Abstract

Financial inclusion refers to a process that ensures the ease of access, availability, and usage of the financial system for all members of an economy. This paper aims to study financial inclusion’s impact on enterprise innovation and compare the different effects of traditional and digital financial inclusion. Existing papers mainly focus on digital financial inclusion’s influence. Based on China’s data, this paper fills the gap by constructing an index system to measure traditional financial inclusion and discussing the impact mechanism of the two kinds of financial inclusion on enterprise innovation (output and efficiency). The results illustrate that traditional financial inclusion inhibits the innovation output of enterprises, while digital financial inclusion has a positive effect. However, both traditional and digital financial inclusion is still in the stage of constraining the innovation efficiency of enterprises. Moreover, the two types of financial inclusion function differently for enterprises of different sizes and ownership. Evidence from China is expected to reveal the features of this relationship and inspire research in more economies.

Keywords

Introduction

Innovation is the primary engine for economic development, which has already been proved by Ulku (2004), who found that R&D had a positive effect on per capita GDP based on 30 countries’ data. In particular, as China’s economic development has entered the “new normal” stage, innovation began to be more crucial to sustained and medium-high-speed economic growth. In 2014, the concept of “widespread entrepreneurship and innovation” proposed by the government accelerated the innovation pace. Therefore, it is important for enterprises, the main force in society, to enhance their innovation capability.

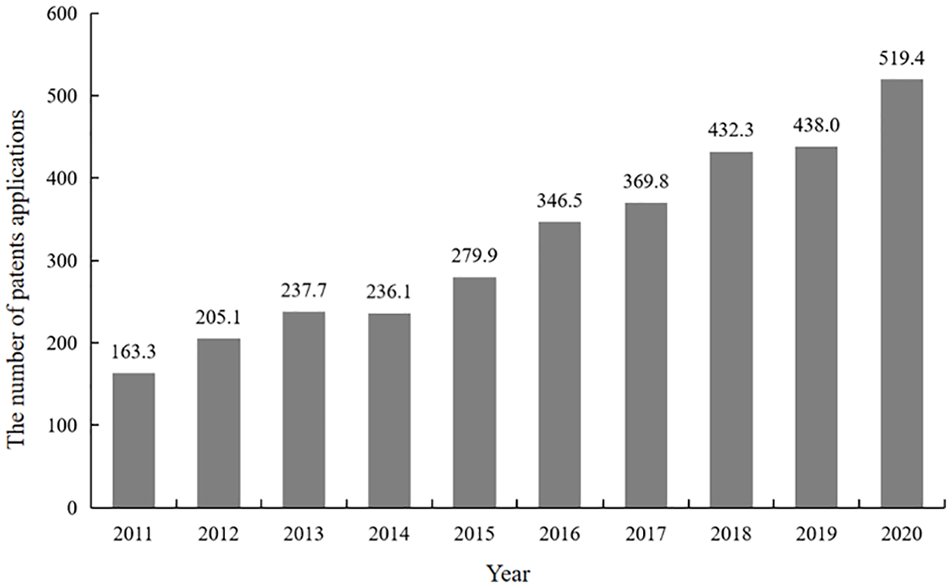

Enterprises in China made remarkable achievements from 2011 to 2020: the overall number of patent applications displayed an upward trend (Figure 1). The annual number of domestic patent applications rose from 1,633,000 to 5,194,000, leaping to the highest figures in the world. Moreover, driven by innovation, in 2020, the output of China’s strategic emerging industries accounted for 11.7% of GDP, and the output of high-tech manufacturing industries increased by 7.1%.

The total number of patents applications in China from 2011 to 2020 (Unit: 10 thousand).

Meanwhile, credit support from traditional financial institutions has also increased a lot. However, due to the high R&D investment costs and the long period of payback for innovation activities, as well as high credit risk and limited mortgage guarantee, traditional finance may still have a certain degree of financial exclusion for these enterprises, so it is often difficult for enterprises to meet the capital needs for innovation. It is confirmed by Campello et al. (2010) that enterprises suffering from financial constraints are more likely to cut spending on tech investment. Ayalew and Zhang (2020) found that enterprises were inhibited from conducting product and process innovation in developing countries. To relieve a firm’s financial constraints, China proposed the development of financial inclusion in 2013 to increase the accessibility to financial resources, especially for small and medium-sized enterprises. The concept of financial inclusion was first proposed by the United Nations in 2005. It aims to provide appropriate and effective financial services to all societies in need of financial services at an affordable cost. Therefore, financial inclusion can improve the allocation of financial resources and stimulate the vitality of enterprise innovation. At the same time, with the application of digital technology in the financial field, digital financial inclusion was put forward in 2016. It expands the boundaries of financial services, thereby reducing costs and enhancing efficiency while rejuvenating enterprise innovation.

This paper refers to the approach used in the paper of Zou and Ling (2018) to classify financial inclusion into traditional and digital financial inclusion, and then compares the influence of these two kinds of inclusion on enterprise innovation. The former refers to financial inclusion services provided by traditional financial institutions, such as traditional banking, insurance, etc. and the latter refers to services supplied by emerging ones, such as Internet financial institutions, etc.

Some studies have proved the positive effect of digital financial inclusion on enterprise innovation ability. For instance, Yang and Zhang (2020) tested whether digital financial inclusion helped SMEs grow sustainably, especially in high-tech industries and competitive markets. Applying the difference-in-difference model, Li and Li (2022) estimated the effect of plans and principles in digital financial inclusion on urban innovation and the results showed that there was a positive influence. However, the specific mechanism can be further explored and it is also worth discovering the different effects that traditional and digital financial inclusion can have on enterprises’ innovative activities. Lu et al. (2022) incorporated both local banks and digital financial inclusion in their study, and suggested that they could alleviate enterprises’ financing constraints. However, their work did not touch the effect of how relieving financing constraints could help enterprises make more investments in innovation. Further, innovation can be measured from several levels, so will there be differences in the impact of financial inclusion? Will factors such as enterprise size or ownership make a difference? For these issues, this paper will explore the impact through theoretical analysis and empirical testing, establishing the relationship between the microdata of enterprises and the macro-financial market. The study aims to make an enlightening discovery on how the development of the financial market can promote innovation by enterprises and also provide guidance for the government and enterprises to make relevant decisions.

The specific selection of China is mainly based on the following two considerations: first, many countries have conducted in-depth studies on the development of financial inclusion in recent years, but most of them are based on traditional financial inclusion, among which the achievements in developing countries such as India are more significant. Back in 2012, Gupte et al. (2012) computed the financial inclusion index for India. Furthermore, Singh and Ghosh (2021) studied the relationship between financial inclusion and economic growth through a large-scale financial inclusion program called PMJDY in India. China, like India, is a country with a large population and wealth gap, so it is more in line with the realistic environment for the development of financial inclusion. Simultaneously, considering the availability of data, this paper chooses China as an example to study the deepening development of financial inclusion. Second, with the application of digital technology in the financial field, its empowering effect on financial inclusion is increasingly prominent. However, there is no clear definition of digital financial inclusion in various countries, and there are relatively few corresponding studies. China is a global leader in digital economy development, with a digital economy growth of $5.4 trillion in 2020, ranking second in the world after the United States, and the rapid development of information infrastructure and digital industry. Moreover, China put forward digital financial inclusion for the first time at the G20 Summit in Hangzhou in 2016, which shows that the research on digital financial inclusion in China has great practical importance. It can guide other countries to develop digital financial inclusion and has certain universality.

Compared with existing research, this paper mainly contributes to the following aspects: (1) By referring to the literature, this paper innovatively establishes an index system to measure traditional financial inclusion as the basis of subsequent research. (2) This paper introduces innovation efficiency in the evaluation of enterprise performance, making the measurement more scientific. (3) This paper compares and explores the influencing mechanism of traditional and digital financial inclusion, by introducing factors such as the innovation cycle and moral hazard, which also enrich and supplement the previous research. (4) Based on theoretical and empirical research, this paper puts forward policy recommendations for the development of financial inclusion, innovation-driven corporations, and financial supervision.

