Abstract

The banking sector has undergone significant transformation in recent years. Nevertheless, combinations of bank-specific and macroeconomic elements present both opportunities and obstacles for bank managers in ensuring the success of their institutions. This paper’s goal is to investigate factors that influence commercial banks profitability in Ethiopia. The current study used quantitative research approach and nine commercial banks were chosen purposively. Data was collected from national bank of Ethiopia and ministry of finance and economic development covering the period of 2007 to 2020. The generalized method of moments is used to (GMM) to analyze the data. The findings of the present research indicate that the size and liquidity of banks possess a favorable and noteworthy influence on the profitability. Conversely, operational efficiency, leverage, credit to deposit ratio, capital adequacy ratio, and interest rate spread has a negative impact on bank profitability. Additionally, inflation has a negative impact on Ethiopian commercial banks’ profitability as determined by return on assets and positive impact on profitability as determined by return on equity, while gross domestic product does not affect bank profitability. Similarly, economic globalization affects bank profitability negatively. The findings of this investigation carry significant ramifications for regulatory bodies of business banks, not only in terms of internal factors but also in consideration of external elements when formulating policies.

Introduction

Banks remain one of the key financial intermediaries in an economy, providing a variety of services. Therefore, the efficiency of financial intermediaries can have a significant impact on modern economies. Banking sector that are stable and profitable can easily resist economic crisis, and contributes to the banking system’s stability (Dietrich & Wanzenried, 2009). Banks play a major role of providing loan and encourage deposit or saving this saving or deposit promote the growth of economy by mobilizing savings and using the mobilized savings in financing the most productive sectors of economic (Alkhazaleh & Almsafir, 2014). As such, business banks are crucial to the financial sector, especially in developing nations with weak and underdeveloped capital markets. In economies where the capital markets are still developing, banking institutions serve as important source of finances for enterprises (Matthew & Laryea, 2012). Therefore, good performance of the bank is usually measured as per its profitability levels and has been essential to shareholders, customers as well as for banks continued survival and expansion (Nkegbe & Ustarz, 2015).

The financial condition in Ethiopia for as far back as decades has experienced numerous administrative and money related changes like other African nations and the remainder of creating world. These changes have realized numerous basic alterations to the financial part of the nation and have urged private banks to join and grow their activities in the business (Lelissa, 2007). Regardless of these changes, as of now, the financial business in Ethiopia is portrayed by functional wastefulness, petite and deficient rivalry and may be can be recognized by its market focus toward the large government possessed business bank and lacking diversification proprietorship structure (Lelissa, 2007). The presence of less productivity and minimal deficient rivalry in the nation’s financial industry is an away from of generally lackluster showing of the part contrasted with the created world budgetary establishments. In this way, it is essential to know the determinants of banks gainfulness for a proficient administration of banking activities planned for guaranteeing development in benefits and effectiveness.

Budget intermediaries play a crucial role in the implementation and operation of current financial activities. Banks are one of the key financial intermediaries in an economy, providing a variety of services. Therefore, the efficiency of banks can have a significant impact on current economies. The financial sector has undergone significant changes in recent years (Al-Jarrah et al., 2010). However, there are various factors such as technological advancements and relentless globalization forces that present potential and challenges for bank management to guarantee their bank remains wealthy and demanding (Scott & Arias, 2011). In comparison, the banking sector faces a higher level of risk than other businesses, and these hazards have the potential to negatively impact the bank’s earnings (Adeusi et al., 2014).

Ethiopia’s finance sector consists of the banking sector, insurance companies, microfinance institutions, savings and credit cooperatives, and the informal financial sector. However, the Ethiopian financial system is not well-developed and is not dominated by banks. According to Eshete et al. (2013), the banking industry accounts for approximately 95% of the total financial sector assets. Despite the increasing supply of financial services from year to year, Ethiopia still remains a highly under-banked country in the world. As a result, the profitability of banks is being questioned due to the limited outreach of the financial system.

Considering the over, a great deal of examination research has thus far occurred regarding the matter of bank determinants productivity for instance, Topak and Talu (2017), Tariq et al. (2014), Samad (2015), Chinoad (2014), Osuagwa (2014), and Tomak (2013) have demonstrated that bank gainfulness is affected by bank-explicit, industry-explicit, and large scale monetary factors nonetheless, these investigations neglects to incorporate the globalization factor. Besides, those literary works without anyone else give opposing ends since they depend on various models and techniques. With regards to Ethiopia, there are distinctive examination have been directed on the determinants of productivity of banks among those explores: Yigermal (2017), Kokobe and Birhenue (2015), Merin (2016), Gemechu (2016), Tesfaye (2012) correspondingly, every one of these investigations demonstrated that bank benefit is impacted by only bank explicit, industry explicit and macroeconomic variables.

