Abstract

The purpose of this research is to evaluate the effect of issuing businesses engaging reputed law firms on the extent of underpricing in developing IPO markets. The consequences of the involvement of prestigious lawyers in underpricing IPO businesses are lacking from a global viewpoint due to a lack of research. This research provides the first empirical investigation of the role of reputable law firms in the underpricing of IPO firms in developing IPO markets. Thus, it expands on Moran and Pandes’s work, which was previously constrained to the US IPO market. We analyze a large dataset of 6,869 newly and publicly traded firms in 10 developing markets between January 1995 and December 2019. We discover that IPO issuers do certainly benefit from engaging reputed attorneys to verify their quality in order to alleviate investors’ ex-ante uncertainty and protect their offers from being significantly underpriced. Our findings have ramifications for IPO founders, investors, academics, and policymakers.

Keywords

Introduction

Research shows that almost 0.99 of Initial Public Offerings (IPOs) firms retains outside lawyers to advise on securities legislation prior to the stage of the official listing (Bates et al., 2018; Coates, 2001; Moran & Pandes, 2019). The quality of law services provided to IPO firms varies depending on the quality of law firms, hence it may affect the IPO market (Chaserant & Harnay, 2015). Prominent lawyers are more costly to hire in return for their thorough due diligence than less renowned lawyers, and so the IPO prospectus prepared by reputed law firms should be more informative to shareholders (Fernando et al., 2015; Okamoto, 1995). These legal firms are necessary to guarantee that IPOs owners adhere to disclosure rules and minimize their clients’ vulnerability to litigation from shareholders and authorities’ lawsuits (Lin et al., 2013; Moran & Pandes, 2019). Despite their obvious relevance and pervasiveness, little research has been conducted on the impact of prestigious lawyers on the IPO market, who serve as a key intermediary between IPO issuers and IPO investors.

IPO literature focuses almost exclusively on the function of reputable underwriting and auditing firms in moderating the ongoing problem of IPO underpricing that largely affects IPO owners’ wealth across countries (Asthana et al., 2019; Barondes et al., 2007; Beatty, 1989; Booth & Smith, 1986; Neupane & Thapa, 2013; S. D. Sundarasen et al., 2018; S. Sundarasen et al., 2021). The underpricing of IPO corporations happens when their share prices surge dramatically from their offer price on the first trading day. The larger the underpricing, the larger the money left on the table by IPO issuers to IPO investors to cash out at the expense of IPO owners’ wealth (Jamaani & Alidarous, 2022). The presence of large information asymmetry in IPO market between IPO owners and investors causes this repeating stock market phenomena to occur (Hanley & Hoberg, 2010; Jamaani & Alidarous, 2019; Rathnayake et al., 2019). IPO investors usually demand larger IPO discount when they perceive large information asymmetry existing in an IPO firm pre-investing (Jamaani & Ahmed, 2020). As a result, the IPO market is an ideal environment for assessing the effects of employing reputable varuses to non-reputable lawyers on the underpricing of IPO companies in developing nations. We focus on developing nations’ stock markets as research shows that developing markets suffer from significant information asymmetry, an absence of institutional transparency, and considerable IPO underpricing as compared to industrialized countries’ stock markets. For example, Jamaani and Roca (2015), Azevedo et al. (2018), Rathnayake et al. (2019), and Jamaani and Ahmed (2022) show that developing equity markets suffer from large degree of information gap between investors and issuers which results in sustaining a asymmetric information environment that continuously affect stock market informational efficiency. Moreover, Hopp and Dreher (2013) and Jamaani and Ahmed (2021) show that IPO companies traded in developing stock markets lack institutional transparency as they are subject to low-level of security exchange regulations, high insider trading, and circulation of private market information. Loughran et al. (1994) also report large IPO discount in many developing countries including 170% in China, 84% in India, 56% in Indonesia, 149% in Jordan, 53% in South Korea, 51% in Malaysia, 240% in Saudi Arabia, 270% in United Arab Emirates. The authors also report low levels of IPO underpricing in number of developed countries including 12% in Netherlands, 9.5% in Spain, 15.70% in United Kingdom, 17.5% in the United States, 7.6 in Denmark, 6.80% in Canada, and 20% in Australia.

Our research is motivated by the necessity to broaden the investigation into the role of reputable law firms in the IPO market beyond developed markets. Our research provides marginal contribution by extending the research conducted by Moran and Pandes (2019), who examined the impact of reputable law firms on the reduction of IPO underpricing in the U.S. market. The current body of empirical research on the association between reputable lawyers and IPO underpricing is sparse, frequently inconsistent, and primarily concentrates on countries with low IPO underpricing, high institutional transparency, and low information asymmetry (Barondes et al., 2007; Bates et al., 2018; Beatty & Welch, 1996; Moran & Pandes, 2019). In contrast, developing markets are prone to considerable information asymmetry and large levels of IPO underpricing. Given these distinctions, it is imperative to determine whether reputable lawyers, who have the potential to be the most effective actors in mitigating legal risk, perform a comparable certifying function in these developing countries. Our research interest is in the extent to which reputable law firms can reduce investors’ ex-ante uncertainty by certifying the quality of issuers, thereby preventing extreme underpricing. It not only improves comprehension of the legal foundation of IPO underpricing by expanding the work of Moran and Pandes (2019), but it also offers ramifications that are particularly pertinent for markets with more severe institutional and information obstacles.

