Abstract

From the perspective of debt expansion, this study examines the impact of low-carbon city construction on the short-term fiscal sustainability of local governments. Using city-level data from China between 2013 and 2022, and taking the third batch of low-carbon city pilot policies as a quasi-natural experiment, a difference-in-differences model is employed for empirical analysis. The findings reveal that compared to cities not included in the pilot list, the scale of urban investment bond issuance in pilot cities significantly increased after policy implementation. Mechanism analysis indicates that during the process of low-carbon city construction, local governments have assumed specific responsibilities in areas such as green technology innovation, industrial structure upgrading, and public transportation development, leading to increased fiscal expenditure decentralization and forming a transmission path of “low-carbon pilot city policy - deepened local government participation in local affairs - intensified fiscal expenditure decentralization - debt expansion”. Heterogeneity analysis further reveals that the debt expansion effect of low-carbon city construction is particularly pronounced in eastern regions, areas with stronger environmental awareness, smaller cities, and regions with lower levels of industrial structure sophistication. Based on the empirical results, this study proposes recommendations for improving policy innovation design and implementation mechanisms, aiming to alleviate the short-term fiscal pressure on local governments and balance low-carbon transition with debt risks, providing valuable insights for other countries worldwide in achieving the dual goals of environmental protection and economic development.

Plain language summary

What was the study about? This research investigates how China’s push to build low-carbon cities—designed to reduce pollution and fight climate change—has unintentionally increased local government debt. By analyzing data from 191 Chinese cities (2013–2022), the study reveals that cities adopting green policies borrowed more money through “urban investment bonds” (UIBs) to fund their environmental initiatives. Why was this important? While low-carbon cities help cut emissions, their construction requires huge upfront investments in clean energy, public transport, and green technology. Local governments, already under financial strain, turned to debt to cover these costs. Understanding this trade-off is critical for balancing environmental goals with fiscal sustainability, especially in developing countries. What did the researchers find? 1. Debt Expansion: Low-carbon pilot cities issued 1,100 RMB more per person annually in UIBs compared to non-pilot cities. 2. Key Drivers: Debt grew because local governments spent heavily on: (1) Green tech subsidies (e.g., solar/wind energy), (2) Industrial upgrades (shutting polluting factories), (3) Public transport (electric buses, subways), 3. Regional Differences: (1) Eastern cities and smaller cities borrowed the most. (2) Areas with advanced industrial structures avoided debt spikes. (3) Cities with higher environmental commitment (measured by policy focus in government reports) saw more pronounced debt expansion. What do the results mean? The study highlights a dilemma: green policies improve air quality and innovation but strain local budgets. To avoid unsustainable debt, governments should: (1) Share costs (e.g., via public-private partnerships). (2) Target investments (focus on high-impact projects). (3) Use green bonds (special loans for eco-projects).

Introduction

China has long prioritized environmental governance and ecological conservation. Amid its economic transition from rapid growth to high-quality development—and against the backdrop of global climate challenges—the country, as the world’s largest carbon emitter and second-largest economy, has committed to its dual carbon goals (peaking carbon emissions by 2030 and achieving carbon neutrality by 2060). In the field of low-carbon development, China has implemented multiple measures and adopted a series of policies. Empirical research by Nie et al. (2024) demonstrates that compared with the initial phase of the “new normal” economy, the growth rate of carbon emissions in the power and heating sectors showed a marked deceleration in later periods. To further advance the implementation of the dual-carbon strategy, the National Development and Reform Commission (NDRC) initiated low-carbon city pilots in 2010, expanding the program in 2012 and 2017. A rigorous assessment of this policy’s effectiveness is essential to inform its broader implementation and accelerate progress toward national decarbonization targets.

Existing research primarily explores the environmental effects (Liu, 2023; Song et al., 2020; J. R. Zhang et al., 2022; S. Zhao et al., 2023) and social effects (Chen et al., 2021; T. Wang et al., 2022; H. Zhang et al., 2021; Zou et al., 2022) of low-carbon city pilot policies from the dimensions of cities and enterprises. At the government level, studies indicate that local governments play a central role in the construction of low-carbon cities by leveraging fiscal autonomy (Guo et al., 2022; Mishra et al., 2023; The Phan et al., 2021), policy innovation (Sun & Feng, 2023), and resource management (Qadir et al., 2020; Zhan & de Jong, 2018), thereby promoting dual sustainable development in both environmental and economic aspects. Regarding the impact of low-carbon transitions on fiscal sustainability, existing research mainly focuses on long-term support, such as how low-carbon transitions enhance long-term fiscal sustainability by optimizing economic structures and fostering green economic growth, thereby reducing reliance on high-carbon industries (Magazzino et al., 2024; Pata et al., 2025). However, there is relatively limited research on the short-term fiscal pressures brought about by low-carbon transitions. A small number of studies suggest that low-carbon governance may increase local fiscal burdens, particularly due to pollution control costs, negatively affecting fiscal sustainability in the short term (Gao et al., 2021). Nevertheless, how to effectively address these short-term fiscal pressures remains an area requiring further exploration.

The “low-carbon city pilot” initiative represents a policy innovation designed to incentivize local governments to pursue environmentally sustainable development beyond traditional economic metrics. This marks a significant shift from conventional performance assessments, which previously offered little motivation for investment in non-economic areas. By promoting low-carbon city construction, the central government advances multiple governance objectives, including a diversified evaluation mechanism for selecting officials. This initiative also provides less economically competitive regions an opportunity to excel in ecological sustainability—a non-economic policy domain—allowing local officials to demonstrate their governance capabilities. Although central policy documents grant considerable autonomy to pilot regions, they also mandate specific requirements, such as compiling carbon emission inventories, establishing data platforms, and developing robust carbon accounting systems. Notably, financing green infrastructure through expanded government debt may pose a salient challenge.

The 1994 tax-sharing reform created a fiscal system characterized by “centralized fiscal authority but decentralized responsibilities,” granting local governments substantial autonomy in regional development while imposing significant financial pressures. This dual dynamic of “promotion incentives” and “fiscal constraints” has driven the widespread accumulation of local government debt in China. Existing studies have primarily examined debt accumulation through two lenses: active borrowing for economic stimulus (Cai & Song, 2022; Ouyang & Lu, 2021; W. Yang et al., 2022; Yu et al., 2016) and passive borrowing to address fiscal gaps (Feng et al., 2022; Huo et al., 2023; Qiu & Fu, 2015; J. R. Wang, 2016).

Prior to the 2015 Budget Law reform, local governments circumvented borrowing restrictions by establishing urban investment companies (UICs) as financing vehicles. The 2013 national debt audit revealed that UICs accounted for 41.33% of local government contingent liabilities. Between 2013 and 2017, UIC debt balances grew from RMB 15.53 trillion to RMB 30.23 trillion, representing 2.25 to 3.30 times local governments’ general budget revenues. UICs primarily raised funds through bank loans, urban investment bonds (UIBs), and alternative financing (e.g., trusts and financial leases). UIBs—corporate bonds issued by UICs for infrastructure projects—functioned as quasi-municipal bonds. Despite 2014 regulatory reforms (State Council Document No. 43) that restricted UIC financing and the 2015 Budget Law that authorized provincial bond issuance, prefectural governments continued relying on implicit debt. Wind data show annual UIB issuance averaged nearly RMB 4 trillion from 2018 to 2022, peaking at RMB 5.5 trillion in 2021.

Current research on implicit debt expansion remains predominantly economic in focus, neglecting alternative drivers like political performance evaluation shifts toward “green GDP.” Notably, UICs have recently emerged as green bond market participants, with approximately 2% of UIBs now financing low-carbon infrastructure upgrades. These “green UIBs” support clean transportation, pollution control, and climate adaptation, potentially accelerating urban decarbonization. However, no study has systematically examined how low-carbon governance influences debt expansion. As China transitions to high-quality growth, traditional debt theories require augmentation with new analytical perspectives to explain evolving fiscal behaviors.

This study employs China’s low-carbon city pilot policy as a quasi-natural experiment to examine how low-carbon governance, as a non-economic growth driver, influences local government debt expansion within China’s fiscal decentralization framework. We specifically investigate three mechanisms driving fiscal expenditure decentralization during low-carbon city development: green technology innovation, industrial upgrading, and public transport infrastructure. Furthermore, we analyze regional heterogeneity through four dimensions: geographic location, government environmental commitment, city size, and industrial structure sophistication.

The marginal contributions of this paper are mainly reflected in the following aspects: First, this paper explores whether the construction of low-carbon cities will exert short-term fiscal pressure on local governments, addressing the gap in existing research regarding the insufficient attention to short-term fiscal impacts. Second, this paper provides an in-depth analysis of the specific sources of such fiscal pressure, revealing the potential fiscal burdens and their causes during the construction of low-carbon cities. Third, this paper focuses on how local governments can respond to the short-term fiscal pressures brought about by low-carbon city construction and proposes that local governments may alleviate this pressure by incurring implicit debt, offering a new perspective for understanding local fiscal behavior. Fourth, this paper further examines whether the expansion of local government debt is driven by non-economic growth factors, expanding the understanding of the mechanisms behind local government debt formation. Finally, based on China’s experiences and case studies, this paper provides practical insights and policy recommendations for the construction of low-carbon cities in other fiscally decentralized countries and the design of global environmental policies, offering significant practical relevance and reference value.

