Abstract

This study utilizes data from China’s A-share listed firms from 2007 to 2021, employing the LP and OP methods to construct total factor productivity indicators, and investigates the relationship between CEOs’ information technology backgrounds and corporate total factor productivity, further exploring the mechanisms of this relationship. The study reveals a significant positive impact of CEOs’ information technology backgrounds on corporate total factor productivity. To ensure the reliability of the findings, the average and lagged values of CEOs’ information technology backgrounds were selected as instrumental variables, and the two-stage least squares method and propensity score matching were used to address endogeneity issues. Robustness checks, including the lagging of the dependent variable, confirmed the stability of the conclusions. Further analysis of the impact mechanisms indicates that CEOs’ information technology backgrounds enhance total factor productivity by promoting digital transformation within firms. Heterogeneity analysis reveals that the positive effect of CEOs’ information technology backgrounds on total factor productivity is significant in firms with high financing constraints and agency costs but not evident in those with low financing constraints and agency costs. These findings provide valuable insights for the selection of CEOs, support for digital transformation initiatives, enhancement of total factor productivity, and promotion of high-quality development.

Keywords

Introduction

Total factor productivity, as a crucial metric for assessing corporate value enhancement, is a key indicator of high-quality economic development. With the rapid advancement of technology, the information technology sector has gradually emerged as a burgeoning industry, prompting more firms to embark on digital transformation to enhance production efficiency and governance outcomes through information technology. In talent recruitment, there is an increasing preference for professionals skilled in digital and information technology. In China, recent trends indicate that more firms are appointing individuals with technical backgrounds as CEOs. Baidu’s CEO, Robin Li, whose background lies in information management and computer science, has guided the company toward relentless progress in search engine technology and AI, placing Baidu at the vanguard of artificial intelligence both in China and worldwide. Liu Gang, CEO of GitLab (Jihu) in China, with nearly two decades of expertise in enterprise-level IT solutions and AI commercialization, has propelled the company’s technological innovation and market expansion across the region. William Li, CEO of NIO, graduated from Peking University with a major in sociology and a minor in computer science, seamlessly blending information technology with the automotive realm to found NIO, thus advancing the intelligent evolution of the electric vehicle industry. Pony Ma, CEO of Tencent and a computer science graduate, wields sharp foresight in steering the company through ongoing digital transformation; from social platforms to fintech, smart healthcare, and intelligent transportation, he has harnessed digital technologies across multiple domains, fostering high-quality growth for Tencent.

As the chief decision-makers within organizations, CEOs with information technology backgrounds bring distinct perspectives and outcomes in organizational decision-making, business philosophy, operational models, organizational innovation, and external financing. Human capital is an indispensable driving force for economic growth, underpinning continuous corporate innovation and progress, and is a pivotal factor in national high-quality development (Ye et al., 2023). The influence of human resource endowments on the improvement of total factor productivity cannot be overlooked (Q. Chen et al., 2020).

Within the distinctive framework of socialism with Chinese characteristics, China’s total factor productivity has assumed fresh significance, with particular emphasis on management, data, and related concepts. In recent years, the development of information technology has also spurred firms to pursue innovations in digital technology continuously. Firms increasingly value senior executives with information technology backgrounds. The Chinese government has consistently emphasized leveraging vast data and diverse application scenarios to promote the deep integration of digital technology with the real economy, empower traditional industries to upgrade and transform and foster new industries, new business forms, and new models, thereby strengthening and expanding China’s digital economy. Countries worldwide are formulating digital economy development strategies, introducing supportive policies, and harnessing the innovations and advantages of digital technology (Doz, 2020). Recent trends reflect the rapid development of information technology and its growing importance in the business realm (Ye et al., 2023). Digital technology has become a vital means of enhancing national digital competitiveness. Amidst the global digital technology revolution, the development of digital technology presents strategic opportunities for improving total factor productivity. Both human capital and technological progress are effective avenues for promoting comprehensive economic quality enhancement (Schumpeter, 2017). Digital transformation can drive technological advancements that elevate total factor productivity (Zhao et al., 2022). Digital technology, by integrating firm resources, optimizing industrial upgrades, and reshaping value advantages, provides the impetus and pathways for enhancing high-quality development through multiplier effects (Jiang et al., 2022). Research has shown that digital technology can optimize innovation elements (Xie & Guo, 2022), reduce costs (Mou et al., 2023), and mitigate capital and labor mismatches (Huang & Wang, 2022), thereby enhancing total factor productivity. China has entered a new era of comprehensive intelligence, prompting enterprises to refine their full-scale smart development strategies and appoint CEOs with strong IT management expertise. The significance of a CEO’s technology background has grown increasingly acute as Chinese businesses urgently seek leaders who can balance technical proficiency with keen business insight, driving digital transformation and growth that aligns with the nation’s high-quality development goals.

Recent studies have determined that digital transformation, as a high-level strategic decision, inherently relies on executive support (Yi et al., 2024). According to the upper-echelon theory, the individual characteristics of managers, such as gender, age, educational background, and distinctive traits, reflect their personal risk preferences and values, which profoundly influence corporate decisions (Li & Cui, 2018). Particularly in Chinese firms, the CEO plays a crucial role, having a decisive impact (Yuan et al., 2024). As a heterogeneous human resource within the firm, the CEO leverages their unique human capital advantages in the digital transformation strategy, facilitating the empowerment of firms through digital means to enhance total factor productivity and corporate competitiveness. The significance of a CEO’s background in information technology is increasingly recognized for its impact on the firm. Many firms have realized that leaders with technical expertise can better comprehend and guide the implementation of digital transformation. Their experience in information technology makes them more willing, daring, and capable of undertaking such transformations. A 2018 survey by McKinsey identified tech-savvy leaders as the primary factor for successful digital transformation, although this conclusion lacks rigorous empirical evidence. Existing research has highlighted the crucial role of CEOs’ information technology backgrounds in corporate innovation and investment efficiency (Li, 2020; Zhang, 2018), yet there has been insufficient exploration linking the CEO’s IT background with digital transformation and total factor productivity.

