Abstract

This article aims to examine the factors affecting the selection of real-time systems or batch systems in auditing, thereby making judgments about the influence of this choice on audit quality. The purpose is to provide recommendations on which cases to use real-time and batch systems, and how they affect audit quality when choosing one of these processing systems. The study investigates the relationship between data processing systems (real-time systems and batch systems) and audit quality. The article measures and evaluates the influence of factors on the choice of real-time systems or batch systems and their impact on audit quality. Auditing financial statements may involve working with real-time systems that record transactions as they occur or batch systems that process transactions in groups over time. Operational audits may include testing a real-time system that monitors and controls activities instantly or a batch system that aggregates operational data periodically. The choice between these systems depends on factors such as the availability and quality of data, the complexity of the system, and the level of audit risk. Real-time systems often include built-in validation and control features that help identify errors or fraud immediately, allowing for timely corrective actions. As a result, auditors can reduce audit risk and improve overall audit quality when using real-time systems. In contrast, batch systems may limit auditors’ access to up-to-date information, requiring them to rely on sampling or extrapolation methods to gather audit evidence. When working with batch systems, auditors may need to perform additional procedures and apply more subjective judgment, which can increase audit risk and reduce audit quality. In summary, factors such as data characteristics, the nature and performance of tests, the timing of information delivery, and available resources all influence the decision to use a real-time or batch processing system.

Implication practices

Theoretical implication

The article helps readers understand how to apply real-time systems and batch systems in auditing. Real-time and batch systems theory development can help entities to understand how to record transactions as they happen, or batch systems process transactions in batches from which to take control measures and integrated authentication to identify errors or fraud immediately, allowing for timely corrective action.

Practical implications

For audit firms, the real-time and batch systems help the auditors themselves design audit procedures in a way that is appropriate to the way the client’s data is handled, minimizing audit risk and improve audit quality. Understanding these two ways of handling data also helps businesses in general control information, ensuring accurate and relevant information.

Originality/value

The study focuses on the role of each real-time system and batch system in auditing, giving opinions that no research has specifically mentioned it. The article also explores practical solutions and ideas for future research, adding uniqueness and value to using real-time and batch systems in auditing and affecting audit quality.

Plain language summary

This article aims to examine the factors affecting the selection of real-time systems or batch systems in auditing, thereby making judgments about the influence of this choice on audit quality. The purpose is to provide recommendations on which cases to use real-time and batch systems, and how they affect audit quality when choosing one of these processing systems.

Keywords

Introduction

The selection between real-time and batch processing systems for audits depends on factors such as data characteristics, audit objectives, system performance, timing of information delivery, and resource availability. Real-time systems are suited for immediate data processing and are particularly valuable in audits that require prompt feedback, such as those involving continuous monitoring of financial transactions or internal control systems. These systems enhance the accuracy and timeliness of financial reporting by recording transactions as they occur, which is critical for audits requiring rapid response and real-time assurance. In contrast, batch processing systems are often preferable for audits involving large volumes of data—such as financial statement audits—because they process transactions collectively, offering potential efficiencies in resource utilization despite longer processing times. The nature of the audit, urgency of data access, and available technological and human resources all play vital roles in determining the appropriate system. An inappropriate system choice may compromise audit quality by limiting the availability of sufficient and appropriate audit evidence. Therefore, aligning the processing system with the audit’s specific requirements and the underlying data characteristics is essential to ensure high audit quality (Kim et al., 2010; Mustapha & Lai, 2017).

There have been many separate studies on real-time systems and batch systems such as Kraetz and Morawski (2021), Friedman and Tzoumas (2016). Some other studies only study the application of information technology in auditing such as Mustapha and Lai (2017), Havelka and Merhout (2013); there are almost no studies on the application of real-time systems and batch systems in auditing.

Real-time systems significantly contribute to audit quality by enabling the immediate recording and validation of transactions. Their ability to provide auditors with timely, accurate, and continuously updated data allows for enhanced risk detection, more effective internal control testing, and quicker responses to anomalies. These features help reduce the likelihood of material misstatements and reinforce stakeholders’ trust in financial statements (Luo et al., 2022).

In contrast, batch processing systems operate by handling data at set intervals, making them well-suited for tasks involving high data volumes or retrospective analysis. Although they may not support real-time monitoring, batch systems remain relevant in auditing by facilitating structured, periodic reporting and supporting cost-efficient audit procedures (Stoel et al., 2012). However, the delay inherent in batch processing can reduce responsiveness and limit auditors’ ability to detect issues promptly.

The selection between real-time and batch systems should reflect the specific audit objectives, the client’s business environment, the nature and timeliness of available data, and the level of audit risk. In many engagements, a hybrid approach—leveraging the real-time system’s responsiveness alongside the batch system’s structured aggregation—offers a comprehensive solution. Each system has distinct advantages that, when combined, can enhance audit efficiency and assurance quality.

From a research perspective, examining how these systems influence audit outcomes provides insights into optimizing audit methodologies. Real-time systems improve fraud detection, support continuous auditing, and are critical in dynamic environments like online banking or real-time inventory control. Batch systems, on the other hand, are essential for processing large transactional datasets and generating consolidated reports efficiently.

This study aims to evaluate how system selection affects audit quality and to propose frameworks that guide auditors in adapting their approaches to different technological contexts. By doing so, it contributes to the theoretical understanding of audit technology integration and supports practitioners in aligning audit techniques with system capabilities. For regulators, these insights offer a foundation to refine audit standards in response to technological advancement. For practitioners, especially in rapidly evolving markets like Vietnam, understanding the interaction between audit systems and audit quality is essential for effective planning, risk assessment, and compliance with international standards amid local economic and regulatory changes.

The article raises the following issues:

* How to use real-time systems and batch systems in auditing? What is the difference between these two methods?

* Under what circumstances will auditors use real-time systems or batch systems?

