Abstract

The impact of carbon market pilot policies on corporate information transparency remains an unresolved issue. This study examines the mechanisms through which carbon market pilot policies influence corporate information transparency from the dual perspectives of external supervision and internal demand. Based on panel data from A-share listed companies in China from 2011 to 2022, the study employs multi-period DID model, two-way fixed effects model, and mediation effect model. The findings reveal: Carbon market pilot policies increase corporate information transparency by an average of 8.07%. This effect is achieved through dual pathways: media governance contributes 10.69%, while financing demand contributes 2.33%. The policy effect is more pronounced for large-scale, non-state-owned, and high-carbon-emitting enterprises, particularly in regions with stronger environmental regulations, higher marketization levels, and greater industry concentration. The study proposes policy recommendations, including optimizing carbon market design and building a multi-dimensional external supervision network. It also suggests innovating green financial tools and emphasizing differentiated, targeted policy design. These measures aim to achieve synergy between environmental governance and high-quality capital market development.

Keywords

Introduction

Carbon markets, as a core market-based tool for addressing climate change, use price signals, and trading mechanisms to accelerate corporate low-carbon transitions. These markets, which trade carbon emission rights, combine financial attributes with resource allocation functions. They impose binding constraints to optimize corporate carbon management while creating external pressures and internal incentives that influence corporate behavior (Gu et al., 2022). Under China’s “dual-carbon” strategy, the framework for environmental information disclosure has been continuously refined. For instance, the Measures for the Management of Enterprise Environmental Information Disclosure (2022) standardized disclosure requirements, while the Basic Principles for Power Market Information Disclosure (2024) facilitated synergy between capital markets and carbon markets.

Corporate information transparency is the cornerstone of efficient carbon market operations. It serves as a key lever for environmental regulation and a critical basis for investors to assess environmental risks and value creation (Zhong, 2018). However, existing research shows that while carbon market pilots have improved the disclosure of basic metrics like total carbon emissions, gaps remain in the transparency of key data such as carbon trading details and emission reduction benefits (Hunka et al., 2025). This contradiction underscores the need for a systematic investigation into the mechanisms by which carbon market pilot policies affect corporate information transparency.

Prior research has established a framework for analyzing environmental regulations and corporate disclosure, evolving alongside policy practices. Early studies focused on the cost-benefit paradox of command-and-control regulations. Porter’s (1996)“Porter Hypothesis” put forward a key idea. It suggested that well-designed regulations could spur innovation. These regulations might also offset compliance costs and enhance competitiveness. As market-based regulatory tools gained prominence, carbon markets emerged as a focal point. For example, Ma and Yang (2025) confirmed that carbon market pilots guide firms to increase investments in emission reduction technologies, while Ji et al. (2024) found that carbon price fluctuations influence corporate risk-taking behavior.

Research on disclosure quality and its economic consequences has expanded. External pressures such as media coverage and institutional ownership, along with internal governance such as board independence and ownership concentration, jointly drive disclosure quality (Bushee et al., 2010; Hermalin & Weisbach, 2012). High transparency alleviates financing constraints (Hadlock & Pierce, 2010), enhances stock liquidity (Agarwal et al., 2015), and attracts ESG investment premiums (Christensen et al., 2022).

However, three gaps persist: Few studies quantify the impact of carbon market policies on transparency or explore heterogeneity. The specific mechanisms linking carbon market policies to transparency remain underexamined. Methodologically, traditional three-stage mediation models suffer from endogeneity issues, while two-stage models have limitations in causal inference (Jiang, 2022).

This paper contributes to the carbon-policy and corporate-disclosure literature in four ways. First, it advances theory by integrating institutional, signaling and market-timing perspectives into a coherent “external-supervision–internal-demand” dual-path framework, thereby uncovering the previously unexplored mechanism through which carbon-market policies shape information transparency. Second, it offers a rigorous causal-inference design: a staggered multi-period DID exploiting the phased roll-out of China’s pilot carbon markets, refined with PSM, placebo, and parallel-trend tests, sharply identifies policy effects free of selection and dynamic confounds. Third, it delivers novel micro-evidence that the pilots significantly and persistently enhance transparency, while documenting pronounced heterogeneity across firm, industry, and regional dimensions and revealing how media governance and financing demand interact with firms’ resource constraints and strategic orientations. Finally, it translates these findings into actionable policy guidance that aligns environmental governance with capital-market efficiency under the “dual-carbon” goals.

Theoretical Framework and Hypotheses

Carbon market pilot policies improve corporate information transparency through direct and indirect effects, as illustrated in Figure 1.

Theoretical mechanism diagram.

Direct Effects of Carbon Market Pilot Policies

Drawing on institutional theory and signaling theory, this study proposes that carbon market pilot policies enhance corporate information transparency through three institutional mechanisms. First, there is the regulative element. It is embodied in China’s Interim Regulations on Carbon Emission Trading Management. This regulation legally mandates key emitters to ensure the authenticity, completeness, and accuracy of their emission data. In doing so, it creates compulsory disclosure pressure. This pressure forces firms to improve their internal verification systems. Second, there are normative elements. These elements are represented by standards such as ISO 14064. They standardize carbon disclosure formats. This helps facilitate integrated reporting of both financial and non-financial information. Third, there are cognitive elements. These elements are cultivated through media campaigns and professional training. They help establish a “low-carbon transparency” ethos. This ethos embeds environmental disclosure into corporate governance practices (Scott, 2013). Empirical evidence strongly supports these mechanisms. Zhu et al. (2024) demonstrate that improved digital carbon communication effectively mitigates information asymmetry and reduces negative market reactions to carbon disclosures. Similarly, Yang et al. (2025) found that enhanced environmental disclosure increases the future cash flow information content reflected in stock prices. Their findings provide valuable insights for managerial decision-making.

