Abstract

Amidst efforts to combat high corruption incidence in Ghana, the Office of the Special Prosecutor Act, 2017 (Act 959) was enacted to investigate and prosecute specific cases of alleged or suspected corruption offenses in accordance with the United Nations Convention against Corruption. Contrariwise there is a weak accountability, probity, and transparency in the Ghanaian Public Sector as asserted by the Transparency International release (2018–2022). Against this backdrop, this aims to analyze the implications of internal audit efficacy (measured with; risk management, environmental sensitivity, and audit effectiveness), on energy saving behavior, and develop a baseline model to enhance energy saving behavior through sustainability audit. The paper utilized a quantitative research approach and cross-sectional survey design to draw data from 405 public officials across different public sector agencies in Ghana. Variance-Based Structural Equation Modeling and SMART-PLS version 3.3.8 have been used to validate the hypotheses herein. The paper has found that internal audit efficacy has significant effect on sustainability audit and energy saving behavior. Moreover, the paper has revealed sustainability audit significantly mediates the relationship between internal audit efficacy and sustainable energy saving behavior among public sector officials. These indicative results have implications on the newly developed model that could be used to enhance energy saving behavior in a country where such studies have been inadequately explored. These results have reaffirmed the relevance of internal audit efficacy and sustainability audit in energy transition polices as well as the realization of sustainable development goals.

Plain language summary

In an effort to stop the high rate of corruption in Ghana, the Office of the Special Prosecutor Act, 2017 (Act 959) was passed. This law gives the Office of the Special Prosecutor the power to examine and pursue specific cases of claimed or suspected corruption crimes, in line with the United Nations Convention against Corruption. On the other hand, a report from openness International (2018-2022) says that the Ghanaian Public Sector has weak accountability, probity, and openness. In light of this, the goal of this study is to analyse the effects of internal audit efficiency (measured by risk management, environmental awareness, and audit effectiveness) on energy-saving behaviour and create a standard model to improve energy-saving behaviour through sustainability audit. The paper found that the effectiveness of internal audits has a big effect on environmental audits and how people act to save energy. The study also found that sustainability audit greatly mediates the link between the effectiveness of internal audits and how public sector employees save energy in a sustainable way. These preliminary results have an effect on the newly made model, which could be used to get people to save more energy in a place where these kinds of studies haven’t been done enough. These results have shown again how important internal audits of effectiveness and audits of sustainability are for energy transition policies and for meeting sustainable development goals.

Introduction

Indubitably, strong internal controls are essential for good governance, sustainable economic growth, poverty reduction, corruption purging, and ultimately Sustainable Development Goals (SDGs). Good governance indispensably entails accountability, transparency, participation, fighting corruption and promoting effective legal and policy frameworks (Endaya & Hanefah, 2016; Erasmus & Coetzee, 2018; Turetken et al., 2020). This paper argues that strong internal controls proxied as internal audit efficacy (risk management, internal audit effectiveness, environmental sensitivity) drives sustainability audit and subsequently affects energy savings behavior of public officials (Amoako et al., 2023; Appiah et al., 2023; DeSimone et al., 2021). The paper has established a symbiotic relationship between audit efficacy and energy savings behavior. There is proliferation of studies (Amoako et al., 2023; Appiah et al., 2022, 2023) that have argued that internal audit functions such as risk management practices, audit effectiveness, environment sensitivity, and standards and policies have effects on resource utilization among public officials. To this end the Special Prosecutor Service Act 2017 (Act 959) was passed to re-enforce good governance through investigation and prosecution of certain cases of alleged or suspected corruption offenses which is consistent with the United Nations (UN) Convention against Corruption (Appiah et al., 2023).

The emergence of SDGs and the ensuing introduction of the Paris Climate Agreement, researchers have linked progress toward the 17 SDGs to effective internal controls. Appiah et al. (2023) argued that due to the misuse of public resources in Ghana, the Institute of Internal Audit Act (Act 658) was enacted in 2003 to ensure integrity, accountability, and transparency in the management of public resources. Amoah et al. (2022) asserted that corruption perception is a bane to sustainable energy consumption. In effect internal auditors are required to step up its functions to reduce corruption incidence and promote sustainable energy savings behavior. The main purpose of internal audit is to help protect the organization through transparency, accountability, and integrity. Internal audit aims to minimize risks and protect assets, ensure accuracy of records, improve operational efficiency, and promote compliance with policies, rules, regulations, and laws (Appiah et al., 2023; Report of The Auditor, 2018). This paper focuses on internal controls and energy saving behaviors, and further argues that any form of laxity in the internal control mechanisms will lead to inadequate internal controls, reduced efficiency, complicate transaction processing, increase transaction processing time, and add no value to operations (Erasmus & Coetzee, 2018; Turetken et al., 2020).

Against this backdrop this paper aims to investigate the impacts of internal audit efficacy on energy savings behavior, and develop a baseline model to enhance sustainable energy saving behavior through sustainability audit with a focus on Ghana. Inferring from the aim of the study, the following three research propositions are essentials to contribute new perspectives on internal audit controls proxied as internal audit efficacy and energy saving. The first proposition presents the effects of internal audit efficacy on energy saving behavior of public officials. The paper argues that internal audit efficacy is required to ensure that energy resources available to public officials are utilized efficiently. Internal audit efficacy has been measured using three sub-constructs, namely; risk management, environmental sensitivity, and internal audit effectiveness (Appiah et al., 2023; Erasmus & Coetzee, 2018; Turetken et al., 2020). The indicative results have showed that effective risk management practices, effectiveness of internal audit, internal audit policies and standards compel public officials to optimize the usage of public resources. Secondly, this paper is among the paucity of studies that examine the indirect (mediation) effect of sustainability audit on the nexus between internal audit efficacy and energy saving behavior. Sustainability audit encompasses the practices of ensure that the organization is meeting its governance responsibilities, managing its sustainability performance, complying with environmental regulations, and adhering to the organization’s sustainability policy (Amoako et al., 2023; DeSimone et al., 2021; Fraser et al., 2020; Rosin et al., 2017; Shukla & Mattar, 2018).

