Abstract

Financial inclusion is increasingly recognized as a vital instrument for promoting economic development and reducing inequality, especially in low- and middle-income countries. Yet, there is limited research on the relationship between financial inclusion and wealth accumulation, especially in developing countries like Vietnam. The moderating role of gender in this relationship is also underexplored. As such, this study examines the effect of financial inclusion on wealth accumulation and the moderating role of the gender of the household head, using the latest data from the Vietnam Household Living Standards Surveys (VHLSS). We address potential endogeneity issues by employing Lewbel’s instrumental variable estimation method. We find that financial inclusion significantly and positively influences household wealth. Moreover, the gender of the household head significantly moderates this relationship, with female-headed households experiencing greater benefits from financial inclusion in wealth accumulation compared to male-headed households. We also find that household income is a mediating channel through which financial inclusion enhances household wealth. This paper contributes to the literature by providing causal evidence on the impact of financial inclusion on household wealth in a Global South context and highlighting gender heterogeneity in this relationship. Policy implications stemming from these findings are discussed.

Introduction

Financial inclusion refers to access to affordable financial services such as savings accounts, credit, insurance, and payment systems. At the macro level, financial inclusion is a well-documented driver of economic growth and sustainable development (Amaliah et al., 2024; Ozturk & Ullah, 2022; Van et al., 2021). At the micro level, it plays a crucial role in enhancing household income and wealth, especially in developing economies (L. Li, 2018; Swamy, 2014; Zhang & Posso, 2019). In resource-constrained environments, access to financial services enables households to save securely, invest in income-generating activities, and build resilience against economic shocks—facilitating both short-term earnings and long-term asset accumulation. However, systemic barriers such as long distances to financial institutions, inadequate infrastructure, and socio-economic exclusion—especially among marginalized groups—often impede access in developing countries. According to the World Bank (2021), only 38.99% of adults in low-income countries have a bank account, compared to 96.36% in high-income nations. This gap in access to financial products and services significantly limits opportunities for wealth accumulation and poverty reduction in the Global South. Therefore, it is imperative to examine how financial inclusion can foster wealth accumulation in such contexts to inform the design of effective, targeted policy interventions.

Prior studies have consistently shown that financial inclusion enhances household economic outcomes. For instance, Wang et al. (2023) find that increased bank branch density enhances rural incomes in China, while X. Li et al. (2011) and Ding and Abdulai (2020) report that microcredit improves per capita income and consumption. Financial inclusion has also been linked to wealth accumulation, as shown by Célerier and Matray (2019) in the United States. Stein and Yannelis (2020) demonstrate that early access to banking services improves employment, and long-term wealth among marginalized populations. A meta-analysis by Biru et al. (2024) confirms that financial inclusion positively affects consumption, income, and asset holdings. Nonetheless, existing evidence is predominantly concentrated in developed countries like the United States. Moreover, while financial inclusion’s economic effects are well-explored, its interaction with gender remains underexamined—particularly in developing countries like Vietnam. This reveals a notable gap in understanding how financial inclusion affects household wealth in developing countries and whether these effects differ by the gender of the household head.

Vietnam presents a compelling case for investigating financial inclusion’s role in wealth accumulation within a developing economy. To address the gaps identified above, this study leverages the two most recent waves (2018 and 2020) of the Vietnam Household Living Standards Surveys (VHLSS), encompassing over 50,000 nationally representative households. Our study differs from previous work in several important respects. First, unlike earlier studies that focus on income or consumption (Biru et al., 2024; Ding & Abdulai, 2020; X. Li et al., 2011) or a wide range of determinants of household wealth (Pham et al., 2024; Vo & Ho, 2023), we specifically analyze the impact of financial inclusion on wealth accumulation. Second, while most prior studies neglect gender-based heterogeneity, we explicitly examine how the effects of financial inclusion differ between male- and female-headed households, thereby providing a valuable foundation for more inclusive and targeted financial policies in developing countries.

This study makes three key contributions to the literature. First, it provides robust empirical evidence on the positive effect of financial inclusion on household wealth in Vietnam, a context where empirical research on this relationship remains limited. Second, it enhances our understanding of gender-based heterogeneity by showing that female-headed households benefit more from financial inclusion, highlighting the potential role of financial inclusion in reducing gender inequality. Third, the study investigates whether household income serves as a mediating channel through which financial inclusion influences household wealth. While some theoretical considerations suggest that financial inclusion may increase income, thereby facilitating wealth accumulation, empirical evidence on this mechanism remains scarce.

