Abstract

Grassland ecosystems play a pivotal role in mitigating climate change via CO2 sink. However, establishing robust methodologies for grassland carbon sink valuation remains complex scientific challenge. This study proposes an innovative application of fair value accounting principles to grassland carbon sink measurement, providing a multidimensional framework for ecological asset valuation. We develop a comprehensive theoretical foundation for fair value measurement through three analytical perspectives: cost-based, market-oriented, and income-driven valuation paradigms. Consequently, three valuation approaches are formulated: the Marginal Opportunity Cost (MOC) Method, Shadow Pricing (SP) Method, and Option Pricing (OP) Method. Through scenario-based comparative analysis, we demonstrate that methodological selection should be guided by carbon sink projects’ development stages and valuation objectives. Specifically, MOC excels in preliminary carbon pricing during project initiation phases, SP is optimal for mature primary markets with established transaction histories, while OP exhibits superior technical capabilities for projects’ future value estimation in secondary market transactions. This study provides practical insights for realizing ecological product value, advancing carbon market operations, and contributing to global climate change mitigation efforts.

Keywords

Introduction

In recent years, the frequent occurrence of extreme weather events globally, such as droughts, heatwaves, and typhoons, has drawn serious attention to the greenhouse effect and the subsequent rise in CO2 emissions. Environmental issues and sustainable development in the current situation have been concerned (D. Gao et al., 2024). Ecosystems offer an alternative for carbon removal alongside industrial emission reductions. Oceans, forests, and grasslands act as carbon sinks by storing and processing carbon. The grassland, the largest terrestrial ecosystem globally, has been recognized as vital for its significant functions in carbon sequestration. Globally, grasslands store approximately 34% of terrestrial ecosystem’s total carbon stock, forests store approximately 39%, and agroecosystems approximately 17% (White et al., 2000, p. 5). The total amount of global soil carbon sink of grassland is close to that of forests and higher than that of farmland (Scurlock & Hall, 1998; White et al., 2000, pp. 1–5). In the ecological aspect, the carbon sink functions of grassland ecosystem are applied through increasing vegetation restoration, reasonable livestock carrying and management, and utilization methods to increase the net positive value of carbon sinks (J. Chang et al., 2021). Economically, the global carbon market enables trading of carbon credits from sinks. Trade income supports grassland restoration. Maximizing grassland carbon sinks fosters sustainability and social benefits. For instance, the European Union requires that grassland management projects related to vegetation utilization and livestock carrying capacity consider grassland’s carbon sink function (Dasselaar et al., 2019, pp. 109–122). Carbon sink projects provide environmental and economic benefits by managing carbon emission rights (D. A. Gao et al., 2024)

Accurately valuing grassland carbon sinks and integrating them into the carbon market supports sequestration and financial returns in animal husbandry. This provides states with a new capital source for sustainability goals (Newell & Paterson, 2020). A key challenge in carbon credit trading is precisely valuing grassland carbon sinks. There is still an ongoing discussion on how to accurately determine the exact value of carbon sinks in different ecosystems. For grassland carbon sink, research lacks systematic valuation methods for different development stages and markets. The traditional measurement methods of ecosystems’ carbon sinks, such as the “market value method” and “substitution method,” are primarily applied to forest carbon sink evaluation. Applying these methods to grasslands risks misvaluation due to differences from forests (FAO, 2010, pp. 1–51). Market value and substitution methods are static, reflecting only daily market conditions. They cannot reflect the dynamic situation of carbon sink projects during different development stages. Inadequate valuation hinders carbon sink trading’s role in carbon reduction. Therefore, it requires additional studies on advanced evaluation methods for grassland carbon sinks based on the specific characteristics of the projects (Cao et al., 2020; Liu et al., 2022; Petrokofsky et al., 2012).

The accounting concept of “fair value” has recently gained interest in carbon sink valuation. It represents “an orderly transaction” that has taken place in the market with the unique advantage of dynamically referencing the development of ecosystem protection. According to IFRS13, the fair value measurement assumes the transaction under an orderly market with sufficient time and information, and no forced transaction to make buyers accept the price offered by sellers (ACCA, 2023). Grassland carbon sinks are valued as fair value in active markets. When the market is inactive, valuation measurements are required. In such cases, the first step is to discuss the rationale for fair value measurement of grassland carbon sinks. Subsequently, aligning grassland carbon sinks with livestock production based on practical conditions, the applicability of different valuation methods is explored and compared, with the estimated values serving as an ideal reference for fair value. The measurement methods could be organized by using multiple functions under its certain measurement process or frameworks (ACCA, 2023; Y. Chen et al., 2018; Zhuang et al., 2022). Fair value measurement can enhance carbon sink management and promote the carbon credit trade.

This study explores the optimal fair value measurement methods for grassland carbon sink projects, proposes a systematic framework for their application, and identifies key implications for sustainable development.

We address following research questions:

This paper contributes to existing research as follows: First, existing research overlooks the dual ecological and economic attributes of grassland carbon sinks. This paper integrates grassland carbon sink valuation with livestock production, applying labor, market factor, utility, and equilibrium value theories. Grassland carbon sink valuation is shaped by ecological, economic, and social values. Second, existing research has not systematically constructed a framework for the fair value measurement of grassland carbon sinks in different conditions. This paper proposes a theoretical framework for fair value measurement of grassland carbon sinks based on accounting standards IFRS 13 by the International Accounting Standards Board—IASB (IFRS, 2024a). From the perspectives of cost, market, and income, this framework introduces the marginal opportunity cost, shadow pricing, and option pricing methods, respectively. Third, existing research lacks consideration of selection methods for different project stages. Based on a discussion of the practical applications of the marginal opportunity cost, shadow pricing, and option pricing method, we suggest that the valuation method for fair value measurement can be selected according to the stage of the carbon sink projects and the purpose of the measurement.

Literature Review

With the growth of global carbon trading, accounting for carbon sink value is increasingly important. However, no unified standard exists for carbon sink valuation internationally. Measurement methods remain a key research challenge (Liu et al., 2022). Grassland carbon sink pricing depends on selecting appropriate measurement methods. The main research contents can be broadly divided into the following categories:

Importance of Grassland Carbon Sinks and Factors Affecting the Value Measurement

Scurlock & Hall (1998) highlighted the importance of measuring both aboveground and belowground components of the carbon cycle and the need to establish an independent system for evaluating the impact of global grassland ecosystems. Ren et al. (2011) highlighted the role of grassland carbon stocks in climate change mitigation and sustainable use. Ni (2002) used the carbon density method to find that alpine grasslands, alpine meadows, and temperate grasslands accounted for 14.5%, 25.6%, and 11% of total grassland carbon storage, respectively. Lyu et al. (2023) quantitatively evaluated the temporal and spatial dynamics of NPP, NEP, and carbon sink capacity of vegetation in the Weihe River Basin from 2001 to 2020. Geng et al. (2024) quantified the spatial and temporal changes and net ecosystem productivity carbon sink patterns of the Qinghai-Tibet Plateau grasslands from 2001 to 2019 using MODIS NPP data and a soil respiration model. They revealed that climate change impacts grassland carbon sinks and sources. Optimizing grassland management enhances carbon sinks. R. Zhang et al. (2020) pointed out that rainfall is the most critical factor affecting grassland carbon sequestration. Y. Zhang et al. (2024) identified key factors for carbon sinks, including climate, grazing, grassland degradation, and land use. Sustainable enhancement of grassland carbon sinks requires coordinated ecological-production-living systems.

