Abstract

This study’s significance lies in its exploration of how Blockchain-enabled banking positively impacts customers’ financial well-being, offering valuable insights for financial institutions, policymakers, and academics, shedding light on the potential of Blockchain technology to enhance financial transparency and well-being in the banking sector. Convenience sampling was employed in our study, with a sample size of 273 banking customers, to investigate their perceptions and experiences related to blockchain technology in the banking sector. The study employs a Partial Least Squares Structural Equation Modeling (PLS-SEM) approach to analyze the data and examine the direct and indirect relationships among key variables: Blockchain features (efficiency, security, and regulatory compliance), perceived information transparency, and perceived financial well-being. The findings reveal that Blockchain features significantly contribute to customers’ perceived financial well-being. Additionally, the study highlights that perceived information transparency mediates the relationship between these features and customers’ perceived financial well-being. These results emphasize the importance of Blockchain technology in enhancing financial well-being through increased information transparency. The practical implications of this study are far-reaching. Financial institutions can leverage Blockchain technology to enhance customers’ financial transparency and well-being. Policymakers may consider regulatory frameworks that encourage the adoption of Blockchain in the banking sector. Academics can explore related factors such as customer trust and knowledge for further insights. Building on the current research, future studies should explore additional factors that may influence the relationship between Blockchain-enabled banking, information transparency, and customers’ financial well-being. Further investigations could consider factors such as customer knowledge, trust, and socio-economic characteristics.

Introduction

Over the last two decades, the financial industry has witnessed a remarkable influx of digital technologies, including telebanking, internet banking, and mobile banking. These digital disruptions have not only transformed the customer experience but also greatly improved the efficiency, effectiveness, speed, convenience, and transparency of banking processes. Information gaps have been bridged, customer-centric interfaces introduced, and outdated technologies replaced (Anderson et al., 2013). Among these digital innovations, blockchain technology stands out as a disruptive force poised to revolutionize banking and finance. It holds the promise of enhancing financial services by employing decentralized ledgers, ensuring secure data access, and maintaining immutability and transparency. Transactions within blockchain are validated cryptographically, with multiple stakeholders acting as nodes, fostering trust, and reliability (Brüggen et al., 2017).

Blockchain’s potential to reduce costs, eliminate intermediaries, and increase transaction speed makes it an appealing choice for financial institutions. It also offers the prospect of financial inclusion for individuals and businesses traditionally underserved by traditional banking systems. Financial technologies have ushered in a new era of innovation in the financial sector, with blockchain technology playing a central role in this transformation (Crosby et al., 2016). Blockchain technology introduces novel, faster, and more secure methods of transferring money at a reduced cost compared to traditional banking services, covering a wide spectrum of financial activities from payments to investment services (Dzogbenuku et al., 2022). It has significantly increased the transparency of financial transactions, rendering traditional data manipulation impractical (Freij, 2020). By eliminating intermediaries and simplifying traditional banking processes while enhancing security, blockchain ensures efficiency and transparency (Frizzo-Barker et al., 2020). It is anticipated that the adoption of blockchain by the banking industry will usher in a revolution in the delivery of financial services, promising benefits for customers. The global banking system could potentially save up to $20 billion by harnessing blockchain technology to boost efficiency and effectiveness (Garg et al., 2021).

While existing research has explored the predictive value of internet banking and mobile banking for customer well-being (George et al., 2022), the impact of blockchain technology on customer well-being remains a relatively uncharted territory. Most studies have focused on perceived benefits and organizational adoption behavior (George et al., 2022). Furthermore, the bulk of blockchain-related literature has concentrated on supply chain management (Guo & Liang, 2016; Hasan et al., 2020), with only a handful examining the perceived benefits and adoption behavior of banks regarding blockchain technology (Hassani et al., 2018; Nanda & Banerjee, 2021). However, the impact of blockchain-enabled banking on customer well-being has been largely overlooked.

Additionally, most of the past studies have been conducted in developed economies where the pace of technological adoption and regulatory compliance is divergent from developing economies. Financial institutions, particularly banks, are perceived to be the lifeline of modern society and act as a catalyst in stimulating and captivating economic growth in developing countries like Pakistan (Abbas et al., 2021; Ali et al., 2022; Naveed et al.,2021). The banking system of Pakistan is currently going through severe issues. Additionally, the banking system needs to ensure cost efficiency and transparency in its operations to comply with regulations and safeguard customers’ well-being (Garg et al., 2021). In response to such a stringent regulatory framework, the banking system of Pakistan has the potential to embrace disruptive technologies to improve its transparency and performance (Naveed et al., 2021). Blockchain-based systems can equip financial institutions in Pakistan with quicker transactions, greater security levels, more reasonable fees, and last but not least, smart contracts. Blockchain technology has brought about a significant transformation in wallet-to-wallet transfers, guaranteeing immediate, secure, and traceable cross-border remittances. Transfers provide convenience, efficiency, transparency, and cost reduction. Remittances play a significant role in Pakistan’s economy, accounting for more than 6% of the country’s GDP and helping to alleviate trade deficits. The adoption of blockchain technology in Pakistan empowers individuals by enhancing banking security, efficiency, and administrative processes. Enhancing control, compliance, and cyberattack resilience is crucial. The adoption of blockchain technology has the potential to drive Pakistan’s banking sector toward enhanced financial development, transparency, and improved consumer financial planning and well-being. However, in the specific case of Pakistan, there is a lack of research on the impact of Blockchain in enhancing customer financial well-being (Nanda & Banerjee, 2021). The effectiveness of Blockchain-enabled banking in improving financial well-being remains unexplored, and the specific mechanisms by which Blockchain technology fosters customers’ well-being have not been thoroughly examined. To address this gap, this study aims to answer the following research questions: (1) How significant is Blockchain-enabled banking in uplifting the financial well-being of bank customers? And (2) What are the underlying mechanisms through which Blockchain-enabled banking enhances customers’ financial well-being?

Based on the proposed research questions, the proposed model is based on transformative service research, linking Blockchain technology to financial well-being. Drawing from the transformative service research framework, the study suggests that banks can adopt Blockchain technology to enhance customers’ financial well-being (Mostafa, 2020). The focus is on investigating customer perceptions of Blockchain-enabled banking and its impact on financial well-being. Additionally, the study examines how the proposed model’s underlying mechanism, namely financial transparency, contributes to sustaining customers’ financial well-being. In summary, this study intends to make several contributions. Firstly, it explores potential interventions, including Blockchain technology, to improve individuals’ financial behavior and well-being. Secondly, it contributes to the existing literature on financial services and their transformative role in shaping customer financial well-being (Yang et al., 2020). Lastly, the proposed model identifies regulatory compliance and transparency as a concrete mechanism to explain the effects of Blockchain technology on financial well-being. In addition to these contributions, this research holds valuable implications for managers and policymakers.