* Identify and measure factors affecting the selection of real-time systems and batch systems in auditing

* Identify and measure factors affecting audit quality when using real-time systems and batch systems

Literature Reviews

Real-time systems in auditing have evolved over several decades as technological advancements have enabled auditors to process and analyze data in increasingly efficient and effective ways. Batch processing systems in auditing were first developed in the mid-20th century to automate the processing of large amounts of data. Before the advent of computers, audits were conducted manually using paper-based systems, which were time-consuming and prone to errors. The earliest batch-processing systems in auditing were developed in the 1950s, using mainframe computers to process large volumes of data. These systems were typically used for financial audits, such as those conducted by the Internal Revenue Service (IRS) in the United States (Daniel et al., 2021; Goodhope et al., 2012).

With the advent of big data technologies, such as Hadoop and Spark, auditors began to develop real-time systems for analyzing large volumes of complex data, such as social media data, sensor data, and machine data. These systems were typically designed for high-volume, low-latency processing and relied on specialized software, such as Apache Kafka, Apache Storm, and Spark Streaming. Today, real-time systems continue to evolve as auditors incorporate machine learning, artificial intelligence, and natural language processing technologies into their systems. These advanced technologies enable auditors to analyze complex data sets in real time, detect anomalies and outliers, and make informed decisions based on the results of their analyses. In summary, real-time systems in auditing have evolved from mainframe-based transaction processing systems to spreadsheet-based financial data analysis systems to extensive data-based real-time analysis systems. Today, batch processing systems in auditing continue to be an essential tool for auditors, allowing them to process and analyze large amounts of data more efficiently and accurately than ever. These systems are now typically integrated with other auditing tools, such as data analytics and visualization, to provide a more comprehensive and insightful view of audit results. Today, auditors continue to explore new technologies and approaches to real-time processing to improve their audits’ accuracy, efficiency, and effectiveness.

Many companies have used batch processing in their audits, as it is a commonly used approach in auditing. Deloitte, one of the “Big Four” accounting firms, uses batch processing in its audits to process large volumes of financial data quickly and accurately. PwC, another of the “Big Four” accounting firms, uses batch processing in its audits to process data from multiple sources, including financial statements, internal controls, and risk assessments. KPMG, another “Big Four” accounting firm, uses batch processing in its audits to automate routine tasks, such as data entry and reconciliation. A multinational technology company, IBM has developed batch processing tools, such as IBM DataStage, to help auditors process large volumes of data quickly and accurately. IBM has developed some batch processing solutions for audits, including the IBM Trusteer Fraud Protection solution, which uses batch processing to analyze transactional data and detect potential fraud. A multinational software company SAP has developed batch processing tools, such as SAP Data Services, to help auditors extract and process data from multiple sources. EY has also used batch processing in its audits, particularly in data analytics. EY’s Advanced Analytics solution uses batch processing to analyze large amounts of data and identify patterns and anomalies to support its audit and assurance services. EY uses real-time systems to monitor and analyze data in real time, particularly in fraud detection. EY’s Fraud Investigation and Dispute Services (FIDS) team uses real-time data analytics tools to identify potential fraud and other financial crimes as they occur. Batch processing is a widely used approach in auditing, enabling auditors to process extensive data efficiently and accurately. Many companies also use batch processing and other technologies to support their audit and assurance services (Bierstaker et al., 2001).

Batch processing in auditing involves processing large amounts of data in batches, typically scheduled and automated. Here are some steps to follow when using batch processing in auditing: (1) Identify the data sources: Determine the data sources required for the audit and identify the file formats, locations, and access requirements for each source. (2) Extract the data: Extract the required data from the identified sources and save it in a suitable format for batch processing, such as CSV or Excel. (3) Create a batch processing script: Write a script or program to process the data in batches, typically using specialized software such as ACL, IDEA, or Excel macros. The script should be designed to perform the required tests and analyses, such as trend analysis, ratio analysis, and duplicate detection. (4) Configure the batch processing environment: Configure the batch processing environment, including the software and hardware required for batch processing. This may involve setting up a dedicated server or using cloud-based processing services. (5) Execute the batch processing: Execute the batch processing script and monitor the progress of the batch processing. Verify that the data is being processed correctly and that the batch processing produces the expected results. (6) Review and analyze the results: Review the results of the batch processing and analyze the data to identify potential issues or anomalies. Document any findings and conclusions. (7) Communicate the results: Communicate the results of the batch processing to the audit team and stakeholders, highlighting any significant findings or issues identified during the audit. In summary, using batch processing in auditing involves extracting data from multiple sources, processing it in batches using specialized software, and analyzing the results to identify potential issues or anomalies. Following best practices in batch processing is essential, such as verifying data accuracy, testing the processing script, and documenting findings and conclusions (Kraetz & Morawski, 2021).

Which batch systems or real-time systems are the most suitable for auditing? The choice of which batch system or real-time system to use in auditing will depend on the specific needs and requirements of the audit engagement. However, here are some of the commonly used batch systems and real-time systems in auditing (Shahrivari, 2014):

Batch system: ACL Analytics: This popular data analytics software used in auditing enables auditors to analyze large volumes of data and identify potential risks and anomalies. IDEA is another popular data analytics software used in auditing. It offers a range of features that enable auditors to analyze data and identify issues and irregularities. TeamMate Analytics: This data analytics software developed by Wolters Kluwer is explicitly designed for auditors. It offers a range of features for data analysis, including predictive analytics, and enables auditors to generate reports and visualizations to support their findings.

Real-time Systems: EY Helix: This cloud-based platform developed by EY uses real-time data analytics to provide auditors with up-to-date information about potential issues or anomalies in financial data. KPMG Clara: This cloud-based platform is designed by KPMG that uses real-time data analytics to provide insights and recommendations to clients. PwC Aura: This data analytics platform developed by PwC uses real-time monitoring to detect potential control issues and provide real-time alerts to clients. Deloitte Real-time Audit: This platform developed by Deloitte uses real-time data analytics to detect potential fraud and other matters in financial data. Again, the choice of batch system or real-time system will depend on the specific needs of the audit engagement. Auditors should evaluate each system’s features and capabilities to determine which is the most suitable for their needs.