The remainder of the paper is structured as follows. Section “Literature Review and Hypotheses” reviews the relevant literature. Section “Data and Methodology” describes the data and econometric strategy. Section “Results” presents and discusses the empirical results. Section “Conclusions and Policy Implications” concludes and outlines policy implications.

Literature Review and Hypotheses

Household Wealth

It is well-documented in the literature that demographic characteristics, such as age, gender, marital status, and others, significantly impact household wealth outcomes. First, using Vietnam Household Living Standards Surveys from 2008 to 2020, Pham et al. (2024) conclude that female-headed households are wealthier than male-headed households in the upper threshold of assets (VND 96.75 million in 2008, 440.25 million in 2018, and VND 634.40 million in 2020), and vice versa. With the same dataset but in 2014, Vo and Ho (2023) have a similar finding that the wealth disparity where female-headed ones take the lead happens at the upper quantiles of net worth. By contrast, based on the Household Finance and Consumption Survey of 22 European countries, it was found that males are 25% more likely to have more wealth (Kukk et al., 2023). Second, age is also a crucial determinant, and wealth appears to have a linear relationship with it (Pham et al., 2024; Van Rooij et al., 2012). Using data from 16 countries, Semyonov and Lewin-Epstein (2013) find a similar conclusion—the net worth of a household increases with age, albeit at a declining degree. Moreover, at age 35, the wealthiest millennials have more net worth than the wealthiest baby boomers, and vice versa (Gruijters et al., 2023). Third, single households (whether the head is male or female) tend to be less wealthy (Semyonov & Lewin-Epstein, 2013). Similarly, households led by the widowed or divorced tend to have lower wealth (Pham et al., 2024). In a France-based study, there is evidence that individuals in long-term partnerships—either married or not—tend to have higher wealth than those who are divorced, separated, or have always been single (Bonnet et al., 2023). Biljanovska and Paglligkinis (2018) also provide evidence for the positive relationship between household wealth and being a couple. Fourth, Liao and Zhang (2021) also suggest that as the number of children increases, household wealth also improves, implying a potential association between household size and wealth. Scholz and Seshadri (2007) contend that children significantly influence a household’s net worth, making them crucial in comprehending wealth distribution. Additionally, they discover that the interplay between fertility and credit constraints notably impacts wealth accumulation. As such, utilizing the China Household Finance Survey, Wang et al. (2020) assert that the size of the family positively and significantly impacts household wealth. However, other scholars (Biljanovska & Palligkinis, 2018) identify a negative correlation as larger households may accumulate less wealth due to higher consumption needs and resource dilution without corresponding income contributions from household members, such as minors and elders. Fifth, racial and ethnic aspects should also be taken into account. By analyzing the non-Hispanic African-Americans and Hispanics relative to non-Hispanic whites in the United States in the 1989 to 2016 period, Wolff (2022) implies that the net worth of the minorities plummets compared to that of non-Hispanic whites from 2007 to 2016. Another study on the wealth gaps between Black-White and Hispanic-White by Adames and Bryer (2024) concludes that racial wealth gaps widen over early adulthood.

Socioeconomic characteristics are also important factors impacting household wealth. First, Pham et al. (2024) also find that household income positively impacts wealth when the threshold of VND 440.25 million and VND 634.40 million is met in 2018 and 2020, respectively. Furthermore, household income significantly affects wealth, and significant nonlinearities in the impact are found (Bloemen & Stancanelli, 2001). Second, employment status is significantly linked with the wealth of a household (Yu et al., 2024), and empirical evidence from Kim (2022) shows that self-employment is a significant determinant of household net worth. Third, ceteris paribus, higher educational attainment is associated with greater wealth accumulation (Semyonov & Lewin-Epstein, 2013). In China, years of education are positively associated with cash and bank deposits, which are the key determinants of household wealth conditions, according to a study by Li et al., (2020). In the same country setting, Wang et al. (2022) find that qualifying for the university level enhances the probability of homeownership and increases total housing wealth, which is closely related to household wealth. Fourth, Davies et al. (2009) have shed light on how household wealth is distributed worldwide, located in the most advanced regions (North America—34%, Europe—30%, and prosperous Asia-Pacific—24%). Pham et al. (2024) assert that those who live in urban areas and have total assets over the threshold of VND 440.25 million accumulate more wealth. Besides, Liao and Zhang (2021) find that, on average, household heads with local urban hukou (i.e., the origin from urban areas) have 315,000 and 266,000 yuan more in housing wealth and total wealth, respectively, than rural hukou ones.