Our findings confirm that prestigious lawyers guarantee that the material presented in IPO prospectuses is free of severe inaccuracies and flaws and is subsequently viewed favorably by investors. Consequently, the IPO businesses’ choice of prominent law firms adds another layer of quality to the information offered to IPO participants. We confirm that high-quality lawyers hired by issuing firms may serve as a certifying indication of dependability in communicating issuers’ private information to investors in the IPO market. This eliminates ex-ante investor confusion about the legal bindings provided in IPO prospectuses, reducing IPO underpricing by 0.096 in developing economies. Our results remain robust after controlling for the role of hiring reputable auditing and underwriting firms, employing quality accounting standards, accounting for differences in formal and informal institutional quality across developing countries. This study is the first empirical analysis of the role of reputed law firms in the underpricing of IPO businesses in developing IPO markets.

This study holds significant implications for IPO issuers, investors, scholars, and regulators, especially in developing markets. Our findings may provide advantages to IPO issuers. Firms in developing economies intending to go public may leverage our findings by strategically engaging reputable law firms. The engagement of reputable lawyers provides a robust certification signal, enhancing prospective investors’ confidence in the firm’s compliance and operational quality, thereby mitigating ex-ante uncertainty. The outcome is that large underpricing is less necessary when reputable law firms are hired, enabling issuers to negotiate more effectively regarding the market value of their firms at listing. This indicates that employing reputable lawyers may enhance market confidence, thereby reducing the impact of information asymmetry and providing strategic value in the market. Additionally, we provide advantages to IPO investors by gaining insights from our research findings, which assist in refining their IPO investment strategies, considering that the reputation of law firms significantly influences the pricing dynamics of new listings. Our findings indicate that IPOs managed by non-reputable attorneys exhibit greater underpricing, resulting in larger expected returns for investors willing to accept higher initial uncertainty. This has implications for investment portfolio building regarding the trade-off between the signaling advantages of reputable lawyers and the potential for excess returns on mispriced offerings that may lack such certification. The study’s findings assist investors in evaluating risk-return profiles within the IPO market, particularly in developing countries. Third, our research is beneficial for scholars in the IPO market. This paper addresses the need to extend and challenge existing literature, particularly concerning developed markets as discussed by Moran and Pandes (2019). It empirically demonstrates a significant negative relationship between the involvement of reputable law firms and IPO underpricing in developing markets. The findings support the dual roles of legal certification and uncertainty mitigation in IPO pricing and suggest avenues for future research. This framework offers scholars a validated structure for analyzing the interactions between legal intermediation and markets across various economic contexts, thereby enhancing the theoretical discourse on IPO underpricing and signal transmission processes. Finally, our study highlights the significance of our findings regarding the influential role of reputable law firms in generating value within developing economies for regulatory bodies and policymakers. The results suggest that promoting a high-quality legal environment and attracting reputable lawyers to participate in the IPO process may mitigate underpricing behaviors that can hinder market efficiency and affect long-term economic growth in developing IPO markets. Regulators in developing countries can enhance the utilization of reputable lawyers by enacting policies that incentivize such practices. This approach will contribute to the establishment of a more transparent and aligned public marketplace, thereby fostering a stable and sustainable financial environment in the future.

The following is the structure of the paper. Section 2 contains a concise overview of the literature. Section 3 examines significant theories and how hypotheses are developed. Section 4 contains a description of the data and methods. The empirical findings and discussion are presented in Sections 5, while the robustness test and conclusion are presented in Sections 6 and 7.

Brief Literature Review

Early on in a company’s IPO listing process, an issuing company hires a law firm along with underwriting and auditing agents to assist it in developing the information product that will guide the price and promotion of the issuing company’s shares to the public (Bates et al., 2018; Beatty & Welch, 1996; Utset, 1995). IPO literature concentrates entirely on the function of underwriting and auditing firms in the IPO process (Asthana et al., 2019; Barondes et al., 2007; Beatty, 1989; Booth & Smith, 1986; Neupane & Thapa, 2013; S. D. Sundarasen et al., 2018; S. Sundarasen et al., 2021). This literature shows strong evidence that issuers’ underwriting and auditing companies have a significant impact on IPO underpricing. Yet, little is known about the impact of law firms in the IPO market.

The legal firm performs a comprehensive due diligence evaluation of the IPO company’s business practices (Barondes et al., 2007). Here, the lawyers compile and verify facts for the IPO prospectus, so minimizing liability risk associated with serious misrepresentations and inaccuracies (Moran & Pandes, 2019; Schneider et al., 1981). A traditional legal assessment will often include an examination of potentially detrimental pledge agreements, cross-default terms, fundamental contracts, related party transactions, and third-party termination rights (McClane, 2015). As a result, lawyers simplify and check the authenticity of information for the IPO prospectus, which assists investors in determining the investment risk and suitability of investment (Bates et al., 2018).