Thus, the paper argues that sustainability audit can serve as a mechanism through which internal audit efficacy drives positive energy saving behavior. Finally, the third proposition is that sustainability audit relates to energy saving behavior in a number of ways including safeguarding public resources by adhere to environmental regulations and sustainability policies (Khan, 2019). These indicative results have implications on the newly developed model that could be used to enhance energy saving behavior in a country where such studies have been inadequately explored. These results have reaffirmed the relevance of internal audit efficacy and sustainability audit in energy transition polices as well as the realization of sustainable development goals, particularly sustainable and clean energy (SDG7) and responsible consumption and production (SDG12). The current study has taking cognizance of previous studies that assessed energy usage from the perspective of corruption and energy injustice. For instance, Boamah et al. (2021) argue that the persistence of corruption, despite intensified anti-corruption endeavors, necessitates a deeper examination of the entitlement beliefs that underpin engagement in corrupt practices. The latest data pertaining to Ghana’s energy sector underscores the potential role of corruption as an informal mechanism for addressing perceived long-standing disparities in energy distribution. Energy consumption in Ghana is affected by various factors, including the uneven spatial distribution of electrical grids, bureaucratic processes involved in grid connections, perceived inequities in electricity billing systems, and the relatively lower energy output of decentralized solar photovoltaic (PV) systems. These challenges have compelled certain energy users to resort to covert methods in order to obtain or expedite access to the electrical grid. The allowance of customers to utilize power credits for offsetting perceived “unjust” pricing has been disallowed in Ghana as a result of inadequate enforcement of net metering tariff legislation. The pursuit of rectifying structural imbalances, inequalities, and various forms of injustice in both spatial and societal contexts has led to the emergence of corruption concepts and energy justice approaches as significant areas of study. This report is organized into five sections as followings: The section “Introduction” presents the introduction section comprising backing to the problem statement, objectives, and contribution, the section “Literature Review” presents the review of literature covering theoretical and empirical reviews, the materials and methods are presented in the section “Materials and Methods,” the results and discussions are presented in section “Results and Discussions,” and the final section presents conclusions, implications, and limitations.

Literature Review

Theoretical Orientation (Contingency Theory) and Research Framework

The underlying theory of the paper is the contingency theory. Contingency theory as proposed by Richard Dart argues that the functions of organization are interdependent. One functional area depends on the other for effectiveness. The functions of internal audit are dependent on several internal and external factors. These include; access to documents, policies, systems, procedures, and standards. To achieve efficiency in energy saving among public officials in Ghana, the internal audit unit requires level of compliance from the public officials such as government regulations, internal proceedings, industry requirements, and standards among others. Proliferations of prior studies (Alzeban & Gwilliam, 2014; Appiah et al., 2023; Endaya & Hanefah, 2016; Erasmus & Coetzee, 2018; Lenz & Hahn, 2015; Turetken et al., 2020) have employed the contingency theory to explain the interdependency between audit functions and organizational outcomes including efficiency, effectiveness, value for money, accountability, and transparency. As showed in the Figure 1. The paper argues that sustainability audit is the mechanism through which internal audit efficacy drives positive energy saving behavior. Energy-saving behavior is influenced by factors which are related to psychology such as attitudes, norms within the society, and the values (Frederiks et al., 2015; Wang et al., 2018). Energy-efficient behavior helps in the improvement in the environment with the reduction of greenhouse emission of gas and pollution of air (Martinsson et al., 2011). Energy-saving behavior is an overarching construct consisting awareness of issues related to energy, interest level, perception of energy conservation management, and responsibility of sensing (Yue et al., 2013). Energy conservation behavior reflects a person’s efforts to reduce overall energy saving (Zhang et al., 2018). It is the habitual practices of households which focus on reduction of specific usage of energy (Trotta, 2018). In a recent study Appiah et al. (2023) adopted the contingency theory in a related study. Internal audit efficacy has been measured using three sub-constructs, namely; risk management, environmental sensitivity, and internal audit effectiveness.

Research framework.

Risk Management Practices and Energy Saving Behavior

Risk management is one of the sub-constructs used to measure internal audit efficacy (Bento et al., 2018; Fan & Stevenson, 2018; Norrman & Wieland, 2020; Tang & Nurmaya Musa, 2011). It is a comprehensive process of identifying, analyzing, accepting, and mitigating uncertainty and risk in the supply chain (Blome & Schoenherr, 2011). It is an ongoing process that is directly linked to changes in the internal and external environment (Abu Hussain & Al-Ajmi, 2012). It is a procedure of identifying risk, analyzing and responding to risk (i.e., things which are in relation to the project and the management of activities which are not known clearly, but which may have a negative impact on project objectives; PMI, 2004). Again, is a way used by the boards, the management and staff in the formulation of strategy throughout the entity in identification of events which are potential and will have influence the entity and ensure that the risks level are kept at low as possible (Songling et al., 2018). It entails the combination of the probability of an event and its consequences (Gitman, 2008; ISO-IEC, 2002). Clearly from the ongoing, internal audit uses risk management practices to positively contribute to the achievement of almost all operational goals, portfolios, and objectives. Thus, risk management practices are an integral part of an organization’s internal audit. Therefore, the study hypothesizes as follow:

H1a: Risk management practices positively relate to sustainability audit among public officials

H1b: Risk management practices positively relate to energy saving behavior among public officials