Financial Inclusion

There is a fast-growing body of literature on the impacts of financial inclusion on various aspects of society and the economy. It is demonstrated that there is a positive correlation between financial inclusion and economic growth, as access to financial services enables both individuals and businesses to participate more effectively in economic activities (Beck et al., 2000). Sahay et al. (2015) show a significant association between higher levels of financial inclusion and improved GDP growth rates, particularly in developing economies. Many studies further indicate that financial inclusion can significantly reduce poverty, by integrating underbanked populations into the formal financial system, thus providing tools for financial resilience (Bettin et al., 2023; Koomson et al., 2020). Suri and Jack (2016) find that mobile banking raises per capita consumption, reduces labor inefficiencies, and lifts households out of poverty. Regarding income inequality, Kling et al. (2022) show that financial inclusion can narrow income disparities by decreasing household underinvestment in education. Using a dynamic panel analysis of 116 countries from 2001 to 2019, de Moraes et al. (2023) further confirm that financial inclusion reduces income inequality. However, Fonseca and Matray (2024) indicate that benefits from financial inclusion are unevenly distributed. Rather than being shared equally, these benefits tend to grow with workers’ levels of education, thereby contributing significantly to wage inequality. This suggests that human capital plays a key role in shaping the impact of financial inclusion on income inequality. Notably, recent studies also indicate that financial inclusion significantly improves well-being (Kamble et al., 2024; F. Li et al., 2025), increases household financial resilience (Liu et al., 2024), mitigates wealth inequality by reducing barriers to investment (Shen et al., 2024), and reduce negative effects of income inequality on water, sanitation and hygiene access (Acheampong et al., 2024).

Bachas et al. (2021) suggest that debit cards lower transaction costs for accessing money and reduce monitoring costs, encouraging beneficiaries to check their account balances more regularly and build trust in the bank. Consequently, debit cards facilitate savings among households. A study in South Africa by Chipunza et al. (2024), using a partial least squares path model, indicates that financial inclusion indirectly enhances consumer well-being by increasing asset holdings, formal channels of saving, credit, and insurance. Popov and Zaharia (2019) observe that increasing financial inclusion through intrastate deregulation has considerably increased female labor force participation. This increase is attributed to three key mechanisms: higher net job creation by private firms, expanding service-oriented sectors, and increasing job opportunities requiring female-specific skills. Fonseca (2023), utilizing individual credit record data and a difference-in-differences design to compare states with varying debt collection restrictions, finds that limiting collections reduces access to mainstream credit, leading to a rise in payday borrowing. This suggests that restricted access to conventional credit may increase predatory lending practices.

Financial inclusion is also shown to promote entrepreneurship (Ajide, 2020), especially female entrepreneurship (Fareed et al., 2017). Silva and Pino (2024) demonstrate that financial inclusion positively impacts roof quality improvements for individuals in slum settlements in Chile. Furthermore, they find that financial inclusion supports self-employment activities among low-income populations. Koomson and Danquah (2021), using two rounds of living standards survey data from Ghana, find that increased financial inclusion correlates with a reduction in household energy poverty. Additionally, they find that financial inclusion boosts household consumption and net income, highlighting its role in alleviating energy poverty. Chen et al. (2023) report that bank deregulation, which enhances financial inclusion, significantly lowers firms’ carbon emissions by improving production efficiency, technological adoption, and asset structure. Consequently, bank deregulation positively impacts corporate environmental performance.

Hypothesis Development

Financial inclusion is expected to reduce information frictions, alleviates credit constraints, and provides mechanisms for risk-sharing and consumption smoothing. Access to savings accounts allows households to accumulate precautionary balances and undertake productive investments; access to credit enables financing of small businesses or durable asset purchases; and access to insurance mitigates vulnerability to income shocks. Together, these theoretical arguments suggest that financial inclusion should positively affect wealth accumulation.

