Abstract

This study investigates the determinants of earning quality by using a sample of 354 non-financial listed firms on the Ho Chi Minh Stock Exchange (HOSE) from 2010 to 2023. We contribute to the existing literature by emphasizing the role of accounting conservatism and CEO characteristics on earnings quality. The empirical evidence indicates that accounting conservatism positively impacts earnings quality. Conservative accounting practices may minimize the manipulative behavior of management, thereby increasing trust in the accuracy and reliability of financial information. Additionally, we found that CEO attributes affect earnings quality in different ways: while the CEO’s duality, gender, income, and tenure have a significant negative relationship with earnings quality, the CEO’s age and ownership have contrasting results. Furthermore, we also discovered that other factors such as a firm’s size, leverage, ROA, loss, and sales growth are positively associated with earnings quality. Our findings are useful references to provide executives, financial managers, and investors with insights into factors that improve firm’s earnings quality.

Introduction

Net income, sometimes known as “earnings,” is one of the most essential pieces of financial information that firms publish. Earnings are the key statistic used to value firms, thus, earnings surprises have a significant impact on stock prices. Net income may not fully reflect a company’s financial performance. If a company reports high net income but negative operational cash flow, it may not be as financially stable as it looks. Breaking out a company’s cash sources is crucial as income statements sometimes lack essential facts. Simply said, if a firm declares a positive net income but low-quality earnings, acquiring the company may be a riskier investment than the financial statements suggest. Understanding the “earnings quality” concept is very important in this era.

A significant body of research has focused on the understanding of earnings quality and its determinants. A substantial body of research has been devoted to examining the nature of earnings quality and identifying its determinants because a company’s earnings quality is a key measure of its long-term health. It also gives analysts greater confidence that the metrics they’re looking at accurately indicate present and future performance. Assessing earnings quality is critical for success in a variety of financial services sectors. Earning quality has an impact on future profit and cash flow forecasts; low earnings quality frequently results in lower future earnings and cash flows, in contrast to current earnings. This will affect debt capacity estimates and the firm’s worth. Furthermore, earning quality assesses how trustworthy a company’s profits are in predicting present and future success. High earnings quality typically indicates that the earnings are free of manipulation by management and are a reliable predictor of future results. Improving earnings quality necessitates that firms disclose more comprehensive and higher-quality information to ensure that market participants are sufficiently informed when making investment and credit decisions. The authors noted that higher earnings quality increases the likelihood of mitigating information asymmetry between firms and their creditors (Dang et al., 2021; Dang, Nguyen, et al., 2020; Dang, Pham, et al., 2020; Van Khanh & Hung, 2020).

Although the concept of earnings quality has been extensively studied in developed markets, most existing models are based on the International Financial Reporting Standards (IFRS), which prioritize faithful representation and the matching principles. In contrast, Vietnam’s Accounting Standards (VAS) emphasize formalism, creating a significant gap between accounting figures and the real financial situation. While Vietnam has initiated the transition to IFRS, the process is slow, fragmented, lacks synchronization, and has yet to yield substantial practical improvements. Moreover, Vietnam’s corporate ownership structure is highly concentrated, mostly state-owned and family-owned corporations. Dominant shareholders often exercise absolute control, while boards of directors lack independence. This environment fosters an ideal setting for earnings management practices aimed at serving the interests of controlling groups in several ways, such as prematurely recognizing revenue, inflating “paper profits,” and concealing losses through internal transactions and fabricated cash flows. Understanding these dynamics of the Vietnamese context provides valuable contributions to the literature on corporate governance, particularly in the context of emerging economies where unique institutional and ownership structures often diverge from those in developed markets.

Prior literature has documented that earning quality is impacted by firms’ fundamentals and characteristics, including capital structure, investment opportunities, and information asymmetries (Wahyuningtyas & Rahman, 2023), firm’s size (Etim et al., 2023; Rahersya & Daito, 2022), pre-managed earnings, efficiency, and liquidity (Etim et al., 2023; Valdiansyah & Murwaningsari, 2022), audit committee (Pujiati & Nita, 2022), auditor size, and audit tenure (Sumiadji et al., 2019), leverage, managerial ownership (Etim et al., 2023), interest rates, foreign exchange rates, and profitability (Wibisono & Andesto, 2023) business model, industry, and macroeconomic conditions (Nakashima, 2019). Nevertheless, studies linking CEO’s characteristics and earnings quality are scarce. Given that no single study has comprehensively examined how earning quality can be affected by accounting conservatism, this work addresses and fills this gap. Our contribution, relative to existing work, is threefold:

First, earning quality is considered a more crucial measure of evaluating how worth an investment in a firm is than accrual quality. It provides a more comprehensive look at long-term profitable ability without interference and uncertain elements, while accrual quality is narrower and only partially contributes to calculating earnings quality by reflecting the difference between accounting profit and cash flow. We believe that earning quality responsibly reveals sustainability and certainty of business results due to its reliable resources. Earnings quality is considered an unobservable variable. Whereas previous academic materials relating to it emphasize accrual quality, which is associated with earnings management techniques as almost the only crucial highlight, we employed the multifaceted concept of earnings quality, including a combination of seven proxies for earnings quality include accrual quality, timeliness of profitability, predictability, earnings smoothing, persistence, value relevance, and conservatism of earnings (Etim et al., 2023; Pujiati & Nita, 2022; Rahersya & Daito, 2022; Valdiansyah & Murwaningsari, 2022). Our finding contributes to the literature in more specific knowledge regarding earning quality contributed elements.