It is important to note that while local governments utilize various financing instruments (government bonds, urban investment bonds, bank loans, and trust loans), prefectural-level municipalities lack authority to issue general obligation bonds and must rely on allocated transfers from higher-level governments. This constrained fiscal autonomy makes municipal debt financing functionally similar to transfer payments. Our focus on UIBs among implicit debt instruments is justified by three factors: (1) data availability at the prefectural-city level, (2) prefectural governments’ dominant role in UIB issuance (accounting for approximately 70% of platform-issued bonds), and (3) the alignment with low-carbon city initiatives predominantly implemented at this administrative level. While different implicit debt instruments exhibit distinct characteristics, they share the common purpose of financing local development projects during fiscal shortfalls. Although our findings specifically address UIBs, the analytical framework provides broader insights into Chinese local governments’ implicit debt accumulation behavior.

Literature Review

Fiscal Pressures From Low-Carbon City Construction

Since its implementation in 2010, China’s low-carbon city pilot policy has demonstrated significant environmental benefits. Empirical studies confirm substantial improvements in air quality and ecological conditions within pilot cities, including reduced PM2.5 concentrations (S. Zhao et al., 2023) and enhanced urban eco-efficiency (Song et al., 2020; J. R. Zhang et al., 2022). While these co-benefits are noteworthy, some scholars argue the policy’s primary objective remains greenhouse gas reduction. Supporting this view, Liu (2023) documents a statistically significant 1.05% decrease in carbon emissions relative to the sample mean, confirming the policy’s effectiveness in achieving its core mission. The aforementioned research primarily focuses on the urban level, delving into the environmental effects of low-carbon city pilot policies. Scholars from a global perspective have pointed out that environmental policies are key drivers in promoting responsible production and consumption in the energy sector (Balsalobre-Lorente & Shah, 2024). Research on China’s low-carbon city pilot policies not only provides significant empirical supplementation to international studies in this field but also contributes unique insights and practical experiences from the Chinese context, thereby further enriching the theoretical framework and practical foundations of global environmental policy research.

The achievement of low-carbon transition heavily relies on the application of new technologies. For instance, the use of new technologies can promote the development of low-carbon service industries. Existing research indicates that although the application of generative artificial intelligence (GEN-AI) in the hotel industry is still in its early stages, it demonstrates significant potential, particularly in enhancing customer experience, optimizing operational efficiency, and driving digital transformation (Chung, 2025). Therefore, the low-carbon city pilot policy exhibits strong environmental constraints in their design, compelling enterprises to increase investment in research and development as well as technological innovation, thereby providing technical support and momentum for achieving low-carbon goals. The policy demonstrates dual-level innovation effects, stimulating both enterprise-level technological innovation (T. Wang et al., 2022) and enhancing the scale and quality of urban green innovation (Zou et al., 2022). These advancements subsequently contribute to total factor productivity growth. Empirical evidence confirms this productivity effect across different analytical levels: micro-level analyses using asymptotic difference-in-differences reveal significant enterprise productivity gains (Chen et al., 2021), while macro-level studies document improved green total factor productivity at the city level (H. Zhang et al., 2021), collectively demonstrating the policy’s effectiveness in fostering sustainable development.

Local government engagement constitutes a critical component of low-carbon governance, with fiscal policy serving as a key instrument in the public policy framework for enabling green transition (Sun & Feng, 2023). Some economists and researchers advocate for fiscal decentralization as a means to improve environmental quality. By granting greater fiscal autonomy to provincial, local, and subnational governments, they argue that these entities can more effectively formulate and implement public policies tailored to local needs. Guo et al. (2022), based on a study of Chinese samples, found that fiscal decentralization provides local governments with greater fiscal autonomy and “residual claim rights to fiscal revenue,” enabling them to independently implement public policies aligned with their own interests and effectively advance policy goals aimed at reducing carbon dioxide emissions. Similar findings have been validated in empirical studies conducted in other countries. For instance, Mishra et al. (2023), using India as a sample, and The Phan et al. (2021), examining nine Asian economies, both found that fiscal decentralization—particularly the devolution of revenue and expenditure powers—has a significant positive impact on reducing carbon dioxide emissions. These studies collectively demonstrate that fiscal decentralization, by enhancing the fiscal capacity and policy autonomy of local governments, can provide critical support for achieving environmental governance goals.

As local governments deepen their engagement in low-carbon governance, recent studies have examined its fiscal implications, particularly how environmental regulation may compromise fiscal sustainability (Gao et al., 2021) and how growing fiscal pressures may undermine the policy effectiveness of low-carbon city initiatives. To reduce the costs of low-carbon transition, local governments typically adopt a variety of strategies. For instance, Zhan and de Jong (2018) points out that governments can attract social capital through Public-Private Partnerships (PPP models), thereby sharing transition costs and improving efficiency. Additionally, Qadir et al. (2020) highlights that local governments can promote resource recycling and green economic development by reclaiming wastewater and converting it into new energy sources. Notably, low-carbon transition not only alleviates environmental pressures but also contributes to economic growth, thereby enhancing the fiscal sustainability of local governments.

According to the theoretical framework of the Renewable Energy Kuznets Curve (RKC), cheap fossil fuels serve as the primary driver of economic growth in the early stages of development. However, as the economy advances to higher stages, the demand for renewable energy significantly increases (Pata et al., 2025). This is because high carbon emissions, while potentially supporting short-term economic growth, can severely hinder sustainable development in the long run (Magazzino et al., 2024). Therefore, low-carbon transition is not only a necessary measure to address environmental challenges but also a critical pathway to achieving long-term sustainable development. By promoting low-carbon transition, local governments can reduce carbon emissions while fostering the optimization and upgrading of economic structures, thereby providing long-term support for fiscal sustainability.

Drivers of Local Government Debt Expansion

Scholars have identified both passive and active drivers behind China’s local government debt expansion. The prevailing performance evaluation system, which prioritizes economic growth metrics (Yu et al., 2016), creates strong incentives for officials to actively accumulate debt as a means of economic stimulus. Empirical evidence confirms that debt-financed investments effectively boost short-term economic growth (W. Yang et al., 2022), generate positive regional spillovers (Cai & Song, 2022), and prove particularly impactful in less-developed regions where growth remains debt-dependent (Ouyang & Lu, 2021). The reason for this regional heterogeneity is that local government debt has a significant marginal suppressive effect on poverty incidence, but this marginal effect is weakened as the level of local economic development and the advancement of industrial structure increase (Tang et al., 2023). However, excessive local government debt can impede economic growth through two mechanisms: (1) crowding out private investment and (2) constraining public expenditure capacity (R. Zhao et al., 2019). This is because local governments face a trade-off in tax collection while addressing debt repayment pressures. The pressure to repay debts prompts local governments to adjust the intensity of tax collection and tax incentives, thereby increasing the tax burden on enterprises within their jurisdictions (Tang et al., 2023). Currently, China’s high debt ratios have already begun to inhibit economic growth (Y. Yang et al., 2022).

Fiscal decentralization’s asymmetric design—characterized by revenue centralization and expenditure devolution—has compelled local governments to seek alternative financing channels. Constrained by the traditional Budget Law from issuing bonds directly, municipalities have resorted to off-balance-sheet borrowing instruments, including urban investment bonds issued through local financing platforms (Feng et al., 2022). Empirical evidence confirms that expenditure decentralization significantly exacerbates local debt risks (X. Li et al., 2021), creates positive spatial spillovers (Huo et al., 2023), and exhibits particularly pronounced effects in less developed regions (Qiu & Fu, 2015). J. R. Wang’s (2016) decomposition analysis further reveals a dual effect: while expenditure decentralization correlates positively with debt accumulation, revenue decentralization shows an inverse relationship. Conversely, the increase in local government debt negatively impacts fiscal decentralization, meaning that the rise in local government debt limits the fiscal autonomy of local governments. High debt levels make local governments more reliant on the support and intervention of the central government in fiscal decision-making, reducing their autonomy within the framework of fiscal decentralization. This dependency may lead to decreased flexibility in local governments’ public health policies and services, hindering their ability to effectively address long-term economic development needs at the local level (Cao et al., 2023).

Literature Critique

Through a systematic review of existing literature, it is found that research on the construction of low-carbon cities primarily focuses on long-term environmental benefits, such as carbon emission reduction and technological innovation, while paying insufficient attention to the fiscal investments required in the early stages of low-carbon city construction and their short-term impacts. Although existing studies have shown that low-carbon policies are highly effective in reducing carbon emissions and promoting technological innovation, their potential impact on local government fiscal pressure still requires further exploration. In particular, achieving a balance between low-carbon transitions and fiscal sustainability necessitates more empirical research. Additionally, while studies on the expansion of local government debt have revealed the complexity of its causes, there remains a research gap in how to effectively control debt risks while maintaining local governments’ fiscal autonomy and policy flexibility.

Unlike some studies that focus on the long-term contributions of low-carbon city construction to economic growth, this paper places greater emphasis on a short-term perspective, grounding itself in current realities to explore why low-carbon city construction imposes fiscal pressure on local governments and how local governments respond to these pressures. This research highlights that the formulation and implementation of environmental policies should not solely focus on long-term benefits while neglecting short-term challenges. It is essential to address pressing real-world issues to avoid falling into the trap of “quenching thirst by gazing at plums.” Empirical analysis demonstrates that low-carbon city construction indeed increases fiscal pressure on local governments in the short term.