From a signaling theory perspective (Spence, 1978), firms’ voluntary carbon disclosures serve as credible signals of sound management practices and regulatory compliance. Importantly, this signaling effect creates positive spillovers to financial reporting. These spillovers occur through two channels. First, the synchronization of accounting processes ensures carbon data reliability. This in turn improves accuracy and timeliness in disclosure evaluations. Second, cross-departmental coordination mechanisms are established for carbon data collection. These mechanisms subsequently elevate overall financial reporting quality. Recent empirical studies provide compelling evidence for these effects. H. Wang and Lyu (2025) found that positive environmental narratives in corporate communications have a significant effect. These narratives effectively signal regulatory compliance. They also align investor expectations. As a result, they significantly increase carbon market returns and volatility. Furthermore, Tang et al. (2025) rigorous analysis confirms that China’s carbon market mechanism successfully reduces managerial short-termism while substantially improving the ESG performance of participating firms.

Indirect Effects of Carbon Market Pilot Policies

The Mediating Role of Media Governance

Media supervision serves as a critical mechanism for mitigating information asymmetry between shareholders and management, effectively addressing principal-agent problems (Becker & Murphy, 1993). Media outlets expose corporate carbon emission violations. This triggers shareholders’ demand for managerial oversight. As a result, firms are compelled to enhance overall information transparency. The purpose is to reduce agency costs. This mechanism incentivizes companies to proactively dismantle information barriers and rebuild shareholder trust. They do this through more comprehensive disclosures. Wei et al. (2025) further corroborate media’s pivotal role in information transmission. Huynh and Dang (2025) specifically examine media coverage in international equity markets. They find a positive correlation between media attention and stock liquidity. This correlation is particularly stronger for firms with lower transparency and weaker brand recognition.

Building on McCombs and Shaw’s (1972) agenda-setting theory, media coverage of carbon market developments such as price fluctuations and emission-reduction innovations rapidly elevates these issues to capital market prominence. In this context, firms strategically disclose emission-reduction investments and R&D progress to attract investor attention, gaining competitive advantage through more comprehensive information disclosure. This dynamic finds empirical support in Adhikari and Zhou’s (2022) event study. The study demonstrates several outcomes. Firms providing complete, voluntary disclosures experience the greatest reduction in bid-ask spreads. Firms offering partial information follow, with a lesser reduction in bid-ask spreads. Non-compliant firms show no improvement in information asymmetry. These results substantiate how enhanced disclosure quality improves market perception. They also validate the agenda-setting mechanism that drives corporate disclosure behavior.

Notably, positive and negative media coverage exhibit distinct pathways for improving transparency. On the one hand, positive coverage spillover effect: Media promotion of low-carbon technologies attracts ESG-oriented institutional investors (Li et al., 2024). To maintain favorable reputation and retain these investors, firms voluntarily disclose additional technical details and financial data, thereby enriching information content. Chen (2024) confirms that positive/neutral coverage significantly improves financing efficiency through enhanced transparency and market trust. Zhu et al. (2024) further contrast this stabilizing effect of positive news with the crash risk amplification from negative coverage. On the other hand, negative coverage coercive effect. Exposure of carbon violations forces firms to strengthen internal audits and promptly publicize rectification plans, improving disclosure timeliness and accuracy (Xia & Shi, 2024). This mechanism proves particularly salient in ESG contexts. Zhou et al. (2024) analyze how negative coverage alters ESG disclosure patterns in banking, revealing how firms adapt reporting strategies to mitigate reputational damage-ultimately driving transparency through external pressure.

The Mediating Role of Financing Needs

Building on market timing theory, carbon market pilot policies reshape corporate financing environments through multiple mechanisms that enhance information transparency. Regarding green financing channels, policy innovations significantly influence corporate financing behaviors (Yuan et al., 2025). First, the carbon asset pledge financing model transforms emission allowances into collateral assets. To meet financial institutions’ risk management requirements, firms must systematically disclose carbon accounting processes, allowance holdings, and changes-objectively improving transparency (Fu & Wang, 2025). Second, green bond issuance mandates require carbon market participants to disclose emission performance, reduction targets, and implementation pathways, driving integrated environmental-financial reporting. Khan and Vismara (2025) corroborate this finding, demonstrating how green bonds align financial investments with sustainability goals while improving environmental performance. The ESG investment wave further amplifies disclosure incentives (Cotugno et al., 2025). As carbon market participants possess inherent “low-carbon attributes”, they are more likely included in ESG portfolios. Consequently, these firms proactively disclose comprehensive environmental, social, and governance information to meet investor preferences (X. Wang & Liu, 2024).

From a reputational perspective, carbon market policies exhibit dual effects on transparency. On the one hand, positive effects: Active carbon market participants improve financing conditions by cultivating green reputations, attracting ESG investors, and reducing equity financing costs-thereby strengthening disclosure incentives (Yuan et al., 2025; X. Zhang & Zheng, 2024). On the other hand, negative Effects. Cost-benefit trade-offs create divergent responses. Long-term oriented firms combine substantive emission reductions with detailed disclosures to build competitive advantage (Sun & Zhu, 2024). Resource-constrained or short-term focused firms may engage in “greenwashing” through selective or ambiguous disclosures, ultimately reducing information quality (Mingqiang et al., 2024). This complex response pattern reflects the nuanced impact of carbon market policies on corporate transparency.

Research Design

Model Specification

We aim to empirically examine the impact of carbon market pilot policies on corporate information transparency. To do this, we employ a multi-period DID model. This model accounts for the staggered implementation of these policies across different regions. This quasi-experimental approach allows us to measure the differential changes in information transparency between treatment and control groups before and after policy implementation, as specified in Equation 1.

