Abstract

In recent years, the dynamics of housing prices have garnered significant attention in China, particularly the inter-city relationships of these prices. Despite its relevance, scholarly discourse has been somewhat constrained by the limitations of methodologies and the depth of discussion, leaving the underlying mechanisms inadequately elucidated. Anchored in the theoretical framework of new economic geography, this study embarks on a comprehensive examination of urban population, integrating pertinent macroeconomic variables to refine the theoretical model concerning the inter-urban housing price dynamics from the vantage point of urban population. Methodologically, the investigation employs benchmark regression analyses and incorporates various interaction terms to assess the impact of urban population on housing price disparities and to elucidate the transmission mechanisms through which macroeconomic indicators, such as household financial behaviors, influence housing price variations via household income. Findings suggest that population plays a pivotal role in driving the disparities in housing prices across cities. Specifically, variables such as the growth rate of deposits, the growth rate of leverage ratios, and the national average growth rate of urbanization exert a positive influence on housing price differentials by impacting urban population. It meas some macro indicators related to household financial behavior can provide a theoretical explanation for urban housing price differentiation. This study contributes to the existing literature by bridging identified gaps, unraveling the mechanisms through which population influences purchasing behaviors, and the allocation of household assets and liabilities. Moreover, it offers critical insights for governmental bodies in crafting policies aimed at stabilizing the investment cycle with precision, which also provides reference suggestions for household investment and savings behavior.

Introduction

In recent years, the dynamics of the real estate market and the fluctuation of housing prices have garnered widespread attention across societal echelons. The real estate industry is a pillar of China’s economy and is of great significance for national economic development. The changes in this industry and the new characteristics that emerge during its development are worthy of our continuous attention and study. Real estate emerges as a principal conduit for monetary allocation and a significant channel for the flux of residents’ wealth, encompassing both residential occupation and investment ventures. It has become commonplace among numerous households to allocate substantial savings toward the acquisition of property, or to engage in borrowing and leveraging strategies for home purchases. The relentless progression of urbanization within China and the continuous population flow predicate a shift in the patterns of property acquisition for dwelling or investment purposes, marking a pivotal aspect of familial financial conduct.

The discourse on the real estate market customarily categorizes major urban centers into tiers-first, second, third, and fourth-based on predefined criteria for analytical scrutiny. The impetus behind capital flow gravitates toward the procurement of premier assets, with the real estate nestled within the core regions of first and second-tier cities being deemed as prime investment targets. This inclination precipitates the further aggregation of financial resources, thereby inflating the housing prices within metropolitan areas. A general understanding prevails among the populace that the investment allure of properties in first and second-tier locales surpasses that of their third and fourth-tier counterparts, leading to pronounced disparities in their respective housing prices. Traditionally, population changes have a significant impact on urban housing price fluctuations. Aspects such as population growth, migration, demographic structure, and aging are all important areas for our attention. Moreover, urbanization in China is continuously progressing, and the connections between urban populations and cities are becoming increasingly close. The allure of enhanced employment prospects and superior wage offerings in larger cities magnetizes population influxes toward these urban conglomerates, resulting in the depopulation of third and fourth-tier cities. This scenario stymies the escalation of housing prices in these areas, leaves land parcels unutilized, and gradually precipitates urban vacuity, thereby exacerbating the differentiation in housing prices across cities. The academic sector, in recent years, has exhibited a paucity of methodological depth and breadth in dissecting this phenomenon, particularly in the elucidation of underlying causatives and mechanisms through the deployment of suitable indexical models.

The differentiation in housing prices among cities at different levels has led to various severe problems. Firstly, the scarcity of land and housing, along with the soaring housing prices in first-tier cities and second-tier cities, significantly increases the difficulty for residents to address housing issues. This phenomenon has also led to the economic transformation into a real estate-centric model due to substantial investments and speculative activities, resulting in the rapid accumulation of risks associated with large-scale credit defaults. Secondly, in third-tier cities and below, the extensive investment in land and housing supply has led to a surplus of land and housing, causing substantial idle and stockpiled resources. This situation results in significant resource waste and financial pressures, with real estate development enterprises facing the risk of bankruptcy and the breakdown of financial chains. Thirdly, the excessive differentiation in housing prices also leads to the misalignment of production factors and economic activities in spatial terms. Therefore, researching and addressing the influencing factors and mechanisms of the excessive differentiation in housing prices among cities is of significant theoretical and practical importance.