Moreover, some studies argue that digital innovation and transformation involve significant uncertainties, and the success rate of digital transformation in Chinese firms is not high. Failure in transformation can lead to substantial financial losses and negative impacts on the firm (Nambisan et al., 2017). Additionally, other studies suggest that an overemphasis on digital transformation, allocating excessive resources to digital initiatives at the expense of product development and production processes, may lead to resource misallocation (Ye & Liu, 2018). This issue remains contentious.

Therefore, under the backdrop of digital transformation, our understanding of the relationship between CEOs with information technology backgrounds and total factor productivity remains limited. This study attempts to incorporate the dimension of CEO personal characteristics into the relationship between digital transformation and corporate total factor productivity. Using A-share listed firms from 2007 to 2021 as the research sample, this study first employs the LP method to measure the total factor productivity of these firms, followed by robustness checks using the OP method. The study reveals a significant positive impact of CEOs with information technology backgrounds on corporate total factor productivity; firms with such CEOs exhibit higher productivity levels compared to those without. After a series of robustness checks, the conclusion remains consistent. For the mediating effect mechanism test, this study adopts the method proposed by Wen et al. (2004), which indicates that CEOs with information technology backgrounds enhance total factor productivity by promoting digital transformation within firms, thereby resolving existing controversies in the literature. Further research shows that this effect is more pronounced in groups with high financing constraints and high agency costs. Finally, conclusions and relevant policy implications are presented.

The marginal contributions of this study are as follows: existing literature has predominantly explored the influencing factors of total factor productivity from a macro perspective. This study, however, analyzes the impact from a micro perspective based on the personal characteristics of CEOs with information technology backgrounds, highlighting the unique role of CEO background traits in corporate development and enriching the research on upper-echelon theory and the drivers of total factor productivity from a human capital perspective. Second, by examining the relationship among CEOs’ information technology backgrounds, digital transformation, and total factor productivity, this study expands the pathways for enhancing corporate productivity and uncovers the pivotal role of CEOs’ IT backgrounds in driving digital transformation. This provides evidence to support the importance of human capital, the improvement of CEO recruitment processes, and the implementation of digital transformation strategies in the new era.

The remaining sections of this paper are organized as follows: Section 2 presents the theoretical analysis and research hypotheses, based on which the hypotheses of the study are proposed; Section 3 outlines the research methodology, including the variables, model settings, and data sources; Section 4 conducts empirical analysis and robustness checks on the data; Section 5 provides further analysis, discussing heterogeneity based on financing constraints and agency costs; Section 6 concludes the study with research findings, implications, limitations, and directions for future research.

Theoretical Analysis and Research Hypotheses

CEO Information Technology Background and Corporate Total Factor Productivity

The CEO represents a mature operational manifestation of a firm’s corporate governance structure, serving as a crucial intermediary to address communication barriers and information transmission blockages between the decision-making and execution levels, acting as the pivotal axis of the power system. CEOs are widely regarded as one of the most critical human resources in a firm, emphasizing and focusing more on the realization of long-term goals and visions compared to other executives (Hambrick & Cannella, 2004). The upper-echelon theory posits that the diversity in educational attainment, life experiences, and professional backgrounds influences CEOs’ investment decisions and efficiency, leading to significantly different performance outcomes (Xiong et al., 2022). For instance, firms led by CEOs with a university degree or higher tend to have higher investment returns (Ling et al., 2021); CEOs with a rich functional background can enhance innovation performance (X. Liu, 2020). As a significant embodiment of specific internal human capital within a firm, the diverse personal characteristics of CEOs, such as tenure, age, educational background, and distinctive traits, can impact corporate risk investment choices, thereby affecting the level of total factor productivity. High-quality human capital within a firm helps absorb advanced management practices, strengthen internal governance, improve employee productivity, and promote the enhancement of total factor productivity (Black, 2019). Simultaneously, the unique human capital forged by varied CEO backgrounds can accelerate technological innovation, improve resource allocation, secure creative and competitive advantages, and elevate total factor productivity (Song, 2023).

Q. Chen et al. (2020) discovered that CEOs with financial backgrounds exhibit more adventurous behavior and are more familiar with financial sector operations, aiding in raising innovation levels and investment efficiency, thus enhancing total factor productivity. This finding remains significant even after employing the Difference-in-Differences (DID) method to control for endogeneity. Dai and Kong (2017) found that CEOs with overseas backgrounds possess a more international perspective, improving their macro-control capabilities, which helps firms make more appropriate financing and investment decisions, optimizing resource allocation and boosting total factor productivity. Song (2023) found that CEOs with a technical background are more conducive to driving and inspiring technological innovation activities within firms, advancing technological levels, and enhancing total factor productivity.

Specific types of human capital are pivotal factors in total factor productivity growth and are among the significant contributors to productivity disparities (Yao & Wang, 2020). Corporate total factor productivity, as a core driver of firm development, has been widely acknowledged. Existing literature highlights that internal factors such as R&D, technology, and human capital significantly influence total factor productivity. Studies have identified that external business, trade, and tax environments (Ochotnický et al., 2020), as well as macro-level factors such as government quality, institutional quality, and economic openness, also impact total factor productivity (Tebaldi, 2016). However, the literature has overlooked the influence of individual-level CEO background characteristics on corporate total factor productivity, especially in the context of the rapid development of big data and artificial intelligence. Firms increasingly value information technology and frequently appoint CEOs with IT backgrounds, raising the question of whether such appointments affect corporate total factor productivity.

Based on the upper-echelon theory, CEOs with information technology backgrounds tend to favor riskier innovative expenditures, offering more innovative business concepts that support continuous innovation to enhance total factor productivity growth (Black, 2019). CEOs with IT backgrounds foster a culture of sustainable development, inspiring employee innovation consciousness, which is beneficial for improving total factor productivity (Wang et al., 2023). Furthermore, CEOs with IT experience emphasize the application of emerging technologies and ensure strict implementation quality, improving information communication efficiency, enhancing governance levels, and ensuring effective outcomes (R. Li et al., 2022). Moreover, in the context of global economic volatility, CEOs’ digital skills have become increasingly crucial for firms. These skills and experiences help avoid ineffective investments in innovation activities, reduce resource misallocation, and improve total factor productivity.

