Abstract

The purpose of this article is to investigate the relationship between audit quality, the role of institutional environments at the provincial level, and earnings management around listing events by using data from 189 newly-listed companies on the Hochiminh Stock Exchange. Audit quality was proxied by Big4, auditor tenure, and auditor industry specialization, while earnings management was quantified as current discretionary accruals. The findings indicated that there was no role for Big 4, auditor tenure, and auditor industry specialization in curbing earnings management, as indicated by the regression result of the full sample. Interestingly, the effect differed substantially across signs of earnings management. The regression results of different forms of earnings management showed a contrast and indicated that the auditor tenure can mitigate the activities of income-increasing activities in the positive model, the auditor tenure and auditor industry specialization can explain the incentives for managing earnings in the negative model. Moreover, this study found no evidence of the impact of provincial governance on earnings management in the full regression model. However, a negative effect of provincial governance on earnings management was found in the case of a motive for upward earnings management, while good governance tends to provide greater benefits to reduce the occurrence of negative earnings management. After controlling for dummy listing and interaction variables that may be related to audit quality and institutional environment, this relationship remains unchanged. Finally, The study’s findings make several contributions to the earnings management literature and are relevant for investors, policymakers, and firms.

Introduction

Earnings management is one of the interesting topics which has received a lot of attention from researchers. Scholars have identified settings such as initial public offerings (IPOs) and seasoned equity offerings (SEOs), in which firms have incentives to manipulate earnings. Before these events, the companies are required to provide information about the history of the company and financial status—called a prospectus, which is a legal document that can be publicly distributed by issuers before going public. However, this information is not sufficient to evaluate the length of the company’s development as well as the financial position of the company. Due to the high information asymmetry in equity issuance, firm insiders, typically managers, have better information than investors. This asymmetry creates an incentive for managers to engage in income-increasing management. The majority of accounting empirical researchers have tried to find evidence of earnings management surrounding corporate events in different markets. Authors such as Aharony et al. (1993), Teoh et al. (1998a, 1998b), Rangan (1998), Shivakumar (2000), DuCharme et al. (2004), Kao et al. (2009), Nuryaman (2013), and Mughal et al. (2021) argued that conflicts of interest between insiders and investors (agency conflict) existed as the largest factor motivating insiders to engage in earnings manipulation. In order to mitigate conflicts between managers and shareholders and reduce agency conflict, the shareholders can establish monitoring systems. The appointment of an external auditor is one of the main monitoring mechanisms to reduce the information asymmetry in firm’s financial statements (Piot, 2001); Piot and Janin (2007), and protect shareholders’ rights by providing reasonable assurance that the financial statements are free from material misstatement due to error or fraud (Watts & Zimmerman, 1990). Thus, “the degree to which financial statement users can rely on an audit opinion depends on the quality of the audit performed” (Christensen et al., 2016, p. 1649). With the importance of the external auditor’s role in detecting earnings management, the topic of audit quality and earnings management has received a great deal of attention from researchers. Nevertheless, there were infamous accounting scandals in recent decades such as Enron, WorldCom, and Waste Management, raising questions about the role of the external auditor as a deterrent regarding engagement in earnings management (Velury, 2003).

In addition, some studies have found a negative relationship between audit quality and earnings management around corporate events, whereas another group of studies has emerged questioning the existence of an association between audit quality and earnings management. The studies of audit quality and earnings management during corporate events indicate that while audit quality and earnings management around the issuance of shares (IPO, SEO) are well documented, there are very few research reported on audit quality and earnings management around new listing events. While the time lag between the issue date and the listing date is short generally ranging from 5 days to 70 days (Boubaker et al., 2017) in developed markets, the delay from the issue date to the listing date is enormous in some developing countries, such as Vietnam. In some countries, IPOs and listings are distinct processes with listing requirements being more stringent than IPO requirements (Allens, 2017), and the actual listing date takes place long after the issue date. Moreover, international scholars make a distinction among auditors in terms of the quality of their audits and the measurement of audit quality is much debated with little understood (Knechel, 2016). The first purpose of this study is to provide a better understanding of audit quality and to assess different aspects of audit quality and its effect on earnings management by focusing on a setting in which the delay from the issue date to the listing date is long and variable in practice.

While prior empirical studies around corporate events have mainly focused on the impact of traditional factors such as audit quality, company size, debt, and performance in developed countries on earnings management, a growing body of research has developed various external factors to examine their effect on earnings management. According to Hoskisson et al. (2000), the institutional theory, with a focus on emerging economies, emphasizes the influence of the systems surrounding firms to explain firm behavior. This approach indicates that different institutional environments lead to differences in managers’ incentives to manipulate earnings. Prior studies document that institutional factors such as the legal system, investor protection, and control of corruption can explain earnings discretion practices (González & García-Meca, 2014; Kimbro, 2002; Lourenço et al., 2020; Memis & Çetenak, 2012; Nnadi et al., 2015), but the studies have largely been able to attribute these differences in earnings management to cross-country variations. Unlike most other studies, this study is to further develop the understanding of perceptions related to earnings management’s manipulation and to assess whether these perceptions may be influenced by sub-national institutional environments in the home country.

In summary, the main objective of this study is to examine the effect of external factors including audit quality and institutional environments on earnings management. This study combines and extends areas of research as follows. First, studies on earnings management and the effect of audit quality on earnings management around listing events have provided conflicting results. Furthermore, previous research has mainly focused on IPO and SEO, while paying little attention to listing events. Therefore, more studies are needed to provide a better understanding of earnings management and the impact of audit quality on earnings management by assessing different aspects of audit quality in the context of listing and in different forms of earnings management. Second, most previous research is cross-country studies examining the effect of institutional environments on earnings management on a global sample, whereas this study examines the role of institutional environments in reshaping the relation between earnings management and audit quality by adding subnational institutional environments to the model. Finally, in the context of undeveloped markets, Vietnam has been chosen for this study not only because it is a developing country with an emerging capital market, but also because of the existence of a unique institutional environment.

Why Vietnam?