Batch processing and real-time processing are two different approaches to processing data in auditing. Batch processing involves processing data in large batches or groups, typically at the end of a reporting period or fiscal year. The data is usually collected and processed in a sequence, with each batch being processed in order and any errors or issues being identified after the entire batch has been processed. In auditing, this approach is commonly used for tasks such as verifying the accuracy of financial statements or reconciling accounts. On the other hand, real-time processing involves processing data as it is received, allowing for analysis and insights to be generated in real-time. This approach will enable auditors to access and analyze data continuously rather than wait until a reporting period or fiscal year ends. In auditing, real-time processing can be used to monitor transactions or detect fraud. The main difference between these two approaches is the data processing timing. Batch processing is a more traditional approach and is often used for tasks requiring high accuracy and precision. On the other hand, real-time processing allows for more immediate analysis and can help identify issues as they occur. In auditing, batch processing and real-time processing can be useful, and the chosen approach will depend on the specific task at hand. For example, batch processing may be more appropriate for verifying the accuracy of financial statements, while real-time processing may be more beneficial for detecting fraud or monitoring transactions (Ross, 1986).

Batch systems process data at set intervals, which can create gaps in the controls and validations that are otherwise present in real-time systems. Batch systems lack immediate data validation checks as transactions are not processed in real time. Errors, anomalies, or incomplete data entries may go undetected until the batch processing is completed, causing delays in identifying and correcting issues. Implementing pre-batch validation checks, such as data completeness checks, range checks, and consistency checks before data is processed in batches. Additionally, post-batch reconciliation controls can help detect any discrepancies between input data and output results. Batch systems do not support continuous monitoring of data and processes, leading to delayed detection of unusual activities or fraudulent transactions. There is also a lack of automated alerts for abnormal patterns or deviations from expected behavior. Introduce periodic monitoring controls between batch runs to identify potential irregularities. Implement automated alert systems that flag discrepancies or unusual patterns immediately after batch processing completes. Using anomaly detection tools on historical batch data can also help identify trends that may indicate control issues. In batch systems, individual transaction controls (such as authorizations, approvals, and logging) may be weaker or entirely missing, as transactions are grouped and processed together. This can make it difficult to trace errors or unauthorized activities back to a specific transaction. Strengthen transaction-level controls by incorporating digital signatures, timestamps, and user authentication data for each transaction within the batch. Implement detailed logging and audit trails that capture individual transaction details, even within batch processing. Batch systems are more vulnerable to fraud since they do not detect or prevent fraudulent activities in real-time. Suspicious activities may remain hidden until the batch is processed, allowing fraudulent transactions to accumulate. Use advanced analytics and machine learning techniques on batch data to identify patterns indicative of fraud. Implement post-batch review procedures that specifically focus on high-risk transactions or unusual patterns and integrate them with fraud detection software (Kourti, 2003).

Previous studies have explored the implications of batch and real-time systems in auditing, focusing on their specific advantages and limitations. Hunton (2003) discussed the benefits of real-time systems in supporting continuous auditing, emphasizing their ability to provide immediate error detection and enhance audit responsiveness. Vasarhelyi and Halper (2018) also highlighted the role of real-time systems in improving audit accuracy and timeliness by integrating real-time monitoring and controls. In contrast, Heidari et al. (2016) examined the cost-effectiveness and efficiency of batch processing for managing large volumes of data, suggesting its suitability for audits where transactions are less time-sensitive. However, these studies primarily examine batch and real-time systems in isolation, without a comparative analysis of how their selection affects overall audit quality in diverse contexts. This study addresses this gap by investigating the factors influencing the choice between these systems and their impact on audit quality, offering a more holistic understanding to guide auditors and regulators.

Theoretical Basis

The theoretical basis for using real-time and batch systems in auditing can be understood through several key concepts and principles in the fields of information systems, accounting, and auditing theory. These systems are designed to support the objectives of auditing by ensuring accuracy, efficiency, compliance, and risk management in financial reporting and operations.

Based on the provided document, two relevant theories for using real-time and batch systems in auditing are Information Processing Theory and Control Theory.

Information Processing Theory

This theory focuses on how information is collected, processed, stored, and used within an organization. It supports the idea that the way data is processed can significantly affect decision-making, performance, and outcomes (Gales & Mansour-Cole, 1995).

Information Processing Theory is crucial for understanding the applicability of real-time and batch systems in auditing. Real-time systems align with this theory by providing immediate processing and feedback, which enhances decision-making and error detection crucial for accurate financial reporting. In contrast, batch systems support the theory’s emphasis on efficiently managing large volumes of data, which helps reduce the cognitive load on auditors and makes it easier to identify patterns, trends, and anomalies during the audit process.

This theory is directly relevant because it explains how different data processing systems (real-time vs. batch) affect the flow and availability of information for auditors. Real-time systems, by providing immediate access to data, enhance timely decision-making and allow auditors to detect errors or fraud as they occur, which is essential for maintaining the integrity and accuracy of financial reports. Batch systems, on the other hand, align with the theory’s focus on handling large datasets efficiently, making it easier for auditors to analyze data trends and anomalies. This study leverages the theory to demonstrate how choosing the appropriate data processing system can optimize audit processes and outcomes depending on the data’s nature and the audit’s objectives.

Control Theory

Control Theory deals with the ways organizations manage and regulate their operations to achieve desired outcomes, including error detection, prevention, and correction (Silva et al., 2021).

Control Theory is relevant because it underscores the importance of continuous monitoring and corrective actions in auditing, both of which are supported by real-time systems. These systems provide auditors with tools to immediately detect and respond to deviations from expected norms, thereby reducing audit risk. Batch systems align with the theory by providing systematic, periodic reviews and controls, ensuring data integrity and compliance over time.

Control Theory is crucial because it underpins the auditing objective of maintaining robust internal controls over financial reporting and operations. Real-time systems are relevant as they allow for continuous monitoring and immediate corrective actions, reducing the risk of undetected errors or fraud. This supports the study’s focus on how real-time systems can improve audit quality by providing ongoing oversight. Meanwhile, batch systems are relevant to control theory as they provide periodic controls and checks at set intervals, ensuring consistent and predictable compliance with audit standards. The study applies this theory to show how selecting between these systems impacts an organization’s ability to manage and mitigate risk effectively.

By integrating these two theories, the study contributes to a deeper understanding of how different data processing systems affect auditing practices, guiding the selection of appropriate systems to enhance audit quality.

