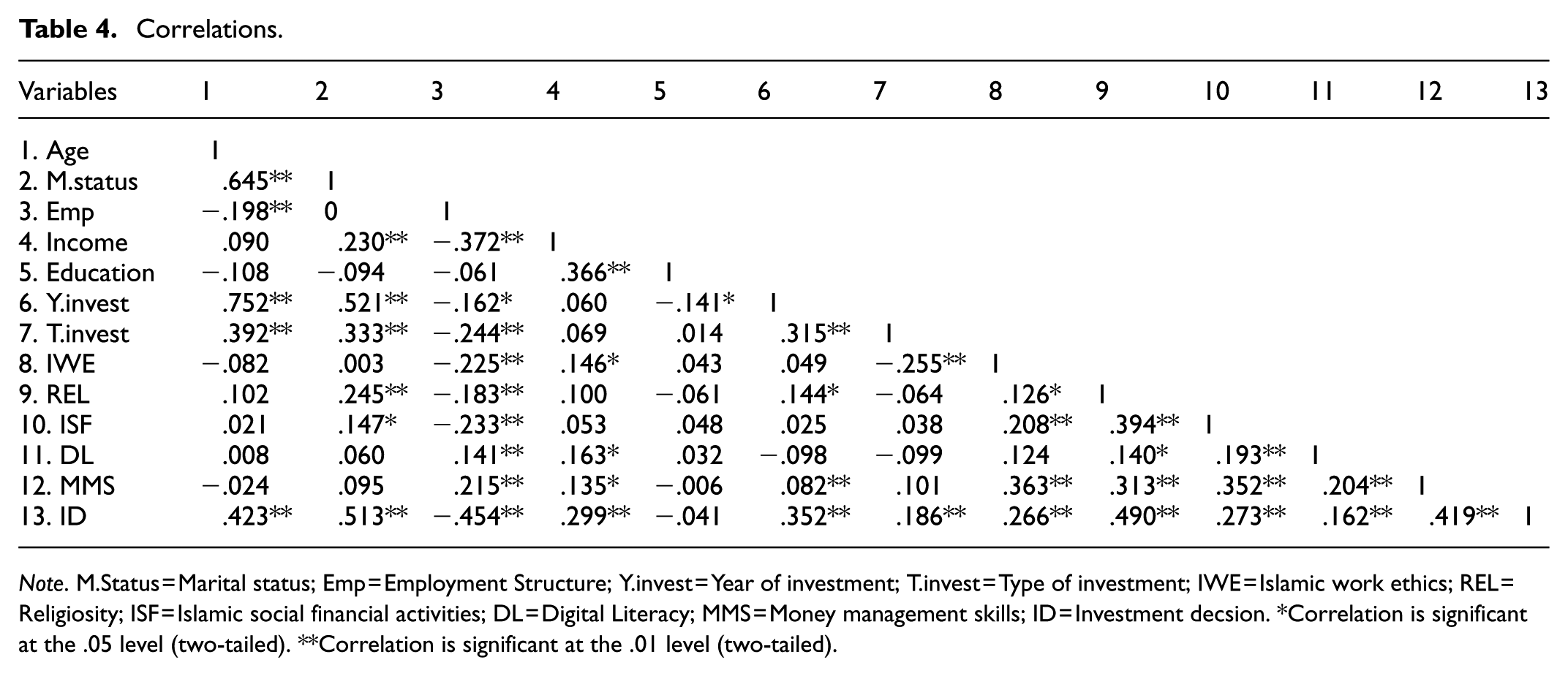

Correlations

The coefficient of correlation among the constructs is given in Table 4. The coefficient values indicate that Islamic work ethics (r = .266), religiosity (r = .490), and Islamic social finance (r = .273) are significantly positively related to investment decisions. Similarly, Islamic work ethics (r = .363), religiosity (r = .313), Islamic social finance (r = .352), and digital financial literacy (r = .204) are significantly positively associated with money management skills. Furthermore, money management skills (r = .419) and digital financial literacy (r = .162) are also significantly related to investment decisions.