Vietnam is a unitary state, which is divided into four tiers of government including central; 63 provinces; around 680 districts; and around 11,000 communes. Each tier of government has both legislative and executive authorities. At the local level such as provincial, district, and commune levels, the highest government authority to exercise legislative authority is an elected People’s Council, and the actual work is conducted by a People’s Committee. Accordingly, provincial governments are the first level local administrative body in Vietnam in which areas of society in localities are managed based on the principle of democratic centralism. However, each province in Vietnam has many disparities in economic development and business culture because of its diverse operations under different historical conditions and within different scopes of competence and having the autonomy to implement policies (Tuyen et al., 2016). Provinces carry out the central government’s laws in different ways (Malesky & Taussig, 2009). Furthermore, according to a full report by the Vietnam Chamber of Commerce & Industry (VCCI) and the United States Agency for International Development (USAID) (2016), “the quality of governance and institutions across provinces has been uneven. While many provinces have made significant improvements in economic governance and business investment, others have lagged behind.” The Vietnamese stock market is completely different from the rest of the developed and emerging economies in the Asia region such as Bangladesh, India, Indonesia, Malaysia, Philippines. While the stock exchanges in these countries have transformed into listed companies on their markets and running as private companies or joint–stock company, the stock exchanges in Vietnam is still run as state-owned institutions and supervised and regulated by the Government. In addition, it is believed that different amount of accounting choices embedded in different accounting standards influences the level of earnings management (Goncharov & Zimmermann, 2007). Many developing countries such as Mongolia, Singapore, India, Malaysia, Pakistan and Thailand show the different approaches in applying their accounting systems toward IAS/IFRS, whereas Vietnam is one of the few countries that has not yet applied IFRS for the preparation and presentation of financial statements. As of today, Vietnam has a different experience as financial statements are prepared in accordance with Vietnam Accounting Standards issued by the Ministry of Finance. According to the Jurdant (2019), the quality of financial statements in Viet Nam is not consistent with international good practice. The result is that the financial statements are not prepared on a basis comparable with those in other jurisdictions. Hence, according to the World Economic Forum for the strength of auditing and accounting standards, Vietnam is ranked 128th of 141 countries surveyed, while Indonesia, Malaysia, Singapore are ranked 74th, 29th, 3rd respectively (World Economic Forum, 2019).

All these characteristics of the Vietnamese market create the motivation to investigate the audit quality, institutional environments, and earnings management.

As a whole, this study investigates two questions that have not been addressed in previous research:

(1) Do audit quality mitigate earnings management around listing?

(2) Do institutional environments affect earnings management around listing?

The remainder of this paper is organized as follows. The next section discusses theoretical motivation and empirical hypotheses. Section 3 presents data and methodology. Empirical findings are reported in Section 4, and conclusions and implications are provided in the last section.

Literature Review and Hypotheses Development

Audit Quality in Determining Earnings Management and Corporate Events

A growing body of research increases attention on earnings management of firms around the time of events (IPO, SEO). Agency theory and asymmetric information theory have been widely adopted to explain earnings management. Following agency theory, the relationship between two parties: shareholders (principal) and managers (agent), who have different interests, exists. This conflict arises when managers tend to operate in their own self-interest rather than in the best interests of shareholders. In addition, with a high degree of information asymmetry during equity issuance events, the information asymmetry between firms and potential investors is likely to exist, such that, managers have superior knowledge and more information than outsiders regarding the firm’s activities. Hence, managers have an incentive to issue stocks at high prices or to increase listing opportunities by manipulating earnings through accounting practices (Algharaballi, 2013; Anh Huu & Chi Thi, 2021; Chang & Lin, 2018; Fan, 2007).

In the context of IPO, scholars have also investigated the existence of earnings management around IPO events (before IPO and in IPO year). Studies addressing this phenomenon have revealed that, on average, IPO firms appear to engage in window dressing in the year before going public or in the IPO year by making income-increasing discretionary accruals (Ahmad-Zaluki, 2009; Chiraz & Anis, 2013; DuCharme et al., 2004; Gajewski & Gresse, 2006; Mangala & Dhanda, 2019; Nuryaman, 2013; Roosenboom et al., 2003; Teoh et al., 1998a, 1998b). While a number of studies have documented that IPO firms engaged in aggressive earnings management during a pre-IPO period in order to inflate income, other studies do not support this finding. Different views are provided by researchers such as Armstrong et al. (2008), Ball and Shivakumar (2008), Chou et al. (2009), Fan (2007), Premti (2013), and Alsultan (2017) who found that firms did not engage in earnings management in the year before the IPO or the year of going public. Similarly, in the context of SEO, a high level of information asymmetry in the SEO event provides an opportunity for managers to manipulate earnings upward to maximize offering proceeds. Rangan (1998) demonstrates that the existence of positive accruals was found during the year around SEO. Confirming Rangan’s view, DuCharme et al. (2004), Kinnunen et al. (2000), Zhou and Elder (2004), Shivakumar (2000), Pastor-Llorca and Poveda-Fuentes (2006), D. A. Cohen and Zarowin (2010), Ahmad-Zaluki et al. (2011), and Chang and Lin (2018) found that managers have attempted to make unusually high income-increasing by taking advantage of the information asymmetry.

In summary, the majority of international studies on earnings management have focused mainly on IPO and SEO events. Furthermore, international evidence on IPOs in developed markets shows that the time lag between the issue date and the listing date is short, generally ranging from 5 days to 70 days (Boubaker et al., 2017). The delay from the issue date to the listing date, however, is enormous in some developing countries, such as Vietnam. In some countries, IPOs and listings are distinct processes with listing requirements being more stringent than IPO requirements (Allens, 2017), and the actual listing date takes place long after the issue date. We are interested in how firms manipulate earnings management around listing events.

