Abstract

Using the comparison of stock performance when different levels of price limits are in place, this study measures the effects of expanding the Taiwan Stock Exchange’s (TSEC) price limit from 7% to 10%. After the price limit widening event, the findings show: (1) the speed of information transmission increased considerably in the three different firm sizes (e.g., a decrease in delay by 0.0933 in large firms), (2) the errors in prices (RRD) increased considerably in the three firm sizes (Large, Medium, Small), and (3) insignificant effects of changes in the lead-lag and asymmetric effects on different-sized portfolios were detected. These findings indicate that widening the price limit leads to improved information transmission at the risk of increasing stock market risk. The order and the asymmetric effects of the spillover of information across different-sized portfolios were not changed by the event. Regulators are advised to bear in mind the trade-off of these effects when setting the optimal price limit levels.

Keywords

Introduction

Price capitalizations are a stabilization mechanism in numerous stock markets by limiting day-to-day price movement. On June 1, 2015, the Taiwan Stock Exchange (TSEC) increased its daily price limit from 7% to 10%, and it raised questions regarding its effect on market quality. Although price limits have been explored a lot, most studies have examined general volatility and volume of trades, not any specific effects caused by the system. In addition, the market’s pervasive presence of retail investors intensifies the effects of the system by way of their trading actions. Empirical studies of the effects of expanding price limits in a single-event framework, especially in the context of information flow, mispricing errors, and lead-lag relations, are scarce. This research closes the gap by examining TSEC, a transparent and electronic market and one that is different in nature compared to the global market.

Information transmission is one of the essential parameters of market quality and directly influences market price discovery. In theory, in a perfect market, stock prices capture all the information transmitted in the market. Nevertheless, price limit regulations that negatively influence the stock market might prevent prices from reaching their equilibrium levels (K. A. Kim & Rhee, 1997), thus breaching the efficient market hypothesis. TSEC’s move to increase the price limit went in line with the trend of other markets and was meant to increase market efficiency, in part, by enhancing the dissemination of information and the ease of price discovery in the market. This paper presents a targeted analysis of the effect of the TSEC’s 2015 event on information transmission, examining a dimension under researched in the context of price limits. This study’s novel contributions are the following:1. single-event framework: This study exclusively considers the same stocks before and after the event. Conventional price limit studies tend to compare the stocks that hit and the stocks that did not hit, introducing potential biases (Deb et al., 2017; K. A. Kim & Rhee, 1997). By studying the same stocks, this study controls for potential confounding factors and allows a purer analysis of the effect of the event; 2. extensive data: Taking advantage of the extensive data of the TSEC’s 2015 event, the study herein presents a thorough analysis of market processes. Berkman and Lee (2002) emphasized that expanding price limits might target trading practices even on days when the stocks did not hit, affecting investor confidence and risk perceptions. This study’s extensive dataset provides a solid analysis of these processes; 3. applicability in other markets: TSEC’s experiences of having narrow and wide price limits prove to be a useful benchmark in other markets. In comparison to studies that compare highly distinct exchanges, including Japan (14%–30% limits) or Malaysia (30% limits) (Chan et al., 2005; K. A. Kim & Rhee, 1997), the present study controls the effects of price limit changes in a single controlled market setting. Such a controlled method facilitates the generalizability of the findings to comparable rule of order settings.

This study’s originality stems from the utilization of a single-event internal comparison method to compare the comparative performances of the same sample group prior to and following the limit change in price, hence, eliminating the endogeneity and sampling problem generated by the “touched and untouched” sample comparison in the previous literature. This method facilitates the research’s discrimination and policy implications. In addition, using the Taiwan market as a specific example, the paper unmasks the structural effect of the increase in price restriction on the order of market risk, order of information transfer, and companies of different sizes, and provides concrete inspiration for reform design in emerging markets and a knowledge gap in the extant literature.

In comparison to the majority of previous research, which focuses on price continuation, transitorily volatility, and abnormal trading volume, the current study changes the orientation of the study to examine potentially critical and under researched areas, and fills knowledge gaps in literature, including: (1) Information Incorporation: An analysis of the effects of price limits on the speed and quality of incorporation of information into stock prices. (2) Price Errors: Exploration of discrepancies in observed stock prices and fundamental values, a primary concern in a market’s efficiency. (3) Lead-Lag Relationships: An analysis of whether the sequential arrival of information across firm of different size is caused by changes in the price limit. (4) Asymmetric Impacts: Assessment of whether the change in the limit of price changes the order of dissemination of information across big and small-sized companies.