In the model specification, the dependent variable

Variable Selection

Dependent Variable

Following Liu et al. (2023) and B. Zhang et al. (2009), we employ the information disclosure evaluation results from the Shenzhen Stock Exchange (SZSE). These results serve as our proxy for corporate information transparency. The SZSE conducts annual assessments of listed companies’ disclosure practices. These assessments are conducted under the Measures for the Evaluation of Information Disclosure by Listed Companies. The SZSE evaluates multiple dimensions. These dimensions include. truthfulness, accuracy, completeness, compliance, clarity and understandability, timeliness and consistency, logical coherence, adequacy, and scientific evaluation framework. Companies are rated on a four-tier scale where A stands for Excellent, B for Good, C for Pass, and D for Fail. We construct a binary transparency variable

Core Explanatory Variable

The carbon market pilot policy serves as an effective market-based instrument to incentivize corporate energy conservation and emission reduction, thereby promoting green and low-carbon development. The pilot program was implemented in phases across China. The first batch, launched in 2013, included Shanghai, Beijing, Tianjin, and Guangdong (including Shenzhen); the second batch, introduced in 2014, covered Hubei and Chongqing; and the third batch, rolled out in 2016, comprised Fujian. This staggered implementation creates a natural experimental setting with well-defined treatment and control groups. Accordingly, we construct our core explanatory variable in the following manner. Treated firms are those located in pilot regions during and after the implementation of the policy, while control firms refer to those situated in non-pilot regions throughout the entire sample period. The treatment indicator equals 1 for firms in pilot regions and 0 otherwise, capturing the exogenous variation in policy exposure.

Mechanism Variables

Media coverage level variable. This paper refers to the studies of Qi and Li (2023) and Luo et al. (2022). It examines different levels of external supervision from two perspectives. These two perspectives are the number of original positive news (Media1) and the number of original negative news (Media2) that enterprises face in online news. The paper conducts logarithmic processing on these numbers. The larger the value, the greater the media supervision pressure that the enterprise is facing.

Financing demand variable. Referring to the research of Demirgüç-Kunt and Maksimovic (1998), the financing demand is calculated by subtracting the achievable endogenous growth from the enterprise growth potential. The larger the value, the higher the financing demand. The calculation formula is (

Control Variables

The transparency of enterprise information is not only affected by the carbon market pilot policies but also by other factors. Referring to the research of Zhao et al. (2024) and Ren et al. (2025), integrating the four dimensions of enterprise financial characteristics, corporate governance, growth operation, and basic characteristics, the following enterprise-level control variables are selected. (1) Enterprise size (

Data Sources

This paper selects the A-share listed companies of the Shenzhen Stock Exchange from 2011 to 2022 as the initial research samples. The reason is that only the Shenzhen Stock Exchange discloses the data of the information transparency level of listed companies. Moreover, given that there are many missing values in the information transparency data of the Shenzhen Stock Exchange, the initial samples are processed as follows. (1) Exclude financial companies and those that were classified as ST, ST*, or PT in the current year; (2) Eliminate samples with severely missing data. All sample data were horizontally truncated at around 1%, and the total sample size was 21,253. The media governance variables are derived from the financial database of the China Research Data Service Platform (CNRDS), while other data are from the CSMAR database.

Descriptive Statistics

Descriptive analysis is carried out from the statistics of sample size, mean value, standard deviation, minimum value, median value, and maximum value of observed variables respectively, as shown in Table 1. The sample mean of corporate information transparency is 0.874, indicating that the overall level of information transparency of listed companies in China is relatively high. The standard deviations of corporate growth and ownership concentration are relatively large, suggesting that these two indicators have a greater degree of dispersion. The gaps between the mean and median of firm size, operating cash flow, asset-liability ratio, proportion of independent directors, ownership concentration, investment opportunities, firm age, and agency costs are small, indicating that these data are relatively evenly distributed and close to a normal distribution.

Descriptive Statistics of Variables.

Empirical Result Analysis

Baseline Regression Analysis

The estimation results of the benchmark regression indicate that the pilot carbon market policy has a significant promoting effect on corporate information transparency (see Table 2). Specifically, as shown in Column (1) of Table 2, when no control variables are included and no fixes are applied to industry, provincial, and time effects, the regression coefficient of the pilot carbon market policy on corporate information transparency is 0.0153, with a significant positive promoting effect at the 1% significance level. Furthermore, as indicated in Columns (2) and (3), after incorporating control variables and fixing industry, provincial, and time effects, the regression coefficient of the pilot carbon market policy on corporate information transparency remains significant at the 1% level, eventually reaching 0.0807. This suggests that the pilot carbon market has increased corporate information transparency by an average of 8.07%. These results fully confirm the effectiveness of China’s pilot carbon market policy in influencing corporate information transparency, thus validating H1.

Results of Baseline Regression.

Note. ***, **, and * indicate statistical significance at the 1%, 5%, and 10% confidence levels, respectively; The values in parentheses are robust standard errors clustered at the provincial, firm and year levels.

Robustness Tests

Parallel Trend Test

There exists a difference in corporate information transparency before and after the implementation of the pilot carbon market policy, and this difference may also be influenced by other unobserved factors. To verify the real impact of the pilot carbon market policy on corporate information transparency, this paper analyzes the validity of the parallel trend through pre-treatment tests, considering both the inclusion and exclusion of control variables. The specific model is as follows.

Herein,

Regression Results of the Parallel Trend Assumption Test.

Parallel trend test diagram.

Replacing the Dependent Variable

Analysts pay continuous attention to firms. This makes corporate information more liquid in the market. Stakeholders can access corporate information more fully. Thus, analyst attention was used as the dependent variable for further regression. As shown in Table 4 (1), when the dependent variable is analyst attention, the coefficient of the carbon market pilot policy is significantly positive at the 5% level. This confirms the robustness of the benchmark regression.