Empirical research broadly supports this theoretical expectation. Wang et al. (2023) find that increased bank branch density promotes rural income growth in China through greater use of financial services. X. Li et al. (2011) and Ding and Abdulai (2020) show that microcredit participation boosts household consumption and income, highlighting the transformative potential of credit access. Célerier and Matray (2019) demonstrate that access to banking services in the United States is associated with higher rates of durable asset ownership, better debt management, and reduced exposure to financial shocks. Stein and Yannelis (2020), exploiting historical variation in access to the Freedman’s Savings Bank, find that financial access not only increased savings but also promoted higher occupational income and real estate wealth accumulation among formerly enslaved Black families. Moreover, Biru et al. (2024), through a meta-analysis of financial inclusion studies, confirm positive impacts on income, consumption, and asset ownership across diverse country contexts. In light of both theoretical considerations and empirical evidence, we propose the following hypothesis:

Furthermore, the impact of financial inclusion is unlikely to be homogeneous across population groups. In particular, gender is a key dimension along which the benefits of financial inclusion may differ. Women often face higher barriers to accessing and using formal financial services (Demirgüç-Kunt et al., 2021; Hess et al., 2021), yet when access is granted, they tend to demonstrate stronger financial management skills and generate greater household welfare gains (Ashraf, 2009; Pitt & Khandker, 1998). For example, Dupas and Robinson (2013) show in a field experiment that offering savings accounts to female market vendors in Kenya led to increased investment and higher consumption, effects not observed among male counterparts. Likewise, Pitt and Khandker (1998) find that microcredit provided to women yields greater gains in household consumption than credit provided to men. These findings imply that once access barriers are lifted, women may be more effective in utilizing financial tools to improve household outcomes.

Several theoretical arguments explain this pattern. First, women are more likely to reinvest financial gains into household well-being—such as children’s health, education, and nutrition—leading to longer-term wealth accumulation. Second, studies suggest that women generally adopt more prudent, risk-averse, and long-term-oriented financial strategies (Ashraf, 2009). Third, household bargaining models posit that increased control over financial resources enhances women’s decision-making power, leading to improved financial outcomes (Duflo, 2003; Ringdal & Sjursen, 2021). This is particularly salient in Vietnam, where post-Doi Moi reforms have significantly increased women’s labor force participation and economic influence. Female-headed households, in particular, are more likely to exercise independent financial control, enabling more strategic use of financial services. This empowerment may allow them to leverage financial inclusion more effectively than male-headed households, where traditional gender norms may still inhibit women’s financial agency. We thus propose the following hypothesis:

Regarding mediating channels, one of the most prominent argument is that financial inclusion may influence household wealth indirectly through its impact on income. Theoretically, access to financial services, such as savings accounts, credit, and insurance, can enhance household income. Access to credit allows households to invest in small businesses and productive assets, generating new income streams. Meanwhile, savings mechanisms help smooth consumption and mitigate income volatility, enabling households to better manage economic shocks and maintain consistent earning capacity. In addition, financial services can improve labor market participation and productivity by reducing transaction costs and enhancing financial planning. In line with the theoretical reasoning above, we propose the following hypothesis:

Data and Methodology

Data Sources

This study utilizes the two latest waves (2018 and 2020) of the Vietnam Household Living Standards Survey (VHLSS), a key source for monitoring socioeconomic trends and guiding economic policies in Vietnam. VHLSSs have been conducted biennially by the General Statistics Office of Vietnam (GSO) with assistance from the World Bank and the United Nations Development Program (UNDP) since 1993, with each wave offering insights into household income, expenditure, health, and living conditions. As the 2022 VHLSS does not include key questions on financial inclusion such as bank account ownership, ATM card use, and savings behavior which are typically found in Section 8 of earlier waves. In other words, the data required to measure financial inclusion are not available in the 2022 wave. Consequently, the 2018 and 2020 datasets serve as the most recent and comprehensive sources for examining how financial inclusion affects household wealth in Vietnam.

Model Specification

The estimation model is specified as follows:

where is the natural log transformation of the household net worth (the difference between total assets and total debt).

Table 1 provides definitions and sources for all variables used in the study. Household wealth is measured as net worth, which is the difference between household assets and household debts. Household income includes all sources of earnings, such as wages, government transfers, agricultural and non-agricultural business activities, and rental income. The financial inclusion index is a composite measure ranging from 0 to 7, based on whether the household owns a bank account, savings book, debit card, credit card, life insurance, non-life insurance, or securities. A higher score reflects greater access to and participation in formal financial services.

Definitions and Data Sources of Variables.

We follow Vo and Ho (2023) to compute adjusted household size, accounting for both consumption needs and economies of scale. The formula is

Table 2 presents descriptive statistics for all variables in the analysis. On average, household net worth is approximately 986 million VND, with a standard deviation of 1.73 billion VND. The values range from a minimum of—76.3 billion VND to a maximum of 80.7 billion VND, highlighting significant wealth inequality within Vietnam. The financial inclusion index has a mean of 0.93, suggesting that nearly all households have access to at least one formal financial service or product on average. Household income averages 232 million VND per year, but the high standard deviation (668 million VND) again signals sharp economic disparities across Vietnamese households.

