Abstract

This study analysed the influence of income growth, energy use, and consumption of renewable energy on carbon dioxide emissions in the selected 24 OECD countries. Using balanced panel data from 1990 to 2016, the study examined the relationship of income, energy use, and consumption of renewable energy with CO2 emissions. To address the issue of cross-sectional dependence stemming from unobserved common factors, given the trading relationships among these countries, we employed the cross-sectionally augmented ARDL (CS-ARDL) and cross-sectionally augmented Distributed Lag (CS-DL) models to investigate the linkages among the above variables. The study revealed a positive correlation between energy use and CO2 emissions, and a negative correlation between renewable energy consumption and CO2 emissions. However, the study found no evidence to support the Environmental Kuznets curve hypothesis. Energy use and renewable energy consumption were also found to be causally linked to CO2 emissions based on the Dumitrescu-Hurlin non-Granger causality test. However, the inverted U-shaped relationship of income growth with CO2 emissions does not exist in the sampled OECD countries. Therefore, it is not advisable for these OECD countries to be dependent on income growth for environmental sustainability. Rather, these OECD countries need to directly cut down CO2 emissions through the use of clean and renewable energy sources, decreasing non-renewable energy use. Moreover, considering the Jevons’ Paradox and the ‘rebound effects’ of energy efficiency gains that may increase overall energy consumption, a comprehensive approach combining energy efficiency and renewable energy integration is essential for mitigating CO2 emissions and promoting environmental sustainability in these OECD countries.

Plain language summary

The study revealed a positive correlation between energy use and CO2 emissions, and a negative correlation between renewable energy consumption and CO2 emissions. However, the study found no evidence to support the Environmental Kuznets curve hypothesis. Energy use and renewable energy consumption were also found to be causally linked to CO2 emissions based on the Dumitrescu-Hurlin non-Granger causality test. However, the inverted U-shaped relationship of income growth with CO2 emissions does not exist in the sampled OECD countries. Therefore, it is not advisable for these OECD countries to be dependent on income growth for environmental sustainability. Rather, these OECD countries need to directly cut down CO2 emissions through the use of clean and renewable energy sources, decreasing non-renewable energy use. Moreover, considering the Jevons Paradox and the ‘rebound effects’ of energy efficiency gains that may increase overall energy consumption, a comprehensive approach combining energy efficiency and renewable energy integration is essential for mitigating CO2 emissions and promoting environmental sustainability in these OECD countries.

Keywords

Introduction

Around the world, pollution in all its forms, primarily driven by human economic activities, jeopardises sustainable economic growth, particularly in developing countries where agriculture chiefly relies on rainfall due to an increase in infrequent and insufficient rainfall. The rising level of major global pollutants, including CO2 emissions, a significant component of Greenhouse Gases (GHG), is likely to increasingly disrupt climatic conditions, with a significant adverse impact on food production and, thus, food security.

The idea that a higher level of economic development will increase environmental awareness and control helps to explain this shift in the income-environmental link in the later stage of development. Increased environmental protection spending will also make renewable energy and the adoption of clean technology more readily available. Additionally, economies evolve, transitioning from less polluting rural and primitive industrial economies to comparatively cleaner service economies (Arrow et al., 1995; Panayotou, 1993). In light of this, it is predicted that this will result in less environmental deterioration at a later stage of economic development.

The theory of the Environmental Kuznets Curve (EKC) provides a theoretical underpinning to investigate the relationship between economic growth and environmental degradation. The EKC concept aroused the interest of several researchers worldwide. It predicts that the relationship between a country’s economic development and environmental degradation is in the shape of an inverted U. This gives people optimism and faith that the declining environmental quality will stabilise and start to improve after economic development reaches a certain level.

As a result, there exists a sound theoretical support in favour of the inverted U-shaped correlation between economic progress and environmental quality. Both structural and behavioural elements may be involved in this relationship. The level of economic activity, the distribution of output across sectors, and technological advancements are examples of structural variables, whereas an example of a behavioural force (Grossman & Krueger, 1995; Kaufmann et al., 1998; Panayotou, 1993) is the income elasticity of demand for environmental quality. Consumers are likely to pay more for better environmental quality (Lekakis & Kousis, 2001; McConnell, 1997; Roca, 2003). As income rises, so does this desire. Transnational trade patterns, the migration of industrial activities, demographic considerations, and the distribution of family income are other factors that are believed to be implicated in this association (Heerink et al., 2001; Heil & Selden, 2001; Magnani, 2000; Shi, 2003).

The EKC theory inspires hope that economic progress and prosperity will continue sustainably after a slow climb and the attainment of a peak in environmental deterioration. Put another way, it assumes that having more money will inevitably lead to pressure to stop environmental damage. This appears improbable in light of the growing evidence of global warming, climate change, and the accompanying adverse economic consequences for the entire world community.