Environmental Sensitivity and Energy Saving Behavior

Environmental sensitivity also known as sustainability sensitivity is one of the sub-constructs used to measure internal audit efficacy (Ghalehkhondabi & Ardjmand, 2020; Pluess, 2015; Pluess et al., 2018; Shrivastava et al., 2017). This includes empathically perceiving and responding to the acute consequences of negative environmental change (pollution, disasters, human development) and threats to the safety, survival, and reproduction of ecological habitats in ecosystems (Sun and Gao, 2015). Sensitivity to manipulation and reluctance to accept simplistic explanations can enhance perceptual sensitivity by increasing awareness of relevant details (Vogus and Sutcliffe, 2012). Environmental sensitivity is the emotional capacity of an individual to perceive the environment empathetically. Understood as “the tendency to learn about, be interested in and act to protect the environment based on formative experiences” (Cheng and Wu, 2014), environmental sensitivity is “an affective quality that causes an individual to perceive the environment more positively” (Cheng and Wu, 2014). Environmental awareness is an “empathetic attitude towards the environment” and is considered one of the variables contributing to responsible environmental citizenship. A strong link has been established between environmental awareness and the development of pro-environmental behavior (Hungerford and Volk, 1990). Environmental sensitivity is defined as an empathetic understanding of, and response to, the serious consequences of adverse environmental change (pollution, disasters, human development) on the ecological environment (including humans and other biological groups) and threats to ecological security, survival, and reproduction (Sun & Gao, 2015). Environmental sensitivity has been defined as an emotional trait that enables people to encounter the environment from an empathic perspective, and environmental sensitivity is empathy toward the environment (Candrea & Hertanu, 2015). Environmental sensitivity is a predictor and antecedent variable of environmental perception (Kunz et al., 2016), environmental sensitivity is a predictor and antecedent variable of environmental behavior based mainly on life experiences (Lu et al., 2016). Therefore, the study hypothesizes as follow:

H2a: Environmental sensitivity positively relates to sustainability audit among public officials

H2b: Environmental sensitivity positively relates to energy saving behavior among public officials

Internal Audit Effectiveness and Energy Saving Behavior

Internal audit effectiveness is one of the sub-constructs used to measure internal audit efficacy (Alzeban & Gwilliam, 2014; Endaya & Hanefah, 2016; Erasmus & Coetzee, 2018; Lenz & Hahn, 2015; Turetken et al., 2020). Effectiveness of internal audit can be seen as an independent and an objective auditing with activity of consulting with the aim of adding value to the organization and improvement of performance. The works of the auditors helps the organization in the achievement of their objectives with the provision of disciplinary and systematic approach in the assessment and effective improvement of management of risk, process of controlling and governance (Getie Mihret & Wondim Yismaw, 2007). Their effectiveness within the public sector should be quantify at the level of which they contribute in the delivery of efficient and effective services (Van Gansberghe, 2005). Internal audit occupies a unique position among internal audit services provided by the public sector and regulators, as the recent scandals in organizations and the global financial crisis have shown (Soh & Bennie, 2011). Effectiveness is defined as the ability to deliver results in line with the stated objective (Arena & Azzone, 2009). Internal audit effectiveness is “a risk-based approach that helps an organization achieve its purpose by positively influencing the quality of management” (Lenz, 2013). Therefore, the study hypothesizes as follow:

H3a: Internal Audit Effectiveness positively relates to sustainability audit among public officials

H3b: Internal Audit Effectiveness positively relates to energy saving behavior among public officials

Sustainability Audit as a Mediator

Another important proposition of the paper is that there is a relationship between sustainability audit and energy saving behavior (Amoako et al., 2023; DeSimone et al., 2021; Fraser et al., 2020; Rosin et al., 2017; Shukla & Mattar, 2018). This paper is among the paucity of studies that examine the mediating role of sustainability audit on the relationship between internal audit efficacy and energy saving behavior. Sustainability audit encompasses the practices of ensure that the organization is meeting its governance responsibilities, managing its sustainability performance, complying with environmental regulations, and adhering to the organization’s sustainability policy (Khan, 2019; Nie et al., 2019; Trotta, 2018; Van den Broek et al., 2019; Wang et al., 2018). The Sustainability audits have three main features: assessing environmental management performance against measurable criteria and links to other criteria and factors, using a qualified audit team and reporting on the organization’s progress (internal, external, or both). The definition covers these three main features. Sustainability audits conducted by internal auditors aim to ensure that the organization is meeting its governance responsibilities, managing its sustainability performance, complying with environmental regulations, and adhering to the organization’s sustainability policy (Darnall et al. 2009). Audits are an important part of ensuring that the information provided complies with financial and non-financial regulations and responsibilities. Sustainability audits automatically collect audit metrics and internal or external auditors regularly review a company’s transactions, processes, controls, and information systems. Sustainability audits are a standard for assessing a company’s performance (Baumann-Pauly et al. 2013) Sustainability audits reflect a technocratic approach to management and control by organizing, standardizing, and generalizing production processes. Sustainability audits aim to extend the scope of control to social-ecological systems (Bell & Morse, 2008). Audits are a new distancing phenomenon that provides a mechanism for building trust and maintaining control when scalability limits direct communication to build trust and undermines previously direct and hierarchical power structures (Reid & Rout 2017). From the presentation herein the study hypothesizes as follow:

H4: Sustainability Audit positively relates to energy saving behavior of public officials

H5a-c: Sustainability Audit positively mediates the relationship between (risk management, environmental sensitivity, and internal audit effectiveness) internal audit efficacy and energy saving behavior of public officials

Materials and Methods

Setting and Research Design

This paper focuses on the public sector agencies and institutions. The Ghanaian public sector is bedeviled with high public corruption index. Amidst efforts to combat high corruption incidence in Ghana, the Office of the Special Prosecutor (OSP) Act, 2017 (Act 959) was enacted to investigate and prosecute specific cases of alleged or suspected corruption offenses in accordance with the United Nations Convention against Corruption. Contrariwise there is a weak accountability, probity, and transparency in the Ghanaian Public Sector as asserted by the Transparency International release (2018–2022). This paper is aimed to analyze the implications of internal audit efficacy on energy usage behavior, and develop a baseline model to enhance sustainable energy saving behavior through sustainability audit with focus on public agencies in Ghana. The paper utilized a quantitative research approach and cross-sectional survey design to draw data from 405 public officials across different public sector agencies in Ghana. Quantitative research design is consistent with the statistical and mathematical modeling required in Structural Equation Modeling (SEM). Moreover, the quantitative research approach also supports the use of numerical data and survey-based design used in the current study. Appiah et al. (2023) has used this approach in related studies.

