Abstract

The novelty of this paper lies in the successful explanation and forecasting of carbon market from the perspective of crude oil attention. In this paper, based on the data on carbon futures and investor attention, several models are adopted to explore the role of crude oil attention on return and realized volatility in the carbon market. The empirical results are generalized as follows. First, crude oil attention granger causes the changes to carbon market, and besides, crude oil attention exerts significant negative impacts on carbon return while positive impacts on the realized volatility. Second, crude oil attention-based models improve the forecast accuracy for return and realized volatility in both short and long horizons and can surely bring investors with significant economic benefits. Third, this paper further confirms the nonlinear connections, the potential influencing mechanism, and subsample performances between crude oil attention and the carbon market. In summary, this paper broadens the framework of carbon pricing from investor attention and proves the importance of crude oil attention in the carbon market.

Introduction

Research Background

In recent decades, global climate issue has received extensive attention from governments and international organizations, thus, reducing carbon dioxide emissions have become one focus of the international community (J. Liu et al., 2023; Nawaz, 2021). In order to reduce carbon dioxide emissions and promote the development of low-carbon environmental protection, several measures are implemented. Among these activities, carbon emissions market is one of the most important means as the market shows outstanding advantages in lowing cost and promoting technology progress and market efficiency, and meanwhile, a well-designed carbon market relies on market-oriented financial means to solve the problem of carbon emissions, transferring technological issue to financial issue. Inside the fascinating carbon market, at least two points are worth noticing. First, due the financial characteristics of the carbon market in constructing financial portfolios, the participants in the carbon market are diversified, including individuals, funds, or institutional investors. Second, most of the allowances are allocated by the national government initially, but the companies specialized at renewable energy, reforestation and capturing greenhouse gases can also exert impacts on the market through carbon offset project; however, currently, with the development of the market, the carbon emission allowances have been gradually affected by marketization mechanism and are no longer only mandated by the authorities. Based on the above points, the carbon market is becoming increasingly focused by the international community, and major economies establish the carbon market, that is, the European Union, the United States and China, to reduce carbon emissions (C. Zhang et al., 2020; Y. J. Zhang et al., 2022; Q. Zhou et al., 2023). Inside all the operating carbon markets, the European Union carbon market shows significant advantages in system design, trading volume, and thus attracts numerous researchers (Dai et al., 2021; Hintermayer, 2020).

The design basis of European Union carbon market, namely the Kyoto Protocol, was expired in 2020, however, the market has still successfully entered the fourth stage in 2021 with the help of the Pairs Agreement. Compared with the previous stages, the fourth stage is more special. On the one hand, during this stage, the European Union requires an annual reduction of 2.2% in total carbon emissions and prohibits the use of carbon credits for offsetting, and after 2026, the free allocation quotas will be gradually abolished. On the other hand, major economies announced to achieve the carbon neutrality in the coming decades, which will inevitably have an impact on the operation of European Union carbon market. Against this background, as the largest carbon market, research on the European Union carbon market is still urgent.

Motivation and Research Questions

Current research on the European Union carbon market is unfolded through many aspects, for example, market mechanism design and impact of carbon market on the global financial system, etc. In numerous research areas, the financial characteristic of carbon prices is one of the focuses since it is a direct reflection of marginal abatement cost under current technical and economic conditions (Y. P. Zhang et al., 2022). Thus, a well understanding and more accurate forecast of carbon price are critical to measure the carbon mitigations. However, according to Segnon et al. (2017) and Zhao et al. (2018), current understanding and forecast for carbon price are not sufficient enough and many puzzles remain to be solved through empirical work, especially in complex and ever-changing environment nowadays, which may make the formulation of climate policies confusing. Thus, motivated by these puzzles, this paper chooses to explore the issue of how to explain and accurately forecast the carbon prices.

Actually, there has been a lot of research focusing on the puzzles regarding the carbon prices, scholars adopted diversified methods pursing an overall understanding and accurate forecast of carbon prices and argued that the information contained in energy related data is crucial to explain and forecast carbon prices (Bachmeier & Griffin, 2006; Duan et al., 2021; Zhao et al., 2018). Thus, discovering more factors based on energy data is important for both academia and industry. Since Merton (1987) put forward the first theoretical model of investor attention, the applications of investor attention become more and more extensive and numerous empirical evidence shows that investor attention plays an important role in financial area (Kou et al., 2018; S. Li et al., 2019). Given the importance of energy related data in carbon market, the energy related investor attention naturally becomes a potential important pricing factor for the carbon market. However, relevant studies are limited. Accordingly, the research questions of this paper are as follows. First, what are the roles of energy related investor attention on the pricing of carbon? Second, can energy related investor attention be used to forecast the carbon market? We believe that responding to these questions through careful and rigorous quantitative inquiry should contribute much to the existing literature in this area. Crude oil is an important impetus to the global economy; thus, this paper chooses the crude oil and unfolds the investigation of energy-related investor attention to carbon market in two perspectives, that is, return and realized volatility.

Marginal Contributions, Empirical Investigations, and Structures

This paper focuses on the connection between crude oil attention and financial characteristics of carbon market. To the best of our knowledge, this study contributes to the literature in the following ways. First, this paper provides another empirical evidence to certify that energy related data is crucial to carbon pricing, which further improved the research framework for the impact of the energy market on the carbon market. Second, this paper broadens the application field of investor attention in financial markets. Specifically, this paper demonstrates that attention on relevant markets can also affect the carbon market.

