Abstract

Maturity mismatch between investment and financing is a major potential risk faced by firms in recent years, which also concerns the controllability of macroeconomic movement risk and the quality and efficiency of economic development. This study explores the mitigation measures of maturity mismatch from the important governance mechanism of Non-controlling Large Shareholders (NCLSs) exit threats. Taking Chinese listed companies on the A-share market over the period 2010 to 2020 as a sample, we find that the exit threats of NCLSs significantly alleviate the degree of maturity mismatch. Furthermore, we investigate the moderating role of the attention of market parties (analyst, media, and investor) on the above relationship. We find that the higher the attention of market parties, the more significant the inhibitory role of NCLSs exit threats on the maturity mismatch. Based on the above research results, we propose countermeasures and suggestions for firms to construct a reasonable ownership structure for NCLSs to engage in corporate governance flexibly and effectively.

Plain language summary

Purpose: This study examines the impact of the exit threats of Non-controlling Large Shareholders (NCLSs) on the maturity mismatch between investment and financing of firms, and the moderating effect of the attention of market parties (analyst, media, and investor) on the above relationship. Methods: The sample of Chinese listed companies on the A-share market over the period 2010–2020 is used for empirical analysis. Conclusions: The results show that the exit threats of NCLSs significantly alleviate the degree of maturity mismatch. The higher the attention of analysts, media, or investors, the more significant the inhibitory effect of the exit threats of NCLSs on the maturity mismatch. Implications: This study helps to understand the causes of maturity mismatch in Chinese listed companies, provides new ideas for how to alleviate this problem, and provides a true and reliable empirical reference for NCLSs to take a flexible and effective way to participate in corporate governance and improve corporate investment and financing decisions.

Keywords

Introduction

According to Morris (1976), rational companies should choose a financing scheme that aligns with their investment duration to minimize the risk of failing to meet debt interest payments due to inadequate cash flow from investment projects. However, in reality, it is common for firms to experience maturity mismatch by using short-term liabilities to fund long-term investments (Bai, 2022a; Cheng, Chiao, et al., 2020; Wang et al., 2021). Both theoretical and empirical evidence suggest that maturity structure driven by short-term liabilities is prone to liquidity risk (Gopalan et al., 2014). The long payback period for long-term investments does not bring sufficient cash flow promptly, so maturity mismatch will magnify the debt service pressure on maturing debts and put the company in financial distress (Bleakley & Cowan, 2010). Such a high-risk behavior may even jeopardize the stability of the entire financial system (Brunnermeier & Oehmke, 2013). In response to COVID-19, commercial banks have become more cautious, frequently withdrawing or reducing loans to mitigate potential risks (Nehrebecka, 2021). As a result, the risk of maturity mismatch has emerged as a significant concern for firms in recent periods, especially in capital markets when market shocks are superimposed (Cheng, Chiao, et al., 2020).

Nowadays, China has involved the “new normal” development mode, and the central government has clearly stated that it must “fight a tough battle to minimize and resolve major risks” and “hold baseline of no systemic financial risks.” One of the micro guarantees to achieve the above macro goals is to prevent the investment and financing term mismatch at the enterprise level. However, the maturity mismatch is particularly acute in China. Long-term financing instruments in the financial market primarily consist of equity, bond, and long-term bank loans. However, the development of Chinese stock and bond markets has been relatively slow, making it challenging for firms to raise equity and bond financing (Bai, 2022a). In the Chinese financial system, banks serve as the primary suppliers and dominant players of financial resources (Allen et al., 2017). Due to pervasive credit discrimination in capital markets and the liquidity premium associated with long-term versus short-term loans, which cannot adequately offset the uncertainty of new liabilities, banks prefer short-term credit facilities to long-term ones (Custódio et al., 2013). In general, firms struggle to negotiate favorable credit covenants with banks and thus have difficulty in obtaining long-term credit facilities (Fu, 2020; Tan et al., 2016). Additionally, because banks are heavily influenced by the government in China, lots of bank loans are allocated to “zombie companies,” which makes it increasingly challenging for other companies to secure bank loans (Fu, 2020). In a financing-constrained environment, relying on short-term debt to sustain long-term investments turns into a forced selection for companies.

Previous studies on Chinese capital market also indicate that, in addition to institutional flaws, human inducements are also important in exacerbating the maturity mismatch. Sun (2019) finds that the irrational behavior of management triggers blind and herd investment and makes the debt maturity structure short, which eventually leads to maturity mismatch. Ding et al. (2020) show that greater autonomy in subsidiaries is accompanied by more serious agency problems among managers and a heightened risk of maturity mismatch. Lai et al. (2019) find that, as a mechanism of risk transfer, directors’ and officers’ liability insurance can encourage management to engage in riskier decision-making behaviors, which in turn exacerbates the degree of maturity mismatch. In Chinese listed companies, the shareholding structure is defined by a high concentration of equity among large shareholders, with controlling shareholders often leveraging their control and information advantages to violate the rights of non-controlling shareholders (Jiang et al., 2015). Gao and Liu (2012) investigate the influence of the equity characteristics of ultimate controlling shareholders on corporate investment and financing strategies and find that either overly concentrated or dispersed equity of the controller triggers the maturity mismatch. Zhong et al. (2018) find that as family controllers hold a larger share of control, the maturity mismatch becomes more pronounced, driven by the intensified self-interest of controllers and banks’ agency risk control efforts. Hence, it is evident that the paramount concern in crafting corporate governance mechanisms for Chinese listed companies lies in effectively overseeing managerial opportunism and curbing the self-interested encroachment by controlling shareholders, which is crucial for mitigating maturity mismatches.