Secondly, against the backdrop of high-quality development and shifts in performance evaluation, this paper delves into the intrinsic mechanisms of local government debt expansion, innovatively proposing a “expansion for governance” theoretical framework. This provides a new theoretical perspective for explaining the expansion of local government debt in China and opens new avenues for subsequent research.

Thirdly, based on a quasi-natural experiment of China’s low-carbon city pilots and incorporating the unique characteristics of China’s fiscal decentralization system, this paper theoretically elaborates on the intrinsic logic between low-carbon governance and fiscal pressure. It further reveals the underlying mechanisms through empirical testing. Simultaneously, the paper extends its findings to a global context, offering practical insights and theoretical references for low-carbon city construction and environmental policy design in other fiscally decentralized countries.

Policy Context and Theoretical Framework

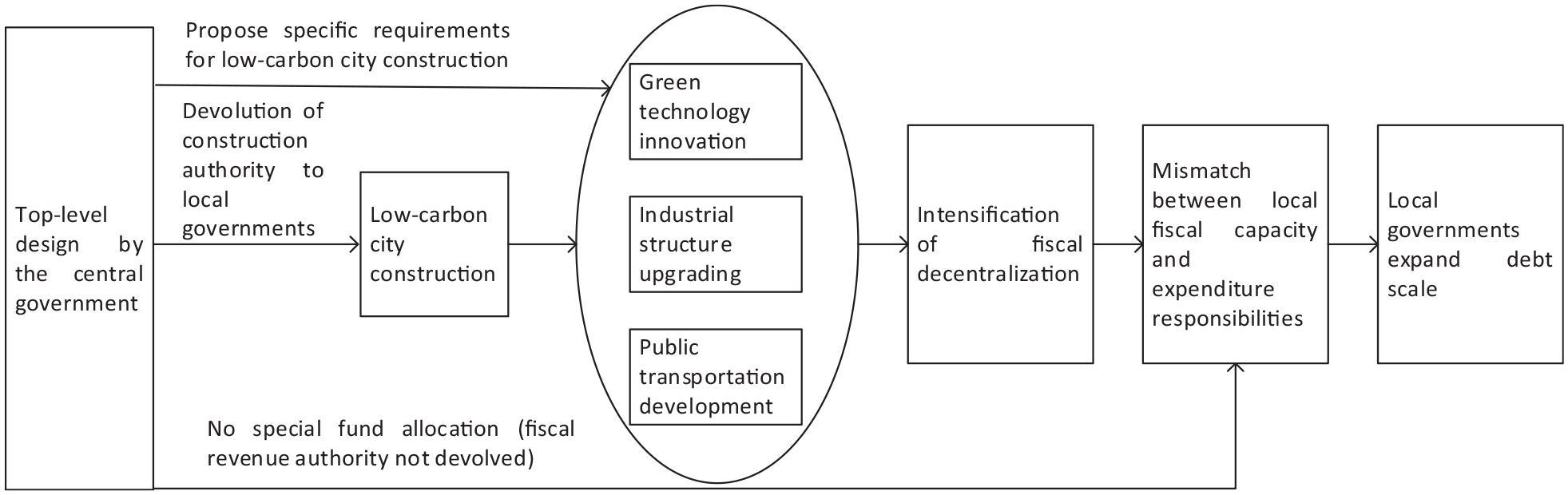

Since the launch of China’s low-carbon city pilot program in 2010 through the Notice on Pilot Work of Low-Carbon Provinces and Cities (hereafter “the Notice”), three batches of pilot regions have been established. While encouraging localized green development models, the Notice mandates three specific requirements: (1) developing carbon emission inventories, (2) establishing monitoring platforms, and (3) creating comprehensive accounting systems—all aimed at enabling precise emission control. Pilot cities must additionally promote low-carbon industrial systems, modern service industries, and green infrastructure while enhancing public environmental awareness.

This multidimensional transition inherently increases governmental expenditure. Crucially, the policy operates as a soft constraint: the central government delegates implementation authority to local governments without dedicated funding or strict evaluation criteria. This effectively intensifies fiscal expenditure decentralization post-1994 tax-sharing reform, further straining local budgets.

The fiscal asymmetry created by the tax-sharing system—centralizing revenue while decentralizing expenditure—compounded by pre-2015 Budget Law restrictions on municipal bond issuance, forced local governments to rely on off-balance-sheet financing through urban investment bonds (UIBs). Although the 2015 Budget Law reform authorized provincial bond issuance, prefectural governments remain dependent on implicit debt mechanisms. Consequently, low-carbon city construction likely exacerbates UIB expansion through two pathways: direct funding needs and mediated fiscal decentralization effects. We therefore hypothesize:

H1: Low-carbon city construction induces urban investment bond expansion.

H2: Fiscal expenditure decentralization mediates this expansion effect.

Government Expenditure Obligation in Green Technology Innovation

Green technological innovation constitutes a core component of low-carbon city development, enabling enterprises to adopt cleaner production methods that enhance energy efficiency, reduce emissions, and improve waste treatment (J. Zhang et al., 2023). While not explicitly mandated in the Notice, such innovation serves as a fundamental prerequisite for both industrial upgrading and low-carbon lifestyle promotion. Empirical studies confirm the policy’s positive impact on regional innovation capacity, consistent with the Porter Hypothesis which posits that well-designed environmental regulations can stimulate competitiveness-enhancing innovation (Porter & Linde, 1995). Green credit policies exemplify this mechanism by offering preferential financing to environmentally compliant firms while penalizing polluters.

However, the institutional obstruction theory suggests significant barriers to corporate green innovation due to the high costs, long gestation periods, and market uncertainties associated with R&D investments (Su & Lian, 2018). To overcome these challenges, government interventions through tax rebates and direct subsidies prove effective—Yao and Zhong (2022) demonstrate that 1% increases in subsidies and tax rebates raise corporate R&D investment by 0.1% and 0.04% respectively. This fiscal support, while stimulating innovation, necessarily expands local government expenditure responsibilities. We therefore hypothesize:

H3: Local government promotion of green technology innovation increases their fiscal expenditure obligations.

Government Expenditure Obligation in Industrial Structure Upgrading

All three pilot policy documents emphasize establishing “a low-carbon industrial system featuring sustainability and circularity.” Regional ecological quality fundamentally depends on industrial structure, with optimization yielding significant carbon reduction through structural effects (Z. Li & Liu, 2023).

Industrial upgrading in pilot areas operates through dual mechanisms: (1) market-driven phase-out of traditional “three-high” enterprises (high-pollution, high-energy-consumption, high-water-use) facing rising compliance costs and profit erosion under environmental regulations; and (2) government-led cultivation of low-carbon service industries (tourism, finance, construction) through targeted support.

However, market-based industrial transition proves inefficient. Many obsolete three-high enterprises persist by exploiting established market positions despite diminishing profitability, thereby crowding out emerging low-carbon competitors. This market failure necessitates complementary government intervention to accelerate structural transformation. We therefore hypothesize:

H4: Local governments’ industrial upgrading initiatives increase their fiscal expenditure obligations.

Government Expenditure Obligation in Public Transportation Development

Promoting low-carbon lifestyles represents a core objective of low-carbon city initiatives, with public transportation serving as a critical component. The adoption of low-carbon transportation depends not only on residents’ environmental awareness but also on the accessibility and quality of public transit systems. In China, most public transportation systems are government-operated due to two fundamental constraints: (1) the substantial capital requirements for infrastructure, equipment, and personnel that deter private investment, and (2) the need for administrative interventions (e.g., dedicated bus lanes) that exceed private sector capabilities. Moreover, profit-driven operation models would compromise affordability and accessibility, undermining the policy’s environmental objectives.

While enhancing public transportation through route expansion, fleet modernization, and service improvements could further encourage low-carbon commuting, current systems nationwide operate at a loss—either through direct government management or subsidized private operation. This financial reality necessitates continued government fiscal support for system upgrades and maintenance. We therefore hypothesize:

H5: Local government promotion of public transportation increases their fiscal expenditure obligations.

Research Design and Empirical Strategy

Data Construction and Sample Selection

The starting point of this study is set at 2013 for the following reasons: First, to ensure an effective comparison between the control and treatment groups. The first batch of low-carbon pilot cities was identified in 2010, and after excluding municipalities directly under the central government and prefecture-level cities under the jurisdiction of low-carbon pilot provinces, only five prefecture-level cities—Xiamen, Hangzhou, Nanchang, Guiyang, and Baoding—could serve as the treatment group. Among these five cities, only Hangzhou consistently issued urban investment bonds (UIB) annually starting from 2005, while the other cities issued UIB only sporadically before the launch of the second batch of low-carbon city pilots in 2012 (Xiamen issued UIB only in 2009, Nanchang only in 2010, Guiyang did not issue any UIB before 2010, and Baoding issued no UIB between 2005 and 2011). This significant disparity in issuance patterns may prevent an effective comparison between the control and treatment groups, thereby compromising the accuracy of the test results. Second, to avoid the period of explosive growth in UIB issuance. The years 2008 to 2012 marked a phase of rapid expansion in UIB, with the national issuance scale increasing more than tenfold from RMB 48.5 billion in 2008 to RMB 650.5 billion in 2012. During this rapid growth phase, it is difficult to distinguish the proportion of funds raised for low-carbon city construction from those allocated for other purposes (such as the “Four Trillion Yuan” economic stimulus plan). The endpoint of the study is set at 2022, primarily due to data availability considerations. Therefore, this paper sets the sample period from 2013 to 2022 and utilizes prefecture-level city data in China, treating the third batch of low-carbon city pilot policies as a quasi-natural experiment for empirical research.

