Abstract

This study investigates the influence of dynamic capabilities like technological, organizational, and environmental on bank performance through the mediating roles of digital transformation (DT) and fintech adoption (FA), employing the Technology-Organization-Environment (TOE) framework. Drawing on data from 325 respondents in the Chennai region of India, a two-stage hybrid methodology combining Structural Equation Modeling (SEM) and Artificial Neural Networks (ANN) was used to validate the proposed model. The findings reveal that technological and organizational capabilities significantly drive digital transformation and fintech adoption but do not directly improve bank performance. In contrast, government support, representing environmental capability, exerts a direct and positive influence on performance outcomes. Importantly, the mediating effect of DT and FA strengthens the relationship between dynamic capabilities and bank performance, underscoring their strategic importance. This research contributes to the literature by integrating dynamic capability theory within the TOE framework, offering a holistic understanding of how banks can leverage internal strengths and external support for successful digital transformation. The results hold practical implications for bank management and policymakers. Strategic recommendations include incentivizing digital adoption through regulatory support, tax benefits, and funding programs to foster innovation while maintaining financial stability.

Plain Language Summary

This study examines how technology, organization, and government support drive digital transformation and FinTech adoption to improve bank performance. Using data from 325 bank employees in Chennai, India, the research applies a hybrid SEM-ANN method. Findings show that while technology and organization support digital initiatives, government support directly boosts bank performance. Digital transformation and FinTech adoption further enhance overall performance when acting as mediators.

Keywords

Introduction

Information and communication technology (ICT) has significantly transformed every aspect of human life (Miklaszewska et al., 2022). This technology has become unavoidable for both society and the business world, as it facilitates the automation of work processes and digitalization, leading to sustained transformation everywhere (Barrett et al., 2015). With the emergence of a new world, companies have focused on a few key areas, particularly cross border integration, innovation, and transformation, in how much organization develop (Lee et al., 2021). The financial sector has been greatly impacted by mobile advancements, highlighting the user-friendly interface of online financial services (Al Nawayseh, 2020). The development of the internet, blockchain technology and industry 4.0 has significantly transformed the business landscape and customer preferences. Digital transformation (DT) involves the shift from traditional banking systems to online platforms and has become a major driver of economic growth, influencing the operation financial services (Nguyen-Thi-Huong et al., 2023; Pan et al., 2022; Tan et al., 2021). Fintech solutions enhance operational efficiency, risk management, and decision making (Moschella et al., 2019). Their adoption is closely linked with DT, further influencing performance (P. Chen & Hao, 2022). The adoption of fintech in banking improves service efficiency, customer experience, and risk management by leveraging technologies such as AI, blockchain, and digital payment (Liu et al., 2021; T. C. Yan et al., 2018).

Navigating the complex realm of fintech, where cutting-edge technologies such as blockchain, artificial intelligence, and big data analytics are revolutionizing traditional financial services (Muduli & Choudhury, 2024). The journey from digital transformation to the banking performance in a sustainable way can be intricate. A bank’s ability to leverage these technologies lays the foundation for effective fintech adoption, enhancing operational efficiency, cost effectiveness, and customer experience (Harris, 2021). This not only strengthens the market positioning, but also establishes sustainable regulatory frameworks and standards for banking performance (Sajid et al., 2023). The operational definition provided in Table 1 clarify these key concepts ensuring a structured understanding of their role in banking performance.

Operational Definition.

This study identifies research gaps in the existing literature regarding, how dynamic capabilities manifest during fintech adoption in the digital transformation of banks, using the TOE framework. The first is the lack of empirical evidence on integrating dynamic capabilities (DC) within the TOE framework. Extensive research has been conducted on DC and Digital transformation (DT) across various sectors however, this paper provides an in-depth investigation of this research gap within the Indian banking sector, specifically concerning the integration of DT with financial regulations and rapid adoption of digital programs. The motivation for this research is to evaluate the adoption of FinTech and DT within the banking sector. Banks have aggressively pursued innovative DT initiatives to enhance customer experience, improve service convenience, and increase accessibility through digital channels. Additionally, a key research gap exists in understanding the dynamic characteristics that drive effective DT within the banking sector. Most studies have focused on developed economies whereas emerging markets such as Indonesia, present specific regulatory and infrastructural challenges that influence digital transformation strategies (Faia et al., 2021). To address these gaps, this study analyzes how banks acquire dynamic capabilities to navigate digital transformation, including the interactions within the TOE framework and influence of external regulatory impacts. By bridging these perspectives and empirical gaps, this research a more comprehensive understanding of how fintech adoption and digital transformation impact banking performance in emerging financial markets.

Further understanding of the relationship between these factors and implications for the banking sector will be developed by addressing the following research questions:

a. How do the capabilities within the TOE framework (technology, organizational and environment) that influence digital transformation and fintech adoption in the banking sector?

b. What is the mediating role of digital transformation and fintech adoption between the TOE framework and bank performance?

c. How does government support enhance the impact of digital transformation and fintech adoption on bank performance?

The financial sector is rapidly evolving with fintech innovations and digital transformations that enhance banking efficiency, service delivery and competitiveness (Ullah et al., 2021). Technologies such as AI, blockchain, and mobile banking have reshaped banking operations. However, most studies focus on technology adoption rather than its direct impact on bank performance (Cumming et al., 2020). While fintech adoption improves efficiency and customer experience its long-term contribution to bank performance remains unclear, as most studies examines behavioral intention rather than performance (Hoque et al., 2024; Nguyen et al., 2024). Digital transformation plays a major role in enabling fintech adoption, yet its role in bridging fintech adoption and bank performance remains unexplored (Aggarwal et al., 2023; Bajunaied et al., 2023). Successful fintech integration requires strong organizational readiness, skilled employees and a supportive regulatory framework (Chittipaka et al., 2023). Despite these factors, existing research has not fully examined how technology, organizational and regulatory frameworks collectively enhance digital transformation and bank performance. This study addresses this gap by analyzing how technology, organizational support, and regulations work together to strengthen digital transformation, enabling banks to maximize the benefits of fintech adoption.

Digital transformation is influenced by several factors within the Technology-organizational-environment (TOE) framework ( G. Zhang et al., 2023). However, DT is formed by both internal and external elements, making a comprehensive approach more important that a single study. From banking to e-banking, blockchain to fintech adoption (Aslam & Jawaid, 2025; Kajla et al., 2024; Megahed et al., 2021), maritime (Jović et al., 2020), information security (Kim & Kim, 2021) and hospitality (Nikopoulou et al., 2023), the TOE framework has been extensively applied across various sectors. Despite studies on dynamic capabilities (DC) and DT a major gap exists in incorporating DC within the TOE framework to analyze fintech driven digital transformation. Limited attention has been given to fintech adoption which is crucial for banks facing fintech disruptions (Leemann & Kanbach, 2022). Furthermore, existing studies lacks a comprehensive mapping of organizational capabilities within TOE framework to drive digital innovation which is the focus of the current research.

This study addresses these gaps by examining how banks acquire dynamic capabilities to support digital transformation in response to fintech adoption. Unlike earlier studies, it highlights the role of TOE components and presents a novel methodological approach by combining (ANN) Artificial Neural Network and PLS-SEM, thereby capturing both linear and non-linear relationships. This offers a strong foundation for digital banking transformation. Digital transformation in the banking sector is no longer discretionary but a necessity, driven by increasing fintech competition, evolving regulations, and growing customer demand for seamless digital services (Harun, 2023). By integrating the TOE framework and dynamic capability with fintech adoption and digital transformation and advanced modeling techniques, this study offers a holistic perspective on sustainable digital transformation in banking.