Second, the adoption of the IFRS international standard framework is crucially important in the context of global economic integration and trade liberalization. As a result, Vietnamese enterprises need to undergo a strong transformation to meet the demanding requirements of global investors. A key step in this transformation is the standardized preparation and presentation of financial statements, improving transparency. This is where the accounting conservatism becomes indispensable, as it contributes to the improvement of a company’s information environment (Kim & Zhang, 2016), reduces the possibility of sharp drops in stock prices (Khurana & Wang, 2019), and enhances the effectiveness of investments (Lara et al., 2016). Applying the principle of accounting conservatism in business will reduce earnings manipulation behavior, prevent manager misconduct, and eliminate future uncertainty. These benefits motivate us to investigate the nexus between accounting conservatism and earnings quality, which provides clearer insights for investors and stakeholders, and fosters greater stability and confidence in both domestic and international financial markets.

Third, CEOs play a crucial role in shaping the firm’s accounting and disclosure practices through their personal and professional characteristics, which directly affect earnings quality. According to upper echelons theory, the attributes of a CEO influence how they perceive and process information, ultimately affecting strategic decisions and financial reporting practices. Meanwhile, agency theory states that under conditions of information asymmetry, CEOs may prioritize their interests by manipulating earnings to achieve personal goals, such as maximizing bonuses, ensuring job security, or enhancing stock prices. The previous studies have examined specific CEO characteristics like age (Le et al., 2020), tenure (Ali & Zhang, 2015; Saito, 2019), duality (Hemdan, Hasnan, & Rehman, 2021), reputation (Francis et al., 2008) but findings have remained mixed. Moreover, the number of studies comprehensively clarifying the relationship between CEO characteristics and earnings quality remains limited (Arif et al., 2023; Belot & Serve, 2018; Nurmayanti & Rakhman, 2017; Shiah-Hou, 2021). This research gap motivates us to further investigate the connection between CEO characteristics and earnings quality.

The structure of this study is arranged as follows. After this introduction, section “Literature review and Hypotheses development” provides a literature review and the research hypotheses. Section “Data and research methodology” describes the data, variables, and methodology. Then, findings and discussions are displayed in section “Empirical Results,” and “Conclusion” section concludes.

Literature Review and Hypotheses Development

Theoretical Framework

Agency Theory

According to agency theory, developed by Meckling and Jensen (1976), it emphasizes the relationship between managers (agents) and shareholders (principals). Managers might prioritize their interests, including maintaining job stability or bonuses, over maximizing shareholder value. This can lead to earnings management, where managers manipulate accounting practices to present a distorted picture of the firm’s financial performance. Such actions can compromise earning quality, making it challenging for investors to evaluate the company’s actual financial health. Accounting conservatism, the tendency to understate assets and overstate liabilities, can be linked to earnings quality through agency theory. When managers are less conservative, they have more discretion in recognizing revenues and deferring expenses, potentially leading to earnings management and a decrease in earnings quality. Conversely, greater conservatism can mitigate agency problems by lowering information asymmetry between supervisors and investors. To mitigate these agency problems, effective corporate governance mechanisms, such as strong boards of directors and independent auditors, can help align managerial incentives with shareholder interests and improve the reliability of financial reporting.

Upper Echelons Theory

The Upper Echelons Theory, proposed by Hambrick and Mason (1984), investigates how top management’s demographics, experiences, and cognitive biases influence organizational strategy and operations. Over time, these top management characteristics will be reflected in the organization’s strategic decisions and performance. For instance, a CEO with strong ethical values and a long-term perspective is more likely to prioritize accuracy and transparency in financial reporting, thereby enhancing the quality of earnings. Conversely, CEOs driven by short-term benefits or personal interests might participate in earnings management to enhance short-term financial results, leading to a decline in earnings quality. This theory emphasizes the critical role of top management in shaping organizational behavior and the importance of effective leadership to ensure financial reporting accuracy and faith in investor confidence. Therefore, to gain deeper insights into an organization’s decisions and operations, it is essential to analyze the cognitive frameworks of top executives through their demographic characteristics.

Signaling Theory

Signaling theory was proposed by Akerlof (1978) and Spence (1973). Signaling theory is based on information asymmetry, indicating that to achieve a particular objective in circumstances where information asymmetry exists, the party holding the information must communicate with the party in need of the information through signals. Based on this theory, management provides investors with a signal in the form of earnings quality. Managers are operators, if they deliberately conceal information, it can affect the decisions of shareholders, thereby causing disadvantages for shareholders. Enterprises that do not send signals or send incorrect signals to the outside can affect decisions and cause losses to related parties. Following signaling theory, larger companies are thought to operate more steadily and have more potential for future financial success. This impression gives investors a good indication that the earnings are of higher quality, which in turn draws more attention from stakeholders (Kusumawardhani & Setyorini, 2024).

Hypothesis Development

The Impact of Accounting Conservatism on the Earnings Quality

A fundamental concept known as accounting conservatism highlights the importance of exercising caution in financial reporting to avoid overvalued assets and undervalued liabilities. It is seen as a mechanism to decrease agency problems and managers’ incentives to overstate earnings. This decrease in agency issues enhances financial reports and earnings quality. Previous studies report mixed results about conservatism’s effect on earnings quality. Some report that accounting conservatism has a positive impact on earnings quality.