Population and Sampling Procedure

The population of this paper consists of state enterprises and government agencies including public-private partnerships corporations. The main target participants for the paper comprised Auditor, Accountant, Finance Officer, Procurement Officer, Operations Officer, Transport Officer, Inventory Manager, and Units Heads. The scope of the paper was limited to the main metropolitan areas in Ghana. Namely; Kumasi, Tamale, Accra, and Takoradi metropolitan areas. These four cities in Ghana are the host of majority of public agencies and enterprises. Moreover, these metropolitan areas provide fair representative of the industry. Besides, the corruption perceptions are highly relatively high in these cities. The sampling size of the study has been selected using the rule of 10 method. Scholars (Hair et al., 2017) have asserted that this method is suitable for SEM. Sample size of 500 has been used for the study, out of which 405 useable responses have been received recording 81% after third round of data gathering. Both online and face to face approaches were used to reach out to majority of the target population. The participants were randomly selected from each stratum, after forming strata using the job designations of the participants. This technique is very efficient in producing fair representatives by reducing sampling error.

Constructs Measurements and Data Collection Instrument

As showed in Table 1, survey based structural questionnaire has been used as the main data collection strategy. The instruments have been adopted and significantly modified and applied in a developing economy context. The measurement items for sustainability audit were adopted and modified from Shih et al. (2006), the measurement items for environmental sensitivity were adopted and modified from Ndubisi et al. (2020), internal audit effectiveness items were adopted and modified from Musah et al. (2018) and Appiah et al. (2022), the measurement items for risk management were adopted and modified from Hassan (2009), energy saving behavior measurement items were adopted and modified from Van den Broek et al. (2019). The instruments were measured using 5-Point Likert Scale where the highest point of the scale was scored 5-strongly agree while the least point of the scale was scored 1-strongly disagree. This type of scale is suitable for measuring public opinion, perception, and attitude. Previous studies (Amoah et al., 2022; Appiah et al., 2023) have used same type of scale in related studies. The instruments also include demographic information such as age, gender, education, experience, job designation.

Measurement Scale and Sources.

Source. Authors Compilation.

Data Analyses

Consistent with the research approach employed for the paper, variance based-SEM has been used to for the data analysis with the aid of SMART-PLS version 3.3.8. The SEM is undoubted, a robust form of the traditional regression analysis (first Generational Analysis). As part of the quality control process techniques employed in the study, the filed data were subjected to screening. Prior to the data analysis. The field data were screened to detect possible omissions, double-entry, and non-completions. The main analyses have been structured into two. Namely; measurement model and the structural modeling. The measurement model focused on the scale validation, specifically, the discriminant validity and convenience validity. The second part of the analysis focused on the structural model (path coefficients). The original sample size was bootstrap using 500 resamples to generate T-values and path coefficients which have been used to test the hypotheses of the study. These procedures were proposed by Hair et al. (2014) to evaluate the structural model. Mediation analysis using the SEM approach was proposed by Hair et al. (2014). SEM is arguably the most efficient form of traditional regression analysis (first-generation analysis) and can handle multiple exogenous mediator variables and outcome variables (endogenous variables) in a single analysis (Cepeda et al., 2017; Nitzl et al., 2016).

Results and Discussions

Participants’ Profile

As showed in the Table 2, more than half of the participants were males (57%) while the rest were females. Slightly below one third (29.1%) of the participants were aged between 25 and 30 years, 21.5% were aged between 36 and 40, 20.5% were aged between 31 and 35, and the least age group (12.8%) were 46 years and above. Slight above one third (34.6%) of the participants had masters’ educational qualifications, approximately, one-third (31.4%) of the participants had attained bachelor degree qualification, only 8.6% of the participants had attained diploma and HND educational qualifications. Regarding work experience, nearly half of the respondents had worked between 5 and 9 years, 27.7% had worked between 10 and 14 years, just 8.6% of the total participants had worked between 15 and 19 years. Around one fifth of the participants were finance officers, 17.3% were accountants, 11.9% were auditors, 16.5% were procurement officers.

Participants’ Demographics Profile.

Source. Field Survey, 2023.

Measurement Model (Scale Validation)