Literature Review

Households’ financial planning involves a comprehensive evaluation of their present and future financial circumstances, encompassing various aspects such as investment, saving, consumption, and managing financial goals. It is an ongoing process aimed at effectively meeting short-term and long-term financial objectives, with the ultimate goal of sustaining financial well-being (Ali et al., 2023; Rubbaniy, Khalid, Rizwan, & Ali, 2022; Yusuf & Ekundayo, 2018). Financial well-being is significant due to its considerable implications for individuals, businesses, and society. Achieving financial well-being means being able to fulfill current and future financial obligations. Extensive research has been conducted to explore the factors and variables influencing households’ financial planning and well-being (Sheel & Nath, 2019). Financial choices and decision-making play a crucial role in households’ financial well-being. These choices include investment decisions, saving decisions, and consumption decisions. Numerous studies have investigated the factors influencing households’ financial choices, such as socio-economic factors, risk preferences, financial literacy, and access to financial resources (Abbas & Ali, 2022a, 2022b; Athari et al., 2022; Rubbaniy, Khalid, Ali, & Polyzos, 2022). Financial goals guide households’ financial planning activities and can be short-term or long-term. Setting specific, measurable, attainable, relevant, and time-bound (SMART) financial goals is emphasized, along with aligning them with personal values and aspirations (Garg et al., 2021).

The link between financial behavior and financial well-being has garnered significant attention. Positive financial behaviors, such as effective budgeting and prudent financial decision-making, have been associated with better financial well-being. Conversely, poor financial behavior, like excessive debt or impulsive spending, can have adverse effects. Financial literacy is a crucial factor influencing financial well-being. It refers to individuals’ knowledge and understanding of financial concepts, products, and services (George et al., 2022). Financial literacy has been linked to improved financial planning, decision-making, and overall well-being. Financial education programs are considered effective in enhancing financial literacy and well-being. Socio-economic factors and external influences also impact financial well-being. The socio-economic context in which households operate can influence their financial opportunities and constraints. Factors such as income, education, employment, and social support systems can play significant roles in shaping financial well-being (Guo & Liang, 2016).

Financial Well-being

Financial well-being has gained significant attention from regulators, managers, and academics due to its multi-disciplinary dimensions and impacts. It has been recognized that households’ financial well-being not only affects their own financial condition but also has implications for the overall economy. Sustaining financial well-being is crucial to maintaining the production line of a country, as households are the end consumers of goods and services. On the other hand, financial vulnerability and strain can lead to psychological and depressive symptoms, impacting individuals, their families, and society as a whole. Financial strain resulting from unhealthy financial behavior has been found to have detrimental effects on individuals, families, and organizations (Hasan et al., 2020). It can lead to poor employee performance, job burnout, and lower commitment within companies. In fact, financial matters have been identified as a leading cause of job-related stress. Additionally, lower consumer financial well-being reduces purchasing power, negatively impacting the financial performance of companies. The extant literature on financial well-being delves into a multitude of factors that contribute to the attainment of financial well-being. These factors encompass a wide range of antecedents, such as financial knowledge, behavioral patterns, consumer spending habits, self-control mechanisms, credit card literacy, bank information transparency, self-efficacy levels, and trust in financial institutions (Hassani et al., 2018). By examining these diverse elements, researchers have sought to gain a comprehensive understanding of the determinants that shape an individual’s financial well-being. The existing body of literature on financial well-being and the perceived capacity to fulfill present and future financial responsibilities remains relatively constrained and fragmented across various academic fields (Yang et al., 2020). The statement made by the user highlights the necessity for further exploration through comprehensive and integrated studies pertaining to the subject matter. The available literature presents a dearth of evidence pertaining to the efficacy of technological interventions implemented by financial institutions in enhancing consumer financial well-being (Garg et al., 2021).

Blockchain Technology and Banking Services

Technological advancements have had a significant impact on consumers’ financial well-being. Over the past decade, disruptive technologies have reshaped various aspects of consumer consumption and, consequently, their financial well-being. Previous studies have shown that technological interventions adopted by financial institutions can encourage desirable financial behaviors in different contexts (George et al., 2022). The literature on electronic and internet banking has extensively explored the transformation of consumer behavior in response to technological advancements. The adoption of emerging digital technologies, such as mobile and online banking, as well as fintech, has the potential to revolutionize customer experiences in the financial sector (Dana et al., 2022). In recent times, Blockchain technology has emerged as a disruptive force that is expected to revitalize the financial sector (Guo & Liang, 2016). Blockchain is a decentralized or distributed ledger that facilitates the recording, validation, and simultaneous access of data among multiple stakeholders. The existing body of research has extensively classified Blockchain as a disruptive technology that provides users with a range of benefits including trust, security, effectiveness, and transparency. These attributes have been widely acknowledged and explored within the literature, highlighting the significant impact that Blockchain has had on various industries and sectors (Hasan et al., 2020). Scholars and experts have consistently recognized the potential of Blockchain to revolutionize traditional systems by introducing a decentralized and immutable ledger that ensures trust and transparency among participants. Furthermore, the enhanced security measures offered by Blockchain have been extensively studied and documented, emphasizing its potential to mitigate risks associated with data breaches and fraudulent activities. The effectiveness of Blockchain The emergence of Blockchain technology has garnered significant attention due to its unique methodology for transmitting information and storing data. This novel approach has the potential to revolutionize the conventional framework of banking and financial services by enhancing their efficiency, convenience, and transparency (Yang et al., 2020). The present discourse revolves around the anticipation that these nascent technologies will enhance financial processes and the provision of financial services, ultimately culminating in heightened levels of customer contentment (Osmani et al., 2021).

In a recent study conducted by Ryu (2018), the author explores the potential of blockchain technology as an emergent disruptive force. The study highlights how this technology has the ability to empower consumers through various means, such as optimizing effectiveness and security, enhancing cost efficiency, promoting transparency, and upgrading regulatory compliance within organizations. By delving into these key aspects, Ryu sheds light on the transformative power of blockchain and its potential to revolutionize various industries. The current state of research on Blockchain technology is characterized by its early stage of development. The majority of existing studies primarily concentrate on the perceived benefits of this technology rather than its actual advantages. The existing body of research has dedicated considerable attention to exploring the utilization of Blockchain technology within various domains, including banking and finance, business law and governance, as well as accounting and supply chain management (Frizzo-Barker et al., 2020). However, the existing body of research provides only a limited amount of evidence on the impact of these groundbreaking technologies on the restructuring of banking and financial services, as well as their potential to revolutionize consumer welfare. The current literature suggests that there is a growing belief among scholars that the adoption of certain technologies could potentially have a transformative impact on consumer financial well-being (Osmani et al., 2021). However, it is important to note that there is a lack of evidence in this area. Hence, it is evident that further investigation in this domain is of utmost importance. This study seeks to investigate the perception of banking customers regarding Blockchain-enabled banking and its potential impact on their perceived financial well-being (Lai & Wong, 2020).