However, research finds that law firms are indifferent in relation to quality of services provided to their clients, hence large variability in the quality of legal services provided to IPO firms might have different outcome for IPO companies (Krishnan & Masulis, 2013; McClane, 2015; Utset, 1995). Evidence indicates that reputable attorneys may undertake more rigorous due diligence assessments than less prestigious lawyers (Barondes et al., 2007; Beatty & Welch, 1996; Ipsen, 2020). Moran and Pandes (2019) believe that reputable lawyers collaborate actively with issuing companies to ensure that investors appropriately assess the risk and return profiles of IPO businesses, and hence should have a better impact on the market pricing of IPO companies’ shares, at least in the near run. Reputable lawyers may offer value to IPO businesses by employing superior legal or negotiating expertise that serve as a quality certification indicator that may alleviate ex-ante investment uncertainty of IPO investors (Boeh & Southam, 2011; Krishnan & Masulis, 2013; Okamoto, 1995). The appearance of reputable legal firms in the IPO prospectus might indicate the high quality of the IPO company and minimize information asymmetry between issuers and investors resulting in lowering investors’ demand for more underpricing as a compensation for uncertainty about the information provided in the IPO prospectuses. However, research on the influence of renowned attorneys on the underpricing of IPO businesses is scarce and inconsistent. Beatty and Welch (1996) find that there is a lack of correlation between the prominence of issuing firms’ attorneys and underpricing or transparent reporting in the US IPO market. In comparison, Barondes et al. (2007) acquire data from the US market from 1986 to 2001 demonstrating that prominent attorneys underprice IPO businesses because of concern about lawsuit risk, despite the fact that the authors’ emphasis was on the impact of reputation of law firms hired by underwriting banks. Further contradictory evidence is found research by Bates et al. (2018) and Moran and Pandes (2019), which found an association between notable attorneys and decreased IPO underpricing in the US IPO market. Despite the inconsistent outcomes found in the US IPO market, research is lacking on the association between the hiring of reputable lawyers and expected IPO underpricing in developing economies. Research suggests that developing markets have a great deal of information asymmetry, a lack of institutional transparency, and large of IPO underpricing in comparison to advanced economies (Azevedo et al., 2018; Boulton et al., 2010; Hopp & Dreher, 2013; Jamaani & Ahmed, 2020, 2021; Jamaani & Roca, 2015; Loughran et al., 1994). This establishes is a research gap in the law and finance literature that we seek to empirically address by examining the role of reputable law firms in the underpricing of IPO firms in developing IPO markets.

A Brief Theoretical Review and Hypothesis Development

Theoretical basis discusses underpricing as a consequence of information asymmetry between investors and issuers of IPO companies and, as well as the role of reputable intermediaries such as solicitors, auditors, and underwriters in the IPO process (Azevedo et al., 2018; Barondes et al., 2007; Beatty, 1989; Beatty & Ritter, 1986; Beatty & Welch, 1996; Booth & Smith, 1986; Datar et al., 1991; Hanley & Hoberg, 2010; Jamaani & Alidarous, 2023; Okamoto, 1995). This study utilizes two prevalent IPO theories, namely the certification hypothesis and the ex-ante uncertainty hypothesis, to explain the anticipated correlation between reputed law firms and IPO underpricing.

Booth and Smith (1986) propose the certification hypothesis as a method for explaining the information asymmetry between IPO businesses’ owners and investors. The certification hypothesis asserts that reputable intermediaries function as reliable third-party validation devices of a firm’s quality, particularly for IPOs (Jamaani & Alidarous, 2019). In markets characterized by significant opacity and asymmetric information—common characteristics of developing IPO markets—the engagement of a prominent law firm in the transaction may serve as a crucial indicator of quality and reliability for investor (Jamaani & Alidarous, 2024b; Rathnayake et al., 2019; S. D. Sundarasen et al., 2018). A reputable legal practice is presumed to possess superior knowledge and does more thorough due diligence (Jamaani & Alidarous, 2023). As the company prepares the IPO paperwork, its reputation for legal and regulatory proficiency indicates that the offering is being developed and will be issued in alignment with stringent standards of correctness and compliance (Moran & Pandes, 2019). This creates a significant endorsement that mitigates investors’ concerns over the quality of information and reduces the perceived risk associated with the transaction (Jamaani & Alidarous, 2024b). As a result, investors may demand a reduced risk premium, leading to a diminished level of underpricing necessary to encourage participation in the IPO (Jamaani & Alidarous, 2023). Studies on developed countries indicate that the signaling role of hiring of reputable intermediaries are often linked to reduced investment uncertainty and IPO underpricing (Beatty, 1989; Liao et al., 2013; Liu & Ritter, 2011; Moran & Pandes, 2019). In contrast, IPO markets in developing countries may exhibit various forms of uncertainty and less mature regulatory frameworks; yet the fundamental signaling function of reputable intermediaries remains relevant. Consequently, in developing IPO markets, it is expected that the involvement of reputable law firms should signify enhanced quality, thereby reducing information asymmetries and minimizing the need for significant underpricing as compensating measures.