Detailed empirical procedure can be summarized as follows. First, this paper adopts several models to illustrate the linear effects of crude oil attention on carbon return and realized volatility. Second, this paper performs several out-of-sample forecasts. The results show that predictive models incorporating crude oil attention outperform the commonly historical average forecasting technology in both short and long horizons. Third, based on the results of out-of-sample forecasts for carbon return, this paper constructs financial portfolios to see whether investor attention of crude oil brings economic benefits for investors and the results show that the inclusion of the crude oil attention does improve the Sharpe ratio and the utility of the portfolio. Fourth, this paper explores and determines the nonlinear impact of crude oil attention on carbon market and the potential influencing mechanism from crude oil attention to carbon pricing. And furthermore, two subsamples are researched to guarantee the robustness of the results. To sum up, crude oil attention is an important factor in the carbon market.

The remainder of the paper is organized as follows. Section “Literature Review” provides a review on the relevant literature. Section “Data and Methodologies” presents the data and methodologies used in the paper. Empirical results for interpretation of carbon return and realized volatility is shown in Section “Results of Explaining Carbon Market from Crude Oil Attention.” The statistical and economic forecasts are shown in Section “Results of Forecasting Carbon Market from Crude Oil Attention.” In Section “Further Discussion,” nonlinear connection, potential influencing mechanism and subsample tests are explored. Finally, the conclusion of the paper is presented in Section “Conclusion.”

Literature Review

Since the establishment of the European Union carbon market in 2005, carbon market has quickly become one of the focal points of academia. Existing studies, on the one hand, focus on the financial characteristics of carbon market, that is, Montagnoli and De Vries (2010) focus on the volatility cluster; Y. J. Zhang and Huang (2015) investigate the multifractal characteristics; Y. Wang and Guo (2018) point out the asymmetry; B. Zhu et al. (2018) argue the non-linearity, etc.; on the other hand, focus on the influencing factor of carbon market, for example, Alberola et al. (2008) and Christiansen et al. (2005) argue that climate factors, such as temperature, rainfall and wind speed can affect the carbon market; Gronwald and Ketterer (2009) illustrate that policy factors affect the carbon market as the supply of carbon allowances is controlled by the authorities, etc. As the carbon market is currently regarded as a common financial market, the prediction in the carbon market also attracts numerous investigations. For example, B. Zhu and Chevallier (2017) and Huang et al. (2021) select the ARIMA and GARCH models, respectively. In order to capture the nonlinear relationship between variables, MS-GARCH, LSSVM-based model, EMD-LSSVAR-ADD and artificial neural networks have also introduced to carbon forecasting (Benschopa & López Cabreraa, 2014; Fan et al., 2015; B. Zhu, 2012; B. Zhu et al., 2017; B. Z. Zhu & Wei, 2011).

Actually, the energy market is also an important factor that affects the carbon market, as the carbon emission resulted by energy combustion is the main source of carbon dioxide (Gronwald et al., 2011; Y. Li et al., 2021; J. N. Liu et al., 2023; Yang et al., 2023; Yasmeen et al., 2020; Y. J. Zhang & Da, 2013). Accordingly, numerous investigations focus on the impacts of energy market on the carbon market. For example, Mansanet-Bataller et al. (2007) and Alberola et al. (2008) investigate the correlation between carbon market and energy market in the early stage and find that the carbon price is closely related to the price of oil and natural gas. The close relationship between carbon and energy markets is further identified by Y. Zhang et al. (2017) and Luo and Wu (2016). Recently, J. Liu et al. (2023) provide a comprehensive investigation on the connection between energy market and carbon market by DCC-MVGARCH and spillover index methods, the authors argue that there are indeed volatility correlations and bidirectional spillover effects for the two markets. Besides, the authors point out that the renewable energy market significantly impacts the carbon market.

In recent years, behavioral finance develops rapidly. From the perspective of limited rationality and market inefficiency, research has confirmed that investor attention plays an important role in asset pricing. For example, investor attention has been widely used in the stock market (Da et al., 2011; Wen et al., 2019; H. Zhou & Lu, 2023), the foreign exchange market (Han, Wu, & Yin, 2018), the cryptocurrency market (Ibikunle et al., 2020; C. Wang et al., 2022; P. Zhu et al., 2021), the agricultural market (Q. Zhou et al., 2022), the oil market (Han, Lv, & Yin, 2017; S. Li et al., 2019; X. Li et al., 2015), and has been proved to be an influential factor for these financial markets. Investor attention impacts the pricing of assets in different term structures and shows to be an important channel for cross-market spillover as well (Wan et al., 2023; Wu et al., 2019; Q. Zhou et al., 2022, 2023). Currently, scholars have introduced investor attention to the carbon trading market, for example, Y. P. Zhang et al. (2022), Y. J. Zhang et al. (2022), and Zheng et al. (2022). Investors also combine the investor attention with the machine learning to argue that market participants should pay attention to the occurrence of events on carbon quota supply and demand, carbon price, environmental change, and the energy market, as these factors may cause huge shocks to the carbon prices (Pan et al., 2023).

By reviewing the related literature on carbon market, energy market and investor attention, it is clear that, currently, application of investor attention is permeating to the field of carbon market, but is still limited, which may lead to deficiencies in the theories of carbon pricing. Considering the importance of energy related data in carbon market, this paper investigates carbon pricing from the investor attention on energy market to extend the framework of carbon pricing and the application of investor attention. Specifically, the detailed investigations are implemented through investor attention on the crude oil.

Data and Methodologies

Data

The purpose of this paper is to analyze the impact of crude oil attention on the carbon market and in order to perform this study, related data on crude oil attention and carbon market is obtained. For carbon market, as futures may be more sensitive to information (Chen et al., 2017), carbon futures prices during the period from February 27, 2017 to February 11, 2022 are downloaded freely from investing (https://cn.investing.com/). The price trend of carbon futures is shown in the following Figure 1. As shown in Figure 1, the carbon price shows a smooth upward trend before 2021. However, after the European Union carbon market enters the fourth stage in 2021, the carbon price has increased significantly, which may mainly relate to the European Union climate objectives and the “Fit for 55” climate legislation.

