Abstract

The relationship between analysts’ attention and non-systematic risk significantly influences the stock market, offering the potential to enhance market transparency, mitigate information asymmetry, and impact investor decision-making and market stability. However, previous literature does not construct a rational framework between analysts’ attention and non-systemic risk. In addition, linear and direct relationships are default in existing studies. Thus, employing mediating effect model, this study wants to explore whether an increased focus by analysts can reduce non-systemic risk in stocks. Especially, we address the mediating impact of earnings management and understand heterogeneity and endogeneity issues in the mechanism. We find that analysts’ attention increases the non-systematic risk of stocks and there is an intermediary effect of accrued earnings management in the impact of analysts’ attention on the non-systematic risk of stocks. In addition, under excessive indebtedness, analysts’ attention has a heterogeneous impact on the non-systematic risk of stocks. This study not only constructs a theoretical framework for how analysts’ attention affects the non-systemic risk of stocks, but also explain the indirect relationships by employing mediating effect model. Furthermore, the explanation of heterogeneity and endogeneity enhances the interpretability and effectiveness of the model regression results. Our study will make a great difference in economic risk management.

Introduction

Non-systematic risks in the stock market, which are typically induced by internal firm-specific factors such as poor management, financial instability, and product defects, possess a high degree of specificity and exert differential impacts across various companies or industries (Dowen, 1988). Given the interconnected nature of global capital markets and the universality of corporate operations, non-systematic risk has emerged as a common challenge faced by stock markets worldwide. Although these risks cannot be eradicated by overall market movements, investors can mitigate their adverse effects on investment portfolios to a certain extent through in-depth analysis and effective risk management strategies. Consequently, a profound understanding and proper management of non-systematic risks are essential issues that global investors and market participants must confront; they are also critical factors in enhancing the quality of investment decision-making and ensuring market stability (Arfaoui & Abaoub, 2010).

Analysts’ attention, serving as a market supervision mechanism, may prove to be an effective means of intervening in and resolving issues related to non-systematic risk in stocks. By conducting in-depth research on listed companies’ financial statements, business strategies, industry status, and market environment, analysts are capable of identifying and assessing these firm-specific risk factors. Their research reports and ratings are often regarded as significant market references, contributing to increased market transparency and reduced information asymmetry, thereby enabling investors to more accurately evaluate corporate value and potential risks (Jo & Harjoto, 2014).

In the context of China’s unique financial market environment, the relationship between analyst attention and non-systematic risk warrants particularly rigorous investigation. Compared to mature markets, China’s stock market exhibits higher volatility, a more pronounced retail investor characteristic, and more complex policy influence factors, which compound the complexity of identifying and managing non-systematic risks (Pan & Mishra, 2018). In-depth research by analysts not only provides investors with critical firm-specific risk information, facilitating more informed investment decisions, but also, to a certain extent, guides market expectations, stabilizes investor sentiment, and reduces irrational market fluctuations (Barth et al., 2001; Chatalova et al., 2016).

In the capital market, stock risk is often used to assess the operational status of a listed company (Purnamasari, 2015). Unlike macro systemic risks, non-systemic risk is a localized risk that affects specific companies or industries, without significant impact on the entire market. This risk primarily originates from specific asset factors and is directly linked to a company’s operational or financial conditions (Hartwig et al., 2021; Koziol & Lawrenz, 2012). In theory, these risks can be mitigated through a strategy of diversified investments. This diversified investment strategy helps balance portfolios and mitigate the impact of specific asset or industry fluctuations on the overall investment portfolio (Lintner, 1965; Markowitz, 1952; Mossin, 1966; Sharpe, 1964). Therefore, non-systemic risk significantly influences individual asset pricing and investment returns for investors. However, within the framework of comprehensive registration system environment, regulatory agencies only conduct formal reviews of publicly available information for listed companies. As for the issuer’s business nature, financial strength, quality, and development prospects, they are not considered as review criteria and value judgments (Hu & Wang, 2023). This lenient capital market environment poses more significant challenges for investors in making value judgments and identifying risks. In this context, the role of analysts is once again emphasized. As crucial information intermediaries between investors and listed companies, analysts play a key role in reducing information asymmetry. They, by reducing the information asymmetry between investors and companies, oversee corporate management, thereby influencing the risk level of company stocks to some extent (Ellul & Panayides, 2018; Engelberg et al., 2020; Francis & Soffer, 1997; Luo et al., 2015; Mikhail et al., 2004). Therefore, we want to know whether an increased focus by analysts can reduce non-systemic risk in stocks. Investigating this question will contribute to a deeper understanding of the analyst’s role in the capital market and reveal their potential contributions to risk management.

Currently, studies on the mechanism of the impact of non-systemic risk on stocks primarily includes pricing models, internal factors of companies, and external environments (X. Lu et al., 2012; Sedunov, 2016; Syuzeva & Zheltenkov, 2021). However, these studies to a certain degree suffer from some shortcomings. First, little study introduces analysts’ attention into the framework of non-systemic risk. This makes it difficult to clearly understand how analyst attention affects the non-systemic risk of company stocks, and thus actual impacts are hard to reach. Second, current studies are primarily based on the direct relationship between them, with little exploration of indirect effects in this mechanism. The non-systemic risk of stocks calculated by valuation models is based on the direct relationship with a linear assumption (X. Lu et al., 2012). However, this idealized relationship is rarely shown in the real capital market. Therefore, these studies cannot accurately grasp the reasons for analysts influencing stock risks. Lastly, there is a neglect of endogeneity and heterogeneity analysis. This study discusses the impact of analyst attention on stock risks. The risk level of stocks itself influences the degree of analyst attention (Hou & Hu, 2023; Wen et al., 2019). When analysts select target companies, the risk level may be a crucial factor. If endogeneity issues are ignored, biased estimates may occur. Additionally, the impact of analyst attention on the risk level of companies may vary depending on the category of the enterprise. Compared to companies with lower credit levels, companies with higher credit levels may have different adjustment attitudes toward their operations when facing analyst attention (Batta et al., 2016; Fracassi et al., 2016). Thus, addressing endogeneity and heterogeneity issues will enhance the robustness of the results.

Therefore, the aim of this study is to explore the relationship between analyst attention and non-systemic risk of stocks. In particular, we want to address the following research questions: (1) How does analyst attention explain the non-systemic risk of stocks? (2) What kind of mediating impact does earnings management play in this context? (3) How to understand heterogeneity and endogeneity issues in the mechanism. By addressing these questions, this study contributes to the previous literature in the following ways: Firstly, this study systematically discusses and constructs a theoretical framework for how analysts’ attention affects the non-systemic risk of stocks. Starting from information asymmetry theory and agency theory, the study analyzes the reverse choices that management of listed companies may make when facing shareholders and investors, which provides motivation for the impact on non-systemic risk of stocks. Combining portfolio theory and the Fama-French factor model, the study conducts further analysis on the non-systemic risk of stocks (Fama & French, 2015). Simultaneously, based on the pressure effect, the study proposes a specific pathway through which analysts influence the non-systemic risk of stocks. Second, this study is the first to focus on the mediating role of earnings management in the relationship between analyst attention and the non-systemic risk of stocks. The management of companies may use the autonomy of their accounting systems to engage in profit manipulation and earnings management. They may respond to profit pressures from analysts by making false statements about actual economic performance. This may lead to investors being unable to better identify the true financial situation of the company. Last, the explanation of endogeneity enhances the interpretability and effectiveness of the model regression results. Additionally, distinguishing the level of indebtedness of companies is beneficial for understanding the differential impact from different perspectives.