The ex-ante uncertainty hypothesis was proposed by Beatty and Ritter (1986), emphasizing the critical role of trustworthy intermediaries in decreasing information asymmetry between investors and issuing businesses. It is argued by the authors that when investors have a high level of ex-ante uncertainty regarding issuing companies, this indicates that investors have doubts about disclosure quality in the IPO prospectus. Prospective investors will be uncertain of the future investment they will make. As a result, IPO investors require a significant discount as fair compensation (Beatty & Ritter, 1986). In IPO markets in developing countries, risks may be intensified due to the ongoing development of financial reporting processes, an underdeveloped regulatory framework, and heightened market volatility (Jamaani et al., 2024; Rathnayake et al., 2019; S. D. Sundarasen et al., 2018). These worries may be immediately alleviated by executing an IPO with the assistance of a reputable legal firm (Jamaani & Alidarous, 2024b). A respectable law firm may mitigate ex-ante uncertainty by verifying that the legal paperwork is complete, clear, and complies with applicable requirements (Moran & Pandes, 2019). Consequently, the perceived risk among investors diminishes since they can now depend on the information provided. Reduced uncertainty leads to a diminished need for substantial compensating discounts, resulting in little IPO underpricing (Badru & Ahmad-Zaluki, 2018). The reduction in information asymmetry and uncertainty facilitated by competent legal intermediaries aligns with theoretical expectations and supports the beliefs established under the ex-ante uncertainty paradigm, hence strengthening the anticipated pricing effects (Jamaani & Alidarous, 2019).

Due to the fact that reputable attorneys charge more for their time and expertise, the IPO prospectus they prepare for IPO companies contains more useful information to investors than that of unreputable lawyers (Fernando et al., 2015; Jamaani & Alidarous, 2024b; Okamoto, 1995). We anticipate that the participation of renowned legal firms in the preparation of IPOs in developing countries will serve a dual purpose, informed by the certification and ex-ante uncertainty hypotheses. Initially, by their reputable accreditation, these law firms convey to the market that the IPO is a high-quality offering that adheres to stringent legal and regulatory standards. Secondly, by diminishing the uncertainty around the offering, they lower the risk premium that investors will need. This could result in lowering IPO underpricing. As a result, we derive the following hypothesis:

H1: IPOs prepared by reputable law firms are projected to suffer from lower IPO underpricing in developing IPO markets.

Data and Methodology

We gather extensive worldwide data from Bloomberg and DataStream for 6,869 listed IPOs corporations traded in 10 developing nations including China, Mexico, India, Brazil, Indonesia, Saudi Arabia, Poland, Turkey, South Korea, and Russia from January 1995 to December 2019. We omit delisted IPO businesses, trust funds, and real estate investment trusts in line with the literature on IPO underpricing (Boulton et al., 2017; Jamaani & Ahmed, 2021; Liu & Ritter, 2011). We follow Banerjee et al. (2011) in defining underpricing (

To test our hypothesis, we apply the OLS cross-sectional linear regression as described in Equation 2, following Banerjee et al. (2011) and Jamaani and Ahmed (2020).

Subscripts i and j denote an IPO business traded in a certain developing economy, while

