Abstract

This study provides a systematic review of the literature on internal auditing (IA) research in 17 Arab countries. It focuses on four key aspects, namely the quality and effectiveness of IA, the objectivity and independence of IA, the consequences of IA, and the challenges facing IA in Arab countries in order to provide insights and avenues for future research in this field. Ninety-one (91) articles collected from the Scopus database between 1996 and April 2022 were analyzed in this study. The results show that there has been an increase in the number of studies that discussed IA, especially in the last 6 years. Most of these studies have focused on the quality of IA and its functions. It also shows that Jordan and the Kingdom of Saudi Arabia dominate the literature published so far in terms of the number of studies. Also, most of the studies were based on agency and institutional theory evaluating the various aspect of IA. This study highlights the lack of in-depth qualitative research that allows researchers to challenge the theories developed in the auditing field, add nuances to the existing theoretical framework, and unpack new theoretical directions. Furthermore, the results also show that the IA literature did not contribute significantly to the knowledge of internal audit functions (IAFs) as specified by the Institute of Internal Auditors (IIA). This study contributes to the body of knowledge by determining future research directions and surveys by interested researchers and regulators, including IIA.

Introduction

During the last few years, the international professional standards were introduced by the Institute of Internal Auditors (IIA) for the practice of internal auditing (IA) (IIA, 2012). However, compliance with these standards varied from one country to another due to several cultural, political, and social factors that affected the internal auditors’ practices (Abdolmohammadi & Sarens, 2011; Alzeban, 2015; Jinyu & Hazaea, 2020). Due to the influence of these aspects on the performance of the internal auditors, the IIA suggested that the Arab countries located in the Asian continent and North Africa is the region in which many procedures and organizational changes are expected to occur due to the great growth of the principles of governance mechanisms in these economies. However, research in these countries is still relatively limited, especially systematic literature review (SLR). In recent years, scarce studies have offered a review of empirical studies related to the Arab countries that took the similarity of these countries; politically, culturally, and religiously. Given the rapid economic developments in recent times, institutions have been required to introduce many modern regulatory and technological requirements due to financial operations’ complexity.