The structure of this paper is as follows: The second section is a literature review, aimed at introducing the theoretical foundations and research methodologies closely related to this study, and conducting an in-depth analysis of potential endogeneity issues; The third section provides a detailed exposition of the research methods, including the selection and measurement of variables as well as the construction process of the empirical analysis model; The fourth section presents the empirical analysis results, thoroughly discussing the relationship between analyst attention and stock non-systematic risk, and addresses mediating effects and endogeneity issues, further validating the reliability of the research conclusions through robustness tests; The fifth section is the conclusion, where policy recommendations and economic implications are proposed based on the research findings. Considering the unique characteristics of China’s stock market, this paper employs the Fama-French five-factor model to calculate the non-systemic risk and constructs a mediation effect model to examine the mediating role of earnings management between analyst attention and stock non-systematic risk. The study’s results indicate that analyst attention increases corporate earnings management behavior, thereby enhancing the non-systematic risk of stocks. This finding has significant theoretical and practical value for promoting the stable development of China’s capital market.

Literature Review

Theoretical Framework

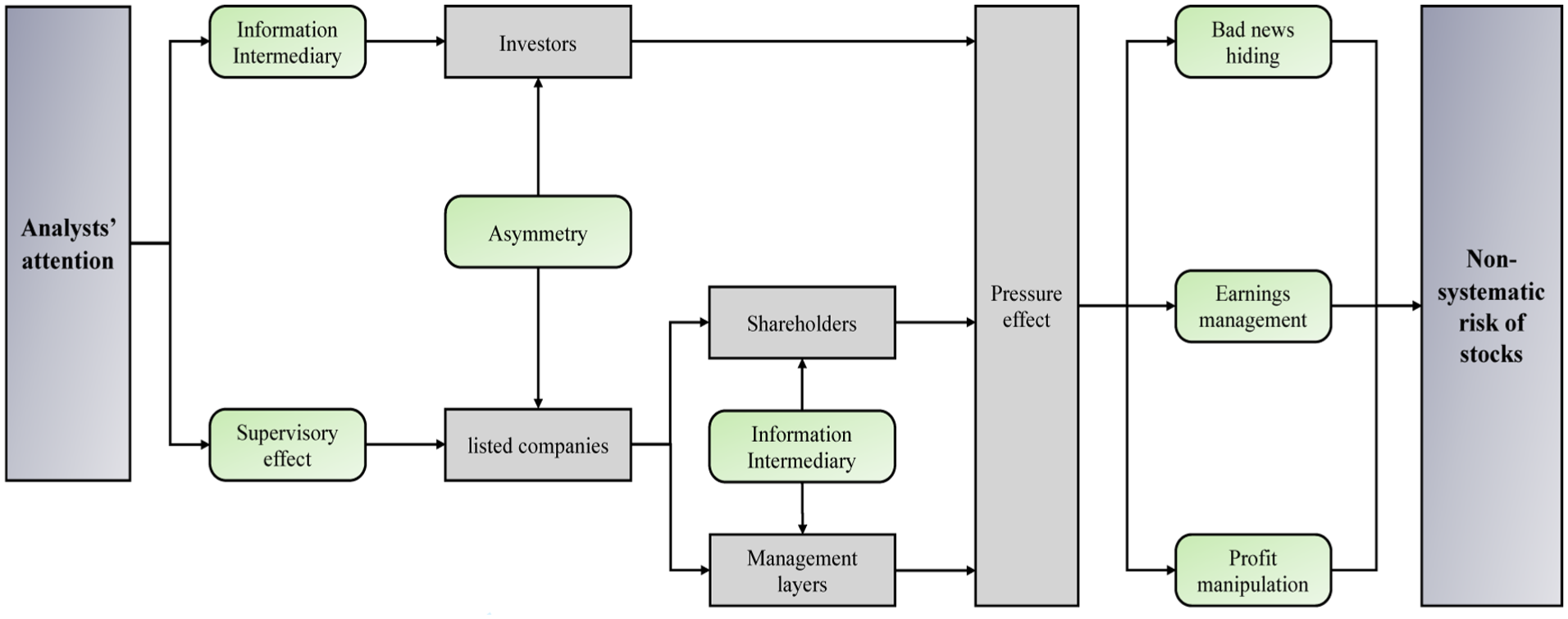

Figure 1 summarizes the mechanism between analyst attention and non-systemic risk of stocks. Analyst attention primarily alleviates the information asymmetry between investors and the listed company (Amiram et al., 2016; Bourveau et al., 2024). Simultaneously, based on agency theory, it also addresses the reverse choices that management of listed companies may make when facing shareholders and investors. This provides motivation for the impact on the non-systemic risk of stocks. Specifically, analyst attention primarily affects the non-systemic risk of stocks through three paths, including concealing bad news, profit manipulation, and earnings management.

The relationships between analyst attention and non-systemic risk of stocks.

Analyst attention influences investor sentiment, which the extant literature widely acknowledges as playing a pivotal role in capital markets (van Eyden et al., 2023). Liu et al. (2024) empirically investigated the impact of brand attention and investor sentiment on the Chinese stock market by analyzing a large-scale comment dataset from the Eastmoney forum. This study revealed significant effects of brand attention and investor sentiment on stock returns and trading volume, noting distinct heterogeneity in these effects across companies with varying brand value. Niu et al. (2023) further refined this perspective, focusing on the dynamic relationship between investor sentiment and industry stock returns in the Chinese stock market. By employing wavelet coherence and wavelet phase angle analysis methods, the study identified varying degrees of association between investor sentiment and industry stock returns under different market conditions. Additionally, cross-regional studies have shown interdependencies in investor sentiment across different regions. Aviral et al. (2021) used sentiment indices and multivariate nonlinear causality tests to uncover causal links between stock market sentiments in various global regions. This study particularly emphasized the necessity of considering nonlinear dynamics and potential structural breaks in capital market analysis, pointing out significant spillover effects of sentiment changes in the Eurozone on U.S., Asian, and Japanese stock markets during financial crises. In the domain of money markets, Sibande et al. (2023) established a direct link between (anti) herd behavior in money markets and investor sentiment, using an investor happiness index based on Twitter data as a proxy variable. The study results supported the significance of investor sentiment in money markets and proposed that real-time investor sentiment signals could serve as an effective tool for monitoring potential speculative behavior in the market. The impact of macroeconomic variables on the stock market is also a focal point of research. Bouri et al. (2018) examined the predictive power of implied volatility in commodity markets and major developed stock markets for implied volatility in BRICS stock markets. The findings indicated that volatility in global and regional stock markets is a key factor in forecasting volatility in BRICS stock markets. Furthermore, Bouri et al. (2020) explored output gaps at different levels to investigate business cycle proxies as potential predictors of volatility in emerging BRICS stock markets. The study noted that despite increased financial integration in global capital markets, emerging economies remain exposed to significant idiosyncratic risk factors in the face of global economic turmoil, which has important implications for global portfolio diversification strategies.

