Abstract

Financial integration creates complexities in risk transmission across commodities, currencies and equities, fuelled by non-immediate information systems, with implications for commodity-dependent nations during crises. Accordingly, this study analyses the time- and frequency-based connectedness between commodities, pressure currencies and equities in commodity-dependent sub-Saharan African states, including Botswana, Ghana, Kenya and Namibia. The study emphasised commodities that contribute immensely to the export revenues of the sample countries, including agricultural (cocoa, coffee, corn and cotton) and IDMs (aluminium, copper, nickel and zinc), spanning from January 2012 to December 2022. Through the Barunik and Křehlík index (BK-18), we revealed varying risk transmissions among the sample markets, with the long-term branded as the period of contagion given the multitude of bidirectional transmissions of shocks among these markets. The time-varying parameter vector autoregression (TVP-VAR) approach further complemented these results with contagion observed during the pandemic, nickel crash, pressure-currency era, as well as the Russia-Ukraine conflict. The results highlight commodities and currencies as net transmitters of shocks, while the sampled equity market served as shock receivers, with few exceptions and these were further substantiated by the TVP-VAR and the nonlinear causality test. The study has uncovered significant implications for policy-making, portfolio diversification strategies and risk management approaches. It is recommended that the central banks of the sample economies implement robust risk management policies that consider these interlinkages and diversify the economy with innovative sectors to reduce the region’s susceptibility to commodity and currency shocks and enhance equity market development.

Keywords

Introduction

The stock market serves as a measure of a nation’s economic well-being, with commodity price movement facilitating this growth (Jacobsen et al., 2019), while integration creates complexities in risk transmissions, fuelled by non-immediate information from the currency market (Sokhanvar & Bouri, 2023). Zankawah and Stewart (2020) asserted that these within sub-Saharan African (SSA) are contingent on market resilience, since their economies and equity markets (EQMs) heavily rely on metals and agricultural components (AGRC) for foreign exchange, exposing them to shocks. For instance, the commodity statistical analyses as delineated in studies (Bianchi et al., 2020; Woode, Idun, & Kawor, 2024) anticipated the global commodity markets to reach $131.3 trillion by 2024 and $139.3 trillion by 2028, with copper ($183 billion), aluminium ($153 billion), nickel ($69 billion) and zinc ($31 billion) being the most traded in SSA EQMs. United Nations Conference on Trade and Development's (2022) further emphasised a notable upsurge in global AGRC trade, from $1.1 trillion to $3 trillion between 1990 and 2020, with the escalating prices of cocoa, coffee, corn and cotton of essence to the EQMs, given their usefulness in the production process of most firms in SSA, as highlighted by studies (Bianchi et al., 2020; Woode, Idun, & Kawor, 2024), which motivates their emphasis in this study.

Despite these growth prospects, the industrial metal (IDM) market underwent upheaval, giving rise to an upsurge in investor sentiment (Koh & Baffes, 2022; Woode, Junior, & Adam, 2024). Thus, nickel witnessed a daily surge of 250% on March 8, soaring from $30,000 to $100,000 and subsequently tumbling to $48,048. This abrupt volatility plunged the industry into disarray, incurring losses in billions of dollars for traders who misjudged the market. Aluminium fluctuated from $4,000 to $2,500, while zinc moved from $4,499.5 to $2,931.4 between March and June. This upheaval was likened to the Great Recession, as reported by Burton (2022), leading the exchange suspending trade for the first time in three decades. Against this backdrop, EQMs in SSA with firms that largely depend on IDM, including the Ghana Stock Exchange (GSE, 2022), reported a decline in the composite (financial) index, amounting to 12.38% (4.61%). Meanwhile, the Botswana Stock Exchange (BSE, 2022) revealed a downturn in the capitalisation and trading value of the mineral sector, totalling 3 million and 638.4 million. This was corroborated by the Nairobi Stock Exchange (NSE, 2022), with a substantial decline of 31% (10.74%) in turnover (composite index) due to reduced trading, leading to 72 million revenue decline. Similarly, the composite index of the Namibian EQM experienced a decline of 5%. Woode, Adam, Owusu Junior, and Idun (2024) tinted the role of the extractive industry, which comprises 23% of the top 100 listed firms in SSA, thereby exposing their EQMs to shocks. In contrast, the prices of most AGRC traded within SSA EQM saw a surge, with the consequent fear gripping the domestic markets (Woode, Idun, & Kawor, 2024). Nonetheless, Organisation for Economic Cooperation and Development (OECD, 2021) has divulged that global risk-driven price pressures is foreseen to augment export earnings of commodity-reliant nations, exerting a favourable impact on domestic currencies. Contrary, the International Monetary Fund (IMF, 2023) disclosed currency depreciation in excess of the 20% threshold, where the Ghanaian Cedis (GHS), Botswanan Pula (BSP), Kenyan Shilling (KSH) and the Namibian dollar (NAD) depreciated by 31%, 25%, 22.3% and 20.3%, respectively, revealing structural challenges at the height of fluctuations.

Despite these challenges and the growing pact between SSA and global markets, studies on commodities, exchange rates (EXCR) and EQMs in the SSA context are narrow in scope, with most emphasis on crude oil and precious metals, as evident by studies (Agyei & Bossman, 2023; Ogbulu, 2018; Oyelami & Yinusa, 2019; Zankawah & Stewart, 2020). Also, most of these studies neglected the sample AGRC and IDM, despite the dependence of these markets on them (see Woode, Adam, Owusu Junior, & Idun, 2024; Woode, Idun, & Kawor, 2024). Subject to the immediate assertion and limitations, the current study examines the connectedness among IDMs (aluminium, copper, nickel and zinc), AGRC (cocoa, coffee, corn and cotton), EXCR (BSP, GHS, KSH and NAD) and equities (BSE, GSE, NSE and NASE) in commodity-dependent SSAs that remain net exporters of these commodities and also susceptible to EXCR shocks during crises. Considering the diverse nature of market participants and the constraints in the static models employed in studies (Adi et al., 2022; Oyelami & Yinusa, 2019; Zankawah & Stewart, 2020), we used the Barunik and Křehlík spillover index (BK-18) as well as the TVP-VAR to capture both the static and dynamic connectedness among these markets based on the model’s superiority (Asafo-Adjei et al., 2024; Owusu Junior et al., 2022; Woode, Owusu Junior, Idun, Kawor, et al., 2024). We complement these results with the Diks and Panchenko causality test due to the limitations of the spillover connectedness and the non-linear nature of the dataset.

This study departs from previous research in three significant ways: We complement existing knowledge by looking into how SSA EQMs from net exporters of the sample commodities respond to shocks from these markets. Unlike previous studies, we incorporate diverse dynamics in AGRC and IDMs through an assessment of their connectedness and ability to transmit shocks into the equity and currency markets in a comparative analysis. This approach unveils their distinct impact, spurred by the recent upheaval in the metal industry, coinciding with surge in AGRC prices. Second, our focus on commodities which account for a significant portion of these SSA’s earnings provides evidence that aids asset allocation. Finally, the use of both frequency and time-varying analysis proves efficient in analysing this connectedness. Per studies (Asafo-Adjei et al., 2024; Baruník & Křehlík, 2018; Opoku et al., 2023; Owusu Junior et al., 2022), these models’ superiority lies in their ability to account for systemic dependence and transmission among markets while also uncovering significant transmitters and receivers of shocks. Therefore, assessments of the connectedness among the sampled markets are equally pertinent given the vulnerabilities of these economies to shocks, commodity financialization and EQM equalisation.