Carbon Sink Value Measurement—Substitution Methods

Early research commonly used substitution methods to estimate ecosystem carbon sink value. These methods included afforestation cost, industrial oxygen production, carbon tax, market value, and net present value methods. Li and Ren (2011) applied afforestation cost and industrial oxygen production cost methods to estimate the distribution characteristics, changes in carbon sink value, and oxygen release value in the Loess Plateau of northern Shaanxi. Cao et al. (2020) studied the costs and influencing factors of afforestation and reforestation in China by applying the land opportunity cost method. They found afforestation carbon sink costs exceeded average prices, posing significant risks. Zhao et al. (2012) estimated the carbon sink value of grasslands in Xilinhot City using its cost price based on the afforestation cost method. Kong and Zhang (2014) used the carbon tax method to estimate the carbon sink value of protected wetlands, providing a reference for wetland carbon sink functions. Pang et al. (2014) employed the market value method to assess the carbon storage service value provided by the alpine wetlands in Zoige Nature Reserve in West China. However, Y. Yu et al. (2019) proposed that the net present value (NPV) method is more practical than other valuation methods. NPV positively correlated with discount rates and carbon prices, illustrating the example of forest and grassland soil carbon sinks in the Qinling region. These methods relying on substitution functions only confirm that carbon sinks have value. The exact carbon sink value remains uncertain due to estimation limitations. Currently, carbon sinks are participating in market transactions as a new production factor. It is necessary to explore more independent and reliable valuation methods based on the formation process and nature of carbon sink projects.

Carbon Sink Value Measurement—Asset Value Measurement

Ecosystem carbon sinks are now measured as natural resource assets. X. Zhang and Wang (2004) proposed that fair value measurement and historical cost measurement are not mutually exclusive, thus a mixed model can be adopted depending on the measurement purpose. Bai and Zhang (2011) emphasized the importance of carbon sinks accounting as assets for trading. The initial measurement of forestry carbon sink projects should use the cost method, with subsequent measurements using fair value or government pricing. J. Wang and Niu (2013) analyzed the asset properties and value influencing factors of forest carbon sinks. They discussed the advantages and disadvantages of using cost, market, and income approaches to evaluate the value of forest carbon sinks. Jia et al. (2015) suggested promoting the measurement of carbon sink value from the perspective of improving biological asset standards. They recommended adding carbon sink asset accounting to biological asset standards. Apply physical quantity measurement in the early stages of carbon sink trade, and then switch to value-based accounting when trading conditions mature. Y. Chen et al. (2018) assessed forestry carbon sinks’ fair value for enterprises, and argued the cost method is unsuitable for forest carbon sinks. Liu et al. (2022), while emphasizing the importance of carbon sink accounting measurement, proposed that the accounting of forest carbon sinks could consider the fair value measurement model. Y. Chen et al. (2023) proposed a set of approaches for forest carbon sink valuation, including the market approach and fair value method. Xiao et al. (2023) emphasized that forming, promoting, monitoring, measuring, verifying, and trading forest carbon sinks have become more significant research areas.

Carbon sink valuation has shifted from substitution to asset-based methods, improving specificity and applicability. Therefore, providing a methodological foundation for the fair value measurement of grassland carbon sinks is necessary. However, existing research lacks a unified standard and consists of theoretical discussions rather than forming a systematic analytical framework. A significant challenge remains in selecting optimal calculation approaches for the fair value of grassland carbon sinks due to the heterogeneity of carbon sink projects. Studies are urgently needed to develop dynamic measurement processes and methodological frameworks for selecting and applying the optimal calculation approaches based on development stages of carbon sink projects (Sommer et al., 2022; Y. Wang & He, 2022; X. Zhang & Wang, 2004). Forest carbon sink accounting is well-studied, but grassland valuation lags behind. This discrepancy is related to the dual ecological and economic production attributes of grassland carbon sinks. Grassland carbon sink accounting should integrate with livestock production, distinct from forestry valuation. This integration is also the entry point and innovation of this study.

Theoretical Foundation

Value of Natural Resource

Fair value analysis of grassland carbon sinks is based on four natural resource valuation theories: labor, production factor, utility, and equilibrium value. Labor value theory measures a commodity’s worth by labor time, extending to natural resources through human involvement in their use and protection (X. Yu, 2010). Production factor value theory views natural resources as essential for production and living. Utility value theory links resource value to scarcity and human demands (Y. Xu, 2005). Equilibrium value theory sets resource prices based on supply and demand (J. Wang et al., 2010). However, market-based valuation of public goods often leads to failure and inaccuracies (G. Zhang & Zhang, 2003). A sustainable approach requires improved natural resource valuation.

Grassland carbon sinks possess both ecological and economic attributes. Their value composition includes economic, ecological, and social value. They also possess characteristics of scarcity, public goods, and externality. For grassland carbon sinks, their economic value is reflected by the economic benefits from the marketization of carbon sink products. Their ecological value is reflected by the benefits of mitigating global greenhouse gas effects and improving human living quality. Their social value is reflected in the sustainable development of regional economies and the improvement of overall social welfare. These three values need be integrated into valuation frameworks.

Price of Grassland Carbon Sinks

The FASB issued “Fair Value Measurements” (FAS157) in 2006, IASB introduced “IFRS 13 Fair Value Measurement” in 2011, and China’s Ministry of Finance revised “Enterprise Accounting Standards No. 39 - Fair Value Measurement” (CAS39) in 2014. These standards uniformly define fair value as the price received for selling an asset or paid to transfer a liability in an orderly market transaction (CAS, 2014; FASB, 2024; IFRS, 2024a; Ronen, 2012; D. Wang et al., 2017). Accordingly, fair value measurement first requires a market. Secondly, market participants must conduct orderly transactions between sellers and buyers. These transactions clearly reflect carbon sinks as assets or liabilities with accounting attributes for trade. If the market participants agree that the market transactions of carbon sinks are orderly, the transaction price is considered the fair price. If the market cannot be considered orderly or is inactive, the measurement and estimation of the fair value of carbon sinks is required.

