Abstract

Information transparency plays a vital role for developing capital markets. Using data of A-share listed companies from 2007 to 2020, this study examined the impact of customer concentration on corporate information transparency from a supply chain perspective. It suggests that a significant negative correlation exists between customer concentration and information transparency. Customer concentration affects the quality of corporate information disclosures. Through the mechanism test, the impact of customer concentration on corporate information transparency is based on the risk effect rather than the substitution effect of private information on public information. Research on regulatory effects points out that a poor internal information environment aggravates the negative relationship between customer concentration and information transparency. However, media supervision and a higher marketization process alleviate the adverse effects of customer concentration on information transparency. This study indicates that firms with a higher customer concentration have a higher risk of information disclosure, which provides a reference point for investors for making investment-related decisions and for the capital market supervision department for formulating information disclosure policies.

Keywords

Introduction

The concept of information transparency was first proposed by the United States Securities and Exchange Commission (SEC). In 1996, the International Accounting Standards Committee issued a statement on “core standards,” in which the SEC considered comparability, transparency, and full disclosure as the three characteristics of “high quality” accounting standards. Vishwanath and Kaufmann (2001) believed that transparency means that information has the characteristics of accessibility, relevance, quality, and reliability. Bushman et al. (2004) defined information transparency as the extent to which external information users can obtain specific corporate information. Piotroski and Wong (2012) defined information transparency as the content of corporate idiosyncratic information. When there is more corporate idiosyncratic information, they believed that corporate information transparency is higher.

Since the outbreak of the global financial crisis in 2008, governments worldwide have taken measures to improve the information transparency of listed companies to deal with the financial crisis and enhance investor confidence. China learned the experience of information disclosure in developed capital markets. Based on that experience and conditions prevailing in China, the Shenzhen Stock Exchange began to conduct a comprehensive evaluation of the quality of information disclosure of its listed companies in 2001, which has become an important measure to improve corporate information transparency in the country.

Previous studies have shown that, as an essential dimension of corporate information disclosure quality, information transparency plays a vital role in alleviating information asymmetry (Dasgupta et al., 2010). Higher information transparency provides more valuable and accurate information for the capital market, enabling investors to evaluate firms and promoting the accuracy of analysts’ forecasts (J. X. Fang, 2007). It is an essential foundation for ensuring orderly development of the capital market. Simultaneously, information transparency has a governance effect. Improving information transparency can alleviate information asymmetry, thereby assuaging the agency problem between large and small shareholders (K. M. Wang et al., 2009), reducing the agency cost of insiders (Lang & Maffett, 2010), and alleviating agency problems between managers and shareholders (Armstrong et al., 2010). Additionally, increased information transparency can reduce a firm’s equity and debt costs (T. Z. Wu & Lee, 2014; Zeng & Lu, 2006). Enhancing information transparency can also effectively reduce firm risk (Lee et al., 2015; Pan et al., 2011; C. Wang & Xie, 2013).

Information transparency plays an essential role in alleviating information asymmetry and reducing risk and financing costs. However, not all firms try their best to improve corporate information transparency for different reasons. According to the signal theory (Spence, 1973), a firm’s information disclosure is a signal to the outside world, and the process of information transmission alleviates information asymmetry. A firm is the one that best knows its own information; however, to maximize its interests, it strategically discloses information to avoid unfavorable news from affecting its stock price or financing costs. This leads to a decline in information transparency. Higher information transparency also makes firms incur additional costs; for example, firms disclosing information may lose their competitive advantage (Botosan & Stanford, 2005). Some firms use information concealment to conduct insider operations, whereas others violate the provisions of the securities market.

In China, the “private network communication” event shocked the capital market in 2021, in which many listed companies indulged in fictitious transactions and illegal activities by concealing relevant information. Through information hiding, these firms reduced the cost of counterfeiting, but adversely affected the development of the capital market. Therefore, improving information transparency and exploring its influencing factors are of great significance for the development of capital markets. Studies have been conducted on the factors that influence information transparency from the perspective of corporate governance (Q. Fu et al., 2019; Irani & Oesch, 2013), institutional investor shareholding (Boone & White, 2015; Hsu et al., 2016), external supervision (X. H. Li & Yang, 2015), and social relations (Qu et al., 2019). However, few studies have examined the factors that influence information transparency from a supply chain perspective.

As important stakeholders of a firm, customers have a significant influence on business strategy (F. Wu & Zhang, 2021). A higher customer concentration causes more significant risks to companies (Chen, 2016). Once investors identify these risks, they cause fluctuations in a firm’s stock price and affect its financing costs. To avoid the impact of customer concentration risks on a firm, its managers may be motivated to selectively disclose information, which will affect the firm’s information transparency. Additionally, a high degree of customer concentration intensifies the flow of private information between firms and their customers. The flow of private information has a substitution effect on public information disclosure (Ball et al., 2000), affecting information transparency. Therefore, this study uses the data of A-share listed companies in Shanghai and Shenzhen from 2007 to 2020 to examine the relationship between customer concentration and information transparency.