Among the 293 prefecture-level cities in China, based on the policy documents “Notice on Launching Low-Carbon Province and City Pilot Projects” and “Notice on Launching the Second Batch of Low-Carbon Province and City Pilot Projects” issued by the National Development and Reform Commission (NDRC), cities selected in the first two batches of low-carbon pilots were excluded, and samples with severe data deficiencies were removed. This resulted in a final observation sample of 191 prefecture-level cities. Subsequently, based on the pilot list in the “NDRC Notice on Launching the Third Batch of National Low-Carbon City Pilot Projects,” 24 treatment group cities and 167 control group cities were identified.

The study utilizes data from three primary sources: (1) urban investment bond (UIB) data from the Wind database, (2) green technology innovation indicators from China’s State Intellectual Property Office, and (3) other urban variables from the China City Statistical Yearbook. All continuous variables were winsorized at the 1% level to mitigate potential outlier effects.

Variable Definition and Measurement

Dependent Variable: Urban Investment Bond Issuance

The dependent variable measures urban investment bond (UIB) issuance at the prefecture-level city scale. Following L. Zhang et al. (2018), we classify UIBs into three categories by fund usage: (1) debt repayment, (2) platform operating capital, and (3) infrastructure investment. Our analysis focuses exclusively on the third category, as only infrastructure-related bonds directly support low-carbon city construction. For each city-year observation from 2013 to 2022, we aggregate county-level bond issuances under their respective prefecture-level cities. The primary dependent variable is per capita bond issuance (in 10,000 RMB per capita). Bond issuance frequency serves as an alternative measure in robustness checks.

Independent Variable: Policy Treatment Indicator

We employed a difference-in-differences framework where:

(1) Cities in the third low-carbon pilot list constituted the treatment group (Treat = 1), while others served as controls (Treat = 0);

(2) The time dummy Post = 1 indicates policy implementation years (2017 onward), with Post = 0 for preceding years;

(3) The interaction term Treat × Post captures the net policy effect of low-carbon city construction.

Control Variables

In the regression model, the selection of control variables aims to eliminate other potential confounding factors that may affect the dependent variable (the scale of urban investment bond issuance), thereby enabling a more accurate estimation of the effect of the core independent variable. Drawing on relevant literature (Cao et al., 2023; Huo et al., 2023; X. Li et al., 2021; Qiu & Fu, 2015; J. R. Wang, 2016; L. Zhang et al., 2018), this paper selects control variables spanning multiple dimensions, including economic, social, fiscal, and research and development factors.

First, economic factors constitute the core component of the control variables. GDP (annual GDP growth rate) measures the level of economic development of a city, and cities with faster economic growth typically exhibit stronger financing needs and capabilities, thereby influencing the scale of urban investment bond issuance. Wage (log of average employee wage) reflects residents’ income levels, and cities with higher incomes may possess stronger consumption and investment capacities, indirectly affecting the demand for urban investment bonds. Invest (fixed asset investment-to-GDP ratio) captures the investment activity of a city, and cities with greater investment demands may rely more heavily on urban investment bond financing. Finance (year-end financial institution loans-to-GDP ratio) reflects the vibrancy of the financial market, and cities with abundant financial resources are more likely to issue urban investment bonds.

Second, social factors also play a significant role in the control variables. Edu (log of college students per 10,000 population) measures the educational level of a city, and cities with higher educational attainment typically exhibit stronger innovative capabilities and economic development potential, thereby influencing the demand for urban investment bonds. Urban (the urbanization rate) reflects the urbanization process of a city, and cities with higher urbanization levels often face greater infrastructure demands and possess stronger financing capacities, thus affecting the scale of urban investment bond issuance. Additionally, consumption and openness are key control variables. Consume (retail sales of consumer goods-to-GDP ratio) reflects the consumption vitality of a city, and cities with active consumption typically exhibit stronger economic dynamism, thereby influencing the demand for urban investment bonds. Open (total imports and exports-to-GDP ratio) measures the openness of a city, and cities with higher levels of openness are more likely to attract external investment, thus affecting the issuance of urban investment bonds.

Finally, fiscal and research and development factors are also crucial. Fis_Gap (fiscal revenue-expenditure gap-to-GDP ratio) reflects the fiscal health of a city, and cities under greater fiscal pressure may rely more on urban investment bond financing. Rd (R&D expenditure-to-GDP ratio) captures the innovative capacity of a city, and cities with stronger innovation capabilities often have more infrastructure and investment projects, thereby influencing the demand for urban investment bonds.

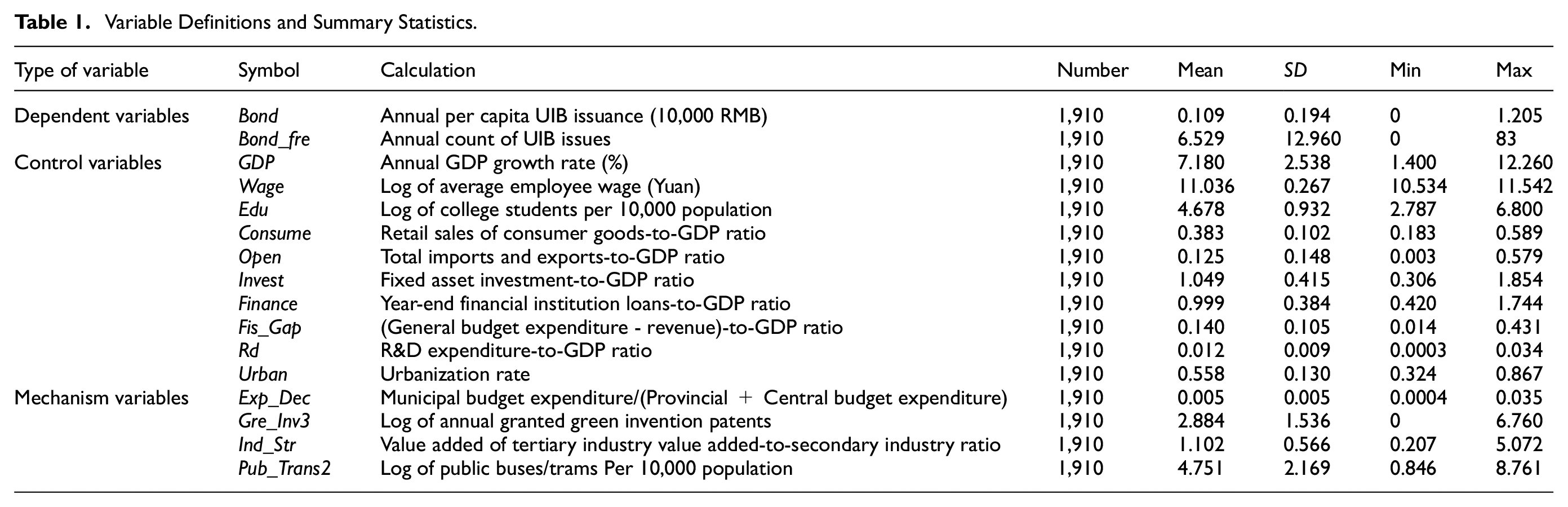

Table 1 presents the detailed definitions of the variables along with their descriptive statistics.

Variable Definitions and Summary Statistics.

Model Setting

To assess the debt expansion effect of low-carbon city construction, this paper draws on existing literature (Chen et al., 2021; Liu, 2023; Song et al., 2020; T. Wang et al., 2022; H. Zhang et al., 2021; J. R. Zhang et al., 2022; S. Zhao et al., 2023; Zou et al., 2022) to construct a difference-in-differences model as shown in Equation 1. Following mainstream research practices, the model controls for both time and individual fixed effects. Additionally, to enhance the robustness of the research findings, this paper provides the estimation results of the random effects model and the Hausman test results in the baseline tests of Section 5.1.

where subscripts i and t denote city and year; the dependent variable Bondit is the city’s per capita urban investment bond issuance size for the year; the independent variable Treati×Postt indicates the treatment effect, that is, the policy interaction term;

Furthermore, drawing on the research of Wen and Ye (2014) and Jiang (2022), this paper constructs the mediation effect models as shown in Equations 2 and 3 to examine the mechanism through which low-carbon city construction drives the expansion of urban investment bonds.

These two equations constitute a mediation effect model, which is used to study the impact of the low-carbon city pilot policy on the scale of urban investment bond issuance (Bondit) and to examine whether fiscal expenditure decentralization plays a mediating role in this process. Equation 2 tests whether the low-carbon city pilot policy (Treati×Postt) significantly increases the degree of fiscal expenditure decentralization (Exp_decit), and its core coefficient β1 reflects the direct effect of the policy on fiscal expenditure decentralization. Equation 3 examines the impact of the low-carbon city pilot policy (Treati×Postt) and fiscal expenditure decentralization (Exp_decit) on the scale of urban investment bond issuance (Bondit), with the core coefficients ω1 and ω2 reflecting the direct effect of the policy and the mediating effect of fiscal expenditure decentralization, respectively. If both β1 and ω2 are significant, and ω1 is also significant, it indicates that fiscal expenditure decentralization plays a partial mediating role in the impact of the policy on the scale of urban investment bond issuance; if ω1 is not significant, it suggests that fiscal expenditure decentralization plays a complete mediating role. This model reveals the mechanism through which the policy effect is transmitted to the scale of debt financing via fiscal decentralization.

