Abstract

Despite its significance, the impact of capital adequacy on sustainable growth for banks has hardly been investigated. We examine the moderating role of capital adequacy on bank-specific characteristics of sustainable growth. This quantitative study is conducted for forty-seven listed commercial banks in Indonesia from 2013 to 2022. It is the first research on the moderating role of capital adequacy on determinants of sustainable growth for banks. The results substantiate the significant adverse influence of profitability, leverage, efficiency, and liquidity on sustainable growth, while a positive influence of lagged sustainable growth and asset efficiency. Contradicting effect of capital adequacy is observed. Capital adequacy moderates profitability, leverage, liquidity, and efficiency from negative to positive, however, it moderates asset efficiency from positive to negative. The limitation is that the study is only conducted for commercial banks in Indonesia, and it does not consider the core equity and non-core equity, bank ownership, mediators, and other moderators on sustainable growth. Future research to address the limitations with a distinct study on the moderating role of capital adequacy on determinants of sustainable growth for dividend-paying banks in ASEAN countries.

Plain language summary

The importance of capital adequacy on bank specific factors to sustainable growth in banks has never been studied, while conflicting results on positive and negative impact on high capital adequacy to profitability in banks. Also, there is no study on the effect of capital adequacy influencing bank specific characteristics on sustainable growth. Moreover, there is no study on determinants for sustainable growth of banks in Indonesia, despite it is crucial to understand the drivers for sustainable growth, especially in the post pandemic era when banks might have constraints to rely on additional new equity. This quantitative study is conducted for forty-seven listed commercial banks in Indonesia over the period of 2013–2022. Our study reveals the adverse influence of profitability, leverage, inefficiency, and liquidity on sustainable growth, while positive influence of lagged sustainable growth and asset efficiency. Contradicting effect of capital adequacy is observed. Capital adequacy moderates profitability, leverage, liquidity and inefficiency from negative to positive, and moderates asset efficiency from positive to negative. Limitation is that the study is only conducted for commercial banks in Indonesia, and it does not consider the core equity and non-core equity, bank ownership, mediators, and other moderators on sustainable growth. Future research to address the limitations with a distinct study on the moderating role of capital adequacy on determinants of sustainable growth for dividend-paying banks in ASEAN countries.

Introduction

With its vital role in the economy, central banks globally enforce capital adequacy regulations following Basel III guidelines (Gao et al., 2022). Greater capital level improves banks’ capacity in liquidity creation is more notable in small banks, and the bank capital role was crucial in the global financial crisis spanning from 2007 to 2009 (C. Zheng et al., 2019). Increased capital and liquidity slacks may serve as a double-edged sword, while enhancing stability, their impact on efficiency varies based on the bank’s existing efficiency level. As regulatory frameworks evolve, tailored approaches are essential to maintain a competitive and resilient banking sector (Bitar et al., 2018, 2020).

Bank supervisory performs bank assessment by relying on the CAMELS framework, which sparks the bank’s capital adequacy research. Banks in the Asia Pacific comparably have robust capital adequacy above 10% of risk-weighted assets (Kočenda & Iwasaki, 2021).Evaluating the adequacy of capital in Indonesian banks is fundamental for various reasons. First, capital is key to preserving financial stability and preventing bank failures, which can have widespread implications for the broader economy (Murtiyanti et al., 2015). Capital serves as a safeguard against unforeseen losses, aiding banks in managing the risks tied to their assets and liabilities, and both preventing and predicting any possible banks’ failures. (I. Ahmad, 2019; Gehrig, 1995; Group of Thirty, 2023; Rahman et al., 2020). In contrast, a non-risk weighted capital ratio similar to an adjusted leverage ratio is effective in bank distress prediction (Mayes & Stremmel, 2014), while either simple or complex capital ratios may serve as bank failure predictors (Estrella et al., 2000). On the other hand, an increase in the financial leverage increase might heighten the bank’s profit margin, as proposed by the agency cost theory, which indicates that debt financing enhances a firm’s profitability (Mehzabin et al., 2023). This is in line with the study of commercial banks in Indonesia with higher CAR would have a lower NIM and lower ROE, but not necessarily a lower ROA (Alwi et al., 2021).

Second, well-capitalized banks can better withstand negative effects from economic fluctuations, thereby stabilizing profitability, however, it diminishes returns on equity (ROE) and returns on assets (ROA) (Irawan & Anggono, 2015; Rosyid & Irawan Noor, 2018; Yahya & Setyono, 2024). Third, a robust capital adequacy ratio (CAR) would enhance investor confidence by demonstrating the bank’s capacity to endure financial disruptions and maintain seamless operations (Silaban, 2017). Fourth, banks as highly regulated industries, are required to comply with regulatory standards set by entities such as international requirements by Basel III (Le et al., 2020) and the Indonesian Financial Services Authority (IFSA) to guarantee that they possess enough capital to sustain their operations (Marlina, 2023).

McKinsey 2022 Global Banking Review report revealed that half of the world’s banks undervalued USD 2.2 trillion (below the 2008 global financial crisis, while another half (including Indonesian banks) had a high ROE (Dietz et al., 2022). The report also reported that the banking sector is no longer monolithic, which was also noted in Indonesia, and concluded that the divergence will become more pronounced. Following COVID-19 with an unattractive capital market to obtain external funding, the importance of internal funds to finance further growth is more apparent. This relates to the concept of sustainable growth, which was introduced by Higgins (1977) to enable banks to assess the capability of firms to internally grow without external new equity.

Sustainable growth was introduced by Higgins (1977) as the highest growth rate for firms to accomplish without any new equity financing while maintaining constant leverage. (Ashta, 2008; Fonseka et al., 2012; Higgins, 1977; Ross, 2022). Publications have shown that bank-specific characteristics such as profitability, retention, asset turnover, and leverage (PRAT) influence sustainable growth (Altahtamouni, 2023; Higgins, 1977; Vasiliou & Karkazis, 2002). Additionally, research on non-PRAT characteristics such as liquidity, asset quality, capital, and efficiency have produced inconsistent results on sustainable growth. Lastly, there is very limited research on sustainable growth for commercial banks in Indonesia the largest economy in Southeast Asia. (Junaidi et al., 2019; Pratama, 2019). Recent research on determinants of sustainable growth with a focus on lending growth in commercial banks in Indonesia demonstrated that bank performance (net profit margin), lending growth and lagged sustainable growth affect sustainable growth positively, while liquidity and efficiency negatively (Linggadjaya et al., 2025).

