Abstract

The purpose of this research is to investigate the effect of macroeconomic factors on the volatility of Somalia’s unregulated exchange rates. While utilizing the EGARCH (exponential generalized autoregressive conditional heteroskedastic) model, this study found that the unregulated exchange rate volatility of Somalia is influenced by its own shocks and the macroeconomic factors. This study implies that although Somali shilling circulated without regulatory authority for the period of the statelessness, this circulation has been accompanied by volatile exchange rates. This phenomenon makes this study an appealing work that should be pursued further. Hence, this study contributes notably to the process of reforming the exchange rate system and the monetary policy of the post-conflict economy of Somalia. In addition, the results of this study imply that even in times of war and lawlessness the laws of economics do not change completely.

Introduction

Exchange rate behavior is important for the people of each country as the exchange rate volatility has a direct effect on the prices of basic commodities (Nor, 2015). The fall down of the Bretton Woods fixed exchange rate system pushed bilateral exchange rates to considerably fluctuate over time (Chit et al., 2010; Flood & Rose, 1999; Frömmel & Menkhoff, 2003; Nor, 2015).

Exchange rate volatility has been increasing due to major changes happening within the global economy (Nor, 2015). Although the reasons behind the volatility of exchange rates differ between developed and developing economies, these changes are taking place due to the fiscal and monetary policies assumed by the governments of every country (Devereux & Lane, 2003; Nor, 2015).

Despite the fact that the issue of exchange rate is given exceptional consideration worldwide owing to its negative consequences on the economy, it also continues to be a hot matter in the emerging economies (Chit et al., 2010; Nor, 2015; Prasad et al., 2003). In the context of emerging market economies, countries are facing continuing challenges in handling boom–bust capital flow cycles as these capital flows have increasingly become volatile. Such situation creates dislocation during the bust and puts upward pressures on currencies during the boom (Ostry, 2016). The emerging economies’ exchange rates have been examined completely due to the numerous and frequent currency crises that occurred in the previous two decades (Nor, 2015). To identify a common policy direction for such disastrous events, numerous studies have analyzed exchange rate volatility of the developing countries (Chit et al., 2010; De Gregorio et al., 2000; Devereux & Lane, 2003; Edison & Reinhart, 2001; Glick & Hutchison, 2005). Notwithstanding the enormous attempts put in examining the volatility of exchange rates, the findings of Meese and Rogoff (1983) are still integral, which suggest that movements in exchange rates are primarily unpredictable (Devereux & Lane, 2003).

In the context of Somalia, the Somali shilling (SOS; the national currency) is used as a medium of exchange and unit of account in small transactions and mainly used by small-scale traders and rural population. It is notable that SOS remains the only medium of exchange and unit of account for the entire livestock and agriculture markets and this is one of the factors behind the resilience of SOS even after the collapse of the central government. On the other side, the divisibility problem of USD was also another factor that encouraged the shilling to remain in the economy because the dollar cannot be used for small transactions (Abdurahman, 2005). Whatever reason and by any means, the SOS did not disappear due to the lack of sovereign support and it continued circulating in Somali markets following the collapse of the government. Although Luther and White (2011b) argue that SOS circulated at a positive value for the past 20 years, there are very limited studies that empirically examine the volatility of the Somali exchange rates.

In 1980s, the formal financial system of the country failed to provide adequate financial services to the people, so underground financial services started, which pushed the whole economy into some form of informal system (Nor, 2012; Nor & Masron, 2017; Nurhussein, 2008). Due to the collapse of the military regime in 1991 and the breakdown of the formal financial system of the country, Somali economy shifted to a complete reliance on informal financial system operating under informal economic activities (Nor, 2012; Nor & Masron, 2017). In terms of monetary system, this period had suffered from lack of monetary authority because the country’s monetary policy was totally collapsed except the reissuance of the 1,000 denominated notes. Somalia’s conventional banknotes continued to circulate in the absence of sovereign support and the public receivability of the notes as a legal tender has not been challenged for a long period (Luther, 2012; Nor & Masron, 2014).

In his study about Somalia’s monetary policy and exchange rates, Abdurahman (2005) concluded that the exchange rate of SOS is affected by a few key items including money supply, livestock trade, remittance, and Khat. 1 Nevertheless, Abdurahman (2005) did not examine these determinants systematically and his study relied on descriptive analysis solely. Similarly, Shortland (2011) found that camel exports, price of rice, and random piracy payments are some of the determinants of Somalia’s bilateral exchange rates (SOS/USD). As her focus was on piracy, the study of Shortland is suffering from several limitations. First, she did not examine factors explaining the volatility systematically; thus, her study did not provide information about the factors contributing to the volatility of exchange rates. Second, due to a sample size problem, her study can contribute little towards understanding of Somali exchange rates. Although there are a number of goods traded (imported or exported), she only used camel (proxy of exports) and rice (proxy of imports). Third, the focus of her study is after 2000, but this period may not show the real picture of the unregulated period.