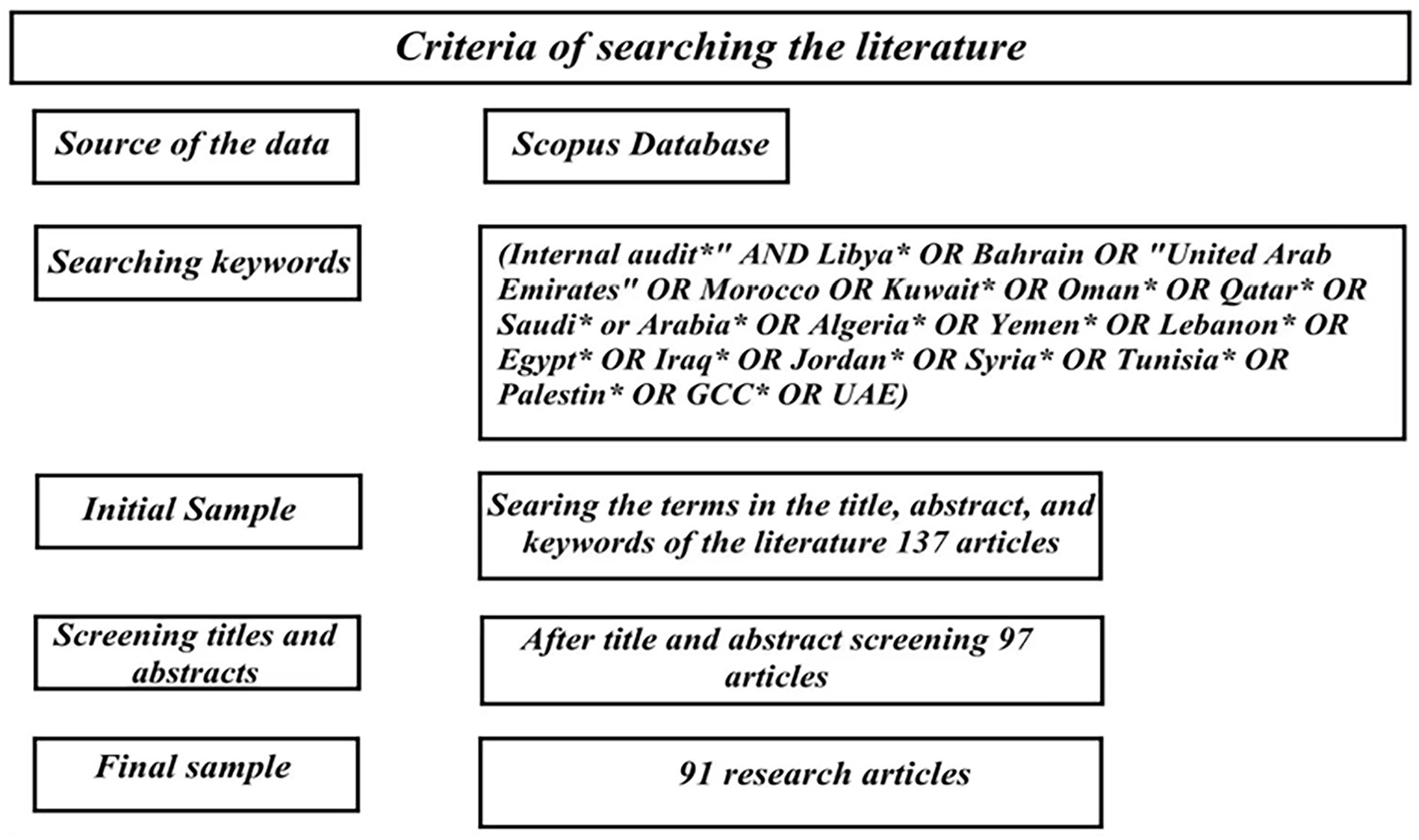

Due to the fact that the Arab countries witnessed significant changes and provided an integrated vision of IA practices for companies operating in the Arab region that are trying to compete internationally. Therefore, we have been motivated to conduct SLR to analyze the research trend on IA in Arab countries. This would provide a comprehensive knowledge map to the existing literature and provide guidance for future research. To do so, this study has searched for all relevant studies on the Scopus database using specific keywords. These keywords have been developed after reviewing similar studies (Kotb et al., 2020), which used SLR to discuss the field of IA post-Enron and argued that this method provides reliable results compared to conventional methods. The initial sample of the search string hit a number of 137 research articles. After that, we screened the titles and abstracts of the document and excluded all studies that have not clearly addressed the IA in Arab countries. This process resulted in a final sample of 91 research articles published between 1996 and April 2022. These articles have been included in this study. As a result of the significant changes, internal audit functions (IAFs) have been granted great opportunities to support management and provide services to various organizational parties, as well as to create direct links with audit committees (ACs). These changes also presented the auditors’ view of IA’s nature and importance through the faced challenges which required the work of the IIA to find the necessary solutions. During successive periods, IIA conducted many surveys to determine the different practices of the IAFs, while investigating the nature of the skills that the internal auditors are needed (Hass et al., 2006; IIA, 2010). The IA is seen as not performing the roles as specified by IIA due to the recent corporate governance (CG) crises that resulted in the companies’ failure (Kotb et al., 2020). Therefore, some wondered why the IAFs did not predict the risk and raise an adequate warning to the companies before the crisis occurred. For example, the failure of the Carillion Company investigations has proven that the internal auditor (Deloitte) has not succeeded in financial control and risk management (Marriage, 2018), which are clearly specified in the Committee of Sponsoring Organisations’ Integrated Framework for Internal Control (known as COSO) framework (Fourie & Ackermann, 2013). The same failure happened in Mohammed Ali Mojil firm in Saudi Arabia (Zerban, 2018). As a result of the failure of some firms, there has been a fear that the IAFs do not perform their specified functions and do not address the risks faced by the institutions. Thus, what is required from the IAFs in accordance with the standards that regulate this profession may differ. Hence, this difference can be interpreted as a gap in the performance expected from the IA to add value.

This paper contributes to the body of knowledge in several ways: First, it provides a detailed investigation of IA’s status in 17 Arab countries from 1996 to April 2022 and highlights the intellectual development of the research in this area. Second, it focuses on four key aspects: the quality and effectiveness of IA, the objectivity and independence of IA, the consequences of IA, and the challenges facing IA in Arab countries. These aspects offer a better understanding of the IA facets in the Arab countries and identify countries that have made remarkable progress in auditing practices and others that still need to provide the appropriate environment to carry out auditing as required. Also, it clarifies audit institutions in the Arab countries and whether there are independent institutions that issue standards and regulations in line with the requirements of the cultural and religious environment of Arab countries. Third, this research provides an overview of the most critical challenges facing IA in these countries and concludes with a simplified review of how future research can contribute to the effectiveness of IA. Our research method offers a deeper understanding of many topics, such as how IA research has changed over time and country and how research methods have changed theoretically and practically, and thus this can improve the vision of how to search in the future to enhance IA performance. Finally, this review calls for the need to strengthen compliance with the new and current regulations that improve the functions of IA. Investors, policymakers, and regulators are required to implement policies that can enhance, and develop the practice of IAFs in light of the Arab environment, which is different from other markets culturally, religiously, and socially.

IIA Membership and CG Code in the Arab Countries

Table 1 shows the countries with a code of CG regulations and highlights the presence of the IIA in these countries. Only two states (Kuwait and Libya) do not have the code for CG despite the failure and collapse of many companies in this region, such as the collapse of Mohammed Ali Mojil company in the Kingdom of Saudi Arabia (Zerban, 2018). Concerning IIA, most countries are linked to agreements. This is evidence of the importance of membership in agencies contributing to developing supportive systems, enhancing confidence, expanding their knowledge base, and adding value to these agencies. Table 1 shows that the states that have not yet introduced the codes of CG are among the states not associated with IIA.

CG and IIA Membership of Arab Countries.

These countries belong to Gulf Cooperation Council (GCC).

Methodology

SLR is one of the most common and widespread tools in the field of business research (Denyer & Tranfield, 2006; Hedin et al., 2019; Sahi et al., 2021, 2022). It is a method by which reflections and insights related to the topic of interest are summarized, shed light on the findings of prior studies, and highlight some directions for researchers and questions that need to be answered in a future research(Massaro et al., 2016; Wagner & Heinzel, 2020). SLR ensures a large degree of transparency and can be replicated (Easterby-Smith et al., 2015). Therefore, this study followed a systematic methodology when determining the sample of literature used in the content analysis. The data were collected from the Scopus database as it has the largest indexed peer-reviewed abstracts (S. F. Khatib et al., 2021; Sahi et al., 2021; Zamil et al., 2023). Several keywords were used to identify the research literature included in the analysis (“internal audit*”

The research inclusion and exclusion methodology.

Results and Discussion

Descriptive Analysis

As shown in Figure 2, the interest in the IA field in Arab countries has only increased in the last 6 years as scholars become more aware of the importance of the topic in improving CG and its major implications on global, regional, national, economic, political, and social levels (Baatwah et al., 2021; Christ et al., 2021). This is due to the increase in business failures (such as Mohammed Ali Mojil firm, World Com, and Enron) and fraud cases in various countries. Also, the IAFs are said to be one of the most important factors in achieving sustainability (Hazaea et al., 2022; Oladejo et al., 2021; Zerban, 2018). While the number of published studies on this topic was less than five articles until 2015. This increase in the researcher’s interest can be explained by the new regulations and policies of IA introduced by governments in recent years.