Carbon price from February 27, 2017 to February 11, 2022.

As for the data on investor attention, inspired by studies such as Vozlyublennaia (2014) and Han, Xu, and Yin (2018), this paper chooses the Google Search Volume Index (GSVI) as a measurement of investor attention. The index shows several advantages in measuring the investor attention. First, individuals preferred a diversified information, and search engines happen to be able to provide information from diversified sources. Second, Google is almost the most popular search engine worldwide. Third, compared with other indicators for investor attention, that is, excess return or turnover, search through Google can help to avoid artificial misleading. According to Google, the GSVI is constructed by the following formula, the index shows the percentage of search volumes on certain keyword relative to the total number of searches over a given period. Based on the advantages, characteristics, and numerous previous applications of GSVI, this paper also selects the indicator to represent the investor attention. In this paper, the GSVI is downloaded freely from Google Trends (http://www.Google.com/trends). Specifically, in the process of obtaining GSVI, this paper sets the search area to “global” and the searches for the keyword of “crude oil” during the period from February 27, 2017 to February 11, 2022. Data on crude oil attention with weekly frequency is obtained and transferred to log-difference for further empirical investigations.

This paper aims to explore two typical financial characteristics of the carbon futures market, that is, return and realized volatility. Thus, all the data is processed to weekly frequency. Specifically, we get weekly return by taking the weekly average of daily return and we construct a time series of weekly realized volatility RVt according to Dimpfl and Jank (2016) by the following equation (1).

Where

This paper constructs the analysis framework based on VAR model, which requires the time series to be stationary. However, the data sample ranges from 2017 to 2022, covering the non-negligible Covid-19 epidemic, which may result to potential structural breakpoints inside the time series. In other words, adopting one type of stationary test may be misleading. Thus, in this paper, an ADF-KPSS-PP-Zivot–Andrews joint test is adopted to certify the stationary status of the selected series. Inside the joint test, the Zivot–Andrews test comprehensively considers the potential breaks. Basic descriptive statistics and stationary test results on the weekly carbon return, weekly realized volatility and weekly crude oil attention are shown in Table 1.

Description Statistics and Stationary Test.

Note. Intercept, Trend and intercept, and None are three types of model specification in ADF-KPSS-PP-Zivot–Andrews joint stationary test.

and * represent significance at 1% and 10% level, respectively.

From Panel A in Table 1, it can be seen that the mean value of weekly crude oil attention is −0.0006, which indicates a decreasing trend of crude oil attention in general. The standard deviation of weekly crude oil attention is 0.2452, compared with other two series, the indicator means that the series is more violate, the results are further certified by the difference between the maximum and minimum value. The non-zero skewness and excess kurtosis of weekly crude oil attention further reflect a fact that crude oil attention can be regarded as a commonly financial time series. The results of Panel B, Panel D, and Panel E in Table 1 show that the initial hypotheses for ADF, PP, and Zivot–Andrews tests are rejected, Panel C shows that the initial hypothesis for KPSS is accepted, the four results jointly indicate that all the three series are stationary. As we seek to explore the role of crude oil attention in carbon forecasting as well, the full sample is divided. In this paper, we set the last 52 weeks to be out-of-sample period for evaluating forecast accuracy.

VAR and Granger Causality Test

Traditional economic and financial models were constructed on the basis of economic or financial theories, failing to provide a rigorous explanation of the correlation between the current status and the past status. In addition, endogenous variables can appear at both sides of equations, making it difficult to estimate parameters or infer characteristics. To overcome the above-mentioned problems, the VAR model is established, and soon becomes one of easiest models in financial analysis (Anggraeni et al., 2017). The VAR model is a linear regression model and is constructed by the lagged terms of all the endogenous variables. According to Balli et al. (2021), VAR model is widely used for estimating and forecasting financial time series, as the model includes a “lead-lag” relationship between variables. The standard formation of VAR model containing two variables is shown below.

In the above equations,

Interactive Relationship

Inspired by Vozlyublennaia (2014), there may exist a feedback mechanism between investor attention and asset return or realized volatility. Thus, in order to accurately track the impacts of crude oil attention on the carbon market, this paper introduces interaction terms between crude oil attention and return or realized volatility in the regression model. Specifically, the model is set up in the form shown in equation (4).

Where,

Joint Impacts with Other Assets

As noted by Ren et al. (2022), the carbon market condition is significantly affected by energy market. Besides, it has been proved that the capital market will also significantly affect the carbon market (Cao & Xie, 2023). In order to accurately capture the impact of crude oil attention on the carbon market, this paper introduces crude oil, natural gas and stock price index into the regression models. Specifically, the regression model can be generalized according to Han, Wu, and Yin (2018) and is shown in equation (5).

Where

Models and Indicators for Evaluating Forecast Accuracy

Considering the fact that the models represented by equations (2), (4), and (5) contain a “lead-lag” relationship, this paper extends these models for out-of-sample forecasting. Detailed models for predicting the carbon market by crude oil attention are show in the following equations (6) to (8). Specifically, when implementing these out-of-sample forecasts, the rolling window method is used.

Where h represents the forecast horizon. When evaluating the accuracy of forecasts, statistical indicators is adopted. In this paper, out-of-sample R squared (

Where T represents the length for the full sample period and window_size represents the length for regression window. The actual value is represented by

According to Rapach et al. (2010), an accurate forecast of asset return does not represent economic benefits. Thus, it is also an attracting issue to explore whether the predictive models can bring investor with significant benefits. In this paper, we do such explorations by constructing financial portfolios. Specifically, this paper supposes the investors who participate in asset allocation construct portfolio by the risky carbon asset and one risk-free asset. Besides, the investors are supposed to be risk-averse investors with mean-variance preference. According to Neely et al. (2014) and Y. Wang et al. (2018), the performance of the portfolio is evaluated by two indicators, that is, utility and Sharpe ratio (SR). Details on utility of the portfolio are shown below.