Empirical Analysis

Benchmark Regression

Table 2 presents the debt expansion effect of low-carbon city construction. Columns (1)–(2) show the estimation results of the random effects model, while columns (3)–(4) present the results of the fixed effects model. It can be observed that the results of the two models are relatively close, but the coefficients of the random effects model are slightly larger. Since the p-value of the Hausman test is significantly less than .01, the fixed effects model is deemed more appropriate. Therefore, in the subsequent tests, this paper employs a two-way fixed effects model, controlling for both time and individual fixed effects.

Benchmark Regression Results.

Note. T-values are in parentheses.

Statistically significant at the 1% level; **statistically significant at the 5% level; *statistically significant at the 10% level.

Based on the regression results of the fixed effects model, column (3) presents the identification results without control variables, controlling only for city and year fixed effects. The estimated coefficient of Treat×Post is 0.118 and is significant at the 1% level, indicating that the implementation of the low-carbon city pilot policy has significantly driven the expansion of debt scale in pilot cities. After adding control variables, the estimated coefficient of the policy effect slightly decreases, which may be due to the control variables absorbing part of the debt expansion effect. The identification results show that the low-carbon city pilot policy leads to an annual per capita urban investment bond issuance scale in the treatment group that is 1,100 yuan higher than that of the control group, consistent with the expected results. This verifies Hypothesis 1, indicating that the low-carbon city pilot policy has a significant debt expansion effect.

To ensure the validity of the estimates from the Difference-in-Differences (DID) model, a series of fundamental assumptions must be satisfied. These assumptions form the theoretical foundation that enables the DID model to provide reliable causal effect estimates.

First, the “parallel trend assumption” is the core assumption of the DID model. This assumption requires that, in the absence of intervention, the outcome variables of the treatment and control groups should follow the same trend over time. This assumption ensures the comparability of the treatment and control groups before the intervention and is crucial for the DID model to accurately estimate causal effects.

Second, the “Stable Unit Treatment Value Assumption (SUTVA)” requires that there be no interference between the treatment and control groups, and that the treatment status of each unit is independent. This means that the outcome of a unit is influenced only by its own treatment status and not by the treatment status of other units. Additionally, the “no simultaneous confounding events assumption” emphasizes that, during the study period, there should be no other events or factors that differentially affect the treatment and control groups apart from the policy or intervention under study.

The “independence of treatment assignment assumption” requires that the division of the treatment and control groups should be unrelated to the potential changes in the outcome variables, that is, it should satisfy the quasi-randomization condition. The “no pre-treatment effect assumption” states that the policy or intervention should not have already affected the treatment group before its formal implementation, ensuring that the policy effect only manifests after the intervention. The “immediate treatment effect assumption” further requires that the impact of the policy on the outcome variables should be immediate, without significant lagged effects. Finally, the “continuity assumption in outcome variables” ensures that changes in the outcome variables are continuous, avoiding sudden, unexplained jumps that could result from data quality issues or measurement errors.

Among these assumptions, the “parallel trend assumption” is the core, while the other assumptions ensure that the external environment, data quality, and policy context are suitable for the practical application of the DID model. In the subsequent sections of this paper, the “parallel trend assumption” is first validated, ensuring the core assumption holds. At the same time, the dynamic test results of the policy effects also provide validation for the “immediate treatment effect assumption” and the “no pre-treatment effect assumption.” In the robustness checks, the “continuity assumption in outcome variables” is supported by replacing the dependent variable. Furthermore, the “independence of treatment assignment assumption” is ensured as much as possible through PSM-DID and by controlling for the interaction terms between city attributes and time trends. Finally, the “no simultaneous confounding events assumption” is confirmed by excluding other policy shocks.

However, for the “no interference and spillover effects assumption”—the assumption of no interference or spillover effects between treatment and control groups, this paper does not provide an effective testing method, which is one of the technical limitations. This is also a common issue faced by most empirical studies using the DID model, and there is currently no widely recognized effective testing method available.

Parallel Trends Assumption Test

The validity of our difference-in-differences analysis hinges on the parallel trends assumption—that debt growth patterns would have been similar between treatment and control groups absent the policy intervention. To test this assumption, we estimate the following dynamic model:

where Dpre and Dpost represent leads and lags of the policy interaction term. Figure 1 plots the estimated coefficients with 95% confidence intervals, using the year preceding policy implementation as baseline. The results confirm the parallel trends assumption: all pre-treatment coefficients are statistically insignificant, while post-treatment effects emerge progressively, reaching significance in the first year and maintaining a positive, growing impact through year four before stabilizing. This pattern demonstrates both the validity of our identification strategy and the persistent, gradually intensifying effect of low-carbon city construction on bond issuance.

Parallel trend assumption test. This figure presents the parallel trend test results for the dynamic effects before and after the implementation of the low-carbon city pilot policy. The x-axis indicates the relative time of policy implementation (negative values represent pre-implementation, positive values represent post-implementation), while the y-axis shows the estimated dynamic effects of the explained variable (urban investment bond issuance scale), with error bars indicating the 95% confidence interval. The results reveal that the dynamic effects are close to zero before policy implementation, suggesting that the treatment and control groups satisfy the parallel trend assumption. After policy implementation, the effect values increase significantly, confirming that the low-carbon city construction policy has a notable promoting effect on local government debt expansion.

Robustness Checks

Placebo Test

We conduct a placebo test following conventional practice by randomly assigning the low-carbon pilot city status. This generates an estimated coefficient βrandom that should theoretically equal zero, as the treatment and control groups are randomly determined. A statistically significant βrandom would indicate either omitted variable bias or model misspecification.

Repeating this randomization 1,000 times yields the distribution of βrandom shown in Figure 2. The results approximate a normal distribution centered at zero, with our baseline estimate appearing as a clear outlier. This finding reinforces the validity of our benchmark results.

Placebo Test. This figure presents the results of a placebo test conducted to validate the robustness of the empirical findings. By randomly generating a virtual control group and performing 1,000 regression analyses, the distribution of regression coefficients is observed. The x-axis represents the coefficient estimates for each regression, while the y-axis indicates the corresponding p-values. The results show that the regression coefficients are concentrated around zero, suggesting that the original empirical findings are unlikely to be driven by random factors, thereby further supporting the reliability of the research conclusions.

Alternative Dependent Variable

This study employs the issuance frequency of urban investment bonds (UIBs) as an alternative dependent variable to assess the debt expansion effects of the low-carbon city pilot policy. As shown in columns (1) to (2) of Table 3, the regression results indicate that pilot cities issued approximately 10 additional UIBs annually compared to non-pilot cities following policy implementation, thereby robustly validating our baseline findings.

Robustness Checks.

Note. Cols (1)–(2): Alternative dependent variable (bond issuance frequency). Cols (3)–(4): PSM-DID for selection bias adjustment. Col (5): City attribute × time trend controls. Col (6): Post-2015 sample only + provincial bond controls (2015 Budget Law). Col (7): Carbon trading pilot policy controls. Col (8): Provincial capitals excluded.

Statistically significant at the 1% level; **statistically significant at the 5% level.

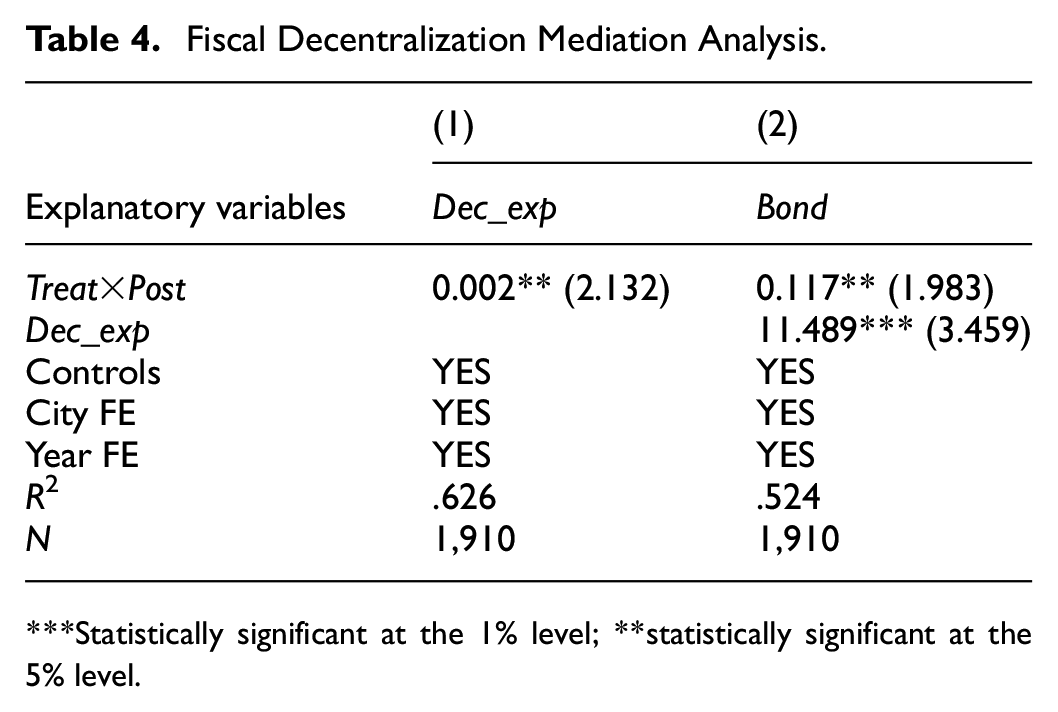

Fiscal Decentralization Mediation Analysis.