The paper structure guides the reader toward the research study. Firstly, the study begins with the development of a theoretical framework, which establishes the research hypothesis. Then, an in-depth examination of the methodology enables a comprehensive data analysis. Finally, the study concludes with the discussion section, where it outlines the research and their practical implications.

Literature Review and Hypotheses Development

Theoretical Framework

This study is based on widely recognized theoretical frameworks, the Dynamic Capabilities view (DCV) developed by (Teece et al., 1997) and the TOE framework (Tornatzky et al., 1990). The DCV posits that variations in bank performance can be attributed to dynamic capabilities which utilize knowledge resources and strategic pathways (Teece et al., 1997; Tornatzky et al., 1990) . Similarly, the TOE framework highlights the influence of technological, organizational and environmental factors on a bank’s ability to adopt innovations and enhance performance. The TOE Framework has been widely applied to technology adoption at the organizational level. In the banking sector it has been demonstrated that the TOE framework is well-suited for fintech adoption and digital transformation as it accounts for technological, organizational and environmental factors. Several studies have highlighted its relevance in higher level attributes, such as technological, organizational and environmental contexts (Al-Okaily, 2025; Al-Okaily et al., 2022; Bayraktar et al., 2024; Ramanathan et al., 2017; Sakas et al., 2023; Srouji et al., 2023). This advancement has supported the TOE as a widely accepted model for analyzing technology adoption in the banking sector (Bany Mohammad et al., 2022). While other theoretical models explain adoption from different perspectives, the TOE framework provides a more holistic approach, offering comprehensive insights into banking technology adoption and usage (AL-Khatib et al., 2024; Al-Mamary & Alraja, 2022). Whereas the traditional TOE framework primarily focuses on general IT adoption, this study develop an extended one that considers the specific dynamics of fintech and digital transformation.

Technology Capability to Bank Performance

Technology capability refers to a financial institution’s ability to incorporate, combine and use new digital innovations to enhance operational effectiveness, customer experience and competitive advantage. According to B. Singh et al. (2024) success in the digital era depends on how well organization leverage technology and adapt to the evolving digital landscape. Effective technology integration leads to increased efficiency, innovation, and accessibility of resources. Technology adoption involves implementing both software and hardware solutions to improve productivity, processing speed, and access to information. In the banking sector, technology capability encompasses infrastructure readiness, including robust IT systems, cloud computing, and cybersecurity frameworks all of which are essential for enabling seamless bank operations. Furthermore, a data analytics and artificial intelligence (AI) have swiftly become fundamental in supporting decision-making and delivering personalized financial services (Al-Dmour et al., 2023). The protection of financial transactions requires the implementation of cybersecurity measures such as fraud detection systems, encryption technologies, and risk management tools. As digital transformation has become a necessity for survival in a competitive environment, banks have invested in advanced technologies such as big data analytics to enhance overall performance. By utilizing these digital innovations banks can significantly improve operational efficiency, customer engagement, and financial performance. So, we hypothesized that

Organizational Capability to Bank Performance

Organizational capability has gained increasing relevance over the last few decades with several scholars exploring its components from multiple perspectives. Strong organizational capability plays an important role in achieving success and improving the operational effectiveness of business enterprises (Mady et al., 2022). Organizations with strong capabilities can identify and act on opportunities leading to the accumulation of resources and skills that enhance adaptive capacity (B. Singh & Rao, 2016). Leadership and strategic alignment are key dimension of organizational capability where top management ensures that digital investments align with business objectives while fostering an innovation-driven culture. Effective leadership enables financial institutions to integrate digital technology into their structures as a strategic tool for long-term competitiveness. Another important dimension is human capital and skills development, which includes employee training, digital literacy programs, and continuous upskilling to meet the ever-evolving demands of the financial landscape (Ahmed et al., 2023). Management structure and collaboration also play a significant role in enhancing financial institution performance. The innovation process can be positively influenced by structured management frameworks that facilitate coordination among public funders, regulators and financial institutions. Standardized approaches to evaluating financial institutions capabilities contribute to skill development and the promotion of innovation. Similarly, research in the hospitality and tourism sectors has demonstrated that management awareness, and organizational capabilities significantly impact overall business performance (Ahmed et al., 2023). Based on this, we hypothesized that

Government Support to Bank Performance

According to Biswas (2022) government support in the form of regulatory frameworks, financial interventions, and stability measures that enhances bank performance. Policies such as environmental regulations and administrative controls contribute to improved organizational efficiency. During financial crisis, supporting interventions like loan relief and subsidies help stabilize firms’ operations result in investment detrimental to long-term sustainability (Ashraf, 2020) . With the rapid growth of fintech, there is an increasing trend toward adaptive government policies. A key initiative, the regulatory sandbox, has enabled controlled innovation, balancing financial security with technological advancement and industry growth. Research has shown that such regulatory frameworks positively impact fintech investments (M. Li et al., 2022) . Regulatory improvements play a crucial role in enhancing competitiveness and strengthening resilience in the banking sector. Thus, government support is essential in establishing balanced regulation that ensure the stability of the financial sector. It promotes performance in banking and ultimately fosters long-term economic development. So, we hypothesized that

Technology Capability to Digital Transformation

Technology, organizational and government support provide insight into understanding the important factors that drive digital transformation. Technology capability an entails organization ability to manage and integrate advanced technologies, automate processes that foster customer experience, and reduce operational cost, contributing to growth and efficiency (Barham et al., 2020; Khin & Ho, 2019; Zuo et al., 2023). Technology adoption brings strong changes to business models, improving products and services for enhanced efficiency. Digital tools help optimize operations, design new offerings, and enable innovative facilities for digital transformation (Jayawardena et al., 2023). According to Siswanti et al. (2024), Islamic rural banks are highlighted by their degree of sustainability and financial performance, identifying financing quality, capital quality, economic performance, and digital transformation. Their findings reveal clear roles of financing and capital quality toward sustainability, in which financial performance mediates that relationship and digital transformation moderates it. They also investigated Indonesia capital from the perspective of smart city application. VBM is scrutinized in Industry Revolution 4.0, where companies use a weighted scale between short-term financial objective and long-term effects of value creation. Digital technology-based infrastructure, such as IoT and big data, is used to maximize resource allocation and enhance performance, yet requires investments in digital infrastructural capacity building (Nugraha et al., 2024). Technological capabilities permit an organization to accelerate innovation within the organization, thus creating digital pathways and mobile applications that improve customer engagement and drive revenue growth (Schepis et al., 2021). Integrating technology with strategic management finally makes way for sustained success and robustness in an increasingly digitized economy. The hypothesis has formulated that

Organizational Capability to Digital Transformation

Organizational capability involves governance structure, resource availability and employee proficiency, which support the implementation of digital initiatives, in line with the strategic objectives and promote learning (Cetindamar Kozanoglu & Abedin, 2021). Organizational capability includes the structure, processes and governance that organizations use to direct digital transformation and innovation (Radziwon & Bogers, 2019). It relates to developing and implementing a digital strategy by aligning digital initiatives with overall business objectives of the organization (AlNuaimi et al., 2022). Organizations with strong capabilities can effectively implement digital transformation into the organizational processes (Xie & Wang, 2021). This capability enables organizations to coordinate their digital strategies alignment with strategic goals, thereby enhancing performance and competitiveness. Hence, we hypothesize that