Correlations.

Note. M.Status = Marital status; Emp = Employment Structure; Y.invest = Year of investment; T.invest = Type of investment; IWE = Islamic work ethics; REL = Religiosity; ISF = Islamic social financial activities; DL = Digital Literacy; MMS = Money management skills; ID = Investment decsion. *Correlation is significant at the .05 level (two-tailed). **Correlation is significant at the .01 level (two-tailed).

The score of R2 (see Table 5) indicates that there is a 28.1% variation in money management skills and 58.5% variation in the investment decision explained by Islamic work ethics, religiosity, and Islamic social finance in the presence of age, education, income, marital status, employment structure, year of investment, and type of investment. The score of f2 (see Table 6) demonstrates that all the constructs display smaller to medium effects in money management skills and investment decisions (f2 = 0.10 -smaller effect, f2 = 0.25- medium effect).

R Square.

F Square.

Structural Model

This study aims to assess the mediating role of money management skills between Islamic practices (Islamic work ethics, religiosity, and Islamic social finance) and the investment decision nexus. Furthermore, this study also scrutinizes the moderating role of digital financial literacy on the relationship between Islamic practices (Islamic work ethics, religiosity, and Islamic social finance) and money management.

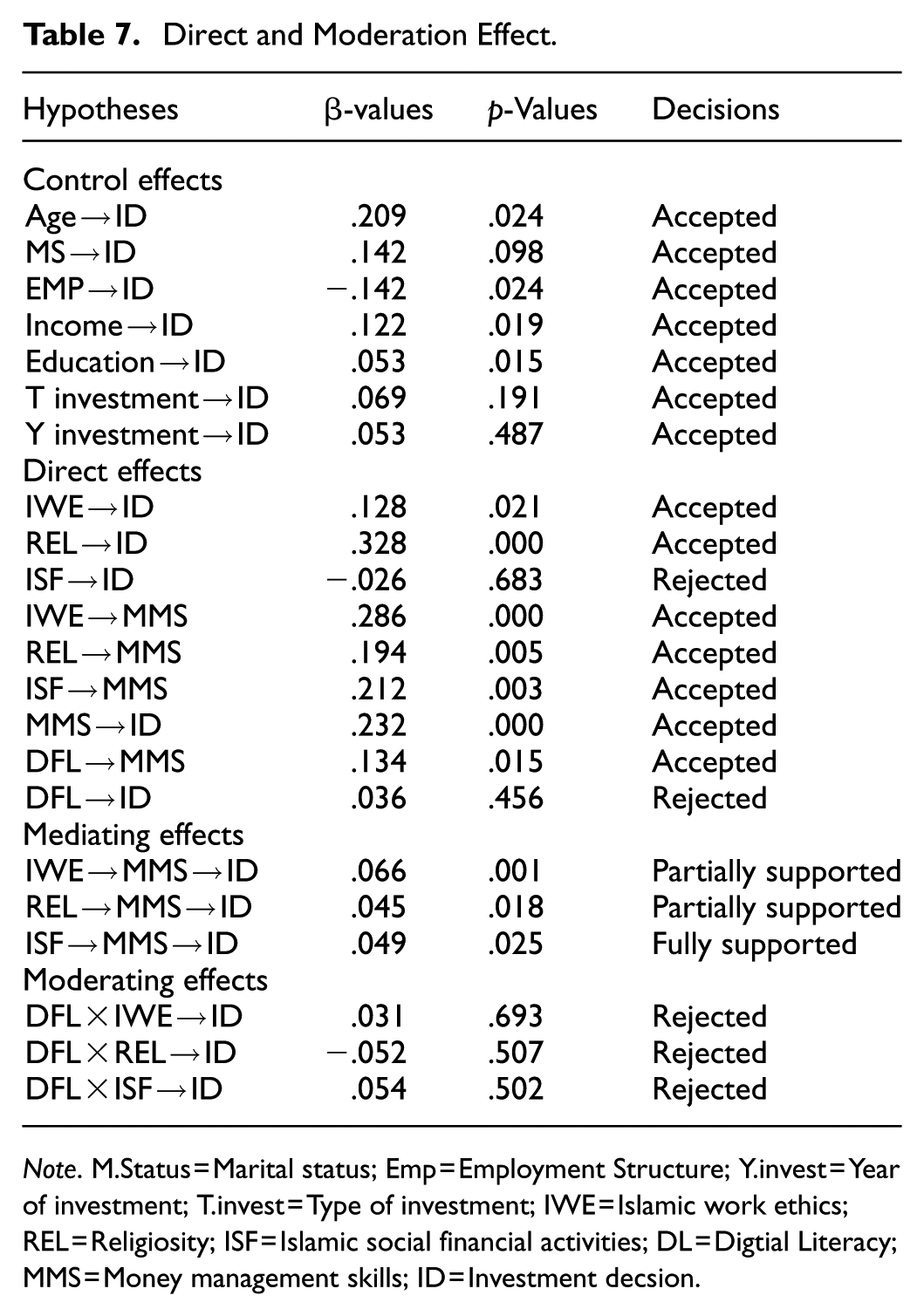

We used the structural model to examine the mediating and moderating effects (see Figure 2). First, the results (see Table 7) indicate that Islamic work ethics (β = .128, p < .05) and religiosity (β = .328, p < .05) have significant effects on the investment decision, while Islamic social finance (β = −0.026, p > .05) has no significant effect on the investment decision. These results favor H1 and H2 and reject H3. Second, Islamic work ethics (β = .286, p < .05), religiosity (β = .194, p < .05), and Islamic social finance (β = .212, p < .05) have a significant positive influence on money management skills. Additionally, money management skills have a positive impact on investment decisions (β = .232, p < .05). Third, regarding the moderating analysis, digital financial literacy (β = .134, p < .05) significantly influences money management skills. In contrast, digital financial literacy insignificantly contributes to investment decisions (β = 0.036, p > 0.05). Similarly, the interaction terms of digital financial literacy × Islamic work ethics (β = .031, p > .05), digital financial literacy × religiosity (β = −0.052, p > .05), and Digital financial literacy × Islamic social finance (β = .054, p > .05) have an insignificant effect on the money management skills. These results show that digital does not moderate the nexus between Islamic practices (Islamic work ethics, religiosity, and Islamic social finance) and money management skills. These results do not support H7, H8, and H9. Fourth, as regards the mediation role of money management skills, the outcomes of the structural model (see Table 7) reveal that the indirect effects of Islamic work ethics (β = .066, p < .05), religiosity (β = .045, p < .05) and Islamic social finance (β = .049, p < .05) on investment decisions are significant. These results show that money management skills partially mediate the nexus between Islamic work ethics and investment decisions and between religiosity and investment decisions. While money management skills fully mediate the nexus between Islamic social finance and investment decisions, these results show that H4 and H5 are partially supported, while H6 is fully supported.

Structural model.

Direct and Moderation Effect.

Note. M.Status = Marital status; Emp = Employment Structure; Y.invest = Year of investment; T.invest = Type of investment; IWE = Islamic work ethics; REL = Religiosity; ISF = Islamic social financial activities; DL = Digtial Literacy; MMS = Money management skills; ID = Investment decsion.

