Abstract

This study matches the digital financial inclusion index with micro panel data from the China Household Finance Survey (CHFS) in 2015, 2017, and 2019, and explores the impact of digital finance on the return rate of entrepreneurship. The results show that the effect is positive—entrepreneurial households in prefectures with higher digital finance obtain higher return rates—and remarkably reliable to a battery of endogeneity and robustness tests. Mechanism analysis indicates that the positive effect of digital finance on the return rate of entrepreneurship is achieved mainly through facilitating external financing and reducing financial transaction costs. Further research finds that the spillover effect of digital finance has obvious Internet bias: the “digital dividend” only extends to the advantaged classes who have access to the Internet—non-rural and migrating rural entrepreneurs, but for non-migrating rural entrepreneurs generally facing digital exclusion, digital finance has little effect on their return rate. The empirical evidence presented in this study has important policy implications for accelerating the digital finance process, promoting high-quality entrepreneurship development, and boosting digital poverty groups to break stratum solidification.

Keywords

Introduction

Over the past 30 years of reform and opening-up, China has experienced sustained rapid economic growth and has become a veritable economic power. However, with the decline of the demographic dividend, the accumulation of risks of the “middle-income trap” and the profound adjustment of international economic patterns, China’s economic development has stopped high-speed growth and entered the stage of “normal growth” (Xie et al., 2018). At present, the promotion of the economic transition from extensive growth to intensive growth relying on innovation and entrepreneurship is a major issue facing China’s development. As an essential part of the supply-side structural reform in China, entrepreneurship can promote economic growth (Samila & Sorenson, 2011), create employment (Glaeser et al., 2010), optimize and upgrade the industrial structure (Yin et al., 2019), and inject new vitality into China’s economic transformation (Hu & Zhang, 2014; Kim & Li, 2014).

In addition to encouraging and supporting entrepreneurial participation, an important issue worth exploring is how to improve entrepreneurial returns. In particular, the coronavirus (COVID-19) pandemic has swept the world in recent years, negatively affecting China’s economy. Individual businesses and “small and medium-sized” entrepreneurial enterprises bear the brunt. Capital liquidity has gradually tightened, financial vulnerability has continued to worsen, and capital survival is facing unprecedented challenges. Thus, exploring ways to boost entrepreneurial vitality and improve entrepreneurial returns is of great practical significance.

Abundant literature discusses the driving factors of entrepreneurial behavior and performance, which can be divided into—macro and micro factors. From a micro spective, scholars have mainly analyzed the personal and family characteristics of entrepreneurs at the individual level, such as gender, life cycle, human capital, social networks, work experience, and risk preference (Lazear, 2004; Rosenthal & Strange, 2012; Roux et al., 2006). On the macro side, the literature mainly focuses on the social and economic environment in which entrepreneurial activities operate and discusses politics, economics, culture, technology, and other social backgrounds (Branstetter et al., 2014; Hopp & Stephan, 2012).

Finance is an essential component of an entrepreneurial environment. Traditional financial development theory is based mainly on the perspective of financial deepening (Beck et al., 2000) and emphasizes the promotion of financial aggregate and scale (Levine, 2005). However, traditional financial theory ignores the premise that people can freely access the financial services they need without being excluded by the financial system. In fact, there is a relatively severe financial exclusion for individual businesses and “small and medium-sized” entrepreneurial enterprises in China. Claessens and Perotti (2007) illustrated that unequal access to financial markets is a major barrier to boosting entrepreneurial vitality and greatly reduces the generation and development of entrepreneurial activity. An increasing number of scholars, such as Demirgüç-Kunt and Klapper (2013), Wei and Lin (2017), and X. Chen et al. (2018), have gradually realized that the promotion of financial development to entrepreneurial activities cannot simply rely on financial deepening but should also pay attention to financial broadening.

Relative to traditional finance, digital finance emphasizes the opportunity equality of residents’ access to financial services and the improvement in the breadth of financial services (Zhang et al., 2021). Digital finance refers to a new financial business model in which Internet companies combine with traditional financial institutions to realize loans and deposits, payments, investments, insurance, and other financial businesses through digital technology (Choi et al., 2014). This concept is similar to the “Fintech” mentioned by Allen et al. (2021). Intuitively, the difference is that the latter pays more attention to technological innovation, while the former is generally seen as Internet companies engaging in financial business, covering a wider range of areas. Regarding development goals, traditional finance focuses on mobilizing more social savings and improving the conversion rate from savings to investment (Levine, 2005). In contrast, the motivation of digital finance is to integrate all social classes and groups into the mainstream financial system, expand the benefit boundaries of financial resources (Gabor & Brooks, 2017), and provide inclusive financial services for socially disadvantaged groups at an affordable cost (Li et al., 2022). In recent years, China’s digital finance has developed rapidly, relying on the technological innovation of digital communication and the promotion and popularization of mobile terminal equipment (Yin et al., 2019). As a new financial model, digital finance significantly improves the availability of financial services and provides a broad space for the development of entrepreneurial enterprises.

Specifically, digital finance boosts entrepreneurial returns in two ways. First, digital finance alleviates liquidity constraints and provides entrepreneurs with credit support. Liquidity constraints are the main barriers to the development of start-up enterprises, especially in underdeveloped rural areas (Carpenter & Petersen, 2002). Traditional financial institutions are reluctant to lend to start-ups for two reasons. First, start-ups lack business records, which increases information asymmetry (Stiglitz & Weiss, 1981) and makes it difficult for financial institutions to identify their integrity. Second, start-ups are small scale, and it is difficult for traditional risk assessment models to achieve economic efficiency in terms of cost. In contrast, based on big data analysis, digital finance can conduct credit and risk assessments for start-ups at a lower cost (Aghion et al., 2007; Herzenstein et al., 2011), which greatly improves the possibility of financing for entrepreneurs. Furthermore, Duarte et al. (2012) proposed that digital finance platforms connect the demand and supply sides of capital, which may be geographically distant. Zhang and Jiang (2021), Zhang et al. (2021) illustrated that digital finance lowers the threshold of financial entry and improves the convenience of financial services. Moreover, digital finance has the feature of inclusiveness that traditional finance does not (Ahlin & Jiang, 2008; Karaivanov, 2012), which will help start-ups establish and develop by providing credit support at a lower cost and greater scope.