Literature Review

When analyzing the factors influencing housing price divergence, it is essential to review the literature on factors driving housing price increases. The essence of housing price divergence lies in the varying trends of housing price increases across different cities. Therefore, in analyzing the factors influencing housing price divergence, we first need to review the literature on factors driving housing price increases. A substantial body of domestic and international literature has explored the factors influencing housing price increases, focusing mainly on four categories of factors. Firstly, demand factors. An increase in population size and density, rising income levels, improved infrastructure, and better education and healthcare all contribute to increased housing demand, thus driving up urban housing prices (Takáts, 2012; Zou et al., 2015). Secondly, supply factors. Tightened land supply and rising construction costs increase housing supply costs, subsequently pushing up housing prices (Chow & Niu, 2015; Glaeser et al., 2017). Thirdly, macroeconomic policy factors. Expansionary monetary policies, such as credit easing and interest rate cuts, typically lead to higher housing prices (Jarociński & Smets, 2008). Fiscal imbalances faced by local governments also significantly contribute to the continuous rise in urban housing prices, with land finance serving as an intermediary variable connecting the two (Gong, 2015; M. Wang et al., 2013). Fourthly, expectation factors. Enhanced expectations of housing price increases and rising optimism among residents can significantly promote housing prices (Abildgren et al., 2018).

As the differentiation of housing price trends in different cities continues, more and more literature is directly focusing on the causes of housing price differentiation, and the factors discussed in this literature can largely be categorized into the four types mentioned above. In terms of demand factors, actually, the inequality in public services is an important factor leading to housing price divergence across cities (Chen & Tang, 2017). In terms of supply factors, the root cause of housing price divergence lies in the spatial mismatch between land supply and demand through comparing land supply policies across different cities regarding supply factors (Han & Lu, 2018). Due to differences in endowment conditions, different cities adopt different land supply strategies, which have heterogeneous impacts on housing prices, thereby leading to housing price divergence (Liu & Yang, 2019) . In terms of macroeconomic policy, the impact of monetary policy on housing prices varies significantly between cities in different provinces, but is relatively consistent within cities in the same province regarding macroeconomic policy factors (Tu et al., 2018). In terms of expectation factors, regarding expectation factors, some authors used panel data from 34 major cities from 2000 to 2013 and showed that the impact of expectations on urban housing prices varies significantly across regions (L. Wang & An, 2016). The literature mentioned above primarily employs two types of traditional econometric methods when analyzing the factors influencing the rise in housing prices and the differentiation of housing prices in different cities. The first type is panel regression models, which mainly include panel fixed effects models, dynamic panel regression models, threshold regression models, panel Probit models, and panel cointegration models. The second type is VAR models, which mainly include traditional VAR models, SVAR models, BVAR models, and TVPVAR models. In fact, due to the market structure of monopolistic competition, the explanation of regional equilibrium in new economic geography is closer to reality. Regional inequality is a core issue in geography and can be measured through various methods and indicators. However, global inequality metrics fail to capture the spatial and non-mobility characteristics of regions, nor do they adequately explore regional inequality in specific directions. While traditional inter-group inequality indices can measure inequality in specific directions, they cannot reflect reversals in regional patterns or changes within groups. Therefore, the specific direction inequality index (PDI) has been proposed as a new method applicable in the field of geography to measure regional inequality in specific directions. It can reflect the spatial and non-mobility aspects of regions, determine the primary direction of regional inequality, and capture changes and reversals in regional patterns (Y. Wang et al., 2012). Research using the PDI differentiation index found that there is a significant spatial differentiation phenomenon in urban residential prices in China, with the main direction of differentiation being the hierarchical distinction between first-tier cities and other cities(Y. Wang et al., 2015).

In essence, the interplay of urban housing prices transcends mere inter-city market dynamics, extending into broader environmental and policy influences at a regional, and notably, national level. The discussed body of literature serves as a foundation for a more nuanced exploration of the mechanisms underpinning inter-city housing price differentiation and the role of population in influencing urban housing price disparities, hence opening avenues for innovation. This study aims to, theoretically, merge macroeconomic perspectives with regional market dynamics. It leverages the new economic geography theoretical framework, with a particular focus on the housing sector and urban population variables, to refine the theoretical model addressing the relationship between urban housing prices. Empirically, this research not only undertakes a benchmark regression analysis of the determinants of housing price differentiation but also, through the incorporation of various interactive variables pertaining to household financial behavior, delves into the transmission mechanisms by which macro indicators of the housing sector influence housing price differentiation via urban population. Consequently, it offers a systematic elucidation of the mechanisms driving housing price differentiation among cities.