Elsewhere, Luther and White (2011a) argued that SOS is positively valued after the state collapse. However, the analysis made by Luther and his coauthor was based on the circulation of Somalia’s unbacked fiat money and how it is in line with the well-known theoretical models of money such as the random matching models of Kiyotaki and Wright (1989, 1991, 1993). Therefore, their study contributes very little towards understanding the volatility of Somalia’s unregulated exchange rates.

As the monetary authority of Somalia is yet to completely supervise the exchange rate of SOS, researchers have brought a number of relevant questions. These questions include the following: (a) Is the unregulated exchange rate volatile? (b) What are the macroeconomic factors affecting Somali exchange rate volatility? Finding a satisfying response for these and other related questions provides imperative inference to policymakers and practitioners alike.

From the available publications, little systematic work has been undertaken to examine Somali unregulated exchange rate volatility. The purpose of this study is twofold. First, it investigates Somalia’s unregulated exchange rate volatility. Second, this study examines the effect of macroeconomic factors on the volatility of Somalia’s unregulated exchange rates. The remainder of this article is structured as follows. In Section “Literature Review,” the literature review is provided. In Section “Data and Methodology,” data and the empirical methodology of the study are presented. Section “Results” provides empirical results of the study. Section “Discussion and Implications” presents the discussion and policy implications of the study.

Literature Review

Volatility of exchange rates have been thoroughly studied using different methodologies. Since the seminal work of Mussa (1986), traditional wisdom suggests that volatility of exchange rates is greater in a flexible exchange rate regime than a fixed one (Kocenda & Valachy, 2006). As it is not directly observable, exchange rate volatility can be identified by employing certain tools and methods (Cheonga et al., 2005). According to Chit et al. (2010), there is no universal consensus on the best proxy to represent volatility as different authors prefer different proxies. Some researchers use only a single proxy, whereas others use multiple proxies (Aftab et al., 2017; Clark et al., 2004; Dell’Ariccia, 1998; Kumar & Dhawan, 1991).

As the volatility in exchange rates is characterized as the clustering of large shocks’ conditional variance, researchers mainly utilize ARCH (autoregressive conditional heteroskedastic) and GARCH (generalized autoregressive conditional heteroskedastic) models to measure the volatility of the exchange rates (Avdis & Wachter, 2017; Bollerslev, 1990; Cheonga et al., 2005; Diebold & Nerlove, 1989). Similarly, there are enormous studies on the possibility of forecasting volatility of exchange rates. The ability of forecasting exchange rate movements is counted as a golden opportunity for large multinational firms that conduct considerable currency transfers. According to Huang et al. (2004), having the ability to know the future exchange rate movement can produce a substantial improvement in the firms’ overall profitability.

In the literature, researchers found several fundamental and technical factors causing exchange rate volatility. Exchange rates are affected by many economic, political, and psychological factors that are highly correlated and interactive in a very complex way (Alagidede & Ibrahim, 2017; Huang et al., 2004; Yu et al., 2010). Likewise, it has been observed that exchange rate volatility is generally caused by governments’ fiscal and monetary intervention, fundamental factors of the economy, financial markets, and financial development (Giannellis & Papadopoulos, 2011; Grossmann et al., 2014; Li et al., 2016; Simpson & Grossmann, 2014). While examining the exchange rate volatility of European Union countries, Giannellis and Papadopoulos (2011) found that monetary side represented by interest rates, domestic stock markets, and industrial production are some of the determinants of the volatility of exchange rate in these countries. While examining the link between macroeconomic factors and exchange rate volatility of ASEAN (Association of Southeast Asian Nations) economies, Chong and Tan (2007) found that macroeconomic factors are the forces behind exchange rate volatility via the probable rigidities of the exchange rates of these countries, coming from the managed float exchange system adopted by these countries.

Exchange rate is considerably affected by speculation and these will in turn influence all markets that are dependent on the exchange rate market. Seasonal movements, capital flight, and political uncertainty are reported to be anticipated shocks that affect exchange rates. However, there is heavy speculation in FX (foreign exchange) markets by quickly purchasing or selling a huge amount of certain currencies, which bring about wide fluctuations in exchange rates.