Hypotheses Development

Factors Affecting the Choice of Batch System or Real-Time System in Auditing

Size, security, and complexity of data: Batch processing may be more suitable for large and complex data sets that require significant processing time, whereas real-time processing may be ideal for smaller, real-time data streams that require immediate processing. Real-time systems may be more susceptible to security risks, such as cyber-attacks or data breaches, than batch systems. Organizations may need to consider the security risks of real-time systems before choosing a real-time system (Hansen, 1983; Havelka & Merhout, 2013). The choice between a batch system or a real-time system in auditing is significantly influenced by the size, security, and complexity of data. For large volumes of data, batch processing is often more efficient because it allows for the processing of data in bulk, typically during off-peak hours. This reduces the computational load on systems and makes it easier to handle and store large datasets. For smaller datasets or when immediate action is required, real-time processing is preferred. It ensures that data is analyzed as it is generated, allowing auditors to identify issues quickly. When security is a significant concern, batch processing may be preferable as it can be performed in a controlled environment, reducing the risk of data breaches. Additionally, sensitive data can be encrypted and processed in a more secure manner. Real-time systems, due to their continuous operation, may expose data to more vulnerabilities. However, they can also be equipped with immediate threat detection and response mechanisms, which are crucial in high-security environments. Complex data often requires extensive computation and transformation, which can be more effectively managed in a batch process. Batch systems allow for thorough analysis without the pressure of immediate results, which is useful for complex data sets. When data complexity requires immediate interpretation or action, real-time systems are necessary. These systems can be more challenging to implement due to the need for advanced algorithms capable of handling complex data on the fly Hunton (2003) in their book “Core Concepts of Information Technology Auditing,” the authors discuss how the complexity and volume of data influence the choice between batch and real-time processing in IT audits. Vasarhelyi et al. (2010) in “The continuous audit of online Systems” explore how the size and complexity of data necessitate different processing approaches in the context of real-time auditing systems.

H1: The greater the size, complexity, and security requirements of the information, the more need to use a batch system

H2: The larger the size, security, and complexity of data, the lower the audit quality

Nature of the audit engagement: Real-time systems may be more suitable for audits where real-time monitoring and analysis are critical, such as audits of financial institutions or fraud investigations. Batch systems may be ideal for audits of historical financial data or other audits requiring significant data processing and analysis (Bruno, 1969; Fu & Soman, 2021).

Real-time processing in auditing allows for the immediate analysis of data as it’s generated, critical for dynamic assessments. Key steps include: (1) Identifying sources of real-time data, like market feeds or social media. (2) Choosing a suitable real-time analysis tool, such as Apache Kafka or Spark Streaming. (3) Setting up the required software and hardware for real-time processing, potentially using cloud services. (4) Creating algorithms for data analysis to detect anomalies or predict trends. (5) Implementing these algorithms and monitoring their outcomes in real time. (6) Evaluating the data to pinpoint any issues, and documenting findings. (7) Sharing insights with the audit team and stakeholders. Effective real-time auditing hinges on accurate data source identification, robust tool selection, meticulous algorithm development, and thorough analysis and documentation of results (Bose et al., 2017; Lunt et al., 1992)

H3: Auditors use a real-time system when the audit requires monitoring the processing and making necessary adjustments to ensure the accuracy and reliability of the data.

H4: The nature of the audit affects the quality of the audit

Operational Efficiency

Real-time processing in systems that handle large volumes of transactions every day can create operational inefficiencies. A single transaction can affect a different number of accounts. However, some of these accounts may not need real-time updates. In practice, doing so is time-consuming, which, when multiplied by hundreds or thousands of transactions, can cause significant processing delays. However, bulk processing of non-critical accounts improves operational efficiency by eliminating unnecessary operations at the critical point. Real-time systems can be more expensive than batch systems due to the need for specialized software, hardware, and personnel. Organizations may need to consider the cost of these systems before choosing a real-time system (Havelka & Merhout, 2007).

Designers must consider the trade-off between productivity and efficiency when choosing a data processing mode. For example, users of an airline booking system cannot wait until 100 passengers (adequate batch size) have gathered at a travel agent’s office before their transaction is processed. Real-time processing is the logical choice when immediate access to current information is critical to serving users’ needs. When the time delay in the data has no adverse impact on user performance and operational efficiency, batch processing can be used (Luo et al., 2022).

H5: Real-time system makes company operations and audits less efficient

H6: Prioritizing operational efficiency will result in lower audit quality

Information time frame: The batch system collects transactions into groups for processing. According to this approach, there is always a lag between the time an economic event occurs and the point at which it is reflected in the company’s accounts. The amount of delay depends on the batch processing frequency. The delay can range from a few minutes to several weeks. Payroll processing is an example of a typical batch system. Employee-related events occur continuously throughout the pay period. At the end of the period, wages for all employees are prepared together in one installment (Shahrivari, 2014).

Real-time systems process individual transactions at the time the event occurs. Since records are not grouped into batches, there is no time lag between occurrences. An example of real-time processing is an airline booking system, which processes service requests from one traveler at a time while they wait (Shays, 1995).

Overall, the choice of real-time systems or batch systems in auditing will depend on the specific needs and requirements of the organization and the audit engagement. Organizations should consider these factors and consult with audit professionals to determine the most appropriate system for their needs.

H7: The high level of concern about the lag between when an economic event occurs and when that event is reflected in the company’s accounts leads auditors to choose a real-time system for their audits.

H8: The larger the information time frame, the lower the audit quality

Resources

Generally, batch systems require fewer organizational resources (such as programing costs, computer time, and user training) than real-time systems. For example, batch systems may use sequential files stored on tape. Real-time systems directly accessing files require more expensive storage devices like magnetic disks. These cost differences are disappearing. Therefore, business organizations often use magnetic disks for batch and real-time processing. The essential resource differences are in systems development (programing) and computer operations. Since the resources for batch systems are often more straightforward than those for real-time systems, they have shorter development times and are more accessible for developers to maintain. On the other hand, up to 50% of the total programing costs for Real-time systems are incurred in the design of user interfaces (Stoel et al., 2012). The real-time system is user-friendly and easy to work with, but when it comes to pop-up menus, online tutorials, and concierge features require additional programing and adds significantly to the cost of the system. Finally, real-time systems require specialized processing power. Real-time systems have to process transactions as they happen, while some systems have to use them 24 hr a day, whether needed or not. Computer capacity reserved for such systems cannot be used for other purposes. Therefore, implementing a Real-time system may require the purchase of a dedicated computer or investing in additional computing capacity. In contrast, batch systems only use computer space while running the program. When the batch job is finished processing, the freed space can be reallocated to other applications (Vasarhelyi & Halper, 2018).