Number of articles per year.

The research sample was distributed among 14 different countries. Table 2 shows that the focus of the prior studies was on the Jordan market, with 24 research articles addressing the IA in this country. Interestingly, this is against the general belief among scholars that the research focus on Arab countries was directed to the Saudi market (Alhajri, 2017). Also, it may be due to the institutions’ interest in supervising audit operations that improve IA performance in light of the reforms introduced by governments in the last decade (Al-Akra et al., 2009; Sawalqa et al., 2012). The second most investigated country is Saudi Arabia with 16 articles, followed by Tunisia (9 articles), Iraq (7 articles), Egypt (5 articles), the UAE (5 articles), and Oman (5 articles). Other countries have received less attention, with less than four studies for each, such as Libya, Kuwait, Bahrain, and Palestine. It should be noticed that very limited cross-country studies (four articles) have been found, which could provide a comparison between different market policy implementations and cultural impact on different aspects of IA. For example, Elbardan and Ali (2011) studied the IAFs and the implementation of enterprise resource planning systems in the UK and Egypt.

Regional Distribution of the Sample Literature.

Leading Research

Table 3 summarizes the 10 most cited papers according to the Scopus Citation matrix. The result suggests that the most influential study conducted by Al-Twaijry et al. (2003) to assess the issues in the development of the IA in Saudi Arabia and found that IA is not well developed because of some restrictions on their degree of independence and a lack of qualified staff. It should be noted that most of the leading studies have focused on the antecedent and determinants of the IA and its effectiveness, while the financial and non-financial outcome has been overlooked (Abu-Musa, 2008; Alzeban & Gwilliam, 2014; Al-Twaijry et al., 2004; El-Sayed Ebaid, 2011).

The Top 10 Leading Studies.

Theories

There are 45 articles that have explicitly applied theoretical ground. In the field of IA, some theories have been used more frequently. Before 2015, only agency theory and institutional theories were used in some literature. Agency theory is used in the literature in 24 articles which is 33.34% of the total articles using theories. Secondly, the institutional theory is used in eight articles which is 11.11%. Resource dependency theory is used in four articles which is 5.55%. From 2015 to April 2022, more theories have been explored in the literature. The social exchange theory and role theory are used in three articles for each theory. The social cognitive, stakeholders and stewardship theories are used twice in the sample literature (see Table 4). Also, 24 different theories were employed in the literature one time. Interestingly, there are 46 articles with no theory that has been explicitly applied. This is one of the most important constraints, as the lack of a theoretical basis in the literature makes it difficult to understand the results.

Theories Used in the Literature.

Note. Other theories include theories such as the theory of respond action, theory of planned behavior, innovation diffusion theory, contingency theory, job stress theory, expectancy theory, organizational support theory, Hofstede theory, communication theory, structuration theory, behavioral theory, framing theory, ethical theory, informational asymmetry theory, certification theory, Islamic accountability theory, a virtue ethical theory, Principal-agent theory, organizational culture theory, legitimacy theory, democratic theory, efficiency wage theory, democratic perspective, and economic theory.

Agency Theory

The agency theory was used in 24 articles in the literature. This theory is related to the conflict of interest resulting from ownership separation (Fama & Jensen, 1983; Jensen & Meckling, 1976). Through agency theory, it is possible to explain the extent of IA’s roles, investigate the IA’s nature, determine the tasks and functions of IA, and discover the nature of the work that internal auditors can provide. Thus, it can be said that the agency theory contributes clearly to achieving the goals of institutions by providing a clear explanation of the characteristics of IAs. This promotes the accountability and transparency of institutions. The IA literature used agency theory to explore areas such as external auditor reliance and IAFs (Al-Sukker et al., 2018), IAFs and internal control quality (Oussii & Boulila Taktak, 2018a), the role of sustainable CG in activating IAFs (Rehman, 2021), IA and financial performance (Hazaea, Tabash et al., 2021), and ACs effectiveness and banks’ performance (Y. A. Al-Matari et al., 2016). Other studies have combined the agency with additional theoretical perspectives to explore the complexity of IA facets by using multiple theoretical frameworks (E. M. Al-Matari & Hussein Mgammal, 2019; Alqudah et al., 2019; Elmghaamez & Ntim, 2016); however, such work is still limited.

Institutional Theory

Institutional theory is used in eight articles. The most important aspect of institutional theory is the ability to emphasize the distinction between what institutions actually achieve and what represents their structures for achieving the external environment (Fogarty, 1996). According to this theory, IAFs can be developed by investigating coercive, normative, and simulated pressures as drivers that play an important role in developing IA performance (Arena et al., 2006). In the IA literature, the institutional theory is used in different studies with various frameworks (Al-Twaijry et al., 2003; Elbardan & Ali, 2012).

Social Exchange Theory

According to Homans (1961), social exchange is a series of repetitive interactions that lead to commitments between two parties, with the actions of one party providing rewards and incentives for the other to act. Social exchange theory is used in three studies in literature, such as antecedents of burnout and its relationship to IA quality (Shbail et al., 2018). Moreover, Obeid et al. (2017) applied this theory in explaining the association between dysfunctional audit behavior and personality traits mediated by job satisfaction. It is noted that there is limited literature that discusses the social view of the internal auditors’ role in achieving the wishes of stakeholders in developing performance in a way that contributes to achieving the goals of institutions. Future research may concern this theory to discuss different aspects of IA depending on the different cultures and environments of Arab countries.