The pressure theory elucidates the external market pressures that companies face, such as market evaluations, media reports, or changes in industry policies (Grégoire & Martineau, 2022; Miao, 2021). These pressures may lead to an increase in non-systemic risks. Under pressure, management may engage in information manipulation, concealment of bad news, profit manipulation, thereby increasing the non-systemic risk of stocks. When a company’s operational performance fails to meet analysts’ predictions, it conveys negative information about the company’s management to the outside world (Sun & Liu, 2011). This leads to a significant decline in stock prices and negative consequences for a company. To avoid these potential negative consequences, management may be compelled to adopt means such as information manipulation, in order to meet or surpass analysts’ profit forecast levels. Relevant studies indicate a close relationship between analysts’ follow-up behavior and aspects of a company, such as earnings management, tax avoidance, and the purchase of audit opinions (Ayers et al., 2018; Kong et al., 2022; Sun & Liu, 2016; Yu, 2008). For example, analyst attention can promote earnings management in companies. In particular, earnings management is divided into real earnings management and accrual-based earnings management. Degeorge et al. (2012) finds that analyst follow-up has an inhibitory effect on real earnings management.

However, accrual-based earnings management has a promoting effect, with management being more sensitive to positive earnings, indicating a substitution effect between accrual-based and real earnings management (Cohen & Lys, 2022; Ipino & Parbonetti, 2017). In addition, analysts also influence companies’ tax avoidance behaviors (Lee, 2021). When star analysts follow listed companies, these companies are more inclined to engage in tax avoidance, and the degree of tax avoidance becomes more pronounced. When analysts cease to follow up, the degree of tax avoidance by listed companies significantly decreases. Research indicate that analysts’ follow-up and issuance of research reports set higher targets for reported earnings for listed companies (Desai, 2003). This induces listed companies to engage in tax avoidance to meet analysts’ targets for earnings forecasts. Studies indicate that the more analysts that track a company, the more likely it is for the company to engage in purchasing audit opinions. When star analysts are among the tracking analysts, companies are more inclined to purchase audit opinions (Graham et al., 2005; Mikhail et al., 2004).

In summary, analyst attention not only affects a company’s earnings management and tax avoidance behaviors but also extends to the purchase of audit opinions. To a certain extent, these behaviors impact the non-systemic risk of stocks through a pressure mechanism.

Analysts’ Attention on Non-systematic Risk of Stocks

This section will explore the topic along two dimensions. Initially, we will provide a comprehensive review of the existing academic literature on analyst attention and non-systematic risk. Subsequently, we will critically assess and analyze the methodologies adopted in current research and their potential limitations.

According to the pressure hypothesis, when a company’s actual performance fails to meet the expectations of analysts, it sends a signal to the market of poor operational efficiency, which may subsequently lead to a significant decline in stock prices, adversely affecting the company (Sun & Liu, 2011). Based on this, management may be motivated to engage in information manipulation or earnings management to achieve or exceed the profit forecasts of analysts. Existing research has shown that the level of analyst attention can influence the company’s earnings management, tax avoidance strategies, and the acquisition of audit opinions, which in turn affect the stock’s non-systematic risk through a pressure mechanism (Degeorge et al., 2013; T. Lu, 2006; Mola & Guidolin, 2009). Specifically, analyst attention can facilitate corporate earnings management (Yu, 2008). Analyst attention has an inhibitory effect on real earnings management, while it promotes accrual earnings management, with this promotional effect being particularly pronounced in situations where management is inclined toward positive earnings, indicating a substitution effect between accrual earnings management and real earnings management (Zang, 2012). Furthermore, analyst attention is closely related to corporate tax avoidance behavior. The presence and number of analysts’ attention are significantly positively correlated with the tax avoidance behavior and its extent of listed companies. Particularly when star analysts pay attention to a company, the company is more inclined to adopt tax avoidance measures, and the degree of tax avoidance is more pronounced. Conversely, when analysts withdraw their attention, the degree of tax avoidance by the company will significantly decrease. This attention indirectly encourages the company to engage in tax avoidance behavior to meet the earnings forecast of analysts by setting higher target earnings (X. Lu et al., 2012). Jiraporn et al. (2012) further reveal the relationship between the number of analysts attention and the company’s audit opinion shopping behavior. The study finds that the more analysts following a company, the more pronounced the company’s tendency to engage in audit opinion shopping, especially when these analysts include star analysts, this tendency is even more significant. Through multi-angle robustness tests, the above conclusion has been further confirmed, indicating that companies have a stronger motivation to obtain more favorable audit opinions through audit opinion shopping behavior when facing more analysts’ attention.

Regarding the approaches in the mechanisms, previous literature primarily employs the following two types. The first is deductive theoretical analysis. Studies utilizing this method emphasize the direct impact factors of non-systematic risk. For instance, Zhou and Han (2018) employed the Analytic Hierarchy Process in conjunction with case study analysis to construct an overarching framework for real estate projects, as well as specific risk indicators for each phase. Experts were invited to score the significance of these risk indicators, thereby exploring the potential for idiosyncratic risk triggers. Ying (2000), grounded in the theory of information asymmetry, analyzed the manifestations, causes, and monitoring mechanisms of non-systemic risks within shareholding commercial banks. Although this method provides a solid theoretical foundation for understanding the factors influencing non-systematic risk, it may be detached from real-world situations and difficult to verify through empirical research. The second is linear regression analysis. Studies using this method generally assume a linear relationship between analysts’ attention and stock non-systematic risk. For instance, X. Lu et al. (2012) conducted an in-depth examination of the traditional Capital Asset Pricing Model (CAPM), which is predicated on the attributes of SMB and HML as factors of idiosyncratic risk and builds related inferences based on these factors. The researchers utilized the residuals of the CAPM model as a proxy for the idiosyncratic risk premium and explored the long-term equilibrium relationship between the CAPM residuals and the SMB and HML factors through cointegration analysis. The results indicated that the SMB and HML factors can significantly account for the idiosyncratic risk premium information embedded in the CAPM residuals. Yu (2008) focused on the role of information intermediaries within the corporate governance structure, particularly the influence of equity analysts on managerial decisions regarding earnings management. The study constructed a multiple linear regression model, considering various indicators of earnings management to assess the impact of analyst activity on such behavior. The findings revealed that in companies with a higher number of analysts, there is relatively less earnings management. Moreover, to address potential endogeneity issues, instrumental variables were employed to enhance the credibility of the research outcomes. While this method can reveal a direct association between the two and clearly indicate the direction and extent of the impact, such an idealized linear relationship is not commonly observed in real capital markets, and it lacks in-depth analysis of endogeneity and heterogeneity. Therefore, in Section 2.3, we will further explore potential endogeneity issues.