Descriptive Statistics and Description of All Variables.

First, we estimate the Equation 1 using OLS regression. Furthermore, given the hierarchical nature of our data, with households nested within 63 provinces, we employ a mixed-effects model (also known as multilevel modeling) to investigate the robustness of our results. Mixed-effects model is increasingly employed in such scenarios in recent years (see e.g., Bruna, 2022).

Endogeneity

Notably, in econometric models, addressing endogeneity is crucial to ensure unbiased and consistent parameter estimates. Traditional instrumental variable (IV) estimation is a common approach to addressing endogeneity, which requires an external instrument satisfying—a variable that is both correlated with the endogenous regressor (relevance condition) and exogenous concerning the error term in the model (exogeneity condition). Finding an instrument that meets relevance and exogeneity conditions is challenging in practice. Identifying a variable that is sufficiently correlated with the endogenous variable and plausibly unrelated to the outcome can be difficult, especially when dealing with complex or multifaceted phenomena. Even when an instrument appears valid in theory, establishing and defending its exogeneity often requires robust empirical justification, which is rarely straightforward and usually controversial.

Several studies are trying to tackle the endogeneity of financial inclusion with the dependent variables. For example, Koomson and Danquah (2021) address the potential endogeneity in their study of financial inclusion’s impact on energy poverty in Ghana by using “distance to the nearest bank” as an instrumental variable (IV). This approach leverages the assumption that proximity to a bank increases the likelihood of financial inclusion but does not directly influence energy poverty other than through financial inclusion itself. This distance serves as a proxy, where shorter distances correlate with easier access to banking services, which in turn could foster better financial participation. Although some find this IV strategy well-grounded and reliable, others may argue that this potential violates exogeneity. Distance to a bank may also correlate with other unobserved factors, like regional development, infrastructure, or household income levels, which independently impact energy poverty. In urban areas, people are generally closer to financial institutions, but this doesn’t automatically guarantee higher financial inclusion due to factors like income variability and financial literacy. Thus, the instrument may lack robustness across different geographic settings and socioeconomic contexts. In addition, there is a risk of self-selection bias in location choice. Households with higher socioeconomic status or those less likely to experience energy poverty may self-select into more developed areas. By virtue of their infrastructure and economic opportunities, these regions tend to offer closer proximity to banks and financial services. At the same time, there is also a risk of Endogenous Bank Branch Location Decisions. Financial institutions often strategically place branches in economically developed regions where the potential for profitable operations is higher. These areas typically have lower rates of energy poverty due to their advanced infrastructure and economic activity. These arguments further weaken the validity of distance to the nearest bank as an instrument, as it may be correlated with regional characteristics that independently impact energy poverty, thus violating the exclusion restriction requirement for a valid instrument.

As such, identifying a valid instrument presents a substantial challenge, particularly in studies that rely on secondary data, where access to data for appropriate instruments is often limited. In this context, Lewbel’s (2012) instrumental variable estimation provides viable alternatives that can be effective and efficient. These methods have been widely used in recent literature (Cruz et al., 2024; O’Sullivan et al., 2021). Details and results from these methods are provided in the sub-section 4.2 below.

Results

Baseline Results

Tables 3 and 4 present the pairwise correlation matrix and variance inflation factor (VIF) for the independent variables, respectively. As shown in Table 2, the correlations between variables are not excessively high. The mean VIF is 2.19, well below the threshold of 5, indicating that multicollinearity is unlikely to affect the model.

Correlation Matrix.

Variance Inflation Factor.

The estimated impact of financial inclusion on household wealth from OLS estimation is presented in Table 5. As shown in column 1, financial inclusion positively and significantly affects household wealth, supporting Hypothesis 1. This effect remains robust after including control variables and year-fixed effects (column 2). While the coefficient on the gender of the household head is negative and insignificant, the interaction term between the gender of the household head and financial inclusion is positive and significant. This suggests that financial inclusion has a stronger effect on household wealth in female-headed households compared to male-headed households, providing support for Hypothesis 2.

Empirical Results From OLS Models.

Note. Clustered standard errors are in parentheses.

p < .1. **p < .05. ***p < .01.

Given the hierarchical nature of our data, with households nested within 63 provinces, using OLS in this context would violate the assumption of independence of observations because individuals from the same province may share similar characteristics and influences. This interdependence could result in biased estimated coefficients and incorrect standard errors. As such, we employ a mixed-effects model (also known as multilevel modeling) to explore further the impact of financial inclusion and the moderating role of gender. Multilevel modeling provides more reliable and unbiased estimates by properly accounting for the nested structure of the data.