Speculation is one of the various factors that affect volatility of asset prices generally. Some observers argue that a high trading volume reflects high speculative activities and this induces the high price volatility. It has been observed that more than 90% of FX market participants in Singapore, Japan, and Hong Kong agree that speculation increases volatility (Carlson & Osler, 2000; Yang & Hamori, 2016). Nevertheless, there are some researchers who claim that rational speculation must reduce exchange rate volatility and this idea stems from the arguments of Freidman (1953), whose position was that only rational speculators will survive in the market (Carlson & Osler, 2000). The findings of Carlson and Osler (2000) illustrate that microstructural factors including the degree of speculative activity are part of the fundamental indicators of exchange rate dynamics. According to Dědek and Gregor (1994), the volume of trade in foreign currencies is very huge and a substantial part of it is in the form of so-called hot money as these funds do not stay in the same place for a long period and the flow very quickly to anywhere high profit is available. As the trading activities of foreign currency exchange markets are based on currencies, which are very liquid, currency prices are expected to move quickly in response to surprises (Sensoy, 2015; Wei et al., 2018; Yang & Hamori, 2016; Yen-Hsien et al., 2017).

While examining bilateral trade between the U.S. and other G7 economies, Shirvani and Wilbratte (1997) found that trade balance significantly responds to exchange rates in the long run but not in the short run. While using the bounds testing approach, Narayan (2006) found that China’s trade balance and its real exchange rate are cointegrated. In their empirical examination of relationship between export and exchange rate, Zameer and Siddiqi (2010) concluded that a 1% change in exports will lead to a 2.0043% change in exchange rate volatility. In their paper, Byrne et al. (2008) investigated the impact of exchange rate volatility on the volume of bilateral U.S. trade sectoral data and found that exchange rate volatility has a robust and significant negative effect across sectors.

Data and Methodology

Data

This study investigates the volatility of Somalia’s unregulated exchange rates using a monthly exchange rate of SOS against USD. Furthermore, the study examines whether macroeconomic factors have a significant effect on the unregulated exchange rate volatility of Somalia. Domestic Price (DP), Imports (M), Money Supply (MS), and Hot Money (HM) are used as explanatory variables in this study. For each of the macroeconomic factors, monthly data were obtained for a period of 216 months from January 1995 to December 2012. Various sources of data were used for collecting data including International Monetary Fund (IMF) Direction of Trade Statistics, Food Security and Nutrition Analysis Unit—Somalia (FSNAU), Food and Agriculture Organization (FAO), and DataStream as reported in Table 1.

Source of Data.

Note. FSNAU = Food Security and Nutrition Analysis Unit—Somalia; FAO = Food and Agriculture Organization; IMF = International Monetary Fund.

Model Specification

The focus of this study is to examine the effect of the macroeconomic factors on Somali unregulated exchange rate volatility. There are no exogenous variables in the mean equation as presented below as the focus of this study is to examine the variance equation (volatility). Furthermore, specifications of the GARCH model only are presented in the modeling.

Mean equation

where SOS t is the exchange rate of SOS to USD and α t , β t , and ε t are the parameters of the model.