Empirical findings of the TSEC event are presented below: (1) Information Transmission: Both delay 1 and delay 2 measures declined considerably following the event for all firm sizes, with the largest declines occurring in larger firms; (2) Price Errors: Large, medium, and small companies experienced a rise in price errors post-event, reflecting increase in market risks following the event; (3) Lead-Lag Relationships and Asymmetric Impacts: There are no changes in the direction of the lead-lag relationships or the asymmetric effects on firm size, corroborating the sequential information arrival hypothesis (SIAH). (4) These findings indicate that expanding the price limit produces both positive and negative effects on market quality. While it speeds up the transmission of information, it also heightens price errors, demonstrating the trade-off between efficiency and risk. Lead-lag stability testifies to the resilience of information distribution patterns in the face of market changes in the price limit. This work contributes essential insights for regulators planning similar policy modifications and points out the subtleties of the effects of price limit reforms on market processes.

The outline of the paper is as follows: Section 2 presents the literature and the formulation of hypotheses, Section 3 describes the data and the method of measuring variables, Section 4 reports the findings of the analysis, and Section 5 concludes the paper with the final discourse.

Literature Review and Hypotheses Development

Traditional limit studies tend to emphasize the potential demerits of price limits, including the lag in price discovery due to the prevention of immediate price adjustment to new information (K. A. Kim & Rhee, 1997). Such a lag negates market efficiency by inhibiting full incorporation of important market news in stock prices. There exist, however, alternative views, which argue that the easing of price limits allows markets to digest and absorb information more efficiently. For example, Ryoo and Smith (2002) analyzed the Korean stock market and found that enlarged price limits enhanced the random walk characteristics of stock prices, reflecting improved market efficiency. Likewise, Seddighi and Yoon (2018) corroborated the findings, and they added that expanded price limits lowered informational frictions and enhanced the speed of price discovery. In a more recent study, Jin et al. (2022) presented strong empirical evidence with the finding that easing the price limits considerably facilitates the speed and quality of price discovery. They assessed price efficiency in measures that capture the timeliness of the incorporation of information in prices.

To complement these results, representatives of the Taiwan Stock Exchange (TSEC) claimed that wider price limits enable more efficient incorporation of market news in stock prices, especially in high-speed markets. Wider price limits adopted by the TSEC in 2015 confirms this view. Nevertheless, when stock prices hit the daily price limit (±10%), further price adjustments are postponed due to trading bans. This retards the dissemination speed of information, above all in situations where the market needs to react in a timely fashion to news. In comparison to markets that do not have a daily price limit, the U.S. market, for one, Taiwan’s market price limits can block the quick absorption and incorporation of salient news (e.g., announcements of corporate earnings or macroeconomic indicators). For instance, the ADR prices might already incorporate the news, whereas movements in the Taiwan local market are postponed to the next trading day. Stock price restriction by the limits could leave the price changes incomplete on a trading day, and they trigger the following day’s compensatory changes, which result in price errors.

Market players, particularly institutional investors, will forecast price movements in response to limits, and speculative trading is likely to intensify deviations from true values. In each industry, a stock price limited by the limit will cause associated stocks to anticipate the news in advance, generating lead-lag effects at the company or industry levels. Trading by institutional investors in large capitalizations serves as a leading indicator, while that in small capitalizations, driven by retail investor attitudes and price limits, will lag. Thus, the existence of price limits in Taiwan will generate a lagging response to foreign events (e.g., U.S. market movements). Institutional investors will seek cross-market opportunities, including the arbitrage of ADR, generating asynchronous transmission of information in the Taiwan stock market. Based on these studies, we hypothesize:

Hypothesis 1: By allowing stock prices to adjust more promptly to news, the enlargement of price limits enhances the speed of information dissemination among firms of various sizes.