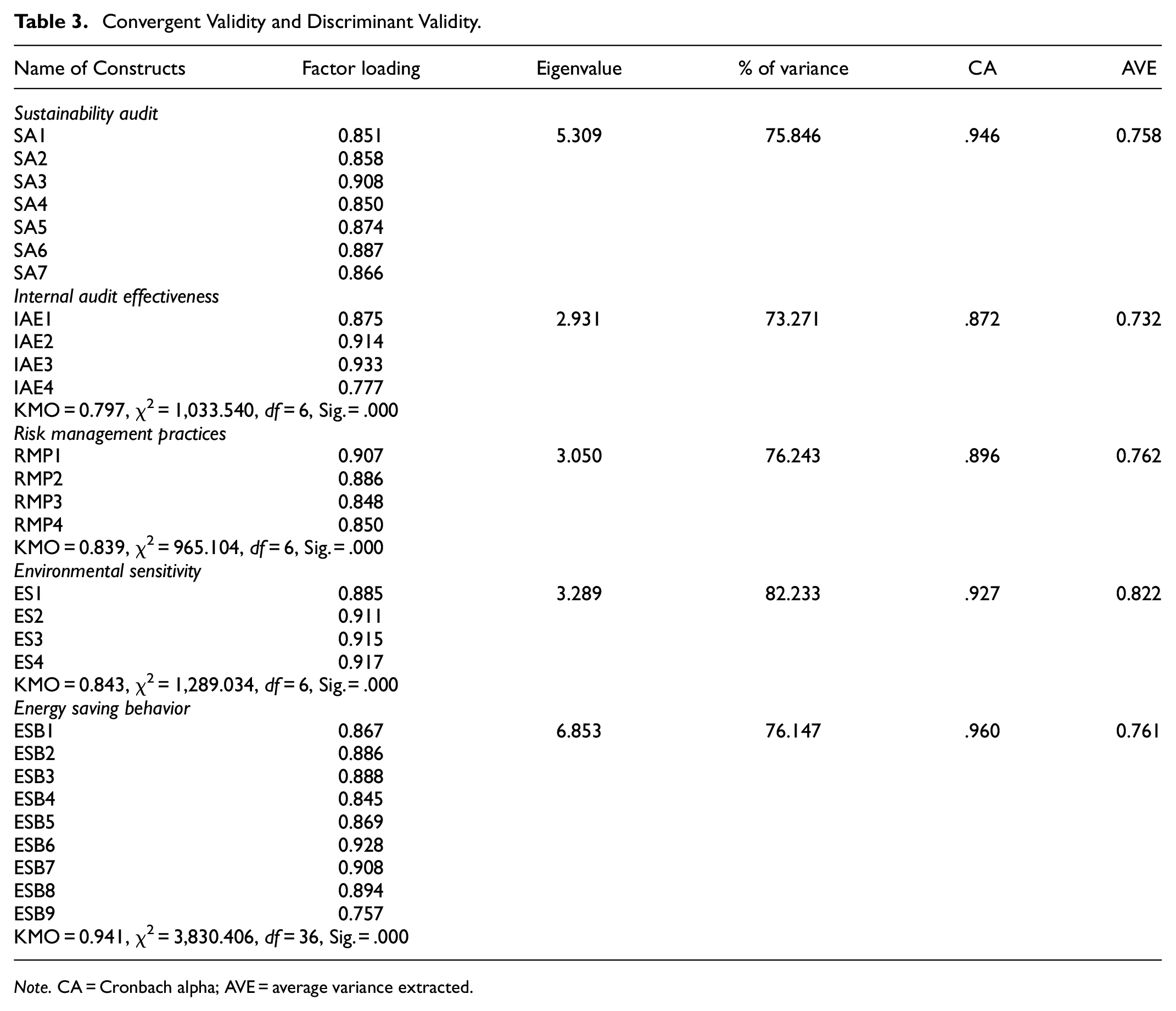

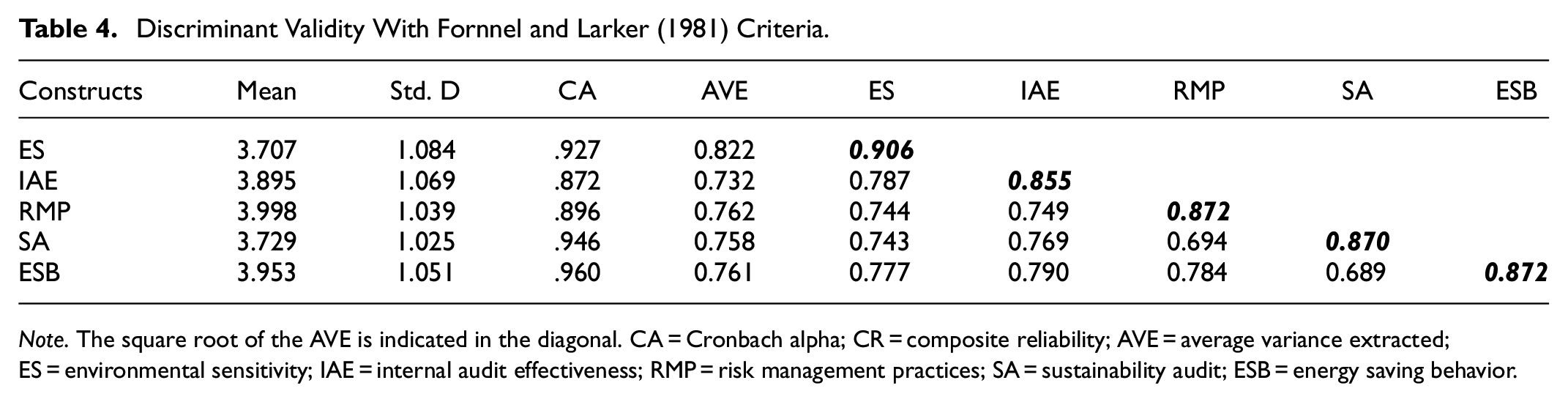

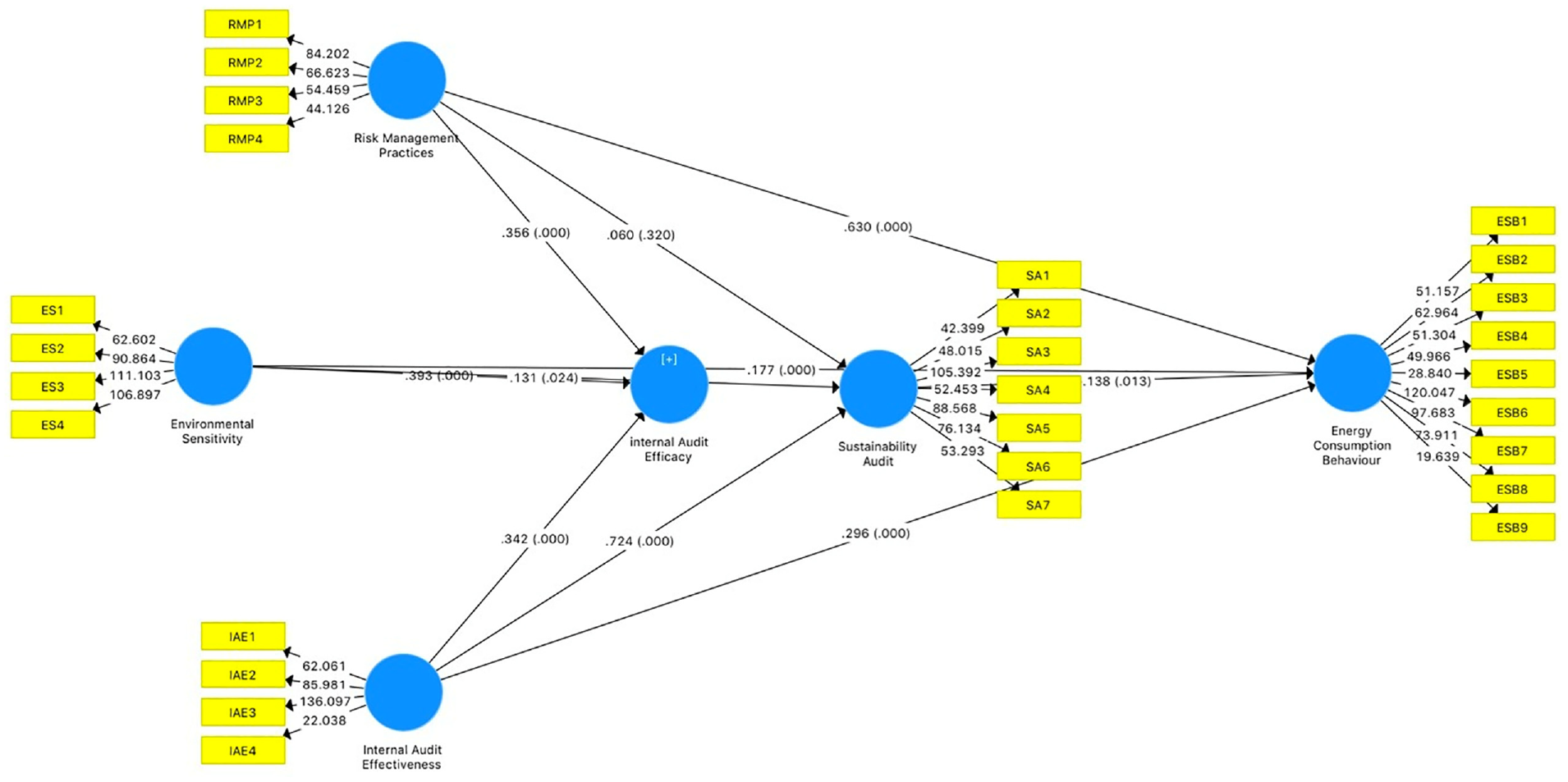

As indicated in the Table 3, the results of convergent validity and discriminant validity have been presented as the measures of the overall scale validation of the model. Specifically, scholars (Hair et al., 2014, 2017) have argued that these tests are not just requirements but also a precondition to ensure continuation to the structural model. Factor loadings, Cronbach Alpha, (CA), and Average Variance Extracted (AVEs) have been conducted to assess convergent validity of the model. The results have showed that sustainability audit was assessed using seven items and obtained .946 CA, 0.758 AVE, and all the individual items loadings exceeded 0.70. Internal audit effectiveness was assessed using four items scoring .946 CA, 0.73 AVE, and 0.77 to 0.933 factor loading range. The risk management was measured using four items, .896 CA, 0.762, and between 0.848 and 0.907 range of factor loadings. Environmental sensitivity was assessed with four items and obtained .927 CA, 0.822 AVE, and between 0.885 and 0.917 range of factor loadings. The scores of the energy saving behavior far exceeds the minimum requirement. These results are indication that the model has met the assumption for convergent model. As indicated in Table 4 the scores of AVEs were square rooted and the outcome compared with correlation matrix. The results have showed that the squared values are mare than the correlated coefficients suggesting that the model has met the requirement of discriminant validity. Figure 2 presents the graphical results on path coefficients and T-values of the model. The structural model results have been presented in the next section.

Convergent Validity and Discriminant Validity.

Note. CA = Cronbach alpha; AVE = average variance extracted.

Discriminant Validity With Fornnel and Larker (1981) Criteria.

Note. The square root of the AVE is indicated in the diagonal. CA = Cronbach alpha; CR = composite reliability; AVE = average variance extracted; ES = environmental sensitivity; IAE = internal audit effectiveness; RMP = risk management practices; SA = sustainability audit; ESB = energy saving behavior.