For instance, through an examination of a sample comprising 90 manufacturing enterprises in Indonesia from 2016 to 2019, Noor et al. (2021) established a positive correlation between accounting conservatism and the quality of earnings. The authors state that a firm applying the accounting conservatism method can help stakeholders avoid conflicts of interest, and the more conservative a company is in its annual report, the better the quality of reported profits information is. Similarly, an investigation undertaken by Putra and Subowo (2016) involving 38 consumer goods enterprises listed on the Indonesia Stock Exchange (IDX) during the timeframe from 2011 to 2014, revealed that a positive correlation exists between accounting conservatism and quality of earnings. This relationship may clarify the importance of conservatism in accounting in limiting the opportunistic behavior of management, leading to more accurate and reliable financial reporting, which ultimately benefits consumers of corporate financial reports. Furthermore, an additional study identified a positive correlation while examining 381 companies registered on the IDX during the interval from 2013 to 2015 (Yasa et al., 2019), indicating that the application of accounting conservatism yields financial reports characterized by management earnings quality, as it may inhibit the opportunistic behaviors of management. Consequently, we hypothesize that:

Hypothesis H1a: Accounting conservatism has a positive correlation with earnings quality.

In contrast, few studies show a negative correlation between conservatism and the quality of earnings. Pratiwi and Pralita (2021) using a sample of 158 nonfinancial companies listed on the Indonesia Stock Exchange (IDX) with a research period from 2016 to 2018, found that accounting conservatism has a detrimental impact on the quality of earnings. The authors suggested that if accrual is negative, then the earnings are classified as conservative, which is caused by lower earnings than cash flows obtained by the company in a given period. Therefore, the second hypothesis is formulated as follows.

Hypothesis H1b: Accounting conservatism has a negative correlation with earnings quality.

The Impact of CEO Characteristics on the Earnings Quality

CEO Age

CEO age has a multifaceted impact on earnings quality through the CEO’s approach to risk, decision-making, and management style, affecting the quality and reliability of a company’s reported earnings. Using a sample of 490 real estate enterprises from 2007 to 2016, Le et al. (2020) reported that elderly CEOs are less involved in earnings management than younger CEOs and tend to be more conservative, increasing earnings quality as CEOs get older. Similarly, Li et al. (2024) evaluate accounting and stock data for U.S.-listed corporations from 2010 to 2022, sourced from the CRSP, Compustat, and BoardEx databases, producing 70,939 firm-to-year observations. They observed that elder CEOs may prioritize transparency and financial stability in their leadership style. Consequently, they may fancy creating and using high-quality financial reports throughout their firm, resulting in higher earnings quality for firms led by those older. On the other hand, Altarawneh et al. (2022) used a data set of 1,957 firm-years of Malaysian listed firms from 2012 to 2016 and proposed the main regression results that CEO age is associated with earnings management, but generates no impact on earnings quality.

Hypothesis H2: CEO age is positively and significantly associated with a firm’s reported earnings quality.

CEO Gender

The CEO’s gender impact on earnings quality is an intricate issue that has gradually become a noticeable topic in corporate governance and finance research. There are many controversial issues regarding this relationship. Zalata et al. (2022) analyzed a large sample of US corporations from 1992 to 2014, demonstrating that female CEOs generate higher earnings quality than their male counterparts. Via evaluating 1,957 Bursa Malaysia-listed firm-year details from 2012 to 2016, Altarawneh et al. (2022) also discovered that companies led by women have higher earnings quality than those led by men. According to this study, female CEOs exhibit greater diligence in enhancing strategic decision-making and are less prone to earnings manipulation. Similarly, Wang et al. (2022) using the sample of Chinese listed companies’ data between 2007 and 2018, strengthened this nexus. They found the same explanation with Zalata et al. (2022). Women in business leadership roles reach higher earnings than men because they are more risk-averse and more willing to obey ethical standards. Okika et al. (2024) analyzed the annual reports of ten consumer goods corporations from 2013 to 2022, listed on the Nigerian Stock Exchange. The study revealed that female CEOs lead to greater financial reporting quality in the consumer goods business because they engage in less earnings manipulation and produce higher-quality financial reports. El-Dyasty and Elamer (2023) used the sample of 1,686 firm-year data registered on the Egyptian Stock Exchange from 2011 to 2020, we found similar findings. They demonstrated that high earnings quality is produced by female directors, who are strongly correlated with the quality of financial reporting. This perspective relied on the fact that executive female directors are less likely to engage in income-reducing earnings management tactics.

Hypothesis H3: There is a significant positive relationship between female CEOs and earnings quality.