The “cost, market, and income” approaches of IFRS 13 are widely used, especially in inactive markets (Cozma, 2015; IFRS, 2024a, 2024b). IFRS 13 outlines their definitions and characteristics. The “cost approach” reflects the amount required to replace the service capacity of an asset at the current time, also known as the replacement cost method. The “market approach” determines fair value primarily based on the market transaction prices of identical or comparable assets or liabilities. The “income approach” converts future income (such as cash flows or earnings) into a single discounted present value, reflecting current market expectations. It can apply the models of present value, option pricing, binomial, and multi-period earnings for pricing. Grassland carbon sinks, as environmental resource products, can be valued using cost, market, and income approaches. Different fair value measurement methods apply to diverse carbon sink projects.

Research Method

This study employed four key research components: (1) accounting attributes and market transactions of grassland carbon sinks; (2) fair value estimation functions; (3) carbon sink pricing perspectives under different conditions; and (4) frameworks for selecting optimal measurement methods. There are following research steps in this paper.

To develop the valuation model, grassland carbon sinks must be assessed as assets with market transaction status. Grassland carbon sinks’ value as a natural resource underpins the accounting attribute analysis. Following IFRS 13, grassland carbon sinks’ fair value is based on active market transactions; when inactive, valuation is required.

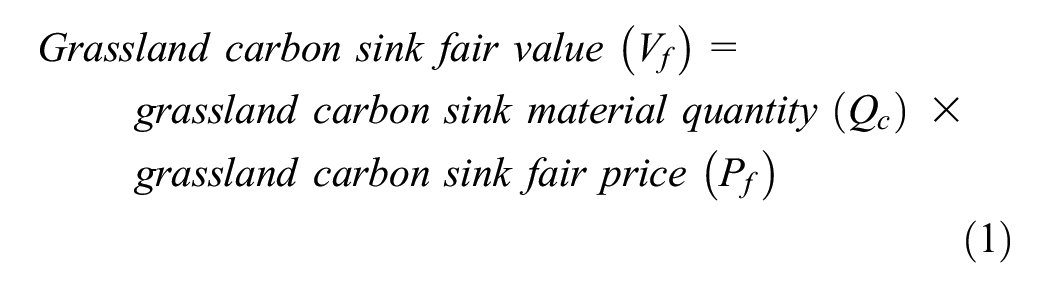

Once grassland carbon sinks qualify as assets with fair value attributes under IFRS 13, their valuation follows this formula.

Equation 1 serves as the base formula for fair value measurement of grassland carbon sinks. Total fair value (Vf) depends on total quantity (Qc) and unit fair price of the grassland carbon sinks (Pf). Qc measured through ecological calculation. The carbon sinks generated by carbon sink projects are converted into carbon credits for trading purposes. Carbon sink formation involves absorption by above-ground vegetation and transformation via plant roots. Natural factors like temperature and precipitation must be considered. Economic and social factors (e.g., resource use, human activity, and livestock capacity) influence grassland carbon sinks and must be included in quantity estimation. Fair value measurement of grassland carbon sinks is tied to sustainable animal husbandry. This study focuses on determining the unit fair price Pf, incorporating ecological and economic factors. Grassland carbon sinks as assets, along with global carbon market growth, enable fair price assessment. The IFRS13 provides the theoretical support of three perspectives for calculating the fair price for different conditions of carbon sink projects: the cost approach, market approach, and income approach. Following these principles, this study selects fair price equations (Pf) suited to carbon sink project stages. Theoretical foundation, model setting, and method application were analyzed. The models were compared by structure, advantages, disadvantages, and applicability. A general measurement framework was developed, with application suggestions based on the analysis.

This study uses data from multiple sources. Grassland carbon sink data, including biomass, comes from net primary productivity measurements. Grazing experiments provide stocking rates. Economic and social data (e.g., grassland type, area, livestock output, pastoralist costs, price indices, and employment) come from statistical yearbooks. Microdata on carbon market transactions come from the World Bank, Chicago Climate Exchange, and Refinitiv Carbon Research Institution. This study focuses on selecting measurement methods for fair value, not calculations or data processing.

Ensuring an Orderly Carbon Sink Transaction

Accounting Attribute of Grassland Carbon Sinks

Grassland carbon sinks generate economic benefits through certified carbon credit trading. As defined by IFRS (2021), an asset is a resource controlled by an enterprise that generates future economic benefits. Grassland carbon sinks qualify as natural assets, yielding benefits via carbon credit trading (IFRS, 2021). They serve beyond animal husbandry and livestock capacity, and function as tangible assets generating income through carbon trading. They belong to both production resources and ecological assets. Thus, accounting principles can estimate carbon sink value.

Orderly Carbon Trade Markets

By 2022, global carbon trading platforms (ETS) doubled over the past decade to 28. ETS coverage rose from 8% to 17%, with emissions increasing from under four gigatons in 2014 to nine gigatons (International Carbon Action Partnership [ICAP], 2023). Currently, seven regions are implementing or developing ETS, including Europe & Central Asia (EU, Switzerland, Kazakhstan), North America (USA, Canada), Latin America (Colombia, Mexico), Africa (Nigeria), and Asia Pacific. These regions represent about 60% of global GDP. The global carbon market includes power, aviation, construction, and transportation sectors (ICAP, 2023). Carbon market prices serve as key references for grassland carbon sink valuation. Table 1 presents historical average carbon credit prices in major trade systems (2017–2022; Refinitiv, 2023).

Annual Average Price of Global Major Carbon Trading Market System 2017–2022.

Source. Refinitiv 2017–2022.

Note. Unit: Eur/ton CO2e.

Figure 1, based on Table 1 data, shows a sharp rise in annual average carbon credit prices across markets. Notably, EU prices surged 14-fold from 5.2 Eur/t CO2e in 2017 to 80 Eur/t CO2e in 2022. UK ETS prices also surged from 2021 to 2022. China had the lowest prices, at 5.3 Eur/t CO2e in 2021 and 8 Eur/t CO2e in 2022. China’s low carbon credit prices stem from uneven carbon projects nationwide. Carbon market maturity varies across China, impacting supply and demand. Since China adopted a unified market price in 2021 (Table 1), prices are expected to rise. Prices in the EU, South Korea, New Zealand, and China reflect secondary markets, while RGGI and California-Quebec represent primary markets. Latin American markets (Mexico, Colombia) were recently established and need time to mature. Overall, carbon credit trade volume and prices are rising. This trend will likely persist due to limited CO2 offset resources. Consequently, global carbon sink prices are expected to rise. Demand for carbon sink projects across ecosystems is expected to grow.

Change of global major carbon trading market system 2017–2022. Diagram created by Author 2023 & data from Refinitiv 2017–2022.