It is crucial to understand the determinants of sustainable growth in Indonesian banks. The sustainable growth of banks incorporates profitability, asset efficiency, leverage, and retention of earnings into one single measure upon which professionals could evaluate the banks’ realistic future growth plans (Mamilla, 2019). Sustainable growth reflects the maximum growth rate without additional new equity financing and maintaining its leverage (Ashta, 2008; Fonseka et al., 2012; Higgins, 1977; Ross, 2022). CAR signifies the proportion of risk-weighted assets—including credit risk, market risk, and operational risk —that are financed by the bank’s capital as opposed to external funding sources (Yahya & Setyono, 2024).Sufficient capital fosters public confidence by showcasing the bank’s ability to effectively manage potential risks linked to its activities (Yahya & Setyono, 2024).

A study on the determinants of sustainable growth in the Indonesian banking sector, with an emphasis on the impact of lending growth specifying a positive impact of lending growth and profitability on the sustainable growth of Indonesian banks. (Linggadjaya et al., 2025). Increased profitability reflects an institution’s ability to generate sufficient earnings to bolster its capital base, thereby establishing a robust foundation for sustainable growth. Strong capital positions enable banks to pursue aggressive expansion strategies, allocate resources to long-term, growth-oriented investments, and enhance their capacity to manage potential risks. (Altahtamouni et al., 2022; Amouzesh et al., 2011; Isnurhadi et al., 2022).

Previously, there were limited studies on the moderating role of CAR in the banking industry. First, a study on the moderating role of CAR on bank liquidity creation on failure risk in banks (C. Zheng et al., 2019). Contrary to the Basel III agreement, which encourages banks to bolster their minimum capital as a buffer for unexpected loss and reduce imprudent risk-taking. stricter capital requirement was proven to fail to increase bank profitability and efficiency. The role of capital in moderating the relationship between liquidity creation and failure risk reveals intriguing dynamics. When accounting for bank capital, liquidity creation is inversely related to failure risk. This inverse relationship is positively moderated by capital. This aligns with the perspective that banks may bolster their solvency by increasing capital in response to the illiquidity risks tied to liquidity creation, and higher capital improves banks’ capacity to generate liquidity. The significant negative effect is more pronounced in smaller banks, with the impact of capital being especially evident during the 2007 to 2009 financial crisis (C. Zheng et al., 2019).

On the contrary, negative two-way interrelationships between regulatory capital and liquidity creation were observed for all 558 commercial banks across 84 countries in 2011 to 2017, which supports the financial fragility-crowding out hypothesis (Yusgiantoro, 2019). This indicates that higher capital requirements can reduce liquidity creation and negatively impact bank profitability (Diamond & Rajan, 1999; Laeven et al., 2014; Mohanty & Mahakud, 2021). Research in emerging economies noted that banks with higher growth rates are susceptible to external shocks leading to financial fragility (Sun et al., 2024).

Second, a study on the moderating effect of capital positively moderates the relationship between loan growth and credit risk, supporting the regulatory hypothesis in banking (Abbas & Ali, 2021). A study on 217 Islamic banks from 38 countries from 2010 to 2019 revealed that a loan increase escalates the credit risk as evidenced by higher loan loss provisions, loan loss reserves, and nonperforming loans. Also, larger Islamic banks exhibited a stronger impact of capital than their medium and smaller counterparts.

Maintaining increased capital levels comes at a cost, often exceeding that of debt, which erodes profitability. Banks may levy higher margins to offset the financial burden associated with sustaining requisite capital levels (Cruz-García & Fernández de Guevara, 2020), and on the other hand, stricter capitalization correlates with reduced credit supply (Gropp et al., 2019). An increase in capital requirements reduces the growth rate in loans by 4.6 times in the United Kingdom context (Aiyar et al., 2016).

While there is an increased capital threshold for banks dictated by Basel III, and the crucial importance of capital adequacy and sustainable growth, there is no study on the moderating effect of capital adequacy on bank-specific characteristics of sustainable growth. Previous research on the moderating role of capital adequacy on profitability concluded that while capital adequacy does not have any direct effect on profitability, however positively moderates the relationships between the profitability of Islamic banks (Yahya & Setyono, 2024).

This study examines the ability of capital adequacy as a moderating variable and concludes the evidence for bank-specific characteristics to sustainable growth. Leveraging data spanning the period 2013 to 2022 empassing 47 listed Indonesian commercial banks, we employ GMM to analyze the relationship. The capital adequacy ratio exhibits a positive correlation with banks’ risk-taking behavior, however, CAR is inversely related to efficiency (Das & Rout, 2020). Research on the impact of liquidity risk on profitability with CAR as a moderating factor remains limited (Meliza et al., 2024). This study thus contributes additional references to the moderating role of CAR on bank-specific characteristics of sustainable growth. As of December 31, 2022, the total number of commercial banks in Indonesia has reached one hundred and six banks, forty-seven of which are listed in the Indonesia Stock Exchange.

This research consists of five sections. The introduction initially provides clarity on the research’s purpose and foundation, previous studies, research gap, research objectives, a brief outline of the study, and its systematic layout. Following this, it presents a theoretical backdrop to develop an empirical research model and the variables involved in constructing the model. To address the research questions, hypotheses will be put forth and examined in the following chapters. The third section, the research methodology, outlines the research type, samples, variables definitions and measurements, and statistical analysis instruments. The fourth section, results displays the statistical test and results. Finally, the conclusion section encapsulates findings, limitations, and future research suggestions.

Literature Review

The sustainable growth theory has existed since 1977 by Higgins as the highest growth rate without any additional equity financing (Ashta, 2008; Fonseka et al., 2012; Higgins, 1977; Ross, 2022). The integration of operating and financial metrics in sustainable growth is important as it has the potential to augment the firm value (Amouzesh et al., 2011; Higgins, 1977).

Impact of Profitability on Sustainable Growth

The capacity for internal financing is closely connected to the firm profitability (Damodaran, 2015). Net interest margin (NIM) is the primary determinant of bank profitability, whilst banks also must manage credit risk as the highest proportion of risks in banks in Indonesia, liquidity risk to manage cash flow in changing economic conditions, and funding risk to obtain funds in the highest efficiency. (Guzel, 2021). NIM represents the intermediation efficiency of a bank (Almarzoqi & Naceur, 2015). The interaction of funding and lending is reflected in NIM, which becomes the primary determinant of banks’ profitability. NIM in banks in Indonesia represents the highest in the Asia Pacific region which competition level in the Indonesian banking industry should be increased to minimize NIM (Nugroho et al., 2022).