Robustness Check

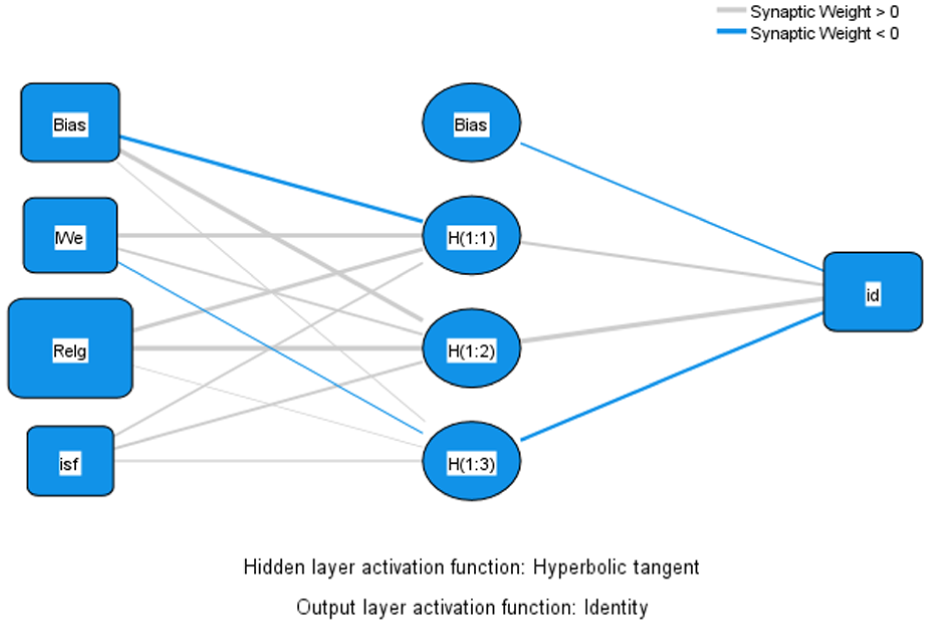

Regression analysis and artificial neural networks (ANN) were performed in SPSS to authenticate the results of Smart-PLS. First, we perform the linear regression analysis using SPSS. We executed five regression models: (a) to check the role of Islamic practices on investment decisions, (b) to assess the influence of Islamic practices on money management skills, (c) to examine the mediating role of money management skills, (d) to analyze the moderating role of digital financial literacy between Islamic practices and money management skills, and (e) to scrutinize the moderating role of digital financial literacy between Islamic practices and investment decisions. The results (see Table 8) obtained from regression analysis are consistent with the outcomes of Smart-PLS. Model 1 shows the impact of control on the dependents. Model 2 shows the direct impact of independent factors on dependents, and Model 3 shows the mediation role. Control variables are age, income, Y investment, EMP, education, MS, etc. Second, we used the ANN technique, which is referred to as “a massively parallel distributed processor made up of simple processing units, which have a natural propensity for storing experimental knowledge and making it available for use” (Sandberg et al., 2001). According to Chan and Chong (2012), ANN is an artificial intelligence technique that can recognize linear and nonlinear relationships in complex modeling. The multilayer perception algorithm method of ANN was used in SPSS to train the model (see Figure 3). “Root Mean Square of Error (RMSE)” was employed to ensure the precision of the ANN analysis. The RMSE scores (see Table 9) for training and testing fall below the threshold level. Furthermore, the sensitivity analysis elucidated the normalized importance, which was assessed as the proportion of their relative significance of exogenous constructs to their maximum relative importance. The Table 10 results indicated that investment decisions were influenced by religiosity (100%), Islamic work ethics (33%), and Islamic social financial activity (21%). So, the results of the ANN analysis demonstrate that religiosity is the most influential predictor of investment decisions.

Regression Analysis.

Note. M. Status = Marital status; Emp = Employment Structure; Y. invest = Year of investment; T. invest = Type of investment; IWE = Islamic work ethics; REL = Religiosity; ISF = Islamic social financial activities; DL = Digital Literacy; MMS = Money management skills; ID = Investment decision.

ANN approach.

Root Mean Square of Errors.

Note. SSE = sum of square of errors; S.D = standard deviation; RMSE = Root Mean square of errors; N = Sample size.

Sensitivity Analysis.

Note. IWE = Islamic work ethics; REL = Religiosity; ISF = Islamic social financial activities.