In the realm of financial services, the banking sector has emerged as a prominent player, catering to customers’ diverse needs in managing their finances, addressing household financial obstacles, and striving toward their financial aspirations (Losada-Otálora & Alkire, 2019). With a plethora of approaches at their disposal, banks have become a reliable source for individuals seeking assistance in navigating the intricacies of their monetary affairs. The significance of innovative technologies in enhancing the delivery of financial services and empowering customers to effectively manage their finances cannot be overstated. In the realm of financial institutions, with a particular focus on the banking sector, there exists a notable inclination toward embracing and accommodating disruptive technologies (Mostafa, 2020). One such technology that has garnered significant attention is Blockchain. The concept of blockchain has emerged as a significant and influential disruptive technology in recent years. It is characterized by a series of information blocks that are securely verified through the participation of distributed networks of nodes, involving a wide range of stakeholders (Nanda & Banerjee, 2021). This technology has garnered attention due to its simplicity and remarkable potential for transforming various industries and sectors. The technology under consideration facilitates the transmission of value between peers, encompassing a wide range of assets, including physical commodities and digital currency, without the need for an intermediary to oversee the process. In a recent study conducted by (Frizzo-Barker et al., 2020), it was found that stakeholders such as entrepreneurs, developers, and technology enthusiasts are highly optimistic about the potential of Blockchain technology to revolutionize the banking and financial sector. These stakeholders emphasize that Blockchain has the capability to enhance transparency and streamline business operations while also bolstering the efficiency and security of the banking system. This sentiment reflects the growing recognition of Blockchain as a transformative force in the industry.

In the realm of business, particularly within the banking sector, the pursuit of efficiency and effectiveness stands as a paramount concern. This enduring focus on optimizing operations and achieving desired outcomes has become an integral aspect of organizational success. The banking industry, like many others, recognizes the significance of streamlining processes and maximizing productivity to remain competitive in a rapidly evolving marketplace (Dzogbenuku et al., 2022). As such, the quest for efficiency and effectiveness has emerged as a central theme in the literature surrounding business practices, with scholars and practitioners alike delving into various strategies and approaches to enhance performance and drive sustainable growth. By examining the advent of various technological advancements, such as mobile banking, internet banking, and the more recent introduction of Blockchain-enabled banking, has significantly impacted the landscape of the financial service market (Osmani et al., 2021). These innovations have given rise to a highly competitive environment within industry (Salamzadeh et al., 2022).

Blockchain-enabled Security and Efficiency

The adoption of Blockchain technology in banking can improve efficiency, effectiveness, and the quality of financial services, benefiting both banks and customers. The enhanced security and efficiency offered by Blockchain-enabled banking allow customers to better manage their financial goals and objectives (Brüggen et al., 2017). However, there is a lack of research addressing the relationship between Blockchain-enabled efficiency, security, and customer-perceived financial well-being. Financial services aim to maximize households’ wealth, and banking services play a pivotal role in driving household well-being. Transformative service research emphasizes the importance of service providers fostering consumer welfare. Banking services have a pervasive impact on consumer well-being, making it essential to examine the concept of financial well-being within the context of transformative service research. This study aims to explore the transformative role of Blockchain-enabled banking services in determining customer financial well-being. Existing studies have primarily focused on the organizational perspective and have been conducted in developed countries, with limited evidence in developing economies. Additionally, there is a lack of research on the customer-perceived benefits of Blockchain-enabled services and their transformative impact on customer well-being. Therefore, this study aims to fill this research gap by examining how Blockchain-enabled efficiency and security in banking services influence customers’ financial well-being. Based on the proposed effect of bank efficiency and security on customer financial well-being, the following hypothesis is formulated:

Blockchain and Information Transparency

In the aftermath of the global financial crisis, banks and financial institutions have faced increasing regulatory reforms and compliance pressure worldwide. Regulatory compliance is a top concern for banks to maintain their legitimacy and reputation. The banking sector, in particular, operates under heavy regulations to ensure discipline, protect stakeholders’ interests, and maintain the integrity of the financial system. Banks are required to adhere to various rules and regulations imposed by industry, government, and international regulators while conducting financial services.

Non-compliance with regulations can lead to severe penalties from regulators and damage the corporate reputation of financial institutions (Freij, 2020). Thus, banks are under growing pressure to elevate their compliance activities as part of their operational strategy to sustain a sound corporate reputation and gain customer trust. Regulatory compliance is also crucial for ensuring a transparent banking system and safeguarding the financial well-being of consumers. The banking sector plays a vital role in mobilizing resources and ensuring the overall financial stability of society. Any pitfalls or failures in the banking sector directly impact on the financial well-being of society as a whole. The tightening of the regulatory environment following the 2008 financial crisis has further reinforced the importance of regulatory compliance in the banking sector. Banks face the challenge of complying with evolving regulations while effectively delivering profitable financial services (Paul et al., 2016). As compliance has become a subject of intense focus and scrutiny, financial institutions are seeking innovative solutions to enhance their compliance efforts. High-tech solutions, including disruptive technologies such as Blockchain, have emerged as enablers for banks to meet escalating regulatory compliance requirements and maintain their competitive advantage (Papalapu, 2015).

Blockchain technology offers significant implications for the banking system due to its robust characteristics and potential to enhance the efficiency and effectiveness of financial services. The continuous flow of financial transactions in the banking system relies on information exchanges among stakeholders, but trust-related issues can arise due to redundancies in finance and record-keeping. Blockchain has the capacity to integrate financial processes effectively while enabling compliance with regulations. By leveraging Blockchain, banks can not only achieve thorough regulatory compliance but also enhance customer trust and ease in managing their financial affairs more effectively (Naveed et al., 2021). Ultimately, Blockchain-enabled regulatory compliance not only enhances the legitimacy and credibility of banks but also contributes to uplifting customer-perceived financial well-being. Therefore, the following hypothesis is proposed:

H 2: Blockchain-enabled regulatory compliance positively impacts customer financial well-being (FW).

The convergence of information technology advancements and the implementation of stricter regulatory measures has resulted in a notable rise in shareholder activism and an escalating demand for transparency. The concept of transparency has emerged as a valuable tool in addressing the issue of information asymmetry and fostering trust among various stakeholders. By revealing information that was previously concealed, transparency aims to bridge the gap between those who possess knowledge and those who do not (George et al., 2022). This literature review explores the significance of transparency in mitigating information asymmetry and its role in establishing trust among stakeholders. In the realm of banking, the concept of information transparency holds paramount significance, as it pertains to the perceived caliber of information disseminated by banks to their esteemed shareholders (Garg et al., 2021). The influence of this phenomenon on the economic prosperity of both individuals and communities is of great importance.