Second, digital finance can improve entrepreneurial returns by reducing financial transactions and information search costs. In contrast to traditional finance, digital finance can overcome distance constraints through the mobile Internet and realize mobile payment, transfer accounts, and other financial functions (Yin et al., 2019), which makes financial services more convenient (Shahrokhi, 2008) and dramatically reduces the financial transaction costs for entrepreneurial enterprises. What draws more attention is that digital technology itself is an important driver of business model innovation (Teece, 2010). As an effective medium for information exchange, digital financial platforms can deliver sufficient information (Zhou & Fang, 2018), helping entrepreneurs explore and grasp business opportunities (Zeng & Reinartz, 2003), realizing the optimal allocation of market resources and simultaneously reducing the cost of information search. For example, the popularity of digital financial platforms (e.g., Alipay and WeChat) has greatly improved the circulation speed and exchange efficiency of business information (Baden-Fuller & Haefliger, 2013; Nykvist, 2008) and has created many new entrepreneurial opportunities, such as e-commerce, online medical care, cloud education, and cloud training (Jack & Suri, 2014). In summary, digital finance enables consumers and merchants to complete online transactions, change the value delivery link of traditional business models, and reduce the cost of financial transactions and information searches for entrepreneurs.

Based on the above theoretical and realistic background analysis, this study attempts to answer the following questions. Can the development of digital finance improve the return rate of entrepreneurship? If so, what are the mechanisms underlying this impact? Is the spillover effect of digital finance the same for different entrepreneurial groups?

Compared with previous studies, this study contributes to the literature in three ways. First, we incorporate digital finance into entrepreneurs’ decision-making processes to provide a more comprehensive framework for understanding the impact of digital finance on entrepreneurial returns. Second, this study empirically discerns how digital finance affects entrepreneurial return rate by considering financial transaction costs, information search costs and credit support as intermediate variables. This study differs from previous studies that have discussed the relationship between digital finance and entrepreneurial participation by focusing on the role of digital finance in entrepreneurial returns. Although there is a general perception that digital finance promotes entrepreneurial behavior (Luo & Zeng, 2020; Xie et al., 2018), it is unclear whether and how digital finance affects entrepreneurial performance. Third, we discuss the role of digital finance for different entrepreneurial groups: “digital dividend” or “digital divide,” to explore whether the development of digital finance reinforces social stratification in the process of digitization. The distinction among the roles of non-rural households, migrating rural households, and non-migrant rural households allows us to offer new insights into this topic.

The remainder of this paper is organized as follows. Section 2 mathematically deduces digital finance’s effect on entrepreneurial returns. Section 3 introduces the study’s data, econometric models, and variables. Section 4 reports and analyzes the empirical results, including the baseline regression, endogeneity and robustness tests, and mechanism analysis. Section 5 discusses role differences in digital finance and their underlying reasons. Finally, Section 6 concludes the paper.

Theoretical Framework and Research Hypotheses

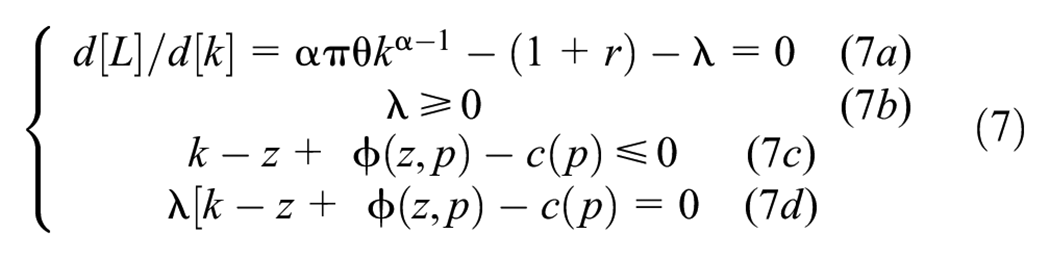

To better understand the mechanism and path of the effect of digital finance on the entrepreneurial return rate, following Evans and Jovanovic’s (1989) theoretical framework of optimal decision-making for entrepreneurship, this section incorporates digital finance into the cost and external financing functions and theoretically analyzes the impact of digital finance on entrepreneurial returns. For simplicity, we assume that if an individual is engaged in ordinary agricultural production or is employed, he can obtain a stable income w, but if he chooses to engage in self-employment, he can obtain business income y:

where π denotes the probability of successful entrepreneurship, k represents the original start-up funds, α reflects the capital-output elasticity coefficient (

In Equation (2), z is entrepreneur’s initial endowment.

where

If

Under the liquidity constraint, the maximization problem is equivalent to:

We introduce the Lagrange function and use the Lagrangian multiplier method to solve the optimization problem under inequality constraints.

Equation 7 outlines the KKT (Karush-Kuhn-Tucker) conditions. Equations 7b and 7c are the initial constraint conditions, and Equation 7d is the complementary slackness condition. According to Equation 7a, the optimal solution for the initial investment k can be expressed as:

When

According to the complementary slackness condition, the maximum initial investment is

Entrepreneurship becomes the rational choice of individuals only when the income from self-employment is greater than that from ordinary agricultural production or employment. That is, to satisfy:

Considering both financing-constrained and non-financing-constrained situations and substituting Equations 8 and 10 into Equation 1, the piecewise function of entrepreneurial income can be simplified as:

This study focuses on the impact of digital finance on entrepreneurial returns. Based on the above theoretical analysis, digital finance provides convenient financial services at an affordable cost, eases entrepreneurs’ credit restrictions, and greatly improves the availability of external financing. Due to:

Equation 13 indicates that the higher the level of digital finance, the larger the choice space entrepreneurs can have for the initial investment and the greater the possibility of choosing the optimal solution

This means that digital finance p cannot completely ease financing constraints. According to Equation 12, digital finance is still positively correlated with entrepreneurial income. Therefore, we propose the following hypotheses:

As mentioned, after considering digital finance, due to

This implies that the revenue function

In summary, on the one hand, entrepreneurs can seek business cooperation with other merchants or customers with the help of a digital financial platform, which reduces the cost of information search and realizes optimal allocation of market resources. On the other hand, by providing more convenient financial services, digital finance improves the efficiency of payment and transfer, reduces financial transaction costs, and further increases the return on entrepreneurship. Based on these theoretical deductions, we propose the following hypothesis:

Methods

Data

The data used in this study comes mainly from two sources: the Digital Financial Inclusion Index (DFI) and the China Household Finance Survey (CHFS) in 2015, 2017, and 2019. The date of the CHFS was collected by the authoritative survey institution: the Survey and Research Center for China Household Finance, Southwestern University of Finance and Economics. The sample sizes were 37,289 in 2015, 40,011 in 2017, and 34,643 in 2019, covering 355 counties across 29 provinces. The digital financial inclusion index is obtained from the Digital Finance Research Center of Peking University. This study focuses on the entrepreneurial returns of self-employed households. According to the household code, we selected only the entrepreneurial households interviewed in all three round surveys, removed some samples that missed key information in the questionnaire, and finally obtained 2,024 entrepreneurial households (the sample sizes in the three periods were 6,072 in total). Furthermore, we used DFI at the prefecture level and matched the two data sets according to the regional code as the panel data-set for the empirical test.

Model and Variables

This study uses a fixed-effects model with panel data to empirically examine the impact of digital finance on entrepreneurial returns. The baseline regression model was set as follows:

Where i and t represent the household and year, respectively.

Further, following the approach of R. M. Baron and Kenny (1986), we construct recursive models to test whether digital finance indirectly affects the entrepreneurial return rate through the intermediary variable M. The recursive models were as follows:

where

Entrepreneurial return rate is the main variable explained in this study. The questionnaire of CHFS directly asks “whether your family is engaged in self-employment,”“total investment in entrepreneurial projects,” and “annual after-tax income of entrepreneurial projects.” Following the approach of Chai (2017), we limit the sample to those engaged in self-employment and use the ratio of annual after-tax income to total investment as a proxy variable for the entrepreneurial return rate. The total investment in the CHFS questionnaire includes shops, cash deposits, inventories, office equipment, machinery, and transportation equipment, but excludes the value of their own housing, which may be used in these projects. Moreover, to verify the robustness of the empirical conclusion, we also use “whether the project is profitable” and “the amount of profit” to reflect the entrepreneurial returns in the following analysis.

Table 1 reports the basic profit status of China’s sample households with entrepreneurship in 2015, 2017, and 2019. Overall, rural households have a lower scale of investment and profit in entrepreneurial projects than urban households, but the ratio of profitable households and the return rate are significantly higher. This result is consistent with the standard capital market theory and verifies the law of diminishing the marginal efficiency of capital, which is common in the investment market. For example, street vendors often have higher return rate than average businesses. In general, rural households are more inclined to operate on shoestrings and participate in more direct labor in the entrepreneurial process, which may lead to a higher return rate of entrepreneurship.

The Profit Status on Entrepreneurial Households in China.

Note. The ratio of profit household is the proportion of households with after-tax income of entrepreneurial projects greater than 0 to total entrepreneurial households; the return rate is the ratio of after-tax income to total investment.

The core explanatory variable (digital finance) of this study comes from the “digital financial inclusion index (DFI),” which is compiled by the Digital Financial Research Center of Peking University. The DFI uses Ant Group’s Alipay transaction account information in China, including various digital businesses, such as payment, investment, credit, insurance, and funds. Data from the Ant Group show that Alipay covers more than half of China’s population and occupies the largest share in the area of mobile payment in China (Guo et al., 2020). Thus, the DFI index can comprehensively measure the popularity and development level of digital finance in various regions of China and has been adopted by an increasing number of scholars, such as Xie et al. (2018), He and Li (2019), and Ma and Hu (2022).

We selected prefecture-level data of DFI in 2014, 2016, and 2018, including the total index and its three sub-dimensions: coverage breadth (CBI), use depth (UDI), and degree of digital support services (DSSI). The advantages of using the previous year’s data in the DFI index are as follows. First, the economic and social effects caused by digital finance are lagged. Second, the entrepreneurial activities of the current period usually do not affect the level of financial digitalization in the previous period, and the predetermined variables are useful for reducing reverse causality.