Principles

In major urban centers, housing price differentiation is notably pronounced. The surge in housing demand within these cities can be attributed to income disparities and population mobility, contrasting with the relatively subdued demand in smaller urban locales. Differences in scale, living standards, work environment, etc. among different cities precipitate labor force spatial mobility, exacerbating the spatial incongruity between housing demand and real estate supply. Consequently, this exacerbates the divergence in housing prices between major and minor urban centers, exerting profound effects on the real estate market dynamics.

Household financial status primarily refers to the asset-liability and cash flow situations of residents’ families. For urban households, common financial behaviors include purchasing assets, borrowing, and saving cash. For households, real estate investment is a significant facet, often financed through withdrawing bank deposits. This investment serves not only for self-occupation but also as a prudent financial endeavor. With the ongoing urbanization across China, varying product types and values exist across different cities. Consequently, households typically opt to procure the best real estate within their financial means to ensure comfort and asset appreciation. Mortgage loans constitute a substantial portion of many individuals’ borrowing endeavors, particularly during real estate market upswings. During periods of market buoyancy, heightened expectations of rising house prices prompt residents to liquidate deposits for real estate acquisitions, often facilitated by bank loans and leveraging to procure premium properties. Conversely, during market stability or downturns, residents may opt to deposit surplus funds in banks, adopt a wait-and-see approach, or even undertake premature loan repayments to mitigate household leverage and financial risks. Moreover, in periods of rapid urbanization, there will be more people entering big cities. From a macroeconomic standpoint, comprehending the aggregate financial landscape of residential sectors assumes paramount importance, where overall leverage ratios and deposit growth stem from individual household behaviors. The population is related to the supply and demand of urban property, which affects housing prices. It is rational to infer that urban population exerts a discernible influence on urban housing price differentiation, with household deposits and leverage ratios modulating housing price dynamics through urban population fluctuations. Furthermore, distinct stages of urbanization development also imprint significant effects on urban population levels.

Based on the literature review and the above analysis, the research questions of this paper primarily focus on examining whether urban population is a cause of price differentiation among cities and whether macro indicators of household financial behavior exacerbate this differentiation. We propose the following hypotheses: (1) Urban population differentiation indeed exacerbates price differentiation; (2) Changes in macro variables of household financial behavior will influence price differentiation through urban population differentiation.

The innovation of this study lies in its enhancement of the theoretical framework governing inter-city housing price relationships. Building upon the foundation of the new economic geography theoretical model, this paper endeavors to refine the understanding of housing price differentiation by incorporating macroeconomic factors and delving into the intricacies of urban population dynamics. Through a meticulous examination of urban population patterns and the inclusion of pertinent macro variables pertaining to residents’ family financial behavior, the theoretical model governing inter-city housing price relationships is augmented. Empirically, employing benchmark regression techniques supplemented with diverse interactive components, this study scrutinizes the impact of urban population on housing price differentiation and elucidates the transmission mechanisms through which macro indicators such as deposit rates, leverage ratio growth, and urbanization rates influence housing price dynamics via urban population fluctuations. By bridging existing gaps in the literature, this research furnishes valuable insights for government policymakers seeking to stabilize investment cycles and steer monetary flows effectively.

Model Specification and Identification Strategy

The empirical model of this paper mainly focuses on testing whether urban population is the cause of housing price differentiation between cities and whether the macro indicators of household financial behavior of residents’ departments aggravate the housing price differentiation between cities. Through the construction of econometric model, the relevant indicators and data and processing are explained, and the possible endogenous problems are analyzed and processed to ensure the robustness of the research conclusions.

Econometric Model Setup

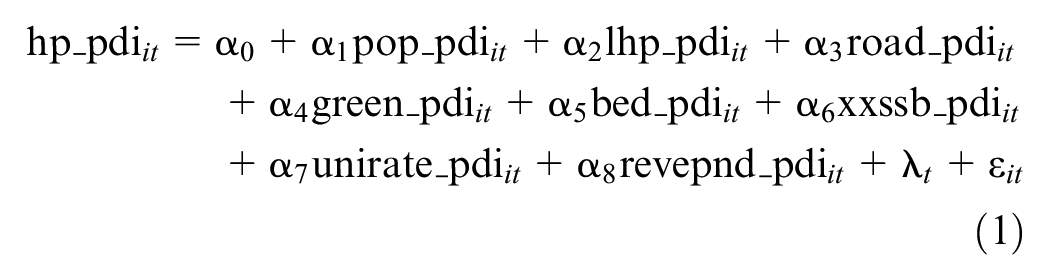

Firstly, adjust the model structure with reference to the benchmark model to test the influence of population between large and small cities on housing price differentiation. The basic measurement model is set as follows:

Here, i denotes the differentiation sample between large and small cities, t represents the respective year, and dependent variable hp_pdi is the housing price differentiation index, measuring the extent of housing price differentiation between large and small cities. Population differentiation index pop_pdi is key explanatory variable. Additionally, control variables such as housing price expectation differentiation index (lhp_pdi), per capita road area differentiation index (road_pdi), green coverage rate differentiation index of built-up areas (green_pdi), per capita bed number differentiation index (bed_pdi), primary school student-teacher ratio differentiation coefficient (xxssb_pdi), university student percentage differentiation index (unirate_pdi) and fiscal income-expenditure ratio differentiation index (revepnd_pdi) are incorporated. It is noteworthy that, theoretically, differentiation indices between large and small cities do not possess individual characteristics. Therefore, this study controls for time fixed effects without considering individual fixed effects.

Secondly, the macro variables including the growth rates of the leverage ratio within the residential sector, domestic credit, deposit rates, and the national average urbanization rate are ubiquitous across urban areas. Through the aforementioned analysis, it becomes evident that these macroeconomic variables indirectly influence housing prices by virtue of their impact on urban population disparities within the housing market mechanism. To investigate the mechanism by which changes in macroeconomic variables within the household financial sector affect housing price differentiation through variations in urban population, interactive terms between macro variables and differentiation indices are introduced into the benchmark model. Specifically, cross-terms involving the growth rates of the leverage ratio within the residential sector, domestic credit, deposit rates, and the national average urbanization rate are incorporated into the model. This augmentation enables a more comprehensive examination of the relationships among these variables and their influence on housing price dynamics. The model is delineated as follows:

Among them, Ai_growth represents the growth rate of leverage ratio, domestic credit growth rate, resident deposit growth rate and national average urbanization rate respectively. The interaction between population differentiation index and Ai_growth indicates that the influence of population differentiation index on housing price differentiation is affected by leverage ratio growth rate, domestic credit growth rate, resident deposit growth rate and national average urbanization rate growth rate. When the interactive term is positive, it means that the acceleration of index growth can enhance the promotion of population differentiation to housing price differentiation, while negative value is the opposite.

Sample, Variable Selection, and Explanation

Sample Selection and Explanation

After excluding cities with severe data deficiencies and those affected by administrative adjustments, this study chose a total of 273 cities at or above the prefectural level across China as the research sample. To obtain a more realistic alignment with urban classifications, the study adopts a classification into first, second, third, and fourth-tier cities. However, given the current lack of academic support for prevalent classification methods, this study opts for GDP scale, population size, and per capita disposable income as key indicators to determine urban tiers. Using data from 2010 to set relevant criteria, the 273 Chinese cities are classified into four groups: first-tier cities (4), second-tier cities (30), third-tier cities (70), and fourth-tier cities (169; Table 1).

Main Cities Groups of China.

In accordance with the aforementioned categorization, we employ the “Specific Direction Spatial Disparity Index” (PDI) method to measure and evaluate the spatial differentiation and changes between the “high-low” groups of regions (or cities). This approach calculates and derives nine specific disparity indices between the four groups, including: the disparity index between first-tier and second-tier cities, between first-tier and third-tier cities, between first-tier and fourth-tier cities, between second-tier and third-tier cities, between second-tier and fourth-tier cities, between third-tier and fourth-tier cities, between first-tier and non-first-tier cities, between first and second-tier and third-tier cities, and between first and second-tier and fourth-tier cities. The formula for calculating the Specific Direction Spatial Disparity Index (PDI) is as follows:

Where xi is the mean value of a certain indicator for the ith city in Group X, yj is the mean value of a certain indicator for the jth city in Group Y. μ is the mean value of the indicator for all measured cities, n is the number of cities in Group X, m is the number of cities in Group Y, MX is the power mean of Group X, MY is the power mean of Group Y. q is any positive value, in this study, it is set to 0.8. In summary, a higher PDI index indicates a more significant differentiation in that spatial direction.

Variable Selection and Explanation

The explained variable of this paper is the house price differentiation index hp_pdi, which uses the average selling price of urban commercial housing, and then calculates the house price differentiation index. As for the explanatory variables of housing demand, this paper selects the population differentiation index pop_pdi as the proxy variable of housing demand differentiation, and selects the urban population data to calculate the population differentiation index. The deposit growth rate is selected to describe the deposit growth rate of residential sector, and the leverage ratio growth rate of residential sector is selected to describe the debt ratio of residential sector. As a macro variable, it has the same impact on any city in a certain period of time, so there is no differentiation index.