Numerous works of literature have endorsed the EKC theory (Apergis, 2016; Awaworyi Churchill et al., 2018; Bilgili et al., 2016; Chen, Wang, & Zhong, 2019; Dogan & Seker, 2016; Dong, Hochman et al., 2018; Lau et al., 2019; Shafiei & Salim, 2014; Sharif et al., 2019; Sinha & Shahbaz, 2018; Yao et al., 2019). Inglesi-Lotz & Dogan, 2018; Liu et al., 2017; Mikayilov et al., 2018; Vo et al., 2020; Zhang & Liu, 2019; Zoundi, 2017)

However, several other studies have found no evidence to support the EKC theory. Similarly, the conflicting findings on the connection between CO2 emissions and renewable energy consumption are also found in another body of literature. A number of studies (Allard et al., 2018; Alvarez-Herranz et al., 2017; Anwar et al., 2021; Balsalobre-Lorente et al., 2018; Ben Jebli et al., 2020; Bilgili et al., 2016; Cai et al., 2018; Dogan & Seker, 2016; Dong, Sun et al., 2018; Inglesi-Lotz & Dogan, 2018; Liu et al., 2017; Ma et al., 2021; Shafiei & Salim, 2014; Sinha & Shahbaz, 2018; Vo et al., 2020; Yang et al., 2021; Yao et al., 2019; Zoundi, 2017) support a negative relationship between renewable energy consumption and emissions. However, some studies have also found either no relationship or a positive relationship between the use of renewable energy and CO2 emissions (Apergis et al., 2010; Menyah & Wolde-Rufael, 2010). Rising economic activity and the utilisation of fossil fuels for energy consumption have been the main causes for the one-and-a-half-fold increase in greenhouse gas (GHG) emissions since 1990 (OECD, 2023).

Numerous studies have attempted to test the validity of the EKC theory predicting an inverted U-shaped connection between environmental deterioration and economic growth, using a range of data analytic methodologies. Most of them, however, are methodologically weak, particularly the studies whose analysis is based on panel data, and which typically do not deal with the issue of cross-sectional dependence. The parameter estimations become inconsistent when cross-sectional units are cross-sectionally dependent (Chudik & Pesaran, 2015; Ditzen, 2021). For calculated parameters to be consistent and dependable, cross-sectional dependence between panel data units must be taken into consideration.

The OECD countries have made little progress in reducing emissions, and due to the recent surge in energy use, GHG emissions are projected to rise further (OECD, 2023). According to the OECD data, 29% of all the GHG emissions in OECD countries are produced by the energy sector, with 24% coming from the transportation sector, 13% from manufacturing, 9% from agriculture, and 25% from other sectors. Despite the general consensus that the use and consumption of fossil fuels is the main source of CO2 emissions, a number of prior studies have found that renewable energy sources generate less emissions than fossil fuels (Ahmed et al., 2017; Petinrin & Shaaban, 2015; Rana et al., 2016). One of the crucial factors driving the expansion of renewable energy sources is the need to increase energy production and consumption while preserving the environment. Renewable energy systems are typically thought to be less polluting than fossil fuels at the moment of use (Liu et al., 2017), despite the fact that they may have major environmental impacts at other phases of the system’s life cycle (Quek et al., 2018). The United Nations’ inclusion of affordable and clean energy as the seventh of its 17 Sustainable Development Goals underlines the important role of clean or green energy and renewable energy consumption in the sustainable development of all nations, including those in the OECD, as indicated by GHG emissions per capita indicate the relative contribution to global greenhouse gas emissions. OECD nations emit significantly more CO2 per person than the majority of other global regions. In 2019, the average CO2 emissions per person in OECD nations were 8.3 tonnes, whereas the global average was 4.4 tonnes (OECD, 2023). The sampled OECD countries are also high-income countries that are suitable for investigating the validity of the EKC hypothesis.

Because of their interconnected trade links, it is anticipated that the panel data on sampled OECD countries are likely to be cross-sectionally dependent. Therefore, it is essential to test and address the issue of cross-sectional dependency brought on by unobserved common factors to ensure the statistical validity of the estimated parameters of the model.

Examining how the use of energy, income growth and the consumption of renewable energy affect carbon dioxide emissions and their consequences for environmental sustainability in OECD countries is the main objective of this research. This study also considers the problem of cross-sectional dependency in the data set by choosing and applying a suitable econometric model to analyse the influence of energy use, income growth, and renewable energy consumption on carbon dioxide emissions.

Theoretical Underpinnings

The connection between energy use, economic growth, renewable energy, and emissions has been thoroughly studied in environmental economics, energy policy, and sustainability research. The following is a list of key theoretical concepts and frameworks that explain these processes:

The EKC Theory

The EKC theory postulates, especially in the context of CO2 emissions, that there is an inverse U-shaped linkage between the level of income and environmental degradation in a country. According to this theory, in the early phase of economic development, industrialisation raises CO2 emissions by increasing energy consumption, which is frequently sourced from fossil fuels. However, as an economy matures, technological advancements, structural shifts, and increased environmental awareness lead to a greater adoption of renewable energy, resulting in reduced emissions (Grossman & Krueger, 1995; Stern, 2004).

Energy Ladder Theory

This theory suggests that energy consumption transitions as societies develop. Lower-income populations rely on traditional biomass (e.g., wood and charcoal), which emits lower CO2 per capita but is less efficient in terms of energy use. As incomes rise, households and industries increasingly adopt fossil fuels, leading to higher CO2 emissions. With higher incomes and technological advancements, societies shift towards cleaner, renewable energy sources in later stages, leading to lower emissions (Hosier & Dowd, 1987).

Decoupling Theory

The decoupling theory focuses on the potential to separate economic growth from environmental degradation. It distinguishes the concept of relative decoupling from absolute decoupling. According to the theory of relative decoupling, CO2 emissions increase more slowly than economic production because renewable energy sources and energy efficiency improvements are not being adopted as quickly. The absolute decoupling theory states that economic growth can occur while total CO2 emissions decline. Often, this is accomplished by incorporating extensive renewable energy sources.