Our analysis divulged weak interconnections and risk transmissions in the short and medium terms, while the long-term was characterised by frequent bidirectional transmissions with the TVP-VAR results complementing the BK-18, especially in the long-term with contagion observed during the pandemic, nickel crash, pressure-currency era, as well as the period of political conflict. The results highlight commodities and currencies as net transmitters of shocks, while the sampled EQMs served as receivers, with few exceptions, substantiated by the TVP-VAR and causality test. Our study contradicts the findings of prior studies (Asafo-Adjei et al., 2024; Bossman et al., 2022; Opoku et al., 2023; Owusu Junior et al., 2020) regarding the prevalence of short-term risk in most global markets. Additionally, the weak risk transmission and enduring characteristics discovered in the short and intermediate frames unveiled the limited susceptibility of SSA markets to external shocks. The outcomes were corroborated by the Diks and Panchenko causality test, which revealed commodities and currencies as the driving forces behind equities across various horizons.

The findings impart insight to the literature and policies, clarifying their influence on currency and EQM resilience. We unveiled a distinctive pattern for SSA markets, emphasising the unique dynamics, which are resistant to shocks. This nuanced comprehension deviates from global trends and suggests diversification for investors. The results contradict the conventional view of long-term stability, offering fresh insights into the temporal facets of risk transmission and the potential for implementing measures to address these shocks. By identifying commodities and SSA currencies as shock transmitters and equities as recipients, the study refines the understanding of inter-asset links within SSA, facilitating more targeted hedging strategies during turmoil. The disclosure that SSA markets display unique risk transmission patterns can attract investors seeking diversification, with the relatively lower susceptibility of these markets to short-term shocks positioning SSA as a more appealing investment destination, thereby encouraging capital inflows and promoting growth. Understanding the role of commodities and currencies in risk transmission enables economic planners, including equity and central bank regulators, to devise strategies that enhance resilience, thus bolstering overall stability. These contributions not only augment our theoretical comprehension but also bear practical implications for policymakers and investors navigating the complexities in commodity and currency markets to drive SSA equities.

The remaining paper is as follows: the second section is a literature review. The third section is about the methodology that describes the research data and sample, variables measurement, pre-estimation data analysis and econometric model. The fourth section discusses the results from the estimation models. The last section christened Conclusions provides concluding remarks.

Literature Review

This section highlights the discussion of theoretical explanations for the connection among commodities, equities and EXCR and delves into studies that confirm these theories.

Theoretical Background

In line with the stock valuation viewpoint, fluxes in raw material prices result in fluctuating product costs, which affect revenue and stock yields available to investors (Enwereuzoh et al., 2021). A similar transmission occurs when investors crowd out their investment from a country or firm due to fluctuating returns during currency fluctuations. Thus, commodity prices determine the movements of the EXCR and equity through investor reactions to variations in equity prices, while firms also respond to same through commodity price flux. Similarly, commodities, equities and EXCR are competing assets and information systems modify their attractiveness (Sokhanvar & Bouri, 2023). In response to content that enhances the EQMs, investors may acquire more equities and divest others, while the reverse occurs with unfavourable equity-based news. This, per studies (Moradi et al., 2021; Sokhanvar & Bouri, 2023), possesses a risk transmission prospect due to shifting interests. Drawing upon the cross-asset trade conduits underscored by Trevino (2020), the inter-market risk transmission within these markets emerges as plausible, particularly with the advent of burgeoning information systems and the continental trade accord. Within this framework, shocks stemming from currency and commodity dynamics in these economies can instigate margin calls, prompting investors to divest assets in alternate jurisdictions.

The FMH on the other hand revolves around the choices that investors make when confronted with specific information (Peters, 1994). Moradi et al. (2021) contend that a market remains stable with adherent investors with diverse horizons. In contrast, investors in pessimistic markets often concentrate on the short term and respond to news and volatility, which result in disruptions (Baruník & Křehlík, 2018). For instance, Zankawah and Stewart (2020) found that currency instability has adverse effects on equity and commodity markets, amplifying market risk, while Katusiime (2018) revealed heightened connectedness during crises. Conversely, Moradi et al. (2021) contended that the FMH offers a novel paradigm for projecting the risk that characterise contemporary financial markets. Within this, we examine the following hypotheses: There are patterns of risk frequency-based transmissions between commodities, currencies and SSA equities. It is anticipated that the findings could aid in implementing policies to mitigate the incessant currency and commodity fluctuations with their effect on EQMs growth through increasing investment.

Per the arbitrage pricing theory (APT), an asset predictability can be realised by analysing its projected return and various economy-wide factors that encapsulate systematic peril (Maitra & Dawar, 2019; Ouma & Muriu, 2014). Despite the clarity of this assumption, the model failed to specify these risk indicators with the justification found in the empirical literature. In this context, studies (Hegerty, 2018; Siddiqui & Roy, 2019) have emphasised EXCR and commodities with simultaneous fluxes while providing justifications for their predictive capacities on equities. Conversely, studies (Katusiime, 2018; Ogbulu, 2018) found a causal nexus between commodity prices and EXCR, with the latter as the predictor, signifying the mutual awareness possessed by these markets in risk and returns. In line with the APT, the current study hypothesises that there exists a predictive capacity of commodities (IDM and AGRC) and EXCR (BSP, GHS, KSH and NAD) in driving the sample EQMs (BSE, GSE, NSE and NASE). These theories apply to these markets since they stress diversity of investors, the risk arising from currency fluctuations and the reliance on commodities against the backdrop of price surges.

Empirical Review

Aligned with the FMH, Vardar et al. (2018) examine the transmission of shocks among equities in developed economies, encompassing the G7 countries and placed emphasis on crude oil, natural gas, platinum, silver and gold and revealed a bidirectional transmission effect between equities and commodities. Similarly, Hegerty (2018) revealed that the Czech Republic exhibits a relatively isolated position with limited international transmissions, Hungary is more susceptible to global spillover effects, while Poland is exposed to events originating within the region. In contrast, Baruník and Křehlík (2018) assess the interconnectivity and overspill between financial markets in the US, confirming that keen frequencies align with periods of increase connectedness, especially when EQMs adeptly and calmly assimilate information. Maitra and Dawar (2019) identified a unidirectional spillover of returns from the multi-commodity to stock indices and EXCR. Specifically, equities were found to exert an influence on EXCR, while the US dollar solely explained the return patterns observed in stock indices. Mollick and Sakaki (2019) revealed that with global EQMs advancing, risk tolerance increases and both oil and EQMs drives currencies. Sokhanvar and Bouri (2023) expounded further on the ongoing conflict and the disruptions in global distribution outlets and revealed a positive influence of commodity price shocks on the value of the Canadian dollar in relation to the euro and the yen. It became evident that price disruptions have an identical consequence to the intensified devaluation of the euro and the yen, with an effect on a global scale.