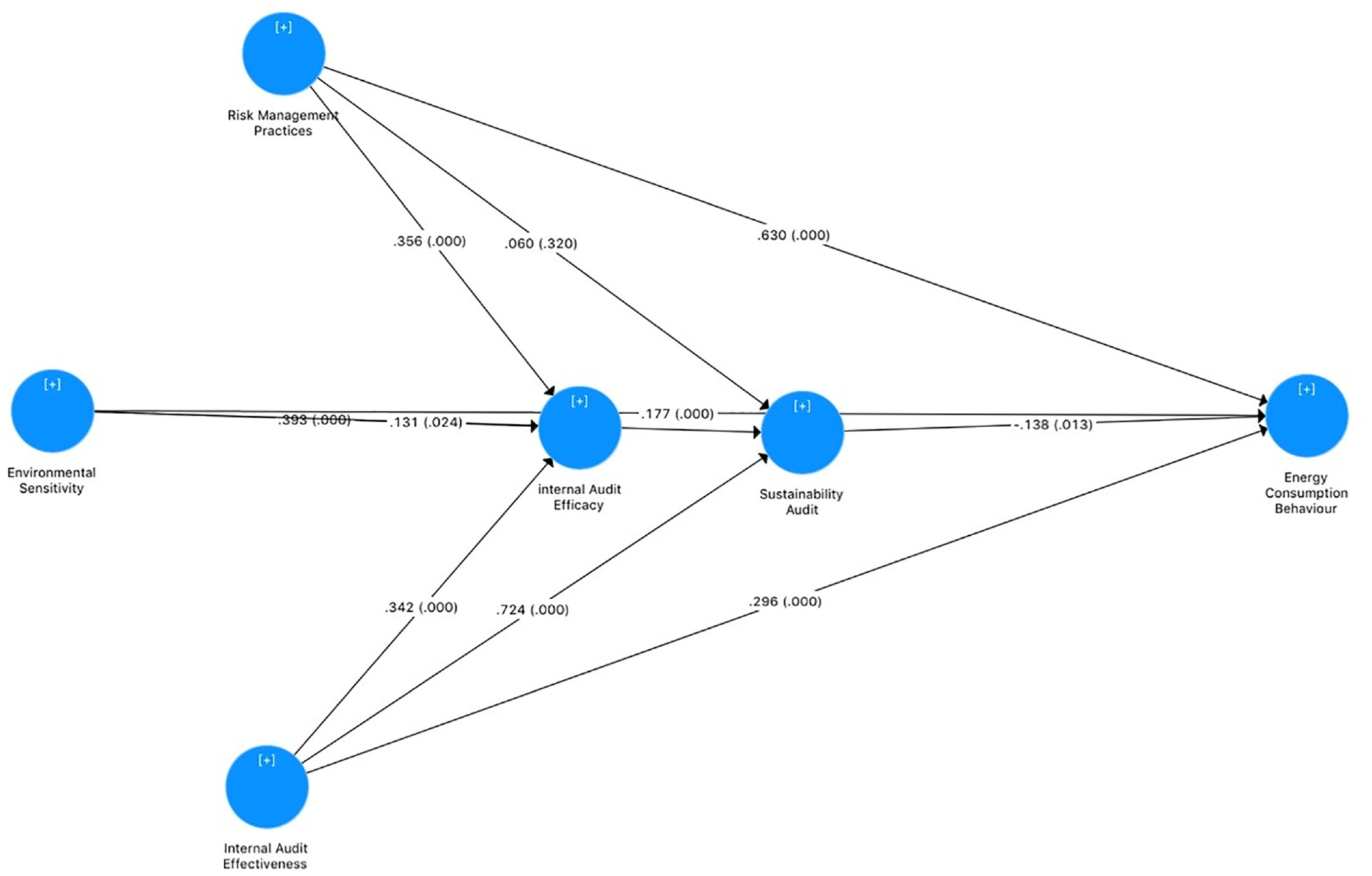

Path co-efficients and T-values.

R-square (R2) and Construct Crossvalidated Redundancy (Q2)

As showed in the Table 5 the results of the R-square (R2) and Construct Crossvalidated Redundancy (Q2) have been presented. The results have showed that the newly developed energy saving behavior has predictive power ranging between 0.77 and 0.83 (R-square scores). These results suggest that between 77% and 83% variability in energy saving behavior have been explained by the dimensions of internal audit efficacy (internal audit effectiveness, risk management practices, and environmental sensitivity), sustainability audit, and energy saving behavior. The results imply that internal audit efficacy has strong predictive power over energy saving behavior. Moreover, the results suggest that there are other factors that are relevant in energy saving behavior which were not considered in the current model. The Construct Cross-validated Redundancy (Q2) has been presented as a means to validate the R-square scores. The Q2 results ranged between 0.578 and 0.629 which is greater than 0 suggesting that the model has a predictive relevance. The next section presents results on path-coefficients and hypotheses testing.

Construct Crossvalidated Redundancy (Q2).

Note. ESB = energy saving behavior; ES = environmental sensitivity; IAE = internal audit effectiveness; RMP = risk management practices; SA = sustainability audit.

Structural Model (Path Coefficients and Hypotheses Testing)

As showed in the Table 6 the results of the structural model have been presented. The results have showed that overall, 9 out of the 10 hypotheses have been supported. With respect to the direct effects the study has revealed that RMP has weak and insignificant (β = .060, T = 0.996) effect on SA. Meanwhile, RMP has significant effect (β = .622, T = 13.015) on ESB, ES has significant effect (β = .131, T = 2.264) on SA, ES has significant effect (β = .159, T = 3.110) on ESB, IAE has significant effect (β = .724, T = 11.871) on SA, IAE has significant effect (β = .196, T = 4.200) on ESB, SA has significant effect (β = .138, T = 2.489) on ESB. Concerning the indirect effects, the study has revealed that SA significantly mediated (β = .356, T = 43.575) the relationship between RMP and ESB, SA significantly mediated (β = .393, T = 51.836) the relationship between ES and ESB, finally, SA significantly mediated (β = .342, T = 57.402) the relationship between IAE and ESB. Figure 3 presents the graphical results on path coefficients of the model. All the hypotheses have been supported except H1a. The details of the results have been discussed in the next section of the paper.

Structural Model—Path Coefficients and Hypotheses Testing.

Note. ESB = energy saving behavior; ES = environmental sensitivity; IAE = internal audit effectiveness; RMP = risk management practices; SA = sustainability audit.