Following the implementation of China’s shareholding reform and the deepening of the mixed ownership reform, the average shareholding ratio of controlling shareholders in listed companies has been on a downward trajectory, contrasting with a notable increase in the number of companies with the NCLSs (as shown in Figure 1). Within the current framework of corporate governance, NCLSs hold a uniquely significant and distinct position, characterized by their dual status as “non-controlling shareholders” and “non-small and medium shareholders,” which can not only effectively supervise the management, but also form mutual constraints with controlling shareholders (Kang & Kim, 2012; Mancinelli & Ozkan, 2006). Both theoretical and empirical research have demonstrated that the governance influence wielded by large shareholders can be categorized into three core mechanisms: the voice mechanism, encompassing active participation and voting; the exit threat mechanism, wherein the potential sale of shares serves as a leverage point; and the exit mechanism, which involves the actual selling of shares as a final measure. The existing literature has explored the voice mechanism and exit mechanism in great depth (Bebchuk et al., 2015; Cheng, Lin, et al., 2020; Cheng, Liu, et al., 2020; Gillan & Starks, 2000; Helwege et al., 2012; Hu et al., 2019; Hui & Fang, 2022; Parrino et al., 2003; Qian, 2011; Yan & He, 2018). In the past few years, the governance impact of the exit threat mechanism has gained prominence and become a focal point of interest in corporate governance, particularly with the advent of behavioral finance (Bai, 2022b; Sun et al., 2021; Xu et al., 2022). Previous studies show that large shareholders exit serves as a check on the self-interested actions of major shareholders and managers (Hope et al., 2017), reduces dual agency costs (Chen, 2019), improves information quality (Dou et al., 2018), and promotes firm innovation (Bai, 2022b; Helling et al., 2020). Nevertheless, there is no literature to examine whether the exit threats of NCLSs can effectively inhibit the high-risk behavior of maturity mismatch. Therefore, this paper draws upon a dataset of Chinese listed companies on the A-share market over the period 2010 to 2020 to empirically examine the effect of the exit threats of NCLSs on the maturity mismatch and further examines the moderating role of the attention of market parties (analyst attention, media attention, and investor attention) on the above relationship to dig deeper into the external conditions that strengthen the role of NCLSs’ exit threat.

The yearly trends in the mean shareholding ratio of controlling shareholders and the count of listed companies with NCLSs.

This article has the following innovations: first, earlier studies treat shareholders other than controlling shareholders as the same group and assumed that these shareholders have weak monitoring ability (Chen et al., 2022), while this article takes into account the heterogeneity and contestability among shareholders and focuses on NCLSs with larger shareholdings, who are more inclined to engage in corporate governance instead of merely “free-riding” (Grossman & Hart, 1980), so the governance effects exerted by NCLSs align more closely with the governance practices characteristic of Chinese listed companies. Second, distinguished from the prevailing studies that concentrate on the corporate governance effect of NCLSs through voting-by-hand and voting-by-feet (Cheng, Chiao, et al., 2020; Hui & Fang, 2022; Yan & He, 2018), this article delves deeper into the effect of NCLSs in corporate governance through exit threats and also provides new evidence on the market conditions needed to strengthen the governance effect of the NCLSs exit threats from the perspective of the attention of market parties (analyst attention, media attention, and investor attention), which significantly contributes to the enrichment and advancement of research within the sphere of corporate governance. Third, given that there may be affiliation or concerted action relationships among shareholders (Bennedsen & Wolfenzon, 2000; Cheng et al., 2013; Cai et al., 2016), this article aggregates the shareholdings of concerted action holders to more accurately portray the actual shareholdings of listed companies and meticulously takes into account the “status” of large shareholders to rigorously distinguish NCLS from controlling shareholders and internal shareholders, thus providing more realistic and reliable findings on the influence of NCLS on listed companies. Fourth, previous literature has mainly examined the impact of NCLSs on a solitary facet of investment and financing decisions from the vantage point of the ownership structure characterized by multiple major shareholders (Jiang, Cai, et al., 2018). This study investigates the influence of the exit threats posed by NCLSs on maturity mismatch from the dual dimension of the investment-financing relationship, offering a significant contribution and enhancement to the current research on how NCLSs affect corporate investment and financing decisions. Fifth, previous literature has primarily delved into the mitigation measures for maturity mismatch by examining the macroeconomic or institutional environment factors that are beyond corporate control (Bai, 2022a). From the perspective of NCLSs, who are the main bearers of the risks and adverse consequences caused by maturity mismatch, this article investigates whether and how the exit threats of NCLSs affects maturity mismatch, which enriches and expands the study of the factors influencing maturity mismatch on the micro-governance level.