CEO Duality

CEO duality concerns the dual position of the CEO, in which one person holds both the position of the chief executive officer (CEO) and the Chairman of the Board in the company, which leads to power and managerial discretion. This structure may lead to potential conflicts of interest, as the individual overseeing management is also responsible for monitoring it, which can result in less rigorous oversight and increased opportunities for financial fraud (Duru et al., 2016; Krause et al., 2014). The lack of separation between certain roles within the organization raises concerns about accountability and transparency, potentially hindering crucial checks and balances. This can lead investors to perceive higher financial risk, decrease confidence, increase the cost of capital, and negatively impact the company’s market valuation and long-term sustainability. Stakeholders may demand more assurance regarding the reliability of reported earnings. In the literature, the study reported that the relationship between CEO duality and earnings quality is scarce. Alves (2023); Hemdan, Hasnan, & Ur Rehman (2021); Shiah-Hou (2021) provided empirical evidence that is negatively and significantly associated with a firm’s reported earnings quality. Based on a sample of Egyptian firms from 2008 to 2019, Hemdan, Hasnan, & Rehman (2021) have found that CEO duality significantly and negatively affects the quality of earnings. The authors state that a CEO who plays two roles has more influence over the company’s decisions while also having fewer restrictions on decision-making and more opportunities to manipulate company earnings quality. Likewise, we found a negative correlation in the research of Alves (2023), which used a sample of non-financial publicly listed companies in Portugal from 2002 to 2016. The researchers imply that conflicts of interest and a lack of accountability may result from CEO duality, ultimately compromising the accuracy of financial reporting. This inverse relationship is highlighted in Shiah-Hou (2021), the author argues that CEO duality may undermine governance monitoring systems as the CEO’s dual role could allow them to bypass or influence governance procedures meant to guarantee financial reporting’s accuracy and transparency.

Hypothesis H4: CEO duality is negatively and significantly associated with a firm’s reported earnings quality.

CEO Tenure

As evidenced by Egyptian-listed firms from 2008 to 2019, the CEO’s tenure was proven to influence earnings quality with a downward trend due to extended time in office, enabling CEOs to build closer relationships with stakeholders, reducing board supervision, and increasing the likelihood of earnings manipulation (Hemdan, Hasnan, & Ur Rehman, 2021). Using panel data of 1,395 firm-year observations from Bangladesh’s listed non-financial enterprises between 2010 and 2019, Arif et al. (2023) discovered similar findings that CEO tenure negatively impacts earnings quality. As long tenures increase control over operational strategies, it leads to greater earnings manipulation. In addition, the research by Setyawan and Anggraita (2017), found that CEO tenure has an unfavorable effect on earnings quality through their methods and experience in earnings management. The research reveals that newly appointed CEOs tend to employ both real and accruals earnings management strategies to artificially inflate their company’s profits during the initial phase of their tenure.

In contrast, some studies reported that longer tenure may decrease earnings management due to several reasons. Hsieh et al (2018) investigated 4,791 Taiwanese-listed firms from 2006 to 2010. Scholars found that top management members (like CEOs) with greater knowledge and longer average tenure have better performance, and are more aware of the litigation risks of earnings manipulation, making them less likely to engage in earnings management, which dramatically improves earnings quality. Nurmayanti and Rakhman (2017) utilized a sample of listed firms on the Indonesia Stock Exchange from 2012 to 2014 to investigate the relationship between CEO tenure and earnings quality, the authors confirmed that increased CEO tenure correlates with improved earnings quality as CEOs gain experience and understanding of the firm’s operations after a long tenure in the CEO position.

Hypothesis H5a: CEOs with long tenures will improve earnings quality.

Hypothesis H5b: CEOs with long tenures will decrease earnings quality.

CEO Ownership

CEO ownership, which represents the proportion of a company’s shares held by its leaders and can affect decision-making and business performance, is a crucial component of corporate governance. Using the sample of 110 non-financial joint-stock enterprises in the Saudi Stock Exchange between 2019 and 2021, Aldoseri and Hussein (2024) found a positive correlation between CEO ownership and earnings quality because CEO has a stake in the company, they are more likely to report higher quality earnings, as they are directly affected by the company’s performance. Petrou and Procopiou (2016) investigate the connection between CEO shareholdings and earnings manipulation using a sample of 16,873 observations from 2,257 publicly traded U.S. The study concludes that higher CEO shareholdings are associated with a decrease in earnings manipulation, leading to higher earnings quality. This suggests that when CEOs have a significant financial stake in their companies, they are less inclined to participate in practices that might distort profitability, such as actions that could threaten their wealth and reputation. Similarly, Saleem Salem Alzoubi (2016) employs a variety of econometric tools, applying both extended and ordinary least squares to a sample of 62 businesses listed on the Amman Stock Exchange, to examine the link between firm ownership and earnings management using a sample of 62 Amman Stock Exchange-listed companies. The findings indicated that certain components of ownership structures, particularly managerial ownership, are effective as management monitors, resulting in lesser earnings management and greater financial reporting quality, resulting in superior earnings quality in firms with a higher ratio of CEO ownership.

Hypothesis H6: Increasing the CEO’s ownership leads to an improvement in the firm’s reported earnings quality.

CEO Income

Compensation is the payment that firm owners make to executives who manage the business. Salary, bonuses, restricted stock, stock options, and other long-term incentives make up the CEO’s compensation. Numerous studies have demonstrated a positive relationship between CEO’s income and earnings quality. According to Otuya et al. (2017), when using data from annual reports of manufacturing companies for the period 2012 to 2016, the authors found a negative and significant relationship between executive directors’ remuneration and earnings management. When the amount of compensation granted to executives is high, discretionary accruals are typically low, leading to reduced earnings manipulations, which, by extension, improves on quality of earnings. In line with these findings, Paiva et al. (2023) analyzed 33 companies listed on the Euronext Lisbon stock exchange between 2015 and 2019. Their results demonstrate that increased managerial compensation is associated with reduced earnings management. It suggests that executives who receive high compensation may be less likely to manipulate financial outcomes.

Hypothesis H7: The CEO’s income is positive and significantly affects on quality of earnings.