Furthermore, Zelalem and Ali (2025) conducted a study on the relationship between globalization and the performance of Ethiopian business banks. In addition, Abebe Zelalem and Ali Abebe (2022) examined the impact of intangible assets on emerging market commercial banks’ financial performance and policy. Zelalem and Abebe (2022) analyzed the influence of balance sheets and income statements on the dividend policies of private commercial banks in Ethiopia. Ali Abebe (2022) explored the effects of IFRS on financial ratios, providing evidence from the banking sector in an emerging economy. Additionally, Ali and Wodajio (2025) investigated how risk management affects the financial stability of banks in emerging economies. Lastly, Ali (2025) researched the factors influencing bank profitability, specifically focusing on the significance of capital structure and dividend policy. In any case, each one of those examinations neglects to incorporate globalization factor because globalization can significantly enhance banks’ profitability by providing access to new markets, diversifying revenue sources, and enabling cost efficiencies. However, it also presents challenges such as increased competition, regulatory complexities, and exposure to global risks that banks must effectively manage to maintain and enhance profitability. Thus, this study provided critical insights that support policy-making, strategic planning, and operational improvements within the banking sector. These contributions help stakeholders understand the complex interactions at play and enable banks to adapt more effectively to the challenges and opportunities presented by globalization. Consequently, with regards to the above conversations, the motivation behind this investigation is to analyze determinants that influence the benefit of business banks in Ethiopia by including globalization factor which has not been included yet. Therefore, this investigation attempted to look for the accompanying objectives:

To look at the influence of bank explicit factor on the profitability of business banks in Ethiopia

To decide the impact of industry explicit factor on the benefit of business banks in Ethiopia

To look at the impact of full scale monetary/macroeconomic factor on the profitability of business banks in Ethiopia

To recognize the impact of globalization on the profitability of business banks in Ethiopia

The rest of the paper contents are structured in the following order: the second section affords review of related literature and section three explains the methodology employed for this investigation. The empirical effects and the overall results are supplied and discussed inside the fourth and the fifth sections correspondingly, and finally, section six is the conclusion.

Literature Review

The theories attempt to clarify the relationship between banks’ specific, industry specific, macro-economic, and globalization factors and bank profitability. The following are theories related with the banks’ profitability determinates.

Both internal and external variables influence banks’ financial success. The internal variables can be referred to as bank-specific elements of profitability because they originate from commercial banks’ financial statements, such as their income and balance sheets (Wahdan & Leithy, 2017). The economic and regulatory environment in which banks operate is made up of external elements, which are unrelated to bank management but typically have an indirect effect on banks as well.

Topak and Talu (2017) decide the bank-explicit, industry explicit, and macroeconomic determinants of business banks in Turkey over the period 2005 to 2015. The examination utilized ROA and ROE as benefit marker while intrigue incomes, other working costs, non-performing advance, liquidity, capital sufficiency, size, real GDP, and expansion as free factor and finally the relapse result shows that intrigue incomes, GDP and size have positive and noteworthy effect. Then again, other working costs, capital ampleness, and non-performing advance are adversely identified with gainfulness estimated both in ROA and ROE.

Serwadda (2018) investigates the variables that affect the earnings of business banks proof from Hungary. The study objective to determine how much longer monetary institution particular (inner) elements effect on the profitability of industrial banks in Hungary for 16 a year length starting from 2000 to 2015. The observe employs goes again on common property (ROA) as a proxy for economic group profitability, and it also considers financial institution specific (inner) elements as impartial variables. The research findings show that the earnings of financial institutions were significantly impacted negatively by non-acting loans, operating costs, and liquidity. The ratio of capital adequacy and interest margin, however, had no bearing on bank profitability.

Muhammad et al.’s (2019) study examined how M&A affects banks’ financial performance using data from emerging economies. Examining the effects of pre and post M&A on the financial performance of Pakistani banks from 2004 to 2015 is the paper’s goal. The outcome showed that the banks’ investment ratios, liquidity, and profitability all considerably and favorably improved M&A performance. However, the solvency ratios show adverse consequences.

Kawshala and Panditharathna (2017) analyze the impact of bank explicit variables of benefit in Sri Lankan household business banks. A relapse investigation is based on firmly adjusted board information. Bank size, capital stores, and liquidity have been distinguished as free factors, While, ROA as gainfulness pointer and finally the relapse finding uncover that size, capital proportion, and store proportion are sure and noteworthy bank explicit determinants of bank benefit in Sri Lanka. While, liquidity is an inconsequential determinant and it has a negative relationship.