As stated earlier, from an agency theory perspective, an external auditor is one monitoring device since it helps stockholders to collect reliable information, as well as mitigate conflicts between managers and shareholders by reducing the information asymmetry in a firm’s financial statements (Jacobides & Croson, 2001; Piot, 2001). In addition, audit studies tend to signaling theory to explain the demand for high audit quality. According to Alsultan (2017) and Titman and Trueman (1986), when firms hire a high-quality auditor during an IPO, it can be observed as a positive signal as a signal regarding the economic value of the firm and a signal of the quality of their financial statements. Hence, the authors support the notion of signals as they present evidence that newly issuing firms send a positive signal of true firm value to potential investors by hiring a reputable auditor. In practice, managers are allowed to exercise judgment in financial reports by selecting accounting methods that could mislead stakeholders. “The demand for auditing services arises from a need to facilitate dealings between the parties involved in business relationships - shareholders, creditors, public authorities, employees and customers” (Arrunada, 2000, p. 1). It means that independent auditors give opinions on the truth and fairness of financial statements in all material respects in conformity with generally accepted accounting principles. The function of the audit can mitigate the information asymmetry, as well as improve financial reporting (Z. J. Lin et al., 2009). Hence, the audit quality is capable of restricting opportunistic earnings management (Balsam et al., 2003; Velury, 2003). Due to the unobservable nature and complexity of audit quality (Firth & Liau-Tan, 1998; Z. J. Lin et al., 2009; Tran et al., 2019), many researchers have tried different ways to measure the audit quality. Therefore, there is no single characteristic that can be used as a proxy for measuring the audit quality (Balsam et al., 2003). Accounting literature has provided a variety of audit quality proxies. The academic frameworks such as auditor reputation (auditor size) (Lennox, 2005; Teoh & Wong, 1993, industry specialization (Balsam et al., 2003; Mascarenhas et al., 2010), tenure (Boone et al., 2008; C.-Y. Chen et al., 2008) show that the audit quality is multidimensional. Empirical research generally agrees that proxies such as the size or reputation of auditors, industry specialization, and tenure are the most commonly used audit quality measure (Z. J. Lin et al., 2009). In addition, a growing body of research has investigated different aspects of the association between earnings management and the audit quality, and these empirical evidence on the effect of audit quality and earning management is not clear (Salehi, Fakhri Mahmoudi, & Daemi Gah, 2019).

The following is an overview of previous studies in regard to auditor size or reputation, tenure, and industry expertise.

Evidence from these studies strongly specified that Big 4 produces efficient auditing more than non-Big 4, and in turn constrain earnings management and therefore, the first hypothesis was proposed:

Hypothesis 1 (H1): Audit quality measured by the auditor size (reputation) is associated with earnings management.

Hypothesis 2 (H2): Audit quality measured by the length of audit firm tenure is associated with earnings management.

Hypothesis 3 (H3): Audit quality measured by the level of auditor industry specialization is associated with earnings management.

In the light of the above discussion, this section provides an overview of proxies that were used to investigate the relationship between the audit quality and earnings management when the audit quality is measured by audit size, auditor tenure, and auditors’ industry expertise. Along a similar dimension, this study is expected that audit quality can reduce earnings management, particularly, for firms with severe earnings manipulation. Nevertheless, this study has two distinct features from previous studies. First, this study focuses on the effect of the audit quality on earnings management around listing events for 4 years around listing (a pre-listing year, a listing year, and 2 years after listing). Moreover, in order to meet the changes of market environment and to improve the openness and transparency of the Vietnamese market, a set of higher standards for listing has been introduced since 2012 with a minimum profit and increasing the minimum level of charter capital. Therefore, we extend the literature by exploring whether this effect is different in the context of changing listing requirements. Finally, this study further examines the role of institutional environments (more on this below).

Earnings Management and Institutional Environments

Like the audit quality, institutional environments are broadly thought of as external control mechanisms to restrict earnings management. Many studies consider institutional environments as an explanatory factor for cross-national differences in reported earnings management. These differences arise from the stakeholder theory. Accordingly, successful companies are those who manage their relationships with key stakeholders effectively (Mitchell et al., 1997). “The relationship a firm chooses to manage is based on the stakeholder attributes of power, legitimacy, and urgency” (Geiger & van der Laan Smith, 2010), P24), while stakeholder attributes are affected by the institutional environments, which vary cross-nationally. Using the stakeholder dichotomy, Ball et al. (2000) argued that accounting earnings, which is a proxy for the level of earnings management, is systematically different in common-law countries compared to code-law countries. The authors concluded that common-law countries exhibit lower levels of earnings management than code-law countries. Consistent with Ball et al. (2000), Leuz et al. (2003), and Othman and Zeghal (2006), in their examination of earnings management, found that firms operating in code-law countries generally have less levels of regulation, litigation, and transparency regarding financial statements compared to that in common-law countries. However, institutional factors are difficult to observe and measure (Voigt, 2013). The literature makes various attempts to develop a series of alternative measures institutions to find a suitable proxy for each research. Based on the regulatory dimension, in a majority of papers examining the relationship between institutional environments and earnings management by using cross-country data, institutions are measured in an indirect way such as the strength of the legal environment (González & García-Meca, 2014; Memis & Çetenak, 2012; Nnadi et al., 2015), investor protection (Ali et al., 2022; Leuz et al., 2003), control of corruption or bribery (González & García-Meca, 2014; Kimbro, 2002; Lourenço et al., 2020; Malagueño et al., 2010; Memis & Çetenak, 2012).

Instead of using cross-country data, a growing number of papers strengthen the evidence of institutional environments and earnings management by using sub-country data. In particular, Ngo and Susnjara (2017) examined the effect of political connections on earnings management among US suppliers to government agencies. Ngo and Susnjara (2017) found that government suppliers engage in more earnings management. In addition, the authors also found that the degree of accruals earnings management may be positively influenced by the level of sales to government contractors. By comparison, in China, D. Chen et al. (2011) examined the different aspects of the institutional dimension, its macroeconomic control, the political cost to profit-taking behavior. D. Chen et al. (2011) found that political costs are negatively correlated with the degree of earnings management. In addition, the authors found that non-state-controlled firms manipulate their earnings downwards. However, by using data of 38 countries, Yamen et al. (2022) found that institutional quality has no significant effect on accrual earnings management.

In a nutshell, the review of the earnings management literature reveals that while cross-country differences in the effect of institutional environments on earnings management are well documented, little is known about the link between earnings management and institutional environments at the local level (subnational institutional environments in the home country). From the works aforementioned, it is worth noting that none of the works investigated the role of institutions in curbing earnings management in an emerging economy, especially at the provincial level. To contribute to the accounting literature review, therefore, this study was conducted to assess the sub-national institution and its different specific aspects that have been not carried out in previous studies.

Based on the above arguments, the next hypothesis is:

Hypothesis 4 (H4): There is a significant impact of provincial institutional quality on earnings management.

Methodology and Data

Empirical Method

Earnings Management Measures

The extant literature addresses three tools of earnings management such as accruals management, real earnings management and classification shifting (Bansal & Kumar, 2021). Under REM, managers can use restructuring of real transactions to manipulate earnings managers from the normal course of business activities (D. Cohen et al., 2020; Roychowdhury, 2006), whereas classification shifting is an earnings management tool used to misclassify income statement items in order to report favorable operating performance metrics (Bansal & Bashir, 2023; McVay, 2006). This study focuses on accrual-based because the accrual-based examination method is the most commonly studied method to detect earnings management in literature. Researchers explained that accounting-accruals are easier to manipulate and have no direct cash flow consequences (Rangan, 1998; Teoh et al., 1998a, 1998b). Accruals are the differences between earnings and cash flows which refer to managers’ opportunistic use of the flexibility in accounting standards to change reported figures. Accrual-based earnings management (AEM) refers to managers’ opportunistic use of the flexibility to select accounting methods and policies to change reported earnings without any cash flow consequences or the firm’s result in the long run. AEM is the most popular studied method to test earnings management because it is easier to manipulate and less risky and less costly. Therefore, this research has applied AEM as a proxy for earnings management.