Literature Review

Traditional Financial Inclusion

Financial institutions play important roles in fund allocation in a market economy. However, the scarcity of funds makes it inevitable that disadvantaged groups might be excluded from the financial system. Therefore, the concept of financial inclusion was first proposed by the United Nations in 2005 in their promotion for the International Year of Microcredit. It refers to the provision of appropriate and effective financial services at an affordable cost to all social strata and groups in need of financial services, with small and micro enterprises, farmers, urban low-income groups, and other vulnerable groups as its key service targets. Both traditional and digital financial inclusion mentioned in this paper fall within the ambit of financial inclusion, but they are divided into traditional and digital according to the different stages and forms of financial inclusion development. Financial inclusion has become an important financial development strategy in many countries. So far, scholars have studied financial inclusion from different perspectives, with the following as the main ones:

First, the financial inclusion index system and measurement were constructed. Beck et al. (2007) measured the degree of financial inclusion development in terms of accessibility and usage of banking institutions’ services. Sarma (2008) added another dimension, the penetration of financial services, to the index measurement and proposed the Inclusive Financial Development Index (IFI), which is widely used. Arora (2010) further used 20 indicators in the index measurement, including financial service coverage, transaction convenience, transaction costs, etc. Demirguc-Kunt and Klapper (2012) provided the first analysis of the Global Financial Inclusion Database, a new set of indicators that measure how adults in 148 economies save, borrow, pay, and manage risk. Chakravarty and Pal (2013) developed an axiomatic measure of financial inclusion and examined the effects of major banking policies on financial inclusion across states in India. Based on banking sector data, Wang and Hu (2013) selected six specific indicators to construct an index from two dimensions (the scope and use of financial services). Jiao et al. (2015) adopted the analytic hierarchy process to measure China’s financial inclusion in three dimensions (the quality, usage, and availability of financial services) and 19 indicators.

Second, the influencing factors of financial inclusion were figured out. Bold et al. (2012) and Claessens (2006) concluded that financial demand and supply have a significant impact on inclusiveness. Based on social and environmental factors, Boulton et al. (2007) and Arora (2012) found that the income gap and urbanization level both had an impact on financial inclusion. Liaqat et al. (2022) investigated how national culture affected financial inclusion, finding that Hofstede’s cultural dimensions are associated with financial inclusion in different signs and levels of magnitude.

Third, the influence of financial inclusion was explored. There are findings mainly about economic growth and poverty reduction. Singh and Stakic (2021) found that financial inclusion had a positive effect on economic growth in SAARC countries. Emara and El Said (2021) obtained similar results in MENA countries and found that countries with low levels of financial access services benefit the most from an improvement in governance. As for the poverty reduction effect, Park and Mercado (2016) took the urban-rural income gap as an indicator to measure poverty and concluded that financial inclusion can significantly alleviate it. Koomson and Danquah (2021) examined the effect of financial inclusion on energy poverty using data from Ghana, finding that improvement in financial inclusion is likely to have a reducing effect. Most of China’s scholars used the Gini coefficient or the ratio of the wealth gap to measure poverty reduction. Ma and Du (2017) selected household consumption levels to measure and confirmed the positive impact of financial inclusion on poverty alleviation. Lu and Zhang (2017) used the poverty headcount ratio to measure and tested the poverty reduction effect of financial inclusion in China.

Digital Financial Inclusion

Digital financial inclusion appeared when the development of financial inclusion reached a certain stage and it could improve the performance of financial exclusion.

Therefore, scholars turned to digital financial inclusion by mainly focusing on these topics: the construction of the index system and the index measurement. Most scholars currently do not have a clear definition of digital financial inclusion. For example, Jain et al. (2021) thought that digital financial inclusion was making financial services accessible through technology intervention, that is, via the Internet, mobile networks, cards, and digital wallets. Some studies have elaborated on its role in financial inclusion by introducing Fintech. Joia and Cordeiro (2021) investigated the potential of Fintech to promote financial inclusion in emerging markets. Using Brazil as an example, they identified three domains related to Fintech. However, there are relatively few studies on the measurement of the indices of digital financial inclusion. Banna et al. (2022) developed an index to measure FinFI, which is like digital financial inclusion. “Digital Financial Inclusion Indexes” (Guo et al., 2020), which were jointly calculated by the Digital Finance Research Center of Peking University and Ant Financial Services, are widely used by scholars in China now. There are three dimensions: coverage breadth, usage depth, and digitization level.

As for the study on the effect of digital financial inclusion, Song (2017) tested that it could narrow the urban-rural income gap. Luo and Zhang (2021) used prefecture-level data to empirically test promotion mechanisms from both direct and indirect aspects and revealed that digital financial inclusion could promote resident entrepreneurship with regional heterogeneity. Alt et al. (2018) pointed out that digital financial inclusion had an important impact on the traditional banking industry, while Qiu et al. (2018) believed that digital financial inclusion increased the operating risk of the traditional banking industry and reduced its profitability. Pramanik et al. (2019) believed that digital financial inclusion promoted the digital transformation of the traditional banking industry. Moreover, digital financial inclusion had positive effects on economic growth (Zhang & Tan, 2019), consumption (Li et al., 2020), urbanization (Zhang et al., 2020), etc. Liu et al. (2021) introduced the level of Internet development as a threshold variable and found that promoting SMEs’ entrepreneurship and stimulating residents’ consumption are two important channels for affecting economic growth.

Promoting Enterprise Innovation

Improving the innovation ability of enterprises is the key to achieving high-quality economic development. Therefore, how to effectively stimulate enterprise innovation has become a common concern of academia and decision-makers. The current study mainly focused on three mechanisms for promoting enterprise innovation.

The first is the capital input perspective. Chen et al. (2017) found that venture capital had a significant promoting effect on the innovation activities of invested enterprises. Their further research found that venture capital influenced enterprise innovation mainly through introducing R&D talents and providing industry experience and resources to increase the number of patents and further stimulate innovation. The second is the investment perspective, which is promoting innovation by increasing enterprise R&D investment. Liu et al. (2020) studied the impact of tax incentives on enterprise innovation from a business life cycle perspective. The results showed that tax incentives significantly promoted enterprise R&D investment and in turn innovation ability. The third is from the perspective of innovation efficiency. Wang and Zhang (2020) included both enterprise innovation input and output and measured the innovation ability by the “speed” rather than the “amount” of enterprise innovation. They found that the executive compensation gap had a significant negative impact on innovation efficiency.

Financial Inclusion and Enterprise Innovation

Scholars have rarely studied the impact of traditional financial inclusion on enterprise innovation. The research on the impact of digital financial inclusion is also limited and innovation efficiency is not considered. Charfeddine and Zaouali (2022) investigated the role of financial inclusion and the institutional environment in promoting entrepreneurship. They found that both indicators positively affect early-stage and established firms. Most scholars in China believed that digital financial inclusion had a positive effect on enterprise innovation, among which the important intermediary factor was financing constraints. Ren (2020) found that digital financial inclusion could increase the cash flow of enterprises and reduce their financial expenses and leverage ratio, thereby alleviating financing constraints. Wan et al. (2020) concluded that corporate financing constraints had a significant intermediary effect on the impact of digital financial inclusion on enterprise innovation. These studies indicated that when the financing constraint was eased, the innovation vitality of enterprises could be stimulated.

By observing the two stages of innovation (R&D and the commercialization of results), Wu and Zhu (2021) studied the direct and indirect impacts of digital financial inclusion on enterprise innovation. In addition, scholars have also studied the intermediary effect of government tax rebates, corporate leverage, risk stability, and financial supervision. For example, Liang and Zhang (2019) found digital financial inclusion promoted enterprise innovation by reducing the debt costs for small and medium-sized companies.

Based on existing literature, we constructed a new traditional financial inclusion index and used Peking University’s digital financial inclusion index. Then we measured the degree of enterprise innovation by output and efficiency respectively, followed by the mechanism analysis and hypotheses. Furthermore, there are empirical tests for the hypotheses, as well as endogeneity tests, heterogeneity tests, and further analysis. Finally, some suggestions are available for enterprises and decision-makers to better enhance their innovation ability.

