Abstract

Given that banking in economies of transition fluctuate heavily, we explore the effect of regulatory norms on performance of banking industry. In particular, we examine the effect of Reserve Requirements, Activity Restrictions, and Capital Stringencies on the overall industry profitability and stability of the financial institutions. We utilize the Generalized Methods of Moments methodology to the panel data regressions over 17 different transitional economies during, and after the crisis period of 2008 through to 2019. Our results show that the Reserve Requirements regulatory norm is the only significant factor that improves the profitability and diminishes the risk of financial instability. The findings are confirmed with our tests over the regional sub-samples. This research sheds the light on the necessities of political and economic reforms in banking for these markets in transition.

Introduction

The fallout from the financial crisis of 2008 had been enormous. Markets were not ready for the crisis and shock which unearthed the harsh reality that many of the reforms, regulations, and newly implemented management strategies had undisguisable weaknesses riddled across many, if not all of the world’s developed and developing economies (Hartwell, 2015). The pre-crisis period of profitability had been growing exponentially for most stable financial institutions (Shehzad et al., 2013). However, the best-assumed risk-adjusted financial models of developed economies struggled during the crisis, offering no viable contingency plan, eventually plunging the markets into despair (Al-Matari et al., 2014). Therefore, these unique challenges required a new set of regulatory standards, heavy financial reforms, and a level up of supervision. Many of the market players introduced vigilant internal checks as part of their permanent audit functions within their respective companies. Many international central regulators directed these entities to correspond with the newly adjusted worldwide measures as the “Basel standards.”

The crisis had questioned whether the existing framework of system regulation and surveillance had in part, been to blame for the crisis itself (Sabato, 2009). These events bubbled up the layman’s distrust toward financial and governmental norms and regulations, and appropriately raised the question of whether newly introduced policies and compliance with them would increase the financial stability and performance of these longstanding financial institutions. King and Levine (1993) studied the economic growth of different countries and found that a well-established financial market positively affected the economic growth of these nations.

Financial institutions differently perceive similar norms and regulations (Julian & Ofori-dankwa, 2013). The “Institutional Difference Hypothesis” developed by Julian and Ofori-dankwa (2013) states that emerging and developed markets differently perceive the reforms because the norms established in developed economies (such as minimum required capital and reserve requirements) are frequently different to those required in emerging or transition economies. Therefore, the application of this hypothesis is adequate in studies related to developing markets.

Moreover, there is a difference in structures of banking industries within countries of emerging markets themselves. Institutional settings define how banks behave. Hence, in this research, we distinguish transition economies from emerging markets (see Table 1), and, therefore, the application of the previous findings related to the emerging markets may not be applicable for transition economies. The focus of this research is on transitional markets only, which have recently switched from planned to open market economies. Since most of the studies are covering the emerging markets, our study will contribute to the literature as a new vision of this relationship in transitional economies.

Overview of Economies in Transition and Emerging Markets.

The hypothesis is that newly imposed regulatory norms increase bank performance and enhance financial stability. In this research, we investigate complete case studies within varying economic zones and regions to cross-examine the results to investigate across a large test sample in compliance with regulatory norms. This scattered examination helps us to identify possible weak areas in given economic zones and eventually employ targeted reforms and norms to enhance their performance. We evaluate systemic risk using the Z-score method, coupled with the methodology of Delis et al. (2012). This methodology was used in the evaluation of financial stability within the Kazakhstani banking industry (Kaliyev, 2019). We hold the shocks of the macroeconomic environment and bank-specific and industry-specific characteristics as control variables. Studying the relationship between bank performance and compliance with the newly adjusted regulations such as minimum required capitalization, activity restrictions, and reserve requirements help us identify the weaknesses of specific areas and help policymakers formulate the targeted reforms.

Additionally, we contribute to the literature examining the question using the GMM approach, a method which can be helpful in consideration of the endogenous variables problem which can often be the case in studies with the panel data. We run regressions across the full sample, regional subsamples, and separate countries to obtain more detailed and precise findings. The data covers almost 100 banks worldwide, representing 17 transition countries between the years 2008 and 2019. We incorporate macroeconomic shocks and banking variables to capture specifics of the institutions and industry variables to enroll country-level features into the model. The regulation effect is represented by the main factors of Basel accord: the activity restrictions, the reserve, and the minimum capital requirements.

Our findings indicate that the Reserve Requirements regulatory norm is the only significant factor that improves the profitability and diminishes the risk of financial instability. The Capital Regulation and the Activity Restrictions regulatory norms have insignificant effect on performance of banks in transitional economies under the study.

The following parts of the paper are organized in the next sequence of sections. Section 2 outlines the characteristics of economies in transition. Section 3 covers the observed literature. Section 4 describes the data and the methodology applied. Section 5 outlines the findings. And section 6 concludes our study.

The Characteristics of Economies in Transition, a Brief Overview

This study covers the transitional economies of eastern and central Europe, Caucasus, Balkan countries, and some peer countries of Latin America in the period of 2008 to 2019.