An orderly carbon market sets a reference price for grassland carbon sinks, but valuation is needed if no market price is available. This paper examines three valuation methods for fair value measurement, assessing their applicability in different market conditions.

Measurement Methods for Fair Price of Grassland Carbon Sinks

Fair value is the product of fair price per unit and total carbon sink quantity (Equation 1). Fair price reflects intrinsic value and can be calculated as input cost per unit carbon sink. Alternatively, it may be derived from the market price in active trading. In Some cases, fair price is based on the present value of future cash flows. In mature, orderly markets, fair price aligns with market price. For immature or inactive markets, alternative valuation methods are required. This study presents a framework for estimating fair price using IFRS 13-based cost, market, and income approaches. We introduce the marginal opportunity cost method (cost-based), market shadow price method (market-based), and option price method (income-based) for fair price estimation.

Marginal Opportunity Cost (MOC)

Theoretical Basis

The grassland carbon sink market is nascent, and its value does not yet reflect its true worth. Accurate fair value estimation requires theoretical cost methods. The marginal opportunity cost (MOC) method evaluates resource from an economic perspective, accounting for production costs, resource utility changes, and scarcity. MOC factors in intergenerational equity and externalities of carbon projects on the environment and society. This approach enables a precise evaluation of grassland carbon sinks.

MOC is widely used for the pricing of water (Z. Chen, 2003), forest (Dai et al., 2013), and coal resources (X. Xu, 1998). Given its economic and ecological traits, MOC is well-suited for pricing grassland carbon sinks. However, MOC application in grassland carbon sinks remains in early stages due to resource complexity and variability.

Model Setting and Calculation Method

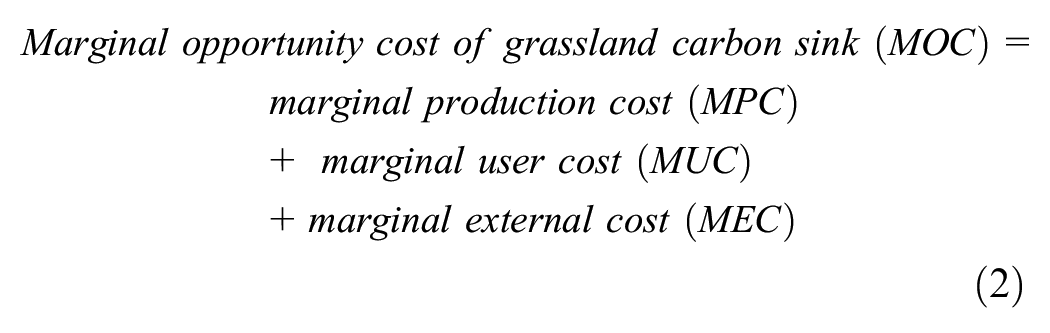

Grassland carbon sink MOC can be estimated via the Average Increment Cost (AIC) approach (Li, 1994). It focuses on determining the total social cost or cost increment associated with increasing each unit of grassland carbon sinks. Effective trading quotas in carbon markets correspond to carbon sink increments (IPCC, 2013). Thus, referencing MOC is essential for pricing grassland carbon sinks. According to prior studies (Z. Chen, 2003; Warford, 1994), MOC is calculated as follows:

Grassland carbon sinks are integral to animal husbandry and natural resource valuation. Carbon sink quantity varies with vegetation use and restoration inputs, and can be categorized into degraded and non-degraded grassland carbon sinks. For both types, MOC is determined by MPC, MUC, and MEC.

Variable Description and Data Processing

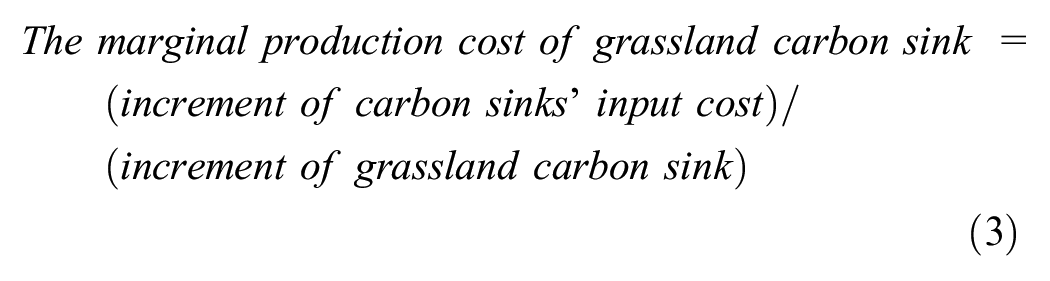

Marginal Production Cost (MPC)

Marginal production cost (MPC) refers to the direct costs (production cost) that must be invested to obtain a single unit of environmental resources (Zeng & Shi, 2010), which includes raw materials, power equipment, salaries, infrastructure construction, and the cost like exploration, management, monitoring, and scientific research expenses, all in the process of utilization that must be invested to obtain resources.

The MPC can be divided into short-term and long-term. There are also two common estimation methods: “direct market price cost accounting” and “average incremental cost accounting.” The first method applies to projects with short input cycles and minor marginal input changes (short-term marginal production cost). It sums all the marginal production costs with the direct market price input for whole cost cycle. The second method applies to the production cost within a long investment cycle and a large amount of one-time investment, and continues to be used in the future cycle (long-term marginal production cost). It evenly allocates the cost incrementally and applies it to every annual new resource acquisition. This part of the marginal production cost equals the average incremental cost of the new resource acquisition (MPC = AIC). Therefore, the long-term marginal production cost is more applicable for grassland carbon sinks obtained most with long-term projects.

For different grassland, the calculation of MPC also follows different forms. For the degraded grassland, the ecological restoration measurement mainly includes fencing, grazing prohibition, rest of grazing, artificial grass planting, and replanting improvement. As a result, the MPC of degraded grassland is (1) Direct costs: grassland rent fee, seeds costs, fertilizer, labor, machinery costs, infrastructure construction costs, fence construction and maintenance costs, natural disaster prevention and control costs, insurance fee, etc. (2) Indirect cost: project management cost, monitoring cost, transaction cost, scientific research management fee, etc. (3) Capital cost: insurance, interest fee, etc. For the non-degraded grassland, the MPC includes direct, indirect, and capital costs but the cost of artificial grass planting and replanting. Other ecological protection measures are consistent with degraded grassland. Implementing a carbon sink project for degraded grassland is longer than non-degraded grassland. Still, the degraded grassland has greater potential to create more carbon sinks. The calculation formula of MPC for grassland carbon sinks is shown as follows:

The increment refers to the increased input cost and carbon sink quantity after the project was built. The total input cost of carbon sinks is calculated by the difference between the total income of livestock husbandry under reasonable carrying capacity and the total production input (cost) in a certain period (R. Chang & Tang, 2008). The total production input equals to the sum of direct cost, indirect cost, and capital cost.