Variance equation

This is the variance equation of a GARCH model where

Results

Unit Root Tests

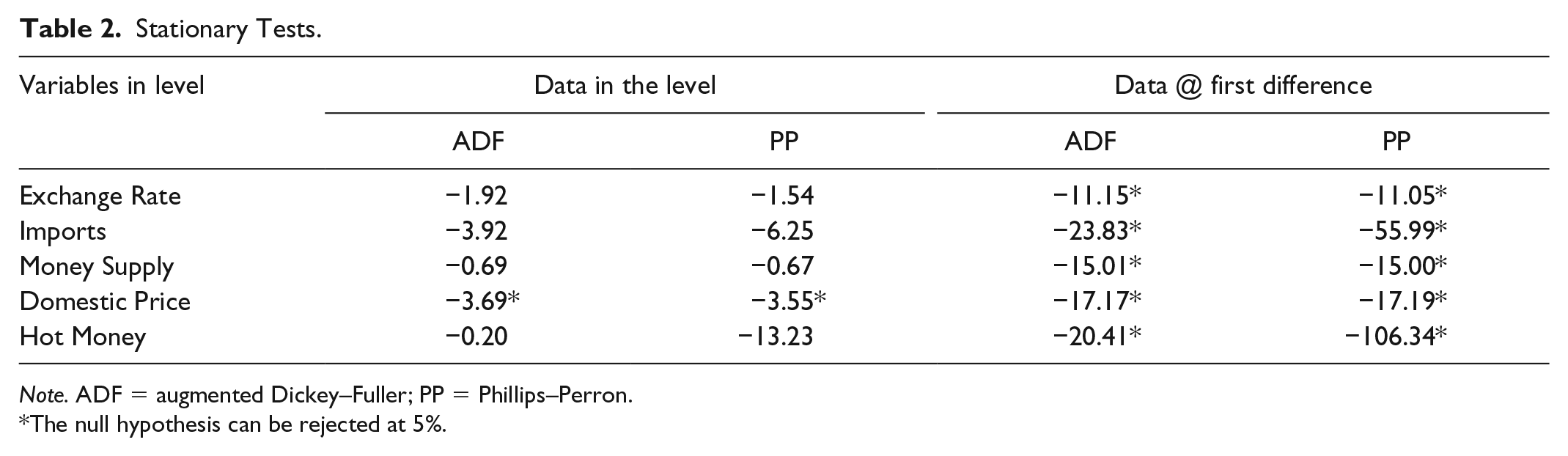

Two common unit root tests, namely, augmented Dickey–Fuller (ADF) and Phillips–Perron (PP), were employed to check the stationarity of the data. All variables, as reported in Table 2, are not stationary at level but are stationary when they differenced once and thus follow unit root process.

Stationary Tests.

Note. ADF = augmented Dickey–Fuller; PP = Phillips–Perron.

The null hypothesis can be rejected at 5%.

Test of Structural Break

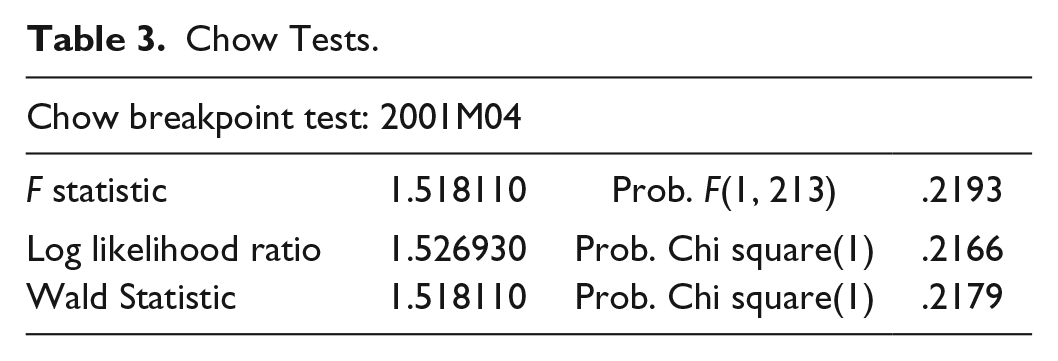

While examining possible structural break, this study utilized the conditional variance produced by the GARCH model. The GARCH graph, as shown in Figure 1, points out the existence of a potential structural break in 2001; however, the Chow test shows the absence of structural break in 2001 as shown in Table 3. To further analyze the existence of a structural break in the data, a Structural Break (SB) variable is included in the model as a dummy variable.

GARCH graph.

Chow Tests.