Theoretical Analysis and Research Hypotheses

Whether the maturity mismatch represents an intentional decision by controlling shareholders and management for irrational or self-interest motives, or a passive decision of the company in response to external financing constraints, it will trigger an increase in corporate risk and a decline in share price, which seriously restricts the sustainable development of the company (Bleakley & Cowan, 2010; Cheng, Chiao, et al., 2020). For NCLSs who maintain a significant shareholding and are invested in the company’s long-term growth, such a high-risk behavior will undoubtedly harm their wealth, and thus NCLSs possess a compelling incentive and the ability to inhibit the maturity mismatch through the threat of exit.

On one hand, NCLSs are highly motivated to inhibit the maturity mismatch through the threat of exit. In contrast to relatively small shareholders who exhibit a “free-rider” motivation (Grossman & Hart, 1980), NCLSs hold a substantial equity stake in listed companies, and their interests are more profoundly impacted by the maturity mismatch, so NCLSs have an incentive to monitor and restrain it. In Chinese listed companies, the shareholding of large shareholders is highly concentrated, and the phenomenon of “rule by the voice of one person” is serious (Jiang et al., 2015). As a result, the decision-making process is likely to become a formality, which hinders the channels for NCLSs to directly intervene in corporate decision-making through the voice mechanism. As China’s shareholding reform reaches its fruition, the gradual implementation and batch expansion of securities margin trading and short selling, alongside the improved traceability of stocks within the financial market, conditions have been created for the implementation of exit threats by NCLSs (Bharath et al., 2013; Edmans et al., 2013; Sun et al., 2021). Before NCLSs completely exit the company, they are inclined to employ exit threats as leverage in negotiations with the controlling shareholder and management, and influence corporate decision-making by threatening them that “selling the shares held will cause share price to plummet.” Based on the above analysis, given the strong will to govern, the obstruction of the voice mechanism, and the background of the significant increase in stock liquidity, NCLSs are motivated to use exit threats to restrain the self-interest of controlling shareholders and management, thus curbing the maturity mismatch.

On the other hand, NCLSs are also well-positioned to mitigate the maturity mismatch through exit threats. Distinct from controlling shareholders with absolute control, NCLSs do not invest in listed companies to acquire and maintain a long-term control position (Xu et al., 2022), which provides convenience for them to influence corporate governance through the strategic deployment of “exit threat.” Once NCLSs perceive that the controlling shareholder and management have self-interest motives in the investment and financing decision, and the direct intervention has little effect, exit threats become a “sharp tool” for NCLSs to restrain the controlling shareholder and management before implementing the exit mechanism. According to the signaling theory, as informed traders, NCLSs’ abnormal exit behavior can signal market concerns like overvaluation and poor growth prospects, potentially triggering a herding effect that leads to plummeting stock prices and substantial losses for controlling shareholders and management (Edmans & Manso, 2011; Dou et al., 2018). The exit threat theory also points out that to avoid the above adverse effects, the controlling shareholders and the management may take measures in advance to stop NCLSs from exiting (Bharath et al., 2013). Therefore, when the exit threats are implemented by NCLSs, controlling shareholders and management will try to meet NCLSs’ demands, thus actively reducing irrational or self-interest-motivated maturity mismatch. Additionally, from the vantage point of the information supervision mechanism, the governance role of NCLSs exit threats is capable of enhancing financial reporting quality (Dou et al., 2018), which helps to effectively transmit favorable information about the company and facilitate creditors such as banks to track the corporate operating conditions, thus alleviating the information risk of banks and enhancing their earnings guarantees, which in turn facilitates the establishment of stable long-term credit contracts between the two parties. When banks are inclined to accommodate corporate demand for both long- and short-term funds, companies can cease to depend on short-term liabilities, consequently reducing the degree of maturity mismatch. In summary, this article posits that:

H1: Ceteris paribus, the exit threats of NCLSs can reduce the maturity mismatch.

If the exit threats of NCLSs can effectively reduce the maturity mismatch, then what external conditions can amplify the impact of these threats? Given the finite nature of time and energy, the attention of market parties, as a scarce resource, exerts a significant role on capital market transactions and pricing (Chen et al., 2022; Dang et al., 2020; Jiang, Zhou, et al., 2018). So, how will the attention of market parties affect the effectiveness of the exit threats of NCLSs on the maturity mismatch?

First, we consider the impact of analyst attention. As a bridge for the information transmission of the capital market, analysts are more sensitive to the exit intention and exit behavior of NCLSs. Analysts can not only use their professional knowledge and skills to deeply interpret the public information of listed companies and their industries (Huang et al., 2017), but also collect, organize, and mine the undisclosed information of companies through internal channels such as telephone interviews, interviews and site visits (Cheng et al., 2016). Analysts make use of their information advantages and analytical ability to make value judgments and write analysis reports, which helps company-level idiosyncratic information to be used by investors and reflected in the stock price through securities trading (Jiang, Zhou, et al., 2018). Therefore, under the influence of analyst attention, investors can respond more promptly and correctly to negative information when NCLSs intend to exit the company, causing a greater drop in stock prices and a greater degree of damage to the wealth of controlling shareholders and management. At this time, the exit threats of NCLSs on maturity mismatch are more effective.