As a result, the marginal production cost of grassland carbon sink is:

ΔCt is the change of carbon sink input, calculated as the increase of cost (apportioned to each year by the average increment method), and then divided by the increment of grassland carbon sink in this period, ΔQt is the increment of the grassland carbon sink, r is the discount rate (opportunity cost of capital) after excluding price changes, and n is the implementation period of the grassland carbon sink project. This is the marginal price of carbon sink estimated according to the average cost increment (Warford, 1994).

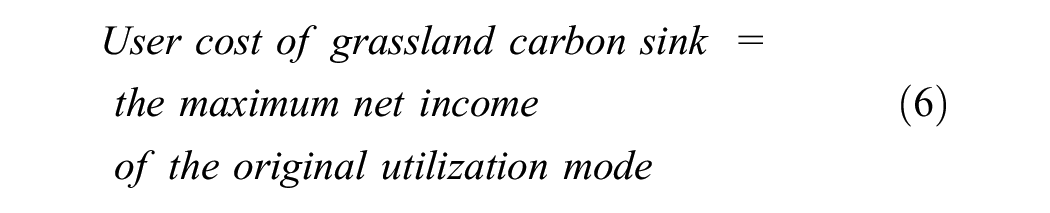

Marginal User Cost (MUC)

Marginal User Cost (MUC) refers to the maximum benefits that may be given up from other purposes when the unit environmental resources are used for one purpose. It also includes the future benefits and values that may be abandoned when the unit’s environmental resources are developed and utilized (Zeng & Shi, 2010). For non-degraded grassland resources, if the grassland carbon sink project is carried out based on the original animal husbandry production, the loss from implementing livestock reduction for the carbon sink project should be considered in the calculation of MUC. When the original grassland resource utilization mode is made for the ecotourism of grassland, the MUC is the income of the original grassland ecotourism. Considering the time or inter-generational cost of grassland resource utilization and development, the possible benefits should be discounted for a certain period. The MUC of degraded grassland is calculated by stages. Its calculation mainly considers the income of raising livestock under reasonable livestock carrying capacity. It has not considered the possible income of other utilization methods. The following formulas present the calculation process of MUC.

Equation 8 is because that if the farmers reduce the livestock number, the carbon sink of their grassland will be increase; same logic, the income of other economic activities on utilizing the land is taken as the opportunity cost.

Marginal user cost of grassland carbon sink (MUC)=income from original mode of utilization

ΔRt is the opportunity cost of replacing the original grassland using the grassland carbon sink project mode. The minimum value of ΔRt for degraded grassland could be 0, and the maximum value is the maximum income under reasonable stocking capacity. For the non-degraded grassland, ΔRt could be the loss of livestock reduction or the income of grassland ecotourism and other utilization methods.ΔQt is the annual increment of grassland carbon sinks. r is the discount rate, and n is the implementation period.

Marginal External Cost (MEC)

The realization of grassland carbon sinks mostly has the typical positive externalities as it can benefit human beings by improving environmental and climate conditions. Currently, the “alternative market value method” is mainly adopted as the marginal external cost (MEC) for the positive external benefits of grassland carbon sinks and emission reduction. For example, the European Union, Australia, etc., often refer to the Swedish carbon tax of 129.7 dollars/ton as the alternative market value (World Bank Group, 2022). China Certified Voluntary Emission Reduction (CCER) takes the average transaction price as 23.5 YUAN/ton (data of December 2020, from China Carbon Trading Network, 2021). Only when the extreme cases of the project fail and cause losses to local farmers are negative externalities of the grassland carbon sink projects. The calculation of MEC follows:

where ΔEt is the carbon sinks’ annual income (positive externality) realized by the carbon sink project determined by the carbon sinks’ annual increment and the carbon sinks’ market price. ΔQt is the annual increment of carbon sink.

Application of Marginal Opportunity Cost Measurement

The method of marginal opportunity cost (MOC) is substantiated as considering the value of various factors such as the marginal production cost (MPC), marginal user cost (MUC), and marginal external cost (MEC). This approach considers not only the production cost of obtaining natural resources but also the factors like inter-generational equity and the externality characteristics of the natural resource development process. It reflects how changes in utility and scarcity of natural resources affect the price of carbon sinks. For measuring the carbon sink in both degraded and non-degraded grasslands, MOC is further flexible to provide alternative methods for specific characteristics of the grassland sink formation. In addition, the MOC method is optimal to be applied in the initial stages of the carbon sink project because the fair price calculated by MOC reflects the initial goals of the carbon sink project in the incremental change of costs from the beginning of the project, and the information and data are limited. Therefore, a fair price estimated by the MOC method can provide a basic reference for grassland’s ecological environment compensation by taking the carbon sink project as an investment in nature resources.

Shadow Price Measurement (SP)

Theoretical Basis

The Shadow Price (SP) method, introduced by Dutch mathematician Jan Tinbergen, aims to address the distortion of natural resource prices caused by market failure by providing a theoretical price for a reasonable allocation of scarce resources. Leonid Vitaliyevich Kantorovich developed the method into a mathematical linear programing approach for calculating the optimal planned price. The SP method refers to the price of various economic resources participating in production under the condition of optimal allocation, reflecting the degree of resource scarcity and its role in allocating and utilizing natural resources reasonably. Additionally, it demonstrates the marginal utility of resources in the market.

Adopting shadow price theory as a replacement for the orderly market price is still a hot topic in discussion. Most literature on carbon sink prices focuses on the price trend and influencing factors of carbon sink market systems in developed countries (Blyth & Bunn, 2011; X. Chen & Shang, 2011). The realization of the grassland carbon sink function mainly depends on the restoration of natural grassland vegetation in Net Primary Production (NPP) or Vegetation Primary Productivity (VPP), which is mainly affected by climate change (temperature, rainfall), and grassland use mode and intensity (livestock carrying capacity; Y. Zhang et al., 2013). Because grassland serves as the production and living basis of herdsmen in pastoral areas, the restoration of grassland vegetation and the realization of grassland carbon sink function are closely related to the development of animal husbandry in these areas. Therefore, the shadow price must reflect the input and output in ecological protection and animal husbandry functions. Cobb-Douglas production function (Su & Zhang, 2010) can be adopted to decompose the grassland carbon sink measurement angles in animal husbandry production as an environmental production factor. It allows us to reflect on the eco-environmental value from the perspective of input-output of animal husbandry production in pastoral areas and obtain the shadow price of grassland carbon sinks through the marginal effect.