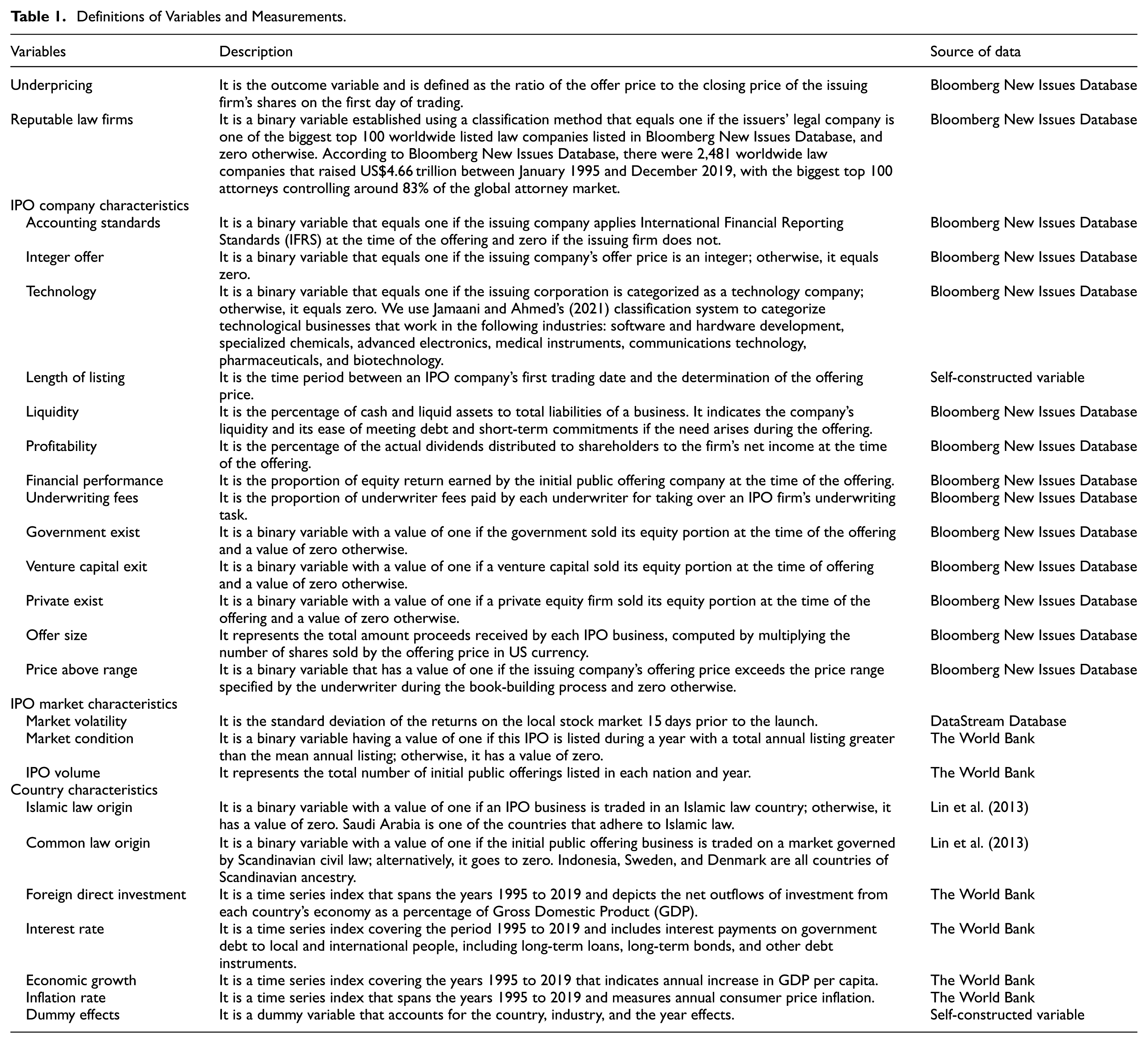

Definitions of Variables and Measurements.

Empirical Results

Descriptive Statistics

Table 2 contains a variety of descriptive statistical indicators for the data used. The table indicates that the average underpricing across our sample of 6,869 newly listed companies is 43%, whereas 21% of the sample’s enterprises hired reputable lawyers when they opt to go public. The table illustrates that Turkey has the lowest recorded underpricing at 3.9%, while Saudi Arabia shows the greatest at 120%. Furthermore, Brazil has the greatest proportion of companies that employ reputable lawyers, at 51%. In contrast, South Korea has the lowest rate, at 2.8%.

Descriptive Statistics. This Table Provides Average Descriptive Statistics Values. Table 1 Presents the Definitions of Variables and Their Corresponding Measurements.

Regression Results and Discussion

Table 3 shows the results for the reputed law firm variable, which examines the influence of highly respected attorneys on the underpricing of initial public offerings in developing nations. The indicator is statistically significant at the .01 level of significance. This demonstrates that employing prestigious law firms may indeed minimize underpricing by 0.096 in developing IPO markets. This solidifies the claim for our hypothesis. As Okamoto (1995), Chaserant and Harnay (2015) note, the appointment of renowned solicitors enhances the stature and legitimacy of issuing corporations. Distinguished attorneys when completing a comprehensive assessment of IPO prospectuses, ensure that the information included in the prospectus is devoid of serious inaccurate statements and deficiencies and is afterward considered favorably by investors. As a result, IPO companies’ selection of famous law companies adds another element of quality to the information provided to IPO participants over and above what is included in the prospectus. Our findings corroborate those of Barondes et al. (2007), Bates et al. (2018), and Moran and Pandes (2019), demonstrating that high-quality attorneys recruited by issuing businesses may serve as a certification indicator of reliability in communicating issuers’ confidential information to investors truthfully. This reduces investors’ ex-ante uncertainty regarding the reliability of the legal bindings contained in the initial public offering prospectuses, hence minimizing IPO underpricing in developing countries. Table 3 provides an adjusted R2 result of .05, which can sometimes appear to be too low at first appearance, but has been a consistent finding in previous international research. For instance, Loughran and Ritter (2004) report an adjusted R2 result of .05; Boulton et al. (2011) report an adjusted R2 result of .03; Shi et al. (2013) report an adjusted R2 result of .05; Leitterstorf and Rau (2014) report an adjusted R2 result of .06; and Chang et al. (2017) report an adjusted R2 result of .03. After adjusting for a variety of IPO business, IPO market, and country factors, our findings are robust.

Regression Results for the Effect of Reputable Lawyers. Table 1 Presents the Definitions of Variables and Their Corresponding Measurements.