The demand for enhanced transparency in information disclosure has been a subject of concern among regulators, who aim to safeguard individuals’ financial well-being against the detrimental consequences of deceptive information. The incorporation of transparency into information disclosure practices by banks has been observed as a response to the regulatory environment. The concept of transparency has emerged as a crucial factor in evaluating the performance and reputation of banks. In recent years, it has become increasingly evident that transparency serves as both a form of performance evidence and an indicator of a bank’s standing within the industry. This literature review aims to explore the significance of transparency in the banking sector and its implications for the overall perception and trustworthiness of financial institutions. By examining existing research and scholarly (Losada-Otálora & Alkire, 2019), the necessity for enhanced transparency arises from the recognition that access to dependable information is crucial in facilitating well-informed decision-making processes pertaining to the allocation of resources.

Existing research has predominantly concentrated on the examination of transparency measures, with a notable dearth of attention directed toward comprehending the intricate relationship between information transparency and the financial well-being of households (Lai & Wong, 2020). The current body of literature lacks sufficient exploration of the role of bank information transparency in determining financial well-being. Furthermore, there is a dearth of documented evidence regarding the mechanism by which transparency influences individuals’ well-being in the financial domain.

The significance of reliable and valid financial information provided by banks is greatly appreciated by customers, as it empowers them to make well-informed decisions. In light of the existing research landscape, it is evident that there is a notable gap in the literature pertaining to the mediating role of bank information transparency in relation to customer financial well-being. Consequently, this study endeavors to fill this void by investigating and analyzing the aforementioned mediating role. By doing so, it aims to contribute to the body of knowledge in this field and shed light on the intricate dynamics between bank information transparency and customer financial well-being (Lai & Wong, 2020).

In this literature review, we explore the role of information transparency as a mediator in the relationship between efficiency and various important factors such as security, regulatory compliance, and customer financial well-being (FW). The hypothesis under investigation is H3, which suggests that information transparency serves as a mediating variable in this relationship. Efficiency is a crucial aspect of any organization’s operations, as it directly impacts its ability to achieve its goals effectively and in a timely manner (Mostafa, 2020). Security, on the other hand, is of paramount importance in today’s digital age, where organizations face numerous threats to their survival. To address the research gap, this study seeks to investigate the role of bank information transparency in determining customer financial well-being. Specifically, it aims to examine how information transparency acts as a mediating variable in the relationship between efficiency and security, regulatory compliance, and customer financial well-being.

H 3: The mediating effect of information transparency is examined in the relationship between efficiency and security, regulatory compliance, and customer financial well-being (FW).

Blockchain and Prevention of Financial Fraud

Financial fraud has long been a concern in the banking and financial sector, leading to significant economic losses and eroding trust among stakeholders. In recent years, the emergence of Blockchain technology has garnered attention as a potential solution to combat financial fraud. Blockchain, a decentralized and transparent ledger system, has inherent characteristics that make it resistant to fraudulent activities (Losada-Otálora & Alkire, 2019). Researchers and industry experts have explored the implications of Blockchain in preventing financial fraud and enhancing the security of financial transactions. Several studies have highlighted the potential of Blockchain in reducing fraud risks and improving the integrity of financial systems. The immutability and transparency of Blockchain transactions make it difficult for fraudsters to manipulate or falsify records. The decentralized nature of Blockchain, with its distributed network of nodes, eliminates the reliance on a single point of failure and reduces the vulnerability to hacking or data manipulation. Furthermore, the use of cryptographic algorithms in Blockchain ensures secure and authenticated transactions, enhancing the overall security of financial operations (Mostafa, 2020). Past studies have also examined specific applications of Blockchain in fraud prevention, such as anti-money laundering (AML) and know your customer (KYC) processes. The use of Blockchain in these areas can enhance the verification and validation of customer identities, making it harder for criminals to engage in fraudulent activities. Additionally, the ability to trace and track transactions on the Blockchain provides an audit trail that can aid in detecting and preventing fraudulent transactions. Based on the literature review, the following hypothesis is proposed:

H 4: The adoption of Blockchain technology in the banking and financial sector has a significant impact on preventing financial fraud.

Trust and integrity are crucial elements in the banking and financial sectors, as they underpin the relationships between financial institutions, customers, and other stakeholders. In recent years, Blockchain technology has emerged as a potential solution to enhance trust and integrity in financial transactions. Blockchain, with its decentralized and transparent nature, offers several features that contribute to building trust and ensuring integrity in the financial system (Yang et al., 2020).

Numerous studies have examined the impact of Blockchain on trust and integrity in financial transactions. Blockchain’s distributed ledger system eliminates the need for intermediaries, reducing the reliance on centralized authorities and enhancing trust among participants. The transparency of Blockchain allows for real-time visibility of transactions, providing stakeholders with greater confidence in the integrity of the financial system (Sheel & Nath, 2019). Studies have also explored the role of cryptographic algorithms in ensuring the security and authenticity of transactions on Blockchain. The use of encryption techniques provides data integrity, preventing unauthorized access or tampering. Smart contracts, which are self-executing contracts embedded in Blockchain, further enhance trust by automating transaction processes and ensuring compliance with predefined rules (Sangroya & Nayak, 2017). Furthermore, the immutability of Blockchain transactions contributes to trust and integrity. Once a transaction is recorded on the Blockchain, it cannot be altered or deleted, providing an auditable and tamper-proof record of financial activities. This feature enhances transparency and accountability, reducing the potential for fraudulent or manipulative behavior. Based on the literature review, the following hypothesis is proposed:

H 5: The adoption of Blockchain technology in the banking and financial sector has a significant positive impact on trust and integrity in financial transactions.

Literature Gap

Based on the extensive literature review we have identified the following potential gap to fill.

Theoretical Framework

Figure 1 displays the theoretical framework for this study and examines the relationship between Blockchain technology and two key dimensions: trust and integrity. It explores how the adoption of Blockchain technology in the banking and financial sectors influences trust and integrity in financial transactions. This study contributes to the existing knowledge on the role of Blockchain technology in the banking and financial sector. It explores how the adoption of Blockchain technology can enhance trust and integrity, which are crucial elements in ensuring the reliability and credibility of financial transactions (Naveed et al., 2021; Osmani et al., 2021; Ryu, 2018). By investigating these relationships, the study provides valuable insights for practitioners, regulators, and policymakers in understanding the potential benefits of Blockchain technology in fostering trust and integrity in the financial industry. The study is based on the framework of transformative service research, which emphasizes the transformative role of services in enhancing consumer well-being. In this context, the study explores both the direct and indirect relationships between Blockchain technology and the dimensions of trust and integrity in financial transactions.

Conceptual model.