Research Model and Development of Hypotheses

Measurement of the Development of Financial Inclusion

At present, there is no unified way to measure traditional financial inclusion. Scholars usually select different indicators to measure for specific research purposes. Therefore, we refer to the evaluation index system proposed by Global Partnership for Financial Inclusion (GPFI), a rather authoritative international organization, and consider the rationality of indicators and data availability, selecting two dimensions (the availability and the use of financial services) to measure traditional financial inclusion.

The availability of financial services refers to the breadth of financial services. From the perspective of supply, there are eight typical indicators that could be representatives, in terms of geography and population respectively (Table 1). Particularly, microfinance companies play a very important role in the development of financial inclusion by meeting the financing needs of vulnerable groups, so relevant indicators are included. The usage of financial services means the depth of financial services. We selected six indicators mainly from the perspective of demand to indicate the degree of use of financial services. Related indicators of the insurance industry were also added, thereby making the measurement of traditional financial inclusion more complete.

The Evaluation System of Traditional Financial Inclusion Index.

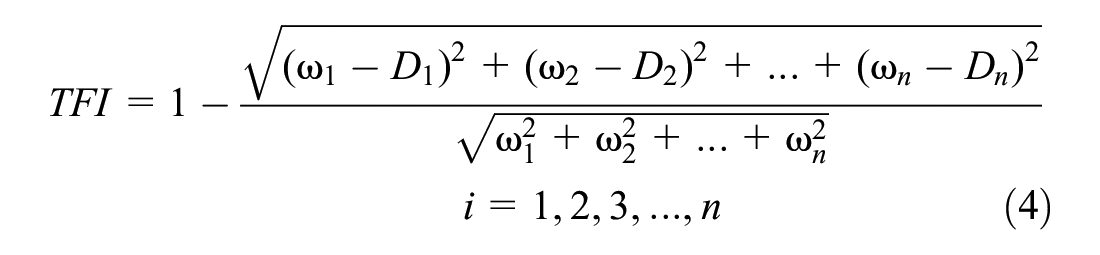

We used the method proposed by Sarma (2008) to measure the development level of traditional financial inclusion in China. Due to the disunity of the dimensions of different indicators, the coefficient of variation method was employed to determine the weight of each indicator, so that the calculation was more objective and accurate. The coefficient of variation (

The formula of the weight of each indicator (

Then the formula for calculating the value of each indicator of financial inclusion under the unified dimension is as follows:

Among them,

The larger the value of Di, the larger the value of TFI, that is, higher degree of inclusiveness. Since some prefecture-level data were not available, traditional financial inclusion indexes of 31 provinces were calculated from 2011 to 2018 and divided by region.

China’s development level of traditional financial inclusion has improved steadily in recent years, and the development trend of most provinces is consistent, decreasing slightly in 2013 and 2014, and then exhibiting an upward trend. From a horizontal comparison, the regional characteristic is “higher in the east, second in the middle, and lower in the west.” The development level in the eastern region is significantly higher than the national average, while the indexes of central and western regions are lower, both less than 0.1. Therefore, these two regions are still at a relatively low level and have great potential for development.

As for the measurement of digital financial inclusion, there are few methods documented in the literature. Most scholars used the index jointly released by the Digital Finance Research Center of Peking University and Ant Financial Services. Therefore, we also used it as the measurement and selected the prefecture-level data from 2011 to 2018. This index was constructed from three dimensions: coverage breadth, usage depth, and digitization level. The first described the number of people using electronic accounts, reflecting the financial environment of the region; the second revealed the degree of use of digital financial services, reflecting the ability of financial services in the region; and the third reflected the transaction cost and efficiency of digital finance in the region.

According to the calculation results, the development of digital financial inclusion in all provinces (cities) from 2011 to 2018 presented an obvious increasing trend and fast progressing speed. In addition, similar to traditional financial inclusion, the development of digital financial inclusion also revealed the same regional difference, but this difference is gradually narrowing, indicating that digital financial inclusion has undergone greater development in recent years.

Financial Inclusion and Enterprise Innovation Output

The core principle of financial inclusion is the establishment of a financial ecosystem to include neglected SMEs and disadvantaged groups. It can alleviate financial exclusion to a certain extent. At present, there are still relatively fewer financial services for emerging technology-based enterprises and SMEs. These enterprises suffer from the problems of limited financing channels, high financing costs, insufficient funds for innovation activities, and the lack of R&D motivation, then consequently inhibiting innovation capabilities (Li & Zhong, 2015). With the emergence of financial inclusion, the financing constraints of enterprises could be eased, which has improved their innovation output capacity.

The prominent indicator of financial inclusion’s impact on enterprise innovation ability is innovation output. Most existing studies used the total number of annual patent applications of the enterprise to measure it (Chen et al., 2017; Liang & Zhang, 2019; Wan et al., 2020). Financial inclusion can alleviate the financing constraints of enterprises by reducing financing costs, broadening financing channels, and improving financing efficiency, thereby promoting enterprises to increase their innovation output.

Traditional financial inclusion’s promotion on enterprise innovation output is mainly realized through two channels: firstly, with the introduction of relevant targeted RRR (reserve requirement ratio) cuts, financial institutions are required to provide long-term funds for enterprises, especially SMEs. Second, the proposal of financial inclusion has made the financial system more inclusive and provided more financial products for enterprises, which is conducive to enriching the financing sources of enterprises.

At the same time, digital financial inclusion in recent years has provided new methods for solving the financing problems of enterprises and promoted enterprise innovation. Gong (2013) believed that digital financial inclusion used the online transaction platform, which cost no resource expenditure in the transmission process. The information collection became more efficient and the information cost of the enterprise was effectively reduced. Liang and Liu (2019) proposed diversified financing channels, such as “financial supermarkets” and supply chain finance, which made up for the deficiency of traditional financial inclusion and effectively reduced the financing constraints faced by enterprises. At the same time, it could collect customers’ credit data in a timely, fast and efficient manner, which helped to improve the service quality and the allocation efficiency of credit funds (Liang & Zhang, 2018). Therefore, compared with traditional finance, digital financial inclusion is more efficient in reducing financing costs, broadening financing channels, and improving financing efficiency by using digital technology. Therefore, it eased the financing constraints of enterprise innovation and provided financial support for enterprise innovation output.

Although both traditional and digital financial inclusion have mechanisms to promote enterprise innovation output, in comparison, traditional financial inclusion may be inferior to digital financial inclusion in terms of using big data to deal with moral hazards. Some phenomena existing in China’s economic development may inhibit the positive effect of traditional financial inclusion on the innovation output of enterprises. Specifically, it can be observed from the following two aspects.

First, the funds generated by traditional financial inclusion may be used in financialization but not innovative activities. From 2011 to 2018, China’s real estate prices rose continually, attracting a large number of enterprises to invest capital in the real estate market. Wang and Rong (2014) found that the faster housing prices rose, the weaker the tendency of local industrial enterprises to develop new products. The reason is that the rate of return that enterprises could realize from investing in real estate was higher than that of enterprise innovation output. Therefore, although the development of traditional financial inclusion has reduced the financing constraints of enterprises, it is still difficult to prevent moral hazard problems. Enterprises have incentives to embezzle bank loans to invest in the real estate market, instead of using them for innovation investment.