***, **, and * denote a P-value at the significance level of 0.01, 0.05, and 0.10, respectively.

Robustness Tests

The Role of Other Intermediaries

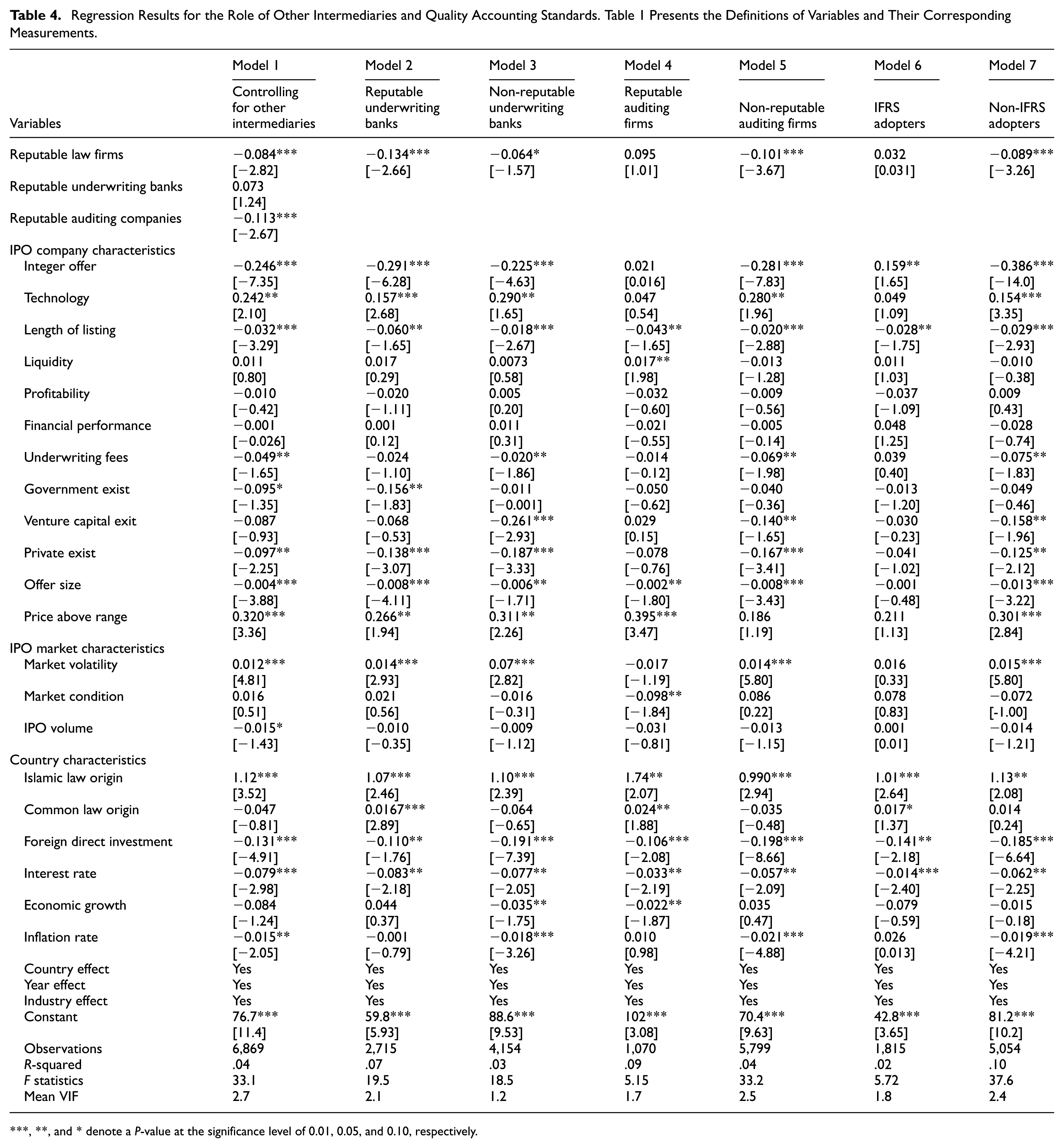

Research shows that IPO companies appoint a legal firm to collaborate with their underwriting and auditing firms to develop IPO proposals that include the necessary business and financial information utilized by authorities and investors (Barondes et al., 2007; S. D. Sundarasen et al., 2018). Thus, we check the consistency of our results after controlling for the role of reputable auditing and underwriting firms. We also add additional tests to capture the impact of reputed lawyers in IPOs underwritten by prestigious versus non-prestigious auditing and underwriting companies. Model 1 in Table 4 reports the results showing consistent findings with what we have reported in Table 3. Interestingly, results in models 2, 3, 4, and 5 in Table 4 show that while reputable law firms seem to work well with reputable underwriting banks in lowering IPO underpricing, the joint hiring of prestigious law and auditing firms brings no benefits to the underpricing of IPO companies. This could highlight a conflict-of-interest problem exists in the IPO market between reputable intermediaries that finds its way to investors, thus it increases their ex-ante uncertainty to the point that the appearance of reputed law and auditing firms does not provide any certification signal to IPO investors (Benzoni & Schenone, 2010; Eberhart & Eesley, 2018; McLeod et al., 2018; Palazzo & Rethel, 2008).

Regression Results for the Role of Other Intermediaries and Quality Accounting Standards. Table 1 Presents the Definitions of Variables and Their Corresponding Measurements.