Based on the above analysis, this study proposes the following hypothesis:

Hypothesis 1: CEOs with information technology backgrounds significantly enhance corporate total factor productivity.

The Impact Mechanism of CEO Information Technology Background on Corporate Total Factor Productivity: The Mediating Role of Digital Transformation

The upper echelon theory elucidates how the cognitive level and functional background differences of senior executives influence corporate strategic decision-making. Managers’ personalities, capital, and behavioral characteristics are pivotal factors affecting these decisions (Hambrick, 2007). CEOs with extensive professional knowledge and rich skill sets are better equipped to discern the value of new opportunities and are more willing to support and undertake the risks associated with transformative changes (Koyuncu et al., 2010). CEOs’ recognition and support of the economic value brought by digital technology foster a corporate culture that prioritizes digital technology development. Additionally, CEOs’ emphasis on digital technology investments leads to the recruitment of more relevant talent, strengthening the digital technology team and integrating digital technology into all aspects of the firm’s development strategy, thereby creating a team atmosphere that values digital technology (Haislip & Richardson, 2018).

Furthermore, CEOs need to communicate effectively to ensure the team aligns with the decision to develop digital technology and achieve unified goals (Haislip et al., 2016). Finally, given the inherent risks in digital technology development, CEOs must better supervise and manage the digitalization process, make reasonable assessments of potential changes, and bolster the team’s resolve to invest in digital technology (Guo, 2016). In the context of the digital economy, manager’s efforts to promote artificial intelligence development and digital transformation are essential processes for maintaining competitiveness and sustainability throughout the corporate lifecycle (Eduardsen, 2018).

CEOs with information technology backgrounds, who are well-versed in digital technologies and possess advanced learning curve capabilities and risk management skills, are adept at identifying competitive threats and swiftly recognizing risks and opportunities, thereby facilitating strategic decisions that maximize value (Helfat & Peteraf, 2015). These CEOs have a positive impact on corporate digital transformation (X. Liu et al., 2023; Y. Wu et al., 2022). Their digital mindset and management proficiency enhance the team’s understanding and learning of digital transformation, elevate the management team’s digital capabilities, and ultimately foster a consensus on digital transformation (Akhtar et al., 2019). Furthermore, a CEO’s information technology background can mitigate technological barriers, promote knowledge dissemination, deepen industry information exchange, and address potential challenges related to technology implementation, enabling the firm to reap the benefits of digital transformation (Hadad & Bratianu, 2019). Research indicates that decision-makers with a background in technology research and development possess a strong digital drive, which can invigorate corporate innovation and better navigate the uncertainties inherent in digital transformation (J. Liu et al., 2022).

Considering that technological innovation and efficiency upgrades constitute the primary drivers of total factor productivity growth (Sari et al., 2016), investments in information technology elevate total factor productivity by introducing cutting-edge technologies and enhancing information systems. Whether through human capital, digital technologies, or digital innovation, the overarching goal remains the pursuit of high-quality corporate development. However, existing literature rarely accounts for the influence on firm value. This study brings both perspectives together, examining how CEOs with IT backgrounds affect digital transformation decisions and how these decisions ultimately boost total factor productivity. Specifically, this study explores whether an IT-oriented CEO can enhance a company’s total factor productivity by promoting the adoption of information technology and elevating operational efficiency. This study posits that such a CEO, as a form of distinguished human capital, not only exerts a direct impact on total factor productivity but also spurs enterprises to embrace and implement digital transformation, harnessing technological progress to reinforce total factor productivity indirectly. Figure 1 illustrates the underlying mechanism. Based on this analysis, this study proposes the following hypotheses:

Hypothesis 2: CEOs with information technology backgrounds enhance corporate total factor productivity through digital transformation, indicating that digital transformation mediates the impact of CEOs’ IT backgrounds on corporate total factor productivity.

Diagram of the mechanism by which the CEO’s information technology background affects total factor productivity.

Research Methodology

Data Collection

This study selects relevant data from A-share listed firms in China for the period from 2007 to 2021. The starting point of 2007 is chosen due to the reform of Chinese accounting standards that year. The data primarily originates from the CSMAR and Wind databases. Digital transformation data is sourced from the annual reports of listed firms, while CEO data is obtained from the “China Listed Firms Research Series” and “China Corporate Characteristics Series” in the CSMAR database, which includes information on board members. The CSMAR data is widely recognized by researchers for its authoritative and professional content. Data for calculating total factor productivity and other variables comes from the GTA database.

The data is processed as follows: (1) Firms with abnormal data that could affect result accuracy are excluded. (2) Firms with missing data are excluded. (3) 127 firms in the financial sector are excluded. (4) 184 firms marked as ST, *ST, or PT are excluded. (5) Continuous variables are winsorized at the 1% and 99% levels.

Ultimately, a total of 31,525 observations from 3,794 listed firms are obtained. The software used for data processing is Stata 17.0.

Variable Definition

Dependent Variable

Corporate Total Factor Productivity (TFP). The TFP of firms is calculated based on the methodologies established by Levinsohn and Petrin (2003;hereinafter referred to as LP) and Olley and Pakes (1996;hereinafter referred to as OP). The methods for calculating TFP are well-developed in existing research and can be categorized into parametric and non-parametric approaches. Parametric methods include OLS, GLS, OP, and LP, while non-parametric methods mainly encompass the index method and Data Envelopment Analysis (DEA).

