Abstract

The study aims to examine the presence of gender difference in Digital Financial Inclusion of Indian bankers reflected through Gender Digital Divide. UTAUT2 model was adopted to examine the Behavioral Intention of bankers to adopt Digital Banking. Structured questionnaires framed on 5-point Likert scale were distributed among 300 bankers, selected through random sampling, and received 260 completed questionnaires. Statistical data analysis was done using PLS-SEM. Findings reveal that five out of the eight UTAUT2 factors (Perceived Usefulness, Social Influence, Hedonic Motivation, Habit, and Price Value) have significant roles for men and three have significant roles for women (Perceived Ease of Use, Personal Innovativeness, and Facilitating Conditions). Research indicates that women are trailing behind in the use of digital banking, which is concerning because their internet banking adoption and usage can motivate other women to use digital media, thereby raising their Financial Inclusion level.

Keywords

Introduction

According to Khera et al. (2022), Digital Financial Inclusion (DFI) is the “fintech-enabled financial inclusion” in which mobile phones or computer devices are important players. Banks are facilitating DFI among clients by providing financial services through technical modes such as ATMs, Internet Banking, and Mobile Banking. These services are bundled and renamed “Digital Banking” (DB), which connect rural areas with cutting-edge technology to achieve DFI. The dynamics of the technology and economic environments force banks to undergo digital transformation to preserve their operational efficiency. According to Kitsios et al. (2021), digital transformation not only brings new services, but also lowers branch costs that would have been incurred for physical branch setup and staffing. Currently, the banking industry is significantly reliant on Information and Technology (IT) infrastructure to increase its profitability. Not only private banks, but even state-owned banks, have begun to move toward digitalization of banking products to survive. Furthermore, customer service is the focus of banks to increase profits and connect people with DB platforms. Shukla and Singh (2014) emphasized the importance of bank employees in motivating customers to adopt DB. They claimed that the positive or negative attitude of bank staff about DB has a substantial influence on consumer technology adoption intention. This was consistent with the findings of Abukhzam and Lee (2010), who discovered that bankers can have two opposing impressions of DB. If bankers consider DB as a tool to lower bank costs while having no detrimental impact on their jobs, this would produce favorable attitude among customers toward DB adoption (via employee DB adoption), otherwise it will affect DB adoption negatively. Shukla and Singh (2014), on the other hand, criticized earlier studies for failing to emphasize the role of employees in DB adoption. Later, Kaur and Ali (2021) backed the employees’ involvement in DB adoption, claiming bankers to be the front-line representatives of the banks. Their favorable attitude about DB may encourage consumers to use the DB channel for their financial activities. Aside from attitude, employees’ adaptation to ever-changing financial technology enables them to provide services that meet the needs of customers and result in customer satisfaction, Lydiana et al. (2023). According to Murad and Ahmad (2023) employees’ adjustment and adaptability of DB technology impacts the technology adoption behavior of clients.

Bank employees’ responsibilities do not end with assisting customers with DB adoption; they must also continue to lead them to a higher DFI level through DB adoption and usage. Bankers who have direct contact with the public are the true promoters of DB services and DFI. Jain (2023) argued that despite the banking sector providing adequate DB facilities, people do not use them. Despite the successful implementation of the Pradhan Mantri Jan Dhan Yojna, Digital India, and Demonetization schemes, which have resulted in enormous financial benefits, India continues to face gender disparities in DFI, Mndolwa and Alhassan (2020). Kulkarni and Ghosh (2021) found lack of financial literacy, digital literacy, smartphone ownership, as the prominent caused of gender gap in DFI. Yeyouomo et al. (2023) expanded this to gender gap in Financial Technology (fintech) where they found that firstly fintech adoption reduces the gender gap in DFI by digitally improving access to savings, and borrowings from formal financial institutions. They also stated that fintech reduces the barriers faced by women in DFI by providing lower transaction charges, reducing bank distance, simplified loan application.

Closing the gender gap in DFI requires eliminating barriers to women’s access to Digital Financial Services (DFSs). Women are prevented from accessing DB services due to a lack of personal touch in online services, resulting in a gender gap in DFI. Ramón Jerónimo et al. (2014) discovered that women’s preference for personal communication with banking personnel increases their trust in banking services. Manta (2019) attributed women’s low DFI to lack of financial literacy, time constraints, and their subordinate status in family and society. Ajina et al. (2023) proposed psychological differences in cognition structure, processing and retrieving information, and decision-making as determinants of gender imbalance in technology adoption in addition to socioeconomic factors. They cited women’s technophobia as the primary cause of their aversion to technology. Sasidharan (2022) claimed women employees to have more technostress than their male counterparts; where the term incorporated techno-strain and techno-anxiety as the dimensions of technostress.

Kumar (2022), Tiwari et al. (2022) advocated for the role of female banking agents or female bank employees in transacting with ordinary women to reduce gender disparities in DFI. According to their findings, the role of women as bankers is important in engaging other women in FI strategies because rural women feel comfortable sharing their financial needs with female banking agents as they receive feminine financial advice. Chamboko et al. (2021) discovered that female customers in the Democratic Republic of the Congo make smaller financial transactions with male agents than with female banking agents. In addition, female customers prefer to meet female agents in cases of larger monetary transactions to avoid disclosing financial information to men. Specifically in rural areas, women need DB to make financial transactions as they face barriers of branch-home distance, time constraints, societal issues, lack of identification documents to open bank account. These barriers call for employing DB technology in the rural areas, Pinto and Arora (2021). The societal pressure preventing women to make transactions with male bankers depicts the need for important role female banking agents in DB adoption and usage among female clients.

To foster a pro-digital attitude among women, it is necessary to investigate the factors that affect her technology adoption. Extensive research has been conducted to understand the gender imbalance in DB adoption among customers, but there is a lack of research on employees of the Indian financial sector who have dual responsibilities: persuade clients to adopt DB and build pro-digital attitudes among women clients to eliminate the gender divide in DFI. Thus, the study aims to investigate the underlying factors that contribute to the gender gap in DFI among bank employees, as reflected through their Gender Digital Divide (GDD). The study uses bank employees as respondents because they have direct influence over customers and have a better understanding of customer attitudes due to extensive experience in the banking industry (Kaur et al. 2021). As a result, the authors were curious to study how the disparity in digital inclusion of both genders representing GDD affects the gap in digital financial transactions depicting DFI, given that banking is now primarily done online. Is this also applicable to bankers? As the bankers serve as role models and propagators for the public to adopt DB, they serve as the study’s sample.