The study investigates the direct impact of the adoption of Blockchain technology on trust and integrity in financial transactions. It examines how the features of Blockchain, such as decentralization, transparency, and cryptographic algorithms, directly contribute to building trust and ensuring integrity in the financial system. The study also explores the indirect relationship between Blockchain technology and trust and integrity through the mediating role of other variables. It examines how factors such as efficiency, security, and information transparency, enabled by Blockchain technology, mediate the relationship between Blockchain and trust and integrity in financial transactions (Mostafa, 2020; Nanda & Banerjee, 2021). These factors act as mechanisms through which Blockchain technology influences trust and integrity. By examining both the direct and indirect relationships, the study provides a comprehensive understanding of the transformative impact of Blockchain technology on trust and integrity in the banking and financial sector. It highlights the multifaceted nature of the relationship and the underlying mechanisms through which Blockchain technology can enhance trust and integrity. This study contributes to the field of transformative service research by applying its framework to the context of Blockchain technology and financial transactions (Losada-Otálora & Alkire, 2019). It expands the knowledge on the transformative role of services in fostering trust and integrity and provides insights into the specific mechanisms through which Blockchain technology can facilitate this transformation.

Methodology

Population and Sample Size

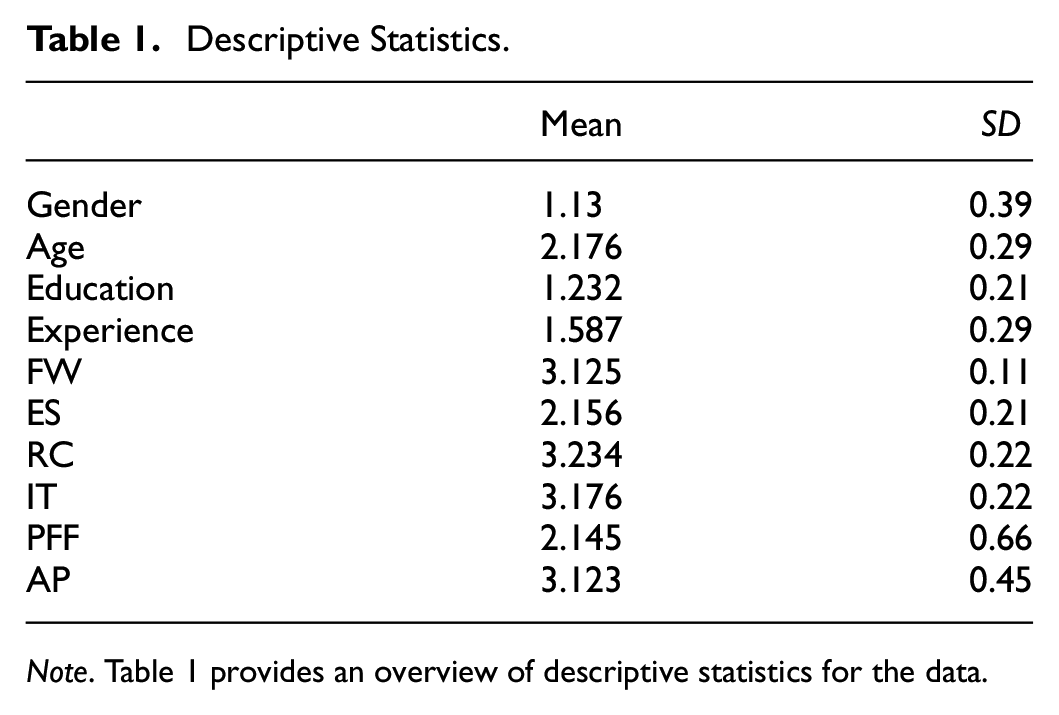

In this section, the methodology employed in the study will be discussed. The research design, data collection methods, and data analysis. In this section, we will discuss the population and sample size considerations in the context of the study. Understanding the population under investigation and determining an appropriate sample size are crucial steps in ensuring the validity and generalizability of the present investigation employed a quantitative research design, utilizing a survey as the primary method of data collection. The study population consisted of individuals residing in Islamabad who possessed bank accounts. The present study employed a convenience sampling method for data collection, in line with prior research conducted by (Dzogbenuku et al., 2022) and (Naveed et al., 2021). This study primarily examines the behavior and activities of individual households who actively participate in Pakistan’s banking sector. In a study involving the distribution of 500 questionnaires, a total of 273 responses (response rate., 54.6%), were deemed suitable for analysis after the exclusion of any questionnaires with missing values. In this study, Table 1 presents the descriptive statistics pertaining to the diverse variables under investigation.

Descriptive Statistics.

Note. Table 1 provides an overview of descriptive statistics for the data.

Table 2 represents the correlation coefficients between different factors related to the financial industry. The correlation coefficient ranges from −1 to 1, where 1 indicates a strong positive correlation, −1 indicates a strong negative correlation, and 0 indicates no correlation. Accuracy and Privacy have a perfect positive correlation with itself (1.000), as expected. It also has moderate positive correlations with Trust and Integrity (.716) and Regulatory Compliance (.726). Additionally, Accuracy and Privacy show moderate positive correlations with Information Transparency (.543) and Prevention of Financial Fraud (.543). Efficiency and Security demonstrate a moderate positive correlation with Accuracy and Privacy (.618). It indicates that as Efficiency and Security improve, Accuracy and Privacy tend to improve as well. However, Efficiency and Security have weaker positive correlations with other factors such as Financial Wellbeing (.401), Information Transparency (.524), Prevention of Financial Fraud (.632), and Regulatory Compliance (.609). Financial Wellbeing exhibits a moderate positive correlation with Information Transparency (.473) and a weaker positive correlation with other factors such as Accuracy and Privacy (.437), Prevention of Financial Fraud (.438), and Regulatory Compliance (.487). Information Transparency has moderate positive correlations with Accuracy and Privacy (.543), Efficiency and Security (.524), and Regulatory Compliance (.550). It also shows weaker positive correlations with Financial Wellbeing (.473), Prevention of Financial Fraud (.461), and Trust and Integrity (.488). Prevention of Financial Fraud has moderate positive correlations with Efficiency and Security (.632), Information Transparency (.461), and Trust and Integrity (.581). It has a weaker positive correlation with Accuracy and Privacy (.543) and a slightly weaker positive correlation with Regulatory Compliance (.503). Regulatory Compliance demonstrates moderate positive correlations with Accuracy and Privacy (.726), Information Transparency (.550), and Trust and Integrity (.715). It has a weaker positive correlation with Efficiency and Security (.609), Financial Wellbeing (.487), and Prevention of Financial Fraud (.503). Trust and Integrity have moderate positive correlations with Accuracy and Privacy (.716), Efficiency and Security (.684), and Regulatory Compliance (.715). It has a weaker positive correlation with Information Transparency (.488) and Prevention of Financial Fraud (.581).

Correlation Matrix.

Note. Table 2 displays the correlation matrix, showing the relationships between variables in the dataset.

Measurement of Variables

The assessment of the incorporated variables was conducted using scales adopted from previous literature. The assessment of financial well-being was conducted using the six-item scale developed by Gerrans et al. (2014) and Prawitz et al. (2006). The perceived benefits of Blockchain banking, namely efficiency, security, and regulatory compliance, have been adopted from Garg et al. (2021) in this study. The incorporation of the mediating variable, perceived information transparency, was derived from the explanatory variable. The measurement of broker information transparency was conducted using a four-item scale adapted from Liu et al. (2015). In addition to the main constructs, the study also included several constructs as control variables. According to Brüggen et al. (2017), the assessment of perceived financial well-being is influenced by personal factors, including gender, age, education, and marital status.