The index method and DEA are often applied to national, industrial, or regional data. Parametric methods are more suitable for specific company data. The LP and OP methods, based on price-weighted approaches, take into account the impact of factor price changes on production efficiency. These methods more accurately measure TFP, reflecting the actual changes in production efficiency. The OLS method, when applied to panel data, requires sufficient justification that the part of observable TFP influencing corporate decisions varies by firm but remains constant over time. The GLS method is typically used to address heteroscedasticity and correlation issues in parametric estimation rather than directly for TFP calculation. The OP and LP methods describe the efficiency of resource and knowledge utilization, indicating the optimal outcomes achieved by the economy in terms of output. The fixed effects model effectively corrects for simultaneity bias and sample selection bias, mitigating endogeneity issues. Both methods are also more suitable for calculating large amounts of secondary data, enhancing their operational feasibility. The concurrent use of the OP and LP methods helps control for biases in estimating corporate production efficiency due to differences in estimation techniques. This study references the calculation methods of Yu (2019) and Wang et al. (2023), constructing the OP calculation model (1) as follows:

Where Y represents corporate revenue; K denotes the net value of fixed assets; L stands for the number of employees; Age is the logarithm of the firm’s age; Soe indicates whether the firm is state-owned; EX signifies whether the firm engages in exports, and Exit denotes whether the firm has exited the market. Year, Prov, and mnd represent fixed effects for the year, region, and industry, respectively. Total factor productivity is derived from the logarithm of the residuals obtained from the regression model (1). Additionally, following practices from other literature, all continuous variables are Winsorized at the 1% and 99% levels before calculating total factor productivity, thereby controlling for the influence of outliers.

Model (2) represents the calculation model using the LP method. The LP method, building upon the OP method, introduces intermediate input M as a proxy variable to address the issue of sample loss caused by the requirement that the investment variable must be greater than zero in the OP method. Referring to the approach by Yu (2019), the cash paid for purchasing goods and receiving services is used as a proxy for intermediate input M. Due to its relative superiority over the OP method, this study employs the LP method to calculate total factor productivity for the primary hypothesis regression while using the OP method for robustness checks. In the primary hypothesis, corporate total factor productivity is derived from the residuals obtained from the regression of model (2), whereas for robustness checks, total factor productivity is obtained from the residuals of model (1).

Mediating Variable

Corporate Digital Transformation (Dig). Existing methods for measuring corporate digital transformation primarily include three approaches. The first approach uses a “0-1” dummy variable to indicate whether the firm has undertaken digital transformation in a given year. The second approach measures the proportion of digital projects within the total intangible assets. The third approach employs the frequency of related digital terms in annual reports as a proxy variable for digital transformation. F. Wu et al. (2021) suggest that the third method effectively captures the firm’s overall strategic direction and future development path, making the term frequency approach both feasible and scientific. Therefore, this study adopts the term frequency method based on existing digital transformation literature, processed as follows:

First, all annual reports of A-share listed firms are obtained from the official websites of the Shanghai Stock Exchange and the Shenzhen Stock Exchange using Python technology. Second, the textual content of the annual reports is extracted using the Java PDFbox library. Subsequently, based on existing literature, the jilbab library is utilized for word segmentation, extracting keywords such as mobile internet, industrial internet, mobile connectivity, internet healthcare, and e-commerce. Keywords with negative prefixes are excluded during extraction, and the frequencies of the remaining keywords are summed to form the total term frequency. Given the right-skewed nature and significant variability of term frequencies, the logarithm of the aggregated term frequency is used as the proxy variable for corporate digital transformation (Dig).

Independent Variable

CEO Information Technology Background (CEO_technology). Referring to R. Li et al. (2022), CEOs with educational or professional experience related to firm information management or information technology are classified as having an information technology background. Thus, if a CEO possesses education or professional experience relevant to firm information management or information technology, the variable is assigned a value of 1; otherwise, it is 0.

Control Variables

Following existing literature (e.g., Shen et al., 2019; Yin et al., 2021; Zhang & Tian, 2020), this study selects the following control variables: firm size (Siz), return on equity (Roe), inventory ratio (Inv), capital occupation by major shareholders (Occ), management shareholding ratio (Msh), proportion of independent directors (Ind), book-to-market ratio (Bm), total asset turnover (Ato), revenue growth rate (Gro), cash flow ratio (Cah), firm age (Age), and the shareholding ratio of the largest shareholder (Top1). Definitions of these variables are detailed in Table 1.

Variable Definitions.

Model Construction

This study employs Model (3) to test the main regression effect. Drawing on the methodology of Wen et al. (2004) for examining mediating effects, this study constructs a system of Equations 3–5, using a stepwise approach to verify the mediating role of digital transformation.

In the first step, this study performs a regression analysis of corporate total factor productivity (TFP_LP) and CEOs with information technology backgrounds to determine whether the total effect regression coefficient, specifically the coefficient of the independent variable, is significantly positive.

In the second step, this study tests the standardized regression coefficient of CEOs with information technology backgrounds on digital transformation in Model (4) and the standardized regression coefficient of digital transformation on corporate total factor productivity (TFP_LP) in Model (5). This involves assessing whether the standardized regression coefficients of the independent variable on the mediating variable and the mediating variable on the dependent variable are both significant.

If the results of the above steps are significant, this study proceeds to the third step. Here, this study conducts a regression analysis involving corporate total factor productivity (TFP_LP), CEOs with information technology backgrounds, and the mediating variable, digital transformation, to examine if the coefficient of the CEO’s information technology background changes. Specifically, this study assesses whether the standardized regression coefficients of the independent and mediating variables on the dependent variable in Model (5) are significant.

If the regression coefficient of CEOs with information technology backgrounds is not significant, it indicates that the mediating effect of digital transformation is significant and plays a full mediating role. If the regression coefficient of CEOs with information technology backgrounds remains significant, it implies that the mediating effect of digital transformation is significant and serves as a partial mediator.