Total accruals are broken into current and long accruals (Teoh et al., 1998a, 1998b). The authors concluded that current accruals are the most manipulated in earnings management (M. L. DeFond & Jiambalvo, 1994; Maijoor & Vanstraelen, 2006; Teoh et al., 1998a, 1998b). Current accruals are reflected as increases or decreases in the balances of current asset accounts (excluding cash) and current liability accounts (Beneish, 1999; Rangan, 1998). Moreover, by using four cross-sectional models to estimate earnings management including two total accruals-based models and two current accruals-based models, Anh Huu and Chi Thi (2021) suggests that managers of newly listed firms in Vietnam attempt to boost their earnings in the year preceding the listing by taking advantage of current accruals, but not in total accrual models. To be consistent with previous studies in the literature review, DCA-discretionary current accruals are used in this study to evaluate earnings management (Ahmad-Zaluki et al., 2011; Anh Huu & Chi Thi, 2021; Nguyen & Thi Duong, 2022; Roosenboom et al., 2003; Teoh et al., 1998a, 1998b).

In addition, Ball and Shivakumar (2008), Armstrong et al. (2008) argue that “using low values of lagged total assets (t-1) in model produce extreme values of discretionary accruals estimates since pre-listing total assets are relatively small and not representative of the listing-year or post-listing year total assets.” This study estimates the DCA models tested as in the following equation:

Current Accruals Model

Current Accruals Measurement

Where:

Institutional Environments

In order to study how the sub-institutional environments affect firms’ earnings management in Vietnam, this study firstly uses the institutional factor at the provincial level as an aggregated index—the provincial competitiveness index (PCI). Since 2005, the PCI has been collected annually in all 63 provinces by the Vietnam Chamber of Commerce and Industry (VCCI) in collaboration with the United States Agency for International Development (USAID). The PCI has served as an important reference for both investors’ decisions as well as the government’s economic initiatives, providing independent, unbiased information on the provincial business environment (Vietnam Chamber of Commerce & Industry (VCCI) & United States Agency for International Development (USAID), 2017). In other words, the PCI index is a performance indicator, which ranks and evaluates the institutional quality of provincial and business environment. The PCI is calculated in a three-stage process as follows: (a) collecting business survey data and published data sources, (b) calculating 10 sub-indices and standardizing to a 10-point scale, and (c) calibrating the composite PCI as the weighted mean of 10 sub-indices with a maximum score of 100 points (Vietnam Chamber of Commerce & Industry (VCCI) & United States Agency for International Development (USAID), 2017). The overall PCI has been built up by 10 component indicators including entry cost for new firms, land access, transparency, time costs of regulatory compliance, informal charges—measuring amount of bribes, proactivity of provincial leadership, policy bias, business support services, labor training, and legal institutions.

Audit Quality Measures

Due to the unobservable nature and complexity of audit quality, many researchers have tried different ways to measure audit quality (Firth & Liau-Tan, 1998; Z. J. Lin et al., 2009). Thus, there is no single characteristic that can be used as a proxy for the audit quality (Balsam et al., 2003), and no consensus on which measures are best (M. DeFond & Zhang, 2014). As a result, accounting literature has provided a variety of audit quality proxies (Salehi et al., 2017). Based on demand and supply factors, M. DeFond and Zhang (2014) classify proxies to measure audit quality into two different groups: output-based measures (such as material misstatements, auditor communication, financial reporting quality, and perceptions) and the input based measures (such as auditor characteristics: auditor size, industry specialist auditors). While input based measures are usually best suited for tests that examine the demand for audit quality arising from client incentives, output-based measures are usually best suited for tests that examine the supply of audit quality affected by auditor incentives for independence. Consistent with the literature regarding audit quality and earnings management, the second approach is chosen for this study. The academic frameworks show that the audit quality is multidimensional such as auditor reputation (auditor size) (Lennox, 2005; Teoh & Wong, 1993), industry specialization (Balsam et al., 2003; Mascarenhas et al., 2010), tenure (Boone et al. (2008); C.-Y. Chen et al. (2008) show that the audit quality is multidimensional. Empirical research generally agrees that proxies such as the size or reputation of auditors, industry specialization, and tenure are the most commonly used in measuring the audit quality (Z. J. Lin et al., 2009; Salehi, Fakhri Mahmoudi, & Daemi Gah, 2019; Salehi, Komeili, & Daemi Gah, 2019), which are therefore chosen for this study.

Audit Firm Size (Reputation)

Confirming earlier studies (Becker et al., 1998; C.-Y. Chen et al., 2008; Lopes, 2018; Myers et al., 2003; Piot, 2001), this study classifies four auditing firms (Big Four) including PricewaterhouseCoopers, KPMG, Ernst & Young, and Deloitte, Touche & Tohmatsu as higher reputational auditors. This study expects that newly listing firms using the Big Four will engage in less earnings management than firms using non-Big-four auditors. A dummy variable is used, which is equal to one if the auditor is a member of the Big Four and zero otherwise.

Auditor Tenure

Prior studies have argued that the length of the relationship between auditor and client can potentially affect the audit quality. However, the literature on the effect of auditor tenure on earnings management has provided mixed results. This study aligns with the previous studies on the audit quality in deciding that the auditor tenure is the most appropriate proxy for measuring the audit quality (Ghosh & Moon, 2005; González-Díaz et al., 2015; Khaksar et al., 2022; Knechel & Vanstraelen, 2007; Myers et al., 2003; Salehi et al., 2017). Therefore, the auditor tenure, which is calculated as the number of consecutive years of experience that the current auditing firm was hired, is used in this study as a proxy for high-quality auditors.