The measurement of the variables in this study followed a methodology that utilized established scales from prior research. In order to evaluate Broker Information Transparency, a four-item scale derived from Liu et al. (2015) was utilized. The scale items were designed to capture customers’ perceptions of the transparency and clarity of their bank’s information, including the disclosure of financial information, access to reliable and accurate information about services, and overall transparency of operations.

The measurement of the Perceived Benefits of Blockchain Banking, particularly in terms of Efficiency & Security and Regulatory Compliance, was conducted using a six-item scale adapted from Garg et al. (2021). The objective of this scale was to measure customers’ perceptions regarding the benefits provided by blockchain technology in terms of improving the efficiency and security of banking services, as well as simplifying compliance with regulatory requirements. The scale items in this study concentrated on customers’ perceptions regarding the enhanced efficiency and security offered by blockchain-enabled banking, as well as its impact on regulatory compliance within the banking sector.

The scale items were designed to capture customers’ perceptions of their level of understanding and awareness of the fraud management measures implemented by their bank. Consistent with previous studies, the researchers have included investors’ gender, age, education, and annual income as control variables. A pretesting survey was conducted in order to finalize the questionnaire design (Afjal et al., 2023). The robustness of the instrument was assessed through pretesting, which evaluated whether the adopted items were appropriate for measuring the relevant constructs and easily comprehensible to the respondents in terms of language, sentence structure, format, and wording.

Data Analysis

The data was examined and analyzed using structural equation modelling (SEM) approaches to test the hypotheses. The utilization of Smart PLS was based on its appropriateness in estimating simultaneous causal relationships among variables. The researchers observed that there is a limited number of studies that have utilized PLS to evaluate SEM in the field of blockchain adoption and financial well-being, based on an extensive literature review. This study aims to address the methodological gap by utilizing partial least squares structural equation modeling (PLS-SEM) to analyze the relationships between studies. PLS-SEM is a technique for estimating intricate cause-effect relationships in path models with latent variables. The utilization of SEM offers the benefit of minimizing measurement error, while also allowing for precise and accurate analysis of the impact of each variable on all other variables (Hair et al., 2012). The collected data was analyzed using a three-step modeling approach developed by Mulaik and Millsap (2000).

Table 3 presents descriptive statistics of the measurement model used in a research study focused on factors related to the financial industry. Each row in the table corresponds to a specific variable representing a factor, and the columns provide relevant information about the items, factor loadings, average variance extracted (AVE), composite reliability (CR), and Cronbach’s α coefficients. The “Variable name” column lists the names of the variables, representing different factors in the financial industry. The “Items” column specifies the items or questions used to measure each variable. The “Factor loading” column displays the strength of the relationship between each item and its corresponding variable. Higher factor loadings indicate a stronger relationship between the item and the underlying construct measures. The “Average Variance Extracted (AVE)” is a measure of the amount of variance captured by the items in relation to the variance due to measurement error. AVE values above 0.5 are generally considered acceptable, indicating that the items adequately represent the underlying construct. The “Composite Reliability (CR)” is a measure of internal consistency reliability, reflecting the extent to which the items within a construct are consistent in measuring the same underlying construct. Higher CR values indicate greater reliability. Lastly, the “Cronbach’s α” coefficient provides another measure of internal consistency reliability. It assesses the average inter-item correlation and indicates the extent to which the items in a construct are correlated with each other. Higher Cronbach’s α values suggest greater internal consistency (Soleimani et al., 2023).

Measurement Model.

Note. Table 3 presents the measurement model, illustrating the relationships between observed variables and latent constructs, assessing the model’s validity and reliability.

The model was utilized to assess the reliability and validity of indicator variables by identifying the connections between latent variables and their indicators, following the recommendations of Hair et al. (2012). Reliability was determined by utilizing the parameters of manifest/indicator reliability and internal consistency reliability (Hair et al., 2012). The determination of validity was based on the parameters of convergent and discriminant validity (Hair et al., 2012). The measurement of convergent validity for the latent variables involved the application of the average variance extracted and outer loading. According to Hair et al. (2017), in order to establish convergent validity. The internal reliability and consistency of the latent variables were assessed using Cronbach alpha and composite reliability. Cronbach alpha is a methodology that calculates reliability estimates by examining correlations between constructs, under the assumption that all constructs possess the same level of reliability. As per Fornell and Larcker (1981), a Cronbach alpha and CR value above 0.70 indicates sufficient internal reliability for the construct.

Table 4 presents the results of the Heterotrait-Monotrait Ratio (HTMT) analysis conducted on various factors related to the financial industry. The HTMT ratio is used to assess discriminant validity by comparing the strength of the relationships between different factors. In the table, the rows represent the focal factor (denominator) and the columns represent the target factor (numerator). The values in the table indicate the HTMT ratio between the focal and target factors. For example, in the cell where the focal factor is Accuracy and Privacy and the target factor is Efficiency and Security, the HTMT ratio is 0.727. This means that the relationship between Accuracy and Privacy and Efficiency and Security is relatively lower compared to the relationships within each factor. The table is symmetric, and the diagonal cells are empty as they represent the HTMT ratios between a factor and itself, which are always 1. Therefore, the diagonal cells are not shown to avoid redundancy. Overall, the HTMT analysis in this table provides insights into the discriminant validity among the factors. Lower HTMT ratios indicate stronger discriminant validity, suggesting that the factors are distinct and not highly correlated. Higher HTMT ratios indicate potential issues with discriminant validity, indicating a stronger correlation between the factors.

Heterotrait-Monotrait Ratio (HTMT) Analysis.

Note. Table 4 provides Heterotrait-Monotrait Ratio (HTMT) analysis, indicating the discriminant validity of the constructs in the model by comparing inter-construct correlations with the correlations of each construct with itself.