The authors conducted the research to find answers to the following research questions:

RQ1: How do technology adoption factors influence male and female bankers’ adoption of Digital Banking? Is this indicative of Gender Digital Divide?

RQ2: How does the adoption of Digital Banking affect male and female bankers’ Digital Financial Inclusion? Is this indicative of the gender gap in Digital Financial Inclusion?

RQ3: How does Gender Digital Divide effect the gender disparity in Digital Financial Inclusion?

The study includes bankers in the positions of Branch Managers/Assistant Branch Managers; Clerical Staff/Cash Department Staff in selected public and private sector banks (Reserve Bank of India, 2011). To the best of our knowledge, this is one of the initial studies to investigate GDD among bank staff by identifying factors responsible for the gender gap in DB adoption. This study contributes by demonstrating the reality of gender bias in the Indian financial sector, raising awareness among the general public, and thus will help to reduce gender disparities in DFI.

Setiawan et al. (2023), explained the need to understand the actors to Fintech adoption by women as its understanding can help to push women from financial exclusion to financial inclusion. To understand the factors affecting technology adoption, various technology acceptance models have been formulated and proved, which are discussed in brief in the next section.

Theoretical Background: TAM, TAM2, UTAUT, and UTAUT2

TAM

The early adoption of technology among users prompted researchers to investigate the factors influencing technology adoption. This was first investigated in the field of psychology. Davis (1989) later adopted it in the field of Information Systems (Granić & Marangunić, 2019). Davis developed the Technology Adoption Model (TAM) in his Doctoral Thesis in 1989, where Perceived Ease of Use (PEU), Attitude Toward Use (ATU), and Perceived Usefulness (PU) explain a user’s intention to use the system. According to his research, two variables “PEU and PU” have a significant impact on technology acceptance, as claimed by Sikdar et al. (2015), by building up the individual’s attitude (positive or negative) toward technology, ultimately infusing to either adopt or reject it. The TAM model demonstrated that adoption and usage of any new technology are determined by an individual’s Behavioral Intention (BI), which is influenced by its Attitude toward technology, as developed by PEU and PU (Bashir & Madhavaiah, 2015). This model piqued the interest of many researchers, who used it to study and validate various versions of technology adoption models.

TAM2

TAM2 was developed by Venkatesh and Davis (2000) to improve TAM by emphasizing that not only PU and PEU are important determinants of technology acceptance and adoption, but also Subjective Norms that vary among individuals such as Image, Social Influence (SI) by peer group, and Voluntariness to adopt technology influence the adoption decision. This model did not include “Attitude,” which was influenced by PEU and PU, according to Malatji et al. (2020).

UTAUT

TAM2 was further extended to the “Unified Theory of Acceptance and Use of Technology (UTAUT)” model developed by Venkatesh et al. (2003), which took four key constructs influencing users’ adoption of technology into account. They concluded that Performance Expectancy (PE: the customer’s expectation of a benefit in job performance from adopting technology), Effort Expectancy (EE: the level of effort to put in to learn new technology), and Social Influence (SI: the degree to which family, friends, peers, and so on influence someone to use new technology) influence the user’s intention to adopt technology. They added a fourth construct, Facilitating Conditions (FC: the extent to which people believe an organizational and technical infrastructure exists to support the system), which has a direct influence on the technology adoption behavior of the user. Lu et al. (2005) defined SI as the views gained from managerial staff, supervisors, peer groups regarding the technology that shape acceptance or rejection of technology. According to Venkatesh et al. (2012), PE, EE, and SI have an impact on BI but BI together with FC determine Actual Use of the system.

UTAUT2

Venkatesh et al. (2012) developed UTAUT2 (extended version of UTAUT), which incorporated three additional constructs into the UTAUT1 model: Hedonic Motivation (pleasure of using new technology), Price Value (monetary expense incurred in adopting the new technology), and Habit (the extent to which people tend to perform behaviors automatically because of learning). According to Venkatesh et al. (2016), the extensions proposed in UTAUT2 resulted in a significant improvement in the variance explained in BI (56%–74%) and technology use (40%–52%). The UTAUT2 model’s variables are included in the questionnaire because it is comprehensive in terms of social, psychological, and economic parameters of technology adoption.

Objectives of the Study

To attain answer to the research questions, following are the objectives of the study:

O1: To examine the impact of technology acceptance model “UTAUT2” on Behavioral Intention to adopt Digital Banking by Indian male and female bankers, indicating GDD.

O2: To assess the impact of DB adoption (retrieved through BI to adopt DB) on Digital Financial Inclusion of bankers, composed of DB Penetration and DB Usage.

O3: To examine the effect of Gender Digital Divide on the gender difference in Digital Financial Inclusion by comparing the models for men and women bankers.

Review of Literature and Hypotheses Development

Impact of UTAUT2 Factors on BI to Adopt Technology

The preceding context is an overview of the well-known and widely used theories by many researchers in their studies, beginning with the TAM (although the TAM model has its roots in earlier psychological studies) and ending with UTAUT2 (though this is not the end). The following literature provides information on how the researchers’ have used the constructs from the aforementioned models in their investigations on different target populations.

Perceived Ease of Use (PEU)

According to Davis et al. (1989), PEU is a consumer’s perception of the ease with which technology can be adopted and used. The positive perception of ease of use of technology leads to a positive intention to use technology. According to Kaur and Ali (2021), PEU is the second most important factor influencing bankers’ perceptions of digital banking. If bankers believe that DB technology is simple, it will have a positive impact on consumers. According to Nguyen and Malik (2022), lower PEU on behalf of women is due to internet anxiety and lower technological aptitude. Increased PEU among female job seekers would improve their attitude and BI toward e-recruitment technology. In the above context, we posit that:

H1a: PEU has significant relation with BI to adopt DB.

H1b: There is a significant difference in PEU among male and female bankers.

Perceived Usefulness (PU)

Davis et al. (1989) define PU as the belief that adopting a specific technology will improve job performance. Patil et al. (2020) discovered that PU is a direct significant positive predictor of actual usage and has an impact on BI in their study on mobile payments adoption by Indian consumers. According to Purohit and Arora (2021), the PU of mobile payment adoption is higher among men than women, owing to the belief that men are more independent in performing financial tasks, whereas women always look up to male members of the family. In the above context, we posit that:

H2a: PU has a significant relation with BI to adopt DB.

H2b: There is a significant difference in PU among male and female bankers.