Ngoc Nguyen (2019) studied the connection between diversification of income and, risks and profitability of 26 Vietnamese business banks (from 2010 to 2018). Empirical results from the studies version imply an inverse relationship between sales diversification and profitability. Particularly, the writer explains that the impact of sales diversification on income is mixed. Specially, the extra the diploma of sales diversification, the greater dangers the financial institution will face, however, the sustainability of the sales is stepped forward.

Dao and Nguyen (2020) examined the elements influencing the viability of business banks in Asian growing nations, which include Vietnam, Malaysia and Thailand. The authors used panel information of 4 entities; 10 banks in Vietnam, 8 banks in Malaysia, 9 banks in Thailand, and all 27 industrial banks from the period 2012 to 2016. As a result of the study, the maximum first rate similarity is that everyone entities display a drastically terrible relationship among operational hazard and banking profitability. Likewise, the extensively negative have an impact on of bank length to profitability is found on models of Vietnam and Thailand and no widespread effect on the version of Malaysia. Meantime, the maximum arguable result comes up with the adverse correlation between credit chance and banking profitability.

Using a sizable sample of US banks, Park et al. (2018) investigated the effect of public listing on bank profitability. The influence is dependent on the size of the bank, according to the findings. In particular, the public listing hurts the profitability of small and medium-sized banks. On the other hand, the effect is favorable for big banks.

The liquidity drivers of banks in the public and private sectors were examined by Bhati et al. (2021). This is accomplished by examining the long-term impact of different macroeconomic, microeconomic, and regulatory policies on the management of liquidity by both bank groups between 1996 and 2016. The study’s conclusions demonstrate that asset-based liquidity is essential for both public and private sector banks. The analysis discovered a strong correlation between liquidity and call rate, discount rate, cash reserve ratio, capital to total assets, foreign exchange reserve with RBI, and size for both private and public sector banks. Additionally, it was noted that while reserve and ROE had a substantial negative link with liquidity, other characteristics, such as asset size and capital, had a significant favorable effect in private banks.

El-Ansary et al. (2020) investigated the factors that influence the profitability of Islamic banks in the Middle East and North Africa. The study found no significance with Basel capital adequacy, but nearly the same substantial link with credit risk, size, capital adequacy, and the impact of income fees and levies. Using simply WGI as a macroeconomic variable and the incidence of self-service banking as a measure of financial inclusion, the same noteworthy correlation between ROA and ROE is confirmed.

Nguyen et al. (2018) used regression evaluation approach on panel information of 13 Vietnamese business banks for the length from 2006 to 2015. The study examined that the subsequent factors have a giant poor impact on the profitability of banks: (i) foreign shareholder’s ownership ratio, (ii) cost to profits ratio, and (iii) credit threat. Meanwhile, (i) state possession, (ii) bank length, and (iii) macro factors together with GDP increase fee and inflation have no linear relationship with the financial institution’s profitability. The final factors within the observation (including capital shape and liquidity hazard) have a negligible effect.

M. T. Rahman and Shaon (2021) investigated determinants of business financial institution profitability in Bangladesh from 2015 to 2019. The findings show that the value-income ratio and debt-fairness ratio have been observed as a poor relationship with the profitability, whereas the capital adequacy and nonperforming mortgage have now not discovered any full-size dating with the profitability.

Methodology

There are three major categories of research approaches. These are: qualitative, quantitative, and mixed research approaches (Creswell, 2014). A method for investigating and comprehending the significance that people or groups assign to a social or human issue is qualitative research. One method for evaluating objective ideas is quantitative research, which looks at how variables relate to one another. In contrast, mixed methods research is an approach to investigation that includes gathering both quantitative and qualitative data, combining the two types of data, and employing unique designs that may incorporate theoretical frameworks and philosophical presumptions.

To achieve the objective of this study quantitative and adjusted board information of 9 banks for the time of 14 years from 2007 to 2020 were used. The information was gathered from the yearly inspected fiscal summaries from National Bank of Ethiopia (NBE) and Ministry of fund and Economic Development (MOFED).

Additionally, the secondary sources had been accrued from books, articles, and thesis and posted reports. As of now seventeen (17) enterprise banks are operating in Ethiopia be that as it could; 9 (nine) enterprise banks had been chosen purposively depending on year of basis and accessibility of required facts. Purposive sampling become used because the usage of purposive sampling allows the researcher to generate significant insights that help to gain a deeper knowledge of the research phenomena through selecting the maximum informative individuals this is great to its unique desires. The dependent variables of this study are both return on asset (ROA) and return on equity (ROE). Whereas, the independent variables were bank specific, industry specific, macro-economic, and globalization factors respectively are discussed below;

The factors that determine the profitability of commercial banks are categorized in this study into macroeconomic, industry-specific, bank-specific, and globalization aspects.