In the African milieu, Ogbulu (2018) examined the extent of volatility transmission between foreign currency, oil prices and the EQMs in Nigeria and revealed an enduring dynamic nexus among the sampled markets, demonstrating the volatile nature of stock prices and the significant transmission from Nigerian oil prices into the EQMs. Zankawah and Stewart (2020) revealed that oil prices have noteworthy spillover effects on the currency and EQMs, which is contingent on whether the oil price is exogenously or endogenously determined. Adi et al. (2022), along with Queku et al. (2022), revealed that previous self-originating shocks and volatilities significantly contribute to current volatilities in the EXCR and oil price domains with a bidirectional transmission of shocks. Opoku et al. (2023) revealed the dynamic nature of the commodity-currency nexus within SSA, with a robust nexus identified at elevated frequencies and that crude oil emerges as the primary transmitter of shocks, with the ZAR exhibiting a predominant influence in risk transmission among metal-producing countries.

Research Gap

The empirical discussion demonstrates that heightened volatility in commodity and EXCR markets adversely affects EQMs, leading foreign trade partners to adopt a sceptical stance regarding investing in these EQMs. Moreover, most studies in SSA emphasised crude oil and precious metals, with none on IDMs at the height of the market crash as well as the combined influence of these markets. Similarly, most studies utilised static models, such as the ARDL, VAR and GARCH, and Copula, despite their limitations as affirmed by studies (Baruník & Křehlík, 2018; Opoku et al., 2023; Woode, Owusu Junior, Idun, Kawor, et al., 2024). In the SSA milieu, only Opoku et al. (2023) utilised the BK-18, yet their study followed the usual pattern and emphasised only commodities and currencies and failed to acknowledge the model’s limitations, highlighted by studies (Asafo-Adjei et al., 2024; Qabhobho et al., 2023). In contrast, the current study complements those of Opoku et al. (2023) by employing both the BK-18 and the TVP-VAR models in examining the frequency-based and the dynamic connectedness of risk among the sample commodities, pressure currencies and SSA equities. The superiority of these models resides in their ability to discern nonstationarity, time-varying instability and asymmetries in returns. Employing the spillover-based model aligns with the framework of the contagion theory and those of the FMH. Given these considerations and the scarcity of studies within SSA, the relevance of the study is justified.

Methodology

The research examines the volatility transmissions among commodities (AGRC and IDMs), EXCR and EQMs in commodity-dependent SSA countries, utilising the BK-18 and the TVP-VAR-based connectedness models. Our decision to employ the BK-18 index was motivated by studies (Bossman et al., 2022; Owusu Junior et al., 2020; Woode, Owusu Junior, Idun, Kawor, et al., 2024), with the TVP-VAR model employed in adherence to the limitations of the former in capturing the time-varying dynamics and structural breaks (Antonakakis et al., 2018; Asafo-Adjei et al., 2024). In parallel, this study utilises the frequency-based Diks and Panchenko causality tests to augment the connectedness approach findings, given that the latter, despite its superiority, yields values devoid of statistical significance. Accordingly, the model’s significance is further emphasised in prior studies (Ghosh & Chaudhuri, 2019; Woode, Adam, Owusu Junior, & Idun, 2024).

Baruník and Křehlík Spillover and Connectedness Index

The BK-18 model incorporates generalised forecast error variance decompositions (GFEVDs) to quantify connectedness, inspired by the work of Diebold and Yilmaz (2012). It is constructed using the local covariance stationarity and matrix of a VAR. The K-variate process is tinted as  at

at

The GFEVD can be expressed as the contribution of the

The measure of connectedness is contingent upon variance decompositions, which involve the transformation of

The pairwise connectivity in Equation 3 determine the system’s overall connectivity. This is the proportion of the variation in projections due to errors other than their own, per Diebold and Yilmaz (2012). This is equivalent to the sum of the off-diagonal components as shown in Equation 4.

For a decomposition of the GFEVD across frequencies, we assign a weight to

Instead of measuring connectedness at single frequencies, it is appropriate to do so across frequency bands. The within-frequency and connectivity across

Diks and Panchenko Nonlinear Causality Test

Despite the ability of linear causality to capture the nexus between financial assets, it fails to incorporate nonlinear dynamics (Diks & Panchenko, 2006; Ghosh & Chaudhuri, 2019; Lundgren et al., 2018; Woode, Owusu Junior, Idun, Kawor, et al., 2024). Diks and Panchenko (2006) was put forth as variational causality test to circumvent the limitations of Hiemstra and Jones (1994).

The causality test of Diks and Panchenko (DKP) takes the following pattern: Presume that  and

and  are the adjournment vectors, where

are the adjournment vectors, where  . The null hypothesis that

. The null hypothesis that  contains additional information about

contains additional information about

The null tends to invariant dispersion bound claim of the  dimensional vector,

dimensional vector,  where Ƶ

t

= ϒt + 1. DKP established that the regurgitated null premise infers:

where Ƶ

t

= ϒt + 1. DKP established that the regurgitated null premise infers:

The estimation of Ƣ from (9) can be expressed as (10)

ɛn consists of a weighted average of local contributions  under the null hypothesis, appears to possess a likelihood of zero. DKP offers additional evidence to back up its contention.

under the null hypothesis, appears to possess a likelihood of zero. DKP offers additional evidence to back up its contention.

Where  represent the sample size and limited mass estimator of a ɖɰ variate arbitrary vector ɯ

i

, measured at ɯ based on the functions

represent the sample size and limited mass estimator of a ɖɰ variate arbitrary vector ɯ

i

, measured at ɯ based on the functions  . Under a conservative bidirectional causal nexus between the sample currencies, commodities and SSA equities, the estimation infers that if the bandwidth élites up the value

. Under a conservative bidirectional causal nexus between the sample currencies, commodities and SSA equities, the estimation infers that if the bandwidth élites up the value

Data Sources and Variable Description

The research utilised daily price data comprising AGRC, IDMs, EXCR and SSA equities. The dataset covers the period from January 3, 2012, to December 30, 2022, resulting in 2,729 observations after missing data. The commodities, EXCR and SSA equities were respectively obtained from Yahoo Finance, the central banks of the sampled SSA countries and EquityRT. The selected SSA EXCR and their respective EQMs for this study include Botswana, Ghana, Kenya and Namibia. The study focussed on AGRC (cocoa, coffee, corn and cotton) and IDMs (aluminium, copper, nickel and zinc). The sample period was determined to account for the pandemic, and the metal crash, among other turbulent periods that were deemed chaotic and impacted most SSA economies (World Bank, 2022). The study utilised the daily returns as