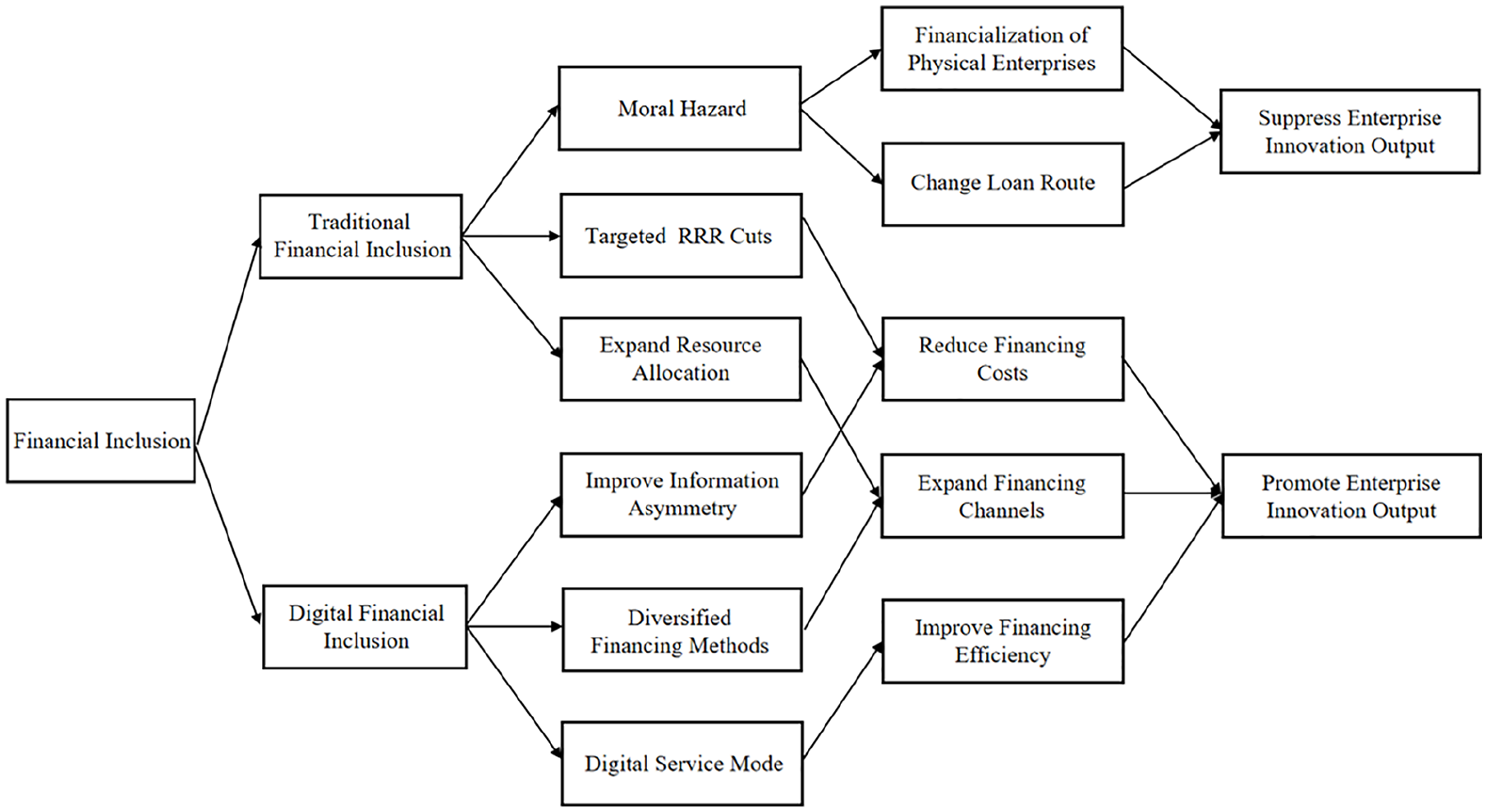

Second, enterprises reduce innovation activities to obtain bank loans, which will also cause traditional financial inclusion to inhibit innovation output. Enterprise loans need to be approved by the bank’s credit department. If an enterprise applies for a loan for R&D investment, it will usually be considered risky and even be rejected by the bank. Therefore, enterprises may obtain funds by reducing the amount of R&D investment in loans, which is manifested in the inhibitory effect of traditional financial inclusion on enterprise innovation. On the contrary, digital financial inclusion has characteristics of a small financing amount, low financing threshold, and traceable fund destination. Therefore, such moral hazards can be better avoided, and enterprises can more effectively expand their R&D investment through financing, thereby increasing investment and capabilities in R&D, which will ultimately increase innovation output (Figure 2).

Based on the above analysis, we predict the following hypothesis regarding innovation output:

Hypothesis 1 (H1): Compared with traditional financial inclusion, digital financial inclusion is more likely to exert a positive effect on enterprise innovation output.

The mechanism of financial inclusion’s impact on the enterprise innovation output.

Financial Inclusion and Enterprise Innovation Efficiency

Innovation needs to go through a long period, so it is limited to measuring an enterprise’s innovation ability by output alone (Wang & Zhang, 2020). Therefore, this paper draws on innovation efficiency as another measuring indicator, which is the ratio of innovation output to R&D input over time. It considers the input cost and uses the “relative level” of enterprise innovation rather than the “absolute level” to measure the capability so that the research can be more scientific and comprehensive. Moreover, innovation activities undergo dynamic progress, and it takes a long process from the initial investment to the final result. Therefore, innovation efficiency can better measure innovation capability in each stage.

The influencing mechanism of financial inclusion on innovation efficiency is different from that on innovation output. This can be explained by enterprise innovation input’s impact on innovation output before and after the proposal of financial inclusion.

Generally speaking, the innovation activities of enterprises are similar to those of organisms, and they also have a longer life cycle (Chen et al., 2015). It takes a period of time to progress from R&D investment to the realization of innovation output, so the overall innovation results usually lag behind the R&D investment, especially in the early stage of innovation (Malamud & Zucchi, 2019). Therefore, innovation efficiency may go through a process of decline and then increase (Figure 3). However, the proposal for financial inclusion could accelerate this process. With the introduction and development of financial inclusion, both traditional and digital financial inclusion are alleviating financing constraints, enabling enterprises to have more funds for R&D investment. But despite this, the necessary time constraint for innovation is still unavoidable, so the lag between innovation output and R&D investment remains to a certain extent. In Figure 3, we simplify the whole cycle of innovation and divide it into two stages, separated by the vertical dotted line. In addition, to compare the status with and without financial inclusion, there are two pairs of lines to trace the funds’ input and innovation output.

The innovation cycle before and after the proposal of financial inclusion.

For the status before the proposal of financial inclusion, the R&D investment is at a lower level (dotted line) and has a slower rate of increase in the first stage. Along with the accumulation of R&D investments, the flow of funds begins to decrease after the peak in the second stage. At the same time, there begins to have innovation output after enough time lag. As innovation output increases, the turning point A comes when enterprises can finally enjoy higher innovation efficiency.

The status will improve after the proposal of financial inclusion. Because of its help, it is possible to have more funds input, especially in the early stage. Therefore, we could have a higher solid curve now. However, the change in innovation output is still small in the first stage. As a result, the efficiency of innovation will decline more significantly, which makes financial inclusion have an inhibitory effect. However, such an effect does not mean that the development of enterprises is hurt. On the contrary, early financial inclusion helps enterprises make a large amount of R&D investment, which will save resources for the continuous innovation and development of enterprises, accelerate the innovation process of enterprises, and make enterprises enter an upward cycle of innovation efficiency earlier and reach the turning point (A’) ahead of the original schedule (A) (Figure 3).

Based on the above analysis, we predict the following hypothesis regarding innovation efficiency:

Hypothesis 2 (H2): We are now still in the early stage in which the development of traditional and digital financial inclusion has a restraining effect on enterprise innovation efficiency.