Eastern Europe (EE) is the region which has shown the fastest growth in the world since the financial crisis Cihak et al. (2013). Authors stated that three main points would boost performance of Eastern Europe after the crisis: portfolio restructuring, regional governance, and innovation in the industry. However, cost-effectiveness needed to be improved. In Hungary, because of the overall weak performance, many banks reduced their operational costs by closing their branches. For example in 2012, almost 90 branches closed their doors. In Poland, the overall banking sector performance was the best in the region. Even after the crisis, ROE and revenues were growing. The reason for that was an open market that was very adjustable to changes as many of the foreign banks were represented within the country with their new technologies, products, and innovations. Reversely, Slovakia faced immense financial instability because of closed doors policy and has been largely struggling to recover from the crisis up until to the year 2013 (Source: World Bank Financial Indicators, June, 2020). In Russia, growth after the crisis was the fastest among EE countries. ROE reached almost 14% in 2011 in Russia. However, the problem with the Russian banking business was its concentration. Almost half of the total banking profit was attributed to Sberbank which was very risky in terms of systemic risk evaluation. In Balkan countries, such as Serbia, the Basel II (Basel Committee on Banking Supervision, June 2004) framework was adopted in 2011. The framework opened up macro-prudential transparency, an increase in capital, better overall risk-adjusted management, and improved corporate governance structure. Argentina introduced CAMEL (Capital, Assets, Management, Equity, and Liquidity) quality regulation in 1994, and Brazil introduced Basel III norms and conditions in 2013. These countries used both cash and time deposits for internal funding, and bonds were commonly used as cross border funding. (Source: World Bank Financial Indicators, June, 2020).

Literature Review

There are two broad strands in the literature of the effect of bank regulation on bank performance. Generally, it can be categorized as positive and negative effects of regulation on sustainable development of the industry. Let us briefly go through the literature that covers the regulatory framework we are in interested in, through this aspect to the problem.

Capital Regulation

John et al. (2000) stated that the regulation of bank ratios would not help control risk-taking. In line with Calem and Rob (1996) study, John et al. (2000) suggest that choosing the optimal management compensation can help maximize the best investment output for the companies in question. As authors indicate, the success formula for regulation is incorporating risk weighted capital, introducing deposit insurances and management compensation scheme which partially resolves potential moral hazard problems. However, Demirguc-Kunt and Detragiache (2000) show that inputting deposit insurances has reversely a negative effect on stability. There are studies like Tullock (1967), Giammarino et al. (1990), and Shleifer and Vishny (1993), which claim that capital regulation has negative effect on bank performance because it increases briberies in transition economy management structures. Barth et al. (2013) indicated that poor regulatory norms can impede bank efficiency growth and contribute to the crisis inception. Moreover, Djankov et al. (2006) demonstrate that concentration can cause systemic risk. Some of the studies such as Keeley (1990) and Bernanke (1983) stated that bank risks affect fragility. Authors state that shareholders with comparably small fractions of shares were willing to take higher risks. Studies of Kane (1985) and Saunders et al. (1990) are confirming these findings. On the other hand, proponents of capital regulation as Bernanke (1983), Kane (1985), Saunders et al. (1990), Keeley (1990), Laeven and Levine (2008, 2009), and Ben Naceur and Kandil (2009) advocate that increasing level of capital requirements will positively affect stability. However, owners of public banks are willing to take higher risk, preferring to invest into higher return projects rather than consolidating the capital, what makes it difficult for the industry to develop. White (1989) in his early work indicated that higher capital reserves are important as banks with a better quality of loan portfolios earn more than those banks with lower quality. Good quality loan portfolios require additional costs. These extra costs must be covered up with extra capital. Dreher and Gassebner (2007) just before the Global Financial Crisis of 2008 stated that capital regulation is important for banks to be more vigilant toward too much risk taking. However, still as per study of Laeven and Valencia (2008), in 85% of the cases in times of crisis, governments had to recapitalize the banks.

Activity Restrictions and Supervision

Triki et al. (2016) examined bank regulations and efficiency in Africa. Authors found that small banks struggle as regulators impose tighter activity restrictions in non-banking services in addition to regular supervisions, what both Barth et al. (2013) and Beck et al. (2011) state can positively affect market development as it diminishes the level of NPL in bank portfolios. However, this requirement diminishes comparative advantage of local financial institutions to foreign owned banks, what the study of Ben Naceur and Omran (2011) indicate as necessity to increase performance of local banks. Supervision open ups gaps in banking business modeling and helps to prevent possible macroeconomic shocks as Micco et al. (2004) indicate in line with foreign entries in the ownership structures that are mostly appearing in transparent markets only. However, Cihak et al. (2013) findings indicate insignificant relationship between regulatory supervision and crisis prevention. Proponents of stricter supervision requirement like Cihak and Tieman (2008), Lau (2010), and Pasiouras (2008) studies indicate that low level of regulation in banking contributed largely into crisis embryo. However, Stigler (1971) indicated that governmental regulation of bank activities and interference into business only negatively affects the market as it creates inefficiency. Recent work of Djalilov and Piesse (2019), however, indicates that exactly the restriction on banking activities is the only regulatory framework that is enhancing efficiency. The studies of Agoraki et al. (2011) and Ayadi et al. (2016) both indicate that supervision has a significant effect on efficiency. Barth et al. (2004) found that more activity diversified banks have more options to take more efficient actions. However, examining restrictions on activities and supervision in banking of transitional economies lack the inclusion of post Soviet Union states like in the studies of Fries and Taci (2005) and Grigorian and Manole (2006), what might create biased findings.