Where wt is the weight of the risky carbon asset in the portfolio, rt is the excess return, and γ denotes the risk aversion degree. Maximizing

Where

Results of Explaining Carbon Market from Crude Oil Attention

VAR

The key step in the process of VAR modelling is to select the lag length. In this paper, we quantified the optimal lag length according to several statistical standards such as AIC and SC, and the results are shown in Table 2. According to the results in Table 2, the optimal lag lengths are set to 3 and 4, respectively.

Selection Process of Optimized VAR Lag Length.

Note. LR = represents the sequential modified LR test statistic; FPE = final prediction error; AIC = refers to the Akaike information criterion; SC = Schwarz information criterion; HQ = Hannan–Quinn information criterion.

Indicates the lag order selected by the criterion.

Based on the selected lag lengths, this paper implements the VAR modelling and the corresponding Granger causality test, the results are shown in Tables 3 and 4, respectively.

Results of VAR Estimation.

Note. The value in the bracket is the standard error of the estimated parameter.

and *** represent the significant level of 5% and 1%, respectively.

Results for Granger Causality Test.

Note. *** represents the significant level of 1%.

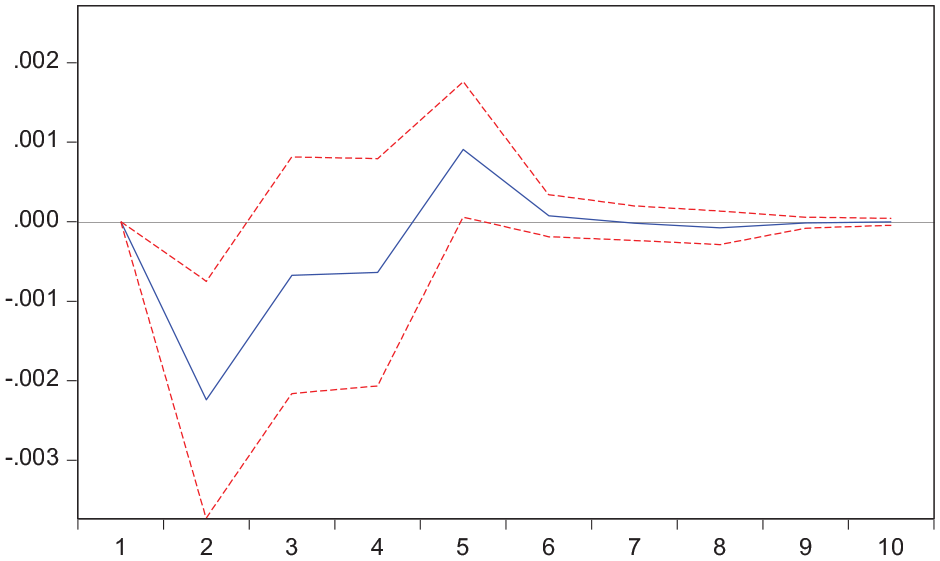

From the above results, it is apparent that crude oil attention has a significant negative impact on carbon market return as the coefficients for

Reaction of carbon return to crude oil attention.

Reaction of carbon realized volatility to crude oil attention.

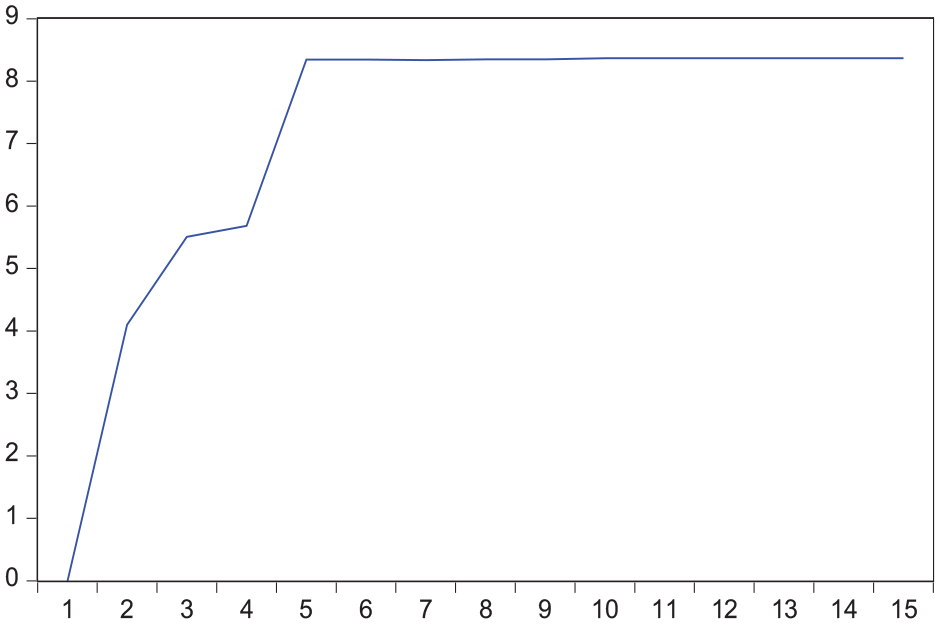

Variance decomposition can further evaluate the importance of different structural shocks by analyzing the contribution of each structural shock to the changes in endogenous variables under the VAR framework. Thus, this study implements the variance decomposition, and the related results are shown below in Figures 4 and 5.

Variance decomposition (carbon return).

Variance decomposition (carbon realized volatility).

Through the results shown in Figures 4 and 5, the contribution of crude oil attention to changes in carbon return remains stable at about 4.6%, while the contribution of crude oil attention to changes in carbon realized volatility remains stable at about 8.3%. The results (4.6% and 8.3%) further illustrate that crude oil attention plays an important role in the carbon market.