Preliminary Analysis

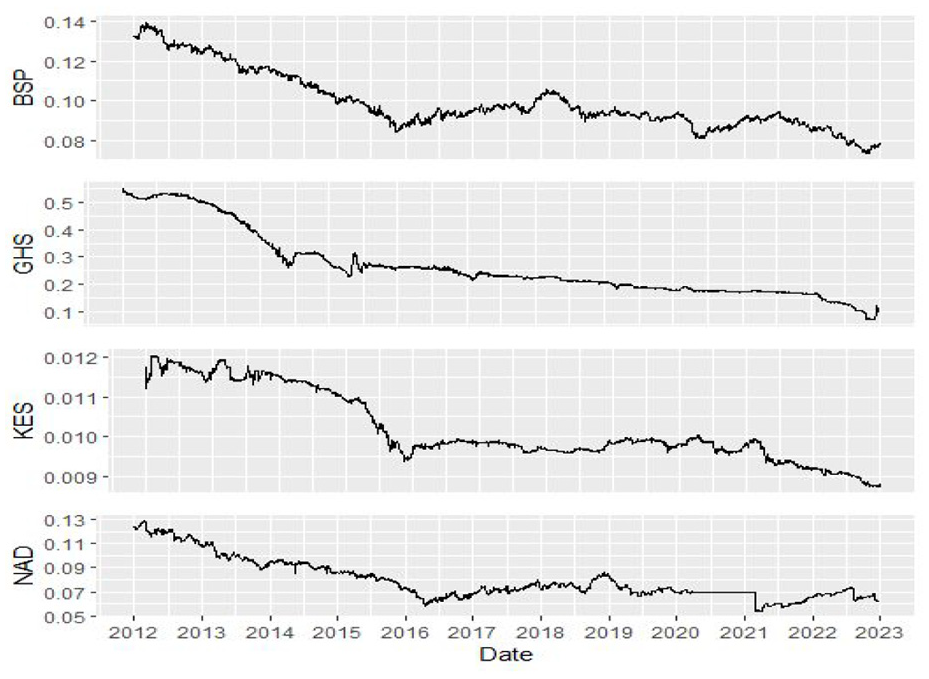

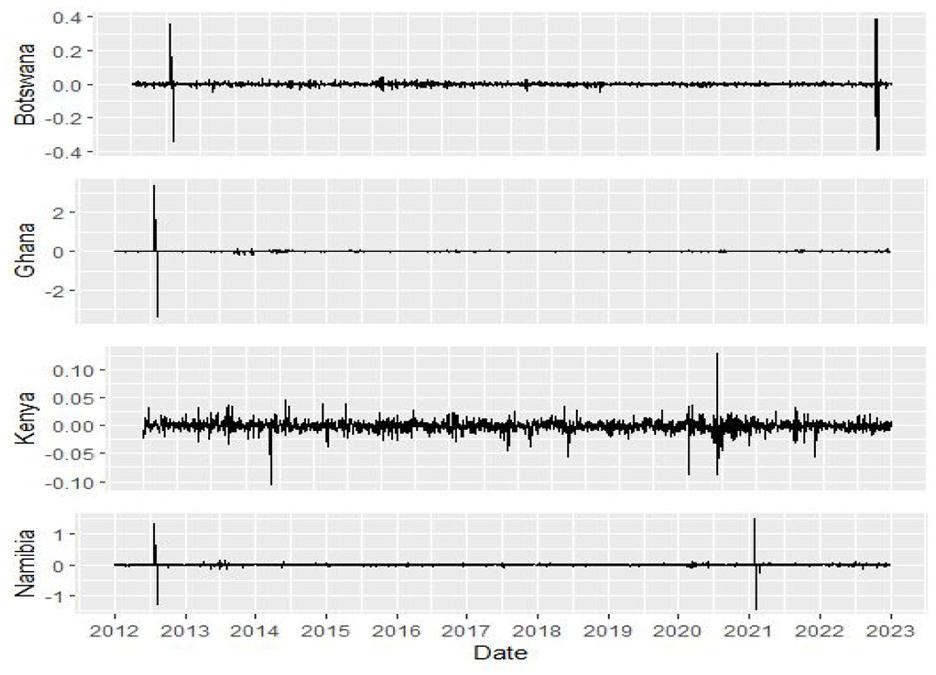

Figures 1 to 4 (Figures 5 –8), respectively, represent the price (return) of the sampled market. The pictorial view reflects that IDM prices (Figure 1) have not been stable, with both upward and downward spirals, while the earlier period was marred by low prices. Figure 2 demonstrates that fluctuations in the market for AGRC were superior to other markets during the sampling period, demonstrating the speculative nature of AGRC. This may partly be explained by commodity prices, specifically those of aluminium and nickel, which express the current equilibrium between supply and demand, which is subject to daily fluxes. The increased decline of these currencies, as shown in Figure 3, may be supported by a downward spiral in the EXCR market over the period, with the return series (Figures 5 –8) remaining stable across all periods.

Plots of industrial metal price series.

Plots of agricultural commodity price series.

Plots of exchange rate series.

Plots of SSA stock price series.

Plots of industrial metal returns series.

Plots of agricultural commodity returns series.

Plots of exchange returns series.

Plots of SSA stock price and returns series.

The descriptive statistics for these markets were highlighted in Table 1. Most of selected IDMs, EXCR and SSA equities exhibited positive mean except for metals (copper), agricultural (cocoa, coffee and corn), GHS and NSE. Also, the highest variation was in the metal (aluminium and nickel), followed by the agricultural (cocoa). Most markets exhibit skewness to the right, with a few left-skewed and leptokurtic behaviour. This demonstrates that all of the variables significantly deviate from normality and that there are fat tails, which was justified by the Jarque-Bera test. The study further assessed unit root, incorporating the Augmented Dickey-Fuller with trend and accounting for structural breaks (Zivot and Andrew), revealing stationarity across the datasets, with breakpoints either in the early days or in the period succeeding the global health crisis. We used the Terasvirta Neural Network (TRS) test for linearity given its superiority as highlighted by Ozcelebi and Izgi (2023), and the results further indicated non-linearity except for tin, zinc, cotton and most currencies at a 5% significance level, justifying the use of a non-linear model.

Descriptive Statistics.

Note. SD, Skew., Kurt., Norm, ADF, TRS and ZVA respectively represents standard deviation, skewness, kurtosis, normality, Augmented Dickey-Fuller, Terasvirta Neural Network Test and Zivot and Andrew unit root test with structural breaks. Optimal lag for ADF is determined using the AIC criteria.

Significance at 1%, 5% and 10%.

Empirical Result and Discussion

This section presents the results from the estimations followed by discussions. We initiate a comprehensive examination of the return and risk transmission effects, exploring their displays within the frequency (BK-18) and time (TVP-VAR) models. The import of the BK-18 lies in demonstrating the anticipated spillovers between the sample markets with precise values. This is vital, as it illuminates how these assets interact across different frequencies and how investors capitalise on the variations or how such fluxes could undermine any stability they seek within these markets. Likewise, the time-varying components help clarify the impact of significant events on connectedness, guiding investors in making decisions. Attention is devoted to the pandemic, the nickel crash and conflicts both within the SSA region and on a global scale, as they are characterised by heightened risk which impact on the examined markets.