Reserve Requirements and Other Regulatory Restrictions

Levine (1997), Dollar and Kraay (2000), and Gaganis et al. (2006) state that poor regulation of the banking system leads to the slowdown of economic growth in general. The necessity for external control is vital as Haselmann and Wachtel (2007) state, where the level of corruption decreases with more effective legal institutions. However, Hamilton et al. (1788) indicated that higher reserve requirements can negatively affect banks as politicians maximize their benefits but not industry overall wellbeing. It is competition that can increase bank efficiency as Bolt and Tieman (2001) indicate. Authors state that higher reserves are necessary in this case as tighter competition increases systemic risk because of lower quality of loans distributed. Studies like Hellmann and Murdock (1997), Klomp and de Haan (2012), and Demirguc-Kunt and Detragiache (2011) found that different dimensions of regulation and supervision affect bank performance in a variety of ways. However, direct effect of reserve requirements affecting better performance is not found. The studies of Barth et al. (2001), Demirguc-Kunt et al. (2004), Caprio and Barontini (2006), and Levine and Leonard (2006) state that higher reserve requirements boost the cost of financial intermediation. There are as well many other effects of regulation as in example Boyd et al. (1998) stated that regulation in general diminishes moral hazard problems, Barth et al. (2013) and Levine (1997) found that a bank’s efficiency improves with external supervision, Jbili et al. (1996), and Arellano and Bond (1991) state that regulation of bank reforms is helpful to decrease economic downturns but increases budget gaps.

Examination of literature on the effect of regulatory norms on the bank industry performance demonstrates that the specifics of banking industries are very diverse, and even for the same countries, results vary quite significantly. In regards to the notion of overall bank regulation, the primary objective is an intention to diminish too high risk exposure and to balance the value added risk to keep the sustainable long term growth (Barth et al., 2001). However, in terms of Activity Restrictions, minimum imposed Capital and Reserve Requirements regulatory norms, there is no direct cause and effect relationship between bank regulation and above mentioned endogenous to bank factors. For example, John et al. (2000) stated that quality of bank risk exposure is not directly affected by regulation norms. This requires control of other factors as new technological innovations and linked with it competition level within banking industry (Claessens & Laeven, 2004). The competition can lead to higher risk attitude. Restrictions on both banking and non-banking activities regulate competitive attitude of market players and increase banking efficiency (Djalilov & Piesse, 2019). In overall, particularly indicated bank regulation norms do not directly affect bank endogenous factors to enhance quality of bank performance and risk exposure, but through control of competitive nature of market players. Literature based findings show, at best, mixed results and largely devoted to developed economies or emerging markets. There is a scarce empirical research on transition economies.

Data and Methodology

Sample

The data were collected from the Bloomberg financial information resource for macroeconomic shocks, country, and bank-specific variables. Global financial crisis categorical variable used as a dummy with the value of “1” in case of crisis for the years of 2008, 2009, and 2010 for all the quarters and “0” otherwise with no crisis period. The following crisis period has been taken based on the work of Pak (2017), where the crisis years were taken as the start of default of the Lehman Brothers investment banking in 2008. The sample itself consists of 97 banks from 17 economies in transition. Nine countries are from Central and Eastern Europe—Bulgaria, Poland, Russia, Ukraine, Estonia, Lithuania, Czech Republic, Slovakia, and Hungary; four Balkan and Caucasus countries—Serbia, Slovenia, Armenia, and Georgia; and two peer countries—Argentina and Brazil. All the data applied is displayed as an unbalanced quarterly panel. The period of examination is covering the years 2008 to 2019. The data collected is based on the International Financial Reporting Standards (IFRS). The regulation data is based on the surveys of regulation from World Bank papers and local country-specific industry surveys.

Regulation Variables

The variables for the regulatory framework are constructed based on the works in the respective literature of Barth et al. (2006), Laeven and Levine (2008), and Djalilov and Piesse (2019). The variables of the regulatory norms of minimum Capital requirements, Reserve requirements, and restrictions of the Activities (non-banking) that we calculate are based on the data obtained primarily from the local statistical agencies of the Central Banks under examination countries, and from the Bloomberg financial information resource:

The variable Capital is based on the work of Barth et al. (2006), where the capital is composed of the assets that include factors such as securities, loans, and cash. We add loans to be recognized as bank specific current asset as it represents economic value in this particular industry (loans with maturity higher than 1 year). The origin of all resources of funds is checked by the external supervisors.

The restriction on Activities of bank regulation norm is constructed following the work of Barth et al. (2006) and Agoraki et al. (2011). The variable consists of activity restrictions in securities markets, activities in insurance, in trading securities, ban on the commissions and fees, and ban to acquire non-banking firms as financial firms. Restrictions are in line with the Basel principles and norms.

The Reserve requirements regulatory variable is based on the study of Demirguc-Kunt et al. (2004). To satisfy the regulatory condition of reserve requirements, reserves must be in line with particular country Central bank policy on minimum required reserves.