Model Setting and Calculation Method

The economic value of the grassland’s ecological performance can be measured by the optimal output value of animal husbandry, providing insight into the relationship between animal husbandry output and the grassland’s ecological environment. We constructed an improved Cobb-Douglas production function to identify the shadow price of grassland carbon sinks in this area (Equation 11). This function uses the output value of animal husbandry in the pasturing area over the years as the total output while taking the number of employees in the pasture area as the labor input, the financial policy subsidy input and the herdsman’s animal husbandry production cost expenditure as the capital input, and the grassland ecological environment as the environmental input factor.

The precondition of the shadow price calculation is that the input of other factors remains unchanged, the marginal product value of a production factor is equal to the factor price, the profit is maximized, and the resources are optimally allocated. We can obtain the shadow price of grassland carbon by using the partial derivative sink.

The improved Cobb Douglas production function in this study is as follows:

Among them, Yt represents the output value of animal husbandry, A represents the technical level, L represents labor input, K represents the production input of animal husbandry in pastoral areas, and E represents the annual carbon sink of grassland as the environmental factor. In addition, α, β, and λ represent the output elasticity of labor, capital and carbon sink, respectively. The least square (OLS) method is used to calculate the formula function (11). The problem can be solved in the form of a logarithmic function:

Among them,

Px is the product’s price (here is the carbon sink), and MPx is the value of the marginal product.

Same logic, the shadow price of unit grassland carbon sink can be expressed as:

Variable Description and Data Processing

The variables of improved Cobb-Douglas production function are the time series data of the annual values of livestock industry output (Y), the number of employees in the livestock industry (L), capital investment in livestock production (K), and the carbon sequestration of grassland vegetation (E) as expressed in following Table 2. The data for the output value of the livestock industry, the number of employees in the livestock sector, and capital investment in livestock production are derived from statistical yearbooks and processed survey data. The data for grassland carbon sequestration are obtained through direct measurements of above-ground biomass and estimation methods for below-ground biomass.

Variables’ Description and Data Processing.

Source. Created by Authors 2023.08.

Application of Shadow Price Measurement

The Shadow Price (SP) method is an innovative approach that treats the ecological environment, specifically the grassland carbon sinks, as an input factor of production and constructs an economic output model. This method highlights the crucial role of the ecological environment as the production factor participating in market transactions. A breakthrough is that the shadow prices under the constraints of traditional production input factors prove that the ecological environment is valuable and measurable. In addition, the SP method provides a theoretical price for a reasonable allocation of scarce resources according to the fair value of the material amount of grassland carbon sinks as the optimal marginal utility. Carbon sink projects could meet a certain level of market failure with the feature of the public good. Comparing the market price and fair value estimated by the SP method can narrow the difference between the two prices by providing substitutions to compensate for the market’s failure to the sellers or buyers. This difference will stimulate future government policies to improve the maturity of the carbon sinks market. Thus, the SP method is a practical tool for measuring resource commodities’ economic value or cost compensation of resource input in a frequently traded market.

Option Pricing Measurement (OP)

Theoretical Basis

Options pricing (OP) is another essential and applicable grassland carbon sink pricing method. By paying a certain fee, the option holder can obtain the option to keep or profit from the underlying assets. The fee is known as the option price. There are numerous OP models based on option pricing theory, including the B-S option pricing method (Black-Scholes Model), binomial option pricing method (binary tree method), Monte Carlo simulation method, finite difference method, deterministic arbitrage method, arbitrage pricing method, and interval pricing method. The most basic OP models are the B-S model for continuous time variables and the binomial model for discrete-time variables (J. Wang et al., 2010).

OP method can evaluate the investment and development of carbon sink projects to provide references for investors or producers. At the same time, option, as a trading method, can allocate emission rights by countries or regions to choose demanders. As the carbon sink market evolves, it will become a necessary supplement to the spot market. Grassland carbon sink has unique characteristics, including time lag in the formation process, development, and transaction at the project level, as it is in line with the nature of option products, and the carbon sink project investment usually faces the challenges of income uncertainty, investment irreversibility, and time delay. OP theory has great potential to calculate the fair value of grassland carbon sink in the greater specific project level and forward estimation to overcome the above estimation difficulties (Yan & Xiu, 2014).

The OP method called the real option stage, evolved from two previous stages—the static and dynamic evaluation stages. The static evaluation stage takes the cash flow value at each time point as the same without considering the time value discount of funds. The main calculation methods include the payback period and return on investment methods. The dynamic evaluation stage (discounted cash flow—DCF) considers the time value of capital, but the discount rate is fixed, which cannot reflect the risk change from the change of the project environment. Dynamic evaluation is an enhanced objective than the static evaluation method. The Net present value (NPV) method is widely applied at this stage. The current third stage, the real options evaluation, considers the time value and opportunity cost and reflects the risk change with the probability of actual value change and risk-free return. It can adopt flexible decisions such as delay, contraction, or expansion and is further suitable for the value evaluation of long-term and complex projects under uncertain conditions. Therefore, it is called the real option stage.

Currently, OP is mainly applied in the investment decision-making of natural resource development, enterprise investment decision-making and value evaluation of high-tech intangible assets, including mineral resource development, oil and gas reserve value evaluation, oil exploration and development, water right option transaction, and intangible asset value evaluation (Guo et al., 2008; Ma & Zhang, 2002; Xie & Chen, 2000); With the development of global carbon trade and the rise of domestic carbon sink project, OP has been commonly tested in the initial allocation of emission rights and the pricing of forest carbon sink options (Guan et al., 2020). However, many of the applications of carbon sink options are only in the theoretical research stage, and no actual transaction has been formed. One of the mature applications is the European Climate Exchange (ECX) which launched carbon sink options trading in 2005. However, many other applications are still in the preliminary stage. For example, the “acid rain plan” in the United States did not achieve the expected optional market trading activity (Hill, 2000).

Model Setting and Calculation Method

The form of the B-S Option Pricing Model (Black-Scholes Model; J. Wang et al., 2010) under the basic assumptions is in the following Equation 15.

of which

To obtain the optional price (c), the factors that need to be determined in B-S Option Pricing Model are the current value of the underlying asset (S), the exercise price of the option (X), the effective period of the option (T-t), the variance of the asset value (σ2) and the risk-free rate of return (r), and the current year of the project (t). For the OP of the grassland carbon sinks, the exercise price of option (X), which is required by the project investment, is the input cost. The term of the option (T-t) equals the formation period of the grassland carbon sinks. The value of the subject matter (S) and its value change (σ) are the grassland carbon sink project’s expected income and income change.

Variable Description and Data Processing

Current Value of the Underlying Asset (S): To measure the fair value of the grassland carbon sink of the underlying asset, the carbon sink project is taken as the expected grassland carbon sink value as “carbon sink price × carbon sink quantity.” The carbon sink price is the trading day’s spot price published by the domestic and foreign carbon sink market.