Discussion and Conclusion

Grounded on the theory of planned behavior (Ajzen, 1991), this research unleashes the importance of Islamic practices: Islamic work ethic, religiosity, and Islamic social finance in money management skills and investment decision making, with a moderating role of digital financial literacy. Previous studies have focused on environmental factors (Brown-Liburd et al., 2018; Maqbool & Zamir, 2021), behaviors, (Ahmad & Wu, 2022; Katper et al., 2019), and demographic factors (Korniotis & Kumar, 2011; Saivasan & Lokhande, 2022) in the literature on the investment decision-making process. However, we interacted with Islamic practices with digital financial literacy to understand their role in managing and investing money. We used empirical evidence from an emerging Islamic country to extract the results.

Based on the results, first, we found that two Islamic practices, namely, Islamic work ethics and religiosity, have a positive and significant influence on investment decisions. These findings are similar to those (El Melki & Ben Salah Saidi, 2023), who found that Islamic work ethics play a prominent role in entrepreneurial decision-making.

These findings are also congruent with the outcomes of (Alshammari & Ory, 2023), who describe that religious announcements significantly contribute to investment decisions. Similarly, Duqi and Al-Tamimi (2019) also demonstrate that religiosity is a significant predictor of investment decision-making in the Malaysian market. Additionally, Kasi and Muhammad (2016) findings are consistent with our results, they also found a positive association between the Islamic beliefs of an individual and their stock market investment decision. Second, our results demonstrate that Islamic social finance does not significantly influence investment decisions. These findings contradict those (Rosman et al., 2019), who concluded that Islamic social finance significantly positively contributes to financial performance. These results are also dissimilar to the findings of (Al-Malkawi & Javaid, 2018), who found that firms paying zakat (social finance) are in a better position to gain positive returns.

Thirdly, our results show that money management skills partially mediate the link between Islamic work ethics and investment decisions, as well as between religiosity and investment decisions. While money management skills fully mediate the nexus between Islamic social finance and investment decisions, these findings portray that Islamic practices (Islamic work ethics, religiosity, and Islamic social finance) significantly influence money management skills, which in turn impact their investment decisions. These results partially support H4 and H5, while they fully support H6. These results are consistent with the empirical findings of Kirby (2008) and Dewi et al. (2020), who posit that religious beliefs significantly influence individuals’ critical thinking skills and financial behavior. These results are also favored by hadith No. 2417 of Al-Tirmizi, which states that all Muslims follow Islamic practices and are accountable for their wealth management while making strategic decisions. These results are parallel with the prior study of Kamaruddin et al. (2021), who found that governance partially mediates the association between Islamic work ethics and enterprise accountability. Similarly, the empirical evidence advocates that all Muslims, regardless of their financial status, are answerable for their wealth management as they are liable for both their assets and liabilities on the day of judgment (Amanda et al., 2018). These results suggested that individuals should emphasize Islamic practices (Islamic work ethics and religiosity) to manage their wealth in a better way to make effective investment decisions. Finally, Islamic work ethics and religiosity are equally essential for managing wealth and investment decisions in the context of the Muslim Republic of Pakistan. These results also reveal that Islamic social finance does not directly influence investment decisions but indirectly contributes to investment decisions through money management skills.

Fourth, considering the moderating role of digital literacy, our findings reveal that digital literacy does not moderate the nexus between Islamic practices (Islamic work ethics, religiosity, and Islamic social finance) and money management skills. These findings clash with the outcomes of Angeles (2022), who reveals that digital literacy strengthens the link between financial services and the investment behavior of owners of SMEs. The main reason for this insignificant outcome in the Pakistani context may be that most investors follow Islamic work practices while managing their wealth and ignore digital information and knowledge. Compared to non-Muslim areas, where digital financial literacy may be more significant, Pakistani investors regularly manage their money by Islamic principles. Even though digital financial literacy did not moderate the relationships, it still showed an impact on money management skills on its own. Furthermore, the lack of beliefs in digital financial literacy may explain why digital financial literacy did not moderate the relationship between Islamic practices and money management skills. It means that digital tools help with financial management, they don’t necessarily strengthen the link between Islamic practices and these skills. This indicates that digital tools help with financial management, they do not necessarily strengthen the link between Islamic practices and these skills. This suggests that while digital tools are used in financial management, the connection between Islamic beliefs and these abilities is not always strengthened by them.