Government Support to Digital Transformation

Government support enables digital transformation by establishing regulations, providing funding incentives, and improving infrastructure. Attractive and effective government policies can generally encourage organizations to adopt new technology, facilitate digital process implementation, and promote innovative features in financial services. Here, prospect theory, suggests that public undertakings and opposition to change can be significantly improved through properly structured policies implemented in an appropriate manner (Doktoralina et al., 2024). According to Putra, Fardinal & Ali, (2024) studied how different levels of government regulation, the capabilities of human resources, and optimization of financial reporting optimization impact Jakarta’s MSMEs. Their research found that the quality of financial reporting did not have a significant direct effect. Thus, they recommended that regulatory compliance and adoption of technology as fundamental condition for fundamentals of financial transparency. Nugroho et al. (2024) conducted a study on the profitability of the banking sector and credit growth before and during the COVID-19 pandemic. Their findings highlight that government support provides essential infrastructure, policies, incentives, and subsidies that help organizations overcome challenges, mitigate risks such as moral hazards and achieve sustainable digital growth (T. Chen et al., 2023). Therefore, we propose that

Technology Capability to Fintech Adoption

The adoption of fintech enhances organizational performance and aids management decision-making. However, when adopting information systems, industries should carefully assess both their advantages and drawbacks to maximize profits and leverage relationship with customers, suppliers and other external stakeholders (Nugraha et al., 2024). With advancements in technology banks have integrated various technological solutions such as the (IOT) into their operations and services. Key characteristics of IT, including security, trustworthiness, and privacy are crucial for the efficient functioning of banking operations. According to Qi et al. (2024) technology capability is a crucial determinant of FinTech adoption, as it entails having the necessary technological infrastructure and expertise to access fintech services. One study demonstrated that users’ technological proficiency correlates positively with their intention to adopt fintech solutions. The findings suggest that while users vary in their characteristics, they also diverge considerably with respect to the technological capabilities, which ultimately determine FinTech adoption (Balaskas et al., 2024). Then we proposed that,

Organizational Capability to Fintech Adoption

Investor preference toward an organization and its competitors is influenced by corporate image, which is shaped by past performance and expectations for future outcomes (Bin-Nashwan & Al-Daihani, 2021; Sura et al., 2017). Organizations that actively pursue digital transformation and innovation engagement are more likely to adopt FinTech solutions, recognizing the benefits of improved operational efficiency and customer engagement (Z. Zhang et al., 2024). According to Kerenyi et al. (2018) the rapid growth of fintech creating high potential for partnering with banks that can adopt the innovative assets of emerging fintech. Findings from Motta and Gonzalez Farias (2022) indicate that connecting with stakeholders and enhancing service delivery through highly innovative, technology-enabled products and services allows organizations to expand. Pizzi et al. (2021) highlight that Industry 4.0 plays a crucial role in the development of financial industries. In future planning, the evolution of fintech remains one of the most crucial factors for industrial growth. Hence, we propose the hypothesis that:

Government Support to Fintech Adoption

Government support refers to all activities that create favorable conditions for the adoption of fintech services among individuals (Jahanmir & Cavadas, 2018; Setiawan et al., 2021) . It includes efforts to develop fintech infrastructure to facilitate easy access to financial services, legislation to ensure the safety of digital transactions, and regulatory measures to maintain the stability of the fintech sector (Abdul-Rahim et al., 2022). According to studies conducted by Osman et al. (2021) government support fosters trust among users positively influencing their readiness to adopt fintech services. The government can promote innovation and establish systems that facilitate technology diffusion or conversely, hinder the diffusion process (Haleem et al., 2020). Strong governmental support is one of the fundamental drivers of the rapid diffusion of fintech adoption in various markets (Kaiser et al., 2022). In this study, government support is considered in terms of proactive regulatory frameworks, pro-fintech legislation, and the establishment of essential infrastructure, such as telecommunications networks, to support the growth of fintech. Thus, the study proposed the hypothesize,

The Mediating Role of Digital Transformation

Digital transformation plays an important role in improving competitiveness and bank performance. Previous research confirms its positive impact, though some findings show mixed results (Westerman et al., 2014). Industries that successfully adopt digitalization tend to generate higher revenues. Managers recognize that innovation enhances performance and acts a mediator in this process. While studies (Kastelli et al., 2024; Valmohammadi, 2017) have examined the direct effect of technology innovation and dynamic capabilities, limited research has explored the mediating role of digital transformation in linking technology, organizational, and government support with performance. Understanding this mediating role is essential for maintaining a sustainable position in the financial sector by delivering innovative services that meet customer needs and boost sales.

Digital transformation plays a crucial role in improving financial reporting processes, enhancing transparency and increasing efficiency in financial institutions (Putra et al., 2024). Studies research by Guang-Wen and Siddik (2023) suggests that financial initiatives aimed at sustainability transform banking activities, with technological innovation acting as a catalyst for sustainable financial outcomes. The shift toward digital and environmentally improves operational efficiency as well as meeting increasing demand for sustainable finance, thereby fostering a greener financial ecosystem. Based on this, the study proposes the following research hypothesis.

Mediating Role of Fintech Adoption

According to Amit and Han (2017) AI, big data, and IoT have driven technological advancements in the banking sector advancing the adoption of fintech. The implementation of these digital technologies has brought significant changes within organization (Buchak et al., 2018) . According to Tripathy and Jain (2020) fintech companies have leveraged this technology to transform financial services, optimize resources and enhance customer engagement. In the banking sector, fintech play a crucial role in mediating adoption. For instance, Tian et al. (2023) examines how the adoption of fintech by banks impacts business performance. The intention to use financing platforms is significantly influenced by various factors which in turn affect business performance (Figure 1). Based on this, the study proposes the following research hypothesis

Conceptual framework of research.

Data and Methods

The respondents were selected from private, public and co-operative sector banks to ensure a comprehensive representation of banks at different stages of digital transformation. The data were anonymized, and no personal information, such as contact numbers or email addresses, was collected. To ensure ethical compliance, informed consent was obtained from all participants before their involvement in the study. Participation was entirely voluntary, with individuals having the right to withdraw at any stage without any repercussions. Furthermore, no minors were recruited for the survey to uphold ethical guidelines and ensure the appropriateness of participant selection. These measures collectively prioritized the privacy, autonomy, and well-being of all participants involved (

The research utilizes four measures to evaluate technology capability (Khin & Ho, 2019; Saarikko et al., 2020), four measures to assess organizational capability (Martinez-Caro et al., 2020; Songkajorn et al., 2022) and five items to assess for government support (Amin et al., 2011). Additionally, four items measure digital transformation (Schallmo et al., 2020; S. Singh et al., 2021), seven item evaluate fintech adoption (Dwivedi et al., 2021), and four items assess bank performance (Miguel et al., 2022; Sledziewska and Włoch, 2021) . The selection of questionnaire item was based on reputed indexed journal and the items were chosen for their high outer loadings, demonstrating validity and reliability. The survey used a 5-point Likert scale, where 1 represents “Strongly disagree” and 5 represents “Strongly agree.”

Tamil Nadu, located in southern India is one of the country’s leading states in financial inclusion and banking activities. With 8,678 commercial bank branches, it ranks as India’s third-largest state in terms of banking infrastructure. Within Tamil Nadu, in and around Chennai, accounts for approximately 30% of the state total banking operations (Kumar et al., 2024). Chennai is recognized as a financial hub and the headquarters of various prominent banks and exhibiting significant financial activity with rapid technological integration, which supports this study (Rha & Lee, 2022). Since their expansion into India, the majority of banks, including domestic financial institutions, have established a presence in key financial centers such as Chennai, confirming its strategic importance in the financial service industry (Tiberius et al., 2022) This study focuses on bank employees involved in implementing digital banking services and technologies with their organizations.