***, **, and * denote a P-value at the significance level of 0.01, 0.05, and 0.10, respectively.

The Role of Quality Accounting Standards

International Financial Reporting Standards (IFRS) research demonstrates that mandatory adoption of IFRS improves reporting uniformity, resulting in increased information symmetry between many users of IPO reports, and might even reduce ex-ante uncertainty of IPO investors (Hong et al., 2014; Jamaani & Alawadhi, 2025; Jamaani & Alidarous, 2022). Therefore, we analyze the consistency of the reported findings after dividing the sample into those that mandate and those that do not require IFRS standards. Model 6 and 7 in Table 4 report that the effect of hiring prestigious law firms remains robust only in countries where they do not mandate IFRS standards. This result could imply that in the eye of IPO investors the effect of IFRS overpowers the role of prestigious law firms in the IPO market since IPO reports prepared under IFRS are claimed to be very informative and trustworthy by IPO investors (Hong et al., 2014; Jamaani & Alidarous, 2022). IPO investors, in countries where IFRS is not mandated, seek certification tool that reduces their ex-ante uncertainty about the quality and reliability of information contained on the IPO prospectus, thus the hiring of prestigious law firms in such countries works well in increasing investors’ confidence resulting in lowering IPO underpricing.

The Role of Formal Institutional Quality

Law and finance research asserts that, in addition to company characteristics (e.g., hiring reputable lawyers) that may exacerbate the information asymmetry between IPO parties, underpricing may be counterbalanced or severely compromised across nations by the predominant formal (i.e., institutional transparency environment) institutions (Banerjee et al., 2011; Jamaani & Ahmed, 2021; Jamaani & Alidarous, 2024b). Additionally, research reveals that, in addition to the importance of reputable intermediaries such as prominent law firms in the initial public offering market, the quality of a nation’s institutional framework may influence the role of intermediaries in financial system (Aggarwal & Goodell, 2009; Alidarous, 2024a, 2024b; Demirguc-Kunt et al., 2004; Emenalo & Gagliardi, 2020; Jamaani & Alidarous, 2025; Khurana et al., 2017; Moran & Pandes, 2019; Poghosyan, 2013). Consequently, we recheck the consistency of our outcomes reported in Table 3 after controlling for the impact of transparency of government policymaking and ethical behavior of firms as proxy for the prevalent formal institutional quality in a country (Jamaani & Ahmed, 2021; Jamaani & Alidarous, 2022). The former proxy demonstrates the ease with which some linked corporate groups can obtain confidential information about changes in legislation and laws affecting their commercial activity (Jamaani & Alidarous, 2022). As a result, this metric serves as a proxy for the public sector’s overall transparency. The latter proxy measures a country’s corporations’ degree of corporate ethics, covering their dealings with public authorities, lawmakers, and other enterprises (Jamaani et al., 2024; Jamaani & Alidarous, 2023). As a result, this metric measures the private sector’s overall transparency. Results reported in Models 1 to 4 in Table 5 show that reputable law firms succeed in providing certifications signal that reduces investors’ ex-ante uncertainty resulting in lowering IPO underpricing occurs in developing market economies where transparency of government policymaking and ethical behavior of firms are high. It can be inferred that in countries with high formal institutional quality, IPO investors view the hiring of prestigious law firms as a significant affirmation of the issuing companies’ dedication to producing high-quality IPO prospectuses and disclosing additional information to the public, thereby alleviating investors’ ex-ante uncertainty about the quality of provided information in the IPO prospectus. The achievement of reputed legal firms in decreasing the information asymmetry issue of IPO investors supports the likelihood of law firms’ concern of lawsuit risk against fraud cases (Jamaani & Ahmed, 2021; Liao et al., 2013; Lowry & Shu, 2002). This perspective implies that a country’s legal structure supports IPO investors’ trust in the certification role of prominent law firms. Investors may be able to prosecute dishonest attorneys and issuers in nations with high formal institutional quality. Investors in these nations appear to trust respected attorneys who can deliver accurate reports (Bates et al., 2018; Moran & Pandes, 2019).

Regression Results for the Role of Formal and Informal Institutional Quality. Table 1 Presents the Definitions of Variables and Their Corresponding Measurements.

***, **, and * denote a P-value at the significance level of 0.01, 0.05, and 0.10, respectively.

The Role of Informal Institutional Quality

Culture and finance research claims that IPO underpricing may be partially mitigated or significantly weakened by the prevailing informal (i.e., cultural norms) institutions in different countries (Al-Awadhi, 2019; Al-Awadhi, Alhashel, & Bash, 2024; Al-Awadhi, Bash et al., 2024; Costa et al., 2013; Jamaani & Ahmed, 2022). This is in addition to firm characteristics (e.g., employing prestigious solicitors) that may improve the information symmetry among IPO parties (Gupta et al., 2018). A significant component of this information asymmetry could be attributed to the development of widely recognized cultural values that permit the establishment of an uncertain business environment between market participants. Jamaani and Ahmed (2022) demonstrate how differences in power distance among developing nations may change the balance of information symmetry, as well as the supply and demand for IPO shares among the major actors in the IPO market, hence affecting IPO underpricing. Scholars use the cultural element of power distance to gain a better understanding of how culture influences peoples’ choices in a variety of business activities (Ashraf et al., 2016; Dang et al., 2022; Jamaani, 2021, 2025; Jamaani & Ahmed, 2022; Krause et al., 2016). They explain that in developing countries with cultures that have a large power distance, the absence of social trust channels to market players increasing the ex-ante uncertainty of IPO investors. Thus, we follow Jamaani and Ahmed (2022) to employ the power distance cultural characteristic developed by Hofstede (2001) to capture differences across countries’ cultures to see if the impact of employing reputable law firms will hold. Models 5 and 6 in Table 5 report that prestigious law firms succeed in reducing IPO underpricing in cultures where the level of power distance is low while reputable lawyers provide no benefits in developing countries with high power distance. We ascribe this discrepancy to the fact that attorneys from low power distance cultures do not appear to exploit IPO management’s cultural intolerance to uneven distribution of information and power. Therefore, prestigious attorneys in such cultures understand that IPO management are hesitant to exchange unreasonable investment decisions for personal fulfillment to achieve a successful IPO listing.