To address potential bias caused by omitted variables, the econometric model also includes a series of control variables. (1) Housing price expectation differentiation index (lhp_pdi): using the lagged housing price as the current housing price expectation, the housing price expectation differentiation index is calculated based on this. (2) Per capita road area differentiation index (road_pdi): the per capita road area differentiation index is chosen to measure differences in urban road traffic construction. (3) Green coverage rate differentiation index of built-up areas (green_pdi): the green coverage rate differentiation index of urban built-up areas is selected to measure the differentiation of ecological environments among cities. (4) Per capita bed number differentiation index (bed_pdi): selecting the per capita bed number differentiation index, which best reflects the medical service situation, as a proxy variable for the degree of differentiation in medical levels among cities. (5) Primary school student-teacher ratio differentiation coefficient (xxssb_pdi): the primary school student-teacher ratio differentiation index is chosen to measure the degree of educational level differences among cities at different levels. (6) University student percentage differentiation index (unirate_pdi): university students represent human capital and also reflect housing demand, which, in turn, can influence housing price changes. (7) Fiscal income-expenditure ratio differentiation index (revepnd_pdi): when local finances are relatively tight, there is a greater incentive to drive up housing prices to obtain more land transfer income.

Data Source and Descriptive Statistics

Data Source

Considering the representativeness and availability of data, the time interval of the selected samples in this paper is from 2003 to 2016. The data sources are as follows: The housing price data comes from China Regional Statistical Yearbook, while urban population data is obtained from China Urban Construction Statistical Yearbook. Per capita road area, green coverage rate of built-up areas, number of hospital beds, number of primary school teachers, number of primary school students, number of college students, financial revenue, and expenditure and other data come from China Urban Statistical Yearbook and official website of National Bureau of Statistics. The growth rate of domestic credit is calculated by the balance of medium and long-term loans of financial institutions, and the growth rate of residents’ deposits is calculated by the data of residents’ income and expenditure. Secondly, this paper also uses interpolation method to fill up the records with obvious abnormal data and individual missing values. Finally, this paper uses the consumer price index (CPI) of the provinces where cities are located to adjust the nominal variables such as house price to the actual variables based on 2003.

Statistical Description

Using the PDI calculation formula and data from 273 cities between 2003 and 2016, nine types of differentiation indices between the four groups of cities are calculated for each variable, resulting in 126 observations. Descriptive statistics for the main variables are as follows (Table 2):

Descriptive Statistics.

Endogeneity Issues and Instrumental Variables

From the theoretical logic point of view, there is endogeneity between population and urban housing price. In view of the endogeneity caused by simultaneous problems and missing variables, this paper refers to Ni Pengfei (2019) and uses tool variables of population to alleviate estimation errors. Urban residents’ water consumption can serve as a suitable instrumental variable for urban population. This is because, on the one hand, an increase in the urban population inevitably accompanies a rise in urban residents’ water consumption. On the other hand, the impact of residents’ water consumption on urban housing prices is minimal. Data on urban residents’ water consumption mainly come from China Regional Statistical Yearbook.

Empirical Analysis

Given that the differentiation index data used in this study belongs to a long panel, FGLS is primarily used for estimation. Before conducting econometric tests, heteroscedasticity, autocorrelation within groups, and cross-sectional correlation tests were performed on the above econometric equations. The test results indicate the presence of heteroscedasticity between groups, autocorrelation within groups, and cross-sectional correlation, suggesting that the use of FGLS for estimation is appropriate. On the other hand, this study employs the instrumental variables set earlier and uses the 2SLS estimation method for estimation. In the 2SLS two-stage instrumental variable estimation process shown in Table 3, the F-values estimated in the first stage are all greater than the critical value at the 10% significance level set by Stock and Yogo (2002) This confirms that the instrumental variables set in this study is appropriate, and there is no weak instrumental variable problem.

Benchmark Regression.

Note. The values in parentheses represent t-values or z-values adjusted for heteroscedasticity.

***, **, * Denote statistical significance at the 1%, 5%, and 10% levels (two-tailed), respectively.

Benchmark Regression

Table 3 reports the test results of population differentiation index on house price differentiation index.