Interactive Effect

This paper estimates the equation (4) to capture the interactive effect between crude oil attention and carbon characteristics, and further certifies the importance of crude oil attention for carbon market. The results are presented in Table 5.

Results of Interactive Effects.

Note. The value in the bracket is the standard error of the estimated parameter.

, **, and *** represent the significant level of 10%, 5%, and 1%, respectively.

As can be seen in Table 5, the crude oil attention still shows a significant impact on carbon return and realized volatility after altering the model specifications. Specifically, crude oil attention shows a negative impact on carbon return while a positive impact on the realized volatility as some related terms in the regression model are significant. Besides, it is obvious that the interactive term of

Controlling Related Assets

Traditional financial markets, that is, oil market, natural gas markets and stock markets, have been proved to be important relevant factors influencing the carbon market. Therefore, this paper attempts to incorporate the relevant factors into the regression model to further explore the impact of crude oil attention on the carbon market. This paper estimates the equation (5) and shows the results in Table 6.

The Estimate Results of Joint Effects.

Note. Brent, WTI and Gas refer to the regression models that control the Brent oil market, WTI oil market and international gas market, respectively. Dow, Nasdaq, and Dax refer to the regression models that control the Dow Jones Industrial index, NASDAQ index, and German DAX index, respectively. The value in the bracket is the standard error of the estimated parameter. Panel A refers to carbon return and Panel B refers to the realized volatility.

, **, and *** represent the significant level of 10%, 5%, and 1%, respectively.

Several interesting findings can be drawn from Table 6. First, crude oil attention is still significant after introducing the related markets as control variables for both return and realized volatility. In other words, crude oil attention can significantly explain the return and realized volatility, and is still an important pricing factor for the carbon market; Second, the effect of crude oil attention on carbon return remains significantly negative, while the effect on carbon realized volatility remains significantly positive, which is consistent with the results in previous sub-sections; Third, in this empirical investigation, energy markets do not influence the carbon return as all the parameters for energy market are insignificant, however, the stock market shows to be an important factor for carbon return; Fourth, both energy markets and stock markets are non-negligible factors for the realized volatility in carbon market, as all the related coefficients are significant; Fifth, the interaction items between the energy markets and crude oil attention, as well as the interaction items between the stock markets and crude oil attention, are crucial factors for carbon pricing as related items are significant.

In summary, crude oil attention shows significant explanatory power in the carbon market. The interesting findings on the negative and positive impact of investor attention on asset return and realized volatility is similar with previous studies (Andrei & Hasler, 2015; Wan et al., 2023; Q. Zhou et al., 2023) and may be explained by the following reasons. Once the crude oil attention increases, it may be attributed by several reasons. The first reason may refer to the uncertainty production of crude oil. Given the fact that the crude oil is a typical heavy industry, which needs a long time to generate benefits, potential capitals exit the industry to avoid potential risks. Considering the profit seeking nature of capital, the capital enters one industry which can provide continuous and stable income, for example, the stock market or the gold market, driving up the prices of these markets. The carbon trading market is still an emerging market, which may not be impressive by investors. Thereby, partial capital exits the carbon market for more profits in other markets, resulting a decrease in carbon return. The second reason may refer to the rapid development of renewable energy technology. As an alternative to fossil fuels, once breakthrough progress is made in renewable energy technology, the crude oil market is inevitably become a focus in the world energy market in addition to the renewable energy. The breakthrough progress may on the one hand, reduces the demand for crude oil as well as the carbon allowances, resulting the carbon return to decrease; on the other hand, the progress makes the renewable energy companies to be undervalued, capital may flow from carbon market to renewable energy market for profits. Third, the sudden increase of crude oil attention indicates that the crude oil market is under the impact of unpredictable events, which may represent the global economy is suffering recession or slowdown in growth rate, this will lower people’s expectations on the oil market and the demand for crude oil, reducing the demand for carbon allowances and carbon return. Maybe due to the above reasons, the crude oil attention and carbon return is negatively connected. As for the realized volatility in the carbon market, due to the herding effect, investors may follow the judgment of the whole market and make irrational trading decisions. As a result, the trading activities of investors in the carbon market tend to be consistent, which is bound to increase the realized volatility in the carbon market. Meanwhile, with the development of information technology, obtaining public information through internet search engines tends to be cost-free, which may further increase the herding effect (Han, Li, & Yin, 2017), resulting a positive connection between crude oil attention and realized volatility.

Till now, based on the empirical investigations in Section “Results of Explaining Carbon Market from Crude Oil Attention,” the first research question can be answered that energy related investor attention, that is, crude oil attention, generates negative impact on carbon return and positive impact of carbon realized volatility.

Results of Forecasting Carbon Market from Crude Oil Attention

Statistic Forecasts

On the one hand, return forecasting is a non-negligible aspect for asset pricing, on the other hand, a good explanatory ability does not mean a good predictive ability (Welch & Goyal, 2008). Thus, it is also an interesting issue to explore whether crude oil attention can be used to predict the carbon market for the return and realized volatility. And besides, the regression models may be over-fitted (Y. Wang et al., 2018), resulting the empirical results to be less convincing. Thus, in this part, we implement some out-of-sample forecasts to further explore the role of crude oil attention in carbon pricing. Specifically, this paper implements a basic empirical investigation to forecast the return and realized volatility in the next period. In other words, we set the parameter of h in equations (6) to (8) to 1. The related results are shown in the following Table 7.

Results for Basic Out-of-Sample Forecasting.

Note. VAR and interactive represent the forecast results by equation (6) and (7), respectively. Brent, WTI, Gas, Dow, Nasdaq, and Dax refer to the regression models that control the Brent oil market, WTI oil market, international gas market, Dow Jones Industrial index, NASDAQ index, and German DAX index, respectively. The six models represent the forecast results by equation (8).

and ** represent the significant level at 10% and 5%, respectively.