Control Variables

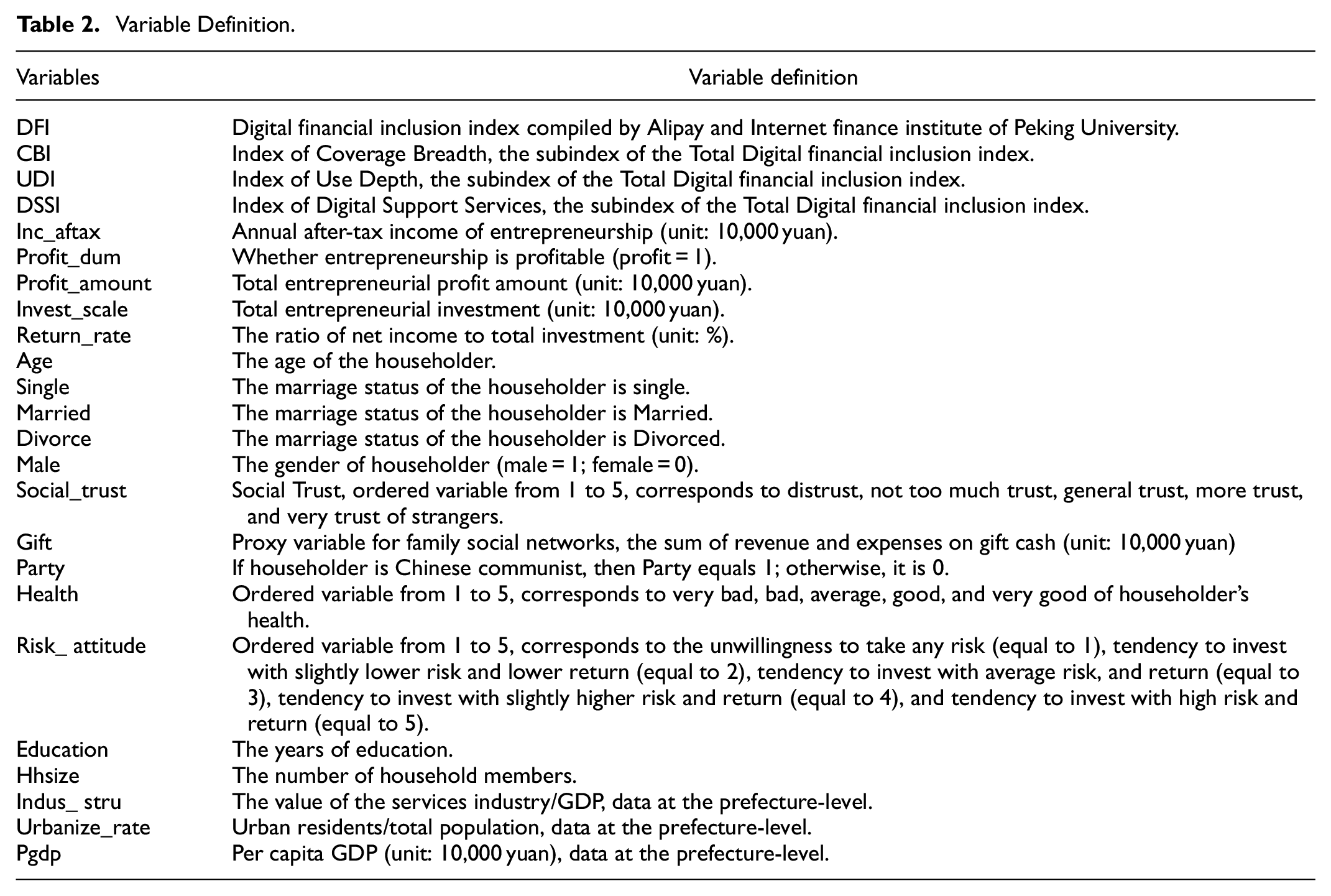

According to the previous literature (Chai, 2017; Xie et al., 2018), control variables that may affect the entrepreneurial return rate are classified into three groups: (1) variables at the individual level, which include gender, age, age squared, political identity, social trust, health status, risk attitude, and education; (2) variables at the household level, including household social networks and household size; and (3) regional economic variables, including the urbanization rate, per capita GDP, and the proportion of tertiary industry. Table 2 provides the definitions of the main variables and Table 3 reports the summary statistics.

Variable Definition.

Descriptive Statistics.

The results in Column (3) of Table 3 show that the average total investment of the sample families engaged in self-employment is 658,000 yuan, the average annual after-tax income is 68,400 yuan, the average return rate of entrepreneurship is 12.43%, more than 83% of the families are profitable, and the average profit is 72,800 yuan. Compared with the means, the medians of the investment scale, annual after-tax income, entrepreneurial return rate, and profit amount are all significantly smaller, and the standard errors of after-tax income and return rate of entrepreneurship are close to three and two times the mean, respectively. This finding indicates that the profit statuses of entrepreneurial households are highly divergent.

Empirical Results and Analysis

Baseline Analysis

Table 4 reports the baseline regression results. Column (1) shows that the coefficient of LnDFI is positive and significant at the 1% level, implying that the development of digital finance plays a vital role in local entrepreneurial practice and improves the operating efficiency of entrepreneurship to some extent, in accordance with the theoretical expectation of Duarte et al. (2012), Zhou and Fang (2018), and Yin et al. (2019). Concretely, every 10% increase in digital finance improves the return rate of entrepreneurship by approximately 0.32%. Considering that the developmental level of China’s digital finance is changing within a relatively large span in recent years, it can be inferred that this is a considerable spillover effect. In Columns (2), (3), and (4) of Table 4, DFI is replaced by the natural logarithm of three sub-indexes: CBI, UDI, and DSSI, respectively. As seen, the use depth and the degree of digital support services positively and significantly affect the entrepreneurial return rate, with marginal contributions of 4.46% and 1.52%, while the effect of coverage breadth is insignificant.

The Impact of Digital Finance on Entrepreneurial Return Rate: Baseline Estimate.

Note. Robust standard errors are shown in parentheses. Other control variables refer to variables with insignificant or unrobust results, including Male, Divorce, Hhsize, Indus_ stru, and Pgdp, which are not reported due to length limitations.

p < .01. **p < .05. *p < .10.

In fact, the index of coverage breadth (CBI) is measured according to the number of registered Alipay users and their bank card binding (Guo et al., 2020). It costs almost nothing to register an e-account, and the acts of registering and binding bank cards do not mean that people actually use the services provided by digital financial platforms. Therefore, there is no direct correlation between the level of coverage breadth and the return rate of local households’ entrepreneurship. In contrast, the index of use depth (UDI) and degree of digital support services (DSSI) are reflected by the facilitation of mobile payments, reduction of financial service costs, and an increase in digital financial transaction frequency (Yin et al., 2019). The relaxation of financial credit access restrictions, reduction of transaction costs, and facilitation of financial services can help people carry out entrepreneurial activities more effectively, which is conducive to obtaining higher return rates for entrepreneurs.