Auditor Industry Specialization

To test the hypothesis 3, a measure of auditor industry specialization is needed. Consistent with Craswell et al. (1995), Ferguson and Stokes (2002), and Mayhew and Wilkins (2003), (Bergen, 2013); Zhou and Elder (2004), a market share is used in this study to measure the auditor industry specialization. This approach supposes that an audit firm will gain knowledge and specialization through experience in each industry. The audit firm industry specialization is defined as follows:

Where:

x: the number of firms audited by the same auditor in an industry

y: the number of firms audited by all auditors in an industry

The ratio is calculated yearly based on all firm-year observations for all industries. When the ratio is greater than 15% in an industry, the audit firm is considered an industry specialist. Consistent with Zhou and Elder (2004) and K. Y. Chen et al. (2005), the cutoff value of 15% was adopted in this study. Therefore, the auditor industry specialization is a dummy variable, equal to one if the auditor is an industry specialist and zero otherwise.

Measuring Control Variables

In order to control the disproportion of firms’ earnings management based on characteristics of firms and to control other cross-sectional effects, several control variables are included in the models including: firm size (Gill et al., 2014; Gong et al., 2008; Kamel, 2012; Kao et al., 2009; Mangala & Dhanda, 2019; Premti, 2013; leverage (Eckbo & Norli, 2005; S. Gao et al., 2017; Gill et al., 2014; Kao et al., 2009; firm age (Ahmad-Zaluki et al., 2011; Myers et al., 2003; Shust, 2015); total accruals (Algharaballi, 2013; Becker et al., 1998; Elder & Zhou, 2002; Yaşar, 2013; Zhou & Elder, 2004; firm performance—Return on asset, operating cash flow, and change of net income (Alsultan, 2017; Chowdhury & Eliwa, 2021; D. A. Cohen & Zarowin, 2010; Dechow et al., 1995; J. Gao et al., 2015; Sitanggang et al., 2020; Teoh et al., 1998a, 1998b).

New Listing Requirements

To be listed on the Ho Chi Minh Stock Exchange (HOSE) in Vietnam, firms must comply with all State (National Assembly, Government, Ministry of Finance) requirements applicable to listed firms. Since September 15, 2012, the new framework with significant changes are set out, introducing much tougher listing conditions regarding the minimum paid up capital, minimum profitability, and publicity. Hence, companies which are eligible to be listed on HOSE after September 15, 2012, are more likely to have high incentives opportunistically to manage earnings upward than companies listed before September 15, 2012. Therefore, the dummy variable named Year2012 is added to the regression model. This variable is equal to one for firms listed after September 15, 2012, and zero otherwise.

Empirical Model

All necessary variables are defined above, the multiple regression models are estimated as follows to investigate the effect of the auditor quality and institutional environments on earnings management:

t: year around listing event including a pre-listing year, a listing year and 2 years after listing

EM i,t : earnings management measured by DCA of firm i in year t

Big 4: a dummy variable which is equal to one for firms hiring a member of Big Four and zero otherwise.

Tenureyears i,t : calculated as the number of consecutive years of experience that the current auditing firm was hired by firm i in year t

Auditindus i,t : equal to one if a firm is classified to that industry, zero otherwise

LEV i,t : the ratio of total debt to total assets of firm i in year t

AGE i,t : the log of firm age of firm i in year t

SIZE i,t : the log of total assets of firm i in year t

TA i,t : absolute value of total accruals of firm i in year t

ROA i,t : income after tax scaled by an average asset of firm i in year t

CFO i,t : cash flow from operation scaled by an average asset of firm i in year t

DeltaNI i,t : change in net income divided by a beginning total assets of firm i in year t

Year 2012: equals to one for firm listed after September 15, 2012, and zero otherwise

Ind i : dummy variable firm i belongs to an industry;

ei, t : error term

According to Anh Huu and Chi Thi (2021), HOSE-listed firms present lower levels of earnings management in two subsequent years after listing than in the year prior to the listing and listing. Hence, in order to investigate whether the relationship between audit quality, institutional environments and earnings management is different in pre-listing years, when compared to post listing years, we extend the model by adding the Dummylisting variable. This variable is equal to one for the post listing years, and zero otherwise. Moreover, we add in the model 4 interactions of each of audit quality and institutional environments variables (Big 4, Tenureyears, Auditindus, PCI) with a dummy that indicates the type of years (Dummylisting). These interactions are necessary to evaluate any differences in the effect of these audit quality, institutional variables between before and after listing.

Model 2

Data Source

Sample Selection

The sample for testing earnings management includes all newly listed firms on HOSE from 2009 to 2017. Because of having differences in reporting practices, financial firms were excluded from the sample. Moreover, due to insufficient data to calculate accruals earnings manipulation, two industries with portfolios of less than six firms were eliminated. Hence, eight industries consisting of materials, energy, consumer staples, industrials, real estate, utilities, consumer discretionary, and health care are included in the sample.

The main reasons for choosing the period from 2009 to 2017 for this study are that financial statements for the previous 2 years are acquired to calculate DCA in the pre-listing year and the availability of data was a major concern before 2009. In addition, the sample was terminated in 2017 to allow sufficient time to estimate earnings management for 2 years after listings. Hence, the final sample includes 189 firms listed on HOSE with a total number of observations of 756 during the period from 2009 to 2017.

Data Sources

This study utilizes two data sources. The first data are obtained from the annual report of the Provincial Competitiveness Index (PCI) which is a result of an ongoing collaborative effort between the Vietnam Chamber of Commerce and Industry (VCCI) and the U.S. Agency for International Development (USAID). The second financial data source was from the prospectuses and annual financial statements. Consistent with the earnings management literature, in order to calculate the coefficients of the discretionary accruals models, a cross-sectional regression was adopted for each year-by-year and by industry. The estimation model was run yearly for each industry. In order to estimate earnings management for the sample of 189 listed companies in the period from 2009 to 2017 in the pre-listing year, the listing year, and 2 years after listing, the prospectuses and annual financial statements of 308 firms from 2008 to 2019 in eight industries were collected from official’s website of HOSE and listed firms’ website.

Empirical Findings

Descriptive Statistics

Table 1 illustrates a summary of the descriptive statistics for all variables including dependent and independent variables. It can be observed in Table 1 that the mean of DCA is 0.0228 with a standard deviation of 0.2063. It refers to the existence of a large variation in earnings management in the sample firms with a DCA minimum of −1.2895 and a maximum DCA of 1.0788, indicating that some firms are more likely to engage in earnings management. In addition, the mean of Big 4 is 0.2275, which reveals that 22.75% of observations in the sample were audited by one of the Big Four. Similarly, the mean of Auditor industry specialization (Auditindus) is 0.2474, which indicates that 24.74% of the sample firms were audited by an industry specialist. The tenure variable provides a mean value that is slightly higher than 3 years. According to Vanstraelen (2000), Carcello and Nagy (2004), Gunny et al. (2007), the mean of 3.0397 years is classified auditor tenure into medium (3–5 years). Moreover, Table 1 also indicates a fairly wide dispersion of PCI with a range from 47.68 to 75.96.