Competition in the banking industry will affect banks’ liquidity creation and effect banks to escalate deposit rates to attract funding and decrease lending rates to encourage lending, which decreases NIM (Kinini et al., 2023). Low NIM might represent the competitiveness of the banking industry. With higher funding costs, the bank has constraints in providing loans with competitive lending rates compared to its competitors. The funding quality which represents the cost of funds significantly affects NIM. (Yiqiang Jin, 2019).

Substantial positive correlation between profitability and sustainable growth rate (Altahtamouni et al., 2022; M. Zheng & Escalante, 2020). Linggadjaya et al. (2024) show that bank-specific characteristics influence profitability (return on assets) with a greater influence for banks with a small ROA and less influence for banks with a large ROA. As the return on assets escalates, the influence intensifies, exhibiting a negative influence on credit risk and efficiency, with a positive influence on asset efficiency.

Impact of Leverage on Sustainable Growth

Leverage, a metric gauging the balance between debt and equity in financing a bank’s assets plays a pivotal role. A debt increase may increase the firm performance, although it is followed by the increased cost of debt (Ross, 2022). The pecking order theory elucidates the rationale behind a firm’s preference for internal financing, specifically retained earnings. The optimal debt-to-equity ratio has the lowest point beyond which the cost of capital begins to increase. Any leverage increase will improve bank performance, however, above a certain threshold, profitability will deteriorate (Modigliani & Miller, 1958). Empirical evidence of the nonlinear and dual-sided relationship between capital and profitability is shown. (Nsanyan Sandow et al., 2021). Lestari (2021) found that leverage positively affected ROA and negatively affected ROE.The relationship between leverage and profitability is U-shaped inverted (Vukovic & Tica, 2022). On the other hand, Al-Homaidi et al. (2018) and Almaqtari et al. (2019) concluded that leverage negatively affected ROA. Towards sustainable growth, leverage has a significant negative relationship (Akhtar et al., 2022; Mamilla, 2019).

Impact of Asset Efficiency on Sustainable Growth

Asset efficiency evaluates how a bank invests in its assets to produce operating revenue efficiently. A higher asset efficiency ratio will entail a higher bank’s profitability (Al-Homaidi et al., 2018; Altahtamouni et al., 2022; Chowdhury & Rasid, 2016; Manaf et al., 2018; Mukherjee & Sen, 2017; Quoc Trung, 2021). Asset efficiency is the most significant driver for sustainable growth positively (Altahtamouni et al., 2022). Asset efficiency positively affects sustainable growth (Isnurhadi et al., 2022; M. Zheng & Escalante, 2020), however, an insignificant impact of asset efficiency on sustainable growth is observed (Osazefua Imhanzenobe, 2020; Vukovic & Tica, 2022).

Impact of Efficiency on Sustainable Growth

Efficiency will affect the bank’s performance. The previous studies concluded that operating efficiency (efficiency) is the most significant predictor of banks’ long-term viability (Ghosh & Sanyal, 2019). According to Shah et al. (2019), sustainable banks are efficient and productive in their daily operations. Operating expenses in the banking industry are comparable high due to tight compliance with regulatory standards (Shah et al., 2019). Efficiency emerges as the most vital element for sustainability (Olmo & Azofra, 2021).

Banks that are less efficient with high funding costs will need to increase their lending rate, however, they must exercise caution to preserve loan portfolio quality and credit risk. During the COVID-19 crisis, efficient banks are more resilient (Mateev et al., 2022). Cost efficiency exerts a greater positive influence on profitability when banks assume increased risk and encounter heightened competition (Fang et al., 2019). The reforms in bank operations will determine the efficiency and effectiveness of serving its customers (Bhullar & Tandon, 2019). Benefits from advancement in digital technology could be reaped by establishing long-term strategies with novelty, innovation, and better value for customers (Acciarini et al., 2021; Na et al., 2022; Sia et al., 2021; Tutak & Brodny, 2022).

Impact of Size on Sustainable Growth

The scale of a bank is indicative of its profit-generating capacity. Banks of a larger scale have the advantage of a larger customer base, larger-scale economies, and diversification, contributing to reduced funding costs and increased profits. A positive effect of size on profitability (Bougatef, 2017; Chowdhury & Rasid, 2016). This is affirmed by Wang et al. (2019), Xu and Wang (2018). Bitar et al. (2020) found that smaller banks benefit more from increased capital and liquidity. During the financial crisis, well-capitalized and liquid banks demonstrated superior efficiency in conventional banks but inconclusive for Islamic banks. For Turkish banks, higher capital levels affect liquidity creation differently for small banks and large banks since the higher capital increases the liquidity creation for small banks and vice versa (Danisman, 2018).

On the contrary, Huang et al. (2019) found a significantly negative relationship, suggesting that larger firms tend to have lower sustainable growth. An expansion in bank size results in elevated costs, thereby establishing a negative relationship between profitability and size (Singh & Sharma, 2016). Size impact positively on sustainable growth (Ramli et al., 2022; M. Zheng & Escalante, 2020). On the other hand, size does not demonstrate any significant impact on sustainable growth (Z. Ahmad et al., 2017).

Impact of Liquidity on Sustainable Growth

Basel III regulations have focused on the requirements of capital and liquidity (Adelopo et al., 2022). The COVID-19 pandemic revealed systemic risks, particularly in banks with high leverage and weak capital, hence most Indonesian banks maintained adequate liquidity (Meliza et al., 2024). The definition of liquidity risk is the risk that a bank is unable to increase its funds in assets or liabilities with the lowest cost (Eltweri et al., 2024; Nikolaou, 2021; Ruozi & Ferrari, 2013). Liquidity risk in banks can arise when there is an over-withdrawal of funds from the institution (Saleh & Abu Afifa, 2020).

Lim and Rokhim (2020) discovered a robust and affirmative effect of liquidity on sustainable growth rate. N. Tran et al. (2018) and Yusuf et al. (2019) point out that profitability and growth heavily depend on liquidity, however, profitable firms are not always liquid. A significant negative effect of liquidity is demonstrated on sustainable growth (Junaidi et al., 2019; Kessy et al., 2021; Pratama, 2019). On the contrary, liquidity has no significant impact on sustainable growth while credit risk and capital adequacy ratios do (Akhtar et al., 2022). On the contrary, liquidity has no impact on sustainable growth (Z. Ahmad et al., 2017).