Control Variables

Since the study covers a number of countries, the possibility of the heterogeneity of the data observed between countries and the banks themselves is high. Hence, following the study of Djalilov and Piesse (2019), we employ variables that are applicable to most of the banks worldwide. Table 2 represents descriptions and formulas of the variables employed in the study.

Definitions and Formulas for the Variables.

Model

To examine the effect of regulation on bank performance and risk for the transition economies, and taking into account the fact that performance measures have dynamic nature as in the study of Djalilov and Piesse (2019), we utilize the Generalized Methods of Moments method. The idea is that GMM helps deal with the endogenous variable problem. Similarly to the study of Agoraki et al. (2011) we can observe the endogenous variables of our model of both weak and strong forms. Djalilov and Piesse (2019) stated that this relationship between today’s and future values of variables can be forward looking, what means that the value of the variable today is correlated with the value of the variable tomorrow. Moreover, the transition economies over the later three decades experienced many challenges that required these countries to take number of reforms both political and economic. Therefore, we consider the values of macroeconomic variables and regulatory factors as endogenous.

Methodology

We follow the study of Altunbas et al. (2011), Dietrich and Wanzenried (2011), and Pak (2017) in building the methodology of evaluating the risk (Z-score) and performance variables against independent variables. As Pak (2017) mentioned, stability is subject to impact by cycles and macroeconomic shock challenges. Hence, following both studies of Dietrich and Wanzenried (2011) and Pak (2017) we incorporate dummy variable into the model representing economic stress. Our baseline equation is the following:

The equation contains the values of the main factors as bank, industry, and country macro-specific variables with the specification for all variables of time

The GMM model is used when the dependent variables are found to be persistent (Blundell & Bond, 1998). In the study, we utilize the performance measures and risk variable regressed against other mentioned factors. The GMM methodology catches up with unobservable factors of the variables. We choose GMM based not only on the statistical significance and persistency of the variables in use but based on the conceptual understanding of the problem. Otherwise, the use of the instrumental variables can be sufficient in terms of an empirical approach to deal with the problems of endogenous variables. Instead, we use the GMM with the lagged differences for the dependent variables. We use the Fixed Effect in the dynamic model considering the fact that individual effects are correlated with the variables in the model. Based on the Hausman test recommendations we can use up to two lags for the macro and regulation variables. Generally, the Hausman (1978) test indicates which effect is more applicable for the dynamic panel data using the correlation results between the constant and coefficient (Pak & Kretzschmar, 2016). Rejection of the null hypothesis of the correlation suggests the use of the fixed effect rather than random effect and vice versa. In addition, theoretically, we refer to the works of Lemmon et al. (2008) and Gropp and Heider (2007) in choosing the Fixed Effect. The authors state that the fixed effect models better identify the variability of the institutional factor that is not time-dependent. Utilizing the Hansen test we check the validity of the instruments. Arellano and Bond (1991) indicated that the autocorrelation in the first order is almost always the case. The true level of the variable autocorrelation can be identified in the second order. The variables in use within the model are not showing the autocorrelation in the second order. However, the problem of the data within the transition economies is generally the subject for the auto correlative behavior as the data can be replicated and averaged between the financial institutions.

The research employs unbalanced panel data. One of the main problems in panel data is the use of endogenous variable. The endogenous variable is the estimative problem. In understanding it, we can follow the study of Tabak et al. (2012), where the problem is explained as simple as the explanatory factors of the model determined together with the dependent variable. Generally, it is quite difficult to come by purely exogenous variables. Therefore, we rely on our self-judgment and literature-based experience in the selection of variables. Moreover, we use the fundamental idea of Arellano and Bond (1991) work, where authors studied the problem of exogenous explanatory variables. The main idea is to build the model with the application of the variables in origin correlated with each other. Using the model we can exclude the risk of correlation between past, present, and future variables of the same measures. This methodology permits to take the lag of the dependent variable without significant consequences and diminish the endogenous variables problem. This GMM methodology recognizes the unobservable factors of the variables in use. Many studies assume that the effect of the explanatory factors on dependent variables is homogenous (Djalilov & Piesse, 2019). For example, the regulatory effect represented through the specific methodology can be equally recognized by all of the banks in the sample. However, banks tend to be heterogeneous in nature. Therefore, the use of the GMM methodology is justified.