Data and Research Methodology

Data

To conduct our analysis, we collected data from 392 non-financial companies listed on the Ho Chi Minh Stock Exchange (HOSE) covering the period of 2010 to 2023. After excluding banks and other financial institutions, we were left with 354 companies (4,833 firm-year observations). We collected the public data from the audited financial statement and annual report. Financial firms are excluded from our sample due to their distinct capital structures and regulatory frameworks, which make their financial characteristics incomparable to those of non-financial firms. All data were “winsorized” at the 98% upper and 2% lower percentiles.

Variable Description

Dependent Variable

Earnings quality determines whether a company’s earnings give a reliable assessment of its current performance and are a good forecast of future performance. In this study, we apply two widest approaches to measure earnings quality are (Dechow et al., 1995) and (Dechow & Dichev, 2002) as follows:

According to Dechow et al. (1995), this approach uses the Equation’s discretionary accruals to determine earnings quality; the better the quality of earnings, the less discretionary accruals there are.

Equation (1):

Where:

✓ TAit is the total accruals for firm i firm i, at year t;

✓ Ait−1 is the asset for firm i, at year t–1;

✓ ΔREVit indicates the changes in revenues of the firm i, which is calculated by revenues in year t less revenues in year t–1;

✓ ΔARit is related to the changes in receivables for the firm i at year t, which is measured by receivables in year t less receivables at year t–1;

✓ PPEit is fixed assets of the firm i at year t;

✓ ε it is the residual error for firm i in year t.

The total accruals of firm i in year t are calculated using the following Equation 2. Therefore, the changes in current assets throughout year t are represented by ΔCA. Changes in the company’s cash flow are referred to as ΔCash. Additionally, changes in current liabilities are shown by ΔCL, while changes in short-term debt are indicated by ΔSTD.

Moreover, our research methodology employs a two-stage process to assess earnings quality, building on the approach of Dechow and Dichev (2002). In the first step, calculate residuals from the industry-year regressions of working capital accruals on current, past, and future cash flows as shown in Equation 3. The results indicate that the better the quality of earnings, the less discretionary accruals there are.

Equation (3):

Where: The operating cash flow for firm i in the previous year (t−1) is represented by CFOi,t−1. CFOit denotes the operating cash flow for the firm i, in year t, and its operating cash flow in the following year (t+1) is denoted by CFOit+1. As our two main measures for evaluating earning quality, we convert the residuals into absolute values and standard deviations in the second phase.