Exercise Price of Options (X): The formation of grassland carbon sink is closely related to animal husbandry production in pasture areas. To obtain the input cost of the grassland carbon sinks, it is necessary to separate the production input of animal husbandry from the ecological input of the grassland carbon sinks. To produce grassland carbon sinks through vegetation restoration, the government and herdsmen need to continue to invest in pastoral areas both in animal husbandry production input and grassland ecological restoration input. However, the current balance account for the main income obtained from the investment only writes the animal husbandry income. The value provided by grassland resources in ecology is not reflected in the input-output accounting process yet. Therefore, we can only calculate the unit value of grassland resources for the carbon sinks by taking the difference between the income and input of grassland vegetation investment for carbon sinks. As a result, this annual unit input is equal to the option value of the input (execution price) of grassland carbon sinks (X. Zhang & Wang, 2004).

Term of Option (T-t): During the implementation of the carbon sink project, each year can be seen as a short-term carbon sink option, and every three or 5 years, or even longer, can be designed as the effective period of different carbon sink option products. However, considering the natural climatic conditions of the study area, especially since the recovery of degraded grassland may take a long time to form effective grassland carbon sinks, the option period can be adjusted according to the actual situation. For example, the total project time T is 9 years. After the project is executed t = 2 years, the option’s term is 9-2 = 7 years.

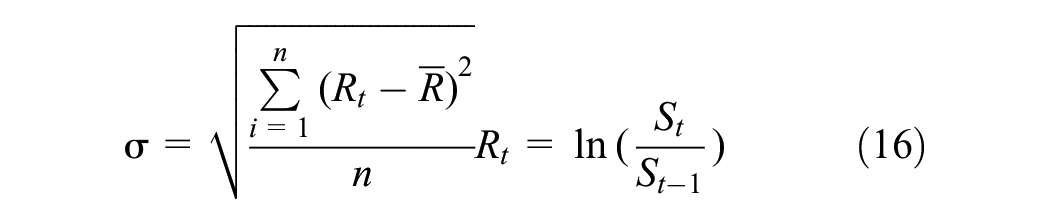

The variance of Underlying Asset Value Change (σ2): The variance change of asset value is calculated using the underlying asset’s value.

Where σ is the standard deviation of the change in the underlying asset’s value, Rt is the annual return of the underlying asset. It is the average return rate of the underlying asset. S is the current value of the underlying asset.

Risk-Free Interest Rate (r): The risk-free interest rate is crucial in financial analysis, used as a benchmark for evaluating the expected return on investment. One common determinant of the risk-free interest rate is the yield to maturity of bonds. In particular, the interest rate on short-term national debt can also be a reliable proxy for the risk-free interest rate. Additionally, depending on the duration of the investment project, interest rates of different maturities on the national debt can be considered as the risk-free interest rate.

Application of Option Pricing Measurement

Implementing grassland carbon sink projects often requires significant early investments that are difficult to reverse. The income from such projects is uncertain, and the time lags in product development and transactions are commonly long. These risks can hinder the development of the carbon sink market, which in turn may affect project development and financial investment. However, the option pricing (OP) method can be used to evaluate the investment and development of carbon sink projects to provide valuable guidance for investors and producers. Additionally, it can be used as a tool for the initial allocation of emission rights for countries or regions, functioning as a trading method to supplement the carbon sink spot markets. This kind of carbon sink option market will become as necessary as the carbon sink spot markets in the future. Applying the OP theory in the evaluation of grassland carbon sink projects can provide a basic reference for investment and project development decisions and facilitate the fair value measurement of carbon sinks through optional pricing. It can enhance market trading flexibility, reduce investment trading risks, and promote the development of the grassland carbon sink markets. Therefore, there is huge potential for applying the OP method when in a mature market, as it is optimal for forward trade exchange.

Comparison of Three Valuation Methods

If the appropriate market prices and orderly carbon sink market transactions have not yet formed, the estimation of the fair value of grassland carbon sinks must be based on project conditions. As a result, this paper introduces three methods from the perspectives of cost, market, and income. The details of the comparison between these three methods are presented in Table 3.

Comparison of Three Methods.

Note. Concluded by Author 2023.

The MOC method captures the total social opportunity cost of carbon sink projects by classifying grassland into degraded and non-degraded types, ensuring a more accurate fair price estimation based on ecological conditions and pastoral production. Its average increment approach aligns with carbon trading demand under “Intergovernmental Panel on Climate Change (IPCC)” regulations. The initial requirements of carbon trade on cost estimation can be well satisfied by MOC. However, the disadvantage of MOC is the complexity of combining calculation with other factors, such as user’s cost and external cost for comprehensive estimation. When there is no direct value or cost measurement for reference, inaccurate results may happen with the MOC. The MOC method fully accounts for social costs, but overestimation in demand for grassland carbon sink and the related price from the human nature of risk avoidance will impede its accuracy. While MOC provides a solid cost baseline, it is best suited for early project stages when cost structures are simpler and data is sufficient to minimize errors.

From a market perspective, the SP method improves upon previous market value theories by providing a theoretical price that allocates resources efficiently. It serves as a substitute for market price, measuring the economic value of resources or as a compensation baseline for investment costs due to market failure. The SP method allows for a comprehensive environmental contribution analysis, by adopting the grassland ecological environment as one of the Cobb-Douglas production function’s production factors. The marginal utility of resources is reflected in the impact of resources by increasing or reducing. The participation of these resources in market transactions is realized as market price. While, the carbon sink price may be undervalued as grassland plays only partial functions in the whole environment. SP is ideal for the stage that the grassland carbon sinks entered to regular and frequent carbon trading, when the shadow and market prices are comparable.

The OP method estimates grassland carbon sink prices based on future income, reducing market risks and guiding investment in carbon projects. By considering the time value of funds, it maintains flexible decision-making by timely measuring the change in the probability of shifting on actual value and the risk-free return rate, making the evaluation results more accurate. However, as an alternative market-based approach, OP faces challenges in voluntary carbon markets with small trade volumes and price inconsistencies, leading to circular substitution and non-specific representation. The voluntary market always uses average transaction prices, but a unified market price is needed to resolve above inconsistencies. Therefore, the B-S Option Pricing method is ideal for valuing grassland carbon sinks in a mature carbon market stage, considering future income.

Figure 2 illustrates the fair value measurement process. The process begins by assessing the necessary for fair value measurement, followed by determining whether the transaction market is orderly. Most carbon markets are not yet at this stage, but theoretically, in highly orderly markets, market price equals fair value. Fair value can be calculated by multiplying unit fair price by the carbon sink project quantity. Three approaches apply at different transaction stages for the unit fair price. In the early stage of grassland carbon sink projects, the opportunity cost method is most suitable. As trading increases to frequent, the shadow price method becomes optimal. While in a mature secondary market, the option pricing method is preferred.