Bank Specific Factors

Industry Specific Factor

Macro-economic Factors

Globalization Factor

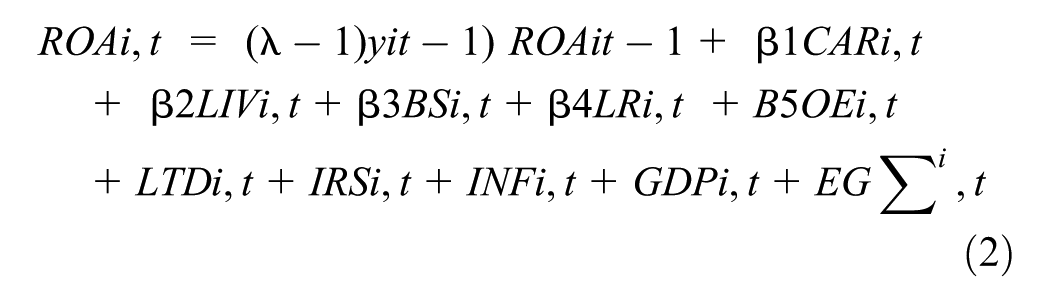

To evaluate the complex relationship between bank profitability and its determining variables, A Generalized Moment Estimator Method (GMM) model was employed in this investigation. The GMM model is a panel data estimator that corrects for endogeneity bias associated with static estimate techniques by using the lags of the dependent variable. Specifically, Arellano and Bond (1991) established the GMM distinction. This estimator uses the first differentiation strategy to address the biases and inconsistencies of the static estimating approaches. However, simulation experiments have demonstrated that when a sequence is short or continuous, the GMM difference seems to be less effective and results in subpar instruments (Bun & Windmeijer, 2010). Thus, the system GMM framework was created to address the constraints of the initial difference estimator. Lagged level conditions are currently frequently utilized as instruments for the differentiated equation, while the GMM approach uses lagged differences of a dependent variable as instruments for the level equation (Blundell & Bond, 1998). The GMM system is comparatively more robust and reliable because the framework uses more techniques. Therefore, precision is improved when applied to a big panel over a brief period of time.

The two-step system estimator is more reliable and asymptotically efficient when handling autocorrelation and heteroscedasticity (Arellano & Bover, 1995). Thus, this study employed the two-step GMM framework to assess how organizational features affect capital structure in a competitive environment. The following diagnostic tests are available to confirm the GMM estimation results. The Hansen test of over-identifying restrictions, the Arellano and bond test of no second-order serial correlation, and the null hypothesis that the conditions of the moments are true are all used. The exogeneity of the subsets of GMM instruments is also measured by a distinction in Hansen statistics. The validity of the GMM estimations is thus indicated by the failure to reject these null hypotheses. In order to match the main ideas of this study with a few modifications, this paper adopted the partial adaption model proposed by Ozkan (2001). The model is provided as follows:

Where:

ROAit, is the Return on Asset of ith bank at year t, CARit, is the Capital Adequacy Ratio of ith bank at year t, BSit, is Bank Size of ith bank at year t, IIQit, is Liquidity Ratio of ith bank at year t, OEit, is Operational Efficiency of ith bank at year t, LTDRit, is Loan to Deposit Ratio of ith bank at year t, LIVit, is Leverage of ith bank at time t, IRS, is the Interest Rate Spread of banks at year t, INFit, is Inflation Rate of the country at year t, GDPi,t Gross Domestic Product of the country at year t, EGit, is Economic Globalization of the country at year t and ROEi,t, is Return on Equity of ith bank at time t.

Empirical Results

Table 1 shows that, the mean estimation of profit for resource was 0.04, with standard deviation of 0.041 and minimum and maximum value of −0.188 and 0.355 respectively. The mean value of return on equity was 0.2265, with a standard deviation of 0.1301 and minimum and maximum value of −0.037 and 0.711 respectively. Capital adequacy ratio estimated by absolute value separated by complete resources having a minimum of 0.033% and 0.507% individually with a mean worth and standard deviation of 0.1375% and 0.0599% separately. The mean value of leverage was 0.9033 with a standard deviation of 0.723 and the minimum and maximum value of 0.251 and 0.94 respectively. The mean estimation of bank size over the time of 2007 to 2020 was 23.486 and standard deviation of 1.37668 with minimum of 19.399 and maximum of 27.3 respectively. The normal estimation of liquidity estimated by all out credit to add up to resources was 46.68%, with standard deviation of 10.19% and the minimum and maximum value of 4.1% and 77% individually.