Impact of Credit Risk on Sustainable Growth

Banks should be prudent in only accepting loan portfolios which commensurate with their risk. Bad-quality assets will put the loan portfolios into bad debt (Kessy et al., 2021). Credit risk has a negative significant impact on sustainable growth (Akhtar et al., 2022). Loan loss provisions (LLPs) represent the highest individual accrual in banks (Beatty & Liao, 2014), which represents a cushion to absorb predicted losses on loan portfolios (Ozili & Outa, 2017; Peterson & Arun, 2018). LLP also serves as an indicator of anticipated loan losses (Ng et al., 2020).

LLPs pose a conundrum for equity investors to ensure the true value of provisions (Wahlen, 1994). A reduction in the subsequent periods will offset an inflated LLP in a period. Banks may modify their LLPs to surge their capital (Moyer, 1990). LLP is demonstrated used to smoothen its earnings management (Ahmed et al., 1999; Kanagaretnam et al., 2004). Delaying LLP and increased lending to reduce NP is observed (Kozak, 2021) while additional LLP is provided during economic uncertainty (Ozili, 2019).

Moderating Impact of Capital Adequacy on Sustainable Growth

Capital structure refers to the mix of debt and equity (Modigliani & Miller, 1958). The trade-off theory suggests an optimal level of capital structure exists with the lowest cost of capital (Luigi & Sorin, 2009; Mao, 2003). Debt financing enhances a firm’s profitability, partly due to the tax shield, and reduces agency conflicts and agency costs between managers and shareholders (Jensen & Meckling, 1976). This is in contrast with banks having high leverage (DeAngelo & Stulz, 2013). Following worldwide central banks impose capital adequacy requirements to have sufficient capital to back up their activities (Gao et al., 2022). While sustainable growth is more aligned with pecking order theory, choosing internally generated funds compared to debt and new equity, minimizes the risks associated with external financing (Myers, 1984). Banks with higher capital would have a better ability to create liquidity in the bank, known as the risk absorption hypothesis (Distinguin et al., 2013).

Maintaining a higher capital margin necessitates costs that surpass the amounts owed by clients, leading to a decline in bank profitability. This is because increased capital requirements can elevate funding costs and reduce liquidity creation, which in turn lowers lending and investment activities, ultimately impacting profitability negatively. A higher capital ratio will crowd out deposits is advocated with the hypothesis of crowding out deposit (Berger & Bouwman, 2009).

A capital increase may serve as a stronger motivation for banks to exert greater effort, resulting in increased lending activities and the generation of liquidity (Donaldson et al., 2018). Increased capitalization will result in greater income and reduced costs (Iannotta et al., 2007; Islam & Nishiyama, 2016). Capital adequacy determines a bank’s sustainable growth rate because asset expansion requires internal and external capital funding (Junaidi et al., 2019). While increased capital allows banks to compete for deposits and loans, it will subject them to diminished performance (Boubaker et al., 2023). On the contrary, other studies reveal different results. In line with asset growth, the bank should diligently implement a growth strategy that aligns with capital adequacy (Isnurhadi et al., 2022).

Impact of the Previous Year’s Sustainable Growth on Sustainable Growth

Previous empirical studies show that lagged profitability has a positive relationship with profitability. (Al-Homaidi et al., 2020; Bolarinwa et al., 2021; Chowdhury & Rasid, 2016; Dang & Huynh, 2022; Horobet et al., 2021; Jallow, 2022; Jumono et al., 2019; Rahman et al., 2020). This aligns with the anticipation that banks are likely to uphold elevated profitability levels from the previous period into the imminent period

Research Method

Data Samples

The population of this research consists of 106 commercial banks in Indonesia by the end of 2022. It utilizes unbalanced annual panel data from commercial banks in Indonesia spanning from 2013 to 2022 to encompass all information within the unit of analysis to prevent information loss. The study used the financial year 2013 as the starting year post-financial crisis of 2008, and the financial year 2022 to present the latest available financial data. Secondary data was used from the Indonesia Stock Exchange, audited financial statements, and annual reports of the respective banks.

Since sustainable growth rate measurement required retention of earnings information, which was only available annually in listed commercial banks, the study could only be conducted for the entire listed commercial banks. The listed commercial banks in Indonesia which reached forty-seven banks were selected with a total of three hundred ninety-nine observations. In terms of the number of banks, listed commercial banks account for 44% of commercial banks; while their total assets, total loans and net income reached 87%, 88%, and 95% of commercial banks.

Variables Measurements

There are 9 main variables in this study. Seven variables are independent variables of bank-specific characteristics, one is a moderator, and one is a dependent variable. Macroeconomic factors as control variables, such as GDP growth, interest rate, and Herfindahl-Hirschman index (HHI). The conceptual framework of this study is presented in Figure 1. The variable, proxy, references, and formulation of all variables are presented in Table 1.

Conceptual framework.

Variables and Dimension Measurement Formulation.

Research Methodology

This study used panel data regression to evaluate the hypotheses. To determine the best model, the non-autocorrelation assumption test was conducted using the Breusch-Godfrey/Wooldridge test, with a non-significant result (p-value more than .05) to confirm non-autocorrelation (Godfrey, 1996). The homoscedasticity test was conducted using the Breusch-Pagan test with a non-significant result (p-value more than .05) to confirm that the model was free from heteroscedasticity. The Durbin-Wu-Hausmann test was used to evaluate endogeneity. A significant test result (p-value less than .05) showed the existence of endogeneity in the model. To address the potential bias, the possibility of cross-sectional heteroscedasticity, autocorrelation, and endogeneity, this study uses the generalized method of moments (GMM) (Baltagi et al., 2007; Dietrich & Wanzenried, 2011).

GMM method effectively managed individual-specific effects, alleviated unobserved heterogeneity concerns, rectified the biases stemming from omitted variables, and eliminated any correlation between the error term and independent variables (Arellano & Bond, 1991; Arellano & Bover, 1995). Additional tests were conducted. First, serial correlation in the error terms was evaluated. The null hypothesis, indicating no serial correlation in the error terms should not be rejected.. Therefore the expected result is non-significant (p-value more than .05) (Baltagi, 2013). Second, the Sargan (1958) test assessed the validity of the instruments or overidentifying restrictions. Rejection of the null hypothesis suggested that overidentifying restrictions are invalid, with an anticipated result of non-significant result (p-value more than .05). When both tests supported the null hypothesis, the First-differences GMM (FD-GMM) was utilized; otherwise, the system GMM (SYS-GMM) model was employed. The developed conceptual model was illustrated in the following equations:

where β = coefficient; t = time (year); i = bank; ε = the error term; C = vector of control variables.