Second, we consider the impact of media attention. As a capital market information delivery platform, the media naturally pay close attention to hot issues such as the exit behavior of NCLSs, and media focus on this event can better attract the attention of small and medium-sized investors who are at an information disadvantage (Bushee et al., 2010), assist investors in more accurately gauging the company’s risk, thereby integrating specific firm information into stock price (Dang et al., 2020), then the cost of controlling shareholders and management to take advantage of the maturity mismatch is greatly increased. In addition, media attention can also play the external governance role of public opinion supervision, the media reports for NCLSs’ abnormal exit behavior will cause the spontaneous concern of the social public, and strong public pressure will affect the image and reputation of the controlling shareholders and management (Dyck et al., 2008), which can restrain their improper behavior in the process of investment and financing decision-making. Therefore, under the influence of media attention, the exit threats of NCLSs have a stronger inhibitory effect on maturity mismatch.

Third, we consider the impact of investor attention. In the capital market, investors’ information-seeking behavior and their attention have a particularly important impact on the market (Chen et al., 2022; Welagedara et al., 2017). Greater investor attention allows for more efficient and prompt interpretation of pertinent information, accelerating the dissemination of that information. Especially for institutional investors, when they pay more attention to a particular stock, they can capture and dig more private information about the company with their professional skills and experience. Even ordinary investors, can comment or ask questions about a stock trading at any time and get answers in real-time in the self-published media with the characteristics of instant communication, which improves their understanding of the disclosed information and trading conditions in the market. Investor attention can significantly mitigate the information asymmetry among companies and the market by broadening the scope of information and enhancing its dissemination, resulting in a more accurate reflection of firm-specific conditions within the stock price. In addition, the higher the investor attention, the stronger the herding effect triggered by the abnormal exit behavior of NCLSs (Li et al., 2019), and thus the more pronounced the negative impact on the rights of controlling shareholders. Therefore, under the influence of investor attention, the negative impact of NCLSs’ exit threats on maturity mismatch is amplified. In summary, this paper posits that:

H2: The attention of market parties (analyst attention, media attention, and investor attention) will strengthen the negative influence of NCLSs exit threats on the maturity mismatch.

Methodology

Sample Selection and Data Source

This study focuses on Chinese listed companies on the A-share market over the period 2010 to 2020 as the subject of our research sample. This article excludes the following categories of companies to uphold data integrity and consistency: (a) companies in the financial sector. (b) companies designated as ST, *ST due to exceptional financial conditions. (c) companies where the controlling shareholder’s equity stake is below 5% or where the controlling shareholder is not the largest. (d) companies with incomplete data. Ultimately, we secure a dataset comprising 26,080 firm-year observations. The data is sourced from the China Stock Market and the Accounting Research (CSMAR) and China Research Data Service Platform (CNRDS). All the continuous variables are winsorized at the 1st and 99th percentiles to mitigate the impact of outliers.

Variable Definitions

Maturity Mismatch

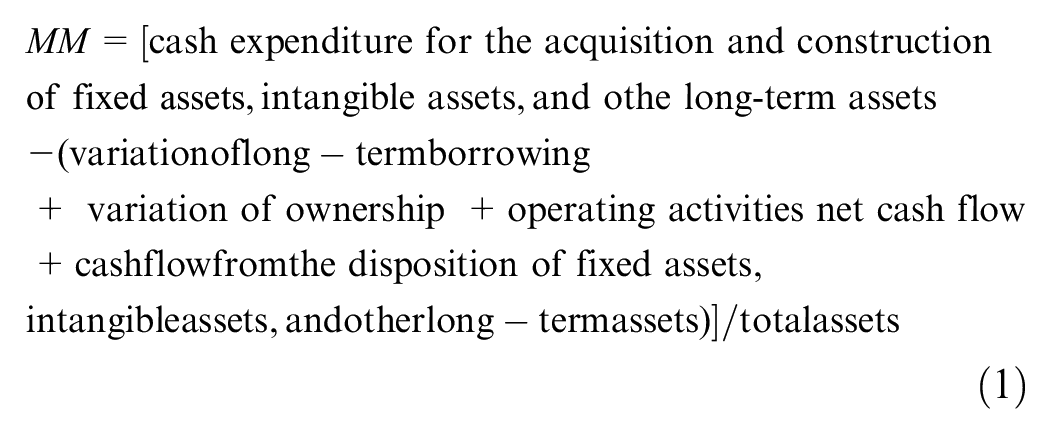

Following the conventions of prior research (Bai, 2022a; Cheng, Chiao, et al., 2020; Wang et al., 2021), this article establishes a metric for maturity mismatch using the financing deficit framework put forward by Frank and Goyal (2004). Specifically, when a company’s long-term investment outlays surpass its long-term debt, such investments are probably financed through short-term liabilities. Consequently, the proxy for maturity mismatch denoted as MM, is calculated as follows.

Where “change of long-term borrowing” was calculated as “long-term borrowing in current period + non-current liabilities due within a year − long-term borrowing during the previous period.” A higher value of MM signifies a greater extent of maturity mismatch.