Personal Innovativeness (PI)

In their study, Agarwal and Prasad (1998) used PI for Information and Communication Technology (ICT) usage and adoption, coining the term “Personal Innovativeness of Information Technology (PIIT).” In the domain of mobile banking, Sulaiman et al. (2007) distinguished between mobile banking users as innovators with a positive attitude toward change and non-mobile banking users as risk-averse individuals who use online banking only when forced to. According to Belghiti-Mahut et al. (2016), PI is closely related to risk-taking attitude; where women avoid risky situations in contrast to men who like to test their capabilities by taking risks. This was supported by van Elburg et al. (2022) who made a gender comparison in the field of mobile-health adoption, claimed that men are open to try new technology as they are more adventurous as compared to women. In the above context, we posit that:

H3a: PI has a significant relation with BI to adopt DB.

H3b: There is a significant difference in PI among male and female bankers.

Social Influence (SI)

Venkatesh et al. (2003) used “SI” to indicate the effect of one’s close relatives’ views on technology usage. Bashir and Madhavaiah (2015) and Lewis et al. (2015) discovered that SI has an indirect relationship with BI through its significant negative effect on Perceived Risk, that is, if SI is higher, the Perceived Risk is lower and thus the BI is higher. Patil et al. (2020) defined SI as the unification of subjective norms, social factors, and image, and discovered SI to be a significant positive predictor of BI. Purohit and Arora (2021) discovered that the effect of SI on mobile payment adoption is positive and higher in females than in males. They backed this up with the belief that in India, women have a lot of social influence from relatives and peers. In the above context, we posit that:

H4a: SI has a significant relation with BI to adopt DB.

H4b: There is a significant difference in SI among male and female bankers.

Facilitating Conditions (FC)

FC refers to the availability of organizational and technical resources to support specific technology. If the lack of any resource interferes with the normal operation of the technological system, this indicates poor FC. Venkatesh et al. (2012) identified four FC indicators: resources to support technology, knowledge of technology usage, compatibility of technical devices for technology, and availability of help when needed in technological usage. In their study on healthcare technology usage and adoption, Zhou et al. (2019) discovered that FC had an insignificant direct relationship with Usage Behavior of Hospital Electronic Information Management System by Ghanaian nurses, but in the same context, with BI as the mediator, FC significantly and positively influenced actual usage. Patil et al. (2020) discovered FC as a significant positive predictor of BI in a study on mobile payments technology adoption by Indian consumers. Ambarwati et al. (2020) investigated the adoption of Online Learning Platforms by Indonesian users and discovered that knowledge of technology, which is an indicator of FC, is a significant predictor of BI. In the above context, we posit that:

H5a: FC have significant relation with BI to adopt DB.

H5b: There is a significant difference in FC among male and female bankers.

Hedonic Motivation (HM)

HM stands for enjoyment or pleasure in the use of technology. Lewis et al. (2015) discovered that HM has a significant impact on Perceived Usefulness, which in turn has an impact on BI. In terms of Arab women’s smartphone adoption, Ameen et al. (2018) stated that both Jordanian and Emirati women attribute their smartphone adoption to the enjoyable experience associated with its use. In the above context, we posit that:

H6a: HM has a significant relation with BI to adopt DB.

H6b: There is a significant difference in HM among male and female bankers.

Habit

A habit is not an inborn natural behavior, but rather one that is learned through repetition of that behavior. So, when a specific behavior toward a specific stimulus is repeated for an extended period, it becomes a Habit. Alsharo et al. (2020) discovered in a study conducted in Jordan among healthcare workers on the use of a Health Information System called “Hakeem” that Habit has a positive and significant relationship with both PEU and PU, but it is a strong predictor of PU. Habit explained 68.8% of the variance in PU and 44% of the variance in PEU. This influences healthcare professionals’ attitudes toward HIS and, as a result, their willingness to use it. Ambarwati et al. (2020) investigated Online Learning Platform adoption among Indonesian users and discovered that Habit (formed through daily repetition and not an addiction) is a significant predictor of BI. In a gender comparison of BI to use smartphones in Jordan and India, Ameen et al. (2018) discovered that habit was a strong determinant for BI to use smartphones as compared to women, as men are said to have better and longer experience with smartphones. In the above context, we posit that:

H7a: Habit has a significant relation with BI to adopt DB.

H7b: There is a significant difference in Habit among male and female bankers.

Price Value (PV)

PV, or the cost of using any technology, refers to internet access fees, service fees, and transaction fees (if the technology is for digital banking). Purohit and Arora (2021) discovered that PV was insignificant for men but had a significant negative relationship for females when it came to mobile payment adoption. Their theory was that females in India are more concerned with cost than with the value of service. In the above context, we posit that:

H8a: PV has a significant relation with BI to adopt DB.

H8b: There is a significant difference in PV among male and female bankers.

Digital Banking Penetration (DBP) and Digital Banking Usage (DBU)

Thulani et al. (2014) concluded that mobile usage is more important in escaping poverty than mobile penetration. A high correlation is observed in mobile and internet use, indicating a significant combined contribution to the DFI model. When considered as independent variables, both mobile usage and internet penetration have a positive impact on FI. Thulani et al. (2014) concluded, taking gender into account, that this positive effect is more visible in male-headed households than female-headed households. In a survey of 144 nations, Antonijević et al. (2022) discovered a significant gender gap in DB access, with men being more frequent users than women. Men also outperformed women in the use of DB, indicating that men have higher DFI than women. They claimed that women are more likely to make cash transactions, lowering their DFI level. In the above context, we posit that:

H9a: DBP has a significant effect on DB adoption indicating DFI.

H9b: DBU has a significant effect on DB adoption indicating DFI.

H9c: There is a significant difference in DBP among male and female bankers.

H9d: There is a significant difference in DBU among male and female bankers.

Behavioral Intention (BI)

Intrinsic and extrinsic motivators influence behavior in the adoption of new technology. The enjoyment and satisfaction gained from using technology are intrinsic motivators. Improved job performance as a result of technology use is an extrinsic motivator. Bashir and Madhavaiah (2015) discovered that BI has a significant influence on customer satisfaction in their study on Online Banking adoption by Indian bank customers. Zhou et al. (2019) discovered that BI has a direct significant impact on the Actual Usage of the technology for patient monitoring in their study on Usage Behavior and Adoption of Hospital Electronic Information Management System (HEIMS) by Ghana nurses. Customers’ positive intentions encourage them to adopt and use technology in-order-to be cheaper, faster, and easier.