In this study, purposive sampling was used to determine the sample based on Hair et al. (2021). The study focused on mid-level professionals, including assistant managers, IT officers, risk, and compliance officers, customer service representatives and cashier, as they play a crucial role in operational efficiency, regulatory compliance and the adoption of digital transformation and fintech solutions within the banking sector. Before full data collection, a pilot study was conducted with 50 bank employees in and around Chennai to assess the clarity, and ease of understanding of the questionnaire. The data collection was conducted between August 2024 and October 2024. To ensure wider accessibility and participation, the questionnaire was distributed online vid Google Form allowing respondents to complete it at their convenience. A total of 400 responses were received. After filtering out incomplete and irrelevant responses, a final of 325 valid responses was retained, maintaining the 1:10 ratio recommended sampling ratio (Hair et al., 2021). The structured sampling, pilot testing, and data screening methods enhance the accuracy and reliability and providing valuable insights into the influence of digital transformation on the banking sector.

Sample Demographics

Table 2 presents the demographic profile of respondents, highlighting gender, bank type, job designation, and fintech service usage. Among 325 respondents, the majority are male (50.77%) and employed in private sector banks (47.25%). Most respondents in this study work as customer service (52%). In terms of fintech adoption, mobile banking is the most widely used service, with 52.31% of respondents. These demographics were considered control variables, based on the assumption that they do not directly influence bank performance.

Demographics Profile.

Note. Created by author.

Descriptive Statistics

Table 3 presents the descriptive statistics of the sample including mean, median, standard deviation, minimum and maximum values. The mean value for gender is 1.49, with a median of 1 and SD of 0.501. For the type of bank, the mean is found 1.76, the median is 2 and the SD 0.687, indicating a higher representation of private bank employees, Job designation has a mean of 1.87, median of 1, and a SD 1.139, reflecting the designation roles. Fintech service usage shows a mean of 1.64, median of 1 and SD 0.751 highlighting different level of adoption among respondents.

Descriptive Statistics.

Note.Created by author.

Data Analysis

This study employed PLS-SEM analysis with SmartPLS 3.3, a widely used method for evaluating the measurement reliability, validity and structural relationship. PLS-SEM is effective in testing hypotheses and identifying casual paths. However, its reliance on linear correlations may not fully capture the complex interaction among variables. To enhance predictive capacity and identify non- linear relationships, this study incorporated Artificial Neural Network (ANN). The ANN model was created utilizing feature scores from the PLS-SEM model, enabling non-linear validation of the relationship (Liébana-Cabanillas et al., 2017). ANN is particularly effective in detecting hidden, complex patterns that statistical models may overlook. ANN was implemented using a multi-layer perceptron with a feed-forward-backward-propagation (FFBP) algorithm, incorporating two hidden layers to enhance learning capabilities (Leong et al., 2020).

We utilized data from the banking sector in India particularly in and around Chennai, conducted demographic and descriptive statistical analysis using SPSS. Additionally, we applied Partial Least Squares Structural Equation Modeling (PLS-SEM) and Artificial Neural Networks (ANN). While SEM generally require a minimum of 100 data records to provide reliable results, our study comprises 325 data records.

According to Astrachan et al. (2014) PLS-SEM is suitable for evaluating complex model with multiple indicator variables. Furthermore, we integrated Artificial Neural Networks (ANN) to uncover non-linear relationship within the model, which are crucial for more effective decision making (Lo et al., 2022). One limitation of PLS-SEM is that it identifies only linear relationships therefore, ANN was used to address this limitation. Furthermore, the most important predictors were ranked based on normalized importance, where the variable with highest influence is highlighted (C. Yan et al., 2022). Figure 2 illustrates the research methodology flowchart. By combining PLS-SEM and ANN, this study strengthens both theoretical validation and predictive accuracy. PLS-SEM provides a structured, statistically confirmation of the hypothesized relationship while ANN examines the strength and non- linearity of these relationships. This hybrid approach enhances the robustness of the findings, making them more generalizable and practically applicable.

Flowchart for research methods.

Results

Measurement Model

Outer Loadings, Reliability and AVE

We conducted data analysis using the two-step approach of Partial Least Squares Structural Equation Modeling (PLS-SEM) as recommended by Henseler et al. (2015). In the initial stage, we evaluated the measurement model by assessing the reliability of the items, retaining those with loadings of 0.50 or higher, as recommended by Hair et al. (2017). To ensure convergent validity, we calculated the Average Variance Extracted (AVE) and confirmed that the values for each latent variable were 0.50 or above. Additionally, we assessed internal consistency reliability by evaluating composite reliability (threshold > 0.70) and Cronbach’s alpha (threshold > .70). While most results met the required thresholds, item FA6 and GS3 consistently failed to meet the outer loading criterion. Therefore, following Ramayah et al. (2018) we removed FA6 and GS3 to improve the model reliability and validity. All other results were within the specified limits, as presented in Table 4.

Construct Validity and Reliability.

Note. Alpha = Cronbach alpha; CR = composite reliability; AVE = average variance extracted; VIF = variance inflation factor.

As shown by a Cronbach alpha coefficient of .754, a rho-A coefficient of .763, a CR coefficient of .844, and an AVE coefficient of .575, technology capability measured using 4 items (TC1 to TC4) with loadings ranging from .718 to .783 is reliable and valid. VIF values varied from 1.378 to 1.605, demonstrating no multicollinearity. Organizational capability was evaluated using four items (OC1 to OC4) with loadings from 0.643 to 0.841. Despite moderate validity, this construct is still considered acceptable, as evidenced by Cronbach’s alpha (CA = .761, rho-A = .784, composite reliability (CR = .846), and average variance extracted (AVE = .581). VIF scores from 1.381 to 1.797 indicating no multicollinearity. Government support was assessed using five items (GS1–GS5) with loadings from 0.774 to 0.828, indicating excellent reliability and validity. GS3 was eliminated due to poor outer loading. A Cronbach alpha of .822, rho-A coefficient of .823, composite reliability (CR) of .882, and average variance extracted (AVE = .652) confirm the construct’s dependability. VIF values ranged from 1.534–2.080 indicating no multicollinearity. The Fintech adoption construct included 7 elements (FA1 to FA7) with loadings ranging from 0.687 to 0.733 indicating moderate reliability. FA6 was omitted due to its low outer loading. Cronbach’s alpha (CA = .810, rho-A = .816, CR = .860, and AVE = .521) confirm its reliability. VIF scores ranged from 1.772 to 1.875 indicating no multicollinearity. Digital transformation was measured using four items (DT1–DT4) with loadings ranging from 0.612 to 0.848. Cronbach’s alpha (CA) of .746, rho-A coefficient of .763, composite reliability (CR) of .841, and average variance extracted (AVE = .572) demonstrate strong construct reliability. VIF scores ranged from 1.380 to 1.900 confirming the absence of multicollinearity. Bank performance has four items (BP1–BP4) with loadings ranging from 0.684 to 0.835. The Cronbach’s alpha coefficient of .757, rho-A coefficient of .767, and composite reliability (CR) .846 confirm strong reliability and validity, although the average variance (AVE) is .580. VIF scores ranged from 1.381 to 1.855 which are acceptable and indicate no multicollinearity.

Discriminant Validity

The Heterotrait-Monotrait (HTMT) ratio was calculated as the measure of discriminant validity. According to recommendation, HTMT values between any two variables should always be below 0.9 for adequate discriminant validity. Table 5 lists the HTMT values, all of which fall below 0.9. This provides further support for the discriminant validity of the model; it also strengthens the confidence in the measurement model ability to exactly capture the constructs under the observations.

HTMT Criterion.

Note.Created by author.