Energy Transition Theory

This theory focuses on the transition from fossil fuel-reliant energy systems to renewable energy systems for lowering CO2 emissions. The transition is driven by technological innovation (e.g., advancements in solar, wind, and storage technologies). policy interventions (e.g., carbon pricing, subsidies for renewables) and social and market dynamics that favour cleaner energy sources (Smil, 2016).

Carbon Lock-In Theory

This theory explains how dependence on fossil fuel-based energy systems creates path dependencies, delaying the adoption of renewable energy and perpetuating high CO2 emissions. Key mechanisms include infrastructure investments favouring fossil fuels, the fossil fuel industry’s political and economic power, and social inertia in energy consumption habits (Unruh, 2000).

Porter’s Hypothesis

This hypothesis suggests that stringent environmental regulations, such as promoting renewable energy, can stimulate innovation and efficiency, leading to reductions in CO2 emissions without hindering economic growth (Porter & Linde, 1995).

Rebound Effect Theory

This theory highlights how improvements in energy efficiency or the adoption of renewables may not lead to proportional reductions in CO2 emissions due to increased consumption resulting from cost savings (direct rebound) and indirect economic effects that stimulate growth and energy use (Sorrell, 2007).

Structural Change Theory

This theory explains how transitions from energy-intensive sectors (e.g., manufacturing) to service-oriented economies can lead to reduced CO2 emissions. Renewable energy adoption accelerates this decoupling process by providing cleaner energy alternatives (Antweiler et al., 2001).

These theories provide a comprehensive framework for understanding the interaction among energy consumption, renewable energy adoption, and emissions.

Literature Review

This section examines the previous empirical research to test the economic hypotheses, its history and justification. Finally, the results of major empirical investigations are presented in tabular form.

Kuznets (1955) hypothesised a relationship between economic development and inequality. Kuznets’ theory states that economic inequality increases in the initial stage of economic development, reaches a peak, and thereafter starts to decline as the economy develops, resulting in an inverted U-shaped relationship between economic development and inequality, known as the Kuznets curve.

Grossman and Krueger (1991) adopted the concept of the Kuznets curve in their study to examine the environmental impact of the North American Free Trade Agreement (NAFTA). During their background research for the World Development Report, they again emphasised the EKC theory as described in Shafik and Bandyopadhya (1992).

The EKC theory explains that as wealth increases due to growing economic activity, it generates and raises the demand for improved environmental quality, encouraging investment, development, and the adoption of better technologies to enhance environmental quality. In most countries, accumulating wealth is the most efficient way to improve the environment, while economic growth frequently causes deterioration in the environment in the early stages of development (Beckerman, 1992). Studies on testing the EKC hypothesis have found evidence to support an inverted U-shaped association between environmental deterioration and income (Grossman & Krueger, 1991, 1995).

Mirza and Kanwal (2017), using the ARDL technique and cointegration analysis, found a two-way causality among energy consumption, income, and CO2 emissions. Stern (1998) examined the knowledge development regarding the EKC and addressed the various critiques levied at some empirical findings and their justifications in the policy literature.

Using the GMM technique, a panel data analysis of 14 Asian countries from 1990 to 2011 revealed evidence supporting the EKC theory (Apergis & Ozturk, 2015). According to their study, CO2 emissions and income have an inverted U-shaped relationship and hence supported the EKC theory. (Ben Jebli et al., 2016) examined the relationship between GDP and per capita CO2 emissions for a panel of 25 OECD countries from 1980 to 2010. They applied both FMOLS and DOLS estimators. Their study also validated the EKC hypothesis for the OECD.

In an analysis of the impact of GDP, renewable energy, and fossil fuels on CO2 emissions in 11 U.S. states using annual data from 1980 to 2015, the EKC hypothesis was shown to be valid only in Illinois, Michigan, Florida, New York, and Ohio (Işık et al., 2019). Furthermore, this study found that fossil fuel consumption in Texas had a negative correlation with CO2 emissions, whereas energy use in Florida had a positive correlation.

Economic growth, energy consumption, and CO2 emissions are all interconnected, and both aspects contribute to the country’s rising CO2 emissions, according a study on Pakistan (Khan & Ozturk, 2020).

The EKC theory was tested in 12 selected East African countries for the period 1990 to 2013 (Demissew Beyene & Kotosz, 2020). The EKC theory was supported by the study’s findings, based on the data analysis using the pooled mean group (PMG) technique.

An overview of previous empirical studies on OECD and other nations is given in the table below. Using panel and time series data analysis, this study examined the relationships among income, energy use, consumption of renewable energy, and emissions (Table 1).

Empirical Studies on CO2 Emissions and their Findings.

Source. The authors.

Most of the prior research has shown that the relationship between GDP per capita and emissions is represented by an inverted U-shaped curve. The bulk of studies on this linkage carried out in OECD countries also corroborate the EKC theory. Previous empirical research has shown that using renewable energy lowers CO2 emissions while using non-renewable energy raises them. However, the literature reviews cited above suggest that there are few studies on OECD countries examining the impact of renewable energy use on carbon dioxide emissions. Additionally, not many studies on OECD countries use a model that quantifies the influence of renewable energy sources and takes cross-sectional dependence into consideration.