Where

Empirical Results and Analysis

Descriptive Analysis

Table 2 presents the descriptive statistics of each variable. The mean value of corporate total factor productivity (Tfp_lp) is 8.86, with a median of 8.76, indicating that the majority of Chinese firms have not reached the average level of total factor productivity. The standard deviation is 1.098, suggesting a certain degree of fluctuation in total factor productivity among Chinese firms. The maximum value of corporate digital transformation (Dig) is 4.96, with a minimum value of 0, a median of 0.69, and a standard deviation of 1.365, reflecting a significant disparity in the degree of digital transformation among different firms in China. The mean value of the independent variable, CEO information technology background (CEO_technology), is 0.0757, indicating that only 7.57% of the CEOs in the sample firms have an information technology background. The standard deviation is 0.264, showing a certain level of variability in the IT background of CEOs among the sample firms.

Results of Descriptive Statistics.

Correlation Analysis

Table 3 presents the results of the correlation analysis. Without considering other control variables, this study finds that the correlation coefficient between CEOs with information technology backgrounds and corporate digital transformation is .028, significant at the 1% level. This indicates a positive correlation between the two, providing preliminary support for subsequent research. Additionally, the Variance Inflation Factor (VIF) values for all variables were checked for multicollinearity, and none exceeded the threshold, indicating that multicollinearity is not a serious concern.

Correlation of Key Variables.

Note.*** and ** are significant at 1%, 5%, and 10%, respectively.

Basic Regression and Mediation Effect Analysis

Using Stata 17.0, this study performed a regression analysis on Model (1). The results are presented in column (1) of Table 4, which reports the basic regression outcomes, specifically the impact of CEOs’ information technology backgrounds on corporate total factor productivity. From column (1) of Table 4, it is evident that the coefficient for CEOs’ information technology backgrounds is 0.0432, significant at the 1% level. This validates Hypothesis 1, indicating that CEOs with information technology backgrounds significantly enhance corporate total factor productivity. These findings are consistent with existing literature (Song, 2023; Zhang, 2023).

Basic regression and mediation effect results.

Note.***, **, and * are significant at 1%, 5%, and 10%, respectively.

Columns (2) and (3) of Table 4 present the results of the mediation effect analysis of digital transformation. First, column (2) shows the regression results between corporate total factor productivity and CEOs’ information technology backgrounds, consistent with the basic regression results. Column (3) reports the regression results of the mediating variable, demonstrating that CEOs with information technology backgrounds significantly promote corporate digital transformation at the 1% level, with a coefficient of 0.6721.

Column (4) of Table 4 examines the mediation effect of digital transformation. The results reveal that when the mediating variable of corporate digital transformation is included, the effect of CEOs’ information technology backgrounds on total factor productivity remains significant at the 10% level. Furthermore, corporate digital transformation significantly enhances total factor productivity at the 1% level, indicating that digital transformation partially mediates the relationship. This implies that CEOs with information technology backgrounds improve total factor productivity by fostering digital transformation within their firms.

These results illustrate that CEOs with information technology backgrounds possess a sufficient digital mindset and, as senior decision-makers, actively choose, support, and implement digital transformation initiatives. They are willing to embrace and drive digital change, assume the associated risks, support digital transformation initiatives, and create a digital vision, thereby paving a successful pathway to enhance total factor productivity.

Endogeneity Treatment and Robustness Tests

Endogeneity refers to the correlation between the independent variables and the error term in a model, which can lead to biased and inconsistent parameter estimates. Common methods to address endogeneity include Propensity Score Matching (PSM), the Heckman two-stage model, Instrumental Variables (IV) using Two-Stage Least Squares (2SLS), variable substitution, and lagged regression. These techniques aim to ensure the accuracy and reliability of the model’s results, thereby better elucidating the causal relationships between variables and avoiding bias induced by endogeneity.

Propensity Score Matching (PSM)

PSM is employed to address selection bias by estimating the propensity scores of the treatment and control groups and then matching similar individuals, thereby reducing the endogeneity of the treatment effect. The calculation of corporate total factor productivity using the LP method is inherently influenced by firm-specific characteristics such as asset size, financial leverage, and revenue. Therefore, to mitigate the impact of these characteristics on total factor productivity, this study uses the previously mentioned control variables as covariates. Through a logit model, a 1:1 nearest neighbor matching is conducted to alleviate the endogeneity problem caused by firm-level characteristics.