Price limits have also come under criticism owing to their ability to accelerate market volatility and distort pricing accuracy. For instance, Berkman and Lee (2002) noted that wider price limits accelerated intraday volatility in stock prices, which in turn caused more significant discrepancies between observed stock prices and their intrinsic values. In a similar vein, W. Kim and Jun (2019) established that the removal of price limits created increased uncertainty in the marketplace, thereby intensifying noise trading and speculative actions. These effects distort the price signals and result in many pricing errors. Behavioral finance models shed more light on these effects. Overreaction and herding are typical reactions to market uncertainty, especially in the context of increased price movements facilitated by wider limits. These reactions tend to create short-term deviations of price from intrinsic values, as evident in research in other markets globally (e.g., Chan et al., 2005).

Individual investors typically have short holding periods and exhibit high sensitivity to price limits. They can withdraw or chase orders at high speed as price levels are at or approaching the limits, which further intensify price volatility. Herding is typical of individual investors during the time of approaching stock prices to the daily limits, and it results in volatile trading volume and fluctuating prices. In addition, individual investor views price limits as a chance to sell or buy, especially when stock prices reach the upper or lower limits, and they intensify the market’s short-term volatility by doing so, whereas institutional investors prefer large-cap stocks (e.g., Aggarwal et al., 2005; Gompers & Metrick, 2001)) and tend to follow the approach of long-term investments and hence are not much disturbed by price limits. When price limits cause irrational short-term volatility, institutional players might indulge in arbitrage practices and, in turn, might further narrow the profit margins of the individual investors; institutional investors, who are better informed and have more advanced tools of pricing and trading (for instance, computer-driven trading), can change strategies at high speed before the price limits are reached. Hence, the above activity might intensify the disadvantages of the individual investors, further deepening market inequality. Since the pricing errors ruin the confidence and efficacy of the market, it becomes essential to understand the correlation of the above errors with price limits. In this regard, we hypothesize:

Hypothesis 2: Broadening price limits increases the magnitude of pricing errors across different types of firms.

Individual investors might view price limits as buying or selling opportunities, especially when the price gets close to the upper or the lower limit, and carry out contrarian trading and further increase market volatility in the short term; institutional investors, however, tend to like large-cap stocks and follow long-term investment techniques and are hence not directly hit by price limits. Institutional investors tend to prefer large-cap companies for several key reasons: superior liquidity and lower transaction costs (Aggarwal et al., 2005; Gompers & Metrick, 2001); higher levels of information transparency and visibility, which reduce information asymmetry and informational risk (Ferreira & Matos, 2008; Hariprasad, 2016; Kang & Stulz, 1997; Merton, 1987); lower risk and more stable performance (S. C. Bae et al., 2011; Del Guercio, 1996; Falkenstein, 1996); and better alignment with institutional constraints related to regulation, oversight, and internal investment policies (Aggarwal et al., 2005; Ferreira & Matos, 2008). These studies collectively demonstrate that institutional investors favor large-cap firms because they enable more efficient capital allocation, lower investment risk, and improved market transparency and tradability. When price limits cause short-term irrational volatility, institutional investors might use arbitrage techniques to capitalize on pricing inefficiencies and further narrow the profit margins of the individual investors; institutional investors, having better information and better trading tools (such as algorithmic trading), can change their strategies quickly before price limits are reached. This might further increase the disadvantages of the individual investors, further accelerating market inequality.

Asymmetric effects in financial markets result from differences in the ability of firms to absorb and respond to new trading information. Firms of larger size reap the benefits of more institutional ownership, more extensive analyst coverage, and greater liquidity, which facilitate the efficient adjustment of their prices compared to smaller firms. These benefits generate persistent asymmetries in the incorporation of the information in stock prices. Both Badrinath et al. (1995) and Menzly and Ozbas (2010) establish the persistency of the asymmetries despite changes in the regulatory framework. Their perspective is based on the premise that the effects of these dynamics arise from structural differences across firms and are not easily mitigated by external measures such as price limit adjustments. Empirical findings in both markets characterized by both tight and liberal price limits indicate the stability of the asymmetric effects of the large and small firms under any regulatory framework. We, therefore, hypothesize:

Hypothesis 3: Broadening price boundaries alters the asymmetric effects across different-sized firms

The lead-lag pattern across firms of different sizes is a manifestation of the sequential arrival of information in financial markets. Large firms, being more liquid and followed by more analysts, generally lead smaller firms in the integration of news in stock prices (Lo & MacKinlay, 1990). This is according to the sequential information arrival hypothesis (SIAH), which argues that news initially manifests in the stock prices of large, heavily followed companies and then seeps through to smaller, illiquid stocks.