The Cross-Sectionally Augmented Autoregressive Distributed Lag (CS-ARDL) model and the Cross-Sectionally Augmented Distributed Lag (CS-DL) model are two sophisticated econometric models chosen and estimated in this work to account for diverse dynamics and coefficients across units. These models are built to tackle the dynamic misspecifications and residual serial correlation. This study also examines the effects of the consumption of renewable energy, alongside income and energy use, after controlling for cross-sectional dependence in the OECD countries being studied.

Data and Model Specification

Since data on energy use and renewable energy consumption are available until 2016, we used a balanced panel of annual data of the 24 OECD countries over the period 1990 to 2016. The dependent variable is the log of CO2 emissions per person. The explanatory variables are the log of real GDP per capita, the square of the log of real GDP per capita, the log of energy use per capita, and the log of renewable energy consumption per capita. The data on the above variables were compiled from the World Bank’s database on the World Development Indicators available on its website (www.worldbank.org).

The descriptions of the variables considered for the analysis are given below (Table 2).

Variables Description.

Source. The authors.

We estimate the following basic long-term relationships:

Where

Due to trade links among the studied countries and resulting unobserved common factors giving rise to the likely problem of cross-sectional dependence, we adopt the CS-ARDL (Chudik & Pesaran, 2015) and CS-DL (Chudik et al., 2016) estimate methods. Dahmani et al. (2023), Namahoro et al. (2021), Okumus et al. (2021), and Sohail et al. (2023) have also used these models in their studies.

We anticipate that the four explanatory variables’ coefficients in the equation above will have the following signs:

The EKC hypothesis will be valid if

Results and Discussion

Cross-Sectional Dependence Test

Firstly, we ascertain whether the variables are cross-sectionally dependent. Following Pesaran (2015), we apply the CD test to check weak cross-sectional dependence in the panel data set. The test’s null hypothesis is that the variable is weakly cross-sectionally dependent. Below are the CD test results (Table 3).

Cross-Sectional Dependence Exponent (Alpha) Estimation and Test.

Source. The authors.

Significant at 1%.

The null hypothesis that each variable has a weak cross-sectional dependency is rejected by the CD test. The estimated values of the cross-sectional dependence exponent (alpha) above 0.5 and about 1 imply strong cross-sectional dependence. Hence, we must choose and apply an estimation method that controls for the issue of the dataset’s cross-sectional dependence. The Common Correlated Effects approaches seek to remove cross-sectional dependence by including cross-sectional averages in the model. The cross-sectional averages are partially separated using this method. To address cross-sectional dependence, we lag each variable and then add the cross-sectional averages of the bases of all variables.

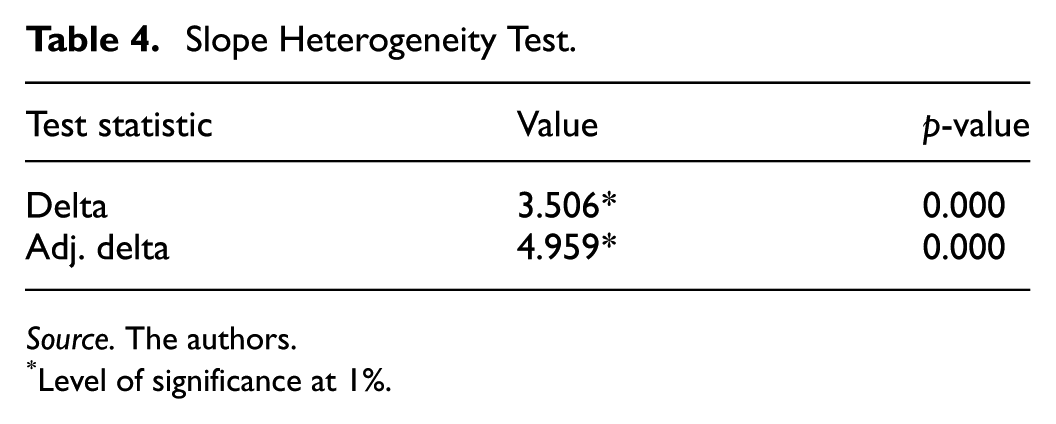

Slope Heterogeneity Test

The panel data could be either homogeneous or heterogeneous. The choice of regression technique depends on whether the panel is homogeneous or heterogeneous. We apply the test for slope heterogeneity to ascertain whether the panel is homogeneous or heterogeneous. The p-values for both the delta and adjusted delta test statistics are significant at the 1% level. Thus, the test rejects the null hypothesis that the slopes are homogeneous and concludes that they are heterogeneous across the cross-sectional units (Table 4).

Slope Heterogeneity Test.

Source. The authors.

Level of significance at 1%.

Panel Unit Root Tests

Cross-sectional dependence among variables is confirmed, and the slope heterogeneity test indicates that the panel is also heterogeneous. The CIPS unit root tests (Pesaran, 2007) are considered to be appropriate for examining cross-sectional dependence in these circumstances. The null hypothesis of the CIPS test is that a variable is homogeneous and non-stationary, while the alternative hypothesis is heterogeneous and stationary.

The Cross-sectionally Augmented Dickey-Fuller (CADF) test (Pesaran, 2007) is another unit root test considered appropriate for variables showing cross-sectional dependence. It was also developed for the panel unit root test. The CADF test employs a t-test in the heterogeneous panels. The CADF test assumes that a variable is non-stationary under the null hypothesis. To remove the influence of cross-sectional dependence, the Dickey-Fuller or Augmented Dickey-Fuller regressions are supplemented by the cross-sectional averages of the lagged levels and the initial differences of individual variables.