In addition to digital finance, householder and family characteristics significantly affect the return rate of entrepreneurship. Columns (1), (2), (3), and (4) of Table 4 report four sets of regression results for the other explanatory variables, while controlling for different digital financial indices. Concretely, when other factors remain the same, the householder changes from single to married, from non-Communist Party members to Communist Party members, risk appetite increases by one unit, years of education increases by 1 year, health status increases by one unit, the sum of revenue and expenses of family gift cash increases by 10%, and social trust increases by one unit, the return rate of entrepreneurship increases by at least 2.12%, 3.68%, 2.23%, 0.81%, 0.42%, 1.26%, and 0.69%, respectively. The enhancement effect of urbanization on the entrepreneurial return rate was approximately 0.11 to 0.16. The age of the householder has an inverted U-shaped effect on the return rate, with a turning point between 31 and 38 years.

These results are generally consistent with the theoretical explanations provided in the literature. The conclusion of marriage brings more extensive business information channels and provides entrepreneurs with more assets or wealth guarantee certificates, which can improve their ability to resist external uncertain risk impacts (del Río & Young, 2008). Families with party members and more gift cash tend to have more extensive social networks or clan networks (R. A. Baron, 2004; Chai et al., 2019), contributing to the effective operation of entrepreneurial activities and increasing their return rates. Education level improves entrepreneurs’ ability to seize business opportunities and identify and avoid market risks, thereby promoting entrepreneurs to obtain higher return rates. The impact of householder’s age on entrepreneurial returns is dynamic, caused by periodic fluctuations in individual risk attitudes and cognitive ability with changes in age (Fabbri & Padula, 2004). Improving health status, risk attitude, and social trust can promote people’s optimistic expectations of uncertain future prospect (Rosen & Wu, 2004), making individuals more willing to bear the costs and risks of entrepreneurship to obtain a higher risk premium.

Endogeneity and Robustness Test

From the perspective of empirical methods, there may be an endogenous bias in the above estimates. First, self-employment activities may stimulate entrepreneurs’ demand for financial services, such as mobile payments and digital credit, while the widespread use of digital financial tools (e.g., Alipay) helps promote the development process of local digital finance. Second, there may have been missing variables. Residents’ entrepreneurial vitality and local digital financial development may be jointly affected by the social environment, social interaction, or behavioral habitus, which are not observable. Referring to the idea of Zhang et al. (2021), we used the geographic information system (GIS) to calculate the average spherical distance from the sampled city to the provincial capitals, Beijing, and Hangzhou as instrumental variable (IV).

The reasons for using IV are as follows. First, geography affects the development of digital finance. The more remote a household is geographically located, the more difficult it is for the government to popularize digital finance. Second, Alipay, a typical representative of digital finance, belongs to Ant Financial and originated in Hangzhou. As national and regional economic centers, Beijing and provincial capitals are not only cities with relatively higher financial digitalization, but also the radiation starting point of the in-depth promotion of digital finance. Therefore, it can be expected that the closer the sample locations are to the provincial capitals, Beijing and Hangzhou, the higher digital finance will develop. Third, geographical distance exists naturally for a long time and is not easily affected by the economic behavior of specific households; therefore, it has good exogeneity.

Table 5 reports the results of the first and second stages of instrument variable regressions based on distance IV. The former (Column (2)) shows that LnDFI is significantly negatively correlated with distance IV, which conforms to the expectation. The latter (Column (4)) indicates that the p-value of the Wald test is .0748, rejecting the null hypothesis “

The Impact of Digital Finance on the Return Rate: Instrumental Variable Regression.

Note. Robust standard errors are shown in parentheses.

p < .01. **p < .05.

Another way to solve the endogeneity problem is to adopt the first-difference model, which estimates the impact of changes in digital finance (LnDFI) on the difference in entrepreneurial return rate (Return_rate). The advantages of this approach are as follows: (1) unobservable trend variables in the time dimension can be “differentiated”; (2) some time-invariant disturbance factors can be filtered out, which greatly reduces estimation bias caused by omitted variables and measurement errors in the model.

Table 6 presents the regression results for the first-difference model. Column (1) shows the regression result of ΔLnDFI, consistent with the baseline results in Table 4. Columns (2), (3), and (4) report the regression results of the three sub-indices: coverage breadth (ΔLnCBI), use depth (ΔLnUDI), and degree of digital support services (ΔLnDSSI). The change in the econometric model does not affect the basic conclusions of this study; the impact of coverage breadth is still insignificant, whereas the coefficients of use depth and the degree of digital support services are positive and significant. This means that greater digitization of financial services will help local entrepreneurs achieve higher returns.

The Impact of Digital Finance on the Return Rate: First-Difference Regression.

Note. Robust standard errors are shown in parentheses.

p < .01. **p < .05.