Table 5 presents the path coefficients and corresponding p-Values from a path analysis conducted on the relationships between different factors in the financial industry. Path coefficients represent the strength and direction of the relationships between the predictor (independent) variables and the outcome (dependent) variables. p-Values indicate the statistical significance of the relationships. In this table, each row represents a specific relationship between two factors. The first column, “Path coefficient,” displays the estimated strength of the relationship between the predictor factor and the outcome factor. Positive coefficients indicate a positive relationship, while negative coefficients indicate a negative relationship. The magnitude of the coefficient represents the strength of the relationship, with larger values indicating a stronger association. The second column, “p values,” shows the p-Values associated with each path coefficient. p-Values assess the statistical significance of the relationship. A p-Value below a predetermined significance level (usually 0.05) indicates that the relationship is statistically significant, suggesting that the observed relationship is unlikely to have occurred by chance. For example, the path coefficient between Accuracy and Privacy (A&P) and Financial Wellbeing (FW) is 0.020, indicating a positive but relatively weak relationship. However, the associated p-Value is .413, which is higher than the typical significance level of 0.05, suggesting that this relationship is not statistically significant. On the other hand, the path coefficient between Accuracy and Privacy (A&P) and Information Transparency (IT) is 0.202, indicating a stronger positive relationship. Additionally, the p-Value associated with this coefficient is 0.004, which is lower than 0.05, indicating that this relationship is statistically significant. The other path coefficients and their corresponding p-Values follow a similar pattern. Some relationships, such as Efficiency and Security (E&S) to Financial Wellbeing (FW) and Trust and Integrity (T&I) to Information Transparency (IT), have negative coefficients, suggesting a negative association between the factors. However, the statistical significance of these relationships varies.

Path Coefficients.

Note. Table 5 displays the path coefficients, demonstrating the strength and direction of the relationships between variables in the structural model.

Table 6 presents the results of a mediation analysis conducted on the relationships between different factors in the financial industry. Mediation analysis examines the indirect impact of a predictor variable on an outcome variable through one or more mediator variables. In this table, each row represents a specific mediation pathway. The first column, “Indirect Impact,” displays the estimated indirect effect or the extent to which the predictor variable influences the outcome variable through the mediator variable. Positive values indicate a positive indirect effect, while negative values indicate a negative indirect effect. The magnitude of the indirect impact represents the strength of the mediation effect. The second column, “p values,” provides the associated p-values for each indirect effect, it assesses the statistical significance of the indirect effect. A p-Value below a predetermined significance level (usually 0.05) suggests that the indirect effect is statistically significant. For example, the first row in Table 6 suggests that Prevention of Financial Fraud (PFF) has an indirect impact on Financial Wellbeing (FW) through Information Transparency (IT). The estimated indirect impact is 0.031, indicating a positive indirect effect. Additionally, the associated p-Value is .031, which is below the significance level of 0.05, suggesting that this indirect effect is statistically significant.

Mediation Analysis Results.

Note. Table 6 presents the results of the mediation analysis, highlighting the intermediary effects and their significance in the model.

Similarly, the second row indicates that Accuracy and Privacy (A&P) has an indirect impact on Financial Wellbeing (FW) through Information Transparency (IT). The estimated indirect impact is 0.049, with a p-Value of .015, indicating a statistically significant positive indirect effect.

The third row suggests that Regulatory Compliance (R&C) has an indirect impact on Financial Wellbeing (FW) through Information Transparency (IT). The estimated indirect impact is 0.061, with a p-Value of .013, indicating a statistically significant positive indirect effect. The fourth row indicates that Trust and Integrity (T&I) has a negligible indirect impact on Financial Wellbeing (FW) through Information Transparency (IT). The estimated indirect impact is −0.011, suggesting a small negative indirect effect. The associated p-Value is .282, which is higher than 0.05, indicating that this indirect effect is not statistically significant. Finally, the fifth row suggests that Efficiency and Security (E&S) has an indirect impact on Financial Wellbeing (FW) through Information Transparency (IT). The estimated indirect impact is 0.047, with a p-Value of .014, indicating a statistically significant positive indirect effect. The graphical representation of both the direct and indirect impact is reported in GDJG2021281 2 (Figure 2).

Figure 2 depicts the structural model, illustrating the relationships between variables and the overall framework of the study.

After establishing the reliability and validity of the constructs, the conceptual model was transformed into a structural model to test the developed hypotheses. In structural modeling, the relationships among latent variables are evaluated using various criteria. The two common criteria used in this study were the coefficient of determination (R2) and the path coefficients. To assess the structural model, several parameters were examined. Collinearity analysis was conducted to ensure that there were no issues with multicollinearity, which can affect the stability and interpretability of the model.

The coefficient of determination (R2) was calculated for the endogenous variables to determine the proportion of variance in the dependent variables explained by the independent variables. R2 values provide insights into the predictive power of the model. Path-coefficient estimation (β) was used to examine the strength and significance of the relationships between the latent variables. Path coefficients indicate the direct effects of the independent variables on the dependent variables. To test the relevance and significance of the path coefficients and loadings, a bootstrapping technique was employed with 5,000 resamples. Bootstrapping allows for the estimation of standard errors and confidence intervals, providing robust statistical evidence for the significance of the relationships.

Discussion and Conclusion

The stringent regulatory landscape has compelled financial institutions to enhance the transparency of their operations, thereby prompting them to embrace novel disruptive technologies. The past ten years have seen a significant change in the banking industry, as there has been a shift from traditional banking methods to internet banking. This transition has been driven by the need to better serve customers and meet their evolving demands (Tiscini et al., 2020). The growing demand for modern information technology in financial institutions has become a prominent topic of discussion in the realm of performance enhancement and regulation. As the financial landscape continues to evolve, institutions are recognizing the need to leverage advanced technology solutions to stay competitive and compliant. This trend reflects a broader recognition within the industry that traditional approaches may no longer suffice in meeting the complex demands of the modern financial ecosystem. Consequently, financial institutions are actively exploring innovative IT solutions to optimize their operations, enhance their performance, and ensure adherence to regulatory requirements. The emergence of blockchain technology has garnered considerable attention as a cutting-edge internet-based application. Its robust characteristics have led to speculation about its potential implications for the banking system. The expected outcome of implementing this technology is to enhance the efficiency and effectiveness of financial services. The objective of this study was to investigate the extent to which the efficiency, security, and regulatory compliance features of Blockchain contribute to information transparency and improve the financial well-being of customers. The research conducted by Losada-Otálora and Alkire (2019) made a valuable contribution to the ongoing discussion surrounding the effects of information transparency on customer financial well-being. The study put forth the argument that the implementation of Blockchain technology in the banking sector promotes information transparency, ultimately leading to an improvement in individuals’ financial well-being. Consistent with the research agenda outlined by Losada-Otálora and Alkire (2019), the primary objective of this study was to examine the effects of emerging information technologies, specifically Blockchain, on enhancing information transparency. Furthermore, we sought to investigate how this improved transparency subsequently affects the financial well-being of customers.