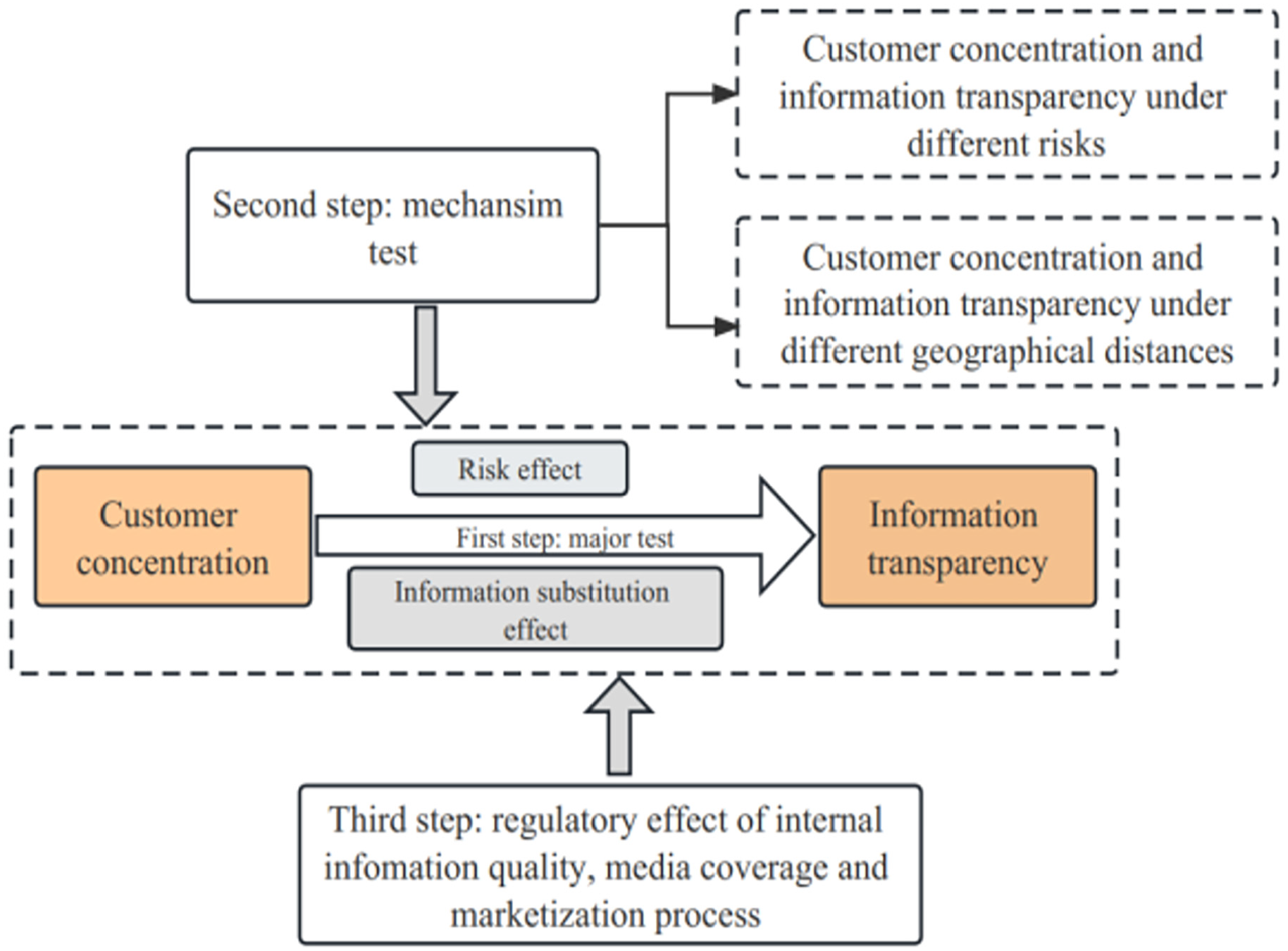

The goal of this study is to explore whether customer concentration affects corporate information transparency based on the type of action mechanism. This study finds that customer concentration affects information transparency. The higher the customer concentration, the lower is corporate information transparency. When firm-risk is high, the impact of customer concentration on information transparency is more significant. In addition, the impact of customer concentration on information transparency is more significant in the close geographic distance group between firms and their customers than in the distant group. This indicates that the impact of customer concentration is mainly based on the risk effect rather than the information substitution effect. Simultaneously, the internal information environment, media coverage, and the marketization process have regulatory effects between customer concentration and information transparency. The study’s conceptual model is illustrated in Figure 1.

Conceptual model.

The marginal contributions of this study are as follows. (a) It enriches the literature on factors affecting corporate information transparency and expands the research boundary. Previous studies on information transparency have focused on corporate governance (Q. Fu et al., 2019; Irani & Oesch, 2013) and external supervision (X. H. Li & Yang, 2015), starting from the perspective of agency issues. This study extends the supply chain perspective and examines the impact of customers on corporate information disclosure behavior of firm. (b) It explores the mechanism of customer concentration’s impact on corporate information transparency and throws light on customer concentration’s impact on corporate information disclosure behavior. It finds that customer concentration mainly affects enterprise information transparency through the risk effect, which is of great significance for investors when making investment decisions. At the same time, it also has a certain guiding significance for the capital market supervision department to supervise firms and formulate policies. (c) Information transparency, one of the features of accounting information disclosure, has essential reference significance for firms and investors. It is as essential as accounting conservatism and accounting information comparability. Previous studies have examined the relationship between customer concentration and accounting conservatism (Hui et al., 2012) and accounting information comparability (H. X. Fang et al., 2017); however, the relationship between customer concentration and information transparency has not yet been researched. The relationship between customer concentration and information transparency can clarify the relationship between customer concentration and corporate accounting information quality.

Theoretical Analysis and Research Hypotheses Development

Many scholars have studied information transparency as an important characteristic of accounting information quality. Several studies have focused on corporate governance. Irani and Oesch (2013) found that corporate governance is an important factor affecting corporate information disclosures. Moreover, corporate governance factors such as board size (Cui & Lu, 2008), insider trading (Gu & Li, 2012), manager defense (Zhang & Zhang, 2017), and equity incentives (Q. Fu et al., 2019) have a significant impact on information transparency. In addition, external supervision is an important factor that affects corporate information transparency. Besides, institutional investor shareholdings (Boone & White, 2015; Hsu et al., 2016; Liu et al., 2018) and media supervision (X. H. Li & Yang, 2015) affect information transparency. Some studies also suggest that political connections (H. Y. Fu, 2013), government intervention (Qu et al., 2019), and institutional environment (Bergloef & Pajuste, 2005) affect corporate information transparency. However, as an important link in an enterprise supply chain, customers are also an essential source of enterprise income. Regardless of the risks they bring to a firm or the information substitution effect generated by their close communication with a firm, they affect a firm’s information disclosure behavior. However, few studies have examined corporate information transparency from the customer perspective.