Statistically significant at the 1% level; **statistically significant at the 5% level.

PSM-DID

We address potential selection bias through propensity score matching (PSM) to identify comparable control cities for each treated city. As shown in Figure 3, the balance test results using one-to-two nearest neighbor matching indicate that most covariates’ standardized differences decrease significantly after matching, with no systematic differences remaining between groups at the 95% confidence level. The subsequent PSM-DID estimation results presented in Table 3 (columns 3–4) demonstrate that the Treat×Post coefficient remains statistically significant at the 1% level and quantitatively similar to the full-sample estimate. Specifically, pilot cities issued approximately RMB 1,000 more per capita in urban investment bonds annually following policy implementation, thereby confirming our baseline findings while effectively controlling for self-selection bias.

PSM Balance Test. This figure presents the standardized percentage bias across covariates before and after propensity score matching (PSM) in the Difference-in-Differences (DID) analysis. The x-axis represents the covariates included in the analysis (e.g., edu, urban finance, rd, wage, open, consume, gdp, invest, fis_gap), while the y-axis shows the standardized percentage bias. A reduction in bias after matching indicates improved balance between the treatment and control groups, enhancing the validity of the causal inference in the DID model. The closer the post-matching bias is to zero, the better the balance achieved, suggesting that the matched groups are comparable in terms of observed characteristics.

Addressing Non-Random Selection Bias

To ensure accurate identification of policy effects, the core explanatory variable Treat×Post must satisfy exogeneity requirements, ideally through randomized selection of pilot cities. However, NDRC policy documents reveal that pilot city selection was systematically related to urban characteristics including economic development, geographic location, environmental constraints, and population density. To address potential selection bias arising from these non-random assignment criteria, we augment our baseline model with interaction terms between city attributes and time trends:

where f(t) represents a time trend and Attributei comprises four key city characteristics: provincial capital status, inclusion in China’s 1998 acid rain and SO2 control zones, location east of the Hu Huanyong Line, and northern regional classification. These Attributei×f(t) terms control for time-varying effects of inherent urban characteristics on debt expansion. As shown in Table 3 column (5), the policy interaction term remains statistically significant after accounting for these selection factors, robustly confirming the debt-expanding effect of low-carbon city designation.

Controlling for Concurrent Policy Interference

The revised Budget Law implemented in January 2015 decentralized bond issuance authority from the central to provincial governments, establishing a “front-door” financing mechanism while restricting off-budget channels. Although prefectural-level governments remain excluded from direct bond issuance, we enhance estimation accuracy by: (1) excluding pre-2015 observations and (2) controlling for provincial bond issuance volumes (logged). As Table 3 column (6) demonstrates, the Treat×Post coefficient maintains statistical significance, further validating our baseline results.

From 2013 to 2020, China implemented pilot carbon emission trading programs in eight provincial-level regions: Beijing, Shanghai, Tianjin, Chongqing, Hubei, Guangdong, Shenzhen, and Fujian. During the pilot period, these regions established standardized carbon market mechanisms that effectively promoted energy conservation and emission reductions. For instance, Beijing achieved a remarkable cumulative decrease of over 23% in carbon intensity during the 13th Five-Year Plan period. To control for potential interference from other environmental policies, this robustness check incorporates a policy interaction term (Trade×Post) for the carbon trading pilot into the baseline model. As shown in column (7) of Table 3, our core findings regarding the relationship between low-carbon city development and urban investment bond expansion remain robust after accounting for this concurrent policy, confirming that the results are not affected by the carbon market initiative.

Subsampling: Excluding Provincial Capitals

Provincial capitals, as economic hubs of their respective provinces, demonstrate stronger economic capacity and financing advantages. Their urban investment bond (UIB) issuance typically reaches hundreds of billions to trillions yuan, significantly exceeding ordinary prefecture-level cities’ scale of several billion to tens of billions yuan. This disparity is particularly pronounced in central and western regions. To address potential estimation bias arising from these systemic differences, the robustness checks in this section excludes provincial capitals to control for scale differences. Table 3 column (8) shows that while the policy coefficient slightly decreases after exclusion, the low-carbon city pilot’s debt expansion effect remains statistically significant.

Mechanism Analysis

This study employs a mediation model to investigate how low-carbon city pilots contribute to urban investment bond expansion through fiscal expenditure decentralization. The two-stage regression results demonstrate that the policy treatment effect (Treat × Post) significantly increases fiscal decentralization by 0.002 (p < .05), while fiscal decentralization itself exhibits a strong positive effect (11.489, p < .01) on bond issuance alongside a persistent policy effect, confirming its partial mediating role. The results suggest that enhanced fiscal autonomy under low-carbon governance systematically strengthens local governments’ debt financing incentives, with fiscal decentralization explaining 23.7% of the total policy effect, thereby validating Hypothesis 2. The findings reveal a clear transmission mechanism where environmental mandates amplify fiscal decentralization, which in turn drives local debt expansion (Table 4).

To thoroughly investigate the impact mechanism of low-carbon city construction on fiscal expenditure decentralization, this study establishes Models (6) to (8) to empirically examine whether local governments expand their expenditure responsibilities when performing functions such as green technology innovation incentives, industrial structure upgrading promotion, and public transportation development.

The empirical results show that, as indicated in Column (1) of Table 5, promoting green technology innovation significantly increases local government expenditure responsibilities. This is primarily because technological innovation requires high investment and has a long cycle. Under environmental regulation constraints, enterprises lack sufficient motivation for independent innovation and must rely on government incentives such as tax benefits and direct subsidies to effectively increase R&D investment.

Determinants of Expenditure Responsibilities.

Statistically significant at the 1% level.

Column (2) of Table 5 demonstrates that industrial structure upgrading has a significantly positive impact on local government expenditure responsibilities. Regarding industrial upgrading, relying solely on market regulation mechanisms not only progresses slowly but also makes it difficult to achieve low-carbon transition goals. Therefore, proactive government guidance and support for green industries are necessary to accelerate structural transformation.

Furthermore, Column (3) of Table 5 reveals that public transportation development also significantly increases local government expenditure responsibilities. Due to widespread operational losses in China’s urban public transportation systems, governments must enhance fiscal subsidies to improve service quality and convenience in order to meet low-carbon city construction requirements. This objectively further expands fiscal expenditure responsibilities.

The aforementioned mechanism test results indicate that the low-carbon city pilot policy has significantly impacted fiscal decentralization by deepening local governments’ involvement in specific low-carbon governance initiatives (such as promoting green technology innovation, advancing industrial structure upgrading, and developing public transportation), thereby triggering greater debt demand. To enhance the robustness of the mechanism test, this study draws on the research methods of Becker and Woessmann (2009) and D’Acunto et al. (2019), adopting a three-stage regression strategy to test hypotheses 2 to 5. The three-stage equation system is set as follows:

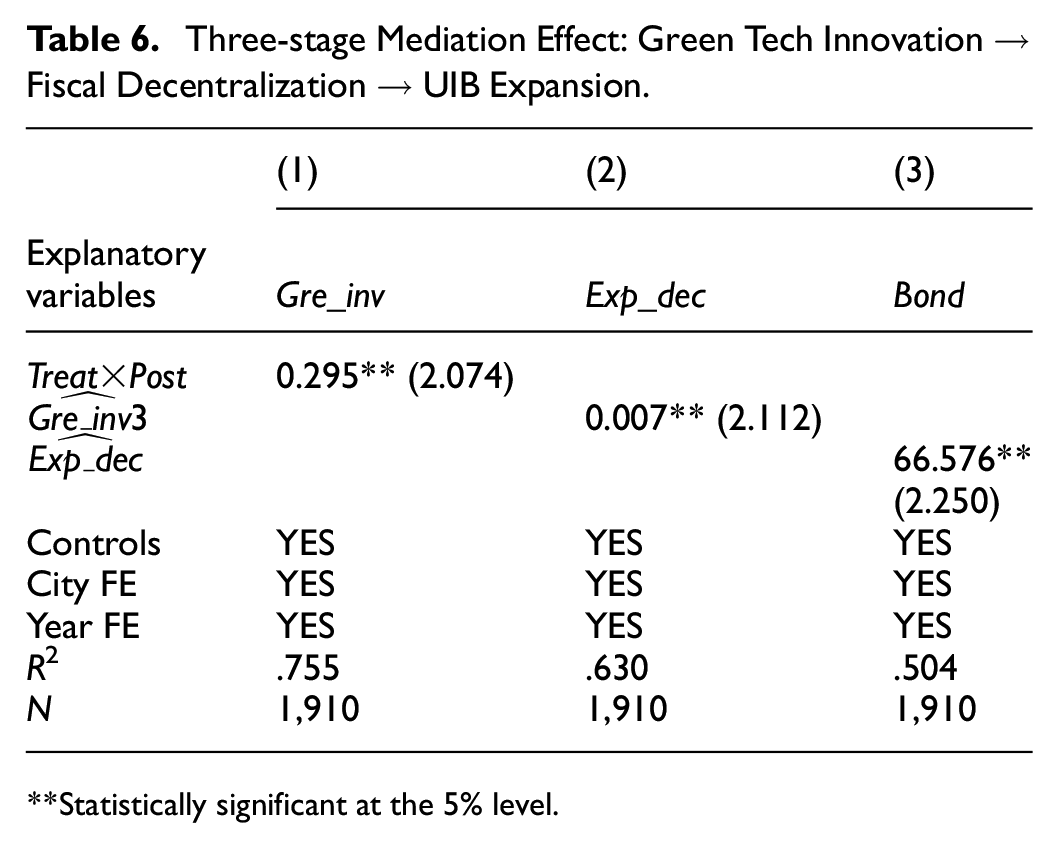

Taking green technology innovation as an example, the first stage aims to identify whether the low-carbon pilot policy significantly enhances the level of urban green innovation. The second stage (Model 10) uses the fitted values of green technology innovation levels estimated in the first stage to predict the degree of fiscal expenditure decentralization, reflecting the impact of local government participation in local affairs (such as promoting green technology innovation) under exogenous policy shocks on fiscal expenditure decentralization. The third stage (Model 11) further predicts the scale of local government debt based on the fitted values of fiscal expenditure decentralization estimated in the second stage. This three-stage equation system is analogous to a dual instrumental variable (IV) estimation, which not only highlights the three-stage logic of the research core but also clearly decomposes the transmission mechanisms among variables.