Research Methodology

Variables

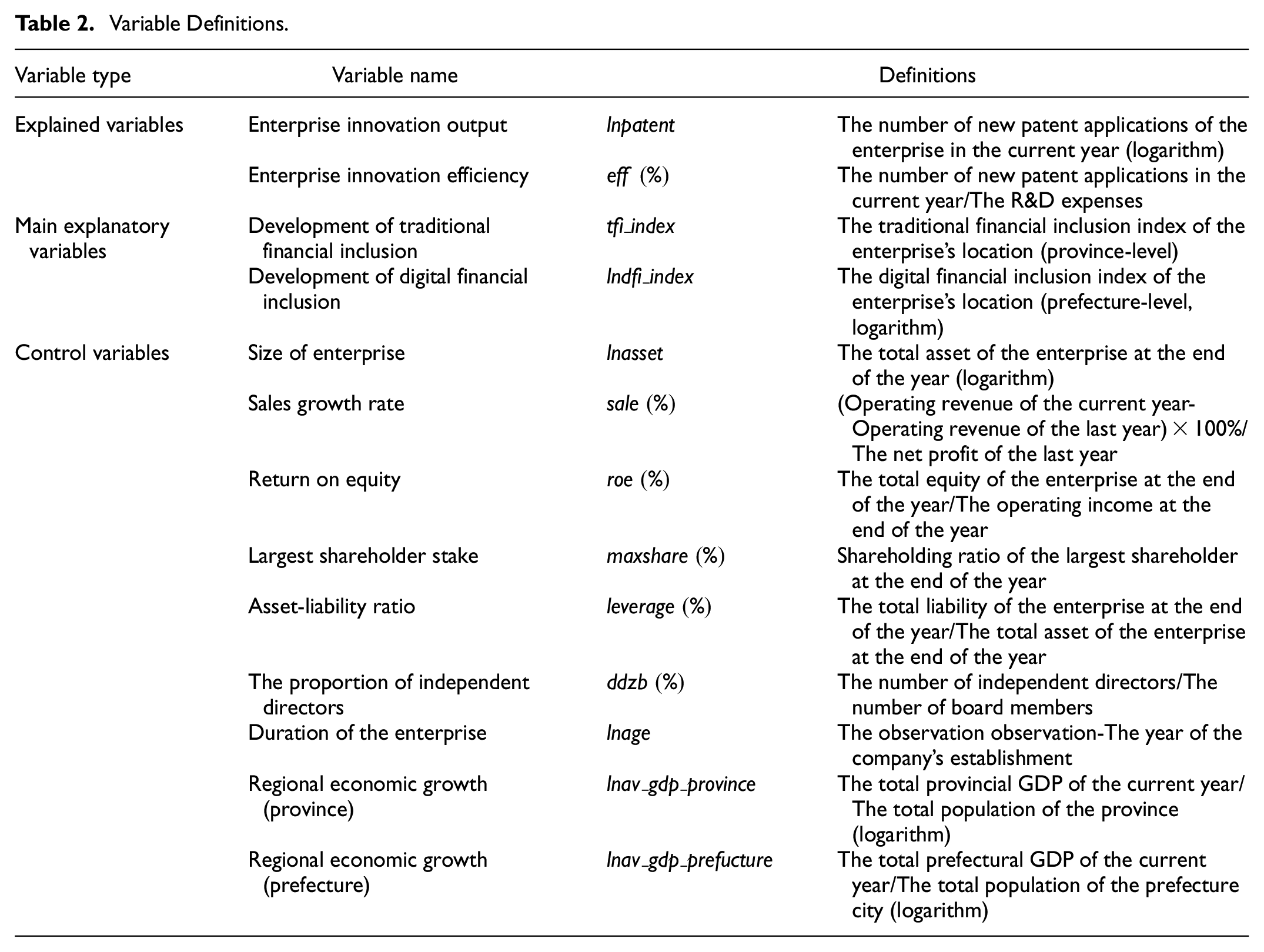

By referring to the existing literature, we used the total number of patent applications of enterprises as an indicator (logarithm) for the innovation output (

The explanatory variables are the traditional financial inclusion index (

Besides, enterprise innovation is also affected by a variety of factors at the micro-level of enterprises and regional factors. We selected the most influential factors as enterprise-level control variables, including the size of the enterprise (logarithm) (

Variable Definitions.

Data

The data for calculating the traditional financial inclusion index mainly came from Financial Operation Report of the 31 provinces (cities) from 2011 to 2018, the National Bureau of Statistics, the People’s Bank of China, and the Wind database. Digital financial inclusion data came from Peking University’s Digital Financial Inclusion Index. The control variables data were from the Wind database. We selected panel data of China’s A-share listed companies from 2011 to 2018. Enterprise innovation data were from CCER China Economic and Financial Database and CSMAR database. We combine three types of data and obtain a set of panel data of 268 prefecture-level cities in China from 2011 to 2018.

Then the data were processed as follows: (1) Exclude companies from the financial sector. (2) Exclude companies prefixed with ST for three consecutive years. In addition, to eliminate the influence of extreme values, the data of the main continuous variables below 1% and above 99% were winsorized. Eventually, 3,908 samples were constructed, and the total observations of patent applications and innovation efficiency were 14,789 and 9,030 respectively.

Table 3 shows the descriptive statistical results of the major variables. In the full sample, the standard deviation of

Statistical Description.

Regression Models

For the research, the following econometric models were constructed respectively:

Among them, the explained variable

Results

Testing of Hypotheses

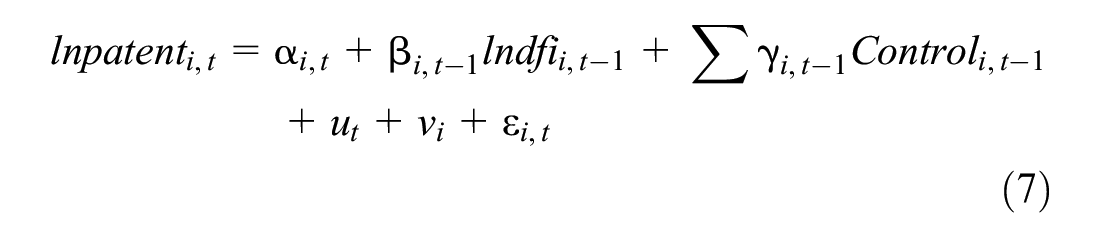

In Table 4, model (1) reports a negative coefficient of the traditional financial inclusion index at the 1% significance level, indicating its significant inhibiting effect on the innovation output of enterprises. In model (2) the coefficient of the digital financial inclusion index is positive at the 5% significance level, indicating a significant promoting effect on enterprise innovation output, which is consistent with H1. Models (3) and (4) respectively verify the impact of traditional and digital financial inclusion on the innovation efficiency of enterprises. The coefficient of the former is negative at the 1% significance level and the latter is negative at the 10% significance level, revealing that the development of financial inclusion during the observation period is still at the stage of restraining the efficiency of enterprise innovation, so H2 is confirmed. Our results for digital financial inclusion are consistent with those of the previous study. And we originally show the results for traditional financial inclusion’s influence on enterprise innovation, which is a supplement to the existing literature. In addition, our results add innovation efficiency into consideration, which contributes to the previous study which mainly focused on innovation output.

The Impact of Financial Inclusion Indexes on Enterprise Innovation.

Note. The robust standard errors are in parentheses.

represent the significance level of 1%.**represent the significance level of 5%. *represent the significance level of 10%.

To verify the different impact of the two types of financial inclusion, we incorporated traditional financial inclusion and digital financial inclusion into one prefecture-level model (for traditional financial inclusion, the indexes of each prefecture city under the same province are the same). Model (5) presents the result of the impact of two kinds of financial inclusion on innovation output. The coefficient of traditional financial inclusion is negative at the 1% significance level and the coefficient of digital financial inclusion is positive at the 1% significance level. Model (6) shows the result of the impact of two kinds of financial inclusion on innovation efficiency. The coefficient of traditional financial inclusion is negative at the 10% significance level and the coefficient of digital financial inclusion is positive at the 5% significance level. Since the signs of the two types of financial inclusion in both innovation models are consistent with the results shown in models (1)−(4), our results in the previous four models are proved to be accurate and convincing.