In line with the theoretical framework of Technological-Structural-Rational (TSR) perspective, the findings of this study provide evidence suggesting that banks could potentially leverage Blockchain technology as a means to enhance transparency. This, in turn, has the potential to play a crucial role in enhancing the overall financial well-being of their customers. By adopting Blockchain, banks can establish a decentralized and immutable ledger system that allows for greater transparency and accountability in financial transactions. This has the potential to address existing challenges related to information asymmetry and lack of trust in traditional banking systems. Consequently, the adoption of Blockchain technology by banks could lead to improved customer confidence, increased efficiency, and enhanced financial outcomes. The present study builds upon and confirms the findings of Brüggen et al. (2017), who put forth the idea that technological interventions have the potential to significantly enhance customer well-being. By expanding upon Brüggen’s work, this study aims to further validate the effectiveness and robustness of such interventions in improving customer well-being. The results of this study indicate that regulatory compliance, which can be considered as a potential characteristic of Blockchain technology, has a noteworthy positive influence on the financial well-being of customers. Similarly, the positive significance of the indirect impact through information transparency is also observed. The potential feature of Blockchain technology as a perceived efficient and secure system has been found to have a significant positive impact on financial well-being. This finding aligns with previous research that has highlighted the indirect effects of such features on various aspects of individuals’ financial lives. By providing a transparent and decentralized platform for transactions, Blockchain technology instills trust and confidence among users, leading to improved financial outcomes. This observation is consistent with the notion that perceived efficiency and security play crucial roles in shaping individuals’ financial behaviors and decisions. Thus, it can be inferred that the indirect impact of these features on financial well-being is an important aspect to consider when examining the potential benefits of Blockchain technology. However, it is worth noting that the current research literature suggests that the direct influence of efficiency and security on financial well-being may not be as significant as previously assumed. Several studies have explored the relationship between these factors and financial outcomes, and their findings have indicated that other variables, such as income level, education, and financial literacy, may play a more substantial role in determining financial well-being. For instance, a study conducted by Smith et al. (Hence, based on the findings of this study, it can be argued that technological interventions like Blockchain can only be considered effective in promoting customer financial well-being if they prioritize and facilitate information transparency. The reliance on information for making informed decisions, especially in the realm of finance, is a prominent aspect of societal dynamics. In addition, it is crucial for financial services to have reliable and valid information. This is particularly important for banks, as they have a vested interest in adopting disruptive technologies that can enhance the reliability and validity of the information they provide. By doing so, banks can improve their information transparency, which in turn can contribute to the financial well-being of their customers. The viewpoint expressed aligns with the findings of Naveed et al. (2021), who proposed that maintaining transparency in bank information is crucial for enhancing customers’ risk tolerance and perceived financial well-being. The results of this study indicate that the impact of Blockchain technology on financial well-being is contingent upon the degree of information transparency. The utilization of Blockchain technology has been proposed as a means to enhance the transparency of bank information, thereby potentially benefiting the financial well-being of customers. The findings of this study provide further support for the assertion made by Brüggen et al. (2017) regarding the significance of technological and behavioral interventions in accurately forecasting an individual’s financial well-being. The viewpoint expressed by the user is consistent with the findings of Nanda and Banerjee (2021). In their study, Nanda and Banerjee argue that enhancing the quality of organizational services can bring about significant positive changes in the subjective well-being of customers. This aligns with the user’s assertion that improved organizational services have a transformative effect on customer subjective well-being.

The study has significant theoretical implications. This study supports Anderson and et al.’s (2013) work and agrees that services can significantly improve customer well-being. The user’s text discusses the importance of disruptive technologies in promoting information transparency and financial well-being. The study builds upon the research of Losada-Otálora and Alkire (2019) and Brüggen et al. (2017), suggesting that innovative information technologies can be beneficial in enhancing information transparency and improving customers’ financial well-being.

The study has practical implications for managers and policymakers, in addition to its theoretical significance. One important research topic in financial well-being is how banks can improve the well-being of individuals and society. The importance of this question is highlighted by the series of financial crises and scandals that have occurred, leading to a decline in trust within the banking industry. This study provides insights that can help financial institutions, such as banks, policymakers, and regulators, enhance the financial well-being of their communities. To achieve their goals, banks and financial institutions can adopt strategies that prioritize transparent information. Bank managers should adopt disruptive technologies to improve the financial well-being of their customers by increasing transparent information sharing. Blockchain-enabled banking can enhance the accuracy and clarity of shared information in banks.

This study’s findings may have significant social implications by promoting greater financial inclusion, transparency, and efficiency in banking services through blockchain technology. Improved access to financial services and trustworthy transactions can enhance the overall well-being of individuals and businesses, contributing to economic stability and social progress.

The adoption of Blockchain-enabled bank transactions would improve the visualization of complex data, making it easier for customers to access and understand. The use of the latter option has potential benefits for customers by reducing fraudulent activities in financial service delivery, which could increase their trust in the banking industry. Trust is crucial in the financial services industry as many economic contracts rely on it. The banking sector in Pakistan is currently dealing with significant issues including FATF jurisdiction, increasing financial scandals, and numerous cases related to money laundering. The transparency of financial institutions is diluted, and bank customers’ mistrust is stirred by these issues. Blockchain-enabled banking offers increased transparency, allowing banks to more effectively monitor operations and detect potential malfeasance and irregularities in the flow of funds. The study examines how perceived information transparency relates to cognitive aspects of financial well-being. Future studies could explore the affective response of customers in relation to their assessment of information transparency, as suggested by literature. Future studies could explore how the cognitive and affective evaluation of information influences customers’ perception of information transparency and financial well-being.

The study emphasizes that various factors can impact how individuals perceive their financial well-being, such as contextual and personal factors (Brüggen et al., 2017). Future research could investigate how the use of Blockchain technology in banking affects customers’ financial well-being.

The findings of this study highlight the importance of conducting further research to gain a deeper understanding of how financial service providers, especially banks, can enhance the financial well-being of their customers. This research aims to provide these providers with specific guidelines and recommendations to effectively address the financial needs and challenges faced by their customers. By delving into this topic, we can contribute to the development of strategies and interventions that can ultimately improve the overall financial well-being of individuals and communities. The complexity and challenges associated with enhancing customer financial well-being have been acknowledged in previous research. However, the present study’s findings indicate that the adoption of disruptive information technologies, which promote information transparency, holds promise for banks seeking to improve the well-being of their customers. The impact of an enhanced level of information technology on information transparency and its subsequent effect on customers’ ability to effectively manage their financial challenges is a topic of interest. It is hypothesized that an improved level of information technology will have a positive influence on information transparency. This, in turn, is expected to increase customers’ propensity to effectively address their financial challenges. Further research is needed to explore the relationship between information technology, information transparency, and customers’ financial management capabilities. Hence, the adoption of Blockchain technology seems to have a positive impact on banks’ operations and service quality. It also has the potential to bring about transformative changes by enhancing transparency and integrity within the banking sector. This, in turn, enables customers to have better control over their finances, leading to an overall improvement in their financial well-being.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: First Author acknowledges the support from National Social Science Fund project “Research on the Mechanism and Countermeasures of Digital Inclusive Finance to Support SME Credit Community Financing” (No. 22BJY076).

Fourth Author acknowledges the support from the Key Project of Education and Teaching Reform of Guangzhou Panyu Vocational and Technical College (Project No.: 2021JG07), and also by Guangdong Higher Vocational Education Teaching Reform Research and Practice Project (Project No. : GDJG2021281).

Data Availability Statement

Data will available on demand.