Hou (2007) elaborated on this framework, demonstrating that structural elements including institutional ownership, cost of information, and market noise entrench the sustainability of lead-lag relations in the long term. Further research by Badrinath et al. (1995) and Menzly and Ozbas (2010) supported these conclusions, highlighting that these processes are enrooted in market frameworks and not likely to be affected by changes in regulations in the form of price limit changes. Price limit triggers market players, particularly institutional investors, to anticipate price movements, leading to speculative trades that potentially magnify divergences from intrinsic values. Within the same industry, when a stock’s price is capped by the limit, associated stocks anticipate the information in advance, generating lead-lag effects between companies. Trading by institutional investors in blue chips serves as a leading indicator, whereas small-cap stocks, subjected to individual investors’ sentiment and limit price. Price limits establish an asymmetric mechanism between institutional and individual traders: the former utilize market volatility in arbitrage or hedging, whereas the latter are hampered by the inability to rapidly change strategies. This dynamic can multiply market volatility and decrease the efficiency of price discovery. Price limit system facilitates the management of excess volatility but weakens the efficiency of markets due to its effects on the transmission of information, price errors, and lead-lag relations. Major market players’ trading habits under the system further reinforce volatility and asymmetry. Whilst the system promotes transparency and stability, ongoing analysis is crucial to consider its long-term effects on market efficiency. The hypothesis is as follows:

Hypothesis 4: Broadening price ranges changes the lead-lag relationship across companies of varying sizes.

Institutional Description of the TSEC, Data Source and Variable Measurements

Institutional Description of the TSEC

The TSEC operates as a fully electronic, order-driven market. Trading hours run from 9:00 AM to 1:30 PM, with traders allowed to enter orders into the system starting at 8:30 AM. The market utilizes a call system to determine opening and closing prices, while a continuous trading system is used throughout the day. Initially, the TSEC imposed a daily price limit of ±7%, based on the previous day’s closing price. However, on June 1, 2015, this limit was expanded to ±10%. TSEC officials stated that the change was intended to align with global practices and improve market efficiency. In contrast, a local magazine expressed concerns that this adjustment could increase market volatility and risks, potentially altering investors’ trading behaviors. When a stock reaches its price limit, a red signal appears on the trading screen, and while trading continues, only orders within the designated limits are executed.

Individuals are the major investors on the TSEC. Statistics show in 2021, individual investors accounted for 60.40% of the trading on the TSEC, more than half of the market trading volume. Institutional investors accounted for the remaining 39.60%. Usually, institutional investors prefer to trade large size company stocks while individuals prefer small company stocks. Furthermore, institutional investors hold stocks longer than individuals, and are thought to be helpful for stabilizing the stock market. Individuals tend to hold stock for very short periods, and they are easily swayed by rumors, creating instability in the stock market.

Data Source

The data used to drive this analysis was obtained from the Taiwan Economic Journal (TEJ) database for the period from January 1 to September 30, 2015. A pre-post event study framework was adopted, focusing on January 1 to September 30, 2015. The pre-event period (January to May) provided a baseline, while the post-event period (June to September) captured immediate effects. The selection of this period ensures clarity in isolating the event impact while avoiding potential confounding events. Prior to this well documented event, there was no way to determine the length of an event period and the corresponding estimate period. The event period must be well known to investors as possibly influencing the stock market. The estimate period is the time when the event has no impact on investors or the stock market.

The event study literature consistently finds that stock prices react very quickly to new policies or major public information disclosures. Under the efficient market hypothesis, markets typically incorporate new information fully on the announcement day or the following day. As such, using a short event window—limited to the day of or the day after the disclosure—is generally sufficient to capture abnormal returns effectively (Bernanke & Kuttner, 2005; Boehmer et al., 2013; Chhaochharia & Grinstein, 2007; Savor & Wilson, 2013). If the event window is too long (e.g., several weeks or months), the analysis may be confounded by other events or external factors, making it difficult to isolate the true impact of the focal event. Therefore, recent studies tend to recommend short event windows (Brown & Warner, 1985; Fama, 1970, 1991).