H9: Auditors will use real-system in case the data is simple, small-scale, and the cost for the audit is low

H10: The larger the resource, the higher the quality of the audit

Effect of Choosing a Batch System or Real-Time System on Audit Quality

Batch processing can have a significant impact on audits. Batch processing refers to processing multiple transactions together in a group or batch rather than processing each transaction individually. This can result in several benefits for organizations, including increased efficiency and cost savings. However, it can also present particular challenges for auditors. One of the critical challenges with batch processing is that it can make it more difficult for auditors to identify errors or irregularities in individual transactions. With batch processing, multiple transactions are combined into a single batch, making identifying specific issues with any one transaction harder. This means auditors may need to spend more time reviewing the batch to identify any potential issues. In addition, batch processing can make it more difficult for auditors to trace transactions through the accounting system. With individual transactions, auditors can easily trace each transaction from start to finish (Yacobi, 2001). However, with batch processing, multiple transactions are combined, making it harder to track individual transactions and identify where they originated from and where they ended up. Overall, the impact of batch processing on audits will depend on the specific circumstances of each organization. While batch processing can provide certain benefits, organizations need to work closely with auditors to ensure that the audit process can effectively identify and address any potential issues that may arise.

Real-time systems are computer-based systems that process transactions as they occur. These systems require auditors to consider different factors when assessing audit quality. Real-time processing controls are essential for ensuring transactions are processed accurately and completely. If these controls are inadequate or absent, there is a higher risk of errors or fraud. Real-time systems must be available and operational at all times. Any downtime or system interruptions can impact audit quality and reduce the reliability of data used in the audit. Real-time systems must provide a fast response time to users. If system response time is slow, this can impact data reliability and may affect audit quality (Shahrivari, 2014).

H11: The choice of batch processing and real-time processing affects audit quality

Research Design

Collect Data

Survey Tools and Measures

We used a survey instrument to collect data to test the hypotheses. The content of the survey forms includes (1) Introduction to research objectives and introductory and screening questions; (2) A set of questions to measure the impact of factors on the selection of batch systems and real-time systems in auditing and the impact of applying batch systems or real-time systems on the quality of the audit; (3) The last part is a thank you note.

The measurement of variables was adapted from previous studies applying batch systems and real-time systems. We select scales with high reliability and then evaluate the appropriateness of the selected scales. We used the Vietnamese questionnaire for the survey, which was then translated into English when synthesizing the results. We conducted 10 in-depth interviews with information technology experts and 25 interviews with independent audit businesses. After these interviews, we have revised some of the content in the questionnaire to suit the application of batch systems and real-time systems better in practice. The questionnaire’s content is evaluated on a 5-point Likert scale, from 1 being “Strongly disagree” to 5 being “Strongly agree.”

Collect Data and Samples

To apply SEM, at least 10 respondents are required for each parameter estimated in the model. A minimum sample size of 200 is generally recommended for stable Maximum Likelihood (ML) estimates. To detect small to medium effect sizes, researchers typically aim for a power of 0.80, which influences the sample size requirement. Larger samples increase the power of the model.

As a general rule of thumb for sample size: A minimum sample size of 100 to 150 respondents is often cited as the absolute lower limit for SEM, regardless of the complexity of the model. A general guideline is to have a minimum of 10 participants for each parameter estimated in the model. For example, if the model has 20 parameters, a sample size of at least 200 is recommended. Many researchers believe that for reliable and stable results, a sample size greater than 200 is desirable.

Therefore, this study distributed 230 questionnaires. Data were collected from April to June 2022 using survey methods. We visited auditing businesses directly (45 businesses), and the rest were coordinated with firms to obtain survey results. Respondents who agreed to participate in the survey were provided with the necessary means and support to ensure the survey was conducted objectively and accurately. All volunteer respondents were informed about the study objectives, and their information was kept confidential. An incentive of 50,000 VND (about 2 USD) was given to each participant. After more than 2 months of surveying, with 230 surveys distributed, we collected 202 surveys. After filtering out incomplete responses, we were left with 192 questionnaires (for each business, we collected about one for analysis).

Data Analysis Methods

We used IBM SPSS 25 and IBM AMOS 25 software to analyze research data. SPSS 25 software is used to analyze Cronbach Alpha, Kaiser-Meyer-Olkin coefficient Measures the adequacy of sampling, Total Variance Interpreted shows the percentage of variation of observed variables, and Pattern Matrix for consideration convergence of factors. AMOS 25 software was used for confirmatory factor analysis (CFA), method variance coefficient, Regression Weights, Standardized Regression Weights, and structural equation modeling (SEM) analysis.

Measurement and structural models are evaluated using indices such as Chi-square ratio and degrees of freedom (χ2/df); goodness-of-fit index (GFI); and root mean square error of approximation (RMSEA; Figure 1).

Model of research.

Factors Affecting the Choice of Real-Time Systems or Batch Systems and Audit Quality

After running the rotation matrix, the coefficient KMO = 0.875 > 0.5, sig = .000 < .05 (Table 1), so the model is satisfactory.

KMO and Bartlett’s Test.

In Table 2:

Total Variance Explained.

Note. Extraction Method: Principal Axis Factoring.

When factors are correlated, sums of squared loadings cannot be added to obtain a total variance.

Initial Eigenvalues:

○ Total: Represents the eigenvalue for each factor before extraction. An eigenvalue is a measure of the variance in all the variables that a particular factor accounts for. Factors with eigenvalues greater than 1 are typically considered significant.

○ % of Variance: The percentage of total variance in the data explained by each factor before extraction.