Path co-efficients and hypotheses testing.

Discussions

The purpose of this paper was to analyze the implications of internal audit efficacy on energy usage behavior, and develop a baseline model to enhance sustainable energy saving behavior through sustainability audit with focus on public agencies in Ghana. The first proposition presents the effects of internal audit efficacy on energy saving behavior of public officials. The results have revealed that internal audit efficacy dimensions such as internal audit effectiveness, environmental sensitivity have positive and significant effects on energy savings behavior which are very consistent with prior studies (Appiah et al., 2023; Erasmus & Coetzee, 2018; Turetken et al., 2020). These results imply that internal audit efficacy is required to ensure that energy resources available to public officials are utilized efficiently. That is effective risk management practices, effectiveness of internal audit, internal audit policies and standards compel public officials to optimize the usage of public resources.

Secondly, this paper is among the paucity of studies that examine the mediating role of sustainability audit on the relationship between internal audit efficacy and energy saving behavior. The paper has revealed sustainability audit significantly mediates the relationship between internal audit efficacy and sustainable energy saving behavior among public sector officials which consistent with prior related studies (Amoako et al., 2023; DeSimone et al., 2021; Fraser et al., 2020; Rosin et al., 2017; Shukla & Mattar, 2018). Sustainability audit encompasses the practices of ensuring organizations are meeting its governance responsibilities, managing its sustainability performance, complying with environmental regulations, and adhering to the organization’s sustainability policy Thus, the paper has established that sustainability audit can serve as a mechanism through which internal audit efficacy drives positive energy saving behavior. Finally, the third proposition is that sustainability audit relates to energy saving behavior in a number of ways including safeguarding public resources by adhere to environmental regulations and sustainability policies (Khan, 2019). The paper has revealed that sustainability audit significantly and positively relates to energy savings behavior. Sustainability audits conducted by internal auditors aim to ensure that the organization is meeting its governance responsibilities, managing its sustainability performance, complying with environmental regulations, and adhering to the organization’s sustainability policy (Darnall et al., 2009). Audits are an important part of ensuring that the information provided complies with financial and non-financial regulations and responsibilities (Khan, 2019; Nie et al., 2019; Van den Broek et al., 2019; Trotta, 2018; Wang et al., 2018). Therefore, sustainability audit is a determinant of energy savings behavior among public officials.

Conclusions, Implications, and Limitations

Conclusions

As part of the deliberate efforts by the successive governments in Ghana to combat high corruption menace, the Act, 2017 (Act 959) was enacted to investigate and prosecute specific cases of alleged or suspected corruption offenses, a decision which conforms to the United Nations Convention against Corruption, yet the actual impacts of these interventions are yet to be felt. It is against this backdrop that the current study was undertaking to analyze the implications of internal audit efficacy on energy saving behavior, and develop a baseline model to enhance energy saving behavior through sustainability audit. The paper has revealed that internal audit efficacy has significant effect on sustainability audit and energy saving behavior. The paper utilized a quantitative research approach and cross-sectional survey design to draw data from 405 public officials across different public sector agencies in Ghana. Variance-Based Structural Equation Modeling and SMART-PLS version 3.3.8 have been used to validate the hypotheses. Moreover, the paper has revealed sustainability audit significantly mediates the relationship between internal audit efficacy and sustainable energy saving behavior among public sector officials. In conclusion, internal audit efficacy contributes significantly to the sustainability audit and energy savings. Moreover, sustainability audit serves as a means through which internal audit efficacy enhances energy savings behavior in the public sector.

Theoretical and Practical Implications

Drawing on the contingency theory with variations the paper has newly developed model that could be used to enhance energy saving behavior in a country where such studies have been inadequately explored. The newly developed model has contextual and situational advantages over existing models which were predominantly developed to with a focus on the developed and high-income economics. This paper is among the paucity of studies that examined the mediating role of sustainability audit on the relationship between internal audit efficacy and energy saving behavior. The paper has highlighted the significance of corporate governance in the management of scarce pubic resources. The concept of sustainability audit generally ensures that the public agencies are meeting their governance responsibilities, managing its sustainability performance, complying with environmental regulations, and adhering to the organization’s sustainability policy. The paper has revealed that sustainability audit can serve as a mechanism through which internal audit efficacy drives positive energy saving behavior. Thus, sustainability audit relates to energy saving behavior in a number of ways including safeguarding public resources by adhere to environmental regulations and sustainability policies. These indicative results have implications on the newly developed model that could be used to enhance energy saving behavior low resources context. The results from the paper have implications on reaffirming the relevance of internal audit efficacy and sustainability audit in energy transition polices as well as the realization of sustainable development goals, particularly sustainable and clean energy (SDG7) and responsible consumption and production (SDG12).

Limitations and Suggestions for Future Studies

Since the current paper was conducted to analyze the implications of internal audit efficacy on energy usage behavior, and develop a baseline model to enhance sustainable energy saving behavior through sustainability audit with focus on public agencies in Ghana. The paper has some few limitations which should be given consideration by future researchers. These include; scope, research approach, and time horizon. The current paper focused broadly on the Ghanaian public sector using multiple agencies and units. It is suggested that future focus should be on selected few or comparative studies between two or more public agencies for example, judicial and police services. Moreover, the current study employed quantitative research approach meanwhile mixed method approach should have given participants the opportunity to share real experience in the subject. Therefore, future researchers are advised accordingly to consider mixed method design in future related studies. Furthermore, the current study employed a cross sectional design. It is suggested that longitudinal studies should be given consideration given the sensitivity nature of the topic. Future researchers should consider adopting Zhao (2010) paper to conduct mediation analysis. Last but not the least, it is suggested that future studies should incorporate energy justice into the sustainable energy consumption model.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Data would be made available upon request