H10a: BI has a significant impact on DB adoption indicating DFI.

H10b: There is a significant difference in BI among male and female bankers.

Figure 1 presents the Conceptual research model that propose the hypotheses from H1 to H10, with the aim to examine the impact of UTAUT2 factors on Behavioral Intention to adopt Digital Banking. The model further aims to examine the effect of DB adoption on Digital Financial Inclusion.

Conceptual research model 1(H1–H10).

Review of Literature on Gender Digital Divide (GDD) or Gender Gap in Digital Inclusivity

GDD refers to the disparity in access to and use of the internet and ICT tools between men and women, which impedes human development. According to the WEF’s “Gender Gap Index” report (2018), India ranked 108th out of 144 nations due to women’s poor performance in personal and professional spheres (World Economic Forum, 2018). Women’s exclusion from the field of technology is a major reason for their poor performance. According to Viadero (1994), the origin of the digital divide between girls and boys begins in school, where girls use the internet for social connection and educational purposes (Weiser, 2000) and to solve real-life problems, while boys use the internet to train themselves for future competition. Humby-Hoff (2002) investigated the second level gender divide, claiming that girls use the internet more for entertainment, whereas Weiser (2000) claims that men use the internet more for entertainment. Chandel and Lakhani (2018) found that entertainment and social interaction are equal motivators for men and women to use the internet. According to Humby-Hoff (2002), because of the complex programming and web design taught in the course, girls are less likely to participate in elective computer classes when offered as an option in school. Gender discrimination in technological space exists not only in the personal world but also at the workplace, according to Patel and Parmentier (2005), who studied the situation of female engineers employed in the IT sector, where women are assigned to software design roles because it is feminine, while men are assigned to hardware related work and also employed on the shop floor level because it is considered masculine. According to Miller and Shrum (2011), there has been a significant increase in the intensity of women’s technology usage, but they lag due to familial or institutional constraints. Yeganehfar et al. (2018) reiterated that while IT has become the backbone of the Indian economy, women are largely underrepresented in these fields and often ignored to participate in tech-savvy organizations.

The Global Systems for Mobile Communication Association (2020) Mobile Gender Gap report highlighted barriers faced by women in mobile internet adoption and usage, stating that 34% of Indian women face a barrier of handset cost in mobile ownership. Nine percent have little or no knowledge of how to use the internet via mobile, 16% have literacy issues, 11% of women believe mobile and internet are useless to them, and 3% have security concerns because strangers may contact and harass them.

Relation of GDD and Gender Difference in DFI

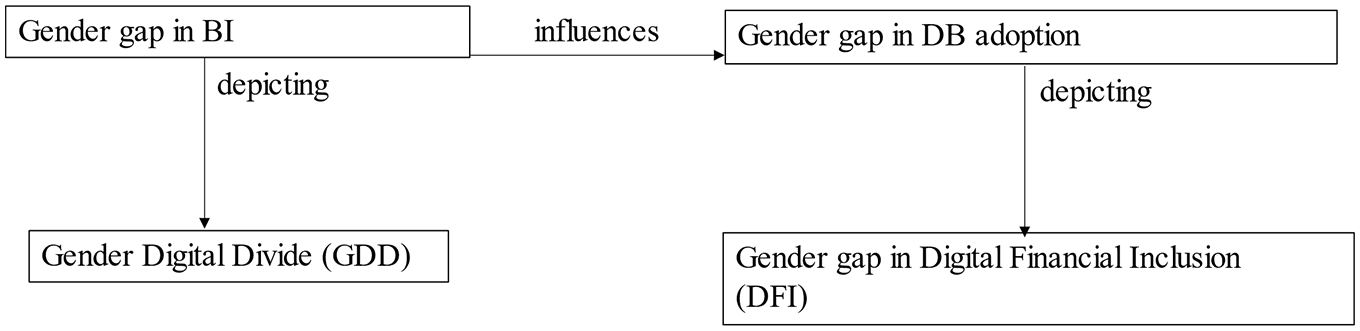

Gender disparities in digital transactions are caused by disparities in digital inclusion. Women are excluded from the internet for a variety of reasons, including cultural, patriarchal, economic, political, and national ones. Potnis (2016) supported this by focusing on socio-cultural inequalities (early girl marriage, dowry, female feticide, domestic violence, household responsibilities); psychological inequalities (male dominance, low self-confidence in women); demographic inequalities (illiteracy, language problem); communication-related inequalities (informal and incomplete communication from family members); health-related inequalities (lack of health facilities, infectious diseases, lack of health insurance). Genesis Analytics (2018) also blamed women’s lack of mobile phone ownership for the digital divide and thus lower DFI of women. Lee and Kim (2014) emphasized that women do not differ from men in terms of internet and ICT access, but also usage. They primarily use their phones for communication rather than information retrieval. In terms of gender, there was a significant difference in life management and resource use, implying that males use mobile for more productive purposes than females. Because women have lower ICT access and usage, they are less inclined to engage in digital financial activities, lowering their DFI level. Gammage et al. (2017), supported mobile access, communication network, and mobile banking as of utmost parameters of DFI, showing a concern that lower access to mobile technology may not improve their DFI as they would not be able to register their names on mobile based financial accounts. The relationship of GDD and DFI is depicted in Figure 2.

Conceptual research model 2 (H11).

In contrast, Bartlett et al. (2022) blamed the gender gap in DFI on differences in attitudes toward financial technology that evolved through social norms. Chen et al. (2023) discovered in their study of 28 economies and 27,000 adults that women perceive financial technology to have privacy and financial risk. According to Tok and Heng (2022), women are uninterested in new payment players because they are afraid of losing financial and personal data, which will prevent them from reaping the benefits of DB. Women are prevented from accessing and using bank accounts digitally due to limited access and use of mobile and computer devices, which impedes their DFI. Researchers have identified a variety of causes, ranging from economic issues to psychological differences between the sexes. Above literature provides with following hypothesis:

H11: GDD extracted from gender gap in Behavioral Intention leads to Gender gap in Digital banking adoption (depicting DFI).

Research Methodology

Constructs of the Research Model

The current study follows a descriptive cross-sectional research design. The research model consists of eight latent constructs derived from the UTAUT2 model. The eight latent constructs are as such: PEU (three items), PU (three items), PI (three items), SI (three items), FC (four items), HM (three items), Habit (three items), and PV (three items). These constructs measure BI (three items), ultimately impacting the dependent variable “DFI.” DBP (three items, six items) measure the degree of DFI of respondents. The constructs of PEU and PU are taken from Davis (1989); SI, FC, HM, PV, and habit are taken from Venkatesh et al. (2012); the construct of PI is taken from Agarwal and Prasad (1998); BI is taken from the study of Ajzen and Fishbein (1975).