Methodology and Modeling

The findings revealed that the majority of the prior empirical studies (75 studies) were quantitative research. Whereas six studies were qualitative (Al-Twaijry 1 et al., 2002; Abuazza et al., 2015; Elbardan & Ali, 2012; Khelil, Hussainey, & Noubbigh, 2018; Khelil, Akrout et al., 2018; Khelil & Khlif, 2022; Sawan & Hamuda, 2014), one review research (Alahmadi et al., 2017), three non-empirical studies (Elbardan & Ali, 2011; Ngoc Huy, 2013), one descriptive study (Hussain & Mallin, 2002), and five mix method studies (Al-Twaijry et al., 2003; Al-Sukker et al., 2018; El-Sayed Ebaid, 2011; Khelil et al., 2016). From these articles, four studies investigate the mediating effect of various factors such as job burnout (Shbail et al., 2018), IA quality (Bshayreh et al., 2019; Mustafa & Al-Nimer, 2018), job satisfaction (Obeid et al., 2017). Limited studies (four studies) have also investigated the moderating impact of several factors like the maturity of enterprise resource planning (Shaiti & Al-Matari, 2020), IA mechanisms (E. M. Al-Matari & Hussein Mgammal, 2019), external auditor’s size (Khlif & Samaha, 2016), and task complexity (Alqudah et al., 2019). It has been found that very limited work considered the interaction of different factors in explaining the complexity of the IAFs and their influence by including moderating or mediating variables (E. M. Al-Matari & Hussein Mgammal, 2019; Alqudah et al., 2019; Baatwah et al., 2021; Shaiti & Al-Matari, 2020). Hence, future studies can take a step further in this direction and consider the interrelation between various factors in exploring the role of IA. Obeid et al. (2017) suggested that more work could investigate job stress, job burnout, and job engagement.

Furthermore, it has been found that the regression techniques used in the literature are widely varied, and multiple regression is the most widely used, and followed by parametric tests. Other studies employed logit regression (Hassan Sabbar & Eltyaf Abdalamer, 2018), generalized least squares (Alzoubi, 2019), ordinary least squares (Al-Twaijry et al., 2004; Ahmed et al., 2021; Alzeban, 2020), and structural equation modeling (Shbail et al., 2018; Mustafa & Al-Nimer, 2018; Rehman, 2021). The latter technique has been slightly applied, and due to its advantages compared to parametric and multiple regression analysis, we strongly recommend it for further research.

Further analysis revealed that the sample literature was based on evidence from the primary data, especially a questionnaire approach in collecting data, where 56 studies have used this approach (Alqudah et al., 2019; Bansal, 2019), while only 14 studies used secondary data (Alzoubi, 2019; Al-Twaijry et al., 2004), and seven researchers utilized both sources of data collection (Al-Sukker et al., 2018; Said Suwaidan & Qasim, 2010). The prior work included a sample of 385 participants (Obeid et al., 2017) and at least 15 surveys (Alzeban, 2015). Having reviewed the literature, we found that small sample size is a common limitation highlighted in prior work, pointing to the need for more research considering a larger sample size (Alhajri, 2017; Alqudah et al., 2019; Al-Twaijry 1 et al., 2002; Shbail et al., 2018).

Thematic and Content Analysis of IA Research

This research revealed that previous studies had investigated various aspects of IA in Arab countries. Some scholars have focused on the quality of IA and its function (35 studies). The consequences of IA have received less attention, such as reporting quality (Alzeban, 2019; Gebrayel et al., 2018), firm performance (Hazaea, Tabash et al., 2021; E. M. Al-Matari & Hussein Mgammal, 2019; Y. A. Al-Matari et al., 2016), earning management (Al-Thuneibat et al., 2016; Alzoubi, 2019), money laundry and fraud detection (Halbouni et al., 2016; Oqab, 2012), and risk management (Mardessi & Ben Arab, 2018). However, more research is needed to address these topics that have received less attention.

The Quality and Effectiveness of IA

Previous studies have significantly enhanced our knowledge of the IA quality determinants, and several factors enhancing it have been identified. It has been suggested that the IA quality can be enhanced by the Big 4 auditors and ACs activities (Khlif & Samaha, 2016; Oussii & Boulila Taktak, 2018b; Sartawe et al., 2017), the management support (Alzeban & Gwilliam, 2014), electronic business management (Bshayreh et al., 2019), the objectivity and professionalism (Matarneh, 2011), culture and individualism (Alzeban, 2015), the level of compliance toward ethical rules (Alsmairat et al., 2018), sustainable CG (Rehman, 2021), and access to information (Krichene & Baklouti, 2021). The IA quality and its determinants appeared to be the most explored topic with 21 research articles (see Table 5). Out of 21 articles on IA quality, five studies were based on a sample from Jordan, three from Saudi Arabia, and only one study utilized cross-country data (Ngoc Huy, 2013). It has been suggested that the great expansion in the business environment and the increased demand for more creditability from institutions and regulatory bodies contributed to the need for IA (Ramamoorti, 2003). It should be noted that effective internal auditors involve in several tasks other than monitoring activities, such as control activities, information and communication, and risk assessment’ as outlined in the COSO framework (The Committee of Sponsoring Organisations’ Integrated Framework for Internal Control). This outline was supported by several researchers (Abu Saleem & Mohammed Zraqat, 2019; Fourie & Ackermann, 2013).

Sample of Studies on the IA Quality.

Note. OLS = ordinary least square; ML = multiple regression; AOV = analysis of variance; SEM = structural equation modeling.

Interestingly, only one study used a moderating factor of external auditor’s size and found that it significantly improves the association between IA quality and ACs (Khlif & Samaha, 2016). Other studies have included mediating the impact of factors like IA performance (Bshayreh et al., 2019; Mustafa & Al-Nimer, 2018). Such work is very limited, pointing to the need for more research investigating the complex nature of IA by evaluating the interaction with various organizational aspects. Although there is a general agreement among scholars on the impact and various determinants of IA quality, there is still a need to explore other organizational aspects that have been overlooked, Chief Executive Officer (CEO) and board characteristics (Oussii & Boulila Taktak, 2018b), the impact of culture (Alzeban, 2015), financial structure, ownership structure, and many others. In future work, researchers may consider addressing the gaps that have been identified in the literature, including a small sample size (El-Sayed Ebaid, 2011; Oussii & Boulila Taktak, 2018b), using longitudinal data (Alsmairat et al., 2018) and conduct qualitative studies.