From the basic results for out-of-sample forecasting, it is obvious that models incorporated with crude oil attention can beat the commonly used forecasting technology. Specific to the results for carbon return forecasting, predictive model that controls the gas market has the best performance as the

Along with the case to forecast the return or the realized volatility in the next period, this paper implements the so-called long horizon forecasts by setting the parameter of h to 2, 3, and 4, respectively (Wan et al., 2023; Q. Zhou et al., 2023). The maximized value for h is 4, as commonly, it is assumed that 1 month contains 4 weeks. Detailed results for the long horizon forecasts are shown in the following Table 8. As shown below, when forecasting the carbon market for its return and realized volatility, the results are similar with the basic out-of-sample forecast.

Results for Out-of-Sample Forecasts in Long Horizons.

Note. Panel A, B, and C represent the results for the parameter of h to 2, 3, and 4, respectively.

, **, and *** represent the significant level of 10%, 5%, and 1%, respectively.

Economic Forecasts

This paper constructs financial portfolios by all the predictive models and the benchmark model to explore whether crude oil attention can bring economic benefits for investors. In order to make the results closer to real transactions, transaction cost (b_cp) is introduced and set to 0 and 10 according to P. Zhu et al. (2021). Besides, according to Wan et al. (2023), the parameter of

Results for Economic Benefits.

Note. Brent, WTI, and Gas refer to the regression models that control the Brent oil market, WTI oil market and international gas market, respectively. Dow, Nasdaq, and Dax refer to the regression models that control the Dow Jones Industrial index, NASDAQ index, and German DAX index, respectively.

Till now, based on the empirical investigations in Section “Results of Forecasting Carbon Market from Crude Oil Attention,” the second research question can be answered that energy related investor attention, that is, crude oil attention, can be used to forecast the carbon market for both statistical and economic levels.

Further Discussion

Nonlinear Connection

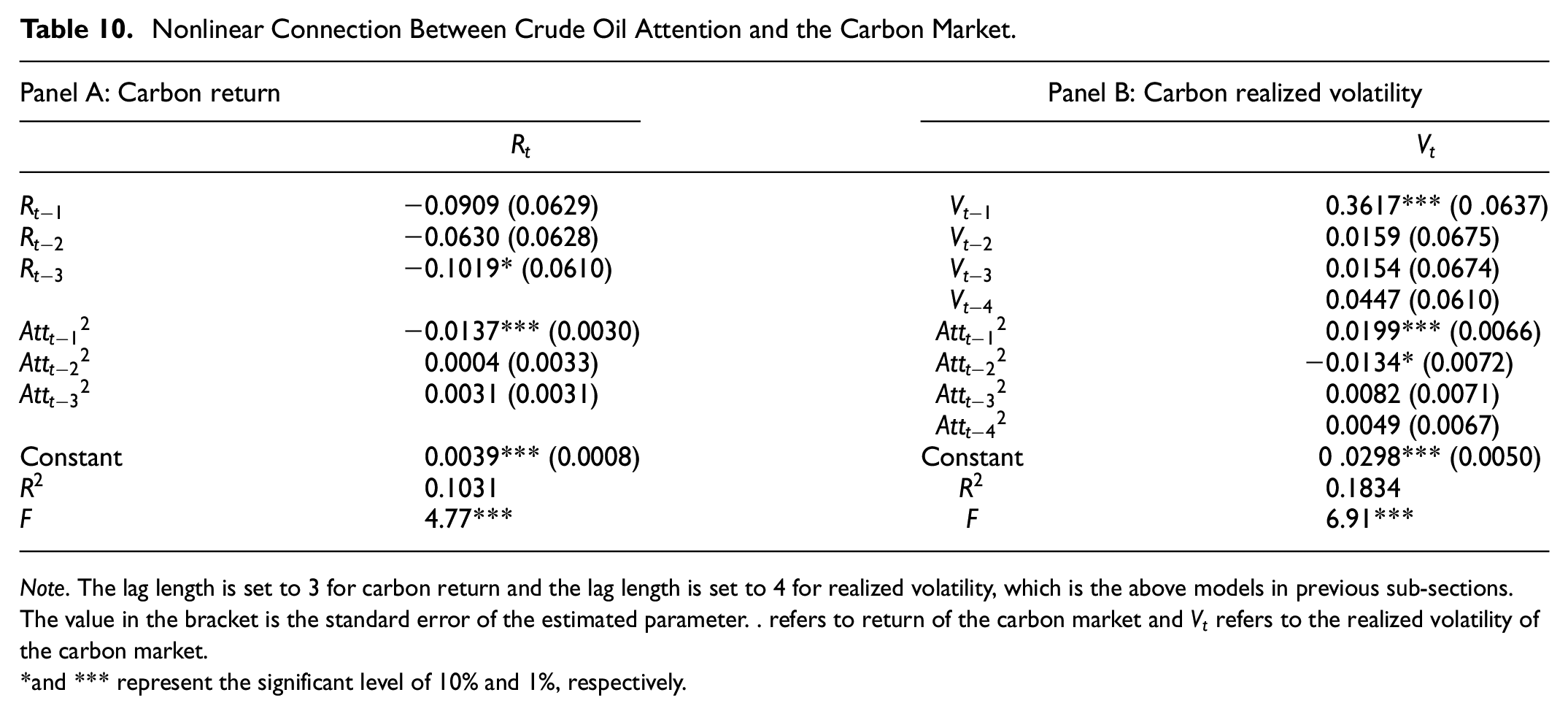

All the above analyses demonstrate that crude oil attention is an important factor in the carbon market and shows linear impact on the determination of return and realized volatility. However, the impact from investor attention to financial market seems more complicated with some nonlinear impacts (Y. P. Zhang et al., 2022). Thus, this paper constructs the following model specification (13) to explore whether nonlinear connection exists between crude oil attention and characteristics in the carbon market. The estimation results for equation (13) are shown in Table 10. As can be seen, in addition to the linear impact of crude oil attention on carbon return, crude oil attention shows an invert U-shaped impact on carbon return as

Nonlinear Connection Between Crude Oil Attention and the Carbon Market.