The sample was obtained using the following procedure: all firms listed on the TSEC were categorized into three groups—large, medium, and small—based on their market capitalization at the end of 2014. A simple random sampling method was applied to select 100 firms from each group. To avoid duplication, any repeated samples encountered during the process were removed, retaining only unique entries. Proportional industry representation was ensured to minimize sampling bias, with 100 firms being randomly selected from each size category. Irretrievable data were excluded from the analysis. To exclude the impact of price limit reform on market capitalization after the event, this paper selects the market capitalization at the end of 2014 as the clustering benchmark and establishes a snapshot of corporate structure before market reform.

Methodology

As noted previously, little empirical evidence exists on the impact of widening the price limits on stock market quality for different sized firms. To fill this gap, this investigation focuses on information transmission, price errors, and the lead-lag relationship and asymmetric impact for different sized firms during the pre-period and post-period. The methodology for analyzing these three issues are as follows.

Information Transmission

The methodology used by K.-H. Bae et al. (2012) to measure information transmission was used to conduct the study. There are two measures: delay 1 and delay 2. Delay 1 was calculated using the following formula:

restricted:

where

Next, delay 2 was measured as follows:

where

Price Errors

The relative dispersion (

where

After comparing the scatters and magnitudes of

Lead-Lag Relationship Among Different Size Portfolios

To test whether there was a lead-lag relationship between various size portfolios and whether the relationship was altered by the event, the vector auto-regression (VAR) model was used:

or

where

The lead-lag relationship model also allowed examination of the data to determine whether there was an asymmetric impact across the large size firm to the medium, and then from the large to the small size firm portfolios using the following hypothesis. By observing the asymmetric impact pre- and post- event, changes in the asymmetric impact across various size portfolios could be determined.

Empirical Results

Summary Results

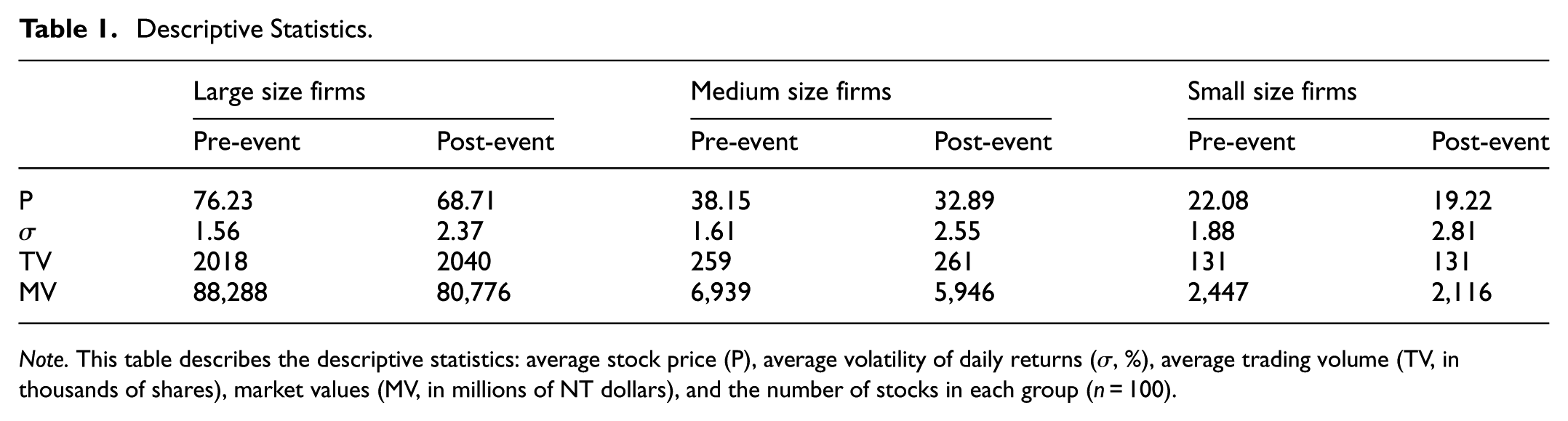

Applying the methodology described above and using transaction data from the TSEC, the following empirical results were reached. The basic data used in this study and the results derived are summarized in Table 1. The descriptive statistics section has been updated to include detailed comparisons of pre- and post-event data for stock prices (P), volatility (σ), trading volume (TV), and market value (MV) across large, medium, and small firms. The interpretation highlights the differential impacts on market dynamics, particularly emphasizing the greater effects on smaller firms.