Descriptive Statistics of the Audit Quality Sample.

The descriptive statistics of control variables as firm characteristics are as follows. The mean of leverage (LEV) is 0.4946, which illustrates that on average in the sample firms, 49.46% of total assets are generated from debt. Moreover, as can be seen from Table 1, there is an existence of a large variation in leverage, with a minimum of 0.0020 and a maximum of 0.9641. The mean value of log of firm age (Logage) is 2.6111, with a minimum of 0.3010 and a maximum of 4.1431. The log of total assets (Size) has a mean value of 9.0164, a minimum of 7.9482, and a maximum of 10.8446. The ratio of operating cash flow (CFO) has a mean value of 0.0506, which indicates that the core business activities of the company are thriving. However, there is an existence of a large variation in CFO with the minimum and maximum values of CFO −1.1 and 1.0490 respectively. The mean value of Return on assets (ROA) is 0.0899, with a minimum value of −0.0856 and a maximum value of 0.7426, suggesting that around listing events, on average, sample firms can use their assets effectively to generate income.

Variance Inflation Factors

Table 2 shows the results of testing for multicollinearity with the use of VIF, as the VIF mean is 1.39, which is much lower than the threshold of 10 (De Jongh et al., 2015; James et al., 2014; O’brien, 2007). The check for variance inflation factors indicates that multicollinearity does not exist among all independent variables. This means that there is the absence of a multicollinearity problem in our model.

Variance Inflation Factors (VIF).

Table 3 illustrates the variables’ correlation matrix included in the regressions. None of the correlations between variables were significantly highly correlated (0.90) to impose multicollinearity threats (Hair et al., 2009). Consistent with established results in the accounting literature, absolute value of total accruals is positively and significantly associated with DCA when one considers the full sample. In addition, the results for the full sample show that while Tenureyears variable has a significant and negative relationship with the earnings management, the opposite was true in case of others main independent variables such as Big 4, Auditindus, PCI.

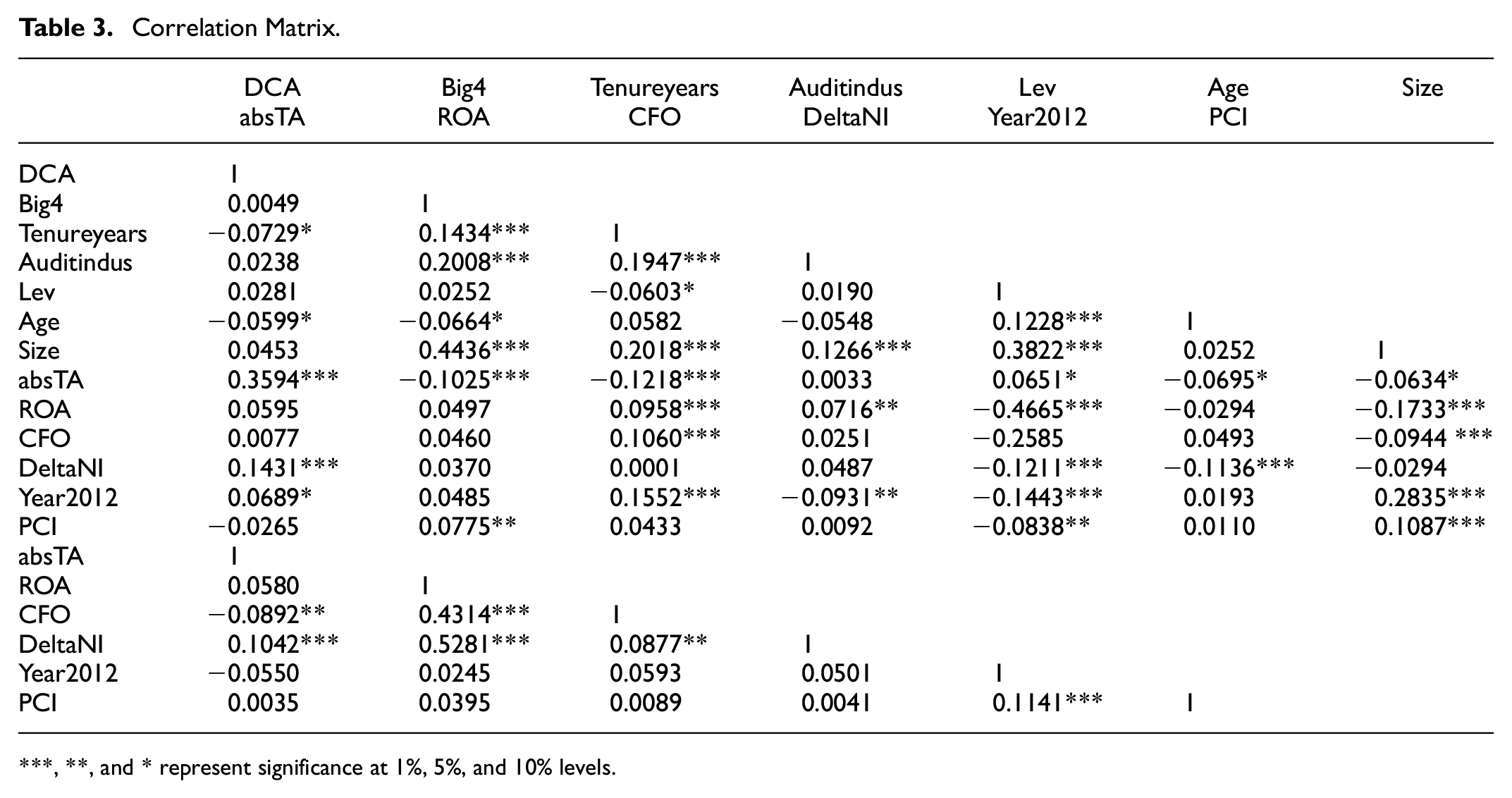

Correlation Matrix.

, **, and * represent significance at 1%, 5%, and 10% levels.