Methodology

Variables and Data

Dependent Variable: Non-systemic Stock Risk Based on the Fama-French Model

In economic activities, enterprises and markets jointly contribute to stock risk. The overall performance of the market affects all companies and assets in the environment, making it systematic risk. However, non-systemic stock risk primarily stems from specific asset factors. Since each company operates in a different business environment, non-systemic risk becomes challenging to measure directly. In this context, we define the portion of stock risk excluding market risk as non-systemic risk. We first calculate the systematic risk of stocks. Using the portion explained by market factors in pricing models as the systematic risk caused by market factors, and the unexplained residual part as the non-systemic risk of stocks (Fama & French, 1993). Then, an asset pricing model that best fits the real market is selected. The residual term in the traditional Capital Asset Pricing Model (CAPM) can serve as an indicator for measuring the idiosyncratic risk of stocks. Although the CAPM model has been widely adopted in both academic and practical fields due to its simplicity, empirical research in the Chinese stock market, as pointed out by Yang and Zheng (2021), indicates that the model does not fully adapt to the specific conditions of the Chinese market. Factors such as the growth rate of the Chinese stock market, investors’ risk preferences, and market efficiency all deviate from the assumptions of the CAPM model, leading to the beta coefficient’s inability to adequately explain the impact of market factors on stock return volatility. Therefore, other factors such as the market risk premium factor, market capitalization factor, book-to-market ratio factor, profitability factor, and investment style factor are considered to be taken into account.

Furthermore, the negative skewness model, as a Supplemental Method, assesses the stock’s specific return by regressing the current period’s stock return against the market returns of the current and the preceding and following periods, using the obtained residual value. It then measures the distribution of the stock return distribution that is below the market mean through the skewness of the return. While this method can provide a certain measure of the stock’s idiosyncratic risk, as L. Wu et al. (2016) have pointed out, it has limitations, mainly in that it only considers the risk of stock returns that are significantly lower than market expectations and does not cover the risk of returns that exceed expectations. Therefore, it may be insufficient for a comprehensive assessment of a stock’s idiosyncratic risk.

Fama-French model made modifications to the Capital Asset Pricing Model (CAPM) by adding market value factor, book-to-market ratio factor, profitability factor, and investment style factor on top of the market risk premium factor, providing a more comprehensive measurement of the impact of market factors on stock returns (Fama & French, 2015, 2017). Lin (2017) found that the model has strong explanatory power for the Chinese stock market. Therefore, this study selects the standard deviation of residual values in the Fama-French five-factor model as the proxy variable for measuring non-systemic stock risk. The specific formula is as follows:

Where

Where

The data utilized are derived from the daily return and factor data of the A-share markets of the Shanghai and Shenzhen Stock Board, including those from the Science and Technology Innovation Board and the GEM. These data sources comprehensively cover the Chinese stock market, ensuring both completeness and representativeness

Explanatory Variables and Control Variables

The most straightforward measure of analyst attention is the number of analysts focusing on a company. Therefore, the core explanatory variable is the number of analysts (teams) tracking the company during the fiscal year (

In selecting a time span, this article attempted to match the daily analyst (team) attention with the non-systematic risk daily data obtained in the previous section. However, it was found that this approach would result in a large amount of missing data, as analysts researching on enterprises and writing research reports require a certain amount of time, which cannot be met with daily or monthly data, and annual calculations are more reasonable. Therefore, this article chooses the total number of analysts paying attention to a listed company within an accounting year as the level of analyst attention for that year.

Based on the above considerations, this article believes that the most direct and objective way to measure analysts’ attention is to calculate how many independent analysts (or teams) have conducted tracking analysis on the company within a fiscal year. This processing method can ensure that our results are more accurate and reliable. It should be noted that it is possible for the same analyst or analyst team to publish more than one forecast report for a company within a fiscal year, but the analyst’s attention count is only 1, which is different from the analyst’s attention level brought by a team publishing only one forecast report. Considering the possible impact of these factors, in the robustness test section, this article also used the number of research reports tracked and published by analysts as a replacement indicator to retest the benchmark regression.

In addition, this study selects feature elements related to corporate structure as control variables, all of which can impact the non-systematic risk of stocks. Reward-to-volatility ration (

Where

Annual Turnover Rate (

The data source employed in this study is the CSMAR database, which stands as a leading institution in the financial data services sector in China. It is widely recognized by both the academic and professional communities for the authority and credibility of its data. Notably, the standardized processing and localization characteristics of the CSMAR database confer a unique advantage in reflecting the economic phenomena of the Chinese stock market.

Mediating Variable and Heterogeneity Variable

Based on the previous analysis, the level of accrual earnings management in a company plays a crucial role in the relationship between analyst attention and non-systematic stock risk. This study focuses on the mediating effect of earnings management in the mechanism. Specifically, the expected earnings level is determined through historical financial data, and a comparison with actual earnings is made to determine the presence of earnings management behavior. The modified Jones model is employed to calculate the extent of accrual earnings management in a company (Dechow et al., 1995), serving our purposes effectively:

Where

In addition, this study investigates the heterogeneity impact of excessive debt levels

Where

This study collected daily return data and daily factor data for the Shanghai A-share market, Shenzhen A-share market, including the Science and Technology Innovation Board (STAR Market), and the Growth Enterprise Market (GEM), from 2015 to 2021, totaling 5,174,164 entries. After removing missing data, the annualized idiosyncratic volatility for each stock was calculated, resulting in a total of 10,605 non-systematic risk indicators after annualization. The detailed information on all variables is shown in Table 1.

Variables Description.

Method

In order to examine the fundamental linear relationship between analyst attention and non-systematic risk in stocks, we initially employ the Ordinary Least Squares (OLS) regression model. OLS regression analysis effectively estimates the magnitude and directionality of the impact of analysts’ attention on the non-systematic risk of stocks. As a classic linear regression model, the precision of parameter estimation and the reliability of statistical inference in OLS provide a robust foundation for further exploration of the potential mediating mechanisms between analysts’ attention and non-systematic risk in stocks (Hayes & Cai, 2007). Through OLS regression, we are able to identify and quantify the influence of analysts’ attention on specific risk factors of stocks, thereby laying a theoretical and empirical foundation for an in-depth analysis of the underlying pathways and mechanisms, as well as for subsequent mediation effect analysis.