In this study, second-order constructs such as the TOE framework were taken from lower-order construct scores. To examine collinearity in PLS-SEM, we used the Variance Inflation Factor (VIF). As shown in Table 6, all VIF values for formative indicators were below the threshold of 3 (Hair et al., 2019) confirming that there was no multicollinearity issue within the TOE framework. To establish convergent validity for the second-order TOE framework, we assessed the Average Variance Extracted (AVE). Since the TOE framework follows a reflective-formative structure, we evaluated its reliability and validity using the repeated indicator approach. Table 6 present both the VIF values and repeated indicator results demonstrating that all values met the required threshold. Although the loading for government support was slightly below the recommended level, the items was retained following the guidelines of Garson (2016) (Figure 3).

Higher Order Construct Measurement.

Reflective-formative model.

Structural Model

The structural model includes model fit, R squared values, and hypothesis testing results. The model has been analyzed to assess its robustness and suitability for the data. In addition to reliability and validity checks, SRMR and NFI were used to evaluate its strength. As proposed by Hu and Bentler (1999), an SRMR value indicates 0.08 indicates a good fit, while some researchers suggest that value below 0.10 level are still acceptable. In this study, the SRMR value is 0.06, confirming the model’s fit. Similarly, the NFI should be 0.90 or higher, with values closer to 1.00 indicating a stronger fit. This model gives an NFI of 0.95, supporting its structural validity. Overall, these results demonstrate that the model is well-fitted and reliable. Table 7 presents the fit indices.

Model Fit.

Note.SRMR =Standardized Root Mean Square Residual; NFI = Normal Fit Index.

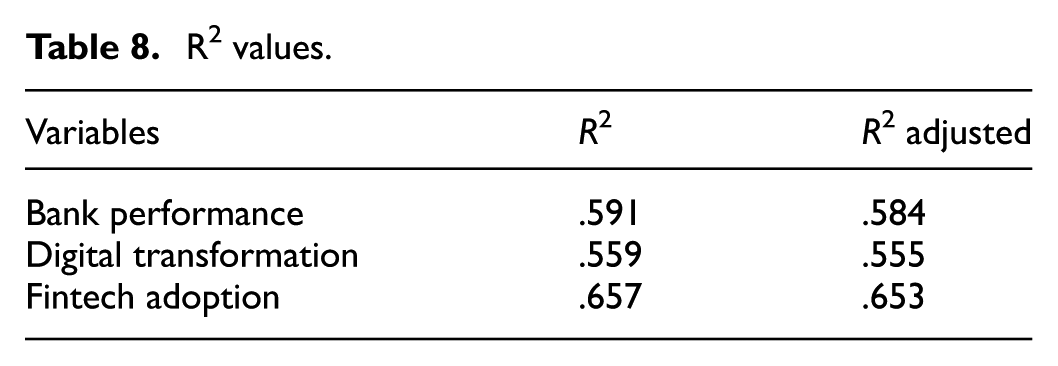

The R-squared (R 2) value in a regression model indicates the extent to which the independent variables explain changes in the dependent variable. The partial least squares algorithm shows that the R 2 values for the original constructs represents the significant power of the model. The model explains approximately 55% of the variations in digital transformation. It explains 65% of the variations in bank’s fintech adoption. Even when considering the number of factors, the adjusted R 2 remains high at 65.3%. The model accounts for 59.1% of the variations in bank performance. When the number of predictors is considered, the adjusted R 2 slightly decreases to 58.4%. These values indicate the extent to which independent variables explain variations in the dependent variable (Table 8).

R2 values.

Hypothesis Testing

Once the measurement model was completed, we determined the appropriate validation strategy for testing the hypotheses. Smart PLS-3 was used to analyze the research hypotheses. The structural model was used to test the hypotheses by calculating p-value and t-values. A hypothesis is accepted if the t-value exceeds 1.96 and the p-value is below .05. To ensure the results, bootstrapping with 5,000 subsamples was performed. Figure 4 and Table 9 displays the results of the hypotheses.

Structural model.

Path Coefficients.

Establishing the Mediation Effect

The mediation effect measures, the extent to which the relationship between a predictor and an outcome change when a mediator is included. In this case, the predictor influences the outcome through the mediator. Researchers have suggested key methods for testing mediation (Baron & Kenny, 1986) proposed using Sobel Z-test, while structural equation modeling (SEM) with the bootstrap approach is also commonly used for a more detailed analysis. The mediation effect of digital transformation and fintech adoption on the relationship between technology, organizational and environmental Capability (TOE) and bank performance was tested using bootstrapping and the Sobel Test. The bootstrapping results for the mediation effect are presented in Table 10.

Mediation Analysis.

Tables 11 and 12 present the results of the Sobel test conducted to assess the mediating effect of (FA and DT) on the relationship between independent variable (TOE) on a given dependent variable bank performance. The Sobel test indicated that the p-value is less than 0.05, assuming that the two-tailed z-test is higher than 1.96. Based on this, the research hypothesis is accepted, confirming that FA and DT mediate the relationship between the relationship between TOE and bank performance.

Influence of the Mediating Variable Using the Sobel Test.

Influence of the Mediating Variable Using the Sobel Test.

IPMA Analysis

Table 13 presents the Importance-Performance Map Analysis (IPMA) offering practical insights for managers to support informed decision making. This analysis evaluates the performance and importance of several latent variables (LVs) and their impact on a target variable. The findings highlight the performance level of different factors, providing a clearer understanding of which latent variables contribute most to enhancing overall outcomes. This information help mangers prioritize initiatives effectively and allocate the resources where they will have the greatest impact.

IPMA Analysis.

The Importance-Performance analysis provides valuable insights into the factors that influencing bank performance. Government support emerges as a pivotal factor achieving one the highest score of 73.655. This indicates that strong regulatory frameworks and government initiatives significantly foster banking operations, enhance growth and innovation in the financial sector. Bank performance with a score of 73.084, reflects a high level of operational efficiency and effectiveness in achieving strategic objectives, demonstrating the institution’s ability to navigate complexities, while providing value to stakeholder. Technology capability, scoring 72.751, highlights a solid foundation in technological resources that is necessary for fostering digital transformation and the effectively adopting fintech solutions. Digital transformation itself 69.424, indicating its significance in integrating digital technologies into banking operations. However, remains substantial potential for further advancements to enhance efficiency and foster innovation. Fintech adoption, with a score of 67.492, signifies moderate level of integration within bank performance. This emphasizes the need for a strategic focus on enhancing overall performance and maintaining competitiveness in a rapidly evolving landscape. Lastly, organizational capability, scoring 65.442 indicates a need for improvement in structural and operational capacities, which are crucial for achieving better performance. This highlights key strategic areas that require attention and development (Figure 5).

IPMA constructs.