Column (1) and column (2) are the regression results estimated by the Feasible Generalized Least Squares (FGLS) method. The results of column (2) show that under the condition of controlling a series of related factors, the effect of population differentiation index on house price differentiation index is significantly positive at the level of 1%, and its influence coefficient is 0.023. Regression results show that the differentiation of urban population among urban groups will promote the further differentiation of housing prices. In column (3) and column (4), tool variables are used and 2SLS estimation method is used for regression. The results of column (4) show that the effect of population differentiation index on house price differentiation index is also significantly positive at the statistical level of 1%, with an impact coefficient of 0.026, which indicates that urban population differentiation will indeed aggravate house price differentiation. This result is similar to that of column (2) .

Mechanism of Leverage Ratio Growth Rate in Residential Sector Affecting Housing Prices Differentiation Through Population Differentiation

Table 4 reports the measurement results after including the interaction term pop_pdi*Leverage_growth between the population differentiation index and the leverage ratio growth rate of the household sector. Using OLS, FGLS, and 2SLS three estimation methods to estimate the model, the results show that no matter which estimation method is adopted, the coefficient of the interaction between population differentiation index and resident sector leverage ratio growth rate is significantly positive. In column (6), the coefficient of the interaction term is 0.005, which is significantly positive at 1% statistical level. In column (8), the coefficient of the interaction term is 0.005, which is significantly positive at 1% statistical level. In column (9), the coefficient of the interaction term is 0.004, which is significantly positive at 1% statistical level. It shows that the growth rate of resident sector leverage ratio will promote the effect of population differentiation on housing price differentiation, that is, the faster the growth rate of resident sector leverage ratio, the greater the promotion effect of urban population differentiation on housing price differentiation. In reality, the rapid leverage stage of residents generally indicates that their investment demand is strong, the market is hot, and the capital demand is large. More people move to big cities, seeking investment and development opportunities. Population growth will provide a foundation for the real estate market, which in turn will give residents the confidence to leverage. That is to say, the growth of residents’ leverage ratio will further aggravate the differentiation of urban housing prices by aggravating the population differentiation of large and small cities. This is consistent with the analysis of the above part of this paper, which further verifies the inference of the theoretical model.

Regression Results With Interaction Terms between Leverage Ratio Growth in Residential Sector and Population Differentiation Index.

Note. The values in parentheses represent t-values or z-values adjusted for heteroscedasticity.

***, **, * Denote statistical significance at the 1%, 5%, and 10% levels (two-tailed), respectively.

In order to further verify the reliability of the above conclusions, this paper uses the domestic credit growth rate as the proxy variable of the growth rate of leverage ratio in the residential sector to test the robustness, and re-estimates the above interactive models by OLS, FGLS and 2SLS. The results in Table 5 show that no matter which estimation method is adopted, the coefficient of the interaction term between credit growth rate and population differentiation index is significantly positive, which further proves that credit growth will promote the effect of urban population differentiation on housing price differentiation, that is, the faster the credit growth rate is, the greater the promotion effect of urban population differentiation on housing price differentiation, and this promotion effect is relatively stable.

Regression Results With Interaction Terms Between Domestic Credit Growth and Population Differentiation Index.

Note. The values in parentheses represent t-values or z-values adjusted for heteroscedasticity.

***, **, * Denote statistical significance at the 1%, 5%, and 10% levels (two-tailed), respectively.

Mechanism of Deposit Growth Rate Affecting Housing Price Differentiation Through Population Differentiation

Table 6 reports the measurement results after including the interactive term pop_pdi*Deposit_growth of population differentiation index and deposit growth rate. Using OLS, FGLS, and 2SLS three estimation methods to estimate the model, the results show that no matter which estimation method is adopted, the coefficient of the interaction between the resident income differentiation index and the deposit growth rate is significantly positive. In column (16), the coefficient of the interaction is 0.086, significantly positive at the 1% statistical level, in column (18), the coefficient of the interaction is 0.086, significantly positive at the 1% statistical level, and in column (19), the coefficient of the interaction is 0.041, significantly positive at the 1% statistical level. It shows that the resident deposit growth rate will promote the effect of urban population differentiation on the house price differentiation, that is, the faster the resident deposit growth rate, the greater the promotion of urban population differentiation on the house price differentiation, and this promotion is more stable. In reality, to a certain extent, the increase in the growth rate of savings rate indicates that the market is relatively stable. Compared with investing in real estate, residents are more willing to turn wealth into cash and deposit it in banks, and may also make preventive savings for future life. When most residents’ enthusiasm for investing in real estate declines, it may be because the housing price differentiation between cities has reached a certain degree, and the housing price that their purchasing power can afford is too different from that in the core areas of big cities.