Independent Variable: Conservatism

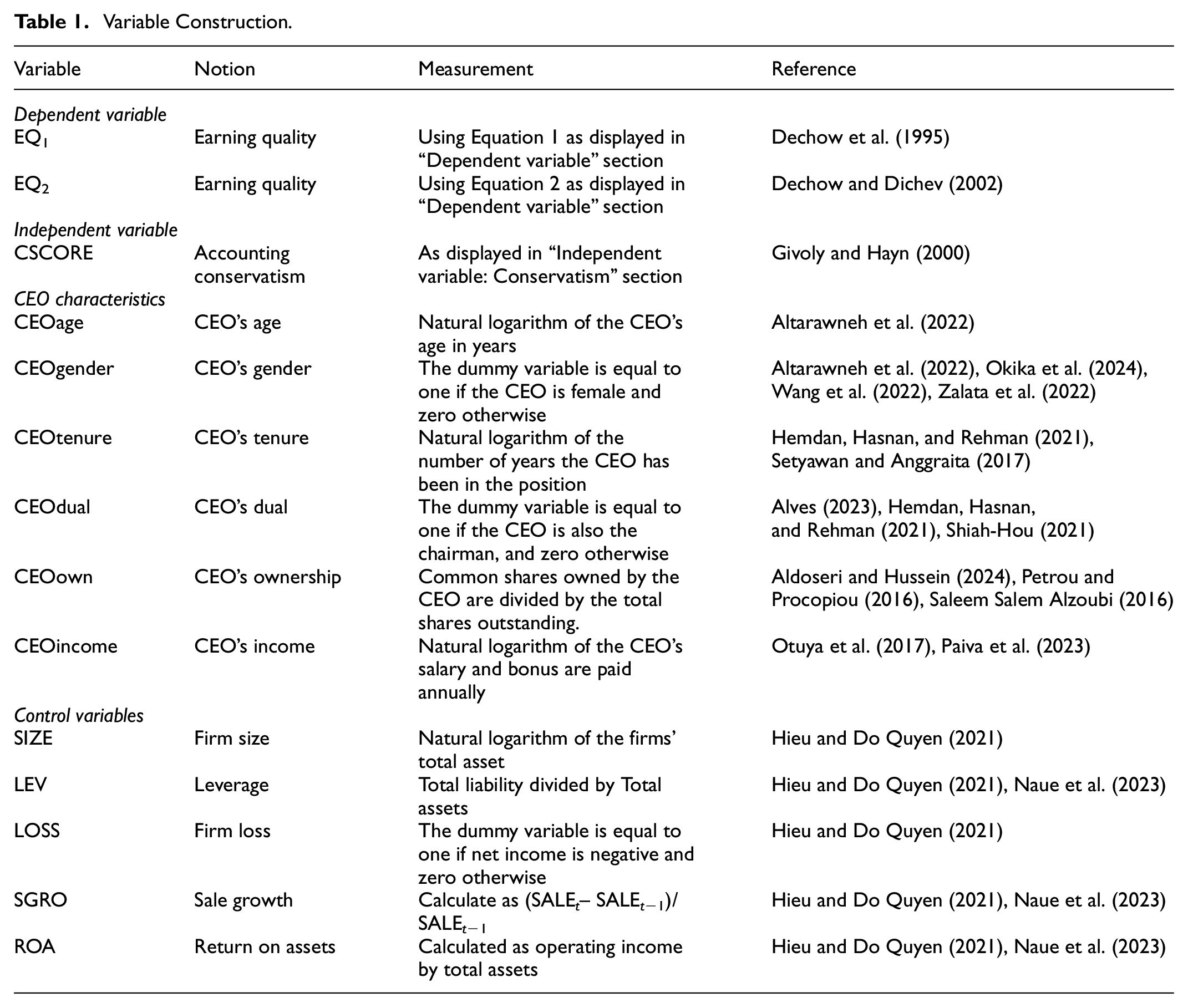

This study uses the (Givoly & Hayn, 2000) model as a proxy to estimate the degree of conservatism using the following formula (Table 1):

Variable Construction.

Where:

✓ CSCOREit is the level of conservatism for the company i at year t;

✓ TAi,t indicates total accruals for the company i at year t,

✓ Ai,t is the book value of assets.

Table 2 presents descriptive statistics for all firm-year observations in the sample. According to the findings, the mean of earnings management degree in terms of discretionary accruals based on Dechow et al. (1995) and Dechow and Dichev (2002) models are 0.058 and 0.033, respectively. The minimum value of accounting conservatism (CSCORE) is −0.180, and the maximum value is 0.113. The average value of firm size (SIZE) is 28.144. Regarding profitability measurement, the average return on assets (ROA) and sales growth (SGRO) are 6.2% and 10.6%, respectively. On average, around 4.8% of listed firms report annual losses (LOSS). The maximum level of debt of non-financial listed firms in Vietnam (LEV) is 89.7%, and the minimum level is 3.7%. In terms of governance characteristics, companies with CEOs holding dual roles and those led by female CEOs are reported to have approximately 21.8 % and 11.2%, respectively. In addition, the age distribution of CEOs ranges from 20 years to 80 years. The average CEO’s ownership percentage is approximately 7.61%, and CEO tenure ranges from 1 to 14 years (Table 3).

Descriptive Statistics.

Source. Authors’ calculation.

Pairwise Correlations.

Source. Authors’ calculation.

Empirical Model

To test our hypotheses, we estimate the regression model outlined below to investigate the relationship between CEO attributes, accounting conservatism, and the quality of earnings:

where:

✓ i and t represent firm and year, respectively;

✓ EQ refers to the two measures of earning quality described above, following Dechow et al. (1995) and Dechow and Dichev (2002);

✓ All other control variables are defined in Table 1;

✓ εit: error term.

There are three types of panel data models with different methods: Pooled Ordinary Least Squares (OLS), Fixed effect model (FEM), and Random effect model (REM). One drawback of Pooled OLS regression is that it assumes homogeneity for all variables and entities, which does not result in controlling for country-specific effects. This can lead to biased estimates due to correlations between independent variables and unobservable effects. Therefore, FEM and REM were used to handle differences between countries over time. The main difference between these two methods is how they handle fixed and random effects. The F-test and Hausman test then were applied to consider the suitability between the Pooled OLS, FEM, and REM. These tests indicate that the REM is more suitable. Breusch and Pagan’s LM test was used for testing random effects, and the Wald test was used to check whether our model is related to the Variance Change. If so, Feasible Generalized Least Squares (FGLS) will solve this problem. After conducting the Wald test to check for heteroskedasticity, the results indicated changes in variance. Feasible Generalized Least Squares (FGLS) were used to correct for heteroskedasticity as displayed in Table 4.