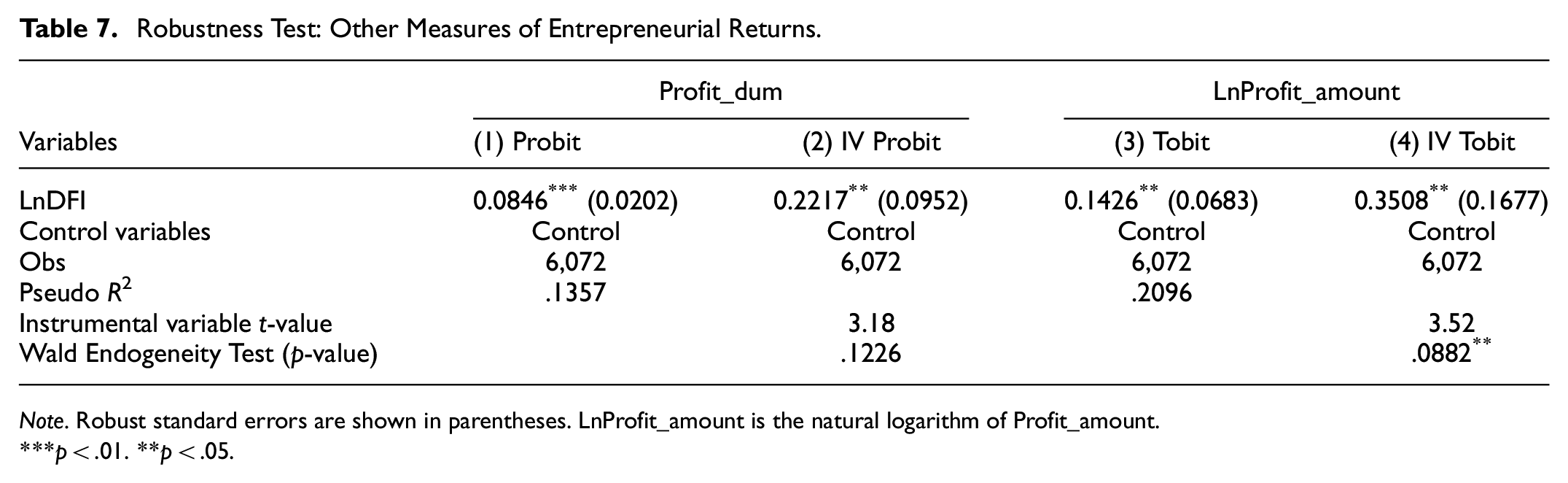

In terms of robustness tests, this study verified the impact of LnDFI on entrepreneurial return rates from two perspectives. In addition to the after-tax income of entrepreneurial projects, the questionnaire of CHFS also asked “whether the project is profitable” and “the amount of profit.” Considering that “whether the project is profitable” is a binary attribute variable. We use Probit and IV Probit models to conduct the regression. Columns (1) and (2) of Table 7 show that when digital finance increases by 10%, the possibility of achieving profit in self-employment increases by approximately 0.85% (baseline effect estimation) and 2.22% (baseline effect + IV estimation), and the coefficients of LnDFI are statistically significant at the 1% and 5% level, respectively.

Robustness Test: Other Measures of Entrepreneurial Returns.

Note. Robust standard errors are shown in parentheses. LnProfit_amount is the natural logarithm of Profit_amount.

p < .01. **p < .05.

Further, we use “the amount of profit” instead of “whether the project is profitable,” columns (3) and (4) of Table 7 report the results. Digital finance still has a positive effect. The marginal contributions of LnDFI to profit are 0.143 (baseline effect estimation) and 0.351 (baseline effect + IV estimation), and both are significant at the 5% level. The amplitude of promotion is considerable, which further verifies Hypothesis 1: The development of digital finance improves the entrepreneurial environment and plays a positive role in the practice of local resident entrepreneurship.

Digital Finance and Entrepreneurial Return Rate: Mechanism Analysis

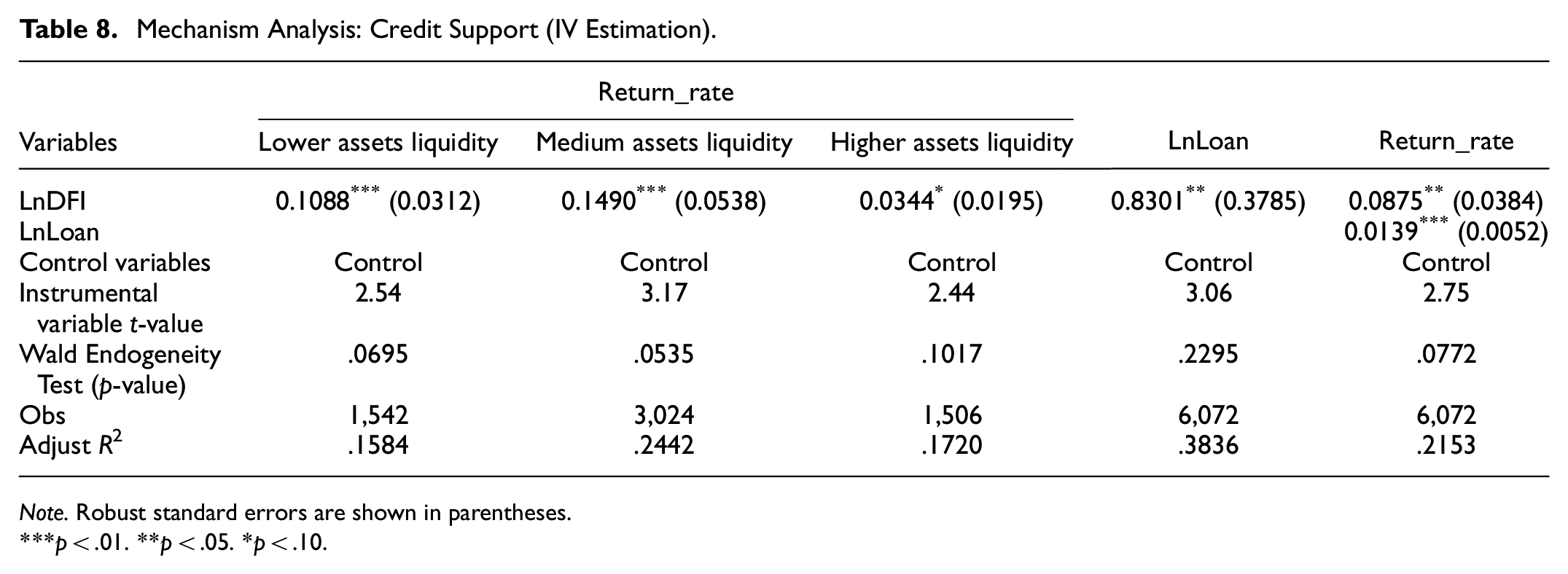

Theoretically, digital finance can improve the return rate of entrepreneurship by improving the availability of external financing and reducing the costs of financial transaction and information search. To verify the credit support mechanism of digital finance, we divide the sample into three groups according to households’ liquid assets: lower asset liquidity (with quantiles below 25%), medium asset liquidity (with quantiles between 25% and 75%), and higher asset liquidity (with quantiles above 75%). The logic is that the fewer liquid assets entrepreneurs have, the more they rely on external financing to address their liquidity constraints. If the credit support mechanism is true, then for entrepreneurs with different asset liquidity levels, the impact of digital finance is heterogeneous: the lower the asset liquidity, the greater the boost effect of digital finance.