Measurement Development

Data through structured questionnaires were collected from both male and female bankers to assess their DFI level. The questionnaire consists of three parts. The first part pertains to the demographic profile of the respondents composed of gender, age, income, and education. The second part of the questionnaire measures items of constructs adopted from the UTAUT2 model on 1 to 5 Likert scale where 1 refers to Strongly Disagree and 5 stands for Strongly Agree. This part consists of questions on constructs adopted from the UTAUT2 model. Third part of the questionnaire consists of questions on DBP and DBU, which measures DFI.

Sample Size Determination

The top six Indian banks according to market capitalization were selected for the study. The sample consisted of three public sector banks (State Bank of India, Punjab National Bank, and Bank of Baroda), and three private sector banks (ICICI Bank, Axis Bank, and HDFC Bank). The sample size was determined based on research undertaken by Kotrlik and Higgins (2001) which has more than five thousand citations.

Where n is the sample size to be determined; Z is the level of confidence which is taken as 95% in the study. Thus, sample size would be calculated as follows:

Thus, considering the above sample size calculation result, a sample of 300 bankers was decided.

Data Collection

Before conducting the pilot study, the face validity of the draft survey was evaluated by a panel of experts in the field. The questionnaire was refined and re-sent for validation after the suggested changes were made. Following approval, 30 randomly selected bankers were subjected to pilot testing. The collected responses were coded and tested for reliability in SPSS version 21, with a Cronbach’s alpha score of 0.901. As part of the data collection procedure, questionnaires were distributed to 300 bankers (50 from each bank) at random by visiting bank branches, as response rates from online questionnaire administration were low.

Descriptive Statistics

Out of the determined and thus distributed 300 questionnaires, 260 completed questionnaires were received making the response rate of 86.67% of which 142 were male respondents (55%) and 118 were female respondents (45%). A major proportion of males (72.53%) and females (68.64%) fall in the group of age 26 to 40 years with the earnings of less than 0.5 million per annum (males: 45.07%; females: 57.63%) having completed their post-graduation (males: 57.75%; females: 63.56%) as displayed in Table 1.

Demographic Profile of Respondents.

Source. The authors’ compilation.

Data Analysis

Structural Equation Modeling (SEM) is used to analyze and interpret inter-relations of multiple constructs consisting of multiple items. SEM is useful where the research model consists of multiple independent variables, dependent variables, sometimes models also consisting of mediators and moderators.

Reliability and Validity of Measurement Model: As a Reflection of Its Quality

The Measurement model defines the relation between items and their latent constructs. Table 2 displays the statistical techniques used for the quality evaluation of the measurement model.

Measurement Model Quality Metrics.

Source. The authors.

Both Cronbach’s alpha and CR in Table 3 have values above 0.70 which is a satisfactory reliability measure.

Reliability Check Criteria.

Source. The authors.

Average Variance Extracted (AVE) measures Convergent Validity assessing the degree to which constructs are different from each other in the instrument. AVE values of both constructs in Table 3 for males and females are higher than 0.50 reflecting more than 50% of variations in the respective constructs were because of their indicators (Bagozzi &Yi, 1988; Fornell & Larcker, 1981).

Table 4 represents another technique of convergent validity where outer loadings of constructs are higher in association with their reflective latent variable and no other latent variables. Outer loadings of more than 0.70 suggest satisfactory indicator reliability (Hulland, 1999). In the above table maximum indicators have outer loadings of above 0.70 except PI and SI which, explaining that they contribute less in the measurement of BI and DB both for men and women where PV also has a low contribution in BI in case of female bankers.

Outer Loadings (Indicator Reliability).

Source. The authors.

Square root of AVE as displayed in Table 3 is a measure of Discriminant validity that assesses distinctiveness of constructs from each other. According to Forner-Larcker criteria, the square root of AVE should be greater than the squared correlation.

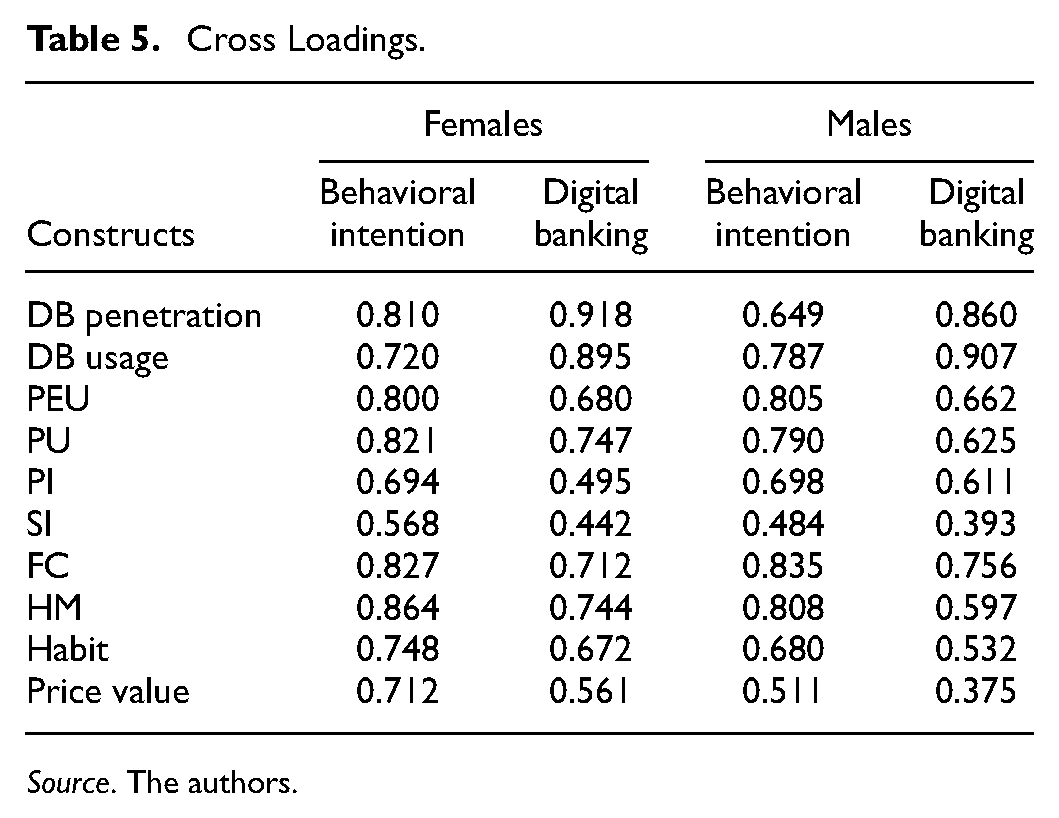

Cross-loadings in Table 5 determine Discriminant Validity. In statistical terms, it is referred to as “item-level Discriminant validity” which assesses that a construct has the strongest relation with its indicators. In the table, it is displayed that all the indicators have higher loadings with their respective constructs rather than other constructs.