Exit Threats of NCLSs

Although the exit threat mechanism has been theoretically established, there are significant challenges in measuring the exit threats in empirical studies in a reasonable way. Research indicates that enhanced stock liquidity bolsters large shareholders exit threats and improves the efficacy of corporate governance (Bharath et al., 2013; Edmans et al., 2013; Sun et al., 2021). Given that China’s Split-Share-Structure Reform has injected liquidity into the stock market, Hope et al. (2017) use this as a foundation to take a difference-in-differences approach to gauge exit threats. However, almost all Chinese listed companies have completed this reform, and changes in NCLSs in listed companies have become frequent since then, so the approach of Hope et al. (2017) neglects the impact of changes in NCLSs on exit threats. Dou et al. (2018) highlight that exit threats are predominantly influenced by the intensity of large shareholders competition and the liquidity of stock. Helling et al. (2020) also measure the exit threats of large shareholders by combining large shareholders with market liquidity.

Similarly to Helling et al. (2020), this article uses an interaction variable (LIQ × NCLSs) of stock liquidity and NCLSs to capture the intensity of the exit threats of NCLSs. Consistent with previous research (Dou et al., 2018), we utilize the average daily turnover ratio of tradable shares as an indicator of stock liquidity. In this study, NCLSs are delineated as external investors whose collective equity stake, in conjunction with their affiliated entities, surpasses 5% of firm’s ownership. We define three proxies to simultaneously portray NCLSs: (1) Dum: a binary indicator that is 1 when the firm has at least one NCLS and 0 otherwise. (2) Num: the count of all NCLSs within the company. (3) Ratio: the aggregate shareholding percentage of all NCLSs in the company.

Model Specification

We construct fixed-effects model to examine whether and how the exit threats of NCLSs affect the maturity mismatch.

Where MM denotes the maturity mismatch, LIQ denotes stock liquidity, NCLSs denotes the non-controlling large shareholders, and LIQ × NCLSs denotes the exit threats of NCLSs. In line with prior studies (Bai, 2022a; Wang et al., 2021), this article incorporates a suite of control variables that might have influences on the maturity mismatch, and the detailed definitions of variables are reported in Table 1. The notations ∑Firm and ∑Year represent firm and year fixed effects, respectively. In model (2), the interaction term (LIQ × NCLSs) coefficient, denoted as β3, is the primary parameter of interest, and if H1 is valid, then the estimated coefficient of β3 would be significantly negative.

Variable Definitions.

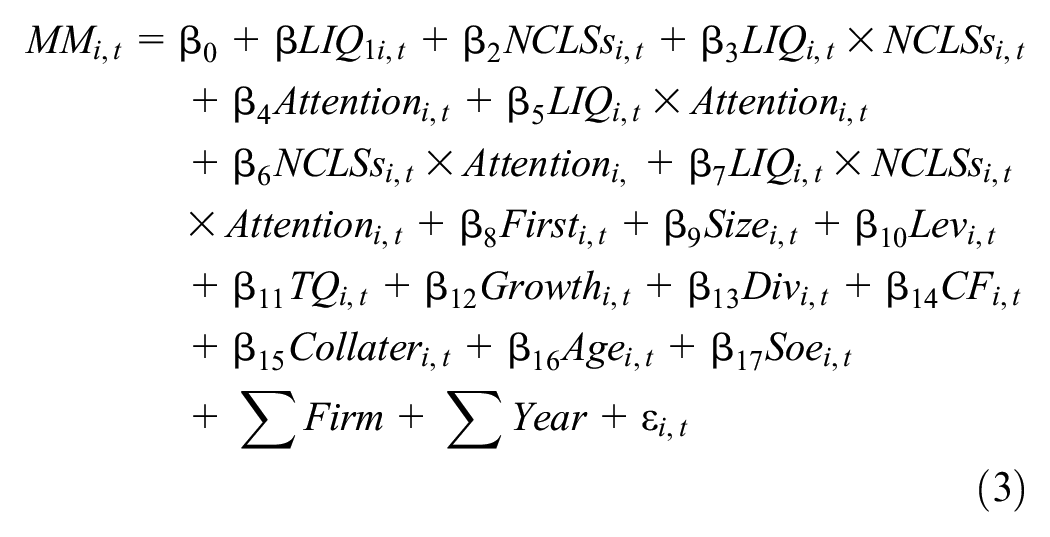

We construct the following model to explore the extent to which the attention of market participants influences the potency of NCLSs’ exit threats in mitigating the maturity mismatch.

where Attention denotes the attention of market parties, which is measured by the following proxies: (1) Analyst attention, we take the natural logarithm of the count of signed analyst teams that make earnings forecasts for the company within a fiscal year as the measurement. (2) Media attention, which is ascertained by calculating the natural logarithm of one plus the total count of media reports concerning the company within a fiscal year. (3) Investor attention, which is proxied by taking the natural logarithm of one plus the total count of stock-related comments made by investors about the company within a fiscal year. In model (3), the interaction term (LIQ × NCLSs × Attention) coefficient, denoted as β7, is the primary parameter under scrutiny, and if H2 is supported, then the estimated coefficient of β7 would be significantly negative.

Empirical Analysis

Descriptive Statistics

The panel A of Table 2 presents the descriptive statistics for the variables, which reveals that the average value of MM is −.084, and its maximum and minimum values are .380 and −.530, respectively, indicating considerable change in the extent of maturity mismatch among Chinese listed companies on the A-share market. The average values for Dum and Ratio are .515 and .085, respectively, signifying that NCLSs are present in approximately 51.5% of the sampled listed companies, yet the mean aggregate equity stake held by all NCLSs within a stand at a mere 8.5%. Although NCLSs are commonly found among the sample companies, their shareholdings are relatively low, revealing that the “single-shareholder dominance” phenomenon is notably pronounced in Chinese capital market. The maximum value of Num, 7, shows that some listed companies have multiple NCLSs, highlighting a significant variation in the distribution of NCLSs across different companies.