Results of Robustness Tests.

Note. *** and ** indicate statistical significance at the 1% and 5% confidence levels; The values in parentheses are robust standard errors clustered at the provincial, firm and year levels.

Excluding Interference from Green Finance Policies

In 2016, seven ministries including the People’s Bank of China and the Ministry of Finance jointly issued Guiding Opinions on Building a Green Financial System. This major policy move marked the official establishment of China’s green financial system. It is a key environmental policy closely related to corporate operation and development. This study controlled for this policy variable (greenfinance) in the benchmark regression model. This was to accurately identify the net effect of the carbon market pilot policy on corporate information transparency. To avoid multicollinearity, year fixed effects were not included. As shown in Table 4 (2), after excluding the impact of green finance policies, the carbon market pilot policy still significantly improves corporate information transparency.

Regressing with the Single-Time-Point DID Method

The first batch of carbon trading pilot regions launched trading at the end of 2013. Thus, 2014 was set as the benchmark year for policy shock to conduct single-time-point regression. If the observation year is 2014 or later, the value is 1, representing the treatment group. Otherwise, the value is 0, representing the control group. As shown in Table 4 (3), after re-estimation with single-time-point DID, the regression coefficient is significantly positive. This suggests that the carbon market pilot policy still significantly improves corporate information transparency.

High-Dimensional Fixing

To capture unique shocks to specific industries in specific years, this paper adds a robustness test with industry-time interaction fixed effects. As shown in Table 4 (4), the absolute value of the coefficient of the core explanatory variable slightly adjusts from 0.0807 in the benchmark model to 0.0932. The significance level remains at 1%. The direction and dynamic trend of the policy effect do not change substantially. This indicates that even with fluctuations in industry heterogeneity over time, the promoting effect of the carbon market pilot policy on corporate information transparency remains robust.

Endogeneity Tests

PSM-DID

The selection of pilot carbon market regions is not entirely random. Different regions in China differ significantly in natural conditions, economic development levels, and social cultures. The selection of pilot regions is influenced by factors such as industrial structure types and regional financial development. This may lead to systematic differences in initial characteristics between the treatment group, which consists of firms in pilot regions, and the control group, which consists of firms in non-pilot regions. This in turn causes sample selection bias. To effectively mitigate this bias, this paper uses the Propensity Score Matching (PSM) method to construct comparable samples. The specific operations are as follows.

First, taking firms as the basic unit of analysis, firms registered in pilot carbon market regions are set as the treatment group. Firms registered in non-pilot regions are set as the control group. Second, considering both firm-level micro characteristics and regional macro characteristics, we select firm-level control variables. These include financial characteristics, corporate governance, growth and operation, and basic characteristics. We calculate the propensity score for firms to enter the treatment group using a logit model, as shown in Equation 3.

In the equation,

On this basis, we sequentially use radius matching, kernel matching, and nearest-neighbor matching within caliper. We screen samples in the control group that are highly similar in observable characteristics. This builds a matched quasi-natural experimental setting. Finally, based on the matched samples, we calculate the average treatment effect of the pilot carbon market policy on corporate information transparency. This is to eliminate the interference of sample selection bias. It helps more accurately identify the net impact of the policy.