Note. The lag length is set to 3 for carbon return and the lag length is set to 4 for realized volatility, which is the above models in previous sub-sections. The value in the bracket is the standard error of the estimated parameter. . refers to return of the carbon market and

and *** represent the significant level of 10% and 1%, respectively.

Influencing Mechanism

All the above analyses demonstrate that crude oil attention affects the financial characteristics of the carbon market. However, the influencing mechanism remains unknown which is still an interesting issue to be explored. Given the close connection between the oil market and the carbon market as well as one theory in behavior finance that investor attention affects trading activities; this paper assumes that crude oil attention affects the carbon market through trading volume in the oil and carbon market. This paper attempts several paths based on trading volume to connect the crude oil attention and carbon market and finally determines the following. First, crude oil attention affects the increment of weekly trading volume in the oil market. Then, the increment affects the growth rate of trading volume in the carbon market. Finally, the variation in the trading volume affects the financial characteristics of the carbon market. Detailed empirical model specifications are shown in equations (14) and (15), where

Influencing Mechanism from Crude Oil Attention to Carbon Characteristics.

Note. The influence from trading volume in one market to its financial characteristics has already been illustrated and is not tested in this paper (Foster & Viswanathan, 1993).

and *** represent the significant level at 5% and 1%, respectively.

Subsample Investigation

In this paper, the sample period ranges from 2017 to 2022. Obviously, the sample period covers the non-negligible Covid-19 period. Thus, in this subsection, the full sample is divided to two subsamples to further investigate the impacts of crude oil attention on the return and realized volatility of carbon asset. The first subsample is located before the epidemic while the second is located after the epidemic. In the detailed settings of subsamples, both epidemic and macro factors have been fully considered, ultimately, the pre-epidemic subsample is set to the period from September 2017 to March 2020, and the post-epidemic subsample is set to November 2020 to November 2021. Such setting is for the following reasons. First, in September 2017, the Federal Reserve of the United States announced that it will start to reduce its balance sheet in October, which is an event that has a significant impact on the global economy, the carbon asset, as a financial asset, is inevitably affected; Second, the United States declared a state of emergency due to Covid-19 in March 2020; Third, due to the spread of Covid-19 in the EU, several countries announced blockade policies and warned that their economies were facing recession in November 2020; Fourth, there are many international events on climate change in November 2022, for example, all parties have reached a consensus on the implementation details of the Paris Agreement. Based on the two subsamples, the correlations between crude oil attention and carbon characteristics are re-visited. Specifically, two types of empirical investigations are implemented on the two subsamples.

First, this paper implements the granger causality test and the corresponding VAR analysis on the subsample which is same with the above subsections. The detailed estimation results are shown in Table 12.

VAR Analysis and Granger Causality for Subsamples.

Note. The value in the bracket is the standard error of the estimated parameter. .

, **, and *** represent the significant level of 10%, 5%, and 1%, respectively.

Through the above results, it can be discovered that no matter which subsample it is considered, crude oil attention surely exerts a negative impact on carbon return, and a positive impact on the realized volatility of carbon asset.