Results of Heteroskedasticity Test

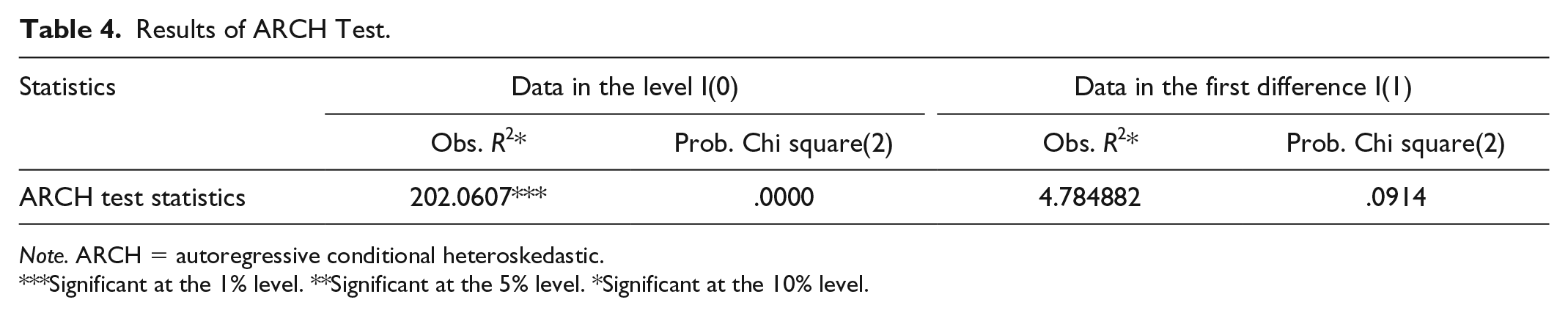

To model the volatility of Somalia’s unregulated exchange rates and examine whether macroeconomic factors affect unregulated exchange rate volatility of Somalia, this study utilizes various models of the GARCH family. Before modeling the volatility while using GARCH models, the study examines the existence of the ARCH effect in the data. In statistics, a collection of random variables is heteroskedastic if there are subpopulations that have different variability from others. In essence, heteroskedasticity is the absence of homoskedasticity. The presence of heteroskedasticity is a key concern in the regression analysis as the existence of heteroskedasticity can invalidate statistical tests of significance (Gujarati & Sangeetha, 2007; Wooldridge, 2013). To check the presence of heteroskedasticity, the ARCH test was employed. As reported in Table 4, the results give strong support for rejecting the null hypothesis of the series and indicate the presence of ARCH effects in the ordinary least squares (OLS) models.

Results of ARCH Test.

Note. ARCH = autoregressive conditional heteroskedastic.

Significant at the 1% level. **Significant at the 5% level. *Significant at the 10% level.

Results of GARCH, EGARCH, and TARCH

After having carried out the heteroskedasticity test and found the existence of ARCH effects, the next task was to model the unregulated exchange rate volatility of Somalia by utilizing a GARCH model. Methodologically, GARCH models estimate the volatility using conditional variance based on previous period’s volatility and previous period’s information about exchange rates. To improve the performance of the GARCH model and overcome its limitations, this study employs EGARCH (exponential generalized autoregressive conditional heteroskedastic) and TARCH (threshold autoregressive conditional heteroskedastic) models. Such combinations are expected to produce accurate and reliable results and enrich the process of finding effective policy formulations.

Residuals of unregulated exchange rates of Somalia are illustrated in Figure 2 before reporting the results of the GARCH. As can be observed from the figure, there is an extended period of low volatility from January 1995 to 1999. Moreover, there is a stretched episode of high volatility from 2000 to 2002. Hence, this enlightens that episodes of high volatility are followed by episodes of high volatility and episodes of low volatility are likely to be followed by episodes of low volatility. As a result, the trend of the data apparently suggests that the residual is conditionally heteroskedastic and thus should be represented by ARCH and GARCH models.

Residuals of Somalia’s unregulated exchange rates.

GARCH and macroeconomic factors

To examine whether macroeconomic factors (domestic prices, money supply, imports, and hot money) have an effect on the volatility of Somali unregulated exchange rate, several GARCH models were tested. This step contributes to the process of identifying a model that is best fitted to the data. Akaike information criterion (AIC) is used to select the fittest model to the data. After testing all models, the results show that the GARCH(1, 1) model fits the data well and provides better statistical results when macroeconomic factors are considered. The fitness of the model has been assured after checking all necessary diagnostic tests.

As reported in Table 5, the coefficients of the ARCH and GARCH terms are significant at 1%. Under normal Gaussian distribution, the model shows that both previous news and previous volatility can influence current volatility. This indicates that the volatility of Somali unregulated exchange rates is affected by its own shocks (ARCH and GARCH factors). Likewise, the study examined whether macroeconomic factors have an influence on the volatility of Somalia’s unregulated exchange rates. As shown in Table 5, except for the dummy variable (Structural Break), all other variables such as money supply (monetary intervention), imports (trade), hot money (speculation), and domestic prices have an influence on the volatility of Somalia’s unregulated exchange rates.

Results of GARCH, EGARCH, and TARCH Models.

Note. GARCH = generalized autoregressive conditional heteroskedastic; EGARCH = exponential generalized autoregressive conditional heteroskedastic; TARCH = threshold autoregressive conditional heteroskedastic; LM = Lagrange multiplier.

EGARCH and macroeconomic factors

While using EGARCH, the study carried out various EGARCH models. As shown in Table 5, the study found that EGARCH(1,1) is the optimal model for the data when macroeconomic factors are taken into consideration. The results of the variance equation show that the GARCH and asymmetric terms are statistically significant. This reveals that past information of the exchange rates can influence current volatility and past volatility can influence current volatility. In addition, the asymmetric term is negative and significant, which confirms the existence of asymmetric response. This asymmetric response points out that volatility seems to rise in response to positive spikes and fall in response to negative spikes. The study found that Somali unregulated exchange rate volatility seems to have an asymmetric characteristic that reveals a negative shock in the market is likely to cause more volatility than a positive shock of the same magnitude.