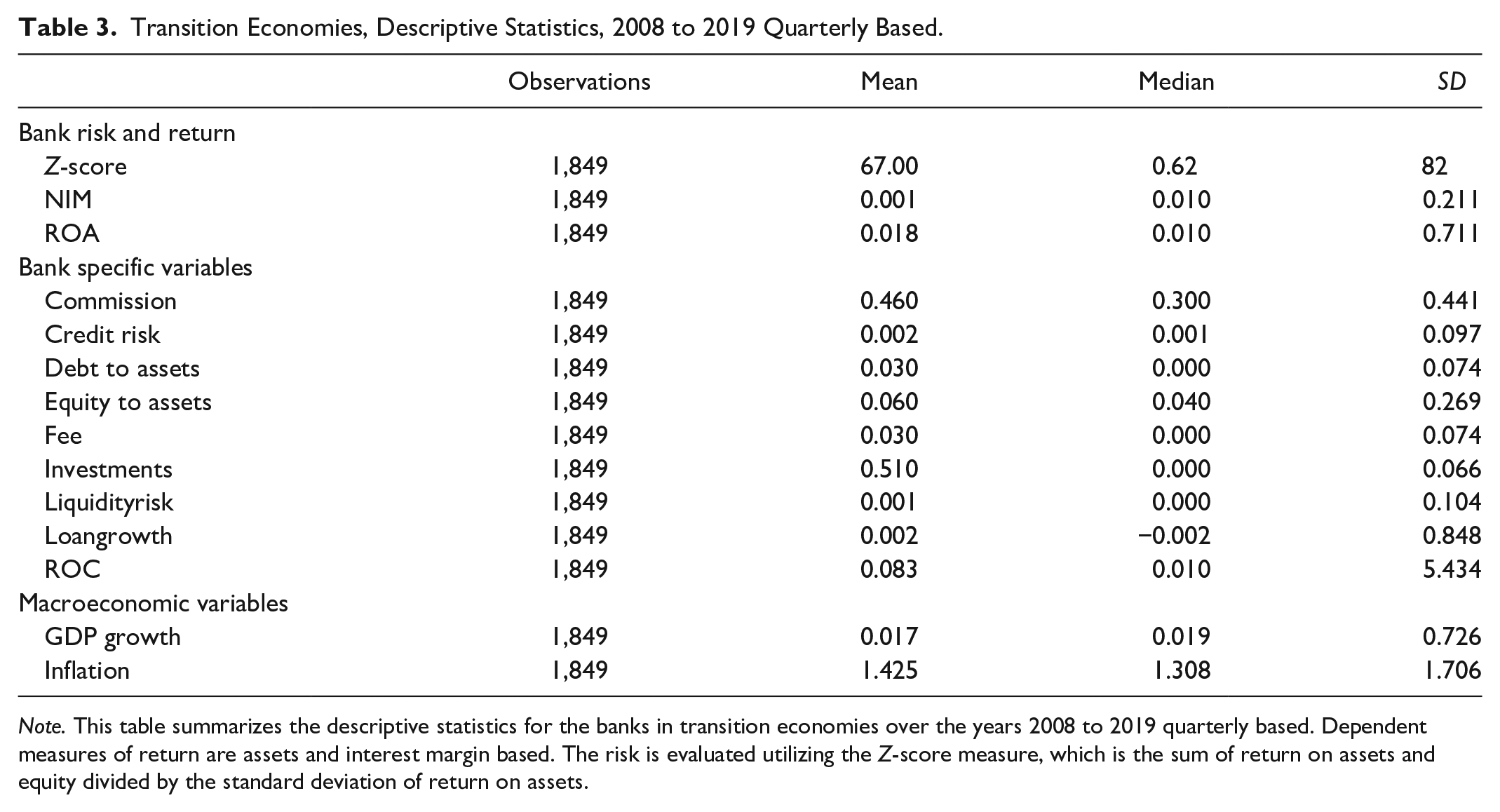

Descriptive Statistics

Table 3 above represents descriptive statistics. The higher the Z-score, the better is the financial stability of the banks. The score for the transitional economies under observation is 67 points suggesting quite a stable financial position overall. However, the range of the score is quite wide, indicating a diverse level of risk for the banks under examination. The Margin of the revenues and costs is positive but not significant, meaning that this profitability measure is highly dependent on only one source of funding. The ROA coefficient is more significant, indicating a mean of 1.8% overall growth for the transition economies. Non-interest earnings are high for the banks in transition economies. Banks in transition industries rely more on traditional interest based earning approach. At the same time, Investments had been immense during examination period. The portion of the income generated through trading securities is very high for all of the banks under examination. Return on Capital is in general, high, with an average a little more than 8% for the sample. This value shows how these banks are setting up their safety nets.

Transition Economies, Descriptive Statistics, 2008 to 2019 Quarterly Based.

Note. This table summarizes the descriptive statistics for the banks in transition economies over the years 2008 to 2019 quarterly based. Dependent measures of return are assets and interest margin based. The risk is evaluated utilizing the Z-score measure, which is the sum of return on assets and equity divided by the standard deviation of return on assets.

Risk and Return

The risk score methodology is a classical way to estimate a financial institution’s attitude toward risk. We calculate the score utilizing the exploitation of Delis et al. (2012), where the score is the sum of return on assets and equity to assets divided by the standard deviation of its return on assets. We employ this method for every bank “i” at time “t.” The sample data is quarterly used and therefore the deduction of the number of observations because of the rolling window does not diminish the significance of the findings.

We use Net Interest Margin (NIM) as liquidity and Return on Assets (ROA) as profitability measures of the bank. The ROA demonstrates operational performance of the banks and represents the bank-specific variable. Al-Matari et al. (2014) have stated that by employing ROA we can observe how profit is generated. On the other hand, the data on the accounting measures of the banks are collected with respect to IFRS standards, but still are provided by the banks themselves. Utilizing NIM we can capture the spread of the revenues and costs of the banks. Observing it, we can make conclusions on how banks make funding decisions.