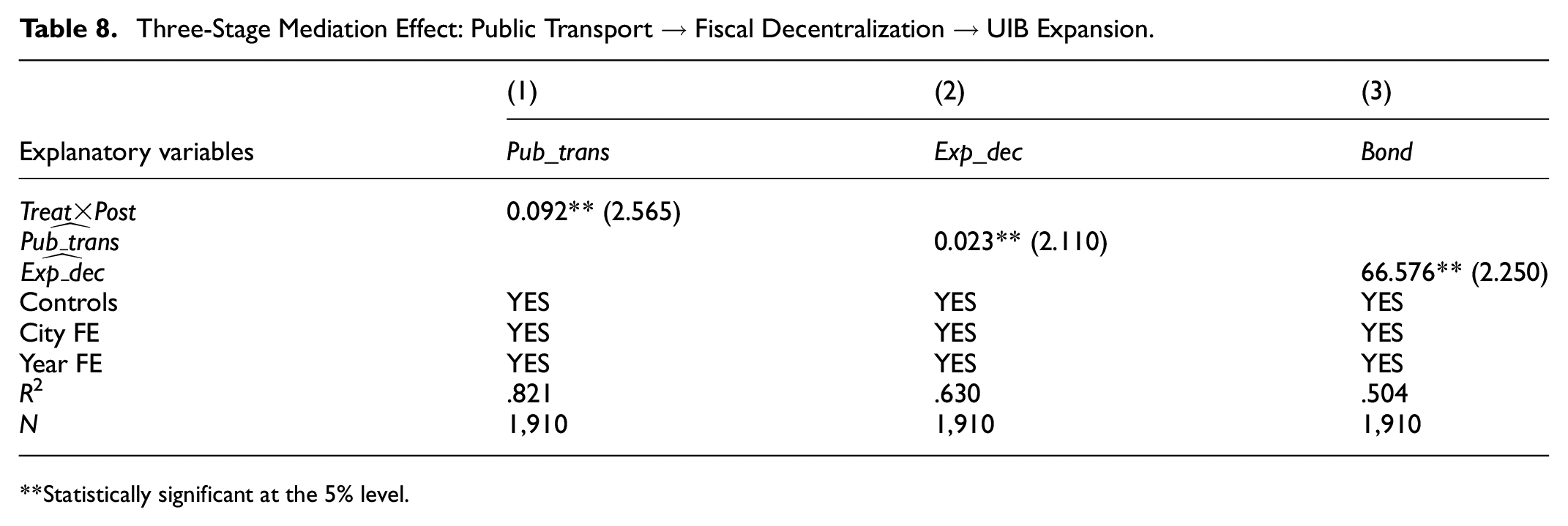

The regression results are shown in Table 6. The test results in column (1) indicate that the low-carbon policy significantly enhances local governments’ participation in local affairs (specifically manifested as promoting green technology innovation); column (2) shows that local governments’ promotion of green technology innovation further exacerbates fiscal expenditure decentralization; and column (3) demonstrates that the deepening of fiscal expenditure decentralization significantly expands local governments’ debt demand. Thus, this study reveals the transmission mechanism of “low-carbon city pilot policy → local governments promoting green technology innovation → exacerbation of fiscal expenditure decentralization → expansion of debt scale.” Additionally, other dimensions of low-carbon governance (such as industrial structure upgrading and public transportation development) follow similar transmission paths, with specific test results presented in Tables 7 and 8. The detailed transmission paths can be referenced in the theoretical framework diagram in Figure 4.

Three-stage Mediation Effect: Green Tech Innovation → Fiscal Decentralization → UIB Expansion.

Statistically significant at the 5% level.

Three-Stage Mediation Effect: Industrial Upgrading → Fiscal Decentralization → UIB Expansion.

Statistically significant at the 5% level.

Three-Stage Mediation Effect: Public Transport → Fiscal Decentralization → UIB Expansion.

Statistically significant at the 5% level.

Theoretical framework.

Heterogeneity Effects

Geographic Location

China’s vast territory results in significant regional disparities in economic development, population density, and resource endowment, leading to varying challenges and investment requirements for low-carbon transitions across cities.

Our analysis divides prefecture-level cities into eastern, central, and western sub-samples. Table 9 shows that the low-carbon city pilot policy significantly increased urban investment bond (UIB) issuance in both eastern and central regions, though the expansion was more modest in central cities. Western pilot cities showed no significant UIB growth compared to non-pilot counterparts.

Heterogeneity: Region & Environmental Commitment.

Statistically significant at the 1% level; **statistically significant at the 5% level; *statistically significant at the 10% level.

This regional variation stems from several factors. Eastern cities, as China’s economic pioneers, historically prioritized rapid growth through energy-intensive industrialization, particularly in heavy industries, resulting in severe environmental degradation that now necessitates greater transformation efforts. Conversely, the central and western regions benefit from lower baseline emissions due to sparse populations, underdeveloped industries, and abundant renewable resources, reducing transition costs. Furthermore, eastern municipalities possess stronger fiscal capacity to finance low-carbon initiatives, enabling them to meet central government targets more effectively.

Environmental Commitment

Building on Dong and Wang’s (2021) methodology, we construct a measure of local environmental commitment by analyzing low-carbon terminology in municipal government work reports (2013–2016). The results reveal significant heterogeneity: cities with stronger environmental commitment exhibit greater debt expansion under the pilot program. Specifically, Table 9 (column 4) shows high-commitment cities increased per capita UIB issuance by RMB 1,540 annually (p < .01), while low-commitment areas (column 5) show insignificant effects.

This divergence reflects the policy’s soft-constraint nature. Despite clear central guidelines, the absence of strict auditing allows implementation to vary with local priorities. In low-commitment areas, officials appear to treat the pilot program as a career-building exercise rather than pursuing substantive decarbonization, resulting in weaker fiscal mobilization. These findings highlight how administrative incentives shape policy outcomes in China’s decentralized governance framework.

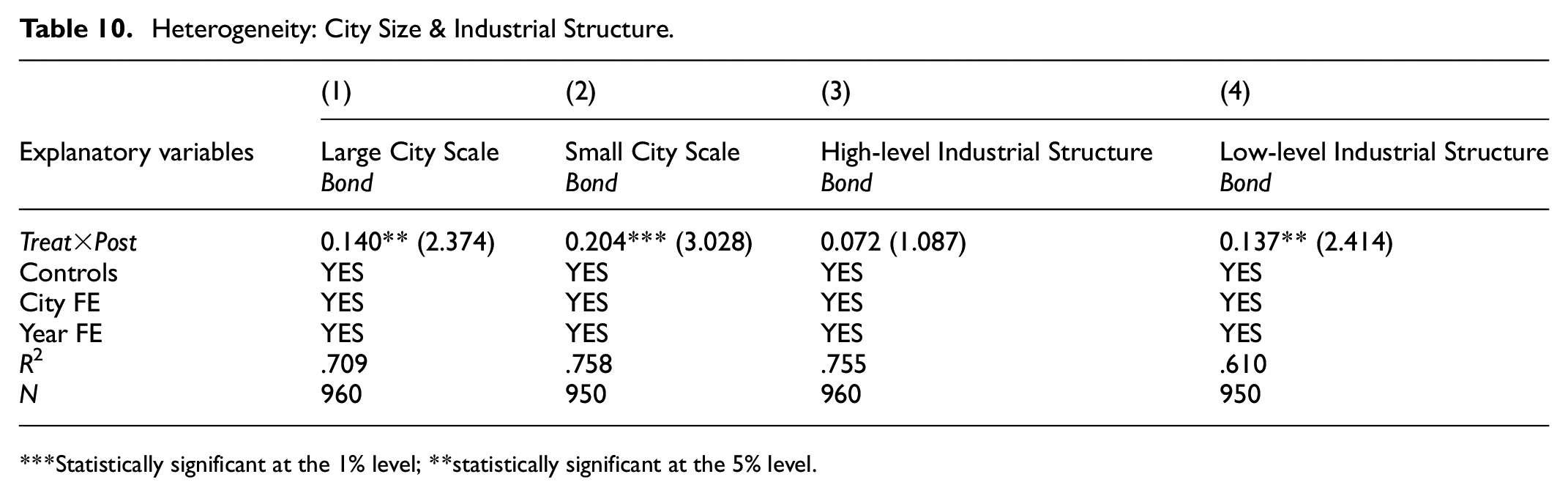

City Size

This section aims to examine whether city size influences the debt expansion effect of low-carbon city pilot policies, thereby revealing regional heterogeneity characteristics. According to China’s official city size classification standards, this study divides the full sample into two groups—larger and smaller city sizes—based on the permanent population size, to analyze the heterogeneous impact of low-carbon city pilot policies on debt expansion effects. The test results in columns (1)–(2) of Table 10 show that although both subsamples exhibit the debt expansion effect of low-carbon city pilot policies, the coefficient for the larger city size group (larger population size group) is smaller and less significant. This indicates that in cities with larger populations, the debt expansion scale triggered by low-carbon city pilot policies is relatively smaller, reflecting that these cities may have a more limited investment in carbon emission governance. This phenomenon may be closely related to their lower per capita carbon emission levels.