The dependent variable (

Based on the previous analysis, it is suggested that accrual earnings management plays an intermediary role in the impact of analyst attention on non-systematic risk in stocks. Therefore, the following model is designed to examine the specific effects of this mediating role:

Where

Where, by comparing

Addressing Endogeneity

A prominent manifestation of endogeneity is the bidirectional causality between non-systemic stock risk and analyst attention. Information asymmetry may be one of the causes of endogeneity issues. Information asymmetry often drives analysts to focus on firms with high non-systemic risk, while analyst attention itself can influence market expectations and subsequent stock risk (Bascle & Jung, 2023; Hou & Hu, 2023; Naqvi et al., 2021; Qian et al., 2019). Moreover, firms’ strategic responses, such as information manipulation and financial adjustments, may also affect non-systemic risk, further complicating the causal relationship (Morbee, 2022; Pyka & Wieczorek-Kosmala, 2012).

Therefore, this study employs various methods to control for endogeneity. Firstly, this study simultaneously investigates the impact of analyst attention on the non-systemic risk of stocks in the next period. Since the dependent variable in the next period cannot influence the explanatory variables in the current period, it alleviates the endogeneity issue between analyst attention and non-systemic stock risk. Secondly, this study creates a new explanatory variable derived from previous analyst attention but not influenced by control variables. Whether the endogeneity of control variables leads to biased estimates of key explanatory variables depends on the relationship between control variables and key explanatory variables. If control variables are correlated with key explanatory variables, the biased estimation of control variable parameters will also affect the estimation of key explanatory variables. Therefore, the best approach is to treat control variables as factors, regress the key explanatory variable (analyst attention) against them, and the residual values represent the portion of analyst attention unrelated to control variables. We select the residual values from the regression results as the portion of analyst attention unaffected by the aforementioned factors, which is the net analyst attention number. Then, we study its impact on the dependent variable, which helps alleviate endogeneity caused by control variables.

Result and Analysis

Before conducting empirical regressions, this study first conducts descriptive statistics for the variables in Table 2. The non-systematic risk values of stocks (

Descriptive Statistics.

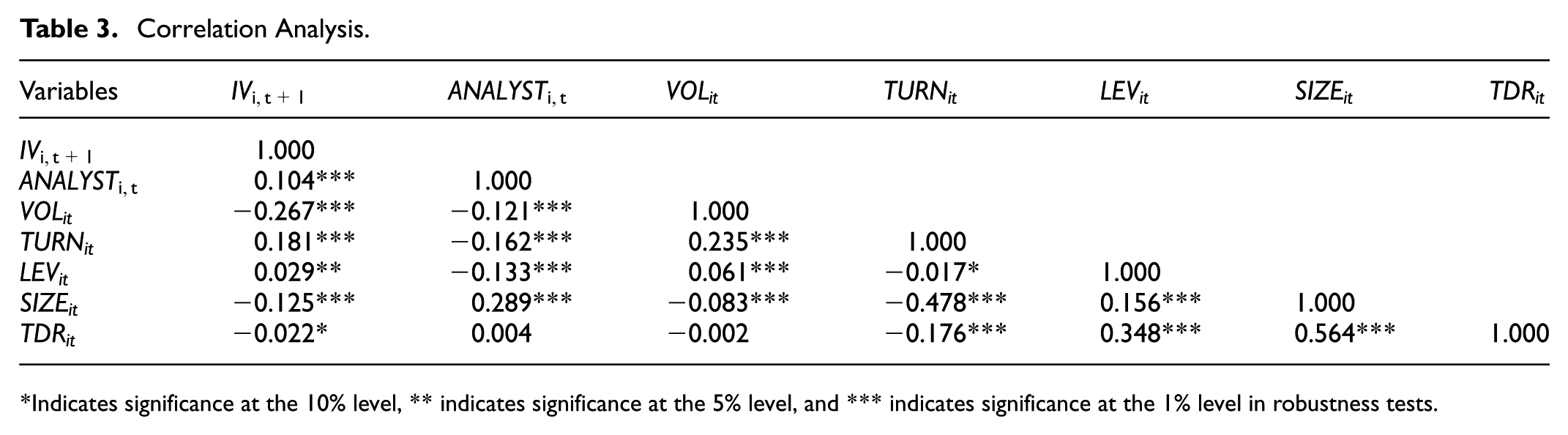

Table 3 displays the correlations among the variables. The correlation coefficients range from .02 to .564, indicating a certain degree of rationality in the selection of variables.

Correlation Analysis.

Indicates significance at the 10% level, ** indicates significance at the 5% level, and *** indicates significance at the 1% level in robustness tests.

Then, the study employs the VIF test to assess multicollinearity issues. As shown in Table 4, the variance inflation factors for different variables are all less than 5, indicating the absence of multicollinearity among the selected variables.

The Results of VIF Test.

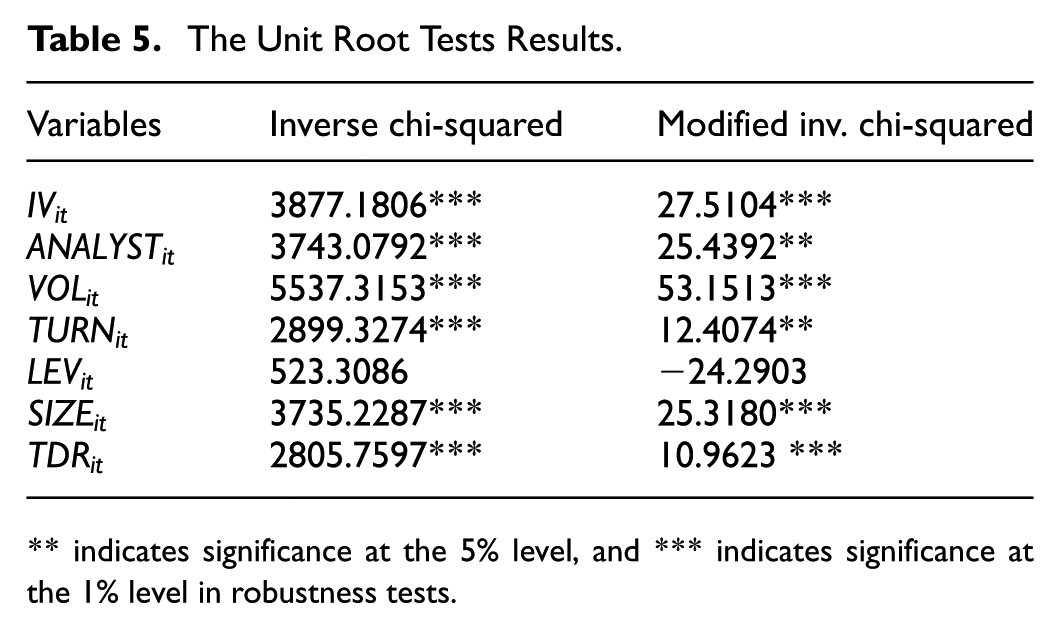

Furthermore, the study conducted unit root tests on all variables to ascertain the applicability of the OLS method. As presented in Table 5, the results indicate that all variables except for the control variable

The Unit Root Tests Results.

indicates significance at the 5% level, and *** indicates significance at the 1% level in robustness tests.