Regression Results With Interaction Terms between Deposit Growth and Population Differentiation Index.

Note. The values in parentheses represent t-values or z-values adjusted for heteroscedasticity.

***, **, * Denote statistical significance at the 1%, 5%, and 10% levels (two-tailed), respectively.

Mechanism of Urbanization Rate Growth Affecting Housing Price Differentiation Through Population Differentiation

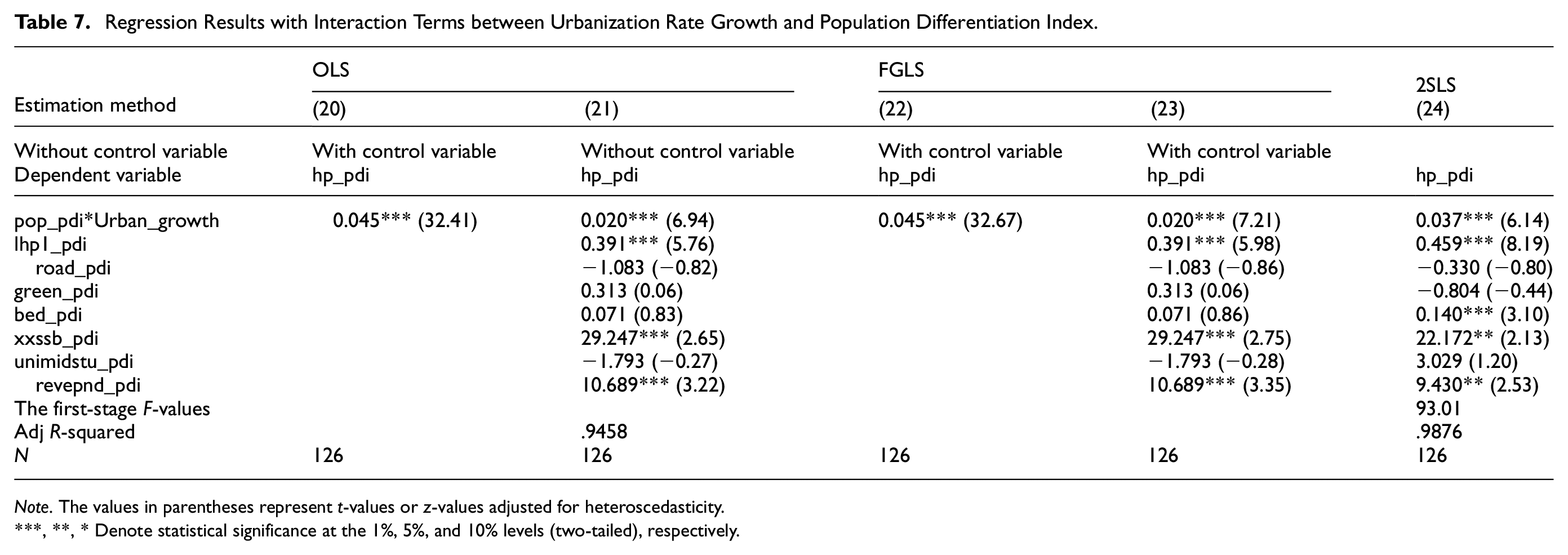

Table 7 reports the measurement results after including the interactive term pop_pdi*Urban_growth of population differentiation index and urbanization rate growth rate. Using OLS, FGLS, and 2SLS three estimation methods to estimate the model, the results show that no matter which estimation method is used, the coefficient of the interaction between residents’ income differentiation index and urbanization rate growth rate is significantly positive. In column (21), the coefficient of the interaction term is 0.020, which is significantly positive at 1% statistical level. In column (23), the coefficient of the interaction term is 0.020, which is significantly positive at 1% statistical level. In column (24), the coefficient of the interaction term is 0.037, which is significantly positive at 1% statistical level. It shows that urbanization rate growth rate will promote the effect of urban population differentiation on housing price differentiation, that is, the faster the growth rate of urbanization rate, the greater the promotion of urban population differentiation on housing price differentiation, and this promotion is more stable. In reality, in the stage of rapid urbanization development, the population differentiation will be further aggravated since the differences in survival and development opportunities between cities. Providing better employment opportunities and development opportunities in high-order cities will attract more population inflow and provide stronger support for high housing prices in cities, while the population in low-order cities will flow out, which will eventually further lead to housing price differentiation. This is consistent with the above analysis. In the process of urbanization, there is a differentiation of housing prices in different cities.

Regression Results with Interaction Terms between Urbanization Rate Growth and Population Differentiation Index.