Descriptive Statistics Summery.

Source. Stata 14 summery statistics results.

The average value of operating efficiency was 58.5% with a standard deviation of 31.54% and minimum and maximum value of −0.08% and 0.88% separately. The normal estimation of loan to deposit was 45.42% and least and greatest worth was 10.8 and 89.1 individually with standard deviation of 23.01%. Interest rate spread on normal was 0.0725% with the standard deviation of 0.0114%, minimum of 0.007% and 0.082% individually. The normal inflation rate of the country for the time of 2007 to 2020 was 13.17% with minimum of 2.7% and 20.35% separately and with a standard deviation of 8.68%. The mean value of gross domestic product was 0.098 with a standard deviation of 0.0179 and minimum and maximum value of 0.606 and 0.135 respectively. At last, the normal estimation of monetary globalization was 1.677 with a minimum and maximum value of 0.233 and 3.587 and standard deviation of 1.0928.

Discussions

The modified R2 value shows that 51.35% of the total fluctuations in the bank’s profitability as determined by ROA and 43.145 measured by ROE was clarified in the model by profitability-related variables. The findings of the two-step GMM system on the connection among the profitability and profitability related variable of business banks in Ethiopia are summarized in Tables 2 and 3. Based on the results, the GMM diagnostic tests’ fundamental requirements are satisfied. First, the p-value of the Hansen statistics indicates the veracity of the GMM results. The p-value for the AR2 test indicates that there is likewise no second-order serial correlation. The Wald statistics demonstrate the common significance of the explanatory factors, and the Hansen test discrepancy validates the homogeneity of the instrument subsets in the dependent variable prediction. The lagged ROA ratio (ROAit−1) and ROE (ROEi,t) is positive in relation to the GMM estimations of the coefficients at a significance level of 1%. The speed of change calculated as (1−λ) is 0.4865 and 56.855, suggesting that commercial banks make a partial adjustment of 48.65% and 56.855% per year. This adjustment procedure is often slow, which indicates that transaction and flotation costs are considerable.

Model 1; Regression Result.

Source. Computed from Stata 14.

, **, and * indicate that significant at 1%, 5%, and 10% respectively.

Model 2; Regression Result.

Source. Computed from Stata 14.

, **, and * indicate that significant at 1%, 5%, and 10% respectively.

Tables 2 and 3 shows that capital ampleness proportion has a negative and irrelevant relationship with Ethiopian business banks benefit measured both by ROA & ROE and the outcome is conflicting with the speculation and flagging hypothesis proposed that a higher value to-resource proportion increment productivity since as per Ezike and oke (2013) the base capital necessity of business banks in Ethiopia is 8% anyway the spellbinding measurements Table 1 shows that the normal estimation of capital ampleness proportion is 13.75% higher than the base prerequisite the delighting negative connection between capital sufficiency proportion and profit for resource seem to come about because of having save past the base necessity that face bank to surprising danger. Moreover, the adverse correlation between capital adequacy and banks profitability is because a higher capital adequacy generally implies greater financial stability, it can potentially come at the cost of lower profitability. Conversely, a lower capital adequacy can boost profitability in the short run but increases the risk of financial distress. However, the finding of this examination is comparative with Topak and Talu (2017), Rundassa and Batra (2016), Kokobe and Birhanu (2015), and Million et al. (2015) researched that a higher value to-resource proportion prompts a lower anticipated return.

Tables 2 and 3 also shows that bank size influence the productivity of business banks significantly at 5% with a p estimation of .00283 and .0169 coefficient of profitability measured by ROA and affects the profitability measured by ROE with a significant value of .036 and coefficient of .0572 separately. The positive coefficient shows that bigger business banks in Ethiopia are superior to the littler banks in outfitting economies of scale in exchanges and the finding of the examination was predictable with the working speculation and, Engdawork (2014), Merin (2016), and Tesfaye (2012) that they indicate a favorable relationship between bank size and productivity. Moreover, the favorable connection between asset size and banks profitability is because larger banks benefit from diversification, and market power, smaller banks may have advantages in terms of agility, customer service, and lower overhead costs. In any case, the examination was in opposite with Kokobe and Birhanu (2015) that proposes bank size had a negative effect on the benefit of business banks, which bolsters that economies of scale and collaborations emerge up to a specific degree of size past that level, money related associations become too mind boggling to even consider managing and dis economies of scale emerge.