Contributions of the Study

This research makes two important contributions to the body of knowledge in the field of investment decision-making in Sharia and conventional stock markets. First, we employed an empirical method to scrutinize the role of Islamic practices, Islamic work ethic, religiosity, and Islamic social finance in money management skills and investment decision-making behaviors, with a moderating role of digital financial literacy. Although previous studies have extensively tested other factors, such as behavioral (Ahmad & Wu, 2022; Katper et al., 2019), environmental (Brown-Liburd et al., 2018; Maqbool & Zamir, 2021), and demographic (Korniotis & Kumar, 2011; Saivasan & Lokhande, 2022). However, so far, the role of Islamic practices and digital financial literacy in emerging Muslim economies has been ignored. Hence, we interacted with Islamic practices and digital financial literacy to unpack their importance in money management skills and investment decision-making. In the digital era, digital financial literacy plays a central role in the investment decision-making process (Lu et al., 2023), because investors spend time on digital media to extract and share information.

Second, the theory of planned behavior (Ajzen, 1991) has been widely tested in the literature on behavioral finance and investment decisions related to Sharia and conventional stock markets. However, this theory did not capture the attention of scholars toward testing the importance of Islamic practices, such as the Islamic work ethic, religiosity, and Islamic social finance. Our research limits this gap by employing Islamic practices as determinants for investment decision-making with money management skills as a mediator, and digital financial literacy as a moderator. Based on the findings, we demonstrate that Islamic practices play a key role in managing and investing money under digital financial literacy.

Practicing Implications

This study has several worthy policy implications for policymakers, investors, and decision-makers in the stock market. We observe that Islamic work ethics and religiosity are both essential for money management skills and investment decisions in the Islamic Republic of Pakistan. Our study recommends that Islamic work ethics and religiosity significantly improve the money management skills of Pakistani investors, which are essential for effective investment decision making, particularly in the Islamic region of Pakistan. Additionally, the mediating role of money activities between Islamic work ethics and investment decisions, as well as between religiosity and investment decisions. This study recommends that investors and policymakers should emphasize Islamic work ethics and religiosity, along with money management skills, in order to make appropriate investment decisions. However, our study displays that Islamic social finance does not directly contribute to investment decisions unless investors have effective money management skills. Hence, investors in the Pakistani stock market are required to have adequate money management skills to make efficient investment decisions. In other words, Islamic social finance indirectly influences investment decisions through money management skills, which suggests that investors should focus on money management skills. However, this study revealed that digital financial literacy does not moderate the nexus between Islamic practices and investment decisions. It could also be a reason for focusing on both Sharia and conventional stock markets. However, despite this, our study recommends that the regulatory authority of the stock market investigate the insignificant influence of digital financial literacy on the nexus between Islamic practices and investment decisions. An articulated assessment of the insignificant moderating role of digital financial literacy will probably help policymakers develop their policies for successful outcomes. Finally, our study suggests that policymakers in the Pakistani stock market should promote Islamic practices to effectively manage the money as a means of better investment decisions.

Conclusion

This research, grounded on the theory of planned behavior, investigates the interplay between Islamic practices, digital financial literacy, and money management skills in shaping decisions to invest in stocks. This study fills a significant research gap by exploring how Islamic work ethics, religiosity, and Islamic social finance integrate with digital platforms to influence financial behaviors, an area that has been minimally explored previously. Using a sample of 241 investors trading on the Pakistan Stock Exchange (PSE), our findings reveal that Islamic work ethics and religiosity significantly influence decisions to invest in stocks, with money management skills serving as a crucial mediator. Interestingly, while Islamic social finance does not directly make decisions to invest in stocks, money management skills fully mediate this relationship.