The following table presents the results of the second-generation panel unit root test. As per the results of the CIPS and CADF tests, y, y2, eu, and re are I(1), whereas co2 is I(0). These variables have a heterogeneous order of integration (Table 5).

Panel Unit Root Test.

Source. The authors.

Note. For both CIPS and CADF tests, the 1% critical value is −2.30, and the 5% critical value is −2.15. In each case, models with individual-specific intercepts are applied.

Level of significance at 1%.

Test of Cointegration

We choose to apply the second-generation cointegration test (Westerlund, 2007) to deal with the problem of cross-sectional dependence in the variables. We use this cointegration test on the variables to check if the panel variables exhibit a long-run relationship and error correction. The test employs four different statistics: Gt, Ga, Pt, and Pa, under the null that there is no cointegration. In light of the Gt and Ga test results, the rejection of H0 is regarded as evidence of cointegration for at least one of the cross-sectional units. However, the rejection of H0 by the Pt and Pa test statistics is interpreted as evidence of cointegration or a long-run relationship among the variables.

The Z-values of the four test statistics (Gt, Ga, Pt, and Pa) are significant at the 1% and 5% levels, respectively. These test statistics reject the null hypothesis of no cointegration among the variables. We therefore conclude that the variables are cointegrated (Table 6).

The Westerlund Panel Cointegration Test.

Source. The authors.

Note. The significance levels at 1%, 5%, and 10% are indicated by the symbols *, **, and ***, respectively.

Therefore, the Westerlund cointegration test unanimously confirms that all five variables, co2, y, y2, eu, and re, are cointegrated. That is, there is a long-run relationship between them.

CS-ARDL and CS-DL Models

These models use contemporary econometric techniques to estimate long-term correlations in panel data, taking heterogeneity between cross-sectional units (e.g., countries, enterprises) and cross-sectional dependence into consideration.

When cross-sectional dependence is unobservable across cross-sectional units, it is incorporated into the error term. In such cases, it is modelled as a common factor. When explanatory variables are associated with the unobserved common factors, then omitted variable bias may result from omitting these factors (Ditzen, 2021). In this situation, the OLS estimator is inconsistent, and the OLS residuals are not independent and identically distributed (iid) (Everaert & De Groote, 2016). Under such conditions, the Common Correlated Effects estimator accurately estimates the long-run coefficients by approximating the unobservable common factors with the addition of cross-sectional averages (Chudik & Pesaran, 2015; Pesaran, 2006).

Considering cross-sectional dependency, dynamics, and the heterogeneity slope, we estimate the linkages between the dependent variable, co2, and the regressors, y, y2, eu, and re, using the CS-ARDL and CS-DL approaches. Next, the residuals are analysed to determine whether a significant cross-sectional dependence exists. We accomplish this by employing the CD test and approximating the cross-sectional dependence exponent.

We assume that the dependent variable is expressed by the following ARDL (py, px) specification:

Where

The vector of long-run coefficients is given by

CS-ARDL Approach

With the addition of cross-sectional averages of the dependent and independent variables, CS-ARDL expands on the traditional ARDL model to take into consideration unobserved common factors that might affect all panel units. Commonly associated effects are controlled for. Heterogeneous dynamics and coefficients across units are permitted. When the panel displays cointegration and unit roots, this approach is appropriate.

The CS-ARDL model is expressed as follows when a general ARDL (Py, Px) model is used, adding lagged values of the cross-sectional averages of the dependent and independent variables to account for cross-sectional dependence:

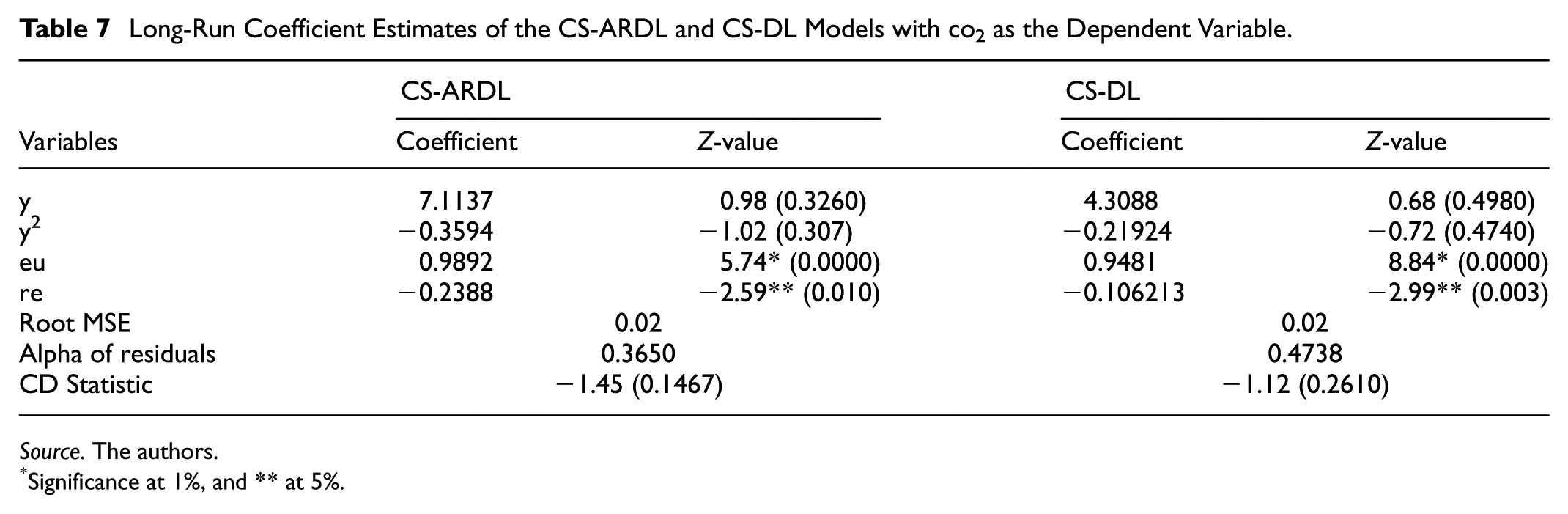

For estimating Equation 3, we use the ARDL (1,1,1,1,1) model, with co2 as the dependent variable and y, y2, eu and re as regressors.

The CS-ARDL regression results are given in Table 7. The adjustment coefficient has a value of −0.93836, which is high and significant. Around 94% of the deviation from the long-run relationship is reduced in a year, suggesting that the long-term relationship is restored quickly. The long-run coefficient of y is 7.11379, while that of y2 is −0.35941. None of these figures is significant at 5%. The long-run values of the coefficients, 0.98929 for eu and −0.23882 for re, are statistically significant at the 1% and 5% levels, respectively. The partial adjustment coefficients have a mean group estimate of −0.93836. According to Table 7, this suggests that around 94% of the disequilibrium is corrected annually.

Long-Run Coefficient Estimates of the CS-ARDL and CS-DL Models with co2 as the Dependent Variable.

Source. The authors.

Significance at 1%, and ** at 5%.

The above test statistics do not support an inverted U-shaped curvilinear relationship between y and CO2. Consequently, the CS-ARDL model results do not support the EKC hypothesis for the OECD countries. Nonetheless, there is evidence to support energy use-driven environmental deterioration and environmental sustainability driven by renewable energy consumption.

CS-DL Approach

CS-DL is a simplification and alternative to CS-ARDL when short-run dynamics are less of a focus. This model directly estimates long-run coefficients using the variables’ distributed lags and their cross-sectional averages. It focuses on the long-run effects directly. It is simpler and more robust in small samples or when the data are highly cross-sectionally dependent. However, the model is less flexible in modelling short-run dynamics than CS-ARDL. The CS-DL estimators exhibit remarkable resilience against misspecifications of dynamics and residual serial correlation. Particularly when T is small, the CS-DL approach’s performance frequently outperforms the alternative panel CS-ARDL estimates (Chudik et al., 2016).

Accounting for cross-sectional dependence, a general ARDL (Py, Px) model including lagged values of the cross-sectional averages of the dependent and independent variables, the corresponding CS-DL model is specified as follows:

Where,

Neither y nor y2 has a long-term effect on CO2, as their respective coefficients of 6.94142 and −0.32697 are not significant at either the 1% or 5% level. However, the values of long-run coefficients 0.85398 of eu and −0.1966 of re are significant at the 1% and 5% levels, respectively (Table 7).

We again conclude that there is no inverted U-shaped linkage between CO2 emissions and GDP per capita since the coefficients of y and y2 are not significant. Thus, the CS-DL model’s results also do not provide any evidence to support the EKC hypothesis. However, we find evidence to support both energy use-led environmental degradation and renewable energy consumption-led reduction in emissions, contributing to environmental sustainability.

The results of the CS-DL and CS-ARDL models are robust, as in both cases, the signs of the long-run coefficients of y, y2, eu, and re are as expected.