Regression Assumption Tests

This study adopted pooled and panel data regression models (fixed effect and random effect). The three results might reveal differences in coefficients, signs, and the number of significant variables. The Hausman test is used to select between the fixed effect model (FE) and the random effects model (RE). In addition, it may be because the pooled OLS regression does not reflect heterogeneity, which is reflected in the panel data regression results. If the pooled method based on the regression model was fitted (when probabilities of Breusch and Pagan Lagrangian were higher than 0.1), the Pooled OLS results will be presented. In this section, the research will interpret a chosen model analysis after using Hausman and Breusch, and Pagan Lagrangian test.

Hypotheses Tests

In the main analysis, the earnings management consists of both positive and negative discretionary accruals. Hribar and Collins (2002) have argued that both effects may bias the test to reject the null hypothesis. In order to examine the existence of differences in the relationship between audit quality, institutional environments, and earnings management based on the sign of engagement in earnings management, the study sample is divided into two groups. The first group contains firms with positive discretionary accruals and the second group contains firms with negative discretionary accruals. Therefore, for each model, the results of multiple regression analyses for full sample DCA, negative DCA, and positive DCA are presented. In addition, in this section, the research only presented the results of chosen models after some tests as mentioned in the research methodology section.

Full Model

Audit Quality and Earnings Management

Table 4 provides a summary of the results of multiple regression for full sample DCA for model 1 and model 2. The results illustrate that the model is statistically significant at the p-value of .0000 for all models. The audit quality, which is measured by Big 4, Tenures, and Auditindus, is statistically insignificant associated with earnings management (DCA). It means that the Big Four audit firms are not associated with lower levels of DCA. The results provide evidence to demonstrate that the Big Four firms are less effective at constraining earnings management in the Vietnamese market. The results also indicate whether financial statements are audited by the Big Four or non-big Four is not significant at all. Similarly, the findings indicate that there were no significant differences in earnings management behavior between firms audited by industry specialist auditors and firms audited by non-industry specialist auditors. In addition, the results for the entire sample suggest that a decrease in auditor tenure does not have an effect on the level of earnings management. The coefficient of DumListing, coefficient of the interaction term of the variables audit quality and DumListing are insignificant, which means that the relationship between the audit quality and the level of earnings management can not be found any differences between before and after listing.

Regression of DCA on Audit Quality and PCI.

: Selected model POLS.

, **, and * represent significance at 1%, 5%, and 10% levels.

Following the methodology applied for testing the association among audit quality, institutional environments, and earnings management, two groups are formed based on their levels of positive and negative DCA. Splitting the sample firms into two groups allows us to observe the differences between these two groups. Tables 5 and 6 report the results and comparisons between these two groups and the entire sample.

Regression of Positive DCA on Audit Quality and PCI.

: Selected model POLS.

, **, and * represent significance at 1%, 5%, and 10% levels.

Regression of Negative DCA on Audit Quality and PCI.

: Selected model POLS.

, **, and * represent significance at 1%, 5%, and 10% levels.

The results for the multivariate regressions for two groups are reported in Tables 5 and 6. The coefficients of the first variable—Big 4 indicating whether firms are audited by high or low reputation auditing firms are not significant in the two models. This result is consistent with those generated by the entire sample that finds no significant difference in DCA between firms audited by Big Four and non-big Four auditing firms. Therefore, H1 is not supported in the multivariate context. The first interpretation is that the Big Four does not curb earnings management in Vietnam. This result is consistent with the finding of Jeong and Rho (2004), Algharaballi (2013), Habbash and Alghamdi (2017), and Alsultan (2017).

For positive DCA, the results presented in Table 5, are consistent with those found only in tenureyears in model 1 and model 2. The coefficient of the main independent variable (tenureyears) is negatively related to DCA at a 10% level while the estimate of the interaction term of tenureyears with the Dummylisting is positive, and they are both statistically significant. It seems that Tenureyears variable can reduce the level of earnings management in the group of companies with positive DCA, but less in post-listing years. Therefore, greater reliance is placed on the results of the positive model, which supports H2.

For negative DCA, while auditor industry specialization has an insignificant relationship with DCA for the total sample model and positive DCA model, the model based on negative DCA shows significantly positive coefficients at a 5% level. Interestingly, the results of model 2 show that the coefficient estimates (t-statistics) of tenureyears in the model of positive DCA is negatively significant, whereas a positive relationship between tenureyears and earnings management is found in the negative DCA model and smaller when compared to subsequent years after listing.

Overall, for firms with positive DCA, tenureyears variable can explain the earnings management’s degree. The findings indicate that the auditor tenure is more effective in constraining income-increasing activities, but less in post-listing years. This result is in line with the report of Myers et al. (2003), who found evidence to suppose that longer audit tenure tends to be associated with lower discretionary current accruals. In contrast, for negative DCA, the first findings from models 1 and 2 indicate that an increase of auditor tenure is associated with higher earnings management. In addition, there were significant differences in earnings management behavior between firms with negative DCA audited by industry specialist auditors and firms audited by non-industry specialist auditors. In other words, firms with incentives to smooth earnings downwards report significantly greater discretionary accruals when they hire industry specialist auditors than firms audited by non-industry specialist auditors. It can be inferred that around listing events, firms engage less in using income-decreasing accruals when they have the industry specialist auditor and longer auditor tenure. The findings from this study develop and extend the limited empirical evidence to explore the role of the audit quality in restricting income—decreasing, therefore, providing support for hypothesis H3 only in firms with negative DCA.

Institutional Environments and Earnings Management

The estimated results are reported in Tables 4 to 6 for the aggregated index (PCI). While the full model shows no significant association between the aggregated index (PCI) of provincial institutional quality and earnings management, the correlation coefficients are significant for the two remaining models. To specify, the results show that for firms with positive DCA around listings, PCI is significantly and negatively related to earnings management at the 1% level and the results persist in provinces and areas with weaker market institutions. This study further finds that negative effects are enhanced by institutional factors in Vietnam as the effects of the PCI on earnings management are stronger in regions (provinces) with a low marketization index. This implies that newly-listed firms using income-increasing earnings management from provinces presenting a lower quality of governance are more likely to have a higher level of earnings management than their counterparts from provinces with a higher quality of governance. By contrast, for firms with income-decreasing around listings (negative DCA), the coefficient of PCI is positive and statistically significant, indicating that the higher quality governance is associated with a higher level of earnings management. It would seem that newly-listed firms using income-decreasing earnings management presenting higher levels of quality governance appear to reduce manager’s incentive to manipulate earnings downwards. Therefore, H4 is supported when the negative DCA model and the positive DCA model are considered; however, the results are not statistically significant when the entire model is used. These findings confirm results of earlier studies pertaining to the impact of institutional quality on earnings management in case of earnings upwards (González & García-Meca, 2014; Memis & Çetenak, 2012; Ngo & Susnjara, 2017; Nnadi et al., 2015). In addition, the analyses presented in this study highlight the relevance of recognizing different relationships between institutional quality and earnings management in two forms: upwards and downwards.