○ Cumulative %: The cumulative percentage of variance explained by all factors up to that point before extraction. For example, Factor 1 explains 36.11% of the variance, and the first two factors together explain 45.35%.

Extraction Sums of Squared Loadings:

○ Total: Shows the eigenvalues for each factor after the extraction method has been applied. It represents the amount of variance accounted for by the factors after extraction.

○ % of Variance: The percentage of total variance explained by each factor after extraction. For example, after extraction, Factor 1 explains 34.75% of the variance.

○ Cumulative %: The cumulative percentage of variance explained by all factors up to that point after extraction. For instance, the first three factors together explain 50.21% of the variance.

Rotation Sums of Squared Loadings:

○ Total: Shows the eigenvalues after rotation. Rotation is a technique applied to make the output easier to interpret by redistributing the variance accounted for by the factors. It doesn’t change the total variance explained but clarifies which variables load on which factors.

○ For example, after rotation, Factor 1 explains 5.375 units of variance, and Factor 2 explains 5.322 units.

Factors with Eigenvalues > 1: Generally, only factors with an eigenvalue greater than 1 are considered significant. In this table, Factors 1 through 7 have eigenvalues greater than 1 before extraction, suggesting that these factors could be retained for analysis.

Variance Explained:

o The first factor (Factor 1) accounts for 36.11% of the variance before extraction but 34.75% after extraction.

o After rotation, each factor (Factor 1 to Factor 7) accounts for a more balanced share of the variance (around 5.0 to 5.4 units), indicating that the rotation helped distribute the variance more evenly across the factors.

Cumulative Variance:

o The table shows that the first seven factors together explain about 66.65% of the total variance (after rotation). This suggests that these seven factors capture most of the data’s variability and might represent the underlying dimensions or constructs measured by the variables.

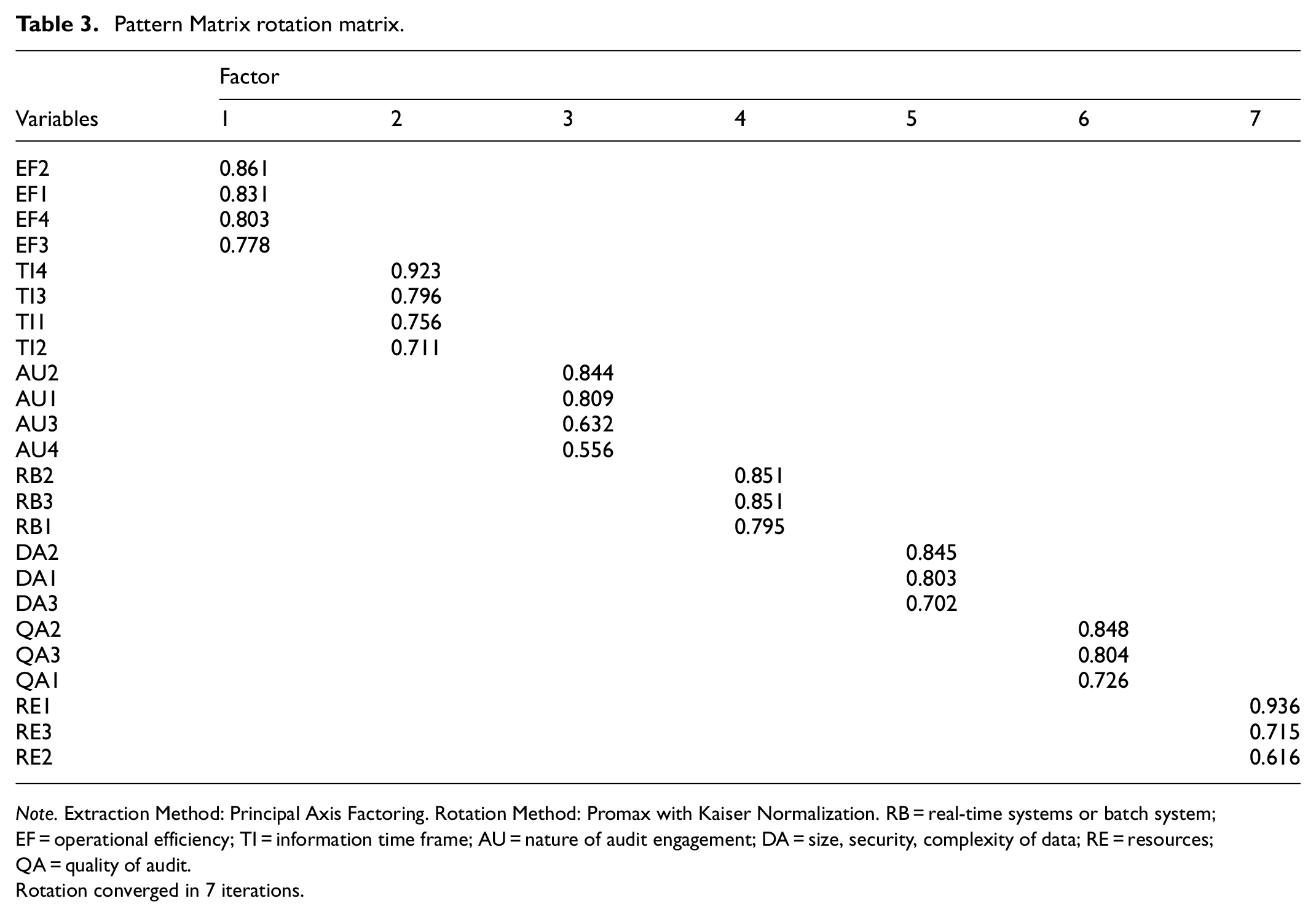

Pattern Matrix rotation matrix (Table 3) is used to analyze factor confirmatory in AMOS software, to see whether the elements are convergent and discriminant.

Pattern Matrix rotation matrix.

Note. Extraction Method: Principal Axis Factoring. Rotation Method: Promax with Kaiser Normalization. RB = real-time systems or batch system; EF = operational efficiency; TI = information time frame; AU = nature of audit engagement; DA = size, security, complexity of data; RE = resources; QA = quality of audit.

Rotation converged in 7 iterations.