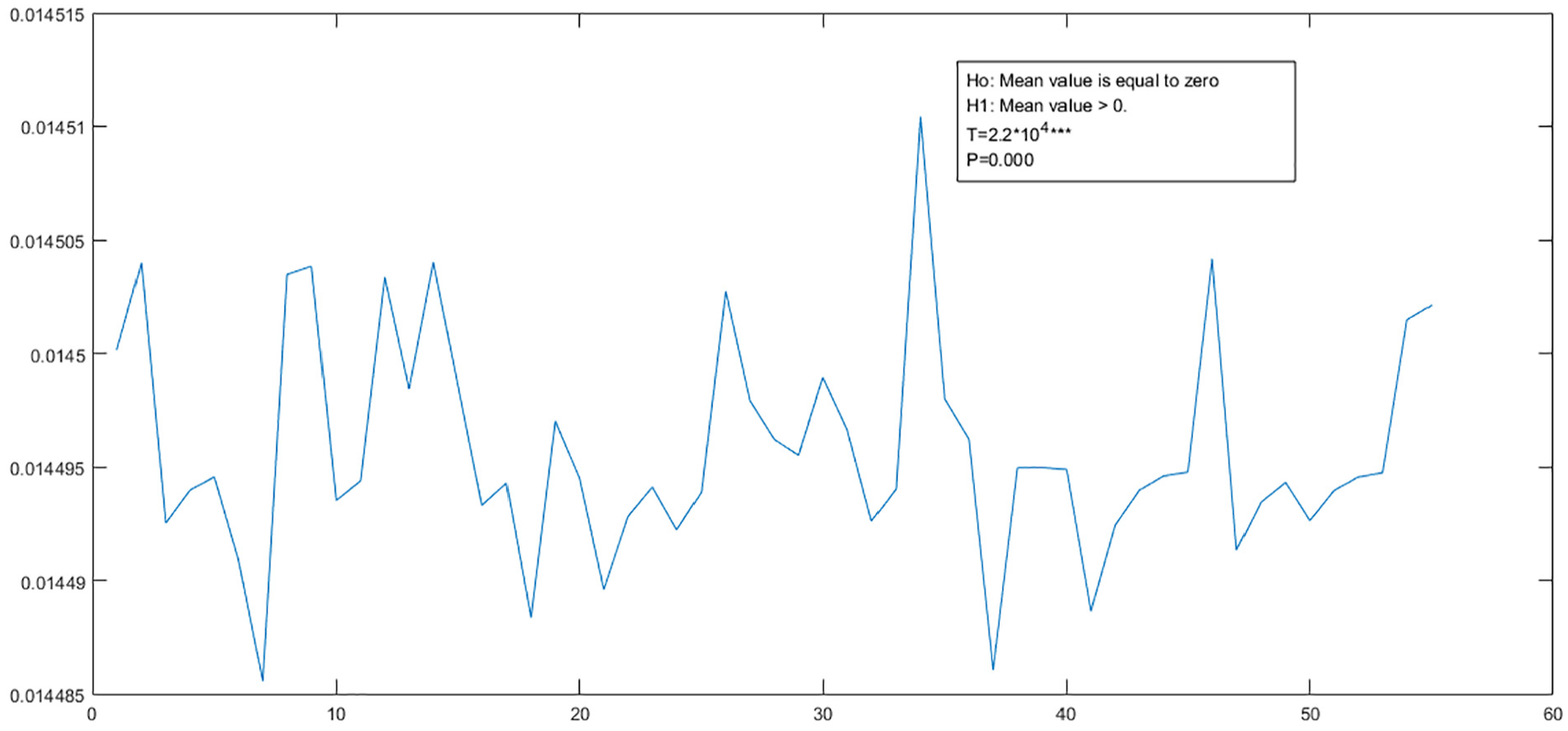

Second, according to J. Liu et al. (2023), a VAR based model is limited to static measurement of the correlation rather than a dynamic correlation. Thus, it is inadequate to measure the potential connections between crude oil attention and carbon return or realized volatility only by VAR model. Thus, on the basis of J. Liu et al. (2023), this paper implements a dynamic correlation coefficient (DCC) analysis to further identify the correlations between crude oil attention and carbon market. Specifically, this paper constructs DCC-GARCH model for each subsample to investigate the dynamic correlation between crude oil attention and carbon return, and the dynamic correlation between crude oil attention and carbon realized volatility. The related results are shown in Figures 6 to 9.

Dynamic correlation between crude oil attention time series and carbon return time series pre Covid-19.

Dynamic correlation between crude oil attention time series and carbon realized volatility time series pre Covid-19.

Dynamic correlation between crude oil attention time series and carbon return time series post Covid-19.

Dynamic correlation between crude oil attention time series and carbon realized volatility time series post Covid-19.

Obviously, the mean value of the dynamic correlation coefficient series between crude oil attention and carbon return is statistically negative, while the mean value of the dynamic correlation coefficient series between crude oil attention and carbon realized volatility is statistically positive. To sum up, the results for the subsamples are same as the full sample, which further demonstrates that the results in this paper are robust.

Conclusion

When individual investors pay more attention to news events, information will be quickly reflected in asset prices, causing variations in asset return or realized volatility. The formation of a global consensus on low-carbon environmental protection provides a unique setting to example the carbon market response to investor attention. Given the close relationship between carbon and energy, this paper connects the crude oil attention and the financial characteristics in the carbon market, that is, return and realized volatility. Utilizing GSVI for “crude oil” as a proxy for crude oil attention, this paper shows that crude oil attention generates a negative impact on carbon return and a positive impact on the realized volatility. The impacts hold even after altering the model specifications. Furthermore, this paper empirically identifies that crude oil attention improves the forecast accuracy and can bring investors with more utility and Sharpe ratio. Finally, this paper implements a further discussion from three aspects and argues that crude oil attention exerts nonlinear impacts on the carbon market; the impact from crude oil attention to financial characteristics in the carbon market has occurred through trading volumes in the crude oil market and carbon market; the negative and positive impacts remain robust for subsamples.

Inspired by the above findings, this paper gives the following recommendations to the carbon market participants. First, regulators in the carbon market should not only focus on traditional sources of risk, but also the social opinion orientation. Policy makers should formulate reasonable policies when necessary to prevent risks from being transmitted from public opinion to the carbon market. Second, investors may refer to the easily obtained GSVI and the simple VAR-based linear model to get an accurate forecasts of carbon market. Based on these forecasts, investor is able to generate benefits or construct the desired portfolios.

To sum up, our results indicate that the energy related investor attention, that is, crude oil attention, retrieved from GSVI is an important factor in the carbon market, which further highlights the importance of energy market and investor attention in carbon pricing. However, potential deficiencies exist. For example, the sign of the causality is not discussed in this paper, adopting more sophisticated models to certify the sign can be explored in future research; spillover index methods are currently popular econometric methods in analyzing the connections between variables, as the methods quantify the magnitude of spillover, the methods deserve in-depth investigations; According to J. Liu et al. (2023), renewable energy market becomes an important influencing factor to the carbon market, exploring the renewable energy market-based investor attention’s roles in the carbon market is also an interesting question; The basic VAR model only requires the time series to be stationary, the model does not take the potential structural breaks in financial time series into consideration, the problem should be focused either. At least the four above mentioned deficiencies are worth researching.

Footnotes

Acknowledgements

We would like to express our great thanks to the editors and reviewers for their helpful suggestions to improve the quality of this paper. Any remaining errors belong to the authors.

Author Contributions

Panpan Zhu implements the empirical process in this paper and writes the original manuscript. Panpan Zhu provides the methodologies used in this paper. Yinpeng Zhang provides the idea and polishes the paper. Panpan Zhu collects the data and revises the original manuscript. All authors read and approved the final manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work is supported by Natural Science Foundation of Shandong (ZR2024QG157) and the Research start-up funds for talents in Taishan University.

Data Availability Statement

The data on carbon futures can be freely downloaded from Investing (https://cn.investing.com/). The data on investor attention can be freely downloaded from Google Trends (![]() ).

).