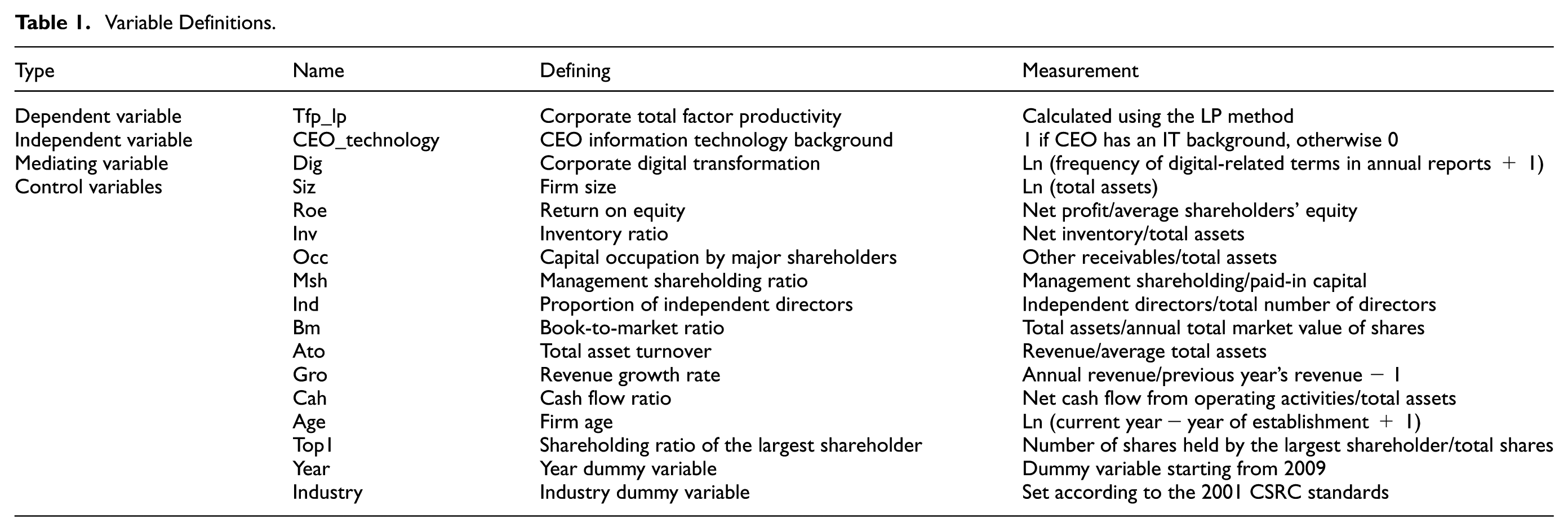

Figure 2 shows the kernel density distribution before and after matching based on the CEO’s information technology background. As illustrated, there is a significant difference in the kernel density curves before matching; however, after matching, the kernel density curves for firms with and without CEOs with IT backgrounds are similar, indicating a good matching effect. The kernel density plots after PSM matching satisfy the common support assumption.

Kernel density before and after PSM matching.

Table 5 reports the regression results after PSM matching. Column (1) of Table 5 shows the impact of CEOs’ information technology backgrounds on corporate total factor productivity. After mitigating the influence of firm-level characteristics through PSM, it is evident that CEOs with information technology backgrounds significantly enhance corporate total factor productivity at the 1% level.

PSM and Heckman Two-Stage Test Results.

Note.***, **, and * denote significance at the 1%, 5%, and 10% levels, respectively, with t-values in parentheses.

Heckman Two-Stage Model

This study employs the Heckman two-stage estimation method to address the potential bias that CEOs with information technology backgrounds might preferentially select firms with higher total factor productivity, thereby avoiding selection bias that may arise during data measurement. This study constructs a Heckman two-stage model to test related endogeneity issues.

In the first stage, following the methodology of Yin et al. (2021), this study uses the average information technology background of CEOs from other firms in the same year and industry (Mean_CEO_technology) as the instrumental variable for the CEO’s IT background. Using this instrumental variable as the independent variable and whether the CEO has an IT background as the dependent variable, this study constructs a Probit model based on the control variables mentioned earlier to calculate the inverse Mills ratio (IMR) for the CEO’s IT background.

In the second stage, this study includes the inverse Mills ratio corresponding to the CEO’s IT background as a control variable in the regression. If the inverse Mills ratio is not significantly different from zero, it indicates that there is no sample selection bias in the equation. If it is significant, it indicates the presence of sample selection bias.

Table 5 reports the regression results of the Heckman two-stage model. Column (2) of Table 5 shows the Probit model regression results for the CEO’s IT background using the constructed instrumental variable. The mean of the instrumental variable, Mean_CEO_technology, is significant at the 1% level, initially indicating the validity of the selected variable. Column (3) of Table 5 presents the regression results after controlling for the corresponding inverse Mills ratio. The coefficient for the CEO’s IT background is 0.0433, which is significant at the 1% level, while the IMR is not significant. This suggests that there is no evident selection bias in the model for the CEO’s IT background, and it continues to enhance corporate total factor productivity.

These results indicate that after mitigating potential selection bias, CEOs with information technology backgrounds still promote corporate total factor productivity, confirming the robustness of the study’s conclusions.

Instrumental Variables 2SLS

The Instrumental Variables (IV) 2SLS method is employed to address endogeneity issues. By using instrumental variables, this study can resolve the correlation between the independent variable and the error term in the causal relationship, thereby obtaining consistent estimates. According to previous research, the information technology background of CEOs can promote corporate total factor productivity. However, it can still be argued that firms with higher levels of total factor productivity might prefer to hire CEOs with an IT background to oversee their operations, leading to endogeneity in the model. Therefore, this study uses the average IT background of CEOs from other firms in the same year and industry (Mean_CEO_technology) and the lagged IT background of the CEO (L.CEO_technology) as instrumental variables. This study then performs a 2SLS regression to test the robustness of our conclusions.

Column (1) of Table 6 presents the first-stage regression results for the instrumental variables. The results show that both the average IT background of CEOs and the lagged IT background of the CEO are significant at the 1% level, indicating the validity of the selected instrumental variables. Column (2) of Table 6 displays the second-stage regression results for the instrumental variables. The findings reveal that, after accounting for the endogeneity issues in the model, the IT background of CEOs continues to significantly promote corporate total factor productivity, with a coefficient of 0.0627, significant at the 1% level. This further corroborates the robustness of the study’s conclusions.

Results of Endogeneity and Robustness Tests.

Note.***, **, and * denote significance at the 1%, 5%, and 10% levels, respectively, with t-values in parentheses.

Lagged Regression

Lagged regression introduces lagged dependent variables as independent variables to control for inherent correlations in the data. Given that the sample data may exhibit reverse causality—whereby corporate total factor productivity might influence the CEO’s background—this study addresses endogeneity issues stemming from reverse causality by lagging the CEO’s information technology background and conducting the regression anew. As shown in column (3) of Table 6, even with the one-period lag, the CEO’s information technology background continues to significantly enhance corporate total factor productivity at the 1% level, affirming the robustness of our conclusions.

Replacing the Dependent Variable

The replacement variable method controls for endogeneity by introducing alternative variables, thereby achieving more accurate model parameter estimates. Given that corporate total factor productivity can be calculated using OLS, LP, and OP methods, each with inherent differences, this study considers that the conclusions might be influenced by the method used to calculate the dependent variable. To ensure consistency in the sample, this study recalculated corporate total factor productivity using the OP method (Tfp_op) and performed the regression again. As displayed in column (4) of Table 6, after replacing corporate total factor productivity with the OP method, the coefficient for the CEO’s information technology background is 0.0436, significant at the 1% level, thereby validating our key conclusions.