Columns (1), (2), and (3) of Table 8 are the subsample regression results for households with lower, medium, and higher asset liquidity, respectively. Digital finance significantly improves all return rates of entrepreneurship in the three sub samples. However, compared with households with higher asset liquidity, the marginal coefficients of households with lower and medium asset liquidity are 7.44% and 11.46% higher, respectively, and are more significant, consistent with expectations.

Mechanism Analysis: Credit Support (IV Estimation).

Note. Robust standard errors are shown in parentheses.

p < .01. **p < .05. *p < .10.

Notably, the diverse effects of digital finance on return rates with different asset liquidities are not sufficient to confirm the existence of a credit support mechanism. First, the correlation between household credit behavior and asset liquidity may not be strong. Second, even if families face liquidity constraints in entrepreneurship, people in China’s unique rural society are more likely to borrow from relatives and friends, not necessarily through digital financing. Therefore, we select a more direct indicator, “the amount of loan,” to further demonstrate whether the path of “digital finance → credit support → entrepreneurial returns” is established.

The sources of borrowing are limited to the bank or non-bank financial institutions (owing to the limitations of the CHFS data, we cannot accurately identify the borrowings from digital financial platforms), excluding the borrowing of relatives, friends, and other private informal borrowings. Columns (4) and (5) in Table 8 show that digital finance has significantly increased entrepreneurs’ loan amounts and that loans from banks or non-bank financial institutions help entrepreneurs obtain higher return rates. Furthermore, compared with Table 4, the marginal effect of digital finance is weakened after considering the intermediary variable “loan amount.” This finding strongly supports Hypothesis 2a: Digital finance can improve the availability of external financing and elevate the return rate of entrepreneurship by alleviating liquidity constraints.

Hypothesis 2b proposes that digital finance reduces costs (including information search and financial transaction costs) necessary in the entrepreneurship process, elevating the entrepreneurial return rate. Theoretically, in contrast to traditional finance, digital finance can overcome distance constraints through the mobile Internet and realize mobile payment, transfer accounts, and other financial functions (Yin et al., 2019), greatly reducing financial transaction costs for entrepreneurs. In this case, entrepreneurs with relatively scarce traditional financial resources or remote locations from bank branches will rely more on the convenient financial services provided by digital financial platforms; thus, the positive effect of digital finance on the entrepreneurial return rate will be relatively large.

According to the time spent for respondents to reach the nearest bank branch, the samples are divided into two sub-samples: “less than 30 min” and “over 30 min.” Columns (1) and (2) in Table 9 show that when the time spent by entrepreneurs is more than 30 min, digital finance improves the return rate of entrepreneurship, with a marginal contribution of 0.163 at the 1% level; in contrast, for communities or villages with more abundant traditional financial services (the time is less than 30 min), digital finance has little effect on the return rate of local entrepreneurship. These results verify that digital finance affects entrepreneurial returns by reducing financial transaction costs.

Mechanism Analysis: Cost Reduction (IV Estimation).

Note. Robust standard errors are shown in parentheses.

p < .01. **p < .05.

In addition, digital finance can rely on digital platforms to deliver adequate information and reduce information search costs by connecting individuals with different resources and demands, thereby increasing the return rate of entrepreneurship. The CHFS questionnaire does not provide direct indicators of whether digital finance reduces the costs of information search but asks the respondents about the importance of using TV, Internet, newspapers or magazines, radio, telephone messages, and others’ notifications as information channels, respectively, which can indirectly reflect whether digital finance stimulates people to use the Internet to transmit or receive market information to some extent. The indicator of information channels was assigned from 1 to 5, corresponding to very not important, not important, general, relatively important, and very important, respectively. Based on the issues discussed in this study, we chose the importance of the Internet as an intermediary variable. Theoretically, the development of digital finance will encourage local entrepreneurs to use the Internet as an information carrier, and the widespread use of the Internet as an information channel can greatly improve the speed and depth of information spread, which will help increase the entrepreneurial return rate.

Based on this logic, following the mediating effect model (R. M. Baron & Kenny, 1986), this section first tests the effect of digital finance on the importance of the Internet as an information channel and then introduces the mediating variable into the determining equation of entrepreneurial returns to observe the change in the estimated coefficient of LnDFI. Columns (4) and (5) in Table 9 show that digital finance significantly increases the importance of the Internet as an information channel for local entrepreneurs. Unfortunately, the intermediary variable is statistically correlated with the return rate of entrepreneurship, and compared with Column (3) in Table 9, the intermediary variable does not significantly reduce the effect of digital finance on the entrepreneurial return rate. This finding implies that a mechanism for reducing information search costs has not yet been approved. This also reflects, to some extent, that the intermediary information services have not yet been fully developed in China’s digital financial system and that its function of transmitting complete information still needs to be strengthened.

Further Discussion: “Digital Dividend” or “Digital Divide”

Whether the continual advancement of digital finance will breed another opportunity inequality between the rich and the poor—the “digital divide,” exacerbate social stratification and widen the existing social gap, or will it provide more convenient financial services for small farmer entrepreneurs, help disadvantaged classes to share “digital dividend,” and promote inclusive economic growth? There are significant controversies regarding the group bias effect of digital finance in the process of informatization. Some scholars, such as Bonfadelli (2002) and Britz and Blignaut (2001), emphasized that the rapid development of digital finance benefits only those superior classes proficient in digital technology. Consequently, the resources and opportunities that disadvantaged groups might have been crowded out or deprived of, resulting in the further expansion of social inequality. However, other scholars held, different from the “elite capture” of traditional finance, the original motivation and goal of digital finance in China were to eliminate the nobility attribute of financial services and lower the entry threshold (Guo et al., 2020), which would have a more profound impact on those disadvantaged groups who have been excluded from traditional finance for a long time (Zhang et al., 2021).