Liquidity proportion is seen as factually noteworthy and decidedly related with productivity with a p estimation of .0379 and coefficient of .00117 measured by ROA and .090 and .12964 measured by ROE separately. This implies keeping other illustrative variable steady a 1% expansion in liquidity had come about 0.000117 and 0.12964-unit change fair and square of profit for resource comparable way measured by ROA and ROE respectively. The favorable connection between liquidity ratio and banks profitability is because adequate liquidity allows a bank to avoid having to sell assets at distressed prices to meet its obligations during periods of stress. The finding of this examination is predictable with Tesfaye (2012), Gemechu (2016), and Merin (2016) that underpins the possibility of old style hypothesis of intrigue that proposes the higher the liquidity the more prominent the benefit be that as it may, the consequence of this examination is in opposite with Shobor and Batra (2016), Chinoda (2014), and Kawshala and Panditharathna (2017) that they proposes liquidity had negative effect on the benefit of business banks in light of the fact that beneficial resource become inactive.

Cost administration or operational proficiency of the banks, estimated by the proportion of working cost to working salary is factually critical at 5% level with a p estimation of .0495 and .004 and with the coefficient of −.00967 and .0724 measured by ROA and ROE respectively. The negative relationship between operating efficiency and banks profitability measured by ROA is because, low operating efficiency can negatively impact a bank’s profitability through increased costs, reduced margins, customer dissatisfaction, and limited growth opportunities. Banks must prioritize operational improvements to enhance efficiency and sustain profitability. While there is a favorable correlation between operating efficiency and banks profitability measured by ROE because improved efficiency leads to reduced costs and increased revenue potential, which ultimately boosts profitability. Banks that focus on enhancing their operational efficiency are likely to achieve better financial outcomes. The after effect of the investigation suggests that all the more operationally proficient business banks detailed higher benefits than those business banks that have poor cost the board over the examination time frame this signifies business banks in Ethiopia have a lot of benefit on the off chance that they can practice productive cost the board rehearses. The after effect of the examination is reliable with Rama and Tekeste (2012), Amdemeskel (2012) that clarify their outcome with the help of proficiency hypothesis that proposes cost contrarily influences the gainfulness of business banks be that as it may, the finding of this examination is in opposite with Samad (2015), Shobor and Batra (2016).

Advance to store proportion, estimated by the proportion of complete advance to store salary is factually critical at 5% noteworthy level with a p estimation of .0124 and a coefficient of −.0924, which is adversely associated with benefit, estimated in kind on resource (ROA). The negative relationship between loans to deposit ratio on the banks profitability measured by ROA is because a higher loan-to-deposit ratio can indicate a bank’s aggressive lending strategy, an excessively high ratio can lead to liquidity issues, increased borrowing costs, and higher credit risk. These factors can ultimately undermine profitability and financial stability, making prudent management of the LDR essential for banks. However, at a 1% significance level, the loan to deposit ratio significantly affects the bank’s profitability as indicated by ROE, with a coefficient of 0.0654. The positive relationship between loans to deposit ratio on the banks profitability measured by ROE indicates that high loan-to-deposit ratio can significantly enhance a bank’s profitability by increasing interest income and demonstrating efficient resource utilization. It also positions the bank competitively in the market and fosters strong customer relationships, ultimately contributing to sustainable growth. The consequence of the examination tells that one birr given as an advance from a store has the impact of birr 0.0924 on banks benefit measured by ROA and 0.0654 respectively in Ethiopia this is on the grounds that business banks advance to store proportion under the time of study is all the more intently way to deal with store, which causes the bank to turn out to be progressively dangerous. The finding of the investigation is steady with Tariq et al. (2014) and Yigermal (2017) and be that as it may, the finding of this examination is in opposite with the finding of Samad (2015).

Leverage has significant negative relationship with Ethiopian commercial banks’ profitability was determined by return on asset and equity with a coefficient 0.001198 for return on asset and 0.00822 for return on equity at 1% and 10% level of relevance respectively. The negative relationship between leverage and banks profitability is because leverage increases risk, interest expenses, and the potential for financial distress. The results of this investigation are in line with Sikandar et al. (2021) and Zafar et al. (2010)Gatsi et al. (2013) and the study is inconsistent with Elangkumaran (2013).