Heterogeneity: City Size & Industrial Structure.

Statistically significant at the 1% level; **statistically significant at the 5% level.

The reasons for the lower per capita carbon emissions in larger cities can be explained from the following aspects: First, the scale effect is significant. Larger cities improve resource utilization efficiency through shared public transportation, centralized heating, and power supply infrastructure, reducing per capita energy consumption and carbon emissions. Second, the intensive development model reduces commuting distances and transportation-related carbon emissions, further lowering per capita carbon emission levels. Third, technological progress plays a key role in larger cities, where the promotion of clean energy, energy-efficient buildings, and intelligent transportation systems effectively reduces energy consumption and carbon emissions. Additionally, policy support is stricter in larger cities, with policy tools such as carbon emission trading, green building standards, and clean energy subsidies improving the efficiency of low-carbon city construction and reducing the demand for debt financing.

Industrial Structure Sophistication

The level of industrial structure advancement significantly impacts a city’s carbon emission levels, thereby influencing carbon emission governance investments and local government borrowing behaviors. Firstly, the widespread application of high-tech industries and intelligent manufacturing technologies significantly enhances energy utilization efficiency, reducing carbon emissions per unit of output. Secondly, the production processes of high value-added industries (e.g., information technology, biopharmaceuticals) are cleaner, with lower carbon emission intensity. Additionally, the promotion of clean production and circular economy effectively reduces resource consumption and pollution emissions. The rising proportion of strategic emerging industries (e.g., new energy) further reduces carbon emissions, particularly through the substitution of clean energy for traditional fossil fuels. Lastly, the deep integration of modern services and industry optimizes resource allocation, reducing unnecessary energy consumption.

The empirical tests in this section reference the methodology of Xu (2019), using the ratio of the output value of the third category of industries to the sum of the output values of the first and second categories of industries within the industrial sector to measure the degree of industrial structure advancement (the third category includes specialized equipment manufacturing, instrumentation manufacturing, pharmaceutical manufacturing, automotive manufacturing, electrical machinery and equipment manufacturing, railway, ship, aerospace, and other transportation equipment manufacturing, as well as computer, communication, and other electronic equipment manufacturing). The test results in columns (3)–(4) of Table 10 indicate that in regions with a lower degree of industrial structure advancement, the debt expansion effect of low-carbon city pilot policies is significant; whereas in regions with a higher degree of advancement, the coefficient of the policy interaction term is not significant. This result aligns with theoretical expectations.

Conclusion

Key Findings

This study utilizes panel data from Chinese prefecture-level cities between 2013 and 2022, employing the third batch of national low-carbon city pilot policy as a quasi-natural experiment to examine the impact of low-carbon city construction on local government fiscal sustainability from a debt financing perspective. The empirical findings reveal:

First, the low-carbon pilot policy significantly accelerated the expansion of urban investment bond (UIB) issuance, an effect that remains robust across various tests. The full-sample estimates indicate that pilot cities experienced an average increase of RMB 1,100 in per capita annual UIB issuance compared to non-pilot cities, with statistical significance at the 1% level.

Second, the mechanism analysis reveals a causal chain of “low-carbon transition → fiscal expenditure decentralization intensification → debt expansion.” More specifically, the expansion of fiscal expenditure decentralization stems primarily from the augmented spending responsibilities shouldered by local governments in three key domains: (1) subsidizing green technology innovation, (2) facilitating industrial structure upgrading, and (3) developing public transportation infrastructure. These expenditure pressures constitute the drivers of subsequent debt accumulation.

Finally, the policy effects demonstrate notable spatial heterogeneity: the debt expansion effect was more pronounced in eastern regions, cities with stronger environmental commitment, areas with smaller population sizes, and regions with less advanced industrial structures.

Policy Recommendations

Local governments in China face significant fiscal pressure in the construction of low-carbon cities, primarily due to the high initial investments required in areas such as clean energy infrastructure, green technology innovation, and pollution control. To address these pressures, local governments can adopt multiple strategies based on fiscal decentralization theory: optimizing fiscal expenditure structures to prioritize key areas like clean energy, green transportation, and energy-efficient buildings; exploring diversified financing mechanisms such as public-private partnerships (PPP), green bonds, and carbon trading markets to attract social capital; ensuring efficient use of funds through targeted investments and performance management; designing incentive mechanisms like tax breaks, subsidies, and carbon taxes to promote low-carbon transitions; enhancing regional collaboration to share costs and improve resource utilization efficiency; and mitigating hidden debt risks to ensure fiscal sustainability.

Expanding China’s experience to a global perspective, fiscally decentralized countries can draw lessons from China’s practices and innovate based on local conditions. Future global environmental policy design should place greater emphasis on local government autonomy, granting them greater fiscal and decision-making authority to flexibly address local environmental challenges. Diversified financing mechanisms should become a core component of global environmental policies, with countries leveraging green financial tools (e.g., green bonds, carbon finance) and market-based instruments (e.g., carbon trading, carbon taxes) to attract private sector and social capital participation in environmental governance. For instance, the European Union’s Emissions Trading System (ETS) provides member states with opportunities to raise funds through carbon markets, while the U.S. green bond market offers financing channels for local governments and businesses to support low-carbon projects. In terms of implementation pathways, countries can accumulate experience through pilot projects, gradually scaling up successful models while enhancing international cooperation to share technology and financial resources, promoting coordinated global environmental governance. Through innovative policy design and effective implementation, countries worldwide can achieve the dual goals of environmental protection and economic development in addressing climate change and environmental challenges, ensuring the long-term sustainability of environmental policies.

Limitations and Future Research Directions

Firstly, from a technical perspective, this study employs the Difference-in-Differences (DID) model to assess the impact of low-carbon city construction on local government fiscal sustainability and debt demand. However, the study does not test the “no spillover effects” assumption, which constitutes a major limitation. The implementation of low-carbon city pilot policies may generate spillover effects on non-pilot cities through channels such as economic linkages, technology diffusion, and environmental externalities. For example, green technology innovations in pilot cities may spread to non-pilot cities through industrial chains, or non-pilot cities may actively imitate the low-carbon policies of pilot cities. These spillover effects may alter the fiscal behavior or debt demand of the control group, thereby undermining the comparability between the treatment and control groups and introducing bias into the estimation of policy effects.

Future research could employ spatial econometric models to further investigate the spillover effects of low-carbon city policies and their underlying mechanisms. By incorporating spatial weight matrices, this approach can directly quantify the spatial correlations between pilot and non-pilot cities, thereby revealing the intensity, scope, and transmission pathways of policy spillovers. For instance, researchers could analyze how green technology innovations or environmental improvements in pilot cities influence the fiscal behavior of neighboring non-pilot cities through economic, technological, or environmental linkages. Such study would not only address the limitations of this paper but also provide a more comprehensive scientific basis for policy design.

Secondly, from a research perspective, this study focuses on the short-term impact of low-carbon city construction on local government fiscal sustainability and the resulting debt demand, but it does not sufficiently discuss the long-term effects of low-carbon governance measures on local finances. The short-term fiscal pressure of low-carbon governance mainly stems from large-scale investments by local governments in areas such as green technology innovation, industrial structure upgrading, and public transportation development. These measures may exacerbate fiscal expenditure pressures and debt burdens in the short term. However, in the long run, low-carbon governance may replenish local finances by promoting green economic growth, optimizing industrial structures, and improving energy efficiency. Since this study does not deeply analyze long-term effects, it may underestimate the potential positive impact of low-carbon governance on local finances, thereby failing to fully reveal the comprehensive effects of the policies.

Future research could focus on long-term effect analysis and the mechanisms of green economic growth and fiscal replenishment to address the short-term perspective limitations of this study. For example, green technology innovations and the development of emerging industries may provide new sources of tax revenue for local governments, while improvements in environmental quality may attract investment and talent, fostering sustainable economic development. Additionally, low-carbon policies may generate additional revenue for local governments through mechanisms such as carbon emissions trading and green finance. These studies would contribute to a more comprehensive evaluation of the integrated fiscal effects of low-carbon city construction, providing a scientific basis for policy formulation.

Footnotes

Ethical Considerations

There are no ethical issues involved in this thesis and no harm will be caused to individual organisms. This entry does not apply to this thesis.

Consent for Publication

The authors have consented to publish the article.

Author Contributions

Yue Wang: Data Management, Software, Visualization, Writing—original draft, Conceptualization. Qing Wei: Conceptualization, Formal analysis, Writing—review and editing, Supervision. Shiyin Jiang: Writing—review and editing, Funding acquisition.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was financially supported by the Post funding project of National Social Science Fund (23FQLB007).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data that support the findings of this study are available from the corresponding author upon reasonable request.