Note. The values in parentheses represent t-values or z-values adjusted for heteroscedasticity.

***, **, * Denote statistical significance at the 1%, 5%, and 10% levels (two-tailed), respectively.

Therefore, through the above empirical research, we verify the influence of population on urban housing price differentiation, and at the same time, through the introduction of cross terms, we verify that leverage ratio growth rate, deposit growth rate and national average urbanization rate growth rate can aggravate housing price differentiation through their influence on urban population differentiation, thus completely presenting the macro indicators of household financial behavior of residents’ departments through the transmission mechanism that affects housing price differentiation by acting on urban population.

Conclusion and Policy Implications

In a multi-city economic system, the dynamics and fluctuations of housing prices across cities result from the intricate interplay of numerous factors. The demographic disparity between large cities and their smaller counterparts, stemming from initial conditions, sets the stage for a mutually reinforcing cycle of change in residents’ income levels, infrastructure development, public services, industrial scale, and population size. Consequently, the housing demand in larger cities outpaces that of smaller ones. Simultaneously, administrative land restriction policies curtail land supply, per capita, in larger cities relative to smaller ones, thereby exacerbating the housing price disparity between the two. Investing money in real estate for investment and value preservation and appreciation purposes is an important investment method for residential households. Household deposit and borrowing behaviors evolve in tandem with market and urban development, reflecting households’ assessments of future economic prospects and market dynamics. Such financial conduct profoundly influences housing price differentiation across cities. Moreover, varying stages of urban development manifest in differences in land quality, market accessibility, competitive landscape, and policy support, all of which contribute to disparities in housing prices among cities. Thus, macro indicators of household financial behavior within residential sectors-facilitated through urban population transmission-amplify relative housing demand in larger cities. Consequently, both the level and growth rate of housing prices in large cities surpass those in small and medium-sized counterparts, further accentuating housing price differentiation among cities. Real estate, essentially a financial instrument, underscores residents’ choices across cities for hedging and investment purposes, thereby widening disparities in housing prices among cities.

To adhere to the principles of urban development and mitigate the excessive escalation and disparity of housing prices among cities, governmental intervention is imperative. Firstly, there is a need to recalibrate land policies and reform the land system. This entails considering adjustments to the strategic framework of urban development throughout different stages of urbanization. Specifically, policies should relax population size constraints in major cities and ease land restrictions within urban agglomerations, thereby enhancing the flexibility of housing supply in larger cities. Conversely, in smaller and medium-sized cities grappling with population outflow constraints or housing inventory surpluses, a reduction in land supply is warranted to temper supply elasticity. Moreover, establishing a market-oriented “land-person matching” trading system and urban construction land quotas is essential to align housing supply and demand dynamics. Secondly, income policies require adjustment and reform to promote labor mobility by fostering favorable employment opportunities. Caution must be exercised against the use of short-term, excessively loose monetary policies to stimulate real estate expansion, thereby averting unsustainable growth trajectories. It is imperative to maintain a neutral monetary policy stance vis-à-vis the housing market, even amidst overall monetary laxity, by adopting a nuanced industry-specific monetary policy and reinforcing financial oversight to curtail the undue influx of funds into the housing sector through loan and interest rate differentials. Thirdly, expediting the establishment of a “one city, one policy” long-term mechanism is crucial. This approach aims to mitigate disparities in real estate loans, interest rates across urban areas, and housing supply-demand imbalances, thus tempering excessive housing price differentials among cities. Furthermore, empowering local governments with primary responsibility for real estate and housing security mandates the formulation of tailored laws and policies on real estate regulation, fiscal revenues, and housing provisions, contingent upon local contextual nuances. Lastly, from a macroeconomic standpoint, vigilant monitoring and adjustments to residential sector deposit and loan dynamics are imperative to quell irrational investments and steer the market toward sustained growth. By fostering innovation in emerging economic domains, stable investment avenues can be cultivated for residents, thereby promoting prudent consumption habits and rational asset management practices. Prudent deleveraging strategies must be adopted to mitigate systemic risks and ensure the long-term stability of the market.

This paper derives empirical data for the PDI based on the Specific Direction Spatial Differentiation Index method for urban grouping, and we reached corresponding conclusions through empirical testing. Further research on this issue could explore other methodologies, which may yield more nuanced and valuable conclusions. Urban housing price differentiation is an ongoing process influenced by many factors, and we have only analyzed it from one perspective.

Footnotes

Ethical Considerations

Not Applicable. This manuscript is about economic research. It is not related to bioethics problems.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.