Loan cost spread influence the benefit of business banks adversely, which is in accordance with what the analyst expects and the outcome is critical at 5% with a p estimation of .0554 and coefficient of −.2743 measured in ROA and significant at 1% significant level with .00171 and significant level of −1.09812 individually this implies one unit change in financing cost spread will have .2743 unit change on the productivity of business banks estimated in kind on advantage for the other way measured in ROA and 1.09812 measured by ROE that is consistent with Elangkumaran and Nimalathasan (2013). The negative connection between loan cost spread and gainfulness is on the grounds that banks pay currently produced using non-premium salary like commission on cash move, remote swapping scale, letter of assurance and different administrations charge. The outcome is reliable with Tomak (2013) and Yigermal (2017). Moreover, the negative relationship between banks’ profits and interest rate spread measured both by ROA and ROE is because a narrow interest rate spread can significantly hinder bank profitability by reducing margins, lowering net interest income, and increasing competitive pressures. Thus, banks in Ethiopia should adapt their strategies to mitigate these effects, focusing on cost management, risk assessment, and exploring alternative revenue sources.

The relapse Tables 2 and 3 shows that inflation has contrarily related with gainfulness of business banks, which is comparative, what the analyst expects with a p estimation of .0577 and coefficient of −.0293 measured by ROA and .090 and .1543 measured by ROE. The negative relationship between inflation and banks profitability measured by ROA is because, inflation can adversely affect bank profitability by eroding interest margins, increasing operational costs, and heightening credit risks. Thus, banks should navigate these challenges carefully to maintain profitability in an inflationary environment. While, the profitability of banks is significantly and favorably impacted by inflation, as indicated by ROE this is because, inflation create opportunities for banks to increase interest income, improve net interest margins, and enhance asset values. By effectively managing their strategies in an inflationary environment, banks can potentially benefit from these positive effects. The antagonism of expansion imply that startling expansion which prompts decline the acquiring of banks, which influence the benefit conversely and the examination uncovers that high inflation increment the banks cost. The finding of this examination is reliable with Merin (2016) notwithstanding; the finding of the investigation is in opposite with the finding of Chinoda (2014) and Tesfaye (2012).

Economic globalization estimated by the proportion of level of import in addition to level of fare partitioned to total national output is measurably critical at 10% noteworthiness level with a p estimation of .091 and a coefficient of .0189 measured by ROA and significant at 1% with p value of .004 and coefficient of .04149 which is adversely associated with benefit estimated in kind on resource this implies a one-unit change in economic globalization came about .0189 and .04149 unit change on return on asset and ROE inverse way. The negative relationship of economic globalization and banks productivity is of on the grounds that globalization brings high calculation among banks that the Ethiopian banks can’t avoid and there is a lot of contrast between the loaning rate and store rate in Ethiopian business banks, which influence the speculation. Moreover, the negative relationship between economic globalization and banks profitability is because globalization increased competition and regulatory complexities. Thus, banks should navigate these dynamics to optimize their performance in a globalized environment. The finding of the examination is predictable with Okeke (2011) and in opposite with the finding of Zhang and Daly (2014).

Classical Linear Regression Model Assumption (CLRMA)

Multi Collernerity

Table 4 displays the independent variables’ tolerance and variance inflation factor (VIF) for the regression analysis. To ascertain whether there is severe multicollinearity between independent variables, the VIF statistics for each independent variable are computed. Multicollinearity is present if the VIF is higher than 10. Tolerance (1/VIF) is also used to assess for multicollinearity. If the tolerance is less than 0.1 and the VIF is larger than 10, multicollinearity is evident (Gujarati & Porter, 2009). According to the table, all of the VIF values are little and none of them are greater than 10. Tolerance values below 0.1 are not present.

Multi Collernerity Test.

Source. Computed from Stata 14.

Normality Test

The results are consistent with the standard distribution assumption, according to the Shapiro-Wilk W test statistics, which display probability values of .09000 and .1623. Additionally, it suggests that the conclusions made for the population parameters based on the sample parameters seem to be accurate (Table 5).

Normality Test.

Source. Stata 14 test statistics result.

Heteroscedasticity and Auto Correlation

To handle heteroscedasticity and autocorrelation, the two-step GMM estimator approach is more reliable and asymptotically effective (Arellano & Bover, 1995).

Conclusions

In light of the survey on past examinations and banking territory hypotheses, the current examination researched the effect of some chosen bank-explicit, industry-explicit, large scale monetary or macro, and globalization factor on the profitability of the Ethiopian financial industry over the time of 2007 to 2020. The bank-explicit elements that were utilized in this examination incorporate factors, like, capital adequacy ratio, bank size, liquidity, operational efficiency, loan to deposit ratio, and leverage then again, interest rate spread is taken as industry explicit factor, inflation and gross domestic product as macro-economic and economic globalization as globalization factor. The study took the industry-specific and bank-specific, macro-economic, and globalization factors as the independent variables. Bank profitability is the study’s dependent variable, as determined by return on asset (ROA) and return on equity (ROE). The study found that capital adequacy ratio has significant and negative effect on the profitability of banks in Ethiopia measured both by return on asset and return on equity. The negative effect of capital adequacy ratio on the banks profitability is because lower capital adequacy can boost profitability in the short run but increases the risk of financial distress.