Customer Concentration and Information Transparency

Based on Risk Effect

When customer concentration is relatively high, a firm faces a higher risk. If customer concentration in a firm is too high, customers have a strong bargaining power vis-à-vis the firm (Piercy & Lane, 2006). They use their bargaining advantages to make firms make concessions in terms of profits, requiring firms to provide more business credit. Therefore, cash flow and business risks are passed on to firms. With high customer concentration, a firm’s revenue is also highly concentrated, leading to major customer dependence. When a firm loses its main customers, it causes significant fluctuations in its cash flows (Dhaliwal et al., 2016). To maintain the relationship with customers, firms make more relationship-specific investments (Irvine et al., 2016), increasing their fixed cost, leverage, and risk. Additionally, a significant relationship exists between a firm’s customer concentration and stock return volatility, and firms with high customer concentration have higher idiosyncratic volatility (Mihov & Naranjo, 2017). In short, high customer concentration causes several risks to a firm (Chen, 2016). Under the high risk pressure caused by high customer concentration, firms selectively disclose information to reduce information transparency. Excessive risks affect investors’ confidence in and appraisal of a firm. Therefore, to show a good external image, when customer concentration is relatively high, firms appropriately reduce the disclosure of some information, reducing their information transparency.

Additionally, as important strategic partners of a firm, customers are essential stakeholders that ensure the stability of a firm’s cash flow. The higher a firm’s customer concentration, the greater is its impact on the firm. Primary customers are an essential source of corporate income. Once firms lose their primary customers, they are exposed to the risk of capital chain rupture. Therefore, firms choose to focus on maintaining relationships with customers. To preserve long-term cooperative relationships with customers, firms whitewash their performance and tend to conduct more earnings management (H. X. Fang & Zhang, 2016; D. L. Luo et al., 2022) to show a good state of affairs. Raman and Shahrur (2008) found that the establishment of a proprietary investment in the relationship between firms and customers increases the requirements for high information quality; however, firms increase profits by growing manipulable accruals and earnings management behavior. Earnings management behaviors are accompanied by corresponding accounting information manipulation. Accounting information disclosure based on earnings manipulation also involves great uncertainty, which causes the transparency of accounting information to decline. At the same time, through proper information disclosure, when the outside world gets to know that a firm is managing its earnings, investors will negatively evaluate the firm, causing stock price fluctuations and increasing its financing costs. Therefore, companies choose vague disclosures to reduce information transparency.

Based on the Information Substitution Effect

Firms disclose information to provide a decision-making basis for their stakeholders. In addition to shareholders and creditors, suppliers and customers with business relationships with a firm are also important stakeholders. Therefore, apart from meeting the needs of financial stakeholders such as investors and creditors, information disclosure should also meet the needs of non-financial stakeholders. Customers play a crucial role in a firm’s business development as an essential contributor of its sales. Therefore, firms pay more attention to the information disclosure needs of customers.

When a firm’s revenue is on account of several major customers, it results in a high degree of customer concentration. Kolay et al. (2016) found the nature of the spillover effects of financial crises. When a customer is in an economic crisis, its supplier’s market value is severely reduced. This reduced market value has a huge impact on the supplier’s cost of replacing a bankrupt customer. Therefore, changing customers results in high switching costs. As a result, firms are concerned with maintaining customer relationships. When customer concentration is relatively high, private information communication becomes an important channel through which customers obtain information from firms (H. X. Fang et al., 2017). When customer concentration is high, more relationship-specific investments are established between customers and firms (Raman & Shahrur, 2008). A firm’s situation affects the value of customer relationship-specific investments. To maintain a good relationship with customers, firms choose private information communication methods to convey their financial situation to customers, avoiding publicly disclosing information that competing firms can use against the firms making disclosures. In addition, customers can evaluate the value of a relationship-specific investment through the information about the performance and risks of a firm (Cornell & Shapiro, 1987). A firm’s customers highly demand information pertaining to the firm. Therefore, they must judge a firm’s condition and decide whether to invest in proprietary investments.

When customer concentration is relatively high, customers have more substantial bargaining power vis-à-vis firms. In such a situation, they require firms to provide them with more information to meet their needs to understand firms’ situation. Consequently, firms communicate more private information with significant customers. In addition, when a customer establishes a contractual relationship with a firm, it also agrees on the terms required to obtain the corresponding financial information from the firm.

Existing research points out a specific substitution effect between private and public information (Ball et al., 2000). When firms release more private information to meet the requirements of customers demanding that information, public information disclosures by such firms reduce. Fan and Wong (2002) found that when a firm’s shareholding structure is relatively concentrated, it discloses less earnings-related information because, under a centralized shareholding structure, firms only need to disclose information to a few owners, which restricts the disclosure of public information. This vague disclosure strategy can reduce threats from competitors and avoid political censorship and social supervision. Studies have shown direct information communication behaviors between firms and customers (Baiman & Rajan, 2002). Correspondingly, once more information is released through private communication between firms and customers, it affects the extent of public information disclosures by firms, thereby reducing their information transparency. In addition, when firms make information disclosure decisions, they also consider the cost-benefit principle. Correspondingly, once more information is released through private communication between firms and customers, it affects the extent of public information disclosures by firms, thereby reducing their information transparency. Based on the risk effect and information substitution effect, Hypothesis 1 is proposed:

Hypothesis 1: Customer concentration has a negative impact on information transparency.

Customer Concentration and Information Transparency Under Different Risk Levels

High customer concentration poses a series of risks to firms (Chen, 2016). If the impact of customer concentration on corporate information transparency is based on the risk effect and a firm makes selective information disclosures for concealing information, resulting in a decline in its information transparency, then the firm’s motivation intensity will differ under different risk levels, and the impact of customer concentration on information transparency will also differ. If the risk of a firm is relatively low, it will have a stronger bargaining power vis-à-vis its customers and a certain risk counterbalance ability. If the risk of a firm is high and the impact of customers on it is superimposed, customers will have a stronger motivation to conceal their relevant information, making the impact of customer concentration on information transparency more significant. Based on this, Hypothesis 2 is proposed.