Baruník and Křehlík Frequency-Based Spillover Analysis

The application of frequency-based analysis facilitates the evaluation of contagion, considering changes in overall connectedness. We take a step forward by investigating the transmission effects among the selected commodities, EXCR and SSA EQMs across various frequencies. Given that the markets for AGRC and IDMs are different and react differently to shocks from the globe and that their capacity as shock transmitters could further be felt at varying times, we systematically look at the framework that explains these differences. The initial (subsequent) system emphasised all sampled markets, excluding the AGRC (IDMs) market. This facilitates a deeper understanding of how shock transmission unfolds from the respective commodity markets to the SSA’s EQMs and EXCR across frequencies.

‘FM_ABS’ tracks transmissions from distinct markets towards the market (jstrok;), whereas ‘ABS_To’ covers transmissions from the market (jstrok;) to other segments, particularly the market (kstrok;). ‘To_WTH’ captures transmissions from the market (jstrok;) to neighbouring financial markets, which incorporate those related to jstrok;’s novelties in markets (kstrok;), whereas ‘From_Within’ captures transmissions from other markets (kstrok;) towards market (jstrok;), which comprise those corresponding to markets (kstrok;’s) novelties in market jstrok;. ‘Net’ represents the resultant shock transmissions (receipts) of a peculiar market. A negative (positive) net coefficient signals a shock-receiving (transmitting) market. In light of the FMH, investors operate with divergent timeframes, which influence their inclination to prioritise different investment aspects. Consequently, several components generate shocks that elicit heterogeneous responses, thereby yielding diverse origins of connectedness with rise to systemic risk across the short, intermediate and enduring-terms (Ahnert & Bertsch, 2022). Baruník and Křehlík (2018) contended that short-term (long-term) components correspond to erratic trading behaviours (fluctuations in economic fundamentals). The results of the frequency-based connectedness and spillage for the markets excluding AGRC are summarised in Table 2.

Total and Net Spillover Connectedness Across Frequency Bands for Industrial Metals, Exchange Rates and SSA Equity Markets.

Highest receiver of total shocks in the system without its own shocks. Highest receiver of shocks including shocks from its own internal transmissions. This and other values positioned in a similar place signifies total connectedness among the sample variables.

Table 2, unveil a mixed trajectory of heightened volatility diffusion within the system, with risk transitioning from 91.22% during the short-term to 91.63% (91.71%) in the medium (enduring) term. This indicates a relatively comparable level of interconnection across frequencies, devoid of a predominant factor. The row-wise values denote the share of variance in anticipated errors, while the values in the columns delineate the extent to which the variability in projected errors of one variable is ascribed to another. The insignificance of short-term market-specific risk transmissions is evident, with a limited significance, notable in the currency realm (BSP, KSH and GHS). The nullification of the insignificant short-term spillage effect invalidates the distinct contentions espoused by studies (Bossman et al., 2022; Owusu Junior et al., 2020) regarding the prevalence of short-term risk in most global markets. The short-term discloses that copper (−0.030), nickel (−0.048), zinc (−0.117), NAD (−0.005), BSE (−0.095), NSE (−0.118), ZAR (−0.03) and NASE (−0.126) were all recipients of net shock, whereas aluminium (0.079), BSP (0.161), GHS (0.108), KSH (0.181) and GSE (0.009) functioned as conduits for disseminating shocks. Those identified as recipients of net shocks emerge as the most susceptible within the system, especially in the short term. In a portfolio, it is imperative to designate these assets as high-risk due to their vulnerability to disruptions, while the transmitters signify potential assets capable of absorbing shocks.

In a similar vein, the intermediate period (0.79–0.10) displayed marginally enhanced outcomes in comparison to the short-term, revealing a blend of noteworthy (aluminium, copper, nickel, BSP, GHS, KSH, NAD and GSE) and negligible (zinc, BSE, NSE and NASE) pairwise transmissions. The BSP, GHS and KSH markets were slightly influenced by their inherent risks, corroborating the contentions of studies (Bossman et al., 2022; Owusu Junior et al., 2020; Zankawah & Stewart, 2020) that risk originating from a market not only diffuses into another but persists within the originating market. Similarly, the KSH (NASE) market emerges as the transmitter (recipient) of overall shocks. Contrary to this, the long-term analysis unveiled traits reminiscent of financial contagion, characterised by numerous bidirectional transmissions. These market showcases a degree of interrelation where the concept of a secure haven (hedge) becomes implausible amidst turbulent (normal) circumstances. The level of risk transmission was evidenced in the convergence of the BSP and GHS markets, showcasing an intensified degree of transmission and persistence, with zinc recording the lowest transmissions. In a comparable trajectory, KSH (zinc) emerged as the preeminent transmitter (recipient) of total shocks within the system, while KSH (6.58) surfaced as the least recipient of shocks. The list of shock recipients within the system encompasses copper (−0.175), nickel (−3.052), zinc (−6.792), NAD (−0.237), BSE (−5.603), NSE (−6.472) and NASE (−6.816), while the remaining markets function as transmitters. Interestingly, the list of net shock conveyors and recipients remains unaltered, with none relinquishing their respective roles.

Remarkably, the most advanced SSA equities (NASE), along with its corresponding currency, served as net recipients within the system, which can be attributed to its elevated level of exposure, owing to the scope of its market, which encompasses domestic and foreign risk, driven by investor participation and the strength of its currencies. This is contingent upon repatriation frequency from these markets, especially by foreign investors. Consequently, such activity is likely to generate adverse volatility effects on these markets in the form of demand and supply shocks, impaired by prevailing uncertainty (World Bank, 2022).

Table 3, presents a summary of the systemic risk transmission in all the sampled markets, except for IDMs. Similarly, the outcomes within the current context demonstrate a blend of both forward and backward escalation in risk transmission, transitioning from 74.05% during the short-term to 73.98% (82.3%) in the medium (long) term. Despite these findings, the most noteworthy disparity among these distinct timeframes lies in the bilateral transmission, wherein there was a progressive spread of risk across the entire market, with the extended time horizons (spanning from 32 days to an unspecified length) being the dominant element among the frequency bands and constituting the most of the total spillovers. Similarly, the majority of short-term transmissions were largely insignificant. GHS (12.21%) served as the highest receiver of shocks from other markets in the system, including shocks originating from its own market. Similar to the system with IDMs, KSH (19.50%) emerged as the prime transmitter of overall shocks, while NASE (0.14%) served as the least transmitter. It was further revealed that coffee (−0.027), cotton (−0.003), GHS (−0.049), NAD (−0.020), BSE (−0.074), GSE (−0.037) and NASE (−0077) were all recipients of net shocks, while the remaining markets acted as net transmitters of shocks. The intermediate-term further exhibited slightly superior results compared to the short-term. GHS (12.07) maintained its role as the highest recipient of systemic risk, including those from its market, while KSH (19.58%) and NASE (0.14%) maintained their respective highest and lowest overall transmission capacities into the system. Comparatively, the long-term yielded similar results as the system with IDMs, with a multitude of bidirectional transmissions, except for zinc, NSE and NASE. Among the pairwise combinations, the highest level of risk transmission was observed in the BSP, KSH and GHS markets, exhibiting an intensified level of both transmission and persistence, with the exception being its transmissions to cotton, NSE and NASE. Similarly, the extent of transmission observed in the long term partially reinforces the notion of contagion.