Additionally, the study discovered that leverage possesses substantial and negative impact on the banks profitability in Ethiopia measured both by return on asset and return on equity. The negative impact of leverage on the banks profitability indicated that leverage increases risk, interest expenses, and the potential for financial distress. Similarly, the study revealed that bank size has a major and favorable impact on the banks’ profitability as determined by return on equity and return on assets. The strong connection between asset size and banks profitability is because bigger banks benefit from diversification, and market power, smaller banks may have advantages in terms of agility, customer service, and lower overhead costs. The study found that the liquidity ratio significantly and favorably impacts banks. profitability measured both by return on asset and return on equity in Ethiopia. The positive relationship liquidity ratio and banks profitability is because adequate liquidity allows a bank to avoid having to sell assets at distressed prices to meet its obligations during periods of stress.

Operating efficiency has significant and negative effect on the bank’s profitability in Ethiopia determined by return on asset. The negative effect of operating efficiency on the banks profitability measured by return on asset is because, low operating efficiency can negatively impact a bank’s profitability through increased costs, reduced margins, customer dissatisfaction, and limited growth opportunities. While, operating efficiency has significantly and favorably impacts the bank’s profitability determined by return on equity in Ethiopia. The positive relationship indicates that improved efficiency leads to reduced costs and increased revenue potential, which ultimately boosts profitability. Interest rate spread has significant and adverse impact on banks’ earnings as measured both by return on asset and return on equity in Ethiopia. The negative relationship between interest rate spread and banks profitability is because a narrow interest rate spread can significantly hinder bank profitability by reducing margins, lowering net interest income, and increasing competitive pressures. Loan to deposit ratio has significant and adverse impact on banks’ profitability as determined by return on asset this is because a higher loan-to-deposit ratio can indicate a bank’s aggressive lending strategy, an excessively high ratio can lead to liquidity issues, increased borrowing costs, and higher credit risk. However, loan to deposit ratio has a substantial and advantageous impact on the banks profitability determined by return on equity this is because high loan-to-deposit ratio can significantly enhance a bank’s profitability by increasing interest income and demonstrating efficient resource utilization.

Inflation has significant and adverse impact on the banks profitability measured by return on asset in Ethiopia this is because inflation can adversely affect bank profitability by eroding interest margins, increasing operational costs, and heightening credit risks. However, according to the study, inflation significantly and favorably affects banks’ profitability as indicated by return on equity in Ethiopia this is because inflation creates opportunities for banks to increase interest income, improve net interest margins, and enhance asset values. Gross domestic product has significant and positive effect on the banks profitability measured both by return on asset and return on equity in Ethiopia. Finally, the study found that economic globalization has significant and adverse impact on the banks profitability determined both by return on asset and return on equity in Ethiopia this is because globalization increased competition and regulatory complexities. Thus, banks should navigate these dynamics to optimize their performance in a globalized environment.

So as to become productive banks better to expand their size, concentrate on store activation system even the base store rate was fixed by National bank of Ethiopia, better to modify the current store rate, viable and proficient in controlling the cost of the bank and the bank better to have viable inner control instruments to diminish the cost of banks, attempt to give credit not past the banks cost since this may cause re-installment hazard, optimal capital structure, build their advantage pay through giving sufficient advance and expanding their interest in various exercises like security, offer and items and the national bank of Ethiopia (NBE) would be advised to keep on applying the arrangement that foreign banks can’t allow to work in the nation until the nearby banks become successful and effective to figure in the worldwide market. Moreover, commercial banks in Ethiopia better to give satisfactory credit administration to help the nearby financial specialists and to make them potential and skillful speculator in the worldwide market. In this way, the export become elevated and banks can get more benefit as premium and salary from the exchanges.

The study does not include any other industries besides banking, used only quantitative research approach that can note fill the gap of qualitative research approach and not include more industry specific, firm specific, macro-economic, and globalization related factors. As a result, future research could go in a variety of directions. First, additional variables like the number of directors, insider ownership, institutional ownership, age, and the firm’s business risk could be investigated. Second, the use of macroeconomic related variables could be a potential extension of the current study. Finally, the findings revealed globalization related factors like political and social globalization, which can be further investigated by future researchers.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data available will be made available upon reasonable request.