OLS Results

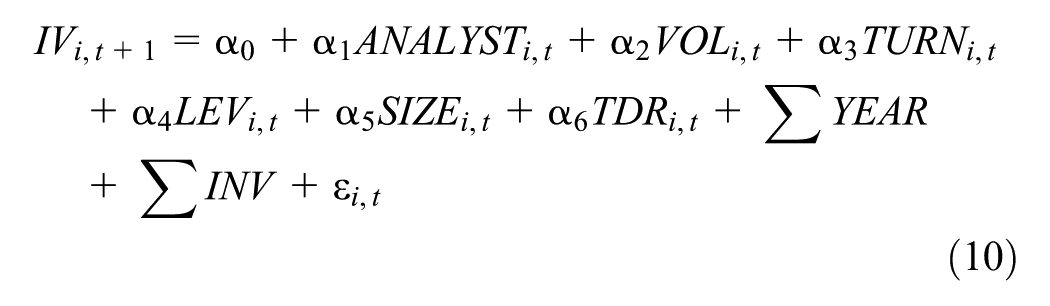

To examine whether there is a linear relationship between analyst attention and non-systematic stock risk, Equation 10 performs OLS regressions on the current non-systematic risk and the future one-period-ahead non-systematic risk. Cluster-robust standard errors are utilized. The regression results are presented in Table 6.

OLS Results.

indicates significance at the 1% level in robustness tests; the values in parentheses represent t values.

From the regression results in columns (1) and (2), it can be observed that the regression coefficients for the analyst attention variable are positive and significantly correlated at the 1% level with both the current and next-period non-systematic stock risks. This indicates a significant positive relationship between the number of analysts’ attention and the level of non-systematic risk in a company’s stocks. In other words, as the number of analysts’ attention increases, the non-systematic risk level of the company’s stocks also increases. This may reflect a high sensitivity of market participants to analyst behavior, where analysts’ opinions, recommendations, or research reports can significantly impact stock prices. Investors may be more inclined to trade in stocks with higher analyst attention, leading to an increase in non-systematic risk. Additionally, analysts’ views may rapidly disseminate through various media and market channels, triggering broader market attention. This amplification effect of information transmission could lead to more investors participating in trading, thereby intensifying the non-systematic volatility of stocks (Cheng et al., 2016; Huang et al., 2014).

Moreover, the collective effect of investor behavior may result in excessive price fluctuations, thereby increasing non-systematic risk. Furthermore, analysts’ views and recommendations may trigger uncertainty about the future development of the company in the market. The results for the next period may further confirm that market participants might overreact to analysts’ information and recommendations, considering them as effective indicators of predicting stock future performance. Analyst research reports may create a buzz in the market, leading to a significant increase in trading activities by investors in the relevant stocks, consequently driving price volatility and increasing non-systematic risk. This overreaction may be due to investors’ high trust in the professionalism of analysts and the rapidity of information transmission and response in the market (Gervais et al., 2001; Klemola et al., 2016; Simon, 1955).

Furthermore, considering the potential lag effect of analysts’ attention, we have introduced the non-systematic risk variable

Figure 2 presents the P–P plot results. Visually, the residuals closely follow the diagonal line, indicating that the observed cumulative probabilities are generally consistent with the expected ones. The de-trended P–P plot further confirms this, showing residuals symmetrically distributed around Y = 0, with the vast majority falling within ±0.04. These results suggest that the normality assumption is reasonably satisfied and support the unbiased estimation of the core explanatory variable ANALYST.

The P-P plot of the model residuals.

Moreover, based on the Central Limit Theorem (CLT), as long as the sample size is sufficiently large, the sampling distribution of regression coefficients approaches normality regardless of the residual distribution(Huber, 1967; Newey & West, 1987). Given that our dataset consists of Chinese A-share firms from 2015 to 2021, with a sample size well over 30, the OLS estimates remain statistically reliable even in the presence of residual skewness.

Finally, we acknowledge that the skewness in LEV may partly result from structural differences across industries, such as varied capital structures or managerial preferences. To address this, our model incorporates industry fixed effects and heteroskedasticity-robust standard errors, which help mitigate biases caused by systematic inter-firm differences (MacKinnon & White, 1985). These adjustments ensure the consistency and validity of the regression estimates even if residuals deviate from strict normality.

The Results of Mediating Effect

Using the level of accrued earnings management to examine its mediating effect on the relationship between analyst attention and non-systematic risk of stocks. Table 7 presents the results of mediating regression analysis.

The Results of Mediating Effect.

Indicates significance at the 10% level, and ***indicates significance at the 1% level in robustness tests; the values in parentheses represent t values.

The impact of analyst attention on emergency earnings management for companies is significantly correlated at the 1% level in column (1), with a positive regression coefficient. This suggests that an increase in analyst attention to a company may elevate its level of accrued earnings management. The results in columns (2) and (3) indicate a significant positive correlation at the 1% level between the level of accrued earnings management and non-systematic risk of stocks in the current and next periods. This signifies that accrued earnings management plays a positive promoting role in the non-systematic risk of stocks. This indicates that accrued earnings management has a positive promoting effect on non-systematic risk of stocks. Combining the theoretical analysis mentioned earlier, when companies engage in earnings management activities due to external pressure, it leads to errors in investors’ analysis and judgment of their financial data, causing deviations in estimations of the company’s future development. As earnings management involves managers making false statements or embellishments about the true economic performance, serving as a negative substitute for accounting information, it damages the foundation of cooperation with investors, significantly impacting investment decisions, leading to a strong reaction in stock prices, thereby increasing the non-systematic risk of company stocks. It can be concluded that the level of accrued earnings management plays a mediating role in the impact of analyst attention on non-systematic risk of stocks.

Heterogeneity Results

This study further discusses the heterogeneous impact of analyst attention on the non-systematic risk of stocks for companies with different levels of liabilities. Regression results are presented in Table 8.

The Heterogeneity Analysis Based on Whether Enterprises are Excessively Indebted.

indicates significance at the 5% level, and ***indicates significance at the 1% level in robustness tests; the values in parentheses represent t values.

To facilitate comparability among regression coefficients, further heterogeneity tests were conducted, and the test results are presented in Table 9.

Regression Coefficient Difference Test.