ANN Analysis

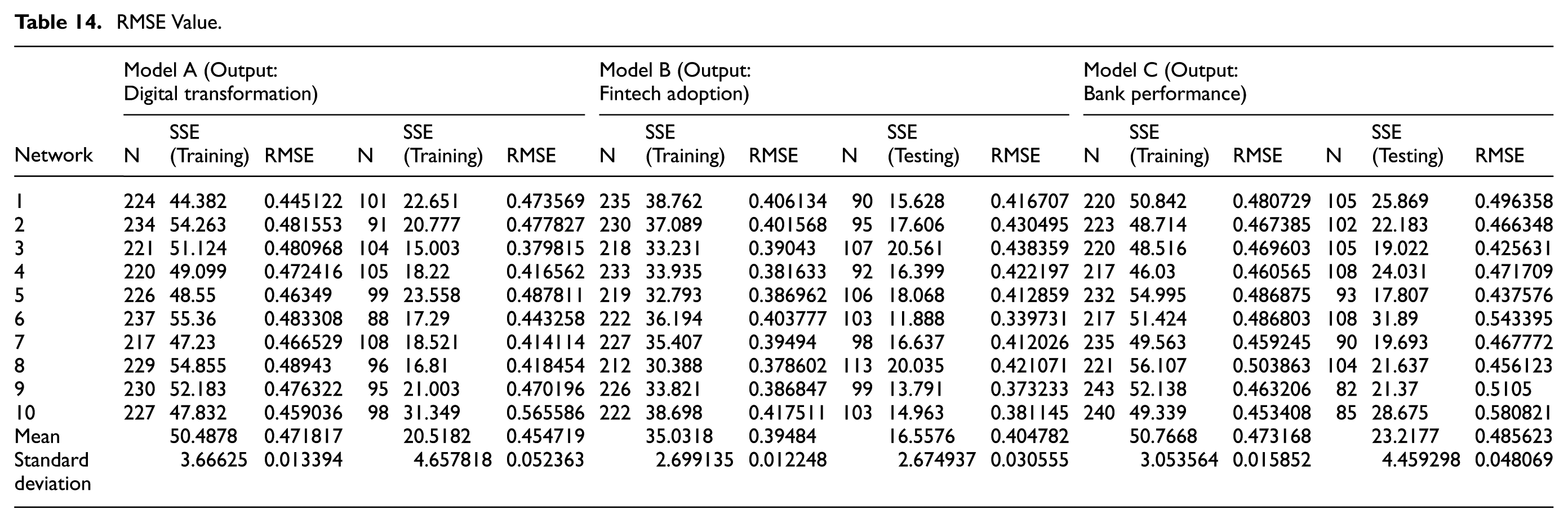

According to Haykin (1994) an Artificial Neural Network (ANN) is a parallel computing system composed of simple processing units capable of retaining practical skills and making them readily applicable. It is aligned with standard regression technique (Lo et al., 2022). In our research we utilized SPSS software to conduct ANN analysis, integrating variables from the PLS-SEM model into the ANN framework. The variables examined include TC, OC, GS, DT, FA, and BP. According to Sharma and Sharma (2019) for data testing and training we utilized cross-validation methods with a 70:30 partition. The scaled conjugate gradient optimization algorithm was used for training. The first model consists of a one output neuron (DT), one hidden layer, and three input neurons (i.e., TC, OC, and GS). Similarly, the second model has one output neuron (FA), one hidden layer, and three input neurons (i.e., TC, OC, and GS). Finally, the third model has one output neuron (BP), one hidden layer, and two input neurons (i.e., DT and FA). The sigmoid activation function was applied to both the hidden and output neuron. Figures 6 to 8 displays the three ANN model (Table 14).

Artificial network diagram for (Digital Transformation).

Artificial network diagram for (Fintech Adoption).

Artificial network diagram.

RMSE Value.

Additionally, the range between the input and output neuron was maintained within (0,1). The ANN model yielded mean RMSE values of 0.471817, 0.454719, 0.39484, 0.404782, 0.473168, and 0.485623. The RMSE (Root Mean Square Error) was used to evaluate the precision of the neural network. The RMSE was computed utilizing the formula

where, SSE denotes the sum of squared errors for both the training and testing datasets, and N represents the sample size for the corresponding datasets.

Next, we performed a sensitivity analysis to determine which independent variables are significant. We ranked the neurons based on the contribution to the dependent variable as shown in Table 15. The Calculation for normalized importance determines the significance of each neuron by dividing its value by the highest observed value and interpreting the results as a percentage (Leong et al., 2013). GS is the primary driver of bank performance followed by fintech adoption.

Sensitivity Analysis.

Discussion

This study examines the impact of technology capability, organizational capability, and government support on digital transformation, fintech adoption, and bank performance using the TOE framework. The findings highlight the significance of these factors in shaping digital banking initiatives, aligning with both theoretical foundation and prior research. The study confirms that technology capability, organizational capability, and government support significantly influence digital transformation and fintech adoption, which aligns with TOE framework (Tornatzky et al., 1990). Technology capability plays a crucial role in banks to adopt financial technologies and digital solutions facilitating smoother digital transitions (Konopik et al., 2022; T. Li & Chan, 2019). The findings indicate that technology capability impacts digital transformation (β = .205, p = .000) and fintech adoption (β = .119, p = .009) supporting previous studies. However, the direct effect of technology capability on bank performance was (β = −.059, p = .315), suggesting that technological investment alone does not result to better financial performance unless it is effectively integrated with organizational processes and government support (Albukhitan, 2020; Bharadwaj et al., 2013). Similarly, organizational capability significantly contributes to the adoption of fintech (β = .333, p = .000) as well as digital transformation (β = .182, p = .003). This finding supports earlier research emphasizing the importance of leadership, skilled employees, and structured business processes in facilitating digital adoption (Vial, 2021). However, the results indicate that organizational capability does not directly impact bank performance (β = .070, p = .330) diverging from previous studies (Akhtar et al., 2024; Hasan et al., 2024). This suggests that organizational resources must be combined with external regulatory frameworks and financial incentives for banks to fully capitalize on digital advancements. Government support is found to be the most influential factor, significantly impacting digital transformation (β = .524 p = .000). These findings align with other studies that emphasize the role of financial regulations, policy incentives, and technological infrastructure in promoting digital banking adoption (Sung, 2019; Wang et al., 2023). Government support has a direct impact on bank performance (β = .256 p = .000), confirming that regulatory frameworks and innovation policies are key drivers of banking performance (Palos-Sánchez et al., 2023; Scaliza et al., 2022). Furthermore, the study examines how fintech adoption and digital transformation mediate the relations between TOE factors and bank performance. The findings indicate that digital transformation partially mediates the relationship between government support (β = .154, p = .001), organizational capability (β = .053, p = .013), and technology capability (β = .06, p = .020) on bank performance, suggesting that banks leveraging digital transformation experience enhanced performance (Nguyen-Thi-Huong et al., 2023). Similarly, fintech adoption act as a partial mediator indicating that fintech solutions improve operational efficiency, customer service thereby improving performance (Zhu & Jin, 2023). It also confirms that both fintech adoption and digital transformation significantly enhance bank performance (β = .294, p = .001; and (β = .298, p = .000) for digital transformation. These results validate prior studies highlighting the contribution of digital banking ecosystems toward operational efficiencies, cost savings and improved customer engagement (Balaskas et al., 2024; Igamo et al., 2024; Sivaramakrishnan et al., 2017). Furthermore, the results emphasize that technology and organizational capability alone are not sufficient for improving bank performance, they must be strategically leveraged through fintech and digital transformation initiatives to achieve optimal results. This aligns with Dynamic Capability theory (Teece et al., 1997) which suggests that financial institutions must continuously integrate technological resources to sustain competitive advantages in an evolving digital environment. The results indicate that both DT and FA play an important mediating role in enhancing bank performance, with FA demonstrating a stronger impact. This implies that banks actively integrate and leverage fintech innovation experience a greater indirect effect on performance compared to those focusing primarily on digital transformation. Previous research (Aldaarmi, 2024; Khalil et al., 2022; Sajid et al., 2023) has also highlighted the DT and FA as mediator, but our study suggest that FA play a more dominant role. Fintech adoption significantly enhances financial accessibility, service innovation and competitiveness indicating that banks should not only focus on digitalizing their process but also actively adopt fintech solution to drive long-term performance growth. Both the bootstrapping and Sobel test confirm the significance of mediation effect for digital transformation and fintech adoption in enhancing bank performance. The result consistently show that FA has a stronger mediation effect emphasizing its role in driving innovation and competitiveness.