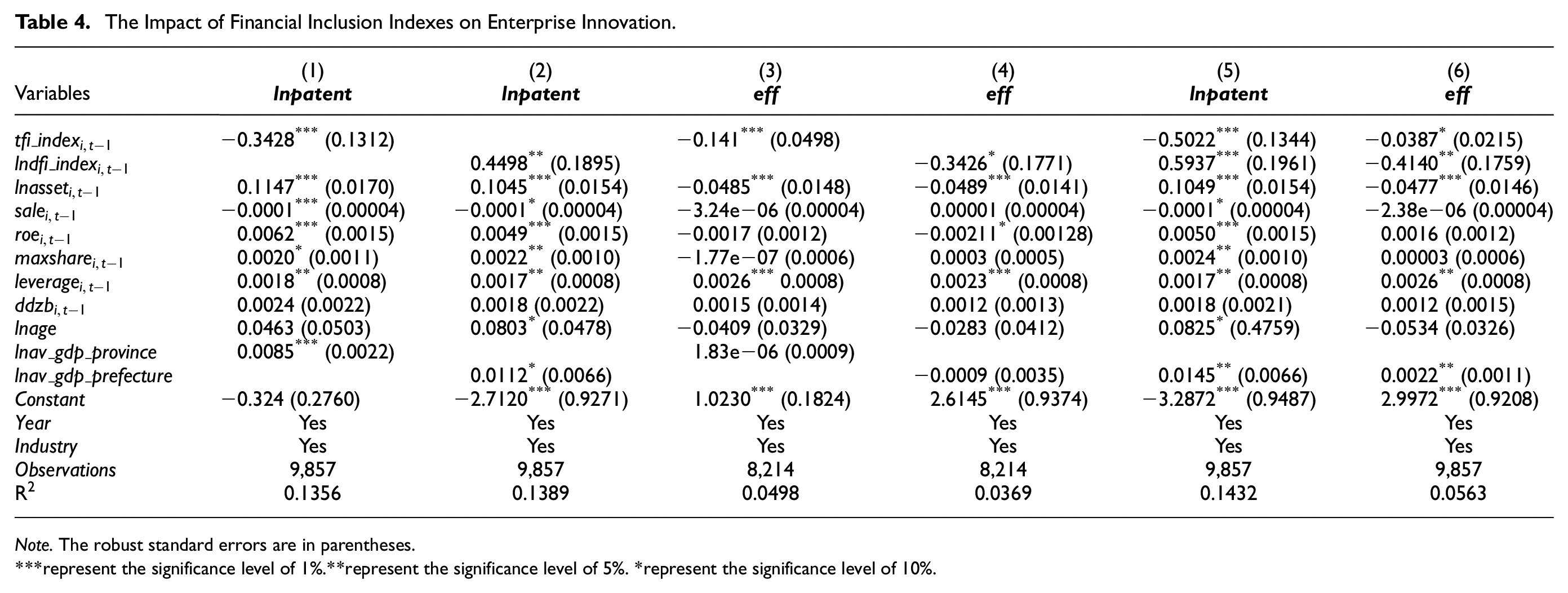

Endogeneity Test

We used a first-order lag of the core explanatory variables to reduce the endogenous problem caused by reverse causality as much as possible. But there might still be endogeneity biases in the regression, such as missing variables. Thus, we referred to the research of Li and Li (2020) and Fu and Huang (2018) and adopted the two-stage instrumental variable method. For traditional and digital financial inclusion, the “bank data during the period of the Republic of China” (the total number of headquarters and branches in each province or city in 1934, logarithm) and the “distance from each prefecture-level city to Hangzhou” (logarithm) were selected as instrument variables respectively to conduct endogeneity tests. The former choice was mainly made because regions with a large number of banks during the period of the Republic of China were more economically developed, and these regions still maintain a relatively high level of development nowadays; however, the number of banks of that period does not affect enterprise innovation. The latter was chosen mainly out of concern of the digital financial inclusion data used in this paper coming from Ant Financial Service, a company whose headquarters are based in Hangzhou. So, the development of digital financial inclusion in different cities may be related to their distance from Hangzhou, but the distance from the enterprise’s location to Hangzhou does not affect the enterprise’s innovation. Therefore, the above two instrument variables both meet the requirements of correlation and exogeneity.

Table 5 shows the regression results. The results of the first stage show that the minimum eigenvalue statistics of both financial inclusion indexes are greater than the critical value of 10, thus the null hypothesis of the existence of weak instrument variables is rejected. Moreover, it can be seen that the distance from Hangzhou has a significant negative correlation with digital financial inclusion at the 1% significance level, indicating its significant negative impact on digital financial inclusion. The number of banks has a significant positive correlation with traditional financial inclusion at the 1% significance level, showing its significant positive impact on traditional financial inclusion. The second-stage results show that, after adding instrument variables, the sign and significance of the coefficient of each variable did not change significantly, which proves the reliability of the empirical results.

Endogeneity Check (2SLS Instrument Variable Method).

Note. The robust standard errors are in parentheses.

represent the significance level of 1%. **represent the significance level of 5%. *represent the significance level of 10%.

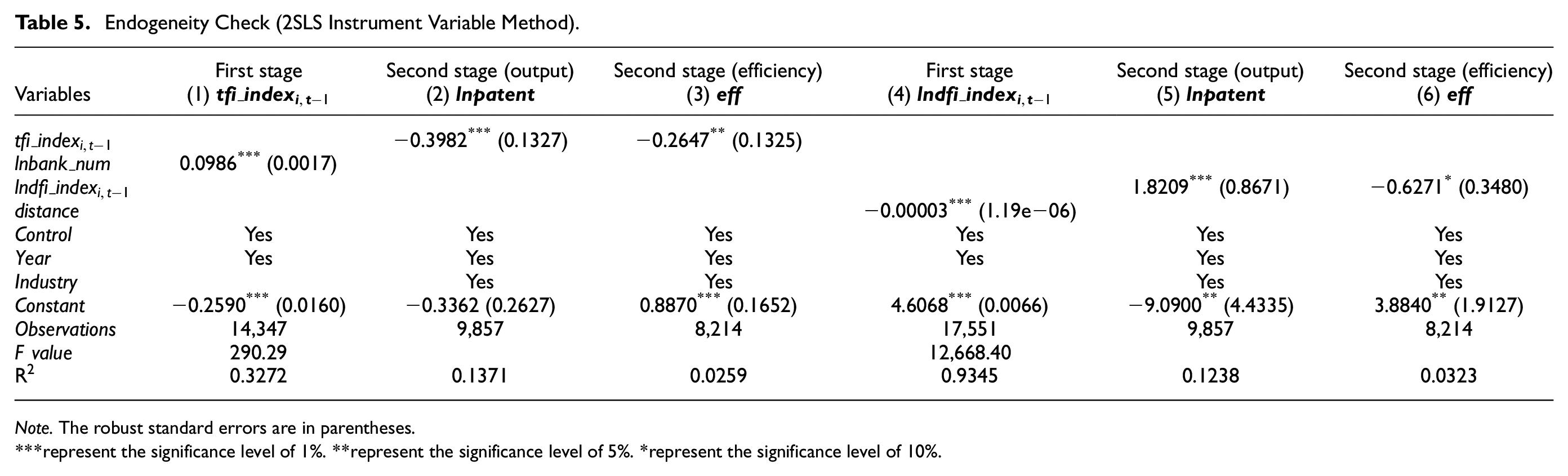

Robustness Test

Three methods were used to test the robustness of the model. First, patents can be divided into three categories: invention patents, utility model patents, and design patents, among which invention patents have the characteristics of providing new technical solutions and can best reflect the innovation ability of enterprises. Therefore, we further used the number of invention patent applications of enterprises (logarithm) as the explained variable and conducted a robustness check on the baseline regression. Columns (1) and (2) of Table 6 show the impact of the two types of financial inclusion on the number of invention patent applications of enterprises. The regression coefficient of digital financial inclusion is 0.2670, and that of traditional financial inclusion is −0.2575, both of which are significant, indicating the positive effect of digital financial inclusion and the negative one of traditional financial inclusion. This conclusion is consistent with the regression results of the baseline model.

Robustness Check.

Note. The robust standard errors are in parentheses.

represent the significance level of 1%. **represent the significance level of 5%. *represent the significance level of 10%.

Second, by referring to Zhou and Zhang (2016), we constructed models (9) and (10) to measure the impact of financial inclusion on enterprise innovation efficiency:

In the models, the cross-multiplication coefficients reflect the change of enterprise innovation efficiency. A significantly positive one indicates the improvement effect of financial inclusion on innovation efficiency, and vice versa. Columns (3) and (4) show that the coefficients of the two types of financial inclusion are both negative and significant at the level of 1%, indicating that both types of financial inclusion hurt the innovation efficiency of enterprises. The results are consistent with the conclusions drawn above.

Finally, we used a different measurement method, the principal component analysis method, to construct the traditional financial inclusion index (

Based on the conclusions of the above three methods, we can say that the results reported in this paper are robust.

Discussion

Hypothesis 1 proposes that the effect of traditional financial inclusion on the innovation output of enterprises is uncertain and may even be negative. The test result is significantly negative, indicating that traditional financial inclusion has a more restraining effect on innovation output. The analysis in the previous parts has been confirmed by practice.