Cross Loadings.

Source. The authors.

Heterotrait-Monotrait (HTMT) ratio measures the correlation among items of reflective constructs whose value should be below 1; suggesting good Discriminant validity, where HTMT values of men and women are less than 1.

Quality metrics of the measurement model reflect all constructs are different from each other and measure varied purposes in the model.

Structural Model

According to Anderson and Gerbing (1988), the structural model is tested to investigate relations among theoretical constructs. R-square value for male bankers is 0.716 and for female bankers is 0.669 which means that Behavioral Intention causes 71.6% variation in Digital Banking in the context of men and 66.9% in case of women.

Variance Inflation Factor (VIF) analyses muti-collinearity between independent constructs. According to Hocking and Pendleton (1983), VIF should be higher than 0.2 and below 5. In Tables 6 and 7, all values of inner and outer VIF are below 5 indicating that there is no muti-collinearity between constructs indicating that all constructs measure different phenomena.

Outer VIF Values.

Inner VIF Values.

Source. The authors.

Results

Path Analysis was conducted to examine the significance of UTAUT2 factors on BI to adopt DB and its influence on DFI level of bankers. The results of the study are divided into four sections:

Results of hypotheses testing (H1–H10)

Resultant model of PLS-SEM

Extraction of results of model 2 from model 1: H11 and explanation

Summarized results

Results of Hypotheses Testing

Table 8 provides with the outer loadings, t-statistics, and p-values of all the hypotheses.

Hypotheses Testing by t Statistic and p Values.

Source. The authors.

p < .001.

According to Table 8, H1a is accepted as PEU has a significant effect on BI to adopt DB for both men and women with t-statistic >1.96 and p < .001. H1b is supported as PEU has more effect on BI in the case of female bankers (0.805) as compared to male bankers (0.800) indicating significant gender difference in PEU. H2a is also accepted as PU has significant effect on BI to adopt DB for both genders with t-statistic >1.96 and p < .001, however, PU has a greater role to play in the case of male bankers (0.821) as compared to female bankers (0.790), thus H2b is also accepted. PI has significant effect on BI (p < .001) to adopt DB claiming the acceptance of H3a with t statistic >1.96. H3b is accepted as male bankers have lower PI (0.64) than female bankers (0.698) depicting significant gender gap in PI. H4a is accepted as SI has a significant effect on BI to adopt DB for both men and women with t-statistic >1.96 and p < .001. H4b is supported as SI has more effect on BI in the case of male bankers (0.568) as compared to female bankers (0.484) indicating significant gender difference in SI. Study supports H5a as FC also have a significant effect on BI to adopt DB among bank employees, with p < 0.001 and t statistic >1.96. Results supports H5b claiming a significant gender gap in FC to adopt DB, where male bankers have lower beta value of FC (0.827) as compared to female bankers (0.835). H6a is supported by the results claiming significant effect of HM (p < .001) on BI to adopt DB among both genders with t statistic >1.96. H6b is also supported where male bankers have higher HM (0.864) than female bankers (0.808). There is a significant effect of Habit on BI to adopt DB (p < .001) and t statistics (>1.96) supporting H7a. H7b is also supported as male bankers higher Habit (0.748) toward technology adoption and usage as compared to female employees (0.680) claiming significant gender divide in BI to adopt DB. H8a find its support from p < .001 claiming significant effect of PV on BI to adopt DB with t statistic >1.96. H8b is also supported where mela bankers perceive PV as a determinant of Db adoption (0.712) as compared to female bankers (0.511). H9a, H9b is supported through p < .001 and t statistic >1.96 stating a significant effect of DBP and DBU on DFI. Also, H9c is supported where there is significant gender gap in DBP, with male bankers having higher DBP (0.918) than female bankers (0.860). Regarding DBU, H9d is supported where male bankers have less DBU (0.895) than female bankers (0.907).

Maximum indicators have outer loadings greater than 0.70, except for PI and SI, which have values less than 0.70, indicating that they contribute less to the measurement of BI and DB for both men and women, while Price Value also contributes less to BI in the case of female bankers.

In the end, five of the eight UTAUT2 factors play significant roles for men and three play significant roles for women, resulting in a higher path coefficient of 0.846 for men and 0.818 for women, as shown in Table 10. This indicates that the digital divide favors men because women have a lower BI value due to a smaller number of contributing factors. This clarifies the GDD.

To examine DFI of bankers, DBP and DBU are assessed. H9a and H9b claiming that DBP and DBU have significant roles in DFI, respectively are accepted with t statistic>1.96 and p < 0.05. But DBP is more for men and DBU is more for women. So DBP has higher role in DFI of male bankers, while DBU has higher role in DFI for female bankers, claiming acceptance of H9c, and H9d, respectively.

According to Table 9, H10a is accepted as BI has significant effect on DB with p < .001 and t-statistic >1.96. H10b is supported that shows significant gender gap in effect of BI on DB adoption that indicated significant gender gap in DFI. The Table 9 shows that one percent change in BI causes 0.846 or 84.6% change in DFI for men and 0.818 or 81.8% change for women. That means BI level (used to understand as Digital Inclusion in the study) is less for female bankers. This can be due to the lesser number of contributing UTAUT2 factors as compared to male bankers.

Significance Testing of Path Coefficient.

Source. The authors.

p < .001.

Resultant Model of PLS-SEM

Figure 3 presents comparative results of DFI of males and female bankers, representing the GDD among them, which is also the third objective of the study.

Comparative results of male bankers and female bankers.