Total and Net Spillover Connectedness Across Frequency Bands for Agricultural Commodities, Exchange Rates and SSA Equities.

Highest receiver of total shocks in the system without its own shocks. Highest receiver of shocks including shocks from its own internal transmissions. This and other values positioned in a similar place signifies total connectedness among the sample variables.

In a similar vein, cocoa (coffee) assumed the role of the foremost (least) recipient (transmitter) of shocks into the system, while KSH, conversely, emerged as the highest transmitter (28.50%) of the overall shocks in the system. NSE (−5,090) stood out as the primary recipient of net shocks, while the KSH (16,552) emerged as the transmitter, followed by corn (13.36). Similarly, the list of net shock transmitters and receivers maintained their respective positions in direction but with varying magnitudes. It is rather overwhelming to acknowledge that the majority of the sampled commodities and currencies with few exceptions emerged as transmitters of shocks, considering the reliance of the SSA EQMs on the aforementioned. According to Workman (2022), a substantial proportion of the total exports of the sampled economies comprise AGRC exposing their EQMs to shocks with the EXCR aiding such transmissions. This also implies that shocks originating from these markets are likely to impact the EQMs, which is in line with the shock transmission assertions of the financial contagion theory (Ahnert & Bertsch, 2022; Trevino, 2020) and the FMH (Bossman et al., 2022; Moradi et al., 2021; Peters, 1994).

Our findings regarding multiple lists of bidirectional risk between commodities and EQMs align with those of Vardar et al. (2018), who identified bi-directional transmission effects between similar markets with further validation in separate studies on bidirectional transmission and causality of volatility across the globe (Mollick & Sakaki, 2019), Eastern Europe (Hegerty, 2018) and Asia (Maitra & Dawar, 2019; Siddiqui & Roy, 2019). Within the SSA context, our findings align with studies (Adi et al., 2022; Katusiime, 2018; Ogbulu, 2018; Opoku et al., 2023; Zankawah & Stewart, 2020), which investigated risk and volatility transmission in the commodity, EXCR and EQMs of Uganda, Ghana and Nigeria. These studies identified a combination of unidirectional (Ogbulu, 2018) and bidirectional (Adi et al., 2022; Opoku et al., 2023; Zankawah & Stewart, 2020) transmissions among the sampled markets. Furthermore, the presence of weak but noteworthy transmissions in the medium term between commodities and currencies further supports the findings of Katusiime (2018), who revealed a modest yet dynamically fluctuating transmission of volatility among EXCR and commodities. Furthermore, the current study affirms the assertions of Opoku et al. (2023) that the risk and return connectedness between SSA currencies and global commodities exhibit robust connectivity solely at elevated frequencies.

We validate the horizon-based risk transmission as proposed by the FMH and affirmed by Moradi et al. (2021). The weak pairwise transmission of risk within the system over the short term can be attributed to the relatively weak integration among SSA countries. Moreover, the absence of regional currencies and the heavy reliance on the USD for regional transactions support the accelerated depreciation of local currencies within the sub-region. Per UNCTAD (2022), intra-trade in Africa stands at a mere 14.4%, with deficit reaching 51%, rendering it vulnerable to external shocks. Moreover, the OECD (2021) expounded on these limitations, attributing them to the dearth of a demonstrated comparative advantage in manufactured commodities. Furthermore, it is worth noting that a significant portion of EQMs firms are owned by foreign investors which contributes to the ongoing currency depreciation, as it highlights the continuous repatriation needs. These deficiencies not only impede the diversification but also recognise the need for competitive and facilitative business, alongside structural changes aimed at augmenting economic complexity.

Globally, the findings are attributed to the recent volatility in commodity prices, influenced by global demand, supply disruptions and geopolitical tensions. Per studies (Agyei & Bossman, 2023; Sokhanvar & Bouri, 2023; Vasin, 2023), monetary policies by central banks worldwide, such as the US Federal Reserve’s quantitative easing (2013–2014) and the European Central Bank’s (2015–2018), contributed to volatilities in SSA countries, with the pandemic further influencing global markets, while investor sentiment underwent rapid shifts driven by geopolitical events. Also, the nickel crash and fluctuations in AGRC prices are instrumental in these dynamics. Drawing on the cross-asset trade channels and financial contagion by Trevino (2020), we infer contagion among the sample markets over the long-term. This is based on the premise that the unrestricted flow of systemic information over the long term and the need for risk management avenues will act as the primary conduit for inter-market risk transmission.