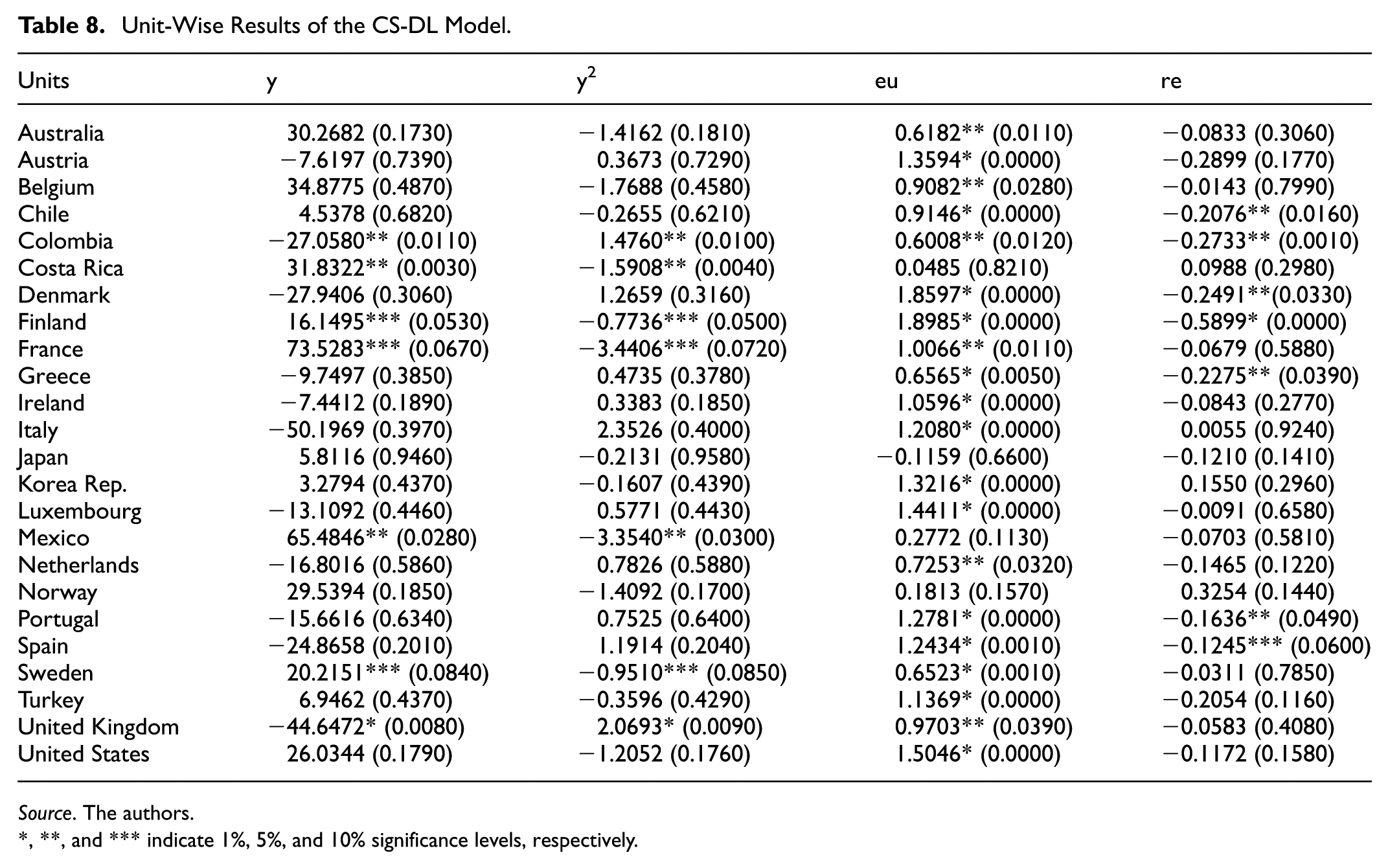

The table below reports the cross-sectional unit-level findings derived from the CS-DL approach. Out of the 24 countries in the sample, only five countries—Costa Rica, Finland, France, Mexico, and Sweden—have results that support the EKC hypothesis. Belgium, Chile, Australia, Austria, Finland, France, Greece, Colombia, Denmark, Ireland, Italy, the Republic of Korea, Spain, Sweden, Turkey, Luxembourg, the Netherlands, Portugal, the United Kingdom, and the United States are among the 20 nations where energy usage is a contributing factor to CO2 emissions. Increases in the consumption of renewable energy decrease CO2 emissions in Chile, Colombia, Denmark, Finland, Greece, Portugal, and Spain. Finland is the only country in the sample where both the EKC hypothesis is valid, as well as the growth in the consumption of renewable energy reduces CO2 emissions (Table 8).

Unit-Wise Results of the CS-DL Model.

Source. The authors.

, **, and *** indicate 1%, 5%, and 10% significance levels, respectively.

Dumitrescu & Hurlin (D-H) Granger Non-Causality Test

In view of the heterogeneous panels, we used the Granger non-causality test to check for causality from the explanatory variables to the dependent variable following Dumitrescu and Hurlin (2012). A bootstrap process with 700 replications was used to generate the Z-bar values and corresponding p-values. When variables exhibit cross-sectional dependence, the technique of bootstrapping is helpful.

The null hypothesis of the D-H Granger non-causation tests is that there is no Granger causality from one variable to another. The D-H test does not reject the null hypothesis that there is Granger non-causality, either from y to co2 or from co2 to y. The tests also do not reject the null hypothesis of Granger non-causality from y2 to co2 or from co2 to y2. However, the tests reject the Granger non-causality from eu to co2, but do not reject it from co2 to eu. Likewise, the tests do not reject the Granger non-causality from co2 to re, but they reject it from re to co2. Consequently, neither y to co2 nor y2 to co2 exhibits Granger causality. Granger causation between eu and co2 and re and co2 is unidirectional (Table 9).

Granger Non-Causality Test of Dumitrescu & Hurlin.

Source. The Authors.

Note.p-Values were computed using 700 bootstrap replications.

Level of significance at 1%, ** at 5%, and *** at 10%.

Surprisingly, our panel data analysis, after adjusting cross-sectional dependence, does not support the EKC theory for the sampled 24 OECD countries, in contrast to the majority of empirical findings (Alam, 2024; Awaworyi Churchill et al., 2018; Ben Jebli et al., 2016; Galeotti et al., 2006; Moomaw & Unruh, 1997) which support the EKC hypothesis based on panel data from OECD countries. For OECD nations, our results accord with (Dijkgraaf & Vollebergh, 2005). It is notable that, like us, cross-sectional dependence was also controlled in (Dijkgraaf & Vollebergh, 2005), whereas other studies have overlooked it. However, this study supports the energy use-led environmental degradation and renewable energy-led environmental sustainability hypotheses, as also supported by previous studies (Alvarez-Herranz et al., 2017; Bilgili et al., 2016; Shafiei & Salim, 2014) for OECD countries.