Governments have implemented measures to ensure a safe, stable and innovative environment as financial institutions increasingly adopt fintech solution. Several important initiatives demonstrate how government involvement accelerates this transformation. For example, regulatory frameworks established by financial regulators such as the Reserve Bank of India (RBI) enable fintech startups and banks to experiment with new financial technologies with a controlled regulatory environment to ensure compliance and foster innovations (M. Li et al., 2022). Another important example is the Unified Payments Interface (UPI), which has transformed the digital transactions landscape in India. With its fast, secure, and low-cost payment system, UPI has encouraged widespread adoption of digital banking services (Zhu & Jin, 2023). Such initiatives not only facilitate digital payments but also help to build consumer trust in digital financial services.

The government is increasingly enforcing cybersecurity and data protection regulations to enhance trust in fintech. Legislations such as India’s Personal Data Protection Bill (PDPB) ensure that financial companies implement strong data governance, AI-led fraud detection, and risk management frameworks to protect consumers from cyber threats (T. Chen et al., 2023). Additionally, regulators are collaborating on open banking frameworks that secure financial data-sharing with third-party fintech providers while maintaining regulatory oversight to spur innovation (Palos-Sánchez et al., 2023). To further strengthen financial security, governments are integrating AI-driven fraud detection tools and real-time credit risk assessment, to help banks mitigate financial risks while ensuring transparency in digital transactions. These efforts enable financial institutions to balance digital transformation with technological innovations, compliance, security, and financial stability.

Theoretical Implications

The theoretical implication derived from this research contribute significantly to the field of capabilities, fintech innovation and digital transformation. By integrating capabilities into the TOE framework, this study highlights the effectiveness of TOE as a model particularly within the banking industry. The integration of TOE with dynamic capability theory enhances the understanding of innovation and organizational development. Furthermore, it provides a framework for banks and financial institutions aiming to maximize resources and capitalize on emerging opportunities effectively.

This research emphasizes the theoretical significance of integrating dynamic capability theory with the TOE framework based on the findings. It suggests that (DCT) can be leveraged to identify and align with the elements of TOE framework. The empirical findings demonstrate that digital transformation capabilities when incorporated into the TOE framework and DCT, effectively facilitate both digital transformation and fintech adoption. This study further highlights the growing importance of a technical-driven approach in guiding digital transformation efforts. Additionally, it validates that applying capabilities through the TOE framework and DCT yields positive outcome for digital transformation improving bank performance. This research makes a significant contribution to the existing literature by showing how performance can be enhanced through digital transformation particularly when guided by the TOE framework and DCT.

While technology capability and organizational capability do not directly influence digital transformation, it shows a positive impact when fintech adoption mediate the relationship. This understands the role of fintech adoption in enhancing the relationship between organizational and technological capabilities aligning with Dynamic Capability Theory within the TOE framework. Finally, this study provides empirical evidence highlighting the significance of government support within the TOE framework environmental dimensions. Government support plays an important role in enhancing digital performance by including risk perception and the regulatory compliance. The empirical findings suggest that government support is essential for managing digital risks successfully, ensuring effective banking regulations and contributing to the overall success of the digital transformation initiatives.

Managerial Implications

This study provides important managerial implications for the banking sector in India, with potential applicability to other countries. Successful digital transformation in banking requires a clear understanding of both technical and non-technical aspect. Key factors influencing dynamic capabilities which integrate technology, organizational capabilities, government support, and fintech adoption. These elements are crucial in driving industry progress toward digital transformation. Moreover, government support plays a vital role in promoting business development by addressing digital risks and establishing appropriate regulatory frameworks. Managers should develop agile strategies that align with evolving regulations while leveraging government-backed incentives such as tax benefits and digital infrastructure investments. By ensuring between digital adoption and regulatory frameworks banks can accelerate digital adoption, enhance operational resilience, and strengthen long-term competitiveness in an evolving financial ecosystem.

Practical Implications

Investing in digital innovation fosters operational efficiency, enhances customer engagement, and improve overall bank performance. Incorporating DT is essential for banks to remain competitive. Banks should integrate fintech into their operations to improve service quality, manage risk efficiently, and encourage active customer participation. This will enable banks stay competitive in an ever-evolving financial environment. Government support plays a vital role in fostering banking innovation by providing regulatory frameworks, policies, and guidelines that facilitate smooth digital transitions while maintaining financial stability. A supportive regulatory environment promotes innovation and improve performance. Policymakers must continuously reform regulations to keep pace with fast-changing digital landscape, thereby enhancing banking performance. As digital transformation evolves it becomes important for financial institutions and regulatory authorities to adapt policies that drive research and development in this domain. Banks, particularly cooperative banks are upgrading their technological infrastructure to accelerate digital transformation efforts. Identifying the key factors influencing digital adoption will help banks enhance their operational efficiency and improve overall performance in a competitive environment. It is essential for banks to recognize the importance of digital transformation and take proactive steps to meet the demands of the financial sector. Digital transformation will not only optimize operations but also ensure long-term success in an increasingly dynamic market.

Limitations and Future Research Avenues

This study highlights the relationship between TOE (Technological-Organizational-Environment) framework, digital transformation, fintech adoption, and bank performance, However, certain limitations provide directions for future research. While this study focuses on employees from banks that broader applicability of the findings. While this study focuses on Chennai, and its surroundings, India due to its large banking presence and rapid fintech adoption, the findings remain relevant to other countries with similar financial systems. Many financial hubs worldwide face challenges related to digital transformation, fintech adoption and regulatory frameworks. In highly regulated banking environments this study’s results provide insights into how regulatory framework influence fintech adoption and banking performance. Future studies should incorporate a more diverse demographic across various banking sector and cultural contexts to enhance the global relevance of the findings.

Additionally, this study is geographically limited to the banking sector, which may not fully capture the global diversity in the influence of digital transformation and fintech adoption. Furthermore, this study employs a cross-sectional approach, analyzing the relationship between variables at a single point in time. Longitudinal research would provide deeper insights into this relationship, particularly in light of rapidly technological and regulatory changes in the financial sector. Such an understanding would give a deeper insight into how companies adapt and sustain performance in the digital landscape over time. Finally, this study recommends exploring moderators and mediators that influence the digital transformation such as financial literacy, digital literacy technological readiness, risk aversion and market conditions. In emerging markets where digital transformation is still evolving, these findings can help policymakers in balancing financial innovation with regulatory challenges. Even in regions with varying technological infrastructures the relationships identified in this study such as the impact of digital transformation and fintech adoption on bank performance remain highly relevant. Future research could test this model in different geographical locations or banking system to compare outcomes and further strengthen its generalizability.

Conclusions

This study set out to examine the impact of digital transformation (DT) and fintech adoption (FA) on bank performance in the Indian context, with data collected from the Chennai region. Leveraging a two-stage SEM–ANN analytical approach, the findings provide compelling evidence that both government support and digital transformation are critical enablers of enhanced banking performance. Digital transformation, through advanced technologies, significantly streamlines banking operations, reduces customer friction, and improves service delivery. Government support—through effective regulatory frameworks, strategic policies, and innovation incentives—emerges as a vital external capability that fosters an environment conducive to technological advancement and operational agility. The study further reveals the strong mediating roles of DT and FA in the relationship between technological, organizational, and environmental capabilities and bank performance. These mediators enhance the indirect effects of internal and external capabilities on performance outcomes. The ANN sensitivity analysis confirms the paramount importance of government support and DT as key performance drivers. Overall, the findings underscore that banks can significantly improve operational efficiency, customer satisfaction, and strategic agility by leveraging digital transformation and fintech adoption. Policymakers and banking leaders should prioritize ecosystem-wide support mechanisms and digital innovation strategies to sustain competitive advantage and long-term performance in the evolving financial landscape.