Further Analysis

Heterogeneity Analysis Based on Financing Constraints

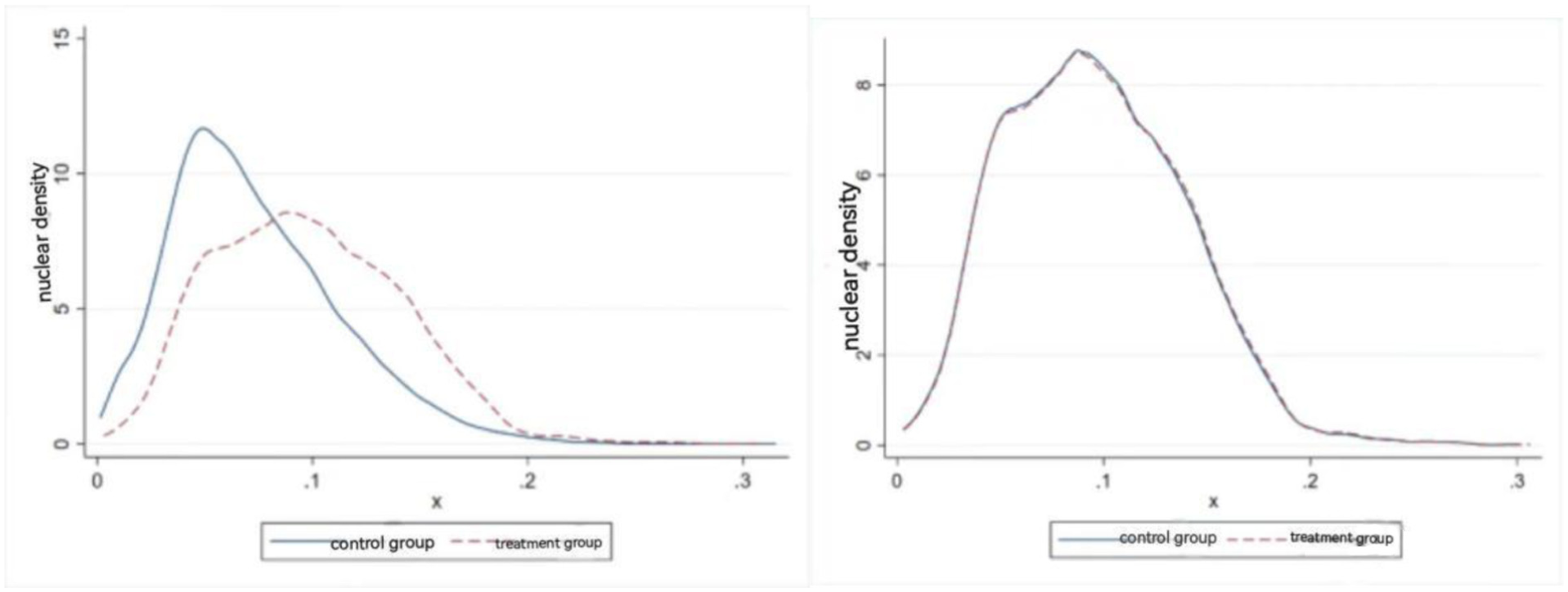

Existing research posits that when firms face financing constraints, the financial support falls short of meeting the actual capital needs required for their rapid and stable growth, thereby inhibiting the improvement of production efficiency (Lu et al., 2023). Consequently, the limitations imposed by financing constraints can suppress corporate R&D investments and other activities, creating a significant resource gap for technological upgrades, which is detrimental to the enhancement of total factor productivity. However, a CEO with an information technology background can serve as a bridge between the firm and other stakeholders, potentially bringing resources that can play a positive role when the firm is facing severe financing issues. To explore whether financing constraints can act as a heterogeneous factor in the influence of a CEO’s IT background on corporate total factor productivity, this study uses the median financing constraint of all firms in the industry for the current year as a benchmark to classify the overall sample with high and low financing constraints for subgroup regression.

Table 7 reports the regression results based on financing constraints. As shown, in the group with high financing constraints, the coefficient for the CEO’s information technology background is 0.0628, significantly enhancing corporate total factor productivity at the 1% level. In contrast, in the group with low financing constraints, the CEO’s IT background does not exhibit a significant relationship. This indicates that there is heterogeneity in the impact of a CEO’s IT background on corporate total factor productivity based on financing constraints.

Regression Results for Heterogeneity.

Note.***, **, and * denote significance at the 1%, 5%, and 10% levels, respectively, with t-values in parentheses.

Heterogeneity Analysis Based on Agency Costs

According to agency theory, shareholders and managers of a firm have different benefit preferences. For owners, their profits are closely linked to the overall value and efficiency of the firm. Owners prefer that the firm’s resources are reasonably applied to enhance corporate value and efficiency. However, when agency costs are high, managers tend to indulge in excessive consumption and asset occupation, thereby misallocating corporate resources, which leads to a loss in resource allocation efficiency and negatively impacts total factor productivity. Therefore, when agency costs are high, there may be significant room for improvement in total factor productivity. To explore whether internal agency issues can influence the relationship between CEOs’ IT backgrounds and corporate total factor productivity, this study measures agency costs using the ratio of management expenses to corporate revenue. The median agency cost within the same industry and year is used as a benchmark to classify firms into high and low-agency cost groups. Firms with agency costs higher than the industry-year median are classified into the high agency cost group, while those with lower costs are placed in the low agency cost group.

Columns (3) and (4) of Table 7 present the regression results for CEOs’ IT backgrounds. The results indicate that in the high agency cost group, CEOs with IT backgrounds significantly enhance corporate total factor productivity, while in the low agency cost group, the relationship does not pass the significance test. This suggests that there is heterogeneity in the impact of CEOs’ IT backgrounds on corporate digital transformation based on agency costs.

Research Conclusions and Discussion

Research Conclusions

Building on a digital transformation perspective and leveraging micro-level enterprise data, this study explores how a CEO’s information technology background boosts total factor productivity, thereby fostering high-quality corporate development. Employing LP and OP methods to measure total factor productivity alongside the Java PDFBox library to extract annual report text for constructing the digital transformation variable, this study analyzes data from publicly listed firms. Our empirical findings confirm a positive association between the CEO’s IT background and total factor productivity, broadening the scope of existing research on productivity drivers and corroborating earlier studies (Song, 2023; Zhang, 2023).