Descriptive Statistics and Differences Test.

p < .01 (The same applies hereinafter).

Furthermore, we categorize the entire sample based on Dum and present the outcome of the differences test in Table 2. The findings reveal that the mean and median values of MM for group without NCLSs are −.078 and −.066, whereas, for group with NCLSs, they are −.089 and −.074, respectively, which are lower than those of the former group. The differences are significant at the 1% level, showing that companies with NCLSs exhibit a reduced degree of maturity mismatch relative to companies without NCLSs.

Correlation Analysis

Table 3 displays the Pearson correlation coefficients among the variables, revealing that LIQ is negatively significant associated with MM at the 1% level (the coefficient is −.030), and similarly, Dum, Num, and Ratio all exhibit significant negative correlations with MM at the 1% level (the coefficients are −.042, −.056, and −.047, respectively). These results provide preliminary indications that stock liquidity and NCLSs can inhibit maturity mismatches. Since we focus on the role of NCLSs exit threats (NCLSs × LIQ) on the maturity mismatch, and the explanatory variables also exhibit significant correlations with the other control variables, our hypotheses require regression analysis to be tested.

Correlation Matrix.

p < .1. **p < .05. ***p < .01.

Empirical Test of Research Hypotheses

The Impact of NCLSs Exit Threats on Maturity Mismatch

Table 4 presents the regression findings based on the fixed effects model for the unbalanced panel dataset. In column (1), we detail the regression findings regarding the influence of stock liquidity on maturity mismatch, with results indicating that the coefficient for LIQ is −.392 and significant, which suggests that stock liquidity significantly curbs the extent of maturity mismatch. Columns (2) to (4) of Table 4 present the regression results examining the influence of NCLSs on the maturity mismatch. The findings indicate that the coefficients for Dum, Num, and Ratio are −.008, −.007, and −.034, respectively, all of which are significant at the 1% level, suggesting that NCLSs can significantly decrease the degree of maturity mismatch. Columns (5) to (7) of Table 4 display the regression analysis on the impact of NCLSs’ exit threats on the maturity mismatch. The results reveal that the coefficients for LIQ × Dum, LIQ × Num, and LIQ × Ratio are all significantly negative, indicating that the exit threats of NCLSs can reduce the maturity mismatch. Thus, H1 is supported.

The Influence of NCLSs Exit Threats on Maturity Mismatch.

Notes. t-statistics in parentheses (The same applies hereinafter). *p < .1. **p < .05. ***p < .01.

Additionally, the regression coefficient for the control variable First in columns (1) to (7) of Table 4 are all significantly positive, suggesting that overly concentrated ownership exacerbates maturity mismatch in Chinese listed firms (Gao & Liu, 2012; Zhong et al., 2018). However, NCLSs possess both the incentive and the capacity to involve in corporate governance through exit threats (Bai, 2022b; Chen, 2019; Hope et al., 2017; Helling et al., 2020), effectively inhibiting the maturity mismatch. The regression coefficients of the control variables Size, Tobinq, Growth, Div, CF, Collater, and Age are significantly negative, indicating that larger and more profitable firms with better investment opportunities, higher growth, and longer time on the market tend to have lower levels of maturity mismatch. Conversely, the coefficient of Lev is significantly positive, suggesting that firms with high financial leverage have reduced access to long-term credit due to elevated debt risk, thereby leading to an increased severity of maturity mismatch. These findings align with previous researches (Ding et al., 2020; Lai et al., 2019; Zhong et al., 2018).

The Impact of the Attention of Market Parties

Columns (1) to (3), (4) to (6), and (7) to (9) of Table 5 present the regression results with analyst attention, media attention, and investor attention serving as moderating variables, respectively. The results demonstrate that the coefficients for LIQ × Dum × Attention, LIQ × Num × Attention, and LIQ × Ratio × Attention are all significantly negative at the 1% level, suggesting that increased attention from analysts, media, or investors intensifies the negative influence of NCLSs’ exit threats maturity mismatch. Consequently, the attention of market parties is an important condition to strengthen the impact of NCLSs’ exit threats on the maturity mismatch, thereby validating H2.

The Impact of the Attention of Market Parties.

p < .1. **p < .05. ***p < .01.