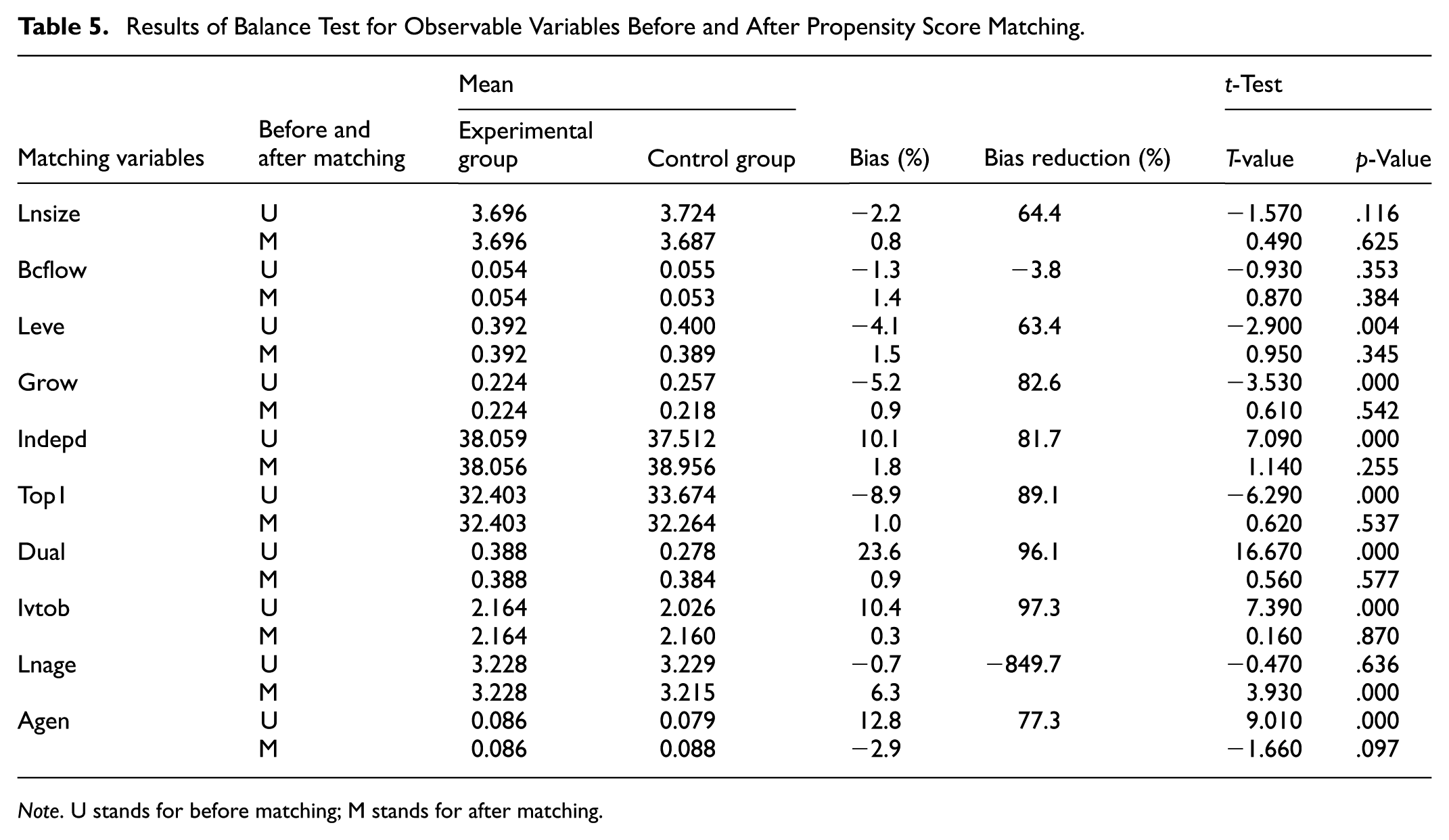

Before PSM estimation, the balance test must be satisfied. This method can effectively solve the problem that samples in the treatment and control groups failed to fully follow the common trend assumption before policy implementation. This paper conducts the balance test using radius matching, and the bandwidth for this radius matching is set as 0.01. The results are shown in Table 5. After matching, the standardized bias is less than 10%, and the p-value is greater than .05. The balance test is passed. That is, at the level of observable variables, the treatment group and the control group are highly similar.

Results of Balance Test for Observable Variables Before and After Propensity Score Matching.

Note. U stands for before matching; M stands for after matching.

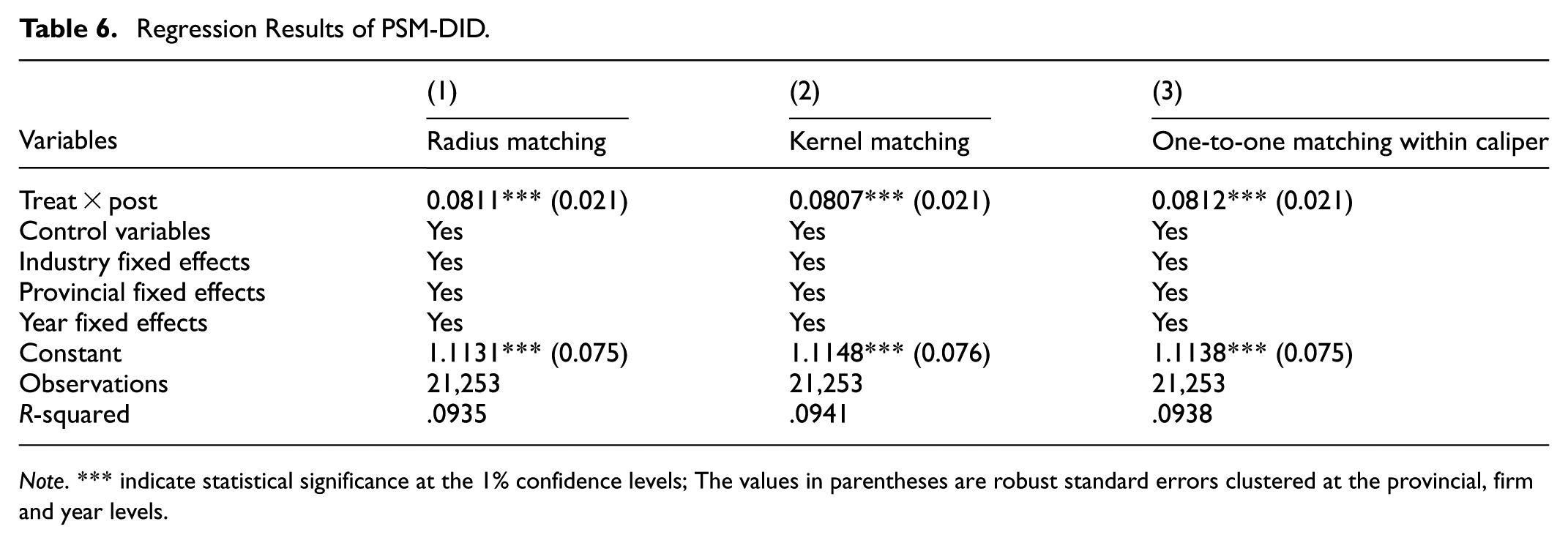

After passing the balance test, this paper further conducts regression on the matched samples. The results are shown in Table 6. The DID coefficient remains significantly positive under different matching methods. This indicates that after comprehensively considering the issue of sample self-selection, the regression results of this paper are reliable.

Regression Results of PSM-DID.

Note. *** indicate statistical significance at the 1% confidence levels; The values in parentheses are robust standard errors clustered at the provincial, firm and year levels.

Placebo Test

The core function of the placebo test is to identify interference from unobservable omitted variables. Its logic is to verify the robustness of the real effect by constructing the fictitious policy shocks. This paper has designed a time placebo test (see the left panel of Figure 3) and a spatial placebo test (see the right panel of Figure 3) respectively.

Diagrams of temporal placebo test and spatial placebo test.