Contrary to initial expectations, digital financial literacy does not moderate the relationship between Islamic practices and money management skills. This unexpected outcome underscores the complexity of integrating digital tools with traditional Islamic financial practices and suggests that simply enhancing digital skills may not be sufficient to influence the use of Islamic practices in investment decisions. However, the significant mediating role of money management skills highlights their importance in bridging Islamic principles and investment actions.

Our research contributes to the theoretical and practical understanding of how Islamic financial ethics can be effectively applied in the modern digital economy. The findings advocate for a stronger focus on developing money management competencies among investors to better align their investment strategies with Islamic ethical standards. This approach not only enhances ethical investment practices but also supports the broader goal of sustainable and responsible investing according to Islamic principles.

These insights are valuable for investors and policymakers seeking to promote ethical investment behaviors through educational programs and policy frameworks that support the integration of digital literacy with Islamic financial practices. Moving forward, enhancing digital financial literacy in conjunction with a deep understanding of Islamic finance can provide a more holistic approach to ethical investing in the global financial market.

Limitations and Directions for Future Research

This research has a few constraints that give future scholars an opportunity for further research. We have focused on cross-sectional data that might have common method bias issues. However, we employed Harman’s single-factor test in SPSS to detect the bias. We recommend interviews and secondary information to articulate the results in a better way. We collected data from investors in Pakistan.

Our study’s focus on Pakistani investors could limit its applicability to other Muslim populations or non-Muslim markets due to Pakistan’s distinct cultural context. A future study could examine the other emerging markets or highly religious countries. Such as Indonesia, Saudi Arabia, Afghanistan, etc., to explore how Islamic finance and digital literacy interact in different cultural contexts. This would enhance our understanding of their role in investment behavior.

Researchers from other countries, such as China, India, and European markets, are encouraged to extend the model in their regions. Moreover, our model is based on particular Islamic practices, we suggest other Islamic activities to get comprehensive information. Researchers can also replicate the model with other religions in their countries to understand if religious practices have a key role in investment decisions.

This research used convenience sampling and self-reported data, which could create bias. For instance, participants may have overstated their religious observances or financial management skills to meet social expectations. These biases should be considered when analyzing the results. Participation was entirely voluntary, allowing respondents to complete the survey at their discretion, free from any coercion. These biases should be considered when interpreting the results. Participation was voluntary, allowing respondents to complete the survey at their discretion, free from any coercion. Future researchers could use random sampling and objective data to prevent these biases, providing more robust and broadly applicable results.

In this study, we did not differentiate between Sharia and conventional stock markets, future researchers should use the unique role of Islamic practices to understand if people who adhere to Islamic practices are more likely to invest in Sharia or conventional stock markets. It will enrich the literature and articulate the results in a better way.

The study emphasizes the connection between religiosity, Islamic work ethics, and money management skills, but does not thoroughly examine the causal factors behind these relationships. A qualitative method, such as interviews or focus groups, could provide a deeper understanding of these dynamics. Furthermore, a mixed-methods approach, combining both quantitative and qualitative data, could further improve future research by offering a more comprehensive insight into how these variables are connected. Our model illustrates digital financial literacy as a moderator. Future researchers can employ other variables to explore if investors need other types of skills and capabilities for managing and investing their money.

Footnotes

Appendix

| Investment decision | ||

|---|---|---|

| 1 | With the given investment opportunities, I would prefer to invest in stock market rather than the fixed income security | |

| 2 | I base my stock buying decisions on company’s historical information such as historical returns | |

| 3 | My stock buying decisions are based on company’s fundamentals (dividend pay-out, cash flows and earnings growth). | |

| 4 | I like to buy the stocks that have high trading volumes | |

| 5 | I like to buy the stocks that recently outperformed the market. | |

| 6 | I like to buy the stock that has been a loser in the recent past because I expect it to recover in future | |

| 7 | I prefer to invest in stocks that are frequently cited in news or advertised | |

| Islamic work ethics | ||

| 1 | Laziness is a vice | |

| 2 | Dedication to work is a virtue | |

| 3 | Good work benefits both one’s self and others | |

| 4 | Justice and generosity in the work place are necessary conditions for society’s welfare | |