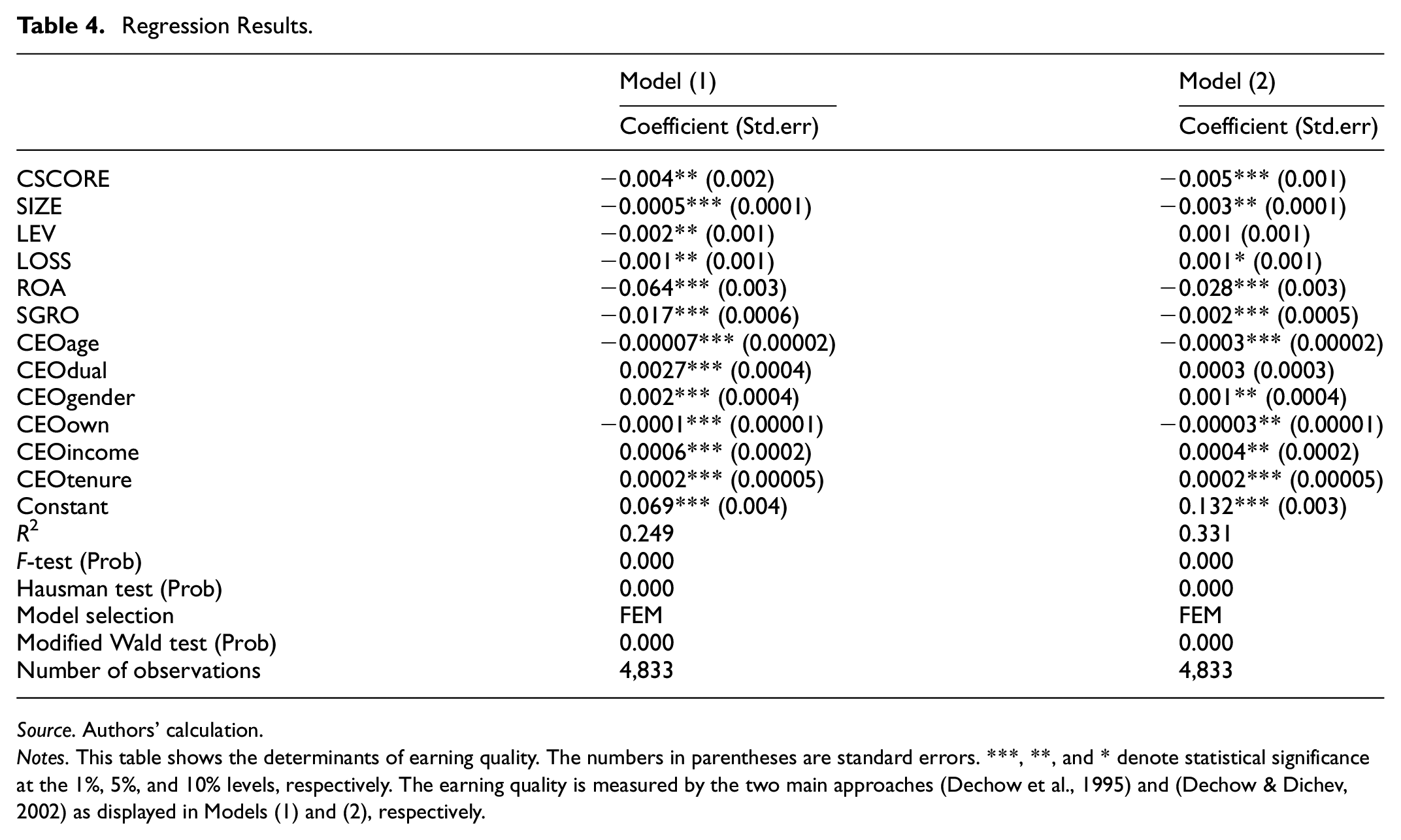

Regression Results.

Source. Authors’ calculation.

Notes. This table shows the determinants of earning quality. The numbers in parentheses are standard errors. ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively. The earning quality is measured by the two main approaches (Dechow et al., 1995) and (Dechow & Dichev, 2002) as displayed in Models (1) and (2), respectively.

Empirical Results

In this section, we present our main results in Table 4. In Table 4, the main dependent variable is total accruals measured by the two widest approaches Dechow et al. (1995) and Dechow and Dichev (2002). The better the quality of earnings, the less discretionary accruals there are. The regressions in Model (1) and (2) allow us to capture the impact of accounting conservatism, CEO characteristics, and the other determinants of earnings quality.

The estimated coefficient for accounting conservatism (CSCORE) is positive and statistically significant. This indicates that firms utilizing more conservative approaches may be associated with higher-quality reported outcomes. One possible explanation for this association is that conservative accounting techniques improve financial reporting credibility by minimizing the possibility of earnings overstatement, thereby enhancing trust in the accuracy and dependability of financial information. Previous studies support this finding as Noor et al. (2021), Putra and Subowo (2016), and Yasa et al. (2019). Therefore, our findings reject Hypothesis H1b and support Hypothesis H1a.

The impact of CEO age on earnings quality is positive and is significant at the level of 1%. This finding supports Hypothesis H2, which states that the correlation between CEO age and earnings quality is positive. Older CEOs can use their experience to make good financial decisions and promote openness, thereby enhancing earnings quality. Our finding is consistent with Huang et al. (2012) and Le et al. (2020).

There is a negative and significant association between CEO gender and earnings quality. This finding rejects hypothesis H3 and suggests that female CEOs are associated with lower earnings quality compared to male CEOs. This correlation can be attributed to increased regulatory scrutiny and pressure. Female CEOs usually face prejudice and mistrust, particularly in male-dominated fields, which constrain them from receiving financial assistance. As a result, they may distort earnings to preserve investor confidence. Our finding contradicts Altarawneh et al. (2022) and Zalata et al. (2022).

As can be seen in Table 4, the CEO duality coefficient is negative and statistically significant. This result suggests that when the CEO holds dual roles, earnings quality tends to decline. The reason is that gathered power may lower the independent monitor, increasing earnings manipulation and opportunistic financial reporting. Furthermore, CEOs playing dual roles may focus on personal interests rather than shareholder profitability, resulting in increased agency costs and significant information asymmetry. Therefore, this finding supports Hypothesis H4.

The estimated coefficient of CEOtenure is negative and statistically significant. This suggests that CEOs who have been in their roles for a long time are likely to decrease earning quality. This relationship can be explained by the fact that CEOs with longer tenure are more likely to develop closer personal relationships with stakeholders, reduce the objectivity, and have an increased likelihood of earnings manipulation to maintain their reputation and the firm’s performance, resulting in significantly improved earnings quality. This finding provides empirical evidence to support Hypothesis H5b and reject Hypothesis H5a. Our findings are in line with Arif et al. (2023) and Setyawan and Anggraita (2017).