Regression Weights results (Table 4 Column “P”) show that: independent variables E.F. (Operational efficiency), DA (Size, security, complexity of data), RE (Resources) have an impact on R.B. (Real-time systems or batch system; sig < .05). Hypotheses H1, H5, and H9 are accepted. The independent variables T.I. (Information time frame), A.U. (Nature of audit engagement) do not affect R.B. (Real-time systems or batch system; sig > .05). Hypotheses H3 and H7 are rejected. Similarly, variables E.F., T.I., A.U., R.B. impact the dependent variable Q.A. (Quality of audit; sig < .05). Hypotheses H4, H6, H8, H11 are accepted. The independent variable DA, RE does not affect Q.A. (sig > .05). Hypothesis H2, and H10 are rejected.

Regression Weights: (Group Number 1 - Default Model).

Note. RB = real-time systems or batch system; EF = operational efficiency; TI = information time frame; AU = nature of audit engagement; DA = size, security, complexity of data; RE = resources; QA = quality of audit.

p < 0.01.

Standardized Regression Weights results (Table 5, Column “Estimate”) show that:

Standardized Regression Weights: (Group Number 1 - Default Model).

Note. RB = real-time systems or batch system; EF = operational efficiency; TI = information time frame; AU = nature of audit engagement; DA = size, security, complexity of data; RE = resources; QA = quality of audit.

Impact on R.B.: The independent variable DA has the most substantial effect with 0.371, followed by E.F. (0.336), RE (0.220); T.I. and A.U. have no impact. Impact on QA: The variable R.B. has the most substantial Effect with 0.389, followed by T.I. (0.358), E.F. (0.229), A.U. (0.227). DA and RE have no impact.

We can see a summary of the data and the relationship between the variables shown in Figure 2 below.

The results of the research model.

In Figure 2: The measurement model have a good fit overall. While the Chi-square test is significant (which can be expected with large sample sizes), the Chi-square ratio (χ2/df = 1.51) and RMSEA (0.051) both indicate that the model fits the data adequately. The RMSEA being very close to 0.05 also suggests that the approximation error in the population is minimal, supporting the model’s validity.

Discussion and Conclusion

Discussion

From the above research results, the selection of real-time systems or batch systems in audit shows that data size, security, and complexity are the most critical factors determining the choice of real-time systems or batch systems in auditing. Data size, security, and complexity are essential factors in deciding between real-time systems and batch systems in auditing because they affect the audit process’s efficiency, accuracy, and reliability. When dealing with large volumes of data, batch processing may be more efficient as it can process data in large batches. Real-time systems may struggle to process such large amounts of data in real-time, resulting in delays and increased costs. However, real-time systems may be more appropriate when dealing with small to medium-sized datasets, as they can process data as soon as it is available, providing the auditor with more up-to-date information. Security is a critical consideration when it comes to auditing. Real-time systems can provide more immediate alerts and monitoring capabilities to help detect security breaches or potential fraud, which can help mitigate risks.

On the other hand, batch systems may require additional security measures to ensure that data is not compromised during processing. Batch systems can be more appropriate when dealing with complex data as they can handle complex calculations and data manipulation more efficiently. Real-time systems may struggle with complex data due to the need for immediate processing, which can lead to errors and inaccuracies. However, real-time systems may be better suited to simple data that can be processed quickly and with minimal complexity. Data size, security, and complexity are important factors when deciding between real-time and batch systems in auditing. Both systems have their strengths and weaknesses, and the choice should be based on the specific needs of the audit and the nature of the data being processed.

The choice between batch systems and real-time systems in an audit depends on the system’s operational efficiency requirements. A batch system may be more appropriate if the system is designed to process large volumes of data quickly. A real-time system may be more suitable if the system requires immediate responses or real-time monitoring. Auditors must consider the system’s operational efficiency requirements when selecting the appropriate audit procedures and tools. The choice of approach can affect the quality and reliability of the audit evidence obtained, so it is essential to choose the most appropriate system for the task at hand.Why does the information time frame not affect the choice to use the real-time or batch systems in the audit? The information time frame can influence the choice of audit procedures and tools, but it generally does not affect the choice between using a real-time or batch system in the audit.

The choice of system depends on the operational efficiency requirements of the system being audited and the type of data being processed. As mentioned earlier, batch systems are generally more efficient for processing large volumes of data relatively quickly. In contrast, real-time systems are designed to process data as it is entered or generated and provide immediate feedback or responses.

The information time frame refers to when the audit evidence is relevant and reliable. The auditor must obtain sufficient and appropriate audit evidence within a reasonable time frame to support their opinion on the financial statements or the internal control environment. However, the system choice does not directly affect the information time frame.

Instead, the system choice is based on the operational efficiency requirements of the system being audited and the nature of the data being processed. A real-time system may be more appropriate if the system requires immediate responses or real-time monitoring. If the system is designed to process large volumes of data quickly, a batch system may be more appropriate.

The choice between batch and real-time systems in auditing is heavily influenced by the characteristics of the system, which often outweigh the nature of the audit activity itself. Example: A financial statement audit for a large corporation involves analyzing millions of transactions across multiple departments. In this case, a batch system is preferable because it can efficiently handle large volumes of data by processing them in groups at scheduled intervals. This allows auditors to perform extensive analysis on aggregated data, identify trends, and detect anomalies over a longer period. The sheer volume of data requires a system that can manage high-capacity data processing without needing real-time monitoring. Even though the audit’s nature (financial statement audit) might require accuracy and completeness, the system’s ability to process large amounts of data effectively becomes the primary factor in choosing a batch system. Example: An internal audit focuses on detecting potential fraud in an online retail platform where transactions occur continuously. A real-time system is more suitable here because it can provide immediate alerts for any suspicious transactions or anomalies as they happen, allowing for rapid intervention. This continuous monitoring is essential to quickly identify and prevent fraud in environments where transactions occur at high speed and frequency. While the audit’s nature (fraud detection) dictates the need for monitoring, it is the system’s capability to provide immediate feedback and real-time processing that makes the real-time system the obvious choice. The ability to respond instantly to threats outweighs other considerations, emphasizing the system’s characteristics over the audit type. Example: An operational audit examines the effectiveness of an enterprise resource planning (ERP) system that integrates various business processes, including supply chain management, accounting, and human resources. Given the complexity of the ERP system, batch processing might be preferred for certain types of data, such as end-of-day financial reconciliations or monthly inventory reports, where real-time data is less critical. The system’s complexity makes it more feasible to validate and control data in a structured, scheduled manner. Although the operational audit aims to ensure overall process effectiveness, the choice of a batch system is driven by the ERP system’s complexity and the need for controlled, periodic processing rather than continuous real-time monitoring. The characteristics of the ERP system—its integration and complexity—are the key factors influencing the choice of a batch system (Kuhn & Sutton, 2010).