A sustainable growth rate is obtained from return on equity multiplied by retention policy. There is much research on bank performance and dividend policy employing GMM. Lagged bank performance positively affects its current year bank performance (Al-Homaidi et al., 2020; Bolarinwa et al., 2021; Chowdhury & Rasid, 2016; Dang, 2019; Gao et al., 2022; Gupta & Mahakud, 2020; Hanzlík & Teplý, 2022; Mubeen et al., 2021; Oino, 2021; Rakshit & Bardhan, 2022; Saleh & Abu Afifa, 2020; Yao, 2018). Lagged dividends positively affect its current-year dividend (G. C. Hartono & Utami, 2016; P. G. Hartono & Robiyanto, 2023; P. G. Hartono et al., 2023; Linggadjaya & Atahau, 2023; Santosa et al., 2023; Tinungki, Hartono, et al., 2022; Tinungki, Robiyanto, & Hartono, 2022). While there is no previous research on SGR using GMM that SGR encompasses profitability and dividend components, which favor GMM as the optimal analytical tool.

Moderating Effect

This study integrates capital adequacy as a moderation variable into the model as presented in Figure 2. The models include interaction terms, computed by multiplying the standardized value of the coefficient of the moderator variable with the standardized value of the coefficient for each variable in bank-specific characteristics, which allows for a test of the moderating role of capital adequacy. This moderation test is also expected to find out how and moderation type.

Moderator effect.

With the moderating variable CAR, the developed conceptual model was illustrated in the following equations:

where β = coefficient; t = time (year); i = bank; ε = the error term; C = vector of control variables.

Robustness Checking

To evaluate the panel regression model and the relationship between variables, a robustness check will be conducted. This method aims to evaluate the extent of changes in the estimated regression coefficient when there are changes in model specifications. Subsequently, a comparison of the coefficient estimation will be conducted (Lu & White, 2014). To perform the robustness test, this research will also study the sub-sample groups with two distinct sampling groups, such as banks that distributed dividends at least once during the research period as dividend-paying banks (DPB) and banks that had not distributed dividends were non-dividend-paying (NDPB). NBPD will have its SGR equal to its ROE since the return on equity will be reinvested fully in the bank. On the other hand, DPB will have its SGR as a fraction of ROE, depending on the plowback ratio being the multiplier.

Empirical Findings and Discussion

Descriptive Statistics

This section reports the descriptive statistics and the results of our research. Table 2 presents the descriptive statistics for the banks. To ensure the result robustness and reduce the outliers effect, a 1% winsorization was conducted on the unbalanced 399 observations from 2013 to 2022. As shown, SGR varies from −68.96% to 22.07% with an average of 1.86% while its standard deviation is quite high at 14.20%. Also shown, NIM varies from 0.24% to 16.05% with an average of 4.89% while its standard deviation is 2.44%. A huge disparity in leverage existed with a minimum of 31.46% to a maximum of 1,475.96% while the average is 587.58% with a standard deviation of 293.74%.

Descriptive Statistics (n = 399).

The Pearson correlation was used to evaluate the relationship between the explanatory and dependent variables as shown in Table 3. The results showed a significant positive correlation between bank performance to sustainable growth at a 1% significance level. However, a negative correlation between efficiency and loan quality with sustainable growth was also observed at the 1% significance level. Leverage and capital were found to have insignificant correlations with sustainable growth. The multicollinearity test was assessed using the VIF, which showed that VIF values ranged from 1.067 (liquidity) to 4.787 (profitability), suggesting no multicollinearity as all values were below 5.

Bivariate Correlation Results and Variance Inflation Factors.

p = .10. **p = .05. ***p = .01.

Table 4 presents the panel unit test results for all variables. The study conducted Augmented Dickey-Fuller (ADF). It is found that each variable in the study is stationary at a level with all variables rejecting the unit-roots hypothesis at 5% significance levels.

Results of Unit-Root Tests.

p < 1%.

The Herfindahl-Hirschman Index (HHI) is closely linked to the concentration ratio. (Chunikhin et al., 2019). Aliev (2017) asserts that HHI is the preferred metric for assessing market concentration in the banking industry. HHI is obtained by squaring each bank’s market share and adding the squared market share. The market share percentage is counted as a whole number and the resulting HHI will range from close to 0 to 100. As seen in Table 5 below, HHI in the Indonesian banking industry exhibits consistent growth over time. An elevated Herfindahl-Hirschman Index (HHI) signifies a higher degree of market concentration, indicating that fewer firms dominate a substantial portion of the market. This often correlates with reduced competitive dynamics and higher market shares fostering less competition.

Herfindahl-Hirschman Index (n = 47).

Dynamic Panel Model

The Breusch-Pagan test yielded a test statistic of 720.83 with a p-value of less than .01, indicating the presence of heteroscedasticity. Similarly, the Breusch-Godfrey/Wooldridge test confirmed the presence of autocorrelation, with a test statistic of 47.292 and p-values below .01. Furthermore, the Durbin-Wu-Hausman test identified endogeneity, producing a χ2 value of 3,326.4 with p-values below .05. These findings strongly advocate for the dynamic panel model (GMM) in this research. This study uses the dynamic first-difference generalized method of moments (FD-GMM). The findings are delineated in Table 6.

Results of Dynamic Panel.

The estimations presented in Table 6 demonstrate consistent coefficients. The Wald chi-square test validates the model’s fit, the Sargan test finds no signs of overidentification restrictions, and the first-order and second-order tests of autocorrelations are negative. The GMM estimations are robust and the standard errors are unbiased. Hence, the results could be reliably determined. Bank-specific characteristics that significantly affect sustainable growth are profitability, leverage, asset efficiency, efficiency, and liquidity.

A negative effect of profitability on sustainable growth is demonstrated. The sustainable growth rate rises as the net interest margin declines. Net interest margin (NIM) only represents the gross profit margin for banks. Several factors may contribute to this negative effect of net interest margin to sustainable growth, such as credit cost (loan loss provision expense), and efficiency, hence while the NIM is high, the retained profit is low, resulting in low SGR. Generally, banks generate higher NIM through consumer loans which requires higher underwriting and collection costs to serve the consumer loans. This is contrary to the study of Puspitasari et al. (2021) that effective management of NIM enhances net income, which leads to a corresponding rise in ROA. Nurwulandari et al. (2022) demonstrating that NIM exhibited a positive, and significant impact on ROA. Conversely, the operating expense ratio demonstrated a negative and significant influence on ROA. This study also demonstrates a positive effect of previous sustainable growth on sustainable growth. However, there is no previous research on sustainable growth using GMM.