Descriptive Statistics.

Note. This table describes the descriptive statistics: average stock price (P), average volatility of daily returns (σ, %), average trading volume (TV, in thousands of shares), market values (MV, in millions of NT dollars), and the number of stocks in each group (n = 100).

We acknowledge that this article categorizes companies by market capitalization at the end of 2014, but market capitalization can change dramatically over post-event, and the industry’s nature will also have an impact on its reaction toward the adjustment of price limits. So, the future study proposes that the same industry can be recategorized by dynamic changes in market value, and the industrial stratification analysis can be carried out, particularly in the case of industries demarcated by different market response systems, to further examine the heterogeneity of the effects of institutions.

Information Transmission

The speed of information transmission was estimated using the measures of delay 1 and delay 2, by applying formulas 1 and 4. Subsequently, a test of significance of these two time periods (before and after the event period) was conducted. The results are presented in Table 2. As shown in Table 2, both Delay 1 and Delay 2 experienced a substantial decline following the event, regardless of firm size. In the case of large firms, Delay 1 dropped by 0.9548 to 0.8615 (−0.0933, p < .01). Medium and small-sized firms showed smaller but significant improvements. This corroborates the hypothesis that price limits of greater width reduce informational obstacles, especially in the case of large companies. For instance, in the case of large size companies, the delay prior to the (after the) event is 0.9548 (0.8615), a fall of −0.0933, which is significant at the 1% significance level. Decrease in the measure of delay goes down as the size of the firm declines (−0.0933→−0.0502→−0.0212). Similar results are the findings in the case of delay 2. The results presented in Table 2 are in line with the beliefs of Ryoo and Smith (2002), Seddighi and Yoon (2018) and Jin et al. (2022). Results support hypotheses H1. Delay 1 and Delay 2 measures fell considerably post-event in the case of all firm sizes. In the case of large companies, Delay 1 fell by 0.9548 to 0.8615 (−0.0933, p < .01). Medium and small-sized companies showed smaller but significant declines. This corroborates the hypothesis that price limits of larger width ease informational obstacles, especially in the case of larger companies. H2 is supported.

Information Transmission.

Note. This table provides the results for the measure, delay 1 and delay 2, respectively. Model:

, **, and * is significant at 1%, 5%, and 10% level, respectively.

There are two explanations for these findings. First, expanding the price limit might have resulted in a decrease in the barriers to information impounded in the stocks. Second, institutional investors favor large size companies compared to small size companies in the TSEC, and institutional investors tend to have more chance of being able to handle the information compared to individual investors. Investor preferences vary by firm size, and larger firms tend to exhibit greater reductions in the delay measure.

Price Errors

Price errors (

(A) Relative dispersion for large firms, (B) relative dispersion for medium firms, and (C) relative dispersion for small firms.

Lead-Lag Relationship Among Different Size Portfolios

After controlling for lagged own-return, the vector auto-regression (VAR) models, model (7)-model (10), were implemented. Equation 11 was implemented to test the question of if there existed an asymmetry effect in different sized portfolios. The empirical results are presented in Table 3.

Lead-Lag Relations Among Portfolios.

Note. This table presents the estimation results obtained with the vector autoregression model (VAR) using the equal-weighted intra-day returns for large, medium, and small size firm portfolios. The model was formulated as follows:

The context preceding the event must first be examined. As indicated by panel A of Table 3, the lagged returns of large size firm portfolios can explain the current returns of medium size firm portfolios. The estimates vary between 0.1222 and 0.2174, and they are significant at the 1%. Likewise, the lagged returns of the medium size firm portfolios can explain the current returns of the large size firm portfolios, and the estimates vary between 0.0705 and 0.0253. Although they are significant at the 1% or the 5%, these values are smaller in size (0.0705–0.0253 vs. 0.2174–0.1222). Additionally, the cross-equation test indicated that the difference in the coefficient of the lagged returns of large size firm portfolios in explaining the current returns of the medium size firm portfolios (0.2174–0.1222) and those of the lagged returns of the medium size firm portfolios in explaining the current returns of the large size firm portfolios (0.0705–0.0253) was positive and significant at the 1% level (the Wald statistic is: 317.50). Finally, the lead-lag relationships between the returns of large- and small-sized firm portfolios were examined. The results are displayed in panel B of Table 3. It had a similar pattern to the findings in panel A of Table 3. So, in both scenarios, the lag returns of the large size firm portfolios in explaining the current returns of the medium (small) size firm portfolios was more robust compared to the lag returns of the medium (small) size portfolios in explaining the current returns of the large size firm portfolios.

From Table 3, Panel B, the suggestion is that the lag returns of large size firm portfolios in predicting the current medium size firm portfolios are more useful than the lag returns of small size firm portfolios. As far as the results are concerned, pre-and post-event, the explanations and implications below are provided. First, on the TSEC, the institutional investors favor large size stocks more than medium (small) size stocks. Large size stock price therefore contains more information than the price of the medium (small) size stock. It is precisely why the lagged large firm portfolio returns exhibit more predictability concerning the current medium (or small) firm portfolio returns. This argument fits Badrinath et al. (1995), Menzly and Ozbas (2010), and favors the SIAH. Second, the lead-lag relation and asymmetrical effect of large firm portfolios and medium (small) firm portfolios were not changed post-event. That is, while the widening of the price limit facilitates information transmission, it does not alter the order or the asymmetric nature of post-event information spillover among portfolios of different firm sizes.

Pre- and post-event lead-lag orderings were the same, wherein large firm returns preceded the returns of medium and small firms. These results support the sequential information arrival hypothesis (SIAH). Such stability is likely due to institutional tastes favoring large firms. Comparative analysis of TSEC outcomes to those of other markets (the Malaysia market, the Japan market, etc.) shows that TSEC’s results follow international trends but also capture market-specific elements. Overall, pre-event or post-event, outcomes support hypotheses 4.

Discussion, Conclusion, Policy Implication, and Limitation

Discussion

Price limits is a significant issue to study in the context of stock market quality. Although numerous studies have surfaced, previous studies have failed to provide any direction and the debate about the effects of price limits remains ongoing. Traditional debates were sidestepped in this work by examining the effects of expanding the price limit on market quality, including the structural effects of the increase in price restrictions on the order of the transmission of information and market risk in different-sized companies, rather than the traditional controversies of the effects of price limits per se. This study fills essential gaps in the literature by investigating the effects of expanding price limits on market quality. This study’s novelty is in using a single-event internal comparison method to examine the same sample group of companies both before and after the change in the price limit, avoiding the endogeneity and sampling bias due to the “touched and untouched” sample comparison in most prior studies. This approach enhances the research’s discriminability and policy significance.

Unlike earlier research that mainly emphasizes price continuation, volatility spillovers, or abnormal trading volume, the present study explores the differential impacts of the price limit on the transmission of information, price errors, and the lead-lag and asymmetric effects across different sizes of portfolios. By using a single-event analysis approach, the study avoids the potential systematic biases in comparing hitting and not hitting stocks (Deb et al., 2017; K. A. Kim & Rhee, 1997). This study extends K. A. Kim and Rhee’s (1997) foundational work by investigating lesser-explored aspects of price limit widening. We addressed three problems and compared results before and after the price limit widening: information transmission, price error, the lead-lag and asymmetric effect across different sizes of portfolios. It provides a more solid insight into the role of the price limit in the stock market, especially in the emerging, like those of Vietnam and India, generalizes the geography and context of the outcome of the study.