TVP-VAR Results

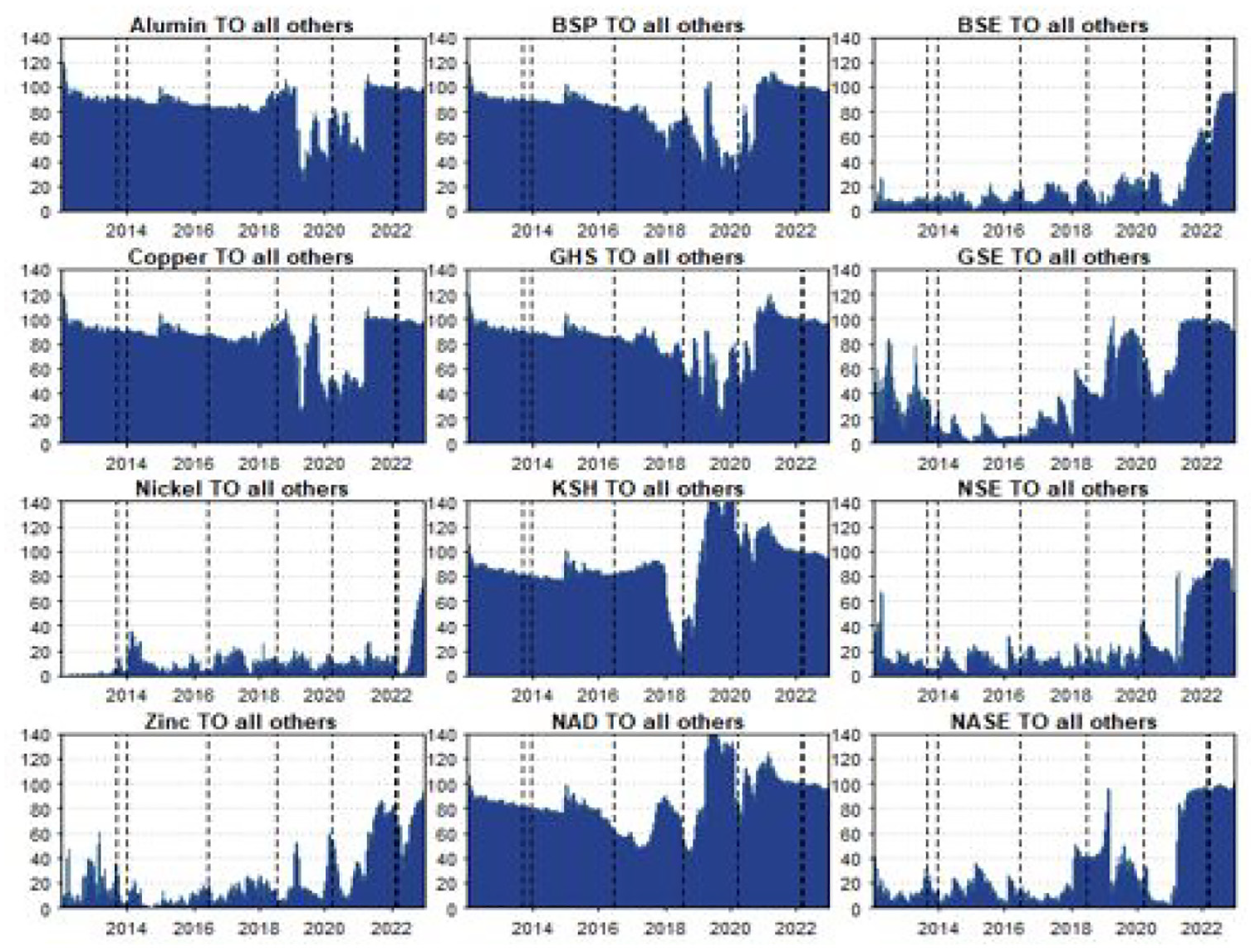

Subsequently, we employ the time-varying components to encapsulate the impact of both global and market-specific events on connectedness. Throughout the period, numerous events, both adverse and beneficial, occurred with the potential to affect market interactions, which should be of utmost importance to market participants. We scrutinise total connectedness, capturing the synchronous movements of risk across the sample markets over calendar times as well as the time-varying shocks transmitted to (market j from all other markets) and from (all other markets to market j). The study prioritises event-specific factors, including but not limited to the Eurozone Debt Crisis (30-08-2013), the Ebola Endemic (16-12-2013), Brexit initiation (16-06-2016), US-China trade tensions and the imposition of 25% tariffs on $550 billion worth of goods, including metallic components (06-07-2017–23-08-2018), the pandemic (11-03-2020), the Russia-Ukraine conflicts (24-02-2022), and the nickel crash (08-03-2022). The outcomes of the dynamic total connectedness for the sample, including IDMs and AGRC, are illustrated in Figures 9 and 10, while those of the directional connectedness are in Figures 11 to 14.

Total dynamic connectedness of spillovers among IDM, EXCR and SSA equities.

Total dynamic connectedness of spillovers among AGRC, EXCR and SSA equities.

Directional connectedness of spillovers from markets j to others in the IDM system.

Directional connectedness of spillovers to markets j from all other markets in the IDM system.

Directional connectedness of spillovers from j to others in the AGRC system.

Directional connectedness of spillovers to j from all other markets in the AGRC system.

Dynamic Total Connectedness

Figure 9 (10) clarifies the dynamic connectedness (TDC) among the sample IDM (AGRC) and SSA currencies and EQMs in response to economic events. Drawing on studies (Asafo-Adjei et al., 2024; Woode, Owusu Junior, Idun, Kawor, et al., 2024), we can observe substantial changes in the spillover patterns over the sample period, highlighted by the dashed lines. The TDC results closely mirror those of the BK-18, particularly in the long term for both systems, with pronounced fluctuations throughout the sample period, ranging from 60% in 2012 and 2013 during the Eurozone debt crisis to 85% to 90% from 2022 to 2023, coinciding with the IDM market crash in Figure 9 and the Russia-Ukraine conflicts in Figure 10, further confirming the time-varying connectedness during periods of crisis. Despite the impact of the pandemic, its influence was less pronounced among the sample markets compared to the Russia-Ukraine conflict (24-02-2022) and the nickel crash (08-03-2022). The pandemic (the third dashed-line) around 2020, has a comparable effect to the Ebola endemic (16-12-2013) and the initiation of Brexit (16-06-2016), underscoring the less-sensitive nature of SSA markets to some external shocks.

The peak volatility surpassing 85%, coinciding with the nickel crash and Russia-Ukraine conflicts, highlights the heightened sensitivity of the EQMs and commodities to market-specific and geopolitical shocks. Additionally, these markets showed increasing levels of connectedness from the later stages of the pandemic era (2021) through the metal crash and currency fluctuations (2022–2023), emphasising their lower responsiveness to short- and medium-term shocks compared to long-term shocks. This supports the BK-18 and contradicts the notion of short-term responsiveness of financial markets to global shocks (Owusu Junior et al., 2022; Qabhobho et al., 2023). Figure 9 reveals that, prior to the market crash, SSA currencies and equities exhibited moderate connectedness, with metals ranging around 40% to 60%. This increased to 70% during the later days of the pandemic, reaching 85% to 90% at the onset of the conflicts and the nickel crash, indicating that while SSA currencies and equities are moderately connected to IDMs, this is intensified by external shocks, confirming the presence of time-varying contagion in the global market during crises (Bossman et al., 2022; Opoku et al., 2023). A similar pattern is observed in Figure 10, with exceptions showing heightened connectedness at the onset of Brexit (16-06-2016) and during the US-China trade tensions (06-07-2018), illustrating the impact of these policies on SSA markets. These events affected SSA equities and currencies through the economy’s reliance on AGRC and IDMs, but the impact was more pronounced through the latter (Figure 9), which recorded the highest connectedness (90%) compared to 80% in (Figure 10).

Considering that a substantial portion of SSA equities is metal-dependent, such connectedness is anticipated to impact the markets and prompt investors to reallocate funds during heightened crises, thereby transmitting risk across markets. The increased connectedness observed in the latter stages suggests that diversification opportunities are viable in the short and medium terms, whereas the long term is unsafe. Notably, the Russia-Ukraine conflict, which resulted in the suspension of natural gas flow and surging global energy prices, with the metal index hitting a record low, and the nickel crash, which caused an unprecedented near-week-long suspension of the IDM market, represent pivotal crises that saw a spike in dynamic connectedness. This aligns with studies (Qabhobho et al., 2023; Sokhanvar & Bouri, 2023) on the elevated levels of connectedness at the onset of global crises and the time-varying impact of global events.

Directional Time-Varying Spillover Connectedness Analysis

The results of the TDC are complemented by the directional spillover connectedness, which aids in discerning the dynamic resilience and susceptibility of these assets to systemic shocks. Figure 11 (13) depicts the directional dynamic connectedness ‘to-all-others’ for the system with IDMs (AGRC), while Figure 12 (14) illustrates the directional connectedness ‘from-all-others’ for both systems. The results align with those of the BK-18, with minor deviations due to the time-varying nature. Figures 11 and 12 confirm the shock transmission and reception capacity of commodities (aluminium and copper) and all currencies throughout the sample periods, peaking at 100% to 140% during the nickel crash era. Sample equities exhibit weak transmissions but receive higher shocks, peaking during crash. Figures 13 and 14 show similar patterns for AGRC, with consistent high-risk transmission and reception among commodities (cocoa and corn) and all currencies, except for NAD during the US-China trade tension. The consistently high shock levels among SSA currencies support studies (Queku et al., 2022; Zankawah & Stewart, 2020) indicating EXCR markets as conduits of risk transmission among commodity and EQMs. The weak risk transmissions among commodities in Figures 11 and 12 (nickel and zinc) and Figures 13 and 14 (coffee and cotton) confirm the risk persistence noted in the BK-18 analysis. Furthermore, it is evident that all sample commodities and currencies exhibiting elevated levels of transmission and persistence in the BK-18 displayed similar traits in the TVP-VAR. All EQMs and commodities (zinc, nickel, coffee and cotton) were the least receivers of shocks, except during sample crisis periods, particularly for GSE. The observation that metals (nickel and zinc) and AGRC (coffee and cotton) exhibited weak transmission and risk reception underscores their role as diversifiers for most SSA equities, especially during normal periods, which is crucial for market participants. Although the study explored dynamic net transmissions among the sample markets, these results, which largely mirrored the BK-18 analysis, are available upon request.