CEOs with IT backgrounds contribute to the improvement of corporate total factor productivity by providing specialized knowledge and technical expertise. Mechanism tests reveal that such CEOs enhance digital innovation capabilities within firms and promote digital transformation by supervising and advising on digital innovation activities, thus boosting total factor productivity. Digital transformation acts as a mediating variable, partially mediating the relationship between CEOs’ IT backgrounds and total factor productivity. CEOs with IT backgrounds typically have a better understanding of the firm’s core business and possess keen insights into technological developments and trends. This enables them to formulate future development strategies more effectively, driving the firm to achieve a competitive edge in the digital era and enhance total factor productivity.

Furthermore, the study finds that the positive impact of CEOs’ IT backgrounds on total factor productivity is significant in groups with high financing constraints and high agency costs, whereas this effect is not evident in groups with low financing constraints and low agency costs. The results highlight the divergence in research findings across various enterprises.

Discussion

Human resources, as the most vibrant and pivotal resource in corporate operations, exert a profound influence on total factor productivity. Centering our research on the micro-level enterprise perspective, we discover that a CEO’s information technology background is both the lynchpin for advancing digital transformation and the critical mechanism for elevating total factor productivity. Building upon prior studies, this study extends the scope of upper-echelon theory, enriches the determinants of corporate total factor productivity, and elucidates the linkage between a CEO’s IT expertise and productivity gains. Simultaneously, it deepens our understanding of how a CEO’s technological proficiency spurs digital innovation and highlights the economic ramifications of IT-savvy leadership in a digital context. Our findings align with those of Cette et al. (2022), who show that employing both internal and external IT specialists can boost total factor productivity by 17%. Furthermore, these findings offer rigorous empirical evidence supporting McKinsey’s 2018 conclusion that digitally skilled leaders are paramount to the success of digital transformation. The key contribution of this study lies in broadening the factors that enhance corporate total factor productivity, reflecting the heightened importance of human capital in the modern era and underscoring the unique role of top executives’ attributes in guiding high-quality economic transformation.

Human resource endowment exerts a pivotal influence on elevating corporate productivity (Chen Qian et al., 2020). A CEO with an information technology background determines the success or failure of a firm’s digital transformation through their cognition and comprehension of digital technologies and innovation outcomes. Digital innovation should holistically account for managerial perception, the construction of digital meaning, and the allocation of digital resources, driving the entire organization toward recognition and understanding of digital technology and novel innovations. Within corporate management, businesses must not overlook the personal traits of CEOs and their respective leadership teams; rather, they should uncover the latent potential of senior executives and fully harness the unique advantages of human resource endowment. By recruiting IT-savvy executives or offering internal skill-development programs, companies can strengthen leaders’ digital innovation awareness. Relying on IT-background professionals’ affinity for technological disruption, along with their deep expertise and industry insight, provides strong support for digital transformation initiatives. Managers themselves must pursue continuous learning, proactively heightening their digital awareness and fostering an organizational culture that encourages innovation.

China’s economic progress hinges on reinvigorating production factors and sparking creative momentum while steadfastly refining lean management policies across the workforce, all relevant factors, and the entire value chain. Harnessing big data, artificial intelligence, and blockchain technologies can propel businesses toward digital transformation and tangibly raise total factor productivity. The Chinese government should refine its talent governance framework, emphasize talent recruitment, enact supporting policies, and fully realize the value of human capital. Furthermore, the government should collaborate with enterprises, each from its vantage point, to leverage the distinctive human and social capital of IT-background professionals, jointly prompting companies to embrace digital strategic transformations and enhance total factor productivity.

With the dawn of a comprehensively intelligent era in China, enterprises confronted by new opportunities and challenges are further defining their strategies for full-scale smart development, and an increasing number of firms are considering hiring CEOs with IT management expertise. China’s institutional environment likewise provides a fitting arena for these research concerns. As the world’s second-largest economy, the country stands at a decisive juncture in its development, with the “new normal” emphasizing high returns on capital at the industrial and financial levels and urgently requiring improvements in total factor productivity at the enterprise level. This imperative underlies the original motivation for this study, and these issues have been effectively addressed herein.

Limitations and Future Research Directions

This study, adhering to rigorous scientific standards and norms, examines the relationship between CEOs with information technology backgrounds and corporate total factor productivity within the context of digital transformation, based on data from Chinese A-share listed firms. The empirical analysis yields relevant conclusions that provide theoretical insights and verification potential. However, the study has several limitations and areas for improvement.

First, in terms of sample selection, this study focuses on Chinese A-share listed firms due to considerations of representativeness and data availability. While the findings offer general significance, they may lack specificity within particular contexts. Different industries have varying levels of attraction for CEOs with IT backgrounds, and the developmental status of industries also varies, making it difficult to generalize CEO decision-making perspectives. Future research could investigate specific industries individually. Additionally, research could be conducted by different market segments, as the nature of listed firms varies across different stock market segments. The main board predominantly features leading enterprises, whereas the Growth Enterprise Market (GEM), SME board, and STAR Market are composed of smaller, private, and high-tech enterprises. These firms have differing levels of attraction and demand for IT talent, making segmented research a future direction worth exploring.

Second, regarding research methodology, this study primarily relies on empirical analysis of secondary data due to limitations in data and information accessibility. Secondary data may not fully reflect the actual conditions of firms. Future research could incorporate in-depth interviews, surveys, and other methods to conduct thorough investigations within firms. This would provide a deeper understanding of how CEOs with IT backgrounds influence digital transformation decisions and identify other key factors impacting total factor productivity, resulting in more comprehensive and nuanced research conclusions.

Footnotes

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Guangzhou Huashang College Mentorship Program (2022HSDS29); Guangdong Provincial Department of Education (Yue Jiao Gao Han [2023] No. 4, Item 1094).

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data supporting this study’s findings are available from the corresponding author upon reasonable request.