Objectivity and Independence of IA

The IAFs organizational independence and internal auditors’ objectivity are important and essential for the success and achievement of the audit objectives (IIA, 2001). The IIA (1999) defines the IA as an independent and objective advisory investigation to protect institutions’ funds and add value. According to the results of studies conducted on institutions in Arab countries, IA’s independence and objectivity are among the main factors that are positively affected by the presence of independent risk management committees, ACs size, and firms connected to the finance sector (Alhajri, 2017; Al-Twaijry et al., 2004), sound CG (Alaraji, 2020), the gender of chief audit executive (Muqattash, 2017; Oussii & Klibi, 2019), and salary (Muqattash, 2017). As presented in Table 6, the investigation revealed that very limited studies has been directed to the IAFs and the quality of small-medium enterprises (Shaiti & Al-Matari, 2020). In general, IAFs in all Arab countries are still full of opportunities for more investigations (Alhajri, 2017).

Sample of Studies on Objectivity and Independence of IA.

Note. SMEs = small and mid-size enterprises.

Table 7 shows the states that have not yet introduced the objectivity and independence regulatory requirements. It is clear from the table that only nine Arab countries out of 17 have made it clear and are obligated to ensure the independence and objectivity of internal auditors’ work. This is evidence of the lack of interest in these countries’ political systems due to the non-democratic political environment and cultural and social factors. We also believe that most countries have failed to find solutions commensurate with the nature that suits countries for ensuring the IA independence and objectivity of IA. For example, in Yemen and Syria, the laws and regulations require ensuring auditors’ independence, but these regulations do not specify how to guarantee the independence of auditing. Many studies conducted in Arab countries emphasized the difficulty of ensuring IA’s independence in Arab countries as a result of cultural, political, and social factors that require a genuine desire to implement laws. Moreover, favoritism and kinship between auditors and some executive directors are among the reasons that contributed to the failure of the independence of IA in the Arab countries (Hazaea, Tabash et al., 2021; Alktani & Ghareeb, 2014). In our sample literature, we noticed that IA’s independence has been studied from several aspects, but the objectivity has not been sufficiently investigated, which could be considered in future studies to determine the factors through which objectivity can be strengthened and resolve the challenges to enhance the IA efficiency in the Arab economies.

Independence and Objectivity Regulatory Requirements in Arab Countries.

Consequences of IA

The IA and organizational outcomes have been relatively less examined in our sample literature. As shown in Table 8, studies have investigated the impact of IA quality on earning management (Qamhan, 2020), firm performance (Alzeban, 2020; Hazaea, Tabash et al., 2021), money laundering and fraud detection (Halbouni, 2015), reporting quality (Alzabari et al., 2019:Albawwat et al., 2021), and Shariah auditing (Alahmadi et al., 2017). For the IA characteristics, five studies have assessed the determinants of IA moral courage and sign-off (Shbail et al., 2018; Khelil et al., 2016). It has been found that the function of IA and its meeting with ACs mitigates the level of earnings management (Alzoubi, 2019) and enhances firm performance (Y. A. Al-Matari et al., 2016; E. M. Al-Matari & Hussein Mgammal, 2019). Other research has documented the important role of IA characteristics in combating money laundering and fraud detection (Alqudah et al., 2019; Halbouni, 2015). These studies, however, are very limited to Jordan and the UAE markets. The lack of studies on IA outcomes has made it difficult to conduct a critical comparison between the prior findings of the sample literature which signifies the need for more research in this area. Future research may examine the IA economic consequences on the capital structure and its costs (Khlif & Samaha, 2016).

Sample Work on the Organizational and Economic Outcomes of IA.

Note. GLS = generalized least squares.

Challenges Facing IA in Arab Countries

There are many challenges that IA faces. These challenges can be divided into two parts. The first part is related to the surrounding environment. These challenges may be political, such as non-democratic systems of government, which significantly affect the independence of auditing, cultural customs, and traditional, religious, or organizational ties. This includes failure to follow international standards and governance systems. The second part is related to those in charge of auditing. As the level of accounting and financial experience that IA members possess, the extent of their knowledge and compliance with the international standards that regulate the profession might be different. In this section, we present some of the challenges that IA faces in Arab countries.

From the previous studies summarized in Table 9, it is clear that IA in Arab countries suffers from significant challenges, some of which indicate that IA in some countries is still in its primitive stages. Studies related to Yemen and Libya showed that the challenges facing IA are the lack of knowledge of IA’s importance and the lack of qualified auditors. Meanwhile, GCC countries face challenges related to family ties and family business ownership. As for Egypt and Tunisia, the inefficiency of the auditors was one of the most important reasons. In general, we believe that IA in Arab countries faces all challenges that could be related to the social, cultural, and political environment or the auditors themselves.

Papers Examining the Challenges Facing IA in Arab Countries.