In the time placebo test, we artificially advance the policy implementation time to construct a fictitious treatment period. After repeated estimations, we find that the placebo effects of most fictitious treatment periods fall within the 95% confidence interval containing 0 (p > .1). This result indicates that the improvement of corporate information transparency is not driven by long-term time trends or other time-varying confounding factors. Instead, it is closely related to the actual implementation of the pilot carbon market policy.

In the spatial placebo test, we generate the fictitious treatment groups by randomly permuting pilot regions. The spatial placebo test approximates a normal distribution. The p-value of the two-tailed test is small, allowing us to reject the null hypothesis that the treatment effect is zero. This means that, in the spatial dimension, differences between pilot and non-pilot regions do not stem from random factors or unobservable regional characteristics. It further confirms the statistical reliability of the core conclusion. The promoting effect of the carbon market pilot policy on corporate information transparency has clear policy directionality. It is not a spurious correlation caused by spatially omitted variables.

Mechanism Analysis

This paper analyzes the impact of the carbon market pilot policy on corporate information transparency. It does so from the perspectives of external supervision and internal demand. The model is set as follows.

Among them,

External Supervision

Table 7 presents estimation results with media coverage as the mediating variable. As shown in Table 7 (1), the estimated coefficient of the carbon market pilot policy is significantly positive at the 10% level, with a value of 0.1345. As shown in Table 7 (2), positive media coverage is significant at the 1% level, with a coefficient of 0.8028. The total effect is 0.1345 × 0.8028 = 0.1080. Similarly, as shown in Table 7 (3), the estimated coefficient of the carbon market pilot policy is significantly positive at the 5% level, with a value of 0.0955. As shown in Table 7 (4), negative media coverage is significant at the 1% level, with a coefficient of 1.1078. The total effect is 0.0955 × 1.1078 = 0.1058. This means the carbon market pilot policy, through increasing media coverage, raises corporate information transparency by an average of about (0.1080 + 0.1058)/2 = 10.69%. In summary, this result shows the carbon market pilot policy significantly improves corporate information transparency by increasing media coverage, verifying H2.

Mechanism Test Results of External Supervision.

Note. ***, **, and * indicate statistical significance at the 1%, 5%, and 10% confidence levels, respectively; The values in parentheses are robust standard errors clustered at the provincial, firm and year levels.

Internal Demand

Table 8 shows estimation results with financing demand as the mediating variable. As shown in Table 8 (1), the estimated coefficient of the pilot carbon market policy variable is significantly positive at the 5% level, with a value of .0077. As shown in Table 8 (2), corporate financing demand is significant at the 1% level, with a coefficient of 3.0272. The total effect is 0.0077 × 3.0272 = 0.0233. This indicates that the pilot carbon market policy, through increasing corporate financing demand, raises corporate information transparency by an average of about 2.33%. This result verifies H3a.

Mechanism Test Results of Internal Demand.

Note. ***, **, and * indicate statistical significance at the 1%, 5%, and 10% confidence levels, respectively; The values in parentheses are robust standard errors clustered at the provincial, firm and year levels.

Further, we analyze using the industry average of corporate financing demand, specifying that if it exceeds the industry average of financing demand, the value is 1; otherwise, it is 0. As shown in Table 8 (3) and (4), the estimated coefficients of the carbon market pilot policy and corporate financing demand are significantly positive at the 1% and 10% levels, respectively. This result further confirms the robustness of the conclusion that the pilot carbon market policy improves corporate information transparency by enhancing corporate financing demand.

Heterogeneity Analysis

The carbon market pilot policy primarily targets heavy-polluting enterprises. Its policy effects are not only deeply related to the industry attributes of enterprises. They also vary due to differences in individual characteristics of different enterprises. They are also affected by provincial factors such as regional governance environment and policy implementation intensity. All these factors may have differential impacts on corporate information transparency. Based on this theoretical logic, this paper conducts heterogeneity analysis from three dimensions, specifically provincial governance, industry attributes, and enterprise micro-characteristics.