Leverage has a significant negative effect on sustainable growth, as also demonstrated by Akhtar et al. (2022), Fonseka et al. (2012), Mamilla (2019). While a positive effect on asset efficiency on sustainable growth is demonstrated. While this is aligned with the effect of asset efficiency on profitability (Al-Homaidi et al., 2018; Altahtamouni et al., 2022; Chowdhury & Rasid, 2016; Manaf et al., 2018; Mukherjee & Sen, 2017; Quoc Trung, 2021), the result is in contrary with the insignificant impact of asset efficiency on sustainable growth (Osazefua Imhanzenobe, 2020; Vukovic & Tica, 2022).

Efficiency is negatively correlated with sustainable growth, and this aligns with the study of Fang et al. (2019), Junaidi et al. (2019), Kessy et al. (2021), Mateev et al. (2022), Rakshit and Bardhan (2022). Similarly, liquidity has a substantial negative effect on sustainable growth and this is consistent with the study of Chen et al. (2018), Junaidi et al. (2019), Kessy et al. (2021), Pratama (2019). The negative relationship is observed between liquidity risk and profitability (Abdelaziz et al., 2022; Duho et al., 2020; Hacini et al., 2021). In contrary with a positive relationship (Ebenezer et al., 2019; Huong et al., 2021; Meliza et al., 2024).

Size does not demonstrate any significant effect on sustainable growth. This is inconsistent in that size has a negative effect on sustainable growth (Huang et al., 2019; Vukovic & Tica, 2022). Similarly, credit risk does not have any significant effect on sustainable growth, which is contrary with Akhtar et al. (2022) with a negative significant impact of credit risk on sustainable growth. The insignificant credit risk on sustainable growth might have been attributed to the government policy intervention issued by the Indonesian Financial Services Authority to undermine the negative impact of COVID-19 (Linggadjaya et al., 2025).

Moderating Effect

Interesting observations in the moderating role of capital adequacy of bank-specific variables on sustainable growth are noted. The reversal of direction is demonstrated as CAR moderates. CAR moderates positively profitability, leverage, efficiency, and liquidity to sustainable growth, while negatively moderating asset efficiency. Insignificant coefficients are shown in size and credit risk. The type of moderator for all those significant moderating variables acts as pure moderators with the insignificant effects of CAR on sustainable growth. Pure moderation in regression models with moderation effects occurs when the moderation variable does not have a significant effect on the dependent variable directly, but the moderator variable affects the strength and/or direction of the relationship between an independent variable and the dependent variable (Sharma et al., 1981).

On profitability, the positive moderating effect is demonstrated. Banks with high capital adequacy ratios would attract funding at lower costs and have access to more funding sources. With lower funding costs, banks could attract and offer loans to good quality debtors with more competitive lending rates, positively moderating sustainable growth. This is aligned with the study of Indonesian banks with high CAR generally have high NIM and vice versa (Nugroho et al., 2022).

On leverage, the positive moderating effect is also demonstrated. Banks with a high capital adequacy would rely less on debt financing resulting in a lower debt-to-equity ratio. Banks with lower DER would be able to obtain additional financing and invest in growth opportunities having a higher SGR.

On asset efficiency, banks with better capital adequacy will have more capacity to invest in assets to improve asset efficiency, however, capital adequacy requirements may impose restrictions on the bank lending practices, increased capital requirements, and limitations on any expansion activities for the bank. Banks may subsequently be required to allocate resources towards regulatory requirements resulting in a lower sustainable growth rate. Furthermore, on efficiency, banks with stronger capital adequacy have the financial capability to invest in process improvement activities such as technology advancement and employee training, hence it will contribute to sustainable growth positively.

On liquidity, banks with higher capital adequacy will be in a better position to access sources of funding favorably in terms of amount and rates, hence it will improve sustainable growth. Table 7 demonstrates the moderating effect of CAR between bank-specific characteristics to sustainable growth.

Moderating Effect.