Endogeneity

Difference-in-Differences Estimation (DID)

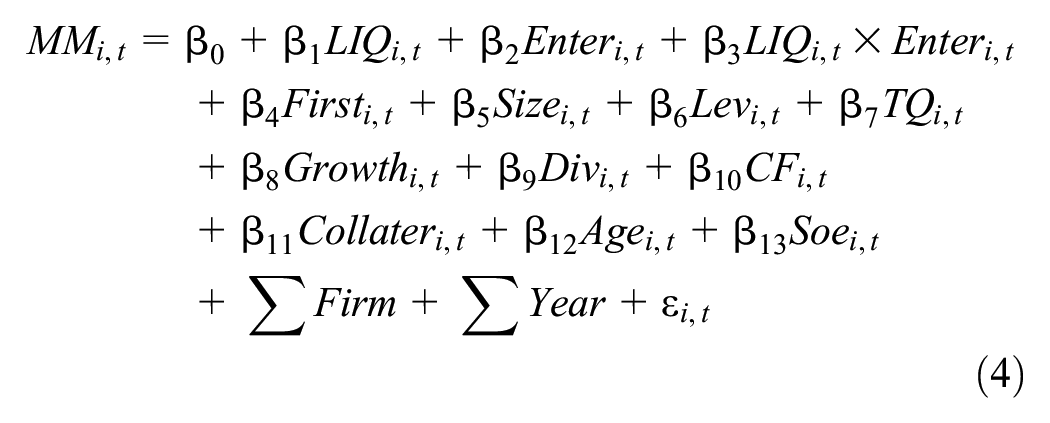

The existence of NCLSs in listed companies may not happen randomly but is intentionally chosen according to the characteristics of the company, which may be influenced by the maturity mismatch in choosing whether to enter the company as NCLSs. Therefore, to mitigate the impact of this endogenous problem, this article establishes the following DID model based on the varying “entry” and “exit” events of NCLSs across different listed companies. For “entry,” the sample of companies that transitioning from having no NCLSs to having NCLSs is used as the treatment group, while the sample of companies consistently without NCLSs is used as the control group. For “exit,” the sample of companies that move from having NCLSs to having none serves as the experiment group, while the sample of firms that consistently have NCLSs acts as the control group. In addition, companies that experienced multiple occurrences of “entries” or “exits” within the research period are excluded from the sample, and it is required that there are at least 2 years of observations both before and after the change. The specific models are as follows:

In model (4), Enter is a binary indicator for the “entry” of NCLSs, assigned a value of 1 when a company transitions from having no NCLSs to having NCLSs, and 0 otherwise. In model (5), Exit is also a binary indicator for the “exit” of NCLSs, assigned a value of 1 when a company transitions from having NCLSs to having none, and 0 otherwise.

The regression results based on the DID method are detailed in Table 6. In column (1), it is observed that the coefficient for LIQ × Enter is significantly negative, indicating that the extent of maturity mismatch significantly diminishes after the company changes from having no NCLSs to having NCLSs, compared to companies that maintain no NCLSs. In column (2), the regression coefficient of LIQ × Exit is found to be significantly positive, suggesting that the extent of maturity mismatch notably escalates after the company changes from having NCLSs to having none, compared to companies that maintain NCLSs. In summary, the results based on the DID method still support our hypothesis that the exit threats of NCLSs can reduce the maturity mismatch.

Difference-in-Differences Estimation (DID).

p < .1. **p < .05. ***p < .01.

Propensity Score Matching (PSM)

To address the selection bias potentially stemming from observable firm characteristics, this article employs PSM for the analysis. In whether NCLS exists, we segment the sample into an experiment group (companies with the NCLSs) and a control group (companies without the NCLSs). Subsequently, we perform 1:1 nearest neighbor matching using control variables from the model (2) as matching criteria, resulting in 20,158 observations. Panel A of Table 7 reveals that there are notable differences between the experiment and control groups before matching, whereas the density curves of the two groups nearly coincide post-matching. This article then re-estimates the regression using the matched subsamples, and as shown in Table 7, the outcomes are consistent with previous findings.

PSM Results.

p < .1. **p < .05. ***p < .01.

Robustness Test

Alternative Proxies of Maturity Mismatch

In model (1), we add “non-current liabilities due within a year” to the calculation of “change of long-term borrowing.” Similarly to Wang et al. (2021), we excluded the effect of “non-current liabilities due within a year” to re-measure the maturity mismatch as a robustness test. Therefore, our second maturity mismatch proxy, MM1, is calculated as follows.

Furthermore, in line with previous research (Bai, 2022a), we employ the classification of liquidity to proxy the degree of maturity mismatch as a robustness test. Therefore, our third maturity mismatch proxy, MM2, is calculated as follows:

Columns (1) to (3) and (4) to (6) of Table 8 present the results with MM1 and MM2 as dependent variables, respectively. Our conclusion still holds by using these alternative measures.

Alternative Proxies of Maturity Mismatch.

p < .1. **p < .05. ***p < .01.

Alternative Samples

In recent years, as Chinese financial system reforms progress and its capital market continues to improve, the access to financing of companies have been diversified, and many companies have obtained the qualification of bond issuance and can increase long-term capital for their long-term projects by issuing bonds, thus effectively alleviating the issue of maturity mismatch. Accordingly, we exclude observations related to the presence of bond financing among listed companies as a robustness test. The results, as depicted in Table 9, are consistent with the previous tests.

Alternative Samples.

p < .1. **p < .05. ***p < .01.