Conclusion

Focusing on a single, documented event, this study avoids confounding variables and provides a benchmark for future studies of price limits using events. Following the price limit widening event, there was a sharp decline in delay 1 and delay 2 measures of firms of all sizes, and the larger the firm size, the more the decline in the delay measures. From these findings, it is reasonable to argue that widening the price limit had a positive effect on reducing barriers to stock conveyed information. TSEC institutional investors prefer large-sized firms, and large-sized firms are more efficient in processing information. Second, in the case of all large, medium, and small-sized firms, the errors in prices increased substantially following the event. This is likely due to augmented risk following the event. Third, there was a transformation in the lead-lag relationship and asymmetric effect across different sized portfolios following the event. This indicates that widening the price limit alters the order and asymmetric effect of information spill-over effect across different size portfolios following the event. Findings affirm the robustness of the lead-lag relations and the asymmetric effects across firm sizes and indicate structural variables overwhelm these processes even in the aftermath of changes in regulations.

Limitation

In the future, work needs to look more directly at investor heterogeneity by including behavioral indicators and distinguishing retail and institutional trading types using more detailed intraday data sets. This will yield more insights about the distributional effects of reforms across different market players and support more fair market design. Due to data limitations, this article has not yet incorporated high-frequency trading data and microstructure variables, such as quote depth and spread volatility, and is unable to directly assess the specific impact of limit price adjustments on trading strategies, algorithmic behavior, and market noise. As strategic trading (such as adjusting order pace and splitting orders) is increasingly common among institutional investors, it is suggested that in the future, the potential impact of the price limit system on market fairness and efficiency can be explored through high-frequency data and micro-structure indicators (such as order imbalance and quote volatility), and used as a basis for policy supervision. As institutional activity becomes more dominated by algorithm and strategic trading, it is crucial to know how these mechanisms mesh with price limit reforms.

It is worth noting that this article groups companies based on their market capitalization at the end of 2014, but the market capitalization may have changed significantly after the event, and industry characteristics may also affect their response to price limit adjustments. Therefore, future research suggests that the industry can be regrouped based on dynamic market value changes and industrial stratification analysis can be conducted, especially for industries with different market response mechanisms such as technology, finance, and manufacturing, to further explore the heterogeneity of institutional effects.

In short, empirical findings suggest the effect of expanding the price limit on market quality is attributable to the outcome in question. In adamic studies, it helps information transmission but also augments price errors, creating difficulties in risk management. Lead-lag relations and asymmetric effects transformed, indicative of limited effects on market composition. Difference-in-difference (DID) is corroborated in the change in the price limit in the same index in different stock exchange markets. Despite the use of vector autoregression (VAR) and relative price dispersion (RRD) in the analysis in this paper, it does not detect potential structural changes and strategic trading activities of a nonlinear type. Future studies could introduce Quantile Regression to assess the heterogeneous effect of limit price changes on different stock segments under different market conditions and integrate different types of machine learning techniques (random forests, LSTM, etc.) to increase the explanatory power of the model.

Policy Implications

For regulators and the policy makers, they need to carefully balance objectives, weighing informational efficiency against market stability. For instance, more investor education in risk management can counterbalance the negative consequences of wider limits. Regulators ought to decide the best price limit level that suits the needs of the market based on the respective policy goals and ultimate objectives they pursue, paying attention to the effects of price limits on other consequences. This study finds that the easing of price limits will speed up information transmission and market risks, and hence the supervision unit needs to design the price limit system accurately and the following needs to be addressed: Firms of varying size and sectors have different reactions to price limit changes and therefore the competent authority should consider the implementation of a “dynamic price limit” system in order to establish tighter volatility ranges for highly volatile or systemically significant firms. (1) Since this article finds that the increase in price errors is serious, the competent authority needs to reinforce the real-time monitoring mechanism, that is, launching an AI risk early warning system to identify abnormal market fluctuations and strategic manipulation behaviors in real time. (2) Retail investors are more affected by the fluctuations in price, and the risk awareness of retail investors and their ability to receive material will need to be enhanced, and the changes in institutional shareholdings and trading behaviors need to be disclosed, etc. (3) Future system adjustment of the price system should come along with quantitative regulation tools and market behavior tracking indicators, and a rolling assessment of the effects of the system should be gradually set up in order to ensure the realization of system effects.

Future study directions are proposed as follows: (1) Investigating longer-term effects using longer dataset. (2) Examining cross-market variations to draw general conclusions. (3) Investigating the detailed effects on trading and portfolio diversification strategies. (4) Examining how investors’ behavior changes reflect to increased price limits, specifically trading strategies and risk attitudes

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Project supported by Zhaoqing University: ZD202404.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.