Robustness Analysis

Dividend-Paying Banks Versus Non-Dividend-Paying Banks

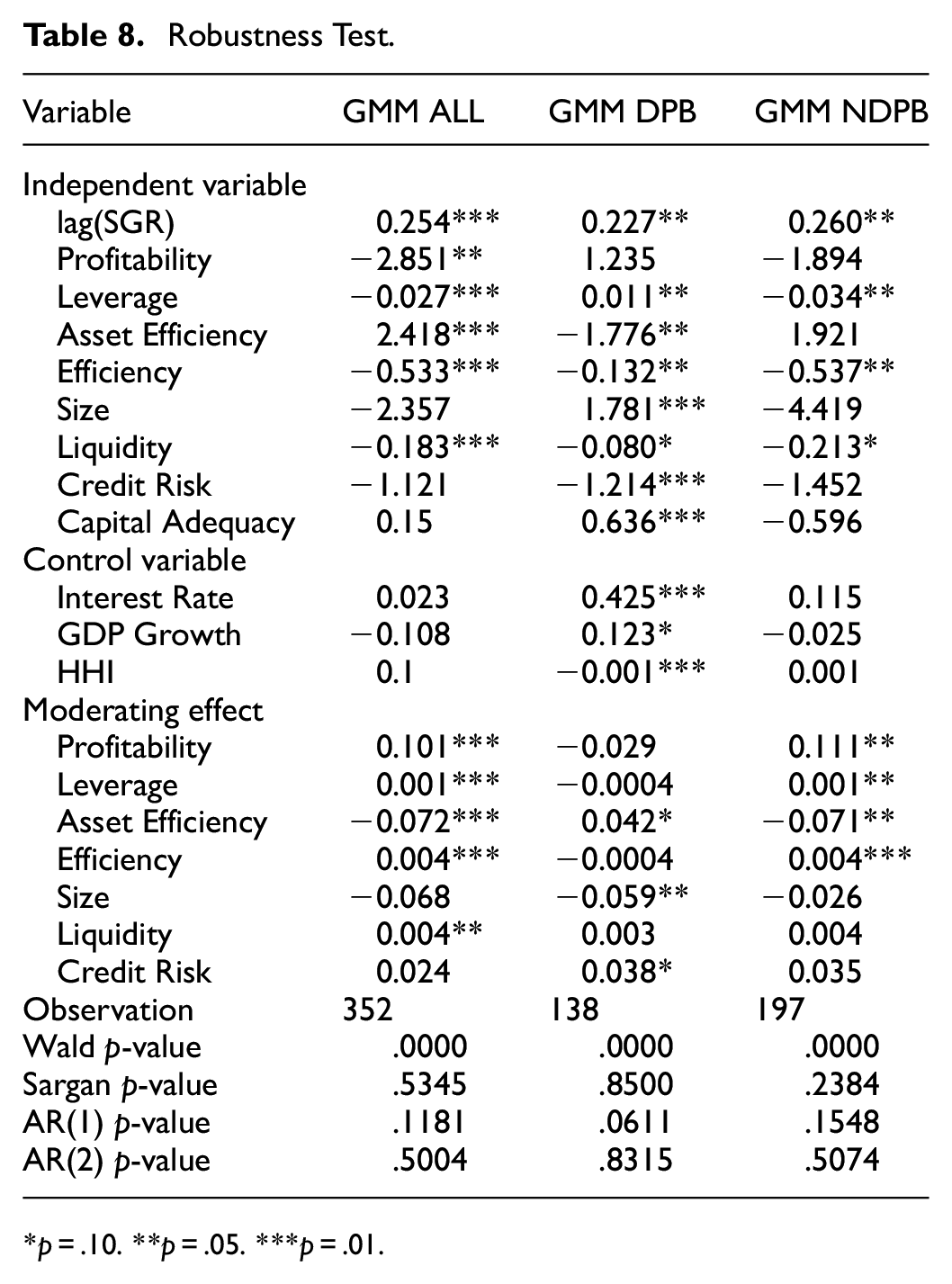

The non-dividend-paying bank will have its SGR equal to its ROE since the return on equity will be reinvested fully in the bank. On the other hand, the dividend-paying banks will have their SGR as a fraction of ROE, depending on the plowback ratio being the multiplier. Banks distribute dividends at least once during the research period which is called dividend-paying-banks. The banks that have not distributed any dividends are called non-dividend-paying banks. According to study of D. V. Tran (2021), heightened market discipline would be a result of paying dividends. As a result, banks will demonstrate decreased risk-taking behaviors. This aligns with the dividend-stability theory. This also aligns with the study of Fu and Blazenko (2015) that although the equity returns of both dividend-paying and non-dividend-paying firms demonstrated no unconditional differences in returns, non-dividend-paying firms exhibited high-risk characteristics due to their financial distress (Fu & Blazenko, 2015). Consequently, the study will also study the sub-sample groups with two distinct sampling groups, which are dividend-paying banks and non-dividend-paying banks. The results are presented in Table 8.

Robustness Test.

p = .10. **p = .05. ***p = .01.

In general, the model exhibits consistent coefficients. The Wald chi-square test validates the model’s fit, and the Sargan test provides no signs of overidentification restrictions. The full-sample analysis of all banks reveals that lagged sustainable growth positively affects the sustainable growth for all sub-samples. Contrary to previous research, this study shows a negative influence from profitability to sustainable growth. Adegbie and Dada (2019), Altahtamouni et al. (2022), Mukherjee (2018), Mukherjee and Sen (2018), Vasiliou & Karkazis (2002), M. Zheng & Escalante (2020) have proven otherwise.

Profitability has a negative effect on sustainable growth for all banks with insignificant positive for DPB and insignificant negative for NDPB. DPB usually has a higher profitability (net interest margin) since it generates a higher excess of interest income over interest expense compared to NDPB. Leverage has a negative effect on sustainable growth for all banks, positive for DPB and negative for NDPB. This study affirms the conflicting effect of leverage on sustainable growth, the positive effect (Mukherjee & Sen, 2017, 2018; Rahim, 2017) and negative effect (Akhtar et al., 2022; Fonseka et al., 2012; Mamilla, 2019). All banks are highly leveraged institutions and rely on leverage strategies to foster growth. The conflicting coefficient might arise due to customers’ preference in putting their funds into DPB. With higher customer funds, DPB has comparably higher leverage than NDPB. Consequently, the effect of leverage would be significantly positive on sustainable growth, while NDPB and all banks demonstrate a significant negative relationship.

Asset efficiency has a positive effect on sustainable growth for all banks, a negative for DPB, and insignificant for NDPB on sustainable growth. The negative CAR moderation for DPB could be understood. Good quality debtors will demand lower interest rates which DPB could afford due to its lower funding cost. Consequently, the asset efficiency (operating income to average total asset) of DPB will be lower. This is in line with the study of Altahtamouni et al. (2022), Isnurhadi et al. (2022), M. Zheng and Escalante (2020). Asset efficiency does not show any effect on sustainable growth for NDPB. Insignificant effect is concluded (Osazefua Imhanzenobe, 2020; Vukovic & Tica, 2022).

Efficiency has a negative effect on sustainable growth for all banks. This aligns with the study of Junaidi et al. (2019), Kessy et al. (2021), Ramli et al. (2022). On the same note, credit risk has a negative effect on sustainable growth for NDPB. This aligns with the study of Adegbie and Dada (2019), Aziz et al. (2018), Isnurhadi et al. (2022), Junaidi et al. (2019), Kessy et al. (2021). While it does not have any significant moderating effect on credit risk for DPB and all banks. On the contrary, size has a positive effect on sustainable growth for DPB, while insignificant for NDPB and all banks. Liquidity has a negative effect on sustainable growth for all sub-sample analyses. This aligns with the study of (Adegbie & Dada, 2019; Isnurhadi et al., 2022; Junaidi et al., 2019; Kessy et al., 2021; Pratama, 2019; M. Zheng & Escalante, 2020).

Capital adequacy has a positive effect on sustainable growth for DPB, while insignificant for NDPB and all banks. Since DPB distributes dividends in line with their net income generation capability. Partly would be distributed and the remaining as retained earnings and would be accumulated as total capital. Consequently, a positive effect is for DPB.

On the other hand, NDPB’s accumulated retained earnings might not be as robust as DPB’s, hence its direction is in contrary. As control variables, both interest rate and GDP demonstrate a positive effect on sustainable growth for DPB while HHI demonstrates a negative effect. No significant effect on interest rate, GDP growth, and HHI to NDPB and all banks.