In this section, the samples are divided into three groups according to the registration of households: non-rural households, migrating rural households, and non-migrant rural households, and the diverse impacts of digital finance on the return rate of entrepreneurship for different social groups are explored. The regression results are shown in Table 10, where (1), (2), and (3) are listed as baseline effect estimates, and (4), (5), and (6) are listed as IV estimates for the instrumental variable. The results of the baseline regression confirm that digital finance significantly affects only the entrepreneurial return rates of non-rural and migrating rural households, with marginal contributions of 8.73% and 1.91%, respectively. The IV estimates also show that “digital dividend” in entrepreneurial activities only extends to non- rural households and migrating rural households. Digital finance does not significantly improve the return rate of non-migrating rural entrepreneurs. From this perspective, the development of digital finance may exacerbate (rather than narrow) the existing urban-rural gap.

Digital Finance and the Return Rate: Heterogeneous Impact for Social Classes.

Note. Robust standard errors are shown in parentheses.

p < .01. **p < .05. *p < .10.

The above analyses illustrate that digital finance can significantly improve the entrepreneurial return rate. However, this causality is limited to non-rural and migrating rural households, which is inconsistent with the predictions of Guo et al. (2020) and Zhang et al. (2021). The underlying reason may be that there is a precondition for digital finance to work: people must have access to the Internet; otherwise, they cannot enjoy the convenient and effective financial products and services provided by digital finance. Restricted by family endowment, cognitive ability, and digital literacy, this part of “digital poor” groups are mainly composed of non-migrating rural households, which results in the structural bias of “digital dividend” among different social groups. The CHFS data show that in the sample of entrepreneurial families, 47.9% of non-migrating rural households have no access to the Internet, while for non-rural households and migrating rural households, the proportions are only 18.7% and 15.4%, respectively. Regarding the distribution of households that do not have Internet access, non- rural households account for 28.1%, migrating rural households account for 7.9%, while non-migrating rural households account for 64.0%.

Based on this logic, this section further conducts subsample regression for the impact of digital finance according to “whether to use the Internet” in the questionnaire of CHFS. Considering that the Internet use status of some households changed between 2015 and 2019, to avoid possible estimation bias, we restricted the sample to those who always used or never used the Internet in the three surveys conducted in 2015, 2017, and 2019. Table 11 shows that, regardless of the OLS or 2SLS estimation, for entrepreneurs with access to the Internet, the positive effect of digital finance on the return rate always holds, and is significant at the 1% level.

The Impact of Digital Finance on the Return Rate: Inequality and Digital Divide.

Note. Robust standard errors are shown in parentheses.

p < .01. **p < .05. *p < .10.

However, for entrepreneurs who do not have access to the Internet, digital finance reduces (rather than elevates) its return rate. This also confirms that due to the “digital divide,” the spillover effect of digital finance appears the Internet bias, which has little effect on the return rate for non-migrant rural entrepreneurs with “digital exclusion.” From the perspective of structuralism (Britz & Blignaut, 2001), the overall development of digital finance may not break the original pattern of social stratification. The key to narrowing the inequality of the “digital dividend” is to promote the structural layout of the “digital countryside,” enhance the digital participation of vulnerable groups, and bridge the gap of “digital literacy.”

Conclusions

Activating entrepreneurship and boosting entrepreneurial returns are important ways of stimulating high-quality economic development. Using matched data from the Digital Financial Inclusion Index and the CHFS for 2015, 2017, and 2019, this study theoretically and empirically explores the impact of digital finance on entrepreneurial returns. The results show that digital finance plays a positive role in entrepreneurial practices and significantly improves the return rate of entrepreneurship. Among the sub-indexes, the entrepreneurial return rate was mainly affected by the depth of use and degree of digital support services, while as the coverage breadth effect was insignificant. The mechanism analysis shows that digital finance improves the return rate of entrepreneurship mainly by facilitating external financing and reducing financial transaction costs; however, the mechanism of information transmission has not been established. Further research finds that different social classes enjoy “digital dividends” unequally—non-rural and migrating rural entrepreneurs are major beneficiaries; in contrast, digital finance has little effect on the return rate for non-migrating rural entrepreneurs.

The policy implications of these findings are as follow. First, we should continue to promote the development of digital finance, particularly by enhancing the depth of digital finance use and improving the level of digital support services. Digital financial platforms should further explore the functions of digital finance on credit, mobile payment, and investment and strengthen its spillover effect in terms of stimulating residents’ participation in entrepreneurship and enhancing entrepreneurial benefits.

Second, in the integration of digital finance with other industries in society, some functions (such as resource sharing and information transmission) have not yet fully functioned. The role of digital finance needs to be strengthened to generate and aggregate various innovation factors, drive the exchange of business information, and promote the optimal allocation of market resources.

Third, digital finance has a structural bias toward different social classes. In entrepreneurial practice, only the advantaged classes proficient in digital technology can benefit from digital finance, which leads to crowding out and deprivation of the resources and opportunities that disadvantaged groups might have and further exacerbates social inequality. Therefore, in the process of the in-depth promotion of digital finance, we should focus on bridging the “digital literacy gap” among small farmer entrepreneurs and boosting digital poverty groups to break the class solidification.

Owing to date limitations, we dicuss only three mechanisms: financial transaction costs, information search costs, and credit support. There may be other ways, especially subjective factors such as fairness perception, psychological preference, and optimistic expectations, by which digital finance affects the entrepreneurial return rate. Moreover, households in the same prefecture had the same level of digital finance in our empirical analysis. Nevertheless, even within the same prefecture, the use of digital finance may vary widely among households. Thus, future studies should explore the measure of digital finance at the household level and its microcosmic effects.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by the National Social Science Foundation of China (23BGL205), Social Science Foundation of Henan, China (2022BJJ071), Soft Science Project of Henan, China (222400410143), Major Project of Philosophy and Social Sciences in Universities of Henan, China (2022YYZD12), and Basic and Applied Research Foundation of Guangdong, China (2022A1515010998).