The results are presented in Table 6. Column 1 reports the null model for household wealth, with an intraclass correlation coefficient (ICC) of 4.2%. This indicates that only 4.2% of the variation in household wealth is attributable to differences across provinces, suggesting that provincial differences are not a significant determinant of household wealth. In column 2, financial inclusion continues to have a positive and significant effect on household wealth, with the coefficient being similar to the OLS estimate. The interaction term between the gender of the household head and financial inclusion remains positive and significant. Interestingly, while the coefficient on household head gender is insignificant in the OLS model, it is negative and significant in the mixed-effects model, implying the existence of a gender wealth gap in Vietnam, though it appears to be not extremely large. The ICC in column 2 drops to 2%, indicating that after controlling for other variables, the variation in household wealth across provinces is relatively small. Overall, the results from the mixed-effects models are consistent with the OLS estimates and provide further support for Hypotheses 1 and 2.

Mixed-Effects Model.

Note. Robust standard errors in parentheses.

p < .1. **p < .05. ***p < .01.

Treatment of Endogeneity

Although OLS and mixed-effects estimations indicate that financial inclusion positively impacts household wealth and that the gender of the household head significantly moderates this effect, potential endogeneity issues may undermine the validity of these results. In this subsection, we identify and address these endogeneity concerns to accurately estimate the effect of financial inclusion on household wealth and the moderating role of gender. First, another proxy for financial inclusion is used to assess the robustness of our findings against measurement error. Second, we employ Lewbel’s (2012) instrumental variable (IV) estimation, which address issues such as simultaneity, omitted variable bias, and measurement error, to examine the impact of financial inclusion and the moderating role of gender on wealth accumulation. Finally, we employ the Rubin causal model as an additional robustness check.

Another Proxy for Financial Inclusion

It could be argued that the financial inclusion index is overly simplified, as it merely sums the values of seven items: bank accounts, savings accounts, ATM cards, credit cards, life insurance, non-life insurance, and securities. To address this, we performed a principal-factor analysis using these seven variables to create a more refined financial inclusion index. The Bartlett test of sphericity was statistically significant, indicating that the variables are interrelated. Additionally, the Kaiser–Meyer–Olkin (KMO) measure of sampling adequacy was 0.63, exceeding the threshold of 0.5, confirming the new index’s reliability. We then use this new financial inclusion index to re-estimate our model. The results from OLS and mixed-effects estimations are shown in Table 7, indicating that the effect of financial inclusion on wealth accumulation remains consistent. Furthermore, gender continues to moderate the relationship between financial inclusion and wealth accumulation significantly.

Changing Proxy for Financial Inclusion (New Financial Inclusion Index From PCA).

Note. Financial inclusion index two is derived from factor analysis of seven variables.

p < .1. **p < .05. ***p < .01.

Lewbel’s (2012) Instrumental Variable (IV) Estimation

Given the difficulty of finding a valid external instrument that satisfies both the relevance and exogeneity conditions in our context, we then use Lewbel’s (2012) instrumental variable (IV) estimation to tackle potential endogeneity issues in our model. This method is particularly well-suited for studies based on secondary data, such as the VHLSS, where traditional instruments are difficult to find or validate. Lewbel’s (2012) instrumental variable approach addresses this challenge by providing a method to generate instruments internally. Lewbel’s (2012) method leverages heteroskedasticity—the variance of the error terms changing with different values of the explanatory variables—to generate instruments from within the dataset. This technique allows for causal inference in models with endogenous regressors even when no external instrument is available, as long as heteroskedasticity is present. This method is increasingly employed in the literature (Hasan et al., 2021; Koomson & Danquah, 2021; O’Sullivan et al., 2021).

To verify the validity of Lewbel’s (2012) approach, we conducted multiple diagnostic tests. The results are reported in Table 8. The White/Koenker and Breusch–Pagan tests strongly confirm the presence of heteroskedasticity, satisfying a key condition for Lewbel’s method to generate valid instruments. Thus, the null hypothesis of the weak instrument is rejected, and the relevance condition is satisfied. Moreover, the Hansen J-test is statistically insignificant, suggesting that the instruments satisfy the exogeneity condition. As such, the results from Lewbel’s (2012) are valid.

Empirical Results From Lewbel’s (2012) IV-GMM.