Provincial Governance Dimension

Heterogeneity in Environmental Regulation Intensity

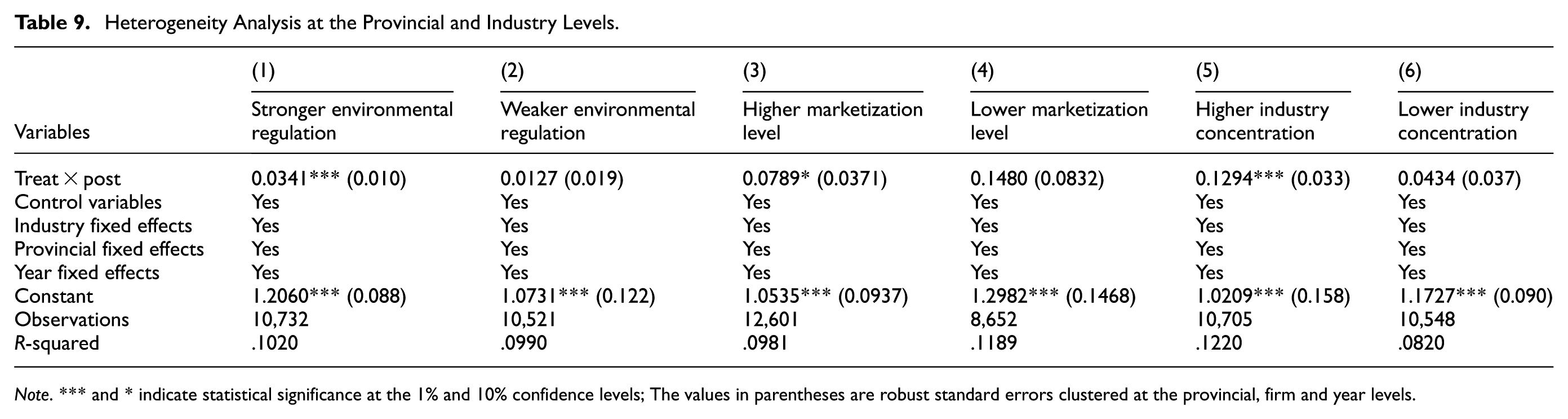

This paper draws on the method of Chen and Duan (2023). It uses the frequency of terms related to environmental protection in provincial government work reports. It constructs an indicator of provincial environmental regulation enforcement intensity. Specifically, if a province’s environmental regulation intensity is higher than the average, it is assigned a value of 1; otherwise, 0. Empirical results in Columns (1) and (2) of Table 9 show that in provinces with higher environmental regulation intensity, the positive impact of the carbon market pilot policy on corporate information transparency is more significant. The reason is that regions with higher environmental regulation intensity provide a more suitable institutional environment for the carbon market pilot policy. This makes the improvement of corporate information transparency not only a result of passive compliance but also a strategic choice for active value-added. This also explains why the same carbon market policy has different effects in regions with different regulation intensities. For example, Zhejiang has higher environmental regulation intensity. The completeness rate of carbon information disclosure by its pilot enterprises is significantly higher than that in some regions with loose regulations. This confirms the synergy between regulation intensity and carbon market effects.

Heterogeneity Analysis at the Provincial and Industry Levels.

Note. *** and * indicate statistical significance at the 1% and 10% confidence levels; The values in parentheses are robust standard errors clustered at the provincial, firm and year levels.

Heterogeneity in Marketization Level

This paper refers to the methods of Yu et al. (2010) and Fan et al. (2003). It calculates the provincial marketization index based on the business environment. It groups regions by whether the index is higher than the average (assigned 1 if higher, 0 otherwise). Empirical results in Columns (3) and (4) of Table 9 show that in provinces with a better business environment and higher marketization level, the positive promoting effect of the carbon market pilot policy on corporate information transparency is more significant. The reason is that marketization level lays the foundation for releasing policy effects by optimizing the operational efficiency of the carbon market. In a highly market-oriented environment, the restrictiveness of policy supervision and the profitability of market mechanisms complement each other. This ultimately drives enterprises to transform information transparency from a cost burden into a competitive advantage.

Industry Attribute Dimension

Heterogeneity in Industry Concentration

This paper draws on the study of Kong et al. (2013). It uses the Herfindahl-Hirschman Index (HHI) to measure industry concentration. The calculation formula is given below (Equation 6).

Here,

Firm Micro-Characteristics Dimension

Heterogeneity in Firm Size

Total assets represent firm size. A value of 1 is assigned if total assets exceed the median; otherwise, 0. As shown in Table 10 (1) and (2), the carbon market pilot policy has a stronger promoting effect on information transparency of large-scale firms. The reason is that compared with small-scale firms, large-scale firms face stricter policy supervision and higher market attention. They have stronger advantages in resources and capabilities, and enjoy higher visibility and influence in the capital market. This differential impact is not policy discrimination, but a natural result of market mechanisms and firm heterogeneity. It also aligns with the original policy intention of the carbon market, which focuses on large firms while leaving small ones to their own devices and aims to achieve precise emission reduction.

Heterogeneity Analysis at the Enterprise Level.

Note. *** and ** indicate statistical significance at the 1% and 5% confidence levels; The values in parentheses are robust standard errors clustered at the provincial, firm and year levels.

Heterogeneity in Firm Ownership Nature

If a firm is a state-owned enterprise, the value is 1; otherwise, 0. As shown in Table 10 (3) and (4), the carbon market pilot policy better improves the information transparency of non-state-owned enterprises. The reason is that, compared with state-owned enterprises, non-state-owned enterprises are more dependent on market feedback and reputation management. They have lower information disclosure costs. They can more flexibly adjust their business strategies and information disclosure methods.

Heterogeneity in Corporate Carbon Emissions

If a firm’s carbon emissions exceed the median, the value is 1; otherwise, 0. As shown in Table 10 (5) and (6), the carbon market pilot policy more significantly improves the information transparency of firms with higher carbon emissions. The reason is as follows. Firms with higher carbon emissions are compared with those with lower carbon emissions. The former face stricter policy constraints. They also face greater market pressure. They have stronger industry demonstration effects. They possess more complete monitoring and accounting systems. Additionally, they receive higher social attention. These factors work together to prompt them to improve information transparency.

Discussion

Although academia has confirmed that policies significantly affect corporate information disclosure quality (Wan & Yu, 2024; Xu et al., 2023), existing studies have paid insufficient attention to corporate information transparency. More notably, some studies suggest that improving information transparency is not entirely beneficial (Xiao et al., 2024). They argue that such improvement may not reduce social harm; instead, it may exacerbate the risk of corporate “greenwashing” phenomenon. As Chen and Duan (2023) point out, existing enterprises’ price measures to curb greenwashing by emerging green enterprises have limited impact. The root cause is that green enterprises can easily imitate such measures without additional costs. However, the carbon market pilot policy has established a set of mandatory and traceable information disclosure mechanisms. Meanwhile, the introduction of market mechanisms has directly linked transparency to corporate interests. It can not only effectively improve corporate information transparency but also the improvement of such transparency has positive significance for alleviating the “greenwashing” phenomenon.

From the perspective of policy design logic, China’s pilot carbon market policy and internationally mature carbon markets like the EU ETS share common ground in core goals. Both take improving corporate environmental information transparency as an important means to promote low-carbon transition. But they differ in implementation paths. Internationally mature carbon markets, after long-term development, have formed sound legal systems and regulatory frameworks. However, China’s pilot policies are in the exploratory stage. They are more dependent on external conditions such as environmental regulation intensity and marketization level.