Under traditional financial inclusion, it is difficult to control the moral hazard of enterprises with the help of big data and/or other technological methods. In addition, due to the continued enthusiasm of the real estate market over the same period, enterprises were more likely to pursue financialization, that is, to use bank loans in the real estate market instead of innovation, resulting in a decline in the innovation output. Furthermore, innovation activities are usually considered high-risk activities, so the loan provision standard for R&D investment is still quite demanding under traditional financial inclusion. Thus, enterprises will reduce their innovation activities to obtain bank loans, which may also result in the inhibitory effect of traditional financial inclusion on the innovation output of enterprises.

Digital financial inclusion can largely resist the above risks. Due to its features such as the traceability of funds, it is difficult for enterprises to move funds to real estate investment. It is also not subject to a strict approval system like that in bank loan channels, so R&D investment can be expanded through financing, thereby strengthening the R&D capability and promoting innovation output.

Meanwhile, we found that there is a certain lag between the innovation output and R&D investment of enterprises. With the introduction and development of financial inclusion, more enterprises have been covered by financial inclusion services, and have obtained financing support and then used the funds for R&D, which has eased the problem of financing constraints to a certain extent, but there is still a situation that inhibits enterprise innovation efficiency in the early stages of financial inclusion development. However, it is this effect in the early stage that makes a solid foundation for the improvement of innovation efficiency in the later stage: based on the accumulation, with the advancement of the innovation cycle, the enterprise can finally realize an increase in innovation output ahead of time, and enter a stage of continuous improvement in innovation efficiency.

Further Analysis

Since enterprises are very diversified in different features which might affect their innovation ability, we further explore the impacts on enterprises of different sizes and ownership.

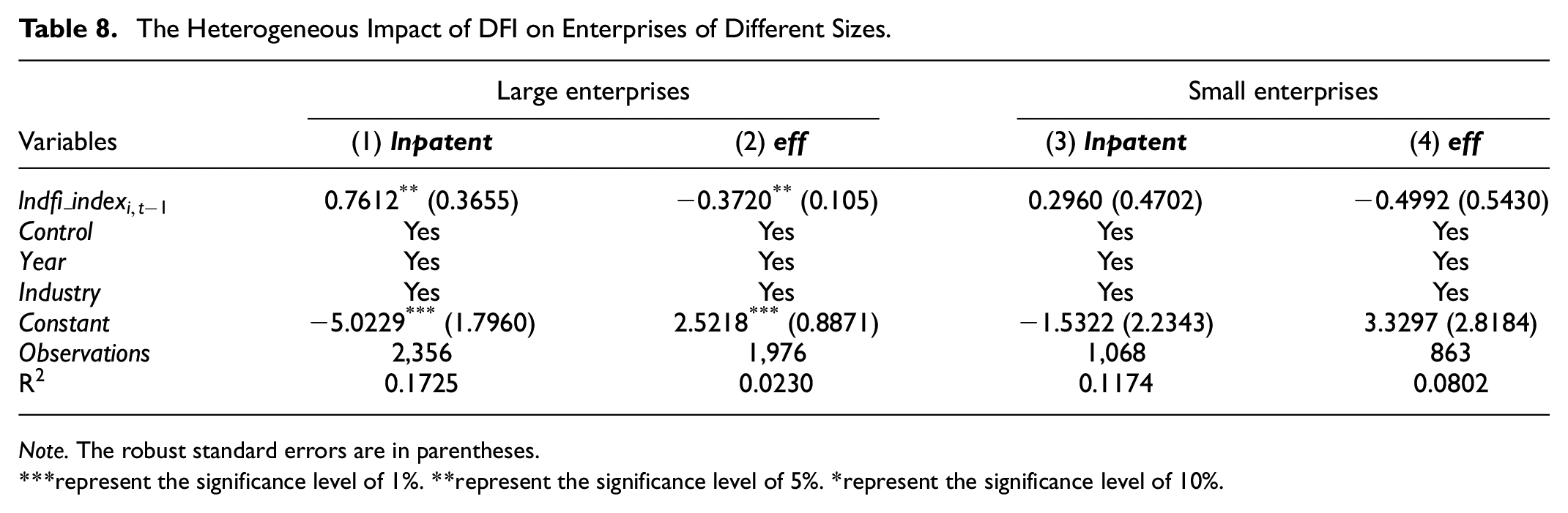

Enterprises of Different Sizes

The sample companies were grouped into three according to the one-fourth and three-fourths quantiles of their assets. Large enterprises mean above the three-fourths quantile, while those below the one-fourth quantile are small ones. The empirical tests of the two types are constructed respectively.

By comparing columns (1) and (3) in Table 7, we can see that the inhibitory effect of traditional financial inclusion on enterprise innovation output is significant for small enterprises, but not significant for large enterprises. By comparing columns (2) and (4), we can see that traditional financial inclusion has an inhibitory effect on innovation efficiency for both large and small enterprises, and this inhibitory effect is more significant in large enterprises.

The Heterogeneous Impact of TFI on Enterprises of Different Sizes.

Note. The robust standard errors are in parentheses.

represent the significance level of 1%. **represent the significance level of 5%. *represent the significance level of 10%.

According to columns (1) and (3) in Table 8, the effect of digital financial inclusion on innovation output is positive at the 5% significance level for large enterprises, but not significant for small enterprises, which indicates a more significant improvement in the innovation output for large enterprises. Similar results can be found in columns (2) and (4), regarding the effect on innovation efficiency.

The Heterogeneous Impact of DFI on Enterprises of Different Sizes.

Note. The robust standard errors are in parentheses.

represent the significance level of 1%. **represent the significance level of 5%. *represent the significance level of 10%.

The above differences in traditional financial inclusion may be explained by the following two aspects: firstly, small companies are more likely to invest in real estate, which can generate higher and faster income. Thus, they have more incentives to use loans for real estate investment, while reducing R&D investment. Wang et al. (2017) proposed that, compared with companies with strong profitability, companies with weaker profitability faced greater market arbitrage opportunities and lower arbitrage opportunity costs, so their financialization has a bigger inhibitory effect on enterprise innovation. Secondly, small companies have relatively low credit ratings, poor loan repayment ability, and high risks. To obtain loan approval from banks, small companies are more motivated to reduce their innovation input when applying for loans, thereby inhibiting their innovation ability. As for digital financial inclusion, its inhibitory effect on efficiency mainly applies to large companies.

Therefore, we can see that both traditional and digital financial inclusion’s current development has been benefiting large enterprises more, although they are supposed to be more inclined to fund medium, small and micro-enterprises. However, even if the innovation output increases in the early stage of the innovation cycle, there will still be a lag. This is manifested in the inhibition of enterprise innovation efficiency.