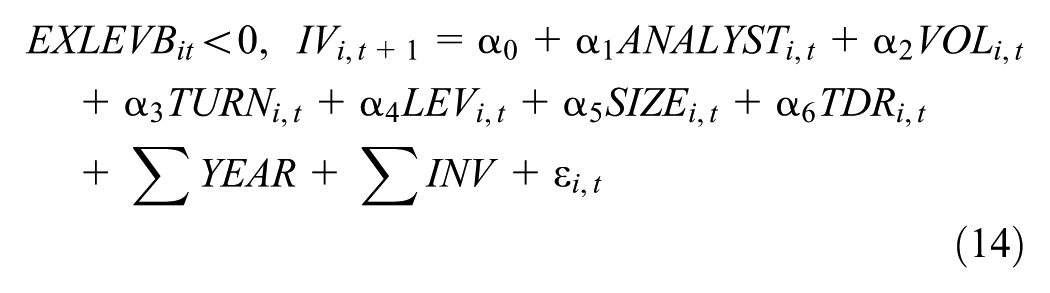

Columns (1) and (2) of Table 8 represent the impact of analyst attention on the non-systematic risk of stocks when companies are excessively leveraged and when companies are not excessively leveraged, respectively. In column (1), the impact of analyst attention on the non-systematic risk of stocks is significant at the 1% level, with a regression coefficient of 0.013. In column (2), the impact of analyst attention on the non-systematic risk of stocks remains significant at the 1% level, but the regression coefficient is 0.011. In the case of excessive leverage, the regression coefficient of analyst attention on the non-systematic risk of stocks is larger. To demonstrate the significant difference between coefficients .013 and .011, the p-value in Table 7 is .0347, which is less than .05, indicating a significant difference between the two coefficients at the 5% level. This implies that for excessively leveraged companies, the positive impact of analyst attention on the non-systematic risk of stocks is more significant. Due to the decline in investment attractiveness, combining the theoretical analysis mentioned earlier, companies with significant debt pressure may be less able to withstand the increase in financing costs. The investment attractiveness of companies may further decline because of the analyst attention. Whether it’s a decline in stock prices or an increase in bond interest, it will worsen the company’s financing pressure, motivating companies to engage in earnings management to meet analyst forecast levels, thereby increasing the non-systematic risk of stocks. Therefore, the results suggest that for those companies with excessive debt, the impact of analyst attention on the non-systematic risk of their stocks is more significant, while for companies with normal debt levels, the impact of analyst attention on their non-systematic risk of stocks is smaller.

Endogeneity Test

Theoretically, this study has already discussed the endogeneity issue between analyst attention and non-systematic risk of stocks. Empirically, endogeneity cannot be completely avoided. Therefore, the regression results in the previous sections provide relatively weak support for the research questions. Despite a series of robust empirical results presented earlier, they confirm a correlation rather than causation. The operating conditions and financial performance of companies themselves may influence analysts’ preferences for attention. In this study, companies with excessively high non-systematic risk of stocks may signify internal issues that are more worthy of exploration and disclosure, leading to an increase in analyst attention. While the inclusion of the next-period dependent variable in the regression model in the earlier sections partially controls for endogeneity, larger firms and those with higher financial leverage may still attract increased analyst attention as a control variable.

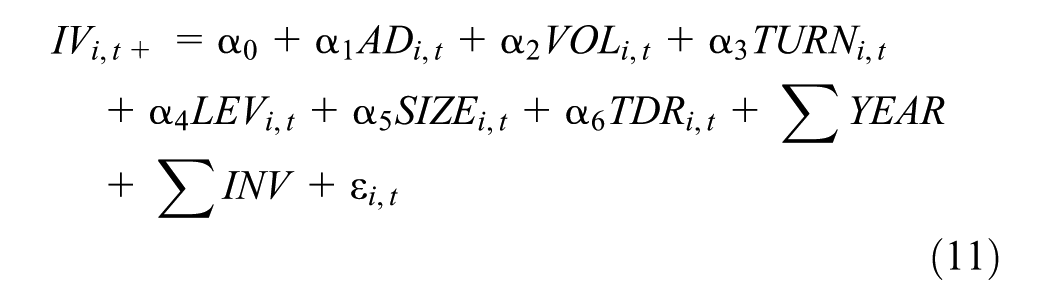

Whether the endogeneity of control variables will lead to bias in the parameter estimation of key explanatory variables depends on the relationship between the control variables and the key explanatory variables. If control variables are correlated with key explanatory variables, the bias in the parameter estimation of control variables will also affect the parameter estimation of key explanatory variables. Therefore, this study creates a new explanatory variable derived from previous analyst attention but not influenced by control variables. The best way is to treat control variables as factors and regress the key explanatory variable, analyst attention, on them. The residual values in the regression results represent the part of analyst attention that is unrelated to control variables. Specifically, following the method used by Yu (2008) to address endogeneity issues in analyst attention, this study regresses the main control variables on the explanatory variable analyst attention, and selects the residual values from the regression results as the part of analyst attention not influenced by the above factors, namely the net analyst attention. Then, we use the net analyst attention as a replacement variable for analyst attention to regress it on the main Equation 10 to alleviate the endogeneity issue, and the regression results are shown in Table 10.

The Endogeneity Results of Net Analyst Focus and Non-systemic Risk in Stocks.

indicates significance at the 1% level in robustness tests; the values in parentheses represent t values.

As shown in Table 10, the positive impact on the non-systematic risk of stocks in the current and next periods remains significant at the 1% level. This result effectively confirms the earlier conclusion that analyst attention increases the non-systematic risk of stocks for companies.

Robustness Tests

This study used the number of analysts (teams) to measure analyst attention. However, this measure did not account for individual attention differences. Therefore, we used the number of research reports tracking a company as a substitute variable for analyst attention and re-conducted regression analysis. The regression results are presented in Table 11.

The Results of the Robustness Tests.

indicates significance at the 1% level in robustness tests; the values in parentheses represent t values.