Moderating Effect on Dividend-Paying Banks and Non-Dividend-Paying Banks

This study also provides the moderating effect of capital adequacy for DPB and NDPB from 2013 to 2022. Intriguing conclusions on moderating CAR impact of bank-specific variables on SGR for DPB and NDPB. Capital adequacy moderates positively on profitability, leverage, and efficiency on sustainable growth for NDPB and all banks, but not for DPB. Hence, capital adequacy is a significant factor for NDPB to increase its capability to generate profit, and attract higher leverage but increase its efficiency. On the other hand, higher capital adequacy moderates positively asset efficiency for DPB, but moderates negatively for NDPB dan all banks. Higher capital adequacy negatively moderates the size of sustainable growth for DPB, which is consistent with the study of Huang et al. (2019) while not for NDPB and all banks. Higher capital adequacy positively moderates credit risk for NDPB, but not for DPB and all banks.

This study reveals the different moderating effects of capital adequacy on DPB and NDPB. This confirms the previous research that there is a need for tailored regulatory approaches, given the diverse impact on banks of varying sizes (Le et al., 2020) and that Basel III has a negative effect on the efficiency and profitability of highly liquid banks (Le et al., 2020). The role of capital adequacy ratio as a moderating variable to sustainable growth functions differently on different types of banks. For non-dividend paying banks, capital adequacy is significant to enhance the banks’ ability to generate profitability and attract higher leverage despite increased efficiency and lower asset efficiency. For dividend-paying banks, higher capital adequacy positively enhances their asset efficiency, negatively moderates size, and increases credit risk on sustainable growth,

Conclusions

The empirical study suggests a negative impact of profitability, leverage, efficiency, and liquidity on sustainable growth moderated by capital adequacy, while a positive impact is driven by asset efficiency and lagged sustainable growth. This partly confirms the previous research on sustainable growth in Indonesia (only two studies so far). It is the first research on the moderating role of capital adequacy on bank-specific characteristics of sustainable growth. The results confirm the significant negative impact of profitability, leverage, efficiency, and liquidity on sustainable growth, while the positive impact of lagged sustainable growth and asset efficiency.

While there is no direct effect of capital adequacy on sustainable growth, the interaction between capital adequacy with profitability, leverage, efficiency, and liquidity results in a significant positive impact on sustainable growth. This suggests that banks with higher capital adequacy enhance the effect of profitability, leverage, efficiency, and liquidity on sustainable growth. Conversely, the interaction between capital adequacy and asset efficiency exhibits a significantly negative impact on sustainable growth, indicating that an increased CAR diminishes the relationship between asset efficiency and sustainable growth. Meanwhile, banks with lower capital adequacy decrease the effect of profitability, leverage, efficiency, and liquidity on sustainable growth, and on the other hand, banks with lower capital adequacy increase the effect of asset efficiency on sustainable growth.

In the robustness test using dividend-paying banks and non-dividend-paying banks, a similar moderator contradicting effect is observed, as it positively moderates profitability, leverage, and efficiency, and negatively moderates asset efficiency in non-dividend-paying banks. In contrast, capital adequacy positively moderates asset efficiency in dividend-paying banks.

Capital adequacy influences bank-specific characteristics on sustainable growth. Acting as a buffer against potential losses, adequate capital reduces the likelihood of bank failures (C. Zheng et al., 2019). This strengthened concept is in line with the Modigliani-Miller theorem, which posits that higher capital levels can lower agency costs and enhance financial stability and that shareholders prefer dividends over profit to reduce agency cost (Jensen & Meckling, 1976).

The moderating effect of capital adequacy is quite significant for managerial implications and theoretical implications. For managerial implications, the significant pure moderation effect of capital adequacy on profitability, leverage, asset efficiency, efficiency, and liquidity emphasizes the crucial of maintaining heightened capital adequacy to mitigate any risks related to these variables. Consequently, a risk appetite statement and strategic planning need to consider the improvement of the capital positions. It is not a mere regulatory exercise, although having robust capital adequacy would be beneficial for the bank’s positioning from the point of view of regulators, both home and host regulators for foreign-owned banks and investors.

For theoretical implications, the results confirm the moderating role of capital adequacy. Previous studies only had limited evaluation of the moderating effect of capital adequacy, as it demonstrated the positive moderating effect of capital adequacy on liquidity risks (Meliza et al., 2024), while liquidity risk is affected by external factors such as economic slowdown, financial troubles, and currency depreciation, as a significant threat to bank profitability (Yumaita et al., 2022). Another study demonstrated that robust capital supports long-term liquidity stability which positively impacts bank profitability as it enhances a bank’s capacity to navigate future conditions that may affect its profitability (Yusgiantoro, 2019).

Capital adequacy positively affects sustainable growth for dividend-paying banks, while insignificant for non-dividend-paying banks and all banks. Since dividend-paying banks distribute dividends in line with their net income generation capability, hence a positive significant effect is for dividend-paying banks. On the other hand, non-dividend-paying banks may choose to reinvest their earnings into the business instead of sharing them with shareholders. Consequently, capital adequacy does not have a significant effect on non-dividend-paying banks. The limitation is that the study does not take into account the core equity and non-core equity, bank ownership, mediators, and other moderators on sustainable growth. Future research is recommended for a distinct study on the moderating role of capital adequacy on bank-specific characteristics to sustainable growth by dividend-paying banks in ASEAN countries.

Footnotes

ORCID iDs

Author Contributions

Conceptualization: R.I.T.L., A.D.R.A., G.S.S.U., K.S.S.; methodology: R.I.T.L., A.D.R.A., G.S.S.U., K.S.S.; software: R.I.T.L.; validation: R.I.T.L., A.D.R.A., G.S.S.U., K.S.S.; format analysis: R.I.T.L., A.D.R.A., G.S.S.U., K.S.S.; investigation: R.I.T.L., A.D.R.A., G.S.S.U., K.S.S.; resources: R.I.T.L., A.D.R.A., G.S.S.U., K.S.S.; data curation: R.I.T.L., A.D.R.A., G.S.S.U., K.S.S.; writing—original draft preparation: R.I.T.L.; project administration: R.I.T.L.; funding acquisition: R.I.T.L.; writing—review and editing: R.I.T.L., A.D.R.A., G.S.S.U., K.S.S. All the authors have thoroughly perused and assented to the final version of the manuscript that has been made available for publication.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The corresponding author could be contacted for datasets and analysis.

Human and Animal Welfare Statement

The authors state that the study does not involve humans or animals. It is a purely quantitative study using secondary data.