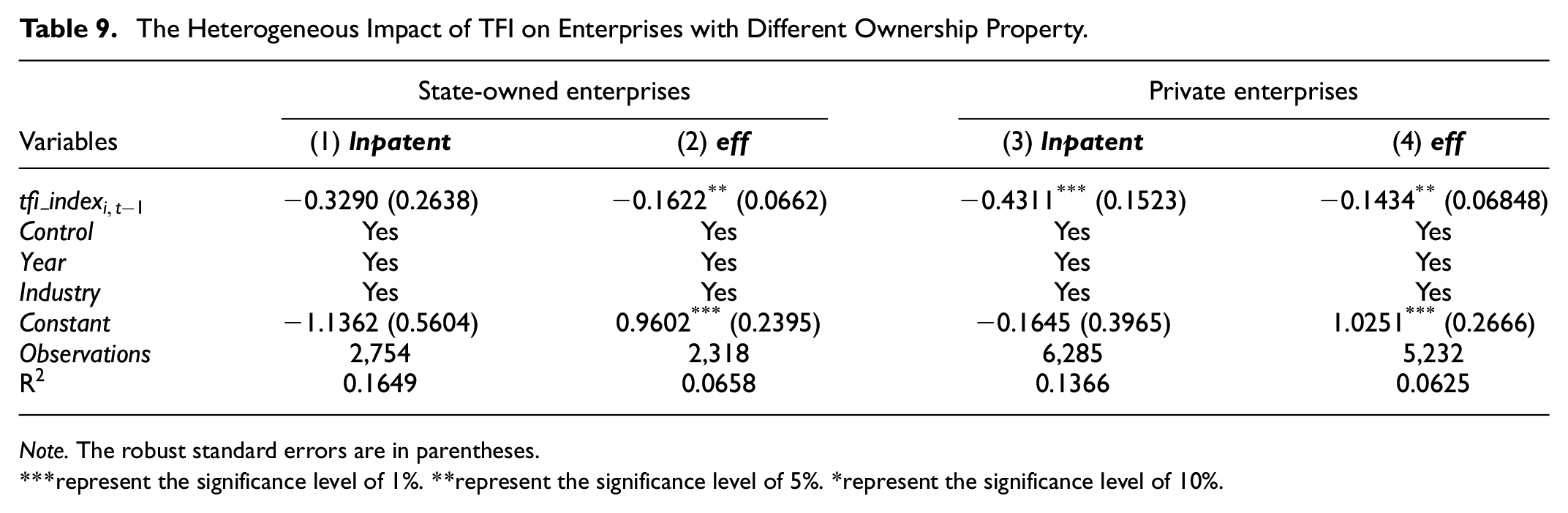

Enterprises of Different Ownership

In China, the feature of ownership varies and plays a crucial role in many fields. According to a survey conducted among more than 2,000 private enterprises funded by the National Social Science Fund Project, as high as 53.8% of enterprises believe that state-owned enterprises have easier access to bank credit and loans than private enterprises (Wang, 2019). Therefore, we divided the samples into state-owned enterprise group and private enterprise group, to figure out the ownership heterogeneity of the impact.

Table 9 shows the heterogeneous impact of traditional financial inclusion. From columns (1) and (3) we can see that the inhibitory effect of traditional financial inclusion on enterprise innovation output is only significant (1% significance level) for private enterprises. The results indicate that traditional financial inclusion mainly restricts the financing channels of private enterprises, and does not substantially impact state-owned enterprises’ financing channels. By comparing columns (2) and (4), it can be found that traditional financial inclusion inhibits the innovation efficiency of both types of enterprises at the significance level of 5%. It can be inferred that traditional financial inclusion mainly restricts the financing channels of private enterprises, thereby inhibiting their innovation output and efficiency.

The Heterogeneous Impact of TFI on Enterprises with Different Ownership Property.

Note. The robust standard errors are in parentheses.

represent the significance level of 1%. **represent the significance level of 5%. *represent the significance level of 10%.

Table 10 shows the heterogeneous impact of digital financial inclusion on the innovation output and efficiency of state-owned enterprises and private enterprises. By comparing columns (1) and (3), it can be seen that the promotion effect of digital financial inclusion on enterprise innovation output is significant (1% significance level) for private enterprises but not significant for state-owned enterprises. The results indicate that digital financial inclusion significantly improves the innovation output of private enterprises. By comparing columns (2) and (4), it can also be found that digital financial inclusion has a significant inhibitory effect on the innovation efficiency of state-owned enterprises at the significance level of 10%. As for private enterprises, this inhibitory effect is not significant.

The Heterogeneous Impact of DFI on Enterprises with Different Ownership Property.

Note. the robust standard errors are in parentheses.

represent the significance level of 1%. **represent the significance level of 5%. *represent the significance level of 10%.

The above different results of traditional financial inclusion may be explained by the following two aspects: first, compared with state-owned enterprises, private enterprises may be more motivated to use bank loans for real estate investment, thereby reducing R&D investment, which leads to an inhibitive effect. Second, the loan approval process of private enterprises is relatively more complicated and demanding; thus private enterprises are more likely to reduce high-risk R&D investment projects to obtain loan approvals, which is reflected in the inhibitory effect of traditional financial inclusion on the innovation of private enterprises. As to digital financial inclusion, it indeed promotes the innovation of private enterprises and improves their financing conditions.

Conclusion

Taking China’s A-share listed companies as samples, we discussed and tested the impact of traditional and digital financial inclusion on enterprise innovation output and efficiency, and further explore the heterogeneous effects for enterprises of different sizes and ownership. The results are as follows.

First, traditional financial inclusion has a significant inhibitory effect on enterprise innovation output, while digital financial inclusion plays a positive role (which is in line with the existing literature). This might be attributed to the financialization of enterprises and the moral hazard of changing the use of loans when enterprises are financed by traditional financial inclusion. Meanwhile, digital financial inclusion monitors the flow of funds through scientific and technological means, and the threshold for financing is even lower. These characteristics can circumvent the shortcomings of traditional financial inclusion.

Second, traditional and digital financial inclusion is still in the stage of restraining the innovation efficiency of enterprises, but this may be the accumulation for the innovation and development of enterprises, thereby accelerating the innovation process of enterprises, and enabling enterprises to enter the rising cycle of innovation efficiency ahead of time.

Third, we examined the heterogeneity effects for enterprises of different sizes and ownership. Traditional financial inclusion mainly restrains the innovation output of small/private enterprises, while digital financial inclusion is more likely to promote the growth of large/private enterprises’ innovation output; the two financial inclusions display a more restraining effect on large enterprises in terms of innovation efficiency.

In addition, we also conducted robustness tests. After changing the measurement methods of the financial inclusion index and innovation variables, the test results showed that the conclusions were still valid and would not be affected by the selection of variables.

Revelation, Limitations, and Future Direction

This paper has studied enterprise innovation from the macro perspectives of traditional and digital financial inclusion and performed further heterogeneity tests, which provide a theoretical reference and practical guidance on the acceleration of digitization, and the support for enterprise innovation.

Firstly, for traditional financial inclusion, while having appropriately relaxed the loan approval for enterprises and promoted the development of “Sci-tech innovation loans,” banks should strengthen their ex-post supervision of loans to ensure that enterprises use loans for innovative R&D investment and prevent business loans from flowing into the housing market. In addition, the inclusiveness of small businesses should be increased. Traditional financial inclusion should make their services more convenient, incorporate and absorb more technology, and particularly providing preferential policies and guidance on the innovation for small enterprises.

Secondly, major efforts should be made to develop digital financial inclusion. While continuing to expand the coverage of digital financial inclusion, we should promote the depth of its use and enable more companies to explore the convenience of digital finance. Meanwhile, digital financing has the advantage of being able to record and query, so that it can better monitor the destination of capital flow and ensure that enterprise loans are used for innovation investment. While developing digital financial inclusion, we must also prevent the financialization of technology enterprises and prevent them from forming a monopoly, to avoid a situation that increases financial leverage and raise loan interest rates that affect the inclusive effect of financial services.

Thirdly, in this paper, the measurement of traditional financial inclusion mainly selected the relevant indicators of traditional financial institutions such as banks, but with the continuous development of digital technology, traditional financial institutions are also constantly introducing digital business and using financial technology to empower the transformation. In the long run, traditional and digital financial inclusion will integrate and eventually run as digital financial inclusion to promote enterprise innovation. But as mentioned above, while enjoying the convenience and efficiency brought by digitalization, we must also guard against the hidden danger of financial risks. Therefore, how to better evaluate and measure digital risks to promote the compliance of financial markets and the in-depth development of financial inclusion is still worth further exploration.

Fourthly, this paper has made a marginal contribution to the field of financial inclusion. Compared with research in other countries, which has mainly focused on traditional financial inclusion without a comprehensive index to measure digital financial inclusion, we first build the relationship between traditional and digital financial inclusion and verified their different effect on enterprise innovation. Providing the example of financial inclusion in China, we are looking forward to the construction of digital financial inclusion index in other countries so that research on financial inclusion can be enriched.

Finally, due to the difficulty of observing the decision-making behavior against the innovation of enterprises and the lack of illegal loan data, we could not verify the function of the two mechanisms of how traditional financial inclusion affects enterprise innovation. This is the shortcoming of this paper, which can be explored later.

Footnotes

Availability of Data and Material

The data set supporting the conclusions of this paper is available upon request.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is supported by the project 2022SYLZD001. (BFSU Double First-Class Major Signature Research: Post-Pandemic Globalization Risk: A Financial Security and Business Risk Perspective).