TARCH and macroeconomic factors

After specifying the EGARCH model with explanatory variables, the next task is to estimate a TARCH model with macroeconomic factors. As shown in Table 5, coefficients of the variance equation show that ARCH and GARCH are not significant at 5%. Moreover, the asymmetric term is negative and insignificant. Except for the dummy variable, the other coefficients of the explanatory variables (Domestic Price, Money Supply, Import, and Hot Money) are significant. This illustrates that the TARCH model is not the best fit for Somali unregulated exchange rate volatility when macroeconomic factors are incorporated.

Model Selection

This study employs AIC to select the fittest model. To further ensure that the preferred model is optimal, serial correlation, normal distribution, and ARCH effect tests were conducted. As reported in Table 6, the EGARCH model outperforms all other models.

Model Comparison.

AIC = Akaike information criterion; GARCH = generalized autoregressive conditional heteroskedastic; EGARCH = exponential generalized autoregressive conditional heteroskedastic; TARCH = threshold autoregressive conditional heteroskedastic.

Discussion and Implications

Discussion

To examine the unregulated exchange rate volatility of Somalia and investigate whether macroeconomic factors have a significant influence on the volatility, this study utilizes a conditional heteroskedastic model, namely, EGARCH. The study established that the volatility of Somalia’s unregulated exchange rates has significantly been influenced by its own shocks as well as macroeconomic factors. The EGARCH model shows that past information, as well as past volatility, has a significant influence on Somali unregulated exchange rate volatility. In addition, the asymmetric term is negative and significant indicating the presence of asymmetric response. The results of the model also point out that domestic price, money supply, imports, and hot money have a significant influence on Somali unregulated exchange rate volatility.

This study is in line with previous studies as the same results have been found by Abdalla (2012) in the context of Arab states. Likewise, this study is aligned with the results of Zahangir Alam and Rahman (2012), who discovered that past exchange rate volatility affects current volatility significantly. While examining the influence of domestic price, money supply, imports, and hot money, the study found that unregulated exchange rate volatility of Somalia is significantly affected by these macroeconomic factors. This gives an added value to this study as it remains one of the limited studies conducted systematically in the context of Somalia at this point of time. Somalia is getting out of decades-old instability and chaos and this makes the country very attractive to different investors locally and internationally. Hence, providing such study does not only help those investors but also give significant policy recommendations to policymakers.

First, this study ascertained that Somali unregulated exchange rate volatility is significantly influenced by money supply. The results of this study are supported by the findings of Abdurahman (2005), who found that money supply has a significant influence on the exchange rate of Somalia in the last years of military regime and during the statelessness in Somalia. The influence of money supply on exchange rates has been phenomenon in Somalia since 1996 where General Mohamed Farah Aidid 2 issued the first Somali banknotes since the fall down of the military government in 1991. The issue of printing Somali banknotes has reached its peak in 2001 and 2002 in which SOS lost its value against USD. The supply of money by the state and federal governments continued until the value of the money become similar to its cost (no seigniorage of money). Prior to General Aidid, President Ali Mahdi imported new Somali notes. At that point, there was no interest to print more money as it was not profitable, and thus the supply of Somali banknotes to the FX market stopped and the FX market felt some sense of relief. Likewise, it has been learned from the experience of SOS in 1990s that cash injections in the form of forged SOS have an immediate effect on the exchange rates (Abdirahman, 2007). Zhang et al. (2016) argue that when excess money is created, local currencies are converted into dollars; consequently, the exchange rate depreciates in the local currency market. This is exactly what has happened in Somalia in the late 1990s and in the beginning of the 21st century when a huge amount of paper money is created by warlords and money-lords (greedy businessmen). The effect of that financial catastrophe is well echoed by every single person, who was present in Somalia during that period. The owners of the businesses refused to accept SOS as it was depreciating at an alarming scale. This created havoc among consumers, in particular, the poor and low-income households, as they become unable to purchase basic necessities for the survival of themselves and their loved ones.