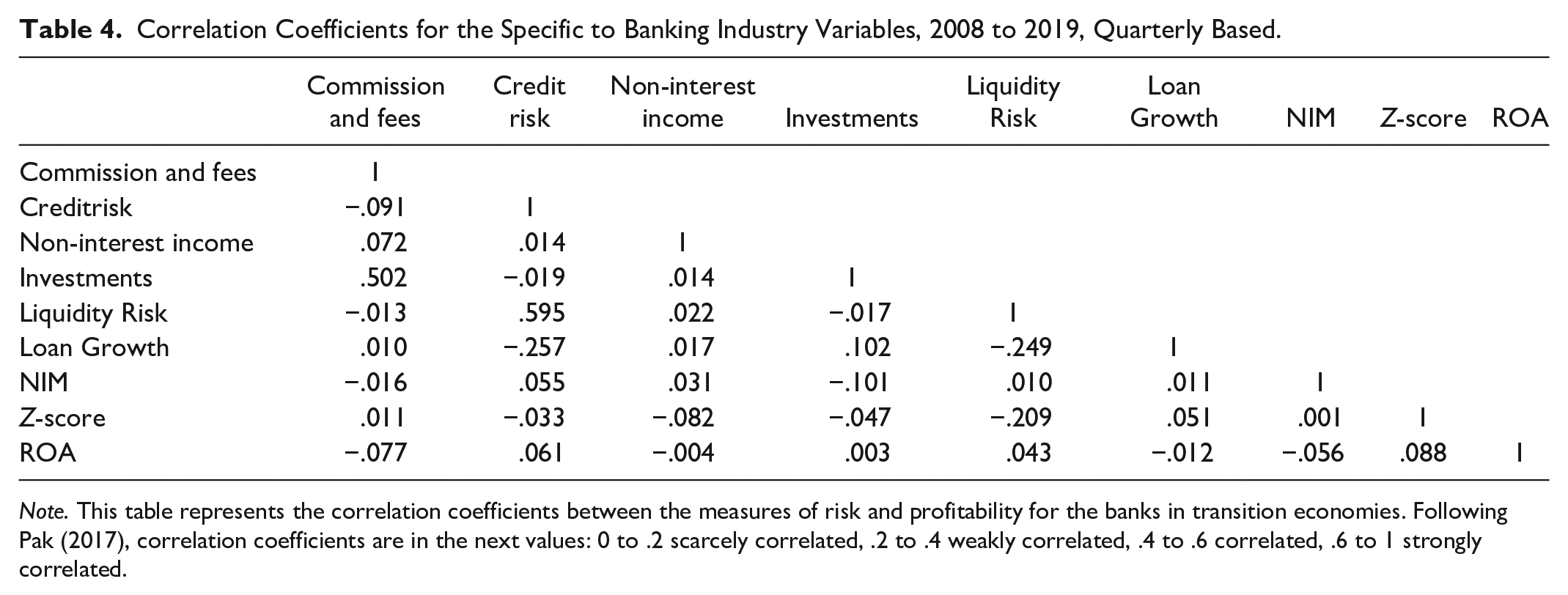

Correlation Matrix

From Table 4, we observe that the Liquidity Risk has high and negative correlation with financial instability. The Liquidity Risk significantly and negatively correlates with the Loan Growth. Trading securities positively correlates with Non-interest earnings. The correlation between Liquidity Risk and Credit Risk growth is significant. Liquidity Risk plays an important role as a factor affecting banking industry performance.

Correlation Coefficients for the Specific to Banking Industry Variables, 2008 to 2019, Quarterly Based.

Note. This table represents the correlation coefficients between the measures of risk and profitability for the banks in transition economies. Following Pak (2017), correlation coefficients are in the next values: 0 to .2 scarcely correlated, .2 to .4 weakly correlated, .4 to .6 correlated, .6 to 1 strongly correlated.

Empirical Results

In the study we consider macroeconomic and regulation variables to be endogenous in line with the study of Agoraki et al. (2011) since the different reforms, norms and regulations were applied by the managers as amendments to diminish the possibilities of risk. Moreover, the policy in the economies of transition had been frequently changing that affects the decisions of authorities in terms of macro-economy. These actions affected the values of these measures further. Therefore, the application of the GMM approach is reasonable with the further use of lag variables. We use seven different combinations for the profitability measures of Return on Assets, Net Interest Margin, and Risk score for the full sample of transition economies. For an in-depth look into the findings, we run separate regressions for the four sub-samples allocated in regions of Eastern European, Central European, Balkan and Caucasus countries. We use the methodology from general to specific in the selection of variables in line with the study of Klomp and De Haan (2012). As a result, we exclude from the observation some of the insignificant variables and parameters such as total assets and quantity of workers. All the coefficients are significant and show comparative stability across different models. As for the unit root test, all the variables under examination are stationary at a level as suggests the Augmented Dickey Fuller test at 5% significance level. The overall validity of the instruments applied in the GMM model is significant as we can observe from the Hansen test.