Institutional Framework Required for IA in Arab Countries

The institutional framework of IA and the type of standards differ from one country to another. Some countries that are not interested in issuing their own standards adopted international standards for IA in general. In the Kingdom of Saudi Arabia, which is one of the largest economically developed Arab countries, there are three institutions responsible for following up and spreading awareness of the importance of following auditing standards and CG. These are (i) the Saudi Arabian Institute of Internal Auditors, (ii) the Saudi Arabian Monetary Authority, and (iii) the Saudi Arabian Capital Market Authority (SACMA). These regulatory bodies work to organize the mechanisms and ways through which joint-stock companies, insurance companies, and banks are managed. The regulations that are issued by these organizations explain how to carry out IAFs, the IA work plan, and how to organize the system that is responsible for the distribution of IA reports. Additionally, the regulatory body of the IIA in Saudi Arabia is trying to assure compliance with auditing standards and all rules by the public sector, and their efforts are expanding to cover the private sector as well (Alzeban, 2019). In Oman, the regulations to adopt the IAFs were introduced in 2002, and companies were required to follow the regulations stipulated in the CG codes, which clarify the functions, components, and mechanism of exercising following the IAFs. It also defines the relationship between internal auditors and the rest of the parties in the companies. On the other side, there is no special institute to issue standards for the practice of IA, whereas the Omani Capital Market Authority issues the necessary regulations and instructions through which the exercise of the IAFs can be organized following international standards (Baatwah et al., 2019).

In Tunisia, the Tunisian IIA is responsible for promoting the practices of IAFs within public sector companies and private institutions. Among the goals are (i) work on developing research related to the practice of IA, (ii) develop and publish IIA standards and demonstrate best practices, (iii) motivate and support public and private institutions to establish and develop IAFs and work on developing relations with universities and government agencies (Dellai & Omri, 2016). In Kuwait, the practice of IAFs is somewhat weak as a result of the absence of specialized institutions in issuing standards and regulations that regulate the exercise of IAFs with the exception of some laws and guidelines issued by the Ministry of Trade and Industry related to governance and the basic rules for the exercise of IAFs (Alhajri, 2017). In Jordan, the internal auditors apply the principles issued by the IIA, while the Audit Bureau is responsible for regulating the practice of IAFs in public institutions. Jordanian Association of Certified Public Accountants is responsible for regulating the practice of IA in the private sector (Al-Sukker et al., 2018). In the United Arab Emirates, five bodies are working to regulate and monitor audit activities in institutions, namely Financial Audit Authority (FAA), Financial Audit Department (FAD), Dubai Financial Services Authority (DFSA), State Audit Institution (SAI), and Abu Dhabi Accountability Authority (ADAA). Among its tasks is to issue some regulations for enhancing audits and their quality to follow up on institutions and assess their compliance with the rules and standards that regulate the audit profession (Malagila et al., 2020).

In Qatar, the Code of CG is regulated by the Qatar Financial Markets Authority, and one of the most important rules and instructions contained in the commitment to good CG guidelines and instructions for auditing practices (Shehata, 2015). In Egypt, two basic laws regulate companies, namely, the Companies Law No. 159 of 1981 and the Market Authority Law of 1992, but they do not include any article obligating companies to exercise the function of IA. On the other hand, Egypt is one of the countries that focused on the necessity of CG, including the practice of CG. IAFs by issuing instructions indicating the importance of the IAFs in helping corporate managers to work to achieve the goals, emphasizing the importance of the independence and objectivity of the IAFs, and clarifying the most important activities practiced through IAFs. Despite this, the practice of IAFs in Egypt is not mandatory. In addition, there are no professional institutions and bodies that regulate and govern this profession, and therefore there is no separate practice of IA, so IA standards issued by the IIA are followed as guidelines, but they are not official and not mandatory (El-Sayed Ebaid, 2011). In Libya, the Administrative Control Authority and the Audit Bureau are the two bodies responsible for following up on the activities of Libyan governmental institutions and the extent to which they apply the standards issued by the IIA. In addition, some regulations oblige government institutions to follow international standards, such as the Government of Libya 1996 regulations (Abuazza et al., 2015).

In Iraq, audit evidence is issued by the Accounting and Regulatory Standards Board, which was established in 1988. Through this council, the basic standards for internal and external audits are issued, the audits are planned and supervised, and the internal control system is studied and evaluated. In addition, government institutions are monitored and supervised. Despite the existence of this council so far, it has not carried out its work fully and effectively as a result of political and economic changes (Hashem, 2018). In Bahrain, there is no regulatory body that issues standards for IA, and there is also no regulatory authority associated with the practice of auditing. On the other hand, companies are required to apply international auditing standards as well as standards issued by the Accounting and Auditing Organization for Islamic Financial Institutions with regard to issues related to Islamic law and under the supervision of the Ministry of Industry and Trade (Al-Ajmi, 2009; Khasharmeh & Said, 2014).

In Yemen, no institutions issue the IA standards as most institutions follow international auditing standards issued by the IIA with supervision and control over government institutions by the Central Organization for Control and Auditing (Hazaea, Zhu et al., 2020). This also applies to Somalia, Djibouti, and Palestine where there are no institutions that issue standards for practice IA, but the implementation of international standards is supervised by government control bodies.

By clarifying the above audit institutions, it is clear that most Arab countries do not have private auditing institutes or bodies that work on issuing standards explicitly and independently of international IA standards, which may reflect negatively on the quality of the practice of IAFs in light of the different cultural and religious environments of the Arab countries that differ from the countries from which international auditing standards were issued, and therefore it can be said that the practices of IAFs in the Arab countries need to establish many institutions that work side by side with international audit institutions. Future studies may look at the roles of bodies and institutions that exist in some countries and whether they play their role in issuing or amending some international standards in line with the different cultural and religious environments of Arab countries, as well as looking at the role that these institutions can contribute to developing the IA practices in the Arab region.