The CEO’s ownership (CEOown) is found to have a positive effect on earnings quality. This indicates that CEOs with significant shareholdings have a greater alignment of interests with shareholders, decreasing agency conflicts. Higher ownership makes them focus more on the firm’s long-term success, encouraging transparency in financial reporting. Our findings support Hypothesis H6 and are in line with studies of Aldoseri and Hussein (2024), Nguyen et al. (2021), Petrou and Procopiou (2016), and Saleem Salem Alzoubi (2016).

Our results show that CEO income has negatively affected earnings quality at a 1% significance level. Higher CEO income may incentivize CEOs to prioritize short-term financial gains, which can reduce the quality of reported earnings. This behavior may result in riskier decision-making, weaker internal controls, and a diminished focus on sustainable profitability. This study has contrary results to the previous studies (Otuya et al., 2017; Paiva et al., 2023). We reject hypothesis H7.

Our findings indicate that firm size (SIZE) has a positive impact on earnings quality, which implies earnings quality increases with the widening of the firm’s size. This finding is supported by Purnamasari and Fachrurrozie (2020) who discovered that larger firms tend to have higher financial reporting transparency than smaller ones. The reason is that as a company grows in size, it tends to have better financial stability and continuity, which reduces the likelihood of engaging in financial statement manipulation. As a result, the financial reporting quality of large firms tends to improve.

Positive impacts are also found for leverage (LEV) on earnings quality, indicating that companies with high leverage tend to have better earnings quality. This finding is consistent with previous research by Lestari and Khafid (2021) and Naue et al. (2023) which indicates that when firms have significant debt, creditors impose stricter oversight to protect their interests. Tighter monitoring decreases the possibility of management manipulating earnings, resulting in more dependable and transparent financial reporting, improving earnings quality.

The figures illustrate a positive and reasonable correlation between loss and earnings quality, with a significant level of 5%. Losses can reflect a company’s honesty when they are transparently reported rather than hidden through earnings manipulation. Through this, the company provides a clearer picture of its real performance, reducing the risk of hidden liabilities and virtual profits, thereby enhancing earnings quality. Our findings conflict with the argument of Hieu and Do Quyen (2021) and Wang et al. (2022).

Return on assets (ROA) is an index of a firm’s profitability that shows how efficiently it utilizes its assets to generate profit. In this study, ROA is regarded as the control variable. At the 1% significance level, the regression result indicates a positive correlation between ROA and earnings quality. Our finding aligns with Raoli (2013). Those who state that companies generating poor outcomes in recent years use more earnings management strategies to enhance future outcomes and avoid disappointments.

The impact of sales growth on the quality of earnings is positive and statistically significant at a 1% level. This relationship is attributed to the fact that companies with increased sales growth create higher revenues, reducing the need for earnings manipulation and improving financial transparency. Additionally, sustainable growth enables businesses to sustain steady profitability, resulting in high-quality earnings. This result aligns with Firnanti and Pirzada (2019) and Naue et al. (2023).

Conclusion

This study employs an empirical investigation into the determinants of earnings quality and how they influence the reliability of financial reporting, based on data from 354 non-financial firms listed on the Ho Chi Minh Stock Exchange (HOSE). Therein, the research emphasizes the role of accounting conservatism and CEO characteristics, including age, ownership, duality, income, tenure, and gender, in shaping the quality of earnings.

The regression results show a positive link between accounting conservatism and earnings quality, suggesting that conservative accounting practices increase the reliability and transparency of financial reporting, hence enhancing investor confidence and earnings quality. Moreover, the research highlights that CEO characteristics are crucial determinants of earnings quality, impacting it from diverse angles. These findings are strongly supported by Upper Echelon Theory and Agency Theory. Specifically, Upper Echelon Theory provides the foundation for understanding how all CEO characteristics are significantly correlated with earnings quality. We found that CEO age and ownership positively contribute to earnings quality, while female CEOs, CEO duality, income, and tenure have a detrimental effect. This aligns with Agency Theory, which proposes that CEOs’ self-interested behaviors can compromise the integrity of financial reporting. In addition, the examination also considers firm-specific factors such as size, leverage, financial loss, return on assets (ROA), and sales growth. All of these factors are proven to generate a positive effect on earnings quality, suggesting that firms with large scale and financial complexity may be better at maintaining high-quality earnings.

This study’s dataset only focuses on the companies listed on the Ho Chi Minh Stock Exchange (HOSE) significantly constrains the generalizability of its findings. The distinct institutional, regulatory, and ownership characteristics inherent to an emerging market like HOSE, such as prevalent state or family control, may not be reflective of other national or international contexts. Future research should expand the dataset to encompass a more diverse range of firms across both developed and other emerging markets, providing robust cross-country comparative analyses. Concurrently, future investigations ought to rigorously address potential endogeneity concerns and explore the moderating roles of specific corporate governance mechanisms and institutional environments in shaping the nexus between CEO characteristics and financial reporting quality.

Footnotes

Ethical Considerations

There are no human participants in this article.

Consent to Participate

Informed consent is not required.

Author Contributions

Thy Le-Bao: Conceptualization, Data curation, formal analysis, investigation, methodology, software, supervision, validation, writing—review & editing. Vy Nguyen-The-Hoang: Data collection, formal analysis, writing—original draft. Thao Tran-Thanh-Mai: Data collection, formal analysis, writing—original draft. Huyen Ho-Thi-My: Data collection, formal analysis, writing—original draft.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is supported by Ton Duc Thang University

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data is available from the corresponding author upon reasonable request.