Conclusions and Practical Implications

How to reduce maturity mismatch has become an important theoretical and practical problem for the high-quality development of micro firms and macroeconomy. NCLSs are the important stakeholders of firms and the forces that cannot be ignored in the capital market, and also the main subjects to bear the risks and adverse consequences caused by maturity mismatch. This study explores the mitigation measures of maturity mismatch from the important governance mechanism of the exit threats of NCLSs. Analyzing a dataset of Chinese listed companies on the A-share market over the period 2010 to 2020, our results suggest that the exit threats posed by NCLSs significantly reduce the level of maturity mismatch. The result remains statistically significant and robust, even after employing a DID estimation and the PSM method to alleviate potential endogenous issues, along with conducting additional robustness checks. Further, we also find that increased attention from analysts, media, or investors amplifies the inhibitory role of NCLSs’ exit threats on maturity mismatch, indicating that market participants’ attention is a crucial factor in enhancing the governance efficacy of NCLSs’ exit threats.

Our contributions are multifaceted: firstly, we incorporate the concept of “threat” from social psychology into the realm of corporate governance research, offering an in-depth examination of how NCLSs’ exit threats influence maturity mismatch, which not only complements the “shareholder activism” perspective championed by the Chicago School but also contributes to the enrichment and development of the theoretical frame of corporate governance model, particularly within the unique context of China. Secondly, this article uniquely integrates the investment and financing periods of firms to investigate the role of NCLSs’ exit threats on maturity mismatch from the perspective of investment and financing relationship and deeply discusses the external conditions to strengthen the role of NCLSs’ exit threats, which expands and deepens the scope and content of scholarly inquiry into the effects of NCLSs on corporate investment and financing strategies. Thirdly, this article incorporates the mechanism of exit threats by NCLSs into the analysis of factors influencing corporate financial decision-making and explores whether and how the exit threats of NCLSs affect maturity mismatch, thereby contributing to the literature on micro-governance influences on the term structure of corporate investment and financing. Fourthly, at present, firms in China generally have problems such as difficult and expensive financing for investment projects and the ongoing taking short-term borrowings to sustain long-term projects. This article provides practical guidance for restricting the high-risk behavior of maturity mismatch from the important governance mechanism of the exit threats of NCLSs, which in turn can offer strategies to prevent the transmission of real economy risks into the financial sector. Fifthly, this article confirms that NCLSs of listed companies in China effectively play the governance role through the exit threat mechanism (threat by mouth), which not only has certain guiding significance for further optimizing the shareholder structure of listed companies but also carries substantial practical importance for regulators in fostering a conducive institutional framework that maximizes the positive governance effects NCLSs’ exit threat mechanism.

Our research carries three key policy implications: firstly, listed companies should recognize the significance of NCLSs in corporate governance when crafting or amending their ownership structure. Companies with a single dominant shareholder should consider incorporating NCLSs to refine their ownership structure and achieve a more balanced distribution of power, which not only helps to improve the efficiency of corporate governance but also strengthens external supervision and prevents controlling shareholders from abusing their power. Companies should take steps to attract quality non-controlling majority shareholders and increase their participation in decision-making. The company should also ensure that non-controlling shareholders have the opportunity to gain insight into the business situation and strategy, especially to provide input in major decisions. Enhancing information transparency ensures that NCLSs have access to necessary information, enabling them to make reasonable decisions, minimize decision-making errors, and ultimately foster the company’s maximum value, aligning with the collective enhancement of both shareholder and corporate interests. Secondly, the regulatory authorities should establish a favorable institutional environment that encourages NCLSs to engage in corporate governance, for example, by advancing mixed-ownership reforms, bolstering the institutional investor community, deepening the capital market’s internationalization, and attracting a broader range of investors to partake in governance activities. The government should improve market liquidity, and provide favorable conditions for NCLSs. Regulators should also improve the cumulative voting system, increase the opportunity for NCLSs to speak on major matters, and encourage them to fulfill a governance role. Concurrently, the regulatory authorities should strengthen the management of information disclosure, standardize the reporting practices of listed companies, elevate the disclosure standards for major shareholders regarding their stake reductions or exits, and strengthen the restrictions on controlling shareholders and management. In addition, the regulatory authorities should improve the investor protection system, strengthen the shareholder litigation mechanism, provide legal protection for NCLSs, and foster the robust growth of the capital market. Thirdly, NCLSs ought to engage proactively in corporate governance, rigorously monitor the actions of controlling shareholders and management, and protect the rights and interests of them. When capable, NCLSs should actively exercise their voting rights to involve in the firm’s decision-making processes, offer insights into industry prospects and solutions, assist in mitigating the decision-making errors, and enhance the efficiency of corporate governance. When the “hand vote” is invalid, the NCLSs should give priority to the “exit threat,” communicate with the controlling shareholders and management, and reach a consensus, rather than directly “vote with their feet” to exit the company. In addition, NCLSs should continue to learn new knowledge, improve judgment, and optimize corporate governance under reasonable supervision. By implementing these measures, NCLSs can augment the company’s value, aligning their interests with the company’s growth to achieve a mutually beneficial outcome.

Footnotes

Author Contributions

In the previous submission, an author Xinxue Gao who made a significant contribution to the paper may have been accidentally omitted. It is necessary to add this author’s information.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors acknowledge the funding support by Fujian Provincial Social Science Foundation Project [grant number FJ2024MGCA018; FJ2025MGCA017], and Huaqiao University's Academic Project Supported by the Fundamental Research Funds for the Central Universities [grant number, 23SKGC-QG07].

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data of this study are available from the corresponding author.