VMD-Based Nonlinear Causality Test

The study employed VMD-based causality to evaluate the reliability of the BK-18. This enables the assessment of the causal nexus between the observed variables across different frequencies, overcomes excessively rejecting the null hypothesis, effectively handles breaks in the dataset and addresses the variational sensitivity (Dragomiretskiy & Zosso, 2013). In the EXCR-EQM nexus, this analysis elucidates whether the dependence aligns with the currency-driven capacity of equity assertions or diverges. If effective EQMs stabilise EXCR, governments can strategically employ the EQMs as a tool to promote stability in local currencies. Therefore, we examine the causal link between the sample markets. The null (alternative) hypothesis assumes the absence (presence) of nonlinear causality. In this study, variable X (commodities and EXCR), serves as the predictor, while variable Y (EQMs) remain the response variable. The null hypothesis is assessed based on the calculated t-stats. and p-value. A threshold of 2.0 is employed for the t-stats., while an alpha level of 5% is used to determine whether to reject or fail to reject the null. We reject the null hypothesis with a simultaneous t-stats above the threshold of 2 and an alpha value of less than 5%. Where both null hypotheses for the joint test are rejected, a bidirectional causal relationship between X and Y is substantiated. Likewise, if one is rejected, a unidirectional causality is established. If neither is rejected, it implies the absence of any causal relationship.

The majority of the results from the original series indicate a unidirectional causal impact of the sampled commodities and EXCR on EQMs, which are further confirmed by the disintegrated series, especially in the long term, where there were series of bidirectional causality among the sampled markets validating the long-term results of the BK-18. This suggests that the variables possess predictive capabilities for each other across frequencies. Also, the variations in causation and the diverse outcomes obtained from the pairwise causalities provide theoretical support for the APT (Jacobsen et al., 2019; Maitra & Dawar, 2019; Mollick & Sakaki, 2019) on the predictive capacities of commodities and currencies on equities and FMH (Biswas et al., 2018; Sokhanvar & Bouri, 2023) on the heterogeneity of participants that amplify market-based alterations. This also aligns with the research of Mollick and Sakaki (2019), highlighting the superior predictive abilities of commodities and EXCR. The results are presented in Table 4 for both the original and frequency-based series.

Results of the Non-Parametric Causality Test.

Note. The test is bidirectional; Ϫ|ϒ represent variable × Granger-causes variable Y, and ϒ|Ϫ demonstrates that variable Y Granger-causes variable X.

***, ** and *Significance at the 1%, 5% and 10% levels, respectively.

Conclusion

Our contribution to the literature resides in the scrutiny of the time-varying connectedness of perils between commodities (AGRC and IDMs), EXCR and the SSA EQMs. This study employs the BK-18 and TVP-VAR algorithms with validation through the causality test. This inquiry stands as the pioneering effort to deploy the BK-18 algorithm in dissecting the interconnectedness of risks in the SSA milieu while also drawing parallels with the recent pandemic and the plummet in IDM. The presence of feeble and statistically non-significant risk propagation in both systems, particularly within short and intermediate terms, signifies that, in spite of enhanced global integration, the SSA market demonstrates reduced susceptibility to external shocks during these periods. This serves as an advantage for diversifying investment portfolios. However, with regard to the bi-directional transmission of risks in the long term, we deduce that alterations in commodity prices and EXCR hold the potential to influence the volatility of SSA EQMs, particularly over extended time horizons. Furthermore, the observation that the majority of the sampled SSA equities act as net absorbers of shocks across all systems underscores the susceptibility of these markets to shocks from the currency and commodity domains. Conclusively, we ascertain that fluctuations in commodity prices and foreign EXCR possess a causal impact on SSA equities. This insight signifies those changes, whether favourable or unfavourable, in these economic facets can precipitate undulations in the SSA EQMs. In synopsis, we underscore the latent advantages of portfolio diversification, the interlinked risks and the causal linkages between shocks in the commodity and EXCR domains and their reverberations on SSA EQMs. These revelations offer guidance for policymakers, investors and market participants, aiding them in making well-informed decisions, formulating effective risk mitigation strategies and fostering market stability and resilience.

Recommendation and Policy Implications

The study’s findings imply that global investors can allocate their investments to the sampled commodities and SSA EQM only in the short and medium term due to feeble risk transmissions, while the long-term analysis reveals the lack of such luxury. Thus, the strong integration revealed through the dynamic models indicate that a portfolio comprising SSA equities will only prove costly for investors since shocks from the commodity and currency markets adversely impact the EQMs during uncertainty. Also, considering the exposure of domestic currencies to shocks from the commodity markets and coupled with similar transmissions from the currency to the EQMs in the long term, central banks and EQM regulators should strengthen their market surveillance capabilities and implement policies that take into account these interlinkages. Also, central banks can implement stress testing and establish contingency plans, including the need for a common currency to enhance intra-regional trade and address potential market disruptions. Additionally, central bank regulators should coordinate their monetary policies with other relevant authorities to ensure coherence and effectiveness and further collaborate with EQM regulators to monitor and manage EXCR fluctuations, considering the transmission within these markets. Also, collaborative efforts with fiscal authorities and regulatory bodies in the form of EXCR stability maintenance policies with managed movements that support competitiveness and investor confidence can help manage the impact of market fluctuations on the broader economy and financial system. This notwithstanding, there is a need for diversification beyond the commodity market, as established by UNCTAD (2022).

Footnotes

Ethical Considerations

This study was performed under the ethical considerations as outlined by the University of Cape Coast regarding studies that utilised existing data. Thus, our study ensures the use of data from legitimate sources, which has been used in several prior studies.

Consent of Participate

This article does not contain any studies with human participants performed by any of the authors.

Author Contributions

John Kingsley Woode; conceptualisation, methodology, software, formal analysis, investigation, data curation, original draft preparation, writing-original draft preparation, review and editing. Anthony Adu-Adare Idun; conceptualisation, software, validation, formal analysis, writing-original draft preparation, supervision, project administration and fund acquisition. Seyram Kawor; revision of manuscript, software, supervision, formal analysis, methodology; Peterson Owusu Junior; conceptualisation, validation, software, investigation, visualisation, supervision, project administration, fund acquisition. Anokye M. Adam; Software, formal analysis, resources, supervision, project administration, fund acquisition. All authors have read and agreed to the published version of the manuscript.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.