Hypothesis 2: Under the risk effect, the higher the risk, the more significant is the impact of customer concentration on a firm’s information transparency.

Customer Concentration and Information Transparency Under Different Geographical Distances

In the case of high customer concentration, which increases private information communication between firms and customers and reduces the need for public information disclosures, the more the private information exchanges, the more significant the impact of customer concentration on information transparency. Therefore, distinguishing the degree of private information exchange can help determine whether the effect of customer concentration on information transparency is due to the substitution effect of private information on public information.

Studies have pointed out that geographic distance between external organizations and firms is an essential factor affecting communication between them (J. H. Luo et al., 2017). Although there are some remote communication methods, such as the internet and teleconferencing, face-to-face communication still delivers soft information. Face-to-face communication is an essential channel to obtain private information (Kong et al., 2015). Hauswald and Marquez (2006) indicated that the closer the geographic distance to the borrower, the more private information the bank can obtain. The closer the geographical distance, the easier it is to obtain more private information (Jensen et al., 2015). Therefore, the geographic distance between a firm and its customer is used as a proxy variable for private information exchange. Hence, it can be inferred that if the communication of private information between a firm and its customer affects the disclosure of the firm’s public information, then, in areas near to the firm, it is more convenient to transmit private information more, and the impact of customer concentration on information transparency is more significant. Based on this, Hypothesis 3 is proposed:

Hypothesis 3: Under the information substitution effect, the closer the geographical distance between firms and their customers, the more significant is the impact of customer concentration on information transparency.

Research Design

Sample Selection and Data Sources

This study considers the data of A-share companies listed on the Shanghai and Shenzhen Stock Exchanges from 2007 to 2020. The initial sample is processed as follows: (a) We exclude listed companies from the financial industry. (b) ST and *ST companies are excluded. (c) Companies with incomplete data are also eliminated. Finally, 19,571 sample observations are obtained from 2,746 listed companies. The media coverage data is from the China Research Data Service Platform, and the remaining data are from the China Stock Market and Accounting Research Database. Data processing is performed using stata14.0 software. All continuous variables are winsorized at the 1% and 99% quantiles to eliminate the influence of outliers.

Model Design

To study the impact of customer concentration on information transparency, a regression model is established, as shown in Model 1.

Model 1:

In Model 1, Tran represents information transparency, CC represents customer concentration, Controls represents control variables and controls the year and industry.

The indicators proposed by Bhattacharya et al. (2003) are used to measure information transparency. The specific calculation method is as follows.

Bhattacharya et al. (2003) proposed three indicators to measure information opacity: earnings aggressiveness, earnings smoothing, and loss avoidance. However, loss avoidance is an indicator of information opacity for all listed companies at the national level. Therefore, we select earnings aggressiveness and earnings smoothing to measure information transparency.

Earnings Aggressiveness (EA): The higher the earnings aggressiveness of a firm, the more opportunities its managers have for selective whitewashing of surplus items. Higher earnings aggressiveness indicates a higher degree of information opacity. The specific calculation method is as follows (Bhattacharya et al., 2003; Lin et al., 2016).

where i represents the firm and t represents the year. EA is earnings aggressiveness, ACC is accruals, and Asset is the total assets at the end of the year. ΔCA, ΔCL, ΔCash, ΔSTD, and ΔTP represent the increase in current assets, in current liabilities, in monetary funds, in long-term liabilities due within 1 year, and in taxes payable, respectively. DEP represents depreciation of fixed assets and amortization of intangible assets.

Earnings Smoothing (ES): Earnings smoothing reflects the possibility of firms concealing performance fluctuations. The higher the earnings smoothing, the higher the degree of information opacity. The specific calculation method is as follows:

where i represents the firm and t represents the year. SD stands for standard deviation (calculated based on the items in parentheses); CFO stands for net operating cash flow; NI stands for a company’s net profit; and Asset stands for total assets at the end of the year.

Information Transparency (Tran): This study sorted earnings aggressiveness and earnings smoothing according to deciles. The higher the value of earnings aggressiveness and earnings smoothing, the lower the information transparency. Therefore, the convergence process is performed when sorting. The higher the values of EA and ES, the lower the ranking. The calculation formula is as follows.

where, Deciles refers to finding deciles. According to formula (4), the information transparency index is in the interval of [1, 10], and the higher its value, the higher the information transparency.

Control Variables: We select firm size (Size), financial leverage (Lev), profitability (Roa [return-on-assets]), development capability (Growth), time to market (Age), firm nature (State), intangible asset intensity (Intan), accounts receivables level (Accrec), inventory level (Inven), business losses (Loss), major shareholder holdings (Top1), the ratio of independent directors (Inra), audit opinion (Opinion), and whether the firm is audited by a Big Four accounting firm (Big4) as control variables. At the same time, we control the year (Year) and industry (Industry). The definitions of these variables are provided in Table 1.

Definition of Main Variables.

Variable Definitions

The meanings and calculation methods of the variables involved in the study and the variables involved in the empirical research are shown in Table 1.