Regarding the impact of enterprise types, in international carbon markets, non-state-owned enterprises are also more sensitive to market signals. However, China’s non-state-owned enterprises are affected by institutional mechanisms. They share similarities with international counterparts in the flexibility of policy response. At the same time, they show stronger cost orientation. This is due to the characteristics of the domestic market environment. In terms of enterprise size, information disclosure of international large enterprises stems more from the pressure of global supply chains. For China’s large-scale enterprises, the improvement in transparency is related to market factors. It is also closely related to another aspect. That aspect is domestic policies’ direct control over key enterprises.

Conclusions and Policy Implications

Conclusions

This paper aims to explore the impact of the carbon market pilot policy on corporate information transparency. It approaches this from the perspectives of external supervision and internal demand. The paper uses data of A-share listed companies from 2011 to 2022. It constructs multi-period DID models and mechanism test models. These models are used to empirically analyze the promoting effect of the pilot carbon market policy on corporate information transparency. They also serve to empirically analyze the mechanism behind this effect. The main research conclusions are as follows.

The carbon market pilot policy has a significant and sustained effect on improving corporate information transparency, with an average increase of 8.07%. This result has passed multiple robustness tests, including the parallel trend test, placebo test, and PSM-DID. It indicates that the carbon market pilot policy effectively improves corporate information transparency through policy supervision and market mechanisms.

The carbon market pilot policy promotes corporate information transparency by an average of about 10.69% and 2.33% through increasing media coverage and corporate financing demand, respectively. Among them, the net effect on positive media coverage is 0.1080, while that on negative coverage is 0.1058. This indicates that media coverage effectively reduces information asymmetry and increases investor attention. Meanwhile, the carbon market pilot policy also exerts the reputation effect to stimulate enterprises’ financing demand, thereby promoting the improvement of corporate information transparency.

When it comes to improving corporate information transparency, the carbon market pilot policy has a more significant effect. This effect is targeted at large-scale, non-state-owned enterprises. These enterprises have higher carbon emissions. The effect is observed under specific conditions. These conditions include higher environmental regulation intensity, higher marketization level, and higher industry concentration. This is closely related to several factors of such enterprises. These factors include their exposure to market supervision pressure. They also include their sensitivity to environmental regulations. Another factor is their intra-industry competition and cooperation relations. Additionally, the demand for transformation and development is part of these factors.

Policy Implications

Based on the above research conclusions, this paper puts forward the following four policy implications.

First, optimize the institutional design of the carbon market and strengthen the incentive mechanism for information disclosure. To start with, establish a phased dynamic quota allocation mechanism. Implement differentiated quota adjustments based on enterprises’ historical emission data and emission reduction targets. Force high-energy-consuming enterprises to improve information disclosure quality through cost internalization. Next, improve the information disclosure standard system of the carbon market. Clarify the accounting methods of carbon emission data and disclosure format requirements. Promote a graduated disclosure framework that integrates mandatory and voluntary components. Additionally, establish a linkage supervision mechanism between the carbon market and financial markets. Incorporate the quality of corporate carbon information disclosure into the green credit rating system. Impose financing restrictions on enterprises with continuous violations.

Second, build a multi-dimensional external supervision network to improve information transparency. To begin with, establish a carbon market information sharing platform. Integrate data resources from ecological and environmental departments, financial regulatory agencies, and third-party verification institutions. Use blockchain technology to achieve real-time tracking and cross-validation of carbon emission data. Next, strengthen legal safeguards for media supervision. Issue the Regulations on Promoting Environmental Information Communication. Standardize media procedures for investigating and reporting carbon market violations. Lastly, implement hierarchical management of corporate environmental credit. Award the “Green Pioneer” label to enterprises with excellent information disclosure. Form a demonstration effect through incentive measures such as priority in government procurement and tax reductions.

Third, develop innovative green financial support tools to stimulate internal demand drivers within enterprises. First, develop carbon quota pledge financing products. Allow enterprises to use their held carbon quotas as eligible collateral. Offer pledge rate preferences to enterprises meeting information disclosure quality standards. Second, establish special transformation funds. Provide interest-subsidized loans to enterprises in high-energy-consuming industries such as steel and cement that have significantly improved their information disclosure quality. Third, establish a mechanism for compensating for the costs of environmental information disclosure. Provide financial subsidies for the expenses of small and medium-sized enterprises in hiring third-party carbon verification services. Reduce their compliance costs for information disclosure.

Fourth, emphasize the differentiation and precision of policy design to enhance the effectiveness of carbon market policies. To start with, continuously strengthen the synergy between environmental regulations and market-oriented mechanisms. Environmental regulations establish a solid baseline for corporate information disclosure. Marketization stimulates enterprises’ motivation to proactively disclose information. Their combination can more effectively promote enterprises to improve transparency and support the sound operation of the carbon market. Next, pay attention to the impact of industry ecology and corporate characteristics. Utilize the demonstration effect in highly concentrated industries to guide the formation of a favorable atmosphere for information disclosure within the industry. Meanwhile, focus on the characteristics of enterprises with different scales, ownership types, and carbon emission levels. Formulate targeted incentives or constraints. Lastly, in the process of integrating with international carbon markets, both draw on mature international experiences and root in China’s realities. Integrate the rules found in pilots with international carbon market regulations. Enhance the international influence of China’s carbon market and enterprises’ environmental information disclosure capabilities in international competition.

Footnotes

Ethical Considerations

This study did not involve any human or animal testing, and therefore no ethical approval was required.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This paper is funded by the Major Project of Philosophy and Social Sciences of Zhejiang Province under the National Influence Construction Think Tank Special Program entitled “China’s Natural Resource Productivity Ranking Research” (ZKZD202402) and Zhejiang Key Laboratory of Ecological Environmental Damage Control and Value Transformation.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data that support the findings of this study are openly available upon request.