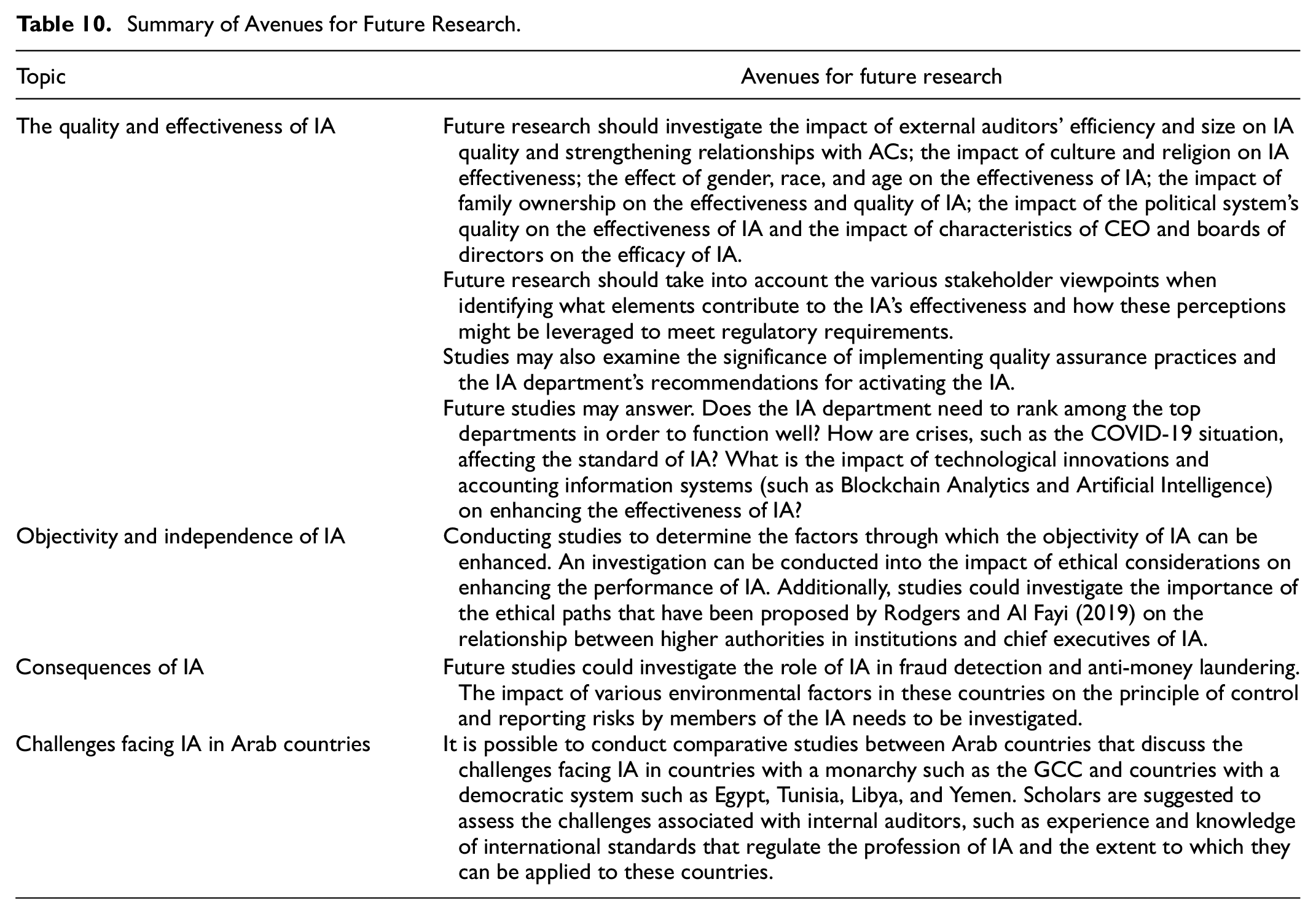

Future Research Avenues

What is the Future of IA Research in Arab Countries?

The results of this research revealed that research related to IA is scarce in emerging economies, including Arab countries (Kotb et al., 2020). Therefore, our results in certain aspects may be critically insufficient. Our knowledge about the factors of effectiveness of IA is still few on the practice side. Consequently, conducting more review research is the most appropriate way to determine how to activate IA and practice it soundly. Several studies have described the IA effect as an underexplored “black box” (Prawitt et al., 2009). In light of the lack of complete knowledge of how to practice all IA stages, academics and researchers should search for that. One of the main reasons for failing to understand the IAFs may be the reliance on positive analysis of the economic literature. In-depth research may contribute to addressing the lack of awareness about various aspects related to the profession of IA and the essential functions of this profession for the success of institutions. It limits broad and in-depth thinking in understanding how and why economic, social, and political factors may affect the appropriate exercise and implementation of IAFs. Another reason is the lack of extensive empirical research based on deep theorizing. In addition, the political systems followed in Arab countries (monarchy regimes and emerging democratic regimes) may be seen as negatively impacting the practice of the IAFs.

Directions Using the General Analysis

Our analysis of the literature showed a clear dominance of the two countries, namely Jordan and the Kingdom of Saudi Arabia. This indicates that the IA literature in the Arab countries focuses on some pivotal countries and neglects others, as some countries do not have even one study. The investigation also showed that most studies focused on discussing IA in one country only, which indicates the absence of studies that discuss IA in many countries despite the similarity of the cultural, political, and social situations of most Arab countries, especially the GCC countries. We believe that future multi-country studies can provide important and essential insights that will help interested people and researchers obtain basic cultural and behavioral differences in IA practices across countries and consider whether these differences can be explained by country characteristics (E. M. Al-Matari & Hussein Mgammal, 2019).

Additionally, the absence of studies that assess the reality of auditing in Arab countries compared to developed countries in this field. Therefore, we believe that there is a need for more research and studies to assess audit levels in the Arab countries, especially the firm economic and environmental consequences. Future studies may discuss the following questions. Is there any country that practices IA as practiced in developed countries? Is any country that practices IA according to what international auditing institutions have defined? We suggest researching new issues may help reinforce IA research and solve unresolved problems.