The main results for the dependent profitability measure of Return on Assets for the full sample of transitional countries are depicted in Table 5. The first column shows the model with the inclusion of all of the regulatory and control variables holding the effect of the Crisis constant. Macroeconomic variables, in this model, positively affect the overall profitability. However, regulation factors in all aspects have a negative impact on the performance of the banks. With the inclusion of Crisis, findings in column two show the complete reverse effect and all the regulatory factors start to have a lesser but positive effect on profitability. We reason this effect of Crisis as the weakness and vulnerability of the general banking systems of the countries under examination and consider that regulation has a very significant role in times of crisis. When there is no crisis, the regulation norms create obstacles for the banks to realize more risk oriented strategies of profit generation and this way decrease possible higher returns from higher risk projects. On the other hand, regulatory norms decrease moral hazard problems. This is what we observe as the crisis factor was included in the model. The effect of capital stringency, higher reserve requirements, and activity restrictions diminish the quantitative effect on the profitability, but the overall effect became positive. As for the control variables, the Loan Growth changes from negative to positive with the inclusion of Crisis in the equation. Investments decrease with the crisis; this is reasonable and comes in line with general economic theory. In general, positive Loan Growth can be explained by the governmental financial support of the state via monetary policy in times of crisis. However, this increases the Credit Risk and negatively affects profitability, as we can observe from column two. We can observe the significant effect of the Crisis factor on other variables. Therefore, we exclude it from the observation of separate regulatory effects. In this case, only the Reserve Requirements factor has a positive impact on profitability. We treat this effect in the way that banks’ performances can be largely dependent on governmental financial support. Separately examined, higher Reserve Requirements positively affect the overall banking performance but with the minimum significance.

Regulation and Profitability, GMM, Quarterly Based, 2008 to 2019.

Note. This table shows the regression coefficients of the Return on Assets profitability measurement model for the full sample of examined banks of transition economies. Standard errors are represented in parentheses. Significance levels of the probability values are indicated as the next: ***, **, * significant at 1%, 5%, and 10% levels, respectively.

Table 6 represents the findings of the profitability measure of Net Interest Margin. In line with the previous findings found from the effect on Return on Assets, Reserve Requirements has a positive sign in all specifications when examined with the Crisis effect, excluding Crisis effect and when studied exclusively. However, the spread between revenue and cost positively affected by all regulatory norms without the inclusion of the crisis into the model as opposed to our previous findings. We explain it as a higher return from a higher risk projects that covers up costs in times of a positive economic state. As we already mentioned following John et al. (2000) examination, there is no direct impact of regulation on the interest margin. However, the findings indicate positive relationship. We explain it as the next: imposed higher requirements of prudential norms for banks push top management to increase the spread of interest margin. In the similar manner, restrictions of non-banking activities make bank managers look for other sources of funding, once again increasing the borrower’s share of interest payments. The GDP growth in almost all specifications has a positive effect apart from the cases where we don’t include Reserve Requirements into our examination, confirming again that this factor has a crucial role in the overall banking model.

Regulation and Profitability, GMM, Quarterly Based, 2008 to 2019.

Note. This table shows the regression coefficients of the Net Interest Margin profitability measurement model for the full sample of examined banks of transition economies. Standard errors are represented in parentheses. Significance levels of the probability values are indicated as the next: ***, **, * significant at 1%, 5%, and 10% levels, respectively.

Table 7 shows us the results of the effect of regulatory norms and control variables on the financial stability of the full sample of economies in transition. All the regulatory factors positively affect the risk in specifications with and without the inclusion of the Crisis effect. In specifications where we examine all regulatory factors separately, only the Reserve Requirements has a positive effect on financial stability, other specifications show negative signs. Commission associates positively with risk, only in case of Crisis inclusion. The other six combinations show negative signs. Commissions and charges increase with crisis and positively affect the financial stability of the industry overall.

Regulation and Risk, GMM, Quarterly Based, 2008 to 2019.

Note. This table shows the regression coefficients of the risk measurement model for the full sample of examined banks of transition economies. Standard errors are represented in parentheses. Significance levels of the probability values are indicated as the next: ***, **, * significant at 1%, 5%, and 10% levels, respectively.

Supplemental Tables 8 to 10 represent the findings for the profitability measures of Return on Assets, Net Interest Margin, and financial stability of Z-score for the peer countries sample of Argentina and Brazil (Supplemental Appendix I). The findings of the Return on Assets are generally consistent with the full sample results. The effect of Reserve Requirements is positive in its separate inclusion. The significance of the regulation is increasingly high when the Crisis factor is included in the model. The effects of all regulation norms are positive in this model. The omission of the Crisis effect shows the negative effect on the performance of the banks in peer countries. Similar results hold for the effect of regulatory norms and control variables on the Net Interest Margin profitability measure in Supplemental Table 9. Macroeconomic variables have positive signs in almost all specifications. The negative signs are in the model where we omit Reserve Requirements as a factor of regulation. The Inflation and GDP Growth have negative signs in cost and revenue spread examination in the specification without Reserve Requirements.

The sub-sample confirms our previous findings of the Reserve Requirements as the crucial factor of the model.