| 5 | Producing more than enough to meet one’s needs contributes to the prosperity of society as a whole | |

| 6 | One should carry work out to the best of one’s ability | |

| 7 | Work is not an end in itself but a means to foster personal growth and social relations | |

| 8 | More leisure time is good for society | |

| 9 | Work enables man to control nature | |

| 10 | Any person who works is more likely to get ahead in life | |

| 11 | Work gives one the chance to be independent | |

| 12 | A successful person is the one who meets deadlines at work | |

| 13 | One should constantly work hard to meet responsibilities | |

| 14 | The value of work is delivered from the accompanying intention rather than its result | |

| Religiosity | ||

| 1 | I enjoy reading about Islam | |

| 2 | It does not much matter what I believe so long as I am good | |

| 3 | It is important to me to spend time in private thought and prayer | |

| 4 | I have often had a strong sense of Allah’s presence | |

| 5 | I tried hard to live all my life according to Islam | |

| 6 | Although I am religious, I do not let it affect my daily life | |

| 7 | My whole approach to life is based on Islam | |

| 8 | Although I believe in Islam, many other things are more important in life | |

| 9 | Prayer is for peace and happiness | |

| 10 | Although I am religious, I do not let it affect my daily life | |

| 11 | I go to masjid mostly to spend time with my friends | |

| 12 | My whole approach to life is based on my religion | |

| 13 | I go to masjid mainly because I enjoy seeing people I know there | |

| 14 | Although I believe in my religion, many other things are more important in life | |

| Islamic social financial | ||

| 1 | I prefer Islamic social finance instruments (i.e., zakat, waqf, sadqa, and sadqa fitter) for the benefits of society | |

| 2 | I pay zakat every year if I meet the prescribe criteria | |

| 3 | I contribute to the prosperity of society via sort form of sadqa on regular basis | |

| 4 | Waqf is a continuous charity, I will must donate (waqf) for the benefit of society | |

| 5 | My donation via zakat, waqf, and sadqa are likely to have an impact on society | |

| 6 | I always encourage interest-free loan and discourage interest | |

| 7 | I intend to help needy person via interest-free loan (qarze hasan) | |

| Digital financial literacy | ||

| 1 | Have a good understanding of digital payment products, such as E-Debit, E-Credit, E-Money, Mobile/Internet banking, and E-Wallet | |

| 2 | Have a good understanding of digital asset management products | |

| 3 | Have a good understanding of digital loan products | |

| 4 | Have a good understanding about digital insurance product | |

| 5 | Have a good understanding of customer rights and protection as well as procedures for service complaints from digital financial | |

| Investment decision | ||

| 6 | Have experience in using digital payment products, | |

| 7 | Have experience using fintech products and services for financing (loans) and investments | |

| 8 | Experience in using fintech products and services for asset management | |

| 9 | Have awareness about the potential financial risks of using fintech, such as the legality of fintech providers, interest rates, and transaction fees | |

| 10 | Have the ability to manage financial activities through digital platforms | |

| 11 | Have good control over financial activities using digital platforms by evaluating expenses on the platform | |

| Money management skill | ||

| 1 | Follow a weekly or monthly budget | |

| 2 | Review and evaluate spending on a regular basis | |

| 3 | Kept a written or electronic record of your monthly expenses | |

| 4 | Estimate household income and expenses. | |

Ethical Considerations

All procedures performed in studies involving human participants were in accordance with the ethical standards of the institutional and/or national research committee and with the 1964 Helsinki Declaration and its later amendments or comparable ethical standards.

Consent to Participate

Implied informed consent was obtained from all participants involved in the study. In line with national regulations and institutional guidelines, written informed consent was not required for this research. During this process, participants were clearly informed about two key aspects: (i) confidentiality: ensuring that any personal information shared by participants would be kept confidential and not disclosed or published. (ii) Use of data: stating that the data collected would be used solely for academic research purposes and not for commercial purposes.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data available on request.