Empirical Results

Descriptive Statistics

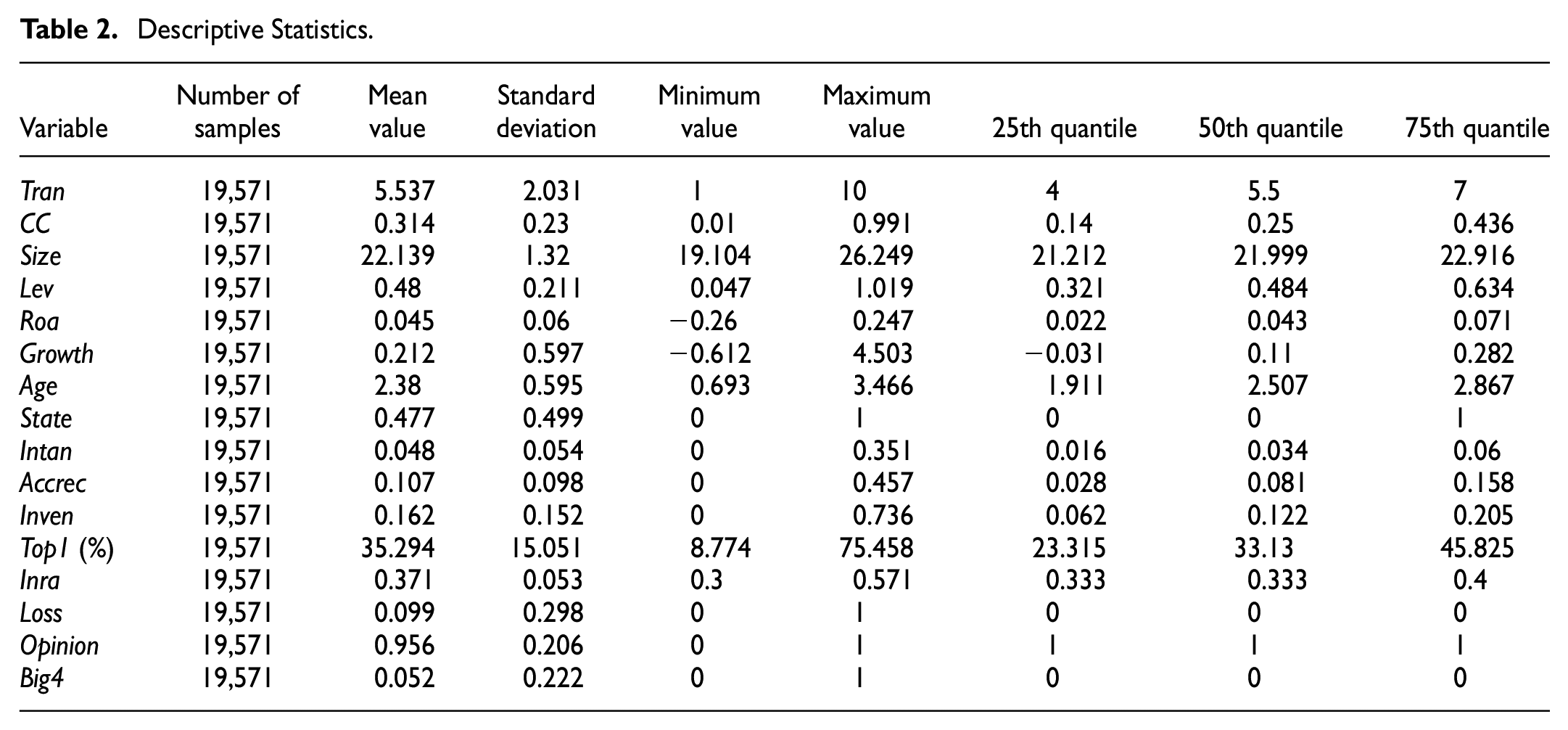

The descriptive statistics in Table 2 show that the minimum value of information transparency (Tran) is 1, maximum value is 10, average value is 5.537, 25th quantile is 4, and median is 5.5. The results show that information transparency (Tran) of most firms reaches the upper-middle level. However, the standard deviation of information transparency (Tran) is 2.031, indicating large differences in information transparency between firms. The average customer concentration (CC) is 0.314. The average sales ratio of the top five customers is more than 30%, indicating that the overall customer concentration level of listed companies in our country is relatively high. In addition, the minimum value of customer concentration (CC) is 0.01. However, the maximum value of CC is 0.991, indicating that the revenue of some firms depends entirely on the sales from their top five customers.

Descriptive Statistics.

Basic Regression Results

Table 3 presents the regression results for the relationship between customer concentration (CC) and information transparency (Tran). In column (1), when controlling for a firm’s basic-level variables, year, and industry, the correlation coefficient between customer concentration (CC) and information transparency (Tran) is −.265. This is significant at the 1% level, which preliminarily indicates that the greater the customer concentration, the lower the information transparency. The degree of customer concentration inhibits a firm’s information transparency. When corporate governance and audit-related variables are added to columns (2) and (3), respectively, customer concentration (CC) still has a significant negative correlation with information transparency (Tran) at the 1% level, which further suggests that customer concentration (CC) has a significant negative impact on information transparency (Tran), thus supporting Hypothesis 1.

Customer Concentration and Information Transparency.

Note. The t-statistics are reported in parentheses.

, ** indicate significance at the 1%, 5% levels, respectively.

In addition, firm size (Size) is significantly negatively correlated with information transparency (Tran). However, operating income growth rate (Growth) and firm age (Age) are significantly positively correlated with information transparency (Tran). Fast-growing firms may need financing, and information transparency needs to be improved to alleviate information asymmetry and lower financing costs. Firms that have been on the market for a long time may also improve their information transparency owing to reputational considerations because of their internal management standards. Information transparency (Tran) has a significant negative correlation with both the holdings of accounts receivables (Accrec) and inventory holdings (Inven). Holding more accounts receivables means that there is a greater risk of bad debts, while carrying too much inventory means that a firm’s operating efficiency is low. Firms have a motive to conceal their poor status on these counts, which reduces their information transparency. In addition, the shareholding ratio of the largest shareholder (Top1) and accounting firm (Big4) have a significant positive correlation with information transparency (Tran), indicating that the largest shareholder holds more shares, has a greater right to speak, can counter the management, and can improve information transparency. As an external supervision mechanism, the Big Four accounting firms’ professionalism and authority also exert external pressure on firms, enhancing their information transparency.

Mechanism Test

To further clarify the influence mechanism of customer concentration on information transparency, we examine whether this is because firms conceal information to reduce their information transparency or because of the substitution effect of private information on public information. Different risk levels and geographic distances from customers are used to test the impact of customer concentration on information transparency.