Conclusion and Implications

Unlike previous studies, this paper considers the relation between audit quality, the role of institutional environments at the provincial level, and earnings management around listing events. Two novel results emerge from this study.

First, the purpose of this study was to evaluate the effect of audit quality on earnings management around listing events. Surprisingly, the coefficient for the Big 4 is not statistically significant in all three models. Financial statements audited by Big Four firms do not differ from those audited by non-Big Four firms in terms of constraining income-increasing activities or income-decreasing activities. Previous studies were undertaken in high legal liability markets in which a high-quality auditor is expected to restrict earnings management (Alhadab & Clacher, 2018; Elder & Zhou, 2002; Myers et al., 2003). Therefore, in the light of findings from testing audit quality and earnings management of Vietnamese firms that financial statements audited by Big Four firms do not differ from those audited by non-Big Four firms in terms of constraining income-increasing activities or income-decreasing activities. In addition, the findings of this study also indicated that there was no role for auditor tenure and auditor industry specialization in curbing earnings management activities around the listing process, as indicated by the regression result of entire current discretionary accruals. However, the regression result of signs of current discretionary accruals showed a contrast and indicated that the auditor tenure mitigates the activities of income-increasing activities only in the positive model, while auditor tenure and the auditor industry specialization can explain the incentives for managing earnings only in the negative model. After controlling for dummy listing and interaction variables that may be related to audit quality, this relation remains unchanged. Given the apparent conflicting evidence, this study contributes to existing knowledge of audit quality and earnings management which has not reached the same conclusions in terms of the role of audit quality in constraining earnings management. This research is the first to examine in a context of around listing, as the existing material is limited in previous literature, where the attention has been paid to the relationship around IPOs and SEOs. Most of studies examining the impact of high quality auditors on earnings management has focused on well-developed capital markets whereas this study examines earnings management practice in an emerging market with the delay from the issue date to listing date. Moreover, this study extends knowledge and shows the first contribution in this setting to the international literature by investigating the role of audit quality in curbing both upward and downward earnings management.

Second, this study examines the association between perceptions of earnings management and institutional environments around listing events at the provincial level. This approach allowed us to consider the role of local governance in the earnings management in two forms—upwards and downwards, not merely its conditional mean. This study found no evidence of the impact of provincial governance on earnings management when the full regression model was used. In contrast, a negative effect of provincial governance on earnings management was found in case of a motive for upward earnings management before and after listing. Interestingly, the effect differed substantially across signs of earnings management. For newly listed firms having an incentive to manage earnings downwards, good governance tends to provide greater benefits to reduce the occurrence of negative earnings management. These results are consistent with the proposition of the existence of the relationship between institutional environments and earnings management by using country-level accounting data when institutional factors measured by the strength of the legal environment (González & García-Meca, 2014; Memis & Çetenak, 2012; Nnadi et al., 2015), measured by investor protection (Ali et al., 2022; Leuz et al., 2003), measured by control of corruption or bribery (González & García-Meca, 2014; Kimbro, 2002; Lourenço et al., 2020; Malagueño et al., 2010; Memis & Çetenak, 2012), or using sub-country data (D. Chen et al., 2011; Ngo & Susnjara, 2017). This study extends the literature by providing the first direct assessment of the relationship between a home country’s level of institutional environments and earnings management practices in two forms. Therefore, the investigation of institutional environments at the country level and earnings management around listing provides another contribution for both international and national literature and for Vietnamese regulators.

The findings shown in this study have implications for investors, policymakers, and firms. For investors, the findings from research provide a new framework for investors to improve their decisions. Investors need to be aware of an aggressive manipulation of accruals in the pre-listing year and should cautiously and carefully consider and should be exercised when investing in newly-issued firms. In addition, investors should not perceive Big Four auditors as providing a higher audit quality than non-big Four auditors. The results also suggest that the longer auditor partner tenure tends to be associated with lower discretionary accruals in firms with income-increasing activities. It means that instead of paying attention to auditor size (reputation), investors should be concerned about the length of the auditor-client relationship of newly listed firms. In contrast, around listing events, firms engage less in using income-decreasing accruals when they have the industry specialist auditor compared to the non-industry specialist auditor. Moreover, investors should perceive that firms that are located in provinces with higher institutional quality will have less positive earnings management in the case of manipulating earnings upward and have less negative earnings management in the case of manipulating earnings downward. For firms, managers should be aware that paying higher audit fees to Big Four auditors will not prevent accruals earnings management. In order to mitigate income-increasing, firms should increase auditor tenure in which the auditor should become better at recognizing material misstatements by gaining experience and better insights into the clients’ business strategies. In addition, to constrain income-decreasing, firms should hire industry specialist auditors as their experience cultivated from auditing one firm is likely to be relevant to other firms in the same industry.

For the policy maker, the findings show that there is no difference in audit quality between Big Four and non-Big Four in detecting earnings management. In addition, the governance quality plays an important role in curbing earnings management as it raises concerns about the power of the legal system and enforcement bodies in the emerging market such as Vietnam. Therefore, in order to strengthen an effective system in monitoring the quality of independent audit services, the authorities should facilitate more investigations and supervision toward audit activities, promulgate the legal framework, and impose strict penalties for frauds and intentional presentation of information distortion in financial statements. At the provincial level, institutional quality improvement should be continued by intensifying administrative procedure reforms through using information technology and enhancing transparency in order to further reduce time costs and reduce the burden of informal charges.

Despite the overall contribution, this study has its own limitations. First, the current study is performed by using the sample of listed firms in Vietnam, hence this study could not be generalized to other settings. Furthermore, due to data limitations, the period of research around listing was limited which may be an inadequate length of time for data analysis. Other limitations were related to the technique of earning management proxies. Using only discretionary accruals may not capture the magnitude and nature of manipulation (Fields et al., 2001) and firms can manage earnings by managing either accruals or real accounts (Ibrahim et al., 2011). Further research can also be performed to have a more comprehensive approach by using varied earnings management techniques such as real earnings management or classification shifting which would be a potential topic for future research

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is funded by National Economics University, Hanoi, Vietnam