Second, the study found that imports can significantly influence the unregulated exchange rates of Somalia. Although Somali exports increased drastically since 1970s following the oil boom in Gulf countries, Somali is still dependent on imports for necessities such as rice, sugar, wheat flour, and oil. Somali exports to Gulf States are seasonal and very marginal compared with its imports. Thus, imports play a crucial role in Somalia’s unregulated FX market because traders either send or ship money abroad in the form of USD to purchase foreign goods. This is very true in some sectors of Somali economy such as livestock and agricultural markets as the basic medium of exchange in these markets still remains SOS. For instance, cattle traders use SOS to buy cattle from the local market, but when they sell their cattle to the Saudi Arabia market, they use USD as a medium of exchange. Hence, they should convert their USD into SOS to buy cattle again from the local market. And that circle continues to repeat. As imports are more than exports, demand for foreign currency remains more than the supply of foreign currency as long as the country is in a trade deficit. Somali trade statistics show that Somalia has been in a trade deficit since the state collapse, and thus supply of USD is always under its demand assuming that trade is the only channel for the supply and demand of foreign currency. As the empirical results confirm, imports can significantly influence the volatility of the exchange rates of Somalia. This study is in line with the findings of previous studies such as Abdurahman (2005) and Shortland (2012), which argue that Somali exchange rate is influenced by imports such as rice and Qat. To reduce the impact of imports on the volatility of Somali unregulated exchange rates, there should be a solid policy that resolves this issue.

Third, this study found that speculation (as measured by hot money) can significantly influence the volatility of unregulated exchange rates in Somalia. To capture the speculative trading, hot money is used, which considers short-term capital flow. In the context of Somalia, the speculative trading could be huge theoretically because of ineffective regulations. In Somalia, the FX market operates without proper regulation, supervision, and protection; thus, currency traders can manipulate the currency prices by either undervaluing or overvaluing. This may create a huge financial crisis in the country as it pushes unpredictable price hikes. These price hikes will not only create price instability in the country but also affect the poor and low-income households in a negative manner. As Somalia was in chaos and civil war, there were various interest groups (both national and international), who used to make news regarding the stability of the country, for example, the news of holding a reconciliation conference and the decision of United Nations to send peacekeeping troops, among others. With the help of this unpredictable news, Somali currency speculators sometimes excessively speculate the exchange rate between SOS and foreign currencies such as USD. Another important point to be mentioned here is that few individuals control the Somali FX market because they have been in the market for more than two decades and have sufficient capital to control the market. Due to their experience and dominance, these individuals are respected by all other currency traders. As Somali currency traders have not been under the surveillance of Somali central bank, they could involve huge speculation transactions without any trouble.

Speculation is sometimes associated with currency crisis and it can lead to a currency collapse. A currency collapse is a situation wherein the value of a national currency falls completely in a very short period of time. Currency collapse can contribute a wider economic crisis with long-term consequences. The South East Asian Financial Crisis in the 1990s is a good example. Although there might be a wide variety of things that can bring about a currency collapse, speculative attack is considered one of the key causes. When a speculative attack takes place, people perceive that the value of the currency goes down, so they choose to sell their currency to avoid any potential loss. As the people start selling the currency, the value begins to decline and this creates more panic among the people causing the value of the currency to drop further and further. A national currency is regulated in order for the local currency to be protected in case excessive speculative attack is detected or a sudden capital outflow is discovered. Hence, it is clear from the results that speculation is a key variable that affects the volatility of Somali unregulated exchange rates and this necessitates the importance of creating an effective mechanism that controls excessive speculation.

Implications

This study found that Somali informal exchange rate volatility is significantly affected by some macroeconomic fundamentals. The results of this study suggest the need for reforming the exchange rate and monetary policies of the country and the immediate need for creating a national currency that can support Somali postwar economic recovery. This study provides some noble contributions to the process of understanding the volatility of Somali informal exchange rates. Money supply, imports, and speculation are found to be three important macroeconomic fundamentals that significantly influence the volatility of Somali informal exchange rates.

It is evident, from these findings, that money supply is a key factor to the volatility of Somali informal exchange rates, and thus Somali policymakers should stress on producing effective regulatory on its monetary issues. One step of starting is to introduce new currency. Technically, the central bank should establish regional offices in each of the country’s main regions and through these offices; the new currency can be put into operation. The country is changing and the capacity of the government is also improving; therefore, the old currency can be replaced with the help of communities and the private sector. Similarly, the private sector should support the government’s effort toward regulating the private sector because a poor monetary policy leads to volatile FX market. We strongly argue that a new currency can be introduced by the new government and such decision is feasible if a proper monetary mechanism is put forward.

Apart from the money supply, import is another macroeconomic factor that significantly influences Somalia informal exchange rate volatility. There are several issues that need to be addressed because imports are associated with capital outflow, which is in the form of foreign currency. In the context of Somali, most of the necessities are imported and the country is spending a huge amount of money on these imports. The current total dependence on imports should be reduced.