Extraction of Results of Model 2 From Model 1, Testing Hypothesis 11

Figure 4 explains the attainment of overall objective of the study, that is, how GDD affects DFI level of Indian bankers. Table 9 and Figure 4 depicts that women bankers’ BI to adopt DB is influenced by merely three UTAUT2 factors (PEU, PI, and FC) as compared to men, whose BI is influenced by five UTAUT2 factors (PU, SI, HM, Habit, and PV). Weightage of BI of men is more, which explains that there exists GDD between Indian bankers, where men have more Digital Inclusion. Now, looking for degree of DFI, PLS-SEM results in Figure 3 highlight that DFI level of men (0.716) is higher than that of women (0.669). Also, path coefficients of male bankers (0.846) in Figure 4 portray that BI (indicating digital Inclusion) have more influence on DFI, that is, there is 84.6% change improvement in DFI is there is 1% change in BI. In contrast, female bankers have lower path coefficient (0.818), which means there their DFI will improve to 81.8%, if BI is improved or changed by 1%. This explains that there exists GDD among men and women bankers of India, where men have more Digital Inclusion (depicted by higher BI value) due to higher contribution by UTAUT2 factors. This results in effect on DFI level (0.716) as indicated by higher path coefficient value (0.846), as compared to men. The results in Figure 4 outline that although there is not a wide gap in DFI of both genders, but in order to improve FI level of common women, female bankers themselves must use more DB.

Model extracted.

Summarized Results

Table 10 presents summarized results representing hypotheses of the study and their status.

Summarized Results.

Source. Authors’ compilation.

Discussion

This study contributes by examining the DFI level of Indian banking sector employees as extracted from their GDD. The authors used the UTAUT2 model to assess BI in order to investigate DB adoption among Indian bank employees, which is then used to highlight the degree of GDD. The study discovers a significant gender difference in BI to adopt DB among Indian banking employees. Furthermore, the findings indicate a significant gender difference in DFI level of bank employees. The study discovered that male banking employees outnumber female employees in DFI, even though all the investigated variables have a significant effect on BI to adopt DB for both genders. All the hypotheses have been found to be have significant effect on BI to adopt DB, but loading of each variable explains their amount of contribution on DFI level of employees.

The study’s findings supported all the hypotheses (H1–H10) related with model 1, thus reflecting that all UTAUT2 factors have a significant effect on BI to adopt DB for both genders. The findings show a significant gender difference in BI to adopt DB, with five UTAUT2 factors found to be significant for men, including PU, SI, HM, Habit, and PV. Support for PU has been reported by Teo (2001), Venkatesh et al. (2003), and Yousafzai and Yani-de-Soriano (2012). Previously published research (Kwateng et al., 2019) supported SI, HM, Habit, and PV as important predictors. Three factors emerged as significant predictors of DB adoption in women. PEU (Legris et al., 2003; Ong & Lai, 2006), PI, and FC are the factors, along with literature support. Men’s digital inclusion is increasing, as is their DFI level, lending support to H11. This matches the findings of Joiner et al. (2005), Antonio and Tuffley (2014), Potnis (2016), Bala and Singhal (2018), and Joshi et al. (2020). According to these studies, women’s digital inclusion is lower than men’s, with a significant GDD. In their cross-country study of 28 countries, Chen et al. (2023) discovered that a gender gap exists in Fintech products as well, with women using 85% fewer fintech products than men.

PEU was discovered to be a significant factor in female employees’ DB adoption. According to Kaur and Ali (2021), PEU emerged as a significant factor responsible for bankers’ perceptions of DB. If bankers believe that DB technology is simple, it will have a positive impact on consumers. Nguyen and Malik (2022), on the other hand, proposed internet anxiety and a lower technology attitude as reasons for women’s lower PEU. According to the study, male bankers have higher PU. Women have lower IT confidence and technology operational capability than men. This could explain why male bankers have higher PU in the current study, according to Sobieraj and Krämer (2020). We found support in the findings of Kim and Park (2018) and Ojo and Adebayo (2023), who stated that male employees find technology more useful at work for improving productivity and outcomes.

PI is also said to be important for female bank employees. This could be due to female bank representatives’ higher education and desire to be innovative in order to advance in their careers. According to Lipovka et al. (2021), male and female employees have positive innovative attitudes, but female managers’ high innovative attitudes are a motivator for subordinates. In comparison to male managers, Na and Shin (2019) attribute female managers’ risk-aversion tendency and non-corruption attitude to their ability to lead business without over-confidence and innovative skills. In addition, Kar et al. (2021) advocated for male employees to reskill themselves through skill development programs in order to maintain a work-life balance.

According to the study, SI places a greater burden on male employees. SI is also a significant factor in technology adoption, as Selamat et al. (2009) discuss in the context of Malaysian bankers. They reiterated that bankers are under pressure to adopt IT to gain greater recognition among peers and from bank management. The findings are supported by Sasidharan’s (2022) research, which found that male employees form social and official networks with coworkers who have high technical expertise to achieve their specific goals, whereas women form more friendship-oriented connections. The gap in gender attitude toward making social network might be the reason of male employees having higher influence of SI on BI to adopt technology, as they might fear disrespect from peers or failure to achieve goals.

Regarding FCs, Chauhan et al. (2020) asserted that FCs are a significant employee motivator among Indian Postal Sector employees. The study’s findings suggest that FCs favor female bankers, which is supported by Akter et al. (2021). According to the study, women are more likely to adopt technology when there are fewer challenges or efforts required to adopt and use the technology in an organization. The greater the infrastructure, the greater the intention of female employees in an organization to adopt technology.

Price Value (PV) is significant for male bankers in the study, whereas Lutfi et al. (2023) find PV to be significant for both genders. This could be due to men’s traditional duties of making household expenditures despite earning a good living. However, Akter et al. (2021) discovered that PV is significant for women because they are wary of unnecessary spending and more concerned about service costs.

HM has been found to contribute more to BI than male employees. According to Vašková (2005), male employees see financial rewards as a motivator for job performance, whereas female employees value interpersonal relationships, respect from superiors, and a positive work-life balance. In the field of DB, the entertaining features of DB apps have a positive and long-lasting effect on the minds of consumers, resulting in a significantly and positively influencing BI to adopt DB, according to Marpaung et al. (2021). In case of employees, Nguyen, and Malik (2022) defined extrinsic motivation as the tangible rewards of perks, job safety, bonus, promotion; while intrinsic motivation as the enjoyment or feeling of fulfillment while using the technology.

Although habit has a significant effect on both male and female employees’ BI, it is found to have a greater influence on male employees. Dhingra and Gupta (2020) defined digital transaction habit because of repeatedly using mobile banking due to a lack of time to visit bank branches. The repetition of a specific activity results in an experience and, later, a habit. Cheng et al. (2020) expanded on this with their finding that Habit had a significant relationship with continued usage intention to use mobile app. They reasoned that people who use the internet and mobile applications on a regular basis develop a habit of using different apps.