As shown in Table 11, after using the indicator of

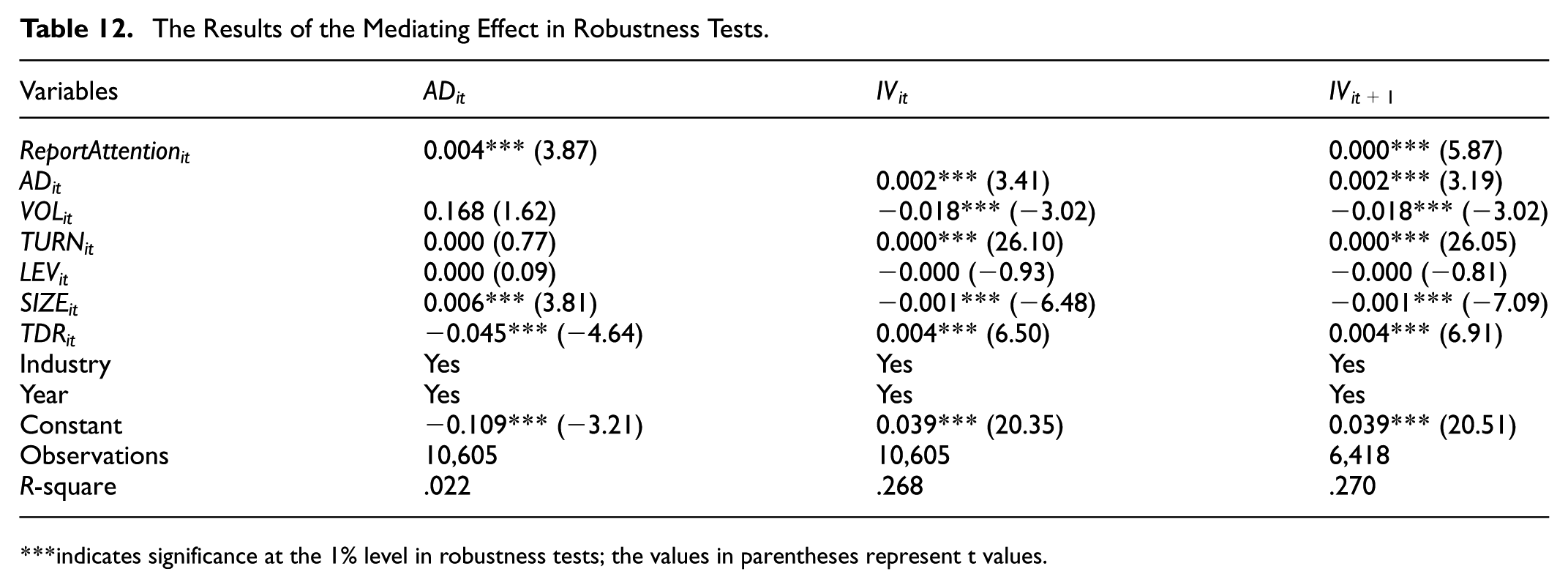

Likewise, we conducted a robustness test for the mediating effect, with results presented in Table 12. After employing the substitute variable

The Results of the Mediating Effect in Robustness Tests.

indicates significance at the 1% level in robustness tests; the values in parentheses represent t values.

Conclusions

In the stock market, non-systematic risks are triggered by internal company factors, such as the efficacy of management, the stability of financial conditions, and issues with product quality. These risks exert differentiated impacts across various companies and industries. Despite the interconnectedness of global capital markets, investors can mitigate these risks through in-depth analysis and risk management strategies. In China, the complexity of market volatility, the characteristics of retail investors, and policy influences make the in-depth research by analysts on listed companies particularly crucial for the identification and management of non-systematic risks. Such research helps to enhance market transparency, reduce information asymmetry, foster prudent investment decisions, stabilize market expectations, and diminish irrational market fluctuations.

This study explores the effects of analyst attention on non-systematic risk of stocks in theory and empirical. Especially, we address the mediating impact of earnings management and understand heterogeneity and endogeneity issues in the mechanism. This study not only constructs a theoretical framework for how analysts’ attention affects the non-systemic risk of stocks, but also explain the indirect relationships by employing mediating effect model. Our study will make great difference in improving the accounting policies and external supervision mechanisms of listed companies, as well as enhancing various mechanisms in the capital market. Overall, we have demonstrated the important role of analyst attention in non-systematic risk, both in direct and indirect. Specifically, this article mainly draws the following conclusions.

Firstly, analysts’ attention increases the non-systematic risk of stocks. Analysts’ attention reveals more operational issues or makes profit forecasts that companies cannot achieve, leading to negative management under pressure. Therefore, this elevates the non-systematic risk of stocks. Secondly, there is an intermediary effect of accrued earnings management in the impact of analysts’ attention on the non-systematic risk of stocks. When companies face the pressure effects generated by analysts’ attention, they engage in profit manipulation and earnings management by exercising a certain degree of autonomy granted by the accounting system. This involves making false statements or embellishments about the actual economic performance to address the profit pressure from analysts, thereby increasing the non-systematic risk of stocks. Thirdly, there is endogeneity between analysts’ attention and the non-systematic risk of stocks. Companies with higher non-systematic risk experience higher heterogeneous volatility in stock prices, attracting more analyst tracking and attention. This study introduces the next-period non-systematic risk of stocks and net analyst attention variables, demonstrating that endogeneity issues do not affect the conclusions of this study. Lastly, under excessive indebtedness, analysts’ attention has a heterogeneous impact on the non-systematic risk of stocks. Faced with the pressure from analysts’ attention, companies with excessive debt experience a greater increase in non-systematic risk of stocks. Overleveraged companies face greater operational pressure, have more motivation for earnings management and profit manipulation, leading to a greater increase in non-systematic risk of stocks in response to analysts’ attention.

Our findings have potential policy implications and economic significance. Our research uncovers a significant impact of analyst attention on corporate earnings management, which prompts a more comprehensive consideration of the role analysts play in corporate operations. On one hand, it is imperative to enhance the supervisory effect of analysts on companies and to establish a more robust intermediary bridge of information between investors and enterprises. This involves refining the codes of conduct for securities firms and analysts, intensifying the supervision of analysts’ behavior in the capital market, and amending and perfecting relevant laws and regulations. On the other hand, we must also be cognizant of the pressure effect that analyst attention can exert on companies. Listed companies may focus excessively on short-term profit performance due to the scrutiny of analysts, engaging in earnings management and profit manipulation, which distorts investors’ judgment of the company’s investment value and increases investment risk. In light of this, it is necessary to restructure the accounting policies and external supervision mechanisms of listed companies, enhance the transparency of information, thereby enabling investors to more accurately analyze the potential intrinsic value of listed companies and mitigate non-systematic risk.

A more comprehensive understanding of the impact of analysts on corporate operations, recognizing the pressure effects of analysts’ attention on companies. Additionally, improving accounting policies and external supervisory mechanisms for listed companies, establishing a more reasonable agency mechanism, and reducing market information asymmetry are recommended. Furthermore, enhancing various mechanisms in the capital market and advocating value investment can provide a more positive market environment for analysts’ information discovery and value analysis. The economic significance of this study lies in highlighting that analysts’ attention may induce management to engage in earnings management to meet market expectations. Such behavior could potentially obscure the true financial status of the company, thereby increasing the non-systematic risk faced by investors. The heightened risk necessitates that investors conduct more prudent assessments of corporate financial reports and market information to identify potential earnings manipulation, leading to wiser investment decisions. Furthermore, this research underscores the role of regulatory bodies in supervising and regulating corporate financial reporting to ensure market fairness and transparency, safeguarding investor interests and market health.

However, this study also has some shortcomings. Besides accrued earnings management, real earnings management and other mechanisms may also play an intermediary role in the impact of analysts on the non-systematic risk of stocks. Since real earnings management pertains to adjustments in actual corporate operations, it typically requires access to more detailed internal data, which are often difficult to obtain. Consequently, these variables are overlooked in the current research, yet they do not significantly impact the conclusions drawn in this paper. The role that real earnings management plays in the influence of analysts on the non-systematic risk of stocks is an issue that warrants in-depth exploration in future research. This is not only related to a more comprehensive understanding of the multifaceted effects of corporate earnings management but also pertains to assessing the potential impact of analysts’ behavior on the long-term value of companies and the stability of the market. Moreover, the study identifies a correlation between the overall stock price volatility and heterogeneous return volatility during the empirical process, suggesting a potential direction for future research.

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Our research received the financial support from: the Humanities and Social Science Fund of Ministry of Education of China [Grant Number: 22YJA790017], National Natural Science Foundation of China [Grant Number: 71772013], and Beijing Institute of Technology Science and Technology Innovation Program “Beili Zhiku” Promotion Plan [Grant Number: 2024CX13006].

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data can be available on request.