As Somali local currency is not accepted in the exporting country, Somali traders must either send the money via financial institutions or export it physically. But, in either way, the money should be in the form of USD. This implies that imports can contribute drastically to the fluctuation of the local currency because traders must convert their funds into USD before they send or export it physically. The empirical evidence of the study also reveals that imports play an important role in Somali informal exchange rate volatility. To lessen the effect of imports on the exchange rate market, the government with the help of the private sector should come up with a strategy that reduces the effect of imports on the informal exchange rate volatility. There are several policy suggestions that can be used by the government with the help of the private sector.

The first policy is to reform the economy of the country wherein a strategic road map is established and domestic businesses are supported by providing a conducive business environment. To properly implement this strategy, the government should develop a periodical National Economic Development Plan (NEDP) that ensures economic strategies are implemented and an appropriate business environment is established.

The second one is to look for a trading partner whose currency is relatively stable compared with USD. Then, a sufficient amount of that currency has to be put into the market under the surveillance of the central bank. This can reduce the effect of imports on Somali informal exchange rate volatility.

The third policy is to discourage imports via two methods: One method is to encourage local businesses to produce the necessities locally and the other method is to ask foreign partners to come to the country and produce necessities locally. Any of these policy suggestions can help Somalia reduce the effect of the imports on the volatility of the informal exchange rates.

The forth policy that could help reduce the dependence on the imports is to introduce social reform policies that can raise the awareness of domestic consumers to change the mind-set of import dependence. Somali media should be engaged in the awareness-raising campaign.

Overall, the current total dependence on imports should be reduced. Consequently, the government should adapt inward-oriented policies that support import reduction and discourage dependence on foreign goods.

The study found that Somali informal exchange rate volatility has been affected by hot money. Foreign capital entering the country supposedly seeking short-term profits is referred to as hot money. Hot money can be a disastrous tool for speculators to attach the domestic currency, and thus Somali federal government should properly regulate the foreign capital entering the country. Such speculative capital inflow affects not only Somali informal FX market but also other financial markets. As Somalia is a small and open economy in a post-conflict period, it should control its capital inflows to avoid the consequences of speculative capital inflows observed in other emerging economies.

The following new polices should be formulated to reduce the effect of macroeconomic fundamentals on Somali informal exchange rate volatility:

Introduce new currency with robust security features.

The use of foreign currency as a medium of exchange should be made illegal and punishable in front of the law.

Exportation or importation of foreign currencies should be limited.

The central bank should facilitate the supply and demand for foreign currency.

Remittance companies should use local currency to transfer remittances. For example, if US$100 is sent to Mr. Ali in Mogadishu and the spot exchange rate is 10,000 per dollar; he will be given 1,000,000 SOS.

All commercial banks should use local currency in their finances.

Opening a foreign currency account should be limited.

All salaries and wages should be quoted and paid in the form of local currency.

Government services should be priced in local currency.

Electronic money (such as EVC-plus and E-MAAL) in the form of foreign currency should be limited.

Electronic money (such as EVC-plus and E-MAAL) should be in the form of local currency (SOS).

Electronic money should be soundly regulated.

Furthermore, the results of this study imply that, even in times of war and lawlessness, the laws of economics remain the same and as such nobody can escape these indispensable laws in all circumstances. This is another appealing contribution of this study, which would be worth considering in the economic literature.

Conclusion

The aim of this study is to examine the volatility of Somali informal exchange rates systematically. Furthermore, the study investigates whether macroeconomic fundamentals have a significant effect on the volatility of the informal exchange rates in Somalia. After the analysis, the study found several important findings. First, this study found that Somali exchange rate volatility is significantly affected by its own shocks (previous information on exchange rates as well as past volatility). Second, one of the key findings of this study is that macroeconomic fundamentals have a significant influence on Somali informal exchange rate volatility. Macroeconomic fundamentals like money supply, imports, and short-term capital flows (known as hot money) have a significant influence on the volatility of Somali informal exchange rates. Third, Somali informal exchange rate volatility can be adequately modeled using the EGARCH model. One of the key recommendations of this study is to replace the current SOS to a new currency with strong security features to get rid of the huge counterfeit notes circulating into economy. In addition, this study recommends inward-looking trade policies to ultimately become inward-oriented economy, which eventually reduces the effect of the imports on the informal exchange rate volatility. Finally, there should be a robust capital control policy that can reduce the effect of hot money on the FX market in particular and the economy in general.

Footnotes

Acknowledgements

The authors wish to thank the Center for Research and Development of SIMAD University for funding this research project.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.