Supplemental Tables 11 to 13 (Supplemental Appendix II) represent the findings of the sub-sample of Eastern European countries. Likewise the sub-sample of peer countries, the number of observations is smaller in these two samples, and therefore the results can be less reliable. Still, we run these models with the purpose of thoroughness, to test our main results. Generally, the findings are in line with the main results in both profitability measures and risk score estimation. However, the significance of the coefficients is lower. The interesting difference with the previous findings is that the Credit Risk factor has a negative trend in full models with and without the inclusion of the Crisis factor (Supplemental Table 11, 1–2 rows). In other specifications, this factor has a positive effect on profitability. Credit Risk negatively affects profitability measures in both cases of the Crisis factor inclusion and omission.

Supplemental Tables 14 to 16 represent the sub-sample of Balkan and Caucasus countries (Supplemental Appendix III). The number of observations is 282 only after the adjustments. Still, the main results are in line with our full sample findings. The effect of the Crisis is moderately significant in both examinations of profitability and quite close in their coefficient scores. The capital ratio has negative signs in all the regression specifications against the financial stability (Supplemental Table 16), stating the fact that the shareholders of the banks in transition economies of Balkan and Caucasus countries rely a lot on governmental financial support.

Supplemental Tables 17 to 19 are representing the findings of the sub-sample of Central European countries (Supplemental Appendix IV). We can observe that the findings are similar to our previous results. For example, the Reserve Requirements is the only regulatory factor positively affecting the profitability in both Return on Assets and Net Interest Margin representations. Other regulatory factors have negative signs in all specifications of separate examination, including and excluding the Crisis factor (Supplemental Table 17).

Thus, we conclude that utilizing the GMM methodology, the Reserve Requirements were found to be the only significant and positive regulatory factor that improves the profitability and diminishes the risk of financial instability of the banking sectors of the transition economies across a full sample of countries. We check and confirm the findings with the tests over the regional sub-samples.

Conclusion

The banking industry has always been the center of interest for both theorists and practitioners. The rebuilding of banking regulation has been at the core of its sustainable development since the financial crisis of 2008. The main objective was to ensure that financial fluctuations would be prevented or at least forecasted and mitigated more efficiently.

In this research, we examine how well regulatory norms would be affecting the factors of profitability, efficient operation, and overall banking industry performance in the transition economies in the period of 2008 to 2019. The expectation is that the effect of regulatory norms in terms of Activity Restrictions, an increase in the level of Reserve and Capital Requirements positively affects overall industry performance and financial stability. However, the previous findings in the related area show contradicting results (Ayadi et al., 2016).

We contribute to the literature in number of points.

Firstly, this work covers the transition economies only. Most of the previous studies have related to developed or developing markets specifically, such as Pasiouras et al. (2009) and Barth et al. (2013). Moreover, we consider both the crisis and post-crisis periods in our examination, which has helped us define the effect of the vast differences in perception on the banks, and the financial changes on a macroeconomic level. Secondly, we utilize the Generalized Method of Moments methodology to diminish the problem of endogenous variables. The most frequent problem in banking data use is the dynamic nature of these variables. The GMM methodology takes into account the dynamic nature of both dependent and independent variables. Thirdly, we examine the results for the thoroughness of our findings utilizing five different regional samples all with different banking industry specifications.

In summary, our conclusive findings from this analysis are the following. Firstly, we found that in a full sample examination the inclusion of Crisis into the model shows that the applications of regulatory norms positively affected the overall performance and financial stability of the industries in question. This shows the weakness and vulnerability of the bank industries in economies in transition because the overall effect of regulation on profitability is negative without the inclusion of the Crisis factor, indicating possible management moral hazard problems in times of positive economic state. Second, we found that in all specifications, only the Reserve Requirements regulation mode exhibits positive regulatory effect, improves profitability, and increases the financial stability of the banks in transition economies. All other factors, control variables, and regulatory norms affect differently the financial stability which confirms that there is no “one size fits all” system.

In general, our findings suggest serious policy implications in banking business modeling. Causal effect of Reserve Requirements is the only regulatory factor improving profitability in all specifications. Activity Restrictions and Capital Requirements are not sufficiently effective in specifications holding the Crisis effect constant. That might be due to the fact that bank management is misbehaving in a positive economic state. Therefore, the effect of these two factors of regulation is only substantial during the crisis period. This leads to the idea that both practitioners and theorists in the face of managers, reformers, and supervisors need to regularly investigate their banking industries for the effectiveness of currently applied regulatory norms. This will help diminish the possibilities of systemic risk taking into account that working groups incorporate specifics of the institutions under examination. Because as Allen and Gale (2004) mentioned, when a financial crisis takes place, it may be once in a generation, but that would be a dramatic collapse in a single moment, a devastating splash where the ripples can be felt by every economy, every institution, and by every one of us.

Appendix I, II, III, IV and supplementary data to this paper can be found at request by contacting the authors.

Supplemental Material

sj-docx-1-sgo-10.1177_21582440211061537 – Supplemental material for Bank Regulation in the Economies in Transition

Supplemental material, sj-docx-1-sgo-10.1177_21582440211061537 for Bank Regulation in the Economies in Transition by Kaliyev Kalizhan Sagatbekovich and Mira Nurmakhanova in SAGE Open

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.