Furthermore, the majority of the studies did not apply theories in their investigation, pointing to the need for further research to apply theoretical lenses in exploring the IA facets in a better manner. Also, future studies can conduct a practical investigation based on the agency theory to investigate the extent to which company managers have the full powers in which they are considered agents of the owners, as well as the possibility of conducting studies into the extent of the owners’ trust or fear of managers who use their powers to achieve personal goals. The Arab environment may be suitable for conducting such studies in the light of the diversity of companies, especially in the GCC countries, where there are family companies, but managers are chosen from outside the owners, and there are also highly mixed companies in addition to public and private companies. In addition, future studies can be conducted based on the theory of the institution to clarify the foundations of IA and the role that government systems play in developing and strengthening the role of IAFs, besides the possibility of investigating that demonstrates a comparison of the role of royal government systems and democratic systems in strengthening IAFs considering government systems in Arab countries monarchy and democracy. Moreover, the search for new methods such as the use of policy research tools, standardization, and the use of framework methods of triangulation to collect and verify data may help researchers and those interested in enhancing knowledge methods of the IA profession.

Future research could discuss the extent to which the internal control system is affected by IA practices and the extent to which the quality of the internal control system of institutions is affected when complying with the professional standards of IAFs. Future studies can expand to clarify the role that internal auditor can play in monitoring activities and identifying methodologies for institutions, in addition to their role in evaluating operational risks.

Finally, the investigation revealed that much more work is needed to address aspects of IA in the countries that have been overlooked or cross-country work to compare different markets. It should be noted that most of the leading studies have focused on the antecedent and determinants of IA and its effectiveness, while the financial and non-financial outcome has been overlooked (Abu-Musa, 2008; Alzeban & Gwilliam, 2014; Al-Twaijry et al., 2004; El-Sayed Ebaid, 2011). Future investigations may consider this issue.

Directions Using the Most Articles Suggestions

We encourage researchers to continue conducting applied studies to determine new factors that may enhance IA effectiveness, either related to auditors or factors related to top management (Alqudah et al., 2019; Khelil, Akrout et al., 2018). We suggest continuing to conduct studies based on interview methods, case studies, and questionnaires as the most appropriate ways through which to know the opinions of stakeholders, auditors, and higher departments on how to organize the IA process (Alsmairat et al., 2018; Al-Thuneibat et al., 2016; Ismail & Sobhy, 2009). Finally, concerning adopting IA standards, the auditors’ knowledge about it is different due to each country’s cultural and social aspects. Future research may investigate this field (Alzeban, 2018). Table 10 summaries the avenues for future research.

Summary of Avenues for Future Research.

Concluding Remarks

This paper provides a comprehensive review of the body of knowledge on IA, including independence discussions, objectives, and challenges facing IA in Arab countries.

The results show that there has been an increase in the number of studies that discussed IA, especially in the last 3 years. The results also show that Jordan and the Kingdom of Saudi Arabia dominate the literature in terms of the number of publications. On the other hand, most of the studies were not based on theoretical grounds (46 research articles). Moreover, the majority of prior studies were quantitative research (65 research articles) with the use of the questionnaire tool for data collection. The investigation revealed that previous studies have investigated various aspects of IA in Arab countries. These studies have focused on the quality of IA and its function (35 studies), while the consequences of IA have received less attention. Our study results revealed that IA independence was negatively affected by religious and cultural factors and non-democratic systems of government. In addition, lack of awareness of the importance of IA in some countries is one of the most important challenges and obstacles facing IA. Several factors which caused a low quality of IA in Arab countries were also identified.

Most Arab countries do not have explicit policies imposed to support IA’s independence with the absence of institutions that can have a role in issuing standards that keep pace with the cultural, religious, and political environments of this region. Our study also indicated that most Arab countries comply with the procedures issued by the IIA, but this has not been followed in practice. We recommend strengthening IA independence by setting up policies and laws commensurate with these countries’ cultural, religious, and political systems. We also recommend that there should be increased openness to IA procedures. Broad reforms were recently introduced by the Arab countries, especially those with a strong economy.

There are many practical implications through the analysis of this study. This study identifies a roadmap for future research, especially for those who are interested in research in these countries, as well as organizations interested in IA, such as the IIA. We believe that considering the current environmental changes as a result of COVID_19, more practical and theoretical research can enhance and contribute to improving the performance of IA. Future studies may take the resilience of the IA system and discuss the mechanism through which audit can be practiced in a risk-based manner considering environmental changes. Future studies can also try to clarify the ingredients and characteristics that internal auditors should exercise the profession of IA effectively.

Similar to other studies, this review is not without limitations. First, the sample literature is limited to IA studies in several Arab countries, and the results may be subjective in some cases but not in all cases. Future work could consider the relevant literature in other contexts. Second, we relied on the Scopus database for data mining as it is one of the largest databases for peer-reviewed studies. Researchers in the future can include other databases such as the Web of Science. In addition, this study looked into IA literature using certain keywords. As such, future studies can utilize other keywords that were not used in this study. Future research should enrich our paper results by tracking research that will be published in the coming periods. SLR provides more credible and reliable results compared to traditional reviews. However, researchers may interpret their results in different ways. Future research may also follow the instructions of Armborst (2017) by providing quantitative matrices to determine thematic proximity and analyze the patterns of key term occurrence in the included studies, as well as calculate the coefficient. We believe that more quality research will strengthen the role of IA in organizations in light of the religious, cultural and political challenges that dominate the Arab countries. The results of this paper also help practitioners and researchers to identify the key issues related to IA in the Arab world.

Footnotes

Acknowledgements

All the authors are grateful to editor, and anonymous reviewers for their helpful comments and suggestions during the review process.

Authors Contributions

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

An Ethics Statements

Not applicable.

Note

Details of the majority of the 91 papers selected are included in this paper. The rest of the papers are available from the first and corresponding author upon request.