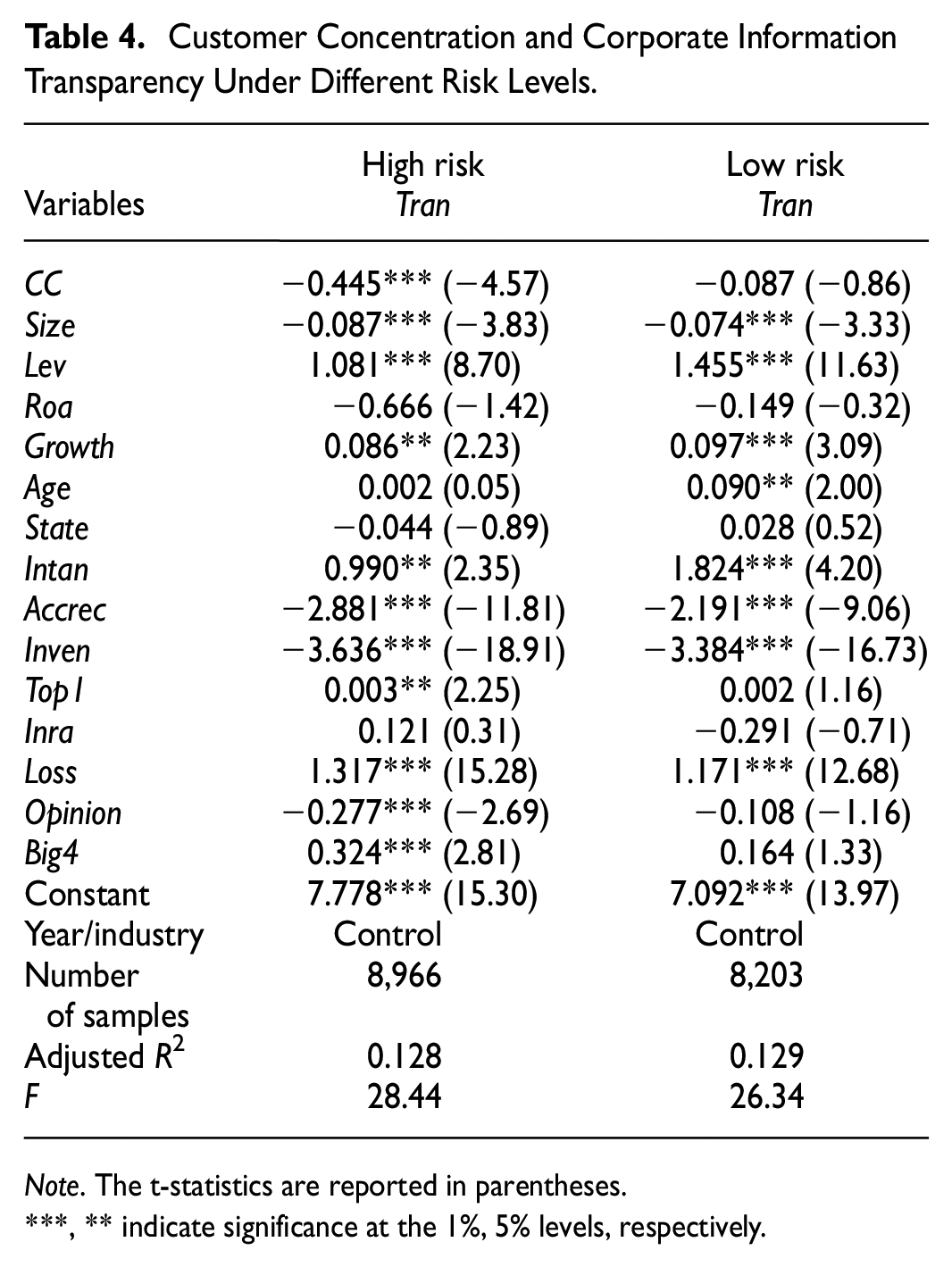

When a firm's risk level is higher than the annual industry average, it falls in the high-risk group; otherwise, it falls in the low-risk group. According to the regression results in Table 4, in the high-risk group, the correlation coefficient between customer concentration (CC) and information transparency (Tran) is −.445, which is significant at the 1% level. The results indicate that customer concentration significantly reduces a firm’s information transparency in the high-risk group. In the low-risk group, the correlation coefficient between customer concentration (CC) and information transparency (Tran) is −.087, which is not significant. The results point out that under high risk, firms reduce their information transparency to conceal information. This result supports Hypothesis 2 and suggests that the relationship between customer concentration and information transparency is based on the risk effect.

Customer Concentration and Corporate Information Transparency Under Different Risk Levels.

Note. The t-statistics are reported in parentheses.

, ** indicate significance at the 1%, 5% levels, respectively.

To verify this mechanism further, we test the influence of customer concentration on information transparency at different geographic distances. In this study, if the customer and firm are located in the same city, they are defined as geographically close; otherwise, they are defined as geographically distant.

Table 5 presents the empirical results of customer concentration on information transparency for different geographical distances. From the regression results in Table 5, it can be seen that in the group with a higher geographic distance, the correlation coefficient between customer concentration (CC) and information transparency (Tran) is −.422, which is significant at the 1% level. In the group with lesser geographic distance, the correlation coefficient between customer concentration (CC) and information transparency (Tran) is −.187, but it is not significant. If this is due to the substitution effect of private information on public information disclosure, customer concentration on information transparency should be more significant in the group with lesser geographical distance. However, it can be seen from the empirical results that Hypothesis 3 is not supported. Therefore, the impact of customer concentration on information transparency is not due to close private information exchanges between firms and their customers to reduce information transparency. The results indicate that customer concentration on information transparency is more due to firms’ initiatives to conceal information when risk is high. This finding supports the presence of a risk effect.

Customer Concentration and Corporate Information Transparency Under Different Geographic Distances.

Note. The t-statistics are reported in parentheses.

, ** indicate significance at the 1%, 5% levels, respectively.