Energy efficiency and a decrease in CO2 emissions could result from the transition from non-renewable to renewable energy sources. However, (Jevons, 1866) describes a paradoxical phenomenon in which improvements in energy efficiency may lead to an overall increase in energy consumption rather than a decrease and, therefore, a rise in CO2 emissions. This paradox can indeed be applied to explain why developed countries may not experience the significant reduction in CO2 emissions that is expected, despite energy efficiency advances and the integration of renewable energy sources.

Energy efficiency gains may result in lower overall energy expenditures, but they may also raise CO2 emissions because of increasing energy use. Improved energy efficiency can also lead to economic growth. As economies grow, the demand for energy in various sectors increases, potentially offsetting the benefits of energy efficiency.

CO2 emissions may also increase due to the Rebound Effect. The rebound effect refers to the phenomenon in which changes in behaviour and consumption patterns partially or wholly offset the expected reductions in energy consumption resulting from efficiency gains. For instance, if vehicles become more fuel-efficient, people might choose to drive more, negating the anticipated reduction in fuel use.

Energy Transition Theory appears to be operating in OECD countries in reducing CO2 emissions. This theory predicts that the transition from fossil fuel-reliant energy systems to renewable energy systems lowers CO2 emissions.

To further lessen the rebound effect and ensure that efficiency improvements result in a reduction in energy use and CO2 emissions, effective laws and incentives are required. Behavioural changes, such as promoting energy conservation and responsible consumption, are crucial.

Therefore, the view that the best way for a country to attain a cleaner environment is through economic growth and development, as argued in (Beckerman, 1992), is not persuasive. Moreover, no empirical study provides evidence and support that economic growth alone enhances environmental quality in a country or region. Hence, relying solely on economic growth is likely to prove futile in the fight against environmental degradation.

For sustainable development, OECD countries should not rely on a high level of income and development. Focussing on optimising energy use and consumption and changing their composition in support of a sustainable environment is the key to combating environmental degradation. The OECD countries need to decrease CO2 emissions by increasing the share of clean energy in total energy use and decreasing the share of non-renewable energy, especially fossil fuel and biomass, or through the adoption of green or sustainable technology, effective incentive programmes, and prudent environmental regulation in order to achieve sustainable development.

Conclusion and Policy Implications

This study examined the relationship of CO2 emissions with energy use, renewable energy consumption and tested the EKC theory in OECD countries. We analysed the annual data compiled from the World Bank’s database on World Development Indicators for 24 OECD countries from 1990 to 2016. The five variables included in log form for the analysis are CO2 emissions per capita, real GDP per capita, the square of real GDP per capita, energy use per capita, and consumption of renewable energy per capita. The test of cross-sectional dependence across cross-sectional units revealed that the panel variables were cross-sectionally dependent. The test of slope heterogeneity indicated that the slopes were heterogeneous across cross-sectional units. In such cases, the appropriate unit root tests for panel variables are the CADF and CIPS tests. Based on these unit root tests, we found the variables to be of mixed order of integration, but none of them was found to be integrated of order more than one. Based on the test of cointegration accounting for cross-sectional dependence, we found the above five variables to be cointegrated.

For a robustness check, we used two methods of the common correlated effects estimator—the CS-DL and CS-ARDL estimators—to estimate the long-term relationship between CO2 emissions per capita as dependent variable, real GDP per capita, the square of real GDP per capita, energy use per capita, and consumption of renewable energy per capita as the explanatory variables. Reliable and consistent parameter estimates were produced by the CS-ARDL and CS-DL models. The analysis did not find evidence to support the inverted U-shaped relationship between GDP per capita and CO2 emissions per capita.

Hence, the EKC hypothesis, which postulates an inverse U-shaped relationship between income per capita and CO2 emissions per capita as a metric of environmental quality, was not supported by the study’s findings. Energy use and CO2 emissions are positively correlated, but consumption of renewable energy is negatively correlated with CO2 emissions. Hence, our study did not support the EKC hypothesis for the sampled 24 OECD nations, even after controlling for cross-sectional dependency caused by unobserved common factors. However, this study supports the hypothesis that energy use leads to environmental degradation and that renewable energy consumption promotes environmental sustainability.

Thus, in OECD countries, income growth does not mitigate environmental degradation; energy use causes environmental degradation, but renewable energy consumption promotes environmental quality. The prediction of Energy Transition Theory that the transition from fossil fuel-reliant energy systems to renewable energy systems will lower CO2 emissions appears to be supported by this study in OECD countries.

Therefore, for a sustainable environment, OECD countries should not rely on economic growth and development. Instead, the key to reducing environmental deterioration is focussing on energy use and renewable energy consumption and altering their composition. OECD countries can directly lower their CO2 emissions by increasing the use of clean and renewable energy, decreasing the use of non-renewable energy, especially fossil fuels, and leveraging green and sustainable technology. Due to the Jevons’ paradox and rebound effects, energy efficiency gains may also lead to an increase in overall energy consumption. Hence, a comprehensive approach that combines energy efficiency, renewable energy integration, and reductions in overall energy demand is essential for mitigating CO2 emissions and realising a sustainable environment in OECD countries.

Our study could not control for green technology used across the sampled OECD countries due to the unavailability of data. The non-inclusion of green technology use in OECD countries as an additional control variable may have influenced the results of our study’s estimated model. Hence, a future study may be conducted by including use of green technology as an additional control variable.

Footnotes

Acknowledgements

The authors express their gratitude to Prof. Md. Abdus Salam, Department of Economics, Aligarh Muslim University, for his valuable input to enrich the article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The authors declare that all the data used for the article will be made available on request.