Process of fair value measurement of grassland carbon sinks.

Discussion

This framework introduces a new approach to valuing grassland carbon sinks, supporting sustainability and fair value measurement (Jia et al., 2015; Liu et al., 2022; X. Zhang & Wang, 2004). It offers insights into natural resource management, advances asset pricing theory, and enhances valuation methods’ application at different stages of grassland carbon sink projects. Although carbon credit trading is in its early stages, demand for fair valuation and market transactions will grow. The MOC method incorporates opportunity costs into pricing, advancing fair value estimation. The SP method considers both market prices and failures, bridging the gap between carbon tax and market value methods, which only apply to existing costs (Kong & Zhang, 2014; Pang et al., 2014; Y. Yu et al., 2019). It offers a price reference for potential market failures (G. Zhang & Zhang, 2003). OP supports forward market development and expands grassland carbon sink projects, serving as a logical extension of the market value method (Cozma, 2015; Petrokofsky et al., 2012; Sommer et al., 2022).

Future supervision must enhance measurement processes to optimize grassland carbon sink pricing, as current public standards remain insufficient. Establishing a unified global carbon sink value is challenging, making independent third-party supervision essential for auditing price estimation and improving data collection. The MOC, SP, and OP methods capture different pricing influences: MOC considers grassland carbon sinks interactions with animal husbandry production, SP assesses eco-environmental impacts on regional economies, and OP accounts for the time value of carbon sequestration. Monitoring these factors and optimizing databases is crucial. Lastly, fair value management must recognize positive externalities, with market stability playing a key role in carbon credit transactions.

Conclusion and Future Work

This study explores fair value measurement methods for grassland carbon sinks, establishing a framework to enhance value realization and sustainable development. Key findings include: (1) In accordance with the theoretical requirements of IFRS 13, FAS 157, and CAS 39 accounting standards, and the formation characteristics of grassland carbon sinks, fair value measurement is applicable to the value measurement of grassland carbon sinks. (2) A theoretical framework was developed using cost-based, market-based, and income-based approaches. Specifically, we propose three innovative valuation methods: Marginal Opportunity Cost (MOC), Shadow Pricing (SP), and Option Pricing (OP). These methods support carbon sink valuation and market implementation. (3) Each method’s applicability depends on measurement objectives and project stages. This framework addresses carbon sink’s valuation challenges and supports ecological preservation and economic sustainability.

In light of the ongoing development and refinement of international carbon markets, proposed valuation strategies include: (1) Market-Based Valuation: When observable prices from primary carbon markets are available on the measurement date, these prices should be adopted as the fair value benchmark for grassland carbon sinks. This aligns with IFRS fair value measurement. (2) Alternative Valuation Methodologies: In scenarios where, orderly market prices are absent during the measurement period, market participants should select valuation techniques based on transaction objectives and market conditions: Marginal Opportunity Cost Method (MOC), Shadow Price Method (SP), and Option Pricing Method (OP). (3) The aforementioned three valuation methods demonstrate distinct situational applicability: MOC serves as a foundational tool for early-stage project feasibility analysis, SP provides dynamic pricing references for liquid markets, and OP enables sophisticated risk-adjusted valuations in mature trading environments. This study offers insights for standardizing carbon sink asset valuation and disclosure. The proposed framework contributes to establishing fair transaction pricing systems, ensuring that all participants are treated equitably, thereby enhancing market transparency and facilitating the sustainable development of global carbon markets.

As carbon markets become more sophisticated, the valuation of grassland carbon sinks must evolve to incorporate future-oriented assessments beyond simple present-value estimation. Activities require improved regulatory oversight of valuation methodologies, comprehensive data acquisition on influencing factors, and promotion of positive externalities. Carbon sink capacity variability due to climate, geography, and management affects valuation. Future research should also develop region-specific calibration parameters and validation protocols.

Key innovations include: (1) Research Perspective Innovation: This study introduces fair value measurement into carbon sink pricing. It constructs a systematic theoretical framework for fair value measurement based on cost, market, and income dimensions, providing methodological guidance for quantifying ecological product value. This approach integrates accounting with ecological economics, filling a valuation gap. (2) Methodological Innovation: This study proposes three valuation methods in alignment with the formation characteristics of ecological products and prevailing accounting conditions. Specifically, the Marginal Opportunity Cost (MOC) Method addresses cost-based analysis, the Shadow Price (SP) Method facilitates market-based valuation, and the Option Pricing (OP) Method is designed for income-driven scenarios. This integrated tripartite framework creates a significant advancement over traditional single-method approaches (e.g., historical cost or net present value methods), offering greater flexibility and scenario-specific adaptability for various carbon sinks valuation. The integration of option pricing theory particularly introduces a forward-looking financial engineering technique to environmental asset pricing, enhancing the predictive capacity of valuation models. (3) Method Application Scenarios: This study discusses the application scenarios of three fair value measurement methods and proposes that the selection and application of these methods should be based on the project phase and measurement objectives. The MOC method excels in carbon pricing in early carbon sink project stages; the SP method suits active primary markets; the OP method offers technical strengths for projects’ future evaluation and secondary market transactions. This selection mechanism aligns valuation techniques with carbon market maturity. The framework provides actionable guidance for matching methodological rigor with contextual requirements throughout the carbon sink project lifecycle.

This study acknowledges a limitation regarding the lack of research data on specific regions or areas’ carbon projects while restricting the examination of the ecological system’s influence on carbon sinks. Further research should evaluate methods considering carbon market changes and ecological systems. Moreover, incorporating social, economic, and ecological factors into the fair value modeling of grassland carbon sinks can provide innovative recommendations for developing grassland carbon sink projects.

Footnotes

Ethical Considerations

This article does not contain any studies with human or animal participants.

Consent to Participate

There are no human participants in this article and informed consent is not required.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Program for Improving the Scientific Research Ability of Youth Teachers of Inner Mongolia Agricultural University [grant number BR220211], National Key Research and Development Program of China-Intergovernmental International Co-operation in Science and Technology: Key Project Sino-Mongolian Agriculture and Animal Husbandry Supply Chain Collaborative Research [grant number 2021YFE0190200], Inner Mongolia Natural Science Foundation Project: Study on Influential Factors and Their Mechanism of Action on Grassland Ecological Protection Behavior of Herder Specialized Cooperatives in Inner Mongolia [grant number 2020MS07021], Key Research Institute of Humanities and Social Sciences at Universities of Inner Mongolia Autonomous Region, Inner Mongolia Institute for Rural Development [grant number KFSM-NYSK0107].

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.