Robustness Test and Endogenous Problem Handling

Robustness Test

To ensure the robustness of the research results, the calculation method of the DD model (Dechow & Dichev, 2002) is selected as a substitute variable of information transparency (Tran1) in column (1) of Table 6. The empirical results in Table 6 show that, in column (1), there is a significant negative correlation between customer concentration (CC) and information transparency (Tran1), and the correlation coefficient reaches −15.292, which is significant at the 1% level. The result is robust.

Robustness Test.

Note. The t-statistics are reported in parentheses.

, ** indicate significance at the 1%, 5% levels, respectively.

Column (2) presents the robustness test, performed by changing the measurement methods for explanatory variables. Column (2) shows the Herfindahl index (HHI) calculated using the sales ratio of the top five customers as a proxy variable for customer concentration. The regression results show that the correlation coefficient between Herfindahl index (HHI) and information transparency (Tran) is −.397, which is significant at the 5% level. This further verifies the robustness of the conclusion.

The information transparency index is determined based on the final average of the deciles of earnings aggressiveness and earnings smoothing. Theoretically, this is in the range of 0 to 10. The calculation results of the sample show that the value of the information transparency index is between 1 and 10. The data on information transparency are discrete-sort data, and the oprobit model is applicable to the testing of sorted data. Therefore, in column (3) of Table 6, the oprobit model test is selected for robustness. It can be seen that the correlation coefficient between customer concentration (CC) and information transparency (Tran) is −.145, which is significant at the 1% level. The result is robust.

Dealing With Endogenous Problems

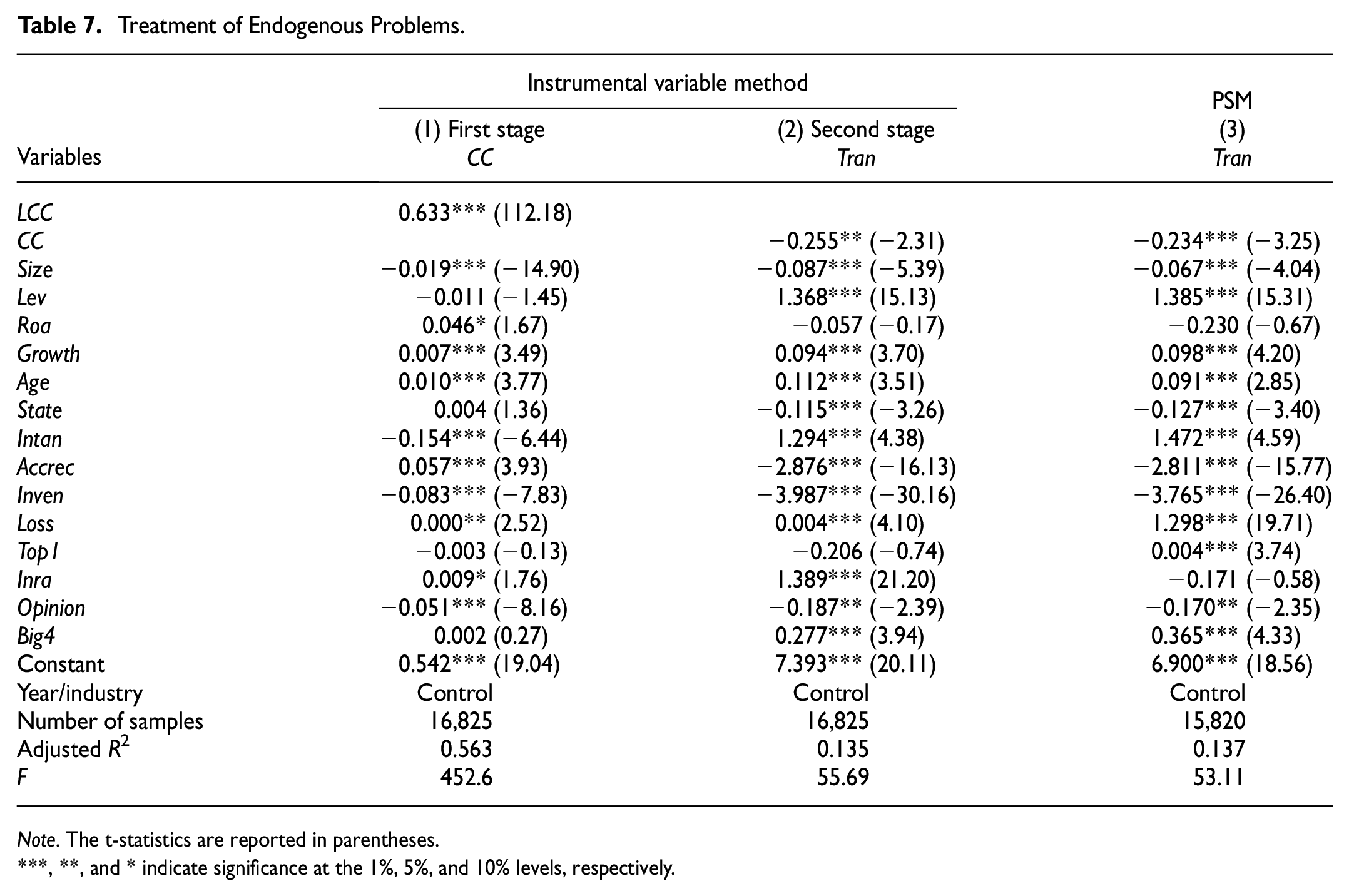

Firms with higher information transparency have a better reputation and image. Their information asymmetry is lower, which attracts more customers to conduct transactions with them, makes customers more dispersed, and creates relatively lower customer concentration. Therefore, information transparency affects a firm’s customer concentration, and there may be a reverse causal relationship between customer concentration and information transparency. Following Itzkowitz (2013), we use the one-period-lagging customer concentration (LCC) as an instrumental variable and the two-stage least squares testing method to deal with possible endogeneity problems. LCC is significantly correlated with customer concentration (CC) but is not directly affected by information transparency. Therefore, it is a reasonable instrumental variable.