Implication

Researching batch systems and real-time systems in an audit context involves examining how these systems operate within an organization’s infrastructure and assessing their reliability, accuracy, and compliance with relevant standards or regulations. Batch systems typically process data in bulk at scheduled intervals. They collect data over a period and then process it in batches. In an audit, understanding batch systems involves evaluating the controls in place to ensure data integrity, security, and proper processing during these batch runs. This may include reviewing batch processing logs, error handling procedures, and the overall reliability of the system. Real-time systems, on the other hand, process data immediately as it comes in, responding rapidly to inputs and providing outputs in near-real-time. Auditing real-time systems involves assessing their responsiveness, accuracy, and reliability in handling data in real-time scenarios. This might involve examining the system’s architecture, monitoring mechanisms, and the effectiveness of controls in place to ensure timely and accurate processing. Auditing these systems involves assessing risks associated with their operation, ensuring they adhere to best practices, and identifying any areas for improvement to enhance their efficiency, reliability, and compliance.

Limitations and Future Research

Auditing both batch and real-time processing systems presents notable challenges and opportunities for further exploration. These systems are inherently complex, making it difficult to evaluate all components thoroughly. Real-time systems, in particular, are highly dynamic and subject to rapid technological changes, requiring audit methodologies to be continuously updated to remain effective. Comprehensive audits of such systems often demand significant investments in time, technical expertise, and advanced tools—especially when dealing with large-scale or high-volume environments where data is processed rapidly and in vast quantities.

To address these challenges, future research should focus on automating audit processes through the integration of AI and machine learning technologies to enable real-time monitoring, anomaly detection, and predictive analysis. Tailored methodologies need to be developed specifically for real-time systems, emphasizing dynamic risk assessment, adaptive control mechanisms, and continuous assurance. Additionally, the potential of blockchain and distributed ledger technologies (DLT) in enhancing audit trail transparency, data integrity, and traceability—especially in real-time environments—warrants deeper investigation. As cybersecurity risks grow alongside real-time data flows, research must also prioritize robust security frameworks that protect data integrity without hindering processing performance.

Scalability and system performance are other critical areas, requiring solutions that ensure reliability as data volumes and processing demands increase. Lastly, evolving audit standards and regulatory requirements necessitate that auditing methodologies for both batch and real-time systems remain flexible and up to date. Advancing these research areas will help overcome current limitations and lead to more effective, efficient, and resilient audit practices across diverse technological and organizational settings.

Conclusion

The choice of a batch system or real-time system in auditing depends more on the information system’s characteristics rather than the nature of the audit engagement. For example, a financial statement audit may involve auditing a real-time system that records transactions as they occur or a batch system that processes transactions in batches. Similarly, an operational audit may involve auditing a real-time system that monitors and controls operations in real time or a batch system that aggregates operational data over a period of time.

For factors affecting audit quality, the choice of a real-time or batch system can significantly affect audit quality. Real-time systems process transactions as they occur, providing up-to-date and accurate information. This can enable auditors to access and analyze data in real-time, increasing the completeness and accuracy of audit evidence. Real-time systems may also have built-in controls and validations that can help identify errors or fraud immediately, allowing for prompt corrective action. As a result, auditors may be able to reduce audit risk and improve the overall quality of their audits when working with real-time systems.

In contrast, batch systems process transactions in batches at predetermined intervals. This means that there may be a delay between the occurrence of a transaction and the update of the system’s records. This can make it more difficult for auditors to access up-to-date information, which may require them to rely on sampling or extrapolation methods to obtain audit evidence. Batch systems may also have fewer built-in controls and validations, increasing the risk of errors or fraud going undetected. As a result, auditors may need to perform additional audit procedures and rely on more subjective judgment when working with batch systems, potentially increasing audit risk and reducing the overall quality of their audits.

The size of the data being audited can affect audit quality because it can impact the auditor’s ability to review and analyze all relevant information. If the data set is too large, the auditor may need to use sampling techniques, increasing the risk of errors or fraud going undetected. However, with proper planning and appropriate audit procedures, auditors can obtain sufficient and appropriate audit evidence even from large data sets. The security of the data being audited is also critical because it can affect the reliability and accuracy of the information. If the data is not adequately secured, there is a risk that it could be altered, deleted, or accessed by unauthorized parties, which could compromise the accuracy of the audit evidence. Therefore, auditors need to assess the system’s security controls’ effectiveness to ensure the data’s reliability. The complexity of the audited data can also impact audit quality because it can affect the auditor’s ability to understand and interpret the information. If the data is too complex, the auditor may be unable to identify all relevant risks and controls, which can increase audit risk. In these cases, auditors may need to engage with subject matter experts or use specialized tools to understand the data better and obtain sufficient and appropriate audit evidence. In summary, data size, security, and complexity can impact audit quality. Auditors need to consider these factors when planning and performing the audit and use appropriate audit procedures to obtain sufficient and appropriate audit evidence.

In summary, factors such as the characteristics of the data, nature of the audit, performance, information time frame, and resources can all impact the choice of batch system or real-time system and the quality of the audit. It is essential for auditors to carefully consider these factors when planning and performing an audit to ensure that they select the most appropriate system and obtain sufficient and appropriate audit evidence.

Footnotes

Ethical Considerations

This article does not contain any studies with human participants performed by any of the authors.

Consent to Participate

There are no human participants in this article and informed consent is not required.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The datasets generated during and/or analyzed during the current study are available from the corresponding author on reasonable request.