Conclusion

This research explores the association between the recruitment of reputable legal firms and IPO underpricing in developing IPO markets using a large cross-country sample covering more than 24 years. As hypothesized, we discover that engaging reputable legal firms does indeed certify to investors the high quality of issuers’ private information. As a result, the appearance of these high-quality legal firms in an IPO prospectus minimizes investors’ ex-ante uncertainty since they serve as a certifying sign of quality, mitigating the asymmetric information dilemma and the issue of underpricing. Our findings stand intact when we account for the participation of reputable auditing and underwriting companies, the use of sound accounting standards, and variations in formal and informal institutional quality among developing economies. Our research has ramifications for IPO founders, investors, scholars, and policymakers. Owners of IPO firms in developing countries should be sure that employing top lawyers before going public provides a certification signal that alleviates ex-ante uncertainty among IPO investors, hence reducing underpricing. In comparison, investors in IPOs may learn to make decisions on investing in newly listed businesses that employ low quality lawyers, since they will earn a higher investment return than investing in IPOs that engage prestigious legal firms. In contrast to the contradictory evidence discovered in developed IPO markets, academics in developing countries may have definitive proof of a significant negative association between the participation of reputed attorneys and underpricing of IPO enterprises. Governments in developing markets may benefit from our results about the vital relevance of verifying that renowned legal firms operate in the best interests of IPO issuers. Prominent lawyers may assist put a halt to the behavior of cheaply selling IPOs, which may discourage future issuers from selling part of their enterprises on the stock market, so impairing economic development.

Limitations and Future Research

Limitations

This study is subject to several limitations that should be acknowledged. First, our cross-sectional design limits causal inference between reputable law firm engagement and underpricing reduction, as noted in similar IPO studies (Butler et al., 2014; Chang et al., 2017). While our highest (lowest) adjusted R2 of .16 (.050) is consistent with prior international IPO research (Boulton et al., 2011; Loughran & Ritter, 2004), it suggests important omitted variables may influence our results. Second, our sample limitation to 10 developing countries may restrict generalizability, particularly to African and Latin American markets not represented in our analysis (Hopp & Dreher, 2013). The binary classification of law firm reputation oversimplifies the nuanced gradations of legal service quality and may not capture local market perceptions or specialized securities law expertise (Fernando et al., 2015). Additionally, our analysis period ending in 2019 may not reflect recent market developments, including COVID-19 impacts and evolving regulatory frameworks affecting IPO markets (Loughran et al., 1994). Third, our focus on first-day underpricing excludes other important IPO outcomes such as withdrawal probability, post-IPO litigation risk, and long-term performance (Jamaani, 2025; Jamaani & Alidarous, 2022; Lin et al., 2013).

Future Research

Several promising research directions emerge from our findings. First, future studies should employ longitudinal methodologies and instrumental variable approaches to establish stronger causal relationships concerns (Banerjee et al., 2011). Propensity score matching and regression discontinuity designs around law firm ranking thresholds could provide quasi-experimental identification strategies. Second, researchers should expand geographic coverage to include broader developing market representation and conduct systematic comparisons between developed and developing markets to examine whether certification effects vary with institutional development levels (Boulton et al., 2010). Third, mechanism identification represents a critical research frontier. Future studies should investigate specific channels through which reputable law firms reduce underpricing, including due diligence quality, disclosure completeness, and legal risk mitigation (Bates et al., 2018; Hanley & Hoberg, 2010). Fourth, measurement innovations should develop continuous law firms reputation measures rather than binary classifications, potentially using network analysis, text analysis of legal documents, and dynamic reputation tracking (Chaserant & Harnay, 2015). Alternative outcome variables including IPO withdrawal, litigation risk, and long-term performance warrant investigation (Jamaani, 2025; Jamaani & Alidarous, 2022; Lin et al., 2013). Fifth, industry-specific analyses could examine whether law firm effects vary across sectors with different regulatory complexities and investor bases. Future cross-border IPO studies could investigate international law firm roles and multiple jurisdiction impacts on pricing outcomes (S. D. Sundarasen et al., 2018). Finally, technological transformation research should examine how legal technology, artificial intelligence, and digital due diligence are reshaping traditional law firm roles in IPO markets (McClane, 2015; Zhao & Zhu, 2025). These research directions collectively offer potential to advance theoretical understanding while providing practical insights for market participants and policymakers seeking enhanced IPO market efficiency.

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors extend their appreciation to Taif University, Saudi Arabia, for supporting this work through project number (TU-DSPP-2024-310).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data is available upon request from the corresponding author.