Note. Clustered standard errors are in parentheses. They are labelled by a number of * on the RHS column and the note below the table.

p < .1. **p < .05. ***p < .01.

As shown in Table 8, after taking endogeneity into account, financial inclusion is still found to influence household wealth positively. The interaction term between financial inclusion and the gender of the household head is also significant and positive. These results are consistent with our previous findings. Overall, the results from Lewbel’s (2012) approach are consistent with the OLS estimation and provide further support for Hypotheses 1 and 2.

Mediation Analysis

This section investigates whether household income acts as a mediating channel through which financial inclusion affects household wealth. Theoretically, financial inclusion improves access to formal financial services such as savings, credit, and insurance, which in turn can increase household income. If higher income, enabled by financial inclusion, subsequently leads to greater wealth accumulation, then household income constitutes a plausible mediating mechanism in the relationship between financial inclusion and wealth.

To formally test this mediation pathway, we follow the classic framework proposed by Baron and Kenny (1986), which involves a three-step procedure. First, the mediator (household income) must be significantly predicted by the independent variable (financial inclusion). Second, the dependent variable (household wealth) must be significantly predicted by the independent variable when the mediator is excluded from the model. Third, when both the independent variable and the mediator are included in the model, the effect of the independent variable on the dependent variable should decrease in magnitude. A decrease in the effect size of financial inclusion implies partial mediation, while full mediation is indicated if the coefficient becomes statistically insignificant. All regressions include the full set of controls to ensure robustness.

The empirical results are presented in Table 9. Column (1) shows that financial inclusion has a positive and statistically significant effect on household income. This satisfies the first condition of the Baron and Kenny’s (1986) test. Column (2) presents the total effect of financial inclusion on household wealth. Consistent with our earlier findings, financial inclusion exhibits a strong positive effect on wealth, with a coefficient of 0.249. Column (3) incorporates household income into the model. As expected, household income itself is a strong and statistically significant predictor of wealth. More importantly, the coefficient on financial inclusion declines from 0.249 to 0.199 after controlling for income, providing evidence of a mediation effect. This reduction in magnitude implies that part of the effect of financial inclusion on wealth transmits through household income. In other words, financial inclusion enables households to increase their income—likely through enhanced labor productivity, entrepreneurship, or greater financial stability—which then contributes to higher levels of wealth accumulation. Thus, Hypothesis 3 is supported.

Mediation Analysis—Baron and Kenny’s (1986) Test.

Note. Clustered standard errors are in parentheses. They are labelled by a number of * on the RHS column and the note below the table.

p < .1. **p < .05. ***p < .01.