Because men have a higher weightage for technology adoption factors, it can be stated that in Indian banks, male bankers are more digitally inclusive than female bankers, indicating that GDD exists among Indian bankers in response to one of the research questions. The DFI level of men is also higher, as shown by the PLS-SEM resultant model. The path coefficient, which depicts the impact of BI on DFI level, is also higher for male bankers, indicating that men have more digital inclusivity; thus, their DB adoption is higher, as is their DFI level. However, studies indicating that GDD is shrinking (Rainer et al. 2003; Riquelme & Rios, 2010) support a smaller difference in DFI between male and female bankers. Female bankers have a good position in Digital Financial Inclusion, according to the results. Women have come a long way in their efforts to eliminate GDD and improve their digital inclusion in the financial system. Nonetheless, the results show that their DFI is lower than men’s, as Mndolwa and Alhassan (2020) support. Adoption and use of DB can give women confidence that it is not only simple to use, but also useful in their personal, professional, and financial lives. Their positive word of mouth can have a positive influence on other women’s attitudes toward DB.

Following a thorough review of the literature, the authors discovered that, while previous studies have focused on the gender gap in DFI in various domains, the gender gap in DFI has not been studied in a sectoral context. Until now, the bankers who are the protagonists of FI and DFI have remained unfocused. As a result, the authors saw this as an opportunity to investigate the GDD prevalent in the Indian banking sector and how this divide is causing a gender gap in DFI. In a survey of 12 private sector BCNMs (Business Correspondent Network Managers) conducted by Thakur et al. (2016) with MicroSave Consulting, 10 of them reported that men, particularly in rural and underserved areas, prefer that their wives make financial transactions with female agents while doing biometric identification where some physical interaction is made, Tiwari et al. (2022). As a result, the authors of this study wanted to understand how the digital disparity between male and female bankers (GDD) influences the gender disparity in DFI, because if this occurs in banking sectors as well, it is cause for concern, as women bankers must improve their adoption of DB channels to make other women more digitally financially inclusive and shrink GDD.

Theoretical Contribution

This study has contributed to the existing literature by merging the parameters of digital adoption and financial inclusion indicating that the technology acceptance model of UTAUT2 can be expanded to have an insight into the financial sector of the society, whereas in previous researches technology acceptance models have been used up to the level of examining adoption on specific types of technologies. The first major research contribution is the introduction of Indian bankers who preach the usage of digital banking for DFI. The second most important contribution is the role of gender in the study. UTAUT2 model has been used to examine the gender digital divide by many researchers but not specifically for any sector. This study is unique in focusing on employees of Indian banks. The study is important as it found that when the analysis was made on a gender basis, only three technology adoption factors namely, perceived ease of use, personal innovativeness, and facilitating conditions were found to be significant for technology adoption of digital banking by women, whereas in the measurement of the digital financial inclusion digital banking usage is more for women in contrast to digital banking penetration for men. This stresses the fact that although, women bankers use digital banking more than men, their penetration level is low, which also attracts us to the view that women have lesser ownership of digital and mobile devices and data packages. Though men have lower digital penetration, still they succeed in digital financial inclusion because their digital adoption contributing factors are more. Digital banking adoption of women should be focused on, only then ladies belonging to other sectors will be motivated and educated by female bankers to use online banking leading to their rise in digitally enabled financial inclusion level.

Implications of the Study

Considering bankers as consumers of digital banking, women are a few steps behind to match the level of DFI of men. The empirical study found that due to a lesser number of contributing factors in technology acceptance by female bankers, their DB adoption has come out to be lower than that of male bankers. This calls for stressing those areas that drag women behind in DFI. RBI can start courses compelling banks to take online sessions of their customers regarding the practical working of their digital banking application so that women find digital banking more useful and practicable. Results also claimed that Social Influence did not bring a significant effect on DFI of women. Female Celebrities can endorse advertisements regarding the easiness and usefulness of DB. Celebrities are the role model of a major proportion of the population thus their comments can have a positive influence on DB adoption among females. DB adoption among women has also resulted to be low due to lesser contribution of Hedonic Motivation (pleasure in using technology). For grown-ups, pleasure of technology usage is due to simple and clear instructions that do not irritate consumers of DB. So, banks or other private players should adhere to short and clear instructions to be provided on digital platforms for banking along with more options to select.

Women have trouble getting access to mobile phones and data packs. Equal pay scales provided by the government can increase their purchasing power, which lowers the cost of data and smartphones. Value has also had a smaller impact on women’s adoption of DB. Even though women bankers’ DFI has increased due to DB usage, DB penetration is still lower among them. Governmental policies can be formulated to ensure that women have access to the necessary facilities by conducting a survey at the regional or state level to determine the extent to which women use online banking services and the internet. The study’s conclusions may be helpful to everyone because the current research treated bankers as regular DB Banking customers.

Research Contribution

To the best of our knowledge, this is the first attempt to analyze the role of DB in DFI among the bank employees. The strength of the study lies in collaborating the concept of GDD with technology adoption and DFI, having evidence from higher path coefficient of male bankers (0.846) as compared to female bankers (0.818). The study examines GDD of bankers in spite being surrounded by latest technology of DB and having immense Financial Literacy. The study breaks the chain of monotonous studies related to customers’ adoption of technology and DFI; and inculcates the indispensable role of financial sector in DB adoption.

Research Limitations and Suggestions for Future Research Work

The study relies on selective sampling, which limits generalization; however, because the employees are from national banks, the study is pragmatic in terms of drawing concrete and practical conclusions. The study’s scope could be expanded by increasing the sample size. In the future, we may introduce blockchain technology to assess its impact on DFI. This study created a model to depict the relationship between GDD and DFI. Future studies can be conducted to validate the model developed in the current study to embrace DFI. Future research can be based on employees’ technology experience and their voluntary attitude toward digital technology adoption. These initiatives will help to accelerate the DFI and reduce the GDD.

Footnotes

Acknowledgements

Author is thankful to her mentor for guiding her through the process of manuscript formation. Also she is thankful to all the respondents who willingly responded to the survey questionnaire by giving a portion of their previous time.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Ethics Approval

No harm has been done to environment or any living being.

Data Availability Statement

In this study, primary data have been collected by the authors through a field survey. The data supporting this study’s findings are available from the corresponding author upon reasonable request.