Table 7 presents the regression results obtained using the two-stage least-squares method. From the regression results in column (1) of Table 7, it can be seen that the correlation coefficient between one-period lagging customer concentration (LCC) and customer concentration (CC) is .633, which is significant at the 1% significance level, indicating that the instrumental variable is reasonable. In the second stage of regression in column (2), there is a negative correlation between customer concentration (CC) and information transparency (Tran) at a significance level of 5%, with a correlation coefficient of −.255. This result is robust and indicates that customer concentration decreases information transparency.

Treatment of Endogenous Problems.

Note. The t-statistics are reported in parentheses.

, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Large differences exist between firms with high and low customer concentration. To solve the endogeneity problems caused by sample selection bias, we refer to Huang et al. (2016) and use propensity score matching (PSM) for further testing. If customer concentration of a firm is higher than the industry average, it belongs to the treatment group; otherwise, it belongs to the control group. Firm size, financial leverage, profitability, development ability, listing time, firm nature, intangible asset density, inventory level, accounts receivable level, major shareholders’ shareholding, and the proportion of independent directors are taken as the basic criteria to match its proximity. PSM revealed no significant differences between the control and treatment groups. Using a matched sample for regression can better explain the impact of customer concentration on corporate information transparency.

Column (3) of Table 7 lists regression results of the matched samples, showing that the correlation coefficient between customer concentration (CC) and information transparency (Tran) is −.234, significant at the 1% level. The results suggest that the higher the customer concentration of a firm, the lower its information transparency. Customer concentration reduces firms’ information transparency, which further verifies the robustness of the conclusion.

Regulatory Effect of Internal and External Factors

To better understand the impact of customer concentration on information transparency, further research is carried out from the perspectives of internal information quality, media coverage, and the marketization process.

The quality of internal control affects the decision-making behavior of a firm, and information activities are one of the essential parts of a firm’s internal control. This study selected financial restatement (Restate) as the proxy variable for a firm’s information environment to study the impact of customer concentration on information transparency in different information environments. The regression results in column (1) of Table 8 show that the correlation coefficient of the cross-term between customer concentration and financial restatement (CC*Restate) is −.334, which is significant at the 5% level. The results reveal that when a firm has a financial restatement, its information status is extremely unfavorable. To enable external investors to identify a firm’s unfavorable status as little as possible, the firm will have a strong willingness to use hidden information. Therefore, a poor internal information environment exacerbates the negative impact of customer concentration on information transparency.

Regulatory Effect of Internal Information Quality, Media Coverage, and Marketization Process on Customer Concentration and Information Transparency.

Note. The t-statistics are reported in parentheses.

, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Media coverage (Media) of firms attracts the attention of external regulatory agencies and makes administrative agencies actively involved (P. F. Li & Shen, 2010). This strengthens the supervision of firms. Under the pressure of external supervision, the management and major shareholders of firms reduce concealing information for their self-interest, thereby enhancing information transparency. Column (3) of Table 8 shows the mediating effect of the media on the relationship between customer concentration and information transparency. The regression results show that if media coverage negatively affects a firm, the cross-term between customer concentration and media coverage (CC*Media) is significantly and positively correlated at the 5% level, with a correlation coefficient of .115. The results reveal that adverse media coverage can substantially alleviate the negative impact of customer concentration on information transparency. The external governance of the media alleviates the adverse effects of customer concentration on information transparency.

Significant differences in the degree of marketization exist among various regions in China, and the institutional environment affects firms’ information disclosures. The study selected the marketization process (Marketi) (X. L. Wang et al., 2021) to measure marketization. The regression results in column (3) of Table 8 show that the cross-term correlation coefficient between the total marketization index and customer concentration (CC*Marketi) is .107, which is significant at the 1% level, indicating that in the high marketization process regions, it weakens the negative impact of customer concentration on information transparency.

Conclusion

Information transparency plays a vital role in alleviating information asymmetry and is an essential dimension of corporate information disclosure quality. Higher information transparency provides valuable and accurate information for the capital market. Therefore, it is essential for firms to pay attention to factors affecting the quality of corporate information disclosures. This study used data of A-share listed companies from 2007 to 2020 to examine the impact of customer concentration on information transparency.

The study’s findings are as follows. (a) A significant negative correlation exists between customer concentration and information transparency; customer concentration leads to a decline in information transparency and affects the quality of corporate information disclosure. (b) Through a mechanism test, it was found that in high-risk firms, the impact of customer concentration on information transparency is more significant. This indicates that the impact of customer concentration on information transparency is based on risk effects, leading firms to actively conceal information and cause information transparency to decline. For firms geographically close to customers, customer concentration does not significantly impact information transparency. In contrast, for firms far away from customers, the relationship between the two is more significant, excluding the influence of customer concentration on information transparency based on the possibility of the substitution effect of private information on publicly disclosed information. This further demonstrates that the influence of customer concentration on information transparency is based on the risk effect. (c) The internal information environment, external supervision, and marketization process impact the relationship between customer concentration and information transparency. A poor internal information environment aggravates the impact of customer concentration on information transparency. Media coverage can play an external supervisory role by alleviating the negative effect of customer concentration on information transparency. In addition, the negative impact of customer concentration on information transparency is eased in regions with a high degree of marketization.

This study expands the research boundary by examining corporate information disclosure from a supply chain perspective. It suggests that firms should also consider their customers’ situation while dealing with the issue of corporate information disclosure. In addition, it serves as reference for the capital market supervision department in formulating information disclosure policies and performing their supervisory functions. However, this study is limited to the customer concentration index. In fact, the complex customer relationship network is an essential factor affecting corporate information disclosure. Future researchers can use data mining to obtain more detailed customer data and examine the relationship between customers and firm behavior from the viewpoint of customer characteristics and relationship networks.

Footnotes

Acknowledgements

We wish to thank the editor and anonymous referees for valuable comments and suggestions.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was supported by Scientific Research Program Project of Hebei Education Department (grant number SQ2022096).