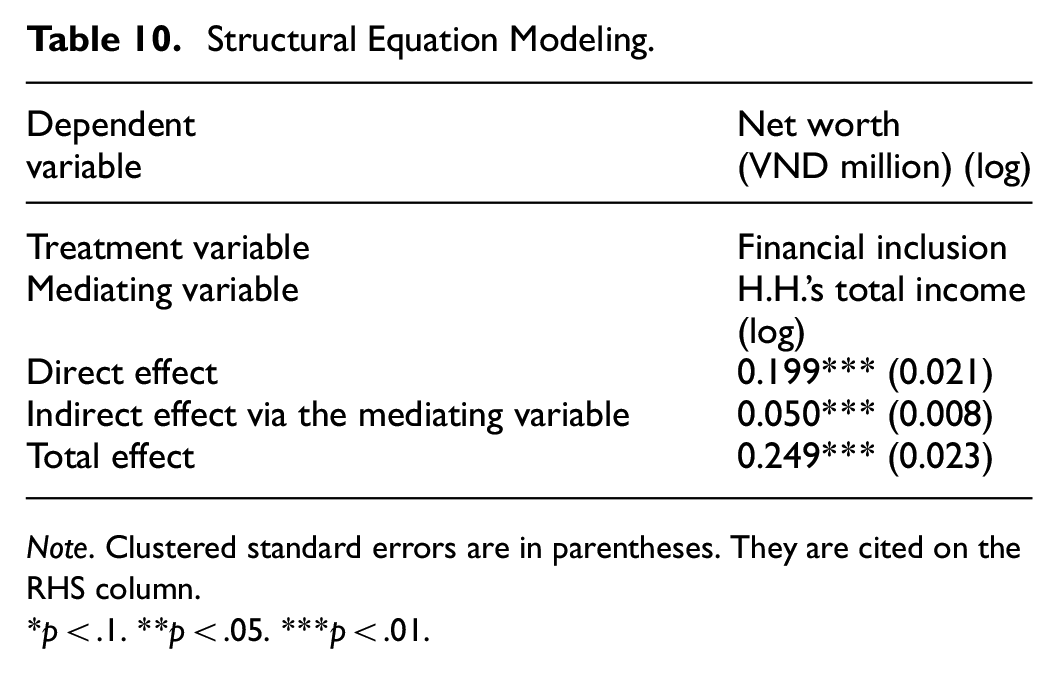

As a further robustness check, we employ structural equation modeling (SEM) to estimate the direct, indirect, and total effects of financial inclusion on household wealth. SEM allows for simultaneous estimation of multiple equations and explicitly models the mediating role of household income within a system of structural relationships. The results are presented in Table 10. We find that the direct effect of financial inclusion on household wealth remains positive and statistically significant. The indirect effect of financial inclusion—operating through household income—is also positive and statistically significant, confirming the mediating role of income. These results are consistent with the results from Baron and Kenny’s (1986) test and provide support to Hypothesis 3.

Structural Equation Modeling.

Note. Clustered standard errors are in parentheses. They are cited on the RHS column.

p < .1. **p < .05. ***p < .01.

Conclusions and Policy Implications

This study investigates the impact of financial inclusion on household wealth and the moderating role of gender in Vietnam, which has rarely been examined in the existing literature. We address potential endogeneity concerns by employing two advanced econometric approaches: Lewbel’s (2012) instrumental variable (IV) estimation. Our findings indicate that financial inclusion positively and significantly affects household wealth. Furthermore, the gender of the household head significantly moderates this relationship, with financial inclusion benefiting female-headed households more than male-headed ones. Furthermore, we demonstrate that household income is a mediating channel through which financial inclusion increases household wealth.

While our study shares some similarities with previous research on household wealth in Vietnam in terms of data sources and variables (Pham et al., 2024), it makes important and distinct contributions to the literature. Specifically, whereas Pham et al. (2024) primarily examine the determinants of household wealth with a focus on socioeconomic and demographic variables such as education and household income, our study concentrates on the role of financial inclusion as a key driver of wealth accumulation. Additionally, our study investigates gender as a moderating factor, thereby contributing to the growing literature on gendered economic outcomes and financial inclusion. In this respect, our research complements prior studies (Célerier & Matray, 2019; Ding & Abdulai, 2020; X. Li et al., 2011; Pham et al., 2024; Stein & Yannelis, 2020) by highlighting the impact of financial inclusion on household wealth and its gender heterogeneity.

Drawing on our findings, several policy implications emerge. First, our results show a robust and positive effect of financial inclusion on household wealth, confirming that access to financial services enables households to accumulate assets and improve their financial well-being. In light of this, the Vietnamese government should prioritize expanding both the physical infrastructure—such as bank branches, ATMs, and mobile banking agents—and the digital infrastructure required to support mobile and online banking platforms, particularly in rural and remote areas. This dual strategy would reduce geographic and technological barriers to formal financial services, allowing more households to save, invest, and manage risk effectively. Second, our findings reveal that female-headed households benefit more significantly from financial inclusion, highlighting a gender-differentiated impact. In response, financial inclusion initiatives should incorporate gender-sensitive policies, such as incentives for banks to offer tailored products to female entrepreneurs, and the promotion of women’s participation in community-based financial institutions like microfinance and savings groups. Third, the government should also strengthen consumer protection frameworks and ensure the transparency, affordability, and reliability of financial products. This would build trust in the financial system and attract people to use financial products and services.

Our study is not without limitations. First, gender is used as the primary moderating demographic characteristic, without concurrently analyzing the role of other key socioeconomic factors such as education level, employment status, or income. These factors not only influence access to financial services but may also interact with gender in shaping wealth outcomes. For instance, the economic empowerment effects of financial inclusion may differ between highly educated women and those with limited education, or between employed and unemployed women. Future research could explore how the effects of financial inclusion vary across combinations of demographic characteristics. Second, while Lewbel’s (2012) heteroskedasticity-based identification strategy offers a useful solution in the absence of traditional external instruments, it is not without limitations. The internally generated instruments, while proven valid through our diagnostic tests, are inherently data-driven and may be perceived as less credible than strong, theory-based external instruments. Future research could address these limitations by employing alternative identification strategies—such as natural experiments, difference-in-differences approaches, or randomized controlled trials—to provide more robust estimates of the impact of financial inclusion on household wealth.

Footnotes

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is funded by Ho Chi Minh City Open University under grant number E2023.03.1CD.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.