Footnotes

Appendix

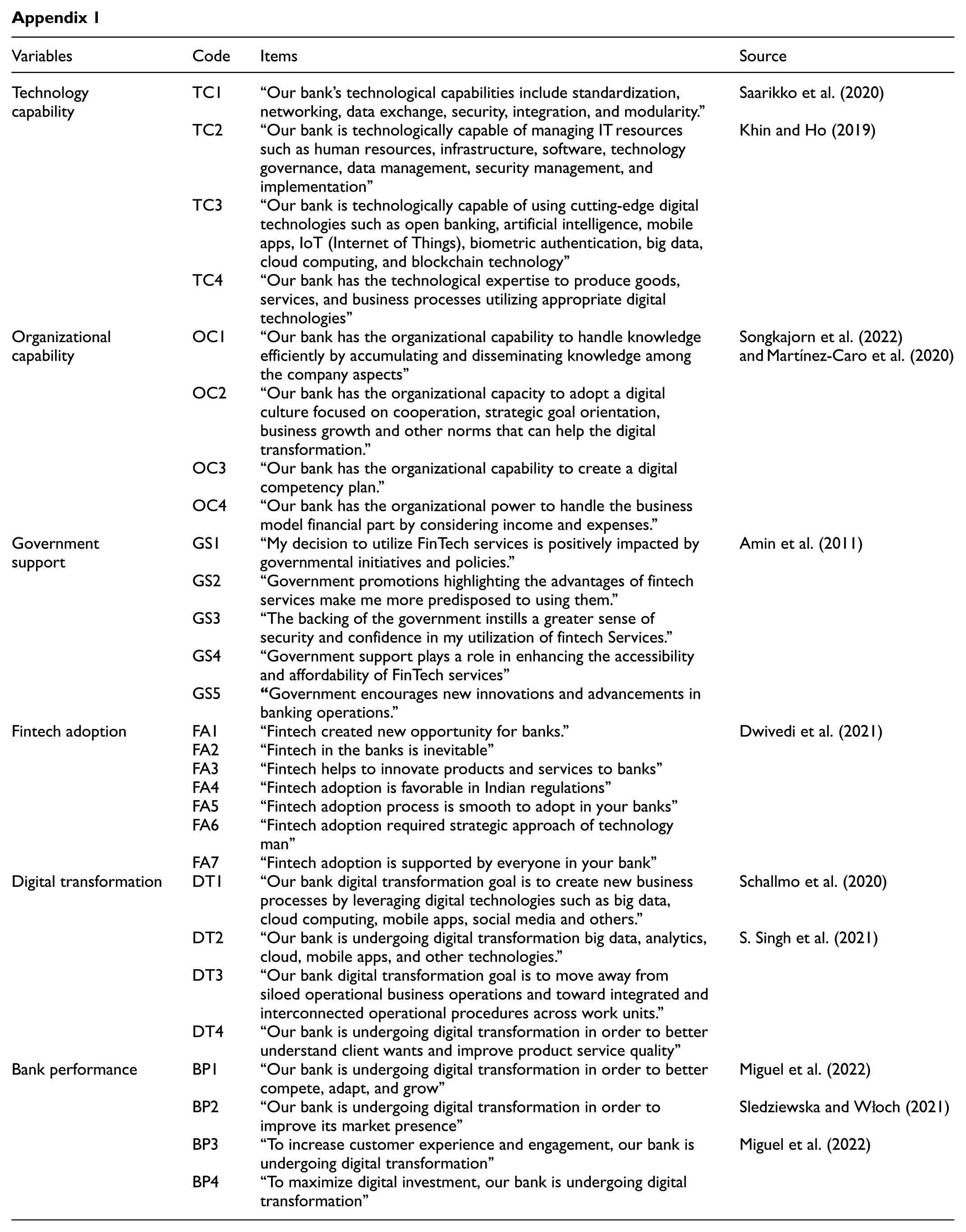

| Variables | Code | Items | Source |

|---|---|---|---|

| Technology capability | TC1 | “Our bank’s technological capabilities include standardization, networking, data exchange, security, integration, and modularity.” | Saarikko et al. (2020) |

| TC2 | “Our bank is technologically capable of managing IT resources such as human resources, infrastructure, software, technology governance, data management, security management, and implementation” | Khin and Ho (2019) | |

| TC3 | “Our bank is technologically capable of using cutting-edge digital technologies such as open banking, artificial intelligence, mobile apps, IoT (Internet of Things), biometric authentication, big data, cloud computing, and blockchain technology” | ||

| TC4 | “Our bank has the technological expertise to produce goods, services, and business processes utilizing appropriate digital technologies” | ||

| Organizational capability | OC1 | “Our bank has the organizational capability to handle knowledge efficiently by accumulating and disseminating knowledge among the company aspects” | Songkajorn et al. (2022) and Martínez-Caro et al. (2020) |

| OC2 | “Our bank has the organizational capacity to adopt a digital culture focused on cooperation, strategic goal orientation, business growth and other norms that can help the digital transformation.” | ||

| OC3 | “Our bank has the organizational capability to create a digital competency plan.” | ||

| OC4 | “Our bank has the organizational power to handle the business model financial part by considering income and expenses.” | ||

| Government support | GS1 | “My decision to utilize FinTech services is positively impacted by governmental initiatives and policies.” | Amin et al. (2011) |

| GS2 | “Government promotions highlighting the advantages of fintech services make me more predisposed to using them.” | ||

| GS3 | “The backing of the government instills a greater sense of security and confidence in my utilization of fintech Services.” | ||

| GS4 | “Government support plays a role in enhancing the accessibility and affordability of FinTech services” | ||

| GS5 |

|

||

| Fintech adoption | FA1 | “Fintech created new opportunity for banks.” | Dwivedi et al. (2021) |

| FA2 | “Fintech in the banks is inevitable” | ||

| FA3 | “Fintech helps to innovate products and services to banks” | ||

| FA4 | “Fintech adoption is favorable in Indian regulations” | ||

| FA5 | “Fintech adoption process is smooth to adopt in your banks” | ||

| FA6 | “Fintech adoption required strategic approach of technology man” | ||

| FA7 | “Fintech adoption is supported by everyone in your bank” | ||

| Digital transformation | DT1 | “Our bank digital transformation goal is to create new business processes by leveraging digital technologies such as big data, cloud computing, mobile apps, social media and others.” | Schallmo et al. (2020) |

| DT2 | “Our bank is undergoing digital transformation big data, analytics, cloud, mobile apps, and other technologies.” | S. Singh et al. (2021) | |

| DT3 | “Our bank digital transformation goal is to move away from siloed operational business operations and toward integrated and interconnected operational procedures across work units.” | ||

| DT4 | “Our bank is undergoing digital transformation in order to better understand client wants and improve product service quality” | ||

| Bank performance | BP1 | “Our bank is undergoing digital transformation in order to better compete, adapt, and grow” | Miguel et al. (2022) |

| BP2 | “Our bank is undergoing digital transformation in order to improve its market presence” | Sledziewska and Włoch (2021) | |

| BP3 | “To increase customer experience and engagement, our bank is undergoing digital transformation” | Miguel et al. (2022) | |

| BP4 | “To maximize digital investment, our bank is undergoing digital transformation” |

Ethical Considerations and Informed Consent

To ensure ethical compliance, informed consent was obtained from all participants before their involvement in the study. Participation was entirely voluntary, with individuals having the right to withdraw at any stage without any repercussions.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The datasets generated during and/or analyzed during the current study are available from the corresponding author on reasonable request.